— Fortnite Competitive (@FNCompetitive) July 28, 2019

Giersdorf pwn3d 99 other opponents, earning a total of 59 points over six matches. The runner up, ‘Psalm’, racked up 33 points, according to IGN.

“Words can’t even explain [how I feel] right now,” said Giersdorf, speaking from the Champion’s circle. “I’m just so happy. Everything I’ve done, the grind, it’s all paid off. It’s just insane.“

Epic Games set aside a total of $40 million in prize money for the Fortnite World Cup, of which $10 million was awarded over the 10-week qualifying stage, and $30 million reserved for the New York City finals, according to Statista.

As the following chart illustrates, you could win the Tour de France, the Hawaii Ironman, the New York Marathon and the Masters Tournament in Augusta and still walk (or limp) away a poorer person than the world’s best Fortnite player. The tournament is part of Epic Games’ campaign of making Fortnite the most lucrative game in esports. Last year, the company pledged to put up $100 million in prize money for Fortnite events through the end of 2019. –Statista

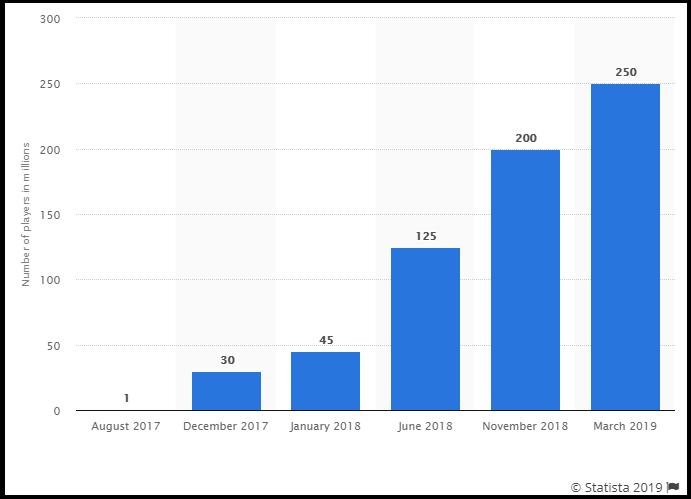

So to all the Fortnite players who can’t seem to put the controller down, just tell Mom you’re working on your retirement when she yells at you to turn off the game and come upstairs for dinner. You’ve only got 250 million players to compete with.

via ZeroHedge News https://ift.tt/314hkbe Tyler Durden

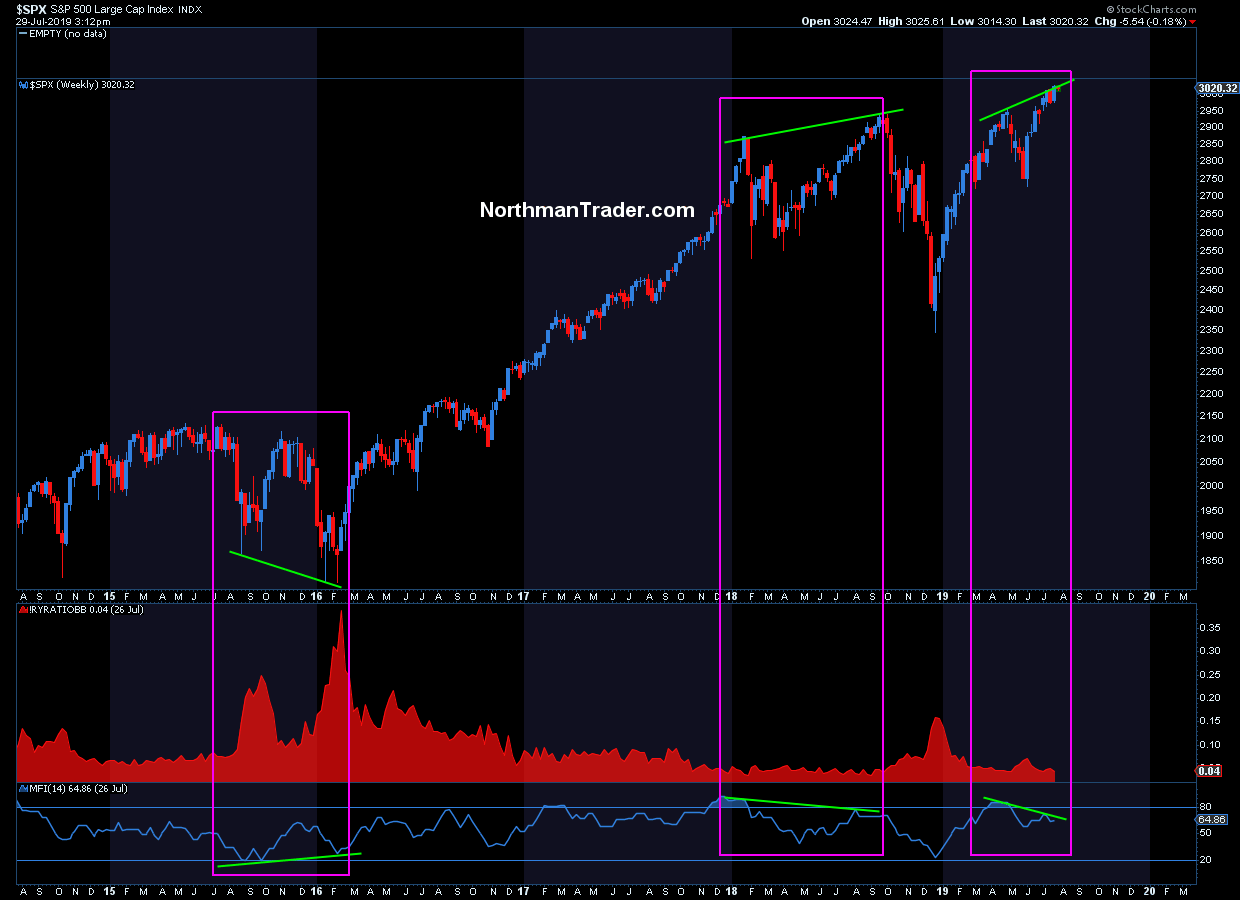

As outlined this weekend put call ratios are fairly low and benign going into this week’s Fed meeting. No worries.

Investor positioning? All in long it appears.

One indicator combination of interest, RYDEX account positioning as well as money flows. During times of market stress we can observe shifts to more bearish positioning and the RYDEX ratio moves higher, this last observed in larger size in 2015/2016. But the times of stress or fear are apparently over. Even last December’s 20% drubbing produced a much lesser spike during a big correction than ever before.

Indeed December’s 20% drop produced barely a blip. The reason? One can only speculate of course, but I suspect the massive switch to passive investing has a lot to do with it. Corrections don’t last anymore, that is been the investor lesson over the past 10 years. There is no reason to fear any longer.

Central banks always step in and after a few days the correction low is made. And investors have been right to take on that attitude. So far.

Indeed we saw the government step in with liquidity calls during Christmas and the Fed switching policy leading to the expected rate cut this week. The end result: A 0.04 ratio on RYDEX, indicating fully long account positioning.

But note that MFI (Money flow index) in the lower part of the chart. It shows a negative divergence. In early 2016 is showed a positive divergence on the new $SPX lows which firmed a major bottom. In October 2018 money flow showed a negative divergence on new highs, now another negative divergence. These divergences appear to be solid signals when the RYDEX ratio is at extremes. Last fall RYDEX also showed fully long positioning ahead of the 20% correction. What”s more extreme than 0.04? 0.03? 0? Everybody all in? Everybody all owning the same few stocks via index funds and ETFs. Nobody ever selling because markets are risk free?

That’s called intelligent investing these days:

Defined as intelligent investing:

Dollar cost average passively into index funds tracking a shrinking investable universe of stocks not knowing what you actually own or are exposed to, where everybody owns the same things but nobody ever sells cause the Fed will keep it all safe.

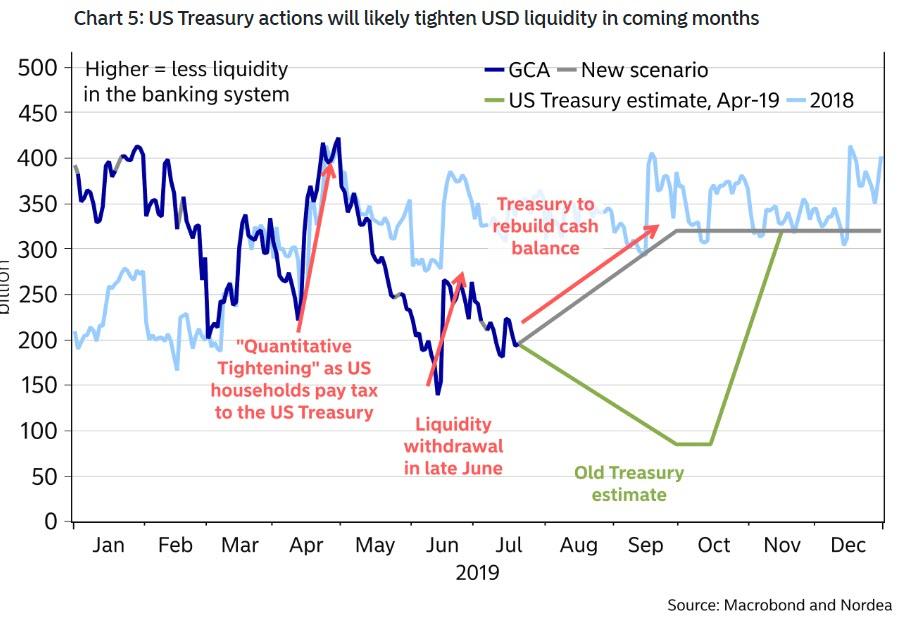

One of the reasons why Trump and Congress were so quick to pass a debt ceiling deal last week is that had they failed to do so, with the Treasury’s cash balance sliding precariously lower and expected to hit $0 by early September, there was a non-trivial chance the US could technically default by the time Congress came back from its August vacation.

Of course, that did not happen, a debt ceiling extension deal was reached, and as a result the Treasury is now free to start reloading its cash balance, and it plans on doing just that. On Monday, the Treasury Department announced its latest quarterly estimates of net marketable borrowing needs for the current (July – September 2019) and upcoming (October – December 2019) quarters. What it revealed was the following:

After borrowing just $40 billion in the past, April-June period, which left the Treasury with a quarter end cash balance of $264 billion, in the current quarter, the Treasury now expects Treasury issuance to explode higher, and borrow a whopping $433 billion in net marketable debt, a massive $274 billion higher – or more than doubling – its prior forecast announced in April 2019.

The reason for this debt issuance flurry? To rebuild the cash balance back to a level of $350 billion, which is where the Treasury expects its end-of-September cash balance to be, up from just $85 billion as of the April 29 forecast.

Looking ahead, during the October – December 2019 quarter, the Treasury unveiled for the first time that it expects to borrow $381 billion in new debt, assuming an end-of-December cash balance of $410 billion with $310 billion of the new issuance going to cover financing needs.

As for the past quarter, in April 2019, the Treasury estimated marketable borrowing of $30 billion and assumed an end-of-June cash balance of $270 billion. The change in borrowing resulted from lower net cash flows partially offset by the lower end-of-quarter cash balance due to the Treasury hitting the debt ceiling.

In other words, the Treasury will sell $814 billion in debt in the current and future quarter… and it will only gets worse from there.

As Bloomberg reports, the Treasury is expected to hold its quarterly note and bond sales at record levels for the third straight time as Washington’s latest budget deal shows that the U.S.’s debt binge will continue. While President Trump once said he would eliminate the national debt, he is now set to approve a budget that will help usher in trillion-dollar annual deficits. As a result, Bloomberg notes that Wall Street securities firms predict that a boost in Treasury issuance may be coming in a year’s time.

Bond dealers see the status quo prevailing at Wednesday’s quarterly refunding announcement. Forecasts are coalescing around the view that the Treasury will keep auction sizes of 3-, 10- and 30-year debt unchanged at a record total of $84 billion, in sales scheduled from Aug. 6-8. To put it in perspective, the tally was $62 billion at the time of the 2016 U.S. election.

The coupons issuance is expected to raise $296bn in new cash from private investors for the August to October period. This amount, coupled with $194bn in bill issuance, will help fund an estimated $272bn of financing needs plus $200bn of cash balance increase.

Additionally, with a July debt limit suspension, bills are expected to increase by $130bn in August, although as DB notes, the risk is that it could run higher. The Treasury’s decision to gradually rebuild its cash balance will help limit some of the pressure in funding markets. Higher repo rates would make issuance of front-end coupons more expensive. For example, 2yr Treasury-OIS has widened about 8bp in July since investors began expecting the August bill supply would put upward pressure on funding rates. In its refunding statement, the Treasury could signal that it would temporarily run a lower cash balance over the next several weeks, which should help alleviate funding market anxiety, although in light of the Treasury’s forecast that seems somewhat contradictory. Indeed, with the Treasury’s decision to quickly rebuild its cash balance back to a level it deems more prudent (say $350bn), the increase to bills over the next 4-6 weeks significantly exceeds most Wall Street forecasts.

The bipartisan deal to suspend the debt limit for two years also paves the way for a $324 billion increase in government spending over the period above existing budget caps. That’s emboldening most dealers to pencil in increases in debt sales by fiscal 2021, which starts in October 2020.

The House passed the debt-ceiling expansion and budget bill on July 25 and Senate Majority Leader Mitch McConnell said he expects his chamber to clear it this week for Trump’s signature.

“The deficit is rising and the impetus toward higher spending is very strong,” said Stephen Stanley, chief economist at Amherst Pierpont Securities. “By the second half of next year Treasury will have to raise coupon sizes again.”

This is good news for Washington’s spenders… and a catastrophe for any deficit hawks left. With the president shoving aside past Republican orthodoxy on fiscal restraint and the issue not prominent among Democrats campaigning to take his job, Washington is showing no signs of slowing spending.

Which means that when it comes to fiscal conservatism, Trump is a Republican in name only, as the fiscal shortfall has continued to soar under Trump as tax cuts, bipartisan spending increases and entitlements weigh on the budget outlook. Meanwhile, socialist candidates for the 2020 presidential election are trying to attract voters with proposals that would only increase the gap such as MMT.

Maya MacGuineas, president of the nonpartisan budget watchdog Committee for a Responsible Federal Budget, called the latest budget deal “a total abdication of fiscal responsibility by Congress and the President.”

What’s clear – as Bloomberg concludes – is the backdrop puts the $15.9 trillion Treasury market on course to balloon in the next couple of years.

“By 2021, Treasury will begin to have a problem, given deficit growth, and need to increase coupon sizes,” said Margaret Kerins, global head of fixed-income strategy at BMO Capital Markets. Then again, if the current administration is still in charge, the world will likely have far more pressing issue than the eventual insolvency of the US to worry about…

via ZeroHedge News https://ift.tt/31cwZW3 Tyler Durden

At least 16 prisoners were decapitated and dozens more were killed during a prison riot in Brazil.

At least 52 inmates died in the riots that involved criminal gangs in Para, located in the northern part of the country.

Two officers were also taken hostage as the rival gangs clashed, reported the AFP news agency on July 29.

At least 16 of the victims were decapitated, authorities said. Others were asphyxiated. President Jair Bolsonaro has described plans to “stuff prison cells with criminals” @terrence_mccoy reports from Rio de Janeirohttps://t.co/yi5EaKSENj

— Matthew Hay Brown (@matthewhaybrown) July 29, 2019

The fight began at the Altamira Regional Recovery Center at around 7 a.m. local time, said a Para state official in the AFP report.

He said that two guards were taken hostage during the clashes before the gangs freed them.

According to BBC, reports in Brazil said that many inmates died of suffocation when the prison was set on fire. A video posted by Brazilian media outlets shows smoke emitting from a prison building, and another showed prisoners on rooftops.

The prison has a capacity for 200 prisoners, but it was occupied by 311 inmates, Sky News reported.

Brazil has a prison population of 704,000, but there is only cell space for about 416,000 around the country, the report noted.

In May of this year, some 55 inmates died at prisons in Amazonas state.

#Breaking: At least 50 inmates got killed in #Para prison in #Brazil, after a riot broke out as gangs fought for 5 hours, with other inmates in the prison whom of 16 inmates got decapitated. pic.twitter.com/CUvczqqkMU

At one prison, 15 prisoners were found dead, with many being stabbed by makeshift knives and strangled, according to the report. Forty prisoners were found dead at another facility, and their reported causes of death were asphyxiation.

Two years before that, about 150 prisoners died during a several-week-long span of violence across several prisons. The violence was blamed by rival gangs.

According to Sky, the riots lasted weeks and was linked to the control of drug-trafficking networks in the area.

In May, Brazil’s justice and public security ministry said it was sending a federal task force to help local officials handle the situation.

“I just spoke with (Justice) Minister Sergio Moro, who is already sending a prison intervention team to the State of Amazonas, so that he can help us in this moment of crisis and a problem that is national: the problem of prisons,” Amazonas state Gov. Wilson Lima said.

Several drug-trafficking and other criminal gangs in Brazil run much of their day-to-day business from prisons, where they often have wide sway. The 2017 slayings were largely gang-related, prompting authorities to increase efforts to separate factions and frequently transfer prisoners.

Authorities have not yet said whether gang wars were behind the latest blood-letting.

Moro had to send a federal task force to help tame violence in Ceara state in January that local officials said was ordered by crime gang leaders angered by plans to impose tighter controls in the state’s prisons.

The Associated Press contributed to this report.

via ZeroHedge News https://ift.tt/2YeypCf Tyler Durden

The numbers are in.. and they are positive (but it’s all relative).

Q2 revenue printed $67.3 million (smashing expectations of $52.7 million) and up 2877% from the previous $17.4 million.

Q2 Adjusted EBITDA: $6.9 million, or 10.2% as a percentage of net revenues; up from a loss of $5.6 million in Q2, 2018

$14 Billion market cap Beyond Meat increased its full-year revenue forecast to $240 million (near the highest analyst estimate of $242 million)

The company has a solid cash buffer:

The Company’s cash was $277.0 million as of June 29, 2019 and total outstanding debt was $30.5 million. Net cash used in operating activities was $22.4 million for the six months ended June 29, 2019.

Capital expenditures totaled $7.5 million for the six months ended June 29, 2019 compared to $10.0 million for the prior-year period.

Adjusted EBITDA to be positive compared to prior expectations of break-even Adjusted EBITDA.

“We are very pleased with our second quarter results which reflect continued strength across our business as evidenced by new foodservice partnerships, expanded distribution in domestic retail channels, and accelerating expansion in our international markets. We believe our positive momentum continues to demonstrate mainstream consumers’ growing desire for plant-based meat products both domestically and abroad,” said Ethan Brown, Beyond Meat’s President and Chief Executive Officer.

“Looking ahead, we will continue to prioritize efforts to increase our brand awareness, expand our distribution channels, launch new innovative products, and invest in our infrastructure and internal capabilities in order to deliver against the robust demand we are seeing across our business.”

Beyond Meat closed down 5.4% ahead of earnings, its biggest decline since June 24, and notably – despite the huge beat and upside outlook – traders are not being squeezed to death yet…

What happens next?

via ZeroHedge News https://ift.tt/2GyySV6 Tyler Durden

A quiet day for sure but the trends remain – dollar and gold higher together, bond yields fading, and stocks clinging near record highs…

Powell better not let the world down!!

Chinese stocks trod water overnight…

UK’s FTSE exploded higher as the pound plunged, Italy underperformed in Europe but the rest of the majors were flat…

And a mixed bag in US stocks too with The Dow clinging to some semblance of positivity as Small Caps and Nasdaq underperformed…

FANG Stocks erased Friday’s gains…

It’s Beyond Meat’s earnings tonight – make or break time for shorts who are paying 144% borrow…

The S&P continues to dramatically outperform the broadest US equity index – not exactly what one would hope for in a broad-based re-acceleration in growth…

Treasuries were bid after Europe closed and ended lower in yields on the day (but traded in a very narrow range)…

30Y Yields erased the losses from Draghi’s disappointment…

The dollar rallied once again – nearing its highest since May 2017…

Cable was clubbed like a baby seal today as no-deal expectations ramp up…

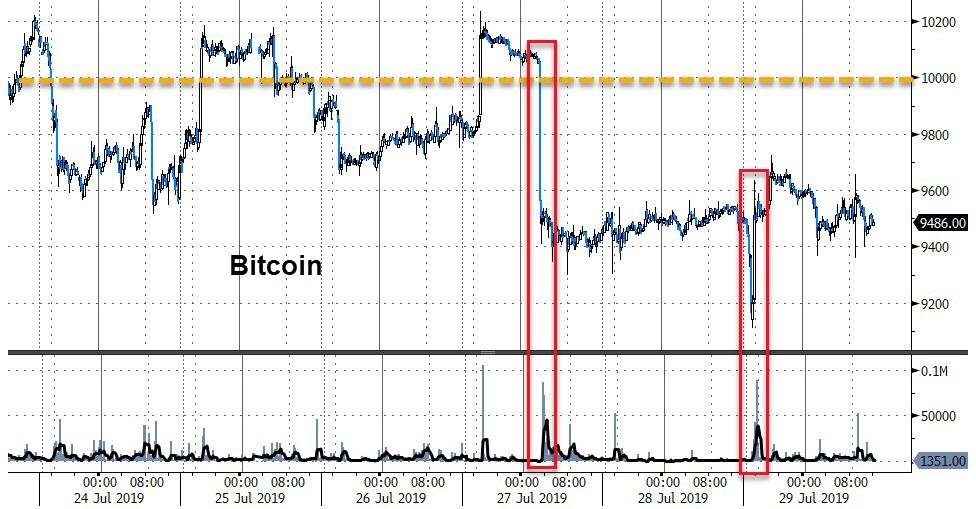

Cryptos had a flash-crashy like move overnight but recovered from that – although they remain lower from Friday…

With Bitcoin holding back below $10,000…

Despite dollar gains, commodities managed gains with Crude and Copper leading but PMs rallying towards the US close…

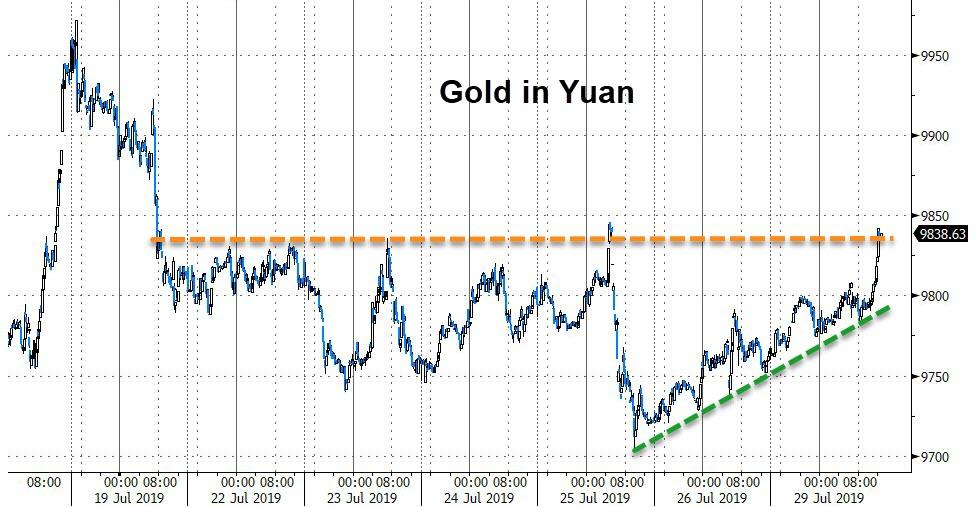

Gold spiked up to pre-Draghi levels…

Oil was volatile intraday testing below $56 and up to $57…

Gold in Yuan jumped up to recent resistance…

And gold in Sterling is very close to a record high…

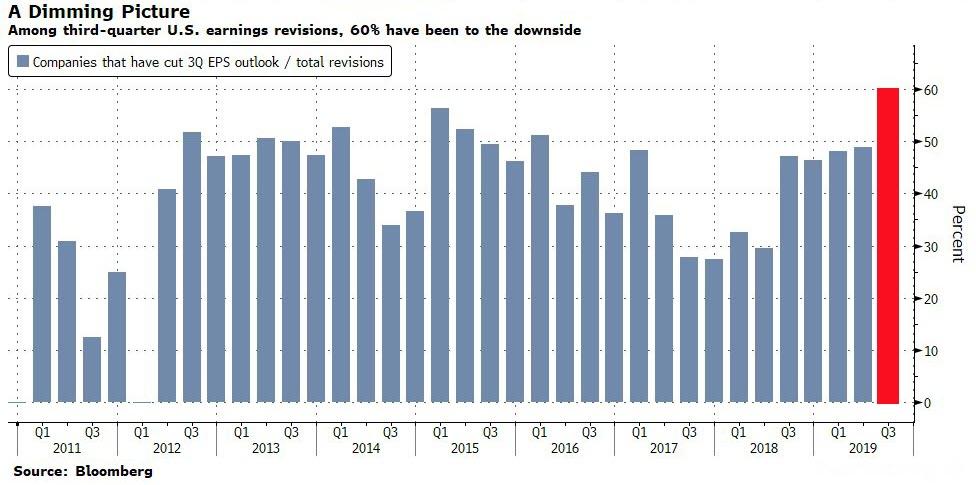

Finally, there’s this… While the S&P 500 is up 20% YTD, earnings expectations for the next 24 months has slumped…

As 60% of companies have cut Q3 EPS expectations in recent weeks…

Will traders sell the Fed news?

via ZeroHedge News https://ift.tt/2Y7ku0C Tyler Durden

It’s not just the melting ice cube known as Deutsche Bank that that is laying off recession-level numbers of traders: according to Bloomberg, Citigroup is also preparing hundreds of job cuts at its slumping trading division as more of the world’s largest firms respond to dormant clients and the rise of the robots with across the board layoffs.

According to the report, Citi – which plans to slash jobs across both its fixed-income and stock trading business over the course of 2019 – will let go at least 100 jobs in its equities unit, or almost 10% of that division.

The mass terminations are not a surprise in light of the chronic decline in Wall Street trading revenues as numerous clients simply refuse to allocate capital to stocks at current levels and pursue the S&P bubble beyond 3,000, certain it’s only a matter of time before the market crashes. As we noted two weeks ago when the big moneycenter banks reported Q2 earnings, the biggest Wall Street banks are facing an identity crisis, pressured by the lowest first-half trading revenue in more than a decade as they contend with reticent clients spooked by a global trade war even as volatility in asset prices hovering around record lows. In other words, despite near perfect trading conditions, bank trading revenues are plunging. One can only imagine what happens if and when trading conditions are even modestly “impaired.”

According to Bloomberg, Citi’s revenue from equity trading tumbled 17% to $1.6 billion for the first half of 2019, driving a 5% drop in total trading. That was lowest equity total among major U.S. firms, according to Bloomberg Intelligence.

Meanwhile, Citigroup executives said this month they would continue to cut costs in the second half of the year after trimming more than analysts expected last quarter.

“We’re going to do everything within our power” to meet a goal of a 12% return on tangible equity this year, CEO Mike Corbat said after the bank announced earnings on July 15.

Citi joins Deutsche Bank, which made the biggest move earlier this month, when the firm announced it was exiting all of equities trading as part of restructuring that included 18,000 job cuts. Other major banks in Europe, including HSBC Holdings Plc and Societe Generale SA, have also announced the layoffs of hundreds of workers in an atmosphere that may be the gloomiest since the financial crisis, yet the S&P is withing spitting distance of new all time highs.

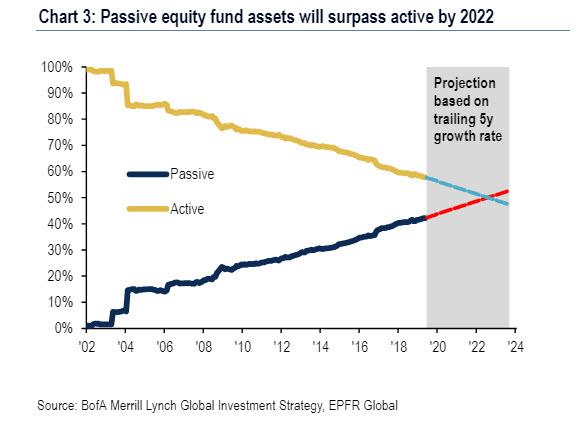

Ironically, in an environment of already depressed liquidity, these layoffs will result in even less prop and flow trading, leading to even lower liquidity, even more accentuated and sharp moves when volatility does spike, resulting in even greater trading losses during the next market correction or bear market, assuring even greater layoffs next time round, as the world finally realizes what we have been saying for the past decade: the market is broken, and between the Fed and algos propping it up, there is simply no need for human traders any more, especially now that Passive investing will overtake Active…

… in just over three years, assuring that carbon-based traders are now a threatened species.

via ZeroHedge News https://ift.tt/2SMtUsA Tyler Durden

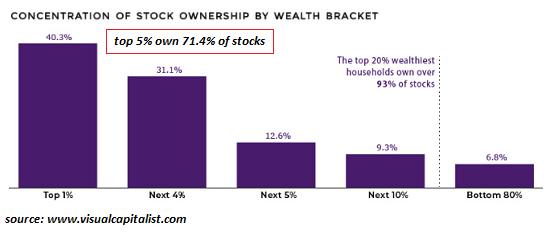

With these speculative and risk management skills accessible only to the wealthy, no wonder only the wealthy have gained purchasing power in the 21st century.

“I am not poor. As a middle class, state employee in Italy, I am probably richer than some 90% of the people living on this planet. But wealth and poverty are mainly relative perceptions and the feeling I have is that I am becoming poorer every year, just like the majority of Italians, nowadays.

I know that the various economic indexes say that we are not becoming poorer and that, worldwide, the GDP keeps growing, even in Italy it sort of restarted growing after a period of decline. But something must be wrong with those indexes because we are becoming poorer. It is unmistakable, GDP or not. To explain that, let me tell you the story of the house that my father and my mother built in the 1960s and how I am now forced to leave it because I can’t just afford it anymore.

Back in the 1950s and 1960s, Italy was going through what was called the “Economic Miracle” at the time. After the disaster of the war, the age of cheap oil had created a booming economy everywhere in the world. In Italy, people enjoyed a wealth that never ever had been seen or even imagined before. Private cars, health care for everybody, vacations at the seaside, the real possibility for most Italians to own a house, and more.

My father and my mother were both high school teachers. They could supplement their salary with their work as architects and by giving private lessons, but surely they were typical middle-class people. Nevertheless, in the 1960s, they could afford the home of their dreams. Large, a true mansion, it was more than 300 square meters, with an ample living room, terraces, a patio, and a big garden.

My parents lived in that house for some 50 years and they both got old and died in there. Then, I inherited it in 2014. As you can imagine, a house that had been inhabited for some years by old people with health problems was not in the best condition.

we started doing just that. But, after a couple of years, we looked into each other’s eyes and we said, ‘this will never work.’

We had spent enough money to make a significant dent in our finances but the effect was barely visible: the house was just too big. To that, you must add the cost of heating and air conditioning of such a large space: in the 1960s, there was no need for air conditioning in Florence, now it is vital to have it. Also, the cost of transportation is a killer. In an American style suburb, you have to rely on private cars and, in the 1960s, it seemed normal to do that. But not anymore: cars have become awfully expensive, traffic jams are everywhere, a disaster. Ah…. and I forgot about taxes: that too is rapidly becoming an impossible burden.

And so we decided to sell the house. We discovered that the value of these suburban mansions had plummeted considerably during the past years, but it was still possible to find buyers.

What’s most impressive is how things changed in 50 years. Theoretically, as a university teacher, my salary is higher than that of my parents, who were both high school teachers. My wife, too, has a pretty decent salary. But there is no way that we could even have dreamed to build or buy the kind of house that I inherited from my parents.

Something has changed and the change is deep in the very fabric of the Italian society. And the change has a name: it is the twilight of the age of oil. Wealth and energy are two faces of the same medal: with less net energy available, what Italians could afford 50 years ago, they can’t afford anymore.

But saying that depletion is at the basis of our troubles is politically incorrect and unspeakable in the public debate. So, most Italians don’t understand the reasons for what’s going on. They only perceive that their life is becoming harder and harder, despite what they are being told on TV.”

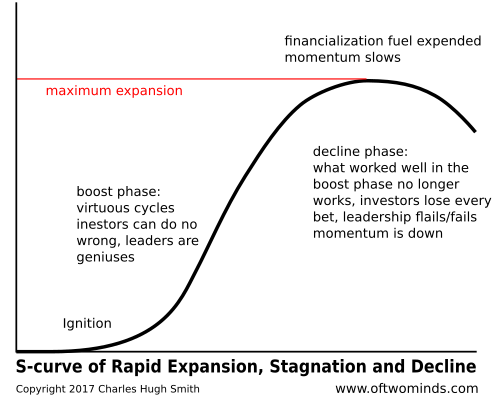

To resource depletion I would add lower returns on both capital and labor–what is known as diminishing returns: the same investment yields less output.

This decay of return on investment manifests as an S-Curve, which is a constant reference point in my work: an investment that earns a large output at first yields less and less, until the yield (output) stagnates and then declines. Increasing the investment no longer reverses the decline, and often accelerates the decline into a crash.

The 1960s “Economic Miracle” (called Les Trente Glorieuses in France, the thirty years of growth from 1945 to 1975) wasn’t just the result of cheap oil/fuel; credit/investment-starved economies generated outsized returns as capital investments expanded production and productivity, raising wages which then increased consumption and production in a self-reinforcing feedback loop.

Labor was relatively cheap, and capital investments in equipment, social investments in infrastructure and human capital investments in education all boosted the productivity of labor while boosting wages and consumption.

Compare this to the present: ordinary financial capital earns 2% at best and zero or even less than zero in developed economies. Owners of capital have a hard time finding any high-yield investment that isn’t a speculative gamble based on financialized leverage or debt.

This is why corporations are pouring trillions of dollars of capital into stock buybacks that generate no new goods and services: they can’t find any productive use for the capital, so they use buybacks to boost the value of their shares.

Professor Bardi labors in higher education. Back when university credentials were relatively scarce, and higher education actually boosted the productivity of the graduates, the labor of professors generated substantial economic value.

Now that college diplomas have lost their scarcity value, and developed-world work forces are over-credentialed, the value of higher education credentials and those who issue them has declined accordingly. In a global economy with an abundance of over-credentialed workers, the claim that more education creates more value is no longer valid.

If there is an oversupply of chemistry graduates, graduating another 10,000 chemistry majors doesn’t boost productivity at all; rather, it misallocated vast amounts of financial and human capital.

The net result is that the return on ordinary capital and labor, even that of college professors, has declined while the cost structure of increasingly complex societies has soared.

If we consider higher resource costs and higher costs of systemic complexity, and declining returns on capital and labor as inputs, we can see that the only possible output of such a system is declining purchasing power, which we experience as becoming poorer: our labor buys less and our savings earn next to nothing unless we have the specialized knowledge and risk appetite to engage in speculative gambles.

With these speculative and risk management skills accessible only to the wealthy, no wonder only the wealthy have gained purchasing power in the 21st century. The result is only the wealthy can afford what was once affordable to the middle class.

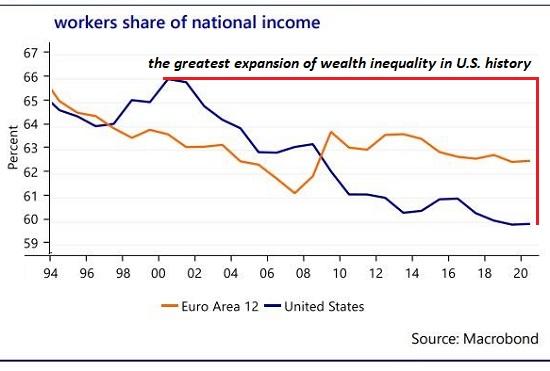

The decline in the value of conventional labor and purchasing power is visible in this chart of labor’s share of the national income.

Ownership of speculative capital is concentrated in the top 5% of households, guaranteeing that speculative gains from asset bubbles are also concentrated in the top 5%– roughly 6 million households, with the majority of the gains concentrated in the top few hundred thousand households.

Outsized gains are now only available to the few with the skills and experience required to gamble high-risk assets successfully, and this is becoming more difficult; even the professional class of money managers are increasingly unable to beat passive index funds.

The top 5% are riding high now that central banks have inflated stupendous bubbles in stocks, housing and other assets, but these gains are speculative.These gains are often viewed as permanent entitlements (i.e. bubbles never deflate), but if history is any guide, those holding speculative gains as if they were a form of savings are in for a rude awakening in the next few years.

One of the constantly repeated mantras of this stock market, which keeps rising no matter how much bad news is lobbed at it, is that it is climbing a wall of worry as investors refuse to participate in the “most hated bull market of all time”. This has been, at its core, the primary reason why JPMorgan’s Marko Kolanovic has been bullish on stocks for the past several hundred points.

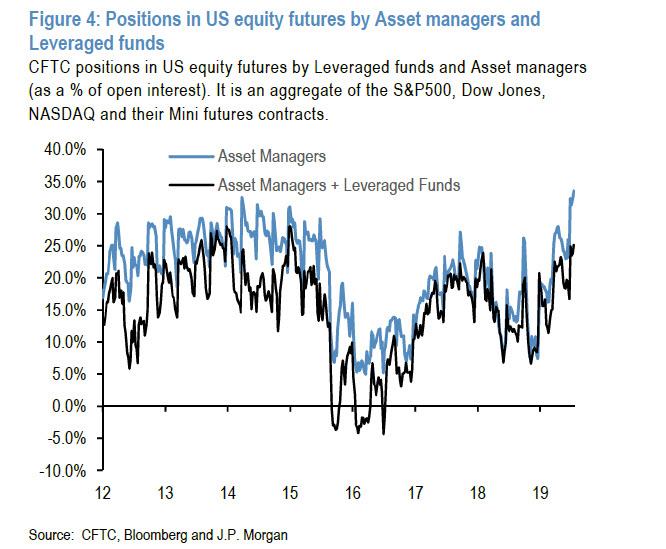

There is just one problem with this conventional wisdom: as often happens, it is dead wrong, and as JPMorgan’s “bad cop” strategist, and now chronic foil to Koalnovic’s unbridled permabullishness, Nick Panigirtzoglou wrote on Friday, not only are investors very much long risk, but most asset classes have now been massively “overbought”, with some positioning levels in record territory.

Case in point, the combined asset-manager and leverage fund positioning in U.S. equity futures the most extended in years this decade, if not ever.

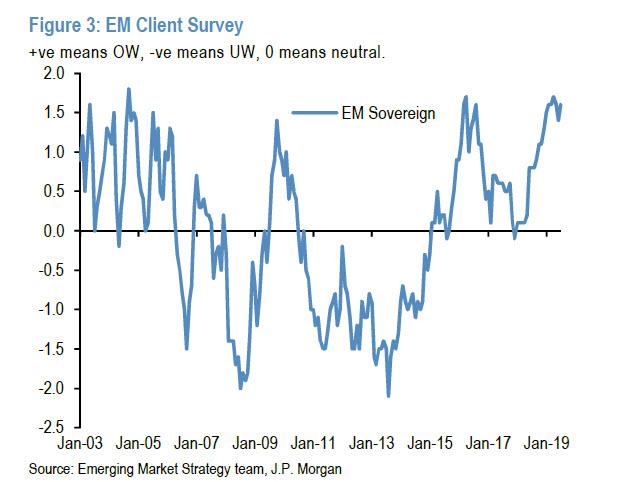

In the EM fixed income space, Panigirtzoglou shows the next chart, which shows that emerging market external debt overweights in JPM’s EM fixed income client survey are near levels last seen in 2005.

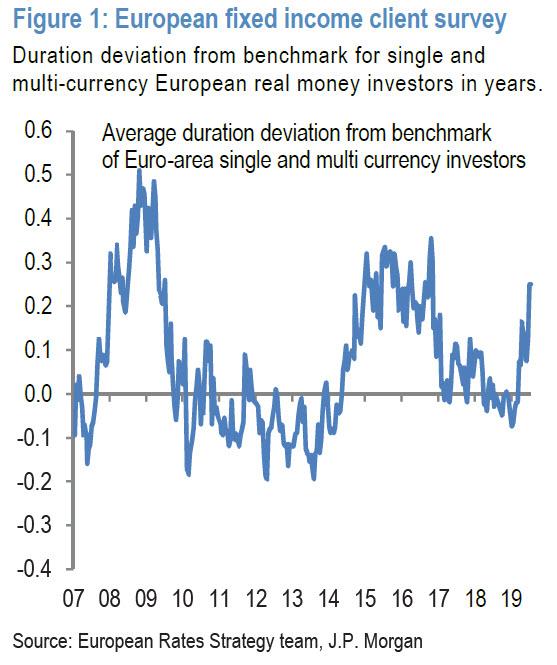

In the government bond space, while not at all time highs, the duration longs implied by European fixed income client survey, whose the most elevated duration longs in four years.

While longs are rushing into both risk and safe haven assets, and pretty much anything that isn’t nailed down, the shorts are getting crushed.

Consider first the chart below, which shows how low the short interest on the biggest US HY ETFs is at the moment, in contrast to the persistently high short interest observed for much of 2018. In other words, relative to last year, investors have closed their short exposure, and added significantly to their net HY exposures, something that is also consistent with the YTD reversal of last year’s HY ETF outflows.

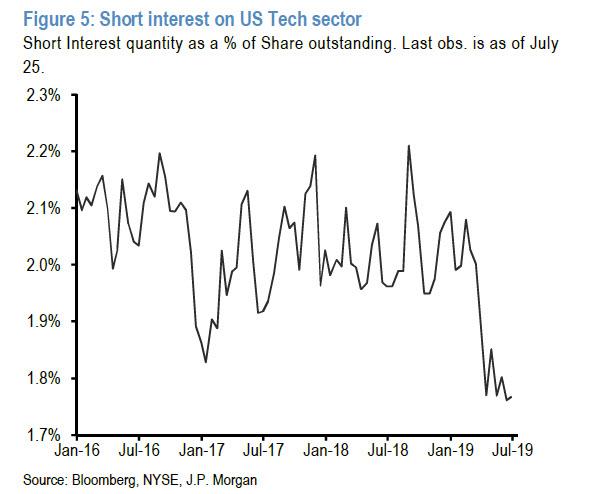

A similar observation can be made in the equity tech space, where shorts have similarly capitulated, “again pointing to overbought conditions for this sector.”

Why is the above relevant? Because as Bloomberg notes, “investors betting the U.S. Federal Reserve is set to extend the market bonanza with a rate cut may have overplayed their hand.”

One such investor is the multi-asset team at Aberdeen Standard Investments, which is preparing for disappointment as it lightens up on equity and emerging-market debt holdings ahead of the Fed’s meeting this week.

“This is an environment where there could be swings in sentiment, and we need to position ourselves for that,” said Ken Adams, head of tactical asset allocation at Aberdeen Standard Investments. “Maybe we won’t see the extent of monetary policy easing that’s now priced in. Investor expectations have become a bit too upbeat.”

Commenting on these observations, Panigirtzoglou writes that “the assets that have benefited from the low yield environment are vulnerable to retrenchment if central banks fail to validate market expectations of easing over the coming months.”

The JPM strategist also notes that whereas the so-called TINA, or There Is No Alternative, argument is often mentioned in client conversations as an argument to keep playing the asset reflation trade even if central banks fail to validate market expectations of easing, he disagrees, and believes that “There Is An Alternative (TIAA) which is dollar cash

which is yielding close to 2.25% (1m T-bills) at the moment well above the 1.4% yield of either the Global Agg bond index or the next high yielder in G10 (1m NZD bills), and above 10y UST yields without taking duration risk.”

And speaking of central bank disappointment, that’s precisely what Morgan Stanley believes will happen if the Fed cuts less than 50bps on Wednesday, something which the NY Fed hinted will not happen when it vocally corrected its president John Williams two weeks ago, when the latter hinted at a double 25bps rate cut on July 31.

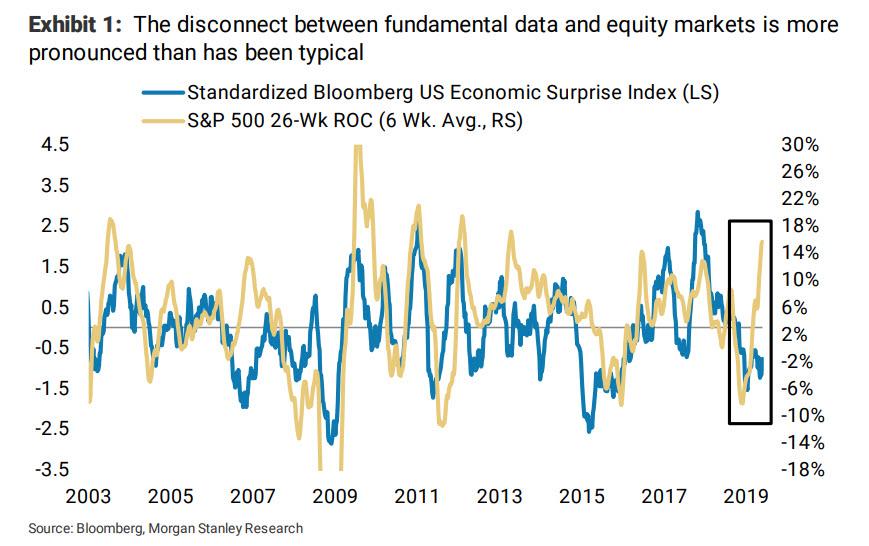

As a reminder, Morgan Stanley also cautioned that the disconnect between fundamental data and actual/promised future central bank easing has never been more pronounced in the equity market…

… and explained that “the growth and market impact of trend-following systematic strategies over the past decade may have driven this sharp divergence.” In this context, Morgan Stanley’s chief equity strategist, Michael Wilson, cautions that “any reversal in stock prices could lead to a faster and deeper drawdown than many are expecting.“

A reversal that would emerge once the Fed cuts by only 25bps, even as a still sizable portion of the market expects at least 50bps of cuts this week…

via ZeroHedge News https://ift.tt/2YqQF6t Tyler Durden

As expected, increased ’dovishness’ by the Fed has gotten markets rallying. Both the S&P 500 and DJIA have touched new highs. From the perspective of late last year, such massive rallies seemed unlikely indeed. While some kind of a Fed pivot was to be expected, the response has been nothing short of “maniacal.”

In March, we noted that markets seemed completely oblivious to the fact that the ability of monetary and fiscal stimulus to uphold economic growth was declining fast and that the momentum of the global economy seemed to be eroding quite notably. But the “monetary drug” administered by the Fed apparently brushed all worries away. Unfortunately, such an artificial remedy only works until it doesn’t.

China on the way down

China has been active on our radar since September 2017, when we realized that it had—almost all by itself—supported the growth of the global (real) economy since early 2009. At that point we also warned that the effectiveness of Chinese debt stimulus was fading fast. During the first part of the current year this issue has grown even more pressing.

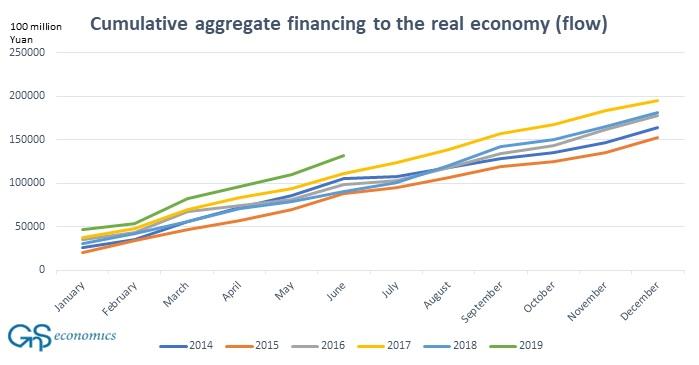

Despite record credit injections and fiscal stimulus (see our June 2019 forecasts for details), Chinese economic growth has remained at sub-par levels. In June, the aggregate social financing of the real economy, again, grew at record pace (see the Figure below), but the response of the Chinese economy was lacklustre, growing just 6.2 percent at an annualized rate. This was the slowest rate since 1992.

As shown in Figure below, the cumulative aggregate financing of the Chinese economy is at record levels with record monthly increases in January, March and June. Even when accounting for the deleveraging of the ‘shadow banking sector’ this is a troubling trend, especially as Beijing has signaled that more deleveraging may be on the way. The Chinese economy is simply not responding to stimulus as before. This implies that the most crucial engine of the global economy is stalling.

Figure. Cumulative aggregate financing to the real economy (flow) in China. Source: GnS Economics, PBoC

Desperation at the Fed

The tone of the Federal Reserve has turned more dovish basically throughout 2019. First, the FOMC panicked at the turn of the year due to rapid and steep deterioration in the stock and credit markets. After that, the Fed has basically turned into a market support machine, and for an obvious reason.

It’s quite clear that if the massively over-valued stock and credit markets crash, so does the economy, and the Fed will be left with little means to stimulate. This implies that even with the (comparatively) robust growth rates of the U.S. economy, the Fed is cutting rates just to support the markets. But this strategy, obviously, only subjects the markets and the economy to ever-greater risks when the economic downturn and market crash eventually arrives. Moreover, as we explained in March, the Fed is trapped. Manic markets go only up or down: there is no “soft landing” in sight.

Recently, a truly ominous “milestone” in market-meddling was reached when the yields of some Euro-junk bonds turned negative. Thus, now even the debt of companies that have a higher probability of default are giving out negative returns to investors! This yield-chasing madness is a direct result of incessant market interference by the Fed and other central banks (see Q-Review 1/2018).

The bailouts and timing

There have been at least three market bailout operations by the major central banks during the past two years. In November 2017, there was a run on the junk bond markets, which was halted by the liquidity injections and asset purchases of the BoJ and the PBoC. In March 2018, the European corporate bond markets froze over, which forced the ECB to step in clear the logjam by further purchases of corporate debt. In December 2018/January 2019, the PBoC and the Fed joined forces (figuratively) to stop the market rout.

As we explained in our June forecasts, the desperate efforts of China and the Fed to prolong the expansion, if continued, may postpone the day of reckoning for few quarters. But, it’s also impossible to estimate how long manic markets will respond positively to monetary stimulus when the real economy starts to crater.

Like manias, panics also start abruptly and often without a clear warning. With its relentless efforts to support the markets, the Fed is inadvertently increasing the likelihood of an abrupt market shock.

With the global economic downturn gathering steam—which will also likely become obvious in the U.S. during the fall—downward pressure on the markets will just keep growing from this point on. It is consequently not outside the realm of possibility that we may be heading toward a cataclysmic market event similar to what was experienced in October 1929.

The central bank fallacy

It remains to be seen whether we will see a supportive rate cut by the Fed next week and the eventual restarting of QE in the event of an unforeseen market event (or even beforehand). The truly worrying issue is that such actions do nothing to solve the underlying issues plaguing the world economy, but, rather, exacerbate them.

Evidence concerning the negative effects of monetary meddling on the drivers of long-run growth, investments and productivity is mounting (see, e.g., our blog on Japan and on the ‘zombification’ of the global economy as well as this, this and this). Further CB meddling, whether effective in supporting capital markets or not, will not just increase distortions, but will likely also cause the economy to weaken further—possibly to the point of collapse.

Central bankers, in their desperation, are playing a dangerous game.

via ZeroHedge News https://ift.tt/2Mmwvbu Tyler Durden