Here in the Battenkill Valley in far upstate New York, the bones of the small towns are still visible while the flesh of the economy that built the towns is now long gone. The Battenkill River runs from the other side of the Vermont line across Washington County to the Hudson River. It’s a swift, clear stream, and back-in-the-day it powered dozens of little factories along its winding way. They made men’s shirts, women’s lingerie, tea trays, ploughs, rye thrashers, boots, paper, and lots more. In a few places you can still find the ruins of these once-grand buildings.

Ruins of the Baxter Marble Mill, later the Bartlett All-Steel Scythe Company

We heard there was a good parade up in Salem, NY, ten miles northeast of here. Salem was a railroad town after 1852. It changed everything for a while. Farmers could send their potatoes and milk all the way to Boston. Slate was abundant nearby and there was a lively commerce in it for roofing and other things. Marble came over from Vermont and was dressed into tombstone blanks, which were sent as far as the Midwest. The railroad itself employed scores of hands in the roundhouse where its locomotives were repaired. This rail connection to distant places and markets must have seemed wondrous.

Waiting for the parade to start in Salem, NY

The system held together for less than 100 years and now it, too, is a ghost presence, along with the factories. History has treated this corner of the country with something that feels like swift injustice. Today, we remain hostages to the automobile, with its geography-negating banality, but you can see the end of that road from here, too, and it is already subject to a very public nostalgia. The Fourth of July parade up in Salem was mostly a parade of motor vehicles: fire engines, EMT trucks, tractors, vintage 1920s flivvers, 1960s muscle cars, one classic hot-rod, and one weird Avanti, a mid-60s product of the then-floundering Studebaker Company — which, ironically, had run a wagon and carriage assembly factory in Salem around 1910, just as cars were being introduced.

These days, even the American Eagle is relegated to sitting in a motor vehicle

The economic history of this place looks like a sequence of great works performed at enormous capital investment, and then quickly trashed for the next new thing. It must have been intoxicating at the time. I’d put the high-tide of it all at about 1900, when all the systems of manufacturing and transport were humming in synchrony. Turns out it was an economy with a surprising purpose: to get rid of itself! And it’s stunning how gone it all is now. What replaced it is not only happening far, far away, but many items made far, far away can’t even be bought within a twenty-mile journey of any town in the county.

I pass through Salem about six or seven times a year for one reason or another. The rather grand old Main Street is usually empty of pedestrians. Only a few of the remaining shopfronts sell useful merchandise so there is no reason to walk down the street. There are several impressive old buildings — skeletons of that ghost economy — clearly falling into terminal disrepair. Yet, on the Fourth of July, the streets were full of life, for a change. Many (like us) had come from far-and-wide. We turned out to show love and respect (and curiosity) for whatever it is this enterprise called the USA is supposed to be now. Mostly, our national situation seems a matter of waiting for various shoes to drop.

The Central House, formerly a hotel, now an evangelical social center

There’s one big advantage to living in this flyover corner of America: it has received next-to-zero of the destructive suburban development overlay that has obliterated the landscape in those parts of the country that can pretend to still be booming.

It is a blessing that I’m keenly aware of. We’re just too far away from the cities, and even from the Interstate Highway network. So, when I behold the economic desolation in these little towns of the Battenkill Valley, I’m aware that, at least, we will not have to dig out from under the burden of the Big Box hell imposed on just about every other place from sea to shining sea, when that economy turns over — a process actually underway now. The K-Mart in my town, Greenwich, NY, shut down in March. When enough of those predatory outfits are gone, someone may get a notion to sell stuff out of our empty main streets shops again. Of course, nobody’s thinking about making stuff that might be sold in those storefronts, but a sense of opportunity may arise quickly as the wind-down of Globalism — and all it implies for local places — becomes self-evident.

via ZeroHedge News https://ift.tt/2RZDF69 Tyler Durden

While Trump has been slamming and badmouthing Jerome Powell before the entire world on his public Twitter account, demanding rate cuts and/or QE, the president has also been keeping periodic tabs on the Fed Chair via brief phone calls, with Powell’s calendar revealing that the two spoke for five minutes on May 20, from 4:42pm to 4:47pm. The call represents the fourth publicly disclosed conversation between the two this year, with May’s telephone call following similar conversations in April and March as well as a dinner meeting in February.

While there were no major fireworks in the market on or around May 20, when the S&P traded down from 2,880 to as low as 2,840…

… the call took place hours before Powell delivered speech at Atlanta Fed conference on financial markets, in which Powell flagged financial stability risks such as record debt, high valuations, leverage and CLO liquidity, and where Powell said the following:

Equity prices have recently reached new highs, and corporate bond and loan spreads are narrow. Both commercial and residential property prices have moved above their long-run relationship with rents, although price gains slowed substantially last year. All of these developments point to strong risk appetite—as might be expected given the strong economy. But there does not appear to be a feedback loop between borrowing and asset prices, as was the case in the run-up to the financial crisis.

One week ahead of the call, on May 14, Trump tweeted his desire for the Fed to “match” what he said China would do to offset economic hardship being caused by tariffs.

According to Bloomberg, Fed spokesman David Skidmore did not comment on what was said between the two.

The conversations came as the president has been attacking Powell for what he views as restrictive interest rates, which he argues undermines U.S. trade deliberations and dampen GDP growth. Just today Trump said that the U.S. “would be like a rocket ship” if the economy had lower interest rates.

President Trump called on the Federal Reserve to lower interest rates after touting the latest job report.

“We don’t have a Fed that knows what they’re doing. … If we had a Fed that would lower rates, you would have a rocket ship” pic.twitter.com/Fzg7Glx9v7

The administration’s frustration at rising interest rates had grown so severe that the White House had reportedly explored the possibility of “legally demoting” the Fed chief.

Briefly addressing those criticisms, Powell said at the Fed’s most recent press conference in mid-June that he doesn’t plan on leaving the central bank anytime soon. “I think the law is clear that I have a four-year term, and I fully intend to serve it,” Powell said at a news conference in Washington.

Asked later at the event when it might be appropriate to publicly address Trump’s criticism, Powell said he doesn’t “discuss elected officials publicly or privately” according to CNBC. The Wall Street Journal first reported on the May telephone conversation between Powell and Trump.

via ZeroHedge News https://ift.tt/2XVPWhK Tyler Durden

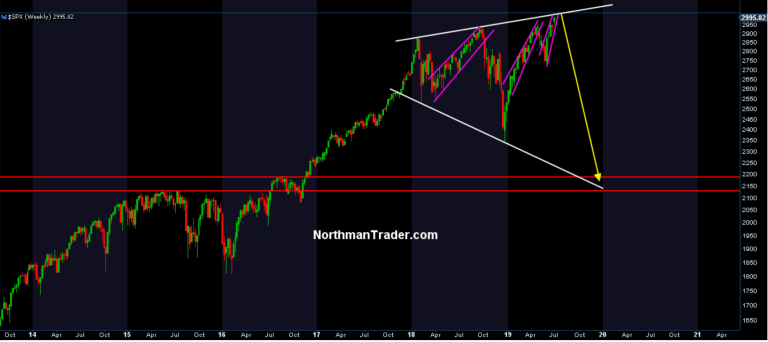

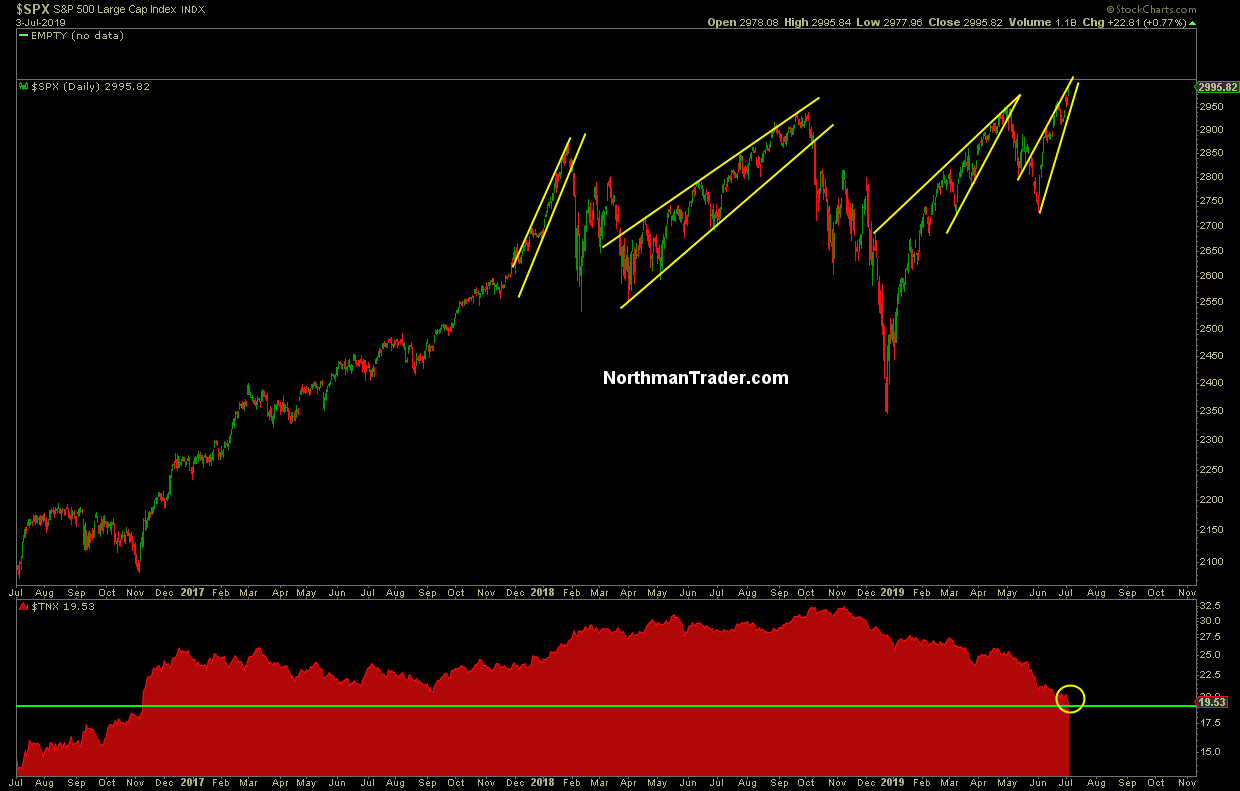

This week we entered the Sell Zone as I called it last weekend. Overnight today $ES hit nearly 3004 and is currently 23 handles lower on the news that the latest NFP report beat while unemployment ticked slightly higher. Whether the sell is now in full swing or more highs are still to come is an open question, after all it’s like arguing with drunks at the bar, you never know what they’ll do next and how far they take the binge. But note what we’re witnessing here is historic but not unprecedented.

The most deceitful time in a cycle is the end of a cycle. Unemployment is low & stock markets keep making new highs despite underlying signals showing reasons for concern which are largely ignored by investors, namely bond yields sinking, yield curves inverting, growth slowing, participation waning, internals weakening. And when that happens new highs may prove to be a great selling opportunity.

I submit we may be seeing all these things now, but perhaps even in a more deceiving manner than ever before.

Why? Because of central banks are desperately trying to extend the business cycle and are thereby distorting markets.

Let’s take note of some facts:

Stock indexes are not making new highs because of revenue and earnings growth. Quite the opposite, earnings growth is negative. The global growth picture is regressive. PMIs have overtly dropped into contraction territory, even in the US key indicators are showing negative growth, durable goods, construction spending, you name it and even employment growth is slowing which is typically what happens at the end of a cycle.

These data trends are reflective of the warning signs coming from the bond market. The German 10 year is -0.4%, The US 10 year has dropped to 1.95%, a full 40% collapse since the November highs (not a single economist had predicted that, they were all above 2.5%-3.5%) and we have inverted yield curves with $13 trillion in global negative yielding debt floating about. Q2 GDP looks to be around 1.3%-1.5% and the NY Fed Nowcast has Q3 GDP currently pegged at 1.2%.

None of these are signs of a healthy expanding economy a point I was trying to make this morning on CNBC:

So why new market highs? Because central banks are desperate to extend the business cycle by any means necessary and right now that is by jawboning markets with more easy money promises of rate cuts and QE, thereby distorting everything. Hence it is no accident that we are currently in a period of asset inflation in everything. Stocks, bonds, high yield credit, commodities, crypto, everything is flying higher. Without economic growth no less, it’s a miracle!

Being forced to cut rates here is an historic absurdity at this point in history and frankly a catastrophic policy failure.

Consider:

Everything central bankers have promised in the past 10 years has turned out to be wrong:

The promised growth has never materialized. In fact this longest expansion in history is also the weakest. And it comes at a very steep price. 105% debt to GDP, highest corporate debt ever, most extreme wealth inequality since the Great Depression. And now we’re running trillion dollar deficits again, the entire economy is held up by debt expansion subsidized by cheap money.

The Fed never met their inflation targets. The dot plot turned out to be a fantasy plot. And now they are looking to cut rates with only 225 basis points to work with at the end of the cycle.

They never normalized policies. For 30 years we’ve seen a consistent trend of lower highs in rates and lower highs in the Fed funds rate. Ever more debt and ever cheaper money is required to maintain the illusion of growth. Meanwhile global debt & wealth inequality have ballooned. Now let’s do it all over again.

What are we doing here, but circling the drain whistling dixie? More cheap money and more debt are the go to solutions that haven’t worked before? And how absurd to want to see the Fed cut rates with unemployment at 50 year lows while running the loosest financial conditions since 1993.

And speaking of 1993, here’s a bit of a historical perspective:

Just to highlight how Fubar this all this:

We’re seeing the loosest financial conditions since 1993.

Back then Fed RAISED from 300bp to 600bp.

Now they want to CUT coming from a low 225bp with historic loose financial conditions still in place.

It’s asinine to cut rates here. pic.twitter.com/Gjzxn0QPpN

So yes, it’s historically absurd to cut rates here. But it reveals an observable truth: The financial system can’t handle the debt it gorged on over the past 10 years. In fact if the Fed were to pursue the 1993 path here everything would collapse. Heck, the ECB can’t even raise rates to get to ZERO or things would collapse. Why do you think it is that the 10 year German bund dropped to 0.4% on the news that Christine Largard would take over for Mario Draghi? Because she’s expected to be Mario on steroids, cutting even more. After all she once called negative rates a net positive for the global economy.

Sure Sherlock:

But hey, economists at the helms of central banks have failed to produce growth, now let’s the give the lawyers a shot, see how Powell and Lagarde legaleeze us through the mess with more rate cuts.

Be careful what you wish for. Fun historical fact: Each time the Fed has cut rates the unemployment was below 4% a recession soon ensued:

Fun historic fact:

Every single time the Fed cut rates when unemployment was below 4% a recession immediately ensued & unemployment shot to 6%-7%.

Again: Every. single. time. pic.twitter.com/OyV8lNkRwz

Now it must be acknowledged that, so far, the Fed and other central bankers have maintained control over equity markets. Dovish promises continue to work, hence we have new highs in market and bottoms are made every time someone like Mr. Powell gives an opportunely timed speech (see June).

Bottomline: We’re witnessing a battle for control between deteriorating fundamentals at the end of a cycle and central banks desperate to keep the business cycle going.

On the technical front we’re watching a multitude of indicators that lead us to believe that these highs may not be sustainable in the current environment and could prove to be a big selling opportunity (see Sell Zone).

One of these indicators is a technical pattern we’ve been tracking for a while, it’s called a broadening wedge, or megaphone, it shows $SPX making a series of lower lows and higher highs:

The premise: If the pattern confirms and fundamentals take control we may see equity markets follow the path that yields have already undertaken: Give back all their gains since the US election in 2016. Indeed the 10 year is already trading back at the levels last seen in November 2016:

What this suggests is that upside risk here is a move into 2990 – 3050 on $SPX and then macro downside risk into 2100-2200. Get a China deal and all this may be moot and delayed, indeed see a sustained move above $SPX 3050, then this setup may be void. But here too I hear a distorted narrative: One the one hand we’re told China tariffs are only a small piece of the global economy, on the other hand a China deal will solve all our problems. I’m sorry, but that’s called playing tennis without the net. But nonetheless there would likely be a relief rally nonetheless on an actual deal. So far we have talk, sometimes less, and sometimes more, seemingly a lot more when markets are down and Larry Kudlow quickly hits the airwaves to try to shore up some confidence as he is again today.

As it stands failure to sustain a move above $SPX 2990 – 3050 and a falling back below 2860-2900 may confirm this technical pattern which suggests 25%-30% downside risk in $SPX.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2NADdNd Tyler Durden

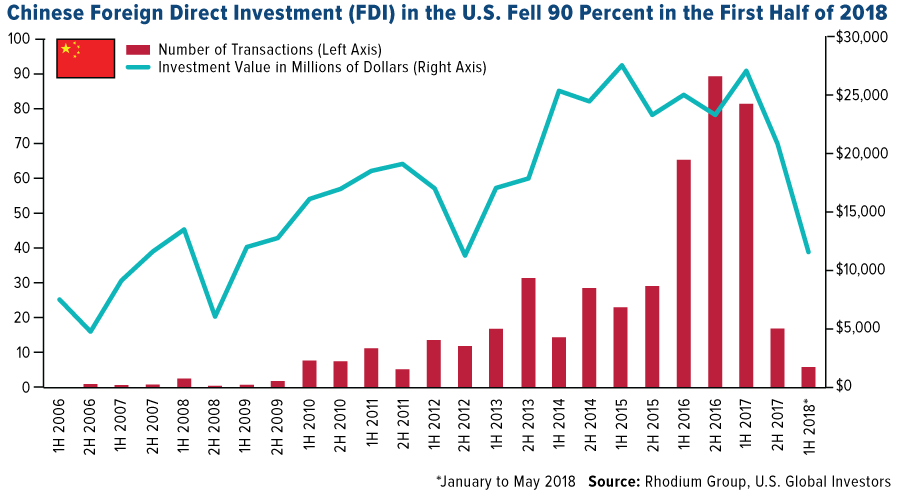

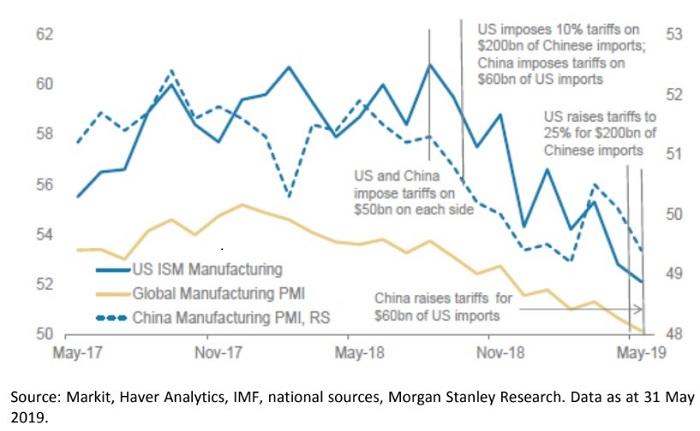

Chinese foreign direct investments in the US, including new factories, has collapsed: down to just $5 billion last year, from $29 billion in 2017 and $46 billion the prior year, according to the Rhodium Group, a New York-based economic research firm with a focus on China.

The US and China trade war has been well underway for one year with both sides imposing punitive tariffs on each other’s goods. President Trump has already imposed a 25% tax on $250 billion worth of imports from China. In a tit-for-tat effort, Beijing imposed 25% tariffs on $110 billion worth of US goods.

The escalation of the trade war has since triggered a significant increase in investments in South and Southeast Asia, but very little in the US, contrary to President Trump’s claims that a trade war would bring companies back to US.

There is some hope that a recent trade war truce between President Trump and President Xi could spark more direct investments into the US from China. But in our opinion, that won’t happen in the near term because a global synchronized slowdown that started before the trade war (1Q18) is being amplified by trade uncertainties, spooking corporate investment and confidence in US markets.

Take, for example, Jushi USA, a supplier of fiberglass reinforcements and fabrics to the bolster the plastics industry in the US, recently opened up a new factory in a deindustrialized part of Columbia, South Carolina, had plans for the second phase of its $400-million project, but had to put it on hold due to the trade war.

About 80 miles to the north, another Chinese businessperson, Zhu Shanqing, invested $200 million into constructing two yarn-spinning plants in a deindustrialize area near Rock Hill.

Shanqing said his new South Carolina mills, part of the Keer Group based in Zhejiang province, along the Chinese coast south of Shanghai, would have employed 650 workers today, not 400, were it not for the trade war driving uncertainties to extremes.

“In the current climate,” he said, “we had to put it on hold.”

The plunge in Chinese investment across the US has been felt the hardest in South Carolina, which has attracted the most investments from China than any other state in recent years.

Over the last decade, Chinese investors plowed $10 billion into greenfield projects in the US, and South Carolina captured 10%, much more than any other state.

South Carolina marketed itself as a state with cheaper operating costs and nonunion labor. To handle increased trade volumes, the port of Charleston made investments and offered incentives to attract global manufacturers, including BMW, Samsung, and Michelin.

This has made South Carolina very dependent on international trade and sensitive to trade disputes.

Joyce Dickerson, chair of the Richland county council, blamed Congress for allowing President Trump to intensify the trade war. She said, “It’s like a domino effect. With a trade war going on, people cannot have stability.”

Dickerson said: “He can’t negotiate with people’s lives like this. His approach is not making America great.”

Trade uncertainty is a lingering unknown and dangerous for corporate sentiment. It has already amplified the cycling down of the US economy and could produce a shock so significant that a recession could form.

via ZeroHedge News https://ift.tt/2YxWj7T Tyler Durden

Georgetown University professor compared the Betsy Ross American flag to a Nazi swastika and a burning Ku Klux Klan cross on Wednesday.

Georgetown University sociology professor Michael Eric Dyson made the comparison on an MSNBC panel discussing Nike’s recent decision to pull a Fourth of July-themed shoe. He made the comparison after host Hallie Jackson asked why people might be upset at the flag’s inclusion on the shoe.

“Words matter. Symbols matter, too. Why don’t we wear a swastika for July 4th?” Dyson asked. “‘Cause, I don’t know, it makes a difference. The cross burning on somebody’s lawn? Why don’t we just have a Nike celebration of the [cross]? Well, because those symbols are symbols of hate.”

The Betsy Ross flag is one of the earliest iterations of the American flag, containing 13 stars to represent the original 13 colonies.

Dyson earlier explained that the flag is offensive because “it hails from the Revolutionary period…which was deeply embroiled in, you know, enslavement,” citing George Washington and Thomas Jefferson as examples of slaveholders. He then explained that “right-wing white supremacists have used it as a rallying cry for their own cause.”

WATCH:

“Right now, this flag has been used by people who wanna pummel African Americans, Latinx, Jews, and other people.”

Earlier this week, Nike canceled the release of the shoe after former NFL quarterback Colin Kaepernick allegedly told the company that the Ross flag is offensive because of its slavery era origins.

That Betsy Ross flag sure fell out of fashion quickly. (Photo: 2nd Obama inaugural, 2013) pic.twitter.com/8xg8xCPLXb

In an email to Campus Reform, Dyson said that coverage of his comments was inaccurate.

“I did not make the comparison. It’s a lie,” Dyson said while referencing a tweet he posted after the segment.

The tweet called on “racists & white supremacists who are using patriotism as a cover” to stop. Dyson also denied making the comparison in the tweet.

In a separate email, Dyson told Campus Reform that he regretted making the association.

“I certainly regret the association. I answered a question about PC culture and used this example,” Dyson said. “I’m even more regretful that the point of the protest/resistance to the flag is lost — its use by bigots to promote their agenda.”

Campus Reform reached out to Georgetown University but received no response in time for publication.

via ZeroHedge News https://ift.tt/2LD89tD Tyler Durden

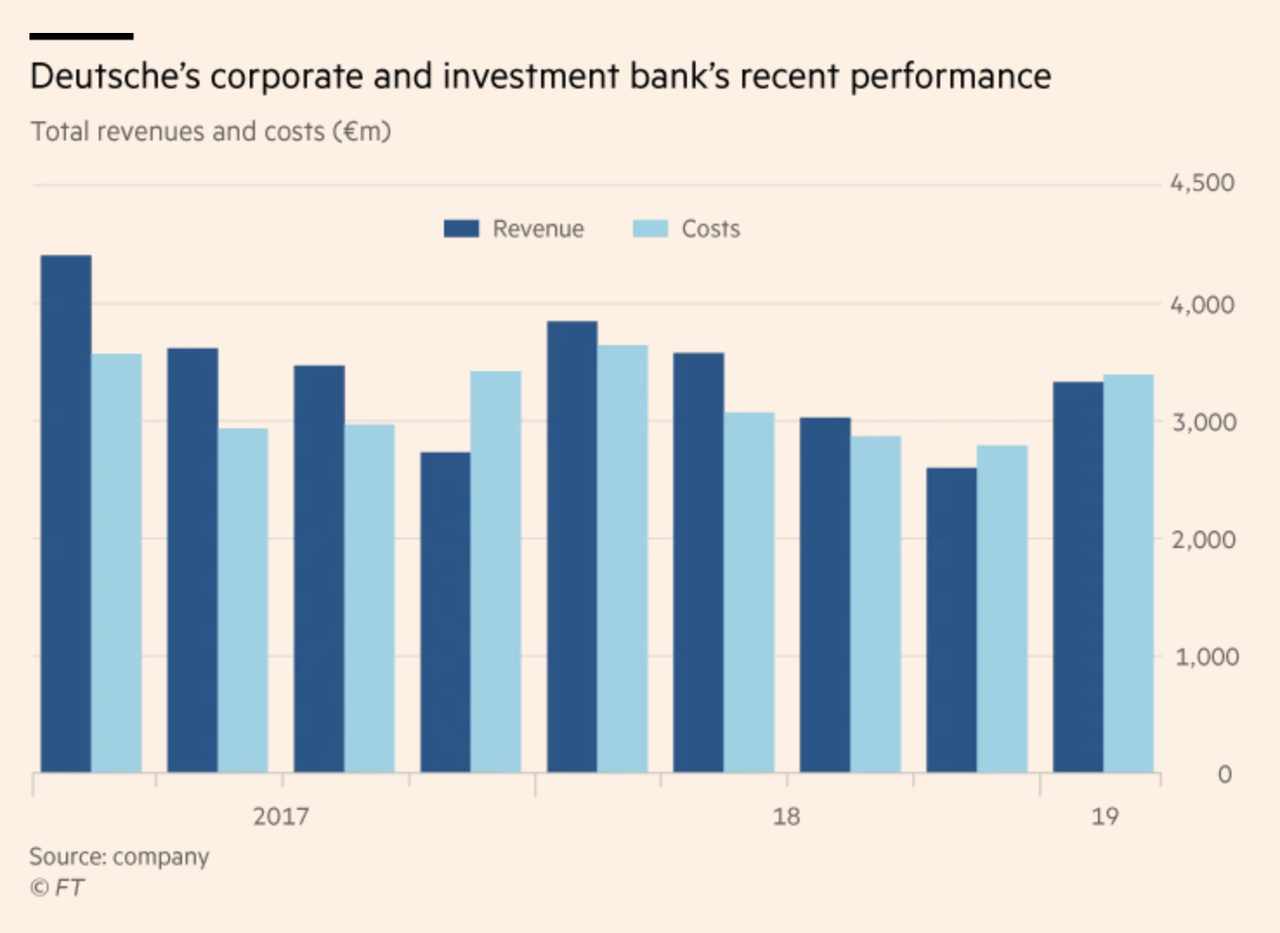

With Deutsche Bank CEO Christian Sewing set to unveil his sweeping restructuring plan to the struggling German banking behemoth’s board on Sunday – a plan that’s expected to focus on brutal cuts to DB’s investment bank – the longtime head of that unit, Garth Ritchie, has reportedly quit, according to the FT.

On Friday, DB said that Mr Ritchie would step aside “by mutual consent”, ending his more than 20-year run at the bank.

But the bank’s mass-firings of both executives and rank-and-file staff are only just beginning.

Garth Ritchie

Though news of Ritchie’s departure was telegraphed well in advance (he was widely expected to depart before Sewing unveiled his turnaround plan to the bank’s board on Sunday), DB has been rocked by some unexpected news that could revive the sense of fear and panic that sent investors running for the exits back in 2016, when many believed a massive DoJ fine might sink the bank.

Echoing a mini-bank run from late 2016 when hedge funds that cleared derivatives trades with the bank started withdrawing excess cash and positions held with the lender, Renaissance Technologies, the giant hedge fund that has been one of DB’s largest prime brokerage clients, has reportedly been taking money out of its prime brokerage accounts with the German lender over the past few months, according to people familiar with the move.

According to Bloomberg, while the secretive quant fund giant remains a major client of Deutsche Bank, it has been quietly moving business to Barclays, Bank of America, and others, according to several sources who weren’t identified. Reps for both DB and RenTech declined to comment when approached by BBG reporters.

Back in 2016, news of the hedge fund bank run sent DB short-term CDS soaring. Though Friday’s news hasn’t had much of an impact on the costs to insure Deutsche Bank debt, that could soon change.

With the head of his investment bank gone and pressure from departing clients mounting, CEO Sewing is expected to take direct responsibility for the unit as he helms what’s expected to be a costly restructuring that could come with a €5 billion ($5.6 billion) price tag and layoffs of some 20,000 – or 1 in 6 – employees across the bank (Sewing will run the investment bank despite coming from a retail-banking background).

According to efinancialcareers.com, Ritchie, who earned €8.2m last year, a larger payday than his boss, had been tasked with ‘refocusing’ the corporate and investment bank in 2018. However, he only achieved 80% of his targets for the year. He has been widely rumored to be on his way out for months.

The bank’s board is widely expected to rubber-stamp Sewing’s plan, which could involve the shuttering or sale of the bank’s US equities business, and other unprofitable or struggling business lines. Sewing’s job cuts are expected to hit the investment bank particularly hard, with the expected elimination of up to 50% of jobs.

Though some believe the job cuts will take place slowly over the course of the next year, one former MD told efinancialcareers that mass firings could happen as soon as Monday, when “Lehman-like” crowds might form outside the bank’s offices in London, New York City and elsewhere.

“You could see Lehman-style scenes outside Deutsche Bank on Monday…It’s very sad what’s happening.”

According to the FT, Chief Regulatory Officer Sylvie Matherat is also set to leave the bank after presiding over an unceasing stream of embarrassing AML losses.

In a farewell email obtained by efinancialcareers, Ritchie said DB’s corporate and investment bank had been his “home for almost half my life and nearly all my work working career.”

“I have thoroughly enjoyed my time here, even the challenging moments,” Ritchie said, adding that he has made many friends at the bank.

To be sure, if Sewing’s restructuring fails to right-size the struggling bank and clients continue to pull their money, the Lehman-style failure could follow in the not-too-distant future.

via ZeroHedge News https://ift.tt/2XnqOMo Tyler Durden

If you have spent literally any time arguing against western imperialism in any public forum, you have had the experience of being accused of “supporting” one of said imperialism’s targets. If you argue against regime change interventionism in Syria, you’ll get accused of being an “Assadist” or “Assad apologist”. If you argue against regime change interventionism in Iran, you’ll you’ll get people saying that you “support the Mullahs”. Enter into any debate of sufficient liveliness and it’s only a matter of minutes before it happens.

There was a meme going around at the height of the most recent failed coup attempt in Venezuela depicting a white, pink-haired socialist placing their hand over the mouth of a dark-skinned Venezuelan and saying “ACKSHUALLY, MADURO IS THE GOOD GUY”. Proponents of the Trump administration’s attempts to topple the Venezuelan government would share this meme in online debates with anti-imperialists as a way of accusing them of whitesplaining to Venezuelans that they should support an evil dictator who is oppressing them. The idea being, of course, to silence those dastardly socialists using the socially progressive value system they claim to uphold. Checkmate, leftists.

There are obviously a number of things that are wrong with this meme, including the skin pigmentation of the average Guaido supporter, the implication that all Venezuelans oppose Maduro, and the suggestion that only white western leftists oppose the Trump administration’s attempts to install a puppet regime in the nation with the largest proven oil reserves on the planet. But the dumbest thing about it is the implication that someone who opposes US regime change interventionism could only be doing so because they believe that Nicolás Maduro is a “good guy”.

The reason debates about western imperialism so frequently get bogged down by moronic arguments about “good guys” and “bad guys” is because human storytelling devices train us from an early age to constantly frame narratives in those terms. Everything we’ve been taught by TV and movies tells us that if a conflict is happening, someone in it must be the protagonist and someone must be the antagonist, and that our job is to figure out which one’s which.

For as long as humans have been telling stories, this is how they’ve been doing it. A hero wants something, has some kind of adventure trying to get it, but a villain tries to stop them. It’s a recipe for exciting storytelling that’s been used since time immemorial, and it works because the standard human ego is structured to spin mental narratives about itself as the central character whose wants are constantly being fulfilled by friendlies and thwarted by hostiles. Almost every story from the earliest prehistoric campfire circles to the latest Hollywood blockbuster has in essence been nothing other than a storyteller using a simple mind hack to attract the interest and attention of their audience, just by making their narrative relatable using the protagonist/antagonist framework which the ego finds so appealing.

We’re always the hero in our little ego narratives about our day-to-day lives. We like people who do things we want and we dislike people who do things we don’t want. We stand transfixed by our babbling mental ego narratives, so we find any similar external narrative mesmerising in the same way.

But it’s just an illusion. There are no “good guys” or “bad guys” in real life, either in our personal lives or in international affairs. There are just people. Some of those people do things we like more often than they do things we don’t like, and vice versa, but that’s not a matter of whether they’re “good” or “bad”, it’s a matter of our personal preferences and how we think people ought to behave. “Good” or “bad” isn’t written on anyone’s DNA or inscribed above their heads upon the fabric of reality; we made it up.

In reality, it’s very possible to oppose US regime change interventionism in Venezuela without having a single thought ever appear in your head about whether or not Nicolás Maduro is a “good guy”. American-led regime change interventionism has a well-documented and historically undeniable history of increasing suffering and death in the nations in which it takes place, and consistently fails to accomplish what its proponents claim it will. You don’t need to have any opinions about who Maduro is as a person to recognize this self-evident fact and oppose yet another US regime change campaign in yet another oil-rich nation.

To preempt the inevitable Godwin’s law counter-argument here, of course it’s useful to discern individual behavior patterns in people and talk about what specific patterns they tend to exhibit. Of course it’s useful to recognize that Hitler did many things that we should always oppose going forward. But notice how the only reason Godwin’s law exists is because the “good guys versus bad guys” dichotomy allows people to associate anyone who opposes their side with Hitler, thereby marking them as the “bad guy” side in a given debate. That’s all anyone who fulfils Godwin’s law is ever trying to do.

It’s very useful to pay attention to the specific behavior patterns of specific individuals, and to make distinctions as to whether or not those behavior patterns are desirable or undesirable to you. But it’s also very useful to understand how the “good guys vs bad guys” dichotomy is leveraged by those who seek to control our thoughts and perceptions.

Think about it: where are we trained to look for heroes in real life? Soldiers and policemen, the violent enforcers of the status quo. Politicians like Donald Trump or Bernie Sanders, depending on which side of the fake partisan divide you’re on. And where are we trained to look for villains? Dictators and rule-breakers, and people who are on the other side of the illusory partisan divide.

Awful convenient for those who benefit from maintaining the status quo, no?

There is one direction in which we are very seldom trained to look for a superhero to come to the rescue, and that’s within. The notion that we ourselves might be the real agents of change in this world is downplayed by the propagandists who fear a surge in populism more than they fear anything else in this world.

Much better to keep people focused on polarizing figures like Donald Trump, who most people seem incapable of viewing as anything other than either a Deep State-fighting superhero or a Hitler-like supervillain whose actions are either all pure good or all pure evil. Divorced from the “good guys vs bad guys” dichotomy, this administration’s behavior can be described in the same way as its predecessors: mostly violent and oppressive with a few helpful things mixed in. Yet it’s rare to find anyone who is capable of discussing Trump outside of the false dichotomy.

And the same would be more or less true of whoever Trump winds up running against in 2020. Even if by some miracle Bernie Sanders or Tulsi Gabbard overcome the rightward-slanted DNC nomination process and go on to beat Trump in the general election, they will with absolute certainty advance many of the destructive agendas upon which the US empire is built. They are not heroes either. This doesn’t mean they’re villains, it just means that “heroes versus villains” is an illusion we’ve been trained since our earliest media-consuming days to buy into.

The world makes a lot more sense when you peel away the lens from your eyes which perceives life in neat little Hollywood-shaped narratives with protagonists and antagonists and clear beginnings, middles and ends. Because it turns out that we’re all actually a bunch of confused primates doing the best we can with the wildly unique and incredibly complex sets of conditioning we’ve been dealt by our individual birth circumstances and life events. The “good guys versus bad guys” dichotomy is just imaginary conceptual overlay on top of a giant biological storm which carries on in cool indifference to our puny little egocentric narratives.

Atoms swirl, cells cluster, and life lifes away as this strange new species stumbles around trying to make sense of the world with its recently evolved extra gray matter and the capacity for abstract thought which comes with it. It has some successes and many failures in trying to figure out how to make living on this spinning rock a little more harmonious, and it will either succeed or it will fail. It’s egoically comfortable to slice this dance up into a narrative about heroes and villains, good guys and bad guys, but it’s really all one twirling, churning, chaotic and beautiful dance.

* * *

The best way to get around the internet censors and make sure you see the stuff I publish is to subscribe to the mailing list for my website, which will get you an email notification for everything I publish. My work is entirely reader-supported, so if you enjoyed this piece please consider sharing it around, liking me on Facebook, following my antics onTwitter, throwing some money into my hat on Patreon orPaypal, purchasing some of my sweet merchandise, buying my new book Rogue Nation: Psychonautical Adventures With Caitlin Johnstone, or my previous book Woke: A Field Guide for Utopia Preppers. For more info on who I am, where I stand, and what I’m trying to do with this platform, click here. Everyone, racist platforms excluded, has my permission to republish or use any part of this work (or anything else I’ve written) in any way they like free of charge.

Former Vice President Joe Biden proclaimed that Russia didn’t meddle in the 2016 US election, apparently forgetting the narrative.

Speaking with CNN‘s Chris Cuomo, the 2020 presidential contender insisted that the Kremlin’s evil designs to influence geopolitical outcomes wouldn’t happen under his watch, and didn’t happen when he and President Obama were in the White House.

“Look at what’s happening with Putin,” said Biden. “While Putin is trying to undo our elections, he is undoing elections in Europe. Look what’s happened in Hungary. Look what’s happened in Poland. Look what’s happened in Moldova. You think that would happen on my watch or Barack’s watch? You can’t answer that, but I promise you it wouldn’t have, and it didn’t.”

Biden’s comments are particularly intriguing, as many – including President Trump – have questioned why the Obama administration didn’t do anything about Russian interference prior to the 2016 election.

The reason that President Obama did NOTHING about Russia after being notified by the CIA of meddling is that he expected Clinton would win..

In May, Trump brought it up again, tweeting “Why didn’t President Obama do something about Russia in September (before November Election) when told by the FBI?”

Why didn’t President Obama do something about Russia in September (before November Election) when told by the FBI? He did NOTHING, and had no intention of doing anything!

A math teacher says she has lost her job at a private school in Southern California for speaking out in defense of Western Civilization – even though she made her comments outside the classroom.

Dr. Karen Siegemund, president of the Los Angeles-based American Freedom Alliance, gave a speech in May at the group’s “Long March Through the Institutions” conference, which “explored the Left’s ongoing multi-decade takeover attempt of numerous public and private institutions to effect a radical transformation of America.”

During her speech, she said “each of us here believes in the unparalleled force for good that is Western Civilization, that is our heritage, whether we were born here or not.”

“It’s kind of shocking, isn’t it,” Siegemund told Mike Huckabee in a recent interview about the experience, noting she has been a teacher for almost 20 years.

“Because of my outside activities, I was told my contract would not be renewed. I praised Western Civilization, and how it’s brought the greatest good to the most number of people, and we are all its beneficiaries, including those not even from here, and that was deemed hostile,” she said.

Huckabee said he thought there might be something more to the story:

“Surely you did not just get fired just because you believe in Western Civilization?”

“No, I did,” she replied.

“I see myself as an educator,” Siegemund added, “and I want all my students to learn critical thinking, to explore, to be skeptical, to value those things that we value, to grow as an individual, that’s always been my stance, which I guess is also problematic. Because there are other teachers who denigrate the president in the classroom, who wear ‘resist’ T-shirts, who promote all kinds of various leftist policies in the classroom — that’s apparently fine — because their contracts have been renewed.”

“I even hesitated to wear anything with an American flag, not hesitated — I did not wear anything with an American flag on it — for fear of that being sort of too subversively patriotic … But I have promoted freedoms and independent thought.”

Apparently the conference might have been the final straw. But Siegemund has launched a GoFundMe page and says she plans to fight the “unfair termination.”

“I am just standing up for what I believe is right,” she told Huckabee.

Her story has resonated with several observers, including on Ricochet and PolitiChicks.

via ZeroHedge News https://ift.tt/2LCSQ45 Tyler Durden

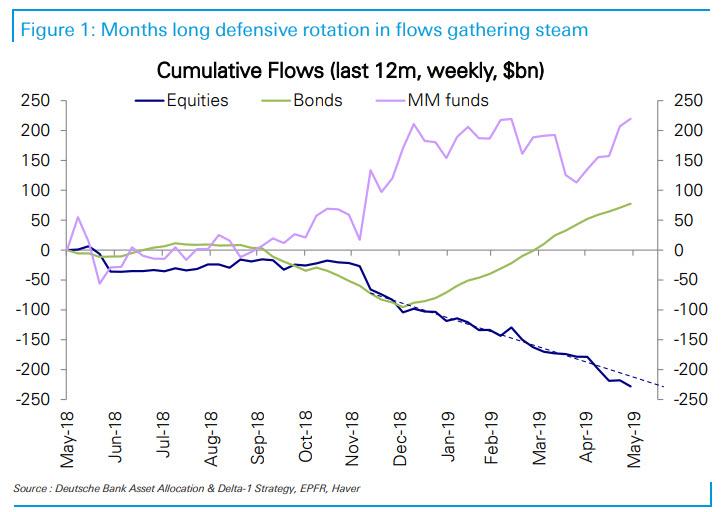

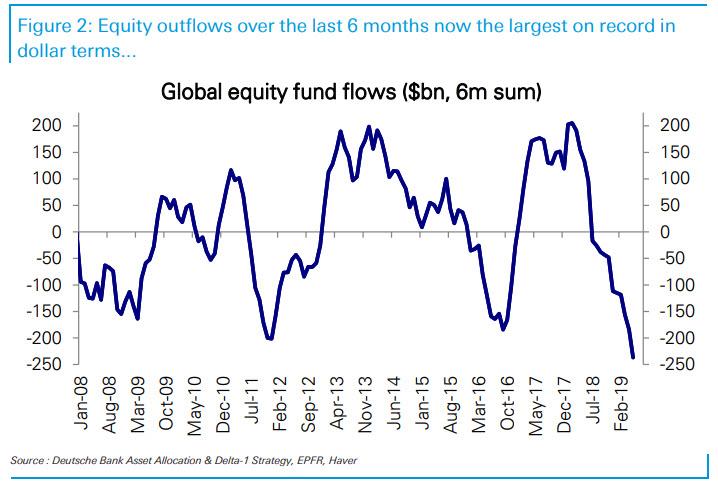

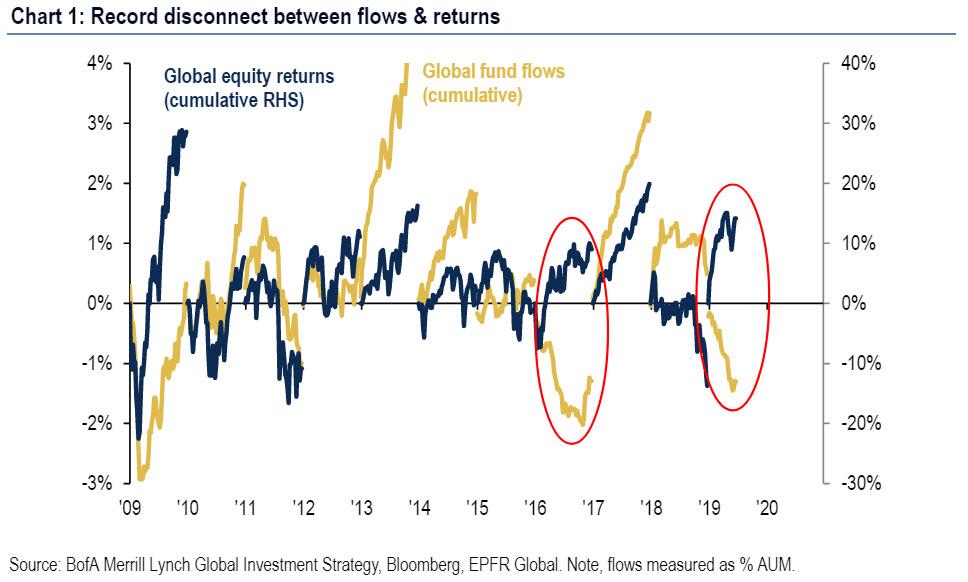

For much of 2019 we have highlighted what we said was the market’s biggest paradox: one where the higher the market rose, the more money investors would pull out of equities, and allocate to bonds.

It culminated several weeks ago when , even as the S&P hit new all time highs, outflows over the last 6 months in dollar terms surpassed the previous record observed over any prior 6-month period.

And, according to EPFR, last week was no difference: just as S&P futures hit 3,000, there was more of the same with Bank of America noting a continuation of the familiar “Risk-off flows” as $6.3BN was allocated to bonds, while a whopping $15.1BN was pulled out of equities, resulting in a new record YTD total of $229BN into bonds, while $154BN was pulled out of equities.

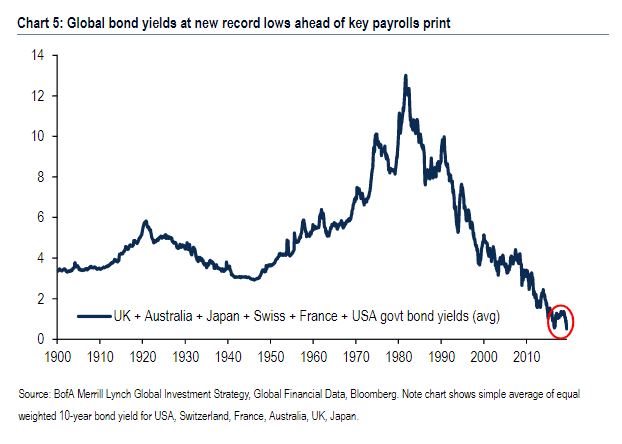

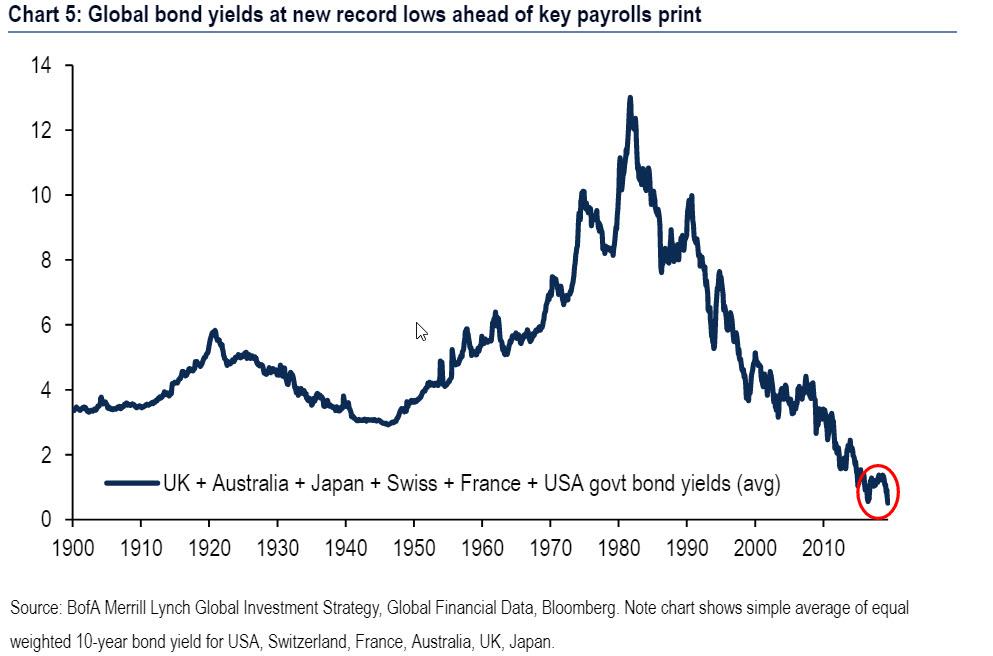

The ravenous appetite for yield – Friday’s post-payroll revulsion which sent the 10Y yield surging from 1.94% to 2.06% in a VaR shockingly quick amount of time – has resulted in global bond yields tumbling to new record lows on Friday.

All of the above means one thing: as BofA’s Michael Hartnett writes, there is now a record disconnect between flows & returns in 2019, with only 2016 a similar year in terms of outflows/returns.

Yet while it is clear that something is clearly broken in the market, where investors don’t believe for a minute that the market’s record gains are sustainable and are cashing out at a record pace, there is still confusion as to what is causing this divergence.

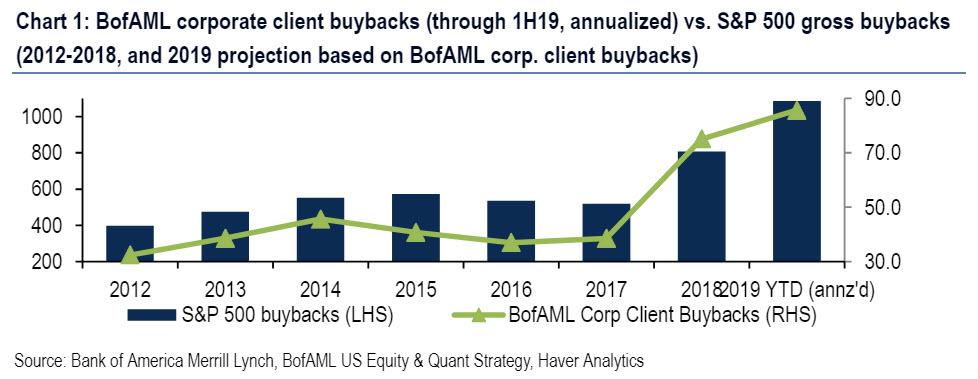

To be sure, the primary culprit we have discussed previously, remains corporate buybacks with BofA pointing out that buybacks remains the #1 source of market support in 2H’19, especially after US banks announced $129bn buybacks next 4 quarters.

In a separate report, BofA also points out that buybacks ordered by its clients are on pace for a record at $43bn in 1H19 vs. $75bn in full-year ’18. This suggests we will see a record, over $1 trillion in S&P 500 buybacks this year (as BofA client buybacks have historically represented ~8% of total S&P 500 buybacks).

And yet, while it is perfectly reasonable to “explain” the market’s record levitation amid investor outflows with price-indiscriminate purchases by corporations themselves, this explanation felt lacking to SocGen, which when observing the $200 billion investor exodus in European stocks coupled with the rally in European stocks, concluded that this paradox is structural.

The issue is familiar – instead of the US, the market in question is Europe, where love for local equities, given the constant redemptions from the region’s stock funds, is lacking to say the least. And yet, at the same time, market gains have pushed up the value of Stoxx Europe 600 Index members, adding as much as $1.5 trillion this year alone.

According to SocGen’s Roland Kaloyan, this is not so much due to buybacks – as Europe has had far less than the US – but rather due to money managers switching from regional to global stock funds, giving them exposure to European equities, but as part of an international portfolio.

“The trend in asset management industry is that funds are exiting traditional regional funds dedicated to the U.S. and Europe and reallocating to global funds,” Kaloyan told Bloomberg.

Such a shift away from regional to international funds in the past three years – which has resulted in withdrawals of $200 billion from European stock funds in the period – is expected to continue as asset managers focus on getting exposure to global industry leaders as opposed to specific geographic locations, according to SocGen. He believes that future exchange-traded and mutual funds will need to be predominantly global to attract investor appetite.

SocGen recommends staying away from small-cap European stocks since this segment is less liquid and more sensitive to fund outflows than larger companies.

“In global funds, investors get exposure to large multinational European corporations. This year’s rally has been driven by quality names and it was driven by global portfolio managers, not regional ones,” said Kaloyan.

Furthermore, this switch from regional funds to global ones also leads to a reassessment of sector valuations, according to SocGen, as stocks that looked expensive within the European equity universe – such as consumer staples – no longer do so within the global space.

So is the explanation of why there has been record outflows from equity funds in Europe just because of adjusting of industry rather than geographic preferences? Perhaps, although that would not explain why the US has similarly suffered from massive outflows, because fund flows between those two nations would be more or less a “zero sum” total. And yet the fact that there continues to be massive outflows from the US and Europe and Asia, and inflows in fixed income suggests to us that SocGen is – sadly – wrong, and that instead of focusing on industries, investors simply want less risk exposure, and as a result are flooding into safe havens such as government bonds (although on days like today when the market is violntly repricing its rate cut expectations, it is probably wiser to replace “flooding” with “dumping”…

via ZeroHedge News https://ift.tt/2YzdIgj Tyler Durden

{kind=link}