Obama Turns John Lewis Funeral Into Political Rally Tyler Durden

Thu, 07/30/2020 – 18:20

Former President Barack Obama turned a eulogy for the late Rep. John Lewis (D-GA) into a Democratic political rally – urging Congress to pass a series of measures he said would ‘continue Lewis’ life’s work.’

Of all the speakers at the memorial, the former President was the only one to leverage Lewis’ death for political purposes.

Obama’s proposals included:

– Automatic voter registration.

– Congressional representation for Washington D.C. and Puerto Rico.

– Making election day a federal holiday.

– Ending gerrymandering.

– Replacing the 1965 Voting Rights Act which would restore federal supervision over state efforts to pass election reforms.

– Ending the Senate’s filibuster rule (famously used by Hillary Clinton‘s mentor, Sen. Robert Byrd (VA), against the GOP’s 1964 Civil Rights Act).

“You want to honor John? Let’s honor him by revitalizing the law that he was willing to die for,” Obama said, while later likening President Trump to segregationist Democratic Gov. George Wallace of Alabama, and the police to Civil Rights-era law enforcement officers beating blacks across the South – condemning “sending agents to use tear gas and batons against peaceful demonstrators.”

Wow, Barack Obama is delivering Lewis’s eulogy & this MF had the nerve to call out federal troops teargassing protestors AS IF HE DIDN’T DO THE SAME THING IN FERGUSON & BALTIMORE LOL

We can only imagine the response if Trump used a Republican’s funeral to propose GOP policies.

Watch:

In his eulogy for John Lewis, former Pres. Obama proposed a swath of voting rights expansions, including:

– Automatic registration

– Adding polling places

– Expanding early voting

– Making Election Day a holiday

– Eliminating the filibuster, if necessaryhttps://t.co/sVteeuYRLupic.twitter.com/sbFTOt1ss6

The Federal CARES ACT passed in March protects renters living in properties with government-backed mortgages from eviction until July 25. While the intent of lawmakers might be to protect what they consider the most vulnerable in our society this sends a grave signal to landlords. Halting evictions cuts away at the very fabric of contracts to lease property and undermines the rights of owners. Ironically in the end this will most likely put more pressure on low-income tenants and result in higher rents.

In the same way, rent controls have proven detrimental to controlling housing markets governments efforts to protect renters from eviction may result in unintended consequences. What seems by many a noble pursuit will cause many landlords to exit the business or take rental units offline. The government’s action of halting evictions could be seen as an extension of current policies that sidestep dealing with the problem that society is creating a growing number of irresponsible tenants. The ugly fact is that government housing cherry-picks the best of the low-income renters providing them with very low rents and nice apartments. The rest they dump on the private sector.

Now that theeviction moratorium has expired, the covid pandemic predicts a wave of evictions is about to take place. The Urban Institute estimates the with the expiration of the eviction moratorium more than 12.3 million or 28 percent of America’s 43.8 million renters are at risk of losing their homes. Landlords that have had enough have begun an unsavory part of their job filing eviction paperwork for tenants who haven’t paid rent for 30 days or in many cases, months. This, of course, comes just as some 25 million Americans are about to lose the generous weekly $600 federal unemployment checks.

Unfortunately, the clowns in Washington are busy playing politics with this.In remarks outside of the White House on Wednesday, Trump and Treasury Secretary Mnuchin acknowledged that while the administration and Democrats remain far apart on any kind of deal. This resulted in them pushing for the extensions of both programs. Trump emphasized that halting evictions and keeping people in their homes has become a priority. A big part of the problem is that letting people remain in the property without paying rent does not stop the bills a landlord must pay from coming due. This rapidly makes being a landlord a money-losing proposition.

80% Of New Units Are High-End Luxury Units

This all adds to the feeling everything is a bit off. It seems reality is starting to hit home assoaring rental costs collide with the fact overall disposable incomes have rapidly eroded for the middle class. The main driver of soaring rents seem to be following new building costs, in particular, land, material, and hard costs mostly driven by labor make it harder to build new buildings at a reasonable cost. This has resulted in some investors moving away from new construction and into remodeling older units which also raises the rents on current tenants ever higher.

Ultimately higher costs for taxes, local fees, utilities, insurance, maintenance cost, general labor, and just about everything will be passed on to the renter. While the market has responded to rental housing needs for higher-income households, there are alarming trends that suggest a growing inability or desire to supply housing that is affordable for middle- and working-class renters this becomes very noticeable when we look at the population with very low incomes. Developers have displayed little interest in, or they simply can’t afford to add anything but luxury units.

There’s a huge unhealthy disparity in high-end rents versus low-end rents across the country and with building cost being similar between constructing high-end versus low-income units why would anyone want to deal with the low end of the market and all the trash that comes with it when you consider that;

Our government has been busy encouraging people who have no business owning a house to buy one regardless if they have any idea of how to maintain it. This government policy is to generate a slew of programs geared to assist first-time home-buyers and others with special incentives and aid. This often means anyone with any kind of credit and even getting all their income from government programs often move out of apartments to buy a house. This creates higher turnover rates and leaves the apartment manager forced to lease the unit to someone with even less income or no credit.

Another part of our government’s housing policy funds and determines what is built, the problem is a massive amount of money is flowing into apartments that most people cannot afford. Low-interest rates coupled with speculators using “Wall Street” money are creatively financing these units out of thin air. From somebody that knows the industry, you can take it to the bank that it will not end well when these new units go online and are unable to meet income projections. A while back, an article in Business Insider warned the US apartment market has become overdeveloped, with supply outpacing demand, especially in the most expensive segment of the market but that has not slowed building.

Building and providing housing to low-income people often proves to be a thankless job that nobody wants. This is beginning to put a great deal of pressure on the system as private sector landlords that do not partner with government programs suffer the abuse. Simply put, government housing policy has failed to address the housing needs of the growing group of dysfunctional individuals that are the bane of society. Few honest people desire to put up with the endless crap such a position constantly dishes out. Inventing market terms such as “sub-luxury segment” to describe basic housing only confuses the issues that need to be addressed.

Housing Policy Throws Older Units “Under The Bus”

The government holds huge responsibility for a rising share of our housing problems in low-income situations because its policies ignore the reality many tenants are simply irresponsible. The main reasons for most evictions center around people not following the rules, damaging an apartment, or not paying their rent. By making anyone with an eviction on their record “ineligible” for most housing programs the government shrewdly and cleverly has sidestepped having to deal with these people. Even with close to half (47%) of all renter households (21 million) pay more than 30 percent of their income for housing, including 11 million households paying more than 50 percent of their income for housing, it is not enoughwhen we are talking about “low incomes” and the amount of damage and grief they dump upon their landlords.

By bending over backward in an attempt to “protect the consumer” the government and courts are creating an army of irresponsible people who go through life exploiting “the system.” We have even have gone to where tax money is being used to pay the legal fees of tenants wanting to fight the very landlords they have wronged. The government has even made it much harder to check the credit of someone wanting to rent claiming it is to protect the potential tenant’s privacy. This ignores the fact those renting an expensive piece of property are putting themselves at great financial risk.

Landlord claims are usually pursued and disputed in the small claims division of the court where getting an eviction or judgment against a bad tenant has become increasingly time-consuming and expensive. Adding to this ugly reality are limits that often allow only a fraction of a landlord’s loss to be covered, these can be as low as $1,500. It is not difficult for unpaid rents and damages to greatly exceed this amount. It must be noted that getting a judgment in your favor does not mean it will ever be paid and that these people continue to move from place to place causing havoc wherever they go.

Stories that delve into what is happening in our communities are important, I consider them as “micro-economic” images of what is occurring in many places across America. A show on Netflix titled “Renters” looks into the misadventures of property managers and their troublesome renters in New Zealand. It reveals similar housing problems exist in many countries. My attitude may be skewed by living in one of if not the lowest rent areas in America. A ZeroHedge article stated that “attractive rents” are a relative term as the monthly dues for a tiny studio apartment in NYC will still run you $2,681, or $64.92 per sq. ft.we’re pretty sure that implies the average studio is roughly 495 square feet…or about the size of the average living room in all those “fly-over states” that elitist New Yorkers love to look down upon. The fact is, rents in my area are often as little as $650 a month for a two-bedroom one-bath 950 sq. ft. apartment. This is far less for essentially the same product.

Footnote; I may have understated how much regulations also add to higher rents. In some states, the government is even debating putting the burden and responsibility for keeping occupied units clean upon the landlord. Also, it is not possible to evict someone during the Christmas Holidays in my area for any reason, you can file but no action will be taken until after the holidays are over. One way to address or level the playing field would be to move away from public housing and give those needing housing aid “rent only vouchers” that could be used with any landlord rather than putting these people into a quasi-government ran project. More on the subject of evictions in the article here.

via ZeroHedge News https://ift.tt/3fbsTnD Tyler Durden

First-Ever Electric Hummer Debuts This Fall, Faster Than Tesla Model 3 Tyler Durden

Thu, 07/30/2020 – 17:40

GMC is set to unveil the first-ever all-electric High Utility Maximum Mobility Easy Rider, otherwise known as Hummer, this fall.

“The First-Ever GMC HUMMER EV has zero limits, and our open-air design provides powerful proof. For the unique open-air experience, easily remove the four roof panels and front T-bar to let the world in. We’ll continue to keep you informed as we prepare to show the world our revolutionary all-electric, zero emissions, zero limits super truck,” GMC’s website said.

GMC makes some very impressive claims, first, it says the new electric Hummer will have 1,000 horsepower, able to rocket the vehicle from 0-60 mph in 3 seconds. Now, wow, that’s supercar fast, if true…

A press release by GMC said the “all-electric super truck” would be unveiled to the public this fall and “will begin production in fall 2021.”

“GMC announced today that its all-electric super truck will debut later this fall and will begin production in fall 2021. Details about the GMC HUMMER EV’s remarkable on- and off-road capabilities will be shared closer to its reveal,” the release said.

Not much is known about the design, but here are some behind-the-scenes shots of what the unfinished all-electric Hummer looks like.

A promotional video of the new electric vehicle was recently released.

The electric Hummer appears to be faster in 0-60 mph takeoff than the Tesla Model 3 Performance.

via ZeroHedge News https://ift.tt/3gem2uZ Tyler Durden

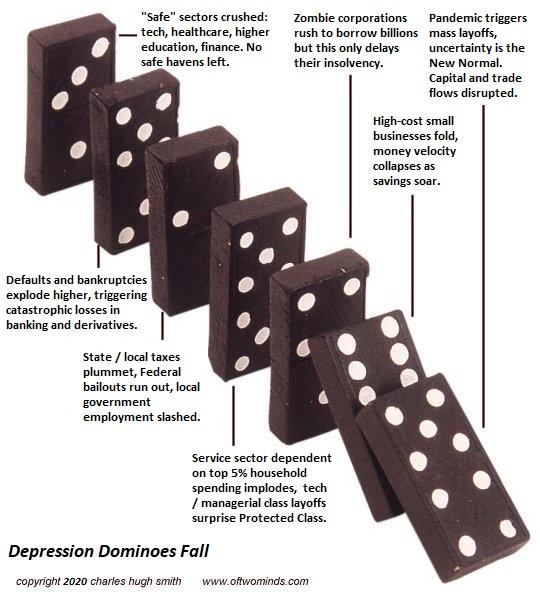

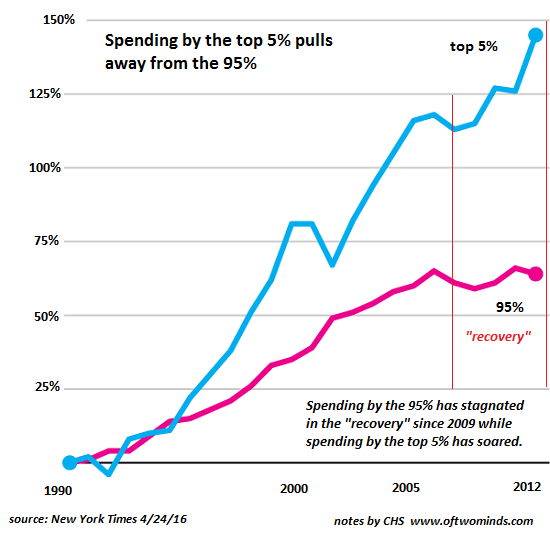

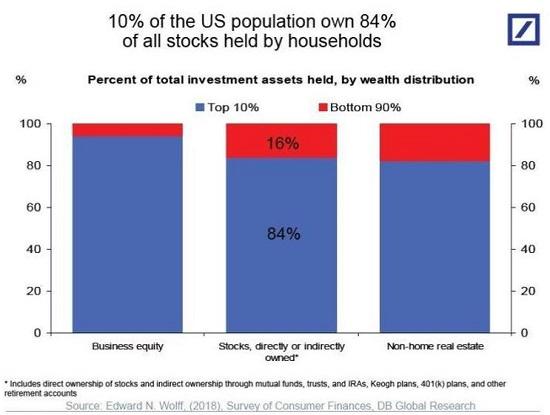

No federal bailout or stimulus can reverse these three dynamics, and no amount of legerdemain can replace the spending of the top 10%.

Few of those anxiously seeking a rebound in consumer spending take into account the top 10% of households account for almost 50% of consumption, and that top 10% skews heavily to the older, wealthier top tier whose free-spending ways have been built on the enormous wealth effect as their stocks, bonds and real estate assets have soared in value over the past 12 years.

The top 10% has largely escaped the significant financial hits cutting a swath through the bottom 90%, but that’s about to change. Few of the top 10% have seen their pensions cut, their portfolios of stocks and bonds shredded, their home value in free-fall or their managerial / technocrat position eliminated. Most are watching the financial devastation from the security of owning 85% of the nation’s assets, and from positions in the protected-class with access to federal money, either directly or indirectly.

Three factors could materially suppress the future consumption of those responsible for 50% of all consumer spending.

1. Age-related caution about exposure to the virus. Not only are many of the top 10% older, many of these households are caring for parents in their 70s, 80s or 90s. Given the heightened risks for these demographics, is it really worth it to go into crowds for entertainment? The short answer is no. Furthermore, these older, wealthier households have been there and done that— foregoing cruises, air travel, fine dining, live music, etc. is not that much of a sacrifice, as they’ve enjoyed all these niceties for decades.

2. As corporate revenues and profits continue sliding, the managerial / tech class will start getting culled. All sorts of positions that looked “essential” before the pandemic are suddenly on the chopping block.

3. The wealth effect is about to reverse as the Everything Bubble finally pops. With the Nasdaq at record highs, bonds rising in value as yields plummet and the real estate market bubbling along on 3% mortgage rates, such a reversal is widely viewed as “impossible.” Of course it is–until it isn’t. All bubbles pop.

All the bright spots of consumption fueled by top 10% spending–rising sales of second homes, RVs, home remodeling, etc.–are based on the incomes and wealth of the top 10% never materially declining. But how realistic is it to reckon a rotten-to-the-core economy dominated by greedy monopolies and cartels and looted by financier skims that is finally in an inevitable free-fall would magically leave the top 10% untouched?

How realistic is it to reckon that the Everything Bubble would magically continue inflating forever when history is conclusive that all bubbles pop?

No federal bailout or stimulus can reverse these three dynamics, and no amount of legerdemain can replace the spending of the top 10%.

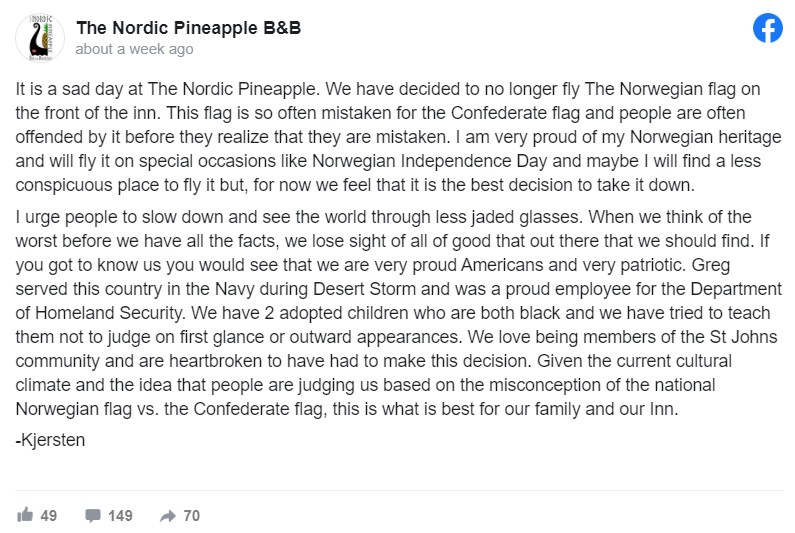

Not The Onion: Michigan Inn Forced To Remove Norwegian Flag Because It ‘Resembles’ Confederate Banner Tyler Durden

Thu, 07/30/2020 – 17:00

Just when we thought the woke PC madness of 2020 couldn’t get anymore absurd, a local incident out of Michigan is so astoundingly stupid that even the AP reported on it with a tone that aptly captures the inanity:

Owners of a Michigan bed and breakfast have removed a Norwegian flag outside of their business after being accused of promoting racism from people who think that it is a Confederate flag.

Kjersten and Greg Offenecker, owners of The Nordic Pineapple, hung the flag opposite of the American flag after they moved into the Civil War-era mansion in 2018, the Lansing State Journal reported. They took both flags down last week.

Entrance to The Nordic Pineapple Inn in St. Johns

“This flag is so often mistaken for the Confederate flag and people are often offended by it before they realize that they are mistaken,” Kjersten Offenbecker, owner of The Nordic Pineapple bed and breakfast, wrote on Facebook last week. She said she was forced to “find a less conspicuous place” for the flag after what amounts to constant harassment over it.

The Nordic-themed business reported receiving“at least a dozen hateful emails,” and a constant barrage of verbal attacks for the Norwegian flag, which merely happens to be red, with a blue and white cross. It had long flown beside the American flag over the boutique hotel’s front steps.

“We love being members of the St. Johns community and are heartbroken to have had to make this decision,” Offenbecker said.

The Nordic Pineapple B&B, via Facebook

Perhaps she’s more heartbroken about how absolutely stupid people are? It appears so…

“It bugs me as far as the stupidity of people,”Greg Offenbecker remarked. “Even if the flag is blowing in the wind or laying limp, there are no stars on it. They look nothing alike.”

“I don’t see it because I grew up with the Norwegian Flag,” Kjersten Offenbecker said. “To me, they are two distinct flags.”

The AP reports the couple, obviously of Norwegian heritage, have two Black children which they previously adopted.

Yet the whole flag kerfuffle has resulted in repeat accusations that they are ‘racist’.

It’s 2020 and though many have high hopes of preserving the Republic, we’re more clearly fast descending into an Idiocracy.

via ZeroHedge News https://ift.tt/3gicA9G Tyler Durden

Apple Soars Above $400 For First Time On Blockbuster Earnings; Announces 4 For 1 Stock Split Tyler Durden

Thu, 07/30/2020 – 16:43

Heading into the current, Q3 quarter – typically one of Apple’s slowest of the year – Wall Street was expecting Apple to report revenue of $52.2 billion, or another slight decline from last year, even though Apple didn’t provide guidance for the quarter and is unlikely to do so again until the coronavirus pandemic ends. Despite the slowdown, AAPL shares rallied a whopping 43% from April through June, Apple’s best quarterly performance in eight years (during what is typically its slowest quarter). As Bloomberg notes, analysts cited everything from the iPhone maker’s App Store revenue growth, the potential of its wearable products, stock buybacks and the potential of its services business as helping outweigh the impact of the coronavirus. The biggest driver of optimism is the release a 5G iPhone, expected later this year. At the same time, while looking at the current quarter, analysts were expecting a continuation of recent trends, including a sizable dip in iPhone sales, at revenue of over $21.3 billion, but a jump in services, with revenue of $13.12 billion.

So with that in mind, moments ago AAPL joined the rest of the megatech sector in reporting absolutely blockbuster results largely boosted by the record stimulus – in both the US and across the world – which included:

Revenue growth of a huge 11%, amid expectations of a decline

iPhone sales were up, on projections of a decline

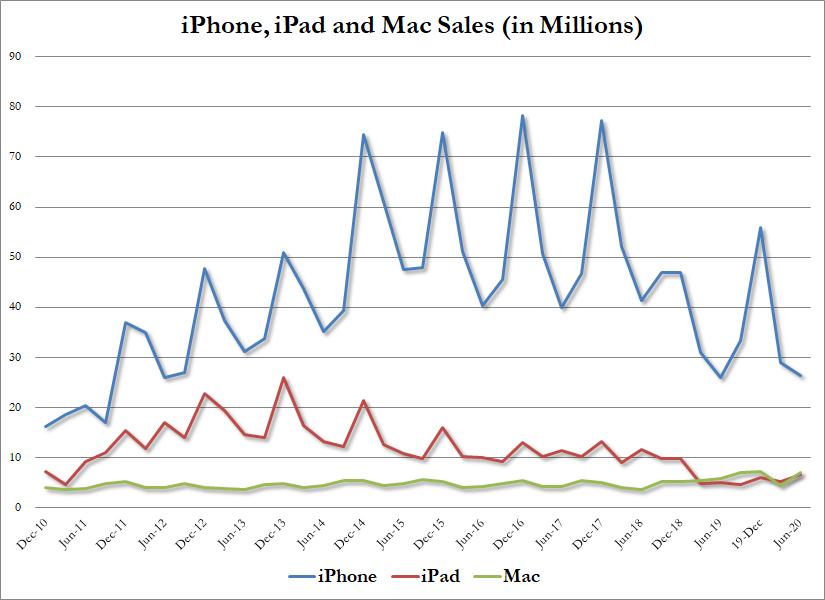

All other categories – Mac, iPad, Wearables, Services – grew

And while Apple didn’t give a forecast again, it did announce a 4 for 1 stock split, clearly anticipating further gains.

Here are the Q3 details:

Revenue of $59.7 billion, smashing estimates of $52.3 billion

EPS of $2.58, also shaprly above the estimate of $2.07

iPhone revenue grew 1.7% to $26.4 billion.

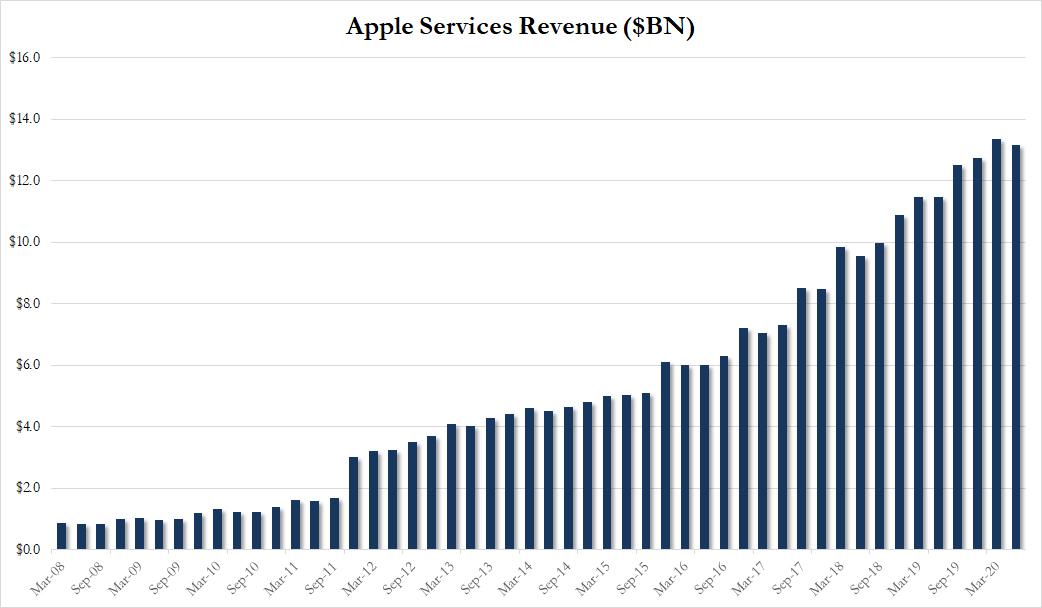

Services grew 15% to $13.2 billion.

Mac sales were up 21% at $7 billion.

iPad revenue grew 31% to $6.6 billion

Wearables, home and accessories jumped 17% to $6.5 billion, est $6.09

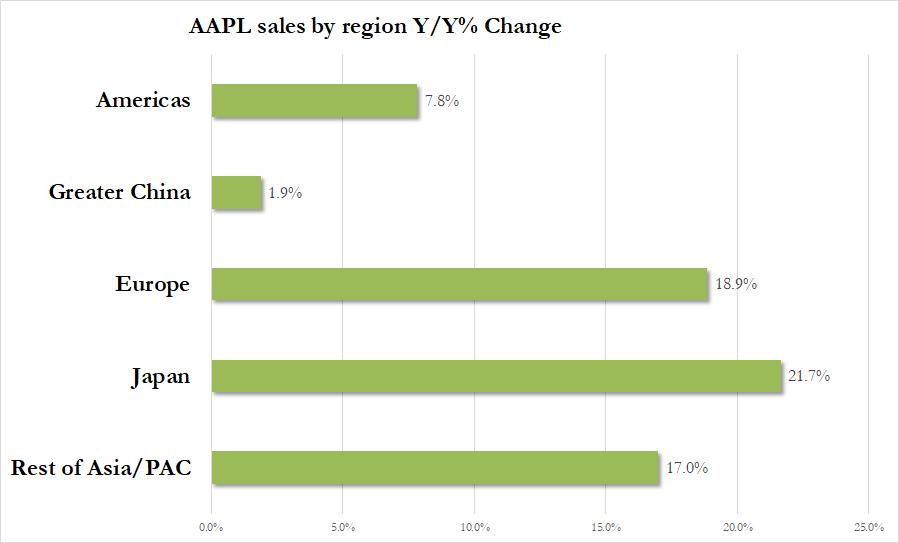

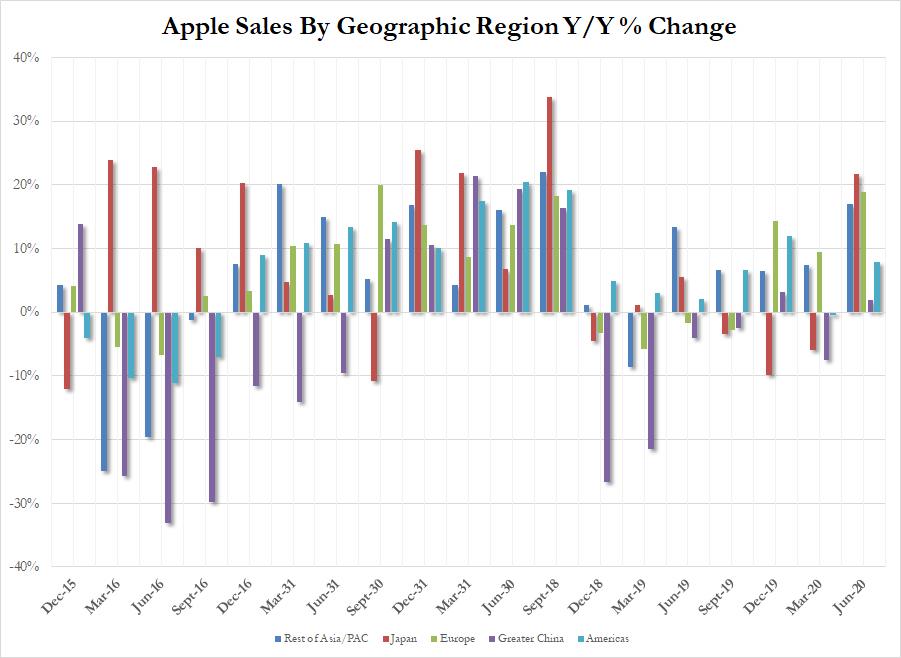

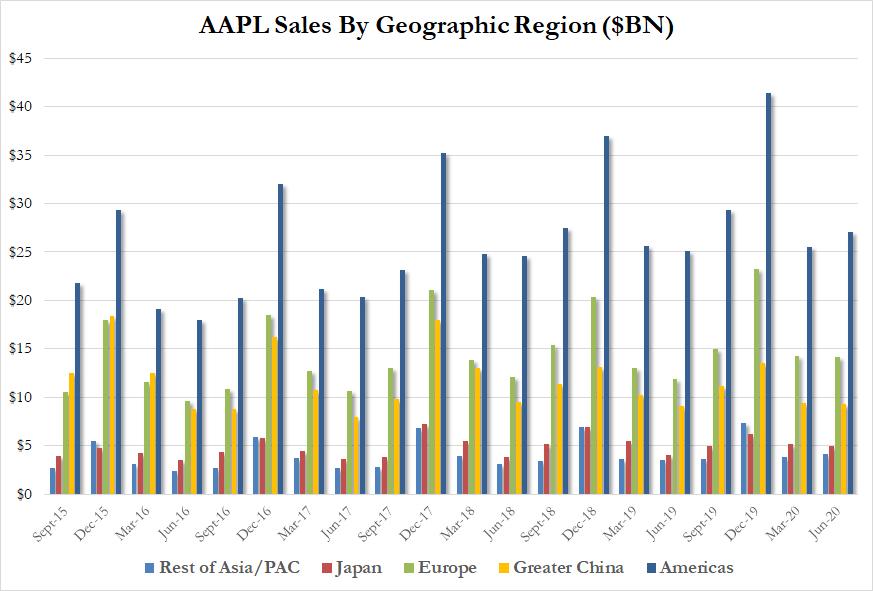

Did Americans use their stimulus checks to buy iPhones and Apple watches? It sure seems that way. Only it wasn’t just America: Apple sales were up in every region with the Americas contributing the most.

For the first time in two years, sales rose Y/Y across all regions:

And while this was supposed to be a slow quarter for AAPL, it was anything but:

Just as remarkable is that contrary to expectations of a decline in unit sales, everything from iPhones, to iPads to Macs saw higher revenues Y/Y, as locked down consumers snapped up new iPhones, iPads and Mac computers to stay connected during the pandemic.

There were a few blemishes, including a rare sequential decline in Service revenue, which dipped to $13.156BN from $13.348BN last quarter.

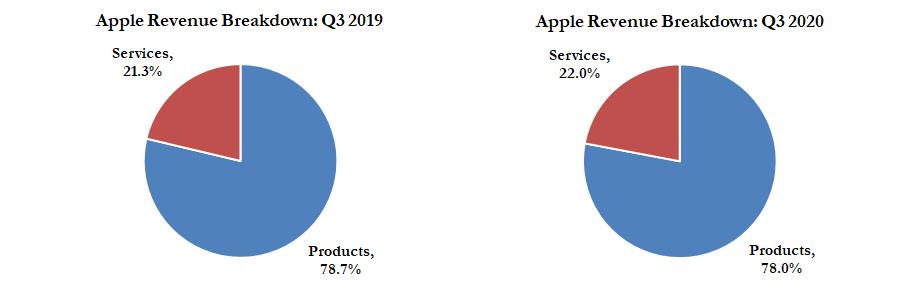

Services dipped from a record 22.9% of total revenue last quarter to 22.0%, still up from 21.3% a year ago:

Discussing the quarter, CEO Tim Cook said:

It was broad-based quarter in terms of our growth. iPhone did better than what we had expected. We saw a slow first three weeks of April where the Covid-19 impact was particularly bad. And then when the lockdowns and point of sales began to come back some, we saw a marked improvement in May and June, more than we had estimated.”

A few more bullet points from the Bloomberg TV interview:

Pandemic “likely” helped results for Mac and iPad due to work from home and remote learning

“Digital services had a really strong performance with record revenues on the App Store, Apple Music, Video, and Cloud Services.”

“Advertising and AppleCare were impacted by reduced economic activity and the store closures”

iPhone and wearables “likely” were hurt due to the store closures.

Store closures “weigh” on results and he expects it to continue to.

“We’re not giving guidance because of the uncertainty.”

And some details on the stock split:

“Each Apple shareholder of record at the close of business on August 24, 2020 will receive three additional shares for every share held on the record date, and trading will begin on a split-adjusted basis on August 31, 2020.”

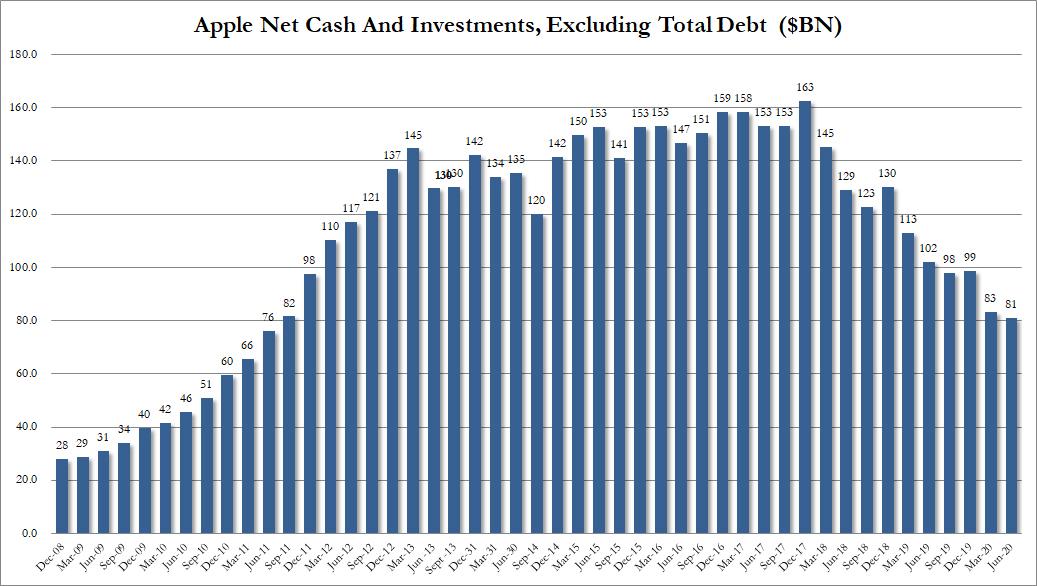

One thing that won’t get prominent notice is Apple’s net cash (excluding total debt), which after hitting a record of $163BN in Dec 2017 has shrunk in half to $81BN, the lowest level in 9 years.

Joining most other tech companies, Apple said that its U.S. employees won’t return to the office until early 2021; earlier in the week Google said that its employees will stay home until next July.

In any case, looking at the market verdict, investors are clearly delighted and just like the other gigatech companies, Apple stock is soaring, and after exploding above $400, has taken out its previous all time high.

via ZeroHedge News https://ift.tt/3jV5haj Tyler Durden

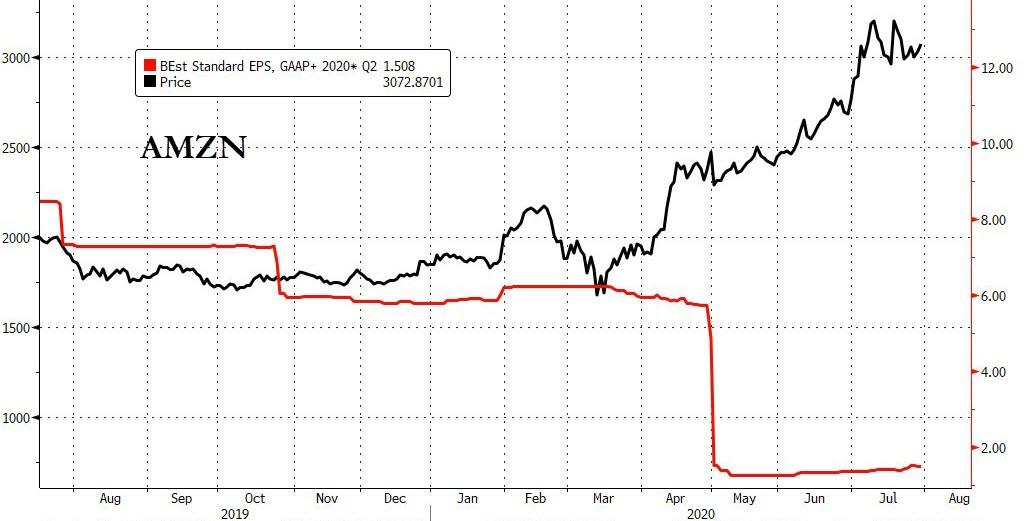

Amazon Soars After Smashing Expectations, Guiding Sharply Higher Tyler Durden

Thu, 07/30/2020 – 16:30

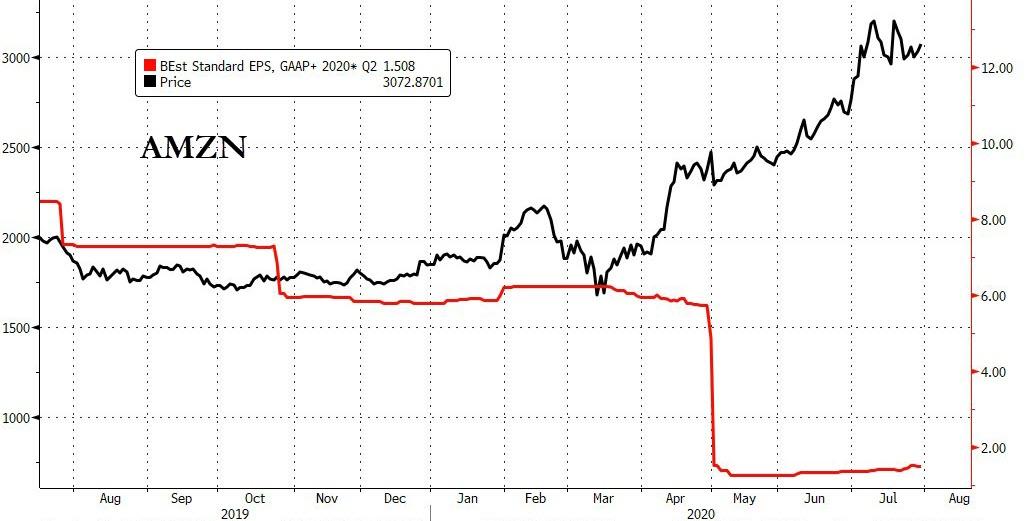

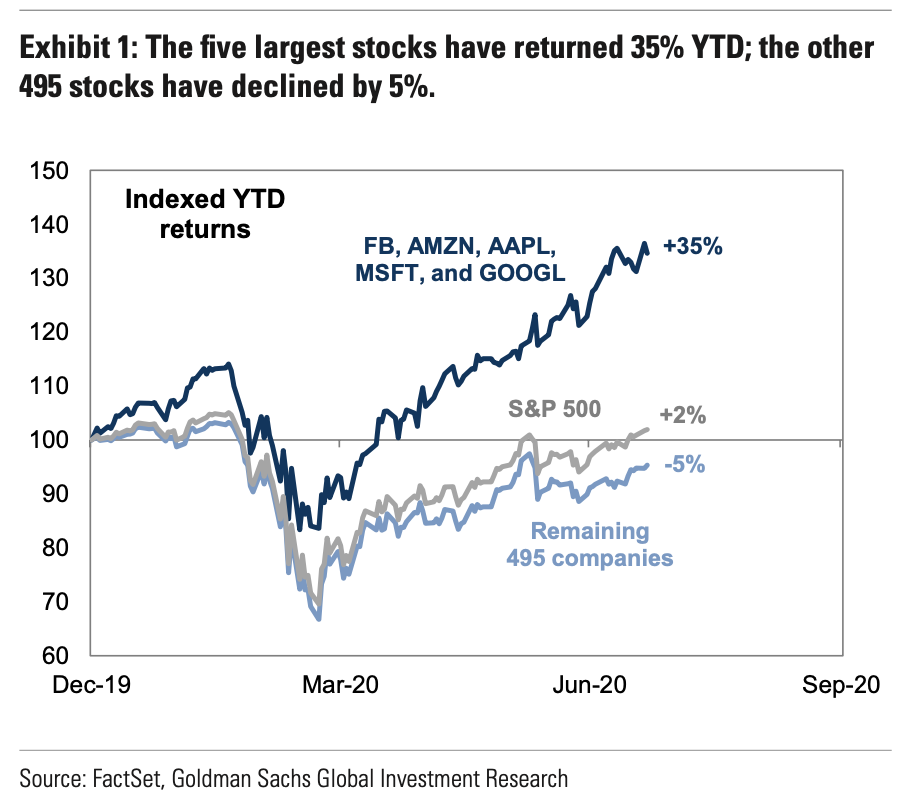

Heading into today’s earnings call juggernaut which sees almost $5 trillion in market cap report among just 4 companies (AAPL $1.7TN, $1.2TN, GOOGL $1TN, AMZN FB $670BN) Amazon had emerged as the one FAAMG stock that was viewed as the cleanest clean shirt among the uber-mega-cap techs (unlike Facebook and Google it has no risky ad exposure; unlike Apple it has no risky China exposure) and despite a drop in its consensus earnings estimates…

… the stock has soared 60% in 2020 hitting a new all time high, and a record market cap of $1.5 trillion, more than $300 billion higher than where it was during its last, Q1 earnings calls (which was a disappointment due to the company’s forecast of shrinking profits) on expectations that the online retailer would be the biggest beneficiary of the transformation in US society to one where most work from home and just order random stuff online while conventional retailers rush to file for bankruptcy.

Which is not to say that the other megatechs have done poorly, on the contrary, the Nasdaq has rallied more than 50% from the depths of the market rout in March and is trading near a record high, thanks almost entirely just to five stocks, among which all the four companies reporting today including Apple, Amazon, Facebook and Alphabet, which are also among the top 5 heaviest-weighted stocks in the S&P 500. Needless to say, an outsized move in any or all of the four would tilt the whole market.

Here, a quick reminder: last quarter, Amazon said the current quarter would come with a multi-billion footnote: while under normal circumstances, Amazon would be expected to reap a second-quarter operating profit of something like $4 billion, instead the company projected a surge in covid-linked costs such as logistical changes, more staff in warehouses, as well as measures to keep them and their corporate peers safe, which would offset the profit. As a result, Amazon forecast an operating income range of $1.5 billion to a $1.5 billion loss, which however clearly did not adversely impact the stock (except for a brief period of a few hours after last earnings were reported).

So was all this optimism – and staggering stock price surge – justified? Well, apparently yes and bigly so because the company not only smashed earnings expectations, but also reported net sales for the second quarter that beat the highest analyst estimate.

Q2 Revenue of $88.9BN, Exp. $81.24BN

Q2 EPS of a whopping $10.30 vs exp. $1.51

Q2 EBIT of $5.843BN vs exp. $420MM

Q2 AWS revenue of $10.81BN, a small miss of expectations of $11.01BN, up 31%

As noted above, Amazon said it spent over $4BN on incremental Covid-19 costs

In other words, Amazon smashed both top and bottom line expectations, despite a small miss on AWS expectations. But it was Amazon’s superb forecast that stoked investors, sending the stock soaring after hours:

Amazon sees 3Q Net Sales $87.0B to $93.0B, both well above the exp. $86.51B

Operating income is expected to be between $2.0 billion and $5.0 billion, compared with $3.2 billion in third quarter 2019. This guidance assumes more than $2.0 billion of costs related to COVID-19.

As shown in the chart below…

… projected Q3 revenue growth of 28.6% (taking the midline) was clearly just as impressive and indicates the company does not expect any headwinds on the topline.

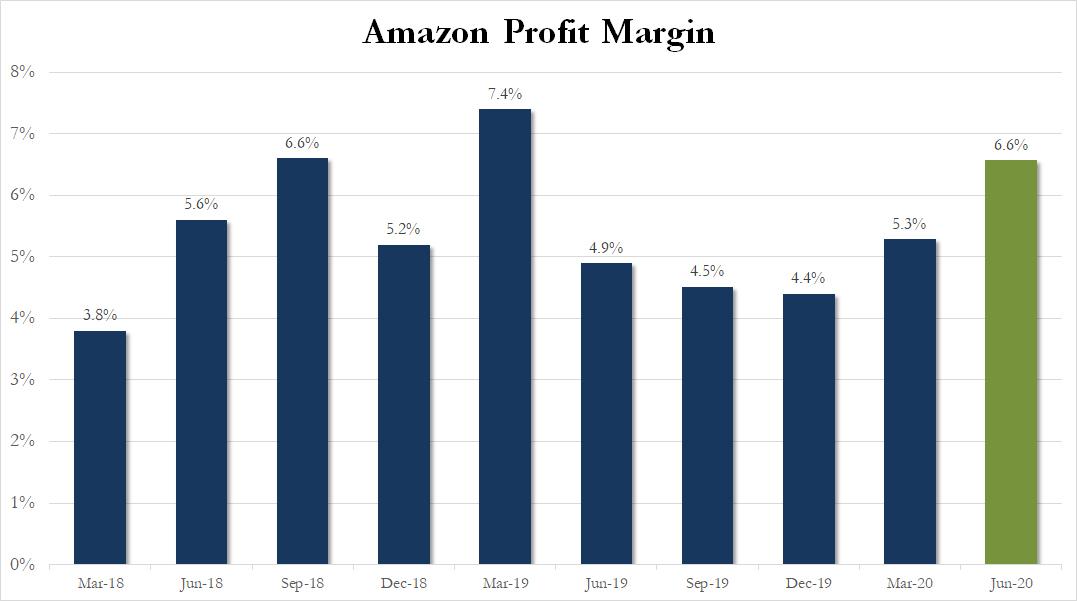

There was more good news in the company’s profit margin which rose sequentially to 6.6%, the second highest in recent history.

Some other headlines from the report:

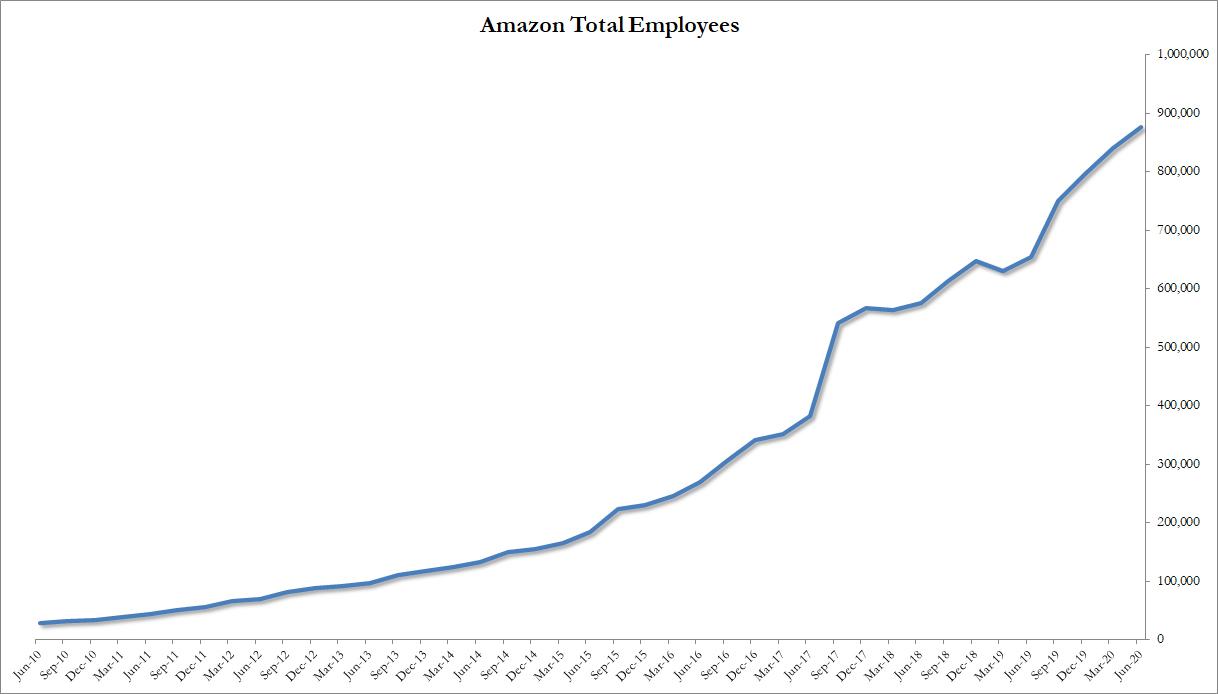

Created Over 175,000 New Jobs Since March

Invested Over $9B in Capital Projects

Increased Grocery Delivery Capacity by Over 160%

Online Grocery Sales Tripled in 2Q vs Period Last Year

3Q Oper Income View Assumes Over $2B Covid-19 Costs

Third-Party Sales Grew Faster Than First-Party Sales

As usual AWS was the primary source of profit, and with $3.357 BN in operating income (up from $2.121 BN a year ago) or 57.5% of the company’s total operating income of $5.843. Meanwhile, the international division finally appears to have stopped burning cash, and after generating $22.7BN in sales, it resulted in its first profit in years, to the tune of $345MM in Q2.

To summarize, AWS revenue growth continues to slow modestly:

Q1 2018: 48%

Q2 2018: 49%

Q3 2018: 46%

Q4 2018: 46%

Q1 2019: 42%

Q2 2019: 37%

Q3 2019: 35%

Q4 2019: 34%

Q1 2020: 33%

Q2 2020: 28.9%

However, offsetting this is that after declining for a year, AWS operating margins posted a rebound for a second consecutive quarter:

Q1 2018: 25.7%

Q2 2018: 26.9%

Q3 2018: 31.1%

Q4 2018: 29.3%

Q1 2019: 28.9%

Q2 2019: 25.3%

Q3 2019: 25.1%

Q4 2019: 26.1%

Q1 2020: 30.1%

Q2 2020: 31.0%

Meanwhile, Amazon’s North America segment margins rebounded from 2.84%, the lowest in three years, to 3.86%.

Commenting on the results, Jeff Bezos said that this was another highly unusual quarter:

“This was another highly unusual quarter, and I couldn’t be more proud of and grateful to our employees around the globe.”

“As expected, we spent over $4 billion on incremental COVID-19-related costs in the quarter to help keep employees safe and deliver products to customers in this time of high demand—purchasing personal protective equipment, increasing cleaning of our facilities, following new safety process paths, adding new backup family care benefits, and paying a special thank you bonus of over $500 million to front-line employees and delivery partners. We’ve created over 175,000 new jobs since March and are in the process of bringing 125,000 of these employees into regular, full-time positions. And third-party sales again grew faster this quarter than Amazon’s first-party sales. Lastly, even in this unpredictable time, we injected significant money into the economy this quarter, investing over $9 billion in capital projects, including fulfillment, transportation, and AWS.”

And speaking of employees, Amazon now has a record 876.8K workers.

Needless to say, with blowout earnings and stellar guidance, the stock is surging after hours, and was approaching it all time high.

via ZeroHedge News https://ift.tt/30grmZf Tyler Durden

What Ad-Boycott? Facebook Shares Jump After Smashing Earnings Tyler Durden

Thu, 07/30/2020 – 16:16

Heading into earnings tonight, Facebook had been making plenty of headlines on twitter as an increasing number of virtue-signalers claim they are boycotting ad spend on the social media network (and not merely cutting costs amid COVID).

“We’re glad to be able to provide small businesses the tools they need to grow and be successful online during these challenging times,” said Mark Zuckerberg, Facebook founder and CEO.

“And we’re proud that people can rely on our services to stay connected when they can’t always be together in person.”

There appears to be zero impact from the ad-boycott (though the boycott didn’t technically start until July 1, the first day of the third quarter, so it’s unlikely there’s any impact visible in these numbers) as Facebook smashed the ball out of the park, beating on every major metric:

*FACEBOOK 2Q EPS $1.80, EST. $1.39

*FACEBOOK 2Q REV. $18.69B, EST. $17.31B (+11% YoY – its lowest since the IPO)

*FACEBOOK 2Q AD REV. $18.32B, EST. $16.92B

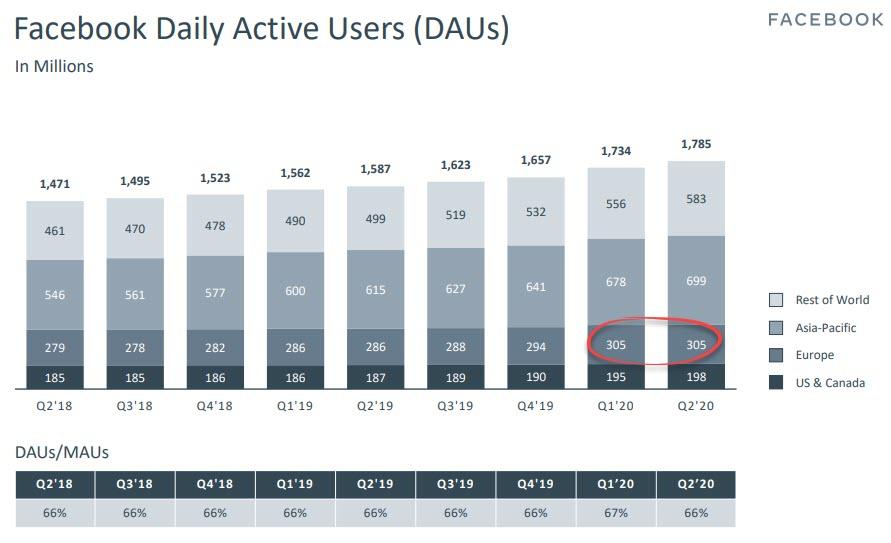

*FACEBOOK 2Q MONTHLY ACTIVE USERS 2.70B, EST. 2.63B (+12% YoY)

*FACEBOOK 2Q DAILY ACTIVE USERS 1.79B, EST. 1.74B (+13% YoY)

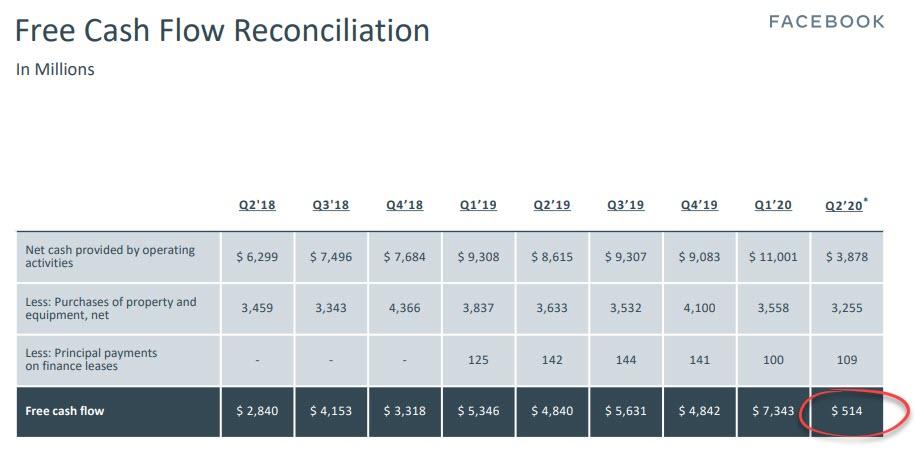

We do note that Free Cash Flow fell significantly…

Looking ahead, Facebook sees DAUs and MAUs “flat to slightly down QoQ,” and ad revenue for Q3 in line with July (which given the boycott may mean weaker) and expects FY20 CapEx at the high of the $14-16bn range.

“In the first three weeks of July, our year-over-year ad revenue growth rate was approximately in-line with our second quarter 2020 year-over-year ad revenue growth rate of 10%. We expect our full quarter year-over-year ad revenue growth rate for the third quarter of 2020 will be roughly similar to this July performance.”

This sent FB shares up almost 9% after hours to a new record high…

Facebook outlines several factors contributing to its outlook, including:

First, continued macroeconomic uncertainty, including the pace of recovery and the prospects for additional economic stimulus;

Second, our expectation that some of the recent surge in community engagement will normalize as regions reopen;

Third, the impact from certain advertisers pausing spend on our platforms related to the current boycott, which is reflected in our July trends; and

Lastly, headwinds related to ad targeting and measurement, including the impact of regulation, such as the California Consumer Privacy Act, as well as headwinds from expected changes to mobile operating platforms, which we anticipate will be increasingly significant as the year progresses.

Finally, we note that Facebook’s headcount was 52,534 as of June 30, 2020, an increase of 32% year-over-year.

via ZeroHedge News https://ift.tt/317t5z0 Tyler Durden

USDollar, Bond Yields Tumble After Greatest Economic Collapse Ever Tyler Durden

Thu, 07/30/2020 – 16:00

A re-weakening in jobless claims data (confirming no v-shaped recovery), a record-breaking collapse in GDP and consumption (admittedly backward-looking) and Trump tweet hinting at election delays all spoiled the party early on in US equity land but around 1030ET ‘someone’ decided this mini-dip was for buying and everything surged ahead of tonight’s mega earnings data. Only Nasdaq managed gains on the day, however with The Dow the biggest laggard…

Look at The Nasdaq… isn’t it pretty!!!

The bounce appeared to be triggered by a technical test by The Dow of its 200DMA and 50DMA…

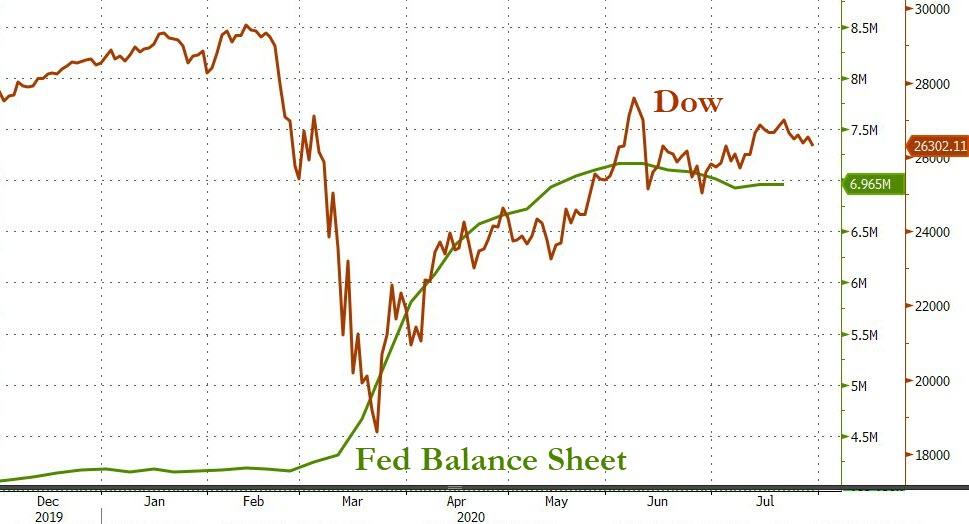

The Fed better be ready to do some more buying…

Source: Bloomberg

FANG Stocks rallied intraday ahead of tonight’s earnings, bouncing off unch for the week…

Source: Bloomberg

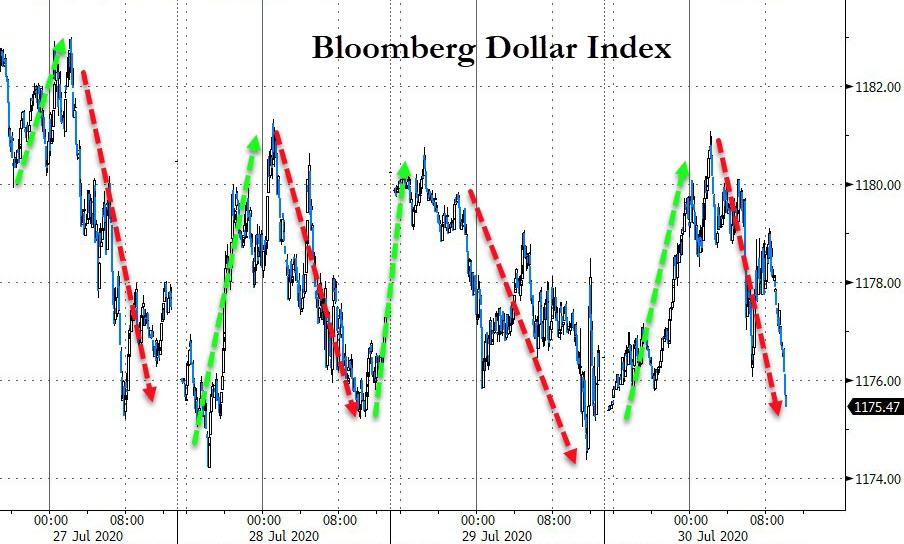

The Dollar continued its pattern of gains in Asia and weakness in Europe and US sessions…

Source: Bloomberg

Breaking down below a critical uptrend line…

Source: Bloomberg

Gold and Silver were spooked briefly higher on Trump’s tweet but retreated to end the day – unusually – lower…

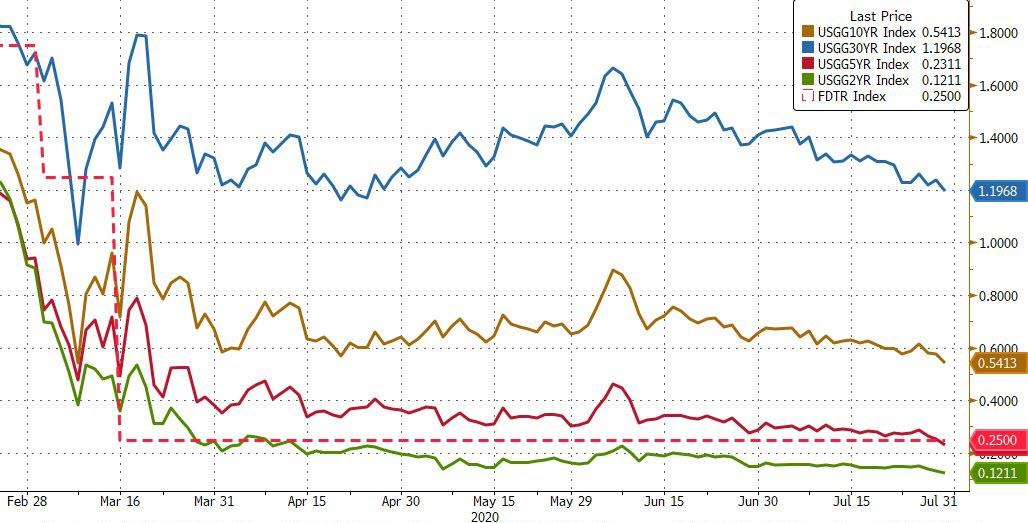

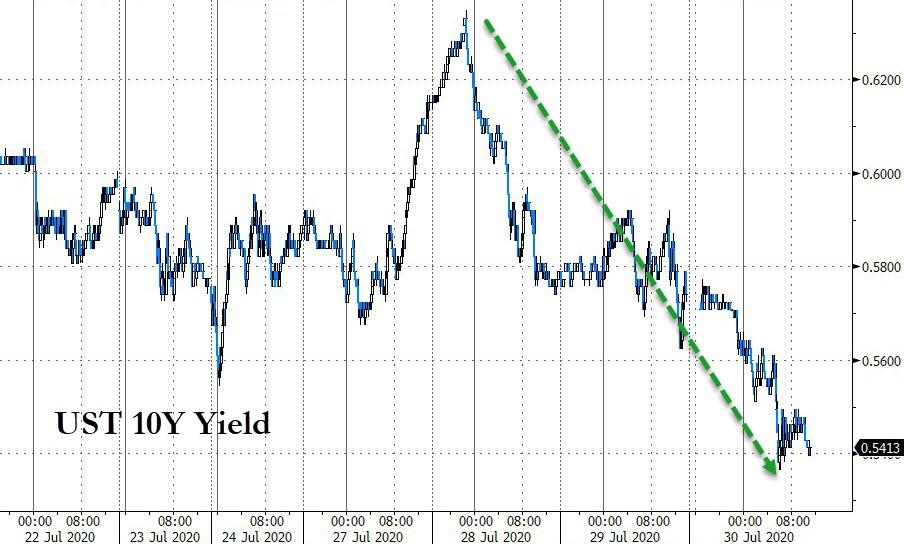

Treasuries were bid with the long-end outperforming (30Y -4bps, 2Y -1bps), 10Y is outperforming on the week…

Source: Bloomberg

Pushing the entire yield curve to record low yields…

Source: Bloomberg

As Stocks remain near record highs…

Source: Bloomberg

With 10Y back at the spike lows from the very worst of the market collapse in March…

Source: Bloomberg

Yield curve has flattened significantly since The Fed statement…

Source: Bloomberg

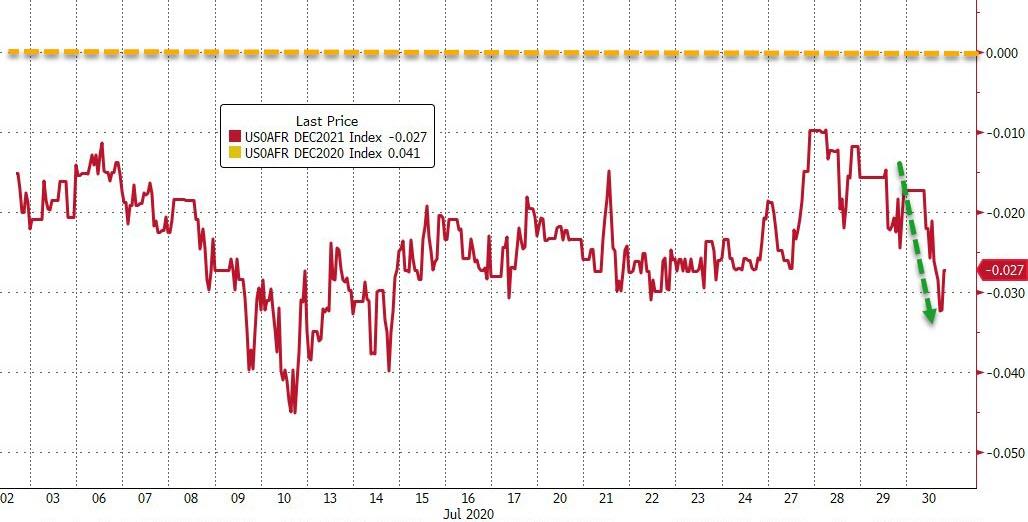

And before we leave ratesville, we note that the Dec 2021 Fed Funds futures is implying a -3bps rate… easing since The Fed yesterday…

Source: Bloomberg

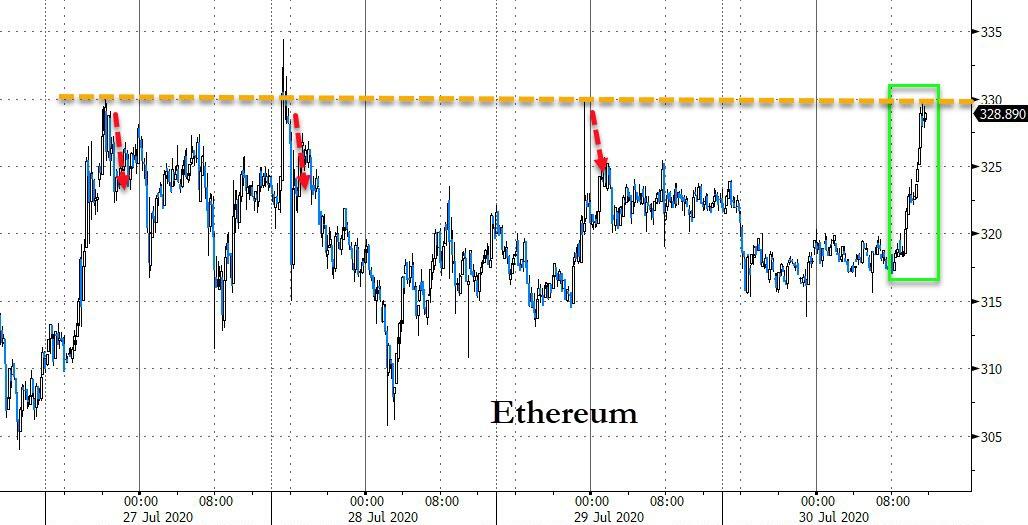

Cryptos were mixed today with Ethereum and Litecoin best but still a big week…

Source: Bloomberg

Ethereum tested back up to $330 intraday…

Source: Bloomberg

The energy complex was hit today with WTI slammed back below $40 to a $38 handle intraday (before panic-buying lifted it back)…

And Nattie tumbling hard…

And finally, ahead of tonight’s earnings-pocalypse, a quick look at the big tech names vs their consensus EPS…

Source: Bloomberg

Notice any similarities?

via ZeroHedge News https://ift.tt/2Do5Etm Tyler Durden

A Hebrew-language channel stated on Wednesday night that the Israeli army expects an attack by Hezbollah during the Islamic Eid Al-Adha holiday.

The Israeli Broadcasting Corporation, Kann, reported that Israel fears a “second attack” by Hezbollah in the next 48 hours, that is, during the celebration of Eid al-Adha.

File photo of Israel’s Iron Dome System.

The news channel reported that, based on this expectation, the Israeli army has strengthened its forces in the north near the Lebanese and Syrian borders, deploying advanced missile systems, special rockets and intelligence-gathering capabilities, for fear of a reaction from Hezbollah, after one of its members was killed in an airstrike on July 20th in Damascus.

The Israel-based news channel quoted a “Lebanese diplomat in Beirut” – whom they did not name – as saying that Hezbollah does not want a comprehensive escalation with Israel, but that it is looking for a real retaliation.

It is noteworthy that the strengthening of the Israeli forces in the northern region comes in light of the tensions along the Israeli-Lebanese border.

המתיחות בצפון | בישראל חוששים מפיגוע נוסף של חיזבאללה שייצא לפועל בתוך 48 שעות. צה”ל מתגבר עוד יותר את הכוחות בצפון במערכי אש מיוחדים, רקטות מיוחדות ויכולות איסוף מודיעין”. הדיווח של @moyshis ב-#חדשותהערבpic.twitter.com/pUPjUTVHAp

Hezbollah previously denied the Israeli army’s claims about their forces attempting a ‘sabotage’ operation in the occupied Sheba’a Farms region near the Syrian and Israeli borders.

via ZeroHedge News https://ift.tt/2Do4E8A Tyler Durden

{kind=link}

{kind=link}

{kind=link}