I don’t think I’ve ever started the Morning Porridge with a quote from a politician, but if even Amber Rudd knows it, then why don’t the rest of the Tories get it?

“It is not enough to be told to shut your eyes, cross your fingers, pick up some magic beans and believe in Britain. We need a skill negotiator and dealmaker, not an instruction for more optimism”.

She was supporting… who was she supporting? Not a clue nor any interest really.. And we still haven’t heard Boris speak.

Lord protect us, and pass me a couple of grams of Columbia’s finest export product to make sure I never end up in Parliament… Enough said about Brexit and the UK Government…

Where is Donald Trump when we need him… ?

Actually, you probably don’t. There is a great in-depth story in Forbes analysing Trump’s business dealings in Moscow. No one will be surprised at the gist of the story: a future US president jumping into bed with developers linked to Putin, apparent bribery and corruption, and a whole strata of Moscow shadies, but the fact Trump Inc (yep, future presidential barbie-doll Ivanka was in on it), was chasing deals that would have brought in literally pennies is the curious thing. Why?

Back in the real world…

After a dose of Donald pimp-slapping the Fed for rates being too high, and telling Xi he has to turn up for G20 trade talks, global markets feel increasingly jaded after the last week of trade non-talk and rate noise. Markets are up, down and twirl it all around… Difficult to see where it goes from here.. I suspect that means we are heading for a very thin summer, the market to start loading up on new fears and non-solutions, and face the next crisis point in Q3. Joy.

There are, of course, a number of threat points. I really need to get on the phone to some of my Italian experts and get the word from Milan on what’s going on in terms of Italy picking a fight with Europe while Draghi is packing his bag, Wiedemann is getting briefed on how to be nice to other Europeans, and the Italians are dreaming up nightmares like Mini-BOTs. Please make it happen so we can have another sovereign debt crisis meaning I don’t have to write about Brexit!

Bloomberg is talking up Raghuram Rajan, ex-Bank of India, as the next Governor of the Bank of England. Lots of people are not going to like it, but it’s a good call. I could say something like the domestic talent for the role isn’t up to much, but I better not as one of them will probably get the job…

Interesting the stories about Foxconn telling investors how it’s got capacity to build all the iPhones it currently assembles in China in the US. That’s an important message about how quickly global supply chains will change as the Trade Spat with China is increasingly characterised as a Trade War and shutters come down.

Which segways neatly into an interesting moment y’day as I was interviewed by Chinese Television about China Threat Theory, Huawei (which I just can’t pronounce properly), and why the West does not trust Chinese IP laws. The Chinese questions – they didn’t send a reporter, just a list of questions for the cameraman to ask – were kind of loaded: Why doesn’t the West accept Chinese IP laws? Are we even aware of the laws passed by China to ensure compliance? Why is the West trying to destroy Chinese IP in the form of Huawei? And why does the west keep pushing the China Threat Theory?

It was very interesting – and I tried not to over-rant. In fact, I’d even claim to have been sane and sensible. On the basis the programme probably won’t like my answers and won’t air them, I thought I might share them here:

The West is distrustful of China IP litigation for a number of reasons including the easy availability – even on official websites – of counterfeit goods, the difficulty in securing convictions due to the inability to collect critical evidence from defendants, and the low importance we feel is ascribed to the crime. There is a suspicion many Chinese businesses regard the possibly of being fined for IP theft as an inconvenience rather that an owner’s right to be respected. We do accept Chinese laws have been introduced and enforcement is improving to protect IP over the past 30 years, but the consensus remains the needs of the state are primary to the rights of foreign IP owners. And, in any historical context, it’s hardly unknown for growing nations to avail themselves of foreign tech on the cheap. Do we need stronger laws and stricter enforcement? It’s an angle many western IP owners would welcome.

Huawei is an interesting case. The danger is the world splits into two tech regimes. Huawei has been a leader setting standards for 5G – it’s going to take time and prove costly if the West now goes a different direction. Huawei may well be a pawn in the current power play between Washington and Beijing, but it’s also at the crisis line between the surveillance capitalism Beijing has enthusiastically embraced, and the personal freedom and privacy espoused across the West. These two approaches to Tech may be mutually exclusive, thus confirming a split tech world.

Not being an expert in Huawei’s tech, then I have to listen to those who are, and when the experts in our military and tech community say Huawei Tech is not complementary with our own, then I have to respect that. If they say its spyware – who am I to argue?

China Threat Theory is an interesting one. I suspect it’s a label dreamt up in some Cadre Propaganda Office in Shanghai to paint China as the victim to the aggressive West. I’m a great admirer of China’s history and culture – especially Chinese landscape painting, but I can understand the fears and frustrations of the West. This is particularly true economically where initiatives such as the Belt and Road are leading to charges of predatory debt diplomacy, and deliberately loading debt into future client states of the new China. History shows that expansionary mercantile will always brush up against incumbents causing pressures and often conflict. These can be addressed through good governance, intermediation and the mechanisms and institutions of global trade and international law. Or nations can choose to be aggressive in their own regions and attempt to bludgeon their way into international markets through financial aid. At the moment, that is how China is being perceived.

I was then asked how does America trying to force China into a trade war affect the global economy? I tried to answer quite honestly – the US is current incumbent, China the growing nation. The US is signalling very simple choices, play by our rules (at this point I didn’t mention the treatment of minorities, the environment or democracy) or we shall isolate you. There is no wish to trigger conflict, but it’s in the US interest to have a completely open China market, or to close it off by drawing lines between the US and its allies vs China. Some have said there in nothing like the ideological struggle between capitalism and communism to underlie the new China US divide, but there is a massive gulf between Surveillance Capitalism under the Eye of the State, and the personal liberties and freedoms the West supports.

I’m going to be very intrigued to see how the Chinese use the interview. I’ll post it on the website if its ever shown…

via ZeroHedge News http://bit.ly/31rqMpZ Tyler Durden

Mortgage applications surged an impressive 26.8% WoW – the largest jump since Jan 2015 – led by a massive spike in refis as mortgage rates tumbled alongside the Treasury market.

30Y rates dropped back below 4.00% – the lowest since Jan 2018…

Prompting a sudden 46.5% surge in refinancing activity (which we saw also saw in early March) and purchases rose 10.0% (after falling the prior week).

Loan size for purchases fell on average last week while the size of refi loans rose spiked…

Refis made up 49.8% of all loans (53.7% of loan value) versus the prior week’s 42.2%, but as the chart above shows, these spikes in activity are hardly a long-term signal of health…

…more a short-term reflection of mortgage banker marketing efforts.

via ZeroHedge News http://bit.ly/2XFDQG1 Tyler Durden

Just weeks ahead of having to face reality report his company’s Q2 numbers, Elon Musk went on the record yesterday during Tesla’s annual general meeting and told the world that there was “not a demand problem” for Tesla vehicles, according to ARS Technica.

As a reminder, this is the same CEO that once promised profitable quarters going forward from Q2 2018 – and who just posted a more than $700 million loss to start off 2019. But the market once again appeared to take Musk’s pump guidance at its word, and Tesla stock shot up in Tuesday’s after-hours session and Wednesday’s pre-market session.

In his initial statement to the audience, Musk reiterated what he said in a conveniently leaked email weeks ago: that there was a chance that Q2 2019 could be a “record quarter”.

Musk said: “I want to be clear that there is not a demand problem… Sales have far exceeded production, and production has been pretty good. We have a decent shot at a record quarter… if not, it’s going to be very close.“

But when asked about profitability, a metric that Musk had already guided for on a consistent basis, his tone was less optimistic. He said: “Profitability is always challenging when you’re a fast-growing company. Last year, we doubled our fleet. It’s hard to be profitable for that level of growth.”

And then, as if to fulfill some double-talk requirement, Musk added: “I think we can be cash-flow positive despite having a very fast growth rate.”

For good measure, he then pivoted to telling the audience he didn’t think it would “be long before we have a 400-mile-range car.”

Musk then continued, discussing battery availability and full self driving. As a reminder, Consumer Reports called the latest version of Autopilot “less competent than a human.” At the general meeting, Musk more than likely did the right thing by not promising any specific dates and timelines for full-self driving, but he did reiterate that the feature “should be able to go from your garage to your parking space at work” without assistance.

He told the audience that his prototype for FSD could “can take me from my house to the office.”

But then Musk admitted that there were ongoing challenges with perfecting the “summon” feature that is supposed to allow your car to find its way to you autonomously in a parking lot.

Musk also said at the meeting that one of the primary constraints for the company was availability of batteries. But how to solve that issue? Get into the mining business, of course, Musk said. Robotaxis are so last month.

Musk said: “We might get into the mining business, I don’t know—we’ll do whatever we have to make sure we can scale at the fastest rate possible.”

Finally, Musk commented that he expects demand for the Model Y to eventually be greater than the S, the X, and the 3 combined. This stands at odds with Morgan Stanely’s Adam Jonas, who dryly said on an investor call last month that “nobody cares about the Model Y”.

Musk was once again incoherent when trying to pin down a timeline for the Model Y: “We expect to hit volume production towards the end of next year,” he said, before saying, “internally, we’re shooting for sooner than that.”

Finally, Musk made two more pivots. First, telling the crowd he hoped to announce a pick-up truck sometime this summer. And second, that the solar roof tiles that investors were promised years ago and has yet to materialize is currently on “full version three” – whatever the hell that means – and that, when finished, it would last 30 years, would be easy to install, and would be low cost.

via ZeroHedge News http://bit.ly/2WFsOnJ Tyler Durden

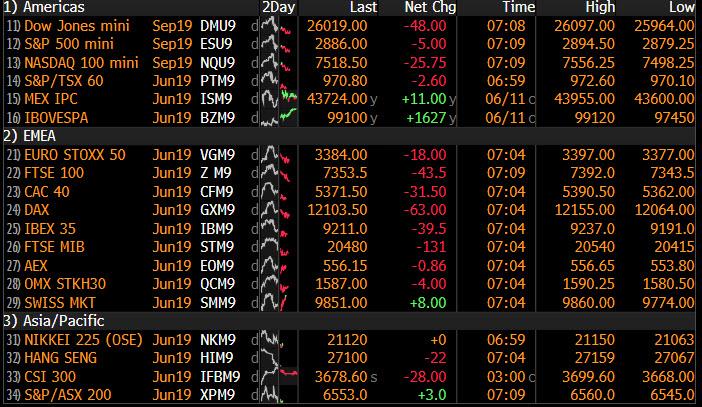

The torrid June rally finally fizzled overnight as stocks slipped around the globe on Wednesday alongside S&P futures, after a six-day rally in the S&P ended yesterday with a whimper amid signs the June revival in risk appetite may have overshot, with trade concerns returning to the fore.

The market mood soured after a protest in Hong Kong turned violent as police were unleashed to contain a “riot”, compounding the negative sentiment, and Treasuries gained. An impending reading on U.S. CPI was set to further cement the Fed’s decision whether to cut rates in June/July.

“I think we are in for a very nervous wait until next week’s FOMC meeting,” Saxo Bank’s head of FX strategy, John Hardy, said.

Europe’s main markets followed Asia by declining early on. London’s FTSE, the DAX in Frankfurt and CAC40 Paris were down 0.2% to 0.4% as traders trimmed some of June’s 4% gains. The Stoxx Europe 600 index headed for its first drop in four sessions.

The rebound in Asia stocks paused on Wednesday as traders stayed cautious amid lingering U.S.-China trade tensions and an escalating protest in Hong Kong. The region’s benchmark declined 0.5% snapping a three-day gain. Hong Kong was the worst-performing market in the region, with the Hang Seng Index falling as much as 2%, after thousands of demonstrators converged on the city’s legislature Wednesday and blocked roads to protest a bill that would for the first time allow extraditions to China.

“The impact was short-lived in the past,” noted Alex Wong, director at Ample Finance Group in Hong Kong. “This time people will look at how the U.S. reacts to this kind of news. The U.S. attitude towards Hong Kong and China are also not the same.”

Japanese stocks halted their three-day advance as electronics makers were the heaviest drags on the index. Trading volume for the nation’s equities dropped almost 20%. Nintendo fell after delaying the release of Animal Crossing: New Horizons. Square Enix Holdings posted its worst two-day slump as investors took profits after the company announced new games at E3. Most of other major Asia markets also declined as the cautious sentiment spreading across the region. China’s Shanghai Composite Index retreated as much as 0.8%, and Jakarta Composite index fell 0.7%.

Then there was the ongoing trade war which has no resolution in sight: President Trump said on Tuesday he was holding up a trade deal with China and had no interest in moving ahead unless Beijing agrees to four or five “major points”, which he did not specify. He said interest rates were “way too high” and the Federal Reserve had “no clue”.

And speaking of the Fed, the FOMC will meet on June 18-19. With trade tensions rising, U.S. growth slowing and hiring in May declining, markets have priced in at least two rate cuts by the end of 2019. Futures imply around an 80% chance of an easing as soon as July. That may change depending on what U.S. consumer price data show later in the session. Headline inflation is expected to slow to 1.9%, with the core rate steady at 2.1%.

In FX, the euro rebounded initially to $1.1336, just short of the recent three-month high of $1.1347, despite Trump’s recent tweet slamming the Euro as “devalued.” The dollar fell against the yen to 108.36 and stalled on a basket of currencies at 96.608.

“The President’s tweets on the USD have the potential to have much more lasting impact in the coming election year,” said Alan Ruskin, global head of G10 FX strategy at Deutsche Bank. “Global conditions are nicely set for what has colorfully been described as a ‘currency war’ or a currency race to ‘the bottom’.”

China’s yuan weakened against the dollar, a day after it climbed the most in two months following the central bank’s moves to shore up the currency. The PBOC set a slightly stronger-than-expected reference rate Wednesday, after showing the largest strong bias in its fix on Tuesday since Bloomberg began releasing fixing forecasts in 2017. The central bank on Wednesday resumed 28-day reverse repurchase agreements for the first time since January, a signal that it seeks to ensure market stability amid seasonal tightness and the aftermath of the Baoshang seizure, according to Qi Sheng, chief fixed-income analyst from Zhongtai Securities Co. In Hong Kong, stocks tumbled and the currency soared in its biggest gain in six months, as interbank interest rates jumped amid protests that closed roads in the city’s financial district.

Benchmark government bond yields fell as caution grew, with the 10Y Treasury down to 2.12%.

In commodities, oil prices dropped over 2% as concern about a global economic slowdown offset expectations that OPEC and its allies will extend their supply curbs. Hedge fund managers have been liquidating bullish oil positions at the fastest rate since late 2018 amid growing economic fears.

Economic data include mortgage applications and CPI, while Lululemon is among companies reporting earning

Market Snapshot

S&P 500 futures down 0.3% to 2,879.75

STOXX Europe 600 down 0.5% to 379.06

MXAP down 0.5% to 156.57

MXAPJ down 0.6% to 511.71

Nikkei down 0.4% to 21,129.72

Topix down 0.5% to 1,554.22

Hang Seng Index down 1.7% to 27,308.46

Shanghai Composite down 0.6% to 2,909.38

Sensex down 0.6% to 39,713.77

Australia S&P/ASX 200 down 0.04% to 6,543.74

Kospi down 0.1% to 2,108.75

German 10Y yield fell 0.2 bps to -0.234%

Euro up 0.09% to $1.1336

Brent Futures down 2.2% to $60.94/bbl

Italian 10Y yield rose 3.4 bps to 2.025%

Spanish 10Y yield rose 0.4 bps to 0.583%

Brent Futures down 2.2% to $60.94/bbl

Gold spot up 0.8% to $1,337.41

U.S. Dollar Index down 0.05% to 96.63

Top Overnight Highlights from Bloomberg

The dollar touched an eight-week low before U.S. inflation data that may back the case for Fed interest-rate cuts. The greenback is weaker against all its G-10 peers so far this month as markets have boosted pricing on Fed easing amid concern trade frictions will sap global growth.

The yen led gains on Wednesday, strengthening for the first time in three days against the dollar

The euro was little changed after Tuesday’s advance; the common currency was pressured after comments from ECB Governing Council member Francois Villeroy de Galhau who said the central bank could increase stimulus if needed

European bond markets traded flat ahead of a large supply slate from Germany, Portugal, Italy and Spain; U.S. Treasuries advanced for a second day, the 10-year yield dropped 2bps to 2.12%

U.S. index futures slipped, the Stoxx Europe 600 index opened lower for the first time in four sessions

Asian equity markets traded mostly subdued after the flat lead from Wall St where the relief rally stalled, and the major indices finished flat to snap a 5 and 6-day win streak for the S&P 500 and DJIA respectively. ASX 200 (U/C) and Nikkei 225 (-0.4%) were mixed with Australia kept afloat by mining names as iron prices in China surged to fresh record highs, while the Japanese benchmark mirrored the indecisiveness of its US peers amid a firmer JPY and with SoftBank among the laggards as a group of US states attempt to block the Sprint and T-Mobile merger. Elsewhere, Hang Seng (-1.7%) and Shanghai Comp. (-0.6%) were negative following another net liquidity drain by the PBoC and pessimism regarding the ability to reach a US-China trade deal at the G20, with underperformance in Hong Kong amid increases in money market rates and mass protests outside government buildings in opposition against the controversial extradition bill. Finally, 10yr JGBs kept rangebound with price action hampered by the indecisiveness in the region and amid a lack of BoJ presence in the market today.

Top Asia News

Nintendo Moves Some Switch Production Out of China: WSJ

Indonesia’s Jokowi Open to Gerindra Joining His New Cabinet

Japan to Propose TPP-Level Tariff Cut on U.S. Farm Goods: Kyodo

Rumors About China Military Going to HK Are Misinformation: Geng

European equities are mostly lower [Eurostoxx 50 -0.5%] in a continuation of the subdued lead from Asia in which Hong Kong’s stock index suffered heavy losses due to the mass protests against the controversial extradition bill. Sectors are mixed, with heavy underperformance across energy names (sector -1.2%) amid the slide in oil prices. Meanwhile, defensive sectors (utilities +0.3%, healthcare +0.4%) are in the green as investors flock to the ‘safer’ and more stable stocks. In terms of individual movers, shares in British American Tobacco (-6.0%) fell to the foot of the Stoxx 600 index as the cigarette maker expects global industry volume to fall by around 3.5%, although the Co. reiterated guidance despite its peer Imperial Brands (-1.8%) cutting guidance for their tobacco business yesterday. Elsewhere, shares in Axel Springer (+11.8%) rocketed after KKR’s Traviata confirmed that it is to make a takeover offer for the company for EUR 63/shr (vs. yesterday’s close at EUR 55.85/shr). Meanwhile, SMI’s LafargeHolcim (-3.1%) fell to the bottom of the index after a major shareholder cut his stake in the company.

Top European News

Brexit Britain Contemplates Another Foreign Central Bank Boss

Reckitt Benckiser Names Laxman Narasimhan as CEO From Sept. 1

Britain’s Banking Upstarts Vulnerable to a Downturn, BOE Finds

Drug to Replace Chemotherapy May Reshape Cancer Care

In FX, the Dollar is on the defensive ahead of US headline inflation data that could provide more justification for the Fed to consider a rate cut, with the index only just holding above chart support ahead of 96.500 in the form of the 200 DMA within a 96.578-722 range.

JPY/GBP/EUR/CHF – All taking advantage of the softer Greenback, as the Yen rebounds towards 108.00 and into decent option expiry territory with 1 bn sitting between 108.40-25 before a further 1.2 bn from 108.10 down to the big figure. Note, Usd/Jpy has also pared gains on a partial retracement in global stocks as improving risk sentiment wanes, but the Franc has not regained as much safe-haven allure given Thursday’s SNB quarterly policy review and the likelihood of more NIRP and intervention iterations – check out the headline feed or Research Suite for a detailed preview. Usd/Chf and Eur/Chf remain above 0.9900 and 1.1200 respectively, with the single currency also consolidating above 1.1300 vs the Dollar and inching closer towards last Friday’s post-NFP highs circa 1.1348 where stops are anticipated, but could be countered by hedges for a 1.2 bn expiry at the 1.1350 strike. Meanwhile, Cable has retested yesterday’s post-UK data/BoE commentary peaks just shy of 1.2750 and Eur/Gbp is pivoting 0.8900 awaiting Tory leadership front-runner BoJo’s official campaign launch.

NZD/CAD/AUD – Ongoing global trade concerns are undermining the non-US Dollars, as the Kiwi remains capped below 0.6600 and Loonie retreats further from best levels towards 1.3300, and perhaps takes heed of the more pronounced recoil in crude prices having decoupled somewhat in wake of supportive Canadian jobs data and the fillip from the US and Mexico clinching a deal to avert tariffs. However, the Aussie is underperforming in the run up to tomorrow’s labour report and probing key Fib support circa 0.6945.

EM – Usd/Try is back above 5.8000 amidst latest Turkish remonstrations about the US not adhering to the spirit of alliance on the missile front and reports that an official response to a letter from Washington is being prepared. Meanwhile, the Lira is also looking pressured ahead of the looming CBRT that could turn more dovish given recent inflation data showing a slowdown in CPI, weaker oil and Try appreciation from worst levels – for more see Ransquawk’s headline feed and/or Research Suite.

In commodities, another day of losses for the energy complex with WTI (-2.7%) and Brent (-2.8%) futures heavily pressured amid the latest surprise build in API crude stocks (+4.9mln vs. Exp. -0.5mln) coupled with risk aversion around the market, whilst the EIA’s downgrade in global oil demand forecast only adds to the bearish sentiment. WTI futures currently hover just above the USD 51.50/bbl level, having dipped below its 200 WMA (52.59) whilst its Brent counterpart briefly fell under the USD 60.50/bbl mark. News flow for the complex has been light thus far with participants now gearing up for the weekly DoEs to potentially reinforce the build in stockpiles seen in the APIs. Elsewhere, gold (+0.8%) resumes its climb as the recent relief rally dissipated. The yellow metal is comfortably above the USD 1325/oz level ahead of US CPI data. Turning to base metals, copper prices are sliding despite a weaker Buck amid the absence of risk appetite in the market, although it is worth noting from a supply point of view that Labour unions at Codelco’s Chuquicamata mine are set to reject the latest wage offer in a vote tomorrow, which could see a operations come to a halt at the largest open pit copper mine. Finally, given the recent supply-driven surge in iron ore prices, Chinese steel mills are facing a slump in profit margins and are reportedly seeking lower grade iron ore to cut costs, thus the spread between medium and low grade iron ore in China has narrowed to two-and-half year lows.

US Event Calendar

7am: MBA Mortgage Applications +26.8%, prior 1.5%

8:30am: US CPI MoM, est. 0.1%, prior 0.3%; CPI YoY, est. 1.9%, prior 2.0%

CPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%; US CPI Ex Food and Energy YoY, est. 2.1%, prior 2.1%

Real Avg Hourly Earning YoY, prior 1.2%; Real Avg Weekly Earnings YoY, prior 0.92%

2pm: Monthly Budget Statement, est. $199.5b deficit, prior $146.8b deficit

DB’s Jim Reid concludes the overnight wrap

According to the Oxford English Dictionary, today I venture into middle age as I turn 45. In some ways that’s quite a relief as I just assumed I had been there for some time. I’ll find out later if my dreams have been realised and I’ll be getting an eyebrow comb for my birthday (see last week’s EMRs for an explanation) and also what the children will be buying me with my own money. Wikipedia has this entry for middle age which makes me feel great. “The body may slow down and the middle aged might become more sensitive to diet, substance abuse, stress, and rest. Chronic health problems can become an issue along with disability or disease. Approximately one centimeter of height may be lost per decade. Emotional responses and retrospection vary from person to person. Experiencing a sense of mortality, sadness, or loss is common at this age.” To commiserate my wife and I are having our first night out alone this year. Let’s hope my sensitivity to champagne hasn’t suddenly changed overnight.

The market’s champagne was put on ice last night though as a five day party that had looked likely to extend into a sixth session started to fade. Despite opening as much as +0.83% and +1.09% higher, the S&P 500 and NASDAQ both faded throughout the day to end marginally lower at -0.04% and -0.01% respectively. The trade-related rhetoric from the White House continued to be somewhat negative, as President Trump said that “it’s me right now that’s holding up the deal” and suggested that he will not back down unless China makes new concessions. Two of his main lieutenants, Commerce Secretary Ross and Acting Chief of Staff Mulvaney, both separately downplayed the odds of an agreement at this month’s G-20, though they did say that talks could get back on track if Trump and President Xi can make positive progress. Despite the continued uncertainty, some of the most trade-exposed equity sectors performed well yesterday, with autos gaining +0.56% and Apple up +1.16%, as headlines circulated indicating that they are prepared to completely adjust their supply chain to avoid manufacturing iPhones in China for the US market.

President Trump complemented his trade remarks with a fresh broadside against the Fed, saying “they don’t have a clue” and that rates are too high. He also called “very low inflation” a “beautiful thing” so we’ll see if today’s CPI report changes that dynamic at all. The PPI data – which we’ll run through below – was at the margin slightly hawkish and helped push 2y Treasury yields higher. Indeed 2y Treasuries closed +2.6bps higher at 1.93% while 10y Treasuries ended -0.5bps lower, meaning the curve flattened-3.13bps to 22.1bps, albeit still above the range for much of the year. The DOW shed -0.05%.

Apart from the political noise, there wasn’t a great deal of new news with markets initially reacting to the China infrastructure spend headlines from this time yesterday. This helped Europe with the STOXX 600 finishing +0.69%. The DAX (+0.92%) was the big out-performer having been closed on Monday, while the FTSE 100 gained +0.31% despite the pound’s +0.30% rally on strong wage data.

This morning in Asia markets are largely heading lower with the Hang Seng (-1.50%) leading the declines as locals protest ahead of a legislative council debate on a controversial bill that would allow extraditions to mainland China. The Shanghai Comp (-0.57%) and Kospi (-0.13%) are also lower while the Nikkei (+0.04%) is trading flattish. Elsewhere, futures on the S&P 500 are trading a touch lower. Crude oil prices (WTI -1.52% and Brent -1.40%) are also falling this morning as a report from the American Petroleum Institute reported that the US crude stockpiles increased by a further 4.85mn barrels last week. In terms of overnight data releases, China’s May CPI and PPI both came in line with consensus at +2.7% yoy and +0.6% yoy, respectively. We also saw Japan’s April core machine orders come in at +5.2% mom (vs. -0.8% expected), the third consecutive monthly rise thereby marking the longest sequence of such gains in the past four years, while May PPI came out in line with expectations at +0.7% yoy.

Back to the UK and yesterday saw the Labour Party table a cross-party motion to prevent a no deal Brexit. If such a bill were to pass, the tensions within Parliament would likely escalate towards a general election. On that theme, the Conservative party leadership contest kicks off with its first ballot tomorrow, where a hard Brexit-supporting candidate is likely to emerge victorious at the end of the process. This dysfunctional setup is outlined in more detail in Oliver Harvey’s latest note ( here ), which also updates his indicative probabilities of likely outcomes moving forward. He thinks the odds that a deal is successfully ratified by end-October are now 25%, while the odds of a no-deal Brexit are 25% as well. The remaining 50% is covered by his modal case for a general election, with 20% chance of a Conservative no-deal platform winning, 20% chance of a Labour/Liberal Democrat soft-Brexit platform winning, and 10% chance of no clear winner. The Brexit story and its consequences still have an enormous amount of runway to go but we are currently in the eye of the storm. This fresh parliamentary vote in a couple of weeks could shake things up again leaving a new PM little choice but to go to the country. ComRes published the first opinion poll overnight that I have seen with all the different potential Conservative leaders vs all the other parties. On this poll Boris Johnson is only one of the candidates that give the Tory’s a majority (140 seats) at the next election alongside a substantial 14% lead. He is the only candidate that reduces the Brexit party’s support enough (below 20%) to do this.

In other news from yesterday, the US May PPI report was at the margin slightly hawkish as we mentioned earlier with the ex food and energy reading printing in line at +0.2% mom but ex trade at +0.4% mom (vs. +0.2% expected). In addition, the healthcare component rose +0.25% mom which, when combined with a bounce back for the portfolio management component, suggests a stronger read-through for core PCE when we get the data at the end of this month. Holding everything else steady, today’s print implies around +7bps to the core PCE number due toward the end of this month.

That data dovetails nicely into today’s data highlight which is the CPI report in the US which should act as the next test for markets. The consensus expects a +0.2% mom core reading which would be enough to keep the annual rate at +2.1% yoy. Our US economists also expect a +0.2% mom reading and note that core goods should rebound slightly from the plunge in April which was the biggest monthly decline since 2006. That said, there are some downside risks from negative payback from shelter inflation. The data is due out at 1.30pm BST.

As for the other data yesterday, there was a decent jump in the May NFIB small business optimism reading of 1.5pts to 105.0 (vs. 102.0 expected). That reading had got as low as 101.2 back in January but has since risen every month. Meanwhile, here in the UK the latest employment data was mostly upbeat – in stark contrast to the April growth data we saw on Monday. The unemployment rate was confirmed as holding steady at 3.8% in April as expected, while 32k jobs were added which exceeded expectations. Regular wage growth also ticked up one-tenth to 3.4% compared to expectations for a small deceleration. So that keeps the hawkish labour market data versus BoE’s supply side narrative still very much intact. It’s worth noting that we heard from a couple of different BoE policy makers yesterday. Vleighe – seen as a centrist – said that “news since May has been disappointing in data and downside risks have intensified” while Broadbent said that “I am not particularly exercised that the future path of interest rates in the market should be exactly the one that is in our forecasts,” and thus made little conscious attempt to try and reprice the market.

In other news, yesterday EU officials confirmed their endorsement of the EC’s decision that Italy had failed to take the necessary steps to reduce its debt load in line with the bloc’s fiscal rules. The EU therefore confirmed that a disciplinary process is warranted. BTPs were +3.4bps higher yesterday, lagging the broader European fixed income rally. Italian politicians continued to speak positively, with Finance Minister Tria saying Italy is committed to a dialogue with the EU over the debt censure and Prime Minister Conte announcing that the leaders of the Five Star Movement and the Northern League will meet over the next few days to decide on a plan that will satisfy the Commission since “we are all determined” to avoid an EDP. That said, the market seems to be at a place where actions will speak louder than words.

To the day ahead now, which is headlined by that May CPI report in the US this afternoon. Other than that we’ll get the May monthly budget statement in the US while the European diary is particularly sparse this morning with nothing of note. Away from the data the ECB’s Draghi is due to speak this morning in Frankfurt where he is due to make welcome comments at a conference. The ECB’s Guindos will also speak.

via ZeroHedge News http://bit.ly/2ICpJLh Tyler Durden

Heading into today’s Turkish central bank decision, there was much speculation if the CBRT would become the latest bank to jump onboard the global easing train, ignoring Turkey’s runaway inflation and cutting rates – despite a consensus call for an unchanged print – to stimulate the contracting economy.

Moments ago the answer was unveiled, and for now, Ankara has decided to wait, even though Erdogan has made his displeasure with high rates very clear in recent months.

Specifically, the central bank’s Monetary Policy Committee kept benchmark 1-week repo rate unchanged at 24%, as expected if above whisper numbers. It also kept all three other major rates unchanged, including the Overnight Lending rate (25.50%), Overnight Borrowing rate (22.50%), and the Late Liquidity Window Rate at 27.00%.

Some highlights from the statement:

“Recently released data show that rebalancing trend in the economy has continued.”

“External demand maintains its relative strength while economic activity displays a slow pace, partly due to tight financial conditions.”

“Current account balance is expected to maintain its improving trend.

“Developments in domestic demand conditions and the tight monetary policy support disinflation.”

“In order to contain the risks to the pricing behavior and to reinforce the disinflation process, the Committee has decided to maintain the tight monetary policy stance.”

“Monetary stance will be determined to keep inflation in line with the targeted path.”

As Bloomberg notes, the central bank changed some of the key wording, now saying that monetary policy was kept tight “in order to contain the risks to the pricing behavior and to reinforce the disinflation process,” departing from previous language on future policy path, and dropping the following sentence that appeared in its April 25 decision: “Accordingly, the Committee has decided to maintain the tight monetary policy stance until inflation outlook displays a significant improvement.”

And while the broader Turkish population, as well as Erdogan, may be displeased with the announcement, Lira long were happy, as USDTRY tumbled from 5.815 to 5.785 in moments after the announcement, as the market had braced for a surprise dovish move, especially with “official inflation” recently reported to be coming in below expectations.

Of course, the trade off to no rate hikes is further economic slowness, something Turkey hardly needs especially as the diplomatic feud over Ankara’s decision to purchase a Russian missile system, risking Washington’s ire and sanctions, still looms.

via ZeroHedge News http://bit.ly/2ZmKTUp Tyler Durden

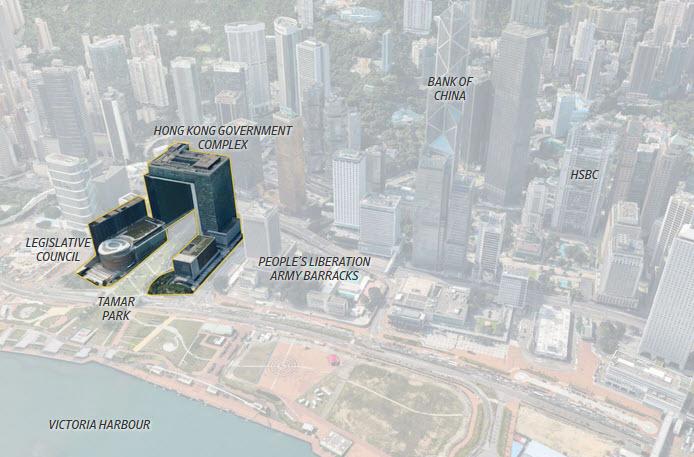

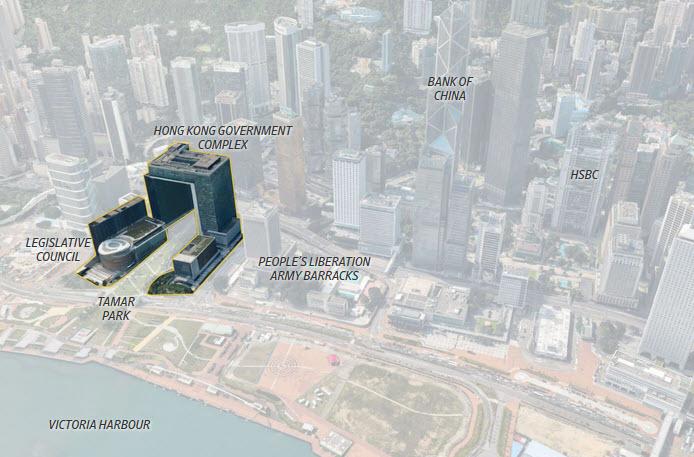

For decades, China has been terrified – and preparing – for a social uprising on the mainland. It was less prepared for one taking place in Hong Kong.

Two day after a massive, 1+ million protest took place in Hong Kong, with demonstrators demanding the end to a proposal allowing extraditions to China, a follow up protest took place with thousands of people blocking local streets, and Hong Kong police defended the use of tear gas and rubber bullets to control a “riot situation” after protesters tried to storm the chamber where lawmakers were expected to take up – and pass – the controversial bill.

As we noted last night, a repeat protest erupted early on Wednesday, and it only got worse as the day progressed as demonstrators – many of them clad in goggles, face masks and helmets -fled to different areas, running through plumes of smoke – threw bricks, bottles and umbrellas at riot police guarding the city’s Legislative Council; they dragged metal barriers and linked arms across roads surrounding government headquarters, in scenes reminiscent of the 79-day street protests that paralyzed parts of downtown Hong Kong in 2014.

The police responded with tear gas, pepper spray and batons. Farther back from the barricades, protesters rapidly ferried umbrellas, gloves, bottles of water and sodium chloride to treat injuries from pepper spray through the crowd to the front.

Hong Kong’s commissioner of police described Wednesday’s demonstrations as “riots” and called on protesters to go home, warning that those who refused “might regret your decision for your entire life.” The remarks by Commissioner Stephen Lo at a news conference came moments after protesters stormed police barricades outside the Legislative Council, leading to the use of tear gas, beanbag rounds and rubber bullets.

“If they are peaceful protesters, please leave,” Mr. Lo said. “If they are violent protesters, then please think twice because you might regret your decision for the entire life.”

At one point there was even speculation that the Chinese army was deployed to Hong Kong.

Police said in a press briefing that some protesters had hurled weapons such as metal barriers and bricks at officers, leaving them with no choice but to contain the crowds with rubber bullets, tear gas, batons, pepper spray and beanbag guns.

Five years ago, the use of tear gas by the police in an attempt to push back against a student democracy protest incited public fury that brought tens of thousands of people onto the streets. That turned into a sustained occupation of several commercial districts for several months in Hong Kong known as the Umbrella Movement, referring to the shield of choice used to fend off police pepper spray.

Due to the violent protests, the Legislative Council delayed debate on the proposal after thousands of demonstrators swarmed the government complex in central Hong Kong, eventually prompting scuffles with police at the chamber doors. The protesters called for Chief Executive Carrie Lam to withdraw the bill, which they argue would blow up the legal wall intended to keep the former British colony’s justice system separate from China’s.

A view of the North side of Hong Kong island, where street protests were held in opposition to a proposed China extradition law.

Lo said his officers had peacefully surrounded the legislature complex but would not permit demonstrators from crossing over the barricade, adding that it was the demonstrators who were the first to use force.

“In terms of using violence, we have guidelines that we are following,” he said, adding that “I think we should all remember who initially started the protest.”

* * *

Trouble erupted midafternoon Wednesday, when hundreds of protesters attempted to push barricades north toward the city’s harbor, then retreated under a bridge after police deployed tear gas against them. All access roads leading to the central government offices, which house the legislature, were blocked, the government said in a statement.

By late Wednesday afternoon, tear gas hung in the air in the city’s main financial and business district. A few office workers looked on as men with masks charged toward the Legislative Council, and the crowd cheered out support and warnings.

So much tear gas was used that commuters waiting at nearby subway stations and people in shopping malls were coughing and tearing up, and many sought medical attention.

Many of the city’s lawmakers, from both the pro-democracy camp that opposes the contentious extradition legislation at the heart of the protests and the pro-Beijing majority that supports it, failed to arrive at the council for a scheduled debate on Wednesday morning, after protesters surrounded the complex and blocked traffic.

Some financial services were also disrupted. HSBC Holdings PLC closed two banking-service outlets in the Admiralty area until further notice, while other banks including Standard Chartered PLC, Bank of East Asia Ltd. and China Citic Bank Corp. temporarily suspended operations at branches near the protest area.

Even though the opposition bloc in the city’s legislature has been weakened after authorities ousted several democratically elected lawmakers through court orders and barred others from running, opposition to the proposed law came from many corners of society, including businesspeople, lawyers and activists, who say the changes would undermine Hong Kong’s relative autonomy and independent judicial system, the US also chimed in: the State Department on Monday said the bill, if passed, could “subject American citizens residing in or visiting Hong Kong to China’s capricious judicial system

According to the WSJ, most of those taking part said they did so spontaneously, filling roles where assistance was needed during the day. Some protesters mounted tram stops nearby, relaying messages and requests for equipment across the heads of the crowd. Keith Liu, a student running a station distributing supplies, said that he didn’t believe the protests could prevent the bill from passing, but that he felt compelled to register his dissent.

“We still have to come out here. We have to fight for ourselves,” he said.

“The government needs to acknowledge that my voice matters,” said Candy Wong, a 27-year-old shop assistant who said she was angered after authorities pressed ahead with the bill even after more than a million people—including herself—took to the streets in protest. Ms. Wong took a day off to join the rally. “If I didn’t come today by next week I may no longer have the freedom to do so.”

via ZeroHedge News http://bit.ly/2IzuoO0 Tyler Durden

Offering yet another example of the trade war will inevitably drive more companies to move manufacturing out of mainland China and to Taiwan or Vietnam instead, Nintendo is shifting production of one of its most popular gaming consoles to limit the impact of US tariffs.

TOKYO— Nintendo Co. NTDOY -2.42% is shifting some production of its Switch videogame console to Southeast Asia from China to limit the impact of possible U.S. tariffs on Chinese-made electronics, said people who work on Nintendo’s supply chain.

[…]

Kyoto-based Nintendo has traditionally relied on the Chinese factories of contract assembly companies to make its videogame hardware.

That includes the Switch console, introduced in 2017.

The Wall Street Journal reported in March that Nintendo planned to update the Switch this year with two new models. One is set to look similar to the current model with beefed-up components, while the other is expected to be a less-expensive model with a new look.

People involved in the supply chain said production in Southeast Asia has started for the Switch, including the current type and the two new models, suggesting Nintendo is getting ready to introduce them soon. They didn’t give specific volume figures but said Nintendo wanted to have enough units to sell in the U.S., the largest market for videogame consoles, when the new products go on the market.

Since Videogame console makers tend to sell their devices at thin margins, in the hopes of earning higher profits on sales of more lucrative games, the move suggests Nintendo is trying to avoid selling its Switch handheld consoles at a loss.

Videogame platform owners tend to sell hardware at a thin profit in hopes of earning revenue from more-lucrative software sales. If Nintendo had to pay a 25% tariff to import its consoles into the U.S., it might be forced to sell them at a loss—something the company has said it wants to avoid.

For the Switch, the latter half of 2019, including the holiday season, is a key period to lock in sales because competitor Microsoft Corp. , maker of the Xbox One, is planning a next-generation console for the 2020 holiday season. Analysts say they expect the new less-expensive model of the Switch to sell for about $200, down from about $300 currently, to propel sales.

The fact that Nintendo’s decision comes just a day after a senior Foxconn executive said Apple’s biggest manufacturing partner had the capacity to move its production outside of China presents an interesting and important message about how quickly global supply chains will change as the trade spat with China intensifies, according to Bill Blain of Mint Partners.

Presumably, it’s a sign that companies aren’t waiting around to see if Trump and Xi manage to come to an amicable solution in Japan later this month. Many are already assuming the trade spat between the world’s two largest economies will persist for months, if not years, and that the US will eventually slap tariffs on the rest of the roughly $300 billion in Chinese imports that haven’t already been impacted.

via ZeroHedge News http://bit.ly/2IzQMac Tyler Durden

The EU is drawing up plans to use technology on the Irish border — despite rubbishing the idea when put forward by Brexiteers.

Eurocrats will deploy “IT systems” to keep trade flowing between Ireland and the EU via Britain if there’s a No Deal Brexit.

In a dossier to be presented to EU leaders next week, officials say a fix “can be implemented swiftly” and that they are in “regular contact” with authorities in Ireland, France and the Netherlands over the contingency plans.

Played for a Fool

Supposedly, technology was an impossible idea when Theresa May asked for such a solution.

The EU played Theresa May like a fool, which of course she was. There was just one little problem: The UK parliament refused to go along.

Now, in the face of No Deal, the “EU is ready to Support the Irish” with technology that supposedly could not work.

Brazen Liars

The EU is nothing but a brazen pack of liars. And Theresa May was in bed with the lot of them.

Please click for a shocking (if you have not seen it yet) video.

The comeuppance and arrogance of the EU towards the UK is staggering. And it’s all captured on film by Lode Desmet, a Belgian filmmaker.

The EU bragged about crushing Theresa May: “We Got More Than We Hoped”

The EU admitted Theresa May wanted a customs union all along.

Michel Barnier spoke on film of “using Ireland for future negotiations. Isolating Ireland and not closing this point, leaving it open for the next two or three years.”

Barnier used the words “permanent pressure” in regards to the backstop.

The EU bragged about “getting rid of the UK on EU terms” and turning the UK into a “colony”

If after playing my video, or the full length 58 minute version, Behind Closed Brexit Doors Part II, you still favor a customs union, your desire must be like Jeremy Corbyn’s: to turn the UK into a vassal or colony of the EU.

The old truism that a ‘sucker is born every minute’ has never been more apt than during the crypto era, when weeks-old ‘companies’ with little more than an incomprehensible white paper and an abundance of bluster managed to raise billions of dollars from crowds of wannabes hoping they might be about to cash in on the next bitcoin.

As many soon learned, that was far from the case. Most ended up holding the bag, and many of the companies that gladly took their money in exchange for now-worthless digital tokens are embroiled in an array of legal troubles, or have devolved into internal squabbling over how the spoils should be distributed.

But with the SEC breathing down their necks, many in the crypto world have turned to an innovative solution: Rejigger the acronym, and suddenly, what you’re doing is legal.

Introducing ‘the IEO’. As WSJ’s Steven Russolillo explains, they’re similar to ICOs, but with one key difference: Digital tokens are sold to investors via a crypto exchange, not directly by the startups themselves. And though the sums raised in these types of offerings are nowhere near the heights of the ICO frenzy, more than $518 million has been raised during 63 IEOs during the first five months of this year. And with the price of bitcoin once again on the rise (the ultimate barometer of interest in crypto), that figure is sure to climb.

Critics of the deals argue the new structure resolves none of the inherent flaws of the old structure (vulnerability to hacks and – oh yeah – outright fraud, to name a few).

As one VC put it: “It’s like ICO 2.0…frauds are waiting to happen. A lot of people got burned in ICO land and I think a lot of people are going to get burned in IEO land.”

Instead of comapny’s issuing these securities directly, presumably trustworthy crypto exchanges act as intermediaries, performing roles akin to that of an investment bank in traditional financial transactions. It’s not in a crypto exchange’s interest to back a faulty IEO, because of the reputational damage. Binance, one of the most popular crypto exchanges, has emerged as a primary backer of IEOs.

Of course, it wasn’t exactly in Lehman Brothers’ interest to engineer its own downfall by hawking ‘AAA’-rated mortgage bonds backed packed to the brim with subprime mortgages.

But we all remember how that turned out.

via ZeroHedge News http://bit.ly/2XF60Rj Tyler Durden

The much-acclaimed series ‘Chernobyl’ tells the story of the 1986 nuclear disaster and the authorities’ attempts to play it down. Ironically, 33 years on, it’s Western leaders who need to learn how to be honest and transparent.

It was the accident which some think led directly to the fall of communism.

“Reformers in the Soviet Union, and Mikhail Gorbachev himself, used Chernobyl as an argument for more accountability and greater frankness, because the initial reaction of the Soviet authorities was anything but transparent. It became a symbol of what was wrong with the Soviet system,” says Professor Archie Brown, author of ‘The Rise and Fall of Communism’, as cited in yesterday’s Sunday Express newspaper.

Just three-and-a-half years after Chernobyl, the Berlin Wall came down, and in 1991, the USSR itself ceased to exist.

Western ideologues were quick to gloat, saying that a system which kept telling people lies and trying to cover things up was always doomed to fail, but in terms of openness and telling the truth, are we really much better than the Soviet Union of the 1980s?

Consider the way a succession of illegal wars has been sold to the public. We were told in 2003 that Iraq had ‘weapons of mass destruction’ which could be assembled and launched within 45 minutes. It was false, patently so, yet the Chilcot Report was only published 13 years later, and even now, no one has been prosecuted in relation to a war which led to the deaths of one million and the rise of Islamic State (IS, formerly ISIS).

In 2011, we went to war again, against Libya. Once more, our politicians were less than honest with us. We were told that we had to bomb because Colonel Gaddafi was going to massacre the inhabitants of Benghazi. Only five-and-a-half years later were we allowed to know the truth. In September 2016, a House of Commons Foreign Affairs Committee report held that “the proposition that Muammar Gaddafi would have ordered the massacre of civilians in Benghazi was not supported by the available evidence… the Government failed to identify that the threat to civilians was overstated and that the rebels included a significant Islamist element.”

Again, we were tricked into war. By ‘nice’ Western politicians, mark you, and not ‘lying’ Soviet ones. Once more, there’s been no accountability. Libya, a country which had the highest Human Development Index in the whole of Africa, was destroyed. It was a far worse disaster than Chernobyl, as indeed Iraq was. When will the HBO dramas on these catastrophes be screening?

It’s not just the illegal wars. There have been cover-ups of plenty of other things, too. Three years after Chernobyl, there was the Hillsborough disaster in which 96 Liverpool football fans were crushed to death. It was the worst disaster in British sporting history. To add insult to tragedy, the fans themselves were blamed. Rupert Murdoch’s Sun claimed on its front page that fans had urinated on policemen and picked the pockets of victims. It took nearly 30 years to get the record formally put right and achieve ‘Justice for the 96’ when a jury held that the fans were ‘unlawfully killed’. The Orgreave Truth and Justice Campaign, which wants a public inquiry into the way striking miners in South Yorkshire were ‘brutalised’ by police in the so-called ‘Battle of Orgreave’ in 1984, are still waiting. In 2016, Home Secretary Amber Rudd said there would be no inquiry.

Where’s the openness and transparency here?

Likewise with the cover-ups over suspected Establishment pedophiles and other high-up wrong-doers. We learnt only this year that Prime Minister Margaret Thatcher had, back in the 80s, personally protected a senior Conservative MP who allegedly had a “penchant for small boys.”

We don’t know whether a leading Soviet politician who was a child-abuser would have been prosecuted. Probably not. But we do know that in Britain in the 1980s, such cover-ups definitely occurred. And who really believes that’s still not the case today?

Bergson and Popper famously divided societies into ‘open’ and ‘closed’ ones, but Western ‘openness’ is not quite as ‘open’ as we’re led to believe. It does not extend to politicians frankly acknowledging the role that Western foreign policy has played in aiding, directly or indirectly, the very same terrorists who have gone on to target Western civilians. That’s a taboo subject, even after the Manchester Arena bombings and the bomber’s link to the MI5-‘sorted’ anti-Gaddafi LIFG, and the slaughter of tourists on the beach in Tunisia by a man who reportedly trained at an IS camp in neighboring ‘liberated’ Libya.

There are many more subjects too that are so taboo I dare not even mention them here. By contrast, dishonest or fact-lite narratives, such as ‘Russiagate’, or the one that holds that the UK Labour Party, an anti-racist party, is ‘awash with anti-Semitism’, hold sway. We CAN talk about these and indeed some commentators talk about little else.

It is the greatest of ironies that at the very same time that we are being told how HBO’s Chernobyl exposes the rottenness of the ‘closed’ Soviet system, a man who does believe in openness and transparency, a free press, and government accountability, is languishing in a maximum security prison in ‘open’ London, facing a possible extradition to the US and sentences of up to 175 years in jail. Julian Assange, whose only crime is wanting to show us what was behind the curtain, is no less persecuted than the Soviet dissidents about whom we heard an awful lot in the 1980s.

It’s been said that if you feud with someone long enough you end up being like them, or at least how you liked to portray them. When we think of the old Cold War and what’s going on today, that seems to have come true.

In its lack of transparency and openness, and the way in which lying has become the new normal, the West is now behaving the way the Soviet Union is supposed to have operated at the time of Chernobyl.

Who, I wonder, will be the equivalent of Mikhail Gorbachev to introduce some much-needed Western Glasnost?

via ZeroHedge News http://bit.ly/2MH6JR8 Tyler Durden

{kind=link}