Reality has begun to dawn across Wall Street’s Economists. This year isn’t going to go the way everyone thought. Even as late as last November and December, the optimism was still sharp about how what was taking place at that moment would be nothing more than a transitory soft patch. They still listened to Jay Powell.

Given a Fed that continues to tighten against the backdrop of increasing Treasury supply, J.P. Morgan forecasts 10-year yields will rise to 2.95% by the second quarter of 2019 and to 3.2% by the end of the year.

Incredibly, these projections were put together on December 20, 2018. Powell had just recently reiterated his strong economy view, the one requiring more rate hikes, the Fed pause still only whispers at that point. Curve collapse was a triviality, apparently, in the face of central bank backbone.

The same bank’s same strategists have now thrown in the towel. Not all the way, at least not yet. They are now calling for much lower rates on the “strength” of at least a couple rate cuts.

According to Bloomberg, the bank is now predicting the 10-year will be just 1.75% by the end of 2018 and 1.65% by next March. Pretty stark contrast compared to what JPM’s CEO was saying at this same time last year.

Even so, as the article notes, this isn’t something they think should be feared. Oh no, there’s a lot to be optimistic about, a lot still left in the tank because the Fed will be on the move!

Despite their new forecasts, JPMorgan’s strategists warned against jumping on the current Treasuries rally, saying that they maintain a neutral call for duration. “We are hesitant to initiate longs given the pace of the rally over the last two weeks and the substantial uncertainty that remains around the path forward for trade policy.”

For their part, JPMorgan equity strategists led by Mislav Matejka still see the potential for gains in global stocks before the next American recession, bolstered by policy support and, in the U.S., buybacks.

If you think trade wars and rate hikes are what led us to this point, then the prospects for a trade deal and rate cuts lend themselves an upside out. If enough can go right, still the soft patch. After all, according to this view, the economy would otherwise be booming.

This remains the background case for most Economists. One appearing on BloombergTV was far more direct in revealing himself this way:

“It’s just a mindless bond market rally — once it gets going, it gets going,” the chief financial economist at MUFG Union Bank said in a recent interview with Bloomberg TV. “I don’t know who’s trading these markets. It doesn’t feel like its [sic] trading completely logically here.”

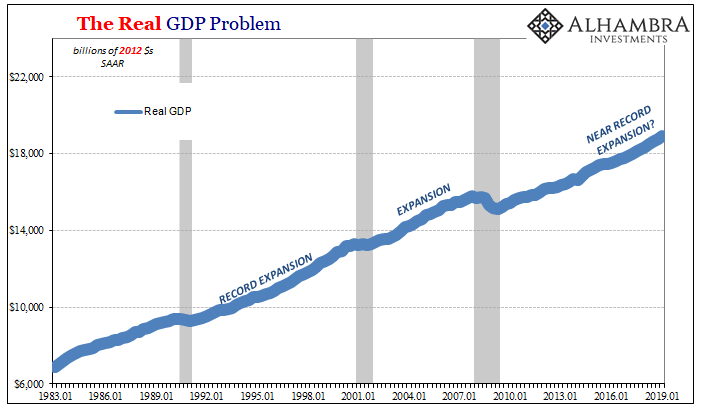

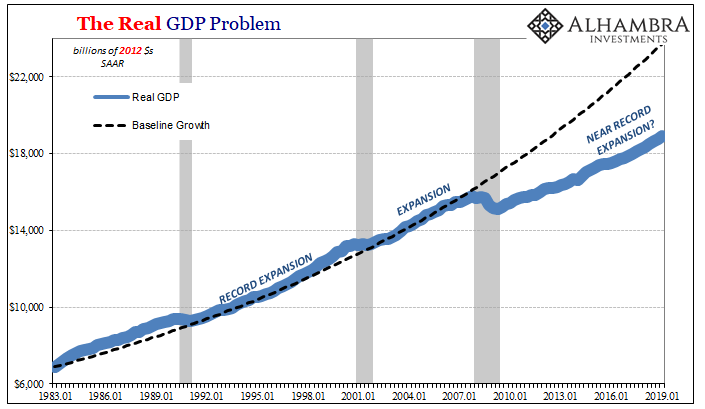

This is the distilled wisdom of the mainstream view, this serious malpractice on the part of the media. All throughout the past few years, it has been reported as fact that the US economy was booming; and even more so why it was. QE had worked, therefore the monetary and financial system cannot be at anyone’s issue.

This view was reported as fact despite the fact that it was the contrary, minority position. This wasn’t how it was ever presented, of course, how it was only ever Economists and central bankers who held to it. The long end of the bond curve, indicating the thinking for the vast majority who matter, never once felt the economy was anywhere near the conditions necessary for taking off.

The various financial curves are treated as out-of-the-way niches, some mysterious triviality about which only a few cranks bother to keep track. Jay Powell is described as a towering figure, the man upon whose opinion everything else flows. It is entirely the other way around.

The bond market is what runs the world. Always has. Therefore, even in 2017 this idea the global economy was about to take off was never more than wishful thinking. If the bond market was against it, that skepticism was always the base case in reality. The bond market in addition to being much larger than stocks could ever hope of being, it is made up of agents whose actual practice (and survival) brings them in close contact to the real money of the real economy.

Economists never had any real market support for their view. Not at any point.

And this is why people have such a hard time understanding the way the world goes. When you are taught the backward, mainstream version, the bond market doesn’t make any sense. “It doesn’t feel like it’s trading completely logically here.” Except, the curves have been making the most sense, and have been most consistent in data therefore forecasting than any other place.

Curves are important notices for every economic situation, but you only hear about them when they are inverted. This isn’t some brand new disagreement. MUFG Union Bank’s Economist is of a blue line believer.

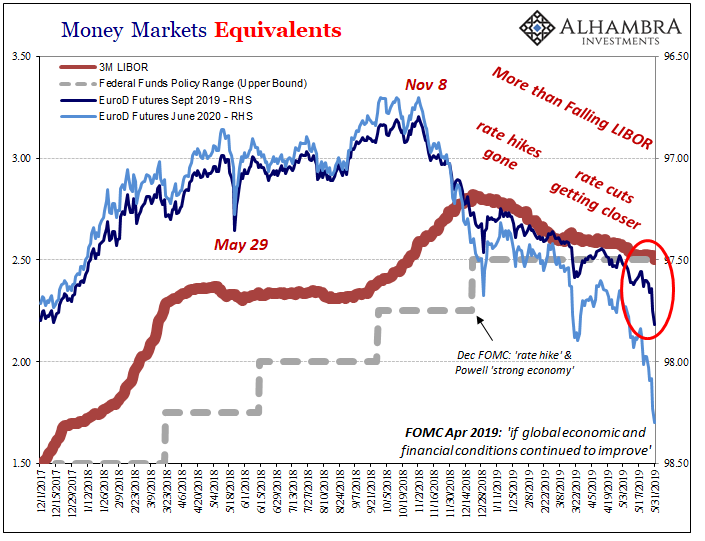

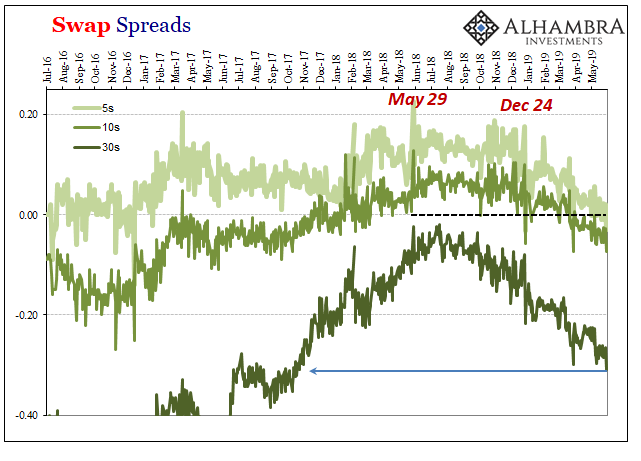

The bond market appreciates only too well what the dotted line has meant all along. Nothing has changed since August 2007. There was only ever a much higher likelihood something would go wrong before it could ever go right. In a nutshell, that’s just what May 29 represented – the very thing that went wrong and proved, all over again, how QE was at best an asset swap and at worst a harmful monetary head fake.

You can’t fix a broken monetary system with a head fake. You can try, but in the end you’d only confuse Economists.

With rate cuts becoming more and more the accepted base case even among these people, you really have to go back to the curves and see the last few years evolve exactly how they predicted. The Economists are already partway to admitting this as true. They’ve already gone from BOND ROUT!!! to rate cuts.

This was no trivial journey. BOND ROUT!!! always meant something specific, the inarguable case of recovery. It would’ve been the point at which central bankers had finally convinced the market the liftoff was more than emotional pleading. I wrote last March, with hysteria raging:

In my view, it’s perfectly clear today that to believe the paradigm is changing is to do so from the same blind position of monetary illiteracy. That’s why it’s been to this point nothing but hype.

To now see the mainstream shift toward rate cuts, it doesn’t matter that they will try to say these will help. By the very fact they have given up on the BOND ROUT!!! it shows the boom was only ever hype. Never happened.

There’s was never the majority position. The recovery was always, always the long shot. It was only presented the other way around by a financial media that does the public a tremendous disservice. The bond market never once climbed aboard the boom. And once you see that, you cannot help but appreciate the very real dangers of 2019.

via ZeroHedge News http://bit.ly/2HUJ6Qy Tyler Durden

A Washington DC district court judge tossed out a lawsuit brought by House Democrats seeking to halt President Trump’s reallocation of funds for a southern border wall.

Judge Trevor McFadden ruled that the matter is fundamentally political and Democrats have a lack of standing to make a legal case.

In February, Trump declared a national emergency over the flood of migrants at the southern border which have overwhelmed the US immigration system. Shortly after, House Speaker Nancy Pelosi (D-CA) and other House Democrats filed their lawsuit, claiming that Trump was “stealing from appropriated funds” and would be in violation of the Appropriations Clause of the Constitution. The politicians contended that this constituted an “institutional injury” to the separation of powers.

McFadden, a Trump appointee, disagreed – writing in his opinion: “This case presents a close question about the appropriate role of the Judiciary in resolving disputes between the other two branches of the Federal Government. To be clear, the court does not imply that Congress may never sue the Executive to protect its powers,” adding “The Court declines to take sides in this fight between the House and the President.“

“This is a case about whether one chamber of Congress has the “constitutional means” to conscript the Judiciary in a political turf war with the President over the implementation of legislation. … [W]hile the Constitution bestows upon Members of the House many powers, it does not grant them standing to hale the Executive Branch into court claiming a dilution of Congress’s legislative authority.The Court therefore lacks jurisdiction to hear the House’s claims and will deny its motion.”

— Judge Trevor McFadden

BREAKING: Judge REJECTS Democrat effort to stop Trump’s use of emergency powers for Wall

Attorney Will Chamberlain, co-founder of Human Events, suggested in January that Trump declare a national emergency at the southern border – and broke down why Democrats would lose a challenge over lack of standing.

— Will Chamberlain 🇺🇸 (@willchamberlain) June 4, 2019

McFadden began by focusing on two guiding Supreme Court cases he called “lodestars”— the 2015 case Arizona State Legislature v. Arizona Independent Redistricting Commission, and the 1997 case Raines v. Byrd.

“Read together, Raines and Arizona State Legislature create a spectrum of sorts,” McFadden wrote. “On one end, individual legislators lack standing to allege a generalized harm to Congress’s Article I power. On the other end, both chambers of a state legislature do have standing to challenge a nullification of their legislative authority brought about through a referendum.”

But, McFadden quickly distinguished the Arizona State Legislature case, which found institutional standing for legislators only in a limited instance. The Arizona case, the judge noted, “does not touch or concern the question whether Congress has standing to bring a suit against the President,” and the Supreme Court has found there was “no federal analogue to Arizona’s initiative power.” –Fox News

McFadden also noted that Democrats still have the power to modify or even repeal an appropriations law if they wish to “exempt future appropriations” from the Trump administration.

“Congress has several political arrows in its quiver to counter perceived threats to its sphere of power,” wrote McFadden. “These tools show that this lawsuit is not a last resort for the House. And this fact is also exemplified by the many other cases across the country challenging the administration’s planned construction of the border wall.”

“The House retains the institutional tools necessary to remedy any harm caused to this power by the Administration’s actions. Its Members can, with a two-thirds majority, override the President’s veto of the resolution voiding the National Emergency Declaration. They did not. It can amend appropriations laws to expressly restrict the transfer or spending of funds for a border wall under Sections 284 and 2808. Indeed, it appears to be doing so.”

As noted by Fox News, McFadden’s ruling contrasted with an injunction issued by Obama-appointed US District Court Judge Hawyood Gilliam last week, who blocked the Trump administration from using the reallocated funds for specific areas in Arizona and Texas.

via ZeroHedge News http://bit.ly/2Z9f8On Tyler Durden

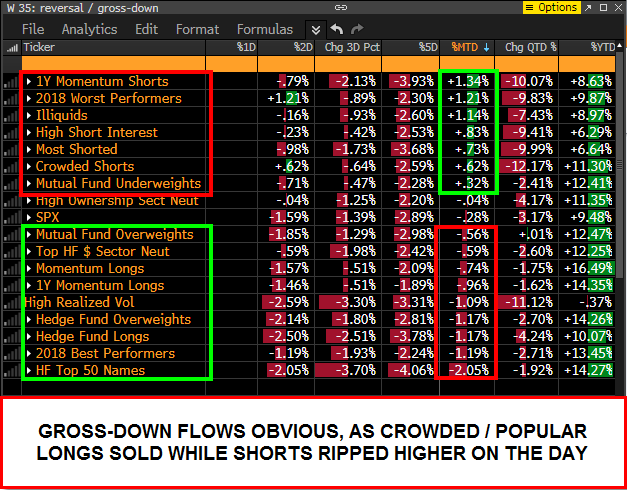

It’s probably a coincidence but on the day we warned that the hedge fund “redemption rush” returned, just ahead of news that UK’s Neil Woodford has blocked redemptions from his £3.7bn equity income fund, that the broader L/S hedge fund community suffered what Nomura calculated was a beating on par with the worst day of 2019.

Specifically, as Charlie McElligott writes this morning, after an extended period of outperformance for long/short hedge funds, “thanks to grossed-up shorts having done their jobs–along with “low nets” that come with them”, yesterday’s below the hood behavior was “outright ugly”, and according to the Nomura strategist was “tied for the worst performance day YTD for his model Equities L/S HF (-1.7% on the session) in classic “gross-down” fashion”, as crowded cyclical shorts exploding higher on forced covers (Materials +3.4%, Energy +1.4%, Industrials +0.7%, Financials +0.7%) while crowded longs – recall our Sunday article “These “Most Crowded Stocks” Face The Greatest Risk Of Wipe Out” which again was published at just the right time – were destroyed (Cons Disc -1.2%, Tech -1.8%, Comm Services -2.8%, Software 8x’s EV/Sales -5.2%) — and as such, “it was rationally the worst day for 1Y Price Momentum factor (-2.3% on session) in nearly two months.“

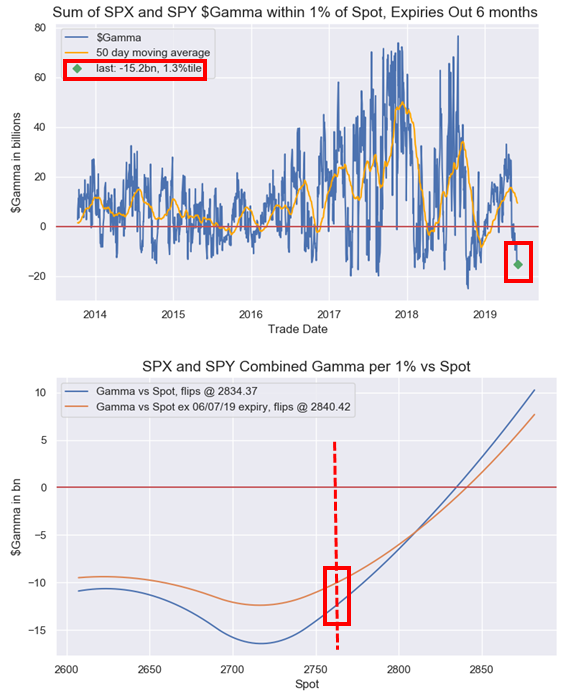

A separate reason for yesterday’s meltdown in hedge fund favorite stocks was the “extreme gamma” positioning we discussed yesterday morning. As Nomura explains, yesterday’s overall Equities trade “was the exact chop-fest you should expect with the “extreme Gamma” market (sum of SPX / SPY $Gamma currently just 1.3%ile since 2013), featuring a 22 handle opening selloff, followed by a 26 handle rally, before a later 30 handle selloff, before another 20 handle rally, a 20 handle selloff, a 15 handle rally, a 25 handle selloff and a 15 handle rally into the cash session close.”

Meanwhile, another way of looking at yesterday’s massive rotation, is that as has been the case frequently in the past, “the big performance drawdown days for US Equities funds continue to come when chronically underweighted / structurally shorted “Value” factor squeezes / rallies against the enormous length crowded into “Growth” factor, which has been accumulated as a duration-sensitive alternative to traditional Defensives”, according to McElligott, and yesterday “was the largest “Value / Growth” ratio reversal higher since late Nov 2016…although nary just a micro-move relative to the decade-long “Growth over Value” phenomenon since the GFC and QE began.”

Said another way—“expensive” Growth stocks were purged (on the somewhat idiosyncratic anti-trust escalations) while “cheap” and heavily-shorted Value stocks were covered—which although only being one day’s worth of behavior IS notable, because it mimics pre-recessionary behavior where Value factor L/S sees signs of life, as Value Shorts (aka expensive Growth Longs) break down first, before Value Longs (aka Cyclicals) begin to outperform on sensitivity to perceived Fed easing / stimulus coming down-the-pipe

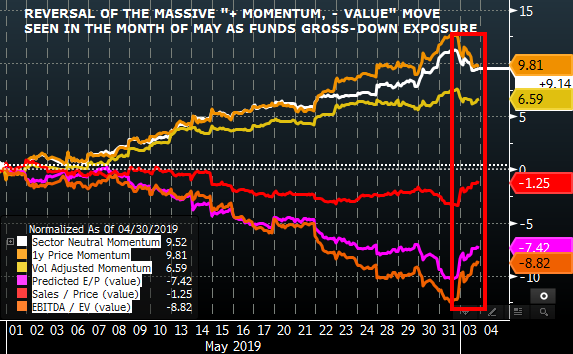

As McElligott shows in the chart below, yesterday was the partial unwind/gross down of much of May’s “slowflation” rally in which momentum soared (long growth and defensives, short cyclicals) while value was hit as a result of the trade war growth scare.

Going back to Monday’s hedge fund hammering, McElligott also notes that when the “Value/Momentum” reversal ratio spikes as it did yesterday, a sharp equities hedge fund performance drawdown follows, something which Neil Woodford is all too familiar with.

Discretionary funds aside, one final observation is what CTAs are doing and about to do. Following on our report from last night that CTAs are now shorting the Russell 2000, and it is only a matter of time before they turn short on the S&P 500, McElligott writes that his own CTA model has seen systematics also “flip short” the NASDAQ (if within range of cover), while CTAs on S&P are in no man’s land: 30 points below re-leveraging levels (2,791 to get to 82% net long), and 25 handles above the 2,735 de-leveraging level to -100% Short”

S&P 500, currently 67.7% long, [2749.6 close yesterday, spot currently 2760], more buying over 2791.31 (+1.52%) to get to 82% , max long over 2938.32 (+6.86%), selling under 2735.48 (-0.51%) to get to -16% , more selling under 2735.2 (-0.52%) to get to -100% , flip to short under 2735.48 (-0.51%), max short under 2735.2 (-0.52%)

And with the S&P now withing close proximity to both buy and sell trigger points for the CTA community, Nomura makes these final observations:

The positioning across Global Equities has tilted boldly “Short”

The Bonds/Front-End “Long” remains massively in-the-money

USD remains a “+100% Long” across all nearly all pairs

Commodities are off the extreme “-100% Short” of last month, with Metals tilting “Neutral to Long,” with Crude “Neutral” and Ag products generally still “Short”

And visually:

via ZeroHedge News http://bit.ly/2Z7KiGa Tyler Durden

Boris Johnson has basked in President Trump’s praise, touting Trump’s endorsement as yet another reason why he should succeed Theresa May as Britain’s next prime minister. But when the opportunity arose for Johnson to meet Trump, the former foreign secretary snubbed the leader of the free world, saying he was “too busy” to meet with him.

Over the weekend, Trump praised Johnson as a “friend” and as a “very talented” politician with whom the US might be able to negotiate a sweeping trade deal (Trump has repeatedly brought up the possibility of a trade deal during his trip, to the delight of Brexiteers who are pushing for a ‘no deal’ exit from the EU). Trump has also compared Johnson favorably to Theresa May (much, we imagine, to the prime minister’s chagrin).

But during a Tuesday morning phone call, Johnson reportedly turned down the opportunity for a one-on-one meeting with Trump because of a Conservative leadership hustings event, according to ITV reporter Robert Peston.

A spokesman for Johnson’s office told British media that the decision was intended to show just how seriously Johnson – who is far and away the favorite to win the Tory leadership contest – is taking the race.

.@BorisJohnson has had a 20 minute phone chat with @realDonaldTrump this morning but declined face-to-face meeting this evening because clashed with One Nation leadership hustings. See attached pic.twitter.com/3hk9yyY17w

The two spoke on the phone for 20 minutes, and Johnson told Trump he looked forward to meeting at a later date.

However, there’s reason to suspect that the snub was a calculated political maneuver. Polls show Trump isn’t particularly popular with British voters, though Johnson remains the most popular conservative in the country.

Instead of meeting with Johnson, Trump will now instead meet with one of his leading rivals, Environmental Secretary Michael Gove, who interviewed Trump in the days before his inauguration. At the time, Gove was working as a columnist for the Rupert Murdoch-owned Times of London.

Trump might also find time to meet with Nigel Farage, whom he recently recommended should be sent to Brussels to lead the next round of Brexit deal talks.

via ZeroHedge News http://bit.ly/2WpYcqf Tyler Durden

Last Thursday, President Trump tweeted he would impose a 5% tariff on all goods coming from Mexico starting next Monday [June 10] “until such time as illegal migrants coming through Mexico, and into our Country, STOP.” The tariff, if authorized by the White House, could make popular Mexican beer like Corona and Modelo, a whole lot more expensive for American consumers, reported CNBC.

On June 10th, the United States will impose a 5% Tariff on all goods coming into our Country from Mexico, until such time as illegal migrants coming through Mexico, and into our Country, STOP. The Tariff will gradually increase until the Illegal Immigration problem is remedied,..

A statement published by the White House said tariffs on Mexican imports would surge to 25% if the immigration crisis at the border is not resolved immediately.

A senior Mexican delegation will start high-level immigration talks on Monday in Washington to hopefully resolve the issue and thwart tariffs.

The announcement of possible duties gaped down Constellation Brands’ stock 8% at one point last Friday.

According to Morgan Stanley, 75% of Constellation Brand’s beer portfolio is “entirely imported” from Mexico. MS said in a research note to investors that a 5% tariff would cut 4% rom the company’s bottom line. In the case of a 25% tariff rate, well, the company’s profits would collapse by 19%.

Jim McGreevy, president and CEO of the Beer Institute, spoke with the Chicago Tribune who said tariffs on Mexico would harm the American trucking industry and farmers along the supply chain if Mexican brewers see a decline in activity. US farmers exported $209 million in barley to Mexican beer producers last year, McGreevy said.

It’s likely that the importer on record will pass along the tariff in the form of higher prices to consumers. The beer industry has already been slapped with $349 million in additional costs thanks to President Trump’s steel and aluminum tariffs.

Chicago-based MillerCoors, which imports the Mexican beer Sol, would be another beer to see possible price hikes if the tariffs went through next week. Heineken, which imports Dos Equis and Tecate, are more beers that could see price hikes. Anheuser Busch InBev, which imports Mexican beer Estrella Jalisco, could also see increased prices.

To “Make America Great Again,” consumers will have to pay up for their favorite Mexican beers – at what point does the blue collar worker, living paycheck to paycheck, start noticing soaring prices thanks to President Trump’s trade war?

via ZeroHedge News http://bit.ly/2QHuzuk Tyler Durden

An Angel who not so much as Fall, as saunter vaguely downwards…”

This is crazy. Some analysts are predicting 3 Fed eases by year end. Australia and New Zealand have cut rates. German yields are now negative 0.21%. Nothing screams recession more loudly!

The market is discounting US rates 70 bp lower. Everyone is listening for what the Fed says next, and it’s a Fed heavy schedule of speakers this week. Fed Head Jerome Powell could firm the tone when he speaks later today, but we’ve already had a former hawk, Lael Bullard warning “downward policy may be warranted”.

What’s really happening? A pre-emptive Fed getting ready to mitigate the negative effects of Trump’s trade twitter war on the economy? Or does the real data really suggest the last thing the US needs is further monetary distortion from overly low rates, and what’s really happening is the Fed pandering to a wobbly stock market? Massive deflationary risk somewhere down the timeline?

The stock analysts are loving it. They see lower rates driving renewed upside – they don’t care about the long-term distortions! All they want is a schweet short-term hit of rate ease to put stocks back into the stratosphere.

When bonds are yielding very little (I was going to say the square root of nothing, but one investment banking pedant sent me pages of maths y’day explaining why that isn’t a good metaphor), then it stimulates dangerous yield tourism. Low rates encourage bad things – like corporates to overleverage themselves to mount stock buybacks with debt – which increases executive bonuses but doesn’t build new factories or infrastructure. The end-result is a more distorted market reliant on lower for ever rates to stop the bubble bursting.

Short-term, its great. Fill your boots with stocks. Long-term…. Be very aware it is not real.

Perhaps the bubble is fraying in the tech sector. Yesterday’s news about anti-trust investigations into names like Facebook, Alphabet, Amazon and others might have been a light bulb moment – but its been enough to remind investors of regulatory risk as the US agencies divvy up names to attack!

Instead of dwelling on the distortions of the Anglo-Saxon markets, lets take a look at Europe. If you really want a disappointing stock to follow, then try Germany’s “leading” bank. It’s so bad, I thought I’d find Neil Woodford listed among the largest holders of the stock!

As Deutsche Bank tumbles to new lows – dragging other lame European banks in its plummeting wake, you have to wonder where it ends? It’s getting embarrassing – you almost wish they’d do the honourable thing. But no, the CEO, Christian Sewing is coming back with yet another plan to cut headcount in rates and equity trading to restore profitability by the end of July.

The cost of CDS protection has rocketed, but I’m actually surprised the bank’s CoCos aren’t lower given Deutsche’s previous history of pleasing investors when its missed calls! I’m afraid DB looks, smells and feels like a complete FUBAR. I’m awarding Bloomberg a “No-Sh*t Sherlock” for pointing out investors are frustrated at its 90% decline since the Global Financial Crisis. NSS!

But its not just Deutsche. Right across the whole European Banking sector the names honk and are spiralling lower in a sea of red. European banks – you’d have to be daft to buy them… yet more than a few stockpickers say… “they will represent value, soon!” Anything – with the possible exception of DB – has value when it is cheap enough.

When I were young… European banks dominated the league tables for bank lending, IPOs and Eurobonds. Today, they are practically absent. Why have the Americans thrived while Europe has rotted? It’s a question of environment and oversight. The US authorities aggressively dealt with banks during the crisis. Lehman demonstrated they were serious. They forced banks to accept recapitalisations and the banks responded by paying back as quickly as they could. And the banks were encouraged to go out and starting banking again.

In Europe, the banking crisis came later, and the banks never so thoroughly cleansed and reinvented themselves. Their underlying weakness was considered a secondary aspect of the European sovereign debt crisis. Free TLTRO money from the ECB kept them afloat, but primarily allowed them to stabilise spiralling European sovereign debt markets. But… there was no rebuild, and no reinvention of banking. European banks remain essentially national banks, meaning post-crisis austerity kept them from any kind of stable recovery, and unable to really address ongoing bad lending.

We all know the European banks’ obvious problems. They are getting spanked by low interest rates, falling bond yields, and rising trade war threats. But it’s a more complex story; rising regulatory costs and compliance will soon exceed 10% of revenues across Europe dismal banking scene. The fact most European banks trade below asset value hints that we don’t believe where the banks value these assets. No surprise. Banks holding assets in basket case countries – yes, I am thinking of Italy – remain vulnerable. Deutsche is the worst – trading at 18% of book value. Isn’t Germany supposed to be Europe’s economic hot spot?

Years of ultra-low and negative European banks has done nothing to improve credit quality. Instead, its enabled Zombie borrowers to survive for longer, meaning any recovery is likely to trigger a normalisation in default rates. And European banks are still plagued by high NPLs.

It’s not just Deutsche. The WSJ recently pointed out that the eight largest European banks have triple the assets, but are worth less than JP Morgan! Italian banks are massively exposed to Italian debt – and there isn’t any way that’s a positive. Even decent names like BBVA and Santander are getting caned – they had the good sense to seek earnings outside Europe, but this week are pulled down by their Mexican affiliations.

Where do we think European banks are going? They are burdened with an overbanked market, aging systems, a lack of resources to digitise and re-invent their services, and there are still no signs of any European banks emerging as cross border champions. European banking union is another EU initiative that seems to have drowned in the sea of bureaucracy that sinks everything. Governments still see their duty as protecting national banking champions. There is repeated regulatory failure; Danske Bank in terms of money laundering and the collapse of Spanish and Italian banks doesn’t help. No European banks are expanding, building market share. Instead they are all and have been retrenching.

If I could think of something positive to say about Europe, But I really can’t….

via ZeroHedge News http://bit.ly/2Ii5P8h Tyler Durden

US equity futures and Treasury yields are trading higher this morning following yesterday’s tech wreck and bond buyathon but relative strength signals are flashing warning signs that the risk of reversion looms large…

Treasury yields are ‘most oversold’ (bonds most overbought) in 21 years…

And stocks are most oversold since the December lows…

We suspect the real canary in the coalmine for a bounce will be HY credit which has been the high-beta horror of this latest collapse…

And has the ‘correction’ run its course as liquidity is re-injected to save the world?

So which is it? Beware the bounce or buy the dip?

via ZeroHedge News http://bit.ly/2XpN1tT Tyler Durden

US stocks futures spiked just before 8 am Eastern Time on Tuesday after the Chinese Ministry Commerce struck an unexpectedly conciliatory tone, saying it believed trade differences should be “resolved through dialogue.”

CHINA HOPES U.S. TO STOP WRONG DOINGS,MEET CHINA HALFWAY:MOFCOM

CHINA COMMERCE MINISTRY SAYS THE DIFFERENCES AND FRICTIONS BETWEEN CHINA AND THE U.S. SHOULD BE RESOLVED THROUGH DIALOGUE AND NEGOTIATIONS

This was a marked departure from rhetoric bashing Secretary of State Mike Pompeo and a travel advisory warning about the risks of traveling in the US.

Nasdaq futures shot higher, setting the stage for an even more robust recovery after the index tumbled into correction territory on Monday.

To be sure, Washington and Beijing have tried this approach before (remember the ‘trade truce’ that now seems like a distant memory?). The approach worked until a deal was reportedly imminent, at which point Beijing reneged on all of its agreements.

via ZeroHedge News http://bit.ly/2Z3hbne Tyler Durden

President Trump and outgoing UK Prime Minister Theresa May are meeting at No. 10 Downing Street as we speak, and in keeping with both the solemn timing of the occasion (Tuesday is the 30th anniversary of the Tiananmen Square Massacre) and the issues of the day (the US-China trade war), Trump is expected to make a last-ditch lobbying effort to try and convince the UK to prohibit Huawei equipment from being incorporated into its 5G network, according to Bloomberg and the AP.

At the urging of the US, the UK has become somewhat more wary of Huawei, though the biggest steps have been taken by the private sector, with the UK’s largest wireless networks dropping Huawei phones from their 5G launch, in part to comply with the US ‘blacklisting’ of the Chinese telecoms giant.

Last month, the Trump administration placed Huawei and dozens of its affiliates on a ‘black list’.The US also issued a separate order banning American telecoms companies from using foreign-made telecoms equipment that could threaten national security (though both orders have been suspended for 90 days).

A few months back, the UK’s cyber-security chiefs had concluded that the risks posed by Huawei could be managed. However, more recently, officials have highlighted serious flaws with Huawei equipment, suggesting that at least some restrictions will be imposed.

Before the meeting, May’s spokeswoman told reporters that the government is still reviewing its policy on Huawei, and will ultimately make a decision based on “hard-headed technical assessments.”

During an interview with the BBC on Monday, Foreign Minister Jeremy Hunt said the UK is “sensitive” to Huawei’s concerns: “We take careful notice of everything the US says on these issues.”

UK Security Minister Ben Wallace said the British government hasn’t made a final decision, though the UK believes in “fair play” and would like to give the company a chance.

Washington launched a lobbying campaign late last year to try and convince its European allies to shut Huawei out of 5G broadband networks, arguing that the company represents a national security threat by creating an opening for the Chinese MSS to spy on citizens and governments. And, as the New York Times pointed out, there’s also concern that Huawei would have leverage to shut down communications networks should there be a conflict with the West.

May’s office also said the two leaders would discuss relations with Iran and the nuclear deal as the administration escalates its military posturing in the Persian Gulf in response to an unspecified Iranian threat. The UK and the other European signatories to the Iran deal have urged the US to reconsider abandoning the deal, and even threatened to find a workaround allowing them to continue trading with Iran in violation of US sanctions.

Chinese officials were already on tenterhooks on Tuesday, with Global Times editor Hu Xijin, a mouthpiece for the ruling Communist Party, accused Secretary of State Mike Pence of being “keen on destroying China’s development capability” after Pence tweeted that the US would honor the victims of Tiananmen Square.

This government of you has ruined positive image of the US. The Chinese now deeply believe key US officials are keen on destroying China’s development capability. When you preach Tiananmen incident and human rights, the purpose is the same as you talk about tariffs and Huawei. https://t.co/yUu0mvP9ug

That tweet was likely only a taste of what’s to come. Later, Vice President Mike Pence is expected to give what has been described as a “hawkish” policy speech on China, which will focus on the country’s human rights record – something that is guaranteed to incense the Chinese leadership at a time when the prospects for a trade deal are dwindling.

via ZeroHedge News http://bit.ly/2wCpAly Tyler Durden

Global stocks rebounded from Monday’s hammering even as worries about a regulatory crackdown on the world’s internet and social media giants compounded mounting global trade and recession jitters, while interest rates remained just shy of multi-year lows as Treasuries dipped for the first time in a week while the dollar was unchanaged.

Europe’s STOXX 600 index recovered from a weak start, reversing earlier losses of as much as 0.7% led by gains in autos and chemicals shares, but tech stocks remained more than 1% lower after reports the US government was gearing up to investigate whether Amazon, Apple, Facebook and Google misused their market power. The Stoxx 600 Automobiles & Parts Index is best-performing as RBC says that it has a more positive bias on the region’s carmakers. BASF (+3%) and Linde (+1.3%) lead gains in chemical stocks.

Earlier, Asian shares dropped as the broadest index of Asia-Pacific shares outside Japan had ended down 0.3%, catching down to the US tech rout, as communications stocks fell while materials shares gained. Most markets in the region were down. The Shanghai Composite Index fell 1%, while Hong Kong’s Hang Seng Index declined for a fifth day in its longest losing streak since April. India’s S&P BSE Sensex Index retreated after reaching a fresh record ahead of the central bank’s rate decision later this week. Emerging-market stocks fell for the first time in three days .

On Monday a combined $85 billion was wiped off Facebook and Google parent Alphabet’s market caps, in the worst rout for the FANG sector in two years…

…which in turn dragged the Nasdaq into correction territory, having lost 10% over the last month.

“That (U.S. investigation) is currently weighing on stocks, but more importantly the market is increasingly pricing in the risk of recession,” said Rabobank senior macro strategist Teeuwe Mevissen. “Sentiment is significantly suppressed.”

Meanwhile, global monetary policy remains in focus this week as the hostile trade rhetoric between the U.S. and China continues. Fed ratesetter James Bullard said on Monday lowering U.S. rates “may be warranted soon”.

Sure enough, after nearly 3 years of resisting any change to its monetary policy, Australia’s central bank cut rates to a record low and on Thursday the European Central Bank is set to detail a fresh dump of cheap money. India is expected to lower its rates too.

After a furious plunge on Monday in a move that left many rates traders shocked, US Treasury yields also rose but remained near recent lows. U.S. 10-year notes yielded 2.0968% after touching 2.06, the lowest since September 2017. All this underlined the scramble to re-price Fed policy and the biggest two-day drop in U.S. two-year Treasury yields since the 2008 crash. The yield curve between three-month and 10-year debt has inverted by as much as 27 basis points, historically a recession signal. More shockingly, the curve between the 3 month and 2 year was the most inverted since the financial crisis.

In FX, the dollar halted a three-day decline and Treasury yields rose as traders awaited clues on monetary policy when Federal Reserve Chairman Jerome Powell speaks later Tuesday. The euro touched its highest level in seven weeks against the dollar before erasing gains after regional inflation data fell slightly short of expectations even as unemployment dropped more than expected. The pound fluctuated after data showed U.K. retail sales in May declined by the most on record.

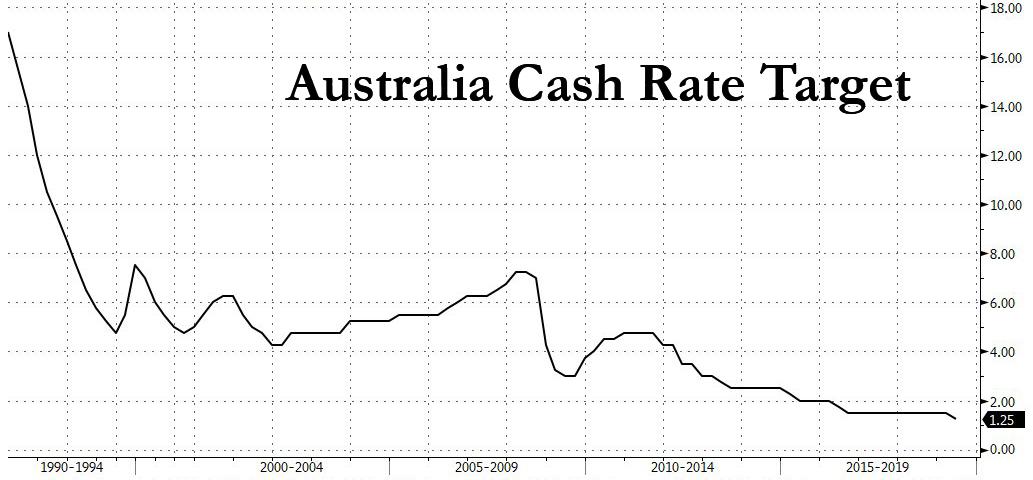

The AUD/USD advanced briefly after the RBA lowered the cash rate by a quarter-point to 1.25%, citing a need to boost employment and spur inflation. It however surrendered the gain as traders interpreted a move by the Australia & New Zealand Banking Group Ltd. to reduce its mortgage rate as a signal that the central bank may need to cut rates further to achieve its desired impact on the economy. Additionally, Australia’s central bank chief strongly suggested he could follow up Tuesday’s interest- rate cut with another reduction as he seeks to drive down unemployment and revive inflation.

EM currencies, however, extended gains to a fourth day, the longest rally since March, as the dollar remained subdued while traders await further developments on the trade front. South Africa’s rand fell by more than 1% after reporting the biggest first-quarter GDP contraction since 2009. The Thai baht, Hungarian forint and Mexico’s peso led the charge higher as MSCI’s Emerging Markets Currency Index climbed to a three-week high. The yuan and India’s rupee were outliers on the day. “Markets continued to digest the implications of a potential tariff on Mexican exports to the U.S.,” Guillaume Tresca, a Montrouge, France-based strategist at Credit Agricole SA, said in a note to clients. “The timeline for dialogue and resolution is pretty tight. Depending on the outcome, FX and rates markets could go through another round of correction.”

Finally, the Turkish lira initially dropped, then rebounded even after Turkish President Erdogan repeated that Turkey will not take a step back from the Russian S-400 missile deal.

“Risk aversion has also been seen with the yen carry trade unwinding as the markets comprehend that the U.S. technology containment strategy towards China is unlikely to reverse,” analysts at Jefferies said in a note. “In the short term, positioning has become so bearish that ‘a ceasefire’ could spark a risk rally,” they said.

In overnight geopolitical news, China issued a warning against travelling to the US; subsequently, China’s Foreign Ministry says it is clear that every set-back in US trade talks was due to the US breaking consensus, have resolve and ability to defend their interests and rights. Elsewhere, Commerce Secretary Ross reiterated President Trump’s message that Mexico needs to do more on illegal immigration in a meeting with Mexico’s Economic Minister, while Mexico said without its efforts a further 500k migrants would reach US this year and that they could take several paths if the US goes ahead with the tariffs including asking for help from WTO or implementing its own tariffs on US goods. This is as the WaPo reported that US Congressional Republicans are discussing moves to stop Trump’s tariffs on Mexico.

Finally, oil fell and was hovering on the edge of a bear market after the Wall Street banks raised the specter of a recession, while Saudi Arabia tried to assure investors that OPEC will avert a supply glut. Brent crude futures are now testing $60 per barrel for the first time in four months. It was last down 0.6% at $60.92 per barrel and U.S. crude was down 0.4% at $53.02. In contrast, safe-have gold was up 0.1% at $1,326.47 per ounce, near three-month highs.

Expected data include factory orders and durable goods orders. Tiffany and Salesforce are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 0.5% to 2,763.00

STOXX Europe 600 down 0.2% to 369.69

MXAP down 0.1% to 152.41

MXAPJ down 0.3% to 499.82

Nikkei down 0.01% to 20,408.54

Topix up 0.01% to 1,499.09

Hang Seng Index down 0.5% to 26,761.52

Shanghai Composite down 1% to 2,862.28

Sensex down 0.1% to 40,218.55

Australia S&P/ASX 200 up 0.2% to 6,332.36

Kospi down 0.04% to 2,066.97

German 10Y yield fell 0.7 bps to -0.208%

Euro up 0.2% to $1.1259

Italian 10Y yield fell 10.8 bps to 2.189%

Spanish 10Y yield fell 1.5 bps to 0.677%

Brent futures down 0.3% to $61.10/bbl

Gold spot down 0.2% to $1,323.23

U.S. Dollar Index up 0.1% to 97.24

Top Overnight News from Bloomberg

Investors are plowing into Treasuries, favoring shorter maturities in particular, on growing conviction the Federal Reserve will cut interest rates this year to contain the fallout from trade tensions. Two-year yields sank to their lowest level since December 2017 and have tumbled by more than a quarter- point since the middle of last week

The Federal Reserve may need to cut interest rates soon to prop up inflation and counter downside economic risks from an escalating trade war, St. Louis Fed President James Bullard said

Yuan watchers arguing that China shouldn’t be scared of the currency breaking 7 a dollar are being emboldened by a former central bank official’s support for their thesis

Germany’s Chancellor Angela Merkel won her rattled government some time as her junior coalition partner agreed to remain on board for a while longer despite the turbulent resignation of its chief.

Italian Prime Minister Giuseppe Conte threatened to resign if the partners in his populist coalition don’t stop posturing, demanding they get to work on new policies to help the country

Oil edged closer to a bear market collapse as Wall Street banks raised the specter of a recession, while Saudi Arabia tried to assure investors that OPEC will avert a supply glut

There is no fundamental change in the view that Japan’s economy is gradually recovering, says Taro Aso, assessing the economic outlook in the runup to a planned sales tax hike in October.

China issued a travel advisory on the U.S. through the end of the year, amid spiraling trade tensions between the two countries

Donald Trump is expected to wade further into the U.K.’s fraught politics on a visit to London, having already dangled the promise of a trade deal if his hosts push on with Brexit

Australia’s central bank chief strongly suggested he could follow up Tuesday’s interest- rate cut with another reduction as he seeks to drive down unemployment and revive inflation

Asian equity markets traded subdued after the headwinds from Wall St where tech underperformed and the Nasdaq slipped into a correction as FAANG stocks were hit on reports of the US launching antitrust and business practice probes into the large tech names. ASX 200 (+0.2%) and Nikkei 225 (U/C) were indecisive as strength in mining names and a widely anticipated RBA rate cut helped offset the tech losses in Australia, while trade in Tokyo was relatively uneventful with exporter sentiment dampened by further unfavourable currency flows. Hang Seng (-0.5%) and Shanghai Comp. (-1.0%) weakened as trade tensions persisted as the US accused China of misrepresenting trade talks and placed the blame on Chinese negotiators back-peddling on issues, while the PBoC’s liquidity efforts resulted to a daily net drain of CNY 90bln. Finally, 10yr JGBs were higher and the 10yr yield dropped to the lowest since August 2016 of below -0.10% amid the risk averse tone and as prices tracked the moves in T-notes following the comments from Fed’s Bullard, while 10yr JGB auction results showed higher accepted prices.

Top Asian News

China to Audit Sanofi, Bristol-Myers in Drugmaker Accounts Probe

Australia Cuts Key Rate to Record Low, Ending Near 3-Year Pause

Major European indices are now firmer [Euro Stoxx 50 +0.6%] and diverting from the negative overnight session as tech suffered with FAANG stocks underperforming on Wall St. due to reports that the US is launching an antitrust and business practice probe into tech names. While tech names still lag, the sectors has come off of lows as equities have been grinding higher this morning with no significant fundamental drivers behind the move. EU sectors are mixed, with the aforementioned tech sector underperforming on the potential probes into tech names; sector heavyweight SAP (-1.5%) is the notable negative tech stock as it comprises a 27.6% sector weighting, and has over a 10% weighting in the DAX (+0.8%). Elsewhere, other notable movers this morning include Hargreaves Lansdown (-4.2%) at the bottom of both the Stoxx 600 and FTSE 100 (+0.2%), following concern over customer backlash as the Co. had promoted the Woodford fund extensively in-spite of its underperformance, the Co. finally removed the fund from their recommendation list on Monday. Towards the top of the Stoxx 600 rests Telecom Italia (+3.3%) after a filing showed the Co’s CFO purchased 150k ordinary shares. Separately, much of the sessions positive stock activity has been driven by broker moves with the likes of Lagadere (+2.2%), Royal Mail (+3.3%), BMW (+1.9%) and Volkswagen (+2.2%) supported by broker moves.

Top European News

U.K. Construction Declines at Sharpest Pace in More Than a Year

ECB Pressured as Euro-Area Inflation Slows More Than Forecast

Billionaire-Backed Coloplast Said to Mull Urology Asset Sale

European Tech Stocks Plunge as U.S. Antitrust Sell-Off Spreads

In FX, the Dollar is trying to recover after another bout of post-Bullard selling pressure pushed the DXY through 97.000, albeit marginally and briefly, with the index back above the big figure and now probing fresh highs within a 97.265-96.987 range as certain G10 counterparts succumb to independent bearish impulses. However, Buck bulls and bears will now be focusing on a raft of Fed speakers to see if other members turn more dovish, and in particular Chair Powell.

AUD/EUR – Both holding up relatively well in the face of seemingly negative factors as RBA Governor Lowe flags further policy easing and a potentially lower than previously forecast OCR by the end of 2019 (was 1% vs the current 1.25% after last night’s 25 bp cut), while Eurozone inflation missed already considerably softer consensus forecasts. Aud/Usd remains firmly above 0.6950 around 0.6975 between 0.6955-93 trading parameters, and Eur/Usd is pivoting 1.1250 where the top of a band of option expiries reside (1 bn from 1.1235), but capped at the 100 DMA (1.1278).

GBP/CAD/JPY – All a fraction firmer against the Greenback, as Cable straddles 1.2650 and shrugs off another poor UK PMI, but the Pound underperforms vs the Euro on political/Brexit grounds (cross hovering just below 0.8900). Meanwhile, the Loonie is also displaying a degree of resilience in the face of weak crude prices and testing offers/resistance ahead of 1.3400 in a 1.3450-20 band and the Yen extended safe-haven gains through 108.00 to 107.85 before losing some momentum.

CHF/NZD – The major ‘laggards’ with the Franc stalling ahead of 0.9900 and Kiwi also finding it tough to breach a round number at 0.6600 vs its US rival as the Aud/Nzd cross rebounds from pre-RBA levels amidst general Aussie short covering and profit taking.

EM – Contrasting fortunes for the Lira and Rand, as Usd/Try retreats further from 6.0000 towards 5.8100 in spite of more talk from Turkish President Erdogan about the merits of Russia’s S-400 system over the US F-35 alternative that could trigger sanctions. However, Usd/Zar has rallied over 1% to just shy of 14.6500 in wake of significantly weaker than expected SA GDP data.

In FX, the energy market continues to be pressured as the ongoing trade concerns dampens global demand output, with WTI (-0.6%) and Brent (-0.6%) on the backfoot in early European trade following on from a lacklustre Asia-Pac session. News-flow this morning has largely been from the OPEC front in which a letter showed that Iran opposes delaying the OPEC meeting to July, whilst Algeria and Kazakhstan have also told OPEC that the early July dates are unsuitable. This comes amid split views as to whether the OPEC/OPEC+ meeting should be at the end of June or in early July (touted dates July 3rd/4th), which Russia is in favour for. Furthermore, sources stated that Russian production this month fell to 10.87mln, down from the prior month’s 11.11mln BPD which was reported via the Energy Ministry. Finally, traders will be eyeing tonight’s API data for any signs of a short-term catalyst, with the street looking for headline inventories to draw by around 1.8mln BPD. Elsewhere, gold (Unch) is choppy and largely unchanged intraday as the yellow metal gave up its gains as the Buck recovered. Meanwhile, copper is little changed as the weaker Dollar countered the soured risk sentiment. Finally, Zinc prices dropped to six-month lows overnight amid a deterioration of the global outlook, with the recent China PMIs pointing to growth of just 4.5%-5%, according to CapEco.

US Event Calendar

10am: Factory Orders, est. -0.95%, prior 1.9%; Factory Orders Ex Trans, prior 0.8%

10am: Cap Goods Orders Nondef Ex Air, prior -0.9%; Cap Goods Ship Nondef Ex Air, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

It looked like we were going to get an up day to start the week yesterday but the rally stalled in the US session as large-cap names dragged down the major indices. The S&P 500 ended -0.29%, despite the fact that 72% of companies in the index advanced on the day, only the eighth day this year where the index ended lower despite the majority of names rallying. The -7.51% and -6.11% moves for Facebook and Alphabet outweighed their smaller peers (a mere $85bn of lost market cap between the two), as the Federal Trade Commission and Justice Department reportedly opened investigations into the two companies respectively. The NASDAQ and NYFANG indexes accordingly fell -1.61% and -3.54% to their lowest levels since February and January, respectively, though the Philly semiconductor index outperformed tech peers by advancing +0.33%.

Meanwhile, in rates, treasuries continued their seemingly relentless rally, boosted by softer data and Fedspeak which raised the expectations for near-term policy easing. Ten-year yields fell another -4.7bps (but up +3.4bps this morning) while 2-year yields dropped -8.0bps (up +5.9bps this morning), taking their two-session move to -22.1bps and their 5-day move to -32.4bps. Both are the sharpest such drops since 2008. Futures markets last night priced a fairly startling 68bps of cuts this year. The front-end rally also continued to support the yield curve, with the 2y10y curve steepening +3.4bps to 23.4bps (+21.3bps this morning) – so that’s one silver lining to this whole episode. In Europe, Bunds did hit an intraday low of -0.221% before ending at 0.201% while the euro was a little bit stronger at $1.1242. Elsewhere HY credit spreads were +12bps wider in the US while oil prices fell -1.21%.

The data was the main talking point yesterday following the final PMI revisions in Europe and then the ISM manufacturing in the US. We’ll touch on the details further down but in short there wasn’t a great deal of change in Europe but in the US we saw a 31-month low for the ISM which was slightly tempered by better under-the-hood component details. That in itself causes some problems for markets though as it creates a bit more of a headache for the Fed as they battle with increasingly aggressive market pricing which has completely shifted towards more than two rate cuts this year and almost four over the next 12 months.

Turning to yesterday’s Fedspeak, the highlight was a series of comments from St. Louis Fed President Bullard, who is a voter this year, who said that “a downward policy adjustment may be warranted soon.” That’s the first time this year that an official has directly called for a rate cut. Bullard noted that “the direct effects of trade restrictions on the US economy are relatively small, but the effects through global financial markets may be larger.” He also conspicuously used the word “now” with regards to policy easing, which raises the odds that he votes for a rate cut as soon as this month’s meeting. Separately, Richmond Fed President Barkin also referenced tariff uncertainty as a potential headwind, though he stopped short of talking about interest rate cuts.

Overnight, the US Secretary of State Mike Pompeo condemned China’s human rights record as we hit the 30th anniversary of the Tiananmen Square incident. He said “We urge the Chinese government to make a full public accounting of those killed or missing to give comfort to the many victims of this dark chapter of history,” in a statement issued at 12.01am Beijing time. Elsewhere, negative rhetoric around the US-China trade war continued with the US Treasury Department and the Trade Representative office saying that its ‘disappointed’ that China is misrepresenting trade talks while saying that the US positions in negotiations have been ‘consistent’ while China ‘back-pedaled’. The joint statement also added that the Chinese have used the ‘White Paper’ and recent public statements to “pursue a blame game misrepresenting the nature and history of trade negotiations between the two countries.” Meanwhile, Bloomberg reported (citing sources) that the Congressional Republicans, worried about the possible economic fallout from President Trump’s plan to impose a tariff on Mexico, are considering whether to revive a resolution of disapproval over the national emergency declaration that underpins Trump’s justification for the tariffs. The action would also stop the president from spending billions on a border wall without congressional approval.

This morning in Asia markets are largely heading lower with the Shanghai Comp (-0.84%) and Hang Seng (-0.33%) trading down while the Nikkei (-0.01%) and Kospi (+0.02%) are trading flattish after erasing earlier losses. Elsewhere, futures on the S&P 500 are up +0.14% though. WTI oil prices are down -0.17% this morning, bringing the four day decline to -10.11%, despite Saudi Energy Minister Khalid Al-Falih saying yesterday that he was committed to doing whatever it takes to stabilize markets.

In other news, President Trump yesterday called on the UK to throw off the “shackles” of European Union membership and strike a free-trade deal with the US. Trump tweeted, “Big Trade Deal is possible once UK gets rid of the shackles,” and “Already starting to talk!” Elsewhere, French President Emmanuel Macron reinforced his hardline stance on Brexit, saying Brexit must happen at the end of October and there should be no more extensions. Meanwhile, the UK’s former foreign secretary Boris Johnson launched his leadership campaign yesterday, saying the U.K. must leave the bloc in October, with or without a deal.

Back to the details of yesterday’s data, where the May ISM manufacturing in the US hit a new 31-month low of 52.1 (vs. 53.0 expected) – down -0.7pts from April. The good news was that both the new orders (+1.0pt to 52.7) and employment (+1.3pts to 53.7) components improved. Even the prices paid component bounced +3.2pts to 53.2. How much of the latest tariff escalation is in the data however remains to be seen. In the meantime a quick refresh of our equities versus ISM regression shows that the US equities are around 5% ‘cheap’ given that markets have fallen more than the data has. Indeed the equity market-implied ISM is actually now below 50 at 49.8. However for this to be a buying opportunity you have to believe the ISM will settle at these levels over the summer in the face of rising trade tensions. That data followed a small -0.1pt downward revision to the rival Markit PMI release to 50.5 while elsewhere construction spending was flat, versus expectations for a slight rise, though the prior month was revised higher leaving the overall trend roughly neutral.

In Europe, the final manufacturing PMI for the Euro Area was unrevised at 47.7 which means it is -0.2pts down from April and 0.2pts higher than the March lows. Our economists did highlight that there were some green shoots of optimism in the details with the new orders subindex up more than +2pts in the past two months (albeit still at a lowly 46.6) while there were similar moves in both output and the new export order series.They also noted that new orders-to-inventories difference, which tends to lead the headline and output indices, is back to August/September 2018 levels – still negative but signalling that we are perhaps past the trough in the manufacturing PMI. The question though is whether a genuine recovery of the manufacturing sector can be expected especially now the trade war has been reignited. Meanwhile, at a country level Germany and France were unrevised at 44.3 and 50.6 respectively while a big drop for Spain (-1.7pts to 50.1) was partly offset by a +0.6pt advance for Italy to 49.7. Greece (-2.2pts to 54.2) was another country that deteriorated however it is only behind Hungary (57.9) at the top of the EU ranks now. Our regression of European equities versus PMIs now has the STOXX fairly valued but equity markets in France, Italy and Spain all slightly cheap. Only Germany appears expensive on this measure due to how low the German PMI is relative to history. However these are a very broad guide and work best for general market valuations especially when there are big outliers. It’s hard to say there are at the moment. On our measure most global equity markets price in high 40s on the manufacturing PMIs/ISM, and in the US we are still above this and therefore cheap, whilst in Europe we are generally at that level or a bit lower.

Here in the UK, the latest PMI reading of 49.4 was a little worrying, printing -2.6pts lower than expectations and also -3.7pts below the April level. It’s worth flagging that rising stockpiles had been behind some of the recent manufacturing resilience in the UK so it isn’t a huge surprise to now see this filter out and therefore the UK start to catch down to the rest of Europe. It’s worth noting also that the last time the UK PMI went sub-50 was in 2016 and when the BoE last cut rates. One ray of positivity came from Sweden’s manufacturing PMI which came in +2.7pts better than expected at 53.1. Sweden, as a highly cyclical economy, has tended to lead the rest of Europe, so its bounce could be cause for optimism moving forward.

In other news, our economists in Germany published their views on the surprising weekend resignation of SPD party leader and chief whip Andrea Nahles over the weekend. They note that the implications are clearly negative, and go as far as saying that it is hard to see how the Groko might still be in place at the end of the year given the current dynamics in the SPD. They highlight that if the SPD pull out of the coalition, then snap elections are most likely as the Greens rejected joining the government on the basis of the 2017 election results. The Greens currently score around 20% in the polls giving them a much stronger weight in a possible future conservative-green government. See more in our colleagues’ report here .

To the day ahead now, which this morning includes the advanced May CPI report for the Euro Area where the consensus expects a +0.9% yoy core reading compared to +1.3% in April. We’ll also receive the April unemployment rate while data in the US this afternoon includes final durable and capital goods orders revisions for April, as well as April factory orders data. Away from that the Fed’s Williams is due to speak just after lunch before the two-day Fed conference gets underway including opening remarks from Powell at 2.55 pm BST.

via ZeroHedge News http://bit.ly/314CAyp Tyler Durden