In an interview with the South China Morning Post earlier this week, former White House Chief Strategist Steve Bannon described himself as a “super hawk” when it comes to China – that was right after he advocated closing US financial markets to Chinese companies and claimed that destroying Huawei is more important than striking a trade deal.

Bannon’s caustic rhetoric about China is nothing new, though he’s definitely made more media appearances to discuss the subject in the past few weeks. Though Bannon has staked out a position that’s far more aggressive than President Trump’s baseline (in its dealings with Beijing, the White House has expertly run the old good-cop bad-cop routine), his warnings about China’s plans to dominate the US have attracted some unlikely sympathizers (Twitter erupted after the NYT’s Tom Friedman said he “really agrees with much of what Steve said” after the two men recently appeared on CNBC together.

And on Thursday, Beijing finally responded to Bannon, with Global Times editor Hu Xijin, whose tweets have occasionally moved markets since the trade-deal talks collapses, said even the most radical Chinese leaders wouldn’t call for driving Apple or McDonald’s out of the Chinese market.

Then, he borrowed a line from American leftists, and accused Bannon of being a fascist: “Political elites like Bannon are turning the US into an economic fascist country.”

Bannon publicly advocated driving Huawei out of Western markets & shutting it down. In China, even the most radical opinion leader won’ t call for driving Apple or McDonald’s out of Chinese market. Political elites like Bannon are turning the US into an economic fascist country. pic.twitter.com/wuy5os9zRq

Bannon told the SCMP that Huawei is a security threat not just to the US but to its allies, and that “we are going to shut it down.” He has also scolded bankers for acting like money men for the Communist Party, and selling out their country in the process.

via ZeroHedge News http://bit.ly/2HwbRmk Tyler Durden

It looks like it’ll be another stormy day in Longsville.

The Tesla “pain trade” continues, as yet another notable Tesla bull is capitulating. Following in the footsteps of Wedbush, Morgan Stanley and Citibank, all of whom offered dismal outlooks and price targets for Tesla in the past few days, Gene Munster of Loup Ventures, who has been defending the company non-stop over the last several years, has now issued a stern warning that he believes Tesla will miss its 2019 delivery target range, according to Bloomberg.

Munster cited shrinking sales in China and the ongoing trade war as the reason for his increasingly bearish commentary.

Munster cut his estimate for Tesla’s full year global car sales by about 10%, to 310,000 vehicles, versus the 360,000 vehicle target that the company put out back in March. Tesla shares are again lower in the pre-market session, trading below $185 for the first time since 2016, and poised to post their seventh straight day of losses. Tesla is down 27% over the last month and anyone who bought stock in the company’s recent equity offering is now suffering major losses.

Munster’s note read:

“We are lowering our numbers as a precautionary measure related to two unknowns, including China’s probable imposition of tariffs on Tesla car imports as well as other impediments such as new regulations on sales or a potential consumer boycott of U.S. goods.”

Loup’s pessimism on the import fees is a “minority view,” he said, that discounts most investors’ expectations that Tesla will remain exempt because of its investment in a Chinese battery factory, according to Munster. Munster’s comments follow Morgan Stanley’s investor call yesterday, where another former bull – Adam Jonas – warned that the next major event for Tesla is a debt restructuring or bankruptcy: “Tesla’s is not seen as a growth story, it’s seen as a distressed credit and restructuring story.”

Regardless, Munster still thinks that Tesla is going to survive, as the growing to EV market will continue to act as a tailwind. He says that the company’s recent $2.4 billion financing should give them a two-year cash cushion, as long as they can exceed 300,000 vehicles per year through 2020.

Which leads to a simple question: what if they don’t?

via ZeroHedge News http://bit.ly/2HRUED1 Tyler Durden

Yesterday’s modest selloff has become an all-out rout, dragging world stocks lower with US equity futures tumbling and global equity markets a “sea of red” as fears grow that the China-U.S. trade conflict is fast turning into a technology cold war and as Wall Street’s denial is finally shifting to acceptance that a lengthy, all-out trade war is now inevitable, and the only way out and for someone to concede is for markets to plunge. Sure enough, that’s what they are doing this morning.

“It’s tin hats on and battening down the hatches for a fair bit of volatility for the next few months,” said Tony Cousins, Chief Executive of Pyrford International, the global equities arm of BMO Global Asset Management. “We are as defensively positioned as we could be,” he said, adding it was impossible to predict what steps Trump was likely to take next in the trade war with China.

Analysts at Nomura warned in a note, “Without a clear way forward during an intensifying 2020 U.S. presidential election, we see a rising risk that tariffs will remain in effect through end 2020.”

While there were no major escalations overnight, China’s Commerce Ministry warned on Thursday that the United States needs to correct its wrong actions if it wants to continue negotiations with China, adding that talks should be based on mutual respect. The United States has escalated trade frictions greatly, and increased chances of a global economic recession, spokesman Gao Feng said at a weekly briefing, adding that Beijing will take necessary steps to safeguard Chinese firms’ interests.

Clearly this is merely the latest verbal escalation in what is now an out of control global trade war, however, the bigger reason for the accelerating rout is that as Bloomberg notes this morning, after months of predicting a trade deal between the world’s two largest economies, “economists at some of the biggest financial institutions are growing increasingly pessimistic.” Goldman Sachs, Nomura and JPMorgan Chase “are among those that have rewritten their forecasts as U.S. President Donald Trump threatens to impose a 25% tariffs on around $300 billion of additional Chinese imports.”

It could be even worse: one expert predicted tensions could endure until 2035. “We don’t think that there is an overnight solution,” said James Johnstone, co-head of emerging and frontier markets at RWC Partners LLC. “The accommodation of China as a rising power is something that the Americans and the West have been contemplating for a long time. This will be a 20-30 year accommodation.”

Asian stocks dropped for a third day, caving to a four-month low led by technology and communications firms, as the rhetoric between Beijing and Washington remained fierce while Europe’s bourses also fell as Brexit worries and gloomy data from Germany and the euro zone added to the nerves.

Most Asian markets were down, with Hong Kong and Taiwan leading declines. MSCI’s broadest index of Asia-Pacific shares outside Japan touched its lowest in four months. The Topix gauge fell 0.4%, with SoftBank Group Corp. and Sony Corp. among the biggest drags. The Shanghai Composite Index retreated 1.4% dropping near their lowest since February, driven by Ping An Insurance Group and Kweichow Moutai. The Indian market bucked the global picture after Prime Minister Narendra Modi’s party scored a historic victory in the nation’s general election with official data showing Modi’s Bharatiya Janata Party (BJP) ahead in 292 of the 542 seats available.

In Europe, trade fear was also rampant, with the Stoxx Europe 600 falling as much as 1%, hitting its lowest level since May 15, amid mounting worries over U.S.-China trade tensions. The Stoxx autos sector was hit the hardest, falling 3.1% to lowest since February; energy sector down 1.7%, industrial sector down 1.6%, tech sector down 1.6%. More ominously, the upward channel that was created early this year, has been breached.

European equities will likely fall further as today’s dismal batch of euro-area economic data weighs on already low sentiment and future profits, especially for all-important cyclical sectors. The biggest surprise was German Manufacturing PMI which slumped once again, dropping from 44.4 to 44.3, below the 44.8 expected. Separately, IHS Markit said the euro-zone business situation could “deteriorate further in coming months.” Germany also reported the latest dire IFO Busienss Climate report, which slumped to a 4 year low of 97.9, down from 99.2 in April, mainly driven by the assessment of current business conditions in the trade, services and, to some extent, manufacturing sectors. By contrast, the assessment of future economic conditions remained unchanged.

U.S. stock futures also pointed to a weak start with the S&P 500 e-minis faltering 0.5%, after the Communist Party’s flagship People’s Daily newspaper published two commentaries assailing American moves to curb Chinese companies, warning the “world won’t tolerate the US breaking rules” even if so far more nations are joining the US in its “campaign” against Huawei so far, including Japan, Australia, the UK, New Zealand, and South Korea likely to fold next (See “World Trade War I: US Asks South Korea To Join Anti-Huawei Campaign“).

In rates, bonds rallied amid a cocktail of risk-off factors, including pressure on U.K. PM Theresa May to resign, weak euro-area data and continuing concern over U.S.-China trade. Portuguese 10y yield drops below 1% for the first time on record, following Spain, while Italian bonds drop amid equity weakness. Over in the US, 30Y Treasury yields dropped to lowest level since January 2018, with the rally starting during Asia hours after China published commentary saying the U.S. wants to start a “technology cold war.” As noted above, German and euro-area PMIs for manufacturing and services miss forecasts, pushing bunds higher and bull-flattening core European yield curves; France underperforms as PMIs beat expectations.

In currencies, trade friction saw the safe haven yen in demand again as the dollar dipped to 110.11 yen and away from the week’s top of 110.67. The dollar was close to session highs, up on the euro at $1.1130 and touched a 1-month high on a basket of currencies at 98.235. Minutes of the U.S. Federal Reserve’s last meeting out on Wednesday underlined its readiness to be patient on policy “for some time” given the uncertain global outlook. The chance of a rate cut seemed to diminish as many Fed policy makers saw recent weakness in inflation as “transitory”, though the latest escalation in the trade war means markets are still wagering on an eventual easing.

Meanwhile, the sterling slide continued as it hit a 4-1/2-month low of $1.2603 weakening against the euro for a record 14th day as the prospect of Prime Minister Theresa May being forced from power brought yet more uncertainty over the U.K.’s Brexit strategy.

Theresa May came under intense pressure after her latest Brexit gambit backfired and fueled calls for her to quit, while prominent Brexit supporter Andrea Leadsom resigned from the government on Wednesday and with British media reporting May could announce her departure date as early as Friday the bets on a more hard Brexit replacement are rising.

Elsewhere, the Aussie declined and China’s yuan dipped even after the People’s Bank of China set its daily fixing at a stronger-than-expected level for a fourth straight day.

In commodity markets, spot gold was a bit higher at $1,274.73 per ounce. Oil prices added to losses suffered overnight after an unexpected build in U.S. crude inventories compounded investor worries about demand. U.S. crude was last down 48 cents at $60.94 a barrel, while Brent crude futures lost 57 cents to $70.41.

Looking at today’s calendar, expected data include jobless claims, PMIs, and new home sales. Medtronic, Royal Bank of Canada, and Intuit are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 0.8% to 2,833.50

STOXX Europe 600 down 1.3% to 374.40

MXAP down 0.7% to 152.74

MXAPJ down 0.9% to 499.21

Nikkei down 0.6% to 21,151.14

Topix down 0.4% to 1,540.58

Hang Seng Index down 1.6% to 27,267.13

Shanghai Composite down 1.4% to 2,852.52

Sensex unchanged at 39,111.07

Australia S&P/ASX 200 down 0.3% to 6,491.79

Kospi down 0.3% to 2,059.59

German 10Y yield fell 2.4 bps to -0.11%

Euro down 0.2% to $1.1132

Italian 10Y yield fell 1.1 bps to 2.26%

Spanish 10Y yield fell 1.8 bps to 0.85%

Brent futures down 1.4% to $70.02/bbl

Gold spot up 0.2% to $1,275.59

U.S. Dollar Index up 0.2% to 98.26

Top Overnight News

The U.S. unilaterally escalated trade tensions and if it wants talks to resume, it needs to correct what it did and show sincerity, according to China’s Ministry of Commerce. The comments are the latest sign that China has no intention of making concessions

U.S. naval ships transited through the Taiwan Strait as faltering trade talks and the Trump administration’s move to restrict Chinese tech companies’ access to the American market fuels tensions.

May’s premiership is hanging by a thread as a high-profile U.K. Cabinet minister quit and a growing revolt over Brexit looked set to force her from power

Euro-area private-sector output remained subdued in May. A Purchasing Managers’ Index inched up to 51.6 from 51.5 in April. The bloc is currently headed for “lackluster” growth of around 0.2% in 2Q, according to IHS Markit

German business confidence in May was the weakest in more than four years as global trade tensions weighed heavily on the economy. The drop in the Ifo index was bigger than forecast and takes the closely-watched gauge to its lowest since November 2014.

Investors see a U.S. rate cut by the end of the year, but minutes of the Fed’s last policy meeting released Wednesday showed officials expect patience on rates to be appropriate for “some time”

U.K. PM May’s premiership is hanging by a thread as a high-profile Cabinet minister quit and a growing revolt over Brexit looked set to force the British leader from power

After months of predicting a trade deal between the world’s two largest economies, economists at some of the biggest financial institutions including Goldman Sachs Group Inc. are growing increasingly pessimistic

Early counting in the world’s biggest election show Indian Prime Minister Narendra Modi’s ruling coalition is heading for another five-year term in office

Oil extended losses after a surprise jump in American crude inventories alleviated concerns over a supply crunch, while the demand outlook remained bleak as there was no let up in U.S.- China tensions

Asian stock indices were mostly lower amid spillover selling from Wall St as US-China trade uncertainty remained at the forefront of market focus with the US mulling restrictions on several Chinese firms and as comments from China suggested and unwillingness to back down, as well as the potential for a prolonged trade dispute. ASX 200 (-0.3%) and Nikkei 225 (-0.6%) were negative with Australia dragged by weakness in its largest weighted financials sector and with energy names pressured after a more than 3% drop in WTI, while risk appetite in Tokyo was suppressed by a stronger currency and weak Nikkei Manufacturing PMI data which slipped into contraction territory. Hang Seng (-1.6%) and Shanghai Comp. (-1.4%) conformed to the negative tone due to the trade tensions and with some sabre-rattling from China in which Foreign Minister Wang Yi labelled US pressure on Huawei as pure economic bullying and warned they will fight to the end if the US uses extreme pressures, while China’s top four official Wang Yang also suggested businesses should be prepared for a lengthy trade war. Indian markets bucked the trend and gained over 2% to record highs as the early election results showed PM Modi’s BJP and National Democratic Alliance were ahead in world’s largest democratic election with the BJP on course to achieve a majority on its own if the early results hold up. Finally, 10yr JGBs were higher as they tracked the upside in T-notes and with price action underpinned by safe-haven demand amid the mostly negative risk sentiment in the region.

Top Asian News

Huawei’s Own Operating System Could Be Ready This Year: CNBC

Modi’s Lead Signals Single-Party Majority in India Vote Count

Thomas Cook Tumbles on Downgrade Showing Default Is Possible

Japanese Shop for Bonds Overseas as Trade War Spurs Gains in Yen

Major European stocks are sliding [Eurostoxx 50 -1.7%] following on from a weak Asia handover wherein mainland China shed over 1.3% and Hang Seng declined in excess of 1.5%, as trade woes remain a grey cloud above markets. Equities in Europe saw a more pronounced decline amidst the release of disappointing EZ Flash PMIs and a downbeat Ifo Survey which was followed by Ifo economists stating that the export dynamic is very weak, business uncertainty remains very high and a recovery in the auto sector is not seen for the time-being. Heavy, broad-based losses are seen across the sectors; albeit healthcare, utilities and consumer staples to a lesser extent given their defensive properties. The IT sector (-2.3%) bears the brunt of a barrage of companies halting shipments to Huawei given the quarrel with the US over security, with Japanese tech giants Panasonic and Toshiba the most recent, albeit the latter announced that it has resumed shipments to the company. Nevertheless, STMicroelectronics (-4.2%), Infineon (-2.6%), Micro focus (-1.2%), SAP (-2.2%), ASML (-1.7%) shares are all pressured. In terms of individual movers, Deutsche Bank (-2.2%) shares found little reprieve as its AGM began following reports that a New York district judge has rejected US President Trump’s efforts to prevent Deutsche Bank and Capital One from complying with a congressional subpoena for the President’s financial records. Co. spokesperson said the bank remains committed to providing appropriate information regarding the investigation. At the AGM, the Co. noted that they are prepared to make tough cutbacks to their investment banking sector, and on DWS (-0.8%) they stated that they remain open to other strategic options. Finally, shares in Thomas Cook (-6.8%) plummeted after Fitch downgraded the Co.’s Long-Term Issuer Default rating to “CCC+” from “B”, outlook negative.

Top European News

French Companies See Fastest Growth in Six Months as Orders Rise

Universal Is Said to Eye Industry Bidder as Buyout Firms Balk

German Business Confidence Weakest Since 2014 on Gloomy Backdrop

Europe’s Biggest IPO of 2019 Gets Thumbs Up From Barclays, HSBC

JPY/CHF/SEK/NOK – The major outperformers as the Yen and Franc benefit from more safe-haven positioning, while the Scandi Crowns derive protection from broad risk-off sentiment with the aid of supportive and upbeat data to justify relatively hawkish Riksbank and Norges Bank policy stances. Usd/Jpy is eyeing bids ahead of 110.00 that are said to be fairly thick and layered, while Usd/Chf is pivoting 1.0100 and the Eur/Chf cross 1.1250. Elsewhere, Eur/Sek has backed off further from recent decade highs (10.8500) towards 10.7300 and Eur/Nok is testing 9.7500 in wake of better than expected jobless rates in April and March respectively (and with Swedish unemployment falling sharply in particular).

DXY – The Dollar is firmer vs the rest of the G10 after FOMC minutes underlining a patient and perhaps longer pause in normalisation than previously anticipated or flagged as it transpires that the transitory assessment on soft inflation is shared by other members aside from Powell with only a minority worried that it might unhinge expectations and warrant a rate cut. On the flip-side, there is a consensus that even if the economy develops in line with expectations it might be prudent to hold off from further tightening given ongoing risks, like trade. Hence, the index is forming a firmer base above 98.000 and inching closer to ytd peaks of 98.346 at 98.274, thus far.

CAD/GBP/EUR/AUD/NZD – All on the backfoot relative to the Greenback, as noted above, with the Loonie unwinding more of its brief post-Canadian retail sales gains and back below 1.3450 amidst a deeper retracement in oil prices and the ongoing US-China trade spat. Meanwhile, the Pound also has the Brexit situation to contend with and a near state of political limbo given that UK PM May is still widely expected to bow to increasing pressure if not this week then sometime after the WAB returns to Parliament and rejected yet again. On that note, the HoC leader Leadsom has now resigned in protest to lift the number of MPs that have departed to 36, and with the EU elections underway Cable continues to decline, just holding above 1.2600 vs Wednesday’s circa 1.2625 base. Similarly, the single currency has slipped under yesterday’s trough and through decent option expiry interest at 1.1150 (1.4 bn) to test support ahead of the 2019 base and more expiries at the 1.1100 strike (1 bn), and more downbeat Eurozone surveys have not helped as all bar the French PMIs missed consensus and Germany’s Ifo readings were mostly downbeat. Looking down under, the Aussie and Kiwi remain rooted near or at new lows for the year, as Aud/Usd is capped ahead of 0.6900 and Nzd/Usd slips further from 0.6500 awaiting NZ trade data.

EM – The Lira has been hit by more US-Turkey sanction jitters and dire sentiment news, this time in the form of a sub-100 manufacturing index, and Usd/Try topped 6.1500 in response before paring some gains. However, the Rand is also under pressure after soft SA data that could tip the SARB towards more dovish guidance later, as Usd/Zar rebounds to 14.4900.

In commodities, the energy complex continues its decline in the aftermath of this week’s surprise builds in US crude stocks coupled with a bleak demand outlook amid the ongoing US-China trade spat. WTI (-1.7%) futures reside just below the 60.50/bbl (having already fallen below its 50 DMA at 62.13/bbl) ahead of its 200 DMA at 60.24/bbl. Meanwhile, its Brent (-1.8%) counterpart recently slipped under its 50 DMA at 70.44/bbl, while gains are capped amid a rising Buck alongside a downbeat risk sentiment and bearish supply data as mentioned above. Elsewhere, gold (+0.2%) edges higher despite a firmer Dollar as investors seek the safe-heaven asset amid trade developments, dismal EZ flash PMIs and German confidence hitting the lowest level in over four years. Meanwhile, the risk-gauge copper (-0.4%) extends its losses with the red metal losing more ground below the 2.70/lb level ahead of its 200 DMA at 2.61/lb. Finally, ING highlights that LME nickel spreads have been tightening recently with the June/July spread trading around USD 32/t vs. USD 50/t last week. This is due to declining inventories which have fallen over 42k tonnes thus far this year, leaving inventories around the lowest levels since 2013.

US Event Calendar

8:30am: Initial Jobless Claims, est. 215,000, prior 212,000; Continuing Claims, est. 1.67m, prior 1.66m

9:45am: Markit US Manufacturing PMI, est. 52.7, prior 52.6; Services PMI, est. 53.5, prior 53

10am: New Home Sales, est. 675,000, prior 692,000; New Home Sales MoM, est. -2.46%, prior 4.5%

11am: Kansas City Fed Manf. Activity, est. 6, prior 5

DB’s Jim Reid concludes the overnight wrap

If I could give advice to readers getting a new kitchen at any point in their lives it would be to read the instructions on the work surface you’ve bought. We didn’t and I left a cast iron pan lid to dry by the side of the sink. When moving it a couple of days ago we discovered a nice brown ring in the new work surface. I sighed, got a cloth and wiped it down. Not one bit of the stain disappeared. I rubbed harder and it made no difference. I then proceeded to put all sorts of surface cleaner on it and again nothing changed. I then got the notes left by the kitchen provider and point 1 said “don’t leave wet cast iron pans on your quartz work surface as it will leave a permanent stain”. That’s pretty much the main thing you can’t do and I did it. Anyway yesterday we got the quote to have it professionally sanded down which apparently is the only way to get rid of it. I nearly fell over backwards in amazement. I’m wondering whether we can make a feature of the brown ring instead!!! Double Sigh!!

One wonders what stains will be left after the next four days of EU Parliamentary elections here in Europe. They used to be fairly dull affairs but with the rise of anti-EU and populist party support, and the bizarre situation where the UK is taking part but likely to leave the Union this year, the next few days should be a fascinating political backdrop for a turbulent few years ahead for Europe. We also have the latest flash global PMIs today, which will be the first glance at the impact of the trade spat on global businesses. Overnight, Japan’s preliminary May manufacturing PMI slipped into contractionary territory at 49.6 (vs. 50.2 last month). Joe Hayes, economist at IHS Markit, said that “the re-escalation of US-China trade frictions has heightened concern among Japanese goods producers.”

The tone this morning in Asia is on the negative side with the Nikkei (-0.71%), Hang Seng (-1.30%), Shanghai Comp (-0.84%) and Kospi (-0.04%) all down. Chinese companies like Iflytek (-5.56%), Hikvision (-4.68%), Xiamen Meiya Pico Information Co. (-5.57%) and Zhejiang Dahua Technology Co Ltd (-2.98%) are all down as they are reported by Bloomberg to be among five firms that the US is considering blocking access to vital American technology. China’s onshore yuan is down -0.10% to 6.9135 while the Indian rupee is up +0.38% alongside Indian equity markets (c. +1%) as early trends in vote counting show that the Modi government is poised to retain power. Elsewhere, futures on the S&P 500 are down -0.37%.

Before we get onto other markets over the last 24 hours lets preview the European elections and the rest of the PMIs. As discussed the EP elections actually take place over the next four days, with each of the 28 countries voting on the day they normally hold national elections. The UK and the Netherlands will kick off proceedings today, but most of the big EU countries (including Germany, France, Italy, Spain and Poland) don’t vote until Sunday. In spite of some countries finishing before then, the votes won’t actually be counted until the polls right across Europe have closed, so Sunday night is when we can start to expect results, with the final outcome on Monday.

DB Research have published a number of previews on the elections, with Kevin Koerner and Barbara Boettcher releasing a five-part countdown, looking at the Brexit delay, the race for the Commission Presidency, the different Eurosceptic parties, what’s happening in Germany, and a final preview yesterday (links here , here , here , here and here ). Meanwhile, Clemente De Lucia and Mark Wall have published a note on the implications for the populist coalition in Italy and market sentiment (link here ).

An interesting (or worrying depending on your view) fact about the EP elections is that in every vote since they began in 1979, EU-wide turnout has fallen, from a high of 62% at the first set in 1979 to just 43% last time round in 2014. Rightly or wrongly, they’re simply not seen as anywhere near as important as national elections but for the EU to succeed it will be difficult if Eurosceptic politics dominate in Brussels. Indeed, populists are expected to perform strongly in the first EP election since the migrant crisis and Britain’s vote to leave the EU in 2016.

According to the polls, we can expect to see some pretty striking results across the continent, with Kevin and Barbara writing that Eurosceptic parties of both left and right could get more than 35% of the seats if the current polls are correct, while for the first time ever the two main centre-right and centre-left groupings are projected to not have a majority between them, although pro-European forces as a whole are expected to. Here in the UK, Nigel Farage’s Brexit Party, which explicitly backs a no-deal Brexit, is polling in first place, while polls have put the governing Conservatives as low as fifth, something for which there is quite literally no precedent. The Brexit party, having only been formed a few months ago, are now poised to come first in a national election. Has a political party ever gone from non-existence to first place in a national poll so quickly?

In Italy, the right-wing Lega is expected to come first, with its leader Deputy Prime Minister Salvini having railed against EU deficit rules and clashed with other countries over taking in migrants. In France, President Macron’s party has been running neck-and-neck with Marine Le Pen’s Rassemblement National, with the final polls putting Le Pen’s party marginally ahead. This will be one to watch when results come through Sunday night/ Monday morning.

Staying with Europe, we have a busy day ahead, which includes the important flash May PMIs this morning. While the data will regardless be followed closely, the complication is that we won’t know the exact survey period until the data is out. So how much of the trade escalation period that gets captured is unknown and it may well differ for each country. This therefore adds a relatively high degree of uncertainty to the data – and makes the revisions in the final readings very important. Nevertheless, the consensus is expected to nudge up modestly for the Euro Area by 0.2pts to 51.7 with equal moves higher for the manufacturing (to 48.1) and services (to 53.0) sectors. Germany’s manufacturing reading will also be under the spotlight after only improving 0.3pts last month to 44.4 – only the second monthly improvement over the last 16 months. The consensus is for it to improve to 44.8 today. It’s worth noting that we’ll also get the May IFO survey in Germany today, which will also be closely watched for the trade escalation impact.

Over in markets, the tug-of-war around trade headlines continued for most of yesterday with risk assets on the back foot once again. The news about the US government considering banning China’s video-surveillance firms now a number of global phone companies announcing that they are no longer selling Huawei handsets was the latest twist in the saga. There was at least one glimmer of hope, however, as US Treasury Secretary Mnuchin suggested that Mr. Trump and Mr. Xi would likely meet at the end of June. He also kept the door open for exemptions to the latest round of tariffs. There was also speculation, fueled by yet another tweet from Xu Xijin, that China may consider blocking exports of rare earths to the US. These are essential for high-tech manufacturing, though the impact of an export ban would probably be so disruptive for both parties that it is probably not imminent. DB’S Michael Hsueh wrote about the subject here , where he explains the issue, the history, and the likely implications of any new limitations. Overall the S&P 500, DOW and NASDAQ slipped -0.28%, -0.39% and -0.45%, respectively, while the beaten-up Philly semiconductor shed another -2.12% to take it’s MTD decline to -13.57%. Energy stocks lagged as well, falling -1.58% as WTI oil fell -2.70% after US inventories rose more than expected again last week. The 4.7 million barrel build was the fourth bigger-than-expected build over the last five weeks. Things were a bit steadier in Europe where the STOXX 600 edged down -0.10% and DAX -0.18%.

The bulk of those moves came prior to the FOMC’s meeting minutes last night which offered a few interesting new comments. None of the macro discussion was news, and it has already been overtaken by the trade war escalation over the last few weeks. But on policy, it was noteworthy that the minutes discussed the future composition of the Fed’s balance sheet. It said “all else equal, a move to (a) shorter maturity portfolio would put significant upward pressure on term premiums and imply that the path of the federal funds rate would need to be correspondingly lower to achieve the same macroeconomic outcomes.” Though there doesn’t seem to be a lot of urgency in announcing any new plans, there is scope for the Fed to shorten the maturity profile of its holdings if it wanted to, since they are currently around 98 months versus the 69 months of the overall universe of outstanding treasury debt. Treasury yields were already lower before the minutes and ended down -4.1bpts, while the dollar traded flat. Curves were broadly flatter, with the 2y10y spread -1.2bps lower at 15.5bps, while EM FX finished marginally lower. Speaking of EM, it’s worth noting that Turkish assets were hit hard again yesterday. The BIST 100 index tumbled -1.92% and officially entered a bear market having dropped over 20% from the March highs, while the Turkish Lira sold off -0.78% (a further -0.40% this morning), taking it past 6.10 again. The Turkish lira is now down -13.63% YtD and is the second worst-performing currency behind the Argentine Peso, which is down -16.07% YtD.

In other news, the mood music over at Downing Street continues to lean towards PM Theresa May’s resignation sooner rather than later. That was certainly what all the headlines suggested yesterday and at one stage it even looked like she may resign as soon as last night. Various newsflow from journalists confirmed that there was pressure for the PM to pull the WAB in its current form. Theresa May will reportedly meet Graham Brady from the 1922 Committee on Friday, where he may push for her resignation. A possible catalyst to drive this timeline will be cabinet pressure, with Leader of the House Leadsom resigning last night. Sterling got hit another -0.35% yesterday, which means it has now dropped on eleven of the last thirteen sessions – for a cumulative decline of -3.88%. The Telegraph deputy political editor said overnight that the 1922 Executive now wants PM May to announce that she will step down as Conservative Party leader by June 10, at its Friday meeting. Sterling is trading down -0.14% this morning.

Those Brexit developments came as core CPI missed on the downside in April after staying put at +1.8% yoy versus expectations for a rise to +1.9%. Recreational and cultural items appeared to be to blame along with package holidays.

As for the Fedspeak, the minutes understandably overshadowed other remarks. NY Fed President Williams reiterated his positive view of the economy, saying that risks from abroad have receded. Nevertheless, he also said that he doesn’t see a need “to move interest rates one way or the other.” Boston President Rosengren said that the trade war “is one of the biggest risks,” while Dallas President Kaplan cited the yield curve as evidence that “expectations for future growth are sluggish.” He suggested that changes are needed to improve the outlook, which skirted close to but stopped short of arguing for a rate cut.

To the day ahead now, which this morning kicks off in Germany shortly after this hits your emails with the final Q1 GDP revisions. A reminder that the preliminary reading showed growth of +0.4% qoq. After that we get May confidence indicators in France before attention turns to those flash May PMIs. Not long after we then get the May IFO survey in Germany before focus turns to the US with claims, the flash PMIs, April new home sales and May Kansas Fed manufacturing survey all due. This evening we’re also due to hear from the Fed’s Kaplan, Daly, Bostic and Barkin when they speak on a panel, while over at the ECB we’ve got Guindos and Nowotny due. The ECB minutes from the meeting earlier this month are also due today. Of course, as mentioned at the top the EU Parliamentary elections also kick off today.

via ZeroHedge News http://bit.ly/2M0Ui1Z Tyler Durden

Instead of hanging on for what would be a fourth vote on the withdrawal agreement she negotiated with the European Union – an agreement that is widely despised in Parliament because of the possibility that the hated ‘Irish Backstop’ could trap the UK in the EU Customs Union indefinitely – Theresa May might instead step down, or set a date for her resignation, according to an FT report.

When the government published its itinerary for future business on Thursday, it left no time set aside for debating the “WAB” – that is, the withdrawal agreement bill – during the week of June 3. Though a senior Tory whip filling in for Andrea Leadsom (who resigned as Commons leader last night) insisted that the government still wanted to debate the bill, anonymous sources cited in the British press were skeptical.

Rumors that May had been preparing to resign on Wednesday night didn’t pan out, but many still expect May to either resign or decide on a firm departure date before the end of the week, as the backlash to the latest iteration of her withdrawal plan – which included a provision for a Parliamentary vote on a second referendum – intensifies. Graham Brady, the leader of the 1922 Committee of Tory backbenchers, reportedly told the prime minister that she would face another leadership challenge if she decides to move ahead with a vote on her withdrawal bill. Leadsom’s departure has also fostered rumors that more cabinet members could follow her lead and resign.

Should the Brexit Party garner a decisive plurality of the vote in the European Parliamentary elections on Thursday – as is widely expected – that would be yet another rebuke to the PM.

Amid all of the uncertainty, the pound weakened on Thursday for the 14th straight session as May’s refusal to go quietly creates more uncertainty surrounding the Brexit outlook.

Looking further down the road, May stepping aside could open the door to an early general election, which would up the chances of Brexit being cancelled or interminably delayed. The currency traded at roughly $1.2645 Thursday morning in New York, not far from its lows for the year.

via ZeroHedge News http://bit.ly/2M5BZJn Tyler Durden

As more companies scramble to comply with the White House executive order prohibiting telecommunications equipment deemed a national security risk – even as the administration extended Huawei a 90-day reprieve – Japan’s Toshiba said Thursday that it had suspended shipments of electronics to Huawei, according to the Nikkei Asian Review.

The suspension will allow Toshiba time to figure out whether any US-originated parts or technologies are being packaged into Toshiba products sold to Huawei. If it were to ship US-made components to Huawei in violation of the ban, Toshiba would risk drawing the ire of the White House.

Toshiba is at least the third major Japanese supplier to cut ties with Huawei, the other two being smartphone chip-maker ARM and Panasonic, which also supplies parts for Huawei phones. Japan’s enthusiastic support of the White House’s crackdown on Huawei shows that the world’s third-largest economy has picked a side in the battle between China and the US, potentially risking the trade war (and possibly even a hot war) across the East China Sea (and perhaps more riots).

Toshiba didn’t say which products would be pulled, but it’s understood that Toshiba has been a supplier of hard-disk drives, discrete semiconductors and high-speed data processing system LSI to Huawei. Toshiba said it did not expect a big impact on its earnings, and that it would resume shipping products that are found not to include US-made components. But given the interlocking nature of supply chains in the global economy, it’s extremely likely that at least some of the components in all of its hard drives were manufactured in the US, and thus would be subject to the ban. Until March of this year, Toshiba and Huawei had been working on an Internet-of-things project, but it has since been abandoned. Google was the first major tech company to turn on Huawei by announcing that it would cut Huawei phones off from access to most of its Android operating system-related services, though that decision has been suspended for 90 days thanks to Washington’s decision to delay the order.

As more companies turn on Huawei, shifting the gravity of the trade dispute to finally focus squarely on Washington’s campaign against the global leader in 5G technology, Chinese media and its critical rhetoric have grown more strident. As the Guardian pointed out, a CCTV bulletin accused Washington of being “delusional” for thinking that “technological bullying” could hurt China. “This shows some American politicians are extremely narrow-minded and cannot tolerate the normal pursuit of development and progress of other countries.”

As for the timing for the next round of talks, neither side is showing much willingness to restart negotiations.

China’s Ministry of Commerce said Thursday via its spokesman Gao Feng that the US would need to “show sincerity” – that is, stop its escalation – if it wants talks to resume, adding that China won’t make concessions on key issues.

China Foreign Ministry spokesman Lu Kang said during his regular news briefing in Beijing that the Chinese government would continue to support Huawei and other Chinese tech companies, and accused the US government of using “ntaional power to oppress other countries’ companies and disturb market functions.” Responding to legislation proposed in the US that would sanction companies involved in China’s construction in the South China Sea, Kang warned Washington not to advance the bill, or face more of a backlash.

Japan and the UK have joined the blockade of Huawei, and South Korean media report that Washington has stepped up its lobbying of the Blue House to ban the use of Huawei telecoms equipment, warning about the potential for espionage. That’s an extension of a strategy Washington has used with other allies to mixed success.

via ZeroHedge News http://bit.ly/2VGDOvO Tyler Durden

On the coasts, most Americans have been so preoccupied with the drama in Washington that they’re probably not even aware of the chaos unfolding across the plains states and the Midwest. But if anything can distract America from the Democrats’ grandstanding, this just might.

Late Wednesday night, a tornado ripped across Jefferson City, the capital of Missouri. The storm, described as a “direct hit” to the capital city, left dozens trapped and injured. What the National Weather Service described as a “violent tornado” landed nearly eight years to the day that another deadly storm leveled Joplin, Missouri. More tornadoes, thunderstorms and flash floods are expected for a large swath of the Midwest between Oklahoma and Illinois.

Across the state, storms have left three people dead, the Missouri Department of Public Safety reports.

Law enforcement can confirm three fatalities in the Golden City area of Barton County and several injuries in the Carl Junction area of Jasper County. #MoWx#GoldenCity#CarlJunction

According to the National Weather Service, the Jefferson City storm moved at 40 mph and blasted debris 13,000 feet into the air. Tornado and thunderstorm warnings were extended into the early morning hours of Thursday.

Tornado Emergency including Jefferson City MO, Holts Summit MO, Wardsville MO until 12:30 AM CDT pic.twitter.com/6xwmTcIdjv

Tornado watches were in place for areas from Oklahoma City northeast to central Illinois overnight. The NWS has received 33 reports of tornadoes between late Wednesday and Thursday morning. Since Tuesday, 60 such storms have been reported.

What CNN described as a “wedge tornado” – that is, a storm that is wider than it is tall – was first spotted around 11:30 pm on Wednesday near Jefferson City. The Fire Department in Jeff City asked residents to “Pray for Us” in a Facebook post.

In Jasper County, wedged in the southwestern corner of the state, another storm ripped through the area surrounding Joplin, coming within ten miles of the city, in some cases.

Because of the severe damage in Jefferson City, Missouri Gov. Mike Parson asked all non-essential state employees to remain at home on Thursday.

Major tornados across state tonight, including Jeff City. We’re doing okay but praying for those that were caught in damage, some are still trapped – local emergency crews are on site and assisting.

— Governor Mike Parson (@GovParsonMO) May 23, 2019

Due to the tornado and severe weather in Jefferson City last night we are asking that all non-essential state employees in the Jefferson City area remain at home on Thursday. We have damage to state buildings and power is down in some areas. Please be safe!

— Governor Mike Parson (@GovParsonMO) May 23, 2019

One woman described to CNN how she and her daughters sheltered in the only room in their house with no windows.

“When it hit… it felt like an earthquake,” said Cindy Sandoval-Jakobsen.

Photos captured the immense bulk of the storm ripping through Jeff City.

For anybody wondering what it’s like to experience such a devastating storm, this first person video offers a faint idea.

🔊🔊SOUND ON: Hear what residents heard just moments before a large #tornado ripped through places like #Eugene and #JeffersonCity in #Missouri. Local officials are reporting extensive damage and multiple people trapped in buildings. We’ll have more details as they’re available. pic.twitter.com/nHUuXjbpbW

The citizens of the European Union are called to vote this week for the European Parliament. It is not a real parliament, and it lacks prospects for becoming one, since all important decisions are taken by the unelected heads of the European Commission and the European Central Bank, dubbed “the worst-run Central Bank in the world”.

These elections capture however the general mood of exasperation with current policies. Conservative and extreme Right parties will rise, reflecting widespread scepticism as to the economic course of the EU and its lack of benefits for the common people. The mainstream Left unfortunately neglects these issues, and it will pay the price.

The conservatives generally blame the weak and scapegoat the refugees, the immigrants, the women, and the poor, while promising to save the middle class from the onslaught of big capital. They create false hopes of easy reform, and they never denounce the exploitation inherent in today’s system. History shows however that small owners manage to resist financial stranglehold only when they make common cause with workers and the poor, and they are not afraid to fight.

The economy looks ever more frail. In all, the Eurozone’s nominal GDP stagnates, shrinking 12% in its six largest economies in 2008-2017. The European Union remains indifferent to the peoples’ needs, while it caters for every whim of the corporations. Even so, Quantitative Easing and other crony capitalist schemes promoted by the ECB, such as the Private-Public Partnerships (PPPs) or the new Targeted Long-term Refinancing Operations (TLTRO-III) cannot save the day.

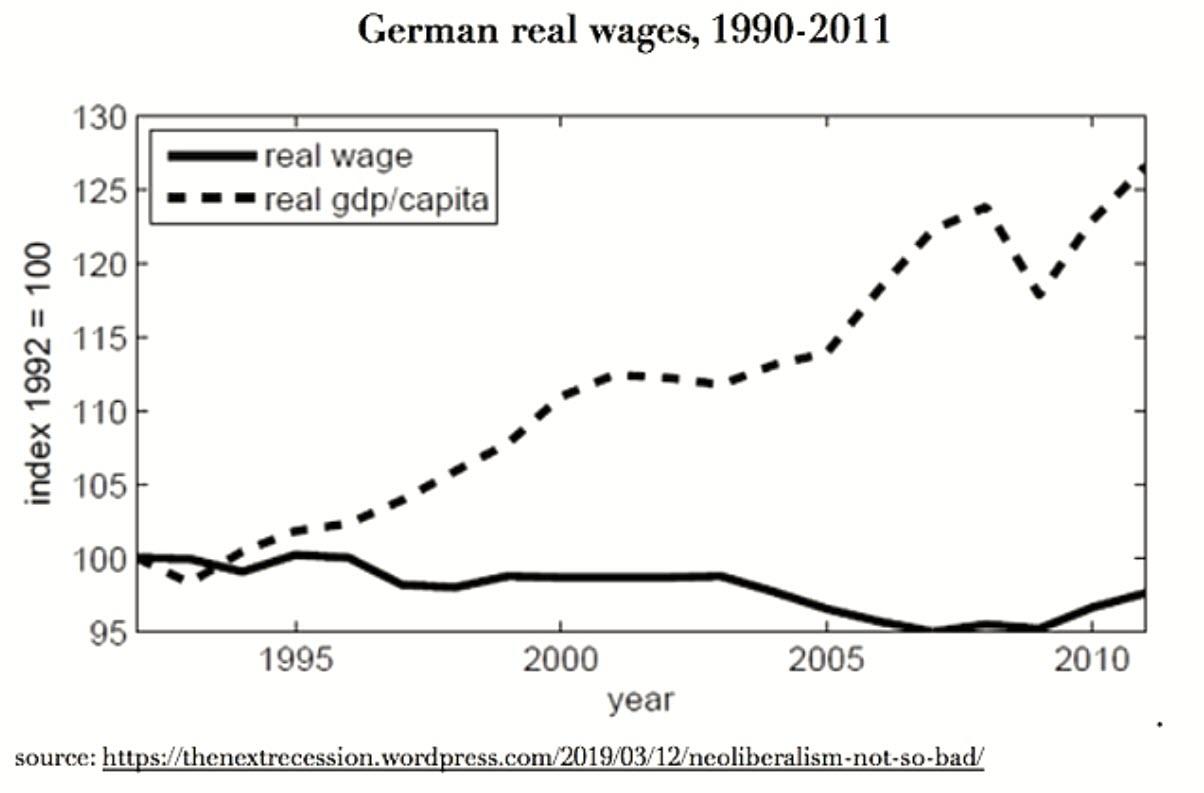

Donald Trump declares bluntly “I don’t care about Europe”, showing that US considers our continent as little more than a collection of vassal states. In all countries inequality rises, corporations rule, and oligarchs impose their will. Liberal France exhibits an abhorrent authoritarianism against the Yellow Vests. Italy chases the refugees and the Roma. Workers’ rights and incomes are eroded everywhere, with women workers hit particularly hard. Even in successful countries, such as Germany, real wages remain below their 1990 level.

Exploitation today is often effected through debt. Public and private debt are crucial mechanisms for the ongoing transfer of wealth and power from the poor to the rich, from the weak to the strong, from the many to the few. Public discussion so far neglects this issue, even though financial expropriation’s explosive potential is well known to insiders and to the mainstream parties.

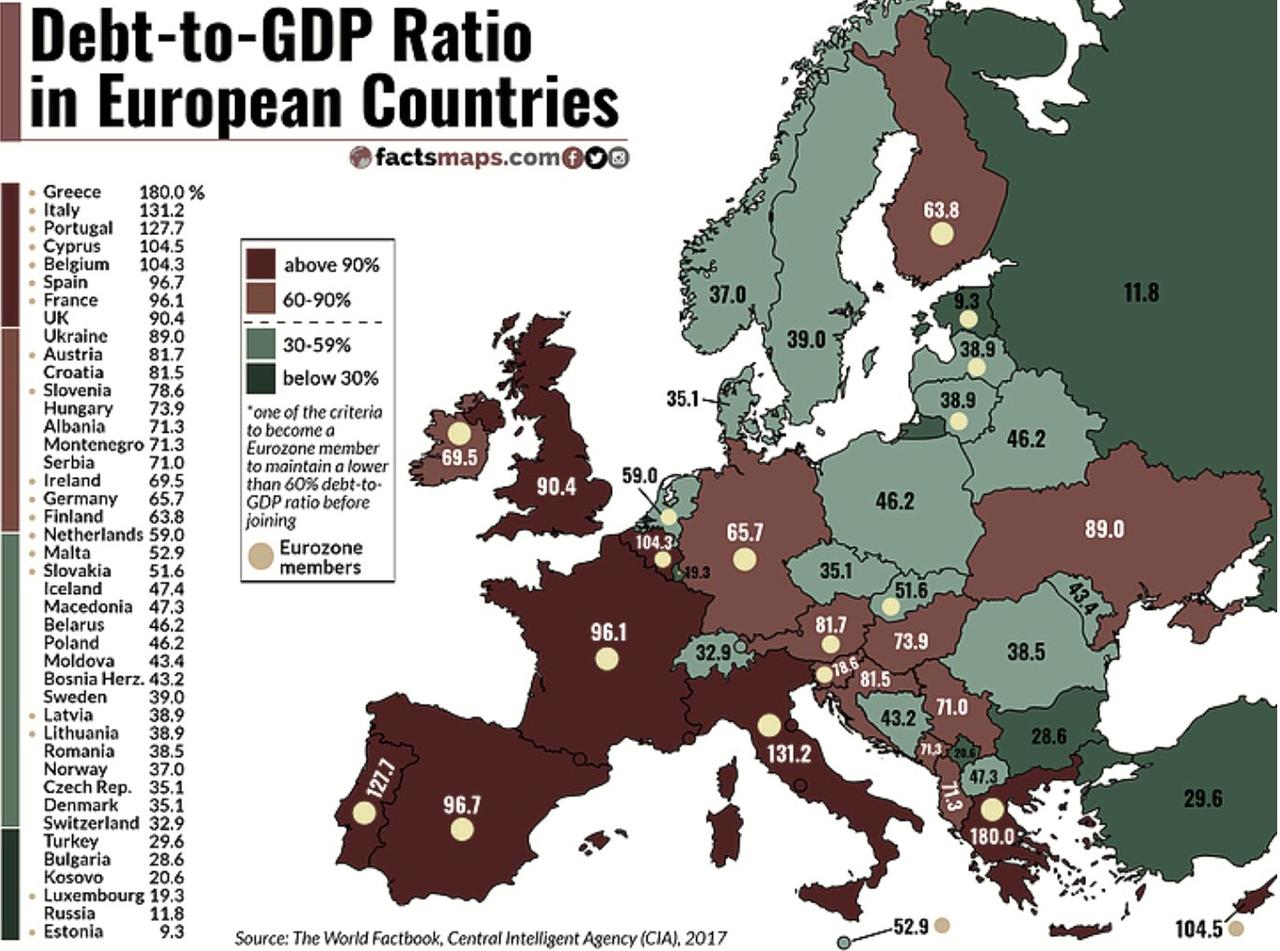

Public debt in today’s European Union totals 13 trillion euro, reaching 80% of its GDP. This average masks huge variations between the European periphery and the core. For example, Greece owes 335 billion euro or 181% of its GDP, Italy 2.3 trillion (132%), and Portugal 225 billion (122%). On the other hand German public debt at 2 trillion is 61% of the GDP, and tax haven Luxemburg’s 12 billion is only 21%.

Public debt is a political choice, not a law of nature. In today’s Europe it is used to subsidise corporations, not the vanishing social state. Instead of covering their needs by taxing the rich, states beg them for loans, get gleefully indebted to them, and promptly pay huge interest to them. Falling further down into the debt trap, states transfer huge resources from the periphery to the centre, and from poor to rich. This gigantic public debt entails the destruction of democratic institutions, turning citizens into debt peons, and stealing our children’s lives.

In 2010 the Troika appointed itself as saviour of Greece from its excessive debt, which then stood at 109%. The European Commission, the European Central Bank and the International Monetary Fund imposed draconian austerity and the liquidation of public property. The Greeks’ sacrifices did not save them, but led to destitution and debt slavery. Parliamentary government became an empty form and a far Right criminal organisation, modelled on Hitler’s Nazis, surged. No European or national institution took responsibility for the debacle. But the peoples of Europe took heed.

The rest of Europe is but one debt crisis away from the fate of Greece. And the global financial bubble is guaranteed to bring this crisis forward, sooner rather than later.

Fiscal pressure leads to revolts or even cataclysmic change – it ushered to the French, the Russian, and the Chinese revolutions. But the debt crisis is not insoluble in itself. States have always the sovereign right to abolish debt, as Iceland did recently. This does not hurt the economy, but gives it a boost. It simply means that the rich will not foreclose for themselves bigger and bigger parts of future production.

We call on all European citizens, within or without the European Union, to check parties’ policies on debt. Parties lacking a clear policy on this issue either do not recognise its seriousness or simply side with the financial oligarchy.

The only responsible way to vote is to support parties promoting debt justice. This includes the abolition of odious public debt, and the resolution of non commercial private debt in favour of the many and poor debtors, instead of the few and rich creditors.

via ZeroHedge News http://bit.ly/2JvNvLK Tyler Durden

Since Nigel Farage officially launched the ‘Brexit Party’ six weeks during a coming-out party in Coventry, Farage and his allies have ridden widespread frustration with a seemingly ineffectual British political establishment to the top of the polls, attracting waves of defectors from the Tories and Labour.

The most recent polls – taken just days before the vote, which, for the UK, will take place on Thursday – show the Brexit Party is up by double-digits over its nearest rival, the Liberal Democrats. Meanwhile, support for Labour and the Tories has dwindled to single-digit levels.

If the Brexit Party succeeds, its candidates will occupy a plurality of the UK’s 73 MEP seats. In the European Parliament, they will join a growing group of euroskeptic parties that have pledged to oppose the Brussels agenda at every turn and, where they can, change it entirely.

Created just four months ago after Farage officially left UKIP, a pro-Brexit party that Farage once led, but that, according to the man who is widely credited as the architect of Brexit, had become increasingly occupied by racists and Islamophobes.

Ironically, the New York Times offers one of the most apt explanations of how Farage managed to pull this off:

As Brexit chainsaws its way through British politics, dismantling decades-old political allegiances, tearing apart the traditional parties and leaving voters confused, frustrated and angry, the Brexit Party is thriving by offering a simple and hard-edge message.

“People feel completely betrayed, they feel abandoned, they feel even hated and despised by the political class and also by the media,” said Martin Daubney, the lifelong Labour voter now standing for the Brexit Party, who used to edit a raunchy men’s magazine before reinventing himself as an anti-pornography advocate. “It feels like a grass-roots political revolution on the streets of Britain right now.”

Should the Brexit Party succeed in winning the largest share of the vote this week, it will send an unequivocal message to the dithering Tories: The people want Brexit, regardless of the details. A Brexit Party success could give pro-Leave Tories the ammunition they need to see it through.

As the Brexit Party has surged in the polls, the backlash from remainers has intensified, culminating with Farage being ‘milkshaked’ during a campaign rally in Newcastle.

His assailant was arrested. But the incident was followed on Wednesday by a swarm of protesters holding milkshakes surrounding Farage’s campaign bus, according to the Independent. If anything, these incidents have only helped the Brexit Party’s standing in the polls. And Farage appeared to take the attack in stride.

Sadly some remainers have become radicalised, to the extent that normal campaigning is becoming impossible.

For a civilised democracy to work you need the losers consent, politicians not accepting the referendum result have led us to this.

Political opponents who have denounced Farage as a fascist are having a much harder time arguing against his heterodox slate of candidates, which includes several former revolutionary communists who once defended the IRA’s deadly bombing campaign.

Though the Brexit party has been vague about its policy positions (apart from supporting the UK’s immediate departure from the EU, even if that means a ‘hard’ or ‘no deal’ Brexit), the party’s candidates would probably join with other euroskeptic MEPs once they take their seats. However, to determine where it stands on other issues, the Brexit Party has said it would set up an online forum where supporters can weigh in, similar to a platform run by the Five Star Movement in Italy.

But more than anything else, the Brexit Party has benefited from disillusionment with Theresa May’s promise that she would take the UK out of the EU on time and in an orderly manner because “Brexit means Brexit.” Her inability to do so may have alienated a whole generation of Tory voters.

“It doesn’t matter what happens from now on, I will never ever stick a cross in the Tory box ever again,” said Andrew Kirby, 44, sitting beside his father. “There’s nothing that could happen. If the Brexit Party doesn’t come to anything, I shall never vote again.”

via ZeroHedge News http://bit.ly/2VXW1Kb Tyler Durden

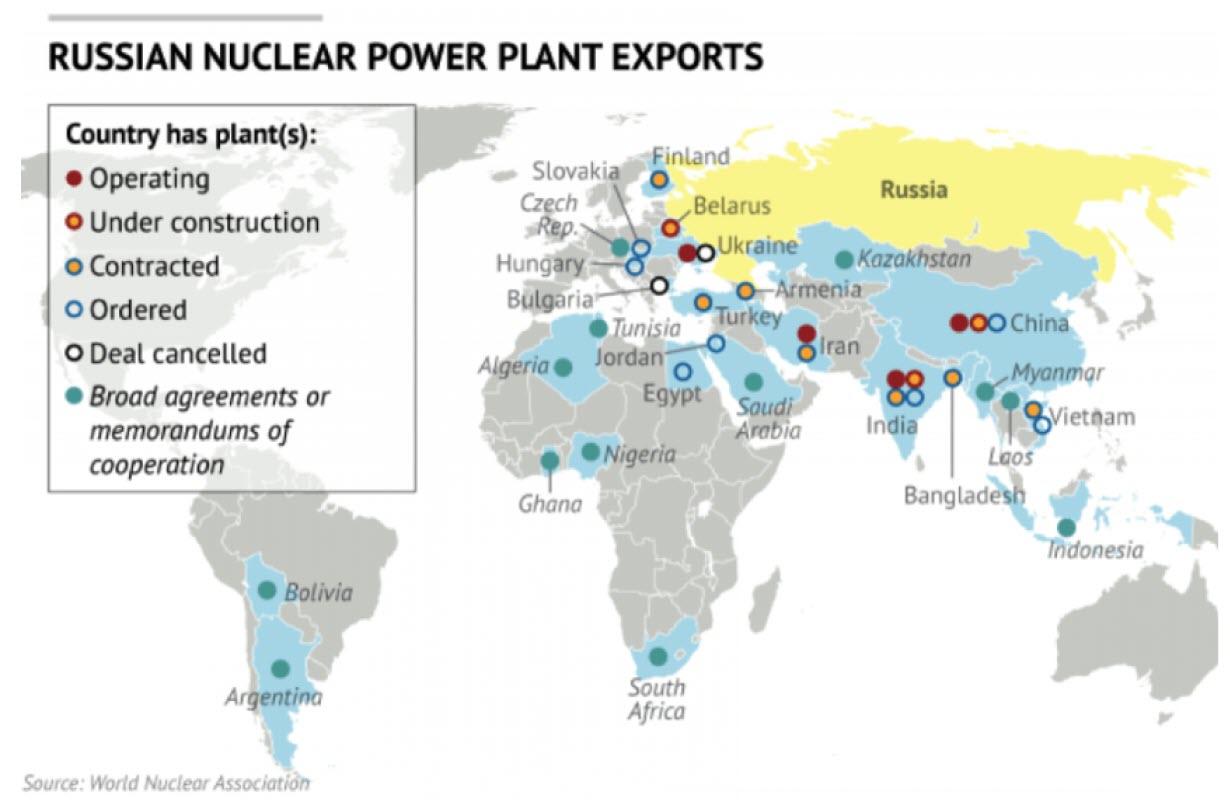

Africa’s economic potential is enormous: the continent contains significant mineral and energy deposits, a young and growing population, and an underdeveloped energy sector desperately in need of investment. Approximately 640 million people, or two-thirds of the entire populace, don’t have access to electricity. According to the African Development Bank, energy poverty reduces GDP growth by 4 percent every year. Russia’s energy industry, in comparison, is booming. Its state-run nuclear energy company Rosatom has an order book of 34 reactors in 12 countries worth $300 billion. Recently, Moscow has set its eyes on Africa where most states have either already struck a deal with the Kremlin or are considering one.

Africa’s long march forward

Currently, only South Africa is operating a commercial nuclear power plant with plans on the table to expand capacity. Another ten states are in different stages of planning and negotiations including Algeria, Egypt, Ghana, Kenya, Namibia, Nigeria, Tanzania, Tunisia, Uganda, and Zambia.

(Click to enlarge)

Energy poverty is a significant problem in the world’s least developed continent. The lack of access to a reliable and affordable source of energy is a severe impediment to economic development. Although the costs of renewables have decreased significantly over the years, technical and geographic limitations impede the rapid rollout of solar and wind energy. Also, Africa is urbanizing much quicker than the rest of the world where cities are expanding by 8 percent every year compared to 2 percent globally – which puts even more pressure on the existing energy systems.

The Russian deal is particularly appealing to countries lacking nuclear knowhow due to Moscow’s comprehensive offer regarding financing, construction, and operation of the facilities. Currently, Rosatom is experimenting with a contract known as ‘build-own-operate’ under which ownership of the plant remains in Russian hands while energy is sold to the host country. This new type of contract is appealing to several African states who lack the means to finance construction. In some instances, the mineral resources of host countries could function as a deposit for any liability comparable to Moscow’s ‘arms-for-platinum’ deal with Zimbabwe worth $3 billion.

The Russian deal is also attractive for countries lacking the necessary infrastructure because Moscow takes back nuclear waste which means that host countries don’t have to worry about storage. From a security point of view, this could alleviate concerns regarding weapons production through plutonium reprocessing or threats from non-state actors.

Russia’s strategy

Moscow’s is reusing its successful Middle East strategy comprised of diplomacy, energy, and security. The Kremlin has presented itself as a ‘clean’ and honest broker lacking the colonial background of most Western countries. Africa’s relative instability and need for cheap energy makes it a good match for Russia which is looking to expand its global presence and find new markets for critical industries such as energy.

From Moscow’s perspective, sanctions and deteriorated relations with the West have increased the need to improve its relations with other parts of the world. Africa is not a new frontier for the Kremlin, which maintained diplomatic and military contact with the continent during the Cold War to counterbalance the U.S. This time, however, Moscow is not driven by ideology but by the need to increase influence and its position as a global power.

Nuclear energy is an obvious option as Russia is a global leader in nuclear technology. The country processes 7 percent of the world’s uranium production, 20 percent of uranium conversion, 45 percent of uranium enrichment, and 25 percent of the global nuclear power plant construction activities. Providing the necessary technology to Africa serves another purpose besides increasing influence and revenue for the state’s coffers. The continent is also home to some of the world’s largest uranium deposits in Malawi, Niger, and South Africa. Access to these resources is essential if Moscow’s wants to maintain its position globally.

A way forward or unnecessary risks?

Without a doubt, Africa is in desperate need of electricity to develop and industrialize. However, according to some critics, Russia’s nuclear involvement in unstable countries could become a global security threat due to those countries’ weak institutions and unstable governments. Moscow’s nuclear strategy will be tested after the first power plants are completed in developing countries in Africa and Asia. The lifespan of these facilities spans decades and they require an adequate and comprehensive approach in order to provide electricity for millions that is both safe and reliable.

via ZeroHedge News http://bit.ly/2JvHCOE Tyler Durden

Western Europe is home to a cluster of developed economies that boost some of the highest standards of living in the world. But that could soon change. Because as Evan Horowitz writes on NBC News’s new “Think” vertical, IQ scores in France, Scandinavia, Britain, Germany and even Australia are beginning to decline.

The trend has been well-documented across Western Europe, and could soon carry over to the US as well. Which means the data have confirmed what millions of Americans who have watched cable news or logged on to twitter over the past three years probably already suspected: The world is getting dumber.

And just like that, another sign of the ‘Idiocracy’ apocalypse has emerged. Though, unlike the movie, which posits that the population of Earth will become steadily dumber as stupid people outbreed their more intelligent compatriots, the cause of the trend in Europe has yet to be determined, because even the children of relatively intelligent Europeans are getting dumber.

Details vary from study to study and from place to place given the available data. IQ shortfalls in Norway and Denmark appear in longstanding tests of military conscripts, whereas information about France is based on a smaller sample and a different test. But the broad pattern has become clearer:Beginning around the turn of the 21st century, many of the most economically advanced nations began experiencing some kind of decline in IQ.

One potential explanation was quasi-eugenic. As in the movie “Idiocracy,” it was suggested that average intelligence is being pulled down because lower-IQ families are having more children (“dysgenic fertility” is the technical term). Alternatively, widening immigration might be bringing less-intelligent newcomers to societies with otherwise higher IQs.

However, a 2018 study of Norway has punctured these theories by showing that IQs are dropping not just across societies but within families. In other words, the issue is not that educated Norwegians are increasingly outnumbered by lower-IQ immigrants or the children of less-educated citizens. Even children born to high-IQ parents are slipping down the IQ ladder.

Possible explanations include: The rise of smartphones and other devices, which have worn away at our ability to focus, the rise of lower-skill service work that isn’t as intellectually stimulating and less-nutritious food.

Whatever the cause, the trend seems to portend a decline in long-term productivity and economic success, factors that have long been correlated with IQ.

But for now, at least, readers can find contentment in the knowledge that it’s not just us: Everybody really is getting dumber.

via ZeroHedge News http://bit.ly/2JBYAuW Tyler Durden