While we had grown somewhat used to seeing horrific self-immolation scenes across various authoritarian regimes in Asia, the US Secret Service confirmed that a man has set himself on fire a short distance away from the White House today.

At approximately 12:20 p.m. a man lit himself on fire on the Ellipse near 15th and Constitution Ave., Secret Service personnel are on scene assisting @NatlParkService and @usparkpolicepio in rendering first aid.

— U.S. Secret Service (@SecretService) May 29, 2019

A Man Set Himself on Fire In Downtown Washington, Across From The White House Today.

The White House Spokesman Hogan Gidley said He could Not Immediately Comment On The Situation. pic.twitter.com/ksJzqrNzb2

Five years ago, a company called Yo raised $1.5 million at a $10 million valuation.

What did investors and end-users get for this much money? An app that allowed users to send the message “Yo,” (and NOTHING else) to their friends.

It didn’t take long for the company to blow through all that cash in typical Silicon Valley manner, and let go of all its employees.

At the peak of investing hysteria, it was that easy to scoop up a couple million dollars to fund your company, no matter how worthless the idea.

With so much easy money from low interest rates and booming stocks, people were dumping money into anything with a pulse.

There’s still a lot of money out there today. But investors have tightened their purse strings and become more discriminating with where they put their money.

Last year’s venture capital was distributed to fewer businesses, and it went to more established companies over startups.

It hasn’t been this hard for early-stage companies to get venture capital investments since 2011. And the number of SaaS (Software as a Service) investments is also at a seven-year low.

With the stock market looking shaky, and investors starting to worry, people are focusing on removing risk, not diving into uncertain new businesses.

But anyone looking to start a company shouldn’t feel like the chance to get funding has passed. There is still one big pool of money that NEEDS to be invested.

In order to take advantage of the tax savings, those funds need to invest that capital inside one of almost 9,000 designated underdeveloped areas in the US called Opportunity Zones.

Right now there are billions of dollars sitting in Opportunity Funds… and the clock is ticking. Opportunity Funds have to deploy 90% of their capital in Opportunity Zones within 6-12 months of receiving the money from investors.

If you have ever wanted to start a business, but worried about having to raise a lot of money, or attract investment capital, this is your chance.

Starting a business in an Opportunity Zone is a way to tap into billions of dollars of capital.

Instead of paying a huge tax bill, investors can put their gains into equity in your company and defer paying capital gains tax until 2026 (plus get a 15% discount if they hold the investment for seven years).

In the meantime, all that money that would have gone to taxes will be growing your company instead.

And a huge plus to investors is that any growth they spur in your business will be tax-free if they hold the investment for ten years.

That means you and your investors can focus on long term growth– not cheap gimmicks that don’t last.

Plus the IRS guidance on Opportunity Zones keeps getting better.

The whole point of these Zones is to bring investment and jobs into neighborhoods that need it most. So the IRS says a business must be active (you can’t just sit on real estate without improving it), and must earn 50% of its income inside the Opportunity Zone.

But the IRS gave three different ways to satisfy the income requirement:

Either your employees (and independent contractors) spend at least 50% of their work time within the Opportunity Zone.

Or at least 50% of the wages of your employees (and contractors) come from performing services within an Opportunity Zone.

Or at least 50% of the income of your business is generated by tangible property located in an Opportunity Zone, and the management or operational functions are performed within the Opportunity Zone.

This leaves the door open to all sorts of businesses.

A storefront business would easily apply, because all sales are in the OZ.

But even something like a landscaping company could work even if all of its clients are outside the Zone, as long as the physical equipment and business headquarters are located there.

Keep in mind that you don’t even have to employ anyone other than yourself.

And there is a wide range of business possibilities. For instance, many of these Opportunity Zones are in beautiful wilderness areas that would be perfect for nature tourism.

Bigger ideas can work too.

The Pearl Fund is a new Venture Capital Opportunity Fund looking for tech-startups with potential to grow at least 10x. Its ultimate goal is to fund “the next Apple or Google.”

But tech startups will have to be careful to deploy the capital properly to meet the requirement of doing business within the Opportunity Zone.

Still, it could be worth the extra effort to attract investors. If you go from an initial $1 million investment to a $100 million valuation in ten years, your investors will pay no capital gains on the $99 million growth.

But you do have to act quickly. A lot of the capital will flow into these funds by the end of the year, because after that, it will be too late to get the 15% discount on deferred capital gains.

And remember, these funds MUST invest their capital within a year of receiving it, which means they are hungry for good businesses to fund.

So this could be the perfect time to start your business.

While most eyes are focused on the collapse of the US yield curve and its recessionary predictions, there are many other critical issues that are flashing red ‘recession-imminent’ flags…

To keep buying the dip, investors have to ignore…

Bonds… (yields at cycle lows, curve at decade flats/inverted)

Lumber… (one of the most important factors in construction is at its lowest level since April 2016)

Copper…(the commodity with the PhD in economics rolled over ahead of stocks)

Global economic data… (suffering the longest negative streak – 286 days – on record)

Hope… (soft survey data has not picked up the mantle of ‘hope’ that stocks have ridden on since the start of the year)

Money Supply… (the fuel for PPT/National Team pumpathons is starting to run dry again)

And finally, why – if everything is awesome – is the market screaming for almost 2 full rate cuts by the end of 2020?

via ZeroHedge News http://bit.ly/2MhU5rv Tyler Durden

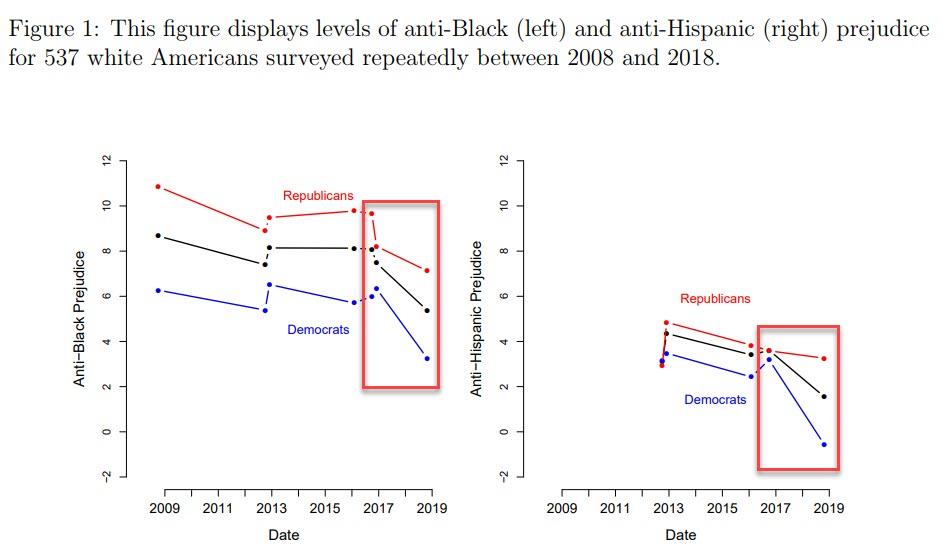

Despite the propaganda, could the Trump era be the least prejudiced in American history?

The left isn’t going to like this one. A recent study on racism in America has revealed some truths that directly contradict one of the progressives’ most beloved narratives. The Democratic Party and its allies in the press have expended no small amount of effort over the past few decades to convince the American public that everyone who isn’t a rabid lefty is a hateful racist.

Of course, President Trump has become the left’s favorite target for race-baiting antics; many claim that the president’s rhetoric and policies have emboldened white supremacists and made America more racially bigoted. But according to researchers at the University of Pennsylvania, that assertion is not quite accurate.

Racism Has Decreased Under Trump

Sociologists Daniel J. Hopkins and Samantha Washington conducted a study to analyze the impact of Trump’s election on prejudice against blacks and Hispanics. They used a panel of 2,500 Americans whose views on race and other matters had been documented since 2008. According to the report, the researchers expected to see an increase in racial prejudice in the Trump era. Yes, it might be difficult to believe that professors at a major university would immediately assume that the president singlehandedly made the country more racist, but it’s true.

And why did they make this assumption? Apparently, they formed their hypothesis based on the idea that people have deep-seated racism lying dormant within themselves, waiting to be awakened by a provocative event. The theory was that Trump’s election somehow pushed the magic “I’m totally a racist” button that lurks in the hearts of men – probably white men, specifically – and instantly transformed them into a legion of slobbering white supremacists bent on the utter destruction of minorities.

But the findings were surprising, and likely a bit disappointing, to the researchers and the media establishment. Instead of an increase in racism, the study revealed a marked decrease. Between 2012 and 2016, racist attitudes had decreased by a small degree, but after 2016, when Trump was elected, racism plummeted. The drop was equally present in Republican voters and Democrats.

Why The Change?

It is apparent that the findings of the study put the researchers and the press in quite a quandary. How could they spin the results in a way that doesn’t damage the narrative? Fortunately for them, being a progressive makes one highly proficient in the sport of mental gymnastics. Instead of acknowledging that America is not as racist as Al Sharpton wants us to think, the researchers posit that perhaps Trump’s racism has been so abhorrent, it made racist Americans want to be less bigoted.

It is possible that “Trump’s rhetoric clarified anti-racist norms… given that the declines in prejudice appear concentrated in the period after Trump’s election, it seems quite plausible that it was not simply Trump’s rhetoric but also his accession to the presidency that pushed public opinion in the opposite direction,” the sociologists wrote.

If this doesn’t quite make sense to you, congratulations! You’re a normal person. But some on the left had another idea. The Spectator suggested the reason racism declined was that it had risen to drastic heights when Obama was in office. It argues that, “maybe social science has got it the wrong way round: it was the sight of a mixed race man in the White House who brought out in the inner racist in Americans who are inclined towards those feelings, while the reassuring sight of white man back in the Oval Office has calmed them down.”

An Alternative Theory

Perhaps it is possible that both theories are wrong, and a wee bit of common sense might be appropriate. The reality is that the president does not have the power to make the country more or less racist. And yes, this also goes for Obama, who many conservatives blame for escalating racial tensions during his time in office. While neither president handles racial issues perfectly, American attitudes evolve on their own and are not subject to the whims of the person who happens to occupy the Oval Office.

This report showed that racial tensions were already decreasing under Obama, albeit at a slower pace. Perhaps some whites reaffirmed their opposition to racism when Trump was elected and the media tried to convince America that he was the Führer, who was going to bring back slavery and put Hispanics in catapults to launch them back over the southern border.

But it does not seem likely that these individuals account for the majority of the decrease. Maybe the truth is that America’s views on racial issues are continuing to evolve, and we are becoming gradually less racist every year, despite the far left’s attempts to foment division between whites and minorities through its favored propaganda outlets. As long as Americans continue to aspire towards the values on which the nation was founded, the country will move farther away from its racist past.

via ZeroHedge News http://bit.ly/2WdABsK Tyler Durden

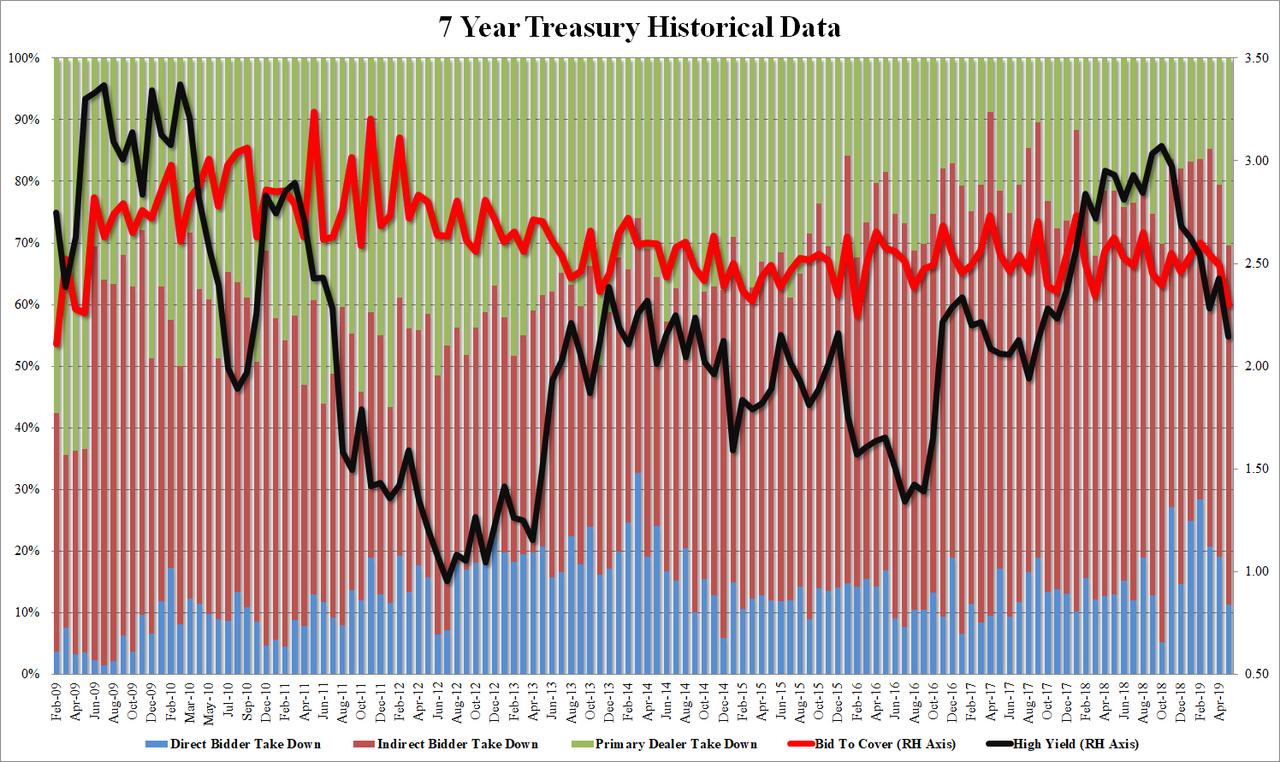

After a strong 2Y, mediocre 5Y, we concluded this week’s trifecta of coupon auctions with, as one may expect, an abysmal sale of $32 billion in 7Y bonds.

With yields sliding lower all day, perhaps it had to do with the concessions into the 1pm auction, but whatever the reason, the 7Y auction stopped at a high yield of 2.144%, which while the lowest since September 2017, also tailed the When Issued by 1.9bps, the biggest tail in at least 4 years.

The internals were just as ugly, with the Bid to Cover tumbling from 2.492 to just 2.298, not only far below the 6 auction average of 2.53, but the lowest since February 2016, and second lowest since 2009.

And with both Direct and Indirect takedown sliding, as Directs took down only 11.3% from 19.1% last month, and half the 6 auction average of 22.5% and Indirects ending up with 58.3% of the auction, Dealers we left holding 30.5% of the auction, the highest percentage since March 2018.

Overall, a dismal auction, although one which can perhaps be ignored as it took place on a day when the 10Y yield tumbled to the lowest in almost two years. Or maybe not, because once the market digested just how ugly the auction was, the 10Y promptly sold off, and in just a few minutes wiped out all of the day’s gains.

via ZeroHedge News http://bit.ly/2Mgu7o8 Tyler Durden

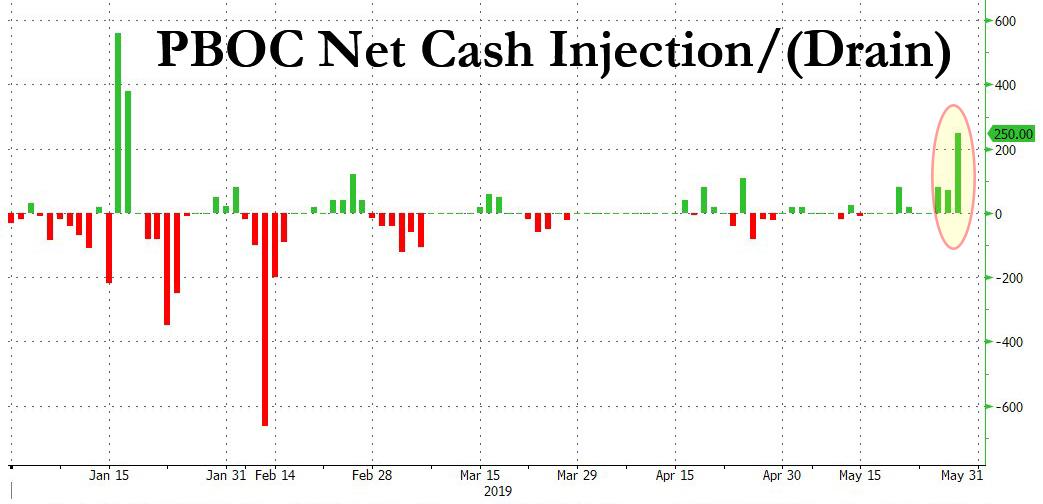

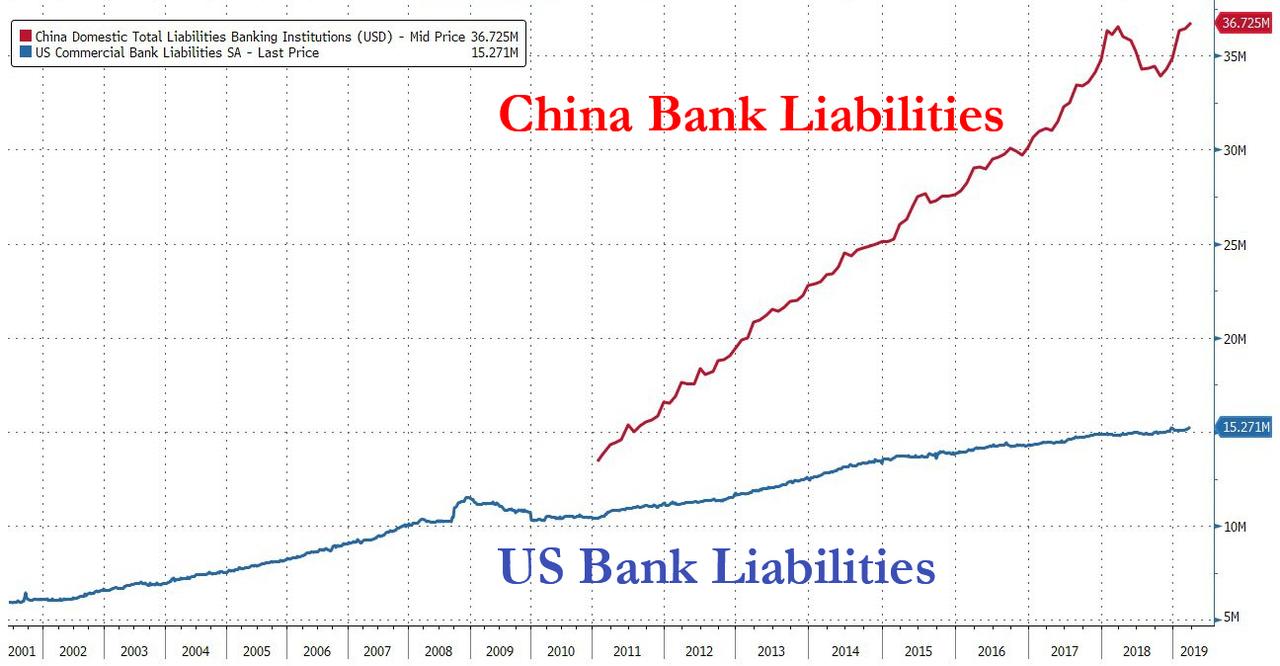

With China’s bond market continues to be hammered in the aftermath of the government’s surprise seizure of Baoshang Bank (see “A Big Wake Up Call”: Chinese Bond Market Roiled By First Ever Bank Failure“), the PBOC – whose open market operations had been in dormancy for much of 2019 – finally panicked and on Wednesday injected a whopping net 250 billion yuan ($36 billion) into the financial system via open-market operations, as it fills what traders have dubbed a growing funding gap following the Baoshang failure.

The consequences of this liquidity flood were instant: China’s overnight repurchase rate, a measure of interbank liquidity, tumbled the most in three weeks, while the benchmark 7-day repo rate also declined. “The operations so far this week send a strong signal that the PBOC is ready to ensure ample liquidity for the market, amid fragile sentiment in the credit and bond market,” said Westpac strategist Frances Cheung. The central bank also set the daily yuan fixing at a stronger-than-expected level to prevent even a hint of speculation that China will be have no choice but to devalue the yuan as part of the “reliquification” of the market.

The PBOC’s massive liquidity injection, which was the largest since January when the S&P was still close to a bear market and started the tremendous Chinese stock market rally, also helped the Shanghai Composite be one of the few markets that closed in the green overnight.

However, while the near-term reaction was favorable to Chinese risk, the paradox is that this only became a viable option as a result of a far greater problem: China’s interbank funding market is starting to freeze.

As we reported on Tuesday, the bank has – or rather had – more than 60 billion yuan of negotiable certificates of deposit (NCDs) and 6.5 billion yuan of subordinated bonds outstanding. Trading in the the company’s NCDs and other bonds was promptly suspended on Monday, with traders fearing that a self-fulfillling prophecy would emerge as contagion spreads to other troubled banks’ NCDs and/or bonds.

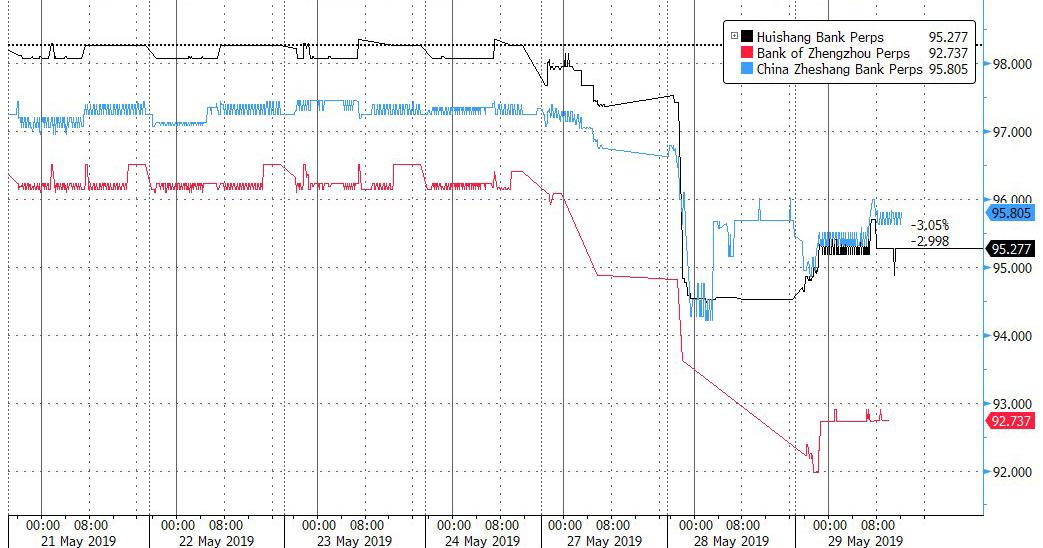

As noted previously, the contingent convertible/perpetual debt issued by some of the more troubled banks such as Huishang, Bank of Zhengzhou and China Zheshang Bank, was hammered over the past three days and has yet to recover.

As an aside, for those asking why NCD’s matter, the answer is because as we explained as far back as two years ago, numerous smaller banks had become acutely reliant on such shadow banking funding mechanisms as Certificates of Deposit, which had become the primary source of short-term funding for many of China’s banks mid-size and smaller banks.

As Deutsche Bank further explained, the banks most exposed to a shut down in this “shadow funding” pathway are medium-sized and small banks, for whom wholesale funding made up 31% and 23%, a number that has risen substantially in the interim period.

The issue of NCD funding is especially troublesome, because as Bloomberg reported overnight, in the aftermath of the Baoshang seizure, some Chinese banks and securities firms “tightened requirements for negotiable certificates of deposits that are used as collateral for funding.” In some cases, private NCDs were shunned altogether, and some financial institutions now only accept NCDs sold by state-owned and joint stock banks as collateral while some have refused to lend money to investors pledging NCDs issued by lenders rated AA+ and below for now.

While the lock up in the NCD market is concerning, it is only partial so far, even as yields on Chinese banks’ NCDs spiked in the past 48 hours after only 44% of the planned amount was issued. Putting this in context, banks typically issue an average of 82% of the planned amount.

“The Baoshang incident is pressuring short-term liquidity,” said a trader at a Chinese bank. “Along with month-end seasonal factors, cash conditions are becoming tighter and pushing up the near-date swap points higher. And that has led the swap curve moving upward.”

Ji Tianhe, China rates and FX strategist at BNP Paribas in Beijing, said that the takeover of Baoshang could be interpreted as a “marginal targeted deleveraging” campaign, and could change the ecosystem of the interbank market.

“Smaller banks are supposed to serve the real economy, but some turned out be very active in interbank trading in order to expand their size. Now this latest move is pushing similar small lenders back to their core business,” Ji said according to Reuters. He added that as small banks are not allowed to borrow in the exchange market and have to largely rely on bigger banks for interbank funding, “they are now facing a challenging funding situation.”

This also explains why traders are casting concerned glances at Chinese bonds, because as Jianghai Securities explained overnight, China’s government bonds may slide as banks sell them to make up a liquidity shortfall from issuing fewer negotiable certificates of deposits.

Analysts at OCBC bank said in a note on Tuesday that the takeover had sparked a sell-off in Chinese sovereign bonds on Monday after reports that corporate deposits and interbank liabilities over 50 million yuan could be subject to a haircut of 20%-30%, “due to concern about the possible break of implicit guarantee.”

“This may cause interbank lenders to reassess their relationship with the smaller lenders,” the analysts said.

But a partial (or complete) freeze of the interbank funding market, which many believe is what was the key catalyst behind the US financial crisis as shadow funding conduits froze up in the aftermath of the Lehman failure, is just one of China’s major headaches. The far bigger one is the risk of a bank run.

And to address that, just around the time Baoshang was about to be nationalized, the central bank set up a wholly-owned deposit insurance fund with registration capital of 10 billion yuan on May 24, according to registration record on a website run by State Administration for Market Regulation. It’s also why on May 26, the central bank said on May 26 that PBOC, CBIRC and Deposit Insurance Fund will guarantee some Baoshang Bank debt repayment.

The good news is that for now, there have been no reports of bank runs, or even jogs, in China, although this is precisely the kind of news that would be throttled and censored as much as possible by Beijing, which can not afford a countrywide bank run, threatening the collapse of China’s massive $35 billion banking system.

China’s central bank will face increasing challenges in the coming weeks to balance liquidity injections and a depreciating yuan, Bank of America Merrill Lynch says.

The last item is that with the PBOC panicking, this may have major implications on the global scene, where the last thing China can afford is to be seen devaluing the yuan. Alas, as Bank of America notes, the PBOC is now trapped as it needs to inject even more liquidity into the system amid deteriorating data, signs of fund outflows, US-China trade tensions and as 463 billion yuan of MLF matures on June 6. The PBOC’s challenge lies in adding liquidity without letting the yuan depreciate too far, and as BofA’s Claudio Piron notes, “leaning more on monetary easing rather than fiscal will cause yields to fall and the yuan to depreciate against the greenback” which is why in preempting this, PBOC has added the massive cash injection through OMO. To be sure, while the PBOC will likely have to inject much more liquidity, the likelihood of a cut in banks’ reserve requirement ratio when the 463BN yuan of MLF expires in June is increasing.

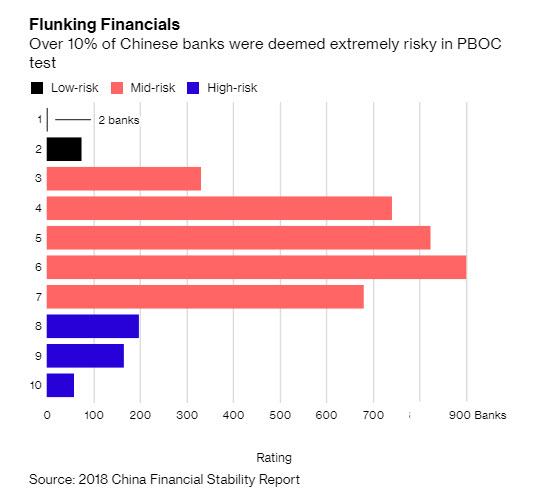

One thing that is certain: Baoshang is just the tip of the iceberg. According to UBS analyst Jason Bedford, who in 2017 was the first to highlight Baoshang’s troubles, there are several other banks that have “identical leading risk indicators” to Baoshang. Hengfeng Bank, Jinzhou Bank Co. and Chengdu Rural Commercial Bank all failed to publish their latest financial statements, have a large portion of their balance sheets invested in “loan-like investment assets” and are subject to negative local media coverage, he said in a note to clients published Tuesday.

As Bloomberg reports, Hangfeng said that it hasn’t completed auditing and reviewing its financial statements. Officials at Jinzhou and Chengdu Rural didn’t reply to requests for comment.

In short expect more Chinese bank failures in the coming weeks.

The bottom line: while much of the world is focusing on the still intangible consequences of the latest round of trade war escalation, China is currently going through a very real, and very problematic rebalancing between adjusting the level of market liquidity without sparking a sharp selloff in the yuan, which would push it below 7.00 vs the USD, and provoking another major, and panicked, capital outflow which could have dire consequences on China’s capital market and economy.

So while focusing on any flashing red headlines over the latest trade war developments, keep a close eye on what is taking place below the surface in China’s banking system, where the risk of substantial deterioration has risen substantially following the first Chinese bank failure in nearly three decades.

via ZeroHedge News http://bit.ly/2Mfft0A Tyler Durden

A Bloomberg report reveals how a Mexican bank employee directed a retirement fraud scheme at American retirees living in San Miguel de Allende, a city in Mexico’s central highlands.

Monex Casa de Bolsa SA de CV Monex Grupo Financiero has been investigating allegations that an employee stole approximately $40 million from American clients.

Marcela Zavala Taylor, the suspected Monex banker at the center of the fraud, allegedly sent American clients falsified statements that showed their accounts were fully funded, said several of the bank’s clients in a Bloomberg interview.

The fraud was discovered in late December when clients couldn’t retrieve funds from their accounts. Bank officials told clients that $40 million in funds from 158 accounts disappeared.

Bloomberg spoke with several clients who said Monex attempted to reach settlements at a massive discount versus what was stolen from their accounts. Others said the bank asked them to file charges against Zavala.

“Legal action is continuing in the case, and details cannot be disclosed so as not to hinder the investigation,” Monex said in a statement. Bank spokeswoman Eva Gutierrez said Monex is working with affected clients and has settled with 70% of them.

Kenneth Karger, a retiree from Texas with property in Mexico, says Monex stole $400,000 from him. It was only last summer when he stopped receiving statements. Karger said, Zavala at the time, told him Monex was transitioning onto a new online banking system, and the account balance would be delayed for some time. Months later, Karger retrieved statements from Monex and discovered unauthorized withdrawals.

Bruce Brown, an Australian retiree who’d lost $250,000, was refunded entirely by the bank after he notified Mexican authorities.

Monex is an affiliate of Banco Monex SA Institución de Banca Múltiple Monex Grupo Financiero, with $5.2 billion in assets under management and operations in the US.

According to Condusef, Mexico’s consumer protection agency, there were 7.3 million complaints of financial fraud involving 18.9 billion pesos (about $1 billion) last year.

The scandal has devastated the expatriate community in San Miguel, as non-citizens have limited rights.

via ZeroHedge News http://bit.ly/2YXLThp Tyler Durden

U.S. gasoline prices jumped the most since 2011 between New Year’s Day and early May this year, a few weeks before the unofficial start of the summer driving season – Memorial Day. But the national average price for regular gas has trended lower since it hit its highest so far this year on May 3.

Average U.S. prices of regular gasoline were down this Memorial Day weekend compared to last year’s and were lower than last week and last month, too.

AAA expected a record number of Americans to have hit the road by car this weekend—at 37.6 million, the number was the most on record for the holiday and 3.5 percent more than last year.

While this year’s Memorial Day average gas price of $2.830/gal is down compared to last year’s average of $2.975, and gasoline prices may continue to drop in the next two to three weeks, analysts and government estimates point to rising gas prices in the second half of the summer season due to higher gasoline demand and gasoline refining margins, and lower gasoline inventories.

The highest average price this year was hit on May 3, at $2.916/gal, according to GasBuddy. The price-tracking website and its analysts believe that the downward movement will continue for another couple of weeks.

Questions remain, however, about the price trends in the second half of the summer, GasBuddy Head of Petroleum Analysis, Patrick DeHaan, told Yahoo Finance on Friday.

For the next two-three weeks, average gas prices are expected to come down as refineries have already emerged from the spring maintenance season, producing more gasoline. Yet, after mid-June, several factors could drive gas prices higher and potentially up to a national average of $3/gal. These include the possibility of a U.S.-China trade deal that would lift global oil prices and the hurricane season in July and August potentially disrupting gasoline supply from U.S. Gulf Coast refineries, according to DeHaan.

Speaking to FOX Business on Friday, DeHaan said that “relief is certainly coming” over the next few weeks, expecting the national average to slip by 5 to 10 cents.

According to AAA, “Increased gasoline stocks amid robust summer demand may help to suppress pump prices” in coming weeks.

Earlier this month, AAA forecast that the vast majority of travelers—37.6 million—would hit the road by automobile this Memorial Day weekend—the most on record for the holiday and 3.5 percent more than last year.

“Overall, prices are very similar to this time last year and, like then, they aren’t letting that deter them from taking summer road trips,” AAA gas price expert Jeanette Casselano said, commenting on Americans’ summer plans.

According to GasBuddy’s 2019 Summer Travel survey, almost 75 percent of Americans said they would take a road trip this summer, up by 16 percent compared to last year. A total of 38 percent cited high gas prices as impacting their summer travel decisions, nearly the same as the gas price sentiment last year.

Vehicle management and reimbursement platform Motus predicted in mid-May that Americans are expected to drive a record number of miles in the third quarter, as employment and population grow. U.S. highway travel is expected to increase by 1.3 percent this summer, and the national average fuel price would be between $2.90 and $3.15 for Q3 2019, Motus market research analyst Ken Robinson said on May 15.

“Price movement will depend heavily on whether OPEC+ countries agree to increase production when they meet at the end of June and how quickly they execute. Additionally, unexpected supply disruptions in unstable areas could also affect these predictions,” Robinson said.

The new IMO rules on shipping fuel could also drive U.S. gas prices higher, as they could lift diesel demand and prices and constrain gasoline supplies in the U.S., Robinson told MarketWatch last week.

The EIA expects U.S. regular gasoline retail prices to average $2.92/gal for the 2019 summer driving season, up from an average of $2.85/gal last summer.

“The higher forecast gasoline prices primarily reflect EIA’s expectation of higher gasoline refining margins this summer, despite slightly lower crude oil prices,” the EIA said in its latest Short-Term Energy Outlook.

via ZeroHedge News http://bit.ly/2EGJlwF Tyler Durden

Tesla is moving things around at its Fremont plant in order to make way for the upcoming Model Y and a newly reported Model S refresh, according to CNBC. The new Model S, Tesla’s flagship car, is said to have a longer-range battery and and a more “minimalist” interior design, according to current and former Tesla employees, who said the company is reportedly aiming for September for its Model S refresh.

The decision to re-arrange the Fremont plant and begin working on assembling two new vehicles comes at a precarious time for Tesla’s cash balance. The automaker recently made another round of “hardcore” cost-saving cuts last week – including ditching toilet paper at some facilities – which begs the question of how capital intensive this new shift at Fremont could be.

Regardless, the company appears to be betting on its ability to redouble its efforts in the luxury segment with the Model S and capture more of the growing SUV segment with the Model Y. CEO Elon Musk had previously suggested the Model Y would be made at Fremont (why wouldn’t it, it’s essentially another Model 3), but no official announcement has been made.

According to Tesla insiders, Tesla will be required to combine the Model S and Model X production into one line to be able to produce the Model Y at the facility. The design of the Model X has been notoriously complex, and it requires a significant footprint on the factory floor to build. Tesla CEO Musk had said on Twitter recently that tours of the facility were being cancelled due to “upgrades”.

Part of the factory is being upgraded, but tours will continue around the parts that aren’t

Insiders say that the Model S refresh will “likely include an interior with the minimalist look and feel of the newer Model 3, the same drive units and seats used in the higher-end Model 3 and a battery that delivers 400 miles of range on a full charge.”

Additionally, after last week’s barrage of sell side downgrades – which included Wedbush, Citigroup and Morgan Stanley, among others – Tesla caught another downgrade mid-week from Consumer Edge, who lowered their price target on the name from $310 to $225, according to Bloomberg.

Their note mentioned that the latest equity and convertible note issuance signals Tesla “is not yet a capital efficient manufacturer with a self-funding business model”. Analyst Derek Glynn also noted a higher cost of capital for the company in the future and mentioned that potential acquirers and suitors for partnerships are few and far between. His most likely scenario is that Tesla “remains an independent company that explores partnerships with large social media platforms to quickly scale its autonomous ride-sharing network”.

via ZeroHedge News http://bit.ly/2HILdXG Tyler Durden

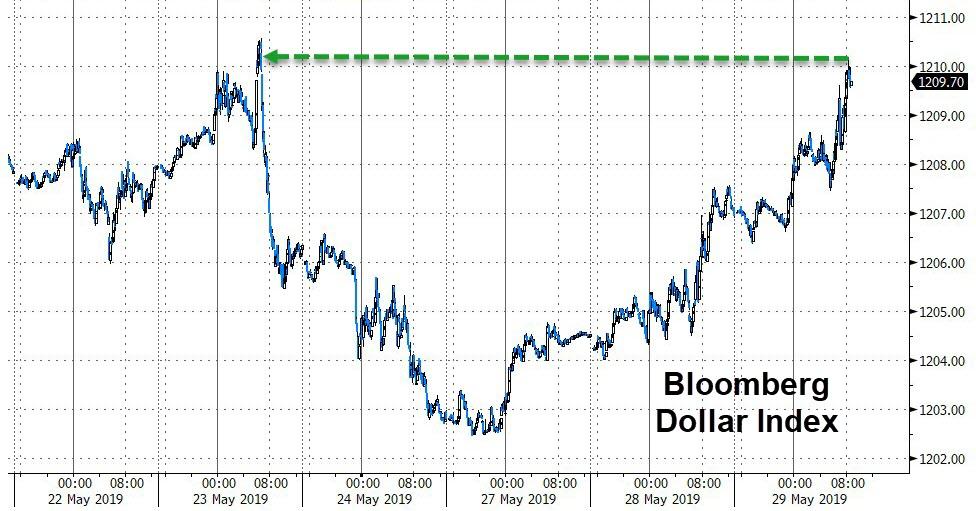

US equity markets just took another leg lower, pushing all back below their 200-day moving-averages as 10Y yields touch 2.21% and the dollar extends recent gains…

The Dow is back below 25,000…

S&P (lower left) and Nasdaq (upper left) join Dow (upper right) and Small Caps (lower right) back below the 200DMA…

As bond yields just keep sliding…

And the dollar soaring…

via ZeroHedge News http://bit.ly/2KcJmvZ Tyler Durden