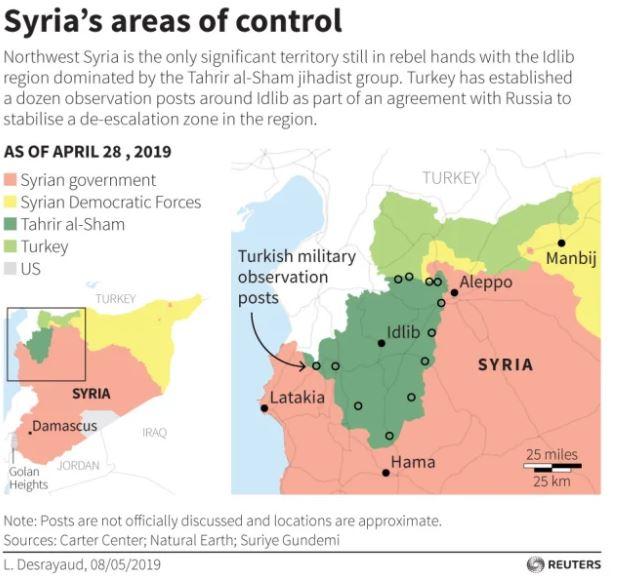

Some 500 Nusra-front militants, accompanied by seven tanks and about 30 pickup trucks armed with mounted heavy machine guns launched three major offensives against government troops in Idlib province on Wednesday, the Russian Defense Ministry said.

The counterattack focused on the town of Kafr Nabudah, which was recently captured by the Syrian government.

Militants also launched a missile attack on Russia’s Hmeymim air base on Wednesday, but nine of the missiles were shot down, and another 8 didn’t reach their target, the ministry added.

Northwest Syria, which runs along Syria’s border with Turkey, is home to the last remaining rebel strongholds, including a swath of land dominated by the Al Qaeda-linekd Nusra Front, which has adopted a new name, Tahrir al-Sham, Haaretz reports.

The increase in shelling in the region has led to the displacement of 180,000 people, while the increase in shelling marked the most intense period of fighting between Bashar al-Assad and the rebels

According to RT, more than 150 rebels were killed during the morning offensive. Three tanks were destroyed, while 24 trucks mounted with heavy guns were also destroyed in the fighting.

via ZeroHedge News http://bit.ly/2HwFowk Tyler Durden

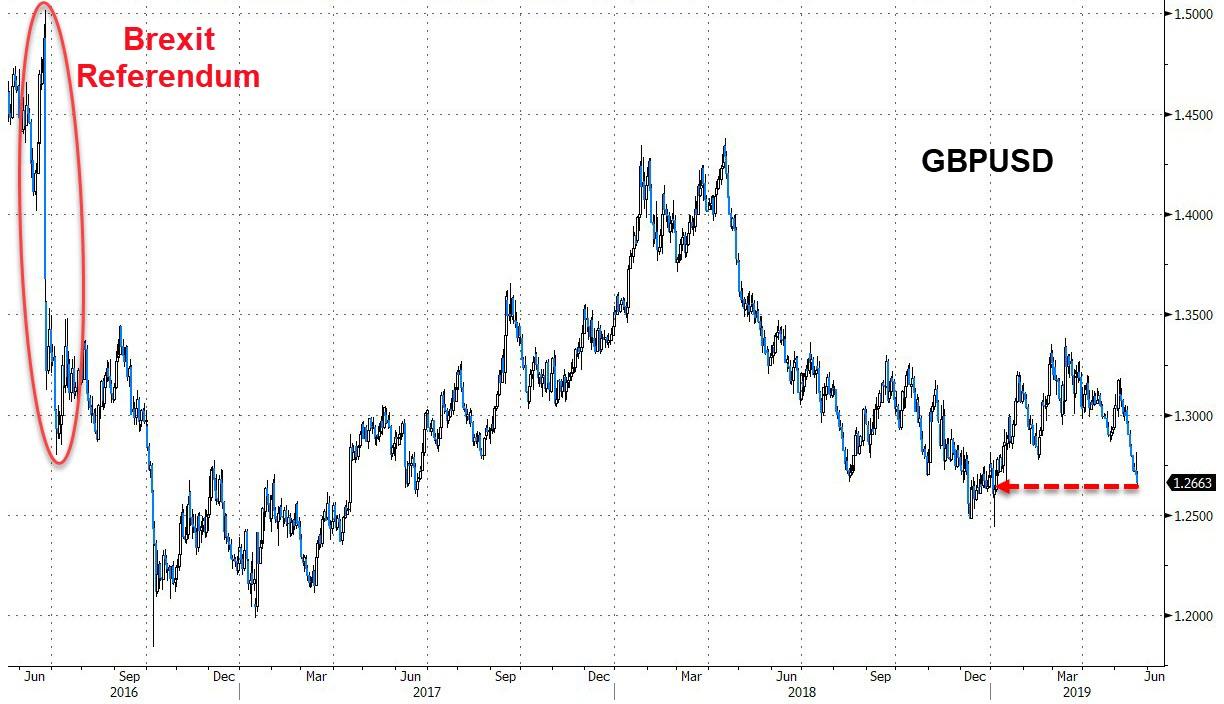

Cable has plunged almost 2 full handles from the post-May-‘New Deal’ hope of yesterday afternoon as it’s increasingly clear her latest and last gambit is dead on arrival…

Bloomberg reports that Theresa May is facing pressure to abandon her Brexit deal and quit as British prime minister within days, according to people familiar with the matter. Several senior government officials said they were shocked that the premier’s new offer intended to win votes in Parliament for her European Union divorce agreement had been so badly received so quickly.

Which just goes to show how disconnected from reality they are. FX traders, however, were not surprised…

Dragging sterling to its weakest level of 2019…

Early year hopes of avoiding a hard Brexit are dashed by the combination of May’s failure and the rising euroskeptic sentiment across Britain (and Europe).

As Mike Shedlock notes,Nigel Farage’s Brexit Party is on a stunning roll. That’s what happens when you take a firm position the public favors.

The final YouGov poll on the European Parliament elections for the UK is in.

She tried to reach out to everyone at the same, offending everyone. May has changed her tune so many times, who the hell even knows what she wants?

The best summation I can come up with is “Any deal is better than no deal“.

Labour

Please be serious.

Jeremy Corbyn is just like Theresa May. He wants to “honor” Brexit, by not doing it.

Two Peas in a Pod

Corbyn is simultaneously for and against another referendum, just like Theresa May!

Despite how they pretend, they are in bed with each other.

Another Poll Needed

YouGov needs another poll: Who is more pathetic? Theresa May or Jeremy Corbyn?

From where I sit, it’s a close call.

* * *

Finally, as Human Events reports,Farage has pledged to field a “full 650 candidates” when Britain has its next general election. The talk behind the scenes at Brexit Party gatherings, is of what a government might look like if Farage and his band of brothers (and sisters) held the balance of power after an election.

Long-term euroskeptic and former President of the Czech Republic, Vaclav Klaus, sums things up well:

“As I look at it from Prague, the British main political parties totally failed, and betrayed and abandoned the British citizens, their own voters. It had, however, one positive side effect: by behaving in this way, they probably and unwillingly created the Brexit Party…

…Dear Brexit friends, you should in the forthcoming elections give the whole rest of Europe a good example. Many Europeans need it, and many are waiting for it. Don’t disappoint them.”

The Turkish Lira tumbled as much as 1% against the dollar, leading a decline across emerging markets…

… while Turkish stock market losses accelerated as the Borsa Istanbul 100 Index falls 1.5%, declining for a 6th day and 13 of the past 14, to touch the lowest level since January 2017, effectively entering a bear market, having tumbled 20% from the March highs.

While there wasn’t a specific event behind today’s mauling of Turkey, which to many investors has become the canary in the emerging markets coalmine, the selling picked up after Turkey said soldiers had been dispatched for training in Russia ahead of the delivery of the S-400 missile-defense system. As Defense Minister Hulusi Akar said additionally, as the deadline of S-400 system delivery looms, Turkey will send more personnel for training in the coming months.

Meanwhile, the Kremlin on Wednesday condemned as unacceptable a US ultimatum delivered to Turkey meant to force Erdogan to cancel a deal to buy Russian S-400 surface-to-air missile systems and purchase U.S. Patriot missile systems instead. According to Reuters, Moscow was responding to a CNBC report which said Washington had given Turkey just over two weeks to scrap the Russian deal and do an arms deal with the United States instead or “risk severe penalties.” More from CNBC:

Turkey has a little more than two weeks to decide whether to complete a complex arms deal with the U.S. or risk severe penalties by going through with an agreement to buy a missile system from Russia, according to multiple people familiar with the matter.

By the end of the first week of June, Turkey must cancel a multibillion-dollar deal with Russia and instead buy Raytheon’s U.S.-made Patriot missile defense system — or face removal from Lockheed Martin’s F-35 program, forfeiture of 100 promised F-35 jets, imposition of U.S. sanctions and potential blowback from NATO.

As extensively reported here previously, Ankara (which recently flipped away from Erdogan’s ruling AKP party in local elections) and Washington have been at odds on several fronts, including Ankara’s decision to buy the S-400s, which cannot be integrated into NATO systems. Washington alleges that the Russian deal, if it goes ahead, would jeopardize Turkey’s role in building Lockheed Martin F-35 fighter jets.

When asked about the CNBC report by reporters on Wednesday, Kremlin spokesman Dmitry Peskov said:

“We regard this extremely negatively. We consider such ultimatums to be unacceptable, and we are going on the many statements made by representatives of Turkey’s leadership headed by President (Tayyip) Erdogan that the S-400 deal is already complete and will be implemented.”

Turkey’s defense minister said earlier on Wednesday that Ankara was preparing for potential U.S. sanctions over its purchase of the Russian missile system even though he said there was some improvement in talks with the United States over buying F-35 fighter jets.

via ZeroHedge News http://bit.ly/2Wq7IJe Tyler Durden

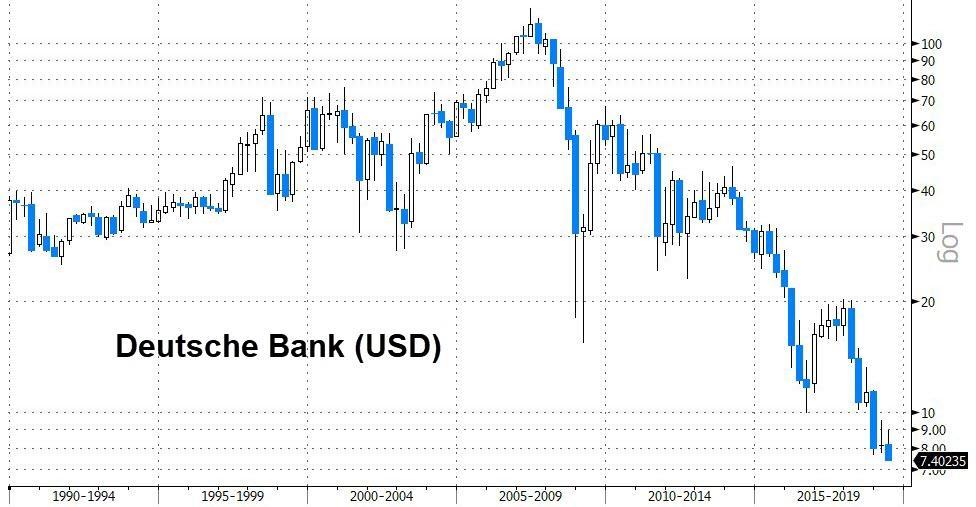

Renowned geopolitical and financial cycle expert Charles Nenner says if there was ever a global canary in the coal mine warning for the financial system, it is Germany’s Deutsche Bank (DB). Late last year, Nenner predicted if DB stock went below $8 a share, “You should be worried.” Recently, DB stock hit all-time lows and now sits around the $7.40 per share level.

Nenner warns, “I see it can hold up to late July, and then it can go to $6.50 (per share)…”

“If it breaks below $6.40, it can go out of business. So, it’s a very serious situation… I think all the markets can have a bounce in a couple of days to the end of July. That’s why DB might hold up, but if it gets below $6.40, the world is in trouble.”

This is not a hyped prediction considering the IMF called DB the “most systemically dangerous bank” in the world in 2016. If DB does break $6.40, do we get a daisy chain of default around the world? Nenner says:

“It is a very dangerous situation. I don’t think DB is the only one. They just got caught. I think if you look at the balance sheets very closely of other banks, especially Europe and Italian banks, you will see a lot of troubling signs also. I don’t think it’s only Deutsche Bank. It’s much more…

If it breaks $6.40, the downside price target is zero. If everybody watches my analysis and it does go below $6.40, everybody is going to run for the exits.”

If DB goes under with its massive book of derivatives, other banks would be in the same trouble as DB. Nenner says,

“Yes, if they have to close their derivatives, who knows which bank is going to lose how much? It’s going to be a big problem.”

On interest rates, Nenner says,

“At the end of the summer, or let’s say at the end of July, we are going to have a long term rise in interest rates for a couple of years.”

On gold, Nenner says,

“A lot of people don’t know that a lot of bull markets in gold are in a deflationary period. We are looking for a long term bull market for a couple of years to come, maybe until 2024. We are fine tuning it, but we are going to go short in the middle of the summer the bonds and go long the gold. I don’t think the weakness in stocks is going to go to the usual September, October and November time period. I think, after July, it will start to be difficult.”

Nenner thinks the stock market will bottom out in the year 2022, and the path from here is mostly down according to his cycles.

In closing, Nenner says,

“Gold prices and silver prices will go up. It’s early, and it’s better to get in early instead of when it’s exploding, and everybody knows you have to now be in gold. It’s always the clever money that is basing their money into gold stocks. The price is going much higher. Remember, my upside price target is $2,500. Right now, it is $1,270, and $2,500 is a substantial move in gold.”

Join Greg Hunter as he goes One-on-One with financial and geopolitical cycle expert Charles Nenner.

At a time when the safety of Tesla’s Autopilot driver-assistance technology is under growing scrutiny, following a former NHTSA head calling for a recall and several fatal accidents associated with Autopilot, the influential Consumer Reports has weighed in with their take on the company’s Navigate feature, a lane changing assistance feature included with the latest Autopilot update. What Consumer Reports found was that Tesla’s automated software was “far less competent than a human driver”.

Tesla’s recent Autopilot update was supposed to allow certain cars to automatically change lanes in an attempt to make driving “more seamless”. But Consumer Reports refuted the narrative, instead saying that the feature simply “doesn’t work very well and can create potential safety risks for drivers.”

The feature was added last month as part of a promised upgrade to a package of driver assist features. To use it, the driver essentially gives the car permission to make its own lane changes and can cancel an automated lane change at any time by using the turn-signal stalk, braking, or holding the steering wheel in place.

The independent test found that the Navigate feature “lagged far behind a human driver’s skill set.”

The report found that the feature cut off cars without leaving space and even passed other cars in ways that violate state laws. As a result, the driver often had to intervene and prevent the system for making poor decisions.

Jake Fisher, Consumer Reports’ senior director of auto testing slammed the technology:

“The system’s role should be to help the driver, but the way this technology is deployed, it’s the other way around. It’s incredibly nearsighted. It doesn’t appear to react to brake lights or turn signals, it can’t anticipate what other drivers will do, and as a result, you constantly have to be one step ahead of it.”

CR said that multiple testers reported that the Tesla “often changed lanes in ways that a safe human driver would not—cutting too closely in front of other cars, and passing on the right.” The article also expressed concern about Tesla’s claims that three rearward-facing cameras could detect fast approaching objects.

Fisher continued: “The system has trouble responding to vehicles that approach quickly from behind. Because of this, the system will often cut off a vehicle that is going a much faster speed since it doesn’t seem to sense the oncoming car until it’s relatively close.”

Fisher also said that merging is an issue for the software: “It is reluctant to merge in heavy traffic, but when it does, it often immediately applies the brakes to create space behind the follow car—this can be a rude surprise to the vehicle you cut off.”

“In essence, the system does the easy stuff, but the human needs to intervene when things get more complicated,” Fisher continued.

From a legal standpoint, the testers also had concerns. Several testers experienced Navigate initiate a pass on the right on a two-lane divided highway, a move that could result in a ticket for an “improper pass” in some states. It also failed to return to the right-hand travel lane after making a pass several times, testers said.

Dorothy Glancy, a law professor at Santa Clara University School of Law in California who focuses on transportation and automation stressed the fact that automated driving software must be programmed to follow local laws.

She said: “One of the issues we lawyers are looking at is the obligation of autonomous vehicles to obey all traffic laws where the vehicle is being used. That can get tricky when there are variations from area to area, even within a state—for example, municipal speed limits.”

Shiv Patel, an automotive analyst at market research firm ABI Research said he believes that Tesla’s hardware is operating near full capacity: “I would say that Navigate on Autopilot would be pushing the upper limits of what could be achieved with the current computer hardware in the vehicle.”

The review then goes on to state the obvious: despite Tesla promising will have full self driving next year, their experience with Navigate suggests it will take longer.

Aside from the massive safety risks associated with Autopilot that we have been sounding the alarm on for years, could it also be that two more Elon Musk promises – self driving next year and millions of robotaxis on the road – may (gasp) wind up not materializing? While we won’t be surprised, Tesla cultists investors who still believe in Musk very well may be.

via ZeroHedge News http://bit.ly/2We9xc5 Tyler Durden

Talks to secure a government bailout have collapsed, and British Steel, the UK’s second-largest steel producer, has officially started insolvency proceedings, putting some 25,000 jobs – 5,000 workers at its Scunthorpe plant and another 20,000 along the supply chain – at risk, the FT reports.

The British High Court has ordered the compulsory liquidation of British Steel, and appointed an Official Receiver to oversee the liquidation alongside accountancy firm Ernst & Young.

The bankruptcy, which was hastened by a loss of business that the company has blamed on Brexit uncertainty, as well as a spike in iron prices (ore prices climbed above $100 a tonne on Friday, the first time they’ve closed above that level since May 2014).

Greybull, British Steel’s private equity owner, and a consortium of the firm’s lenders managed to assemble a rescue package worth £30,000 ($38,000). The only problem is the funds were contingent on a match from the UK government. But the money fell through at the last minute as ministers judged that it would violate EU rules.

The deal’s biggest proponent, Theresa May’s business secretary, Greg Clark, will now need to explain why he approved an earlier £120 million ($152 million) loan to help British Steel meet an EU environmental bill, but can’t save the company from bankruptcy.

As the FT explains in a video, the earlier bailout was required because under its previous owners, British Steel had used the EU’s system of carbon-credit trading to raise money by selling excess credits then covering its short position at the beginning of the following year.

But this year, the EU ruled that since the UK is leaving the bloc, its companies don’t deserve any more credits, leaving the company on the hook for a massive bill.

Unions in the UK have demanded that the government do something, while Labour Leader Jeremy Corbyn warned on Tuesday that the collapse of British Steel would be ‘devastating’.

Our steel industry doesn’t just provide thousands of jobs, it has a major role to play in ushering in a Green Industrial Revolution and securing a sustainable future for British manufacturing.

In a statement, Clark insisted that the government had done all it can, but that it can’t risk violating EU laws stipulating that any financial support must be made ‘on a commercial basis’

“We have shown our willingness to act, having already provided the company with a £120m bridging facility to enable it to meet its emissions trading compliance costs,” he said. “The government can only act within the law, which requires any financial support to a steel company to be on a commercial basis. I have been advised that it would be unlawful to provide a guarantee or loan on the terms of any proposals that the company or any other party has made.”

If the company goes under, it’s unclear what will happen to its Scunthorpe plant, or the thousands of jobs there. But it certainly raises questions about who benefits, and who suffers, thanks to unmitigated free trade. By imposing tariffs on imported steel and aluminum, Trump has sought to spare American steel companies a similar fate.

via ZeroHedge News http://bit.ly/2HurLOi Tyler Durden

S&P futures were lower on Wednesday as investors sought safety in bonds, the Japanese yen and Swiss franc in muted trade amid renewed worries over the U.S.-China spat after reports Washington is considering cutting off the flow of American technology to as many as five Chinese companies including Hangzhou Hikvision Digital Technology, the world’s largest supplier of video surveillance products, expanding the US crackdown on China beyond Huawei to include world leaders in video surveillance. The dollar and 10Y yield were unchanged ahead of today’s FOMC Minutes.

Tuesday’s brief relief over Washington’s temporary relaxation of curbs against Huawei evaporated after reports that the White House is considering further sanctions on Chinese video surveillance firm Hikvision. As Reuters notes, fears of another blacklisting reinforced worries that U.S. President Donald Trump is looking beyond sealing a trade deal with China to a potentially bigger battle aimed at curbing Beijing’s technology ambitions.

“I think the debate is just starting about what the implications of all this could be if it escalates. It’s my biggest concern,” said Simon Webber, lead portfolio manager on the global & international equities team at Schroders. “If we get retaliation, if we start deconstructing supply chains, if we get countries asking whether they can rely on products and services overseas, then we’ll have much more uncertainty and a much more worrying environment,” said Webber.

Despite the return of trade fears, Europe’s Stoxx 600 reversed earlier losses as technology and personal-goods shares advanced, after earlier declining with Chinese equities amid fears of a new front in the trade war. Qualcomm tumbled after a the company lost a landmark anti-trust case, wiping out half of the company’s post-AAPL settlement gains.

Asian stocks edged modestly higher, led by utility and technology firms, after falling on Tuesday. Markets in the region were mixed, with India climbing and Japan slipping, its Topix gauge down 0.3%, driven by Takeda and Keyence. China’s Shanghai Composite also retreated 0.5%, with Kweichow Moutai and PetroChina among the biggest drags. The S&P BSE Sensex Index rose 0.7%, as large financial firms contributed the most to the rally. The latest Trump threat dampened Australia’s post-election optimism slightly, but stocks still hovered near the 11-year highs scaled on Monday. Australia’s stocks index is the only major global bourse to notch up gains since Trump ramped up his battle with Beijing on May 6, largely due to the election euphoria, while South Korea’s KOSPI is the biggest loser.

“Some in the markets will continue to cling on to hopes of the United States and China reaching an agreement at the upcoming G20 meeting,” said Masahiro Ichikawa, senior strategist at Sumitomo Mitsui DS Asset Management. “But the ongoing trade conflict looks to be a protracted one, and its potentially negative impact on various economies is becoming a running concern.”

As Bloomberg notes, stock and bond markets have been fluctuating as investors try to size up how much damage the trade war will bring to global economic growth and supply chains, while the Trump administration considers adding video equipment to its growing blacklist of sales to China. With traders in wait-and-see mode, the VIX has been retreating and on Tuesday touched its lowest level in almost three weeks.

“There is a broad expectation for a growth slowdown and the trade tensions are really adding to these kinds of worries,” Jingyi Pan, Singapore-based market strategist at IG Ltd., told Bloomberg TV. “A lot of this may not have followed through to the economic data.”

In FX, amid a modest risk-off sentiment, investors sought havens in the Swiss franc, Japanese yen and German government bonds. The yen strengthened away from two-week lows against the dollar, rising 0.1% to 110.39 yen, while the Swiss franc was higher against the euro and the dollar. Moves across all financial markets were largely muted, though, as many investors preferred to keep to the sidelines. The standout was the pound, which was down 0.2% at $1.2650, its lowest since January amid a deepening crisis over the UK’s exit from the EU after Prime Minister Theresa May’s final gambit failed dramatically.

In emerging markets, stocks extended their advance from the lowest level since January and currencies climbed as traders wait for minutes of the Federal Reserve’s last policy meeting. Russia’s ruble climbed the most among peers and bond yields fell before a regular weekly debt sale. The rand erased early declines after Deputy President David Mabuza asked for his swearing-in as lawmaker to be postponed in what’s seen as President Cyril Ramaphosa making good on promises to clean up his government. South Korea’s won also reversed losses after authorities warned traders that the currency’s recent decline is excessive. They will hold an emergency meeting to discuss the won’s weakness. With the market focusing on Fed minutes, Credit Agricole strategist Dariusz Kowalczyk remains “cautious about EM exposure given that, while most negative news on the U.S.–China front is out, the trajectory of the relationship remains negative and it is difficult to see an offsetting global factor.”

Meanwhile, the Turkish lira languished at the other end of the spectrum, posting the biggest drop among a handful of decliners, as tension between the U.S. and Turkey showed no sign of abating. The currency is also is paying the price for its pre-election efforts to tinker with the markets.

In overnight geopolitics, US state Department said it is seeing signs Syria could be renewing its use of chemical weapons including alleged chlorine attack on May 19th, while it added that US and its allies will respond quickly and appropriately if Syria government uses chemical weapons. Meanwhile, Saudi Arabia’s Cabinet said the country will do what it can to avoid any war following the condemnation of Iranian actions in the region, while it affirmed commitment to achieving balance in oil market and working towards its stability.

The main event on today’s calendar are the FOMC minutes from the most recent Federal Reserve policy meeting. In a Bloomberg interview, St. Louis Fed president and uber dove, James Bullard, said the central bank may have “slightly overdone it” by raising interest rates in December, though it’s premature to talk about a rate cut. Maybe in another 100 points lower in the S&P it won’t be that premature.

In commodities, WTI futures were down 0.6% at $62.567 per barrel after API data showed that U.S. crude stockpiles rose unexpectedly last week. Oil was also pressured by Saudi Arabia reiterating that it would aim to keep the market balanced and try to reduce tensions in the Middle East.

Expected economic releases include mortgage applications and FOMC minutes. Analog Devices, CIBC, Lowe’s, and Target are among companies reporting earnings.

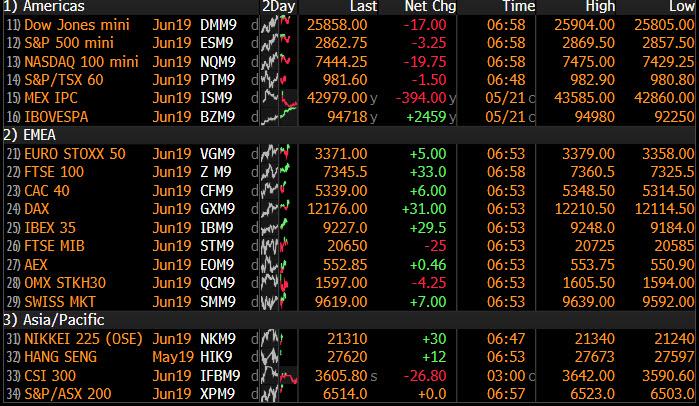

Market Snapshot

S&P 500 futures down 0.2% to 2,861.00

STOXX Europe 600 down 0.03% to 379.40

MXAP up 0.1% to 154.00

MXAPJ up 0.2% to 505.31

Nikkei up 0.05% to 21,283.37

Topix down 0.3% to 1,546.21

Hang Seng Index up 0.2% to 27,705.94

Shanghai Composite down 0.5% to 2,891.71

Sensex up 0.6% to 39,220.90

Australia S&P/ASX 200 up 0.2% to 6,510.71

Kospi up 0.2% to 2,064.86

German 10Y yield fell 1.1 bps to -0.074%

Euro up 0.02% to $1.1163

Italian 10Y yield fell 5.6 bps to 2.271%

Spanish 10Y yield fell 0.8 bps to 0.866%

Brent futures down 0.7% to $71.71/bbl

Gold spot little changed at $1,274.45

U.S. Dollar Index little changed at 98.02

Top Overnight News from Bloomberg

The U.S. is considering cutting off the flow of vital American technology to as many as five Chinese companies including Hangzhou Hikvision Digital Technology Co., widening the dragnet beyond Huawei to include world leaders in video surveillance

U.S. central bankers may have “slightly overdone it” by raising interest rates in December, though it’s premature to talk about a rate cut, said Federal Reserve Bank of St. Louis President James Bullard

Theresa May is facing pressure to abandon her Brexit deal and quit as British prime minister within days, according to people familiar with the matter. Several senior government officials said they were shocked that the premier’s new offer intended to win votes in Parliament for her deal had been so badly received so quickly

South Korea became the latest Asian central bank to step up defense of its currency as the U.S.-China trade war took a toll after it warned traders that the won’s recent decline is excessive

Asian equity markets were indecisive as the momentum from Wall St, where all majors gained as Huawei’s reprieve inspired the trade sensitive sectors, somewhat dissipated as markets await the next developments in the US-China trade saga and upcoming FOMC minutes. ASX 200 (+0.2%) and Nikkei 225 (U/C) were mixed for most the session with Australia subdued by weakness in mining related stocks as well as financials, while the Japanese benchmark was kept afloat by recent currency weakness and after varied data releases including better than expected Machine Orders. Hang Seng (+0.2%) and Shanghai Comp. (-0.5%) diverged with the mainland cautious amid ongoing trade uncertainty and with Hangzhou Hikvision heavily pressured after reports that the Trump administration is considering restrictions on the Co. This has also weighed on other tech names, although losses in the broader market were stemmed after a liquidity injection by the PBoC and with the central bank seeking to further reduce borrowing costs for small businesses. Finally, 10yr JGBs initially softened amid gains in Japanese stocks and with participants sidelined ahead of a 20yr auction later, although prices then recovered on strong auction results in which the b/c rose to its highest on record.

Top Asian News

Citic, Baidu Are Said to Seek Up to $1 Billion for Online Bank

Asia’s Worst Currency Is in Taiwan as Foreign Funds Depart

Korea Warns Currency Traders as Won’s Sudden Decline Takes Toll

Turkey Burns Bridges With Markets as Costs of Lira Defense Mount

Choppy trade for European indices [Eurostoxx 50 +0.3%] following on from an indecisive Asia-Pac session as the region awaits further impetus in regard to trade talks ahead of tonight’s FOMC Minutes. European equities are now mostly higher as equities gained traction ahead of US’ market entrance. UK’s FTSE 100 (+0.5%) outperforms its peers as exporters are bolstered by the Brexit-dented Pound. Sectors are posting broad-based gains, whilst energy stocks bear the brunt of the falling prices in the complex. In terms of individual movers, Royal Mail (+6.2%) spiked higher on the back of optimistic earnings coupled with a dividend cut to fund a turnaround, whilst Spanish listed DIA (+5.4%) continues to benefit from Santander’s care package, which was announced yesterday. Meanwhile, Babcock (-8.4%) shares plummeted after the Co. noted that the upcoming FY earnings are to be impacted by a number of significant factors. Looking at analysis from Nomura Quant, the report notes that CTAs have dissolved long positions in a majority of regions and are now roughly neutral in the FTSE 100, Nikkei 225, Hang Seng and TAIEX, with bearish positions limited to the KOSPI and TOPIX, albeit bullish stances are ongoing for the DAX and NIFTY 50. Apart for the DAX, CTAs have a low equity exposure, “so the risk of a drop in share prices from systematic cutting of existing long positions looks limited” says Nomura.

Top European News

Merkel Was Lobbied for a Top EU Job at Romanian Summit in May

UBS Is Poised to Settle Tax Case With Italy for $110 Million

U.K. Inflation Climbs Above Target on Energy Costs, Air Fares

Draghi Says Euro Zone Must Overcome Impasse on Risk Sharing

In FX, the Sterling’s slump continues, with Cable breaching another technically significant level at 1.2670 after a 360°-plus turnaround from 1.2800+ knee-jerk highs on Tuesday when UK PM May unveiled her new Brexit blueprint with the carrots of a 2nd referendum and temporary EU customs union, while Eur/Gbp has now surpassed strong chart resistance ahead of 0.8800 in the form of the 200 DMA (0.8793) on the way to a 0.8815 high and the cross is on course to extend a run of consecutive rallies to 13 sessions. The marked turnaround in sentiment comes amidst widespread uproar over the latest WA proposal and even more rebellion against the PM, especially from the 1922 faction that is set to meet at 4 pm and could launch a confidence vote as soon as today. Back to the pilloried Pound, 1.2650 could offer symbolic support vs the Dollar ahead of a Fib at 1.2638, if option expiry interest between 1.2665-70 in 500 mn fails to stem the tide, while 0.8840 may cap losses against the single currency. Note, UK inflation data has been largely ignored, but for the record CPI was slightly softer than forecast and PPI input prices well below consensus.

DXY – The index remains toppy above 98.000 after several attempts and failures to clear chart hurdles ahead of the 2019 highs, with the Greenback sitting tight and rangebound vs G10 counterparts in advance of the FOMC minutes, bar Sterling as noted above.

AUD/CAD/NZD – The non-US Dollars have clawed back some of their recent losses with the Aussie back within touching distance of 0.6900, Kiwi pivoting 0.6500 and Loonie straddling 1.3400. All eyes on the aforementioned account of the Fed’s recent policy meet, but Canadian retail sales data could provide the Cad with some independent impetus beforehand.

CHF/EUR/JPY – All treading water vs the Usd as the Franc hovers just above 1.0100 and Euro trades mostly above 1.1150 following yesterday’s brief probe below, but the topside capped ahead of decent expiries at 1.1180 (1.5 bn). Meanwhile, the Yen is meandering between 110.37-62 after reported offers from Japanese corporates and asset managers, and with Fib resistance noted at 110.71 also keeping the headline pair contained.

EM – The Rand is on the rebound regardless of softer than anticipated SA inflation data, with Usd/Zar near the bottom end of a 14.4400-3500 range ahead of Thursday’s SARB policy meeting amidst perceptions that the tone will remain hawkish even though there are grounds for a reassessment of projections signalling a hike by the end of 2019. Conversely, the Lira is still struggling and testing support at 6.1000 vs the Buck amidst reports that Russia and Turkey are ready to fulfil S-400 order commitments irrespective of US protestations.

In commodities, WTI and Brent futures are on the backfoot after the API reported a surprise build in US crude inventories (+2.4mln vs. Exp. -0.6mln), marking a 5th consecutive week of builds reported by the institute. Brent futures current reside below the USD 71.50/bbl level whilst WTI futures fluctuates on either side of USD 62.50 with PVM highlighting “critical” support levels at 62.54 and 62.31 which, if breached, could cause a decline in prices towards the 61.63/22 area, according to the analysts. Participants will be looking ahead to the more widely looked at EIA crude inventory report with headline crude stocks expected to decline by just over 2.5mln barrel. Elsewhere, precious metals are relatively tentative and awaiting any US/China update ahead of the FOMC Minutes release later today (preview available in the Research Suite). Meanwhile, copper prices are sliding as the Buck gains more ground against a backdrop of a trade war between the world’s two largest economies. Despite this, mining giant Antofagasta expects the copper market to tighten this year and note a positive outlook for the red metal in 2019 and beyond. Spot copper declined through USD 2.7/lb to touch levels last seen in late January.

US Event Calendar

10am: Fed’s Williams Hosts Economic Press Briefing

10:10am: Fed’s Bostic Makes Opening Remarks at Dallas Fed Conference

2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

While the direction of travel for the trade negotiations still feels decidedly negative in the medium-term, markets had their fourth up day in six yesterday. Momentum was helped by news that the Commerce Department has granted a relief period for certain US broadband companies and wireless customers using Huawei equipment. The NASDAQ recouped +1.08% and about two-thirds of Monday’s decline, while the semi-conductor index rose +2.13% – and therefore retraced about half of Monday’s decline. The S&P 500 and DOW also rose +0.86% and +0.77%, respectively, despite retail names struggling following some disappointing results out of Kohl’s (-12.36%) and JC Penney (-7.39%) with both citing the trade spat as a problem for their business.

The move for the wider equity markets saw the VIX fall back below 15 (-1.4pts) though and back to the lowest since May 3rd – the last business day before Mr Trump’s out of the blue first Trade escalation Tweet. It was a broadly similar story in Europe where the STOXX 600 rose +0.47% and the DAX +0.78%. In credit HY spreads were 3-4bps tighter in the US and Europe while in bond markets we saw 10y Bunds touch the lofty heights of -0.063% (+2.3bps) and Treasuries hit 2.426% (+1.1bps). The 2s10s curve did however fall -2.4bps to 16.8bps as the front-end sold off a little more. In commodities gold pulled back -0.25% while a better day for risk also helped EM equities and FX to climb +1.27% and +0.19% respectively.

On the trade front, things were relatively calm yesterday but is again dominating the headlines this morning. The CNH did strengthen yesterday for a second consecutive session for the first time since before the recent trade fracas erupted. While the US’s 90-day reprieve for Huawei was positive, it was noteworthy that President Trump directly linked the Huawei decisions with trade policy, saying that he deferred an initial decision until the trade talks stalled. Chinese state-media editor Hu Xijin said on twitter that the US’s “irrational behaviors” are making Chinese policymakers “wonder if Washington is in a rush to reach a trade deal. Conclusion of the Chinese: drag it out. Americans are about to have a nervous breakdown.” While the market largely ignored the comments, the rhetoric certainly isn’t calming down.

Overnight the New York Times reported that the Trump administration was considering curtailing the flow of American technology to China’s top maker of video surveillance gear, Hikvision. The stock fell as much -9.6% before recovering to trade -4.4% lower. Bloomberg reported that the Trump administration is also considering blacklisting Zhejiang Dahua Technology Co. The stock traded down as much as -8.9% before recovering to trade -4.8% lower.

Markets are largely up in Asia though with the Nikkei (+0.22%), Hang Seng (+0.30%) and Kospi (+0.31%) all up while Chinese markets are trading flattish with the CSI (+0.05%), Shanghai Comp (-0.02%) and Shenzhen Comp (-0.04%). Elsewhere, futures on the S&P 500 are also trading flat (+0.05%) and the Chinese onshore yuan is down -0.11% to 6.9096. In terms of overnight data releases, Japan’s adjusted April trade balance came at -JPY 110.9bn (vs. -JPY 37.5bn expected) as exports declined (at -2.4% yoy vs. -1.6% yoy expected) while imports jumped (at +6.4% yoy vs. +4.5% yoy expected). Overnight BoJ board member Yutaka Harada, a consistent dissenter on BoJ policy, said that a sales tax rise set for October could tip the economy into recession and weigh on prices, delaying progress toward the central bank’s 2% inflation target.

There was volatility in the pound yesterday as Prime Minister May presented a fourth, and likely final, gambit to get her WA deal passed, and the reaction was not positive. The pound initially rallied as much as +0.69% on the pre-speech headlines (especially around potential 2nd referendum language), but it ultimately retraced to end -0.19% weaker after the adverse reaction by MPs became clear.Her ten-point plan included a new provision to let Parliament vote for the option of a second referendum if they backed her deal first, which was a new concession. Though she added some new language about the Irish border, a potential vote on a new customs agreement and lots of other details, her core deal was basically unchanged. The move comes ahead of the week of June 3, effectively making this maneuver the last opportunity for May to reach a solution. The parliamentary math is pretty straightforward in that May needs to gain support from at least a portion of Labour MPs while retaining the backing of her Conservative caucus. As it turned out, we later found out that she has so far failed to get Labour’s support and has lost the backing of many within the Tory party. Jeremy Corbyn came out directly against the proposal and several prominent Tory MPs who supported the WA previously came out in opposition to it. Meanwhile, The Sun has reported overnight that senior backbenchers on the Tory 1922 committee’s executive will mount new bid to force a confidence vote in PM May. Bloomberg also reported overnight that PM May is facing pressure to abandon her Brexit deal and quit as British prime minister within days.

Looking forward, DB’s Oliver Harvey remains pessimistic on the pound. His latest update ( here ) was published before yesterday’s news, but still outlines the likely avenues moving forward. If anything, the latest developments reinforce his bearish bias. Any more negative responses to the new proposed deal and Prime Minister May could resign as soon as this week and attention will shift to the likely Conservative leader contest. That will probably yield a hard-Brexit supporting PM, which in turn will incrementally raise the odds of a hard Brexit. Separately, Chancellor Hammond spoke at the CBI’s (a business lobby) annual dinner last night, where he warned against a no-deal Brexit. He also focused on fiscal responsibility, possibly with an eye toward influencing a potential incoming leadership team, saying “we must not undo a decade of hard work (and must) resist the ever-present temptation to write checks the country cannot afford.”

Three regional Fed presidents spoke publicly yesterday, but the only truly interesting remark came from Boston Fed President Rosengren, who said that an average inflation targeting regime “would not change the Fed’s inflation target over the cycle.” That’s the latest comment in tacit support of an average inflation targeting regime, though the bar for the Fed to radically change policy at its upcoming policy review is high. Rosengren’s comment was especially interesting since he is one of the more hawkish members of the committee. Away from that, his comments repeated the Fed’s recent mantra about transitory inflation, there being no need to change policy, and for inflation to gradually return to the 2% target over time. Chicago Fed President Evans and Atlanta Fed President Bostic mostly delivered similar remarks. Elsewhere, Fed’s Bullard (voter) said overnight that the US policy makers may have “slightly overdone it” by raising interest rates in December, while adding that it’s premature to talk about a rate cut. However, he flagged the idea that “a quarter point in an environment where the U.S. economy is surprising to the upside again in 2019 …. would probably send a signal that we are serious about hitting the 2% inflation target”. On the US-China trade war he said that “For this to actually affect Fed policy, these tariffs would have to stay on for quite a while, something like six months; at the end of six months if there was still no prospect of a resolution then I think that is the point it would start to weigh on Fed policy.”

Staying with the Fed, this evening we’ll get the FOMC minutes from the meeting earlier this month. Usually there would be a reasonable amount of focus on the minutes however, given the trade developments since then it’s likely that the they will be somewhat discounted as being stale. That being said the inflation debate will still be relevant and as a reminder Powell noted that several “transitory” factors had been weighing on inflation of late. Our US economists noted that subsequent Fedspeak since Powell’s press conference suggest that there is a solid contingent of officials that agree with this cut of the data, though some find persistently below target inflation as troublesome, regardless of the causes. Therefore, it will be interesting to see how the debate plays out, especially in light of concerns around inflation expectations and the Fed’s policy framework review.

In other news, it was another quiet day for data releases yesterday. In the US existing home sales in April were reported as declining -0.4% mom compared to expectations for a +2.7% rise. In Europe consumer confidence improved 0.8pts to -6.5 in May – however it wasn’t clear if this captured the trade escalation period – while in the UK the May CBI survey showed weakness in both domestic and export orders, as well as subdued inflationary pressures.

Looking at the day ahead now, this morning we’ll get the April inflation data docket in the UK where the consensus expects a small increase in the annual core CPI reading from +1.8% to +1.9% yoy. We’ll also get the March house price index reading for the UK along with April public sector net borrowing data. In the US it’s quiet until we get to the FOMC meeting minutes this evening. Away from that we’re also expecting comments from the Fed’s Williams and Barker this afternoon, while the ECB’s Draghi, Visco and Praet are all due to speak this morning. Draghi is making the welcome address at the ECB colloquium in honour of Peter Praet so it’s unlikely that we’ll get anything particularly market moving.

via ZeroHedge News http://bit.ly/2HvIzVa Tyler Durden

Just weeks after Qualcomm secured a clear victory in its long-running legal battle with Apple, sending the chipmaker’s shares rocketing higher, a federal judge in San Jose ruled against the company in a high-profile anti-trust lawsuit that could seriously disrupt Qualcomm’s business model.

The decision sent Qualcomm shares plunging as much as 11% in premarket trade, erasing half of its gains from the Apple settlement.

The decision sided with the FTC, which initially sued Qualcomm back in January 2017. Released late Tuesday, the decision, handed down by US District Judge Lucy Koh, found Qualcomm violated anti-trust laws by charging unreasonably high royalties for its patents. Koh challenged the company’s practice of collecting chip royalties based on a smartphone’s price, according to WSJ.

The judge ruled that Qualcomm’s licensing practices had “strangled competition” in “key parts” of the chip market.

President Trump’s decision to add Huawei to a US ‘blacklist’ hammered chip stocks earlier in the week. More bad news was the last thing Qualcomm investors needed.

via ZeroHedge News http://bit.ly/2Qg0RMD Tyler Durden

China’s telecom giant was greeted with more bad news on Wednesady, when Britain’s largest cell phone operators pulled Huawei phones from their 5G networks, joining other global telecoms groups in dropping launch plans after the Chinese group was hit by a US export ban that could stop it using Google’s Android operating system.

As the FT first reported, EE, part of British Telecom, had planned to offer Huawei phones as part of its launch on Wednesday of the UK’s first 5G network, but reportedly decided to “pause” this due to uncertainty over whether they could use Android software developed by Google after the Chinese group was included on a blacklist that forbids US companies to supply it with technology, a spokesman for the carrier said.

Marc Allera, chief executive of EE, said the company had “paused” the launch of Huawei’s 5G phones because it did not have the “surety of service” it needed to offer long-term contracts. “We’ve had to hold that back,” he said.

Despite the launch snub, BT will still rely on Huawei, the world’s largest provider of networking gear and No. 2 smartphone vendor, as it’s supplying much of the infrastructure for the new network, alongside Finnish equipment vendor Nokia Oyj.

Allera said EE has tested its 5G network using Huawei technology and has had “no indications” from the UK government to change course. He said the supply chain restrictions were a concern but that the UK would not benefit from a lengthy delay to 5G launches while the situation is being resolved.

“There are so many scenarios and we don’t have any clarity. But we can’t stand still,” he said. “Nothing is crystal clear but we have to work within that ambiguity.”

At the same, UK’s Vodafone also said it would suspend Huawei’s Mate X phone from its 5G line-up. Vodafone had planned to launch the handset in the summer on its 5G network, but a spokesman said on Wednesday that “Huawei’s 5G handset is yet to receive the necessary certifications”.

Vodafone is suspending Huawei’s Mate X phone from its 5G line-up.

Separately, the FT reported that two of Japan’s largest mobile phone carriers also said they would delay the launch of a new smartphone by Huawei as global mobile operators scrambled to deal with the proposed US export restrictions on the Chinese telecoms equipment maker. The decision on Wednesday by SoftBank and KDDI will affect the Huawei P30 Lite smartphone, which was due to go on sale in Japan on Friday. NTT DoCoMo, Japan’s largest carrier, said it was also considering cancelling pre-orders for the Huawei handset.

Ironically, the escalating crackdown against Huawei products has overshadowed the launch of UK’s 5G services as networks have lobbied the government not to ban the Chinese company from 5G network builds. Until today’s reversal, EE scrambled to be the first to launch 5G networks against Vodafone which goes live in July. EE will charge a premium for the faster network of about £5 and has partnered with Google and Niantic, the company behind Pokémon Go which has developed a Harry Potter-themed game, for the launch.

Even more ironically, today’s 5G launch isn’t really a 5G launch – the real think will have to wait about 3 years. The initial UK version of 5G will be the equivalent of an enhanced 4G network offering speeds 10 times faster than today’s smartphones. Its full 5G network will be launched in 2022 with ultra-low latency services available in 2023.

BT’s 5G service will be available across the U.K.’s six biggest cities from May 30 and will reach 16 urban areas by year-end, Allera said. Customers could buy 5G subscription plans and pre-order 5G-enabled devices from Wednesday morning. BT will still offer a 5G home router from Huawei, according to slides shown at the launch.

EE’s Allera said the launch of 4G paved the way for the rise of Netflix and Uber and 5G could have a wider effect. “We take it for granted now but it changed our behavior. So what new services will rise on this new network? We don’t know, but our job is to build that network,” he said.

According to Bloomberg, EE was the first U.K. operator to offer 4G in 2012 and used Huawei gear to build the core of that network. Growing pressure on US allies to restrict Huawei forced carriers to review their ties to the company and devise back-up plans in case of bans or supply disruptions. Huawei executives have repeatedly denied its systems are vulnerable to espionage even though they have since vowed to “safeguard” their systems against backdoor spying, effectively confirming that the Trump admin’s skepticism is justified.

via ZeroHedge News http://bit.ly/2JVuFwV Tyler Durden

A crypto startup backed by legendary VCs Peter Thiel, Alan Howard and Louis Bacon is buying back shares from its seed investors in a round of ‘share buybacks’ that will massively inflate its valuation – at least on paper.

Block.one, a crypto startup that raised $4 billion during one of the most successful ICOs in history, has decided to pay back (some might say pay off) its earliest investors by buying back their shares – initially purchased for about $22.50 – for $1,500. That’s a staggering 6,567% return, spread across two years. By comparison, bitcoin climbed 1,900% between the beginning of 2017 and its peak in December.

While it once promised to build a new ‘secure’ version of the Internet, Block.one hasn’t done much with its massive mountain of capital. Aside from a few venture investments, the company has invested the bulk of its capital in Treasury bonds and a portfolio of cryptocurrencies.

Peter Thiel

Block’s founders insist that the money is being put to good use. The company is building out its new ‘secure’ version of the Internet, as well as a social media product that the company plans to release in June. The company has also made $174 million in venture investments, a fraction of the $1 billion in investments it has pledged to make.

Still, critics have accused CEO Brendan Blumer of creating a vehicle to ‘hoover up’ investors’ money’.

“They designed a very clever mechanism to hoover up as much capital as possible,” said Richard Burton, San Francisco-based founder of Balance.io, a blockchain company that designs applications for open source financial products. “Bitcoin was started on a shoestring and Ethereum raised just a few million dollars, which goes to show you don’t need anything like the money Block.one raised to launch and scale a successful network. It should be beholden on them to explain why they needed that much and what they are doing with it.”

So as Blumer tries to defend his reputation, he has apparently hit on the strategy of a stock ‘buyback’ that will value the company at $2.3 billion, up from a $40 million valuation from its 2017 seed round.

Block has tried to portray the buyback as a bid for legitimacy, but there are some who aren’t convinced.

“A private buyback of this sort signals to me that the company believes that there are few growth opportunities in sight, or badly wants to consolidate ownership and avoid outside scrutiny,” said Nic Carter, a partner who focuses on blockchain at investment firm Castle Island Ventures in Boston. It has not invested in Block.One or EOS tokens.

We wonder: Will ‘share buybacks’ or ‘token buybacks’ become a sign that high-flying ICOs that raised hundreds of millions, or billions, off the strength of a white paper and a convincing pitch have given up on their ambitions? Unfortunately for those who bought in during the token sales, not everybody can receive a payout at a massive premium. If anyone walks away with a profit, it will be the biggest valley players who bought in on the best terms.

via ZeroHedge News http://bit.ly/2VV8Jtj Tyler Durden

{kind=link}