The revolving door between politics and Wall Street continues as former Chicago mayor and longtime Democratic operative Rahm Emanuel will join boutique investment bank Centerview Partners LLC.

As The Wall Street Journal reports, Mr. Emanuel, who left office last month, will open a Chicago office for Centerview and advise clients on merger deals and other matters, he said in a joint interview Wednesday with Centerview co-founders Blair Effron and Robert Pruzan.

“Our job is to help clients make big decisions,” Mr. Pruzan said. “Rahm has spent his career in the room where big decisions are being made.”

“Rahm’s leadership and vast experience providing strategic advice, coupled with a track record of successful planning and execution, will bring tremendous value to our firm and our clients. Establishing a presence in Chicago is a logical next step for Centerview as we continue to grow, and it positions us to better serve existing and new clients throughout the Midwest.”

Mr. Emanuel said:

“I am excited to use my lifelong experience as an advisor and problem solver in both the public and private sectors in this next chapter of my career, and thrilled to be joining Centerview Partners – a pre-eminent firm that advises leading global companies,” “I know the Centerview team well and look forward to working with an accomplished and respected group to provide clients in the Midwest, nationally and around the world with trusted, independent advice.”

Mr. Emanuel has had an extensive career in public service, most recently as Mayor of Chicago for two terms beginning in 2011, during which time he oversaw increased economic development that has revitalized the city, expanded the public education system, and improved public parks, amenities, transit and other infrastructure projects. He previously served as Chief of Staff to President Obama, where he helped secure the passage of landmark legislation, including the unprecedented stimulus package that ushered the country through the great recession and the passage of the Affordable Care Act. From 2003 to 2009, Mr. Emanuel served in the U.S. House of Representatives, where he held a number of leadership positions, including Democratic Congressional Campaign Committee chairman and Democratic Caucus chairman. Mr. Emanuel served as director of the finance committee of Bill Clinton’s 1992 presidential campaign and later as Assistant to the President for political affairs and Senior Advisor for policy and strategy.

And now its time to really cash in…

“Never let a lost election go to waste…”

via ZeroHedge News http://bit.ly/2ZeYVHP Tyler Durden

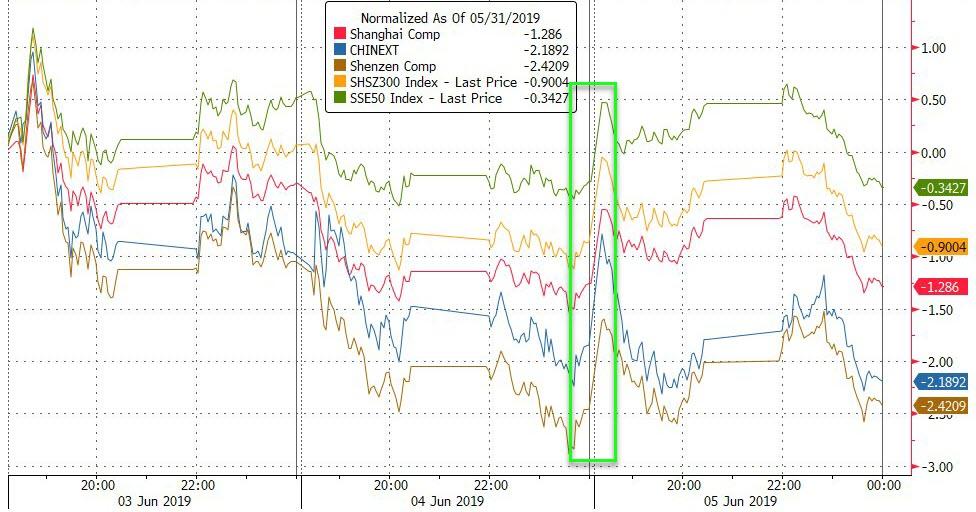

Weak China PMI was greeted with a buying panic early on but by the close, Chinese stocks were lower on the day (with the tech-heavy indices leading the drop)…

European stocks finally slowed their manic buying spree (but ended higher)…

US equity markets extended yesterday’s gains…Trannies – green – continue to lead the week (Nasdaq – blue – flatlined from the gap open today)…

But Small Caps closed red…

As the short-squeeze seems to be running out of juice…

Today’s gains were dominated by Defensive stocks, with Cyclicals notably underperforming…

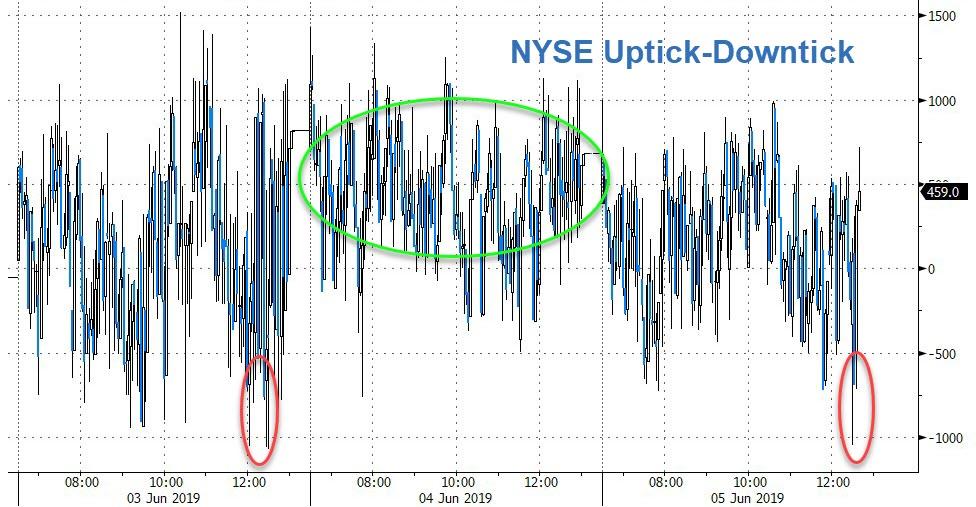

Stocks saw a notable sell program hit around 3pmET (same as we saw Monday)…

BUT as one comic noted, for the third day in a row, stocks are suddenly cheaper in the last 10 minutes of trading as stocks went vertical once again. Dow futures are up almost 900 points from Sunday night lows…

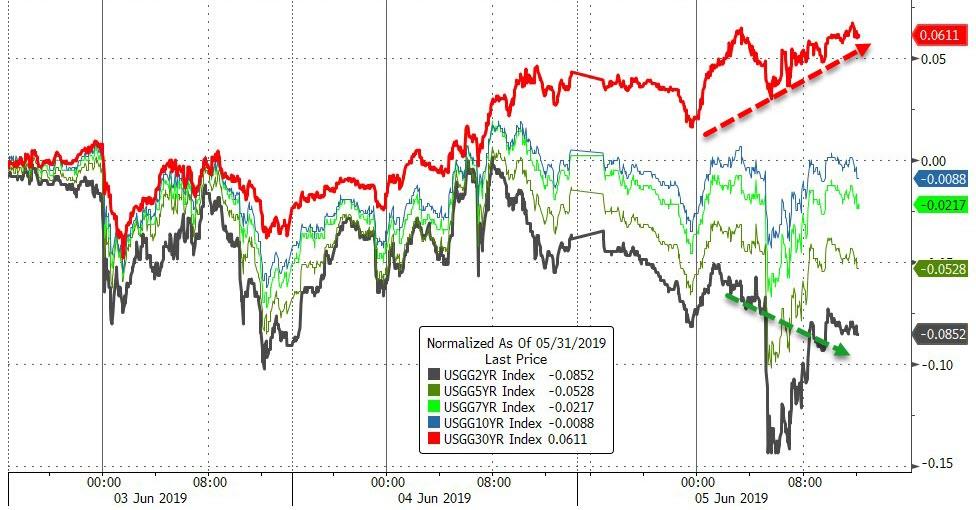

Stocks extended their decoupling from bond yields today…

Very mixed day in bond-land today with the entire curve lower aside from the long-end (30Y +2bps, 2Y -4.5bps)

Which has sparked a massive steepening in 2s30s…

But the short-end remains dramatically inverted…

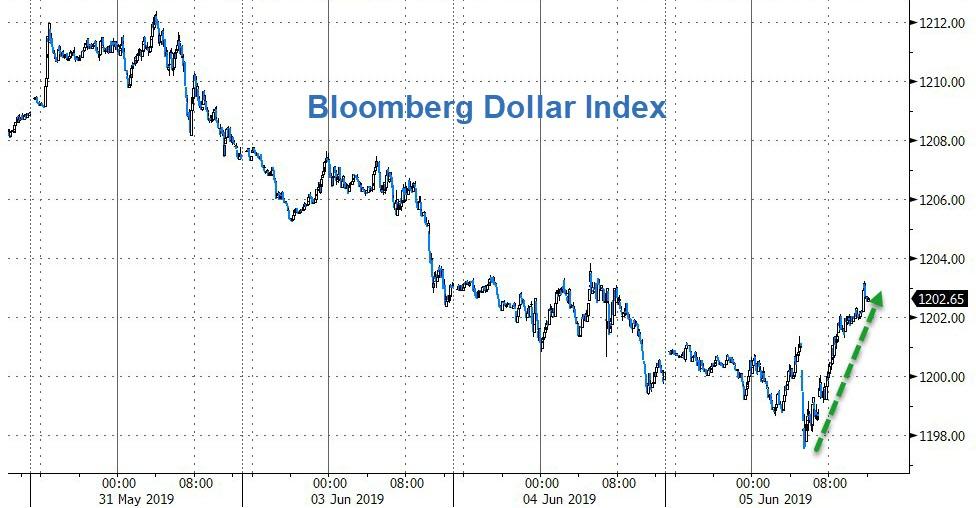

After 4 straight days down, the dollar index spiked today – best day in 6 weeks (back to yesterday highs only though)…

Yuan was weaker today…

NOTE how far from offshore yuan (market levels), the yuan fix has been held.

Cryptos managed modest (2-5%) gains today but remain lower on the week…

Copper and Crude were ugly today as PMs early gains leaked away as the day wore on…

Gold is up 6 days in a row…

Testing (and fading) at Feb highs…

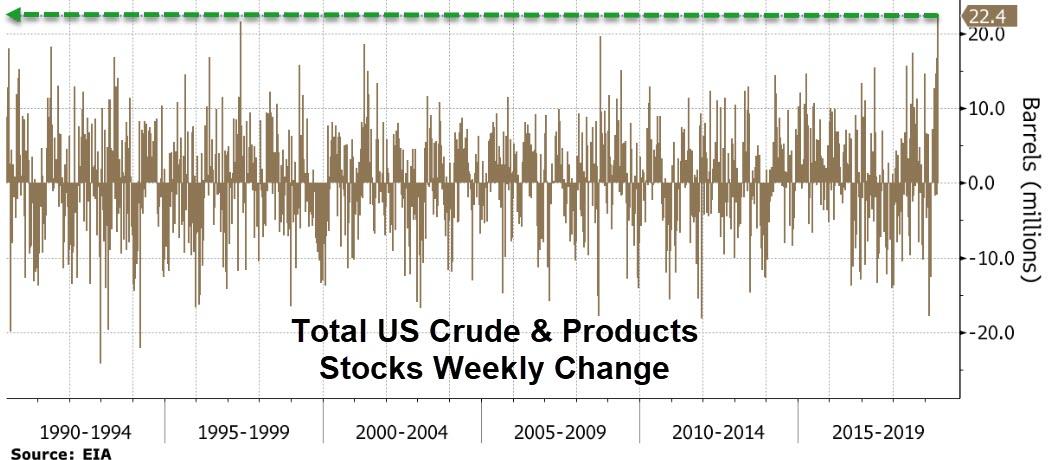

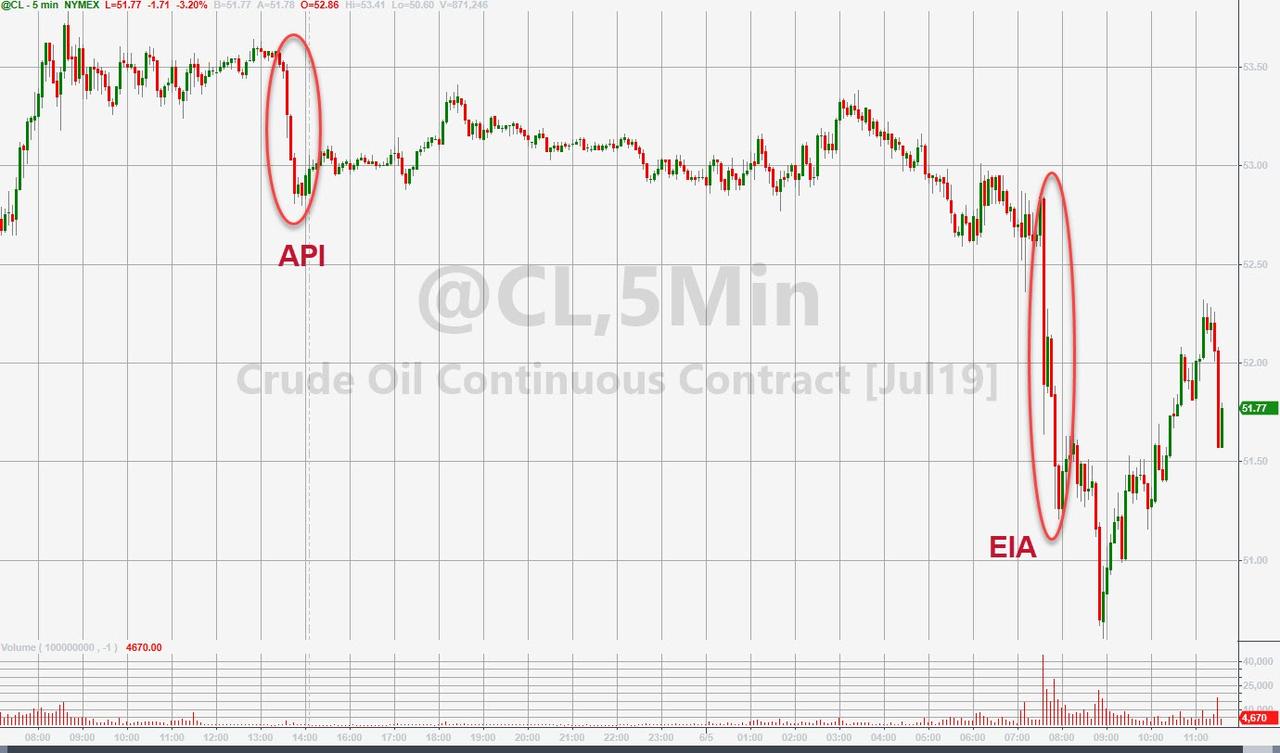

Oil prices collapsed into a bear market today (down 22% from highs) after a surprise build across all products produced the biggest aggregate inventory build since 1990…

“It’s the perfect storm, in a way, of increased supply coupled with perceptions of slowing demand growth,” said Marshall Steeves, energy markets analyst at Informa Economics in New York.

WTI tested down to a $50 handle (before ramping into the close) – the lowest since January 9th…

Brent fell back below $60 for first time since Jan…

Both down around 22% from recent highs, which stocks are summarily ignoring for now…

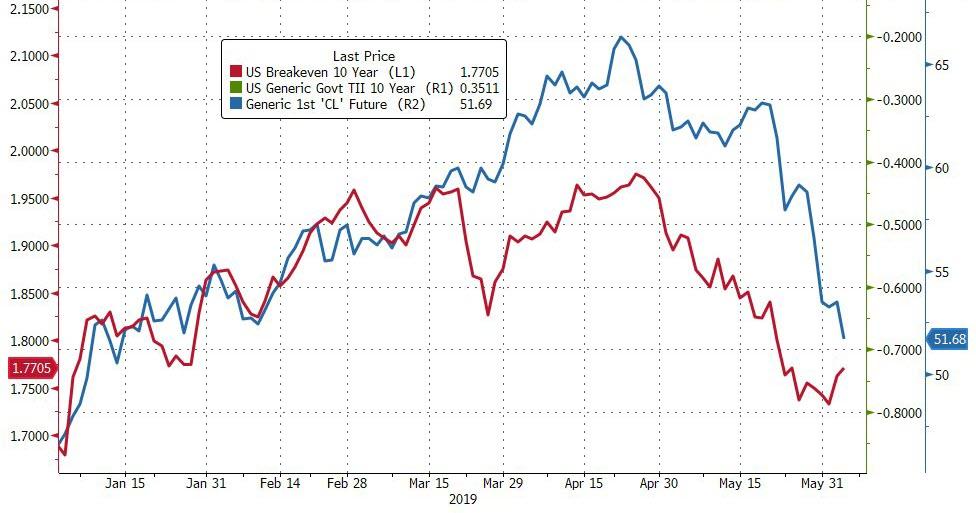

Is oil catching down to inflation breakevens?

Judging by HY Energy credit markets, WTI has further to fall…

The recent outperformance of gold (safe haven) vs oil (growth scare) is impressive (an ounce of gold now buys almost 26 barrels of WTI – up from just 20 barrels two weeks ago)…

Finally, we give Rosie the last word:

Does this chart look bullish? 16 months of nothing except the dividend, volatility, and acute anxiety. The S&P 500 has crossed above and below the 2,800 threshold no fewer than 19x since first testing the milestone in Jan/18. Looks like an elongated topping formation to me. pic.twitter.com/3YaRu7YLuH

There is no greater example of the divide among Democrats right now than the debate over whether or not to try and impeach President Trump over allegations that he obstructed, or attempted to obstruct, the Mueller investigation.

While some Democrats such as Reps. Alexandria Ocasio-Cortez (NY), Rashida Tlaib (MI) and House Majority Whip Jim Clyburn (SC) had been frothing at the mouth to launch lengthy impeachment proceedings that would drag out embarrassing details in front of the American public, establishment Democrats – following Pelosi’s lead – have strongly rejected calls to impeach on the basis that the Republican-led Senate would reject the process and “exonerate” Trump, giving him a boost going into 2020.

On Wednesday, Pelosi acknowledged that Democrats calling for impeachment are bringing ‘vital energy’ to the party’s oversight efforts, while attempting to downplay the divide over what to do.

“I see in some metropolitan journals, and on some TV, that we are trying to find our way or are unsure about [our direction],” said Pelosi. “Make no mistake, we know exactly what path we’re on. We know exactly what actions we need to take. And while that may take more time than some people want it to take, I respect their impatience.”

Speaker Pelosi on impeachment: “Make no mistake, we know exactly what path we’re on. We know exactly what actions we need to take. And while that may take more time than some people want it to take, I respect their impatience.” https://t.co/9G7KaACD9Dpic.twitter.com/eBe4J3KKv3

Pelosi also noted that impeachment doesn’t mean that Trump would automatically be removed from office.

Speaker Pelosi on the concept of impeachment, and what she says many in the public think happens with impeachment: “They think that you get impeached — you’re gone — and that is completely not true.” pic.twitter.com/Yyc9URNdRy

At least 55 House Democrats are on record endorsing an impeachment inquiry, according to The Hill.

Last week, House Intelligence Committee Chairman Adam Schiff – who swore up and down that he had evidence of Trump-Russia collusion that was “more than circumstantial” – effectively threw cold water on impeachment, telling The Hill last week “Where it ends I don’t know,” adding “I presume it ends with Donald Trump being voted out of office.”

Even House Judiciary Chairman Jerrold Nadler (D-NY) – who is aggressively pursuing all things Trump with his own post-Mueller investigation – told WNYC on Friday that while there is justification for impeachment, “you cannot impeach a president if the American people will not support it.”

In the latest appeal to stop talk of impeachment, former Senate Majority Leader Tom Daschle penned an Op-Ed in the Washington Post titled: “Listen to Pelosi, Democrats. Now’s not the time to impeach Trump.“

“House Speaker Nancy Pelosi (D-Calif.), meanwhile, has resisted the growing calls for Trump’s impeachment coming from within her caucus; from several of the 2020 presidential contenders; and the literal chants of “impeach” that arose from the crowd as she addressed the California Democratic Party State Convention this past weekend. She insists that before taking such a drastic step, Democrats must build an “ironclad” case.

She’s right. And the party should listen to her.

…

Pelosi understands that if congressional Democrats get ahead of the public and impeach Trump on, essentially, a party-line vote in the House, but then fail to gain the two-thirds Senate supermajority required for conviction — which is almost certain, given the way many Senate Republicans have bent over backward to excuse Trump’s questionable behavior — they risk making the mistake Republicans made 20 years ago, making Trump the new “comeback kid” and jeopardizing their own 2020 prospects.” -Tom Daschle

Daschle closes by saying “Democrats should approach 2020 understanding that Trump has something like a 50-50 chance of winning reelection, rather than acting like impeachment is just an acceleration of the inevitable,” adding “We can’t afford the confusion such an outcome would create. At stake is the fabric of our republic: our democratic institutions and the rule of law.“

via ZeroHedge News http://bit.ly/2IjDZZf Tyler Durden

Back in 2018, the list of voices speaking up about the risks inherent in the leveraged loan market, included the who is who of financial icons and regulators among them the IMF, Fed, BIS, JPMorgan, Guggenheim, Jeff Gundlach, and Howard Marks (as we documented back in December)with even Janet Yellen chiming in that declining underwriting standards for corporate loans could lead to more bankruptcies and prolong the next economic downturn.

Now we can add the CEO of one of the largest US bank (not to mention one of the largest loan issuers in the US).

Speaking at the Economic Club of New York, Bank of America CEO Brian Moynihan, warned that the U.S. economy is on solid footing except for one potential trouble spot: leveraged loans.

As Bloomberg reports, Moynihan said that his bank has repeatedly said it focuses on “responsible growth” and sticks to lending standards it’s had for years. Yet, in somehow trying to split hairs, he said that leveraged finance threatens to become an issue in the broader market, he said.

“It’ll be ugly for those companies if the economy slows down and they can’t carry the debt and then restructure it, and then the usual carnage goes on,” Moynihan said, echoing Yellen in bringing attention to collapsing covenant protections and weakening terms in the wider market for riskier corporate lending.

“We don’t see anything yet because the economy’s good, the companies are making money,” Moynihan said on Tuesday. “The issue that’s there is in the leveraged finance.”

The irony, of course, is that issuance of leverage loans is a business that Bank of America has dominated for a decade, and is sits atop the league table for leveraged-loan bookrunners for the 10th consecutive year, according to data compiled by Bloomberg. Infact, as Bloomberg commentator James Crombie pointed out, “BofA has sold most of these loans.”

Moody’s recently said covenant quality for Q4 2018 was close to a record low, and the rating company sees no signs of improvement this year.

The trend toward weaker terms is something “we should worry about,” Moynihan said. “We aren’t lowering standards because we tried that once and it didn’t work so well,” he said, to laughter in the audience. The laughter in a few years when BofA has to be bailed out again will be far more muted.

The leveraged loan market is relatively small, meaning any shakeout is less likely to affect broader markets, according to Moynihan. The “real debate” belongs with the leveraged finance deals that are done outside of banks, Moynihan said — echoing views of financial watchdogs who’ve expressed concerns that risk has shifted outside their purview.

Not helping, last month Fed chair Powell said that the market looks a lot like the mortgage industry in the run-up to the subprime crisis. “But U.S. regulators are watching closely this time around and the financial system is better shielded”, Powell said, not actually believing his words.

Why is Moynigan’s warning especially ironic? Because in just 2019, Bank of America has been the bookrunner on some $317 billion of leveraged loans, accounting for 10.8 percent of the market share. That compares with $688 billion for last year, when Bank of America led the loan portion of Blackstone Group’s buyout of Thomson Reuters Corp.’s Refinitiv unit. Leveraged loan volumes this year have dipped amid a flight from riskier assets and as investors pull money from loan funds as a pause in rate hikes dims their allure.

Besides the increasingly troubled credit market, Moynihan said overall economic activity and confidence remain strong among U.S. consumers and businesses. Even a recent slowdown in capital expenditures by businesses is consistent with a healthy economy, he said, adding that strong underlying economic data are more important indicators of growth than the possibility of a recession signaled by an inverted yield curve.

In a final irony, Moynihan’s testimony took place at the same time as the House Committee on Financial Services conducted a hearing today titled: “Emerging Threats to Stability: Considering the Systemic Risk of Leveraged Lending.” As Grant’s Interest Rate Observer, Philip Grant wrote last night, “an analysis of the leveraged loan market (“Tomorrow’s debt hearings”) in the July 13, 2018 edition of Grant’s Interest Rate Observer predicted that a cyclical crack-up would lead to unwanted (for industry practitioners) attention from Washington.” He was right. This is what else he said:

That July 2018 examination identified the erosion of creditor protection via widespread cov-lite documentation, deteriorating credit quality and aggressive earnings additions or cost-savings assumptions from issuers, called add-backs that can artificially inflate projected results. As noted by S&P’s LCD unit in a report last year, loans related to mergers and acquisitions are particularly susceptible to such add-backs of late, with a record 22% of M&A related-loans featuring add-backs greater than 50% of EBITDA in the first half of 2018, double the pre-2008 high.

Despite a suddenly-wobbly stock market, the M&A train keeps rolling. According to data from Bloomberg, more than $40 billion in corporate transactions were logged yesterday, the second-busiest deal day of the year.

Credit quality continues to wane. As noted by investment fund Driehaus Capital Management, LLC’s Twitter account this morning, the proportion of loans rated double-B (the high end of junk territory) now foot to less than 30%, down from 50% at the beginning of 2008. Single-B-rated issuers now comprise nearly 30% of loans, up from less than 10% in early ‘08.

The shift in the average leveraged loan rating since the crisis is quite notable. From 50% BB back in Jan08 to <30% now, as single B loans became the tranche of choice. YS #DriehausAltspic.twitter.com/iP7L36HYXB

Those red flags haven’t yielded much pain yet, as the S&P/LSTA Leveraged Loans Index has returned a solid 5.5% year-to-date, while LCD reported yesterday that the May default rate registered a skinny 0.93%, well below its historical average of 2.93%. But some investors aren’t waiting around: According to Bloomberg, the Invesco Senior Loan ETF saw its largest funds outflow on record yesterday.

via ZeroHedge News http://bit.ly/2JZko3H Tyler Durden

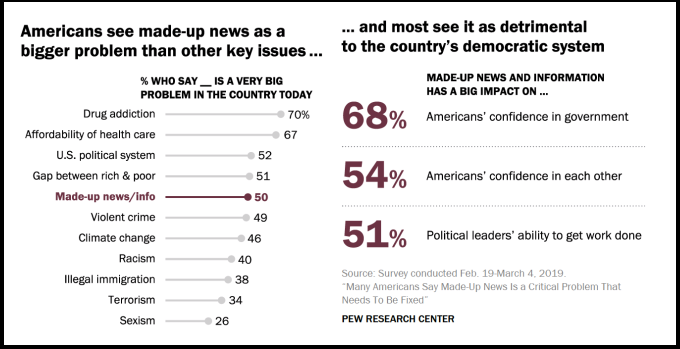

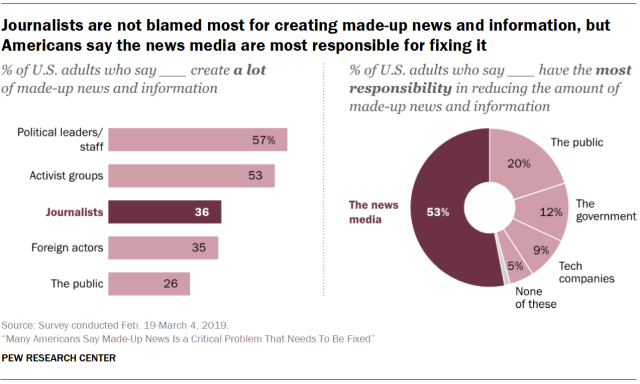

A new survey from Pew Research Center has found that Americans view fake news as a bigger threat than terrorism,violent crime, climate change, racism and illegal immigration.

The survey also found that 68% of US adults say that made-up news and information “greatly impacts Americans’ confidence in government institutions,” while 54% say it’s having a major impact on confidence between fellow Americans, and 51% say it impacts the ability of political leaders to get work done.

Who’s to blame? According to those surveyed, political leaders and activists are more responsible for fake news than journalists, however they believe that it is the primary responsibility of those in the news media to fix the problem. They also said that the issue will become worse down the road.

The vast majority of Americans say they sometimes or often encounter made-up news. In response, many have altered their news consumption habits, including by fact-checking the news they get and changing the sources they turn to for news.

In addition, about eight-in-ten U.S. adults (79%) believe steps should be taken to restrict made-up news, as opposed to 20% who see it as protected communication. –Pew

Nearly four-in-ten (38%) of Americans reported ‘often’ coming across made-up news and information, while another 51% say they ‘sometimes’ do. In response, Americans have changed their news and technology habits.

Around 78% of respondents say they fact-check news stories, while 63% have stopped getting news from a particular outlet. 52% say they have changed the way they use social media, while 43% have reduced their overall consumption of news.

Concern about made-up news has also affected how U.S. adults interact with each other. Half say they have avoided talking with someone because they thought that person would bring made-up news into the conversation.

In the digital environment, half of social media news consumers have stopped following someone they know because they thought the person was posting made-up news and information, and the same percentage have stopped following a news organization for this reason. –Pew

Republicans more concerned than Democrats

According to the survey, Republicans express greater skepticism than Democrats about fake news coverage, tend to blame journalists more for it, and generally see fake news as a larger problem.

A solid majority of Republicans and Republican-leaning independents (62%) say made-up news is a very big problem in the country today, compared with fewer than half of Democrats and Democratic-leaning independents (40%). Republicans also register greater exposure to made-up news. About half of Republicans (49%) say they come across it often, 19 percentage points higher than Democrats (30%).

One of the starkest differences, though, is in assigning blame for creating made-up news and information. Republicans are nearly three times as likely as Democrats to say journalists create a lot of it (58% vs. 20%).

Republicans also place more blame on activist groups, with about three-quarters (73%) saying these groups create a lot, close to twice the rate of Democrats (38%). Political leaders and their staff, though, rank high for both sides of the aisle – half or more of each party say they create a lot. And while members of both parties say the news media bear the primary responsibility for fixing the situation, that feeling is considerably more pervasive among Republicans (69%) than Democrats (42%). –Pew

Satire is no biggie

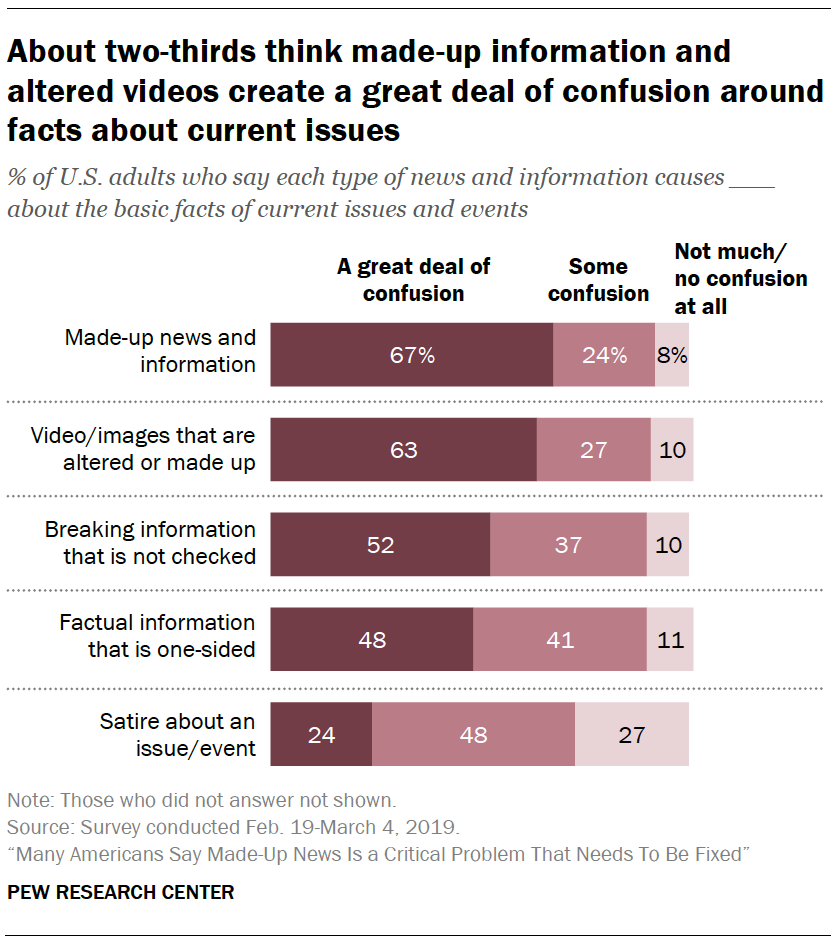

Pew also asked about distinctions between five types of information; ‘Fake News’, altered video/images, breaking news that is unverified, factual information that is biased, and satire about an issue or an event.

The survey found that 67% say fake news designed to mislead causes a great deal of confusion about the basic facts of current issues, while 63% say the same about fake video / images. Of those polled, 79% and 77% respectively say that something should be done to restrict this type of content.

A whopping 24% said that Satire causes a “great deal of confusion,” while 48% said it causes “some confusion” and 27% saying not much if any.

Americans feel that political divides in the country are the greatest obstacle to addressing the problem of made-up news and information. Almost two-thirds (64%) see those divides as a very big challenge. Between 41% and 44% cite the ability to make money from made-up news, digital technology, the public’s lack of effort and low awareness about current events as very big hurdles to a solution.

Americans see a lot of made-up news and information being generated around two major topics: politics and elections (73%) and entertainment and celebrities (61%). Both politics and entertainment far exceed all of the other four topics asked about.

In a related finding, Americans say that far more made-up news gets created around national issues and events than around local ones. About six-in-ten (58%) say a lot of made-up news is created around national issues, compared with 18% who say the same about local issues.

When it comes to identifying very big problems connected to keeping the public informed about current issues and events, about half of Americans (49%) put the amount of made-up news and information in that category. A similar percentage (51%) cites the public’s ability to distinguish between facts and opinions as a very big problem, compared with 37% who see journalists inserting their own views into coverage as a very big problem in how the public stays informed.

via ZeroHedge News http://bit.ly/2WmJn7I Tyler Durden

In December, Peter Schiff predicted that the Federal Reserve was about to hike rates for the last time and that the next step would be rate cuts. Yesterday, Jerome Powell made comments widely interpreted to signal the rising likelihood of a rate cut. The Fed chair dropped the word “patient” from his vocabulary, saying the central bank would respond as “as appropriate” to the perceived economic impacts of tariffs and other economic data.

Peter appeared on Fox Business Countdown to the Closing Bell with Liz Claman to talk about what’s next up for the Fed and how it will impact the economy.

“I don’t think that Powell would even open the door to the possibility of a rate cut if he wasn’t prepared to walk through it.”

Peter said the reason he knew the Fed would end the hiking cycle in December was because the stock market was tanking and he knew the only way the central bank could stop the carnage was to take the rate hikes off the table.

“Well, now it’s falling again, and so now all they’ve got left in their quiver is to actually cut rates.”

Claman pointed out that the stock market was popping at the mere suggestion of a rate cut.

“Exactly!” Peter said. “But I think people are wrong if they think it’s going to work again.”

“The Fed was able to inflate an enormous bubble with QE one, two and three, and keeping rates at zero for as long as they did. But the next time, it’s not going to work.”

“They’re right. But they’re wrong on the outcome. We’re going to have stagflation. It’s inflation that’s going to be the problem. And the economy is headed into recession, but the Fed should not be cutting rates because it’s stoking the inflation fire.”

Claman asserted that we don’t have inflation fires. She said we are “way below” the 2% CPI target the Fed uses as a gage.

“We’re not way below. We’re barely below the 2% number. But that’s just the way government measures it. Of course, in reality, prices rise faster than what the CPI reveals.”

Peter reiterated that the Fed is going to go back to 0% interest rates, and he pointed out that there isn’t a lot of room between the current rates and that zero level. He said the real “stimulus” is going to be QE 4, which will be bigger than the first three rounds combined.

“The Fed is going to go back to QE. They are going to do whatever they can to try to stop the bear market and to try to prevent the recession. But they’re going to fail. They are going to make it worse this time.”

During his remarks, Powell said that this isn’t unconventional policy anymore. He called it “business as usual.” Peter said the reason we didn’t have a dollar collapse and inflation didn’t take off in the aftermath of the Great Recession was because everybody thought the Fed’s monetary policy was temporary. They thought it was an emergency measure, that the central bank would eventually normalize rates, and that it would shrink its balance sheet.

“But when the markets realize what they should have realized from the beginning – that this is a permanent expansion of the balance sheet; this is debt monetization, that there is no end in sight, that it’s going to be zero percent forever, then the bottom is going to drop out of the dollar and then we’re going to get all the inflation that we should have had, only more.”

Liz asked Peter what people should do to prepare. One of the things he emphasized was to buy gold. Even above $1,300 an ounce, the yellow metal is a bargain.

“Remember, we got as high as $1,900 back in 2011 when people were actually worried about QE. Well, they were right to worry. The mistake was in thinking that everything was OK. So, when we go back to QE and zero percent interest rates, gold is not stopping at $1,900. We’re going to $5,000 to $10,000.”

via ZeroHedge News http://bit.ly/2WqjpQW Tyler Durden

Oil prices collapsed into a bear market today (down 22% from highs) after a surprise build across all products produced the biggest aggregate inventory build since 1990…

“It’s the perfect storm, in a way, of increased supply coupled with perceptions of slowing demand growth,” said Marshall Steeves, energy markets analyst at Informa Economics in New York.

WTI tested down to a $50 handle (before ramping into the close) – the lowest since January 9th…

Brent fell back below $60 for first time since Jan…

Both down around 22% from recent highs, which stocks are summarily ignoring for now…

via ZeroHedge News http://bit.ly/2wETGok Tyler Durden

The shocking blocking of redemptions from Neil Woodford’s, £3.7bn Woodford Equity Income Fund – after serial underperformance led to an investor exodus – is still sending shockwaves across the US asset management arena two days after it was first reported.

“I can’t remember anything quite like this” said Peter Walls, veteran manager of the Unicorn Mastertrust fund, after trading in Woodford’s fund was suspended. “I mean going back over decades really, there were quite a few funds that just didn’t pick up the telephone and suspended dealing in the dark days of the crash of ’87 and black Monday and all that but this is quite big stuff,” he said in an interview with CityWire.

As we reported on Monday, redemptions from Woodford’s flagship fund were suspended yesterday to allow the manager “time to reposition the element of the fund’s portfolio invested in unquoted and less liquid stocks, in to more liquid investments.”

The problem is that the fund’s extensive holdings of unquoted and illiquid stocks has presented a major challenge for Woodford in meeting redemption requests from investors; the subsequent news of the redemption halt has prompted even more selling as outside holders dumped the positions to frontrun the liquidating fund.

“I have to say if you look at some of the investments that went into [the] open-ended fund, you think well how on earth was that going to work?” said Walls.

Walls assessment was shared by wealth manager St James’s Place, which this morning terminated its £3.5bn relationship with Woodford in what the FT said was “a devastating blow to the veteran investor following the suspension of his UK Equity Income fund on Monday.”

The announcement capped a disastrous week for Woodford, who was already reeling from the decision by Kent County Council to take back a £266m investment mandate and by Hargreaves Lansdown to drop the investor’s funds from its best buy list.

St James’s Place, a top-tier wealth manager and Woodford’s most important commercial relationship, said on Wednesday it had appointed Columbia Threadneedle Asset Management and RWC Partners to manage the three funds formerly managed by Mr Woodford. As the FT notes, Woodford was responsible for the UK High Income Unit Trust, UK Equity, Income Distribution and SJPI UK High Income funds for St James’s Place, accounting for a total £3.5bn — around a third of his total assets under management in May.

The company had grown increasingly nervous about Mr Woodford’s performance last month and had stepped up scrutiny of his funds amid customer requests for redemptions.

Separately, Woodford’s second open-ended fund – which will soon be gated too – has shrunk to its lowest level since launching, after investor flight picked up pace at Britain’s best-known portfolio manager afraid that that fund too would soon be gated. Income Focus, which Woodford launched to great fanfare with £500m of investor capital in 2017, has fallen to £473m this week on the back of investor redemptions and poor performance. It has shrunk 14 per cent since the start of May.

Meanwhile, in a video posted on Tuesday night, Woodford appealed to investors not to abandon the Income Focus fund. “It doesn’t have any exposure to illiquid or unquoted securities and consequently isn’t exposed to the same issues that the Woodford Equity Income fund is,” he said, although investors clearly no longer believe Woodford.

“And it’s positioned, I believe, for the economic and market environment that we’re likely to see over the medium and long term.”

“Considering all of the negative publicity surrounding Woodford, the fund [Income Focus] will probably, rightly or wrongly, be tarred with the same brush as the Equity Income fund,” said Justine Fearns, a manager at Chase de Vere, adding she expected outflows from Income Focus to continue.

The only question is when this next fund will itself be permanently gated, as will Woodford’s career in the asset management industry.

Meanwhile, as we first said on Monday, what is most bizarre about this latest hedge fund fiasco is that the gating takes place with global markets still just shy of all time highs. One can only imagine what will happen to the rest of the hedge fund sector if the current swoon accelerates and drops another 5%, 10% or more, sending other hedge funds scrambling to liquidate their own holdings of the most crowded stocks. Those who succeed to sell first, they just may survive to fight another day.

But an even bigger concern is whether this gating by one of the UK’s most iconic hedge funds sparks a redemption frenzy, first in England, and then, across the globe in what may soon become a rerun of the redemption panic that struck in December, resulting in the first S&P bear market since the financial crisis. Only this time, we doubt the market will recover just minutes after triggering the infamous -20% threshold.

via ZeroHedge News http://bit.ly/2JXAN8R Tyler Durden

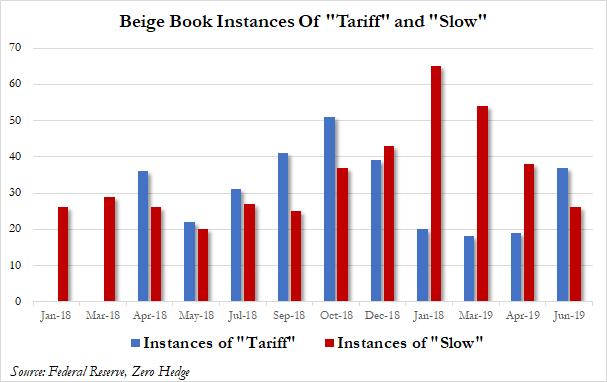

Back in April, the Fed downgraded its assessment of the US economy through its Beige Book surveys, characterizing the economic growth as only “slight-to-moderate.” Now, in the latest Beige Book release, published moments ago, the Fed signaled a “slight improvement” in the economy, describing economic activity expanding at a “modest pace overall” from April through mid-May, and dropping the “slight” classifier.

Almost all Districts reported some growth, indicating they’re handling the headwinds to the economy well, including the tariffs and a lack of available workers, while a few saw moderate gains in activity.

Manufacturing reports were generally positive, but some Districts noted signs of slowing activity and a more uncertain outlook among contacts. Residential construction and real estate both showed overall growth, but both sectors saw wide variation in sentiment across Districts. Reports on consumer spending were generally positive but tempered. Tourism activity was stronger, especially in the Southeast, but vehicle sales were lower, according to reporting Districts. Loan demand was mixed but indicated growth. Agricultural conditions remained weak overall, but a few Districts reported some improvements. The outlook for the coming months was solidly positive but modest, with little variation among reporting Districts.

Most districts saw modest or moderate growth in jobs and wages, though regions including Richmond and San Francisco cited difficulties finding workers or highlighted tight conditions. Wage pressures remained “relatively subdued” with some employers boosting benefits, contrary to widespread reports of continued labor shortages.

Inflation remained non-existent, at least according to the Fed, with overall prices increasing at a “modest pace” in most districts since the previous report. While several districts noted faster growth in input prices than in final selling prices, firms generally reported input cost increases in the modest-to-moderate range indicating that so far American consumers are not paying for the trade war with China.

What is perhaps most surprising is that the various regional Feds did not paint a gloomier economic picture in response to escalating trade war fears and rising tariffs. Even so, after three consecutive Beige Books in which “tariffs” saw few references, the latest report saw a doubling in the use of “tariffs”, although variants of the phrase “slow” surprising declined from 38 in April to just 26, from a recent high of 65 in January.

While they received less prominence than in late 2018, trade and tariffs were mentioned in several regions including Philadelphia, which cited uncertainty as delaying business investment. Dallas also said trade uncertainty was weighing on business sentiment. Some of that may be affecting manufacturing. Richmond, for example, said factory shipments and new orders declined. The picture for commodity inputs was varied across the nation, with some sources spotting lower steel prices while others said costs remained elevated.

Unlike today’s dismal ADP print, the report painted a generally positive, if not uniformly so, signal ahead of crucial data Friday on employment in May. As recent high frequency indicators have indicated, there has been some notable weakness across the US economy, including weak reports on retail sales, factory orders and home purchases which have sparked concerns about slowing growth as President Donald Trump’s trade war with China weighs on businesses.

As Bloomberg notes, in one example of labor pressures highlighted in the report, several restaurants in Charleston, South Carolina, closed because they were so short-staffed. One business moved to counter service and switched to disposable utensils to stay open.

Meanwhile, as noted here extensively in recent weeks, farms reported struggles across the U.S. In the Minneapolis district, a wet spring threatens the planting season, with some growers saying they might not be able to plant at all this year. Anecdotes from Chicago echoed these troubles, with farmers challenged by poor weather and low crop prices.

Below are selected anecdotes from the Fed’s Beige Book, as compiled by Bloomberg:

Boston: Manufacturing contacts cited tariffs as their main pricing issue, indicating that they were generally able to push price increases to customers. One reported that they added a surcharge to cover the tariff on goods from China, which customers accepted; once they found an alternative supplier, they removed the surcharge

New York: A number of businesses in New York State have noted ongoing challenges from the recent minimum wage increase; some reported that they are investing more in automation

Philadelphia: Tariffs remained a key concern for many manufacturers. Contacts noted that much of the impact from the initial 10 percent tariffs was absorbed along the supply chain before reaching the consumer. However, they expect much more of the impact from the 25 percent tariffs to be passed through to the consumer

Cleveland: Many contacts are concerned that the increased tariffs on goods traded with China will further exacerbate softening manufacturing activity in China, leading to less demand for American products from Chinese manufacturers

Richmond: Several restaurants in Charleston, SC, closed because they couldn’t find enough staff. Moreover, one restaurant moved to counter service and disposable utensils in order to remain open with a smaller staff

Atlanta: Regarding trade policy uncertainty, some transportation contacts developed contingency plans to reduce capital expenditures and headcount to offset tariff-related revenue shortfalls

Chicago: Contacts indicated that it would soon be too late to plant corn in some areas and that switching to soybeans, while possible, would be costly due to wasted fertilizer and the low price of soybeans

St. Louis: Contacts reported that larger firms were offering higher pay to attract workers, particularly for entry-level positions, but that small businesses were struggling to raise wages at the same rate

Minneapolis: A Minnesota manufacturer increased hourly wages for welders from $18 to $22 to better compete for labor

Kansas City: Regional contacts indicated that farm income decreased modestly and farm loan repayment rates slowed slightly since the last survey period

Dallas: Several agricultural producers in southern New Mexico expressed concern over the lack of labor force growth and the strain that immigration restrictions have imposed on their current workforce. They also mentioned that the recent authorization of hemp production provides an opportunity as an alternative to pecan production, as the pecan industry has been negatively impacted by tariffs.

San Francisco: A contact in the California utility sector observed that some price inflation resulted from wildfire-related costs

The bottom line is that absent significant deterioration in the economy and/or trade war, this report will not help those both inside the Fed and outside, who are now eager for a rate cut as the economy simply is not in such a dire state as to need it (yet).

via ZeroHedge News http://bit.ly/2QKMIHA Tyler Durden

We’ll start with one important observation about today’s US equity rally: healthy, happy markets don’t surge 2% in a single session. Worried markets do. Remember the old traders saying – stocks take the stairs up but the elevator down. Even if you take the stairs 2-at-a-time (an excellent core exercise, I am told, if you don’t use the handrails) you don’t get a 2% day.

Still, we’ll take the reprieve as a chance to quickly review the state of US equity fundamentals and valuations. Five points here, with data from FactSet’s weekly Earnings Insight report:

#1: The S&P 500 trades for 15.9x forward 12-month estimates:

That is lower than the 5-year average of 16.5x, but as we’ll shortly see earnings growth is lower so that makes sense.

It is, however, notably higher than the 10-year average of 14.8x, supported by low global interest rates.

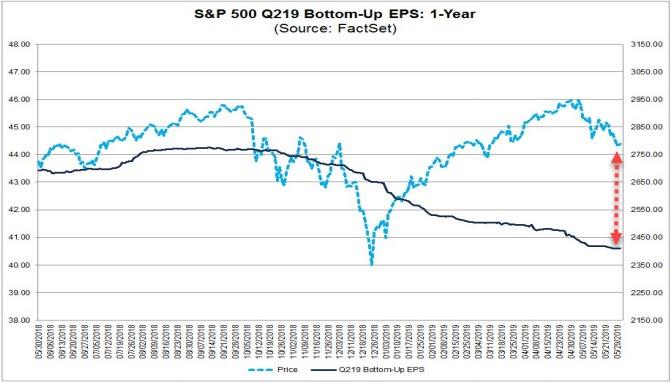

#2: Analysts expect the S&P 500 to post 3-4% earnings growth in 2019 and 10% in 2020:

US corporate earnings growth since 2009 has compounded annually at 10.5%, albeit in fits and starts. When oil prices collapsed and US economic growth slowed from 2014 – 2016, S&P earnings flattened at $119/share. It was only in 2017 and 2018 that they resumed growing, reaching $162/share last year.

Analysts have been reducing earnings estimates all year, down from 6% in January for 2019 to the current 3-4%. Also worrisome: any 2019 growth at all relies on Q4 delivering a 7% comp to last year’s weak period.

#3: There is a wide dispersion in 2019 earnings expectations by sector, but even the “best” growth is unremarkable:

Sectors expected to show above-average earnings growth: Financials (+7.2% versus 2018), Consumer Discretionary (+6.7%), Utilities (+6.4%), Industrials (+5.2%) Communication Services (+5.1%) and Health Care (5.0%).

Those with below-average earnings prospects: Energy (-8.8% versus 2018), Materials (-6.4%), Consumer Staples (+0.2%), Technology (+0.3%) and Real Estate (+2.6%).

#4: Despite those collectively sluggish expected results, sector valuations are “country mile” wide:

Sectors trading for +18x: Consumer Discretionary (20.2x), Real Estate (19.0x), Consumer Staples (18.7x), and Utilities (18.2x).

Sectors trading for less than 15x: Financials (11.3x), Health Care (14.7x), and Energy (14.8x).

Clustered around the 15.9x mean S&P 500 valuation: Tech (17.9x), Communication Services (17.4x), Materials (15.3x), and Industrials (15.1x).

#5: Saving the most important for last, the critical issue for US stocks is a disconnect between expected revenue growth and earnings expectations:

For most of 2019, revenues should grow at 4-5% but earnings growth will remain flat. Earnings leverage – the most powerful source of upside surprises – is entirely absent.

If revenues fall short, as would happen if the US/global economies falter, then earnings will quickly tip over into negative territory. Companies will respond by cutting staff and investments, and the current cycle will end.

The Federal Reserve can cut rates all it wants and this problem will still exist. Lower interest rates may elevate multiples, but the fundamental lack of earnings leverage is the real issue facing US stocks.

Summing up, US stocks are neither climbing stairs nor taking elevators; they are on a tight rope, gingerly feeling out the next step. Seeing the Fed unravel a safety net today certainly helps investor confidence. But to transit safely, we’ll need to see corporate earnings leverage lend a hand. We believe it can – no management team can survive very long if they increase costs faster than earnings. But this issue is the critical one for US stocks over the remainder of the year.

* * *

The rally gave us the breather we needed to round up the usual (economic) suspects for a look at what they can tell us about general market conditions. Our basic idea here is that while equity markets may be a bit panicked, we want to see if currencies and fixed income are similarly agitated. Here’s what we see:

#1: Treasury – Eurodollar (TED) Spreads

The difference between 3-month Treasury yields and 3-month LIBOR

A signal of dollar availability outside the US.

High readings (above 0.5) indicate potential stress in the global financial system and are especially negative for emerging market economies.

Takeaway: concerns about a US/global recession are not creating any significant stress in the global financial system just yet. This is likely due to the belief the Federal Reserve will reduce its benchmark rates later in 2019 and keep liquidity flowing.

#2: Italian Long Term Sovereign Debt

We look at 10-year Italian debt for comparability to liquid German and US sovereign bonds.

Yields here are 2.52% today, 273 basis points higher than German 10-years and 38 basis points above US Treasuries.

These spreads are in line with the 1-year average versus Bunds (276 bp) but modestly wider than US 10-years (11 bp).

Takeaway: despite Italy’s political situation, its still-high unemployment rate and worries over Eurozone economic slowing, Italian bond spreads remain at/near historical levels. Another positive sign, in other words.

Also worth noting: even at their low point for 2019 (back in April) high yield spreads only got back to their 1-year average for a few days.

Takeaway: like US equity markets, high yield is clearly struggling to price the risk of an imminent recession. Spreads are 81 bp above their 1-year average, almost 2 standard deviations away from the mean. The market’s optimistic view about future Fed rate cuts is not helping here.

Also worth noting: there’s a lot of hand-wringing in fixed income circles around BBB credits, many of which could see downgrades to junk in a recession.

Takeaway: the investment grade corporate bond market is not as fretful as high yield or equities. Spreads are modestly wider than 1-year averages (8 basis points) but this is well within 1 standard deviation (12 bp) from the mean over the period.

#5: Offshore Chinese yuan/dollar exchange rate

The offshore yuan market, based in Hong Kong, is more indicative of true exchange rates than the onshore market controlled by Beijing.

The key level to watch is 7.0 yuan/dollar, a level the currency has approached but never breached since trading started in 2010.

Sharp depreciations – such as those potentially caused by US-China trade war concerns – give rise to concerns of capital outflows.

Current level: 6.92, less than 1% away from the 7.0 all-time high.

Takeaway: offshore yuan levels are still quite close to the 7.0 level, but holding firm. Moreover, China certainly has the firepower to defend the yuan by selling some of its $1.3 trillion in US Treasuries (Hong Kong plus Chinese holdings).

#6: The value of the dollar

Investors mostly watch the DXY Index, but we also look at the Fed’s Trade-Weighted Dollar Index

The DXY Index sits at 97.08, 1% off its May 30th high. More importantly, DXY right now is 5% below its all-time high of 102.21 (October 2016).

The trade-weighted dollar, by contrast, is at both 1 and 10-year highs right now at 129.6.

Takeaway: even today’s more dovish Fed pronouncements have done little to weaken the dollar (DXY -0.1% as of 2pm ET). While the old rubric that “a strong dollar is in the long-term best interests of the US” is true, it also puts a damper on S&P 500 corporate profitability since 38% of revenues there come from non-US sources.

The bottom line: there’s both good and bad news in this quick tour around the world’s capital market pressure points. On the plus side, this is not 2008 by any stretch of the imagination. Capital is still flowing (TED spreads, Italian bonds, investment grade bonds). On the negative side, marginal destinations – high yield and (of course) equities – are twitchy about what comes next.

In the end, we’re most concerned about currencies just now. We don’t hear much about the dollar’s strength, but it does impact everything from US corporate earnings to Chinese economic stability. A weaker greenback should come as the Federal Reserve starts to move convincingly to easing, which also looks to be the trigger for a sustainable move higher for US stocks.

via ZeroHedge News http://bit.ly/2XtXpkk Tyler Durden