Violent clashes with protesters in Memphis, Tennessee resulted in at least 24 police officers with injuries. The protests came following the shooting death of a man killed by US Marshals during an attempted arrest, according to Reuters.

Two journalists were also injured when a protesting crowd attacked police with bricks and rocks.

Memphis Mayor Jim Strickland said:

“At least 24 officers and deputies were injured — six were taken to the hospital. Multiple police cars were vandalized. A concrete wall outside a business was torn down. The windows were broken out at fire station 31.”

The Tennessee Bureau of Investigation says it has been called in to investigate the shooting, which occurred after US Marshals attempted an arrest of a man wanted on multiple warrants. The TBI said that the man rammed his vehicle several times into police cars before exiting the vehicle with a weapon.

The TBI release stated:

“The officers fired striking and killing the individual.”

Shelby County Commissioner Tami Sawyer claimed that nearly 300 people joined to protest the shooting. She tweeted: “Every life lost should matter…every single one. How many times will this be ok? It cannot continue to be.”

Memphis Police Director Michael Rallings told NBC at a news conference:

“The officers did an enormous job tonight showing restraint in a very volatile situation. Officers had to don protective gear as the crowd threw objects, and a ‘chemical agent’ was used to disperse the crowd.”

The Memphis Police Department reported on Twitter that after the shooting, some police officers “received minor injuries” from people throwing “bricks/rocks” at them. A local newspaper in Memphis reported that the “tense standoff” wound up escalating with dozens of people.

Mayor Strickland concluded:

“Let me be clear—the aggression shown toward our officers and deputies tonight was unwarranted.”

Rallings concluded:

“I do want to commend individuals that did not decide to commit acts of violence toward the police officers, that showed restraint — I know that there were many individuals in the crowd that tried to assist in keeping everyone calm. My message tonight is that, is we should all wait and make sure we know exactly what happened before we spread misinformation or we jump to conclusions.”

He said police supported the right to protest, “but we will not allow any acts of violence, we will not allow destruction of property.”

via ZeroHedge News http://bit.ly/2KRCUun Tyler Durden

Well, we didn’t have to wait long for ’John Wick: Chapter Portobello’ to begin, did we? Brent crude spiked 4.5% before giving up around half of those gains as a further two oil tankers–one Norwegian, one Japanese–were attacked in the Straits of Hormuz, forcing the evacuation of both vessels; that as Japanese PM Abe sat down with the Iranian government to try to dial down tensions with the US – and as the leadership refused to accept any message from President Trump. The US have now accused Iran of attacking the two ships, which follows on from two other recent tanker attacks, drones hitting Saudi oil pumps, and a missile hitting a Saudi airport this week. The easy market response was long oil, obviously, as well as a ‘Risk Off’ further leg down in bond yields. But who did this and why? And what does that say will happen next? Logically, it was either Iran, or the US, or a third party:

Iran is suffocating under US sanctions, a known instigator of such actions via proxies, and threatening the EU with walking away from the nuclear deal if they won’t help it out. An attack like this would be incredibly reckless…unless they are desperate enough to up the ante to see if a war-averse White House will press ahead with another ruinous Middle East conflict ahead of the 2020 elections and in the face of a Cold War with China. If that is the case then expect more provocations and more Risk Off even as Iran calls this all “beyond suspicious”, “economic terrorism”, and “sabotage diplomacy”.

The US is divided between neo-cons champing at the bit to take on Tehran, war-averse Trump, and a Pentagon now looking at China–and Russia–as the real threat: notably, CENTCOM has said a war with Iran is not in the US strategic interest – and it isn’t. Why would Trump order an attack on a Japanese ship just as Japanese PM Abe is in Iran as emissary to try to de-escalate (a situation the US has escalated in typically Trump fashion)? In short, although the US has from–Gulf of Tonkin, WMD–this seems less likely.

Third parties are a short short-list. Mainstream media will no doubt follow murky social media to point a finger at the Saudis and Israelis – and the latter more than the former. Yet would either want to precipitate a major war that would drag them in when economic sanctions on Iran are biting? Perhaps. But also consider the political blowback of being found out as war instigators in Washington could be existential.

In short, one could argue that the largest risk is that it is the Iranians who are upping the stakes vs. US economic pressure,…in which case the US has very difficult choices to make on both fronts. Jaw-jaw or war-war? The bell-weather(?) Fox News is already suggesting Trump’s hand may be forced by Iran’s actions. As with China and trade war-war that backdrop certainly supports our long-held view of lower yields, stronger USD, and weaker EM FX…and perhaps weaker GBP too given Boris Johnson handily won the first round of the Tory party leadership election and, barring error, appears to be next UK Prime Minister.

Even if we ignore politics/risk off/John Wick, lower yields lie ahead. Consider the RBA for example, as Aussie 3-year bond yields are now below 1% and 10s at 1.38% when we started the year at 2.31% with market talk (from others!!) of when, not if, the RBA would hike again. For years the Reserve Bank have been boasting about the strength of the labour market as I argued the jobs data are inaccurate, looking at under-employment argues there is lots of slack, and there are 15-20K of new arrivals every month. Now suddenly say the RBA says the unemployment rate needs to be as low as 3.5% to address those issues: given we are 5.2% and rising, that’s a whole lot of monetary policy stimulus ahead! Have they read back-issues of my Aussie monthly page? Had a Damascene conversion? Or are they looking at the housing market and saying “Whatever it takes, mate”.

I also must add that in the US we also just saw import prices negative m/m and y/y again with the Chinese exporting DEFLATION not inflation despite 25% tariffs on USD250bn of goods (albeit perhaps this hasn’t fully kicked in). Who pays for tariffs? Certainly not US consumers so far. Nothing for the Fed to worry about on that front anyway.

The one unalloyed good piece of news today is that there are tentative signs that the Hong Kong government might be prepared to delay the debate on controversial extradition legislation that has triggered discussion of existential risks to its status as a global financial centre. However, there are also calls for further public protests on both Sunday and Monday, and things can change fast…

…everywhere!

via ZeroHedge News http://bit.ly/2Zsuj5M Tyler Durden

One day after traders were greeted by a sea of green – on potential world war news – we are back to the sea of red as global stocks struggled and safe haven bets were back in play on Friday with German bond yields plumbing record lows after the latest dismal Chinese data dump sparked fears about the health of the global economy and concerns of a new U.S.-Iran confrontation intensified (which, by the way, was somehow bullish for risk yesterday).

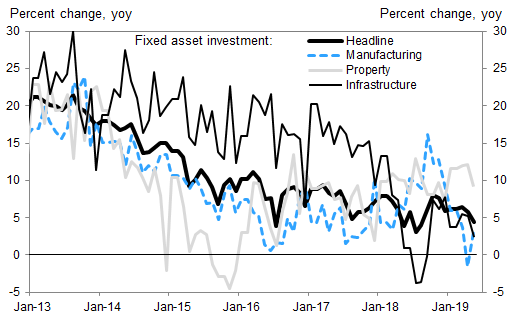

Beijing May activity reported overnight was very weak and painted a fairly gloomy picture of the world’s second largest economy as the trade war with the United States starts to bite. May industrial output growth slowed to a more than 17-year low, the weakest since since 2002, and well below expectations, while fixed-asset investment also fell short of forecasts. Retail sales growth accelerated and surprised to the upside however.

The full breakdown:

Industrial Output for May: 5.0%, est. +5.4% (range +5.1% to +6.4%, 35 economists), down from +5.4% last month.

May retail sales +8.6% y/y; est. +8.1% April +7.2%

Jan.-May fixed-asset investment excluding rural households +5.6% y/y; est. +6.1% (range +5.2% to +6.5%, 34 economists). Jan.-April +6.1%

Commenting on the data, Goldman said “May activity growth was very weak” noting that IP month-over-month annualized growth was around 2.6% based on our seasonal adjustment, which was higher than April but still at a weak level. The shifting Labor Day holiday distorted IP, and to a lesser extent FAI, data on the downside, but the impacts were limited as there was a difference of only one vacation day which could not fully explain the extent of the data weakness. The impacts of shifting holidays tend to be larger on retail sales data. April retail sales data was exceptionally weak and the reversal of the distortion was the main driver of the rebound in retail sales in May. The slowdown in property transactions year-over-year growth was partially due to an unfavorable base effect, but sequentially transactions also cooled in April-May as the government marginally tightened property policies in a few cities such as Changsha, Xi’an, Beijing etc.

As a result, expectations for more stimulus in China continue to grow as the Sino-U.S. trade dispute threatens to escalate into a full-blown trade war that many fear could push the global economy into recession.

“The Chinese data was disappointing, especially the industrial output numbers,” said Chris Scicluna, head of economic research at Daiwa Capital Markets. “That’s given bond markets additional momentum.”

The dismal Chinese data saw yields on German 10-year Bunds — one of the safest assets in the world — fall to fresh record lows, the yield dropping as low as -0.27%.

U.S. Treasury yields were also grinding lower, last seen just above 2.06%, the same level they hit one week ago when the dismal jobs print virtually assured a rate cut by the Fed. Safe-haven bond yields have already fallen in recent days amid rising speculation about monetary easing by major central banks. Meanwhile, Spain bond yields have fallen for the first time below 0.5%.

Speaking of Europe, the Stoxx 600 Index fell as much as 0.8%, hitting a session low, with 18 out of 19 sectors dropping, led lower by tech and banks. The Tech sector index was biggest drag on the Stoxx 600, down 1.9%, on contagion from U.S. chip giant Broadcom, which cut guidance and warned of a slowdown in demand due to trade tensions and the U.S. ban on Chinese tech and mobile phone company Huawei Technologies. European tech shares led the indexes lower, with semiconductor companies Infineon, AMS, STMicroelectronics, Siltronic and Dialog Semiconductor all dropping between 2%-3% after Broadcom outlined the impact of a total halt in sales to Huawei.

“The sales warning from Broadcom is also weighing on markets this morning as it suggests that both semiconductor and auto sectors are under pressure worldwide,” said Market Securities strategist Christophe Barraud in Paris, adding that expectations for a rebound were now shifting from the second half of this year to 2020. “Given both these sectors are key for world trade, it’s not good news for trade.”

The Stoxx banks index slumped 1.1% as European curves continue to flatten; defensive utilities sector is the only sector that posts gains, up 0.3%

Earlier in the session, Asian stocks swung between gains and losses, with markets in the region mixed. While Japan’s Topix Index gained 0.3%, shares in Hong Kong and China dropped. In its third-day of losses, the Hang Sang Index fell another 0.7% as calls increased for the city’s leader to delay an extradition bill. China was the the region’s worst-performer, with the benchmark Shanghai Composite falling 1% after the abovementioned ugly economic data dump hit overnight. India’s S&P BSE Sensex Index declined 0.5% amid cash-crunch woes.

Over in the US, index futures were in line for a lower open, with the S&P e-mini pointing to a 0.2% fall.

With the week ending, all eyes now turn to the Fed’s June 18-19 meeting which will show investors if the U.S. central bank’s monetary policy stance matches market expectations for a near-term rate cut. A Reuters poll showed a growing number of economists expect the Fed to cut interest rates this year although the majority still expect it to stay on hold.

“There is a large degree of uncertainty going into next week’s FOMC (Federal Reserve Open Committee) meeting as market reaction will differ significantly depending on whether the Fed hints toward easing policy,” said Shusuke Yamada, chief Japan FX and equity strategist at Bank Of America Merrill Lynch. “A wait-and-see mood is likely to begin prevailing in the markets ahead of the FOMC.”

Elsewhere, growing worries about a new U.S.-Iranian confrontation after two attacks on two oil tankers in the Gulf of Oman on Thursday added to the unhappy mood, resulting in an oil price surge. Washington blamed Iran, but Tehran bluntly denied the allegation. But U.S. and European security officials as well as regional analysts left open the possibility that Iranian proxies, or someone else entirely, might have been responsible. The attacks set crude prices on a roller coaster ride, with Brent futures slipping 0.2% to $61.18 per barrel. Brent surged 2.3% on Thursday after the Norwegian- and Japanese-owned tankers both experienced explosions.

In the latest development, the US Navy Destroyer USS Mason was en route to the area where the 2 oil tankers were attacked, while it added it has no interest in engaging in new conflict in the Middle East and that it is ready to defend US interests as well as freedom of navigation. Furthermore, the US released video footage of Iranian military removing an unexploded mine from the Japanese tanker that was attacked in the Gulf of Oman. Iran categorically rejected the US unfounded claim regarding tanker attacks according to Iranian mission to the UN, while there were also comments from Iran Foreign Minister Zarif that US allegations against Iran without evidence shows the B team is moving to Plan B of sabotaging diplomacy.

In FX, the safe haven yen advanced after data showed China industrial output slowed in May to its weakest pace since 2002. The dollar’s index against a basket of six major currencies was little changed initially, but spiked to session highs after China warned the US not to get involved in Hong Kong matters. The Swedish krona led gains in the Group-of-10 currencies after Swedish inflation rose faster than expected, while the euro stayed close to $1.13 where hefty expiries rollover Friday. The euro was steady at $1.1282 while the greenback inched down 0.2% to 108.19 yen. The Australian and New Zealand dollars fell on Friday as bets on interest rate cuts undermined demand and Group of 20 meeting later this month sidelined investors.

Expected data include retail sales, industrial production and University of Michigan Consumer Sentiment Index. No major company is scheduled to report earnings.

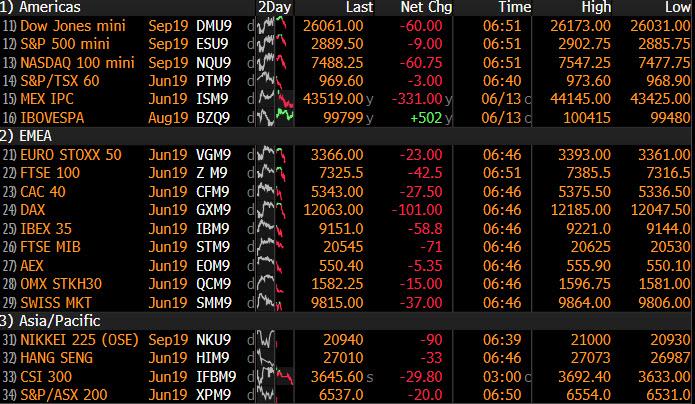

Market Snapshot

S&P 500 futures down 0.3% to 2,891.25

STOXX Europe 600 down 0.5% to 378.55

MXAP down 0.07% to 155.50

MXAPJ down 0.5% to 507.16

Nikkei up 0.4% to 21,116.89

Topix up 0.3% to 1,546.71

Hang Seng Index down 0.7% to 27,118.35

Shanghai Composite down 1% to 2,881.97

Sensex down 0.5% to 39,551.96

Australia S&P/ASX 200 up 0.2% to 6,554.00

Kospi down 0.4% to 2,095.41

German 10Y yield fell 2.1 bps to -0.262%

Euro up 0.04% to $1.1280

Italian 10Y yield fell 7.6 bps to 1.989%

Spanish 10Y yield fell 4.6 bps to 0.497%

Brent futures down 0.2% to $61.22/bbl

Gold spot up 0.8% to $1,352.75

U.S. Dollar Index up 0.1% to 97.13

Top Overnight News from Bloomberg

President Donald Trump is still waiting for a response from Chinese President Xi Jinping about meeting to restart trade talks, economic adviser Larry Kudlow said while warning Beijing may face consequences it if refuses the invitation

The Trump administration blamed Iran for attacks on two oil tankers near the entrance to the Persian Gulf, escalating tensions between the two rivals despite denials from officials in Tehran and a lack of public evidence for the U.S. claim. U.S. releases video it says is of Iran removing mine from ship

Rivals to be Britain’s next prime minister are holding private talks over joining forces in an attempt to stop the pro-Brexit favorite, Boris Johnson, running away with the contest, people familiar with the matter said

China’s industrial output growth slowed to the weakest pace since 2002, highlighting the headwinds the economy is facing as it grapples with the tariff war with the U.S.

Hong Kong girded for another mass march against a China- backed extradition bill Sunday, as the city’s leader, Carrie Lam, faced new calls to withdraw the legislation after clashes between protesters and police

Allies of Hong Kong leader Carrie Lam began questioning her tactics as lingering tensions prompted lawmakers to postpone debate on a controversial extradition bill until at least next week

White House Press Secretary Sarah Huckabee Sanders is leaving the Trump administration after a turbulent tenure marked by attacks on the media, dissemination of false information and the near-disappearance of the daily press briefing

Asia equity markets traded mixed as they awaited Chinese Industrial Production and Retail Sales data, where retails sales beat on expectations, nevertheless Asia-Pac indices remained mixed as risk-off sentiment prevailed. ASX 200 (+0.2%) was lifted by strength in commodity-related stocks but with gains capped due to weakness in the largest weighted financials sector amid anticipation of a lower rate environment and with AMP shares heavily pressured after it received compliance orders from the financial regulator APRA. Nikkei 225 (+0.4%) was also underpinned by the mining sectors which saw Chiyoda as the biggest gainer, while Sony shares were also bolstered after activist investor Loeb called on the Co. to spin off its semiconductor business. Elsewhere, Hang Seng (-0.7%) was subdued and Shanghai Comp. (-1.0%) was indecisive amid trade uncertainty and after the PBoC’s efforts resulted to a net weekly injection of CNY 65bln vs. last week’s CNY 320bln net drain. Finally, 10yr JGBs followed suit to the recent upside in T-notes, while the BoJ was also present in the market with today’s Rinban operation heavily concentrated in the belly of the curve.

Top Asian News

Indonesia on Alert as Court Hears Prabowo’s Election Challenge

As Trade War Hits, China Factories See Slowest Growth Since 2002

Japan Display Is Likely to Miss Friday Deadline for Bailout

Turkey Work Underway to Counter U.S. Sanctions, Official Says

Major European indices are mostly lower [Eurostoxx 50 -0.4%], with the exception of the SMI (+0.2%), as the region temporarily side-lines the prospect of Fed rate cuts and succumb to the risk-off sentiment as a result of rising US tensions with China, Russia, Germany, Iran, Turkey and India. Sectors are largely in the red with defensive stocks faring better, gains in the healthcare sector are keeping the SMI afloat. Meanwhile, IT names plumbed the depths with the sector heavily underperforming after a warning from Broadcom regarding a slowdown in global chip demand. As such, Infineon (-5.1%), STMicroelectronics (-4.0%), Dialog Semiconductor (-3.1%), ASML (-3.0%) and ASM (-2.7%) are all near the foot of the Stoxx 600. On the flipside, Scor (+2.6%) and Royal Mail (+2.0%) are in positive territory amid positive broker moves.

Top European News

Kier Tumbles After Report Some Credit Insurers Withdraw Cover

Buffett’s Berkshire, Engie Drive Europe’s Bond Sales Bonanza

Finance Chiefs Agree on Euro-Area Budget But Skirt Funding

Spain’s Sabadell Is Said to Weigh Sale of Consumer Finance Unit

In FX, the Dollar index continues respect resistance above the psychological 97.000 level (on a closing basis) and ahead of the recent range top at 97.370, as safer currency havens outperform amidst heightened geopolitical and global trade tensions. Moreover, the Dollar remains capped by growing expectations that the Fed will flag a rate cut next week following a run of macro data pointing to a more pronounced slowdown in the economy and benign inflation that that challenges the transitory theory put forward by Powell and other at the last FOMC gathering. On that note, impending retail sales and ip reports could cement an ease in July if not this month. DXY currently relatively contained within a 97.154-96.942 range.

JPY/SEK – The Yen has nudged back up towards 108.00 vs the Buck, and is only really lagging behind Gold in the aforementioned risk-off climate plus the Swedish Krona in the G10 stakes due to firmer than forecast CPI and CPIF metrics that keeps the Riksbank on track to raise the repo. However, Usd/Jpy is still encountering underlying bids ahead of the big figure and may also be propped by decent option expiry interest between 108.00 and 108.15 (1 bn). Back to Scandinavia, Eur/Sek has extended post-inflation data declines through technical support at 10.6500 (10 DMA) and briefly below 10.6400 vs 10.7100+ at one stage.

NZD/AUD – The major losers yet again, and with the Kiwi now underperforming after NZ manufacturing PMI only just held above the 50.0 threshold. Nzd/Usd has slipped under 0.6550 towards 0.6525 and Aud/Nzd is pivoting 1.0550 even though the Aussie has relinquished the 0.6900 handle and chart support a pip below amidst another round of more aggressive RBA policy easing calls (NAB now predicting 3 cuts in 2019 from 2 previously and RBC reckons the OCR will be lowered to 0.5% by May next year).

EUR/CAD/CHF/GBP – All lower against the Greenback as well, albeit to a lesser extent compared to the Antipodean Dollars and to varying degrees. The single currency is retreating further from 1.1300 where massive expiries run off (4.4 bn) and the Loonie has reversed to test support ahead of 1.3350 having lost some of Thursday’s oil-powered momentum as crude prices simmer down after the post-tanker attack spike. Meanwhile, the Franc has pared gains across the board with Usd/Chf at the upper end of a 0.9966-26 band and Eur/Chf back above 1.1200 on SNB reflection (renewed and reemphasised convictions to keep NIRP or even cut deeper and continue intervention). Elsewhere, Cable has is now pivoting 1.2650 with independent bearish impulses from the ongoing UK political hiatus and resultant suspension of any real Brexit developments, but BoE Governor Carney may provide some additional impetus later.

EM – No respite for the Lira it seems as Usd/Try rallies through 5.9000 to 5.9300+ and not far from chart resistance around 5.9500, including a 50% Fib of the retracement from last month’s highs to earlier June lows. The latest catalyst, warnings from Turkey’s Foreign Ministry that any US sanctions will be reciprocated.

The energy complex is poised for a weekly loss as the two tanker attacks off the coast of Oman only provided brief reprieve for the declining prices, with trade woes and rising US supply outweighing concerns in the Middle East. This morning also saw the release of the IEA monthly report in which the agency cut their outlook on oil demand growth by 100k BPD, which is in-fitting with the OPEC (70k BPD) and EIA (160k BPD) downgrades to oil demand growth for 2019 released earlier in the week. The report also noted that OPEC supply in May fell to the lowest since 2014 due to Iranian sanctions, in which Iranian oil production fell to the lowest since the 1980s. WTI and Brent are lower on the day and currently pressured by the continuation of the risk aversion. Elsewhere, gold has continued to advance as the yellow metal benefits from the risk-off sentiment, with prices now above the key USD 1350/oz ahead of strong trend-line resistance at USD 1358.50/oz. The rally in gold has spilled into other precious metals with silver hitting one-week highs and platinum gaining almost 1%. In terms of base metals, copper remains subdued amid the broad risk tone whilst Dalian iron ore touched new record highs as Chinese steel mills kept demand steady for the metal

US Event Calendaar

8:30am: Retail Sales Advance MoM, est. 0.6%, prior -0.2%; Retail Sales Ex Auto and Gas, est. 0.4%, prior -0.2%

9:15am: Industrial Production MoM, est. 0.2%, prior -0.5%; Manufacturing (SIC) Production, est. 0.1%, prior -0.5%

10am: U. of Mich. Sentiment, est. 98, prior 100; Current Conditions, est. 109, prior 110; Expectations, est. 92, prior 93.5

10am: Business Inventories, est. 0.5%, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

Bloomberg have a competition on their terminals to predict every match in the Cricket World Cup. Unbeknown to me, my co-authors Craig and Quinn entered. I didn’t realise it was on until too late. Craig, like myself, is a cricket fan. Quinn is an American who knows nothing about cricket and a week or so ago made himself a laughing stock on our team by predicting that around half the games in this tournament would be ties. For those not familiar with one day cricket, a tie probably occurs every several hundred games. However two weeks into the tournament Quinn is near the top of the leaderboard as what we didn’t appreciate is that many of the games he marked as a tie would be rained off and giving him technically the correct answer. He has therefore had an uncanny knack of predicting our awful weather this past week. So for those that want a UK weather forecast, please have your umbrella to hand between these dates as Quinn has predicted another series of ties around then: June 22-26.

Predicting the daily swing in oil prices is proving to be one of the main challenges in markets at the moment. Indeed one day after Brent dipped -3.72% and to a five-month low, it recovered much of these losses in a single swing yesterday after bouncing back +2.37%. The catalyst was the attacks on tankers in the Gulf of Oman, the second attack in a month near the Strait of Hormuz chokepoint, which has led to fears that accelerated hostilities in the region are to return. The US Secretary of State blamed Iran for the attacks, in comments that President Trump subsequently retweeted, and overnight the US released a video demonstrating Iran’s involvement, saying an Iranian boat removed an unexploded mine from a US ship. US officials also suggested that a military response has not been ruled out. Separately, data from the US Energy Information Administration showed that in March, the US imported the lowest amount of crude oil from OPEC countries since March 1986, continuing a decade-long trend of lower US crude oil imports from the OPEC countries.

Unsurprisingly anything linked to oil benefited yesterday. The S&P energy sector rose +1.25% which carried the S&P 500 to a +0.41% gain, while the NASDAQ and DOW closed +0.57% and +0.39% respectively. The STOXX 600 finished +0.16%, with the DAX outperforming (+0.44%). Despite the geopolitical noise, the VIX traded fairly flat at 15.75. Interestingly, govies were actually better bid too with 2y and 10y Treasuries ending -4.7bps and -3.0bps lower respectively, sending the former to its lowest level since December 2017. So the simultaneous equity and rates rally was back in full force. In Europe 10y Bund (-0.5bps) and OAT (-0.2bps) yields edged lower, but the real action was in the periphery. Spanish 10y yields slid -3.1bps to a new all-time low of 0.537%, while BTPs rallied -7.7bps following strong demand at the 20-year auction. The latter move came despite increased political tension in Italy, where Deputy PM Salvini reportedly told his supporters to “be ready” for a possible early election.

One of the drivers for the rally in European bonds has been expectations for more accommodative policy from the ECB. DB’s Mark Wall has updated his forecasts in this note to reflect the latest macro information and the recent update to DB’s Fed call. In short, two trends are developing in ways that will push the ECB toward easing: escalation in the trade wars and a change in the relative monetary policy stance now that the Fed looks likely to cut rates this year. Mark now expects the ECB to cut its deposit facility rate at the September meeting, and anticipates 2020 growth to decelerate to 1.0% as a result of the anticipated slowdown in US growth. Similarly, DB’s China team has revised down their 2019 and 2020 growth forecasts by 0.1 and 0.2pp respectively, to 6.2% and 5.8%, also mostly as a function of lower expected US growth. If the trade war evolves as we expect, the PBoC is likely to ease rates policy and allow the yuan to weaken to as far as 7.3 versus the dollar. Zhiwei’s full China update is available here .

This morning in Asia equity markets are mostly trading lower. Although Japanese markets have pared back opening losses to trade higher, with the Nikkei +0.29%, elsewhere the story is less positive. The Hang Seng (-0.57%) is currently on track for a third consecutive move lower, while the Shanghai Comp (-0.26%) and the Kospi (-0.25%) have also lost ground. We should note that we’re still due to get China’s May activity indicators data. Bloomberg suggests that the data is out at 8am BST. For what it’s worth, fixed asset investment and industrial production are both expected to hold steady, however retail sales is expected to rise in year over year terms. This will probably dictate much of today’s mood. The other breaking news overnight that we’re just seeing is the AFP news agency reporting that French finance minister Le Maire has said that EU ministers have agreed to President Macron’s proposal for a Eurozone budget, although with no other information at present the question for markets will be how substantive this agreement actually is. President Macron has been previously disappointed by the reluctance of a number of northern European countries to set up a Eurozone budget as large as he’d like.

Back to yesterday and while there wasn’t a great deal of other news to digest for markets, we did have the first Conservative Party leadership contest which revealed overwhelming support for Boris Johnson in his bid to become the next PM. He took 114 votes with Jeremy Hunt a reasonable way back in second place at 43 votes. Gove, Raab, Javid, Hancock and Stewart all made it through to the next round which is due to take place next Tuesday, and where candidates will need to secure 33 votes (10% of the total). Brexiteers Leadsom and McVey were eliminated yesterday along with Harper. The BBC’s political editor Laura Kuenssberg tweeted last night that Health Secretary Hancock was “mulling over” whether to continue in the race, having come in 6th place with 20 votes. It’s clear from the first round that Johnson is the clear frontrunner and although history tells you frontrunners often don’t win the Tory leadership race it’s hard to see him being toppled outside of an “event” that derails his campaign. Sterling bounced a bit following the results before closing a touch weaker at -0.10%.

In US politics, no developments were immediately market-moving, but the White House did say that “we’re moving in that direction” with regards to a Trump-Xi meeting at the G20. Top economic advisor Larry Kudlow said that “President Trump has indicated his strong desire for a meeting (…) if the meeting doesn’t come to bear, there may be consequences.” So that event, set to start two weeks from today, will be key. Away from the China conflict, the passage of the USMCA deal (to replace NAFTA) still looks precarious, as Canadian Foreign Minister Freeland said that talks are “on the right track” but stopped short of giving a timeline for ratification.

As for the data, in the US the latest weekly claims reading ticked up to 222k and a little more than expected to a five-week high. The import price index meanwhile declined more than expected in May, by -0.3% mom at both the headline and core level. Previous dollar strength appeared to explain much of the weakness in non-petrol prices.

Prior to this, in Germany there were no final surprises in the May CPI report where the headline reading was confirmed at +0.3% mom and +1.3% yoy. Elsewhere, industrial production for the Euro Area in April was confirmed as declining -0.5% mom, as expected.

To the day ahead now, where this morning we’ll get the final May CPI revisions for France and Italy. Bisecting that data is the China May activity indicators while in the US this afternoon the main highlight should be the May retail sales report, while May industrial production, April business inventories and the preliminary June University of Michigan consumer sentiment survey are also due. Away from that we’re due to hear from the BoE’s Carney this afternoon.

via ZeroHedge News http://bit.ly/2KiOwXY Tyler Durden

After senior American senators introduced legislation on Thursday requiring that the US president to protect Americans from the effects of the proposed Hong Kong extradition law and sanction individuals responsible for abducting booksellers, journalists and activists, senior Chinese officials on Friday were predictably less than thrilled.

And while more Hong Kong officials urged the government to ‘pause’ the process for passing the extradition bill, senior Chinese officials have reportedly summoned officials from the US embassy in Beijing to issue a stern warning to Washington not to interfere in the situation in Hong Kong

CHINA’S FOREIGN MINISTRY SAYS LODGED STERN REPRESENTATIONS TO U.S. REGARDING HONG KONG

CHINA’S FOREIGN MINISTRY SAYS SUMMONED SENIOR U.S. EMBASSY OFFICIAL IN BEIJING

CHINA’S FOREIGN MINISTRY SAYS URGES U.S. TO STOP INTERFERING IN HONG KONG AFFAIRS IMMEDIATELY

CHINA’S FOREIGN MINISTRY SAYS URGES U.S. TO NOT TAKE ACTIONS THAT HARM HONG KONG’S PROSPERITY AND STABILITY

CHINA’S FOREIGN MINISTRY SAYS CHINA RESOLUTELY OPPOSED TO U.S. INTERVENTION IN HONG KONG

The news helped push the dollar higher, and it’s certainly not helping bolster the market’s appetite for risk.

via ZeroHedge News http://bit.ly/2XLnw6D Tyler Durden

It sounds like the setup for a terrible gag: How many Democrats can you squeeze on to a debate stage?

Well, the DNC is about to find out.

According to Bloomberg, the DNC has unveiled the list of candidates who will take part in the first presidential primary debates of the 2020 election.

The group of 20 ‘finalist’ candidates will be split into two groups of ten, and each will perform in one of the two ‘first round’ debates to be held in Miami on June 26 and June 27. Each group will be selected ‘at random’, with a proper mix of high- and low-polling candidates.

To qualify for the debate, the DNC required candidates to show a threshold of at least 1% support in major polls, or 65,000 individual donations from at least 20 states. If more than 20 candidates qualified, the DNC would decide who to cut (which would have given them a great excuse to get rid of Bernie before things start getting out of hand like they did during the last go-round).

Here’s the final list of contenders:

Joe Biden, former vice president

Elizabeth Warren, U.S. senator from Massachusetts

Bernie Sanders, U.S. senator from Vermont

Pete Buttigieg, South Bend, Indiana, mayor

Kamala Harris, U.S. senator from California

Beto O’Rourke, former U.S. congressman from Texas

Cory Booker, U.S. senator from New Jersey

Kirsten Gillibrand, U.S. senator from New York

Michael Bennet, U.S. senator from Colorado

Amy Klobuchar, U.S. senator from Minnesota

Tim Ryan, U.S. congressman from Ohio

Eric Swalwell, U.S. congressman from California

Tulsi Gabbard, U.S. congresswoman from Hawaii

Jay Inslee, Washington governor

John Hickenlooper, former Colorado governor

Julian Castro, former secretary of Housing and Urban Development

Bill de Blasio, New York City mayor

John Delaney, former U.S. congressman from Maryland

Andrew Yang, entrepreneur

Marianne Williamson, spiritual healer

The unfortunate few who did not qualify for the debate are: Montana Governor Steve Bullock; Miramar, Fla. Mayor Wayne Messam and Congressman Seth Moulton of Massachusetts.

Clearly overcompensating because it’s still rattled by how it shot itself in the foot by favoring Hillary Clinton over Sanders during the last go-round, the DNC insisted that its methodology for choosing the debate participants was transparent, and as inclusive as possible.

“Each candidate was invited based on the qualification criteria agreed to by the DNC and NBC News, announced publicly in February,” the committee said in a statement.

Of course, by allotting so many candidates to participate, it virtually guarantees that the party’s ‘frontrunners’ – Bernie Sanders and Joe Biden – likely won’t get as much air time and attention as they should, given their hopes for taking on President Trump, who has the media’s full attention (as well as its scrutiny).

via ZeroHedge News http://bit.ly/2XaDXfx Tyler Durden

Are Hong Kong’s student demonstrators winning the battle to kill the hated extradition bill? It’s starting to look that way…

According to the South China Morning Post, the city’s largest English language newspaper, the city council are considering ‘pausing’ their plans to pass the bill – which would likely slow, but not stop, the process.

This comes after dozens were injured and nearly one dozen arrested on Wednesday, the most violent day of the protests so far. The city’s advisors are reportedly “torn”, with some advocating that city executive Carrie Lam offer a sop to the protest movement that has badly shaken the city, while others believe the government must push ahead with its plans.

Bernard Chan, the counsel’s non-official convenor, said it would be “impossible” to rush the amended legislation through, while city executive Carrie Lam Ching-choi and Fanny Law Fan Chiu-fun have both advocated taking a step back.

Advisors also said they had underestimated the backlash from the business community over the bill and the public’s violent reaction, which brought the city to a standstill as thousands occupied critical motorways.

Of course, nobody wanted to see the city’s legislature “paralyzed” by a single piece of legislation either.

“What happened on Wednesday is saddening and is not something that we would want to see,” Chan said in a radio phone-in programme.

“We indeed need to review what to do.”

“Our first task right now is on how to mollify the public to avoid more clashes in future.”

A group of 22 former lawmakers, meanwhile, sent Lam a letter imploring her to withdraw the unpopular bill immediately, and exhorting her advisors to resign if it isn’t abandoned. In the letter, the former lawmakers asked Lam to listen to Hong Kong’s “future generation” – that is, the students who have been flooding the streets and getting embroiled in scuffles with police.

Signatories included former secretary for security Peter Lai Hing-ling, former chief secretary Anson Chan Fang On-sang, former deputy secretary for economic services Elizabeth Bosher and former Legco Senior Member Allen Lee Peng-fei. Ultimately, the letter asks why the bill must be rushed through the process when so many are asking for more time for the legislature to review it.

“This is our future generation to be cherished, how can anyone with a heart not be pained to see the treatment they received?” the statement read.

“A deeply divided society, serious concerns of the international community – are these the sacrifices to be made to satisfy the will of the chief executive? What great public interest is supposed to be served by the hurried passage of this Bill?”

“We call on the chief executive to yield to public opinion and withdraw the Bill for more thorough deliberation. We call on her governing team, including all principal officials and members of the Executive Council to do their duty to advise her so to do. Should their advice be ignored, we call upon them to resign.”

The former security secretary who drafted the existing extradition law, meanwhile, said both sides needed to take a step back and reassess and cool down. Withdrawing the bill temporarily would be one way to accomplish this.

Of course, with Beijing breathing down its neck, the notion that the city council will simply ‘back down’ in the face of public pressure seems a little far-fetched, no matter how violent the protests become.

via ZeroHedge News http://bit.ly/2MOstL1 Tyler Durden

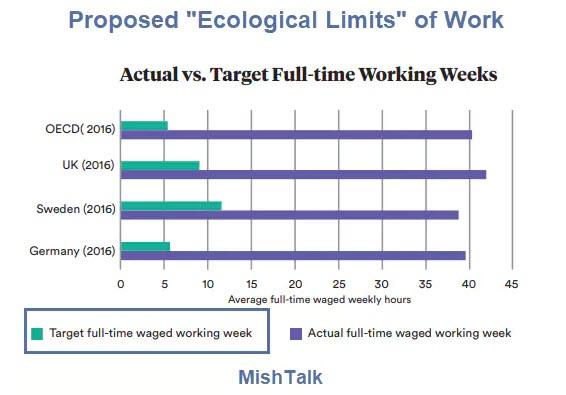

It’s the Labour party shadow chancellor, McDonnell, who supports 10 hours.

Vital Contribution

Shadow Chancellor John McDonnell, who has previously backed a four-day working week, said: ‘This is a vital contribution to the growing debate around free time and reducing the working week.’

Leo Murray, adviser to Shadow Treasury minister Clive Lewis, said: ‘I like this take a lot.’

Following Jeremy Corbyn’s election as Labour leader in 2015, he appointed McDonnell as his Shadow Chancellor. Alongside Corbyn, McDonnell has been seen as a key figure on the left-wing of the party. As Shadow Chancellor, McDonnell pledged to increase spending on infrastructure and research, describing his vision for the economy as “socialism with an iPad“.

An Honest Marxist

In 2006, McDonnell said that “Marx, Lenin and Trotsky” were his “most significant” intellectual influences. Footage emerged of McDonnell in 2013 talking about the 2008 global financial crisis and stating, “I’ve been waiting for this for a generation! We’ve got to demand systemic change. Look, I’m straight, I’m honest with people: I’m a Marxist.”

Green Revolution

The Government continues to fail on climate change.

And even some of the Tory leadership candidates have close links to climate change denial.

The inspiration for this obviously mad work time limit is a publication by Philipp Frey: The Ecological Limits of Work.

Supposedly, a “1 percent decrease in working hours could lead to a 0.8 percent decrease in GHG emissions.“

That is not enough to save the planet, but a 75% net reduction reduction in hours worked, varying by country, along with other improvements, allegedly will.

The Government continues to fail on climate change.

And even some of the Tory leadership candidates have close links to climate change denial.

Sweden needs to reduce hours worked by about 70%, Germany by about 86%, and the UK by about 75%.

The study claims “Actual working hours levels vastly exceed the levels that might be considered sustainable.”

Unfortunately, “Working time reduction as an isolated policy by itself will likely be insufficient to combat climate change.”

The report concludes “In addition to shortening the working week quantitatively and pushing for a substantial reconfiguration of the economy, a more qualitative approach to a politics of time might also be needed.“

Just when you thought the global warming madness could not quickly get any nuttier, it quickly got nuttier.

If you support Labour leader Jeremy Corbyn who praises the economic model of Venezuela or McDonnell, a Marxist who embraces a 10-hour work week, your head is not screwed on straight.

via ZeroHedge News http://bit.ly/2Xg4GaA Tyler Durden

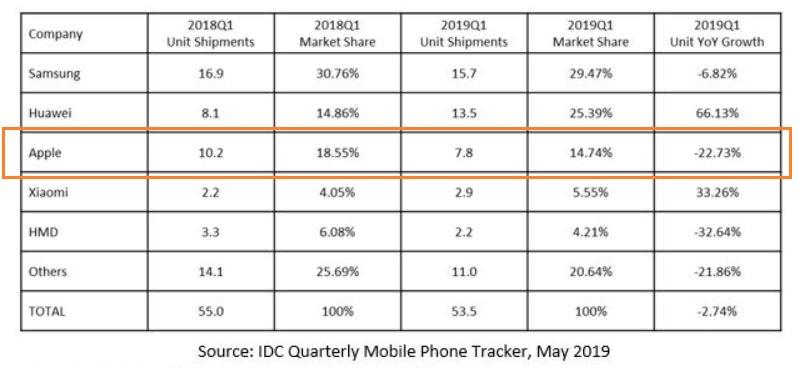

A new report from the International Data Corporation’s (IDC) latest Quarterly Mobile Phone Tracker shows Chinese smartphone makers are solidly outperforming Apple and Samsung across European markets.

Huawei and Xiaomi, two of China’s top smartphone producers, recorded YoY unit sale increases for all regions across Europe in 1Q19, while all other major smartphone companies experienced declines.

Huawei’s unit shipment in Europe jumped 66% YoY in 1Q19, while Xiaomi increased 33% YoY. During the same period, Samsung’s unit shipments dropped 7%, while Apple’s unit sales plummeted by 23%.

“In brands, Huawei continued to make incremental advances, and so did Xiaomi, while Apple had a tough quarter, with its 23% market share across Europe the lowest Q1 result in five years,” said Marta Pinto, research manager at IDC EMEA.

“The market has been changing in the last few quarters in relatively predictable ways,” said Pinto. “Shipments have slowed as consumers hold on to devices for longer, Apple has been challenged with its latest devices, and Chinese manufacturers have been making strides each quarter.”

Simon Baker, program director at IDC EMEA, said, “Europe has been a global focus of vendor concentration in recent quarters, with some of the smaller players under a lot of pressure. Looking ahead, it is no longer possible to see clear trends as before. The blacklisting of Huawei in the U.S. on May 16 is creating so many unknowns, and uncertainty is the new keyword in the industry as global geopolitics — unconnected directly with Europe or EMEA — becomes the single most important factor in how the market will develop over the rest of the year.”

Overall EMEA shipments reached 83.7 million units in 1Q19, a 3% drop YoY — confirming the smartphone slowdown isn’t just gaining momentum as the world continues to cycle down through summer, but Chinese smartphone makers have displaced Apple and Samsung as the top players in Europe.

via ZeroHedge News http://bit.ly/2RoQQ0x Tyler Durden

Since the idea was first floated there has been rampant speculation about how/when Lega Leader Matteo Salvini would introduce the Mini-BOT parallel currency to assist Italy’s fiscal situation.

The mini-BOT or Mini-Bill of Treasury, is a small denomination bond that the treasury can sell which can be used by businesses and people as an alternative domestic currency.

As Mike brings up, without mandating their usage Italy skirts the letter of EU law prohibiting any country from issuing its own currency.

The big question is, will there be a bid for these mini-BOTs? Very likely. Relative to the Italian economy the euro is over-valued, it is too strong. But the euro would be under-valued relative to a mini-BOT trading at par to the euro.

And Gresham’s Law tells us that under-valued currencies are driven from the market and hoarded while over-valued ones circulate. It’s important to dispense with the “bad money drives out good money” idea. It clouds the analysis.

And with the Italian government then saying that they will take the mini-BOT or euros for payments of taxes and fees, now they have a bid. They can then circulate within the Italian economy while scarce euros are preferentially put to use in settling international trade.

The EU is, of course, dead set against this and ECB President Mario Draghi called this proposal illegal. But that’s irrelevant. The real threat to Salvini’s plans here, which is what Italy needs, is within his own government.

Mike rightly points out that Salvini’s Prime Minister Giuseppe Conte is a technocrat. I’ll go one further and remind you what I wrote last week, that Conte, President Sergei Mattarella and Finance Minister Giovanni Tria represent a Troika of Technocrats that work for Brussels and not Rome.

Where I disagree with Mike in his analysis is the political fallout, not the economic analysis.

Salvini did very well in the European parliament elections and many speculate he will trigger elections soon to get rid of di Maio and Conte.

For now, we have the strange case of deputies Salvini and di Maio at odds with Conte and the Economy Minister, Giovanni Tria.

Conte threatened last week to resign last week and he could do so at any time. “I want a clear, unequivocal and speedy response,” Conte said, calling for “loyal collaboration” from all ministers.

This government won’t last long.

The Italian Troika will be the ones who take down the current government if they do it at all. And if the mini-BOT proposal gains steam within the Italian parliament and is forced onto Tria’s table at the Finance Ministry, something has to happen.

Salvini will not take this government down. Salvini has ruled that out as long as Five Star Movement (M5S) goes along with his part of their shared agenda. They got their major plank with Universal Basic Income. Now it’s Salvini’s quid to their quo.

With Di Maio surviving a leadership vote the coalition is strong. The hardliners within M5S who would give Salvini a harder time have been beaten back.

Salvini’s best play here is to let the traitors hang themselves and let Brussels overplay their hand. Both of these things continue to happen while he keeps coming across as someone intensely interested in solving Italy’s domestic problems and leaving the bigger political problems to themselves.

So it will not be Salvini that takes down this Italian government. It will be Conte, Tria and Mattarella who will do so if they think they can get a hung parliament vote out of the Italian populous, forcing Salvini to ally with a minor party, like Silvio Berlusconi’s Forza Italia, which would have the whip hand in coalition talks.

And that could happen with the new electoral law which only appoints two-thirds of the seats via vote proportion while the other are all chosen via first-past-the-post. I don’t have a good feel for how that would shake out.

But here’s the rub. Just like in the U.K. you’ll notice Jeremy Corbyn not calling for a no-confidence vote in the Tory/DUP government. And we don’t see the DUP pulling out of the failing coalition. Why?

Because they know they would get stomped in a general election to Nigel Farage’s Brexit Party. And then they would lose their best chance to scuttle Brexit before the Tories regroup under Boris Johnson later this summer.

The same calculus is on the table for Mattarella, et. al. Would a new election gain them an advantage over a re-jiggered Lega/M5S government with Salvini as the senior partner? If the answer is no then the Italian Troika will hold the line for Brussels and use their positions to sabotage Salvini at every turn.

They will only threaten to take down the government if it strengthens their hand. In fact, I think Conte already tried that and Salvini flipped him off, Italian-style.

Moreover, I think taking down the government to keep Brussels happy is political suicide. It will only strengthen Salvini’s hand. And if Lega and M5S campaign on the same issues in parallel they could sweep in with 60+% of the vote between them and then run the table on the Italian Troika and Brussels.

Remember, Mattarella way over-stepped his authority last year when he vetoed Salvini’s first choice for Finance Minister, Paola Savona. Impeachment was discussed. Eventually Salvini gave in, nominated Tria and Conte to satisfy Mattarella and formed the government.

If a new election were to leave Lega/M5S in a stronger position and Mattarella tries to usurp power again, he could get impeached and removed from office. And that would change the entire dynamic.

Italy needs the mini-BOT or to leave the euro entirely. Salvini is right that German Austerity is killing the country, strangling it. And don’t kid yourself, that is the plan.

This is why the EU is threatening Italy with unprecedented budget fines for what amounts to $3 to $4 billion. It’s ludicrous and it shows the weakness of their hand if they are willing to go this route over such a small thing.

But that’s where their only leverage is over the government, through their hand-picked finance minister.

Mike is right that the mini-BOT is a Trojan Horse. In more ways that one. It is the issue that can force the current unstable structure of Italy’s government to its crisis point and the Italian people can then decide who really works for them.

You don’t have to go home, but you can’t stay here.

Daytime drinking, which we previously reported had become a point of contention at Lloyd’s of London, has now been banned for metals traders at the London Metal Exchange. What used to be a staple of the open outcry pit at the LME is no longer, according to Bloomberg.

In a meeting on Thursday, the LME notified its open outcry dealers that it is now expecting a zero tolerance alcohol policy for floor traders, who are responsible for setting the global benchmark prices for metals like copper and aluminum. The exchange said that they could impose fines and trading bans on individuals for breaking the rules.

The LME already bans what Bloomberg called “engaging in drunken behavior” (like buying equities?) on the floor, but this policy would go further to break the long-held correlation with open outcry traders and heavy drinking that stretches back to Victorian times.

For instance, Nigel Farage, who started his career on the trading floor before politics, has often recounted details of “his booze fueled exploits” during his career in London. It is just one account that has helped perpetuate the image of drinking being associated with being a metals trader.

Many member firms of the LME have also sought to clean up the industry’s reputation. The exchange added rules in April that would prohibit members from holding “sleazy parties” at venues such as strip clubs and casinos – because the LME isn’t a casino in and of itself, right? The ban was part of a new code of conduct, which we’re sure will likely be ridiculed as it’s passed around the table over pints at lunch by long established metals traders.

The ban also follows the zero-tolerance policy announced by Lloyd’s of London that we wrote about months ago, after Bloomberg Businessweek reported a “deep-steated culture of sexual misconduct” in the UK capital’s insurance market. The LME was previously located on the same road as Lloyd’s, and metals traders often frequented the same pubs as Lloyd’s dealers.

via ZeroHedge News http://bit.ly/2wSiXeT Tyler Durden