The House vote to establish procedures for a possible impeachment of President Trump, along party lines with two Democrats opposing and no Republicans favoring, was exactly what Alexander Hamilton feared in discussing the impeachment provisions laid out in the Constitution.

Hamilton warned of the “greatest danger” that the decision to move forward with impeachment will “be regulated more by the comparative strength of parties than the real demonstrations of innocence or guilt.” He worried that the tools of impeachment would be wielded by the “most cunning or most numerous factions” and lack the “requisite neutrality toward those whose conduct would be the subject of scrutiny.”

It is almost as if this founding father were looking down at the House vote from heaven and describing what transpired this week. Impeachment is an extraordinary tool to be used only when the constitutional criteria are met. These criteria are limited and include only “treason, bribery, or other high crimes and misdemeanors.” Hamilton described these as being “of a nature which may with peculiar propriety be denominated political, as they relate chiefly to injuries done immediately to the society itself.”

His use of the term “political” has been widely misunderstood in history. It does not mean that the process of impeachment and removal should be political in the partisan sense. Hamilton distinctly distinguished between the nature of the constitutional crimes, denoting them as political, while insisting that the process for impeachment and removal must remain scrupulously neutral and nonpartisan among members of Congress.

Thus, no impeachment should ever move forward without bipartisan support. That is a tall order in our age of hyperpartisan politics in which party loyalty leaves little room for neutrality. Proponents of the House vote argue it is only about procedures and not about innocence or guilt, and that further investigation may well persuade some Republicans to place principle over party and to vote for impeachment, or some Democrats to vote against impeachment. While that is entirely possible, the House vote would seem to make such nonpartisan neutrality extremely unlikely.

It is far more likely that, no matter how extensive the investigation is and regardless of what it uncovers, nearly all House Democrats will vote for impeachment and nearly all House Republicans will vote against it. Such a partisan vote would deny constitutional legitimacy to impeachment. It was because of this fear of partisanship in the House that the framers left the ultimate decision to remove an official to the Senate. The framers intended the Senate, which was not popularly elected at the time the Constitution was written, to be less partisan and act more like judges.

The Supreme Court chief justice presides over the Senate removal trial of a sitting president, and adding that key judicial element would seem to demonstrate a desire by the framers to have a presiding officer whose very job description is to do justice without regard to party or person. In both of the previous removal trials of President Johnson and President Clinton, however, the chief justice played a traditionally symbolic role.

If President Trump is impeached, it is certainly possible that his lawyers would ask Chief Justice John Roberts to play a more substantive role. If the grounds for impeachment designated by the House include criteria such as maladministration or corruption, his lawyers could plausibly demand the chief justice to dismiss the charges as unconstitutional.

After all, the framers explicitly rejected maladministration as a ground for impeachment and removal. James Madison, the father of our Constitution, argued that such open criteria would give Congress far too much power to remove a duly elected president. It would, he feared, turn our republic into a democracy in which the chief executive served at the pleasure of the parliament and could be removed by a simple vote of no confidence.

How many times have we heard from Democrats that “no one is above the law” in reference to President Trump? That is true, but neither is Congress above the law. It cannot substitute its own criteria for those mandated by the Constitution. The House vote may have been necessary to establish procedures. But the partisanship strongly suggests that what Hamilton regarded as the greatest danger may be on the horizon, namely a vote to impeach a duly elected president based not on “real demonstrations of innocence or guilt” but rather on “comparative strength of parties.”

“What Are You Thinking?”: Pelosi Warns 2020 Candidates They’re On The Wrong Track

House Speaker Nancy Pelosi thinks Democrats running for president in 2020 might strike out against Trump with ultra-liberal policies that fire up the party’s progressive base, yet might not go over so well with swing voters in flyover states.

Proposals pushed by Elizabeth Warren and Bernie Sanders like Medicare for All and a wealth tax play well in liberal enclaves like her own district in San Francisco but won’t sell in the Midwestern states that sent Trump to the White House in 2016, she said. –Bloomberg

“What works in San Francisco does not necessarily work in Michigan,”Pelosi said in a wide-ranging interview with Bloomberg. “What works in Michigan works in San Francisco — talking about workers’ rights and sharing prosperity.”

“Remember November,” she added. “You must win the Electoral College.”

And while she didn’t back any particular candidate running for office, Pelosi said Democrats should be focusing on “lower costs of prescription drugs, bigger paychecks by building infrastructure, and cleaner government.“

She also worries that candidates like Warren and Sanders are going down the wrong track by trying to ‘out-left’ each other to court fellow progressives while abandoning moderate voters that the party needs to win back from Trump.

“As a left-wing San Francisco liberal I can say to these people: What are you thinking?” Pelosi said. “You can ask the left — they’re unhappy with me for not being a socialist.“

Pelosi also expressed concerns that voters don’t care about the Green New Deal promoted by Bernie Sanders and Elizabeth Warren, which calls for rapid, radical reductions in carbon emissions.

“There’s very strong opposition on the labor side to the Green New Deal because it’s like 10 years, no more fossil fuel. Really?” said Pelosi.

The speaker’s concerns reflect those of many Democratic leaders and donors who believe that left-wing policies will alienate swing voters and lead to defeat.

Warren and Sanders are betting on a different theory — that voters who float between parties are less ideological and can be inspired to vote for candidates who represent bold new change in Washington.

Pelosi said Democrats should seek to build on President Barack Obama’s Affordable Care Actinstead of pushing ahead with the more sweeping Medicare for All plan favored by Warren and Sanders that would create a government-run health care system and abolish private insurance. –Bloomberg

Instead, Pelosi says Democrats need to salvage Obamacare:

“Protect the Affordable Care Act — I think that’s the path to health care for all Americans. Medicare For All has its complications,” she said, adding that “the Affordable Care Act is a better benefit than Medicare.”

Warren on Friday announced that her Medicare for All plan would cost $52 trillion (raising federal spending by $20.5 trillion over 10 years), and would be funded through a wave of taxes on large corporations, the wealthy, cracking down on tax evasion, an $800 billion reduction in defense spending, and putting newly legalized immigrants on the tax rolls. The Biden campaign called her plan “mathematical gymnastics” which would raise taxes on the middle class. Warren hit back, accusing Biden of “running in the wrong presidential primary.”

“Democrats are not going to win by repeating Republican talking points,” Warren said while speaking in Des Moines, Iowa. “So, if Biden doesn’t like that, I’m just not sure where he’s going.”

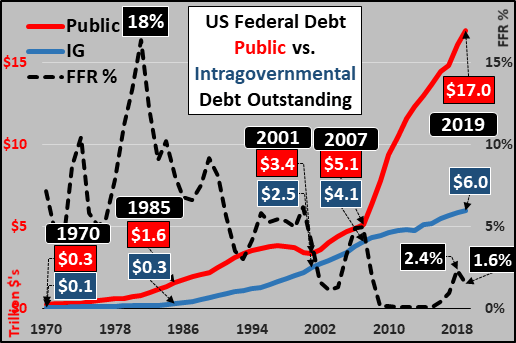

Today, the annual issuance of Treasury debt crossed the $1 trillion mark for the 2019 calendar year (crossing $23 trillion with two months still to go). Below, surging public (marketable) debt, slowing intragovernmental (Social Security and other trust funds) deb, versus the Federal Funds Rate (cost of short term money).

The fact that all that Treasury issuance has come in the last three months should be noteworthy, but heck, the Treasury had some catching up to do after another debt ceiling impasse!?! Still, over the same period, the Federal Reserve has cut interest rates by 35%. Over that same period, the Fed has ceased QT, pivoted, and initiated some of the most aggressive QE we have yet seen. This has increased the Fed’s balance sheet over $260 billion in just over two months, since the Fed’s pivot of late August. Over the same period, the Fed has engaged in the most aggressive monetization of debt (decreasing bank held excess reserves against increasing Fed assets) we have seen since the depths of 2009?!? Suffice it to say, these are not signs of strength or confidence but instead signs of panic. But why???

But before I answer that, this is also a big day for me and my blog. My blog, Econimica, is about to pass 1 million reads (and my articles re-posted gratis elsewhere thanks to ZeroHedge, DollarCollapse, GoldSilver, Ricefarmer, 321Gold, TheSoundingline, TheAutomaticEarth, etc. have long passed 10 million reads). Glamorous as the life of a blogger is, I can’t say if the reason I only make $2 per article on my blog is because I drink too much or if my drinking is a coping mechanism for only making $2 an article?!? All I can say is I create content that answers my own questions and these sites seem to appreciate this (for FREE). I have nothing to sell, make no suggestion for purchases, and offer no advice. I simply provide the data and hope able minded persons will come to their own conclusions. But on this momentous occasion, I thought I’d take the uncharacteristically sober opportunity to suggest what is happening and why.

For hundreds or even thousands of years, the study of demographics (statistical data relating to the population and groups within it) was a sleepy backwater somewhat akin to watching the grass grow. So much so that economists no longer bothered themselves with the minutiae involved. Economists built models (assuming demographics would forever remain static) on the idea that if ever more capital was freed, more supply would be created, and rising demand would consume ever more.

However, at this point in time, the changing demographics are everything. If you don’t understand the demographics, you really don’t understand what is happening and why previous economic theories no longer make sense.

To put it simply, certain populations (wealthier) and certain age groups (wealthier working age adults) do the vast majority of consuming and undertake the vast majority of new loans (debt) which pushes the quantity of “money” and consumer demand ever higher. But today I detail that growth (where it counts) is at an end among the populations and age groups that drive demand. The net result is the end of rising consumption, rising credit, and the rising growth in “money”.

In our fractional reserve system, something like 10% of deposits are held back and the remaining 90% are loaned out. Thus, the vast majority of “money” is lent into existence via banks as customers take out new loans or credit. But again, not all customers are alike, as it is wealthier young adults and middle aged adults that undertake the bulk of new loans for homes, cars, education, etc. Conversely, elderly are generally credit averse and far more likely to pay down or pay off existing loans than to undertake new loans. This makes sense since the labor force participation rate among elderly (70+ year-olds) is about 10%, in comparison to labor force participation rates of 80%+ among 25 to 54 year-olds. So, elderly live on fixed incomes and generally live within their means. That isn’t to say that credit isn’t on the rise among the elderly, just nowhere near the levels it is utilized by the working age population (20 to 70 year-olds).

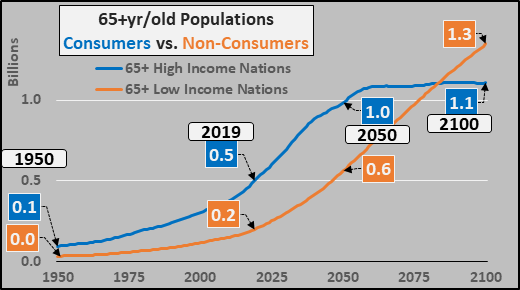

Global Picture

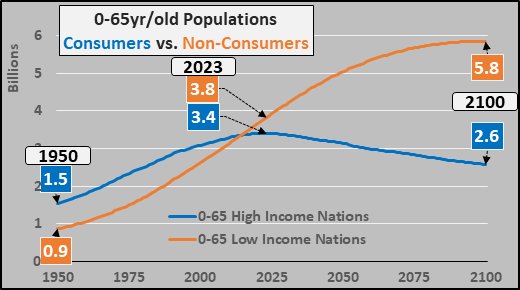

On a global basis, the chart below splits the global under 65 year-old population in half. In blue, the under 65 population of nations that make above $4,000 annually per capita (or on average above $16,000 per capita) and those making less the $4,000 (or those averaging below $1,600 per capita annually). Noteworthy is despite the large inflow of immigrants from poor nations, the global consumer population under 65 years-old will begin declining by 2023 and decline indefinitely thereafter. All population growth from there on will be among the under 65 year-old non-consumers (or poor nations) and as the next chart below shows, among the non-credit wielding wealthy and poor elderly.

Below, decelerating over 65 year-old population growth through 2050 before the wealthy elderly cease growing, leaving only the poor elderly to rise alone through 2100.

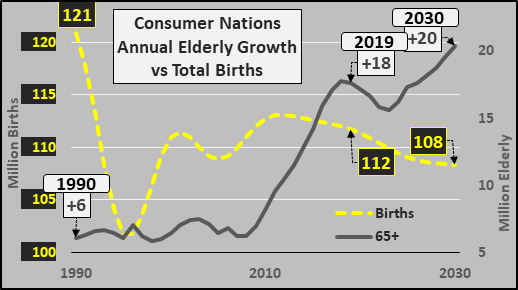

Or a single chart to detail the situation (below). Despite an influx of immigration, the total births in the wealthier half of the world have declined over 7.5% since 1990 (yellow dashed line) versus the tripling of annual growth among the wealthier nations combined 65+ year-old population. Simply put, nothing like this has happened in the last ten thousand years…and nothing like this is likely again for the next ten thousand. Aka, “the demographic moment”, the “inflexion point”, or the moment where “shit hits the wall”.

Shifting to the US

According to the Fed’s Survey of Consumer Finances HERE, 75+ year-olds are half as likely to utilize credit as the working age population, and among the half of 75+ year-olds with debt, they have less than half as much debt as the middle aged. Translated, 75+ year-olds create less than 25% the credit than that of the working age population.

So, what happens to credit creation (and growth of the money supply) when population growth slows and shifts to those least likely to undertake new loans or credit? Que the Treasury, Federal Reserve, Congress-critters, + Trump.

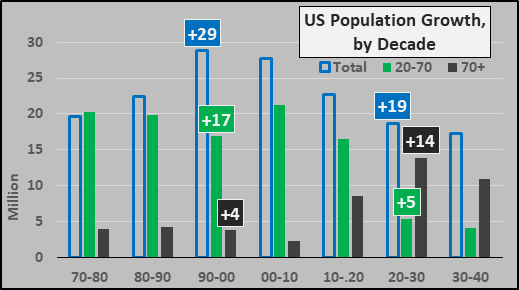

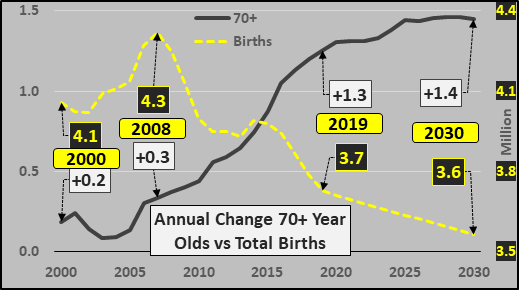

Below, US population growth in the upcoming decade will be far slower than previous decades. On a decade over decade basis, US population growth will be almost 35% slower than during peak growth seen from 1990 to 2000 (or growing about 10 million fewer than peak growth). Second, growth will shift from the working age population (20 to 70 year-olds) to the 70+ year-olds (the non-working population).

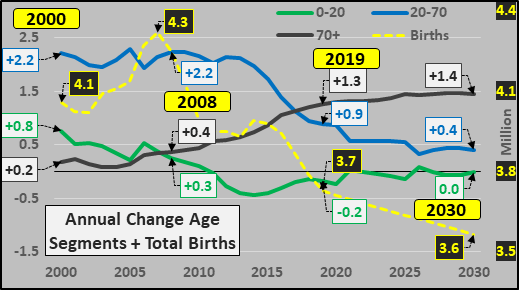

Looking at the annual population growth of the US, by age segments, plus total annual births, below. The large deceleration of growth among the working age population is plain (blue line) and the tripling of annual growth of the 70+ year-olds isn’t hard to pick out (grey line). The 14% decline in births since the ’07 peak is also noteworthy (yellow dashed line).

From 2020 through 2030, total population growth slows 20%, and 75% of what population growth remains is among 70+ year-olds…total reversal from previous decades.

Below, looking specifically at the opposite ends of the spectrum. Tanking births (yellow dashed line) versus huge growth among the elderly population (grey line), also known as an inverting pyramid…BTW, this is not a structure known for its stability (LOL)!

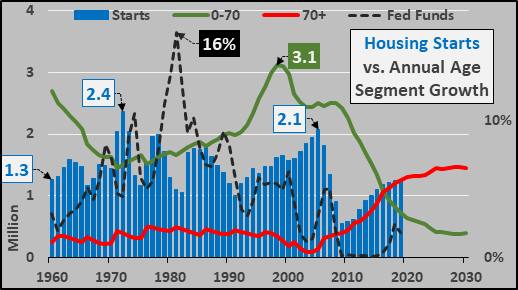

Below, looking at housing starts (blue columns), federal funds rate (black dashed line), and the annual growth of the 0 to 70 year-old (green line) versus 70+ year-old (red line) populations. The issue is minimal growth among the working age (coupled with full employment among this population) versus a deleveraging elderly population. An economy primarily driven by new housing and all that orbits new housing (infrastructure, factories, manufacturing, durable goods, etc.) is set to endure little to no organic demand growth (but of course the US federal government and the Fed can follow the Japanese or Chinese models to continue creating “bridges to nowhere” and “ghost cities” to perpetuate the inevitable).

What does this mean? This should mean that the growth of the money supply lags significantly or doesn’t grow at all. The population that typically utilizes credit is growing minimally and the population that sparsely uses credit (or net pays off debt) is growing rapidly in the US and among consumer nations. The natural outcome wouldnotbe asset inflation and bull markets…at least not organically.

But in a system where the growth of credit (“money”) is necessary simply to pay the interest, only if we look behind the veil could we see how this “bull market” is being made.

To follow through on my point of aged based credit creation, I’ll utilize the 2016 (most recent) Federal Reserve Survey of Consumer Finances (HERE), detailing the changing situation from 1989 through 2016. It is laid out juxtaposing age groups; young adults (under 35 year-olds) prime adults (45-54 year-olds) and elderly (75+ year-olds).

Utilization of Debt (Any)

First, the percentage of families utilizing debt has been consistent aside for the increased reliance among the elderly.

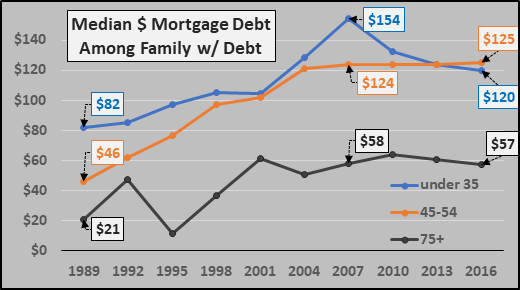

Mortgage Debt

Next, the percentage of families with mortgage debt has been declining for young and prime aged adults since 2007 while the reverse has been true among the elderly (below). However, still less than one quarter of 75+ year-olds have outstanding mortgage debt versus over half of prime aged adults.

Since 2007, median mortgage debt among those families carrying mortgages (percentages above) has decreased among the young, remained flat among the prime aged adults and elderly (below). But again, less than half the number of elderly carry mortgage debt, and those that do carry less than half of the working age or young adult populations.

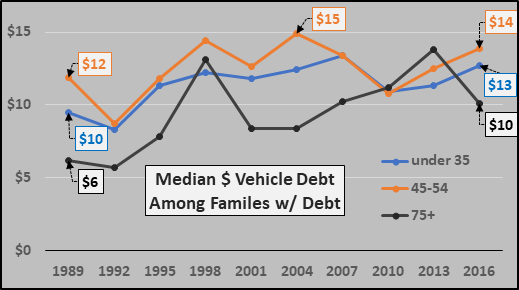

Vehicle Debt

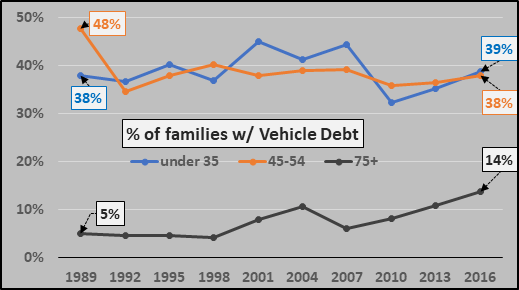

The percentage of families with vehicle debt is fairly consistent among young and prime aged adults, less than half among elderly despite gently rising.

Fairly consistent median vehicle debt among families with debt and fairly consistent accross age groups.

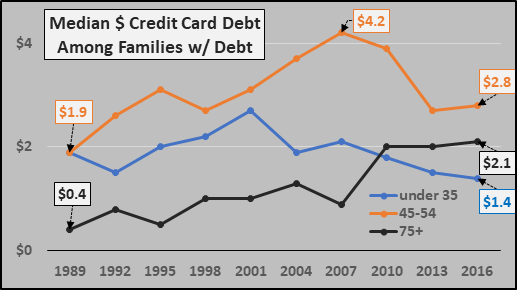

Credit Card Debt

Below, the percentage of families w/ credit car debt, by age groups. Elderly are almost half as likely to have outstanding credit card debt.

Below, median credit card debt is declining amid all segments except the elderly.

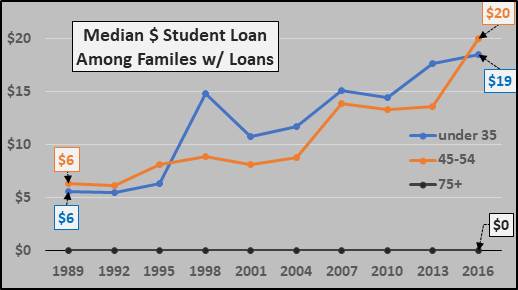

Student Loan Debt

The percentage of young adults and prime aged adults carrying student loan debt continues to crank upward (below). Of course, the percentage of 75+ year-olds with student loan debt is essentially zero. Or said otherwise, the primary vehicle for credit creation (money growth) is entirely avoided by the population that is set to experience all the growth for the next two decades!?!

Below, rising median student loan debt among students and their parents that carry student loans. As for the only population that is set to grow in abundance over the next two decades, the elderly…not so much.

Conclusion:

The very negative organic demographic outcome of a serious review of credit creation and money growth should be plain. But this is where so many have gone terribly wrong and lost gobs of money…in a centrally controlled world, bad is good! The “badder” the underlying fundamentals, the “gooder” the synthetically driven growth!!! The worse the organic situation, the more the poor are hammered and the wealthy made wealthier. The weaker the potential growth of demand, the stronger the rationale for the Fed, central banks, and federal governments to delay the inevitable. And when I say delay the inevitable, I (nor the Fed or like actors) know if this is a year, a decade, or ??? It is simply an all-in bet with nothing to cover the eventual, inevitable losses.

All population data is via UN World Population Prospects 2019.

Assad Calls Trump “Best US President” Ever For “Transparency” Of Real US Motives

Arguably some of the most significant events since the eight-year long war’s start have played out in Syria with rapid pace over just the last month alone, including Turkey’s military incursion in the north, the US pullback from the border and into Syria’s oil fields, the Kurdish-led SDF’s deal making with Damascus, and the death of ISIS leader Abu Bakr al-Baghdadi. All of this is why a televised interview with President Bashar Assad was highly anticipated at the end of this week.

Assad’s commentary on the latest White House policy to “secure the oil” in Syria, for which US troops have already been redeployed to some of the largest oil fields in the Deir Ezzor region, was the biggest pressing question. The Syrian president’s response was unexpected and is now driving headlines, given what he said directly about Trump, calling him the “best American president” ever – because he’s the “most transparent.”

“When it comes to Trump you may ask me a question and I’ll give you an answer which might seem strange. I tell you he’s the best American president,” Assad said, according to a translation provided by NBC.

“Why? Not because his policies are good, but because he is the most transparent president,” Assad continued.

“All American presidents commit crimes and end up taking the Nobel Prize and appear as a defender of human rights and the ‘unique’ and ‘brilliant’ American or Western principles. But all they are is a group of criminals who only represent the interests of the American lobbies of large corporations in weapons, oil and others,” he added.

Syrian President Assad said on Thursday that President Trump is the best type of president for a foe due to his open talk of annexing Middle Eastern oil. pic.twitter.com/B9AZdnwoRK

“Trump speaks with the transparency to say ‘We want the oil’.” Assad’s unique approach to an ‘enemy’ head of state which has just ordered the seizure of Syrian national resources also comes after in prior years the US president called Assad “our enemy” and an “animal.”

Trump tweeted in April 2018 after a new chemical attack allegation had surfaced: “If President Obama had crossed his stated Red Line In The Sand, the Syrian disaster would have ended long ago! Animal Assad would have been history!”

A number of mainstream outlets commenting on Assad’s interview falsely presented it as “praise” of Trump or that Assad thinks “highly” of him; however, it appears the Syrian leader was merely presenting Trump’s policy statements from a ‘realist’ perspective, contrasting them from the misleading ‘humanitarian’ motives typical of Washington’s rhetoric about itself.

That is, Damascus sees US actions in the Middle East as motivated fundamentally by naked imperial ambition, a constant prior theme of Assad’s speeches, across administrations, whether US leadership dresses it up as ‘democracy promotion’ or in humanitarian terms characteristic of liberal interventionism. As Assad described, Trump seems to skip dressing up his rhetoric in moralistic idealism altogether, content to just unapologetically admit the ugly reality of US foreign policy.

Ever since he announced that he was running for president, Joe Biden has been the frontrunner for the Democratic nomination. And the good news for the Biden campaign is that he is still leading in most major national polls. But the bad news is that his numbers have been steadily falling. At one point, his average level of support in national polls was over 40 percent, but now it is down to just 26.7 percent.

And the really bad news is that Biden is falling behind other candidates in Iowa and New Hampshire. In fact, according to the latest poll Biden is now in fourth place in Iowa…

Joe Biden slipped into fourth place among presidential candidates in the 2020 Iowa caucuses, behind front-runner Elizabeth Warren, Bernie Sanders and a surging South Bend, Ind., Mayor Pete Buttigieg, according to a new poll released Friday.

The Massachusetts senator polled at 22 percent, ahead of Vermont Sen. Sanders at 19 percent, Buttigieg at 18 percent and the former vice president at 17 percent, the New York Times/Siena College poll of likely participants in the caucuses showed.

This wasn’t supposed to happen.

In particular, Biden is really having a hard time getting young people behind him. At this point, he has the support of “only 2 percent of voters under 45” in Iowa.

That is abysmal.

A fourth place finish in Iowa would not be fatal for Biden as long as he came back strong in New Hampshire.

In New Hampshire, a University of New Hampshire/CNN poll conducted October 21-27 with a margin of error of 4.1 points found Sanders at 21%, Warren at 18%, and Biden at 15% — a dramatic drop of 9 percentage points from the July UNH/CNN poll, where Biden was at 24% support.

If Biden does not finish in the top two in either state, history indicates that it will be extremely difficult for him to win the Democratic nomination. The following comes from CNN…

Now, it’s not as if you must win these early contests. You probably need to come close though. George McGovern won neither in 1972, though he placed second in both Iowa and New Hampshire. Bill Clinton didn’t win either in 1992, though Iowa was ceded to home state Sen. Tom Harkin and Clinton came in second behind Paul Tsongas in New Hampshire. Put another way, no one has won a major party nomination since 1972 without coming in the top two in either Iowa or New Hampshire.

Public perception will be greatly shaped by the results of the first two contests. If Biden does poorly in both states, the mainstream media will be full of stories about how his campaign is in disarray, and donors and supporters will start looking for greener pastures.

So Biden better get his act together if he wants to be the Democratic nominee. And he potentially got some good news on Friday when Beto O’Rourke dropped out of the race…

O’Rourke said in a statement posted on Medium that his “service to the country will not be as a candidate or as the nominee,” adding that it is in the best interest of the Democratic Party to unifiy around the nominee.

“Though it is difficult to accept, it is clear to me now that this campaign does not have the means to move forward successfully,” he said.

Will this help Biden more than the other candidates?

O’Rourke was polling in the very low single digits, and so he didn’t have a lot of support. Many believe that at least some of O’Rourke’s supporters will migrate to Biden, but considering the fact that O’Rourke was so progressive this could also end up helping Elizabeth Warren and Bernie Sanders too.

But of much more importance is how the fundraising numbers will move in the weeks ahead. Unfortunately for Biden, he has been lagging the three other major Democratic candidates…

As of 2019’s third fundraising quarter, Sanders, Warren and Buttigieg reported $33.7 million, $25.7 million, and $23.4 million in cash on hand, respectively, compared with just $8.9 million for Biden.

Joe Biden’s presidential campaign announced Friday that it raised $5.3 million in online donations last month as the former vice president seeks to reassure voters as to the vitality of his White House bid.

If the Biden campaign continues to flounder, establishment Democrats are going to become increasingly tempted to recruit another big name to enter the race.

Michelle Obama has repeatedly insisted that she will never run for public office, but Hillary Clinton has been dropping hints in recent weeks that she may be interested.

However, if she is going to make a move she needs to do it soon.

As for Biden, his biggest problem is that he just can’t help being Joe Biden.

When a young female Democratic activist recently approached him with a hard question, he once again put his foot in his mouth…

You might have seen the video doing the rounds this week: Joe Biden, who was asked a tricky question by a young activist, responds about as condescendingly as humanly possible — “Look at my record, child.”

I was that young activist, and my encounter with the man who wants to be president taught me that he is not up to the task.

In this cultural environment, it is political suicide for someone running for president to call a young woman that is asking him a tough question a “child”.

Almost every time Biden appears in public, he loses more votes.

It probably would have been best if his handlers had just kept him locked away from the public entirely throughout this process, but at this point the race has gotten so close that doing such a thing now is just not possible.

And this is especially true now that Biden has fallen behind in both Iowa and New Hampshire.

Biden supporters better hope that he can cook up a comeback in at least one of those states, because as it stands right now it is looking quite doubtful that he will be the Democratic nominee.

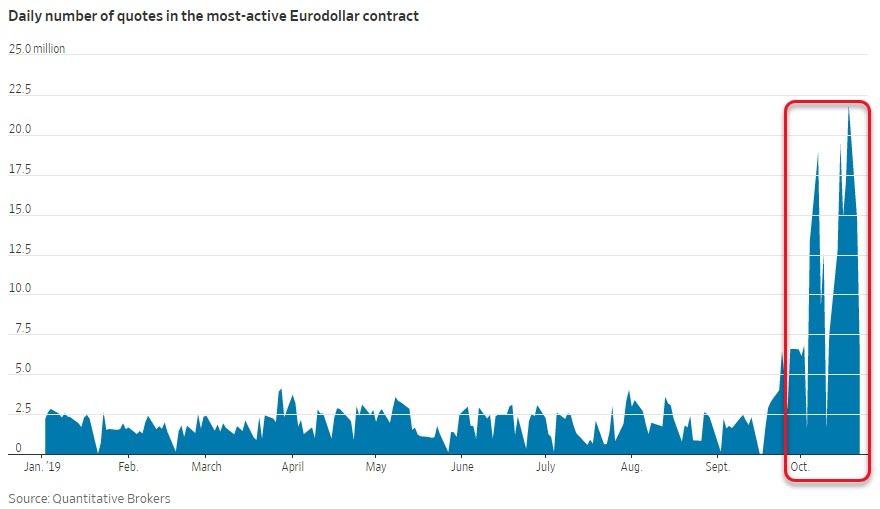

“Fundamentally Rigged” – Runaway Algos Spark Chaos, Crackdown In World’s Most Important Futures Market

The eurodollar futures market is among the most important for the functioning of global financial markets, providing faux-credit fillers for institutions everywhere as well as critical signaling (whether reflexive or not) on the future path of interest rates (and thus what The Fed is expected to do, or will do).

So, it seems appropriate to worry when that critical credit market is over-run by chaos-producing algos who seem to have moved on from front-running stocks (because it’s all buybacks all the time) to the vastly less-liquid (and notably wider tick-spreads) eurodollar market.

As The Wall Street Journal reports,over the past two months, the volume of data generated by activity in CME’s Eurodollar futures soared 10-fold, according to exchange statistics.

The torrent of data strained trading systems and prompted complaints to the exchange, traders said. Want to get an idea of just how insane that level of data is…

This Oct. 7 video nicely illustrates the CME data-surge issue I wrote about yesterday. UO, Z1 and H1 are Sept ’20, Dec ’20 and March ’21 Eurodollar futures. Quote sizes are spinning around wildly as algos race each other behind the scenes. pic.twitter.com/Kb0q37fhEp

The data surge, which hasn’t been previously reported, wasn’t caused by an actual increase in trading. Instead, the Journal notes that it mainly consisted of digital messages that showed changes to quotes to buy or sell Eurodollar futures – i.e. algos spoofing each other.

And in this case, the chaotic explosion in quotes was caused by a standoff between two firms whose algorithms entered a loop, racing each other to be the market’s biggest player, according to Emergent Trading, a small Chicago-based firm that said it was one of the two dueling traders.

Emergent founder Brandon Richardson estimated that his firm and its rival were responsible for 90% of messaging volumes during the surge…

…

After Emergent entered the Eurodollar market, it discovered there was an advantage to quoting prices for more contracts than any other market maker. The benefit: If another trader bought or sold Eurodollar futures, executing against quotes from different market-making firms, the market maker with the biggest quote would get notified 10 millionths to 20 millionths of a second before its next-biggest competitor, Mr. Richardson said.

It subsided Monday after CME took emergency measures to halt it, announcing new penalties for firms that bombard its markets with too many messages:

“We believe this change, which already has had a positive impact, will encourage responsible messaging practices going forward.”

Starting this week, CME will fine traders $10,000 whenever their messaging exceeds a certain threshold and cut off their connections to the exchange after repeat violations.

But, as WSJ notes, Mr. Richardson said the policy benefits large market makers, because they can establish dozens of connections to CME, while a smaller firm such as Emergent might get less than 10.

“It’s fundamentally rigged against a small player,” Mr. Richardson said.

A CME spokesperson, of course, rejected this assertion, but it is nevertheless a worry that as the Fed’s liquidity spigot is wide-open every day and uncertainty over the Fed’s future path of rates remains high that the most critical market for short-term credit is increasingly exposed to the possibility of flash-crashes (which in this case, thanks to the leverage created, will almost definitely ripple into the rest of the global financial markets).

– Federal Reserve Chairman Jerome Powell, October 30, 2019.

The man from the good place. “As I was going up the stair, I met a man who wasn’t there. He wasn’t there again today, Oh how I wish he’d go away!” [PT]

Ptolemy I Soter, in his history of the wars of Alexander the Great, related an episode from Alexander’s 334 BC compact with the Celts ‘who dwelt by the Ionian Gulf.’ According to Ptolemy’s account, which survives via quote by Arrian of Nicomedia some 450 years later, when Alexander asked the Celtic envoys what they feared most, they answered:

“We fear no man: there is but one thing that we fear, namely, that the sky should fall on us.”

Today, at the risk of being called Chicken Little, we tug on a thread that weaves back to the ancient Celts. Our message is grave: The sky is falling. Though the implications are still unclear.

Various Celts – left: fearsome warriors; middle: fearsome warriors afraid of the sky falling on their heads; right: Cernunnos, fearsome Celtic horned god amid his collection of skulls. [PT]

The sky, for our purposes, is the debt based dollar reserve standard that has been in place for the past 48 years. If you recall, on August 15, 1971, President Nixon “temporarily” suspended convertibility of the dollar into gold. The dollar became wholly the fiat money of the Treasury.

At the G-10 Rome meeting held in late-1971, Treasury Secretary John Connally reduced the new dollar reserve standard to a bite-sized nugget for his European finance minister counterparts, stating:

“The dollar is our currency, but it’s your problem.”

The Nixon-Connally tag team in the White House. [PT]

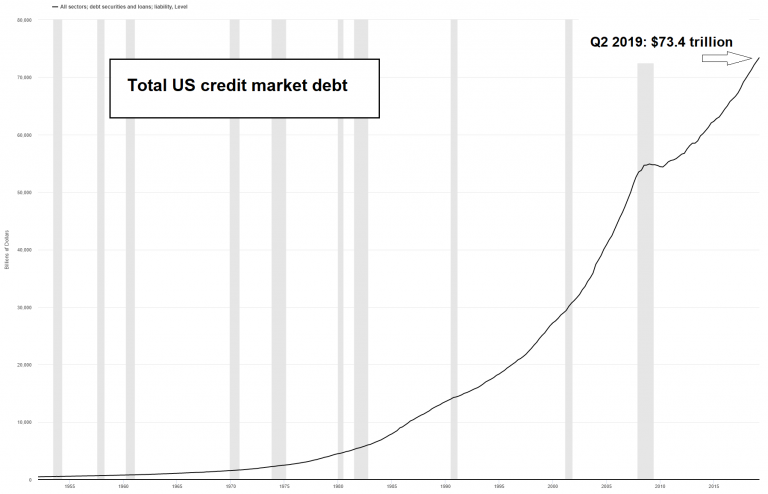

Predictably, without the restraint of gold, the quantity of debt based money has increased seemingly without limits – and it is everyone’s massive problem. What’s more, over the past 30 years the Federal Reserve has obliged Washington with cheaper and cheaper credit.

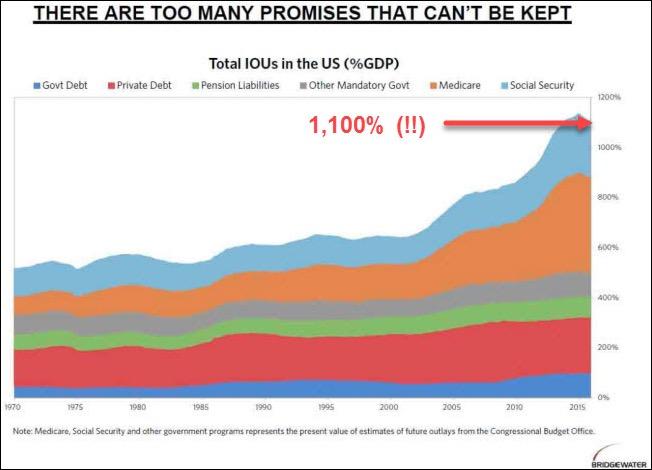

Hence, public, private, and corporate debt levels in the U.S. have multiplied beyond comprehension. Total US debt is now on the order of $74 trillion. The consequences, no doubt, are an economy that is equally distorted and disfigured beyond comprehension.

Behold the debt-berg in all its terrible glory. [PT]

Selective Blind Spots

America is no longer a dynamic, free-market economy. Rather, the economy is stagnant and operates under the central planning authority of Washington and the Fed. The illusion of prosperity is simulated by spending trillions of dollars funded by history’s greatest debt bubble.

Simple arithmetic shows the country is headed for economic catastrophe. Clearly, Social Security and Medicare face long-term financial challenges. Current workers must shoulder a greater and greater burden to pay for the benefits of retired workers.

At the same time, the world that brought the debt based dollar reserve standard into being no longer exists. Yet the dollar reserve standard and the Federal Reserve still remain as legacy institutions.

The divergence between the world as it exists – with its massive trade imbalances, massive debt loads, wealth inequality, and inflated asset prices – and the legacy dollar reserve standard is irreversible. Unless the unstable condition that has developed is allowed to transform naturally, there will be outright collapse.

Rather than adopting policies that allow for economic transformation and minimizing the ultimate disruption of a collapse, today’s planners and policy makers are doing everything they can to hold the failing financial order together. They are deeply invested academically and professionally; their livelihoods depend on it.

You see, selective blind spots of the best and brightest are normal when the sky is falling. For example, in 1989, just two years before the Soviet Union collapsed, Paul Samuelson – the “Father of Modern Day Economics” – and co-author William Nordhaus, wrote:

“The Soviet economy is proof that, contrary to what many skeptics had earlier believed, a socialist command economy can function and even thrive.” – Paul Samuelson and William Nordhaus, Economics, 13th ed. [New York: McGraw Hill, 1989], p. 837.

Could Samuelson and Nordhaus possibly have been more clueless?

The bizarre chart illustrating the alleged “growth miracle” of the “superior” Soviet command economy, as seen by Samuelson – published about one and a half years before the Soviet Bloc imploded in what was undoubtedly the biggest bankruptcy in history. [PT]

The Federal Reserve is a Barbarous Relic

On Wednesday, following the October federal open market committee (FOMC) meeting, the Federal Reserve stated that it will cut the federal funds rate 25 basis points to a range of 1.5 to 1.75. No surprise there.

But the real insights were garnered several days earlier. Leading up to the FOMC meeting Fed Chair Jerome Powell received some public encouragement from one of his former cohorts – former President of the Federal Reserve Bank of New York, Bill Dudley. What follows is an excerpt of Dudley’s mental diarrhea, which he released in a Bloomberg Opinion article on Monday:

“People shouldn’t be as worried as they are about the risk of a U.S. recession. That said, it wouldn’t take much to trigger one, which is why the Federal Reserve should take out some insurance by providing added stimulus this week.

“Sometimes, an adverse event and human psychology can reinforce each other in such a way that they bring about a recession. Given how slowly the economy is growing, even a modest shock could do the trick.

“This danger bolsters the argument for the Fed to ease monetary policy at this week’s meeting of the Federal Open Market Committee. Such a preemptive move will reduce the chances that the economy will slow sufficiently to hit stall speed. Even if the insurance turns out to be unnecessary, the potential consequences aren’t bad. It just means that the economy will be stronger and the inflation rate will likely move more quickly back toward the Fed’s 2 percent target.”

Retired former central planner Bill Dudley. These days an armchair planner, and as deluded as ever. [PT]

Dudley, like Samuelson, believes he can aggregate economic data and plot it on a graph; and, then, by fixing the price of credit, he can make the graphs appear more to his liking. He also believes he can preempt a recession by making ‘insurance’ rate cuts to stimulate the economy.

Like Samuelson, Dudley doesn’t have a clue. The Fed cannot preemptively stop a recession. And after the dot com bubble and bust, the housing bubble and bust, the great financial crisis, zero interest rate policy, negative interest rate policy, quantitative easing, operation twist, quantitative tightening, reserve management, and many other failures, the Fed’s standing is clear to everyone but Dudley…

The Federal Reserve is a barbarous relic. The next downturn will be its death knell. Alas, what comes after the Fed will probably be even worse. Populism demands it.

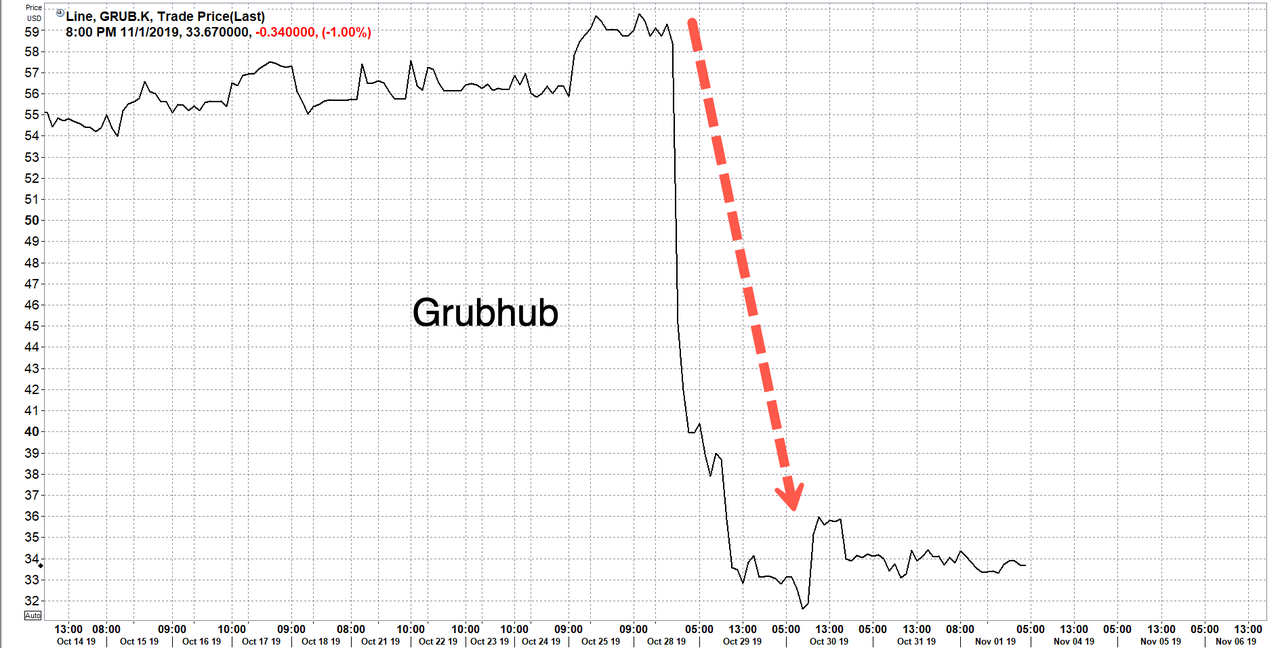

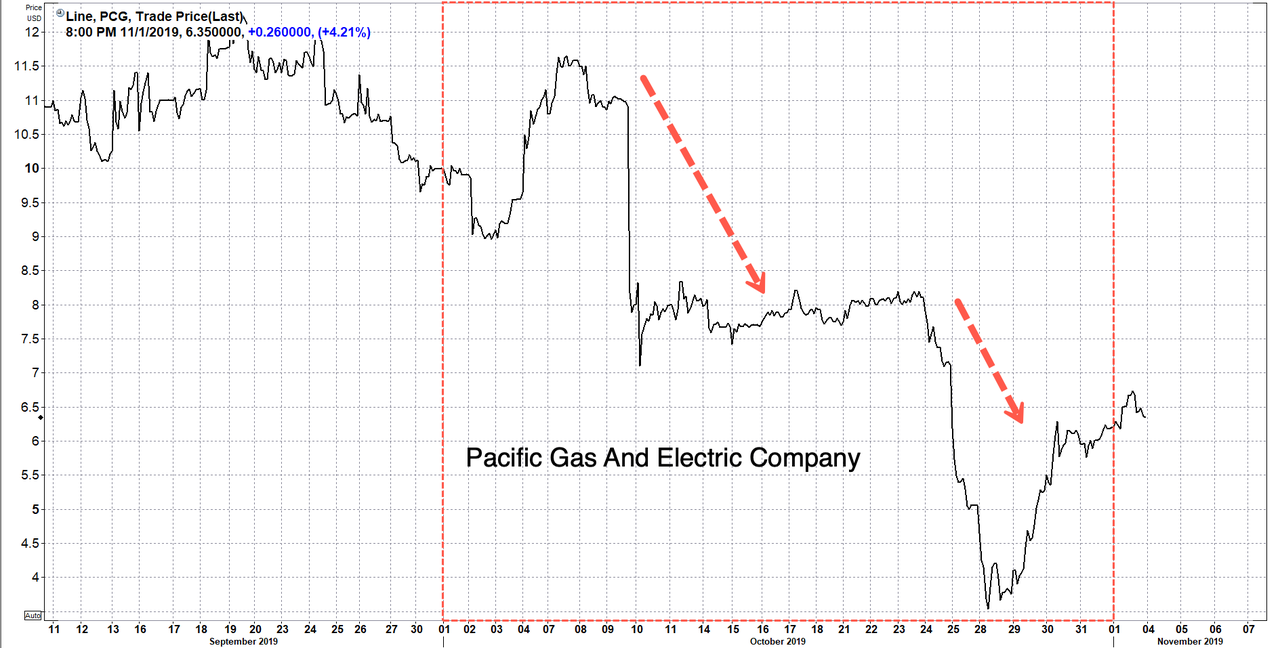

Bear Party: Short Seller Chanos Records “Best Month” Ever After Grubhub & PG&E Implode

Famous short-seller Jim Chanos’s Kynikos Capital Partners recorded the most profitable month ever in October, following large bearish bets against Grubhub and Pacific Gas and Electric (PG&E).

The bears are back, well maybe just Chanos at the moment, as he posted returns of 5.3% in October and year-to-date gains of 20.4%, according to investors who spoke with the Financial Times (FT).

Chanos told FT that “October has been one of our best months, both absolutely and relatively, in a long time.”

Grubhub shares plunged 43% last week following a pessimistic outlook by the company, who blamed most of its woes on competition, such as DoorDash and Uber Eats.

Chanos was recently on CNBC, making his bearish case against the food delivery business.

PG&E shares during the month were nearly halved.

Several of California’s most recent wildfires were blamed on the electric company after a windstorm blew down powerlines and sparked fires. To prevent further fires, PG&E conducted rolling blackouts across the Bay Area, plunging millions of people into the dark.

Chanos has been quoted in the past as saying PG&E’s equity will go to zero. “We also question whether PG&E will be able to exit bankruptcy-court protection in the foreseeable future,” he told investors.

FT notes that Chanos rolled his shorts against both companies into November.

It’s likely that Chanos has already planned, or is planning, the next big short as an earnings recession is ahead, the economy is rapidly slowing, and what’s driving stock prices higher at the moment is President Trump’s tweeting — does this mean an epic blow-off top is underway?

In that last 25 years, Chanos, through Kynikos Capital Partners, returned investors a net annualized gain of 26.9% through September, and this is more than double the returns of the S&P500. He does admit to FT that the fund has underperformed in recent years, saying, “we have a long way to go to erase some of the pain from the past few years.”

Today we live in a bifurcated economy: it is boom times for some and bust times for others.

Your personal situation depends largely on how close you fall on the socioeconomic spectrum to the protected elite class, towards which the central banks are directing their money-printing firehoses.

Why should we care about this bifurcation? History.

2,000 years ago, in Plutarch’s time, it was already ‘old wisdom’ that unhealthy wealth imbalances ended badly for society:

Even those near the top of the wealth pyramid don’t aspire to live surrounded by an impoverished underclass, forced to live hiding behind their fortifications and guards, hoping the unrest of the masses doesn’t get any worse.

But sadly, the US is not far off from this fate…this is Los Angeles:

The streets of San Francisco, Seattle, and a growing number of other once-proud American cities look very similar.

I care about our social stability which is why I believe in having a strong and vibrant middle class – something the US Federal Reserve is working to destroy with every intervention. It has been a shameless champion of the entrenched ultra-rich and powerful; at the expense of everyone else. Because of this, I’ve been a fierce critic of the Fed and its policies.

Money vs Real Wealth

I happen to know a good deal about our current system of money; how it is created, how it functions, its benefits and its darker aspects. I find it critical to remember that it isn’t actually “real”. Rather, it is a concept. Specifically, it’s a social contract. An agreement. Albeit one enforced at the end of a gun – or, as seen here, an eviction sheriff enforcing the local tax codes:

So while money isn’t “real” in itself, we value it because it is a claim on real things.

Having a lot of it currently entitles you to a great deal of privileges and power, which are a direct outcome of the spending of that money.

Money can be converted into houses. And cars. And massages. Also groceries, electricity, cell phone services and prescription drugs. These and ten billion other things are what money allows you to buy — the things you actually need or want.

So money is the means, but it is not the real wealth. ‘Real wealth’ is the things that money enables you to acquire.

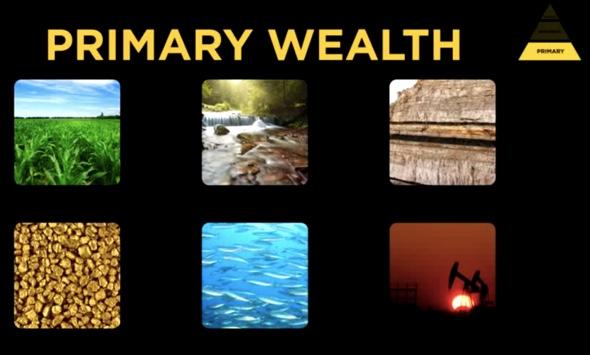

The Three Types Of Wealth

Going further, we can break real wealth into two discrete forms. Primary wealth is the wealth of the land and its functioning ecosystems. It is clear air, fresh water, thick ore bodies, and rich soils:

Secondary wealth is a finished form produced from raw materials. It is primary wealth brought to market. It is fresh produce on the grocery shelf, cut lumber (or even a fully-constructed building), and rolled steel in giant coils:

Tertiary wealth, on the other hand, is not actually “real”. But most people mistake it as a comprehensive representation of “wealth”.

Similar to money, tertiary wealth is merely a claim on primary and/or secondary wealth. A share of General Electic a stock-based claim on the company’s means of production.

And debt (and bonds) is a future claim on money. And money, as we know, is a claim on real things.

It’s All About The Amount Of Claims

Why is it relevant to parse these distinctions so carefully?

Because there has to be a balance between the claims and the wealth.

Too many claims and we call that inflation. Each individual claim is reduced and diluted by every additional new claim brought into being. Beyond a certain amount, each claim becomes increasingly worthless.

Deflation is when there’s overproduction, or too much ‘real stuff’ relative to money. Prices fall, which is a perilous condition for a debt-based money system. There needs to be ever more money to pay off both the principal and interest components of past loans, or else defaults start cascading through the system.

Do you get now why we need to be very concerned with the balance between the claims and the real stuff?

History is full of examples when people first forgot and then violently remembered these truths. Through history, the balance has swung recklessly — almost chaotically — between inflation and deflation.

Another such phase transition approaches. These moments are billed as periods of wealth destruction, but they actually aren’t. Instead, they are periods of wealth transfers from the unaware to the observant.

We’re facing this approaching crisis for two main reasons. One, we’re repeating the forgetfulness and hubris of previous societies. And two, the complexities of our current situation are more challenging than ever before.

Man of our actions are driven by the strong human preference to push our current problems into the future. When problems and predicaments are compounding/exponential in nature like those we’re currently facing, every can-kicking deferment only makes the pain much greater when it finally arrives.

And as for the increased complexities, for the first time in our history as a global species, we are waking up to the fact that the world is no longer our infinite treasure basket with an unlimited ability to absorb our waste streams.

Instead, it is finite. And its already groaning under the weight of one unit of global GDP extraction and waste. The central banks are tirelessly seeking to double the size of the economy, and then double it again.

One can easily make the argument that 1x GDP is already ‘too much’ for the planet. Disappearing fishes, soil, insects, birds, amphibians, reptiles and large animals all indicate that ‘too much’ was a while ago.

But even for those who believe we haven’t exceed the Earth’s carrying capacity yet, it’s certainly true that there’s some sort of a limit somewhere. Is it when there’s 1.5 times as much consumption and waste as today? 2 times as much? 3 times?

When is the right time to act as if these limits matter to our future welfare? Not now! is the rally cry of the Federal Reserve and other central banks. Their remit begins and ends with fostering more credit growth as fast as possible. Full stop.

It’s all they care about. And if they have to continue to throw a couple of younger generations and the entire middle-upper, middle, and lower classes under their inequality-bus to achieve more growth in credit markets, then you’d better believe that’s what they’ll do.

The basic problem is that money is not real wealth. But newly printed money has real purchasing power. What happens when purchasing power is increased but more real wealth is not auto-magically created at the same time?

Easy: the claims on real stuff become diluted. Every unit of money in circulation has a tiny fragment of purchasing power removed from it when a new unit of purchasing power is created ‘out of nothing.’

You might think “what a flawed plan!,” but that’s exactly wrong. That’s precisely the plan. Coin clipping was the ancient Roman practice of diluting the currency by recalling every coin in circulation (or as many as possible), shaving off a tiny bit from each of them, and then reissuing a larger quantity of coins that each weighed a tiny bit less than before.

Today it’s far easier to achieve the same outcome. New electronic digits are spewed out into the world and perhaps 0.1% of the population could even tell you that it’s happening. Perhaps only 0.001% could tell you exactly how.

But the effect is the same as coin clipping. Each new currency digit launched ‘from nothing’ into circulation has immediate purchasing power. By definition, all of the pre-existing currency in circulation loses a ‘unit-share’ as a consequence.

With trillions upon trillions in circulation, nobody really notices. Again, that’s both the point and by design.

For the US, this chart explains what’s coming in grotesque detail:

This is the total debts of the US, which represent future claims on money — which, remember, itself is a future claim on real wealth.

GDP represents, imperfectly, the ‘real stuff’ in this story. As you can plainly see, the claims (red line) are compunding at a far faster pace than GDP (blue line).

It gets even worse — far, far worse — when we include America’s unfunded liabilities into the mix, seen here expressed as a percentage of GDP:

What possible ways are there to resolve that chart with people’s expectations, hopes and dreams?

Well, we could grow GDP really, really fast for a very long time. Like 75 or even 100 more years.

By which point the US economy alone will be 5x larger than the entire global economy currently is. Now remember that already the Earth is screaming “enough!” We can only imagine what happens if the US alone becomes 5x larger than today’s entire world economy…

However, because such tremendous growth requires energy, a LOT of it, and because no suitable replacements for fossil fuels yet exists, and because fossil fuel supplies are set to decline for reasons related to depletion and geology, that kind of 5x growth is just not likely to materialize. It’s not possible; the fuel to power it isn’t there.

It’s not a good bet at all.

So what happens when huge claims slam into physical constraints? The excess claims evaporate. As they have many times throughout history.

This is where the wealth transfer comes in. And you want to be sure to be prepare for it, and on the correct side of it as it happens.

Time Is Running Out

The end of money approaches.

To quote the famous Austrian economist Ludwig Von Mises:

“There is no means of avoiding the final collapse of a boom brought about by credit expansion.

The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

How many people reading this think that given the choice between dealing with unpleasant consequences now vs. printing up more money (via MMT, more QE, etc.) and facing the music at a later date that there’s even any contest at all?

Of course they’ll opt to print more now. Now is never a good time to face the music. There are delicate issues right here and now to balance. A tough moment in a trade negotiation, an election, disturbing weakness in the IPO market, etc.

Further, there’s nobody of any consequence who has the requisite vision or leadership to stomach such a period of tough decisions. There’s no Paul Volker at the Fed; just a bunch of clueless market-following political animals who are afraid of any and every wiggle downwards in stock prices. They are the market’s lapdogs now; completely unworthy of admiration or respect.

Which is why we predict more printing and borrowing. Enormous new piles of money and credit will be issued, likely at ever-lower rates of interest.

The world economy is performing sluggishly and appears to be sickening further. This is due to too much debt. But no matter, the central banker’s response is automatic: The world needs more credit at even cheaper prices!

And, of course, more central bank interventions to keep everything from falling apart. After all, the central bankers are the heroes in this story, right??

It will be something of a miracle if the next US presidential election doesn’t open the MMT floodgates, which would only accelerate the pace of currency debasement.

The pressure is building. Nobody knows when all of that newly-issued money and credit will have to be ‘trued up’ against the amount of real stuff out there. But it will. It always does.

That moment will be referred to by the press as a period of wealth destruction.

If a deflationary outcome occurs – which we give a 15% chance of happening – 401ks will be shredded, bonds will lose value, defaults will spike, stocks will crater and the dollar will spike as institutions and entire countries scramble to repay their debts from a dwindling pool of money.

If an inflationary outcome does– the remaining 85% probability – money will become worth less and less. But the press will unhelpfully lament the situation as some great mystery, like rain falling from a clear sky. Of course, understanding inflation is not terribly difficult, but it behooves the power structure to pretend as if it were really just too difficult to comprehend. Inflation is always a monetary phenomenon. Too much money chasing too few goods and services.

Either way, the sword will fall. And after the dust settles, there will be clear winners and losers. Those with the proper framework and agility will prosper. They will understand that what actually happened was that wealth was transferred from those who thought they owned it (the claimants), to those who actually did (the possessors).

The only remaining questions are whether the wealth transfer comes about in the form of an inflationary destruction, like in Venezuela today, or as a deflationary bust more in the fashion of Greece recently (which lost its ports, roads, and utilities to foreign banks and creditors as a consequence of running up too much debt it couldn’t repay).

Either way, by deflation or inflation, the prudent financial responses remain the same. Own hard assets. Have multiple income streams. Be able to source a percentage of your own food locally and generate your own energy at home (solar, rocket mass heaters, etc.).

We cannot possibly predict when the current Everything Bubble will finally end, but when it does, you at least will not be fooled. You will have seen it coming and will know its causes. You will be among the educated and alert who will know that the real wealth has merely been transferred.

Further, you will know that the beneficiaries of that wealth transfer will almost certainly be – surprise! – the banks and other financial elites that the Fed has so carefully enabled and protected. The winners have been pre-selected, as have the losers.

The danger in that, of course, is if the financial elites haven’t thought their cunning plan all the way through. They may not like what follows next as an enraged populace finally wakes up to the enormous fraud that has been perpetrated upon it.

We shall see.

More and more people in the US and in other countries are waking up to the ways in which the financial and political elites have gamed and rigged the system in their favor. Angry protestors are increasingly taking to the streets to voice their displeasure.

We predict more of that. A lot more.

In Part 2: Time Is Growing Scarce, we closely examine the warning signals (some of which the Fed is itself providing!) that the global economy is much weaker than admitted, and that the great wealth transfer is about to ramp into high gear.

Interested in making it through the coming chaos with your wealth — and more important, your integrity — intact? Read on.

Trump Freezes Lebanon Military Aid After Israel Voiced Concerns

Amid recent statements by both Iranian and Hezbollah leaders accusing the United States of hijacking the massive anti-corruption protests which have gridlocked Lebanon for over the past two weeks, the White House has made the dramatic and unexpected move of freezing US military aid to the Lebanese Army.

The money, part of a military aid package totaling $105 million, had been approved by Congress and the State Department, and requested by the Pentagon. Interestingly, proponents of the package argued that it would allow the Lebanese Army to grow more independent, making it less cooperative with Hezbollah.

According to Reutersthe aid was frozen two days following Tuesday’s resignation of Lebanese Prime Minister Saad al-Hariri, who in a parting speech admitted he’d “reached a dead end” amid the protests which have reportedly involved one million people, or up to 25% of Lebanon’s total population, and further called on “all Lebanese to protect civil peace”.

Protests have gridlocked Beirut over the past two weeks, via the AP.

The United States, said the report, has frequently voiced “concern over the growing role in the Beirut government of Hezbollah, the armed Shi’ite group backed by Iran and listed as a terrorist organization by the United States.”

Secretary of State Mike Pompeo this week called on Beirut to take steps for a new unified government which focused on rooting out endemic corruption.

Though no specific reason was given as to why the White House has targeted Lebanon for an aid freeze, Trump has lately signaled his disdain for the amount of foreign aid Washington hands out around the world, seemingly with no strings attached.

On Friday, an Israeli media report revealed that officials in Tel Aviv had lobbied the White House to condition any US Lebanese aid based on the country removing advanced arms in possession of Hezbollah — something it should be noted that Lebanon’s national forces are likely incapable of, given the Shia paramilitary organization is actually considered stronger.

The Foreign Ministry ordered Israeli diplomats “in all relevant countries,” including the US and European states, to emphasize the need to cease providing aid to Lebanon as long as the Iran-backed Hezbollah terror organization does not cease upgrading its military capabilities that could target Israel, the official added. — Times of Israel

“In discreet talks with various capitals, we made it clear that any aid meant to guarantee the stability of Lebanon needs to be conditioned on Lebanon dealing with Hezbollah’s precision-guided missiles,” a senior official told The Times of Israel. “Anything short of that will be problematic, in our eyes.”

This could mark a big first step in Trump cutting of aid to ‘dysfunctional’ governments and/or governments made up of elements which are hostile to the United States, as is the case with the designated group Hezbollah.

{kind=link}