Several California police departments have stopped using “predictive policing” software but not because they want to protect your basic human rights and dignity. The reason the software won’t be used is that it isn’t effective enough…yet.

Several police departments were disappointed that they won’t be able to punish thought crimes.

Palo Alto police spokeswoman Janine De la Vega told the Los Angeles Times:“We didn’t get any value out of it,” after using the software for three years. As for Mountain View, California’s police department, which spent over $60,000 of taxpayer money on the software that was designed to violate the rights of the taxpayers stolen from to fund it, it was dubbed a “disappointment.” The police department used the software for over five years before dropping the program last June. Rio Rancho, New Mexico Police Captain Andrew Rodriguez said: “It wasn’t telling us anything we didn’t know.”

The software is a bold violation of the basic human right to free thought and those who use it are nothing more than freedom-trampling tyrants. The Los Angeles Police Department took an authoritarian leap in 2010 when it became one of the first to employ data technology and information about past crimes to predict future unlawful activity. The software is called PredPol, and is known as the “predictive policing tool” developed by a University of California at Los Angeles professor and the Los Angeles Police Department.

The LAPD itself was forced to admit following an internal audit that after eight years, there was “insufficient data” to show PredPol to be effective in reducing crime. This was largely due to massive inconsistencies in oversight, criteria, and program implementation.

In April, the department shelved another Orwellian program, which was found to be using “inconsistent criteria” to label people as future violent criminals. Last August, after a lawsuit from privacy and civil liberties groups forced the department to cough up its PredPol records, the LAPD discontinued another dystopian part of the program that picked out a list of “chronic offenders” every shift based on alleged gang membership, previous arrests, and one “point” for every “quality police contact.” –RT

Regardless of whether there’s data or no data, LAPD Chief Michel Moore doesn’t want to let PredPol go, claiming it is more accurate than human analysts at predicting where criminals will strike next. But even his defense of the program is a far cry from early publicity materials that trumpeted “‘cliff-like’ drops in crime often within months of deployment” among PredPol’s early adopters.

Winston Smith toes the Party line, rewriting history to satisfy the demands of the Ministry of Truth. With each lie he writes, Winston grows to hate the Party that seeks power for its own sake and persecutes those who dare to commit thoughtcrimes. But as he starts to think for himself, Winston can’t escape the fact that Big Brother is always watching. –1984’s book description

The haunting reality is that we are almost there, and may have passed the point of no return.

via ZeroHedge News https://ift.tt/2L6gMgK Tyler Durden

After getting kicked down an elevator shaft by a well prepared Kamala Harris during the first Democratic primary debates, former Vice President Joe Biden has gone from “Apologize for what?” to “I’m sorry” over remarks he made about working with segregationist Democrats when he entered DC politics.

Photo via Marianna Sotomayor, NBC News

Speaking to a mostly black audience at a Sumter, South Carolina campaign stop, Biden told supporters “Was I wrong a few weeks ago to somehow give the impression to people that I was praising those men who I successfully opposed time and again? Yes I was. I regret it. I’m sorry for any of the pain or misconception,” according to NBC News.

Biden, 76, asked the audience: “Should that misstep define 50 years of my record for fighting for civil rights and racial justice in this country?” adding “I hope not. I don’t think so.”

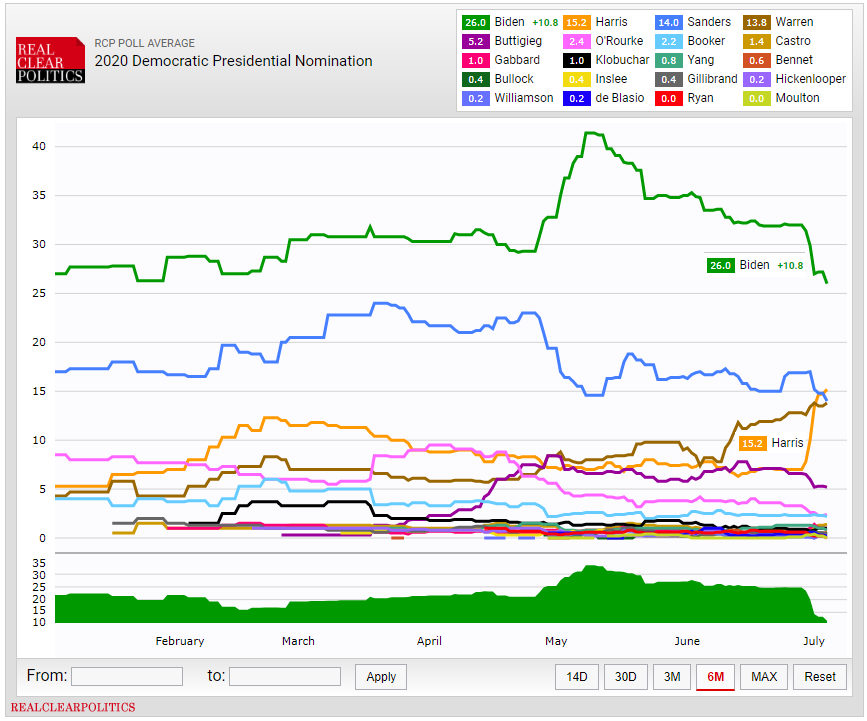

Meanwhile, Biden’s numbers appear to be in freefall – while Harris has quickly overtaken both Bernie Sanders and Elizabeth Warren according to RealClearPolitics.

Turns out nobody really cared about Biden’s flagrant groping of women and children, or allegations that he abused his position as Vice President for extreme nepotism. Mentioning that he worked with segregationist Democrats in the 1970s to “get things done,” on the other hand, has caused a double-digit drop from lead in early May.

via ZeroHedge News https://ift.tt/32eWqHt Tyler Durden

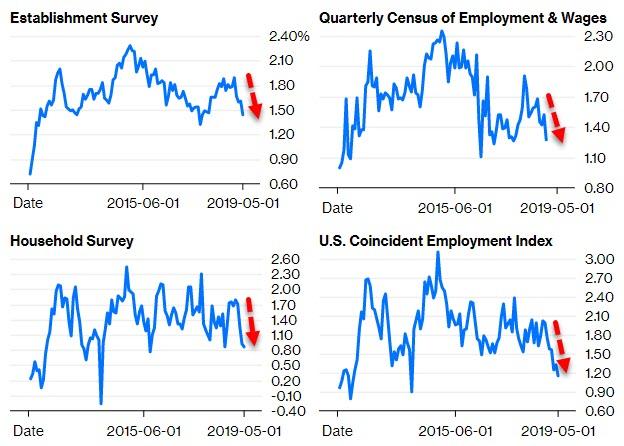

Jobs growth is substantially slower than the headline employment data indicate…

As the U.S. election cycle gets underway, expect much debate over just how strong the economy really is after becoming the longest uninterrupted expansion in America’s history. After all, the jobless rate is at a half-century low and the S&P 500 Index is at a record high. The bond market, though, is signaling that the Federal Reserve will soon be forced to ease monetary policy to shore up the economy. How can that be?

A key part of the answer lies with jobs “growth,” which has been slowing much more than most probably realize. Despite the better-than-forecast jobs report for June, the fact is the labor force has contracted by more than 600,000 workers this year. And we’re not just talking about the disappointing non-farm payroll jobs numbers for April and May.

Certainly, that’s caused year-over-year payroll growth, based on the Labor Department’s Establishment Survey – a broad survey of businesses and government agencies – to decline to a 13-month low. But year-over-year job growth, as measured by the separate Household Survey – based on a Labor Department survey of actual households – that is used to calculate the unemployment rate is only a hair’s breadth from a five-and-a-half-year low. (The data in the charts below don’t reflect Friday’s employment report.)

Heading South

Multiple indicators suggest a significant slowdown in the labor market is underway

Source: U.S. Government, ECRI

Growth in the Economic Cycle Research Institute’s more comprehensive U.S. Coincident Employment Index (USCEI), which includes both those figures and more, has fallen to its worst reading since late 2013. Because it subsumes data from both surveys, its verdict about overall job growth is more reliable than the others.

But there’s even more cause for concern. Months from now, the Establishment Survey will undergo its annual retrospective benchmark revision, based almost entirely on the Quarterly Census of Employment and Wages conducted by the Labor Department. That’s because the QCEW is not just a sample-based survey, but a census that counts jobs at every establishment, meaning that the data are definitive but take time to collect. Since it is retrospective, few pay any attention but the QCEW offers critical information for those wanting to verify that the job market is as strong as the headlines would lead you to believe.

The latest QCEW data are available through 2018, but note how much worse the 2018 QCEW data look than the Establishment Survey data, even though the two appear fairly similar in previous years, for which the latter has already undergone the requisite revisions. The Establishment Survey’s nonfarm jobs figures will clearly be revised down as the QCEW data show job growth averaging only 177,000 a month in 2018. That means the Establishment Survey may be overstating the real numbers by more than 25%.

Separately, according to the Household Survey, the number of people unemployed has dropped by more than 400,000, or 6.50%, since December. But the number employed has also declined, by almost 200,000. So their sum total – the labor force – has fallen by almost 600,000, or about 0.33%.

Since the unemployment rate is the ratio of the number unemployed to the labor force, the numerator has seen a bigger proportionate drop than the denominator. This is why the jobless rate has fallen from 3.9% to a half-century low of 3.6%. While that makes a great headline, it isn’t good news. Said another way, employment as measured by the Household Survey has actually declined this year by almost 200,000, while twice as many who were earlier unemployed have apparently given up looking for jobs.

The notion of the tight labor market drawing people into the labor force from the sidelines is largely a myth. Digging under the headlines reveals that job growth looks to have been substantially slower last year than the headline payroll jobs data indicate. Meanwhile, the decline in the jobless rate to a half-century low obscures the unflattering truth that almost half a million people have left the labor force just this year. These facts are in sharp contrast to strong job growth narrative.

Politicians of all stripes are in the business of myth-making, so it’s no surprise that they’ve been touting the robust health of the labor market, even as the ground shifts beneath their feet. But slowing job growth and a shrinking labor force virtually dictate that there will be a new chapter to the jobs story as campaigning goes into full swing.

via ZeroHedge News https://ift.tt/2YDXNO3 Tyler Durden

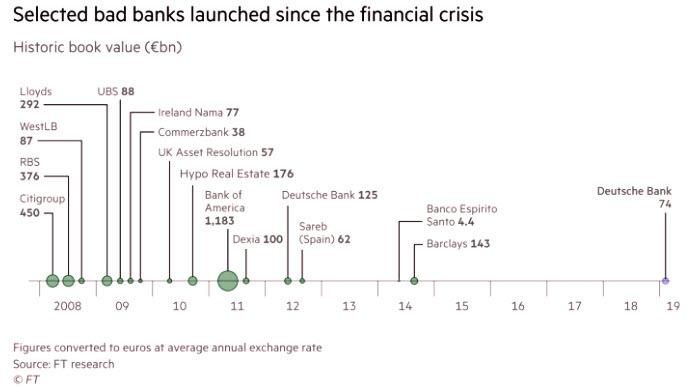

The bank which only a decade ago dominated equity and fixed income and sales trading and investment banking across the globe, and was Europe’s banking behemoth, is no more.

On Sunday afternoon, in a widely telegraphed move, Deutsche Bank announced that it was exiting its equity sales and trading operation, resizing its once legendary Fixed Income and Rates operations and reducing risk-weighted assets currently allocated to these business by 40%, slashing as many as 20,000 jobs including many top officials, and creating a €74 billion “bad bank” as part of a reorganization which will cost up to €7.4 billion by the end of 2022 and which will result in another massive Q2 loss of €2.8 billion, as the bank hopes to slash costs by €17 billion in 2022, while ending dividends for 2019 and 2020 even as it hopes to achieve all this without new outside capital.

“Today we have announced the most fundamental transformation of Deutsche Bank in decades,” CEO Sewing said in a statement. “We are tackling what is necessary to unleash our true potential.”

In what has been dubbed a “radical overhaul”, the biggest German lender, unveiled one of the most comprehensive banking restructurings since the financial crisis, closing most of its trading unit and splitting off €74bn of its assets as the struggling German lender calls time on its “20-year attempt to break into the top ranks of Wall Street.”

“These actions are designed to allow Deutsche Bank to focus on and invest in its core, market leading businesses of Corporate Banking, Financing, Foreign Exchange, Origination & Advisory, Private Banking, and Asset Management” the bank said in a Sunday statement.

The exit of Global Equities and a significant reduction in Corporate and Investment Banking risk weighted assets

Deutsche Bank will exit its Equities Sales & Trading business, while retaining a focused equity capital markets operation. In addition, the bank plans to resize its Fixed Income operations in particular its Rates business and will accelerate the wind-down of its existing non-strategic portfolio. In aggregate, Deutsche Bank will reduce risk-weighted assets currently allocated to these businesses by approximately 40%.

The bank will create a new Capital Release Unit to manage the efficient wind-down of the assets related to business activities, which are being exited or reduced. These assets and businesses represented EUR 74 billion of risk-weighted assets and EUR 288 billion of leverage exposure, as of 31 December 2018.

A significant restructuring of businesses and infrastructure

Deutsche Bank will implement a cost reduction program designed to reduce adjusted costs to EUR 17 billion in 2022 and is targeting a cost income ratio of 70% in that year.

To facilitate its restructuring, Deutsche Bank expects to take approximately EUR 3 billion of aggregate charges in the second quarter of 2019, of which approximately EUR 0.2 billion would impact Common Equity Tier 1 capital. These charges include a Deferred Tax Asset write-down of approximately EUR 2 billion and impairments of approximately EUR 0.9 billion. Additional restructuring charges are expected in the second half of 2019 and subsequent years. In aggregate, Deutsche Bank currently expects cumulative charges of EUR 7.4 billion by the end of 2022.

Managing the transformation through existing resources

Deutsche Bank management intends to fund its transformation from its existing resources without requiring additional capital. This reflects the bank’s current strong capital position as well as management’s confidence in the high quality and low risk nature of the assets, which it is exiting. In connection with these decisions, the Management Board intends to recommend no common equity dividend be paid for the financial years 2019 and 2020. The bank expects to have capacity for payments on additional tier 1 securities throughout the transformation phase.

Updated capital and leverage targets

The Management Board believes that the future business mix is consistent with a lower capital requirement. After consultation with the bank’s regulators, the bank now intends to operate with a minimum CET1 ratio of 12.5% going forward. As a result of the significant deleveraging actions, the bank targets a fully-loaded leverage ratio of 4.5% by the end of 2020 rising to approximately 5% by 2022.

Of course, none of the above will come for free, and the bank will incur second quarter charges related to the restructuring described above, resulting in a pretax loss before income taxes of approximately EUR 500 million and a net loss of EUR 2.8 billion. The silver lining – if one excludes all these “one-time” charges – which is ironic for the bank which has been restructuring every quarter for the past few years – Deutsche Bank expects to report second quarter 2019 income before income taxes of approximately EUR 400 million and net profit of EUR 120 million.

As the FT notes, the new strategy by CEO Christian Sewing “signals a retreat from Deutsche’s global ambitions and its aim to be Europe’s main rival to Goldman Sachs”. Instead, one year ahead of Deutsche’s 150th anniversary, Sewing is refocusing the lender on its historic roots — financing German and European corporate clients and domestic retail banking.

As we noted previously, the bank with the €43.5 trillion in gross derivatives notional…

… will be hard-pressed to ringfence all of its toxic assets in a relatively modest €74 billion silo. What is just as notable is that the use of a bad bank, an artificial crutch that was prevalent during the financial crisis and shortly after as shown in the chart below…

… confirms that many if not most of Europe’s banks are just as challenged as they were a decade ago, and only the ECB’s actions prevented the market from grasping the true severity of the situation. Which, in a sense, is paradoxical because it is the ECB’s NIRP/QE policies that made Deutsche Bank’s historic restructuring inevitable.

Finally, while as many as 20,000 jobs are also expected to be cut, the bank did not mention headcount reductions in its initial statement (we expect this news will be presented to workers in a more intimate context). Most of the job losses are set to come at the investment bank, particularly the underperforming operations on Wall Street and in the City of London.

Not only the rank and file will be affected: as we reported yesterday, two top executives have already departed as part of the overhaul — Garth Ritchie, investment banking chief, and Frank Strauss, head of retail banking. Sylvie Matherat, chief regulatory officer, is also expected to leave, as are the bank’s debt chiefs Yanni Pipilis and James Davies.

While it is unclear if the bank can achieve its ambitious agenda in the next 3 years, one thing is certain – the Deutsche Bank that saw RenTec close out its counterparty exposure in recent weeks anticipating what was coming – is no more, and it remains to be seen if the “successor” will be any more successful.

via ZeroHedge News https://ift.tt/2FX6bRc Tyler Durden

Acting Homeland Security Secretary Kevin McAleenan on Sunday rejected “unsubstantiated” allegations that children were living without adequate food, water or sanitation at a Clint, Texas Border Patrol facility.

Speaking with ABC‘s Martha Raddatz, McAleenan said the reports were unsubstantiated “Because there’s adequate food, water. Because the facility is cleaned every day,” adding “Because I know what our standards are and I know they’re being followed because we have tremendous levels of oversight.”

“Let’s be clear, this is an extraordinarily challenging situation. We had an overflow situation of hundreds of children crossing every day. That’s why we were asking for funding from Health and Human Services to provide adequate bed space so those children could be moved from that immediate border processing facility to a more appropriate setting for children,” McAleenan added.

“So I’m not denying that there are challenges at the border. I’ve been the one talking about it the most. What I can tell you right now is that there’s adequate food, water, and the reason those children were at Clint station in the first place was so they could have medical care and shower facilities.”

Acting DHS Sec. Kevin McAleenan defends calling the report on unsanitary conditions at the Clint detention facility “unsubstantiated.”

The Clint Border Patrol station has been at the center of controversy, and was one of two border facilities visited by Democratic lawmakers last week, including Rep. Alexandria Ocasio-Cortez (D-NY) and Rep. Joaquín Castro (D-TX) who snuck a recording device into the El Paso Border Station #1 to covertly record women in a “cramped cell.”

This moment captures what it’s like for women in CBP custody to share a cramped cell—some held for 50 days—for them to be denied showers for up to 15 days and life-saving medication. For some, it also means being separated from their children. This is El Paso Border Station #1. pic.twitter.com/OmCAlGxDt8

Responding to concerns over conditions at detention facilities, the Arizona CBP posted a video last week showing the inside of a processing center in Tucson, showing that the migrants have access to clean water and supplies.

Since Thursday, Southern California has been hit with a series of earthquakes and aftershocks all the way up to two that measured 6.4 and a whopping 7.1 magnitude. The epicenter of both quakes was near the town of Ridgecrest, with a population of nearly 29,000 people.

The Earthquakes

On the Fourth of July, the strongest earthquake in 20 years struck, with the epicenter in the Mojave Desert. This earthquake registered a 6.4 on the Richter scale. The tremblor resulted in cracked roads, leaking gas lines, house fires, and multiple injuries.

Among the aftershocks was a 5.4, at 4 am Friday morning.

But that wasn’t the worst of it. More than 1700 aftershocks hit the area, which, according to seismologist Zachary Ross, “might be slightly higher than average.” Initially, it was believed that the Independence Day earthquake was the main one, but it turned out to be a foreshock.

And then, at 8:19 Friday night, a 7.1 struck 11 miles from Ridgecrest.

“The quake was felt downtown as a rolling motion that seemed to last at least a half-minute. It was felt as far away as Las Vegas, and the USGS says it also was felt in Mexico.”

…San Bernardino County firefighters reported cracked buildings and a minor injury…

….There were reports of trailers burning at a mobile home, and State Route 178 in Kern County was closed by a rockslide and roadway damage.

But Kern County Fire Chief David Witt says it appears no buildings collapsed. He also says there have been a lot of ambulance calls but no reported fatalities…

…Mark Ghillarducci, director of the California Office of Emergency Services, says there are “significant reports of structure fires, mostly as a result of gas leaks or gas line breaks throughout the city.”

He also says there’s a report of a building collapse in tiny Trona. He says there could be even more serious damage to the region. (source)

California governor Gavin Newsome has declared a State of Emergency. There have been fires, gas leaks, power outages, water outages, road damage, and rock slides. While only one building was reported to have collapsed, Kern County Fire Chief David Witt warned that other buildings may have been weakened after being hit by two quakes in a matter of just over 24 hours.

Although no major damage was reported, Los Angeles felt significant movement from the second earthquake.

In downtown Los Angeles, 150 miles away, offices in skyscrapers rolled and rocked for at least 30 seconds.

The Los Angeles commuter rail service Metrolink said on Twitter it has stopped service in the city of 4 million people for the time being.

Disneyland in Orange County and Six Flags Magic Mountain in Santa Clarita closed their rides.

Juan Fernandez and Sara Donchey, two news anchors for the local CBS affiliate in Los Angeles, were seen live on the air seeking shelter as the quake struck on Friday.

‘We are experiencing quite a bit of shaking if you bear with us a moment,’ Donchey said. ‘We’re making sure nothing is going to come down in the studio here.’ A visibly terrified Donchey then grabs Fernandez’s arm.

‘This is a very strong earthquake,’ she said. ‘8:21 here and we’re experiencing very strong shaking. I think we need to get under the desk Juan.’ Donchey then got under the desk and the station cut to a commercial break. (source)

No major damage occurred in Los Angeles.

The Naval Air Weapons Station in the Mojave was evacuated.

The Naval Air Weapons Station in China Lake has evacuated all non-essential personnel and their families.

Naval Air Weapons Station China Lake says it is not fully operational after back-to-back major earthquakes hit Southern California.

The station said Saturday in a Facebook post that its non-essential personnel were evacuated.

The installation in the Mojave Desert covers an area larger than Rhode Island and is the Navy’s largest single landholding.

The Facebook post says normal operations were halted until further notice and it was not clear when they would resume. (source)

The tiny town of Trona suffered extensive damage.

Trona, known as “the gateway to Death Valley” because it’s the last town before the Mojave Desert, suffered extensive damage.

Fire officials say as many as 50 structures in the small town of Trona were damaged by the magnitude 7.1 earthquake Friday night in Southern California.

In addition, San Bernardino County Supervisor Robert Lovingood said Saturday that damaged water lines prompted FEMA to deliver a tractor-trailer full of bottled water to the town, and firefighters were checking numerous reports of gas leaks.

The town was temporarily cut off after the earthquake, when officials shut down a highway connecting Trona to Ridgecrest because of rockslides and cracks in the roadway.

Julia Doss, who maintains the Trona Neighborhood Watch page on Facebook, said residents reported that chimneys and entire walls collapsed during the quake.

She said the only food store in town has been shuttered. (source)

If you’ve ever driven through Trona, you know it’s not a wealthy town. Residents will be hard hit by repair bills.

According to PBS, the affected area can expect hundreds more aftershocks.

Since this region is currently experiencing two earthquake sequences at the same time (the one caused by the 6.4 quake on the Fourth of July and the one caused by the 7.1 shake on July 5), residents should prepare for a boatload of aftershocks less than 6.0 magnitude.

While these two quakes shook things up pretty dramatically, they don’t even hold a candle to the long-expected “Big One,” according to seismologists.

Seismologists say the “Big One” would be 125 times stronger than Thursday’s earthquake and 44 times stronger than the 1994 Northridge earthquake, which killed 57 people and caused $49 billion in economic losses. (source)

Michael Snyder wrote of the quote above:

Of course that figure is just an estimate and it is based on a hypothetical magnitude 7.8 earthquake.

Theoretically, a magnitude 9.0 earthquake would release 7,943 times as much energy as the Ridgecraft earthquake, and that would easily be the most destructive natural disaster that we have ever seen in all of U.S. history up to this point.

So, no, as big as it was, this was NOT “The Big One” that Californians have been dreading for decades. It wasn’t even on the same fault line as the one causing the most concern. Read Snyder’s articlefor more details.

Even in a small town like Ridgecrest and those surrounding it, looting and burglary has erupted after the quakes damaged buildings and took down critical infrastructure. Mayor Peggy Breeden told reporters that some “bad people” came into the community and tried to steal items from businesses.

The mayor of Ridgecrest says there were two reports of burglaries in the Southern California city following the 7.1 earthquake Friday night.

Mayor Peggy Breeden said Saturday that some “bad people” came into the community and tried to steal items from businesses.

Police Chief Jed McLaughlin said one business was burglarized, with an expensive piece of equipment stolen.

A home was also broken into and police are waiting to see what was taken. (source)

Fortunately, it looks like the looting is relatively minor at this point. But when the legendary “Big One” strikes, people may not get so lucky.

It’s important to remember that the aftermath of natural disasters can be the most dangerous time, particularly in areas with higher populations. Every prepper should have a home defense plan for situations such as these.

Gov. Newsom said some nice things about President Trump

Perhaps the most newsworthy part about this entire situation is the fact that Democratic Governor Gavin Newsom, an ardent supporter of California’s Sanctuary State declaration, has said some really nice things about President Trump, who is working hard to reduce the number of illegal immigrants in the United States.

Gov. Gavin Newsom says President Donald Trump has called him and expressed commitment to helping California recover from two earthquakes that hit the state in as many days.

Speaking to reporters after touring the damage zone, Newsom said Saturday that he and Trump talked about the struggles California has been through, including two devastating wildfires that happened just six months ago.

The Democratic governor said “there’s no question we don’t agree on everything, but one area where there’s no politics, where we work extremely well together, is our response to emergencies.”

“He’s committed in the long haul, the long run, to help support the rebuilding efforts,” Newsom said of Trump. (source)

What preppers can learn

It’s always important to study disasters when they occur. We can learn a lot, including what the emergency response looks like, what kind of damage was incurred, how soon the looters show up, and the struggles people face in the aftermath.

During these two earthquakes, there was property damage but injuries were limited. A number of fires occurred, probably due to electrical systems shifting. Gas lines leaked, the power was out for many, and public water lines were damaged. There is no place to purchase food if you don’t have it, or to buy or acquire water. Anyone unprepared out there in the dryest desert in America is at the mercy of emergency responders.

Evacuating isn’t easy due to cracked roads and rockslides. (This is why it’s always important to have multiple routes out and a versatile bug-out plan.) However, looters, said to be from out of town by Mayor Breeden, arrived fairly quickly.

Here’s hoping that the 7.1 is indeed, the biggest to hit these areas, although the once-per-minute aftershocks must surely be unsettling.

Those living near the San Andreas fault line should take note of what happened in this small town and use the information to prepare for the Big One that is at least one hundred years overdue.

via ZeroHedge News https://ift.tt/2XuWZP1 Tyler Durden

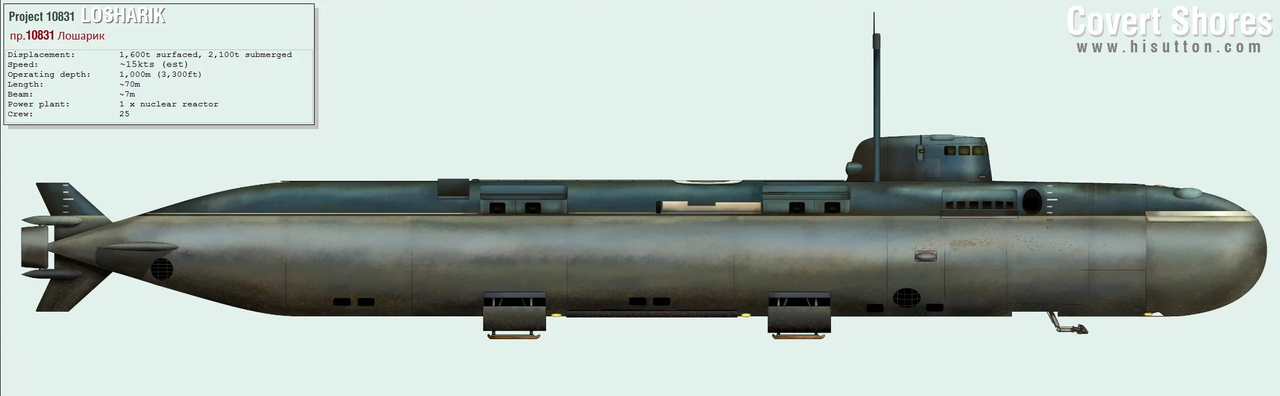

A high-ranking Russian military official says that 14 sailors who died in a recent fire aboard a nuclear submarine averted a “planetary catastrophe” before they perished.

While speaking at a funeral for the fallen servicemen, the official did not elaborate on what they did to avert said catastrophe, as the entire incident remains shrouded in mystery, according to Russian news outlet Open Media.

“Today we are escorting the crew of a research deep-water apparatus, who died while performing a combat mission in the cold waters of the Barents Sea. 14 dead, 14 lives. At the cost of their lives, they saved the lives of their comrades, saved the ship, did not allow a planetary catastrophe,” he said.

The Russian government has faced accusations of a cover up following the fatal accident – refusing to reveal the submarine’s name and mission under the guise of state secrets, while delaying other information such as the date of the accident itself, and the fact that the vessel was nuclear powered.

According to The Independent, “Several sources have identified the vessel as the A-31, or the Losharik submersible; a nuclear-powered unarmed vessel capable of deep sea missions. Its exact design is shrouded in secrecy, but it is believed to be an experimental 70m-long craft operating in conjunction with a larger mothership submarine. Developed over 15 years beginning in 1988, it is described as the Russian military’s most advanced deep water vessel.”

Local news agency Severpost reported that the smaller submarine was likely tethered to the larger Podmoskovye atomic submarine when it emerged from the Barents Sea at the mouth of the Kola Bay.

Citing an unnamed fisherman, the publication claimed the submarine was travelling quickly back towards base, but without obvious signs of distress. –The Independent

Contradictory reports as to what type of Russian sub had accident; some say AS-12 “Losharik” (in red box), others its BS-64 carrier submarine, both depicted in this photo published by @novaya_gazeta: pic.twitter.com/kIkGX9s4Qh

Russia’s defense ministry has labeled the 14 dead servicemen “Heroes of Russia.” They were buried in the Serafimov cemetery in St. Petersburg near a monument to the 118 Russians killed in the Kursk nuclear submarine disaster in 2000.

via ZeroHedge News https://ift.tt/32cMn5L Tyler Durden

While the market rallied last week and continues to flirt with all-time highs, not surprisingly, volume was exceedingly light because of the July 4th holiday on Thursday. As Carl Swenlin noted:

” SPY has formed a bearish rising wedge, and the VIX penetrated the upper Bollinger Band, which is short-term bearish. The wedge looks particularly weak because price rose off the bottom of the wedge this week, but it failed to reach the top of the wedge before touching the bottom of the wedge again today.”

With a majority of short-term technical indicators extremely overbought, look for a correction next week. What will be important is that any correction does not fall below the early May highs.

Furthermore, with participation continuing to narrow, it continues to look like the August/September time frame for a larger corrective cycle is still in play.

Such corrective actions would coincide with emergence of risk factors from trade, to disappointment from the Fed, to a disappointing earnings cycle and rising recessionary indications.

This doesn’t mean sell everything and go to cash. It goes suggest carrying some hedges, a higher than normal level of cash, and a rotation into “defensive” positioning will likely remain prudent.

Employment

The employment number on Friday was strong as we anticipated. This puts the Federal Reserve in a more difficult position with respect to cutting rates in July. The markets initially sold off on the news but did manage to stage a bit of recovery by late afternoon as “hope” remains high the Fed will cut rates regardless.

However, let’s take a look at a couple of “off the run” indicators about employment.

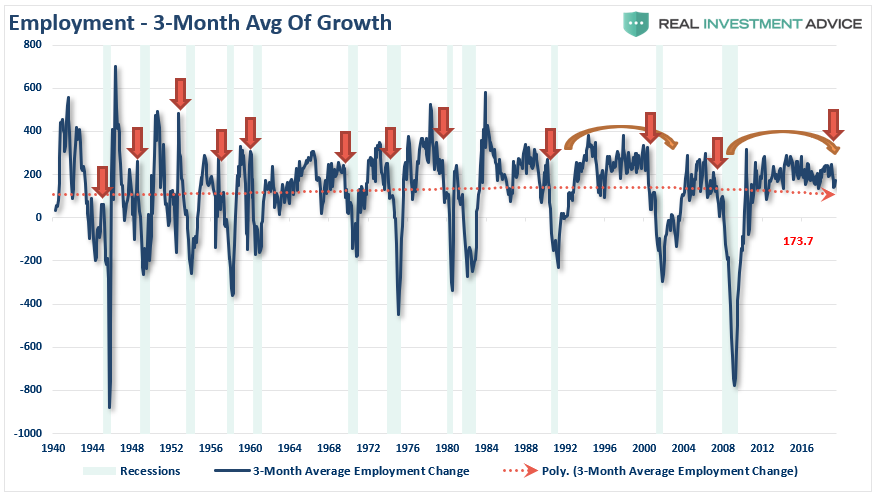

First, the Fed looks at the 3-month average of employment, still a lagging indication, to smooth out month to month variability. The chart is below:

Clearly, not only has the trend turned lower as of late, but has been weakening since 2015. This is commensurate with a late-stage economic expansion. However, the current weakness has been consistent with previous ebbs and flows of the business cycle and is not currently “weak” enough to suggest cutting rates in July is warranted.

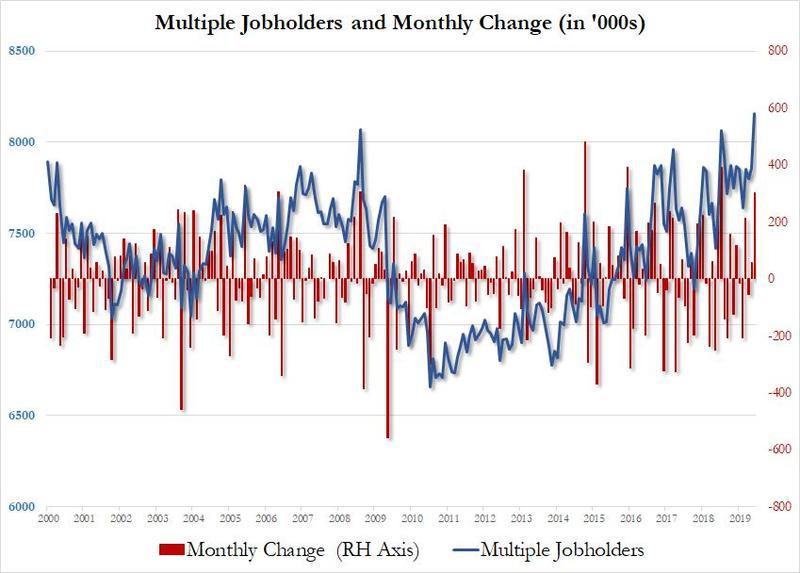

Second, the “quality of jobs” continues to deteriorate as shown by the surge in “multiple part-time job holders.” Per ZeroHedge on Friday:

“While the headline payrolls number was stellar, coming in higher than even the most optimistic Wall Street forecast, one aspect of today’s jobs report that will likely become a major talking point for Democrats and other critics of the Trump economy, is that the number of multiple-jobholders soared from 7.855 million to 8.156 million, a monthly surge of 301,000 – the biggest since July 2018, and an indication that the jobs number was far weaker than the headline represents if one excludes all those workers who represented two jobs to the BLS’ various surveys.”

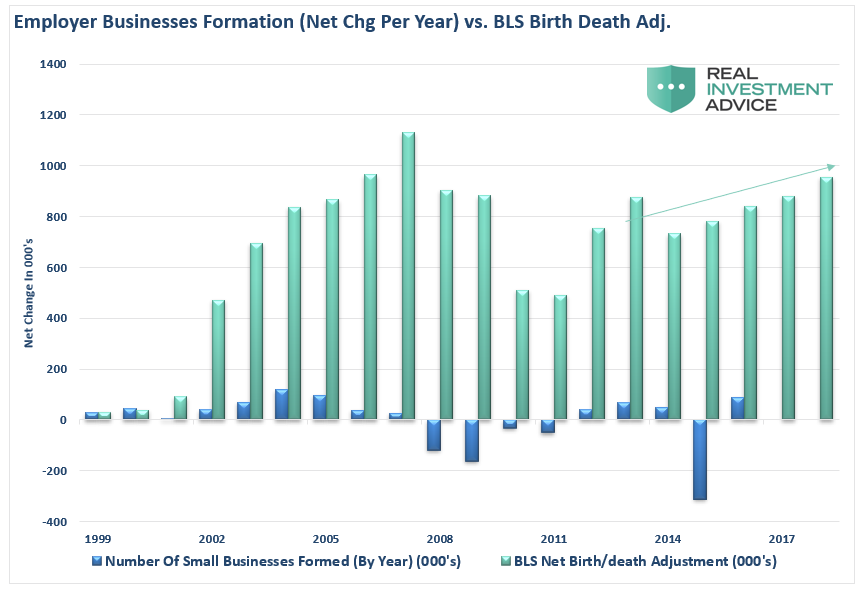

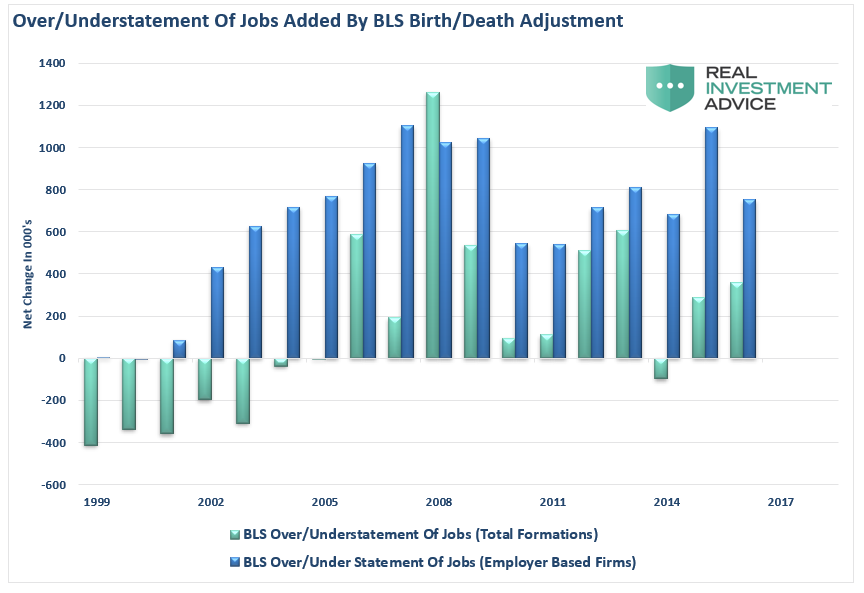

Lastly, the “birth-death adjustment” is, as we say in Texas, a “load of S***!”

Every month, the BLS adds numerous jobs to the non-seasonally adjusted payroll count to “adjust” for the number of “small businesses” being created each month, which in turns “creates a job.” (The total number is then seasonally adjusted.)

Here is my problem with the adjustment.

The BLS counts ALL business formations as creating employment. However, in reality, only about 1/5th of businesses created each year actually have an employee. The rest are created for legal purposes like trusts, holding companies, etc. which have no employees whatsoever. This is shown in the chart below which compares the number of businesses started WITH employees from those reported by the BLS. (Notice that beginning in 2014, there is a perfect slope in the advance which is consistent with results from a mathematical projection rather than use of actual data.)

These rather “fictitious” additions to the employee ranks reported each year are not small, but the BLS tends even to overestimate the total number of businesses created each year (employer AND non-employer) by a large amount.

How big of a difference are we talking about?

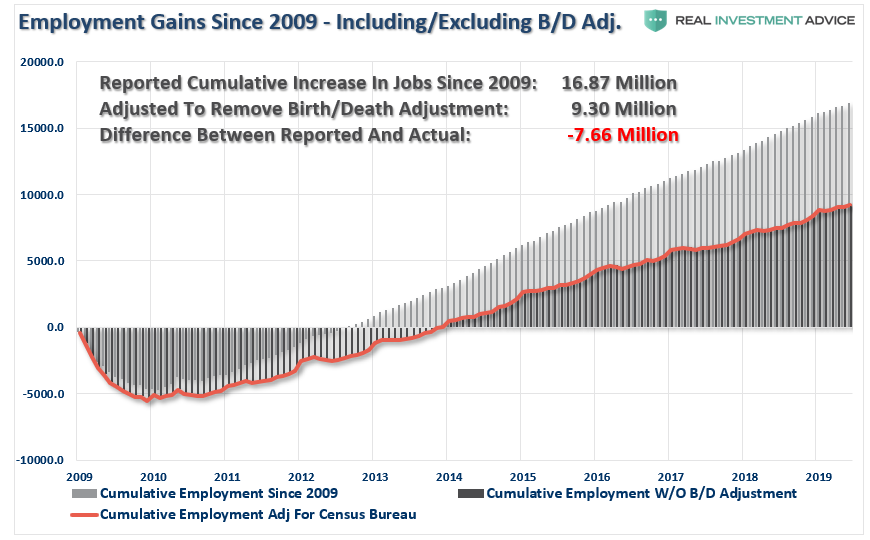

Well, in the decade between 2006 and 2016 (the latest update from the Census Bureau) the BLS added roughly 7.6 million more employees than were created in new business formations.

This data goes a long way in explaining why, despite record low unemployment, there is a record number of workers outside the labor force, 25% of households are on some form of government benefit, wages remain suppressed, and the explosion of the “wealth gap.”

However, while this data should concern you about the real strength of the economy, it is NOT data the Fed considers with respect to monetary policy decisions.

Volatility Warning

In the past we have spoken of the high-levels of complacency by investors in the market. As my friend Doug Kass recently pointed out, there are a litany of things investors should be concerned about:

The U.S./China trade negotiations last weekend didn’t “move the ball forward.” The outcome was just as expected with no promise of a substantive deal in the near future. (The two sides remain quite far apart with regard to the core issues of intellectual property and technology transfer, among other debated items).

The future U.S./China trade negotiations will not produce tangible results over the next 12 months.

Global cooperation and coordination is at an all-time low

Uncertainty of trade policy and the destruction of the post World War II political and economic order (in an increasingly flat and interconnected world) is consequential to future worldwide economic growth.

The precipitous drop in global bond yields is a sign of an imminent contraction (relative to consensus expectations) in global economic and U.S. corporate profit growth.

There is a lack of “natural share price discovery” in the face of monumental shifts in market structure (from active to passing investing.)

The dominance of products and strategies that worship at the altar of price momentum raise the risk of a major “Flash Crash.”

We are currently in an “earnings recession.”

Unbridled fiscal spending has adverse consequences.

There is over $12 trillion of sovereign debt having negative yields.

Large levels of debt in the system raised the risk of a credit-related event if something “breaks.”

The Federal Reserve (and other central bankers) can not catalyze economic activity (by lowering rates) from current low levels (“pushing on a string.”)

The current low level of interest rates are an important factor in holding down business fixed investment.

Current consensus economic and profit growth expectations will not be met in 2019-20.

GDP growth cannot exceed the rate of labor growth and productivity.

The recent downturn in high frequency economic data will be market impactful at some point.

Yet, despite all of this, implied volatility is flirting with record low levels.

As the old saying goes: “What could possibly go wrong?”

As You Jump In, They Are Jumping Out

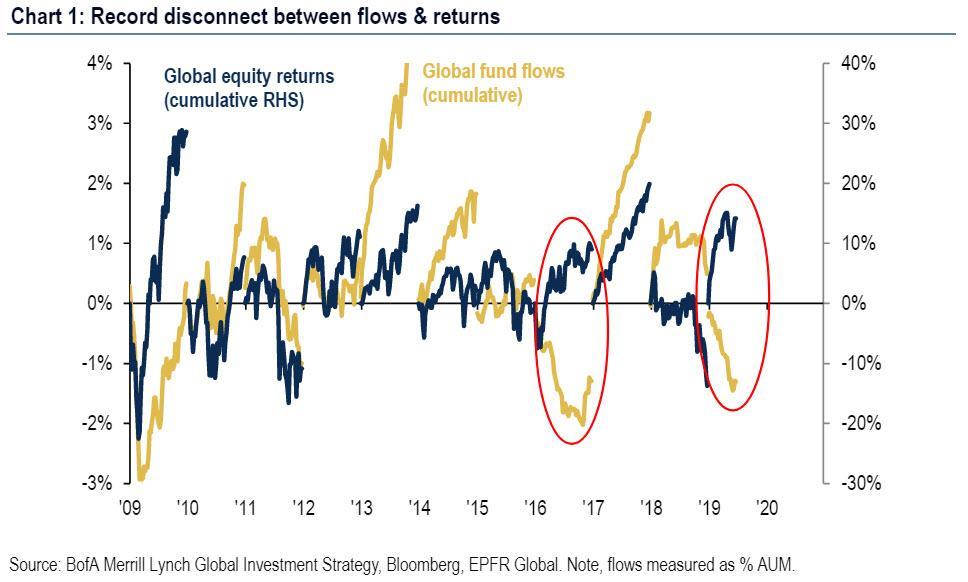

As the S&P climbs toward 3,000, individuals are clamoring to get in. Interestingly, while retail investors are chasing stocks, institutions continue to “de-risk” as $6.3B was allocated to bonds and $15.1B was pulled out of equities. The net result was a new record to date totaling $229B flowing into bonds, with $154B was pulled out of equities, according to Zerohedge.

“As BofA’s Michael Hartnett writes, there is now a record disconnect between flows & returns in 2019, with only 2016 a similar year in terms of outflows/returns.”

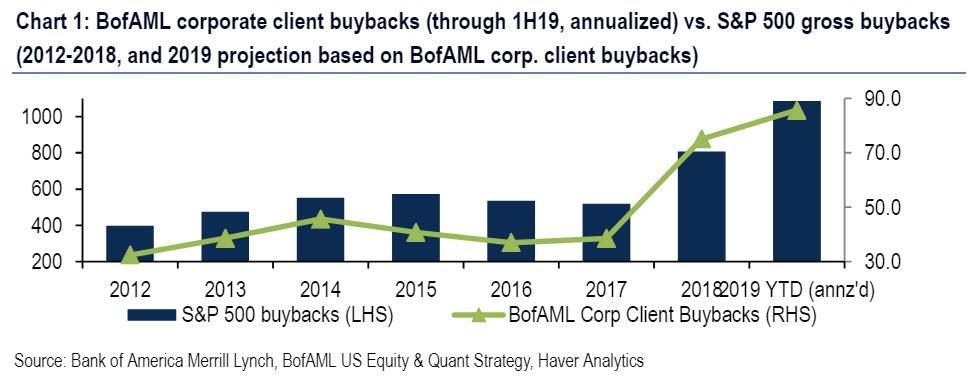

So, how is it that stocks remain near record highs? The primary culprit, as discussed previously, remains corporate buybacks which remain the primary source of market support in 2019. This is especially the case after US banks announced $129 bn in buybacks over the next 4 quarters.

Buybacks, according to BofA, are on pace for a record at $43B so far this year versus just $75B for the entirety of 2018. This suggests a record of over $1 trillion in S&P 500 buybacks for 2019.

Of course, the only reason retail investors own stocks at all is because the media tells them to.

After all, if you aren’t at the “casino table” you are missing out. Right?

One thing you might want to ask yourself, if you indeed believe the former, is why “rich people,” own more bonds than stocks generally speaking?

If buybacks are indeed supporting market performance, it is worth noting that such support can be turned off like a water spigot.

Which means someone is going to be left “holding the bag.”

Just make sure it isn’t you.

via ZeroHedge News https://ift.tt/2YDOihR Tyler Durden

In a move that will likely result in even greater political instability in Europe, which in recent years has become the primary target for every migrant holed up in Libya and just waiting for the chance to cross the Mediterranean, The New Arab reports that Libya’s UN-backed government is contemplating shutting down slave migrant detention centers and releasing all the detainees for their own safety, after airstrikes targeted one such center on Tuesday in a devastating attack which killed at least 53 people.

The strike left at least 130 wounded when it hit a hangar in which the migrants were detained in the Tripoli suburb of Tajoura. In the aftermath of the deadly bombing, Fathi Bashagha, the interior minister of Libya’s Government of National Accord (GNA) told the assistant to the UN special envoy to Libya, Maria do Valle Ribeiro, his government was accountable for the safety of Libyan civilians, including detained migrants.

However, Bashagha said the authority did not have the capacity to protect the centers in the face of airstrikes from advanced F16 jets, according to ministry.

Ribeiro also discussed the Tanjoura attack with Mohammed Al-Shibani, Libya’s deputy interior minister for migration affairs, agreeing on the need to transfer the hundreds of survivors to safer accommodation.

The Libyan justice ministry condemned the attack, vowing to work with humanitarian and migration organisations to repatriate the migrants or resettle them in third countries, because Libya’s compromised security situation could not provide them the safety they require.

Despite this, it was revealed on Thursday that around 300 migrants of the centre’s original 600 detainees were still being held there, while the International Organisation for Migration (IOM) said it was providing humanitarian assistance to the remaining detainees. The IOM was unable to confirm reports that dozens of migrants had fled on Tuesday night after the raid.

The UN’s humanitarian office OCHA, quoting survivors, said guards at the centre fired on migrants trying to flee causing no casualties, but the GNA interior ministry denied this as “rumours and false information”.

Needless to say, a similar rumor in the US – where migrant detention centers have become the focal talking point in domestic politics – could well spark a second civil war.

The IOM said its teams had “located” and transferred to hospital “a group of injured migrants who left Tajoura after the attack in the surrounding neighbourhood”. “Innocent lives were lost in the attack on Tuesday night, and immediate action is needed from all sides,” the IOM’s Libya chief of mission, Othman Belbeisi.

Naturally, the GNA and its arch-foe, militia leader Khalifa Haftar traded blame for the deadly assault, but despite a storm of outrage, a divided UN Security Council failed to unanimously condemn the attack in an emergency meeting Wednesday after the US did not endorse a proposed statement.

Migrants from Algeria, Morocco, Sudan, Somalia and Mauritania as well as other African nations were among the victims, Amin al-Hachmi, a spokesperson for the GNA health ministry said. The majority of migrants at the centre in Tajoura, a suburb east of the capital Tripoli, were from Eritrea and Sudan.

Two of the five hangars that made up the centre were hit by the air strike, while “hangar number 3”, which housed more than 120 migrants, took a direct hit.

According to the IOM, of the more than 600 migrants detained in Tajoura, 187 were registered with its “Humanitarian Voluntary Return” programme, which helps migrants go back to their home countries.

“The IOM continues to call for an end to the arbitrary detention and reminds all parties that civilians are not a target,” it said in a statement.

Some 3,300 migrants are still detained in and around the Libyan capital in centres “considered at-risk” in light of the fighting between the opposing forces of Hafter and the GNA, the IOM added.

Crater left behind by the missile that went through the roof then explodes amid the migrants. Another hit a building about 50 metres away. pic.twitter.com/9cXLKp4WWX

Rights groups say migrants face horrifying abuses – with many sold into slavery or worse – in Libya, which remains prey to a multitude of militias vying for control of the oil-rich country and which has emerged as a northern African proxy war between various middle-eastern nations. Their situation has worsened since Haftar – supported by the UAE, Egypt and Saudi Arabia – launched on 4 April an offensive to conquer Tripoli, where the Turkey-backed GNA is based.

UN agencies and humanitarian organisations repeat regularly their opposition to the return of migrants arrested at sea to Libya, where they find themselves in “arbitrary detention” or at the mercy of militias. The North African country that has been wracked by chaos since the 2011 uprising against dictator Moammar Gaddafi.

via ZeroHedge News https://ift.tt/2Jjp4Qr Tyler Durden

A pervasive belief throughout both the mainstream and independent media is that when faced with the threat of an economic downturn, central banks will act unconditionally to lower interest rates and inject fresh stimulus into markets by way of quantitative easing. One theory is that they will do this to stave off a collapse of the economy amidst rising trade ‘protectionism‘. But is the idea of central banks enacting policy to avert economic disaster one that stands up to scrutiny?

To gain a broader understanding of how banks behave before and after a financial crisis is triggered, the historical actions of the Federal Reserve are a good place to start.

The Great Depression

In a 2013 article written by Gary Richardson of the Federal Reserve Bank of Richmond, Richardson candidly explains how in 1928 and 1929 – leading into an impending stock market crash – the Fed were raising interest rates. According to Richardson, they did this ‘in an attempt to limit speculation in securities markets‘.

Conditions at the time included an influx of borrowed money being poured into the stock market, which contributed heavily to the soaring price of shares. A month before the crash that eventually manifested into a depression, the Dow Jones stood at a record high of 381 points.

Today, the Dow Jones is approaching an all time high of 27,000, and since it’s post crisis low of 6,469 has increased by 317%. A combination of ultra accommodative monetary policy and corporate stock buybacks has been responsible for much of this rise.

There were two significant ramifications from the Fed’s decisions to raise rates prior to the Great Depression. The first was that economic activity in the U.S. began to slow and, to quote Richardson, ‘because the international gold standard linked interest rates and monetary policies among participating nations, the Fed’s actions triggered recessions in nations around the globe.’

Two years after the stock market crashed in 1929, the Fed responded to what was now an international financial crisis by again tightening monetary policy. They also presided over a fall in the money supply, which from the fall of 1930 to the winter of 1933 declined by 30%. Richardson pointed out that this caused increased levels of debt, reduced consumption and increased unemployment. Banks, businesses and individuals had no alternative but to file for bankruptcy.

Richardson put this down as a ‘mistake‘ by the Fed, and insisted that actions which damaged the economy were unintentional.

In an economic letter published by the Federal Reserve Bank of San Francisco in 1999, economist Timothy Cogley outlined how from January to July 1928, the Fed raised the discount rate from 3.5% to 5%, and ‘engaged in extensive open market operations to drain reserves from the banking system‘. Over three-quarters of the Fed’s stock of government securities were sold.

By comparison, since the back end of 2017, the Fed has been actively reducing the size of its treasury securities and mortgage backed securities. Over $600 billion has been rolled off so far, a total that comprises both asset classes.

In the first half of 1929, the Fed kept monetary policy on hold, in spite of a slowing economy. Cogley mentions how economists have since argued that this inaction by the Fed was the cause of the downturn that followed.

In the aftermath of the October stock market crash, the New York Fed ‘bought government securities on its own account in order to inject reserves into the banking system.’ But after the recession had begun in 1930, monetary policy ‘resumed a contractionary stance.’ This, according to Cogley, ‘contributed to a further decline in economic activity and share prices.’

As with Gary Richardson, Cogley stressed that the Fed’s actions were ‘mistakes‘, the consequences of which were ‘unintended‘.

Finally, in a document from 1965 attributed to the Federal Reserve Bank of St. Louis, the points made by Richardson and Cogley are reinforced. Interest rates moved higher in the years leading up to October 1929. At the beginning of the great depression came a respite where rates began to fall, but ‘despite the continued contraction in economic activity, interest rates rose markedly in late 1931.’

***

Is it a viable explanation to say that the Fed’s actions nine decades ago were ‘unintended mistakes‘? Are we to believe that each time they make a policy ‘mistake‘ that they have no awareness of what the subsequent consequences will be?

To challenge this idea, we can turn to the current chairman of the Federal Reserve Jerome Powell. Around the time he assumed office in February 2018, the Fed released the minutes from a series of FOMC meetings held in 2012. During the meeting of October 23th/24th, Powell spoke about the future reversal of the quantitative easing programme that began following the collapse of Lehman Brothers in 2008. Here is an extract of those comments:

Right now, we are buying the market, effectively, and private capital will begin to leave that activity and find something else to do. So when it is time for us to sell, or even to stop buying, the response could be quite strong; there is every reason to expect a strong response.

I think we are actually at a point of encouraging risk-taking, and that should give us pause. Investors really do understand now that we will be there to prevent serious losses. It is not that it is easy for them to make money but that they have every incentive to take more risk, and they are doing so. Meanwhile, we look like we are blowing a fixed-income duration bubble right across the credit spectrum that will result in big losses when rates come up down the road. You can almost say that that is our strategy.

Two things stand out from Powell’s words. Firstly, that when the Fed begin reversing accommodative measures (which they did in December 2015 with their first rate hike in nine years), he fully anticipated a hostile reaction from markets. Secondly, there is an awareness that tightening policy would be a catalyst for puncturing the post-crisis bubble that has built up since the Fed cut rates to near 0% and inflated their balance sheet to hold over $4 trillion in assets. ‘You can almost say that that is our strategy.‘

The only conclusion that can be drawn from this is that the Fed ARE aware of the consequences of their actions, and have pushed on regardless with raising interest rates and off loading assets from its balance sheet. What Jerome Powell outlined is what he now presides over. He understood what would eventually happen if the Fed started to withdraw support from markets. Yet, they tightened policy anyway and continue to do so. It is not until September that the Fed plans to halt its balance sheet reduction programme.

Aside from the balance sheet, the betting now is that with the U.S. economy slowing, the Fed will reverse course in the short term and cut interest rates, and move towards introducing a forth round of quantitative easing to prevent an economic collapse. But when you look as far back as the Great Depression, and then to the more recent financial crisis of 2008, there is no precedent for them to do this.

The Fed neither prevented the Great Depression nor the crash of 2008. Their actions leading into both periods served to ensure a crisis was inevitable. Through monetary policy they knowingly built up unsustainable economic bubbles. Rates were rising in the run up to the 1929 crash, and were rising as late as June 2006 leading up to the 2008 downturn.

Granted, the 2008 crisis was different in the sense that the Fed began cutting interest rates in September 2007. But their actions were not enough to prevent a full blown financial crisis twelve months later.

What we are witnessing today looks increasingly similar to that which occurred ninety years ago.

When Donald Trump won the U.S. election in November 2016, interest rates were at 0.25%. Rates have moved higher eight times since, and currently stand at 2.25%. Back in 1929, just months prior to the stock market crash, the Fed paused on raising rates any higher. They did not cut rates until AFTER a crash had begun. And even this was short lived, with rates moving higher as the Great Depression took hold.

Ten years ago, when commenting on the Federal Reserve’s response to the financial crisis, then Fed chairman Ben Bernanke remarked that the Fed’s policy in the 1930s was ‘largely passive‘, and that political upheaval made ‘international economic and financial cooperation difficult.’

Assuming that the Fed do not raise rates in the near term, this description of circumstances ninety years ago will mirror the present day.

I would like to say to Milton and Anna: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.

In my view this is exactly what they are doing. If so, then it points to The Fed as knowingly and purposefully inducing an economic collapse. The difference between 1929 and 2019 is that this time the Fed have a ready made scapegoat to conceal their intent behind – that being the actions of the Trump administration in regards to trade.

Incidentally, the Great Depression of the 1930s saw a rise in ‘protectionist‘ trade policies, chiefly through the imposition of tariffs. A contraction in global trade soon resulted.

As I have written about previously, the most recent Fed communications confirm that they intended to carry on conducting monetary policy in accordance with their mandate for 2% inflation. To develop this position, consider the latest soundings from the Bank for International Settlements.

Last weekend the BIS released their Annual Economic Report, along with a speech by General Manager Agustin Carstens. The subject of global trade was dominant throughout. On speaking about trade tensions, Carstens said that they ‘bring up questions about the viability of existing supply chain structures and the very future of the global trading system.’ This corresponds to an article I posted back in October 2018, which looked at how the International Monetary Fund, The World Bank and the World Trade Organisation had published plans for ‘Reinvigorating’ and ‘Modernising’ the W.T.O.

I have long since argued that the model which globalists routinely utilise to instigate widescale ‘reforms‘ is to use crisis scenarios as opportunities. It is unlikely to be a coincidence that as trade tensions increase, internationalists are seeking to redefine global supply chains and the institutions which preside over them.

In his speech, Carstens also commented that because of trade tensions and slowing growth, the normalisation of monetary policy was now ‘in a holding pattern‘. He spoke of how ‘the course towards normalisation has called for some deviations.’

Deviations, but in the Fed’s case not as yet a U-Turn.

On the international level the policy position remains that monetary accommodation should be maintained where inflation is below target, and withdrawn where inflation is close to or above target. But Carstens made it clear that ‘monetary policy cannot be the engine of higher sustainable economic growth.’

The editorial of the annual report expands on this. With central banks putting ‘the very gradual monetary policy tightening on pause‘, it warns that ‘should inflation start to rise significantly at some point, it would induce central banks to tighten more.’

The trade conflict initiated between the U.S. and China, a potential escalation of tariffs with Mexico and the EU, and the possibility of no withdrawal agreement upon the UK’s departure from the EU, is a powder keg for a resurgence in global inflation. I will be discussing this further in an upcoming article.

The Federal Reserve’s next interest rate decision is at the end of July.

If as I suspect the Fed make no immediate movements, with the economy continuing to slow and economic activity weakening still further, it will be important to recognise that this would not be without precedent. They have done this before and been the cause of economic catastrophe. It would not be a surprise to see history repeat itself, and for the Fed to once again oversee the premeditated decline of the economy.

via ZeroHedge News https://ift.tt/2L3HgzD Tyler Durden

{kind=link}