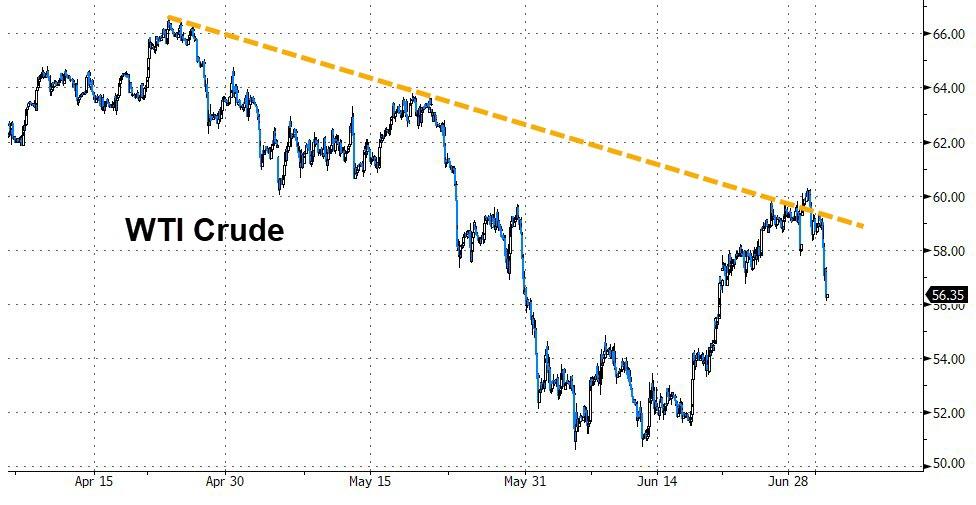

Oil suffered its worst reaction to an OPEC meeting since 2014 today, plunging almost 5% prompting OPEC Secretary-General Mohammad Barkindo to tell reporters in Vienna that, “the drop in crude prices on Tuesday was an ‘anomaly’.” Not everyone agreed.

“There are concerns that demand might slow to where it overpowers supply,” Bart Melek, head of commodity strategy at Toronto’s TD Securities, said in an interview.

The “gloomy” data, especially from China, “is very much part and parcel of what we’re seeing.”

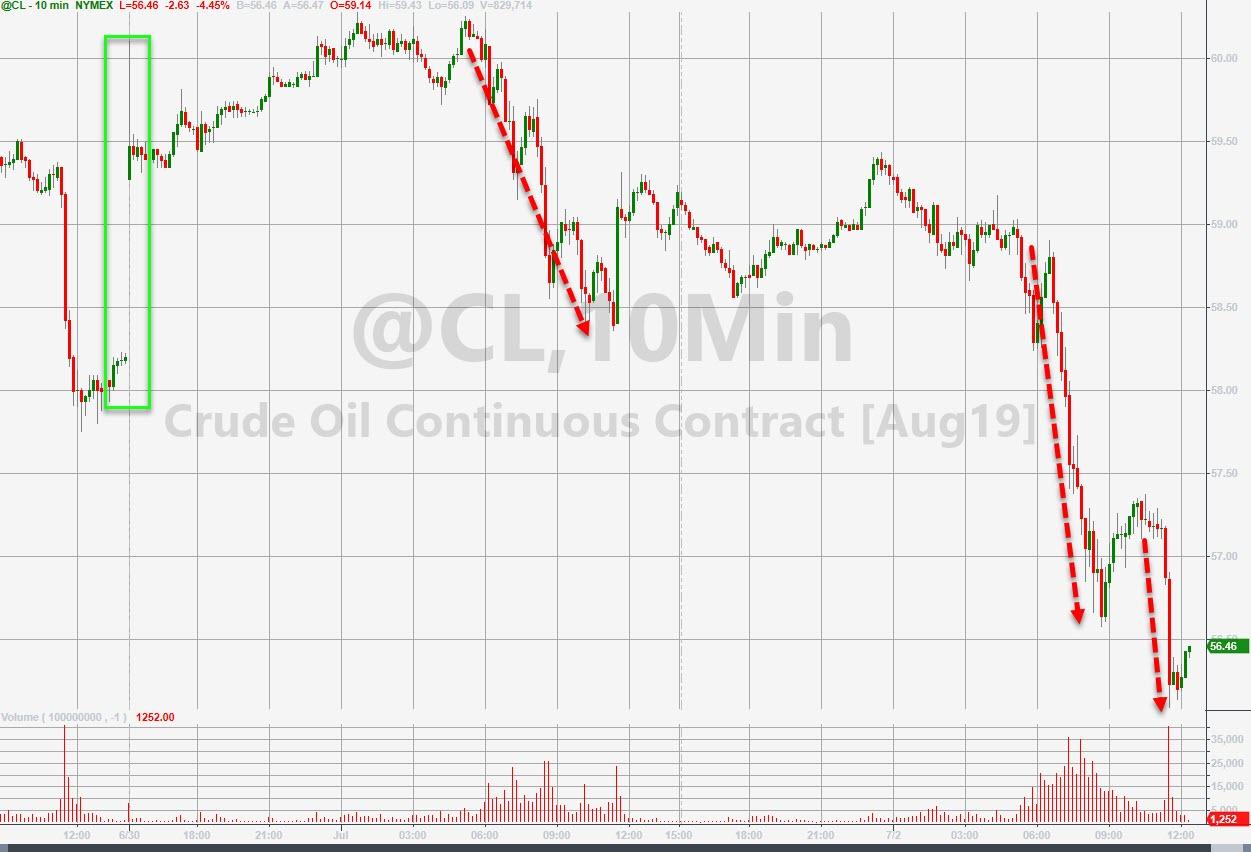

API

Crude -5mm (-3mm exp)

Cushing +882k (-1.26mm exp)

Gasoline -387k (-2.2mm exp)

Distillates -1.7mm (=1.0mm exp)

After last week’s huge crude draw, expectations were for another decent-sized draw and API reported a bigger than expected crude draw…

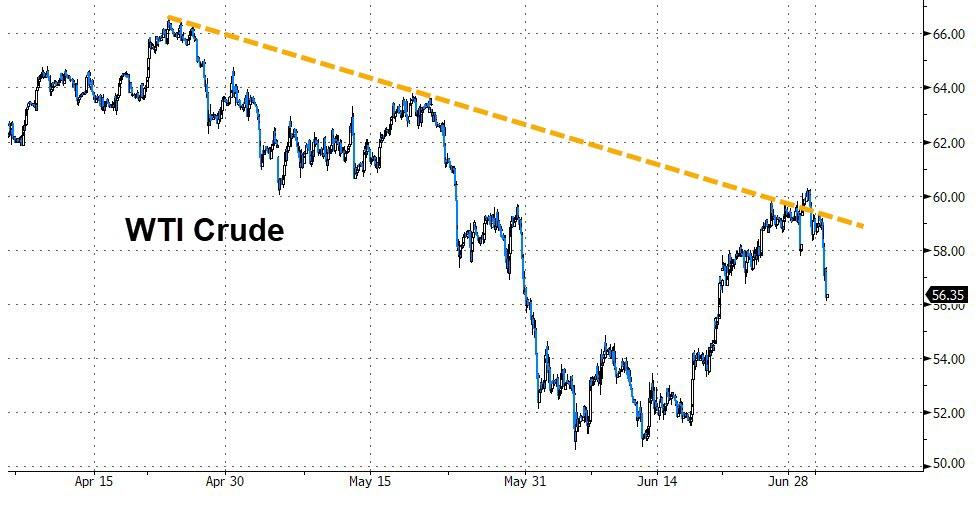

WTI rolled over at a key trendline level…

But was unable to hold a modest rebound after the API print…

via ZeroHedge News https://ift.tt/2LyuY1A Tyler Durden

Our monetary system is broken. It’s given us low growth, a shrinking job force, inequality beyond what a healthy economy would produce, inefficiency, and the unnatural growth of finance as a portion of the economy.

Our aging Federal Reserve System starves both small businesses and Silicon Valley of the capital needed to grow jobs and wages.

Fed policy translates into zero-interest-rate loans for the government and its cronies, and little or nothing for savers or small businesses. And it has transformed Wall Street from an engine of innovation into a servant of government power.

But I believe America can be set on the right path towards a robust and broadly shared capitalism again with just three steps.

Step 1: Abolish Capital Gains Tax on Currencies

This country already allows gold currency. The Treasury mints millions of one-ounce silver eagle dollars that are worth more than twenty dollars apiece and one-ounce gold eagle fifty-dollar pieces that are worth $1,150 apiece.

Virtually all of these are hoarded.

Though it has been legal since 1987 to use them at their metallic value, that route leads to a capital gains tax on their appreciation.

Since the appreciation of a gold or silver piece is by reasonable definition all inflation, the tax is simple confiscation (like all capital gains taxes on spurious inflationary profits).

The move of gold and silver coins into circulation would offer a corrective of constitutional money for any dollar debauchery by the Fed.

Step 2: Remove Obstacles to Alternative Forms of Money

Despite imprudent governmental interference, the internet remains a bastion of American power, with U.S. companies such as Apple, Google, Amazon, Microsoft, Facebook, eBay, Cisco, Qualcomm, and scores of others capturing the bulk of all internet revenues.

The internet plays a central role in the American economy. But there is a profound flaw in its architecture, as I have explained before. It was designed for communications, not transactions.

Around the globe, transactions are shifting toward the internet. Although online purchases remain between 6-7% of all commerce, internet trade is expanding rapidly.

But to buy something on the Internet, you often have to give the supplier sufficient information — credit card number, expiration date, address, security code, mother’s maiden name, and so on — to defraud you or even to steal your identity.

This information therefore has to be protected at high cost in firewalled central repositories and private networks, which are irresistible targets for hackers.

With transactional overhead dominated by offline financial infrastructure, micropayments are uneconomic, and the internet fills with fake offers, bogus contracts, and pop-up hustles. Some 36% of web pages are bogus, emitted by bots to snare information from unwary surfers.

The internet today desperately needs a new trusted and secure payment method that conforms to the shape and reach of global networking and commerce.

It should eliminate the constant exchanges of floating currencies, more volatile than the global economy that they supposedly measure. It should be capable of transactions of all sizes. And it should partake of the same monetary sources of stable value that characterize gold.

The new system should be distributed as far as internet devices are distributed: a dispersed organization based on peer-to-peer links between users, rather than a centralized hierarchy based on national financial institutions.

Fortunately such a payment system has already been invented. It is set to become a new facet of internet infrastructure.

It is called the bitcoin blockchain.

The bitcoin blockchain is already in place. It functions peer-to-peer without the need for outside trusted third parties. And it follows theorist Nick Szabo’s precursor, bitgold. Its value, like gold’s, is ultimately based on the scarcity of time.

Even if bitcoin proves flawed, scores of companies are developing alternatives based on the essential blockchain innovation that can serve as a successful transactions medium for digital commerce. The existence of such a system would enable sellers on the internet, such as content producers, to name their own prices and collect their funds directly.

And the very process that validates the transaction would prohibit spam. There would be no hassle of bartering content for advertising revenues at some aggregator such as Google. Aggregators with advertising clout would merely add inefficiency to an automated system that minimize transaction costs.

The internet would have a money system of its own.

With a low market price for goods and services — Google and other players could charge millicents for their services and still make a mint — the internet economy would transcend its current den of thieves and hustlers.

It could attain its promise as a frictionless facilitator of human creativity rather than as a channel of chicanery. Its markets would impel the world toward new realms of knowledge and wealth.

But the success of a new global standard of value on the internet entails a ban on taxation of internet currencies. If only government currencies escape taxation, alternative currencies such as bitcoin will always be relegated to niches.

Step 3: Fix the Dollar

That brings us to the third step: fixing the U.S. dollar.

How do we do this?

Monetary scholar Judy Shelton already devised a play. The chief instrument would be the creation of Treasury Trust Bonds — five-year Treasuries redeemable in either dollars or gold. They could be enacted either through legislation or as a Treasury initiative.

Legislation would specifically authorize the issuance of five-year Treasury securities that pay no interest, but provide for payment of principal at maturity in either ounces of gold or the face value of the security, at the option of the holder.

The instrument would be an obligation of the U.S. government to redeem the nominal value (“face value”) in terms of a precise weight of gold stipulated in advance or the dollar amount established as the monetary equivalent. The rate of convertibility (in gold grams) is permanent throughout the life of the bond; it defines the gold value of the dollar.

As Alan Greenspan declared in the Wall Street Journal during the previous era of monetary turmoil, in 1981:

“In years past a desire to return to a monetary system based on gold was perceived as nostalgia for an era when times were simpler, problems less complex and the world not threatened with nuclear annihilation. But after a decade of destabilizing inflation and economic stagnation, the restoration of a gold standard has become an issue that is clearly rising on the economic policy agenda.”

In fact, Greenspan suggested that “Shelton bonds” would pave the path to the future…

“The degree of success of restoring long-term fiscal confidence will show up clearly in the yield spreads between gold and fiat dollar obligations of the same maturities. Full convertibility would require that the yield spread for all maturities virtually disappear.”

Of course, as Fed chairman, Greenspan went on to become a major maestro of monopoly money at the Fed. And in his subsequent books he expressed many regrets and misgivings about the nature and role of central banks.

But in an era of new monetary turmoil, Shelton bonds still have traction. In addition, as bitcoin blockchain innovations spread through the internet, borrowers could also issue bonds with a bitcoin payoff. So new systems based on gold and blockchain innovations can evolve into a new world monetary infrastructure.

These are the three steps that can restore integrity to the monetary system.

As I explained previously, this is how we can save Main Street from the menace of monopoly money, transcend the dismal science of stagnation and decline, and restore the American mission and dream.

via ZeroHedge News https://ift.tt/2Nt9Z32 Tyler Durden

Yesterday Donald Trump signed a law that forbids the IRS to seize the bank accounts of business owners based on nothing more than the allegation that they “structured” their deposits or withdrawals to evade federal reporting requirements. That kind of odious money grab—which, like other forms of civil forfeiture, did not require criminal charges, let alone a conviction—provoked bipartisan outrage in Congress after it was publicized by the Institute for Justice, the libertarian public interest law firm.

Since 1970 the humorously named Bank Secrecy Act has required financial institutions to report transactions involving $10,000 or more to the Treasury Department, because such large sums of cash are obviously suspicious. You know what else is suspicious? Transactions involving less than $10,000, because they suggest an attempt to evade the government’s reporting requirement, which has been a federal crime, known as “structuring,” since 1986.

Suspicion of structuring was the sole justification when the IRS seized $60,000 from Maryland dairy farmer Randy Sowers in 2012, $446,000 from Long Island candy and snack wholesaler Jeffrey Hirsch that same year, $33,000 from Iowa restaurateur Carole Hinders in 2013, and $107,000 from North Carolina convenience store owner Lyndon McLellan in 2014. The negative publicity generated by stories like those led the IRS to announce in 2014 that it would no longer pursue forfeiture in cases where there was no evidence of illegal activity beyond structuring itself. The Justice Department unveiled similar restrictions in 2015.

Section 1201 of the Taxpayer First Act, the bill that Trump signed yesterday, codifies the shift in IRS policy, saying, “Property may only be seized by the Internal Revenue Service” in structuring cases “if the property to be seized was derived from an illegal source or the funds were structured for the purpose of concealing the violation of a criminal law or regulation other than” structuring. The law also requires that the IRS notify the owner within 30 days of a seizure and mandates a hearing to consider whether there was probable cause for the seizure within 30 days of the owner’s request.

“Previously,” the Institute for Justice notes, “property owners targeted for structuring had to wait months or even years to present their case to a judge.” Sowers and Hirsch, both I.J. clients, “ultimately recovered their wrongfully taken money, but only after years of legal proceedings and high-profile media coverage.”

I.J. senior attorney Darpana Sheth, who heads the organization’s National Initiative to End Forfeiture Abuse, welcomed the demise of this particularly egregious kind of legalized theft. “Innocent entrepreneurs will no longer have to fear forfeiting their cash to the IRS, simply over how they handled their money,” Sheth said in a press release. “Seizing for structuring was one of the most abusive forms of civil forfeiture, and we’re glad to see it go.”

The restrictions in the new law do not apply to the Justice Department. I.J. says a campaign it organized resulted in “464 petitions from owners seeking to recover their money that had been seized for structuring.” Of the 208 petitions relating to forfeitures pursued by the IRS, the agency granted “roughly 84 percent and returned over $9.9 million to property owners.” Of the 256 petitions related to cases involving the DOJ, the IRS recommended that the department grant 194. But the DOJ had accepted just 41 petitions, or 21 percent, “and refused to return more than $22.2 million as of last summer.”

from Latest – Reason.com https://ift.tt/2XQG60B

via IFTTT

Yesterday Donald Trump signed a law that forbids the IRS to seize the bank accounts of business owners based on nothing more than the allegation that they “structured” their deposits or withdrawals to evade federal reporting requirements. That kind of odious money grab—which, like other forms of civil forfeiture, did not require criminal charges, let alone a conviction—provoked bipartisan outrage in Congress after it was publicized by the Institute for Justice, the libertarian public interest law firm.

Since 1970 the humorously named Bank Secrecy Act has required financial institutions to report transactions involving $10,000 or more to the Treasury Department, because such large sums of cash are obviously suspicious. You know what else is suspicious? Transactions involving less than $10,000, because they suggest an attempt to evade the government’s reporting requirement, which has been a federal crime, known as “structuring,” since 1986.

Suspicion of structuring was the sole justification when the IRS seized $60,000 from Maryland dairy farmer Randy Sowers in 2012, $446,000 from Long Island candy and snack wholesaler Jeffrey Hirsch that same year, $33,000 from Iowa restaurateur Carole Hinders in 2013, and $107,000 from North Carolina convenience store owner Lyndon McLellan in 2014. The negative publicity generated by stories like those led the IRS to announce in 2014 that it would no longer pursue forfeiture in cases where there was no evidence of illegal activity beyond structuring itself. The Justice Department unveiled similar restrictions in 2015.

Section 1201 of the Taxpayer First Act, the bill that Trump signed yesterday, codifies the shift in IRS policy, saying, “Property may only be seized by the Internal Revenue Service” in structuring cases “if the property to be seized was derived from an illegal source or the funds were structured for the purpose of concealing the violation of a criminal law or regulation other than” structuring. The law also requires that the IRS notify the owner within 30 days of a seizure and mandates a hearing to consider whether there was probable cause for the seizure within 30 days of the owner’s request.

“Previously,” the Institute for Justice notes, “property owners targeted for structuring had to wait months or even years to present their case to a judge.” Sowers and Hirsch, both I.J. clients, “ultimately recovered their wrongfully taken money, but only after years of legal proceedings and high-profile media coverage.”

I.J. senior attorney Darpana Sheth, who heads the organization’s National Initiative to End Forfeiture Abuse, welcomed the demise of this particularly egregious kind of legalized theft. “Innocent entrepreneurs will no longer have to fear forfeiting their cash to the IRS, simply over how they handled their money,” Sheth said in a press release. “Seizing for structuring was one of the most abusive forms of civil forfeiture, and we’re glad to see it go.”

The restrictions in the new law do not apply to the Justice Department. I.J. says a campaign it organized resulted in “464 petitions from owners seeking to recover their money that had been seized for structuring.” Of the 208 petitions relating to forfeitures pursued by the IRS, the agency granted “roughly 84 percent and returned over $9.9 million to property owners.” Of the 256 petitions related to cases involving the DOJ, the IRS recommended that the department grant 194. But the DOJ had accepted just 41 petitions, or 21 percent, “and refused to return more than $22.2 million as of last summer.”

from Latest – Reason.com https://ift.tt/2XQG60B

via IFTTT

Stocks and bond yields sink on a trade truce, oil tanks on an OPEC deal, and AUD spikes on a RBA rate cut…

Chinese stocks went nowhere overnight…

European markets slipped early on the tariff headlines but recovered by their close…

Major decoupling between Small Caps and Trannies and the rest of the market today (the latter barely unchanged as the former tank). Nasdaq outperformed as markets rallied in the last hour mysteriously just as they did yesterday…

As the short-squeeze ammo appears to have run out…

Any equity gains were dominated by a bid for defensives…

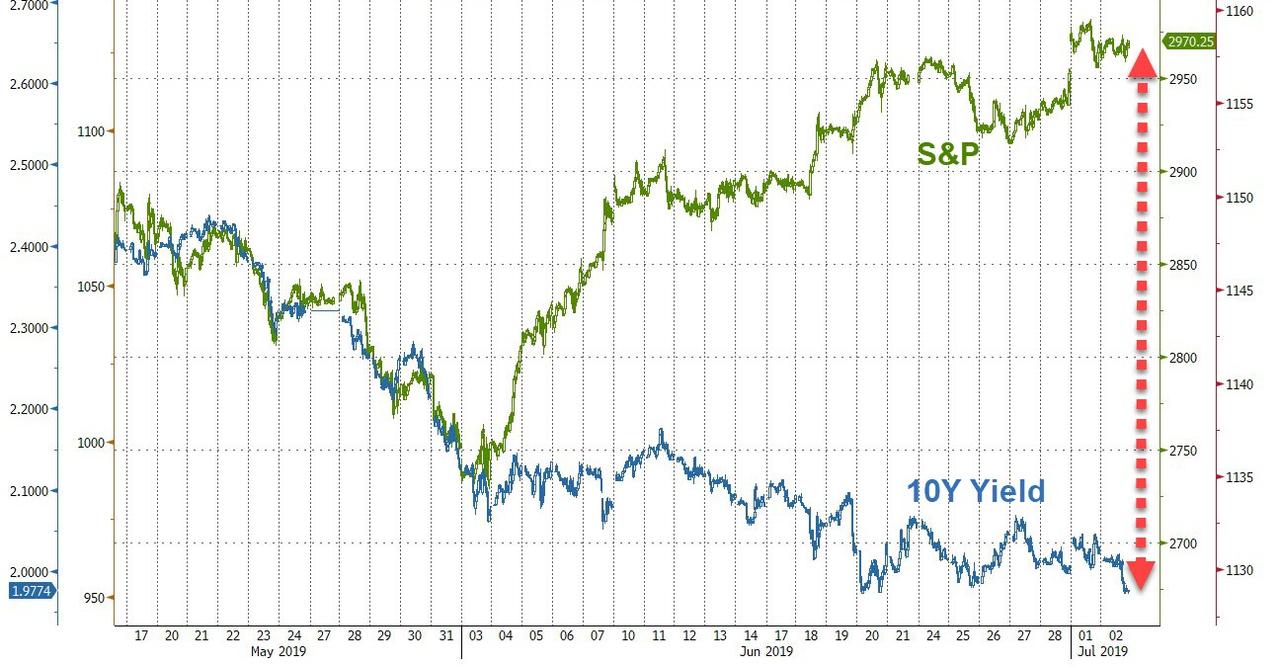

Stocks and Bond yields decoupled…

Treasury yields tanked today leaving all but 2Y now lower since the hype of the trade-truce…

10Y Yields tumbled back below 2.00% again…and held there…

Pushing 10Y Yields to the lowest close since Nov 2016…

Market expectations for July remain at 80% for 25bps cut and 20% for 50bps cut…

Stocks decoupled from FX carry today…

Cryptos staged a big recovery today after another ugly night…

Bitcoin ripped back above $10,000 after toying with it for 24 hours (up $1200 from today’s lows)…

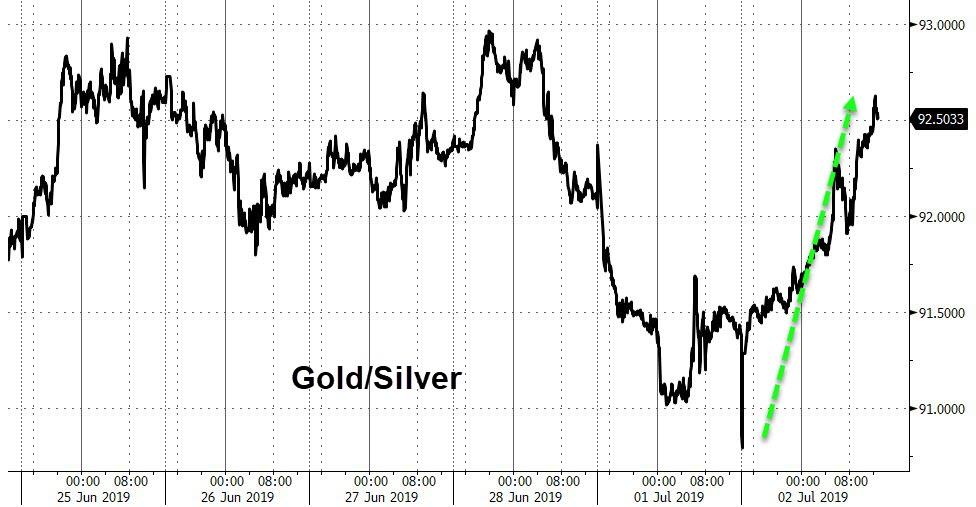

PMs outperformed notably as copper and crude extended their losses…

Gold surged back above $1400, erasing the trade-truce losses…Gold’s best day since Oct 2018 (on the heels of Lagarde as ECB head?)

While silver rallied on the day, it continues to underperform…

Stocks and oil prices decoupled today…

WTI dumped on the day, despite OPEC+ production cut agreements…

WTI tested the trendline and failed…

Copper and Stocks decoupled

Finally, the jaws of death widen further…

via ZeroHedge News https://ift.tt/2JjbCuB Tyler Durden

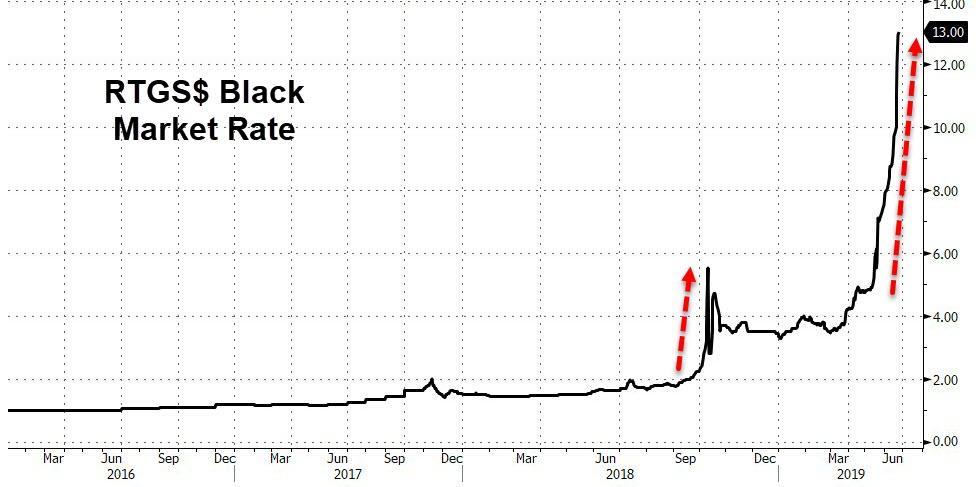

According to Zimbabwe’s President Emmerson Mnangagwa, the reintroduction of the Zimbabwean dollar (which was officially abandoned a decade ago), the banning of the use of other international currencies, and the resulting hyperinflation (analysts are already forecasting a 100% inflation rate for 2019) are simply important steps to “restoring normalcy to our economy.”

But as anybody who has lived in, or visited, Zimbabwe over the past couple of decades, “normal” isn’t exactly a high bar. Considering that, under ex-leader Robert Mugabe, the Zim dollar once depreciated to 35 quadrillion per $1 (transforming the wheelbarrow into an essential tool for facilitating routine, every-day transactions like buying groceries), we’d think Zimbabweans are looking for something different, rather than a return to the country’s insanely dysfunctional status quo.

Of course, Mnangagwa’s decision to revive the hated Zim dollar might be more pragmatic than it first appears: After all, South Africa banks had largely cut Zim off from the country’s most stable supply of American dollars (the de facto currency of choice for Zimbabweans hoping to protect their wealth), so Mnangagwa’s decision to ‘ban’ the greenback might be the political equivalent of shouting ‘you can’t fire me because I quit!’ at a former employer.

But regardless of the government’s motives, this doesn’t change the fact that Zimbabweans have been struggling with shortages of cash, fuel and electricity for months. And now, the country’s ‘everything shortage’ is impacting the hopes and dreams of any Zimbabwean who still harbors hopes of leaving Zimbabwe.

That’s right: Zimbabwe’s government is so broke, the company that prints its passports is refusing to supply any new booklets until the government has taken care of its debts.

Tendai Mpofu applied for new passports for his sons more than two months ago. Their current ones expire this month, just when they’re due to travel to South Africa for a school sports event. It may be a long wait before they get new documents.

With inflation at almost 100% and an acute lack of foreign currency, Zimbabwe is facing its worst economic crisis in more than a decade. While President Emmerson Mnangagwa has said that the passport company is refusing to print anything until the government has cleared its debts, others say Zimbabwe is simply too broke to import the ink and paper needed.

And it’s not only passports that are in short supply: The government is also running out of the cheap plastic it uses to print ID cards.

An official at the passport office said the situation is “dire” and passports were only being issued for emergencies. Identity cards are also hard to come by – metal cards were replaced with plastic ones but now plastic is in short supply.

No need to panic, though – the government has the (admittedly dire) situation under control.

Home Affairs Minister Cain Mathema told the state-run Herald newspaper recently that things will improve and that the government was “working on it.”

via ZeroHedge News https://ift.tt/3251Vsq Tyler Durden

For decades now it’s been a sellers’ market for American universities. Conventional wisdom held that the most important way to succeed in life was to get a college diploma, no matter the cost. Perhaps you’ve noticed university tuitions going up and up. And up. Inexorably.

And so has the debt incurred by their students and those students’ parents. It now totals about $1.6 trillion.

This being another tedious presidential election season, such a massive debt burden has attracted the attention of feeding politicians seeking to reap votes from younger Americans tasked with repaying the loans they signed up for.

As we wrote here earlier this week, Bernie Sanders, Elizabeth Warren, Julian Castro and a growing list of the growing field of candidates have announced various plans to make public school tuitions free and to forgive these massive debts using — you guessed it — new taxes on someone else, namely the well-to-do.

Now comes a new wrinkle in these schemes and the universities’ hopes of continuing to reap huge tuition increases.

A new poll of nearly a quarter-million Americans has found fully two-thirds of them have buyer’s remorse about their diploma, their major and the higher education experience in general. How much longer do you think folks are going to keep paying such fees that produce such dissatisfaction and unhappiness?

Not surprisingly perhaps, the new survey found the top regret was incurring immense debts for that higher education, a debt whose payments run on for many years, causing postponed marriages and families. An estimated 70 percent of college graduates this year finished school with loans to repay averaging $33,000.

Even older baby boomers are incurring college debts as they return to school for training in new areas not affected by automation and other labor-saving methods. The survey by PayScale found that even Americans over age 62 had some $86 billion in unpaid debts, theirs or their childrens’.

The second largest graduate regret was their choice of college majors. Sen. Marco Rubio has noted in speeches that the occupational demand for Greek philosophers has not been good for about 2,000 years.

Three-quarters of humanities graduates expressed regrets over their choice of study areas, tied to their difficulty finding employment in those areas at higher paying jobs enabling them to pay down the debt.

Most satisfied were majors in math, science, tech and especially engineering. More than a third of computer science grads and four-in-ten engineering grads had no regrets about their area choice of studies.

Interestingly though, teachers expressed the least regrets over their career choices, second least to engineers, despite the chronically low pay of such educators.

via ZeroHedge News https://ift.tt/2XKMRkq Tyler Durden

Several families of the nearly 350 people who died in two Boeing 737 Max crashes say they haven’t received so much as a letter of condolence from the planemaker, according to Business Insider.

The parents of a woman killed on one of the flights told Business Insider they had received “no condolences” and “no direct communication” from Boeing despite numerous public apologies by the plane maker and said Boeing CEO Dennis Muilenburg “talks to other people but not us, the victims’ families.”

Nadia Milleron and Michael Stumo lost their 24-year-old daughter, Samya Stumo, when the Boeing 737 Max 8 jet operated by Ethiopian Airlines crashed in March, killing all 157 people on board. –Business Insider

And while we’re guessing the Boeing legal department may have been involved in the decision not to directly contact the families of inevitable (and current) plaintiffs as the likely cause of the crashes became more clear, attorneys representing over 50 families of those killed told Business Insider that their clients were treated similarly.

Miami-based aviation attorney Steve Marks said that Boeing’s response was not “unusual” from manufacturers, however the company’s reaction was “worse” than a typical response.

Nadia Milleron, whose daughter was killed in the Ethiopian Airlines crash of a Boeing 737 Max, at a press conference announcing a wrongful-death suit against Boeing in April. (REUTERS/Kamil Krzaczynski)

According to Marks, Boeing “came out really quickly after the second tragedy, and said: ‘We own it, it’s our problem’,” yet “has since backed those comments off, in many different ways, which I think has only inflamed the situation, as far as the families are concerned.”

Aviation attorney Mike Danko similarly told Business Insider that it’s “not unusual” for a manufacturer not to apologize or offer support following fatal plane crashes, noting the company’s public apologies.

Boeing has repeatedly publicly apologized for the crashes. Its CEO, Dennis Muilenburg, first apologized in a Boeing video in April, three weeks after the second crash. In the video, he said that the company was “sorry for the lives lost” and that the “tragedies continue to weigh heavily on our hearts and mind.” –Business Insider

In May, Muilenburg apologized publicly, saying the company was “sorry for the loss of lives in both accidents,” and “sorry for the impact to the families and loves ones that are behind.”

That said, the 737 Max situation is unique in that the crashes are suspected to have been caused by a known flaw in the plane’s anti-stall system which had been raised by pilots, while over 400 pilots are now in a class-action lawsuit against the company, accusing Boeing of an “unprecedented cover-up” of “known design flaws.”

Muilenburg admitted at the Paris Air Show in June that Boeing had “made a mistake” in handling the anti-stall system, and that the company’s communication was “not acceptable.”

Kenyans mourning family members and friends who died in the Ethiopian Airlines Flight 302 crash. (REUTERS/Baz Ratner)

Not good enough, say the families.

Milleron and Stumo told Business Insider that Muilenburg “never apologized for killing our daughter.”

Stumo said Boeing “put a camera in Muilenburg’s face,” referring to his video apology in April.

“A true apology is when you sit across the table together and exchange sentiment — at the very least.”

Milleron said the apology needed to say: “I did this wrong thing to you and I am sorry. I regret this specific wrong that I did to you.”

“That’s an actual apology,” she said. “If they just say they are sorry to a camera, not to the actual persons that they’ve harmed, that is not an apology at all.

“I don’t understand how he could possibly think so, and I don’t think the American people see that as an actual apology.” –Business Insider

According to Danko, the aviation attorney, Boeing could have reached out and said something as simple as “We’re so sorry for what happened and for the unspeakable loss you’ve experienced. We haven’t yet gotten to the bottom of what happened but are committed to doing so. We want to make sure that no one else has to go through what you’re going through now. We will not rest and our plane will not fly again until we’re 100% convinced of that.”

via ZeroHedge News https://ift.tt/324lBwt Tyler Durden

In late April, Juan Guaido launched an attempted coup in Venezuela, one which the US figured would be an easy success to sweep him into power after months of insisting he was the legitimate ruler. As July starts, Guaido seems no closer to power than ever.

“We’re on track but it’s the wrong track,” said Rafael Narvaez, a taxi driver in the western coastal city of Punto Fijo.

“I thought that finally the moment had come to recover our country,” Narvaez, 43, said. “Now I’m disappointed.”

The US-backed coup idea didn’t work, and that was effectively the only real plan they had. Unilaterally declaring regime change was clearly never going to work, and since Guaido wasn’t even running for president in the last election, failing to get the military to overturn the vote was really his last major shot.

Yon Goicoechea, a member of Guaido’s policy team, acknowledged there was “fatigue” among Venezuelans.

“We have to fight against demobilization and despair,” he said. “We Venezuelans have to keep consistent in our support for Guaido and be patient.”

The Venezuelan public is catching up to something President Trump apparently figured out awhile ago, as indications are that he was already getting bored of the Venezuela issue because of the lack of progress.

via ZeroHedge News https://ift.tt/2FKQDjC Tyler Durden

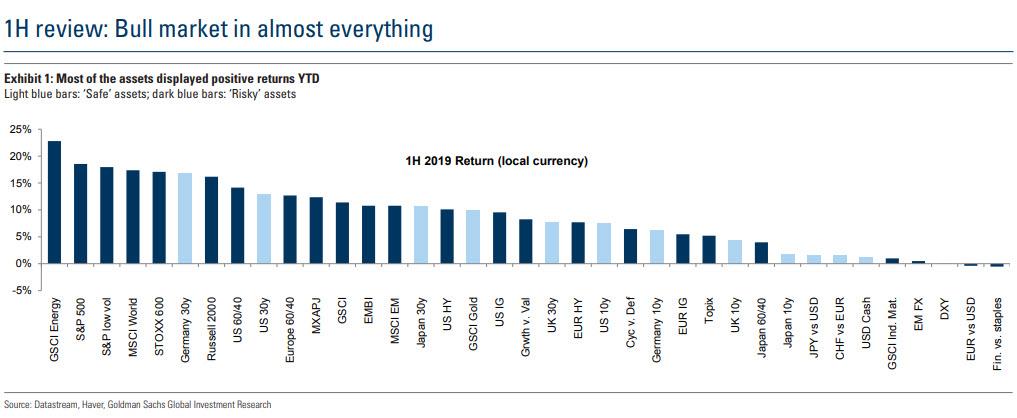

Earlier today, we reported that the S&P 500 posted the best June return (+6.9%) since 1955, with all 38 major assets tracked by Deutsche Bank ending the month with a positive total return. If one looks at monthly data back to the start of 2007, “this has only ever happened once before” according to Deutsche Bank’s Craig Nicol. Amazingly, that was back in January of this year, just after Steven Mnuchin called the Plunge Protection Team. In other words, January and June of this year are the only months in the last 150 which have seen all assets post a positive total return.

Such performance is, for lack of a better word, unprecedented.

In a follow up note, Goldman picks up on this observations with the bank’s Alessio Rizzi writing that much in contrast to last year, most of the assets delivered positive performance YTD.

Having said that, with growth data softening again in May, risky assets have been range-bound since. The equity correction in May has been relatively small and followed by a sharp recovery in June supported by more dovish central banks and fading trade tensions concerns.

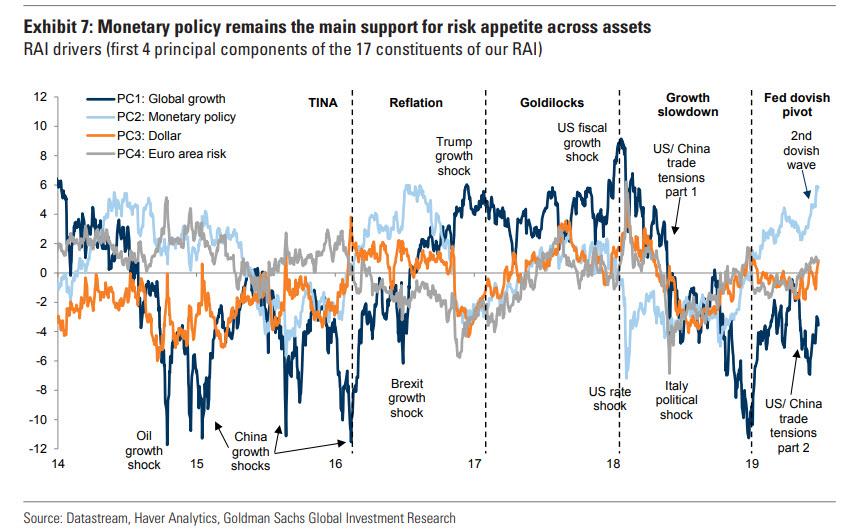

So what has been behind this unprecedented move higher in risky, safe haven and all other assets?

Take a wild guess…. and you’re probably right.

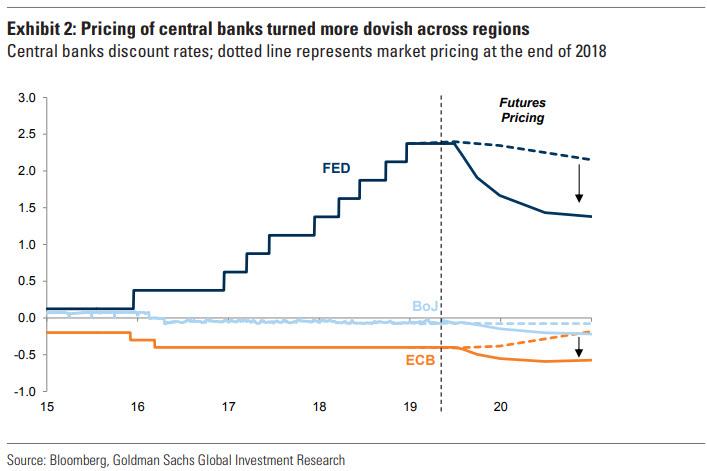

As Goldman answer, since June, there has been a second dovish wave with increased expectations for more ECB easing post Draghi’s Sintra speech and the June FOMC meeting. As a result, Goldman’s proprietary indicators shows that “monetary policy” remains the main driver of risk appetite and expectations are now very bullish.

The same was true in 1H 2016 but after the Brexit shock on June 23, ‘global growth’ expectations picked up, further boosted by Trump being elected in 3Q, which drove a more traditional ‘risk on’ pattern with equities rallying and bonds selling off.

And here it is again, for the cheap seats: “while global growth has softened YTD, the boost from easier monetary policy has driven more appetite both for risky and ‘safe’ assets. Market expectations have turned much more dovish since the end of 2018.”

Some more color:

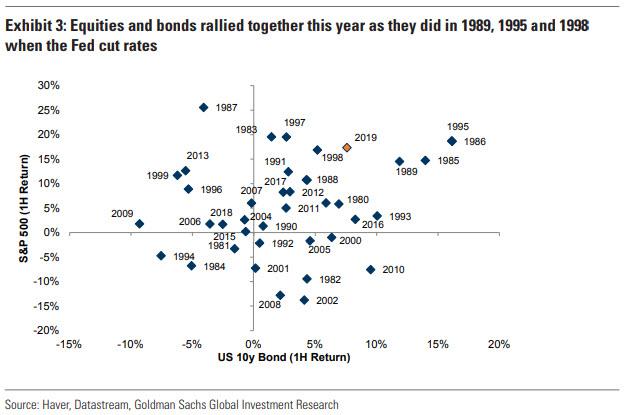

… the market is now pricing c.3 cuts and similarly investors have priced further ECB easing. As a result, both equities and bonds rallied and had one their best starts of the year since the 80s. This is not unusual after dovish monetary policy shifts, e.g. when the Fed starts cutting interest rates; in fact 1989, 1995 and 1998 were strong years for equity and bonds.

So with the Fed, and only the Fed, the driver of most if not all market upside in 2019 (as a reminder, in June PE multiple expansion – i.e., rate expectations – and not earnings were responsible for 90% of the upside), here are some of the consequences:

Due to the weak growth, the leadership within risky assets has been defensive – low vol stocks, defensive sectors and growth stocks outperformed. US low vol stocks had their best start in the last 30 years and a 6-month return similar that post the GFC trough. Investors have been reluctant in adding exposure to riskier assets and fund flows into equity have been quite negative, comparable to previous bear markets.

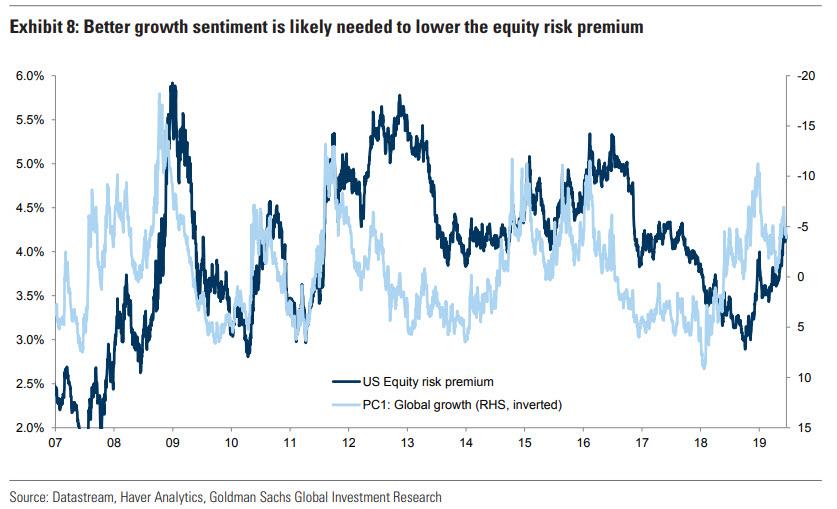

Additionally, the continued lack of positive growth news (and the preponderance of negative news) during the equity rally YTD also helps explain the growing gap between equity and bond yields – the US equity risk premium has increased alongside the de-rating of ‘global growth’ expectations as investors remain relatively cautious. The same has been true across regions and in those markets with increased secular stagnation concerns, such as Europe, where the de-rating of equities relative to bonds has been even larger.

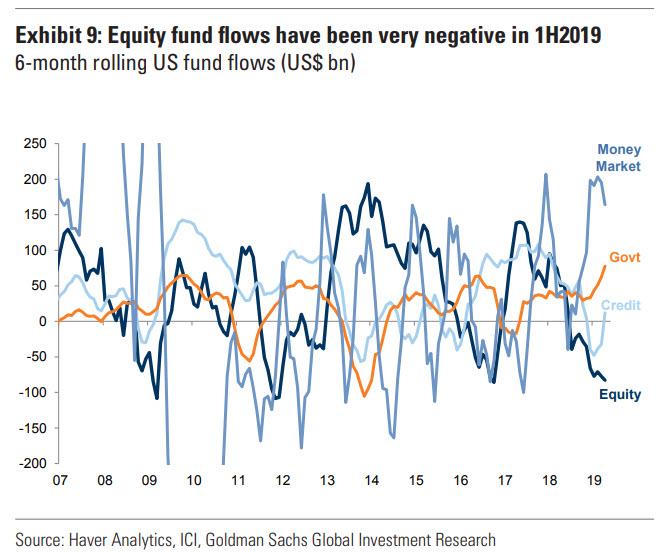

The same investor cautiousness shows in fund flows – in the last 6 months, US equity fund flows have been the most negative since the global financial crisis, while there have been large inflows into money market funds and more recently credit and government bond funds due to the more carry-friendly backdrop.

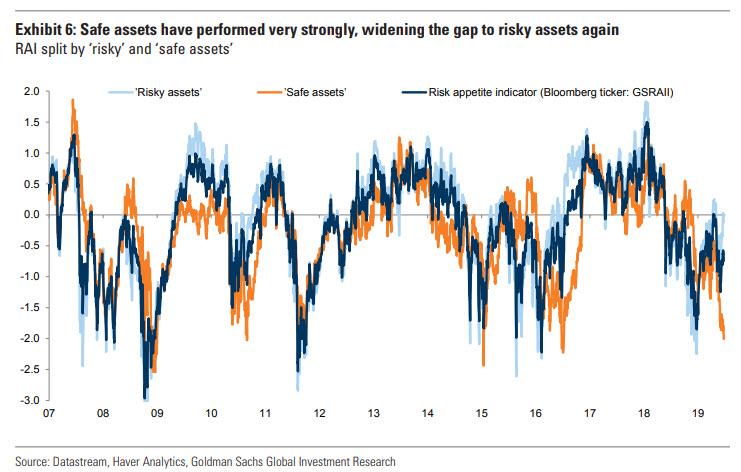

Finally, there is a large gap between risk appetite in ‘risky’ and ‘safe assets’ – Goldman’s aggregate index for ‘risky assets’ is close to neutral again while the continued strong rally of global bonds and safe havens such as Gold and the Yen signal very low risk appetite. The same gap exists between global equities, with the S&P 500 at all-time highs and 10-year bond yields heading to all-time lows. This, according to Goldman, is common in ‘bad news is good news’ regimes, when monetary policy drives a strong search for yield – the same was the case in 1H2016, when easier monetary policy stabilized markets.

So if not growth and not profits, and only the Fed is pushing stocks to new all time highs (on a string), how much longer can this farce of a market continue to levitate? The truth? Nobody knows of course, but as even Goldman now admits, “eventually growth has to take over as the main a driver to drive a procyclical rotation across and within assets.”

via ZeroHedge News https://ift.tt/2RT7AwT Tyler Durden

{kind=link}

{kind=link}