We’ve an exciting week’s play in prospect here in the Global Financial Markets. Highlight will be Friday’s G20 meeting and the expected/hoped for Trump Xi trade rapprochement. What if it doesn’t happen? There are a thousand and one reasons it might well still be cancelled, and just as many market participants suspect a meeting won’t result in anything tangible, meaning the trade war deepens, global recession fears escalate, another $300bln of tariffs are slapped on, and goodnight record stock prices. Oh dear… never mind.

If there is one place to watch this week – focus on events in Hong Kong. This week’s planned series of HK demonstrations, and the ongoing challenge it presents to Beijing to respond, has the possibility of seriously destabilising the already fractured global picture.

But, first the markets – we’re about to enter the summer doldrums. July and August are always thin, illiquid months with low volumes. We might get a negative market direction develop, but major market crashes tend to bide their time for the autumn..

With Wall Street at record highs, and over $12.5 bln of bonds now trading at negative yields – the financial asset markets look…. well, just plain wrong! Everyone knows it! There can’t be a serious financial investor on the planet that doesn’t get it – that stock and bond prices are only so high because they expect ultra-low interest rates to be boosted by another bout of central bank easing.

The wake-up-smell-the-coffee moment might be some time coming. Investors expect the distortion to continue, so why shouldn’t they continue to coat-tail the central banks? A failed G20 this week nails down “lower-for-longer” central bank support. So what if China and the US have a full scale trade war, rates will remain low so corporates can continue to leverage themselves up to fund stock-buy backs, and drive the market higher..

(Somewhere at the back of my mind, the little voice is screaming… what about the long-term, what about the long-term..

Maybe this time it’s going to be different. We’ve got two massive potential geopolitical dust-ups in prospect:

In the Gulf, Trump is trying to goad the Iranians into throwing the first punch – all the mumble-swerve about new sanctions, and calling back a strike (that was still loading on the carrier’s deck) 10 mins from “bombs gone” almost reads like a Monty Python sketch. Trump’s bellicosity must fascinate psychologists – is he trying to maintain his record as a President who hasn’t committed troops, or is it the posturing of a bully or a coward? Who cares, an Iran stand-off could become a sizable, but not unsolvable, market headache.

Then there is Hong Kong. The demonstrations are quite extraordinary. This week’s planned series of demonstrations ahead of G20 will put enormous pressure on Xi and the party to act. If China goes in strong-armed, then the West will have to respond. Whatever Beijing says or does will trigger an Occidental reaction – a badly worded Trump tweet could undo the prospects for the meeting on Friday.

The Beijing authorities know the miscalculated attempt to enforce extradition on Hong Kong has backfired badly. It has become a PR nightmare, but also puts pressure on Xi domestically – he may be President for life, but there are plenty who would replace him….

There are profound regional implications. Although many of China’s SE Asian Governments will be looking at the protests in horror – mass protests scare them (which is why Singapore is so quiet), and others seek to appease China (like the Philippines) – the demonstrations could highlight nationalist zeal in the face of China’s attempts to grab the South China Seas. The potential for conflict is rising.

Hong Kong, whatever Beijing thinks, will not be a quick fix. 30 years after Tiananmen Square, The Party believes the Confucian “the state is always right” accommodation it has reached with the population – support the party and it gives you prosperity and national pride – is unassailable. But HongKongers aren’t like that. A little freedom is dangerous thing – an infectious bug to be stamped out. It is a pernicious little thing. Difficult to eradicate when the HongKongers are spread across the globe. Pretty horrifying to read some of the some of the stories of Social Media abuse: https://www.bbc.co.uk/news/world-us-canada-48721969

Meanwhile, we also have the difficult issue of the EU leadership to resolve later this week. The 28 European leaders failed to agree on how to carve up the senior leadership roles last week, so they try again later this week before the new European Parliament meets to rubber stamp whatever they agree. Democracy in action is a wonderful thing..

via ZeroHedge News http://bit.ly/2xcCFlG Tyler Durden

In a stunningly frank moment during a Sunday Meet the Press interview focused on President Trump’s decision-making on Iran, especially last week’s “brink of war” moment which saw Trump draw down readied military forces in what he said was a “common sense” move, the commander in chief threw his own national security advisor under the bus in spectacular fashion.

Though it’s not Trump’s first tongue-in-cheek denigration of Bolton’s notorious hawkishness, it’s certainly the most brutal and blunt take down yet, and frankly just plain enjoyable to watch. When host Chuck Todd asked the president if he was “being pushed into military action against Iran” by his advisers in what was clearly a question focused on Bolton first and foremost, Trump responded:

“John Bolton is absolutely a hawk. If it was up to him he’d take on the whole world at one time, okay?”

WATCH: President Trump tells Chuck Todd that he has doves and hawks in his cabinet. #MTP#IfItsSunday

Trump: “I have some hawks. John Bolton is absolutely a hawk. If it was up to him he’d take on the whole world at one time.“ pic.twitter.com/JKVB2IvMVU

Trump began by explaining, “I have two groups of people. I have doves and I have hawks,” before leading into this sure to be classic line that is one for the history books:“If it was up to him he’d take on the whole world at one time, okay?”

During this section of comments focused on US policy in the Middle East, the president reiterated his preference that he hear from “both sides” on an issue, but that he was ultimately the one making the decisions.

When pressed on the dangers of having such an uber-hawk neo-conservative who remains an unapologetic cheerleader of the 2003 Iraq War, and who laid the ground work for it as a member of Bush’s National Security Council, Trump followed with, “That doesn’t matter because I want both sides.”

Image source: Reuters

And in another clear indicator that Trump wants to stay true to his non-interventionist instincts voiced on the 2016 campaign trail, he explained to Todd that:

I was against going into Iraq… I was against going into the Middle East. Chuck we’ve spent 7 trillion dollars in the Middle East right now.

It was the second time this weekend that Trump was forced to defend his choice of Bolton as the nation’s most influential foreign policy thinker and adviser. When peppered with questions at the White House Saturday following Thursday night’s dramatic “almost war” with Iran, Trump said that he “disagrees” with Bolton “very much” but that ultimately he’s “doing a very good job”.

Bolton has never kept his career-long goal of seeing regime change in Tehran a secret – repeating his position publicly every chance he got, especially in the years prior to tenure at the Trump White House.

Tucker’s epic “bureaucratic tapeworm” comment:

But Bolton hasn’t had a good past week: not only had Trump on Thursday night shut the door on Bolton’s dream of overseeing a major US military strike on Iran, but he’s been pummeled in the media.

Even a Fox prime time show (who else but Tucker of course) colorfully described him as a “bureaucratic tapeworm” which periodically reemerges to cause pain and suffering.

via ZeroHedge News http://bit.ly/2L9rp1A Tyler Durden

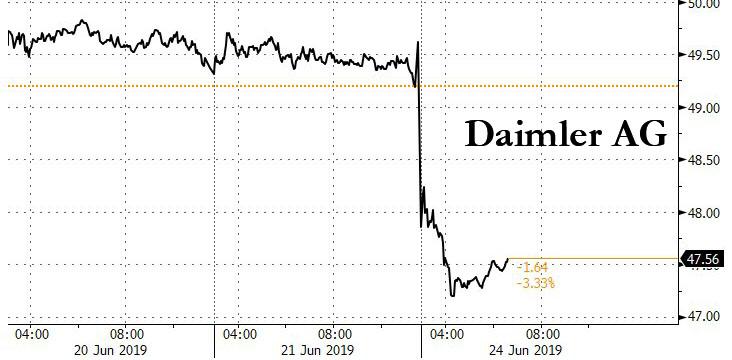

Daimler is haunted by old issues at the same time the global automotive industry appears to be in full collapse, and the company’s new executive team is still “unearthing skeletons from the diesel scandal era”, according to Bloomberg. The company said late Sunday that operating profit will not grow this year – marking the company’s third downgrade over the course of a year after promising a slight earnings gain for 2019.

The company blamed the ongoing allegations of emissions tampering in diesel cars for the cut. Daimler stock fell almost 5% overnight, erasing its gain since the beginning of the year. The company’s stock plunge helped contribute to a broader 0.5% drop in the DAX and 1.2% sell offs in VW and BMW in the overnight session.

And this puts new pressure on new executive duo Chief Executive Officer Ola Kallenius and Chief Financial Officer Harald Wilhelm to follow through on their plans to rope in costs and restore profitability.

Arndt Ellinghorst, an analyst in London at Evercore said: “It all comes back to the same old fact: Daimler needs to execute better. The endless array of so called “one-time” effects raises questions regarding process, management information systems and ultimately accountability of management.”

Former CEO Dieter Zetsche left his position after two profit warnings and a plunging stock price in his last year as CEO. Daimler ended his last year down by more than 33%, far outpacing stock falls by competitors BMW and Volkswagen.

The German car industry continues to face major issues, including a global automotive recession and the trade war between US and China. And even though the diesel crisis first reared its head in 2015, it has now engulfed the entire industry. For instance, regulators recently issued a mandatory recall for about 40,000 Mercedes GLK SUVs for potentially illegal software to skirt emissions rules.

In Germany, authorities had already slapped Daimler with a recall of 774,000 diesel cars in Europe last June over the use of prohibited devices that regulated their emissions. Dorothee Cresswell, an analyst at Barclays Equity Research said: “Clearly both the near term operational challenges and possible questions around Daimler’s corporate culture are issues that must be addressed with urgency by Daimler’s new CEO.”

The auto manufacturer is facing investigations in Europe and the US over alleged excessive pollution from its diesel vehicles. Daimler has already agreed to software upgrades for millions of cars, and has so far been able to elude fines. This is in contrast to VW, who has shelled out more than $34 billion in fines and provisions as a result of the scandal.

Daimler also said on Sunday that its van unit will be unprofitable this year, with a return of sales of -2% to -4%. This division’s unexpected fall came as plans to produce a Mercedes-Benz pick up truck in South America fell through.

For the company’s new executives, the latest revision offers a “kitchen sink” chance to clean house and have a more comprehensive restructuring. Last month, shareholders approved a new corporate structure that will give Daimler’s divisions for cars, trucks and mobility services more independence. Some investors may even want the company to create a separate listing for its trucks division, a move that would be similar to one made by VW.

The question still remains as to whether or not Daimler and its new executives have hit “rock bottom” in terms of financial expectations yet. Marc-Rene Tonn, an analyst at Warburg Research said: “We fear that Sunday’s profit warning may not be the last for the current year.”

via ZeroHedge News http://bit.ly/2N6wCKg Tyler Durden

Italian yields tumbled on Monday, with the 10-year yield falling as much as 5 basis points to 2.1% – its lowest level since May 2018 – after Brussels signaled that it would be willing to wait before launching a disciplinary process against Italy over the country’s rising debt plans, potentially allowing the two sides to seek a compromise.

Instead of triggering the Excessive Debt Procedure when the European Commission meets on Tuesday, the panel is going to give the Italian government another chance to revise its spending plans.

According to the FT, the truce will buy time for Rome’s populist government to reach a deal and avoid budget sanctions and fines that could stretch into the billions of euros. Even though the squabbling over Italy’s debt has returned after purportedly being settled late last year, debt investors are cheering the news because it signals that some members of the populist government might still be open to compromise.

For one, Prime Minister Giuseppe Conte, considered more of a technocrat than Deputy PMs and coalition leaders Matteo Salvini and Luigi Di Maio, is hoping to do enough to avoid an infringement procedure, the FT reports, citing figures from within the Italian government. Conte and Finance Minister Giovanni Tria are trying to find budget savings that might convince Brussels to dispense with moving ahead with the sanctions process.

Rome wants to use a €5.2 billion ($6 billion) net improvement in its 2019 spending plan to mitigate its financial position. “It is not Mr Conte’s intention to sign an infringement procedure and we want to move within the rules. However, we also expect to be offered some room for interpretation [of those rules],” one person with knowledge of the prime minister’s thinking said. “We are confident the procedure won’t kick off.

The Italian finance ministry will send a letter responding to the commission’s assessment this week, and the commission has until early July to inform the various EU finance ministers whether it wants to proceed with the EDP. Officials say Wednesday, the due date for Rome to submit a spending review to the Italian parliament, is also a key moment.

Given that Italy is the third largest eurozone economy and, after Greece, has the highest debt-to-GDP, the outcome of these negotiations could have serious repercussions across the bloc. From a financial stability standpoint, the worst-case scenario is that the EU moves ahead with its plans to fine Italy, forcing Italy to the brink of a banking crisis, followed by a hasty exit from the euro, possibly to be replaced by the BoT.

via ZeroHedge News http://bit.ly/2IEJ3J1 Tyler Durden

S&P futures levitated on Monday, rising to a high of 2,962 and just shy of a new record, alongside buoyant Asian stocks while European shares slumped as the Stoxx 600 Index reversed an earlier gain following the third profit warning from Daimler, and a slump in German business confidence; the dollar dropped to three-month lows as hopes waned for progress in China-U.S. trade talks at this week’s G20 meeting, while Trump was expected to announce even harsher sanctions against Iran today.

The European Stoxx 600 index fell 0.2%, reflecting losses in Paris and Milan. Stocks in London were little changed. Germany’s export-sensitive DAX fell 0.5% after a profit warning by Daimler caused its shares to drop nearly 5%.

Europe’s woes were compounded by the latest slump in German business confidence as trade tensions weighed on manufacturers. The June Ifo Business Confidence dropped to 97.4, its lowest level since late 2014, while an index of expectations also worsened, even though the news was largely priced in and the euro barely moved on the news and was up 0.2% at $1.1392 in early trading.

“It could get worse, maybe not much worse but a little,” said Ifo President Clemens Fuest in a Bloomberg Television interview. “It’s justified to at least postpone any tightening of monetary policy. But I don’t think further easing will help very much. Mario Draghi has rightly pointed out that governments need to use other instruments.”

Earlier in the session, gains in Asia saw the MSCI regional and global stocks gauges rise again towards last week’s six-week highs. Asian stocks advanced, led by health care and consumer discretionary firms, as investors awaited possible new sanctions against Iran and gauged the probability of a U.S.-China trade deal later this week. Markets were mixed in the region, with Australia climbing and Singapore retreating. Japan’s Topix reversed earlier losses to close 0.1% higher, with Sony and Daiichi Sankyo among the biggest boosts. The Shanghai Composite Index advanced 0.2% as U.S. and China trade teams prepared for a meeting between Donald Trump and Xi Jinping on the sidelines of the G-20 summit in Japan. The S&P BSE Sensex Index edged 0.2% lower, driven by Reliance Industries and Infosys, as India’s central bank deputy chief Viral Acharya asked to resign from his post

Investors are waiting to see if Presidents Donald Trump and Xi Jinping can de-escalate a trade war that is damaging the global economy and souring business confidence. The leaders will meet during a G20 summit in Japan which starts on Friday. Wall Street also looked in line for more gains after closing lower on Friday. S&P 500 e-minis pointed to a 0.2% rise at the open.

China Vice Commerce Minister Wang Shouwen said China and US trade teams are having discussions, while he added that both sides should make compromises and hopes G20 sends a clear signal on fighting against trade protectionism. At the same time, China Assistant Foreign Minister Zhang Jun said the world economy faces increasing risks and the international community recognizes harm from protectionism, while he added that G20 should ensure unity and cooperation but also stated that China will safeguard its fundamental interests and will not allow anyone to interfere with its internal affairs no matter what forum.

“G20 is turning into a high-stakes poker game for risk, and if the sideline talks between Trump and Xi fail and trigger an escalation in tariffs, the odds of a full-blown global recession increase exponentially,” said Stephen Innes, managing partner at Vanguard Markets.

On Monday, Chinese Vice Commerce Minister Wang Shouwen said China and the United States should be willing to compromise in trade talks and not insist only on what each side wants. U.S. Vice President Mike Pence’s decision on Friday to call off a planned China speech was also considered a positive sign. Pence had upset China with a fierce speech in October that laid out a litany of complaints ranging from state surveillance to human-rights abuses.

Still, virtually all analysts doubt the two sides will come to any meaningful agreement. Tensions are reaching beyond tariffs, particularly after Washington blacklisted Huawei, the world’s biggest telecoms gear maker, effectively banning U.S. companies from doing business with it.

“Any high hopes ahead of the G20 meeting may be disappointed,” said Benjamin Schroeder, senior rates strategist at ING in Amsterdam. “In the end, uncertainty will persist and central banks could still be pushed closer to invoking their contingency plans.” (For Goldman’s preview of what to expect at the G-20, see this article).

Overnight, a Chinese newspaper said FedEx Corp was likely to be added to Beijing’s “unreliable entities list” following yet another delivery fiasco involving a Huawei shipment.

In FX, the dollar index slipped 0.1% lower to 96.11 after its biggest weekly drop in four months last week, when the Federal Reserve said that it may cut interest rates soon to bolster the U.S. economy. The dollar has led a broad selloff in major currencies as global central banks signaled a dovish outlook on monetary policy amid growing signs of a weak global economy. The dollar fetched 107.39 yen, having slipped as low as 107.045 on Friday, the lowest level since its flash crash on Jan. 3.

“The market is not expecting more Fed rate cuts than it had so far, but that the reasoning behind them is being interpreted in a different manner,” Commerzbank’s head of FX and commodity research, Ulrich Leuchtmann, wrote in a note to clients. “While for a long time the expected weakening of growth, fears of a recession and low inflation were used as reasons for rate cuts, another reason has now been added to the list: the Fed caving in to the White House.”

The euro rose to a three-month high of $1.1387 against the dollar, while the Aussie gained for a fifth day as central bank Governor Philip Lowe said there are limits to what further monetary easing can achieve. In developing markets, the Turkish lira strengthened as much as 2% after Turkey’s main opposition party won Istanbul’s re-run election for mayor, a blow to President Tayyip Erdogan.

In rates, European government bonds climbed alongside U.S. Treasuries, where 10- year yields fell 2bps to 2.03%, its first decline in two days.

In cryptos, the resurgent Bitcoin pulled back from 18-month highs after jumping more than 10% over the weekend. Analysts said the gains came amid growing optimism over the adoption of cryptocurrencies after Facebook announced its Libra digital coin.

Meanwhile, gold resumed its rise amid economic woes, looming U.S. interest rate cuts and tensions between Tehran and Washington: the precious metal stood at $1,404.79 per ounce, not far from Friday’s six-year high of $1,410.78. The rising tensions between Iran and the United States, after Iran shot down an American drone, also pushed oil prices higher. U.S. Secretary of State Mike Pompeo said “significant” sanctions on Tehran would be announced.

Brent crude futures rose 0.4% to $65.42 per barrel, near Friday’s three-week high of $65.76. U.S. crude futures were up 0.9% at $57.91, standing at its highest in over three weeks

Over the weekend, President Trump said that they are moving ahead with additional sanctions on Iran aimed at preventing it from getting a nuclear weapon and that military action is still on the table, while other reports also noted the White House is pressing for additional options including in cyberspace and other additional clandestine plans to counter Iranian aggression in the Persian Gulf. Subsequently, Iranian Navy Commander says the downing of the US Spy drone was a “firm response” and can be repeated, according to Tasmin News. Russian Deputy Foreign Minister says Russia and allies will counteract US sanctions on Iran. Additionally, Russia’s Deputy Foreign Minister stated that the US is deliberately increasing tensions with Iran.

Today’s expected data include Chicago Fed National Activity Index and Dallas Fed Manufacturing Outlook. No major company is scheduled to report earnings

Market Snapshot

S&P 500 futures up 0.2% to 2,957.25

STOXX Europe 600 down 0.2% to 384.00

MXAP up 0.3% to 159.71

MXAPJ up 0.2% to 525.93

Nikkei up 0.1% to 21,285.99

Topix up 0.1% to 1,547.74

Hang Seng Index up 0.1% to 28,513.00

Shanghai Composite up 0.2% to 3,008.15

Sensex down 0.2% to 39,127.17

Australia S&P/ASX 200 up 0.2% to 6,665.44

Kospi up 0.03% to 2,126.33

German 10Y yield fell 1.0 bps to -0.295%

Euro up 0.2% to $1.1392

Italian 10Y yield rose 0.4 bps to 1.786%

Spanish 10Y yield fell 2.2 bps to 0.416%

Brent futures up 0.5% to $65.52/bbl

Gold spot up 0.3% to $1,404.21

U.S. Dollar Index down 0.2% to 96.07

Top Overnight News from Bloomberg

In the first signs of negotiations since talks broke down in May, U.S. and Chinese trade teams are discussing next steps after Presidents Donald Trump and Xi Jinping agreed to meet on the sidelines of the upcoming Group of 20 summit in Japan, a senior trade official said in Beijing

Turkish opposition candidate Ekrem Imamoglu won the redo of the Istanbul mayor’s race by a landslide on Sunday, in a stinging indictment of President Recep Tayyip Erdogan’s economic policies and his refusal to accept an earlier defeat

Turkish President Recep Tayyip Erdogan, weakened by an opposition party’s landslide victory in Istanbul’s repeat election, scrambled to reassert his standing as the country’s most dominant politician in half a century by refocusing attention on a crucial trip to Asia

Australian central bank chief Philip Lowe threw his support behind those casting doubt on how effective a new round of monetary policy easing by major economies would be in supporting global growth

President Trump is threatening Iran with additional sanctions as soon as Monday, but there’s not much left for the U.S. to target because most of the Islamic Republic’s economy is already crippled under the weight of financial restrictions. Oil gains on the threat of new sanctions against Iran

Viral Acharya, deputy governor of the Reserve Bank of India, resigned six months before his term ends, Business Standard reported, citing him

Boris Johnson faces mounting pressure to submit to public scrutiny, after his rival in the race to be U.K. prime minister tried to turn questions about the front-runner’s character to his advantage

President Trump denied that he’d threatened to demote Federal Reserve Chairman Jerome Powell but said he’d “be able to do that if I wanted”

President Trump sent North Korean leader Kim Jong Un a personal letter, and the U.S. is ready to restart talks with Pyongyang “at a moment’s notice,” Secretary of State Michael Pompeo said

New Zealand plans to introduce a bank deposit protection regime to bring it into line with other developed nations and increase public confidence in its lenders

A slump in German business confidence deepened in June as trade tensions weighed on manufacturers. U.S.-led protectionist threats have clouded the growth outlook in Europe’s largest economy for months, contributing to a manufacturing slump

The Reserve Bank of India will lose one of its most outspoken officials, further raising questions about the independence of the central bank six months after the governor resigned under a cloud. Deputy Governor Viral Acharya has asked to leave the central bank not later than July 23, 2019, citing “unavoidable personal circumstances”

Asian equity markets began the week somewhat choppy with participants tentative ahead of the Trump-Xi meeting at the G20 this week and following the mild pullback last Friday on Wall St where all majors ended slightly lower on the day, but still notched gains of more than 2% for the week. ASX 200 (+0.2%) was initially led lower by underperformance in Consumer Staples and as comments from RBA Governor Lowe appeared to question the impact easing could have on the economy, while a non-committal tone was seen in the Nikkei 225 (+0.1%) amid a mixed currency. Hang Seng (+0.2%) and Shanghai Comp. (+0.1%) were indecisive after the PBoC refrained from open market operations and as global markets await the latest developments in the trade war saga including the Trump-Xi showdown this week, while the US recently added 5 Chinese entities to its blacklist barring them from buying US parts without government approval. Finally, 10yr JGBs were subdued with after recent similar moves in T-notes and as yields bounced back from multi-year lows, while demand was also dampened after stocks in Tokyo pared opening weakness and amid the absence of the BoJ in the market.

Top Asian News

India Poised to Lose Outspoken Central Banker as Acharya Resigns

Pakistan to Get $3b in Deposits, Investments From Qatar

China Is Going Bananas for Bananas as Purchases Surge to Record

Nostrum Oil & Gas Studies Options Including Sale of Company

A choppy day for European equities thus far [Eurostoxx 50 -0.4%] following on from a similar Asia-Pac session as markets await the Trump-Xi showdown later this week. Major bourses are mostly in the red, losses for the DAX (-0.5%) stem from declining auto names after Daimler (-4.7%) issued its third profit warning in 12 months, citing losses caused by the diesel emission scandal; hence, Volkswagen (-1.2%) and BMW (-1.2%) have fallen in sympathy. Sectors are also lower with consumer discretionary names pressured by Daimler’s profit warning. In terms of individual movers, Leonardo (+2.4%) shares spiked higher at the open amid speculation that the Co. is considering bidding for Maxar Technologies’ space robotics business, which sources state could be valued over USD 1bln. Meanwhile, Carrefour (+1.6%) shares are underpinned after it reached an agreement to sell 80% of its Chinese operations with the transaction representing an enterprise value of EUR 1.4bln. Finally, Morphosys (+7.2%) shares are bolstered amid news that a treatments primary endpoint was met.

Top European News

German Business Confidence Takes Another Dive as Economy Wobbles

Italy Wins Temporary Reprieve in Bid to Stop EU Punishment

Hunt Says Johnson Dodges Scrutiny as Race for U.K. PM Heats Up

Santander Pays Allianz $1.1b to Terminate Spanish Venture

In FX, the USD has fallen further following last week’s dovish Fed policy meeting and Friday’s relatively weak PMIs, with the DXY faltering after a fleeting attempt to pare losses and probe above 96.200. The 96.000 handle looks under threat and could be relinquished amidst strength elsewhere, with Gold edging back over Usd 1400/oz and Eur/Usd eyeing 1.1400. Note also, the pressure could build as the week unfolds with at least one currency rebalancing model flagging a strong sell signal for the end of June, Q2 and H1, not to mention the G20 where US President Trump is due to meet his Chinese counterpart Xi for extensive trade talks.

NZD/AUD – Perhaps surprisingly given ongoing global trade and geopolitical uncertainty, the Antipodean Dollars are outperforming major peers, or rather deriving most momentum from their US rival’s demise. The Kiwi is pivoting 0.6600 and Aussie 0.6950 ahead of this week’s RBNZ meeting on Wednesday with rates widely tipped to remain unchanged before another cut in August, while comments from RBA’s Lowe may have dampened some dovish expectations as he questioned the effectiveness of easing to support the economy in the context of moves by other Central Banks aimed at sustaining growth and reaching inflation targets.

CAD/EUR – The next best G10 currencies, as the Loonie consolidates recovery gains through 1.3200 after its post-Canadian retail sales wobble, with some support from firmer crude prices, and the Euro draws encouragement from the latest German Ifo survey that was not as weak as forecast overall. Moreover, the institute maintained its 2019 GDP estimate and played down the prospect of a recession even though the economy is in the doldrums, or heading that way. However, Eur/Usd has tested the 50 DMA (1.1390) after clearing 200 DMA and WMAs, but falling just short barriers at the next big figure where the top end of 2 bn option expiries lie (from 1.1390 coincidentally).

CHF/GBP/JPY – All narrowly mixed vs the Buck as the Franc stalls ahead of 0.9750 and Pound meets resistance above 1.2750 in the form of a 38.2% retracement of the fall from 1.3185 to 1.2506 at 1.2766. Meanwhile, the Yen has retreated a bit further from 107.00 and into a 107.29-48 band with technical support seen a fraction under (107.27 Fib) and decent expiry interest a whisker above (1.3 bn at the 107.50 strike).

EM – The Lira has rebounded further from recent lows and in large part on the back of a resounding result at the 2nd Istanbul election that will not be contested this time. Indeed, President Erdogan congratulated the victor after the landslide saw Imamoglu defeat ex-PM Yildirim by whopping 800k votes. Usd/Try is hovering towards the bottom of a 5.7085-8200, with additional support for the Lira from an improvement in Turkish manufacturing sentiment.

In commodities, WTI and Brent futures have retreated from highs in recent trade as the upside momentum seen in the complex somewhat wanes ahead of this week’s US-Sino meeting. Over the weekend, US President Trump announced the intention of further tariffs on Iran to stem the country’s nuclear developments, although Russia’s Deputy Foreign Minister noted that the US is deliberately raising tensions with Iran and stated that Moscow and allies will counteract US sanctions on Tehran. WTI futures hover around USD 58/bbl (having hit an intraday high of USD 58.20/bbl) whilst its Brent counterpart trades just below the USD 65.50/bbl mark and closer to the bottom of today’s range. Elsewhere, gold prices hover around 6yr highs amid dovish central banks and rising tensions in the Middle East. Meanwhile, copper prices declined back below the USD 2.7/lb level as the red metal side-lines strikes at Chile’s Chuquicamata copper mine and takes the cue from the subdued risk tone heading into the G20 summit. Finally, Chinese Rebar steel traded near eight-year highs as demand picks up while output curbs have been extended in an attempt to reduce air pollution.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 0, prior -0.4

10:30am: Dallas Fed Manf. Activity, est. -2, prior -5.3

DB’s Jim Reid concludes the overnight wrap

Welcome to the last week of June and ever longer nights here in the northern hemisphere. Many months ago I got time off for good behaviour and booked in to play a 2 day golf tournament over this past weekend. It had a cut at the halfway stage to qualify for Sunday’s final round. However our recent weekends have been busier than anticipated and we desperately needed time to buy two sofas for the new house. After high level negotiations we agreed that if I missed the cut we’d go sofa shopping Sunday morning. If there was a greater motivation to play well then this was it. All Saturday all I could think of when I stood over the ball was that if I made a mistake then I’d have to spend hours the next day comparing different levels of cushion comforts and fabrics. Alas that pressure proved too much and Sunday was spent with scatter cushions and not scattering it around the golf course as I did on Saturday. I wonder if Rory and Tiger are under the same pressure to make the cut at the Open.

I hope there are some nice sofas in Osaka next weekend as the main event this week will be the much anticipated G-20 summit on Friday and Saturday with the Trump/Xi meeting on the sidelines of the utmost importance. It’ll also be interesting to see what global leaders make of trade tensions and the recent growth slowdown, and whether the US will sign up to the accord. Back to US/China tensions, today’s multiple times rearranged speech from VP Pence – expected to be critical of China – has again been postponed as progress seems to be being made between the two sides. So there will be hope that positivity can continue to extend after they meet. If it doesn’t the problem is that the tariffs on the last $300bn of Chinese exports into the US will be very close to being ready to be imposed. So a bit binary but the fact that they are meeting means that we’re in a better place that we were this time last week. Staying with global politics, the US/Iran relationship darkened further last week and over the weekend the US national security adviser suggested fresh sanctions could come as early as today. So another one to watch especially as it appeared that Mr Trump pulled back from planned military strikes last week. He did appear a little conciliatory over the weekend and suggested he is ready for talks. WTI crude oil price is trading up +0.66% this morning.

Just on that upcoming meeting between Trump and Xi, China’s Vice Commerce Minster Wang Shouwen said overnight that “Compromise will be on both sides. It will be a two-way street,” while adding that China’s principles for the trade talks remain the same, including “mutual respect, treating each other as equals, win-win outcomes, working together and respecting the rules of the World Trade Organization.” To highlight that talks will not be easy, the Trump administration has put five more Chinese tech entities on a trade blacklist. The accompanying statement from the US Commerce Department said the new entities listed were part of China’s efforts to develop supercomputers. It said they raised national security concerns because the computers were being developed for military uses or in cooperation with the Chinese military. Companies added to the backlist included AMD’s Chinese joint-venture with partner Higon – THATIC, Sugon, Chengdu Haiguang Integrated Circuit and Chengdu Haiguang Microelectronics Technology.

Asian markets have started the week generally on a slightly firmer footing with the Nikkei (+0.19%), Hang Seng (+0.23%) and Kospi (+0.08%) all up while the Shanghai Comp (-0.09%) is down. Elsewhere futures on the S&P 500 are trading +0.32%. Elsewhere, in mayoral re-elections in Istanbul, opposition candidate Ekrem Imamoglu won 54% of the vote, with the ruling AK Party’s candidate, former Prime Minister Binali Yildirim capturing 45% (per Bloomberg). The report further added that Turkish President Erdogan, who had called for re-election post Imamoglu’s previous win, accepted the outcome of the rerun but has hinted the new mayor could run into legal problems. He suggested Imamoglu might be tried for allegedly insulting a provincial governor, and a prison sentence could lead to his ouster. The Turkish lira is trading up +0.79% this morning. Staying in Europe, the FT has reported overnight (citing sources) that the European Commission won’t formally trigger its excessive deficit procedure for Italy during a meeting tomorrow. The report also added that the Italian PM Giuseppe Conte is determined to follow EU budget rules to avoid an infringement procedure. This seems to be trying to buy both sides some time to come to an agreement.

In other news, the US President Trump continued with his attack on the Fed Chair Powell by saying in a NBC’s interview, conducted Friday and broadcast on Sunday, that “I’m not happy with his actions. No, I don’t think he’s done a good job.” He also denied that he’d threatened to demote Federal Reserve Chairman Jerome Powell but said he’d “be able to do that if I wanted.”

Moving on, in terms of key data this week, the highlights in the US this week include Durable Goods (Wednesday), final Q1 GDP revisions (Thursday) and PCE inflation (Friday). We’ll also get plenty of survey data. Fed Chair Powell will speak (Tuesday) and part two of the Fed’s stress tests results will be released (Thursday) after all passed in round one late on Friday. In US politics, on Wednesday twenty contenders for the Democratic presidential nomination are due to debate over two nights. This includes Senator Elizabeth Warren and front runner Joe Biden. In Europe today’s IFO in Germany is going to be important and given that 5yr5yr Euro inflation swaps hit record lows last week prior to Sintra, June’s CPI reports in Europe (Thursday and Friday) will be of note. The full day by day week ahead is published at the end.

After a busy week of macro news, Friday turned out to be relatively calm. For the most part, market moves were minor retracements of the week’s earlier action, with equities giving back a part of their gains, rates rising slightly after their big rally, and credit spreads widening a touch. The most noteworthy data on Friday, the flash PMIs in Germany, France, and the US, was mixed, with European readings doing better than expected but the US’s falling to a post-crisis low. The S&P 500 ended the week +2.20% (-0.13% Friday) and touched a new all-time high closing level on Thursday, while the NASDAQ and DOW made similar moves, up +3.01% and +2.41% (-0.24% and -0.13% Friday) respectively. In Europe, the STOXX index ended +1.57% (-0.36%) and Italian equities outperformed, with the FTSE MIB up +3.77% (+0.13% Friday). High yields credit spreads ended the week -16bps and -35bps tighter in the US and Europe (+1bps and -1bps Friday).

The moves in currencies continued their trends from earlier in the week, with the dollar dropping -1.40% (-0.44% Friday) and the euro gaining +1.43% (+0.66%). Oil also continued to rally, with WTI staging its strongest week since 2016 as US-Iran tensions heated up. That rally was worth +9.81% (+1.78%) for WTI, and a relatively more modest +5.40% (+1.41% Friday) for Brent. Gold advanced +4.28% (+0.77% Friday) to its highest level in five years. Energy-linked stocks performed well, with the S&P energy sector up +5.16% (+0.82% Friday), and the higher prices also sparked a move higher in inflation breakevens. Five year-five year inflation swap rates rose by +17.0bps and +6.3bps (+0.04bps and -0.8bps Friday) in the euro area and US, respectively after the central bank moves of last week. Those moves in inflation expectations added some nuance to the moves in bonds, where rises in breakevens were offset by falling real yields. Ultimately, the 10-year treasury ended -2.3bps lower (+2.9bps Friday) at 2.057% while bund yields were -3.0bps lower (+3.3bps Friday) at -0.285%. Treasuries had dipped below the 2% mark earlier in the week and bunds brushed a new all-time low. US 2s10s steepened +4.5bps (+3bps on Friday) on the week but traded in an 11.5bps range. For us the fact that the Fed went more dovish and the curve steepened was a sign that the market trusts them for now.

via ZeroHedge News http://bit.ly/2LeBzOr Tyler Durden

Beijing is demanding answers from FedEx, after the American package-delivery and logistics service again botched the delivery of a package sent by Huawei, the Chinese telecoms giant at the center of the US-China trade spat.

FedEx said on Sunday that an operational error prevented a Huawei package from being delivered to the US just weeks after the US delivery firm said an error led to several of the firm’s packages being misdirected.

“The package in question was mistakenly returned to the shipper, and we apologize for this operational error,” FedEx told Reuters in an emailed statement.

The package had been bound for the US, but was mistakenly returned to its sender in China (unlike the last misdirected packages, which were re-routed to FedEx facilities in the US, even as the packages were destined for other Asian countries).

In response to that incident, Beijing launched an investigation into FedEx that it stressed was in no way meant to be retaliation for the trade war, and also threatened to create a list of “undesirable entities” and place FedEx on it.

Chinese Foreign Ministry spokesman Geng Shuang said during a regular press briefing in Beijing that, since this wasn’t the first time FedEx made a mistake like this, it should offer a more detailed explanation for what happened. Geng was ominously quiet about whether this latest incident might land FedEx on the “undesirable entities” list, though he did accuse the US of “bullying” that hurts Chinese companies and American companies alike. Geng urged the US to stop this behavior and create a more “conducive” atmosphere for cooperation.

via ZeroHedge News http://bit.ly/2KyMaV6 Tyler Durden

Johannesburg’s worst-kept secret looks like any other suburban bar, with a bartender who has nothing unusual to offer. Then someone emerges from the back to present the “other menu.” There, marijuana—or “dagga,” in Afrikaans slang—is listed alongside beer and cider. Customers in business suits hand over a few hundred rand, choose from the selection of strains and edibles, and relax. Shortly thereafter, a “special” rainbow rice crispy treat shows up unceremoniously, wrapped in colorful plastic like a convenience store snack. Clouds of smoke drift over the pool tables. Bob Marley plays from the jukebox. Everything appears safe, casual, and aboveboard.

But the Amsterdam vibes are deceiving. Johannesburg’s funky new drug scene actually exists in a precarious legal gray zone.

Despite reports last year that South Africa’s Constitutional Court had decriminalized marijuana, that ruling only protects adults who “use or cultivate or possess cannabis in private for [their] personal consumption.” Selling weed or consuming it in public remains illegal. And just as in the U.S. and elsewhere, partial decriminalization tends to benefit some groups of people more than others.

“The bottom line is: If you’re growing cannabis out of sight and out of smell, then there is no problem,” says Julian Stobbs, 59, the director of social activism for the marijuana legalization nonprofit Fields of Green for All. “But that excludes anyone who doesn’t have land or privacy. What if you’re in a fourth-floor flat? What if you don’t have a backyard? What if you’re living in a township with six other families?”

Stobbs points out that the new ruling is least likely to benefit black South Africans. Although they make up 79 percent of the population, they directly own just 1.2 percent of rural land and 7 percent of formally registered property in towns and cities. Complying with the law essentially requires being a property owner, and most black South Africans are tenants.

Johannesburg’s libertarian mayor, Herman Mashaba, is a businessman and self-described “capitalist crusader.” As former chairman of the Free Market Foundation, Mashaba might seem a likely candidate to focus on the business potential of full legalization—but there’s a catch. To win leadership of South Africa’s largest city, he had to form a tense coalition between his party, the Democratic Alliance (D.A.), and the Economic Freedom Fighters (EFF), an “anti-capitalist” party that has called for a ban on liquor advertising and announced its desire to make provinces under its jurisdiction “drug-free.” So when Mashaba talks about drugs, he rides the fence.

“The D.A. believes the [2018 Constitutional Court] judgment will go a long way in unclogging the criminal justice system, which is often overburdened with cases of persons found in possession of or consuming cannabis in their personal capacity,” he says. “We are, however, concerned that the public is not adequately educated on the implications of the judgment and that people do not recognize that the possession and/or consumption of cannabis in public remains a criminal offense.”

There’s more bad news: While South Africa’s pro-cannabis Dagga Party raised enough money to participate in the May 2019 national elections, it missed the deadline to transfer funds due to a bank error and will not be on the ballot.

“We failed (so far) as a movement to become active in political discourse within the precincts that determine policy direction and decision-making for South Africa’s future,” wrote leader Jeremy Acton in a statement on the Dagga Party’s website. “Let’s make a promise to ourselves that we are walking together towards a South Africa that WILL give the Cannabis resource to the future of our Children.”

from Latest – Reason.com http://bit.ly/2N6kt88

via IFTTT

Johannesburg’s worst-kept secret looks like any other suburban bar, with a bartender who has nothing unusual to offer. Then someone emerges from the back to present the “other menu.” There, marijuana—or “dagga,” in Afrikaans slang—is listed alongside beer and cider. Customers in business suits hand over a few hundred rand, choose from the selection of strains and edibles, and relax. Shortly thereafter, a “special” rainbow rice crispy treat shows up unceremoniously, wrapped in colorful plastic like a convenience store snack. Clouds of smoke drift over the pool tables. Bob Marley plays from the jukebox. Everything appears safe, casual, and aboveboard.

But the Amsterdam vibes are deceiving. Johannesburg’s funky new drug scene actually exists in a precarious legal gray zone.

Despite reports last year that South Africa’s Constitutional Court had decriminalized marijuana, that ruling only protects adults who “use or cultivate or possess cannabis in private for [their] personal consumption.” Selling weed or consuming it in public remains illegal. And just as in the U.S. and elsewhere, partial decriminalization tends to benefit some groups of people more than others.

“The bottom line is: If you’re growing cannabis out of sight and out of smell, then there is no problem,” says Julian Stobbs, 59, the director of social activism for the marijuana legalization nonprofit Fields of Green for All. “But that excludes anyone who doesn’t have land or privacy. What if you’re in a fourth-floor flat? What if you don’t have a backyard? What if you’re living in a township with six other families?”

Stobbs points out that the new ruling is least likely to benefit black South Africans. Although they make up 79 percent of the population, they directly own just 1.2 percent of rural land and 7 percent of formally registered property in towns and cities. Complying with the law essentially requires being a property owner, and most black South Africans are tenants.

Johannesburg’s libertarian mayor, Herman Mashaba, is a businessman and self-described “capitalist crusader.” As former chairman of the Free Market Foundation, Mashaba might seem a likely candidate to focus on the business potential of full legalization—but there’s a catch. To win leadership of South Africa’s largest city, he had to form a tense coalition between his party, the Democratic Alliance (D.A.), and the Economic Freedom Fighters (EFF), an “anti-capitalist” party that has called for a ban on liquor advertising and announced its desire to make provinces under its jurisdiction “drug-free.” So when Mashaba talks about drugs, he rides the fence.

“The D.A. believes the [2018 Constitutional Court] judgment will go a long way in unclogging the criminal justice system, which is often overburdened with cases of persons found in possession of or consuming cannabis in their personal capacity,” he says. “We are, however, concerned that the public is not adequately educated on the implications of the judgment and that people do not recognize that the possession and/or consumption of cannabis in public remains a criminal offense.”

There’s more bad news: While South Africa’s pro-cannabis Dagga Party raised enough money to participate in the May 2019 national elections, it missed the deadline to transfer funds due to a bank error and will not be on the ballot.

“We failed (so far) as a movement to become active in political discourse within the precincts that determine policy direction and decision-making for South Africa’s future,” wrote leader Jeremy Acton in a statement on the Dagga Party’s website. “Let’s make a promise to ourselves that we are walking together towards a South Africa that WILL give the Cannabis resource to the future of our Children.”

from Latest – Reason.com http://bit.ly/2N6kt88

via IFTTT

In his latest attempt to one-up Elizabeth Warren and establish his brand of “democratic socialism” as something entirely different from the progressive capitalism practiced by some of his peers, Bernie Sanders is preparing to unveil a new plan that would involve cancelling all of the country’s outstanding $1.6 trillion in student debt.

The massive student-debt jubilee would be financed with a tax on Wall Street: Specifically, a 0.5% tax on stock trades, a 0.1% tax on bond trades and a .005% tax on derivatives trades.

Additionally, Sanders’ plan would also provide states with $48 billion to eliminate tuition and fees at public colleges and universities. Thanks to the market effect, private schools would almost certainly be forced to cut prices to draw talented students who could simply attend a state school for free.

Reps Ilhan Omar of Minnesota and Pramila Jayapal of Washington have already signed on to introduce Sanders’ legislation in the House on Monday.

The timing of this latest in a series of bold socialist policy proposals from Sanders – let’s not forget, Bernie is largely responsible for making Medicare for All a mainstream issue in the Democratic Party – comes just ahead of the first Democratic primary debate, where Sanders will face off directly against his No. 1 rival: Vice President Joe Biden, who has marketed his candidacy as a return to the ‘sensible centrism’ of the Democratic Party of yesteryear.

By introducing the student-debt plan, Sanders has outmaneuvered Elizabeth “I have a plan for that” Warren and established himself as the most far-left candidate in the crowded Democratic Primary field. Hopefully, this can help stall Warren’s recent advance in the polls. The plan should help Sanders highlight how Biden’s domestic platform includes little in the way of welfare expansion during the upcoming debate.

via ZeroHedge News http://bit.ly/31PN19h Tyler Durden

Draghi’s shenanigans get hilarious, months before his term ends.

So here’s ECB President Mario Draghi, whose term ends in October, and he’s at the ECB Forum in Portugal, and in a speech on Tuesday titled innocuously, “Twenty Years of the ECB’s monetary policy” – so this wasn’t a press conference after an ECB policy meeting or anything, but a speech on history at an ECB Forum – he suddenly threw out a whole bunch of stuff…

How, “in the absence of improvement” of inflation, “additional stimulus will be required,” in form of “further cuts in policy interest rates” and additional bond purchases, and how “in the coming weeks, the Governing Council will deliberate how our instruments can be adapted commensurate to the severity of the risk to price stability,” and that “all these options were raised and discussed at our last meeting.”

Whoa! Wait a minute, said the good folks who were part of the ECB’s June meeting. These options were not discussed, they told Reuters on Tuesday.

Draghi had ventured out there on his own – apparently trying to push his colleagues into a corner single-handedly as his last hurrah.

His vision laid out on Tuesday was quite a change from the June 6 post-meeting announcement, which didn’t mention anything about even discussing rate cuts. It said that the ECB expects its policy rates to “remain at their present levels at least through the first half of 2020,” before the ECB would begin to raise them, with the bias still on raising rates, not cutting rates. That was less than two weeks ago, and there had not been another ECB policy meeting since then.

Interviewing six “sources” at the ECB with “direct knowledge of the situation,”Reuters found that these policy makers “had not expected such a strong message and that there was no consensus on the path ahead.”

At the June 6 policy meeting, any possibility of a rate cut or renewed asset purchases had been mentioned “only in passing” and without any substantive discussion. The discussion had instead focused on the new package of loans for the banks, the sources said.

The sources told Reuters that ECB policymakers were worried “Draghi was flagging his measures so strongly to markets as a ‘fait accompli’ that there would be no chance for them to disagree with them in at the next policy meeting on July 25,” Reuters reported.

“But they added that, with a global trade war escalating and financial worries around Italy already high, there was little appetite for a fight in July,” Reuters said.

Several sources told Reuters that, because very little new economic information on the Eurozone will come out before the July 25 meeting, “it would be difficult to justify coming to a different policy conclusion than in June.”

And at the June meeting, the conclusion was to delay rate hikes – and there was no mention of rate cuts.

The sources told Reuters that the debate about which policy measures to implement, when, and in what order was still wide open, with policy makers having very different opinions.

For some the first step should be a change in the ECB’s policy message. Others favor a reinforcement of the pledge not to raise rates for a longer time.

Others favor restarting the asset purchase program to bring borrowing costs down for governments so that they could spend more during a downturn, though that would be handicapped by the “issuer limit” that prevents the ECB from holding more than 30% of a country’s sovereign bonds. But the ECB could dispose or circumvent that limit, “some” sources said.

Some policymakers lean toward rate cuts, the sources said. And other policymakers think the ECB should not make any changes at all unless economic data deteriorated substantially and inflation expectations dropped further below the ECB’s target.

But there was no consensus, and there had been no substantive discussions of these topics at the last meeting that had focused on the modalities of the new bank loan package.

What is hilarious is how Draghi was outed as a fabricator and schemer on the very same day he made his additional-stimulus-will-be-required speech, by people who were surprised by his speech, some of whom felt “powerless,” as Reuters put it, and knew he was trying to box them into a corner with his devious move. This has the smell of a palace revolt at the ECB against the head honcho and his last hurrah.

via ZeroHedge News http://bit.ly/2X3C8C3 Tyler Durden

{kind=link}