Minneapolis Mayor Jacob Frey has had enough of with the militarized “warrior cop” who treats every interaction with citizens as though we’re a potential threat. So this month he announced that the city was going to ban police participation in “warrior-style” training that fosters paranoid overreactions and makes it more likely that innocent people will be shot.

In response, the Minneapolis Police Union has declared that Frey’s order is unlawful and is partnering with a national organization to give officers this forbidden training for free.

It’s not hard to understand why Frey would want to put the brakes on the warrior-cop mentality. This past weekend, Connecticut officials released surveillance video of two officers opening fire on an unarmed couple’s car in New Haven as the man exits the automobile with his hands up. And that’s just one recent example. A skim through our police coverage at Reason will net you story after story of officers choosing to shoot or punch or Tase people for the slightest of provocations. Even complying with police orders might not be enough to protect you, as the young man in New Haven discovered.

Fortunately, he wasn’t injured. Others have not been so lucky. In March, North Carolina police shot and killed a man who appeared to be following their orders to put down a gun. In 2017, jurors in Arizona acquitted a Mesa officer who shot and killed a man who was attempting to follow the officer’s orders to crawl down a hallway.

In the Minneapolis area Frey represents, Philando Castile’s fatal shooting at the hands of a St. Anthony police officer became a national news story. Castile was abruptly shot and killed by Officer Jeronimo Yanez at a traffic stop after telling the officer he had a gun (which he had a permit to carry). Yanez was ultimately acquitted of any charges for the shooting.

Yanez had taken 20 hours of training in a program called “The Bulletproof Warror“—the kind of program Frey wants to stop. It encouraged the officer to treat all encounters as potential threats to his safety. By contrast, Yanez received all of two hours of training in de-escalation tactics.

The “warrior cop” mentality has also led to the use of violent, dangerous SWAT raids to execute basic search warrants in situations where they’re not called for, often in the perpetuation of the drug war. This mimicking of “shock and awe” military-style raid tactics have led to innocent people—even children—hurt or killed.

And then, when the justice system attempts to hold officers responsible for these deadly overreactions, the training itself is invoked in court to justify these actions. One psychologist who teaches officers to see every encounter as a potential threat then presents himself as an expert witness on the stand, where he tells juries that it was reasonable for cops to fear for their lives regardless of whatever actions the citizens around them were taking. Yes, even if it turns out they’re unarmed and completely innocent of any criminal behavior.

So Frey should be commended for trying to bring about an end to this sort of training. But the Minneapolis Police Union doesn’t agree. The Minneapolis Star Tribunereports:

Lt. Bob Kroll, president of the police union, was undeterred on Wednesday, saying in an interview that he consulted with the union’s attorneys, who said Frey’s directive was unlawful. Kroll also defended the training, saying, “It’s not about killing, it’s about surviving.”

Frey said in a statement that the city attorney’s office was consulted during the drafting of the policy, and, “They are confident in its legal position.”

Frey says that any officer taking this training in violating of the city’s policy will be disciplined.

On Friday it looked like the two sides had come to an agreement, and Frey said that the union had “come around” and accepted the ban. But the union then put out a statement that said they had not come to such an agreement, and that the mayor and city had in fact agreed that no officer would be punished for going to any sort of off-duty training.

It’s not entirely clear how Minneapolis could stop police officers from taking these courses on their own time, as long as they’re not using any city resources and they’re not getting paid for doing so, but perhaps we’ll see.

from Latest – Reason.com http://bit.ly/2INVL9z

via IFTTT

Investors can play the greater fool theory and ride the rally, but a safer approach is warranted.

It was only a few months ago that the U.S. Federal Reserve was intent on continuing to increase interest rates. But now, some policy makers are even hinting that the next move may be a rate cut, and they may even pursue other forms of policy easing despite equities reaching record highs again. If that is the message Fed Chairman Jerome Powell will provide at his press conference Wednesday following a two-day meeting with policy makers, it would spur equities to even greater heights and drive yields on Treasury securities even lower.

To see why this is a likely scenario, it helps to understand why the move toward further policy easing may occur. Maintaining healthy employment and stable inflation are the twin objectives of Fed policy. Since the 2008 financial crisis, three Fed chairs have attempted without success to reach and sustain a 2 percent inflation goal. They rationalized that near-zero interest rates and three bouts of quantitative easing would take the economy toward that target. But despite the Fed’s balance sheet having more than quintupled from $800 billion in late 2008 to a peak of $4.5 trillion by 2015, inflationary pressures have remained dormant.

The inflation numbers for the first quarter released Friday showed a further easing of inflationary pressures. The core personal consumption deflator that excludes food and energy fell from an already low 1.8 percent in the final quarter of 2018 to 1.3 percent in the first three months of 2019. Inflation this low could quickly turn into deflation, as has been Japan’s experiencesince the early 1990s. Negative inflationary expectations become self-sustaining since they encourage consumers and investors to postpone spending, further deepening a downturn.

Federal Reserve Bank of Chicago President Charles Evans told the Wall Street Journal this month that if the core inflation rate held at around the 1.5 percent area for a few months, he “would definitely be thinking about taking insurance” by cutting rates. Robert Kaplan, head of the Federal Reserve Bank of Dallas, also indicated that if inflation persisted at low levels, he would have to take that into account in setting rates.

Even if Powell suggests at his May 1 press conference that such a move could occur within a few months, that may not be the end of the easing cycle. The Fed is unlikely to succeed in raising the inflation rate now any more than it has been able to do in the past decade. Even if a rate cut is accompanied by an announcement that the Fed would resume bond purchases, that may not pressure inflation higher.

Low inflation in recent years has been the result of an aging U.S. population that tends to consume less, Trump administration policies that have discouraged immigration of young workers who could have contributed to spending, and a labor force participation rate that is still below pre-crisis levels. These issues are structural and do not respond to monetary stimulus measures. Furthermore, if rates are reduced, low- and middle-income workers will find themselves losing out on interest income as they did in the years after the crisis. This too will curb consumption and hold back inflation.

Under these circumstances, the Fed will likely double up on policies that don’t work, sending financial asset prices even higher; failure may only breed further efforts in the same direction. This expectation is borne of experience. When the Fed deemed that the first effort at quantitative easing that was announced in late 2008 was not sufficient to spark faster inflation and put economic growth at an acceptable pace, it introduced second and third versions of bond purchases, providing a backstop to financial assets for several years.

How then would the rally end? A few more rounds of lower rates and putting more cash in the hands of investors may eventually send valuations to unsustainable levels. At some point, perhaps by mid-2020, further Fed easing may only increase the anxiety level in markets regarding what bad news central bankers are aware of that investors are not privy to. That would be the time when even the Fed may not be able to support markets.

Of course, in such a scenario, investors can play the greater fool theory and go with the upward market momentum and ride the rally. A safer approach would be to gradually reduce their presence in risk assets over the coming months.

via ZeroHedge News http://bit.ly/2LaDYLR Tyler Durden

The leader of a New Mexico militia which has been detaining border crossers is expected to appear in an Albuquerque court on Monday to face federal weapons charges, according to Reuters.

Larry Hopkins, leader of the United Constitutional Patriots, was charged with being a felon in possession of a firearm after the FBI claims it found guns during a 2017 visit to his home.

The 69-year-old was arrested by the FBI on April 20, several days after his militia was accused by the ACLU of illegally detaining migrants – prompting New Mexico’s Democratic Governor Michelle Lujan Grisham to call for them to stop.

Hopkins in 2017 allegedly boasted of training volunteers to kill former President Barack Obama, former Secretary of State Hillary Clinton and financier George Soros, an FBI agent said in court papers.

The United Constitutional Patriots has helped the U.S. Border Patrol, which has been overwhelmed by record numbers of Central American families seeking asylum, detain some 5,600 migrants in New Mexico in the last 60 days, the group said. –Reuters

Hopkins’ defense attorney, Kelly O’Connell, says that the charges are unrelated to the militia’s actions at the border, and stem from an October 2017 report that a militia was being run out of Hopkins’ home in Flora Vista, New Mexico, according to FBI Special Agent David Gabriel.

The United Constitutional Patriots (UCP), meanwhile, have been patrolling the border with rifles and camouflage uniforms which beat the group’s eagle insignia. They have posted dozens of videos on YouTube depicting UCP members detaining migrant families, who are then made to sit and wait at gunpoint until Border Patrol agents arrive.

Upon entering Hopkins’ home, agents collected nine firearms ranging from rifles to pistols – which Horton was illegally in possession of due to at least one prior felony conviction, according to the complaint.

A federal grand jury has returned an indictment charging Hopkins with being a felon in possession of firearms, the same charged he faced in the original complaint, the U.S. Attorney’s Office said in a statement on Friday. The indictment allows prosecutors to avoid a preliminary hearing in the case. –Reuters

The UCP leader faces a maximum of 10 years in prison if convicted.

via ZeroHedge News http://bit.ly/2V4ogpZ Tyler Durden

At the peak of its power in 1350 BC, thousands of years ago, ancient Egypt was like nothing ever seen before.

The great Kingdom was thriving under an efficient system of agricultural production and trade with foreign nations.

Egyptians had learned to adapt to the natural irrigation of the Nile river to produce surpluses of food, which supported a larger population, trade specialization and social and cultural development.

Mineral exploitation in the surrounding areas gave Egyptians great resources with which to trade with foreign empires – and led to great wealth for the kingdom.

New technologies were invented at an astonishing pace: there are records of discoveries in medicine, construction, and mathematics dating from Ancient Egypt that we still use today (yes, that’s how they built the Pyramids).

Ancient Egypt also gave us the first peace treaty ever, and new forms of literature.

Nefertiti, the wife of the Pharaoh Akhenaten, led a religious revolution away from a common belief in several gods, to the worship of just one – the Sun god – the first instance of monotheism ever recorded.

And famously, Egypt’s art scene thrived.

Monuments, sculptures, masks, statues, amulets – you name it. Egyptians were great craftsmen, and their art was widely circulated around the world.

Today, most of the world’s major historical art museums carry some form of Egyptian art.

So it should come as no surprise that despite the more than 3,000 years that have passed, antiquities from Ancient Egypt have tremendously grown in value.

This week, a granite statue from ca. 1350 BC will be on auction sale in New York for a starting price of $4.5 million.

And a Scarab amulet will start at $80,000.

I don’t know about you, but I’m interested in anything that holds value with that kind of longevity.

That’s one of the reasons why gold is such a sensible asset to hold: it’s scarce, portable, and has been valuable since ancient times.

Egyptian art is even more scarce. No one can go back in time and create more of it.

So as a means to preserve wealth over the long-term, it makes sense to consider owning some rare, collectible assets as part of a larger strategy… rather than having 100% of your savings in fundamentally flawed paper currencies.

We had some of the world’s foremost experts teaching us. It was 100% educational… there was absolutely nothing to buy and sell.

And we learned about so many different types of assets– rare coins, antique firearms, vintage cars, works of arts, Swiss watches, comic books, etc.

We even arranged for one of the most prominent museums in the country to shut down for our group, where we enjoyed cocktails and a private tour with the curator and a handful of talented artists.

Collectible assets, just like anything else, derive value from supply and demand.

And supply is all about scarcity.

Again, you can’t go back to Ancient Egypt and make another amulet. You can’t ask Leonardo da Vinci to paint another masterpiece. You can’t go back in time to 1952 and print another Mickey Mantle rookie card.

In addition to scarcity, quality is another important factor: collectibles in better condition will typically be stronger stores of value.

For example, a ‘mint condition’ Mickey Mantle rookie baseball card is worth millions of dollars, whereas one with just a bit of wear and tear is worth around $800,000.

Similarly, rare coins in flawless condition will hold value better than the same coin with scratches and scuffs.

Demand with collectible assets tends to be strongest with brands, or historical events, that have the widest following.

Beatles and Elvis memorabilia, for instance, has far greater appeal than, say, Roy Orbison, simply because their worldwide fan bases are so much larger.

There are far more World War II or American Civil War aficionados than there are for the War of 1812. So there is far more demand for World War II and Civil War artifacts.

Historical documents (another category of collectible assets) signed by Abraham Lincoln, George Washington, or Winston Churchill have far greater demand than those from Grover Cleveland or Arthur Balfour.

They’re more expensive, but the extra premium you pay will most likely hold its value (and grow) in the years and decades to come.

Collectibles are also quite interesting because they’re so portable. You could walk across a border with a single rare coin in your pocket that’s worth over $1 million… which also makes collectibles a very private way to store wealth.

Another benefit is estate planning. At some point, each of us is going to pass away. And a collection of coins or artwork is a LOT easier to pass along to your heirs than traditional financial assets (like bank accounts and stocks).

Most of all, collectibles can really be fantastic assets. We discussed this weekend that, for the past several decades, a number of different collectible categories ranging from vintage Ferraris to Andy Warhol paintings have vastly outperformed the stock market over the past few decades.

It’s not to say you should run out and by an $80,000+ Egyptian artifact. It’s important to first find something that appeals to you, and learn as much as you can about it.

And a lot of highly desired collectibles can be had for just a few thousand dollars, so the entry point can be quite low.

But at a time when central banks continue to debase their currencies and western governments are drowning in debt, it makes sense to consider ‘forever assets’ that can hold their value for generations to come.

There is a “crisis” brewing in America which will affect more Americans than the subprime crisis in 2008.

What is it?

It’s the pension and retirement crisis.

According to a recent report from the National Retirement Planning Week the three “legs” of the retirement “stool” are Social Security, private pensions and personal savings. None are in great shape.

The average Social Security check is $14,000 a year, hardly a cushy retirement.

23% of boomers ages 56-61 expect to receive income from a private company pension plan; and,

“Using faulty assumptions is the lynchpin to the inability to meet future obligations. By over-estimating returns, it has artificially inflated future pension values and reduced the required contribution amounts by individuals and governments paying into the pension system.”

This is a critically important point to understand as it is why a vast majority of Americans are trapped in the same “quicksand” as pension funds and don’t realize it.

For years, Wall Street has espoused the “myth of compounded average returns.”This is the same myth which has not only infected pension funds, but has led to the same false sense of future financial security in personal retirement planning nationwide. An article from IBD further perpetuates this myth:

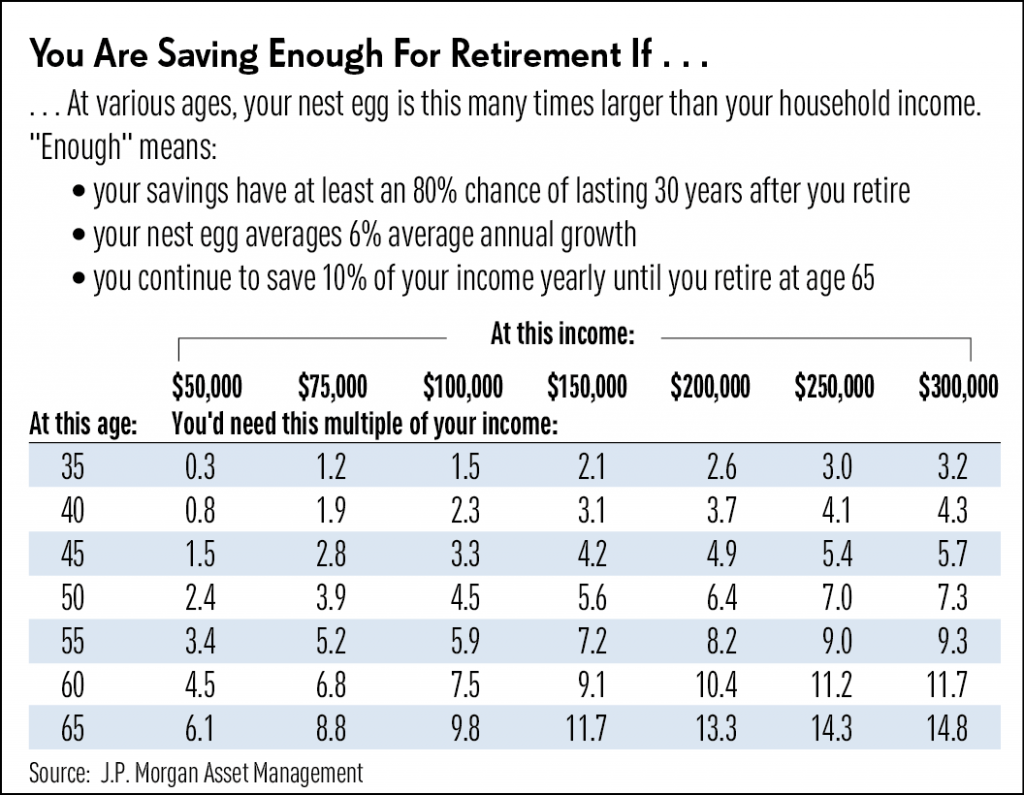

“J.P. Morgan says ‘enough’ means the nest egg is big enough to have at least an 80% chance of surviving 30 years in retirement.’

The financial firm’s number crunchers also assume that, before retirement, you keep kicking in 10% of your income each year to your nest egg. In addition, they assume that your retirement portfolio grows an average of 6% a year before retirement and 5% a year in retirement.“

And there it is. The biggest mistake you are making in your retirement planning by buying into the “myth” that markets “compound returns” over time.

They don’t. They never have. They never will.

The chart below shows a compounded return rate of at 4-8% with $5000 annual dollar cost averaging (DCA) contributions made monthly (as noted above 10% of $50,000 which is roughly the median wage), and using variable rates of return from current valuation levels. (Chart assumes 35 years of age to start saving and expiring at 85)

Just as with “pension funds,” the issue of using above average rates of return into the future suggests one can “save less” today because the “growth” will make up for the difference.

Unfortunately, it just doesn’t work that way.

Financial Insecurity

While we can argue about market returns, compounding rates, etc., in order for any of that to matter we have to assume Americans have money, or savings, to invest to begin with.

A new report by Forbesstates that 23% (nearly one in four) Americans are saving not even one penny from their paychecks.

As part of its 2019 Savings Survey, First National Bank of Omahaexamined Americans’ habits, behaviors, and priorities when it comes to saving, monthly spending, and retirement planning. The findings showed that nearly 80% of Americans live paycheck to paycheck.

The 2018 Planning & Progress Study gathered data in an online survey from over 2000 Americans over the age of 18. In that survey, they found:

78% said they were “extremely” or “somewhat” concerned about affording a comfortable retirement.

“According to a survey from Gallup, 43 percent of adults between the ages of 50 and 64 expect to rely on Social Security during retirement. This number has been steadily increasing since 2001. However, only 24 percent of respondents in the 2018 Planning & Progress Survey believe it’s extremely likely that Social Security will even be available when they plan to retire.”

That fear is likely not so misplaced as Reason noted:

“Social Security will be insolvent and unable to pay the full value of promised benefits by 2035—that’s one full year later than previously expected—and Social Security’s costs will exceed its income by 2020, according to a new report published Monday by the program’s trustees.

At the end of 2018, Social Security was providing income to about 67 million Americans. About 47 million of them were over age 65, and the majority of the rest were disabled. If nothing changes, the Social Security Trust Fund will be fully depleted by 2035 and the program would impose across-the-board cuts of 20 percent to all beneficiaries.”

Meanwhile, demographics are blowing up the basic premise of how Social Security is funded. There were 2.8 workers for every Social Security recipient in 2017. That’s down from 3.3 in 2007, and that’s way down from the 5.1 workers per beneficiary that existed in 1960.

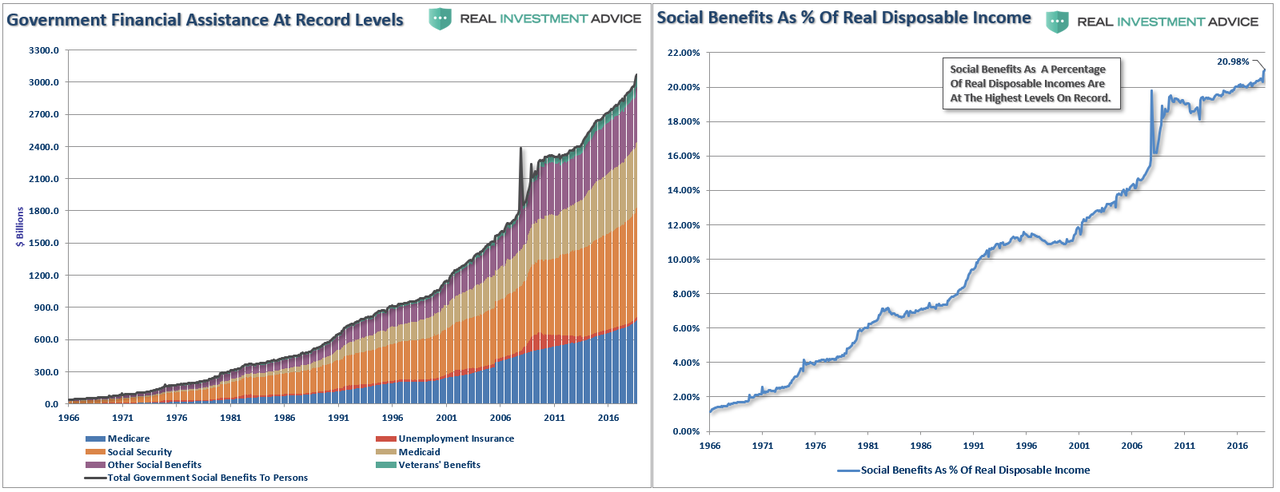

Furthermore, the two programs function mostly as a giant conveyor belt to transfer wealth from the young and relatively poor to the old and relatively rich, allowing the average person (who now lives to be 78) more than a decade of taxpayer-funded retirement. As I have shown previously, welfare now makes up the highest percentage of disposable personal incomes in history despite record low unemployment, rising wage growth, and the longest economic expansion in U.S. history.

Those entitlement programs are also the primary drivers of our national debt, which just hit $22 trillion, and the deficit, despite tax reform is now pushing in excess of $1 Trillion, which has never been seen during an economic expansion.

Won’t Or Can’t

Asking people to save “more” really isn’t an option.

The lack of savings, of course, is directly related to the rising cost of living versus the lack of wage growth over the last 35-years which led to a massive surge in debt to maintain the standard of living.

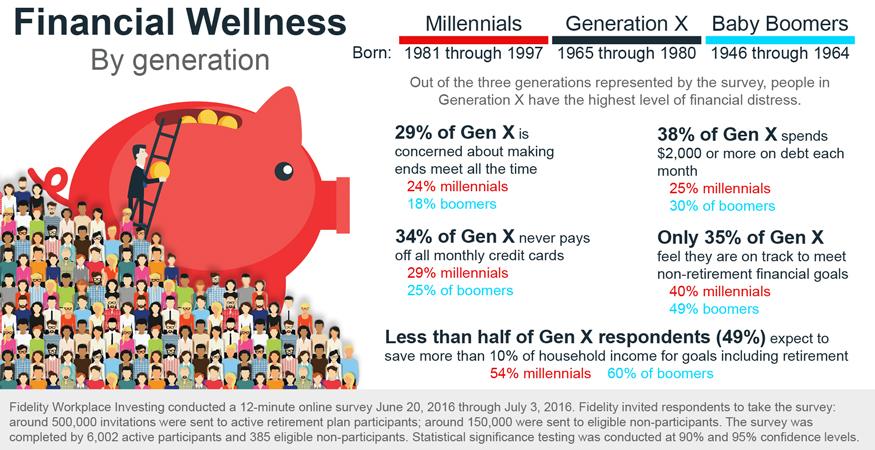

Fidelity provided some further insights into the savings problem which shows it permeates Boomers, Generation X’ers, and Millennials:

“Generation X is squarely in middle age and beset on all sides by bills. Many in Generation X have dependents at home—84% in the survey said they have at least one. They may also still be paying off their own student debts—just more than one in four survey respondents from Generation X says he or she is still paying for his or her own education.

There are all kinds of money problems, but the solutions are generally the same: Save more, spend less, or find a higher-paying job—or maybe all three. But this is easier said than done.”

The massive shortfall in “savings” is going to be a problem in the future.

But everyone saves money in their 401k plan?

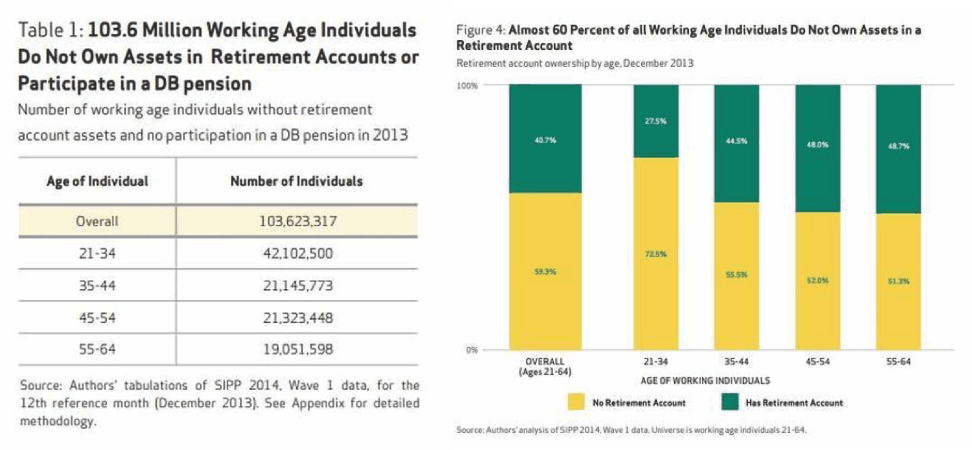

A report from the non-profit National Institute on Retirement Security which found that nearly 60% of all working-age Americans do not own assets in a retirement account.

Here are some additional findings from the report:

Account ownership rates are closely correlated with income and wealth. More than 100 million working-age individuals (57 percent) do not own any retirement account assets, whether in an employer-sponsored 401(k)-type plan or an IRA nor are they covered by defined benefit (DB) pensions.

The typical working-age American has no retirement savings. When all working individuals are included—not just individuals with retirement accounts—the median retirement account balance is $0 among all working individuals. Even among workers who have accumulated savings in retirement accounts, the typical worker had a modest account balance of $40,000.

Three-fourths (77 percent) of Americans fall short of conservative retirement savings targets for their age and income based on working until age 67 even after counting an individual’s entire net worth—a generous measure of retirement savings.

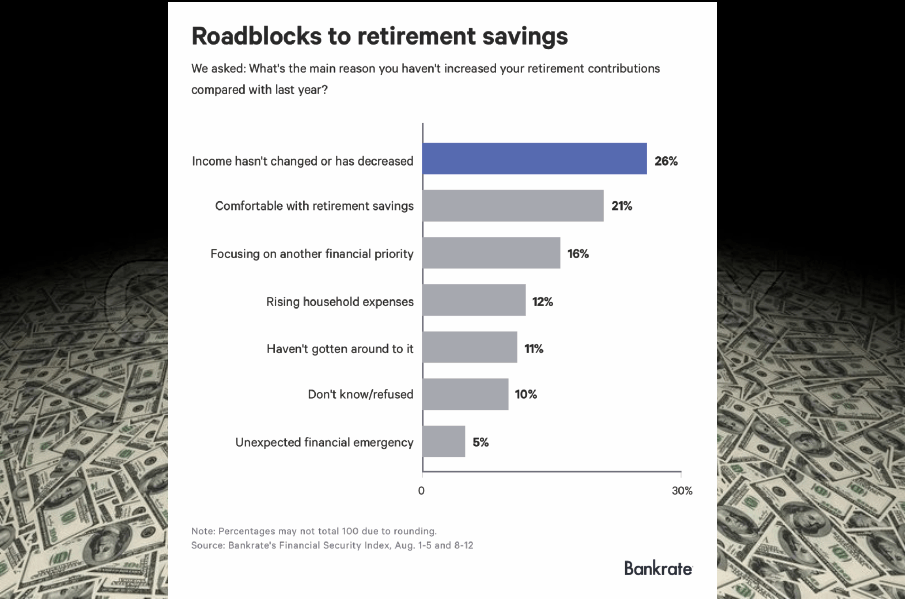

“13 percent of Americans are saving less for retirement than they were last year and offers insight into why much of the population is lagging behind. The most popular response survey participants gave for why they didn’t put more away in the past year was a drop, or no change, in income.”

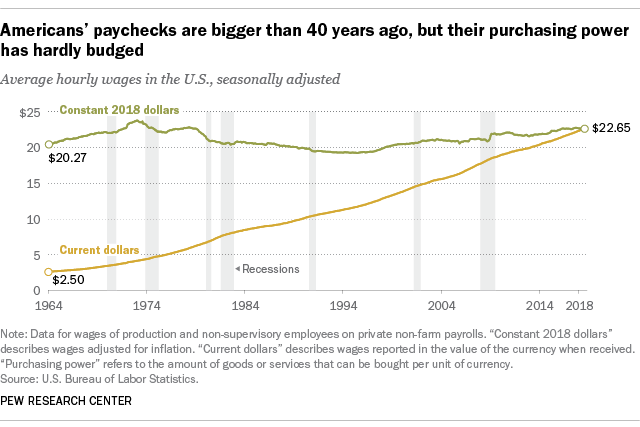

The cost of living has risen much more dramatically than incomes. According to Pew Research:

“In fact, despite some ups and downs over the past several decades, today’s real average wage (that is, the wage after accounting for inflation) has about the same purchasing power it did 40 years ago. And what wage gains there have been have mostly flowed to the highest-paid tier of workers.”

But the problem isn’t just the cost of living due to inflation, but the “real” cost of raising a family in the U.S. has grown incredibly more expensive with surging food, energy, health, and housing costs.

Researchers at Purdue University recently studied data culled from across the globe and found that in the U.S., $132,000 was found to be the optimal income for “feeling” happy for raising a family of four.

Gallup also surveyed to find out what the “average” family required to support a family of four in the U.S. (Forget about being happy, we are talking about “just getting by.”) That number turned out to be $58.000.

The chart below shows the “disposable income” of Americans from the Census Bureau data. (Disposable income is income after taxes.)

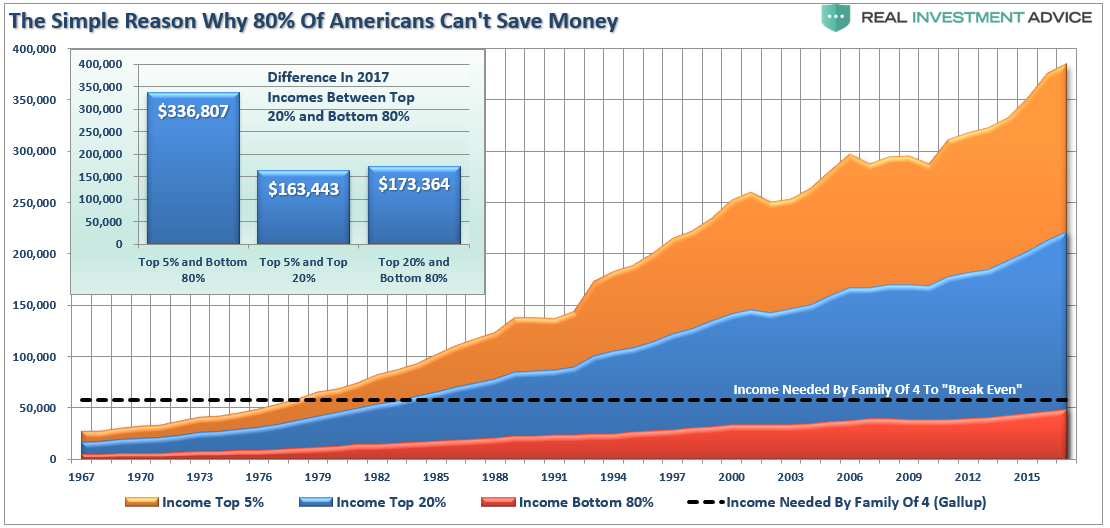

So, while the “median” income has broken out to all-time highs, the reality is that for the vast majority of Americans there has been little improvement. Here are some stats from the survey data which was NOT reported:

$306,139 – the difference between the annual income for the Top 5% versus the Bottom 80%.

$148,504 – the difference between the annual income for the Top 5% and the Top 20%.

$157,635 – the difference between the annual income for the Top 20% and the Bottom 80%.

If you are in the Top 20% of income earners, congratulations. If not, it is a bit of a different story.

Assuming a “family of four” needs an income of $58,000 a year to just “make it,”such becomes problematic for the bottom 80% of the population whose wage growth falls far short of what is required to support the standard of living, much less to obtain “happiness.”

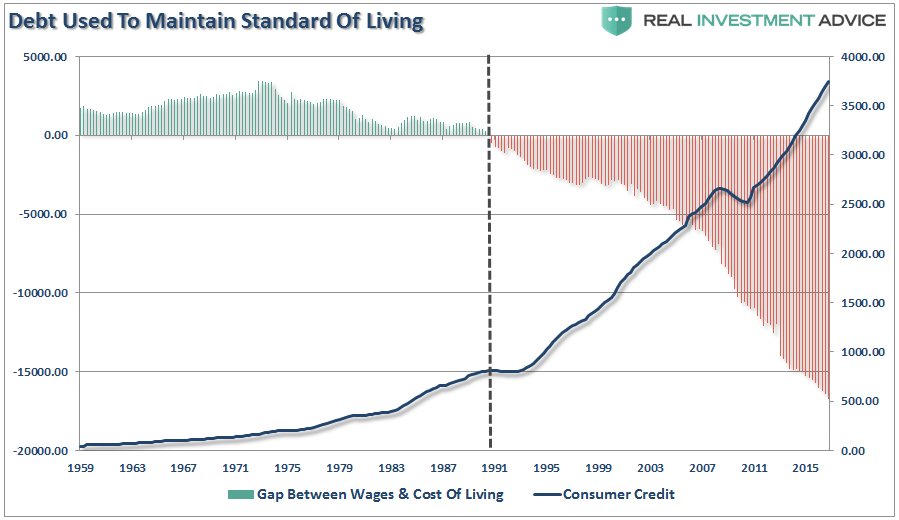

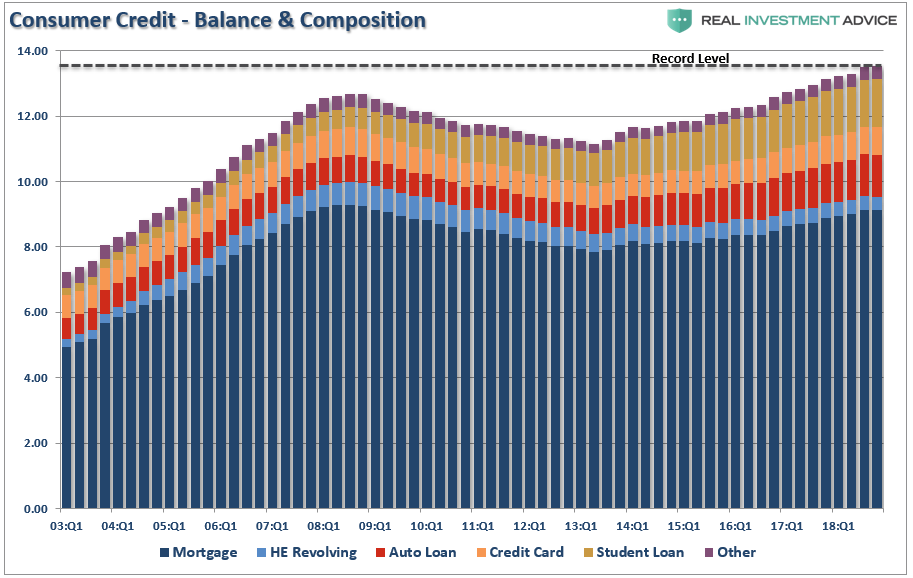

The “gap” between the “standard of living” and real disposable incomes is more clearly shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living so consumers turned to debt to fill the “gap.” However, following the “financial crisis,” even the combined levels of income and debt no longer fill the gap. Currently, there is almost a $3200 annual deficit that cannot be filled.

This is why we continue to see consumer credit hitting all-time records despite an economic boom, rising wage growth, historically low unemployment rates.

The mirage of consumer wealth has not been a function of a broad increase in the net worth of Americans, but rather a division in the country between the Top 20% who have the wealth and the Bottom 80% dependent on increasing debt levels to sustain their current standard of living.

With the vast amount of individuals already vastly under-saved and dependent on social welfare, the next major correction will reveal the full extent of the “retirement crisis” silently lurking in the shadows of this bull market cycle.

For the 75.4 million “boomers,” about 26% of the entire population heading into retirement by 2030, the reality is that only about 20% will be able to actually retire.

The rest will be faced with tough decisions in the years ahead.

The good news is that if Alexandria Ocasio-Cortez is correct, none of this will be a problem if climate change kills everyone in the next 12 years.

via ZeroHedge News http://bit.ly/2GIm1Pq Tyler Durden

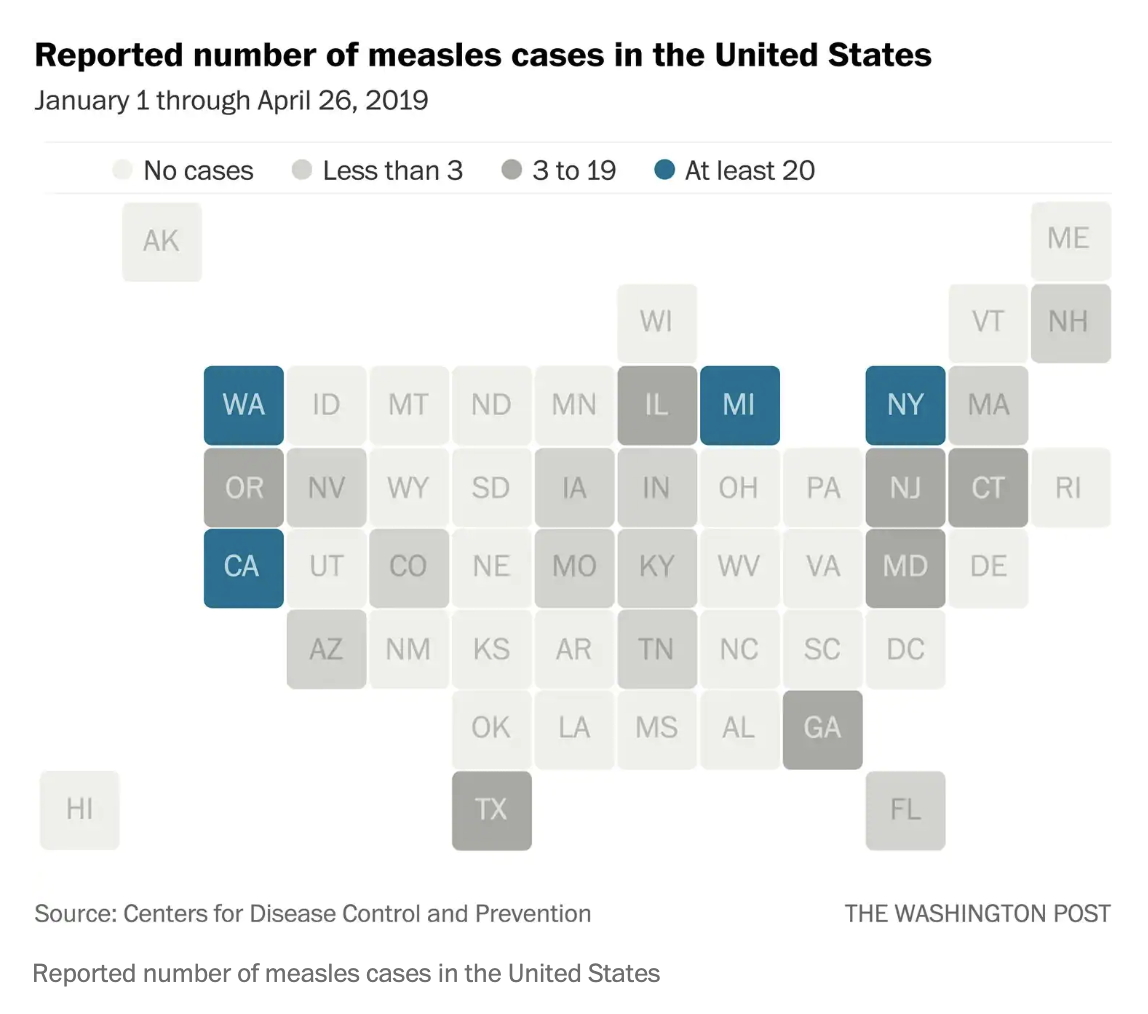

As more than 1,000 students have been quarantined in California and New York State has begun issuing expensive summons to at least 12 unvaccinated people who have dared to defy its mandatory vaccination order, the CDC on Monday confirmed that the number of measles cases documented in the US since the beginning of the year has climbed to 704 cases in 22 states, the largest number of cases documented in a single year since 1994…and it’s only April.

The outbreaks are a huge setback for public health officials in the US, who had declared that measles had been eliminated back in 2000.

The worst outbreaks have been documented in Orthodox Jewish communities in Brooklyn and New York’s Rockland County. Some 88% of cases have been associated with these religious communities. To combat the outbreak, NYC has instituted a policy of mandatory vaccinations, and Rockland County has threatened a $2,000-a-day fine for any unvaccinated individuals who mix with the general public.

In a statement Monday, Health and Human Services Secretary Alex Azar underscored the seriousness of the outbreaks: “We have come a long way in fighting infectious diseases in America, but we risk backsliding and seeing our families, neighbors, and communities needlessly suffer from preventable diseases. We are very concerned about the recent troubling rise in cases of measles. Vaccine-preventable diseases belong in the history books, not in our emergency rooms. The suffering we are seeing today is completely avoidable. Vaccines are safe because they are among the most studied medical products we have.”

Currently, the US leads the developed world in the number of unvaccinated children.

Outside New York, the worst outbreaks have been documented in California, Washington and Michigan.

Here are key facts about measles:

Public health officials blame the measles resurgence on the spread of misinformation about vaccines. A vocal group of parents opposes vaccines, believing that ingredients in them can cause autism. Social networks have resorted to censorship to prevent the spread of any related postings.

The largest outbreaks are concentrated in Orthodox Jewish communities in New York City’s Williamsburg neighborhood, where some 390 cases have been confirmed, and Rockland County north of New York City, which has recorded 201 cases. Those figures include infections from last year and are not directly comparable to the CDC numbers.

Other outbreaks have been reported in Washington state, New Jersey, California’s Butte County and Michigan.

The disease is highly contagious and can be fatal, killing one or two of every 1,000 children who contract it, according to the CDC. It can also cause permanent hearing loss or intellectual disabilities. It poses the greatest risk to unvaccinated young children.

The United States’ 2000 declaration that measles was eradicated meant that the disease was no longer present in the country year round. Measles remains common in some countries in Europe, Asia and Africa, and unvaccinated travelers to those countries can bring it back to the United States. The current outbreaks are believed to trace back to visits to Israel and Ukraine.

New York City officials said some 21,000 people have received the measles-mumps-rubella vaccine in affected areas since the outbreak began in October. The city has begun fining unvaccinated adults.

Lawmakers in Oregon, California and Washington state are considering bills to eliminate nonmedical exemptions that allowed unvaccinated children to attend public schools.

In order to achieve herd immunity that protects those unable to get the measles vaccine, such as infants and people with compromised immune systems, 90% to 95% of the population needs to be vaccinated.

via ZeroHedge News http://bit.ly/2J3Fdd0 Tyler Durden

Beto O’Rourke, the former Texas congressman who’s running for the 2020 Democratic presidential nomination, today released a four-part, $5 trillion plan to fight climate change.

The framework for O’Rourke’s plan, which is posted on his campaign website, promises he will make quick use of his executive authority, though it also pledges the candidate will work with Congress. O’Rourke is not proposing that the federal government fully fund his plan, which sets it apart from Rep. Alexandria Ocasio-Cortez’s (D–N.Y.) much-criticized Green New Deal. Rather, O’Rourke believes a “$1.5 trillion investment” from the federal government will “mobilize” trillions more in additional investments from the private sector to combat climate change.

Part one of the plan would use of executive authority “not only to reverse the problematic decisions made by the current administration, but also to go beyond the climate actions under previous presidents.” O’Rourke says he’ll reverse President Donald Trump’s decision to back out of the Paris climate agreement, and he promises to strengthen emissions standards, reduce various sources of pollution, and require that federal lands plan for net-zero emissions by 2030.

Part two is where Congress comes in. “In the very first bill he sends to Congress,” the plan says, “Beto will launch a 10-year mobilization of $5 trillion directly leveraged by a fully paid-for $1.5 trillion investment—the world’s largest-ever climate change investment in infrastructure, innovation, and in our people and communities.” How are we supposed to pay for that initial investment? The plan doesn’t go into specifics, though it does say “structural changes to the tax code” will “ensure corporations and the wealthiest among us pay their fair share and that we finally end the tens of billions of dollars of tax breaks currently given to fossil fuel companies.”

The proposal does give some specifics on where that $1.5 trillion will go. A total of $600 billion will be invested in “infrastructure necessary to cut pollution across all sectors,” including “$300 billion in direct resources through tax credits and another $300 billion in direct resources through additional investments.” Another “$250 billion in direct resources” will go to various scientific endeavors meant to determine how to achieve net-zero emissions by 2050, as well as “the climate science needed to understand the changes to our oceans and our atmosphere; avoid preventable losses and catastrophic outcomes; and protect public safety and national security.”

Finally, $650 billion will be spent on the people whose lives are affected by climate change. O’Rourke hopes this investment will “mobilize” additional spending in such areas as housing and transportation as Americans adapt to the effects of climate change.

The third part of the plan focuses on that guarantee of net-zero emissions by the middle of the century. “To have any chance at limiting global temperature rise to 1.5 °C and preventing the worst effects of climate change, the latest science demands net-zero emissions by 2050,” the plan says. “By investing in infrastructure, innovation, and in our people and communities, we can achieve this ambition, which is in line with the 2050 emissions goal of the Green New Deal, in a way that grows our economy and shrinks our inequality.” The plan promises O’Rourke will “work with Congress to enact a legally enforceable standard—within his first 100 days.”

“We will harness the power of the market, but also recognize that the market needs rules in order to function equitably and efficiently—not just incentives, but accountability too,” the plan adds.

The “latest science” to which O’Rourke’s plan refers is a 2018 U.N. report that says the world must cut its dependence on fossil fuels by 2050. Climate activists have seized on this report, claiming we’re racing against the clock to save the world. But as Reason science correspondent Ron Bailey explained last month, the doom-and-gloom predictions are exaggerated:

The IPCC asked a group of climate scientists to evaluate how it might be possible to keep the global mean surface temperature from rising 1.5°C above the average temperature of the late 19th century….The report’s authors calculated that in order to have a significant chance of remaining below the 1.5°C threshold, the world would have to cut its carbon dioxide emissions by 40 to 50 percent by 2030 and entirely eliminate such emissions by 2050. So yes, the report says there’s an expiration date if humanity decides to aim for that temperature target. But is it an expiration date for doom? Not so much.

According the report: “Under the no-policy baseline scenario, temperature rises by 3.66°C by 2100, resulting in a global gross domestic product (GDP) loss of 2.6%,” as opposed to 0.3 percent under the 1.5°C scenario and 0.5 percent under the 2°C scenario. In the baseline 3.66°C projection, the estimate of future GDP losses ranged from a low of 0.5 percent to a high of 8.2 percent. In other words, if humanity does nothing whatsoever to abate greenhouse gas emissions, the worst-case scenario is that global GDP in 2100 would be 8.2 percent lower than it would otherwise be.

Let’s make those GDP percentages concrete. Assuming no climate change and an global real growth rate of 3 percent per year for the next 81 years, today’s $80 trillion economy would grow to just under $880 trillion by 2100. World population is likely to peak at around 9 billion, so divvying up that GDP suggests that global average income would come to about $98,000 per person. Under the worst-case scenario, global GDP would only be $810 trillion and average income would only be $90,000 per person. Doom?

Part four of O’Rourke’s plan cites the parts of the country that have been fighting (or at least prepping for) extreme weather. O’Rourke calls for raising spending by a factor of ten “on pre-disaster mitigation grants that save $6 for every $1 invested”; he supports legislation “to make sure that we build back stronger after every disaster”; he wants to invest “in the climate readiness and resilience of our first responders”; and he says we should support U.S. troops “with technologies that reduce the need to rely on high-risk energy and water supply.”

O’Rourke’s climate plan is his first major policy proposal. It could set him apart from many of the other 2020 Democratic candidates—though stopping climate change is already the main platform of one other presidential hopeful, Washington Gov. Jay Inslee.

from Latest – Reason.com http://bit.ly/2ZKErr9

via IFTTT

Beto O’Rourke, the former Texas congressman who’s running for the 2020 Democratic presidential nomination, today released a four-part, $5 trillion plan to fight climate change.

The framework for O’Rourke’s plan, which is posted on his campaign website, promises he will make quick use of his executive authority, though it also pledges the candidate will work with Congress. O’Rourke is not proposing that the federal government fully fund his plan, which sets it apart from Rep. Alexandria Ocasio-Cortez’s (D–N.Y.) much-criticized Green New Deal. Rather, O’Rourke believes a “$1.5 trillion investment” from the federal government will “mobilize” trillions more in additional investments from the private sector to combat climate change.

Part one of the plan would use of executive authority “not only to reverse the problematic decisions made by the current administration, but also to go beyond the climate actions under previous presidents.” O’Rourke says he’ll reverse President Donald Trump’s decision to back out of the Paris climate agreement, and he promises to strengthen emissions standards, reduce various sources of pollution, and require that federal lands plan for net-zero emissions by 2030.

Part two is where Congress comes in. “In the very first bill he sends to Congress,” the plan says, “Beto will launch a 10-year mobilization of $5 trillion directly leveraged by a fully paid-for $1.5 trillion investment—the world’s largest-ever climate change investment in infrastructure, innovation, and in our people and communities.” How are we supposed to pay for that initial investment? The plan doesn’t go into specifics, though it does say “structural changes to the tax code” will “ensure corporations and the wealthiest among us pay their fair share and that we finally end the tens of billions of dollars of tax breaks currently given to fossil fuel companies.”

The proposal does give some specifics on where that $1.5 trillion will go. A total of $600 billion will be invested in “infrastructure necessary to cut pollution across all sectors,” including “$300 billion in direct resources through tax credits and another $300 billion in direct resources through additional investments.” Another “$250 billion in direct resources” will go to various scientific endeavors meant to determine how to achieve net-zero emissions by 2050, as well as “the climate science needed to understand the changes to our oceans and our atmosphere; avoid preventable losses and catastrophic outcomes; and protect public safety and national security.”

Finally, $650 billion will be spent on the people whose lives are affected by climate change. O’Rourke hopes this investment will “mobilize” additional spending in such areas as housing and transportation as Americans adapt to the effects of climate change.

The third part of the plan focuses on that guarantee of net-zero emissions by the middle of the century. “To have any chance at limiting global temperature rise to 1.5 °C and preventing the worst effects of climate change, the latest science demands net-zero emissions by 2050,” the plan says. “By investing in infrastructure, innovation, and in our people and communities, we can achieve this ambition, which is in line with the 2050 emissions goal of the Green New Deal, in a way that grows our economy and shrinks our inequality.” The plan promises O’Rourke will “work with Congress to enact a legally enforceable standard—within his first 100 days.”

“We will harness the power of the market, but also recognize that the market needs rules in order to function equitably and efficiently—not just incentives, but accountability too,” the plan adds.

The “latest science” to which O’Rourke’s plan refers is a 2018 U.N. report that says the world must cut its dependence on fossil fuels by 2050. Climate activists have seized on this report, claiming we’re racing against the clock to save the world. But as Reason science correspondent Ron Bailey explained last month, the doom-and-gloom predictions are exaggerated:

The IPCC asked a group of climate scientists to evaluate how it might be possible to keep the global mean surface temperature from rising 1.5°C above the average temperature of the late 19th century….The report’s authors calculated that in order to have a significant chance of remaining below the 1.5°C threshold, the world would have to cut its carbon dioxide emissions by 40 to 50 percent by 2030 and entirely eliminate such emissions by 2050. So yes, the report says there’s an expiration date if humanity decides to aim for that temperature target. But is it an expiration date for doom? Not so much.

According the report: “Under the no-policy baseline scenario, temperature rises by 3.66°C by 2100, resulting in a global gross domestic product (GDP) loss of 2.6%,” as opposed to 0.3 percent under the 1.5°C scenario and 0.5 percent under the 2°C scenario. In the baseline 3.66°C projection, the estimate of future GDP losses ranged from a low of 0.5 percent to a high of 8.2 percent. In other words, if humanity does nothing whatsoever to abate greenhouse gas emissions, the worst-case scenario is that global GDP in 2100 would be 8.2 percent lower than it would otherwise be.

Let’s make those GDP percentages concrete. Assuming no climate change and an global real growth rate of 3 percent per year for the next 81 years, today’s $80 trillion economy would grow to just under $880 trillion by 2100. World population is likely to peak at around 9 billion, so divvying up that GDP suggests that global average income would come to about $98,000 per person. Under the worst-case scenario, global GDP would only be $810 trillion and average income would only be $90,000 per person. Doom?

Part four of O’Rourke’s plan cites the parts of the country that have been fighting (or at least prepping for) extreme weather. O’Rourke calls for raising spending by a factor of ten “on pre-disaster mitigation grants that save $6 for every $1 invested”; he supports legislation “to make sure that we build back stronger after every disaster”; he wants to invest “in the climate readiness and resilience of our first responders”; and he says we should support U.S. troops “with technologies that reduce the need to rely on high-risk energy and water supply.”

O’Rourke’s climate plan is his first major policy proposal. It could set him apart from many of the other 2020 Democratic candidates—though stopping climate change is already the main platform of one other presidential hopeful, Washington Gov. Jay Inslee.

from Latest – Reason.com http://bit.ly/2ZKErr9

via IFTTT

Even if you disable GPS, deactivate phone location tracking, and turn off your phone, it’s still possible for Google and the NSA to monitor your every move.

Over the last two decades, cell phone use has become an everyday part of life for the vast majority of people around the planet. Nearly without question, consumers have chosen to carry these increasingly smart devices with them everywhere they go. Despite surveillance revelations from whistleblowers like Edward Snowden, the average smart phone user continues to carry the devices with little to no security or protection from privacy invasions.

Americans make up one of the largest smartphone markets in the world today, yet they rarely question how intelligence agencies or private corporations might be using their smartphone data. A recent report from the New York Times adds to the growing list of reasons why Americans should be asking these questions. According to the Times, law enforcement have been using a secret technique to figure out the location of Android users. The technique involves gathering detailed location data collected by Google from Android phones, iPhones, and iPads that have Google Maps and other Google apps installed.

The location data is stored inside a Google database known as Sensorvault, which contains detailed location records of hundreds of millions of devices from around the world. The records reportedly contain location data going back to 2009. The data is collected whether or not users are making calls or using apps.

The Electronic Frontier Foundation (EFF) says police are using a single warrant—sometimes known as a “geo-fence” warrant—to access location data from devices that are linked to individuals who have no connection to criminal activity and have not provided any reasonable suspicion of a crime. Jennifer Lynch, EFF’s Surveillance Litigation Director, says these searches are problematic for several reasons.

“First, unlike other methods of investigation used by the police, the police don’t start with an actual suspect or even a target device—they work backward from a location and time to identify a suspect,” Lynch wrote. “This makes it a fishing expedition—the very kind of search that the Fourth Amendment was intended to prevent. Searches like these—where the only information the police have is that a crime has occurred—are much more likely to implicate innocent people who just happen to be in the wrong place at the wrong time. Every device owner in the area during the time at issue becomes a suspect—for no other reason than that they own a device that shares location information with Google.”

The problems associated with Sensorvault have also concerned a bipartisan group of lawmakers who recently sent a letter to Google CEO Sundar Pichai. The letter from Democrats and Republicans on the U.S. House Energy and Commerce Committee gives Google until May 10 to provide information on how this data is used and shared. The letter was signed by Democratic Representatives Frank Pallone and Jan Schakowsky and Republicans Greg Walden and Cathy McMorris Rodgers.

Google has responded to the report from the Times by stating that users opt in to collection of the location data stored in Sensorvault. A Google representative also told the lawmakers that users “can delete their location history data, or turn off the product entirely, at any time.” Unfortunately, this explanation falls flat when one considers that Android devices log location data by default and that it is notoriously difficult to opt out of data collection.

No matter what promises Google makes, readers should remember that back in 2010, the Washington Postpublished a story focusing on the growth of surveillance by the National Security Agency. That report detailed an NSA technique that “enabled the agency to find cellphones even when they were turned off.” The technique was reportedly first used in Iraq in pursuit of terrorist targets. Additionally, it was reported in 2016 that a technique known as a “roving bug” allowed FBI agents to eavesdrop on conversations that took place near cellphones.

These tools are now undoubtedly being used on Americans. The reality is that these tools—and many, many others that have been revealed—are being used to spy on innocent Americans, not only violent criminals or suspects. The only way to push back against this invasive surveillance is to stop supporting the companies responsible for the techniques and data sharing. Those who value privacy should invest time in learning how to protect data and digital devices. Privacy is quickly becoming a relic of a past era and the only way to stop it is to raise awareness, opt-out of corporations that don’t respect privacy, and protect your data.

via ZeroHedge News http://bit.ly/2XRovBN Tyler Durden

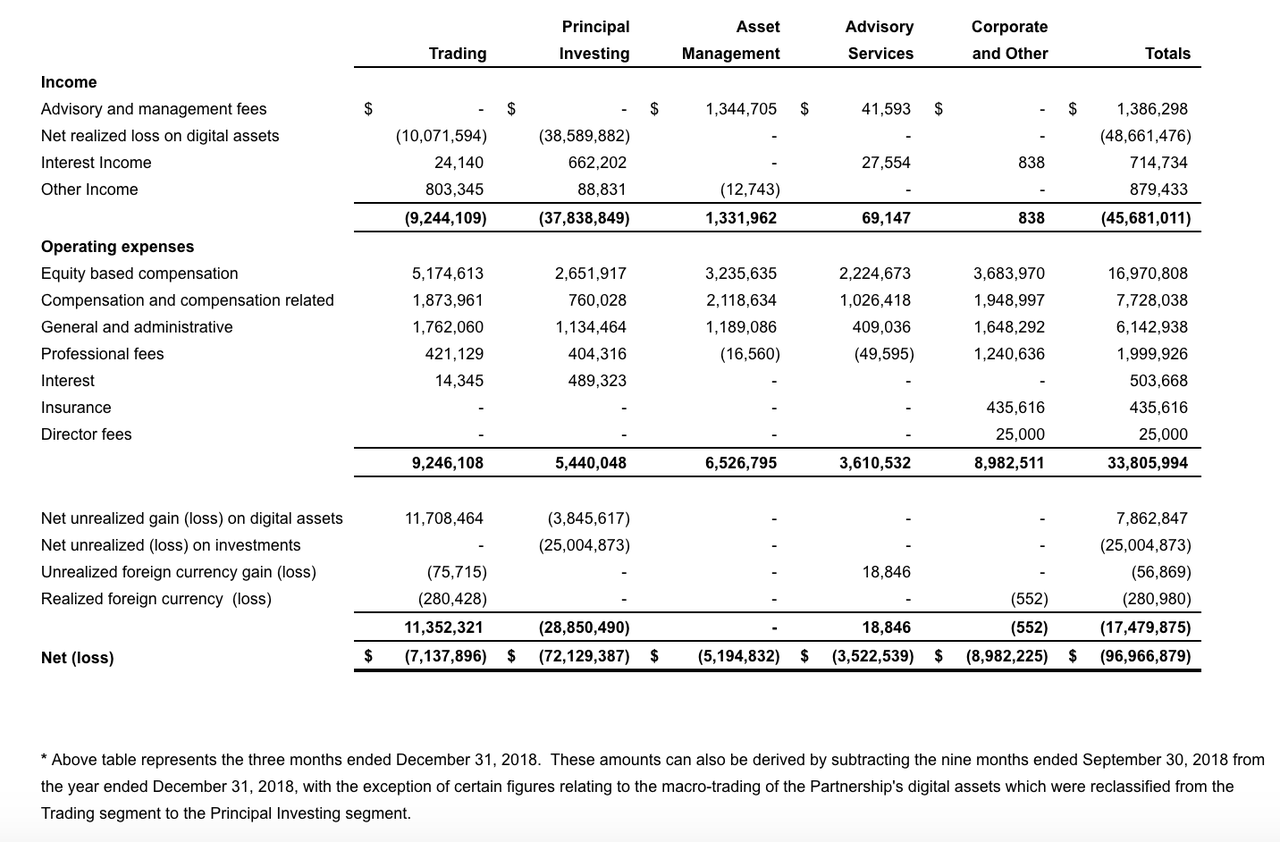

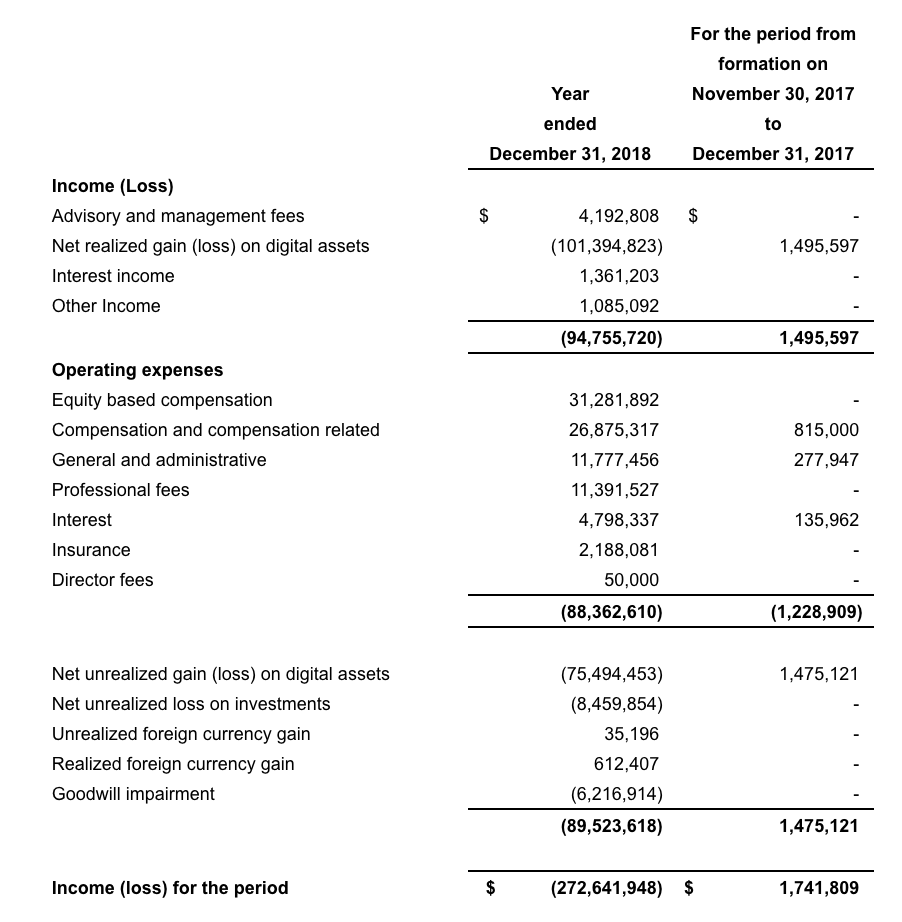

Mike Novogratz’s Galaxy Digital has finally released full-year results for 2018. And what started out as a nine-figure loss, according to financials released all the way back in Q3, the firm had already brooked a $134 million loss, combining realized and unrealized losses, by the end of Q1. By the end of Q3, that loss had widened slightly to $136 million.

By the end of the year, total realized and unrealized losses for the firm founded by the former Goldman partner and Fortress fund manager, which both invests in cryptocurrencies, as well as blockchain-focused startups, had ballooned to $272.7 million, an ignominious start for the company’s first full year of operations.

Mike Novogratz

As of Dec. 31, Galaxy had $249.1 million in digital assets and investments, down from $323 million at the end of September, the company said in a statement.

The additional losses in Q4 were primarily a result of a net realized loss of $48.7 million on the firm’s digital assets (as the firm’s trading arm trimmed some of its losing positions) and a $25 million unrealized loss on its investments.

For the full year, the firm’s total losses on its crypto holdings amounted to $177 million, with nearly $100 million more lost on operating expenses and investment writedowns.

But Novogratz is pressing forward. In the statement, he touted eight new investments closed in the fourth quarter, and upped its investment in three existing startups.

Novogratz said things had already started to turn around in 2019, as crypto prices have rallied off their lows. In particular, bitcoin has held above $5,000.

“While 2018 was a challenging year for the industry, I am pleased with the ways in which our team navigated difficult market dynamics, and believe we are well positioned to scale our business strategically over time. We have used our capitalized position to both identify and invest in a number of unique opportunities, while also continuing to build an institutional-quality platform,” Novogratz said in a statement.

“The first few months of 2019 have yielded a notable increase in activity across our business lines. We are already benefiting from both the strong foundation we laid in 2018 as well as the year-to-date rally in digital asset markets. We expect to continue to build upon this positive momentum through the remainder of 2019 and beyond.”

Since the start of 2019, the company said its Galaxy Benchmark Crypto Index Fund, a passively managed index fund which tracks the Bloomberg Galaxy Crypto Index, has generated inflows and was up about 19% so far this year.

via ZeroHedge News http://bit.ly/2GRc3fF Tyler Durden