Today’s AM fix was USD 1,245.75, EUR 906.13 and GBP 757.76 per ounce.

Yesterday’s AM fix was USD 1,228.50, EUR 895.60 and GBP 749.95 per ounce.

Gold rose $11.90 or 0.97% yesterday, closing at $1,240.60/oz. Silver soared $0.39 or 2% closing at $19.87/oz. Platinum climbed $19.49, or 1.4%, to $1,372.74/oz and palladium edged up $2 or 0.3%, to $733.50/oz.

Gold in U.S. Dollars, 5 Day – (Bloomberg)

Gold edged up to a near one week high today as the dollar weakened and technical support held again prompting funds and investors to allocate funds togold. Given the poor fiscal and monetary state of the U.S., we expect the dollar to weaken in 2014 which should contribute to higher gold prices.

Trading was subdued on the COMEX yesterday as hedge funds and banks turned their attention to the Fed’s policy meeting next week. Volumes in the futures market and the physical market are thin due to little price movement, a lack of news and the wind down in the run up to Christmas.

COMEX Net Long Position – Jan 2006 to Dec, 2013 – (Bloomberg)

There is a risk of a sizeable short covering squeeze after last Friday’s U.S. Commodity Futures Trading Commission (CFTC) data showed hedge funds had cut their bullish bets on gold to the lowest since July 2007. This means that the speculative hot money is the least bullish on gold since 2007.

This suggests that recent heavy selling in gold might have run its course and that speculators and weak hand investors have liquidated their positions which are now being held by stronger hands.

The CFTC data showed that hedge funds also raised their bearish bets in gold to near a 7 and a 1/2 year high. This heightens the risk of a short covering rally. The majority of hedge funds are momentum and trend driven and therefore they tend to often get market bottoms and tops wrong.

They frequently go long at market tops and go short at market bottoms and are therefore considered a good contrarian signal.

Where Are Bail-Ins Likely To Take Place

Bail-ins are likely to happen at banks that are close to failure in countries that have adopted the FSB bail-in conventions and or do not have financial resources to bail-out their banks. Thus, deposits in failing banks in G20 nations may be subject to bail-ins.

The total debt to GDP ratios, household, corporate, financial and sovereign debt, in Japan, the UK and the U.S. are all at very high levels. All three countries have banks whose outlook is far from positive.

Many analysts warn that many Wall Street and City of London banks are bigger now than they were prior to the collapse of Lehman.

The Eurozone debt crisis has abated in recent months but many analysts and economists are concerned that it is only a matter of time before the debt crisis returns with Greece, Spain, Portugal, Italy and Ireland all remaining vulnerable.

European banks have been recapitalised but should the sovereign debt crisis return or a new global systemic crisis happen, à la Lehman Brothers, individual banks may again face capital shortages.

Greece, Cyprus, Spain, Italy, Portugal and Ireland all remain vulnerable. However, other countries in the EU also have risks, including the UK, the Netherlands, Switzerland, Denmark & France.

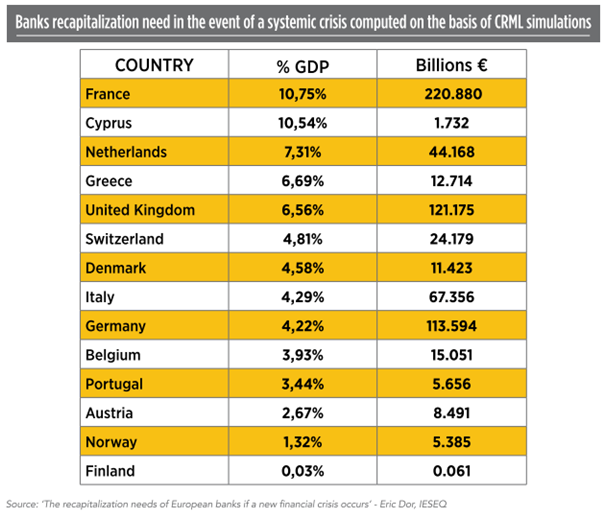

A recent paper by Eric Dor of the IESEG School of Management in France, warned how most European governments remain very exposed to their banks, especially France.

The paper computes the total recapitalisation needs of the banking sector of each European country in case of a new systemic financial crisis. It looks at ratios that would represent the increase of public debt, in percentage of GDP, that would result from a recapitalisation of the big national banks by each country.

France which would incur the highest cost in percentage of GDP, if the big banks in France had to be recapitalised with public monies. After France, Cyprus, the Netherlands Greece, the United Kingdom and Switzerland are the most vulnerable.

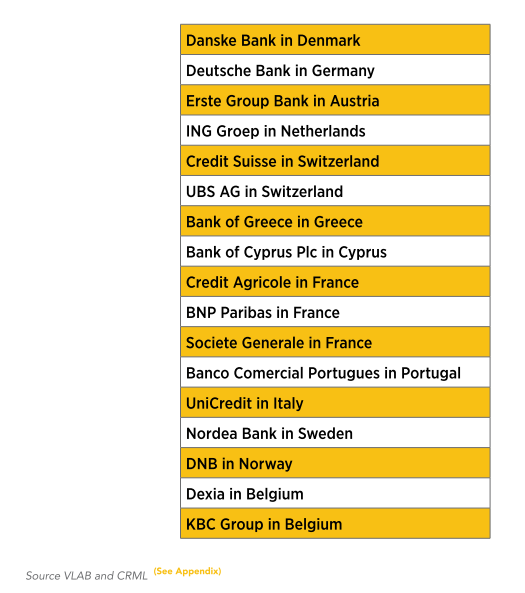

The research highlighted the vulnerability of many large European banks and the capital shortages of these banks in the event of a systemic crisis. Particularly vulnerable banks in each country, according to data compiled by the Center for Risk Management of Lausanne (CRML) and the VLAB of Stern Business School at New York University were (in no particular order):

Stor and his colleagues concluded that:

“The potential capital shortages of the banking sectors of many European countries in the event of a new systemic crisis are very high.”

When Could Bail-Ins Take Place?

The readiness for the bailin regime depends on how quickly each participating jurisdiction implements supporting legislation. Given the recent updates (see below) from a number of regulators and central banks, it appears that they are well positioned to have the necessary legal framework in place to support resolution authorities by about 2015, if not before.

The Financial Stability Board released an updated report in November 2012, titled “Recovery and Resolution Planning: Making the Key Attributes Requirements Operational” requesting input from regulators, supervisory authorities and banking institutions, in which it stated that:

“Reforms are now underway in many jurisdictions to align national resolution regimes and institutional frameworks more closely with the Key Attributes”.

In March 2013, the Reserve Bank of New Zealand stated that it had “been working closely with registered banks for the last two years to put (bail-in) functionality in place”, and intended for the pre-positioning requirements to be in place by 30 June 2013.

The FSB has a Standards Implementation Committee which is currently “reviewing progress on legislating the Key Attributes” and was expected to produce a report by the second quarter of 2013.

EU leaders plan to agree on the ‘Single Resolution Mechanism’ by the end of 2013, for adoption by the European Parliament in 2014, and implementation in January 2015.

The UK and U.S. appear to already have the supporting powers and legislation in place for bail-ins, based on powers granted in the UK Banking Act of 2009 and the Dodd Frank Act of 2010, respectively.

The exact timing of any bank rescue involving a bail-in obviously would then depend on the need for the bank to be rescued.

Emergency resolutions and legislation would be likely in many countries in the event of another Lehman Brothers collapse and another global credit and financial crisis.

Download our Bail-In Guide: Protectin

g your Savings In The Coming Bail-In Era(11 pages)

Download our Bail-In Research: From Bail-Outs to Bail-Ins: Risks and Ramifications –

Including 60 Safest Banks In The World List (51 pages)

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/gBkrr3oc960/story01.htm GoldCore

The National Security

The National Security According to the Los Angeles Times, 18 current

According to the Los Angeles Times, 18 current