While we already knew that St Louis Fed president and FOMC voting member James Bullard dissented with Wednesday’s decision to keep rates unchanged, pushing for a 25bps cut instead, moments ago former Goldman and PIMCO employee, and current Minneapolis Fed president, Neel Kashkari – who is a non-voting FOMC member in 2019 but is voting again next year – said that he advocated for a 50bps cut this week.

In an essay posted both on the Minneapolis Fed website and on Medium, titled “A Strategy to Re-anchor Inflation Expectations“, Kashkari writes that “In the Federal Open Market Committee meeting that concluded on Wednesday of this week, I advocated for a 50-basis-point rate cut to 1.75 percent to 2.00 percent and a commitment not to raise rates again until core inflation reaches our 2 percent target on a sustained basis.”

Why? “I believe an aggressive policy action such as this is required to re-anchor inflation expectations at our target.”

He elaborates:

Since I became president of the Federal Reserve Bank of Minneapolis in January 2016, I have advocated against interest rate increases because I did not see sufficient evidence that inflationary pressures were building, and I believed there was still slack in the labor market. These views led me to formally dissent against rate increases in March, June, and December 2017. More recently, I supported the Committee’s decision in January 2019 to pause further rate increases.

In the past few months, the job market has slowed, wage growth has flattened, inflation has continued to come in below our 2 percent target, inflation expectations have fallen, and the yield curve has inverted.

Minneapolis Fed economists estimate that long-run inflation expectations are currently around 1.7 percent. While that may seem like a small miss from our 2 percent target, it means we will have less ammunition to respond to a future downturn because real interest rates, net of inflation, drive economic activity.

He also accuses the FOMC Committee of being “consistently too optimistic in forecasting inflation returning to 2 percent. Core inflation is the best predictor we have of future headline inflation. My proposed strategy keeps rates on hold for as long as necessary until we actually hit our target. I believe such a strong, credible commitment will boost inflation expectations, while not allowing them to drift too high. If economic conditions weaken or if inflation fails to return to target, this strategy does not preclude further rate reductions. This strategy will also support further job growth, stronger wage growth, and continued economic expansion.”

Clearly Kashkari, whose dovish bias is hardly a surprise as together with Bullard, he has been the committee’s biggest dove for years, has been spared the indignity of purchasing food, medical services, tuition or paying for college on his own personal card, and instead has had the benefit of the Fed’s charge card, where all inflation seems to disappear. Unfortunately for the common person this is hardly the case, as we explained two weeks ago in “Lower Income Americans Are Begging The Fed For Less Inflation“, and prior to that in “How The Fed’s New Monetary Policy Will Crush America’s Poorest” in which we showed that:

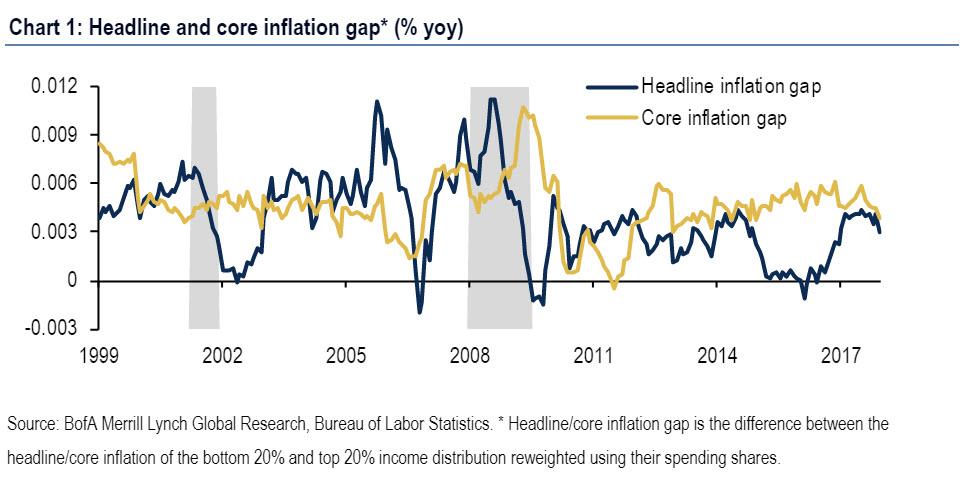

… the lowest income cohort generally experiences higher inflation than the highest income group, because they spend more income share on rent, food at home, and other inflationary items. This can be shown by comparing the inflation rate of the bottom 20% and the top 20% income distribution, reweighted by their spending shares. As shown below, inflation runs above for lower income households given their spending composition.

Naturally Kashkari is unaware, or simply chooses to ignore the fact that the Fed’s “inflation at all costs” (literally) policy cripples America’s poor and middle class, and only benefits those in the top 10% who own financial assets, which in turn continue to rise to all time highs making the rich richer, while the poor get poorer by the year.

Alas, this is not important to Kashkari and those like him who believe that the Fed should resume punishing savers at the expense of debtors and financial asset holders, as if that will somehow magically restore the US economy to its former luster. Also, it may be worth asking why a decade of ultra low rates resulted in the slowest recovery in US history, and why the Fed is advocating a return to those same conditions that resulted in a dead end.

In any case, Kashkari clearly has a strategic goal with his letter, with which he hopes to get on Trump’s good side and be appointed next Fed chair, replacing Powell when Trump finally fires him.

via ZeroHedge News http://bit.ly/2KwqBEG Tyler Durden