Authored by Richard Breslow via Bloomberg,

It’s a trader’s job to make money. And the only way of doing that is to get it right in judging where prices are going. In that sense, its a fool’s errand to complain about losing money because the market got it wrong. It is what it is. And asset prices don’t always move for the reasons that one expects. That’s why people place stops. And yes, that’s why they use technical analysis.

But in fact, markets in the truest sense, just like analysts and policy-makers, get things wrong all the time. They just don’t always know it at the time.

[ZH: Traders are 100% sure of a rate-cut in July… just like in November, they were 85% sure that The Fed would hike rates in July]

It’s hard to look at this week’s action and not conclude that, while you can tie what has happened into a neat and tidy narrative, some markets have had better weeks than others. And it would be a bad mistake to extrapolate further and future moves indiscriminately across all instruments.

It’s no great revelation that the art of economic forecasting, and communicating, has taken a lot of reputational hits this year. One man’s flip-flop is another’s “I got it wrong.” Which has made it particularly problematic to assume the other person necessarily knows something that you don’t.

Studying supposed “reaction functions” is an important and grossly overused practice. We all know that central bankers want things to go well. What that means varies over time. And it would appear that’s happening ever more rapidly. Conflicting imperatives result in “well” not always meaning the same thing. Anyone who thinks all decisions are made solely with reference to a specific and immutable mandate are refreshingly naïve.

And this is especially true in a world where global conditions and their headwinds have become everyone’s business. It is unlikely that a who’s who of central banks all chose a single week to get on the same messaging page. And can’t be the case that disappointing inflation expectations suddenly became a universal revelation.

Inflation expectations are important. For real and potential policy reasons. But it certainly feels like there is an element of misdirection in what has prompted this switch. Which will matter greatly in investing going forward. At the moment, who will be the new ECB head, G-20 trade discussions and a whole host of other issues are all equally important subtexts.

The equity market has its quadruple witching hour today. That will make interpreting today’s price action difficult at best. Still, the resilience of the market is impressive. We’ll see. Other markets will be more interesting.

WTI crude suddenly looks pretty good. Given the news, it remains to be seen whether this is “transitory” or not. But these technical breaks have the potential to become self-fulfilling prophesies. And the situation is fluid.

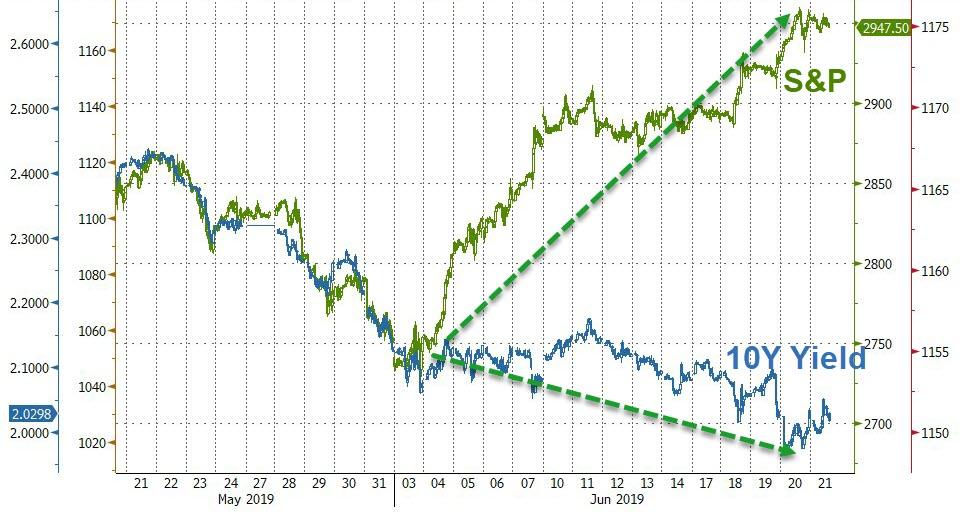

Treasury yields look like they are attempting to stabilize. And that holds whether looking at the two- or 10-year. Stay tuned. Tens are currently almost equidistant from last week’s close and this week’s low.

And while everyone seems to hate the dollar with various levels of vitriol, it’s important to ask why. Commentators seem to think that the FX market is the only one unaware that rate cuts are priced into the market. In a weird way, it’s a shame that today’s European PMI’s were not bad. It has distracted from the relative strength of the U.S. and European economies and feeds into what may be a false narrative. Still, all eyes on the DXY’s 200-day.

At least for a short while.

via ZeroHedge News http://bit.ly/2L01jya Tyler Durden