In an age echoing with the angry Manichean cry of #MeToo, HBO’s drama Share is a puzzling artifact, less a shout than a murmur, taciturn to the point of confusion, a murky exercise in ambiguity.

First-time writer-director Pippa Bianco based Share on her 13-minute short film of the same name, which won an award at Cannes in 2015. I’ve never seen the bare-bones short version, but it sounds only tangentially related to HBO’s bigger, longer production. Even the names of most of the characters have been changed, as if Bianco is willfully snapping ties to her earlier work.

This new Share is about a teenager named Mandy (British newcomer Rhianne Barreto) who wakes up on her front lawn with no memory of how she got there. But there are unwholesome signs: puffy face, dark circles around her eyes, ugly scrapes on her back, and a bruise inside her left elbow, the kind you get from a vaccination or a blood test or a you-know-what.

The next day, a video begins circulating among the cell phones of Mandy’s friends, showing her lying face down on a floor, surrounded by laughing guys, as somebody pulls her jeans down. Who’s doing the pulling is not visible, and what—if anything—happens afterward is unknown.

At this point, Share seems like a well-made but entirely predictable parable of the perils of toxic masculinity and strong drink. But it veers off on a different trajectory. Mandy doesn’t tell any adults what happened and seems more curious than outraged, wondering exactly what was done to her and by whom. When her parents find out about the incident, she’s perplexed by their demand for action. “We have to do something,” insists her mother (Poorna Jagannathan, HBO’s The Night Of.) Replies the confounded Mandy: “Why?”

It’s only after her parents’ intervention that Mandy’s life begins to implode. Along with several teammates, she’s kicked off her high school basketball squad when the investigation of the video shows they were all drinking heavily that night. The cops talk her parents into submitting her to hypnosis to see if she can recover memories of what happened.

Their inquiry goes nowhere except to the local news media, which shred her privacy. As her friends melt away—though some of them try to stay close, a glass shield seems to have grown up between them—her life devolves into nightly rounds of a car-racing video game in which she suicidally slams her vehicle into walls. Mandy seems as much a pawn of her would-be protectors as of her molesters.

At least, that’s my understanding. Share is not always easily comprehended. It’s got the shaky-cam photography and sparse dialogue of a prototypical indie film, along with fleeting, blurry imagery of uncertain meaning. This is all apparently intended to simulate the confusion and progressive withdrawal of a sexual trauma victim, but it does its job a bit too well.

Barreto, the 21-year-old actress who plays Mandy, is remarkably talented at conveying the stress of a character who listens much more than she speaks. But in the end, Bianco’s script is just too terse for its own good. Share is thoughtful, but it’s not entirely clear where those thoughts are headed. Give Bianco credit for making a film about a rage-inducing topic that doesn’t shout; but a little less mumbling would have been welcome.

from Latest – Reason.com https://ift.tt/2YYWRnz

via IFTTT

When it came to the character of witnesses upon whom he relied during his nearly two-year investigation, Robert Mueller clearly didn’t discriminate. He even relied on a man convicted of child porn charges – Lebanese businessman George Nader – to give evidence against people in Trump’s circle.

Now, Nader on Friday was indicted on new charges of importing child pornography and traveling with a minor to engage in illegal sexual activity,Politico reports.

Some of the charges stem from a search of Nader’s iPhones that was conducted in April 2018, when he was detained and questioned by agents on behalf of Mueller after arriving at Dulles Airport.

It’s unclear what Nader told Mueller, though it’s believed his testimony pertained to actions by Erik Prince, the Blackwater founder and brother of Betsy Devoes, who Mueller alleged met with an ally of Russian President Vladimir Putin in the Seychelles around the time of Trump’s inauguration. It was alleged that Prince was trying to set up a “back channel” to Trump. Nader is allegedly an emissary of the UAE.

Soon after the images were discovered, prosecutors reportedly filed a criminal complaint against Nader over the images, but they kept the charges under seal, and Nader’s lawyers were never informed of his impending arrest all the while that he continued to cooperate with the Mueller probe.

That means that Mueller kept a suspected child abuser and pornographer on the streets while it used him as a witness. And now that Nader is no longer useful, he is finally being charged.

Nader was initially arrested on a criminal complaint last month after flying into JFK airport from an international destination, and he was, unsurprisingly, ordered held without bail. He was wearing an Alexandria jail jumpsuit during a five-minute hearing in US District Court in Virginia on Friday. She set a trial date for Sept. 30. Nader’s lawyers stressed the fact that he cooperated with Mueller when asking that he be released on bail, but their requests were denied. They argued that he couldn’t possibly pose a threat to children since Mueller allowed him to enter and exit the country multiple times while he was cooperating in the probe.

The Lebanese businessman has a shadowy record that includes a 1991 conviction on child pornography charges in the US – for which he served only six months in a halfway house thanks to his role in helping to free American hostages in Beirut. He has also been charged and convicted in the Czech Republic in 2002 on 10 cases of sexually abusing minors, and eventually received a one-year prison sentence.

None of this apparently phased Mueller.

via ZeroHedge News https://ift.tt/2LyFAOH Tyler Durden

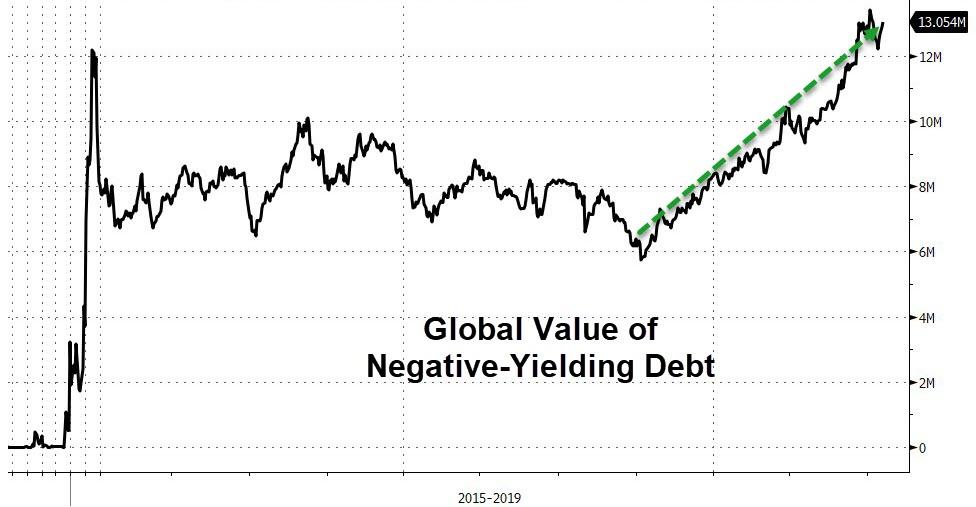

From a low last October of just under USD 6 trillions the value of the Bloomberg Barclays Global Aggregate Negative-Yielding Debt Index has more than doubled, increasing in value by over USD 7 trillions over the last 8 months to establish an all-time record of USD 13.2 trillions earlier in late June.

The current situation is a manifestation of the inability of global financial markets to emerge from the era of ultra-low bond yields that central banks engineered in the wake of the global financial crisis.

Non-conventional policies pursued by central banks in recent years have lead neither to a rise in sluggish rates of economic growth nor to an end in the disinflationary trends within the global economy.

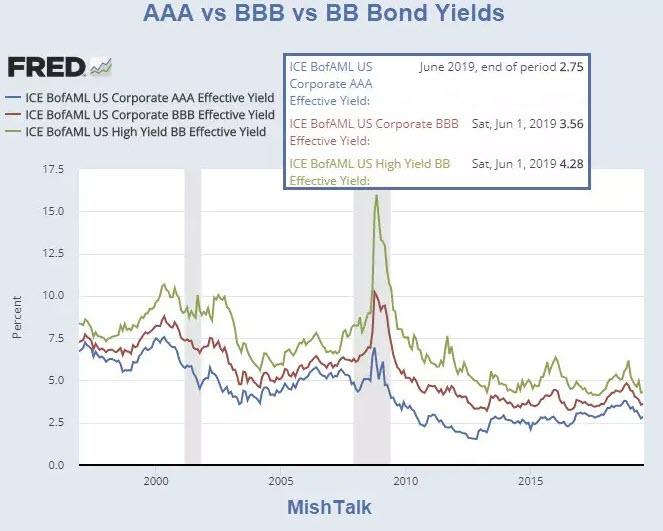

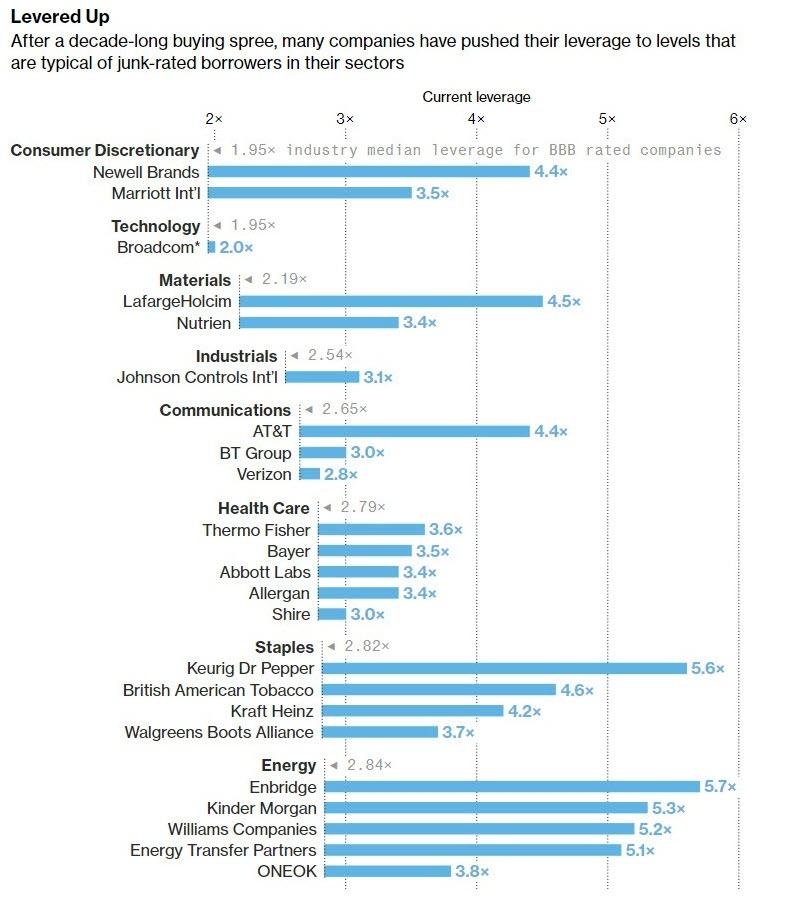

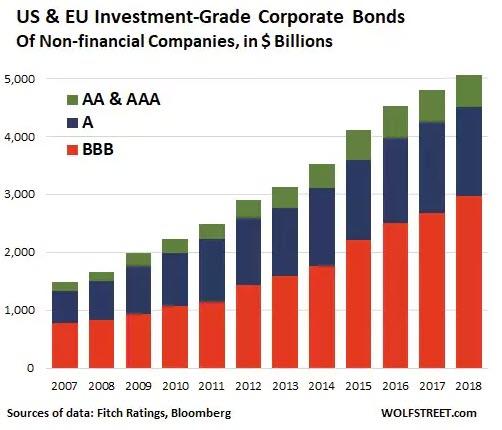

After a decade-long buying spree, many companies have pushed their leverage to levels that are typical of junk-rated borrowers in their sectors.

Bloomberg News delved into 50 of the biggest corporate acquisitions over the last five years, and found more than half of the acquiring companies pushed their leverage to levels typical of junk-rated peers. But those companies, which have almost $1 trillion of debt, have been allowed to maintain investment-grade ratings by Moody’s Investors Service and S&P Global Ratings.

This M&A-fueled leveraging of corporate balance sheets contributed to a surge in debt rated in the bottom investment-grade tier and now represents almost half of the outstanding market, Bloomberg Barclays index data show.

The above article and chart is from October 11, 2018. The leverage (and bubble) is bigger today.

In the next downturn, many bonds in the BBB-category will transition to junk, and many junk bonds but also some investment-grade bonds – if the past is any guide – will transition to default. Two-notch downgrades are not uncommon: one day you wake up, and your “BBB” investment-grade bond is a “BB+” junk bond.

To avoid a downgrade to junk, companies will try to shore up their balance sheet. This means curtailing or stopping share buybacks and slashing dividends.

This is a process GE went through. After blowing nearly $14 billion on share buybacks in the four years through 2017 to prop up its shares, GE stopped on a dime and transitioned to dismembering itself to pay down debts. The share buybacks stopped cold. Then it slashed its dividends to near-zero. And its shares have plunged.

GE now sports a credit rating of “BBB+” with negative outlook, three notches from junk, after getting hit by a round of two-notch downgrades late last year. Despite having already cut off some major limbs to reduce its debts, GE still has $97 billion in long-term debt. And GE is still trying hard to dodge further downgrades.

Richter’s article is from April 9, so again the situation is worse now than as-reported then.

In the latest sign of financial markets going into uncharted territory, more than a dozen junk bonds, which usually carry high yields, now trade in Europe with a negative yield.

It is a stark illustration of how ultraloose monetary policies have turned debt investing into a choice about how to lose the least amount of money.

There are about 14 companies with junk bonds worth more than €3 billion ($3.38 billion) that are trading with negative yields, according to Bank of America Merrill Lynch. They include telecom giant Altice Europe NV and tech-equipment company Nokia Corp.

Everything Bubble

Stocks

Bonds

Consumer Confidence

Buybacks

Faith in Central Banks

The “everything bubble” has at its roots central bank policy of yield suppression.

Central banks made it easy for corporations to borrow money for leverage buyouts, to buy back shares, and for zombie corporations to get enough funding to stay alive.

Investors (speculators actually), especially retiring boomers, are as optimistic as they were in 2007 when they viewed their own house as a retirement vehicle, not a place to live.

Investor Faith

Investor faith in central banks has never been higher.

At the individual level, baby boomers see the stock market is up so they buy a car and have a nice vacation.

Corporations borrow money to buy back their own shares or to make insanely leveraged buyouts.

Hedge funds buy low-yielding junk bonds in belief yields will get even more ridiculous.

Deflation Coming

The Fed is hell bent on producing inflation. The sad part is they do not now how to measure it. Inflation is all around us: In junk bonds, in equities, and in home prices.

How do you put the monetary genie back in the bottle?

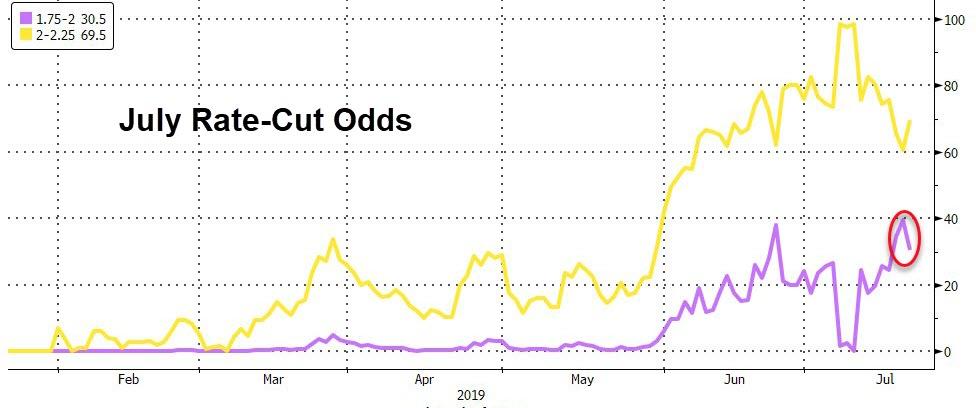

That is what the Federal Reserve is scrambling to figure out today after a day of unprecedented miscommunication by NY Fed president John Wiliams, who as we reported on Thursday, not only singlehandedly repriced market expectations for a 50bps rate cut on July 31, but went so far as to hint that ZIRP is coming back. The fact that even uber dove, St Louis Fed president James Bullard, afterwards said they were expecting 25bps at best, was their desperate attempt to reset market expectations back to 25bps, but by then it was too late, and as of moments ago, the market was pricing in roughly 40% odds of a 50bps rate cut in two weeks, down from 70% yesterday.

In retrospect, Williams made a massive communication mistake.

As Bank of America explained earlier today in a note from chief economist Michelle Meyer titled “The 50bps head fake”, in which she wrote that “on Thursday NY Fed President Williams gave a speech titled “Living Life Near the ZLB” arguing for monetary policy to be proactive and aggressive when confronting an “adverse” outlook. He argued that when short-term interest rates are close to zero, policymakers shouldn’t “keep their powder dry” and that they could not afford to take an “`wait and see’ approach to gain additional clarity about potentially adverse economic developments.” Shortly after, in a TV interview, Vice Chair Clarida strongly argued that it is prudent to take preventative measures with monetary policy when close to the zero lower bound (ZLB). Together, these comments moved markets closer to a 50bp cut at the end of the month.”

However, in an unprecedented move, the NY Fed subsequently released a statement stating that President Williams’s speech on Thursday afternoon was not intended to send a signal that the Fed might make a large interest rate cut this month but rather it was “an academic speech on 20 years of research.”

Why did the NY Fed do this?

Simple: as BofA explains, “the FOMC was uncomfortable with the market moving toward a 50bp cut and wanted to push the market back to a 25bp baseline.” In other words, as Meyer puts it, “Williams unintentionally misguided the markets”.

Which is also why the NY Fed had no other choice but to issue a press release given that the Fed’s blackout period starts on July 20th. If the Fed remained silent, the market would be convinced of a 50bp cut. This, as BofA summarizes, “was a debacle in communication” and here is what the bank thinks the Fed has meant to say

Take out an insurance policy: As Williams argued, the “best thing you can do for your children is to get them vaccinated. It’s better to deal with the short-term pain of a shot than to take the risk that they’ll contract a disease later on.” The Big Three” – Powell, Clarida and Williams – have all stated that it is prudent to take preventative measures with monetary policy when close to the zero lower bound (ZLB). They are worried about heightened uncertainties and risks about the outlook.

The current US data are irrelevant: As Powell noted in his testimony to Congress, his policy decision was not swayed by the strong jobs report. We have also since received a strong reading on core CPI, exceptionally robust retail sales and a rebound in manufacturing surveys. Even in the face of such data, Clarida stated that the Fed is not setting policy based on the current baseline but on the outlook. Again, this goes back to the idea of risk-management, and it tells us to ignore the recent US data.

The Committee will fall in-line…or else: Fed officials who had previously pushed back on a near-term cut – Dallas Fed’s Kaplan and Kansas City Fed’s George, for example – have most recently hinted that they would support a near-term move lower in rates. Chicago Fed President Evans was more explicit in a recent interview advocating for easier policy in order to generate above-target inflation.

As such BofA believes that the Fed is going to cut at the end of the month, most likely by 25bp.

But wait, there’s more, because in a just published confirmation that BofA was indeed correct, in a top-billing article published moments ago on the WSJ, to avoid any further confusion, the Fed leaked using Wall Street’s paper of choice, that “Officials aren’t prepared for bolder action by making a half-point cut, as analysts and traders have speculated in recent days, according to the officials’ recent public statements and interviews” with the article adding that “the larger move appears unlikely for now because officials have said recent economic developments haven’t signaled an imminent downturn.”

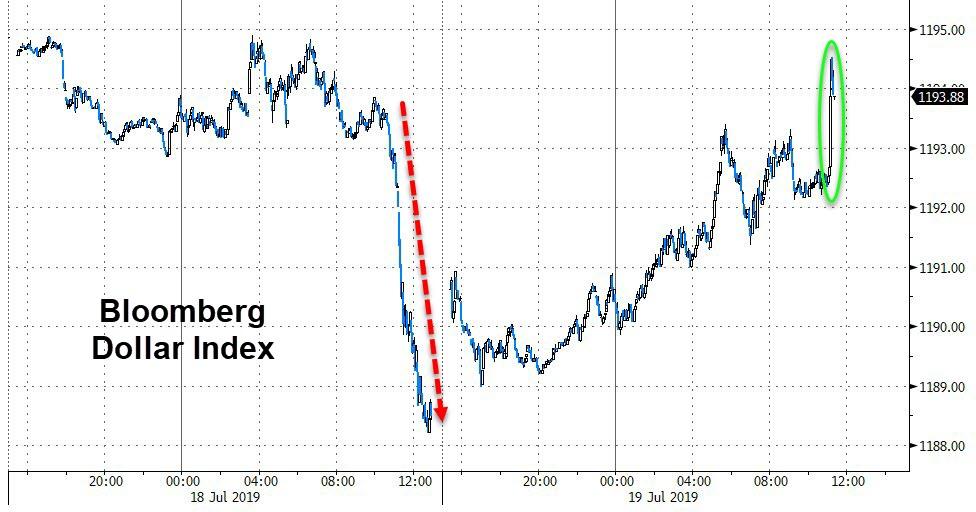

The market reacted rapidly and adjusted the odds of a 50bps cut down to 30% (from over 70% after William’s comments last night).

As expectations for Fed rate-cuts in 2019 shifted back below 50bps…

2Y Yields spiked.

And the dollar jumped.

Stocks were a little more mixed as the spike in crude prices offset some of the hawkish tilt of The Fed’s leak.

via ZeroHedge News https://ift.tt/2Sq4yAw Tyler Durden

There’s good news on the criminal justice reform front today as the FIRST STEP Act of 2018 frees thousands more from federal prison.

The Department of Justice has announced some hard numbers showing who is benefiting from the federal sentencing reform bill. Some figures worth noting:

More than 3,100 federal prisoners will be released due to the increase in “good time” credits that inmates can earn as part of the act.

Nearly 1,700 federal prisoners have had their sentences retroactively reduced by a part of the law that decreases the disparity in sentencing between those convicted of crack cocaine crimes and those convicted of powder cocaine crimes.

The Justice Department has approved 51 “compassionate release” sentence reduction requests for elderly, sick, or disabled prisoners. This is an increase over 2018, where only 34 requests were approved. The FIRST STEP Act gave prisoners increased access to this option.

There had been concerns that the spending bills passed earlier this year did not include the $75 million per fiscal year that the bill wanted to spend on prison education, training, and re-entry programs. But the feds say they have figured out how to redirect $75 million of existing Justice Department money to fund these efforts for fiscal year 2019.

FAMM, a national criminal justice reform organization that fights against mandatory minimum sentences and for more clemency and compassionate releases, praised today’s announcement.

“Every day of freedom is important,” said FAMM President Kevin Ring in a statement. “The good time credit will benefit more than 150,000 people in federal prison today and many more going forward. We’re happy for the families who get to welcome home their loved ones a few weeks or months early.”

It’s these types of positive reform outcomes that prompted Reason reporter C.J. Ciaramella to declare that “Criminal Justice Is Having a (Long Overdue) Moment” in our special Good News/Bad News issue of Reason, on newsstands right now. Check the issue out here, and read more from Ciaramella about what should come next after the FIRST STEP Act here.

from Latest – Reason.com https://ift.tt/2M0exeB

via IFTTT

There’s good news on the criminal justice reform front today as the FIRST STEP Act of 2018 frees thousands more from federal prison.

The Department of Justice has announced some hard numbers showing who is benefiting from the federal sentencing reform bill. Some figures worth noting:

More than 3,100 federal prisoners will be released due to the increase in “good time” credits that inmates can earn as part of the act.

Nearly 1,700 federal prisoners have had their sentences retroactively reduced by a part of the law that decreases the disparity in sentencing between those convicted of crack cocaine crimes and those convicted of powder cocaine crimes.

The Justice Department has approved 51 “compassionate release” sentence reduction requests for elderly, sick, or disabled prisoners. This is an increase over 2018, where only 34 requests were approved. The FIRST STEP Act gave prisoners increased access to this option.

There had been concerns that the spending bills passed earlier this year did not include the $75 million per fiscal year that the bill wanted to spend on prison education, training, and re-entry programs. But the feds say they have figured out how to redirect $75 million of existing Justice Department money to fund these efforts for fiscal year 2019.

FAMM, a national criminal justice reform organization that fights against mandatory minimum sentences and for more clemency and compassionate releases, praised today’s announcement.

“Every day of freedom is important,” said FAMM President Kevin Ring in a statement. “The good time credit will benefit more than 150,000 people in federal prison today and many more going forward. We’re happy for the families who get to welcome home their loved ones a few weeks or months early.”

It’s these types of positive reform outcomes that prompted Reason reporter C.J. Ciaramella to declare that “Criminal Justice Is Having a (Long Overdue) Moment” in our special Good News/Bad News issue of Reason, on newsstands right now. Check the issue out here, and read more from Ciaramella about what should come next after the FIRST STEP Act here.

from Latest – Reason.com https://ift.tt/2M0exeB

via IFTTT

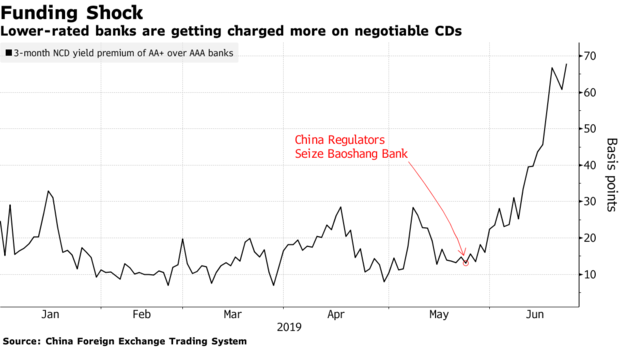

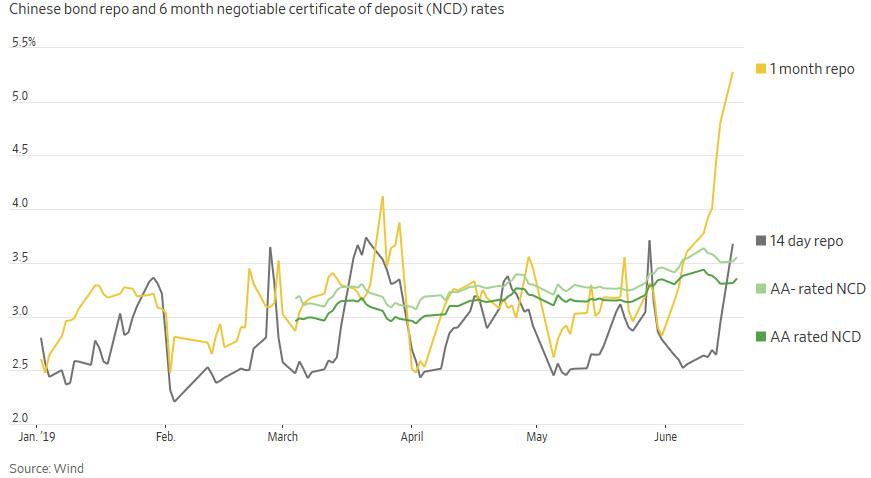

Ever since the unexpected failure of China’s Baoshang Bank in late May, which caused a freeze in the interbank market among smaller, less credible (and government bankstopped) banks, and which sent rates on Negotiable Certificates of Deposit (NCDs), various bank bonds and assorted report rates sharply higher…

… investors have fretted that China appears on the verge of a “Lehman moment”, where wholesale interbank liquidity and overnight funding markets suddenly lock up. The reason for this, as weexplained last month, is that China’s short-term lending market for banks and other financial institutionshas for years operated under the assumption that Beijing wouldn’t allow big losses in the event of defaults or insolvencies(hence the reason whyBaoshang’s failure was a shock). That confidence has been shaken by regulators’ unusual public takeover of the troubled Chinese bank near Mongolia last month, and the even more stunning public admission by the central bank that “not all of Baoshang Bank’s liabilities would necessarily be guaranteed.”

“Bank failure always causes greater concern given systemic fears,” said Owen Gallimore, head of credit strategy at Australia & New Zealand Banking Group, suggesting greater pressure on the private sector ahead.

Naturally, with China growing at the slowest pace in recent history, beset by shadow bank deleveraging, trade war, a shaky transition to a consumer economy and China’s first evercurrent account deficit, these stresses come at a very bad time for the normal functioning of the local economy.

Furthermore, nonbank borrowing through bond repos and interbank loans skyrocketed since China’s central bank began easing monetary policy in early 2018, hitting a net 74 trillion yuan ($10.7 trillion) in the first quarter of 2019, according to Enodo Economics, and up nearly 50% from a year earlier. As the WSJ redundantly warns, “funding troubles for brokerages and other asset managers therefore pose big problems for both financial stability and the real economy.”

Meanwhile, as we warned as far back as March 2017, problems would eventually migrate from the smallish market for negotiable certificates of deposit, used mostly by small banks, into the vastly greater bond repo market. Here, while key one-day and seven-day weighted average borrowing rates had remained low thanks to huge central bank cash injections – such as the 250BN yuan we described back in May – longer tenors such as the 1 month repo have marched sharply higher.

As an aside, for those asking why NCD’s matter, the answer is because as we first explained two years ago, numerous smaller banks had become acutely reliant on such shadow banking funding mechanisms as Certificates of Deposit, which had become the primary source of short-term funding for many of China’s banks mid-size and smaller banks.

As Deutsche Bank further explained, the banks most exposed to a shut down in this “shadow funding” pathway are medium-sized and small banks – such as Baoshang – for whom wholesale funding made up 31% and 23%, a number that has risen substantially in the interim period.

Some more background: in China, the funding flow goes like this (per Bloomberg): big national banks lend to smaller regional lenders, which then provide financing to non-bank peers such as brokerages and funds. They in turn use the money to invest in corporate bonds.

“Smaller banks play a key role in this chain,” said Ming Ming, chief fixed-income analyst of Citic Securities Co. Right now investors are quite “risk averse and everyone wants to mitigate counterparty risks. If things get worse, China’s financial market liquidity could collapse,” he added.

In this context, troubles with NCD funding are troublesome, because as Bloomberg reported recently, in the aftermath of the Baoshang seizure, some Chinese banks and securities firms “tightened requirements for negotiable certificates of deposits that are used as collateral for funding.” In some cases, private NCDs were shunned altogether, and some financial institutions now only accept NCDs sold by state-owned and joint stock banks as collateral while some have refused to lend money to investors pledging NCDs issued by lenders rated AA+ and below for now.

Worse, as Bloomberg followed up last month, the interbank market had started to also freeze up as a result of counterparty suspicions: one month after Baoshang, Chinese bond traders in China are “rethinking counterparty risks as shock waves from a government takeover of a bank ripple through the country’s financial markets.”

As a result, and in an ominous echo of what happened before, and certainly after the Lehman failure, it suddenly got far harder for corporate bonds to be accepted as collateral for repo financing as lenders increasingly demand top quality bonds such as Chinese sovereign bills and policy bank notes as pledges, with Bloomberg noting that “traders are having second thoughts on taking even AAA rated short-term bank debt as security in the wake of last month’s seizure of Baoshang Bank”

As a result, funding among China’s financial institutions has become clogged, in some cases to the point of paralysis, which has already caused borrowing costs to spike for brokerages and smaller banks. All this could mean even higher default rates one year after China reported the highest amount of bonds defaults in modern history.

Meanwhile, in the aftermath of the Baoshang failure, one of the most opaque areas of China’s credit markets – the practice of companies buying their own bonds – has been getting far tougher, and is further contributing to financing difficulties that are already bedeviling the nation’s policy makers.

As Bloomberg discussed last month, at issue is a sharp increase in scrutiny by financial institutions of the collateral that their counterparties offer up in the repurchase market, a crucial channel for short-term funding. If the debt sold by issuers that indirectly purchased a portion of their own bonds – which could account for as much as 8% of China’s corporate bonds, according to Citic Securities – is shunned, that would squeeze liquidity for a swathe of the nation’s businesses, a funding freeze that spreads beyond China’s banking sector and affects even the highest quality corporations.

That’s precisely what appeared to be happening over the past two months when despite regulators’ best efforts to a potentially catastrophic seizing up in the repo market and short-term collateralized lending between banks, some institutions moved to avoid riskier securities. The moves, as Bloomberg notes, “showcased the fragility of confidence toward borrowers that lack state backing in a financial system still dominated by state-sector banks.”

Conditions became especially challenging for firms that obtained funding via unorthodox methods: one such practice is known as “structured issuance”, where a company transfers cash to an asset manager to buy a slice of the bonds the company is itself selling. The manoeuvre helps give the appearance of greater demand for its securities and stronger ability to obtain funding. What could make the practice untenable is if asset managers can no longer use those securities held in custody as collateral for repos.

“Since some repo transactions have defaulted recently, it is unclear whether companies can continue to borrow money from the structured issuance method, said Meng Xiangjuan, chief fixed-income analyst at SWS Research Co. in Shanghai. “If it stops, some issuers will certainly face difficulties operating their business normally, and their debt-repayment pressure will rise,” she said.

It gets worse.

As Bloomberg reported recently, while the practice of self-financing a portion of bond issuance is well known among credit analysts and ratings companies, “observers have been loath to name the firms involved, making this a particularly murky part of China’s debt market.” Citic Securities, for its part, hazarded a total of about 1.5 trillion yuan ($218 billion) worth of securities outstanding that were sold in part via structured issuance.

And so, in addition to the somewhat specialized NCD market, the one place where China’s creeping funding freeze has become apparent is in the repo market, which is collateralized by bonds and other securities which the market no longer accepts at fave value.

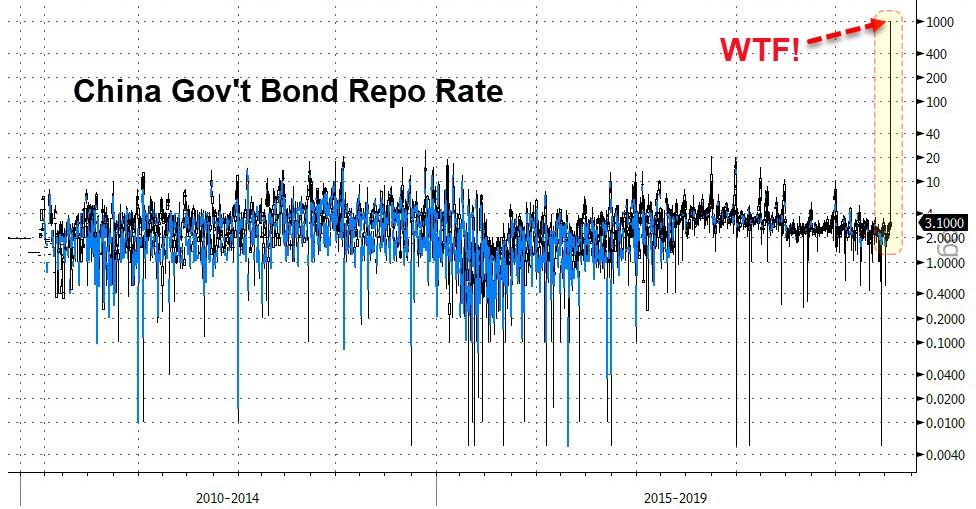

This creeping “Ice Nining” of China’s banking system, and its closest encounter with the proverbial “Lehman moment” yet, came overnight when, inexplicably, the four-day repo rate on China’s government bonds (i.e., the cost for investors to pledge their Chinese government bond holdings for short-term funding) on the Shanghai exchange briefly spiked to 1,000% in afternoon trading!

It is unclear what may have snapped, because as of 3:30pm local time, the repo rate had fallen back to 3.1%, which begs the question: did some bank just have a sudden liquidity run/freeze and was willing to pay anything for immediate access to funding? An exchange official had no idea what had caused the massive spike, and an official told Bloomberg that the Shanghai exchange needs to check details of the trade before it can comment.

To be sure, it may well have been a fat finger: back on July 8, the PBOC said it had suspended some traders at Ping An Bank and China Merchants Bank for a year for involvement in “abnormal” trades, when the two lenders were involved in overnight bond repo trades in the interbank market that put the price at 0.09% on July 2, the PBOC said.

However, that was a fat finger that sent repo lower, and there have been numerous such instances in the past. What is odd, and what makes the overnight move unique, is that this was the first time ever that the government repo rate shot up.

So was this a hint that China’s (long overdue) Lehman moment is finally upon us?

While we wait for the Shanghai exchange to give the “official” version of events, there is some good news: one reason for optimism is that the Fed is now certain to cut rates at the end of the month. Recall that the last time China’s money markets locked up over counterparty risks, was in the aftermath of brokerage Sealand Securities’ initial refusal to pay out on a repo-like agreement in late 2016, when the Fed was in tightening mode. As the WSJ’s Nathaniel Taplin writes, “a dovish Fed gives China’s central bank more room to cushion any further money-market ructions with ample liquidity without worrying too much about destabilizing capital outflows.”

It would be ironic if China’s “white knight” savior from repocalpyse is none other than the Fed.

Alas, here too there is more back news: unlike now, in late 2016 China’s economy was improving and so was corporate creditworthiness. That is no longer the case, and as such, investors should keep a very close eye on China’s money markets in the days ahead to make sure that the spike to 1,000% was a one-off event. One or more such unprecedented lock ups in the interbank market, and a repo market freeze that until now was relegated to a handful of banks and brokerages will promptly “contaminate a fragile financial ecosystem”, one which as the Baoshang shock of May 24 shows, is no longer unreservedly backstopped by Beijing.

via ZeroHedge News https://ift.tt/32F6wSs Tyler Durden

In The General Theory of Employment, Interest and Money, John Maynard Keynes wrote:

“The ideas of economists and political philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influences, are usually the slaves of some defunct economist.”

I think Lord Keynes himself would appreciate the irony that he has become the defunct economist under whose influence the academic and bureaucratic classes now toil, slaves to what has become as much a religious belief system as an economic theory.

Men and women who display appropriate skepticism on other topics indiscriminately funnel facts and data through a Keynesian filter without ever questioning the basic assumptions. Some go on to prescribe government policies that have profound effects upon the citizens of their nations.

And when those policies create the conditions that engender the income inequality they so righteously oppose, they often prescribe more of the same bad medicine. Like 18th-century physicians applying leeches to their patients, they take comfort that all right-minded people will concur with their recommended treatments.

This is an ongoing series of a discussion between Ray Dalio and myself (read Part 1, Part 2, Part 3, and Part 4) . Today’s article addresses the philosophical problem he is trying to address: income and wealth inequality.

Last week I dealt with the equally significant problem of growing debt in the United States and the rest of the world. The Keynesian tools much of the economic establishment wants to use are exacerbating the problems. Ray would like to solve it with a blend of monetary and fiscal policy, what he calls Monetary Policy 3.

The Problem with Keynesianism

Let’s start with a classic definition of Keynesianism from Wikipedia, so that we can all be comfortable that I’m not coloring the definition with my own bias (and, yes, I admit I have a bias). (Emphasis mine.)

Keynesian economics (or Keynesianism) is the view that in the short run, especially during recessions, economic output is strongly influenced by aggregate demand (total spending in the economy). In the Keynesian view, aggregate demand does not necessarily equal the productive capacity of the economy; instead, it is influenced by a host of factors and sometimes behaves erratically, affecting production, employment, and inflation.

The theories forming the basis of Keynesian economics were first presented by the British economist John Maynard Keynes in his book The General Theory of Employment, Interest and Money, published in 1936 during the Great Depression. Keynes contrasted his approach to the aggregate supply-focused “classical” economics that preceded his book. The interpretations of Keynes that followed are contentious, and several schools of economic thought claim his legacy.

Keynesian economists often argue that private sector decisions sometimes lead to inefficient macroeconomic outcomes which require active policy responses by the public sector, in particular, monetary policy actions by the central bank and fiscal policy actions by the government, in order to stabilize output over the business cycle. Keynesian economics advocates a mixed economy—predominantly private sector, but with a role for government intervention during recessions.

And Keynesian economists (of all stripes) want fiscal policy (essentially, government budgets) to increase consumer demand. If the consumer can’t do it, the reasoning goes, then the government should step into the breach. This of course requires deficit spending and borrowed money (including from your local central bank).

Essentially, when a central bank lowers interest rates, it is encouraging banks to lend money to businesses and telling consumers to borrow money to spend. Economists like to see fiscal stimulus at the same time, as well. They point to the numerous recessions that have ended after fiscal stimulus and lower rates were applied. They see the ending of recessions as proof that Keynesian doctrine works.

First, using leverage (borrowed money) to stimulate spending today must by definition reduce consumption in the future. Debt is future consumption denied or future consumption brought forward.

Keynesian economists argue that bringing just enough future consumption into the present to stimulate positive growth outweighs the future drag on consumption, as long as there is still positive growth.

Leverage just equalizes the ups and downs. This has a certain logic, of course, which is why it is such a widespread belief.

Keynes argued, however, that money borrowed to alleviate recession should be repaid when growth resumes. My reading of Keynes does not suggest he believed in the unending fiscal stimulus his disciples encourage today.

Secondly, as has been well documented by Ken Rogoff and Carmen Reinhart, there comes a point at which too much leverage becomes destructive. There is no exact way to know that point.

It arrives when lenders, typically in the private sector, decide that borrowers (whether private or government) might have some difficulty repaying and begin asking for more interest to compensate for their risks.

An overleveraged economy can’t afford the higher rates, and economic contraction ensues. Sometimes the contraction is severe, sometimes it can be absorbed. When accompanied by the popping of an economic bubble, it is particularly disastrous and can take a decade or longer to work itself out, as the developed world is finding out now.

Every major “economic miracle” since the end of World War II has been a result of leverage. Often this leverage has been accompanied by stimulative fiscal and monetary policies. Every single “miracle” has ended in tears, with the exception of the current recent runaway expansion in China, which is still in its early stages.

Insufficient Income Causes Recessions

I would argue (along, I think, with the “Austrian” economist Hayek and other economic schools) that recessions are not the result of insufficient consumption but rather insufficient income.

Without income, there are no tax revenues to redistribute. Without income and production, nothing of any economic significance happens. Keynes was correct when he observed that recessions are periods of reduced consumption, but that is a result and not a cause.

Entrepreneurs must be willing to create a product or offer a service in the hope there will be sufficient demand for their work. There are no guarantees, and they risk economic peril with their ventures, whether we’re talking about the local bakery or hairdressing shop or Elon Musk trying to compete with the world’s largest automakers. If government or central bank policies hamper their efforts, the economy stagnates.

The Reason Keynesianism Sticks

Many politicians and academics favor Keynesianism because it offers a theory by which government actions can become decisive in the economy. It lets governments and central banks meddle in the economy and feel justified.

It allows 12 people sitting in a board room in Washington DC to feel they are in charge of setting the most important price in the world, the price of money (interest rates) of the US dollar and that they know more than the entrepreneurs and businesspeople who are actually in the market risking their own capital every day.

This is essentially the Platonic philosopher king conceit: the hubristic notion that a small group of wise elites is capable of directing the economic actions of a country, no matter how educated or successful the populace has been on its own.

And never mind that the world has multiple clear examples of how central controls eventually slow growth and make things worse over time. It is only when free people are allowed to set their own prices of goods and services and, yes, even interest rates, that valid market-clearing prices can be determined. Trying to control them results in one group being favored over another.

In today’s world, savers and entrepreneurs are left to eat the crumbs that fall from the plates of the well-connected crony capitalists and live off the income from repressed interest rates. The irony of using “cheap money” to drive consumer demand is that retirees and savers get less money to spend, and that clearly drives their consumption down.

Why is the consumption produced by ballooning debt better than the consumption produced by hard work and savings? This is trickle-down monetary policy, which ironically favors the very large banks and institutions.

If you ask Keynesian central bankers if they want to be seen as helping the rich and connected, they will stand back and forcefully tell you “NO!” But that is what happens when you start down the road of financial repression. Someone benefits. So far it has not been Main Street.

The Great Reset: The Collapse of the Biggest Bubble in History

New York Times best seller and renowned financial expert John Mauldin predicts an unprecedented financial crisis that could be triggered in the next five years. Most investors seem completely unaware of the relentless pressure that’s building right now. Learn more here.

via ZeroHedge News https://ift.tt/2JEHPOv Tyler Durden

This doesn’t exactly inspire confidence in WeWork’s (otherwise known as “the We Company”) upcoming IPO.

An investigation by the Wall Street Journal has determined that WeWork co-founder Adam Neumann has cashed out more than $700 million from the company using a mix of stock sales and debt.

If that number seems unusually large, that’s because it is: CEOs typically wait for their company to go public before cashing out. And though WeWork is still private and doesn’t publicize sales of stock by insiders, WSJ’s reporters believe that Neumann’s cash-out is one of the largest on record for a tech unicorn headed for a public offering.

Neumann remains the CEO of WeWork as well as its single largest shareholder, but the exact size of his holdings in the company now is unknown. As of the end of 2017, a company that controlled Neumann’s and his co-founder’s stake in the company showed they held a combined 30% of the company, which was recently valued at $47 billion during its latest round of investment in January. The company plans on moving ahead with the listing later this year or early next year, and initially filed confidentially for an IPO late last year.

Of course, such a large cash-out raises questions about the CEO’s confidence in the company and calls the lofty valuation for the cash-burning machine that is WeWork into question – particularly given the vulnerabilities built-in to the company’s business model that have been highlighted by skeptics. Like Lyft and Uber before it, WeWork’s losses have doubled alongside its revenues.

Since WeWork was founded nine years ago, Neumann has invested heavily in real estate. He spent more than $80 million for at least five homes and his other investments include commercial properties and stakes in start ups. He has also given away more than $100 million, according to people familiar with his finances.

It’s extremely rare for a private company to publicize a top executive selling stock prior to an IPO. But among the instances that are well known, Neumann’s transactions rank among the largest in dollar terms.

Neumann, who is 40 years old, has sold shares during most investment rounds since 2014 – though he didn’t take money out during the January round. He is also taking out loans of several hundred million dollars backed by his shares. On the other hand, he has used some of the proceeds to purchase more shares by exercising stock options early, a sign that he’s also betting on shares to move higher. As Neumann has pulled money out, holders of junk bonds issued by the company have gotten hammered.

The majority of Neumann’s wealth remains connected to the company. JP Morgan has been the bank helping him borrow against his shares and the bank has separately been working with the company to structure a debt deal that would raise as much as $3 billion to $4 billion ahead of its IPO.

Venture capitalists have been skeptical of pre-IPO sales by executives. Most investors would prefer that insiders keep their wealth tied to the company until it goes public so as to keep their interests totally aligned. But how was Neumann able to pull off such a massive cash-out? Though he was speaking generally and not specifically about Neumann and WeWork, Bill Gurley, a partner at WeWork investor Benchmark, said: “…the practice is driven by investors who come in at the late stage and they beg the founders to take liquidity because they’re trying to get more ownership.”

On the other hand, it isn’t 100% unheard of for founders to sell small chunks of the their shares in very late stage financing deals.

“Over the last five years there’s been a growing level of comfort among the VC community to let founders sell,” said Andrea Walne, a partner at Manhattan Venture Partners.

But several of the most recent examples of founders selling prior to the IPO paint an ugly picture:

Some of the other largest publicly-known sales of stock before an IPO include Zynga Inc.founder and CEO Mark Pincus’s deal to take more than $109 million off the table before the social-gaming company’s 2011 IPO. Eric Lefkofsky, as executive chairman and co-founder of Groupon Inc., sold more than $300 million in Groupon stock before the 2011 IPO. Both deals attracted criticism at the time, particularly after the companies’ stocks later traded at lower valuations.

More recently, Snap Inc. disclosed that co-founder Evan Spiegel sold roughly $8 million in stock and borrowed $20 million from the company before its 2017 IPO. Slack Technologies Inc. disclosed CEO Stewart Butterfield sold $3.2 million of stock between September 2016 and Slack’s June public listing.

Since 2013, Newman has bought four homes in and around New York City and paid $21 million for a 13,000 square-foot house in the Bay Area that has a guitar shaped room.

Some savvy real-estate investors are already sounding the alarm about Neumann and WeWork.

I spoke to the most successful real estate investor I know. Very, very wealthy. Said he thinks WeWork is a fraud that is guaranteed to go bust. https://t.co/sUWnF4aXKM

But one doesn’t exactly need to be a genius to figure out that Neumann is essentially a con artist. He has raided his own company’s coffers by buying properties and leasing them to WeWork. He has also used the company’s money to support a private elementary school for his own kid. Don’t let the company’s PR machine – which has sought to portray Neumann as a workaholic savant – fool you.

Then again, if one “community adjusts” Adam Neumann’s cash out (the company’s preferred term for the financial engineering it has applied to its income statement)…

…they could determine that he’s actually putting money in to the company.

via ZeroHedge News https://ift.tt/2JQceYV Tyler Durden

Americans east of the Rockies are sweltering as daytime temperatures soar toward 100 degrees or more. It is now customary for journalists covering big weather events to speculate on how man-made climate change may be affecting them, and the current heat wave is no exception. Take this headline in The New York Times: “Heat Waves in the Age of Climate Change: Longer, More Frequent and More Dangerous.”

As evidence, the Times cites the U.S. Global Change Research Program, reporting that “since the 1960s the average number of heat waves—defined as two or more consecutive days where daily lows exceeded historical July and August temperatures—in 50 major American cities has tripled.” That is indeed what the numbers show. But it seems odd to highlight the trend in daily low temperatures rather than daily high temperatures.

As it happens, chapter six of 2017’s Fourth National Climate Assessmentreports that heat waves measured as high daily temperatures are becoming less common in the contiguous U.S., not more frequent.

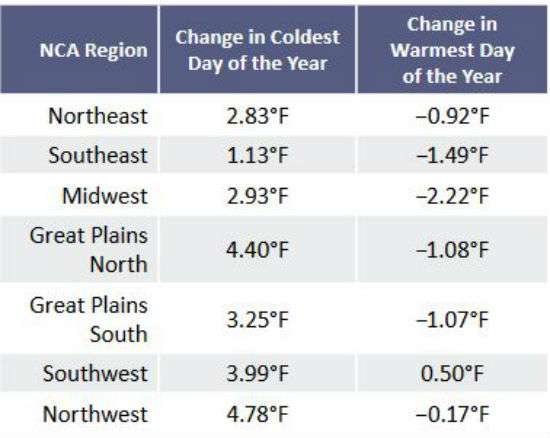

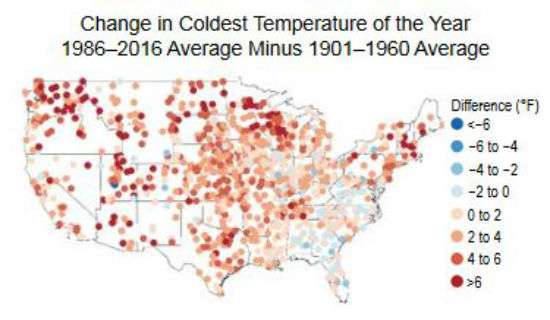

Here, from the report, are the “observed changes in the coldest and warmest daily temperatures (°F) of the year for each National Climate Assessment region in the contiguous United States.” The “changes,” it explains, “are the difference between the average for present-day (1986–2016) and the average for the first half of the last century (1901–1960).”

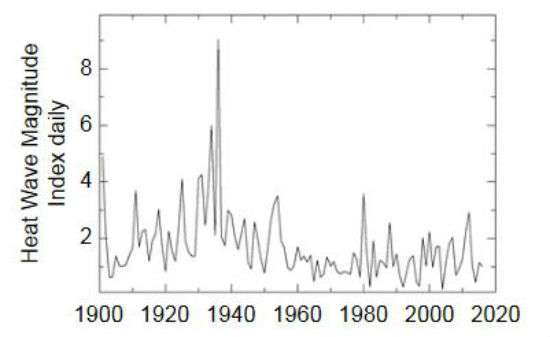

And here is the Heat Wave Magnitude Index, which shows the maximum magnitude of a year’s heat waves. (The report defines a heat wave as a period of at least three consecutive days where the maximum temperature is above the appropriate threshold.)

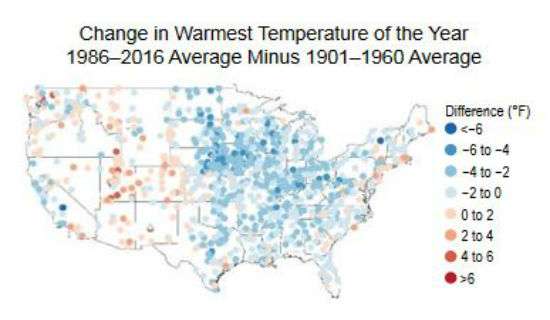

The maps below, from the Fourth Assessment, illustrate the trends in the warmest (generally daytime) and coldest (generally nighttime) temperatures in the contiguous U.S.:

According to the Intergovernmental Panel on Climate Change, climate models tend to significantly underestimate the decrease in the diurnal temperature range—that is, the difference between minimum and maximum daily temperatures—over the last 50 years. The panel’s latest report notes that there is “medium confidence” that “the length and frequency of warm spells, including heat waves, has increased since the middle of the 20th century” around the world. Medium confidence means there is about a 50 percent chance of the finding being correct. (The report does deem it “likely that heatwave frequency has increased during this period in large parts of Europe, Asia and Australia.”)

Heat wave trends aside, the Fourth National Climate Assessment reports that “the annual average temperature over the contiguous United States has increased by 1.2°F” if you compare the period of 1986–2016 to that of 1901–1960. Outside the lower 48 states, Alaska’s average winter and summer temperatures have increased since 1950 by 7°F and 2.6°F, respectively.

Big tip of the hat to the University of Colorado’s invaluable Roger Pielke Jr.

from Latest – Reason.com https://ift.tt/2M3dZEL

via IFTTT

“Every day of freedom is important,” said FAMM President Kevin Ring in a statement. “The good time credit will benefit more than 150,000 people in federal prison today and many more going forward. We’re happy for the families who get to welcome home their loved ones a few weeks or months early.”

“Every day of freedom is important,” said FAMM President Kevin Ring in a statement. “The good time credit will benefit more than 150,000 people in federal prison today and many more going forward. We’re happy for the families who get to welcome home their loved ones a few weeks or months early.”

{kind=link}