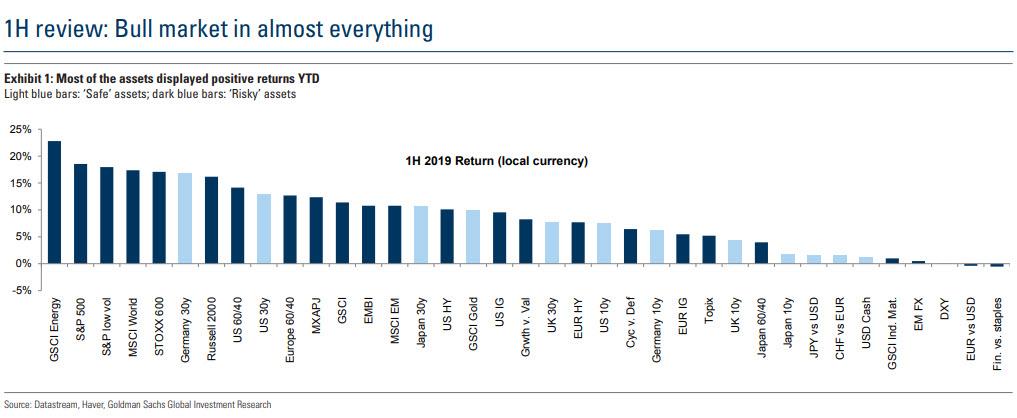

Earlier today, we reported that the S&P 500 posted the best June return (+6.9%) since 1955, with all 38 major assets tracked by Deutsche Bank ending the month with a positive total return. If one looks at monthly data back to the start of 2007, “this has only ever happened once before” according to Deutsche Bank’s Craig Nicol. Amazingly, that was back in January of this year, just after Steven Mnuchin called the Plunge Protection Team. In other words, January and June of this year are the only months in the last 150 which have seen all assets post a positive total return.

Such performance is, for lack of a better word, unprecedented.

In a follow up note, Goldman picks up on this observations with the bank’s Alessio Rizzi writing that much in contrast to last year, most of the assets delivered positive performance YTD.

Having said that, with growth data softening again in May, risky assets have been range-bound since. The equity correction in May has been relatively small and followed by a sharp recovery in June supported by more dovish central banks and fading trade tensions concerns.

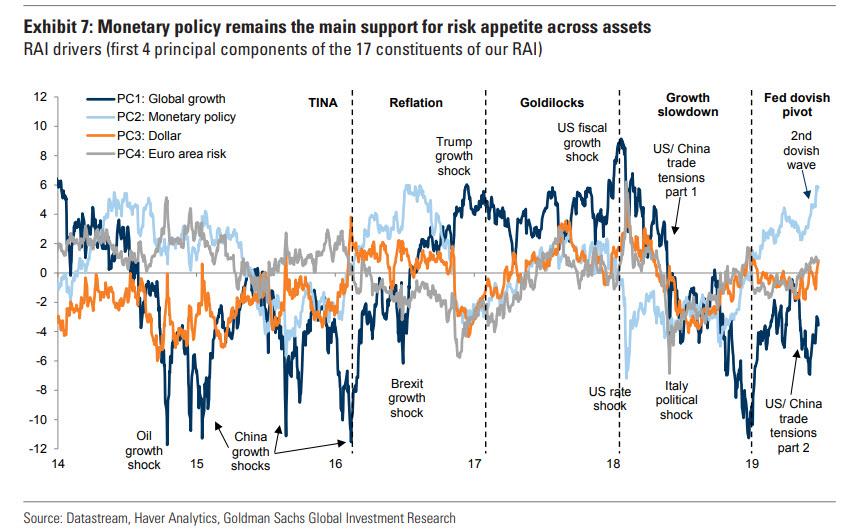

So what has been behind this unprecedented move higher in risky, safe haven and all other assets?

Take a wild guess…. and you’re probably right.

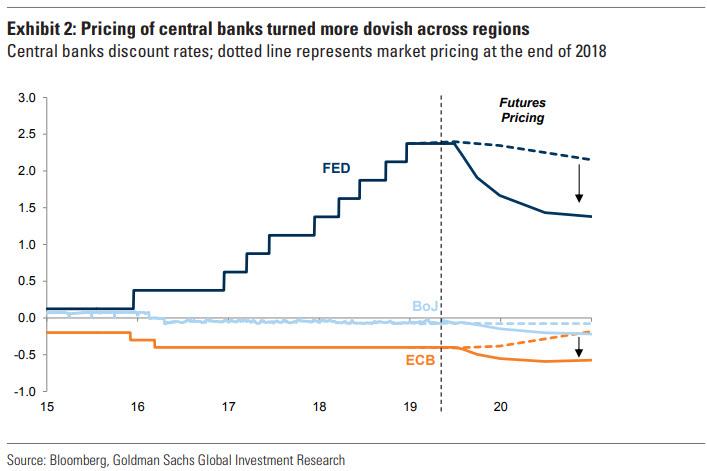

As Goldman answer, since June, there has been a second dovish wave with increased expectations for more ECB easing post Draghi’s Sintra speech and the June FOMC meeting. As a result, Goldman’s proprietary indicators shows that “monetary policy” remains the main driver of risk appetite and expectations are now very bullish.

The same was true in 1H 2016 but after the Brexit shock on June 23, ‘global growth’ expectations picked up, further boosted by Trump being elected in 3Q, which drove a more traditional ‘risk on’ pattern with equities rallying and bonds selling off.

And here it is again, for the cheap seats: “while global growth has softened YTD, the boost from easier monetary policy has driven more appetite both for risky and ‘safe’ assets. Market expectations have turned much more dovish since the end of 2018.”

Some more color:

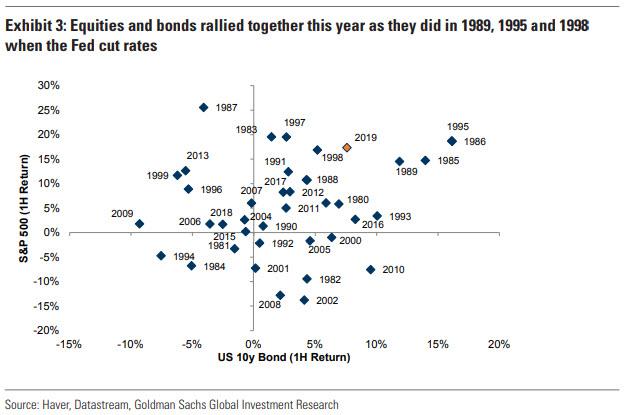

… the market is now pricing c.3 cuts and similarly investors have priced further ECB easing. As a result, both equities and bonds rallied and had one their best starts of the year since the 80s. This is not unusual after dovish monetary policy shifts, e.g. when the Fed starts cutting interest rates; in fact 1989, 1995 and 1998 were strong years for equity and bonds.

So with the Fed, and only the Fed, the driver of most if not all market upside in 2019 (as a reminder, in June PE multiple expansion – i.e., rate expectations – and not earnings were responsible for 90% of the upside), here are some of the consequences:

Due to the weak growth, the leadership within risky assets has been defensive – low vol stocks, defensive sectors and growth stocks outperformed. US low vol stocks had their best start in the last 30 years and a 6-month return similar that post the GFC trough. Investors have been reluctant in adding exposure to riskier assets and fund flows into equity have been quite negative, comparable to previous bear markets.

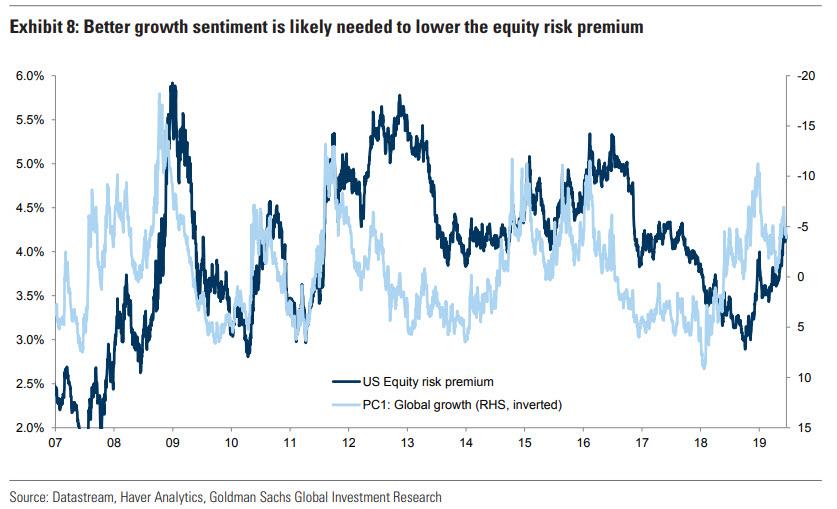

Additionally, the continued lack of positive growth news (and the preponderance of negative news) during the equity rally YTD also helps explain the growing gap between equity and bond yields – the US equity risk premium has increased alongside the de-rating of ‘global growth’ expectations as investors remain relatively cautious. The same has been true across regions and in those markets with increased secular stagnation concerns, such as Europe, where the de-rating of equities relative to bonds has been even larger.

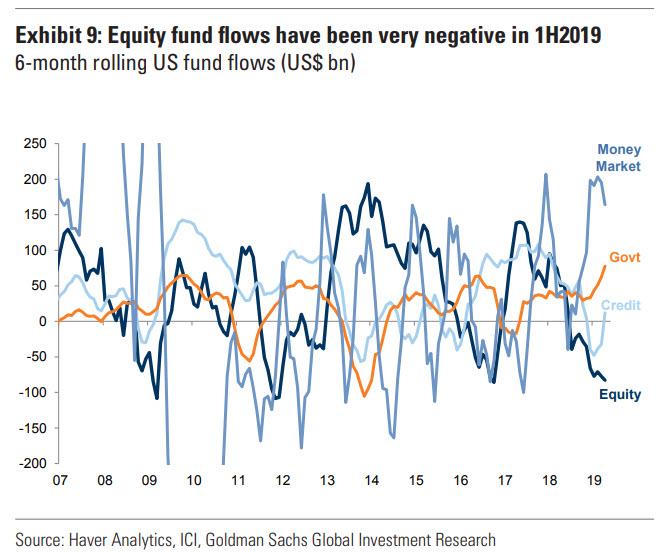

The same investor cautiousness shows in fund flows – in the last 6 months, US equity fund flows have been the most negative since the global financial crisis, while there have been large inflows into money market funds and more recently credit and government bond funds due to the more carry-friendly backdrop.

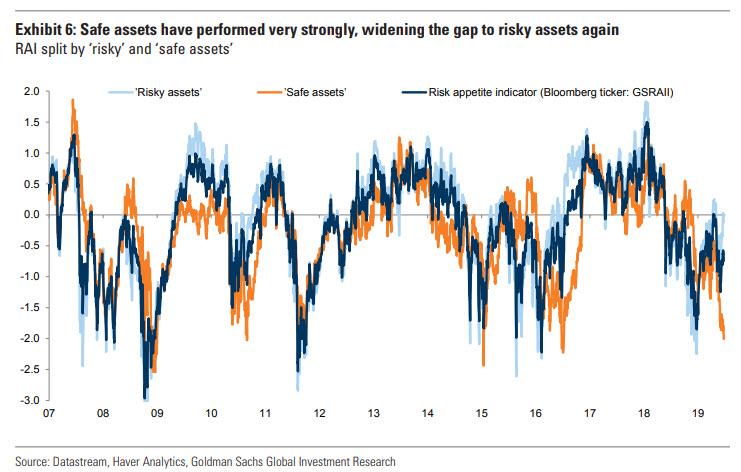

Finally, there is a large gap between risk appetite in ‘risky’ and ‘safe assets’ – Goldman’s aggregate index for ‘risky assets’ is close to neutral again while the continued strong rally of global bonds and safe havens such as Gold and the Yen signal very low risk appetite. The same gap exists between global equities, with the S&P 500 at all-time highs and 10-year bond yields heading to all-time lows. This, according to Goldman, is common in ‘bad news is good news’ regimes, when monetary policy drives a strong search for yield – the same was the case in 1H2016, when easier monetary policy stabilized markets.

So if not growth and not profits, and only the Fed is pushing stocks to new all time highs (on a string), how much longer can this farce of a market continue to levitate? The truth? Nobody knows of course, but as even Goldman now admits, “eventually growth has to take over as the main a driver to drive a procyclical rotation across and within assets.”

via ZeroHedge News https://ift.tt/2RT7AwT Tyler Durden

OPEC and its partners have decided to roll over the existing production cut agreement for another 9 months. After weeks of deliberations, infighting, global pressure and media hype, OPEC and Russia have confirmed the global oil market still needs support. OPEC officials stated the latter to the press, repeating Russian President Putin’s and Saudi Minister of Energy Khalid Al Falih’s former statements. Russian President Vladimir Putin said on Saturday that he had agreed with Saudi Arabia to extend existing output cuts of 1.2 million barrels per day, or 1.2% of global demand, until December 2019 or March 2020.

Fears about a possible US-China Trade War, resulting in lower global economic growth, and the continued growth of US shale output has put oil prices under pressure, especially after several unexpected inventory builds earlier this year. The geopolitical instability in the Persian Gulf, a looming military confrontation in the East Mediterranean and sanctions on Iran, Venezuela and even Russia, did nothing to quell the negative price spiral. Emotions were ruling, not facts. Oil prices, however, now seem to get some space to rally, as China and the U.S. have agreed to renegotiate a trade deal, demand still appears to be growing, and US storage volumes have shown signs of reversing. Oil bulls have regained a bit of hope, but financial analysts are still warning for a possible negative price correction, based on the still unresolved China-US situation. Strangely enough the same analysts are not incorporating possible negative repercussions from the ongoing situation in the strait of Hormuz, a looming conflict in Libya and the still relatively strong economy.

At the same time, optimism within OPEC itself is waning, as severe rifts in the cartel have occurred in preparation to this week’s OPEC Vienna meeting. Iran and Venezuela are increasingly putting their foot down, as they claim that the rest of OPEC, especially Saudi Arabia and the UAE, are taking advantage of the US sanctions. The last weeks the Kingdom, but also the UAE, have signed major deals with China, Japan and South Korea to lock-in future demand in these countries. The Iranian sanctions, even if they have not brought exports to zero as US president Trump likes to claim, have been a boon for other OPEC producers, filling in the gaps left by Tehran in Asia and Europe. Iran’s geopolitical supporter no. 1 Russia also has taken advantage of the Iranian predicament.

This situation has stirred up anger in Tehran and Caracas. In contrast to official statements made by the separate Arab OPEC countries, all have taken the opportunity to expand market share. Iran will have a hard time to regain its position. At the same time, Venezuela is confronted by the same developments, leaving the heavy-oil producer no chance to regain its former glory for a very long time.

At present, Iran does not have a lot of instruments to counter the Saudi-UAE-Russian actions. Blocked by US sanctions, no economic options are available to the Iranian regime. Still, Tehran has been able to deliver a major blow the last hours. Without leaving the cartel, Iran has openly defied the growing willingness inside of OPEC and Russia to formalize the ongoing OPEC+ cooperation.

In a surprise remark to the press, Iran’s oil minister Bijan Zanganeh said that he will veto OPEC’s long-mooted charter intended to formalize its oil market coordination with Russia and nine other non-OPEC partners. The latter means not only a blockade of Saudi-UAE dreams to incorporate Russia officially, but it also is a slap in the face of Russian president Vladimir Putin and Russia’s Energy Minister Novak. The two Russians have been eager to formalize the OPEC+ deal, supported on the Saudi side by Crown Prince Mohammed bin Salman. The formalization seems to have been one of the discussion points between Putin and MBS at the G20 in Osaka, Japan. The Iranian threat also will complicate the OPEC+ meeting, which is set for Tuesday, after the official OPEC meeting.

The Iranian move is almost a rehearsal of the 2007 Riyadh meeting, when Tehran and Caracas blew up the 2nd OPEC Heads of State Meeting. By supporting an OPEC production agreement, but blocking a formal participation of Russia, Tehran keeps its position in balance. If the Saudi-Russian cooperation would be formalized and included under the OPEC umbrella, Tehran fears to be pushed out of the power centers. Officially Iran wants to block the OPEC+ formalization due to Saudi-UAE support for US Iran sanctions, but Tehran wants to be in power when deals are made between OPEC and Russia. With a formalization of the OPEC+ situation, the Riyadh-Moscow-Abu Dhabi trilateral becomes the decision making center without interference of others. Tehran fears a so-called unilateralism by OPEC+ (Moscow/Riyadh). Iranian Oil Minister Zanganeh reiterated that he fears that OPEC+ could mean the end of the current Middle East led oil producers group. With the incorporation of Russia the power center would clearly move to Riyadh-Moscow.

Looking back at today, a production cut agreement has been reached, and the official statements will follow after the OPEC+ meeting. Brent and WTI prices are expected to inch higher the next couple of days. An internal power struggle, as some expect, inside of OPEC, however, could blow up the current stability with a big bang. An open battle between Tehran and Riyadh, combined with increased military and proxy actions in the Persian Gulf, could be the last drop in the bucket.

Regional military actions against Iran, or more worrying Iranian proxies in Iraq, could effectively reshape the supply situation in crude markets. No reason at present suggests that oil bears can lean back. Global crude supply is more in danger than financial analysts are recognizing. The Iran situation could easily involve Iraq or trade routes at the same time.

via ZeroHedge News https://ift.tt/2KT9cGo Tyler Durden

Hypersonic weapons travel at five times the speed of sound and are designed to hit any target in the world in about an hour. Russia and China have been leading the charge into the development and deployment of this next-generation weapon system.

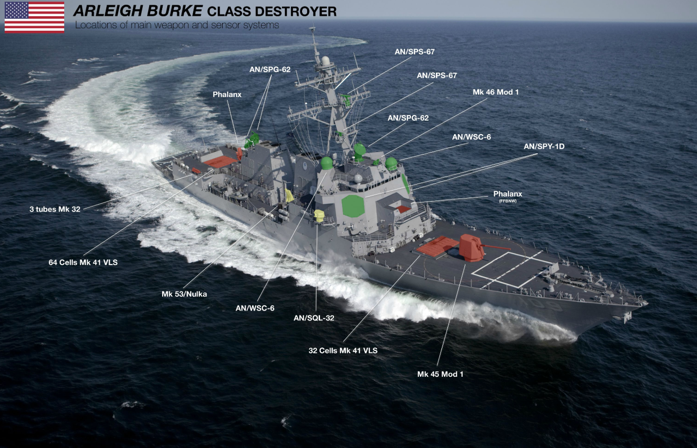

The head of US Naval Sea Systems Command, Vice Adm. Thomas Moore, told an audience last month that Arleigh Burke-class destroyers could be getting a new launcher that would be designed for hypersonic weapons.

“Vertical launch system has been a real game changer for us. We can shoot any number of things out of those launchers,” Moore said.

“We’ll probably change those out and upgrade them for prompt strike weapons down the road.”

Allowing launchers to fire hypersonic missiles on destroyers would considerably increase the effectiveness of the Navy’s strike capabilities. Current weapons on these vessels include Tomahawk Land Attack Missile, is a subsonic missile that can easily be defeated by Russia and China.

There are 66 Arleigh Burke-class destroyers in service with the Navy. In the last 8 to 12 months, the Navy has ramped up its freedom of navigation missions with these ships across the South China Sea, sometimes 12 nautical miles away from China’s militarized islands.

Thomas Callender, a retired submarine officer and analyst with the Heritage Foundation, said the Pentagon had spurred programs to field hypersonic weapons that can strike Russia and China. These weapons would likely be placed on submarines first, then on surface ships.

“They’re looking at putting hypersonics on submarines first because where you can get access,” Callender said. “You can potentially then put them on surface ships as an added capability for them, but the submarines would be the priority for access and the ranges you can achieve.”

The Navy has begun sea trials of the next-generation of guided missile destroyers, called USS Zumwalt (DDG-1000), will likely replace the destroyers in the next five to ten years and has larger missile tubes that could fire hypersonic missiles, former Surface Warfare Director Rear Adm. Ron Boxall told Defense News last year.

Boxall said larger missile tubes allow more missiles to be stored into each cell, but can also be used to store larger hypersonic weapons.

“We are going to need, we expect, space for longer-range missiles,” he said. They are going to be bigger. So the idea that you could make a bigger cell, even if you don’t use it for one big missile, you could use it for multiple missiles — quad-pack, eight-pack, whatever.”

The Navy is working with the Army to develop a booster for hypersonic missiles, and the Army teamed up with the Navy and Air Force to build a hypersonic glider that can outmaneuver the world’s most advanced missile defense shields.

Russia announced the deployment of its Kinzhal hypersonic missile in May.

A December 2018 US Government Accountability Office (GAO) report warned that the current ballistic missile defense system in the US is powerless against hypersonic missiles from Russia and China.

US Air Force Lt. Gen. Samuel Greaves, director of the Missile Defense Agency, said last year that he supports Undersecretary of Defense for Research and Engineering Michael Griffin’s push to develop space-based sensors that would defend the nation from hypersonic attacks by America’s adversaries.

“The hypersonic threat is real, it is not imagination,” Lt. Gen. Greaves explained last summer at the Capitol Hill Club.

Griffin warned that the US could be falling behind in hypersonic arms race.

“In the last year, China has tested more hypersonic weapons than we have in a decade. We’ve got to fix that.”

The newest indication from the US Navy is that hypersonic missiles could be deployed on destroyers and submarines in the early 2020s to counter Russia and China.

via ZeroHedge News https://ift.tt/307LUAc Tyler Durden

Amid reports of severe abuse and neglect in the immigrant detention centers the Trump administration is running, human rights campaigners are planning hundreds of demonstrations on Tuesday to demand the closing of the prisons and the reunification of all families who have been separated by the government.

MoveOn was joined by the ACLU, the Center for Popular Democracy, and other organizations in planning at least 184 events in cities and towns across the country. Beginning at 12:00pm local time and throughout the afternoon, critics of President Donald Trump’s immigration policies will assemble outside their representatives’ offices and at other public venues for the #CloseTheCamps protests.

The organization provided a map on its website of the events that have been planned so far.

“It’s going to take all of us to close the camps,” MoveOn wrote.

The demonstrations are taking place a day after lawmakers including Reps. Alexandria Ocasio-Cortez (D-N.Y.), Ayanna Pressley (D-Mass.), Joaquin Castro (D-Texas), and Rashida Tlaib (D-Mich.) traveled to El Paso, Texas to visit a detention centers in the area.

The delegation reported that the immigrants they spoke with were living in cramped cells where they slept on floors, had not had access to medications or been able to bathe in weeks, were in a state of emotional turmoil, and were exhibiting health problems including hair loss.

“We’re talking systemic cruelty [with] a dehumanizing culture that treats them like animals,” Ocasio-Cortez said of what she witnessed in the camps.

“Horrifically, these conditions aren’t an accident,” wrote MoveOn. “They are the byproduct of an intentional strategy by the Trump administration to terrorize immigrant communities and criminalize immigration—from imprisoning children in inhumane conditions to threatening widespread raids to break up families to covering up reports of immigrants dying in U.S. custody and abuses by ICE and CBP agents.”

MoveOn wrote that the three demands of Tuesday’s protests include cutting off all funding for the arrests and deportations of immigrants as well as closing the camps.

“It’s time to fight back against the racist regime that is causing suffering in our name,” tweeted Act.tv, a progressive activism network supporting the demonstrations. “History will remember those who stood against the atrocities.”

via ZeroHedge News https://ift.tt/2YsXEga Tyler Durden

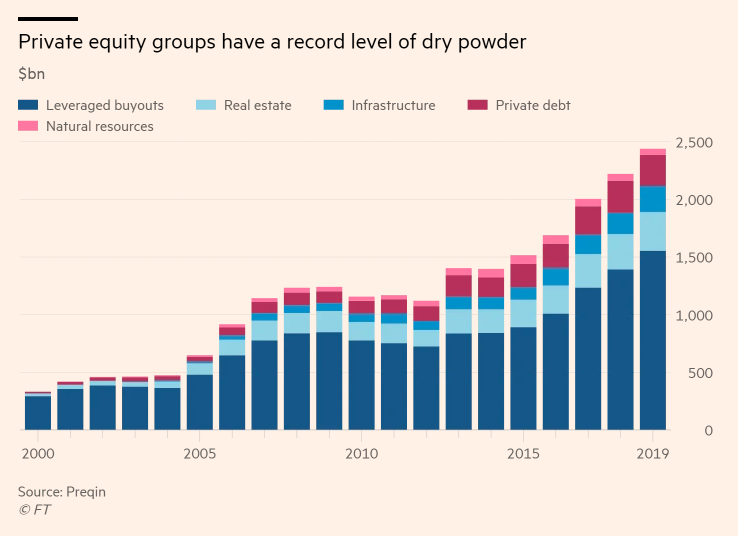

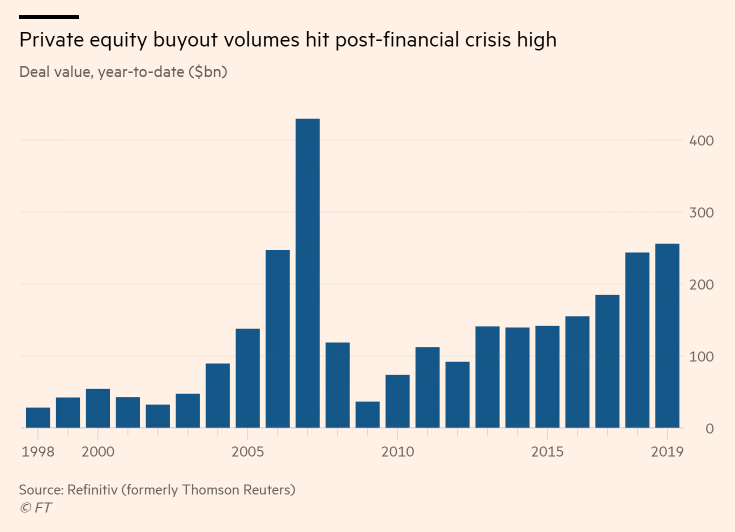

Dealmaking in the world of private equity is at its highest level since the lead up to the global financial crisis, according to FT. Additionally, there appears to be no end in sight to the ongoing “buyout boom”, as PE firms rush to deploy dry powder to the tune of almost $2.5 trillion.

This cash pile is despite the fact that 2019 has been marked by several $10 billion plus megadeals, even amidst volatile financial markets and trade tensions.

The appetite for getting deals done at places like KKR and Blackstone has been stoked by the enormous amount of cash on the sidelines, which has been raised from pension and sovereign wealth funds. When combined with the fact that borrowing costs are still near record lows, the environment for financing takeovers remains ripe.

In addition to the nearly $2.5 trillion of dry powder on the sidelines, tens of billions of dollars are being raised for new funds, giving PE groups even more ammunition.

The value of leveraged buyouts was up to $256 billion in the first six months of 2019, marking the second largest first half on record. It even eclipsed the pace of 2006 when PE groups targeted household names like Harrah’s and Clear Channel. PE dealmaking has accounted for 13% of global acquisition activity this year, the highest since 2013.

Simona Maellare, the global head of financial sponsors at UBS said:

“Deal volume in private equity has been very good. A number of transactions have kept the machine going. I expect the second half of the year will follow the same pace of the first half. Deals can be financed, competition for assets is vivid, everyone has a lot of money.”

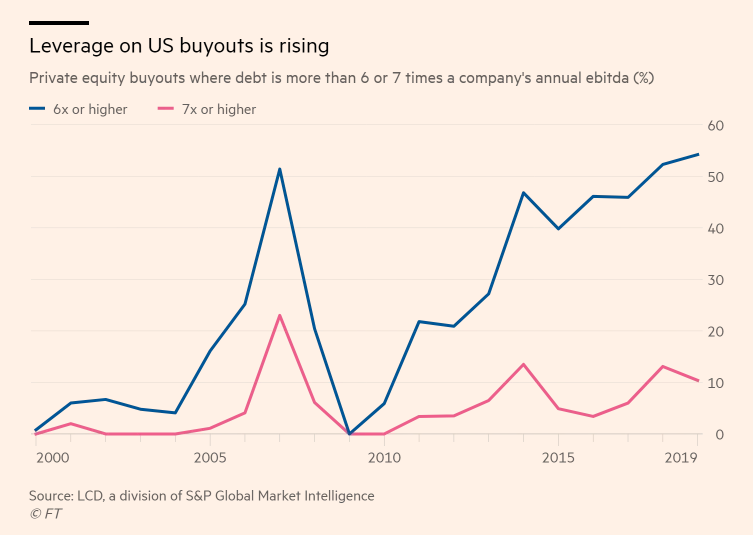

And so, those running leveraged buyout shops are getting more aggressive in their takeover efforts. At the same time, leverage levels are rising as a result of a relaxed attitude from US regulators and takeover sizes growing.

FT notes several deals that have passed $10 billion in size this year:

Those giant transactions include Blackstone’s record $18.7bn takeover of the US warehouses portfolio of Singapore-based GLP, the biggest private real estate deal in history, as well as EQT’s $10.1bn purchase of Nestle’s skincare unit and the $14.3bn sale of fibre optic cable owner Zayo Group to Digital Colony Partners and EQT.

The buyouts come as private equity groups across the globe amass ever-greater firepower in new multibillion-dollar funds. London-based Cinven recently raised €10bn for its latest flagship fund and Boston-based Advent International collected $17.5bn from investors. Luxembourg-based CVC is seeking to raise more than €18bn for what would be Europe’s largest ever private equity fund at launch next year. Its rival EQT is looking to raise about €14bn by 2020.

Rob Pulford, Goldman Sachs’ head of financial and strategic investors group for Europe, the Middle East and Africa commented: “There has been a significant amount of fundraising among the big private equity groups in the past two years. Several have deployed their new funds quickly and are now getting ready to come back to market again, there is no let-up in the pace of fundraising.”

via ZeroHedge News https://ift.tt/2Ysqihn Tyler Durden

“Such is the belief currently which is being driven primarily by the ‘Pavlovian’ response of a more ‘accommodative’ Federal Reserve which is expected to cut rates sharply by the end of this year. It is also the ‘hope’ there will be a resolution to the ongoing ‘trade war’ with China at the G-20 Summit next week.”

“As we suggested previously, the most likely outcome was a truce…but no deal.

While the markets will likely react positively next week to the news that ‘talks will continue,’ the impact of existing tariffs from both the U.S. and China continue to weigh on domestic firms and consumers.

More importantly, while the continued ‘jawboning’ may keep ‘hope alive’ for investors temporarily, these two countries have been ‘talking’ for over a year with little real progress to show for it outside of superficial agreements.

Importantly, we have noted that Trump would eventually ‘cave’ into the pressure from the impact of the ‘trade war’ he started. This was evident in this weekend’s agreement.

By agreeing to continue talks without imposing more tariffs on China, China gains ample running room to continue to adjust for current tariffs to lessen their impact. More importantly, Trump gave up a major bargaining chip – Huawei.”

So, yes, the market rallied on Monday given “relief” that no NEW tariffs will be imposed. However, such does not counter-act the negative impact from the existing tariffs which continue to weigh on both producers and consumers.

Secondly, the agreement to temporarily put the “trade war” on hold also takes the pressure off of the Federal Reserve to cut rates in July. If the employment report on Friday keeps the unemployment rate at historic lows, and shows growth of around 150,000 jobs, as is currently expected, there is a rising probability the Fed will remain on hold.

This is not what the markets are betting on currently.

As I noted last week, assumptions are always a dangerous thing as markets have a nasty habit of doing exactly the opposite of what the masses expect.

Nonetheless, the market rally on Monday was expected and followed along with BofA’s recent analysis:

“Of these 4, two are most remarkable: the best/best and the worst/worst cases. The first one sees a Dovish Fed statement, coupled with a G-20 deal, which according to BofA will send the S&P > 3000, and the 10Y yield to 2.00%, while the worst possible outcome would be if there is a 1) a hawkish Fed surprise and 2) no Deal at the G-20, which would send the S&P below 2,650, or potentially resulting in a 12% drop in the market, while sending 10Y yields to 1.50%and pushing gold above its 5 year breakout zone as the VIX surges.”

Hartnett was correct in his outlook with the “best” possible of outcomes.

Still A Sellable Rally

While the current breakout to new highs is indeed bullish, it is important to note the entirety of the “June rally,” which was proclaimed the best in 80-years, barely recouped what was lost in just the month of May.

Importantly, the market, which was deeply oversold at the beginning of June, and formed the basis of our “sellable rally” call, is now back to extremely overbought. Such suggests limited upside from current levels. The chart below shows that previous test of multiple support levels, and the rally back to overhead resistance, which we are once again challenging.

As noted previously, while there is a “rush” to bid up equities due to recent “talk” from the White House and the Fed, the reality is that nothing has really changed.

A Trade deal wasn’t reached and China will continue to refuse to give in to demands for economic reform. Additional tariffs are coming by the end of the summer.

Existing tariffs, which were just ratcheted up at the beginning of June, have not been fully recognized in the economy as of yet. More “pain” is coming by the end of the summer.

While the markets think that Trump has the “upper hand,” it is China for now. They can hold out to economic pressures far longer than Trump as Xi is not facing re-election. China knows this.

The Fed has now started to recognize their “independence” has been threatened. Look to Powell to flex his muscles a bit in July and NOT cut rates particularly if the June jobs report is moderately strong.

The Fed is still reducing its balance sheet.

The point is there are more than a few outcomes which could disappoint the financial markets and why this remains a “sellable rally” for now.

But aside from the technical underpinnings, which remain moderately unfavorable for higher highs currently, there is also a deteriorating fundamental backdrop.

Negative Earnings Guidance

I have been noting for the last several quarters, the consistent and large decline in forward earnings expectations. From our last analysis:

“As of the end of the Q4-2018 reporting period, guess where we are? Exactly 11% lower than where we started which, as stated then, has effectively wiped out all the benefit from the tax cuts.”

“Importantly, the estimates for the end of 2019 are still too high and will need to revised lower over the next couple of quarters as economic growth remains materially weaker. The burgeoning debts and deficits, corporate and household leverage, and slower job growth will ensure slower growth into year end.”

That expected reduction in both 2019 and 2020 estimates is underway. As John Butters ofFactsetrecently penned:

“Heading into the end of the second quarter, 113 S&P 500 companies have issued EPS guidance for the quarter. Of these 113 companies, 87 have issued negative EPS guidance and 26 companies have issued positive EPS guidance.

The number of companies issuing negative EPS for Q2 is above the five-year average of 74. In fact, if 87 is the final number for the second quarter, it will mark the second highest number of S&P 500 companies issuing negative EPS guidance for a quarter since FactSet began tracking this data in 2006 (trailing only Q1 2016 at 92).”

“What is driving the unusually high number of S&P 500 companies issuing negative EPS guidance for the second quarter?

At the sector level, seven of the 11 sectors have seen more companies issue negative EPS guidance for Q2 2019 relative to their five-year averages. However, the Information Technology and Health Care sectors are the largest contributors to the overall increase in the number of S&P 500 companies issuing negative EPS guidance for Q2 relative to the five-year average.”

Why is this happening?

“It’s the economy, stupid.”

As economic growth slows, companies have to begin to adjust for lower levels of consumption. This initially shows up in things that under the immediate control of corporate decision makers like unspent capital investment. It’s easy to shelve a project, or development, that money was committed to but not yet spent. As Chetan Ahya, Morgan Stanley Chief Economist recently stated (via Zerohedge):

“…It was clear that the global capex cycle had ground to a halt. Capital goods imports, a capex proxy, began their descent in mid-2018, when trade tensions first re-emerged. In July 2018, they were tracking at 18%Y on a three-month moving average basis but plummeted to 2%Y in January 2019 and an estimated -3%Y in May 2019. In aggregate, private fixed capital formation (investments in fixed assets) in the G4 and BRIC economies fell from a peak of 4.7%Y in 1Q18 to just 2.8%Y in 1Q19.”

The next decline occurs in how companies “frame” their outlook. Are they more optimistic, or less?

“Corporate sentiment has also declined to multi-year lows. Global PMIs for May fell in broad-based fashion, with only about one-third of the countries we track reporting a PMI above the 50 expansion threshold. In the US, our Morgan Stanley Business Conditions Index recorded its largest one-month decline ever, plunging to a level not seen since June 2008. Other business sentiment gauges, such as the regional Fed and German Ifo and ZEW surveys for the month of June, paint a fairly bleak picture too. What’s more, consumer sentiment is also starting to sour, with the Conference Board’s Consumer Confidence Index for June falling to the lowest point since September 2017.

But with stock prices at all-time highs, why worry about these risks?

A key reason why we worry about downside risks is that the adverse impact of trade tensions is non-linear. As earnings growth slows and uncertainty and costs rise, the levered corporate sector will face tightening financial conditions. Given higher corporate leverage, this will probably be most pronounced in the US, particularly for companies with weaker balance sheets. Defaults could accelerate, bringing corporate credit risks to the fore, thus amplifying the initial trade shock with even tighter financial conditions, which could impair lending, weaken confidence further and exacerbate the slowdown in growth. Rekindling animal spirits will not be easy.”

The Last Sign

These are not trivial issues for investors. While the market will be focused on the employment number on Friday, this is probably one of the “worst” indicators to look at due to its “lag” to the rest of the important fundamental and economic factors.

Why? Because companies are “last to hire, last to fire.”

Employees are expensive to hire, train, and maintain. Good talent is extremely hard to replace. So, companies are slow to hire, due to the cost, and slow to fire because they don’t want to give up good talent to potential competitors. When unemployment, along with jobless claims, do begin to tick up, that is generally the last sign before a recession sets in.

However, since interest rates are a reflection of underlying economic strength, it is not surprising there is a decent relationship between sharp declines in interest rates and employment. The chart below is the annual rate of change in both rates and employment.

Don’t be surprised to see weaker employment numbers in the months ahead. As Bloomberg also noted:

“Falling bond yields have been the big surprise of 2019 so far and there’s an excellent chance they will grind lower in the second half — and take stocks with them — as weak growth spurs global monetary easing.

Given how tough it has been to forecast bond yields, getting that call right for the rest of the year is key.

A reminder of how difficult that can be comes from San Francisco Fed President Mary Daly. Twice last week she said it’s very hard to say what the central bank should do, including comments that she’s unsure ‘whether interest rates will be lower a year from now.’

Surveying the outlooks our team came up with at the start of 2019, it’s clear our biggest misses were all in bonds.

The same goes for those readers who took part in our surveys. Treasury yields finished June more than 100 bps below the consensus for end-2019, while bunds were ~75 bps lower and Italian yields a whopping 105. Bond analysts were also far too bearish.”

The problem with equities at all-time highs, with yields and economic growth declining sharply, is that it has consistently led to terrible outcomes for equities, and not the other way around.

Bloomberg came to the correct conclusion:

“What looks more likely is that equities ultimately succumb to the macro logic that has fueled this year’s bond rally.”

via ZeroHedge News https://ift.tt/2Jj9wuV Tyler Durden

Following through on threats to hit more European imports with tariffs seems unlikely to change the fact that most Americans disagree with President Donald Trump’s trade war.

If anything, higher import taxes on items like Scotch whisky, French cheeses, and Italian pasta will only add to domestic opposition to Trump’s trade policies. What is the president going to say: that Scotch should be made in America?

On Monday, the Office of the U.S. Trade Representative announced plans to consider tariffs on 89 European-made items worth an estimated $4 billion annually. Those will be added to a list of proposed tariffs on European Union (E.U.) imports that the Trump administration unveiled in April. Together, the two lists represent items worth an estimated $21 billion annually.

This latest U.S.-E.U. trade spat is effectively a fight between Boeing, the American-based airplane manufacturer, and its European-based rival, Airbus. Both are heavily subsidized by their respective governments, and both have been suing one another at the World Trade Organization for years over claims that the other is unfairly helped by that corporate welfare. Trump administration officials have stressed that the Boeing-Airbus fight is wholly separate from the Trump administration’s other trade policies, which have included other threats to impose tariffs on European-made goods, including cars.

But none other than Trump himself has conflated the two, tweeting in April that Airbus is one example of how the E.U. has “taken advantage of the United States” and promising that “it will soon stop.” For the general public, too, drawing a distinction between the different actions is surely rather difficult. The White House’s willingness to turn to tariffs as a magical solution to complex or imaginary problems—from China’s theft of intellectual property, to migrants crossing Mexico to reach to the U.S., to the national security risk presented by Toyotas—makes it more difficult to make the case that tariffs are actually justified in a specific situation.

And Americans are growing weary of the trade war, new polling suggests.

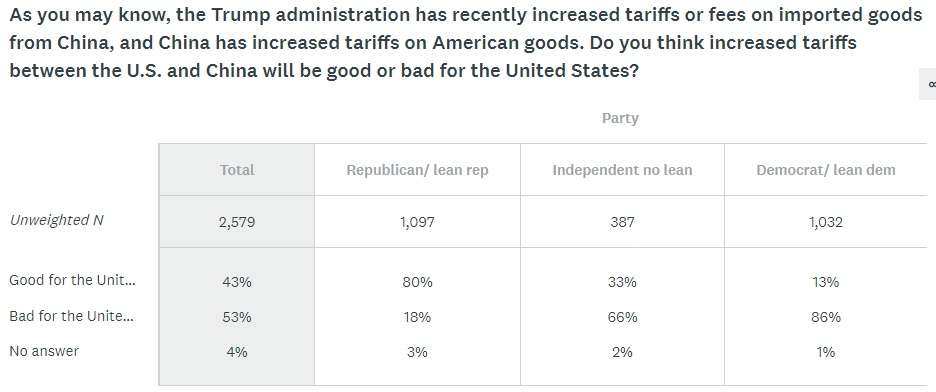

A New York Times/Survey Monkey poll released Sunday shows that 68 percent of respondents—including a majority of Republicans—say Trump’s trade policies will raise prices.

A clear majority—53 percent—say Trump’s Chinese tariffs will be “bad” for the United States, while only 43 percent believe they will benefit the country.

The poll also found that Republicans, no surprise, are far more likely to believe tariffs will create more domestic jobs (75 percent say they will), while only 14 percent of Democrats agree. Those types of questions used to be far less partisan, but Trump seems to have changed that—although trade policy “continues to rank low among the issues that voters are focused on,” the Times notes.

Even so, opposition to tariffs among Democrats and independent voters would seem to be a political liability for Trump. After meetings between Trump and Chinese President Xi Jinping at this week’s G-20 summit again failed to result in a trade deal, Trump could face more domestic political scrutiny over policies that have cost consumers and businesses without much to show for it.

Democrats may have a hard time taking advantage of that liability in next year’s election, however, because leading candidates like Sens. Bernie Sanders (I–Vt.) and Elizabeth Warren (D–Mass.) support protectionist trade policies too. Warren, in particular, has indicated that she thinks Trump should go further in erecting barriers to trade.

Not all the Democratic presidential candidates share that view, thankfully. In last week’s debate, Andrew Yang and Pete Buttigieg made strong, if brief, attacks on Trump’s tariffs. “Manufacturers, and especially soy farmers, are hurting. Tariffs are taxes,” Buttigieg said before turning to attack what he said was Trump’s overblown concern with trade deficits.

Unfortunately, the moderators didn’t ask Warren or Sanders any questions on trade. But if polls continue to show that most Americans are opposed to Trump’s protectionism, it will provide a political opportunity for Democrats to exploit and good fodder for voters trying to sort out differences among the many, many candidates trying to unseat Trump.

In the meantime, slapping more tariffs on European imports is unlikely to convince Americans that Trump’s trade policies are working. Artificially inflating the price of a bottle of Scotch or a hunk of fancy cheese won’t bring those jobs to the United States—and setting those tariffs in order to tip the scales toward the corporate welfare hogs at Boeing isn’t a great look, either.

from Latest – Reason.com https://ift.tt/2Jhns8F

via IFTTT

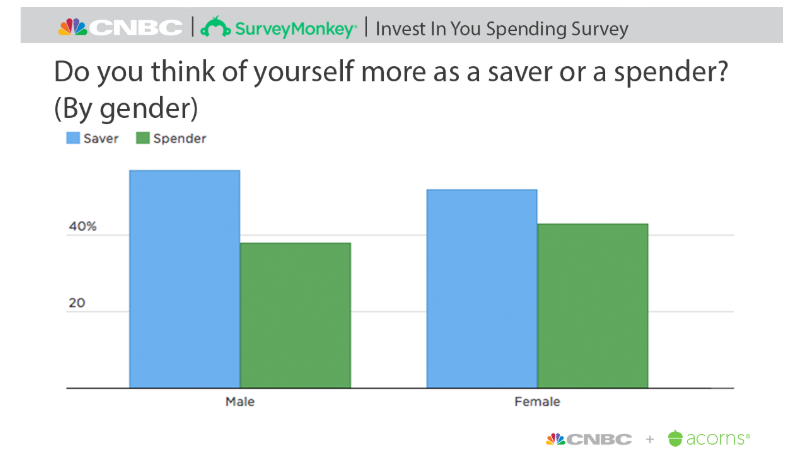

A third of all Americans have cut their spending this year, according to a new survey by CNBC. And for a country indoctrinated by a system that encourages spending and abhors savings, readers may be surprised to learn that a majority of the respondents, that 54% of survey respondents still described themselves as savers.

The survey polled men and women across the country, and looked at changes in people’s money behaviors. Many people are taking a critical look at their spending and preparing for “what ifs”, the survey concluded.

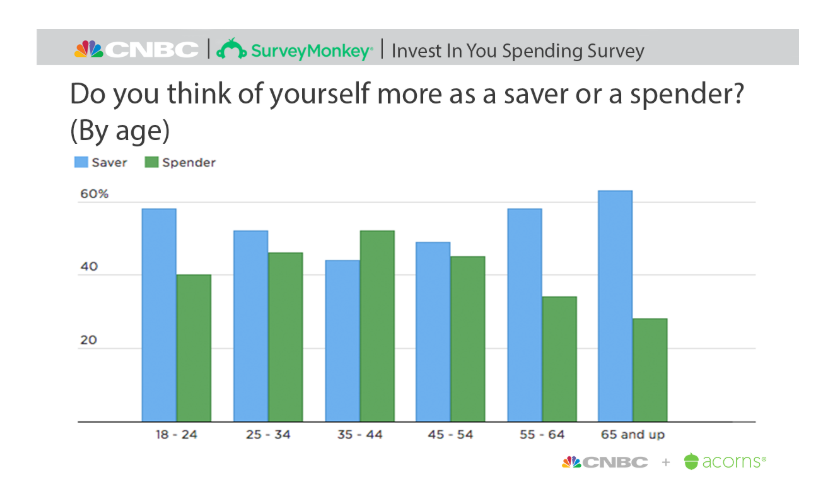

Spending versus saving habits were relatively equal across age groups. The 35 to 44-year-old group showed higher levels of spending, which then moved back toward saving as people neared retirement. 63% of seniors described themselves as savers and 28% described themselves as spenders.

And regardless of demographic, a third of Americans say that they’ve cut spending over the last year. They have done this as a result of a loss of household income, new debt, fears of recessions and medical expenses.

Most of the people spending less did so due to job losses, followed by people that took on new debt. It’s also worth noting that the number of Americans filing for unemployment rose more than expected last week. African-American respondents were far likelier to cut spending at 43%. Divorced men were the only group that came close, at 39%. Unemployment could be to blame again, as the survey found that twice as many black respondents as white pointed to “loss of job” as the reason that they were spending less.

Laura Wronski, chief researcher at SurveyMonkey in San Mateo, California said: “This ranks high for everyone, and much more so for blacks. Jobs and the economy is the No. 1 issue for blacks by a wider margin”, which is strange considering the BLS has been reporting near record-low unemployment for African-Americans.

Marc Morial, president and CEO of the National Urban League says that jobs remain a major issue: “When you look at national statistics, while unemployment numbers are at an all-time low, unemployment is still persistently higher among blacks than whites. If you lose your job, you have to make some hard trade-offs in your life.”

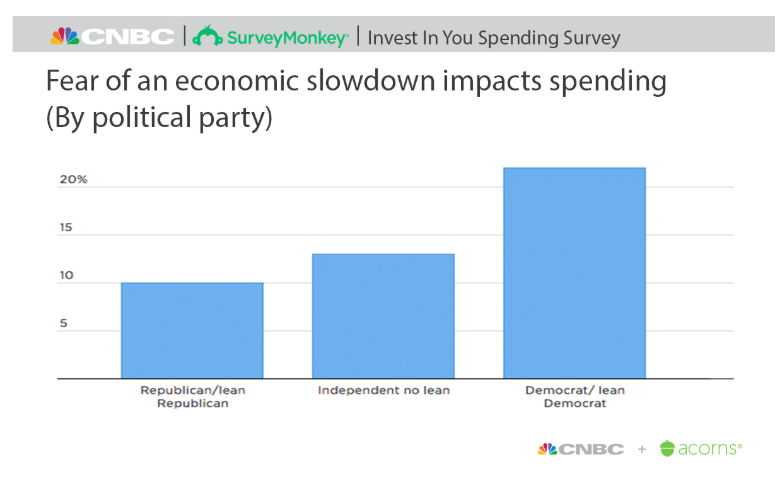

From a political standpoint, two times as many Democrats as Republicans said they’d cut spending due to anxiety over the economy.

Former FDIC chair Sheila Bair said: “I’m for anything that increases financial resilience. If you’re trying to do forecasting, it’s better to be on the conservative side and increase your cash reserves. Where’s the harm in that? Trying to predict the direction of the economy, though, might be a waste of resources. It’s like trying to time the stock market. You’ll never get it right.”

Republicans, on the other hand, were likelier than Democrats to say their confidence in the economy led them to spend more. Overall, however, Democrats were more likely to say they were spending more.

And impulse spending, believe it or not, is an issue that affects both genders. In fact, 23% of men say they’ve spent more than $100 the last time they made an impulse buy, versus 16% of women.

On the other hand, slightly less than a quarter of respondents who increased their spending said it was due to getting a better paying job. The top expense of those polled was delivery and take out meals:

Takeout or delivery meals were the top expense, with 28% of the general population. But those who identify themselves as spenders are far more likely than savers to say they spend $200 a month on convenience meals.

People seem to have their spending under control, Wronski said, noting the survey didn’t show much spending on alcohol or tobacco. “People are aware of the amount of money they’re spending and trying to spend it responsibly.”

In addition to job loss, the widening inequality gap is likely contributing to Americans tightening their financial belts, as well. Gabriel Zucman, an economist at the University of California, Berkeley told Tuscon.com: “The recovery has been very disappointing from the standpoint of inequality.”

More than 33% of the household wealth gain as a result of the “recovery” – amounting to $16.2 trillion— went to the wealthiest 1%, figures from the Federal Reserve show. In addition, the homeownership rate fell to about 60% in 2016 from roughly 70% in 2004. And despite the market nearly quadrupling during the recovery, the proportion of middle-income households that own stock has actually declined.

Lael Brainard, a member of the Federal Reserve’s Board of Governors said in May: “Many households find it challenging to make key middle-class investments because incomes at the middle are not keeping up with the rising costs of education and homeownership, and it is difficult to save enough.”

And consistent with the results from the CNBC survey, data shows that the widening inequality gap has disproportionately affected African Americans:

As financial inequalities have widened over the past decade, racial disparities in wealth have worsened, too. The typical wealth for a white household is $171,000 — nearly 10 times that for African-Americans. That’s up from seven times before the housing bubble, and it primarily reflects sharp losses in housing wealth for blacks. The African-American homeownership rate fell to a record low in the first three months of this year.

via ZeroHedge News https://ift.tt/2XKvQa2 Tyler Durden

Following through on threats to hit more European imports with tariffs seems unlikely to change the fact that most Americans disagree with President Donald Trump’s trade war.

If anything, higher import taxes on items like Scotch whisky, French cheeses, and Italian pasta will only add to domestic opposition to Trump’s trade policies. What is the president going to say: that Scotch should be made in America?

On Monday, the Office of the U.S. Trade Representative announced plans to consider tariffs on 89 European-made items worth an estimated $4 billion annually. Those will be added to a list of proposed tariffs on European Union (E.U.) imports that the Trump administration unveiled in April. Together, the two lists represent items worth an estimated $21 billion annually.

This latest U.S.-E.U. trade spat is effectively a fight between Boeing, the American-based airplane manufacturer, and its European-based rival, Airbus. Both are heavily subsidized by their respective governments, and both have been suing one another at the World Trade Organization for years over claims that the other is unfairly helped by that corporate welfare. Trump administration officials have stressed that the Boeing-Airbus fight is wholly separate from the Trump administration’s other trade policies, which have included other threats to impose tariffs on European-made goods, including cars.

But none other than Trump himself has conflated the two, tweeting in April that Airbus is one example of how the E.U. has “taken advantage of the United States” and promising that “it will soon stop.” For the general public, too, drawing a distinction between the different actions is surely rather difficult. The White House’s willingness to turn to tariffs as a magical solution to complex or imaginary problems—from China’s theft of intellectual property, to migrants crossing Mexico to reach to the U.S., to the national security risk presented by Toyotas—makes it more difficult to make the case that tariffs are actually justified in a specific situation.

And Americans are growing weary of the trade war, new polling suggests.

A New York Times/Survey Monkey poll released Sunday shows that 68 percent of respondents—including a majority of Republicans—say Trump’s trade policies will raise prices.

A clear majority—53 percent—say Trump’s Chinese tariffs will be “bad” for the United States, while only 43 percent believe they will benefit the country.

The poll also found that Republicans, no surprise, are far more likely to believe tariffs will create more domestic jobs (75 percent say they will), while only 14 percent of Democrats agree. Those types of questions used to be far less partisan, but Trump seems to have changed that—although trade policy “continues to rank low among the issues that voters are focused on,” the Times notes.

Even so, opposition to tariffs among Democrats and independent voters would seem to be a political liability for Trump. After meetings between Trump and Chinese President Xi Jinping at this week’s G-20 summit again failed to result in a trade deal, Trump could face more domestic political scrutiny over policies that have cost consumers and businesses without much to show for it.

Democrats may have a hard time taking advantage of that liability in next year’s election, however, because leading candidates like Sens. Bernie Sanders (I–Vt.) and Elizabeth Warren (D–Mass.) support protectionist trade policies too. Warren, in particular, has indicated that she thinks Trump should go further in erecting barriers to trade.

Not all the Democratic presidential candidates share that view, thankfully. In last week’s debate, Andrew Yang and Pete Buttigieg made strong, if brief, attacks on Trump’s tariffs. “Manufacturers, and especially soy farmers, are hurting. Tariffs are taxes,” Buttigieg said before turning to attack what he said was Trump’s overblown concern with trade deficits.

Unfortunately, the moderators didn’t ask Warren or Sanders any questions on trade. But if polls continue to show that most Americans are opposed to Trump’s protectionism, it will provide a political opportunity for Democrats to exploit and good fodder for voters trying to sort out differences among the many, many candidates trying to unseat Trump.

In the meantime, slapping more tariffs on European imports is unlikely to convince Americans that Trump’s trade policies are working. Artificially inflating the price of a bottle of Scotch or a hunk of fancy cheese won’t bring those jobs to the United States—and setting those tariffs in order to tip the scales toward the corporate welfare hogs at Boeing isn’t a great look, either.

from Latest – Reason.com https://ift.tt/2Jhns8F

via IFTTT