Sixteen US Marines stationed at Camp Pendleton in California were arrested on a series of charges ranging from human smuggling to drug-related offenses, according to Fox News, citing officials.

The U.S. Marine Corps said in a news release that 16 Marines were arrested during a Battalion formation at Camp Pendleton in California.

“Information gained from a previous human smuggling investigation precipitated the arrests,” USMC officials said in a statement. –Fox News

Additionally, eight more Marines were “taken aside” by investigators who want to know their level of involvement in alleged drug offenses unrelated to Thursday’s arrests, according to the report.

“1st Marine Division is committed to justice and the rule of law, and we will continue to fully cooperate with Naval Criminal Investigative Service (NCIS) on this matter,” reads a statement from officials. “Any Marines found to be in connection with these alleged activities will be questioned and handled accordingly with respect to due process.”

This isn’t the first human smuggling arrest at Camp Pendleton, where two Marines were taken into custody on suspicion of transporting illegal immigrants for money, according to Fox 5.

Byron Darnell Law II and David Javier Salazar-Quintero were arrested near Jacumba Hot Springs in East County on July 3. Each Marine faces one felony count of seeking monetary compensation for moving unauthorized immigrants into the country after they had crossed the border, the San Diego Union-Tribune reported.

Three unauthorized immigrants were with Law and Salazar-Quintero at the time of their arrest. It was unclear how many other unauthorized immigrants Law and Salazar-Quintero had moved previously, though both men allegedly admitted to their involvement in previous transports and said another person had also been involved in the operations. –Fox 5

According to the complaint, Salazar-Qhintero admitted to picking up immigrants near Jacumba Hot Springs at least four times.

via ZeroHedge News https://ift.tt/2Mgm1u8 Tyler Durden

Gold’s dramatic move above $1400 has caught the investment establishment by surprise. Physical gold ETFs, as a proxy for direct portfolio investment, amount to only 0.05% of the estimated $250 trillion of global investment values. As well as being badly wrongfooted, investment managers have little understanding of the role of gold as money, believing it to have no role in the monetary system. They will have to undergo a rapid re-education. This article addresses their common misconceptions.

Introduction

One month ago, gold made a dramatic move above a three-year consolidation (delineated by the pecked lines in Chart 1), confirming for technical analysts that a bull market in gold dating from the December 2015 low at $1,050 is alive and well. Chart 1 shows that a basing process has actually been in train for over six years, highlighted by the lower rectangular box.

Technically, the post-Lehman crisis bull market, when gold more than doubled, was ripe for a set-back. After peaking at $1920 intraday in September 2011, the Cyprus banking crisis in 2012 failed to collapse the Eurosystem and the gold price fell heavily. The topping-out process is highlighted by the upper smaller box in the chart. But that is now irrelevant. What is relevant is gold appears to be breaking out of a multiyear base, solid enough to offer the prospect of a potentially strong bull market in the dollar price of gold.

For trend-chasing investors who form a large majority by sheer weight of managed money, this is the primary consideration. They will have ignored the debate about the weaknesses of fiat currencies, geopolitical tensions with the Asian superpowers and America’s acts of trade immolation. That was always going to be the case until such time as gold broke convincingly through the $1350 technical price ceiling. With the price now establishing itself at over $1400, an appraisal of the reasoning behind gold’s breakout is timely for these investors.

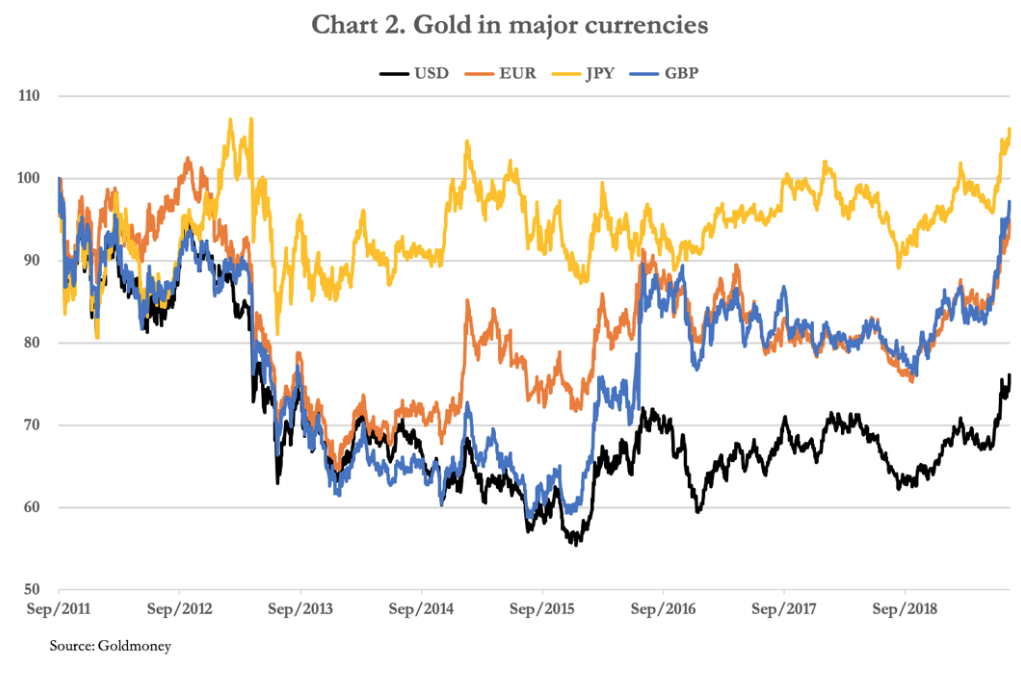

The dollar price is no more than a headline indicator for investors whose portfolio performance is not measured in dollars. Gold’s performance measured in other currencies has been far better. Since the price peak in September 2011, by mid-December 2015 the dollar price of gold had lost 45% of its value and has recovered to a net loss of only 24%. The gold price measured in the other major three currencies has performed significantly better, with the price in Japanese yen even higher now than it was at the time of the dollar’s 2011 all-time high. This is shown in Chart 2.

Furthermore, while the dollar price has only just caught the attention of mainstream dollar investors, residents of Euroland and Britain have seen gold in euros and sterling recover to within six and four per cent of the 2011 high respectively. Nearly three months ago, it was said that the gold price in 72 currencies stood at all-time highs. Given that emerging market and developing economy currencies tend to be weaker than the majors it is probably true.

Those who watch dollar headlines before jumping on a trend are late arrivals to a party already in full swing. Since the dollar price of gold bottomed in late-2015, the sterling price aided by the Brexit debacle has risen 63%, proving to be an excellent hedge against a falling pound. Gold priced in euros is up 45% from its lowest point, proving the wisdom of ordinary Germans who are the largest group of gold buyers in the Eurozone.

At a time of zero and negative interest rates and bond yields, these returns are doubly impressive. But there are remarkably few bulls on board with reasonable portfolio exposure. According to the World Gold Council, at end-June gold ETFs held 2,548 tonnes of bullion worth $115bn at current prices. While there are other gold-related regulated investments and derivatives, this feedstock of the raw stuff is tiny compared with the total value of global portfolio assets, which is probably in excess of $250 trillion. Given that nowhere is physical bullion a regulated investment, direct holdings of vaulted investment bullion are unlikely to be significant in this context. Putting physical gold being held as an unrecorded asset to one side, to find physical gold in investment portfolios you have to dig very deep. On these figures, ETF bullion represents only 0.046% of estimated global portfolio values.

Estimates of physical exposure in portfolios should not be taken too literally, but from these estimates we can see that for all practical purposes gold’s breakout has left the trend-chasing establishment with almost nothing. For this reason, there is now likely to be a scramble to understand why gold has broken out. Portfolio managers will be keenly aware they are likely to come under pressure from clients to participate and will want to have answers.

This article is addressed to the portfolio managers and investors who are in the unfortunate position of not yet owning any gold or find themselves underweight in gold-related investments and are considering what to do about it. But first we must dispel some of the common myths about the role of gold, so we can approach the subject with clarity.

Myths about gold as an investment medium

On Monday, Tom Stevenson, an investment director at Fidelity International, in his regular column in The Daily Telegraph wrote an article headed “Gold’s lustre may help hedge your bets if markets head south.” For a senior portfolio manager to recommend some portfolio exposure to gold supports this article’s contention that investment managers have noted the trend, but it appeared to present Stevenson with some difficulties arising from some common fallacies.

As a starting point, his article provides us with material to work with. His bias is clearly anti-gold. But his concern the gold price is telling him something important is evident from his headline, and he then enters into a mea culpa as to why gold should not be considered a normal investment. Stevenson trots out the usual anti-gold-bug stuff, claiming gold being only of interest to the kind of people who stockpile tinned goods and Kalashnikovs. But he also lists some of the alleged disadvantages of gold, commonly believed in the investment management industry.

Stevenson states it pays no income, is expensive to store and insure, it has no intrinsic value, no real use beyond looking pretty, it’s extremely volatile, it’s a greater-fool investment requiring another buyer to believe it’s going higher, and it’s value was higher forty years ago in real inflation-adjusted terms. We shall address all his points.

Before doing so, we must set one thing straight. What he didn’t mention is the common belief in investment management circles that gold is no longer money. We shall start with this issue, given its overriding importance, before addressing Stevenson’s other presumptions.

Myth 1. Gold is no longer money

The first step towards understanding the role of gold is to recognise it is money. It still competes with today’s fiat currencies as money and predates them by many millennia. Over the millennia there have been many other forms of money tried, and apart from silver, they have always failed. The gradual emergence of unbacked fiat currencies, particularly from the 1920s onwards, is the only monetary challenge to gold’s long history as money that has yet to fail.

With today’s state-issued currencies unbacked by anything other than public credibility in their issuers’ standing, the US dollar has loosely replaced gold as the principal currency against which all the other currencies are measured. This was by design: since 1971 the US Treasury has embarked on a campaign to deny gold’s role as money, promoting the dollar as the reserve currency instead.

In the past, when a state-issued currency was freely convertible into gold, its currency circulated as a gold substitute. Today, no currency is convertible into gold, so gold does not circulate as money even indirectly. By insisting its state-issued currency is used for tax payments, and therefore is the basis for everyone’s accounting, a government ensures it is the circulating medium. But another important function of money is as a store of value, preserving it for the lapse of time between it being earned and finally spent, and in this function state-issued currency fails.

The continual loss of purchasing power in fiat currencies since gold backing was removed has rendered them unsuitable as a savings medium. Only gold retains sound-money attributes and is still valued as such in a number of populous nations. In fact, the naysayers who claim gold is no longer money are only a very small proportion of the world’s population, given the general public as a whole in the advanced nations have no definite view on the matter. It is a common error to assume neo-Keynesian economists speak for entire populations.

For ordinary people, gold will become an increasingly important refuge, given the prospect of an acceleration in monetary inflation as the world tips into recession. With government spending already out of control, governments are relaxing budget discipline even further while promising greater spending. Consequently, the monetary quality which will become more valued is the ability to preserve value and it is upon this quality that gold markets are beginning to place a premium.

That is why gold is being valued as a more stable form of money, despite the fact it is not commonly found in general circulation. However, in the growing certainty that fiat currencies will die, gold can and will rapidly return to circulate as money.

We can now address Stevenson’s unfounded presumptions.

Myth 2. Gold doesn’t pay interest

Only hoarded gold, like physical currency cash, does not pay interest. Gold is loaned and borrowed for interest, just like fiat currencies. When markets are acting freely without state interventions and distortions, gold should have a lower originary interest rate than a fiat currency for the same loan term, because it is no one’s liability, unlike a fiat currency. The originary rate is shorn of all loan risks other than a pure time-preference value.

Today’s bullion market sets gold’s interest rate in the context of dollar interest rates. In London’s forward market, gold’s interest rate is termed its lease rate, which is derived from the gold forward rate (GOFO) and the London dollar interbank offered rate. GOFO is the rate at which a bullion bank is prepared to lend gold to another bullion bank on a swap basis against US dollars. The notional formula is the gold lease rate equals LIBOR minus GOFO.

In the days of the gold standard, when currencies were accepted as gold substitutes, the originary interest rate was that of gold. While it was impossible to quantify, because actual loan rates depended on borrower risk, the originary rate, as described above, was set by time preference. Expressed as an annualised interest rate, gold’s originary rate was normally in the order of two or three per cent.

Compared with today’s unbacked currencies, gold’s interest rate was very stable, but it was not immune to changes in its purchasing power. There were some fluctuations in supply, such as those caused by the Californian and South African mining booms. The rate of technological progress, to the extent productivity was advanced, lowering the general level of prices over time was also an important factor, which meant that a saver would experience the purchasing power of savings increase. For this reason, savers were prepared over time to accept a lower rate of interest on gold than would otherwise be the case.

The modern mantra that gold does not pay interest is simply untrue.

Myth 3. Gold is expensive to store and insure

This is untrue. At Goldmoney, fully insured annual storage fees for gold in LBMA approved vaults range between 0.01% and 0.018%.[iii] ETFs and mutual funds charge far higher rates for management, administration and custody. There is ample margin for Fidelity to pay Goldmoney’s vaulting and insurance fees, and for Fidelity to enjoy a substantial mark-up within its existing fee structure. We won’t hold our breath.

Myth 4. Gold has no intrinsic value

From Wikipedia, the definition of intrinsic value is as follows:

“In finance, intrinsic value refers to the value of a company, stock, currency or product determined through fundamental analysis without reference to its market value. It is also frequently called fundamental value.”

It is clear from this definition that the financial concept of intrinsic value depends on the income stream generated by an asset. In the case of a currency, this can only relate to the interest it earns for a lender. Like a currency, gold pays interest on being loaned out, so it must have an intrinsic value.

The concept of intrinsic value applied to money is little more than a red herring. But if we are to pursue it, we should observe that the suppression of interest rates reduces the intrinsic value of a currency, that zero interest rates remove it altogether, and negative rates give rise to negative intrinsic values.

On this basis, gold will always have an intrinsic value, while unbacked currencies in the current financial climate often do not. Gold clearly wins over today’s currencies on this basis.

Myth 5. Gold has no real use beyond looking pretty

We can all agree gold looks pretty. But it is also incredibly durable. Gold’s physical qualities and its rarity have made it the money of choice for diverse people and their cultures throughout the long history of mankind’s economic cooperation.

For Stevenson to imply that gold is only ornamental infers that the marginal price of gold is set by its supply and demand for that function. This is not the case. Gold is demanded in Asia for its property as a readily realisable store of value. It is a mistake to think diverse Asian communities, including the poorest in society, waste significant sums of their governments’ currencies on the frivolous function of making their women look pretty.

To have one’s accumulated wealth held beyond the control of government has proved to be a wise decision for the middle and lower classes in populous countries such as India, as well as all the other nations between Turkey and Indonesia inclusively. An Indian has seen the price of gold increase from under 200 rupees when Bretton Woods failed to nearly 100,000 rupees today. It is not so much a rise in the price of gold; rather it is a measure of the loss of purchasing power of the rupee. In Asia, where half the world’s savers reside, gold is the basis of a wise man’s family pension fund. Lack of gold ownership could be his western equivalent’s folly.

Clearly, gold is much more than a bauble upon which rupees and rupiah are continually wasted by ignorant natives. And if it is only pretty, why is it that central banks are adding to their gold reserves at a record pace?

Myth 6. Gold is volatile

This observation is in the same category as that which states the sun rises in the morning and sets in the evening. It appears to be true, but it is the result of the earth’s own rotation, not the sun rotating round the earth. Those that say gold is volatile subscribe to a flat-earth fallacy that ignores the volatility that arises from currencies.

Measured in dollars, in 1971 the price of a barrel of oil was $3.60. At that time, the official gold price, before gold backing for the dollar was suspended in August that year, was $42.22, which meant oil was priced at 0.085 ounces of gold. Today, the oil price is $57, an increase in the dollar price of nearly fifteen times. Measured in gold, the price is 0.04 ounces, roughly half the price in 1971.

Energy, typically measured by the price of oil, is the most important of all commodities to human life. The price in gold-ounces is demonstrably more stable than the price in dollars. Clearly, the volatility is in the currency and all the other currencies that defer to it, not gold.

Myth 7. It’s a greater-fool investment

That gold is a greater-fool investment, requiring another buyer to believe it is going higher, is surely the most preposterous statement for any investment manager to make. The whole basis of equity investment and dealing in derivative markets is just that. With this statement, Stevenson has defined his own company’s stock in trade. Every investment, putting aside bonds held to maturity, requires an exit strategy. If Stevenson and his colleagues apportion equities into their clients’ portfolios without one, they would have good cause to remove their funds and seek a manager who at least looks before he leaps.

With respect to gold, nothing is further from the truth, which is why it is so important to understand that at its most fundamental level gold is money and not an investment to be traded. You can trade it of course, but the ultimate purpose of owning gold is to spend it.

Myth 8. Gold’s value was higher 40 years ago in real terms

Besides being highly selective with his timing to make his point, Stevenson’s statement that gold has failed to keep pace with inflation over the last forty years is presumably made to emphasise gold is a disappointing investment. As an investment, it therefore must be under-priced, given gold is widely recognised to be a hedge against paper currencies losing purchasing power.

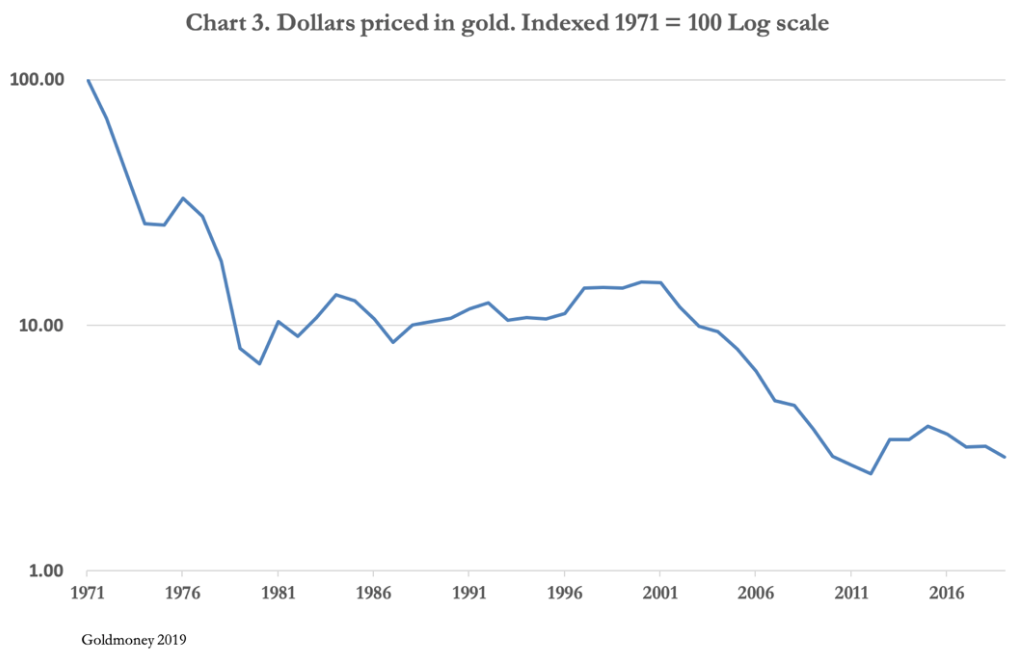

Stevenson’s approach is to only wrongly view gold as an investment, when in fact it is money. It is in the same category as uninvested cash, though with its own special sound-money characteristics. It is intended to be spent, not to be compared with financial assets. But as cash, it has retained purchasing power, which is more than can be said for the dollar. Since the Bretton Woods Agreement was terminated in August 1971 by President Nixon, the dollar has lost 97% of its purchasing power measured against gold.

If gold has produced a bad return for a dollar portfolio, one wonders what Stevenson thinks is a good one. To be fair, the performance of the S&P 500 Index gets close.

At the end of the same month the Bretton Woods Agreement was suspended, the S&P 500 Index stood at 97.24. Today it stands at 3,000. Therefore, the S&P500 has risen 30 times, while over the same period gold has risen nearly 33 times. Ignoring dividends, dealing costs to constantly rebalance the S&P index and the interest earned on gold, the performance is remarkably similar. But that is before considering the increased risk factors facing equities today, factors which are enormously positive for gold.

There is growing evidence of a developing global recession and a US slowdown. On the eve of these enhanced investment risks, the upside for the S&P500 seems limited at best, while there is a growing likelihood of an equity bear market developing. At the same time, the loosening of the Fed’s monetary policy clearly boosts prospects for the gold price.

The consequences of an accelerating money supply

An investor observing gold’s breakout and wondering if it leads to higher gold prices will be aware of the growing certainty that monetary inflation will accelerate. These events are connected.

Monetary inflation has been a longstanding problem. Most investors are wholly unaware that since 1971, measured in gold, the dollar has lost 97% of its value, reflecting the expansion of money and bank credit. This is illustrated in Chart 3, which is to a logarithmic scale.

Some of the loss of the dollar’s purchasing power is likely to be due to an increase in the purchasing power of gold, as the price of oil quoted above illustrates. But there are now reasons to believe the dollar and most other state-issued currencies are due for another significant loss of purchasing power.

In President Trump we observe a leader who in chronological order has attempted to restrict imports, bully the Fed into lowering interest rates, and is now pushing for a “competitive” dollar. The consequence of his administration’s trade policies has been to disrupt international trade to the extent that the evidence is it is contracting. The impact on all major economies has been to threaten them with recessions which could turn out to be significantly worse than the temporary slowdowns we have seen from time to time since the Lehman crisis.

Central banks are now concerned they have run out of road, confirmed by the Bank for International Settlements in its Annual Economic Report 2019, dated 30 June. In calling for “a better balance between monetary policy, structural reforms, fiscal policy and macroprudential measures”, the BIS, which represents all central banks is saying there is little more central banks can do to stabilise the global economy. That is not the way politicians, hooked on easy money will see it. Despite monetary policy makers’ misgivings, they have no policy alternative to more easing of interest rates and more expansion of their money supplies.

At the same time, governments are contemplating how they might provide spending or fiscal stimulus. Like China, some are contemplating infrastructure spending, and others, such as America and Britain under Boris Johnson are pursuing tax cuts. No government is prepared to reduce spending. It all adds up to one thing, and that is another round of massive monetary inflation.

What has not yet been appreciated are the consequences, and that is what the breakout in gold’s price, illustrated in Chart 1, is all about.

Chart 3 is about the bigger picture, taken from when there was a run on the US Treasury’s gold, and it could no longer swap dollars for gold at the then devalued rate of $42.22 per ounce. Today, we are on the verge of another run against currencies. Just imagine for a moment the combination of looming recession, negative interest rates still imposed in the EU, Switzerland, Denmark, Sweden and Japan, and now the prospect of competitive devaluations. And then ask yourself, what are the prospects for the gold price measured in these devaluing currencies?

Conclusion

Not only do global bond markets offer minimal or even negative returns, but there are growing signs the corporate sector is coming under pressure from a gathering recession. The strains in the fiat-money financial system are growing, with unsustainable corporate and consumer debt becoming an urgent consideration. This puts the investment management industry in a difficult, even impossible position.

From this viewpoint, the only investment opportunities that are now emerging, beyond increasing fiat cash balances, are unregulated. These are a dash into cash in the form of gold, and speculation in cryptocurrencies. Unregulated investments are anathema to compliance officers and therefore investment managers. Even when wrapped up in ETFs, which are regulated, the investment management industry has been slow to accept them. For the purpose of this article, we have put cryptocurrencies to one side. This is about physical gold.

Having invested intellectually in fiat money concepts for at least since the demise of Bretton Woods, investment managers have reduced portfolio exposure to gold and related investments to probably as low as it can get. Now that its dollar price has broken out of a multi-year torpor, gold offers the prospect of enhancing portfolio returns, which is why it is catching the attention of the investment management industry.

For most investment managers, the process of unlearning the theory of state money will be a painful one. Tom Stevenson is not alone, and his article in the Daily Telegraph exposes a worrying degree of ignorance among so-called investment experts about monetary affairs in general, but particularly about the role of gold as money.

With governments everywhere itching to increase spending without raising taxes and as the global economy sinks into a trade and credit-cycle induced recession, budget deficits will fuel monetary inflation at a faster pace than seen before. Re-learning that gold is sound money is now the most urgent priority for all those charged with responsibility for other peoples’ investments.

via ZeroHedge News https://ift.tt/2OlAFmC Tyler Durden

A bipartisan group of eight state attorneys general met with US Attorney General William Barr on Thursday to discuss “the real concerns consumers across the country have with big tech companies stifling competition,” according to Politico.

“Our bipartisan coalition of eight state attorneys general was pleased with the opportunity to meet with U.S. Attorney General Barr to talk about the real concerns consumers across the country have with big tech companies stifling competition on the internet,” reads a joint statement from the state AGs, which include Texas, Mississippi and Louisiana.

A Justice Department spokesperson declined comment. Some of the states that had planned to attend the meeting, including Nebraska and Arizona, have opened inquiries into Google’s practices. Representatives from the Nebraska and Arizona offices did not immediately return requests for comment.

The potential state action adds yet another layer to the growing scrutiny of the power of online platforms. In announcing its antitrust review this week, the DOJ said it will consider “widespread concerns” expressed about search, social media and online retail services. –Politico

Meanwhile, Facebook co-founder Chris Hughes is has been meeting with regulators to make the case for breaking up the social media giant, according to the New York Times.

Chris Hughes has joined leading academics to argue to government officials that Facebook has engaged in anticompetitive behavior for almost a decade. (Photo: Vincent Tullo for The New York Times)

In recent weeks, Mr. Hughes has joined two leading antitrust academics, Scott Hemphill of New York University and Tim Wu of Columbia University, in meetings with the Federal Trade Commission, the Justice Department and state attorneys general. In those meetings, the three have laid out a potential antitrust case against Facebook, Mr. Wu and Mr. Hemphill said.

For nearly a decade, they argue, Facebook has made “serial defensive acquisitions” to protect its dominant position in the market for social networks, according to slides they have shown government officials. By scooping up nascent rivals, they assert, Facebook has thwarted potential competitors, making it easier for the social network to charge advertisers higher prices and to offer a worse experience for users. –New York Times

“Mr. Hughes’s involvement stands out because few founders have gone on to argue for the dismantling of their company,” adds the Times.

Facebook announced on Wednesday that the FTC had begun an antitrust investigation into the company, while the DOJ and lawmakers have embarked on their own antitrust review of the tech industry.

via ZeroHedge News https://ift.tt/2Mgyk9J Tyler Durden

A short video clip in which Rep. Ilhan Omar (D–Minn.) appears to call on Americans to “be more fearful of white men” went viral this week, prompting denunciation from Sen. Marco Rubio (R–Fla.), who wondered whether journalists will ask Democrats to criticize Omar’s statement as racist.

The 41-second clip, though, is extremely misleading, and specifically cuts out an important clarifying line.

Omar was asked by Al Jazeera to respond to the conservative argument that it is legitimate to fear “quote-unquote Jihadist terrorism, whether it’s Fort Hood, or San Bernardino, or the recent truck attack in New York.”

Omar’s truncated response, featured in the viral video clip, seems to suggest that she thinks the government should instead be profiling white men. “I would say our country should be more fearful of white men across our country because they are actually causing most of the deaths within this country.” The clip then immediately cuts to Omar saying, “We should be profiling, monitoring, and creating policies to fight the radicalization of white men.”

If that were actually the point Omar was trying to get across, or even all she said, it would certainly be an idea worth criticizing.

But this is not what she’s saying. As the full video makes clear, Omar included a caveat: After she says the line about why the U.S. should be more fearful of white men, she adds, “and so if fear was the driving force of policies to keep America safe, Americans safe inside of this country…” and then she says “we should be profiling, monitoring, and creating policies to fight the radicalization of white men.”

Just to be abundantly clear, here is her full, unedited comment, in response to the prompt, “A lot of conservatives, in particular, would say the rise of Islamophobia is a result not of hate, but of fear”:

I would say our country should be more fearful of white men across our country because they are actually causing most of the deaths within this country and so if fear was the driving force of policies to keep America safe, Americans safe inside of this country, we should be profiling, monitoring, and creating policies to fight the radicalization of white men.

Omar was not endorsing the creation of a state apparatus to surveil white people, but rather, suggesting that if we’re going to base our decisions about public safety and surveillance on which racial or ethnic or ideological group causes the most violence, it is hypocritical for conservatives to focus on Muslims and not whites.

In fact, white men who identify as, or associate with, white nationalists have in recent years been responsible for more violent acts than radical Muslims, even though crimes committed by the latter group are far more likely to be labeled terrorism. This point came up frequently when I testified before the House subcommittee on civil rights and civil liberties last May, and it has been a topic of concern among American leftists for years. Ideologically-motivated violence is a small proportion of overall violence, of course. In 2017, there were just 34 “extremism-related” deaths in the U.S., according to the Anti-Defamation League. Eighteen were committed by white nationalists, and nine were committed by Islamic radicals.

According to The Intercept, which racial group causes the most violence in general depends on how you count and categorize acts of violence (and on 9/11 being excluded):

Some studies by academics, think tanks, civil rights groups, and news organizations have suggested that right-wing terrorism poses the greater threat. A 2017 report from the U.S. Government Accountability Office on terrorist violence from September 12, 2001 through December 31, 2016 found that while slightly more people have been killed by Muslim extremists than by their right-wing counterparts, right-wing extremists were responsible for three times as many violent acts. Research by the Anti-Defamation League on 573 “extremist-related fatalities” from 2002 to 2018 found that 80 percent of the victims were killed by right-wing extremists.

In any case, it’s true that a myopic focus on Islamic violence neglects the rising threat of white nationalism. Neither threat should prompt Americans to willingly sacrifice their civil liberties or accept mass surveillance based on skin color or religious identification, but Omar was calling out hypocrisy and is well within her rights to do so.

from Latest – Reason.com https://ift.tt/2Yo6Guc

via IFTTT

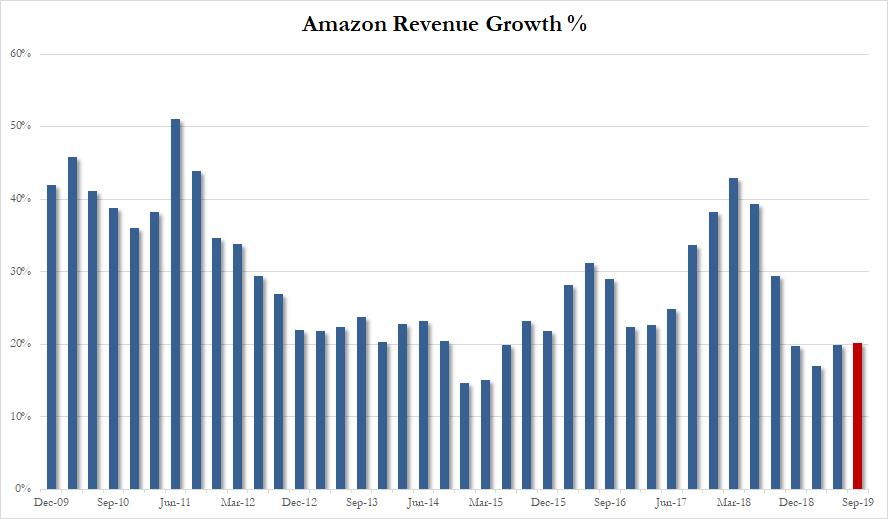

Last quarter, when Amazon reported otherwise respectable earnings, the market hammered the stock after AWS growth slowed again and Amazon guided to the lowest revenue growth since 2001, despite broadly higher margins. And, as the company reported moments ago, while its guidance may have been slightly downbeat, it wasn’t too far off as Amazon reported Q1 net sales of $63.4BN, above the $62.46BN consensus estimate, while generating $5.22 in Q2 EPS, missing the $5.56 expected.

Here are the summary Q2 highlights:

Earnings per share of 5.22$, missing expectations of 5.56, but up from $5.07 in 2Q 2018

Sales of $63.4 billion, above expectations of $62.4 billion, and also up 20% YoY from $52.8 billion

Operating income of $3.08 billion, missing expectations of $3.7 billion, and just up from $2.9 billion

AWS sales of $8.381 billion, also missing the $8.5 billion expected, but up from $6.1 billion

While AMZN missed on most of Q2 metrics, the good news here is that Q2 revenue did come in higher than sellside expectations, rising 20% in Q1, and looking ahead, the recent top line slowdown is expected to moderate, as the company now expects Q3 net sales between of $66BN and $70N, with the midpoint of $68BN ,coming in just above the Wall Street consensus estimate of $67.22BN. If revenue comes in right on the midpoint, it would represent another modest rebound from recent lows, rising 20.2% in Q3.

But if the company’s top line guidance was the good news, its profit outlook was not, as Amazon’s guidance for Q3 profit came in well below analyst expectations with the company expecting to make just $2.1 billion to $3.1 billion in operating income, well below the Wall Street analyst estimate of $4.3 billion.

More bad news: after the company’s profit margin nearly doubled to an impressive 7.4% in Q1 2019, largely thanks to the increasing contribution from AWS, in Q2 profit slumped again, and the profit margin of 4.9% was the lowest going back to Q1 2018.

Another negative: after the company’s international loss shrank to just $90MM in Q1 2019, it once again swelled, rising to $601 million in Q2.

Meanwhile, the all important Amazon Web Services was once again responsible for more than half of Amazon’s entire profit, with the division generating $8.381BN in revenue (below the $8.5BN expected), and up from $7.7BN in Q1, generating $2.12 BN in operating income, a 25.3% operating margin, down from $2.22BN in operating income in Q1, and sharply lower from the 28.9% margin reported last quarter. Even so it was responsible for 69% of the company’s total operating income of $3.08BN.

But even more concerning was the slowdown in AWS revenue, which rose just 37%, down from 49% a year ago and down from 42% last quarter. As Bloomberg puts it, AWS’s growth rate of 37% continues to slow as the business grows, “but it’s still a cash machine.”

To summarize, AWS revenue growth:

Q1 2018: 48%

Q2 2018: 49%

Q3 2018: 46%

Q4 2018: 46%

Q1 2019: 42%

Q2 2019: 37%

And AWS operating margin:

Q1 2018: 25.7%

Q2 2018: 26.9%

Q3 2018: 31.1%

Q4 2018: 29.3%

Q1 2019: 28.9%

Q2 2019: 25.3%

Looking at the rest of Amazon’s business, Q2 marked two years since Amazon announced it was buying Whole Foods Market. Alas, as Bloomberg notes, the read on how the grocer is performing under Amazon remains murky. Whole Foods accounts for almost all of the sales in Amazon’s “physical stores” segment. That was $4.33 billion, barely changed from $4.31 billion a year ago, with razor thin margins. “Complicating matters, that total does not include online orders from the dozens of markets where Whole Foods stores serve as grocery delivery depots.”

And while Amazon reported strong revenue and an impressive sales outlook, the reason why the stock is sharply lower is due to the disappointing profit outlook, suggesting continue big spending on delivery which pressures margins, and the ongoing slowdown in AWS.

Perhaps realizing that it needs to focus much more carefully on costs, Amazon announced labor initiatives, pledging to upskill 100,000 of its employees across the U.S. by 2025, dedicating over $700 million to provide employees across its corporate offices, tech hubs, fulfillment centers, retail stores, and transportation network with access to training programs that will help them move into more highly-skilled roles within or outside of the company.

The stock, for those who don’t have a screen in front of them, tumbled as much as $100 to $1,900 after hours, before recovering some losses.

via ZeroHedge News https://ift.tt/2YuaspG Tyler Durden

A short video clip in which Rep. Ilhan Omar (D–Minn.) appears to call on Americans to “be more fearful of white men” went viral this week, prompting denunciation from Sen. Marco Rubio (R–Fla.), who wondered whether journalists will ask Democrats to criticize Omar’s statement as racist.

The 41-second clip, though, is extremely misleading, and specifically cuts out an important clarifying line.

Omar was asked by Al Jazeera to respond to the conservative argument that it is legitimate to fear “quote-unquote Jihadist terrorism, whether it’s Fort Hood, or San Bernardino, or the recent truck attack in New York.”

Omar’s truncated response, featured in the viral video clip, seems to suggest that she thinks the government should instead be profiling white men. “I would say our country should be more fearful of white men across our country because they are actually causing most of the deaths within this country.” The clip then immediately cuts to Omar saying, “We should be profiling, monitoring, and creating policies to fight the radicalization of white men.”

If that were actually the point Omar was trying to get across, or even all she said, it would certainly be an idea worth criticizing.

But this is not what she’s saying. As the full video makes clear, Omar included a caveat: After she says the line about why the U.S. should be more fearful of white men, she adds, “and so if fear was the driving force of policies to keep America safe, Americans safe inside of this country…” and then she says “we should be profiling, monitoring, and creating policies to fight the radicalization of white men.”

Just to be abundantly clear, here is her full, unedited comment, in response to the prompt, “A lot of conservatives, in particular, would say the rise of Islamophobia is a result not of hate, but of fear”:

I would say our country should be more fearful of white men across our country because they are actually causing most of the deaths within this country and so if fear was the driving force of policies to keep America safe, Americans safe inside of this country, we should be profiling, monitoring, and creating policies to fight the radicalization of white men.

Omar was not endorsing the creation of a state apparatus to surveil white people, but rather, suggesting that if we’re going to base our decisions about public safety and surveillance on which racial or ethnic or ideological group causes the most violence, it is hypocritical for conservatives to focus on Muslims and not whites.

In fact, white men who identify as, or associate with, white nationalists have in recent years been responsible for more violent acts than radical Muslims, even though crimes committed by the latter group are far more likely to be labeled terrorism. This point came up frequently when I testified before the House subcommittee on civil rights and civil liberties last May, and it has been a topic of concern among American leftists for years. Ideologically-motivated violence is a small proportion of overall violence, of course. In 2017, there were just 34 “extremism-related” deaths in the U.S., according to the Anti-Defamation League. Eighteen were committed by white nationalists, and nine were committed by Islamic radicals.

According to The Intercept, which racial group causes the most violence in general depends on how you count and categorize acts of violence (and on 9/11 being excluded):

Some studies by academics, think tanks, civil rights groups, and news organizations have suggested that right-wing terrorism poses the greater threat. A 2017 report from the U.S. Government Accountability Office on terrorist violence from September 12, 2001 through December 31, 2016 found that while slightly more people have been killed by Muslim extremists than by their right-wing counterparts, right-wing extremists were responsible for three times as many violent acts. Research by the Anti-Defamation League on 573 “extremist-related fatalities” from 2002 to 2018 found that 80 percent of the victims were killed by right-wing extremists.

In any case, it’s true that a myopic focus on Islamic violence neglects the rising threat of white nationalism. Neither threat should prompt Americans to willingly sacrifice their civil liberties or accept mass surveillance based on skin color or religious identification, but Omar was calling out hypocrisy and is well within her rights to do so.

from Latest – Reason.com https://ift.tt/2Yo6Guc

via IFTTT

Share of Google parent Alphabet are up 6% after-hours following a better than expected print in top- and bottom-line.

Alphabet said second-quarter sales, excluding payments to partners, came in at $31.71 billion. Analysts were looking for $30.84 billion, according to data compiled by Bloomberg.

Sales from Google’s own online properties, including Search and YouTube, climbed 18% to $27.34 billion.

“Our effort to build a more helpful Google for everyone brings countless opportunities to help users, partners, and enterprise customers every day,” said Sundar Pichai, Chief Executive Officer of Google.

“From improvements in core information products such as Search, Maps, and the Google Assistant, to new breakthroughs in AI and our growing Cloud and Hardware offerings, I’m incredibly excited by the momentum across Google’s businesses and the innovation that is fueling our growth.”

Cost-per-click fell only 11% on the year, and paid clicks on Google properties (like search and YouTube) were up 28%.

“With revenues of $38.9 billion, up 19% versus the second quarter of 2018 and up 22% on a constant currency basis, we’re delivering strong growth,” said Ruth Porat, Chief Financial Officer of Alphabet and Google.

“Our ongoing investments in compute capabilities and engineering talent reflect the compelling opportunities we see across the company.”

Alphabet’s Effective Tax Rate fell from 24% to 18%…

Additionally, Alphabet authorized an additional $25 billion in share buybacks.

That was all a welcome relief from the first quarter of this year, when Google missed Wall Street revenue expectations and saw its shares plunge.

Investors love it…

via ZeroHedge News https://ift.tt/2JZOgus Tyler Durden

Steve Ballmer mimics the excitement in the room ahead of Draghi’s press conference…

But the euro shows the post-Draghi disappointment nothing-burger…

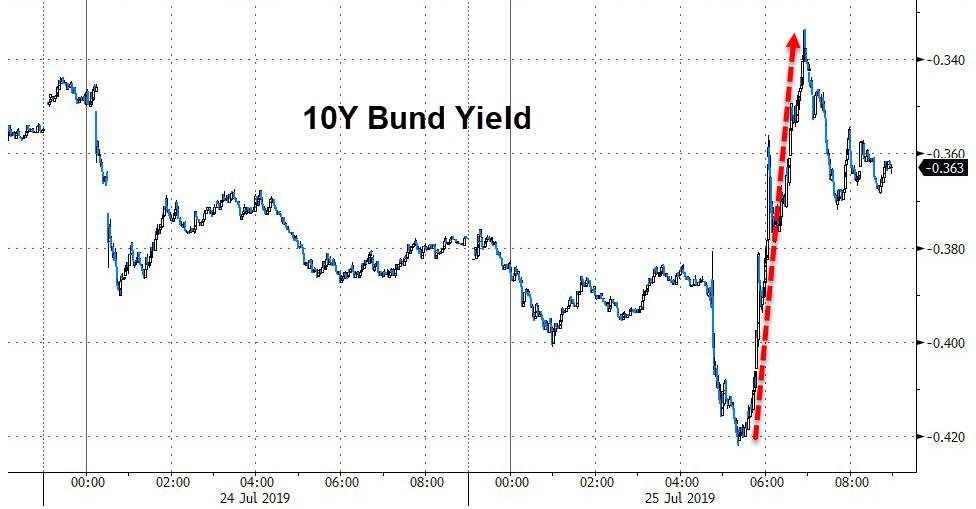

German Bund yields spiked as Draghi began speaking but buyers came back in after he finished with yields ending just 1bps higher on the day (after making a new record low)…

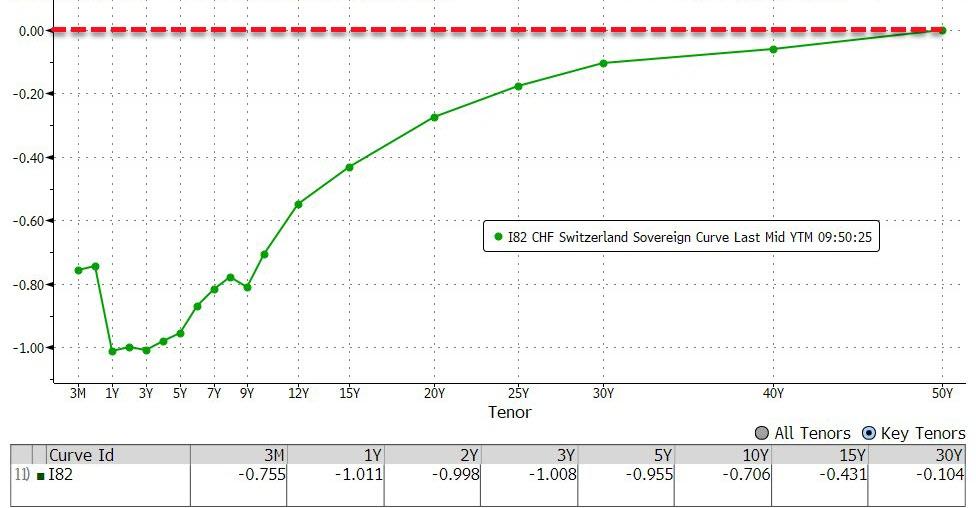

And the entire Swiss yield curve – out to 50Y – is now negative…

Chinese stocks lifted overnight with tech-heavy ChiNext outperforming…

US Small Caps were the day’s biggest loser (after being yesterday’s big winner).. weak close

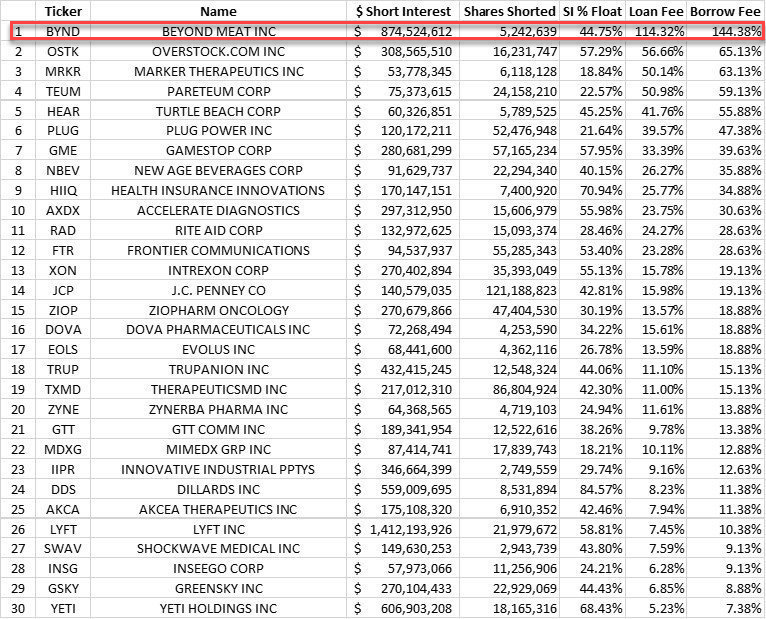

“Most Shorted” stocks plunged by their most since May 13th…

S&P tested back below 3,000 intraday but was bid each time…

Dow Futures pushed down to 2-week lows…

Tesla was monkeyhammered 15% lower…

Boeing puked…

Facebook was FUBAR (after tagging record highs immediately after earnings)…

But BYND is beyond belief…

With a massive $875 mm (44.75% of float) short…

VIX mini flash-crashed to an 11 handle ahead of the bell as Draghi spoke but pushed back above 13 as stocks sank…

Which is notable since VIX calls have been aggressively bought…

HY Credit risk compressed on the day – despite the broader derisking, but VIX and IG risk increased…

Treasury yields jerked higher on Draghi’s disappointment today (up 3-4bps across the curve)…

10Y Yields spiked intraday from 2.00% to 2.10% before leaking a little lower…

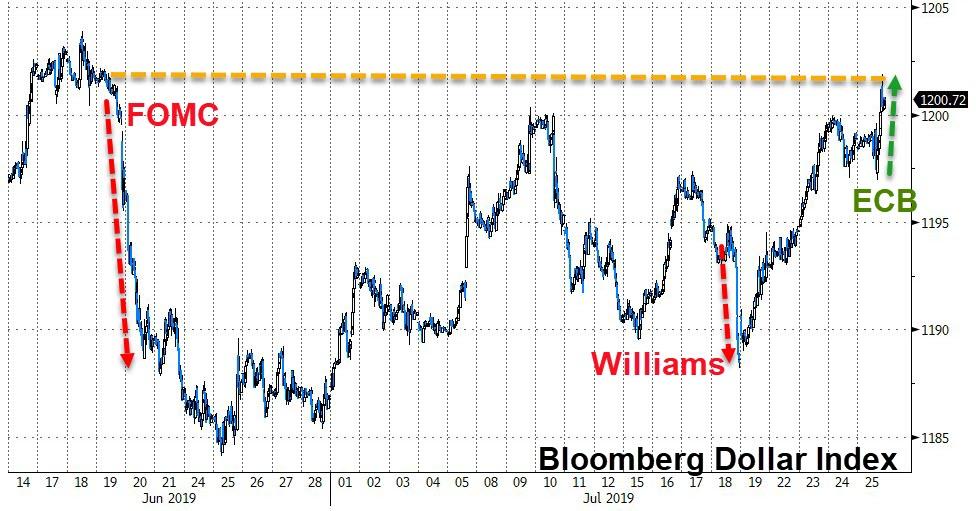

The Dollar Index ended higher, despite the roundtrip on the EUR…

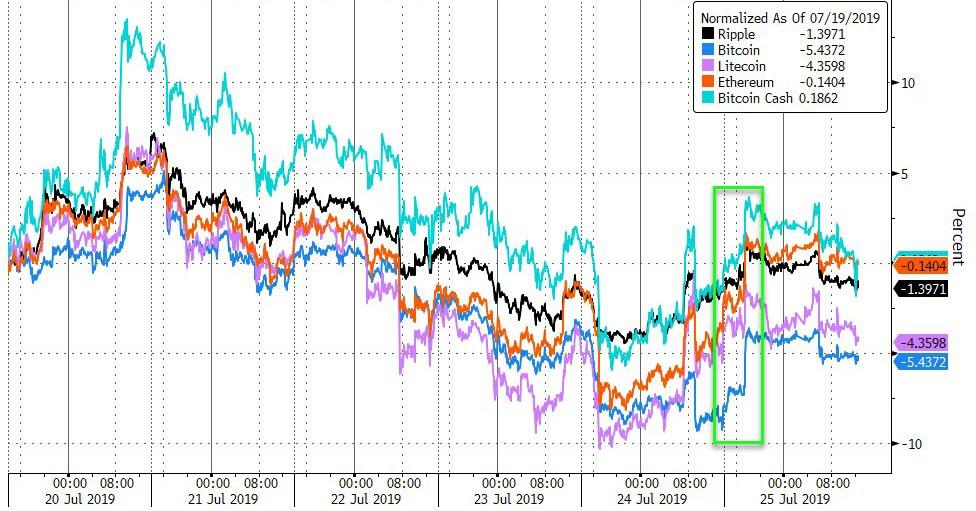

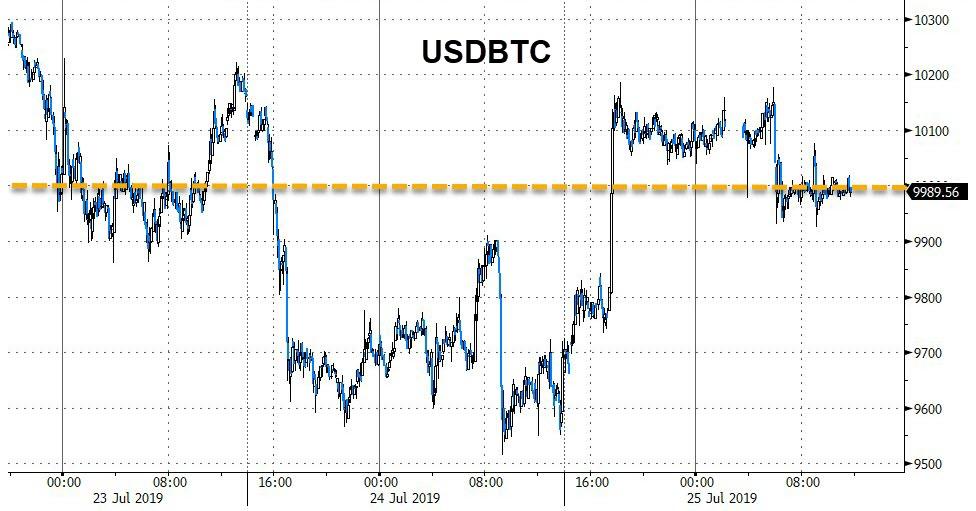

Bitcoin and Ethereum managed gains on the day but broadly speaking, Cryptos are lower on the week…

Bitcoin spent the day hovering around $10,000…

Commodities all drifted lower during the US day session…

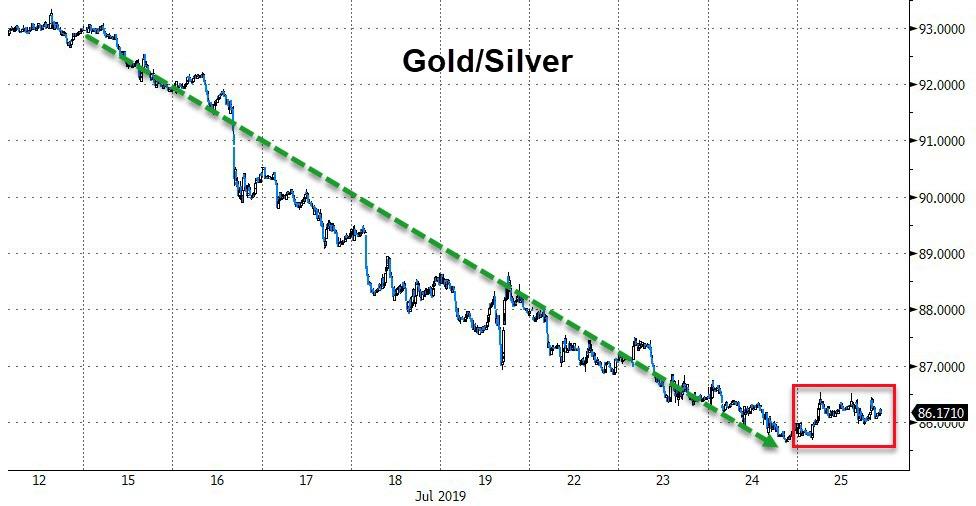

Gold modestly outperformed silver for the first time in 10 days…

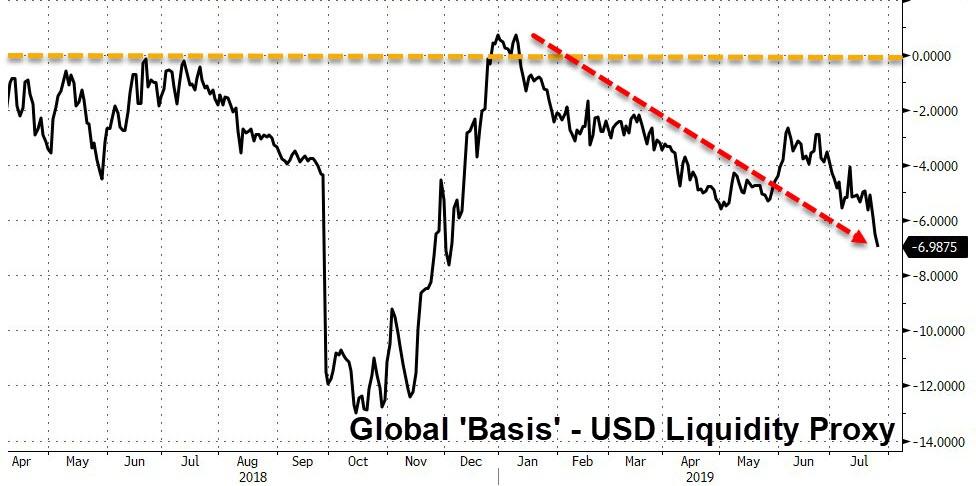

Finally, The Fed better cut now that The ECB has waited… USD liquidity measures are screaming for some help…

via ZeroHedge News https://ift.tt/2JUTyJ3 Tyler Durden

A gay couple recently filed a lawsuit challenging the legality of a State Department policy that denies automatic citizenship to children of married US-citizen same-sex parents born abroad (in this case through a surrogacy arrangement):

Derek Mize and Jonathan Gregg, who married in New York in 2015, had their daughter Simone Mize-Gregg via surrogacy in England in 2018, their lawyer said in a statement. Both fathers are listed on the birth certificate.

When they applied for Simone’s US citizenship, the US consulate in London rejected their application… “The Immigration and Nationality Act (INA) states that children of married U.S. citizens born abroad are U.S. citizens from birth so long as one of their parents has lived in the U.S. at some point, but the State Department routinely denies that right to same-sex couples and their children,” the statement says.

“The State Department’s policy is not only cruel, it is unconstitutional. The government refuses to recognize Jonathan and Derek’s marriage and all of Simone’s rights as a U.S. citizen,” Aaron C. Morris, one of the couple’s attorneys and executive director of Immigration Equality, said…..

The lawsuit says that, “Because she is the child of two men, the U.S. Department of State evaluated Simone’s citizenship under the standards only applicable to children ‘born out of wedlock’ and refused to recognize Simone’s U.S. citizenship.”

The full text of the complaint filed by Mize and Gregg’s counsel is available here. It argues that the State Department policy violates both the Immigration and Nationality Act (which does not, in its text, distinguish between same-sex and opposite-sex marriages), and the Constitution.

Simone might have qualified for US citizenship even under the rules for children “born out of wedlock.” But in such cases, the law mandates that the biological US-citizen parent must have lived in the US for five consecutive years, and Jonathan Gregg was one year short.

The plaintiffs here are absolutely right that the State Department’s policy is both cruel and unconstitutional. In Sessions v. Morales-Santana (2017), the Supreme Court struck down a law that made it easier for foreign-born children of unwed US-citizen mothers to acquire citizenship than foreign-born children of unwed citizen fathers. The Court emphasized that “Laws granting or denying benefits ‘on the basis of the sex of the qualifying parent…’ differentiate on the basis of gender, and therefore attract heightened review under the Constitution’s equal protection guarantee.” It also concluded that the law in question could not possibly pass heightened scrutiny, because the sex discrimination it imposes does not substantially advance any important government interest.

The same reasoning applies to the State Department policy on children of same-sex parents. Here too, the government discriminates based on the sex of the parents in question. If both are the same sex, they are treated differently than if they are not. And, here too, there is no defensible government interest that is advanced by the sex discrimination in quest.

The State Department automatically grants citizenship to foreign-born children of US opposite-sex married couples who use a surrogate or a sperm donor. It does not require both parents to have a biological connection to the child, and treat it as “born out of wedlock” if one parent does not. There is no reason, other than rank bigotry, to deny the same treatment to children of same-sex married couples. The government cannot even claim that the policy is justified by a supposed need to to privilege biological parents over non-biological ones, since the rule does not similarly disfavor non-biological parents in opposite-sex marriages.

I continue to believe that the Court would have done better to simply rule that laws banning same-sex marriage are unconstitutional because they discriminate on the basis of sex, as Northwestern law Professor Andrew Koppelman and I urged in an amicus brief we filed in Obergefell. Among other things, that approach would have made clear that all government discrimination against same-sex couples is presumptively unconstitutional.

But the Supreme Court has since clarified—in a 6-3 ruling in Pavan v. Smith (2017)—that the Obergefell entitles same-sex married couples to the same “rights, benefits, and responsibilities” of marriage as opposite-sex ones. That surely includes the right to transmit citizenship to their foreign-born children. Even Obergefell itself indicates that one of the main reasons for striking down laws banning same-sex marriage is to ensure that children of same-sex parents have access to “the recognition, stability, and predictability marriage offers.” There are few more denials of “recognition, stability, and predictability” than a rule that essentially prevents some children from living in the same country as their parents (or, in this case, from doing so for more than 90 days at a time).

In a similar case decided in February, a federal district court ruled that the State Department policy violates the Immigration and Nationality Act, and therefore chose not to rule on the constitutional issues. That ruling is now under appeal. If the courts rule that the State Department policy is permissible under immigration laws enacted by Congress, the combination of Pavan,Obergefell, and Morales-Santana should doom it on constitutional grounds.

If judges conclude that the relevant parts of the INA are ambiguous, lower courts must interpret the statute to treat same-sex and opposite-sex couples equally, in order to avoid constitutional problems. In NFIB v. Sebelius(2012) and other cases, the Supreme Court made clear that it will adopt almost any reasonably plausible interpretation of a federal statute that avoids the risk of making it unconstitutional. I am no great fan of this “constitutional avoidance” canon. But it is binding Supreme Court precedent, and lower courts have to follow it.

Elsewhere, I have argued that the right to live and work in the US (and other countries) should not be so heavily dependent on a “hereditary aristocracy” of citizenship determined largely by circumstances of birth. But the right way to address this injustice is to increase freedom of movement for non-citizens, not to make the current system of hereditary rights even more restrictive by adding a dose of sex discrimination into the mix. In any event, this broader moral issue does not change the legal analysis that applies to cases like this one.

from Latest – Reason.com https://ift.tt/2OsufSW

via IFTTT

Blow was more than a bit triggered by yesterday’s performance by Robert Mueller and Congressional Democrats, tweeting “I’m soooooo frustrated and disappointed” that “Dems are basically reading Mueller quotes from his report” (which he was totally unfamiliar with).

Dems are basically reading Mueller quotes from his report and asking, “is that correct”? You have had this report for five months! You already knew it was correct! You already knew he was a criminal. And you have done NOTHING! I’m soooooo frustrated and disappointed.

Of course, the ‘fatal flaw’ in Blow’s logic – i.e. House Speaker Nancy Pelosi’s stance, is that if House Democrats move to impeach Trump for attempting to obstruct an investigation over a crime he didn’t commit – using all the ‘smoking guns’ and ‘gotchas’ contained in the Mueller report – it’ll backfire more than a 1965 Karmann Ghia right into the 2020 US election after the Senate shuts the whole thing down.

On Wednesday afternoon, Trump tweeted his assessment of the Mueller testimony – calling it a “devastating day” for Democrats, who are “a mess” (h/t Tony Lee, Breitbart).

{kind=link}