Yesterday Donald Trump effusively thanked the Republican legislators who went to bat for him during the Muellerhearings. “I very much appreciate those incredible warriors that you watched today on television—Republicans—that defended something, and defended something very powerful, very important,” he told reporters. “Because they were really defending our country. More than anything else, they were defending our country.”

Sound familiar? During his rally in North Carolina last week, Trump excoriated Rep. Rashida Tlaib (D-Mich.), who in January promised “we’re going to impeach the motherfucker.” In Trump’s mind, that comment was evidence the Tlaib hates America. “Tlaib also used the F-word to describe the presidency and the president,” he said. “That’s not nice, even for me. She was describing the president of the United States and the presidency with the big, fat, vicious—the way she said it—vicious F-word. That’s not somebody that loves our country.”

Whatever you think about the case for impeachment, this is a pretty creepy way of describing people who dare to criticize the president, profanely or not. Yesterday on Twitter, Trump called the argument that he obstructed justice when he tried to stop, limit, and control the Mueller investigation an “illegal and treasonous attack on our Country.” Trump likewise has called former Deputy Attorney General Rod Rosenstein’s suggestion that Justice Department officials record their conversations with him after he fired FBI Director James Comey “illegal and treasonous.” The Mueller investigation itself was a “Phony & Treasonous Hoax” involving “treasonous acts,” according to the president.

Even failing to applaud Trump during his State of the Union address might qualify as treason, he suggested last year. “Somebody said ‘treasonous,'” he said during a visit to Cincinnati. “I mean, yeah, I guess, why not. Can we call that treason? Why not? I mean, they certainly didn’t seem to love our country very much.” When The New York Times published an anonymous op-ed piece by an administration official who was critical of the president, that was also “treason” in Trump’s book. Likewise Democratic opposition to his immigration policies.

Legally speaking, treason, which is punishable by death, happens when an American wages war against the United States, “adheres” to the country’s enemies (defined as nations or organizations that are at war with the U.S.), or “gives aid and comfort” to them. Trump is obviously speaking more loosely (although he did say last May that investigating his 2016 presidential campaign was “TREASON,” which “means long jail sentences”). But even colloquially, treason implies a betrayal of the nation. Hence Trump is equating attacks on him with attacks on the country.

His fans may see no problem with that, since they like Trump and therefore are not guilty of treason, according to his definition. But they might react differently to a Democratic president who routinely suggested that criticizing him, investigating him, or calling for his impeachment is or should be illegal because it gives aid and comfort to America’s enemies. Correct me if I’m wrong, but I don’t recall Barack Obama or George W. Bush using that sort of rhetoric when people said they should be impeached.

For Trump’s detractors, the temptation to turn the treason charge around is strong. Former White House adviser Stephen Bannon said Donald Trump Jr.’s June 2016 meeting with a Russian lawyer who claimed to have dirt on Hillary Clinton was “treasonous.” Last February, Malcolm Nance, a counter-terrorism and intelligence consultant, opined that “the president of the United States may have committed treason.” Political consultant Rick Wilson, former CIA Director John Brennan, former State Department official John Shattuck, presidential historian Jon Meacham, and New York Times columnist Charles Blow, to name a few, have all accused the president of treason. In those cases, there is at least a hypothetical foreign nexus, but Trump’s alleged misdeeds still do not meet the legal definition, which requires aiding a country that is at war with the United States.

All this talk of treason is about as productive as Trump’s response to the charge that he’s racist. I’m not a bigot, he says; you’re a bigot. When everyone’s a traitor, no one is a traitor, because the word loses all meaning. Tossing it around so casually is poisonous to rational debate and feeds a hyper-partisan atmosphere in which every position someone takes has to be judged, first and foremost, by whether it is pro- or anti-Trump. Is it possible for Americans to argue about politics and policy without accusing each other of betraying the country? It’s not a rhetorical question.

from Latest – Reason.com https://ift.tt/2GtRYeS

via IFTTT

I’m often asked if recession is coming, and for quite different reasons. Some people worry about their investments. Others are worried about their employment or their kids. Political types wonder if and how recession could affect the next election.

To all those people, for quite some time now, my answer has been: “Yes, but not just yet.” That’s still what I think today, but more of the early warning signals I have used in the past are beginning to flash again.

Looking at the data, I see some good news but also some leading indicators weakening. I see smart people like Dave Rosenberg argue we may already be in recession today. And I see Wall Street not really caring either way, so long as it gets enough rate cuts to prop up asset prices. None of that is comforting.

Today we’ll look around and see what is happening. Because I try to be aware of my own biases, we’ll consider some more optimistic views, too. They may not be convincing, but it’s important to confront them.

As you’ll see, the storm clouds are gathering. Someone is likely to get hit. It might be you.

Let’s begin by reviewing where we are. I think we all agree this recovery cycle has been both longer and weaker than in the past. Any growth is good, of course, and certainly better than the alternative. But the last decade wasn’t a “boom” except in stock and real estate prices.

(Quickly, let’s put to rest the myth that the longer a recovery goes, the greater the likelihood of a recession. That’s a tautology. Recoveries don’t stop because of length. Back to the main point…)

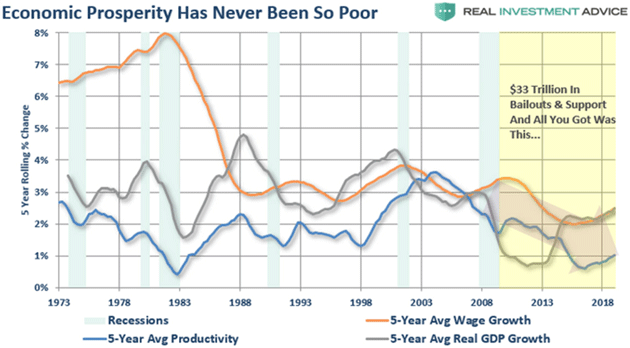

I like this Lance Roberts chart because it shows long-term (5-year) rates of change, over a long period (since 1973) in three key indicators: Productivity, wage growth, and GDP growth. You can see all three are now tepid at best compared to their historical averages.

These measures have been generally declining since the early 2000s, suggesting that whatever caused our current problems preceded the financial crisis. But we don’t need to know the cause in order to see the effects which, while not catastrophic (at least yet), are worrisome. And, as Lance points out, a decade of bailouts and dovish monetary policy didn’t revive previous trends.

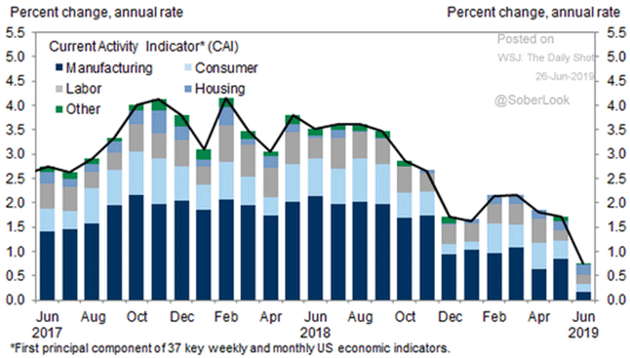

The growth deceleration is also visible if we zoom into the recent past, via the Goldman Sachs Current Activity Indicator. It peaked in early 2018 (not coincidentally, at least in my opinion, about the time Trump started imposing tariffs on China) and slid further this year. Much of it is due to a manufacturing slowdown, but the consumer and housing segments contributed as well.

Source: Goldman Sachs via The Daily Shot

Again, this doesn’t say recession is imminent. The US economy is still growing by most measures. But the growth is slowing and, unless something restores it, will eventually become a contraction.

My friend Lakshman Achuthan of the Economic Cycle Research Institute (ECRI) makes the extraordinarily valid point: Recessions don’t happen from solid growth cycles. Economies generally move into what he calls a “vulnerable stage” before something pushes them into recession. We all pretty much agree that the US economy, not to mention the global economy, is in a vulnerable stage. It won’t take much of a shock to push it into recession.

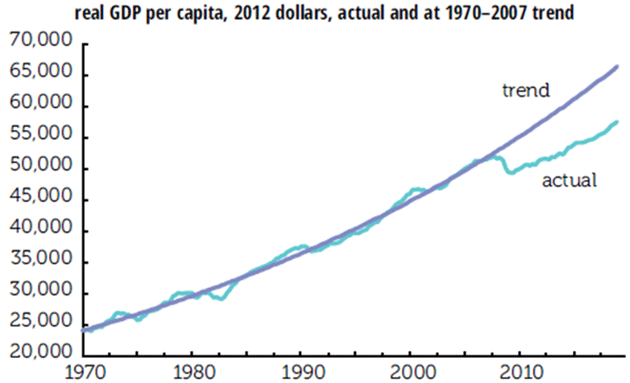

That’s bad news for many reasons, but one is that we have a lot of catching-up to do. My friend Philippa Dunne recently highlighted some IMF research on lingering damage from the financial crisis. Per capita real GDP since 1970 is now running about $10,000 per person below where the pre-crisis trend would now have it. Philippa calculated that at current rates, the economy won’t be where it “should” be until the year 2048.

A recession will push us even further below that 1970–2007 trend line. And all the zero interest rate policies (ZIRP) and quantitative easing in the world will not get us back on trend, just as it did not after 2008. No matter how fast we try to run, it will get even harder to catch up with that trendline.

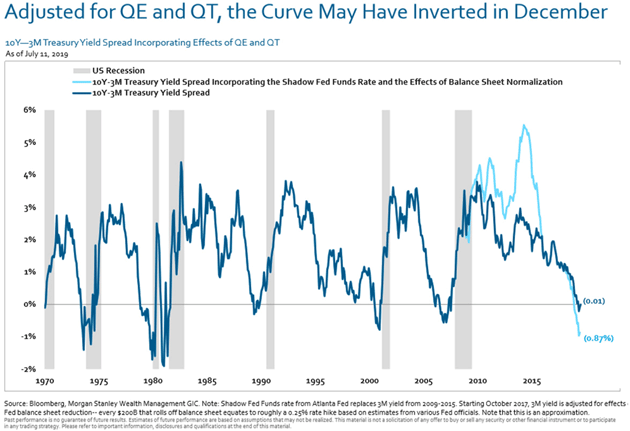

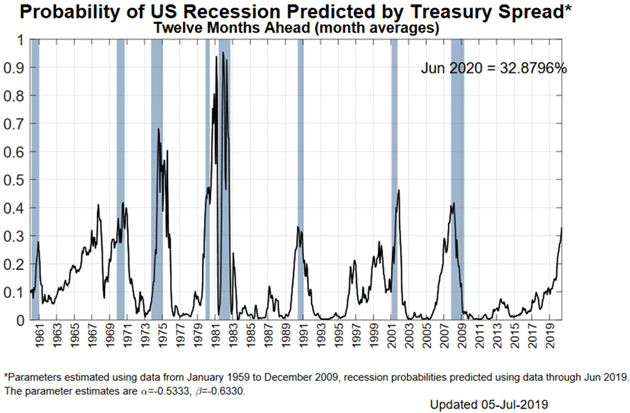

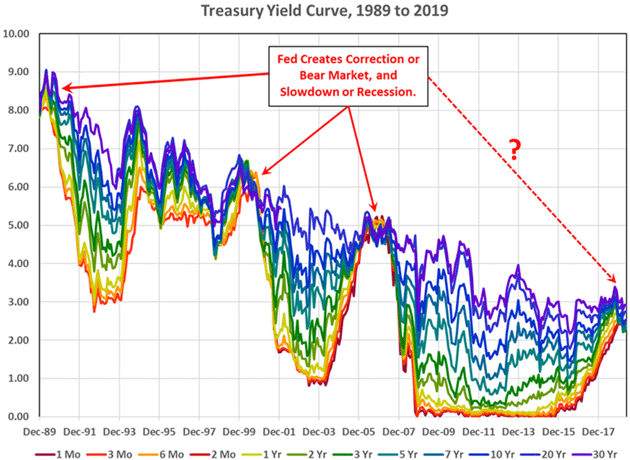

The inverted yield curve is one of the more reliable recession indicators, as I discussed at length last December in The Misunderstood Flattening Yield Curve. At that point, we had not yet seen a full inversion. Now we have, and it appears in hindsight perhaps the curve was “inverted” back then, and we just didn’t know it.

You may recall that the Powell Fed spent 2018 gradually raising rates and reducing the balance sheet assets it had accumulated in the QE years. This amounted to an additional tightening. I said it was a mistake but alas, the Fed didn’t listen to me. In fact, I repeatedly argued that the Fed was running an unwise two-variable experiment by doing both at the same time. Many serious observers wonder which is more problematic for the economy. I think the balance sheet reduction has had more impact than lower rates.

If you assume, as Morgan Stanley does below (and I have seen variations of this from numerous other analysts) every $200B balance sheet reduction is equivalent to another 0.25% rate increase, which I think is reasonable, then the curve effectively inverted months earlier than most now think. Worse, the tightening from peak QE back in 2015 was far more aggressive and faster than we realized.

Let’s go to the chart below. The light blue line is an adjusted yield curve based on the assumptions just described.

Source: Morgan Stanley

But even the nominal yield curve shows a disturbingly high recession probability. Earlier this month, the New York Fed’s model showed a 33% chance of recession in the next year.

Their next update should show those odds somewhat lower as the Fed seems intent on cutting short-term rates while other concerns raise long-term rates. But it’s still too high for comfort, in my view.

But note that whenever the probability reached the 33% range (the only exception was 1968), we were either already in a recession or about to enter one. For what it’s worth, I think Fed officials look at their own chart above and worry. That’s why more rate cuts won’t be surprising. And frankly, and I know this is out of consensus, I would not rule out “preemptive quantitative easing” if the economy looks soft ahead of the election next year. Just saying…

But that’s not everyone’s view. Gavekal gives us this handy chart showing inversions don’t always lead to recession right away. (I noted 1968 above and I think 1998 is a separate issue. But then again, that’s me.)

Fair enough; brief inversions don’t always signal recession. But as noted, when you consider the balance sheet tightening, this one hasn’t been brief. Note also that an end to the inversion isn’t an all-clear signal. The yield curve is often steepening even as recession unfolds.

One thing seems certain: While the yield curve may not signal recession, it isn’t signaling higher growth, either. The best you can say is that the mild expansion will continue as it has. That’s maybe better than the alternative, but doesn’t make me want to pop any champagne corks.

Rob Arnott of Research Affiliates is simply one of the finest market analysts anywhere. He has won more awards and accolades than almost anyone I know. I am honored to call him friend and frequently get the benefit of his commentary about my letters or in this case, a note I used in my Over My Shoulder service from a former Fed economist. I’ll let Rob speak for himself:

I’m fascinated that there are so many economists and pundits who think that cutting rates is a bad idea, when many (sometimes the same people!) thought ZIRP was fine for a half-dozen years.

I was struck by Yellen’s recent comments that it’s “very difficult” to bring long rates down. This would seem to lend credence to Bianco’s assertion that yield curve inversion doesn’t “predict” a recession; it “causes” a recession. The “causality” is a controversial idea. My argument: The long end is set by the markets, not regulators. It is high when inflation and/or growth expectations are strong, and low when inflation/growth expectations are low. When the long end falls below the short end (or the short end rises above the long end), the long end is telling us that people are happy to lend long-term at rates lower than the short-term cost of capital and are disinclined to borrow at rates at or above the short-term cost of capital. This probably means some blend of risk aversion and pessimism. The Fed waits until it sees signs of weakness, so it’s always behind the curve. By the time there is objective evidence of weakness, it’s too late for the Fed to do a thing.

This is also why critics are wrong to criticize Steve Moore or Judy Shelton for wanting higher rates before Trump’s election, and lower rates today. The graph below suggests that the long bond was begging the Fed to normalize, within months after the Global Financial Crisis had passed. And is now saying “we’re running out of time to ease.”

Source: Research Affiliates

For what it’s worth, I think an inverted yield curve is similar to a fever. It simply tells us something is wrong in our economic body. And sadly, at least historically, Rob is right. The Fed has always been behind the curve. To Powell’s credit, he may be trying to get in front of it, at least this time. I am less hopeful about the results, for different reasons I will describe in another letter someday.

The yield curve and other financial indicators are, while interesting, somewhat disconnected from the “real” economy. What’s happening on Main Street, where real people buy and sell real products used in everyday life? The news isn’t reassuring there, either.

The physical goods we buy—food, clothing, furniture, houses, and most everything else—have one thing in common. They (or their components) travel long distances to reach us. Sometimes it’s from overseas, sometimes domestic, but none of us live in close proximity to all the things we need. The market economy brings them to us.

People have aptly compared the economy’s transportation sector to the body’s circulatory system. It’s a good metaphor. Blood delivers nutrients to your organ just as trucks deliver products to your home. Problems begin when those deliveries slow… and they are.

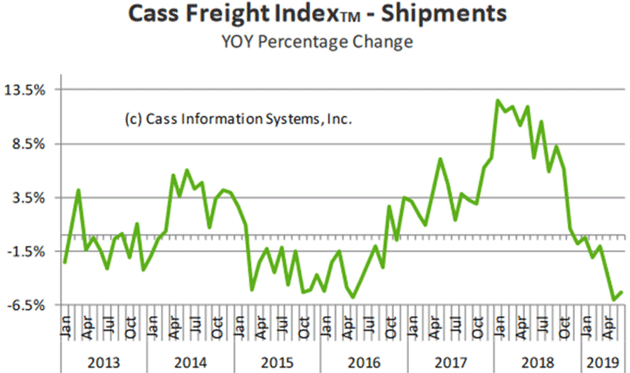

The Cass Freight Index (which I have followed for more than a decade) measures shipment volume (by quantity, not cost) across the economy: truck, rail, air, ship, everything. The chart below shows its year-over-year percentage change.

You can see shipment growth picked up in 2016 following an extended weak stretch. This continued into early 2018 then a steep slide ensued. (Note that this is about the same time as the manufacturing contraction shown in the Goldman Sachs chart above and coincides with the first Trump tariffs.) Annual growth went below zero in December 2018 and has been there ever since—now seven consecutive months.

“What’s the big deal?” you may ask. Look how long that 2014–2016 contraction lasted. It didn’t signal a recession. Two points on that…

First, that retreat sprang from an oil price collapse that began in November 2014 and quickly affected US shale production. This greatly reduced freight volumes.

Second, while it didn’t spark a generalized recession, that particular part of the economy had its very own recession, and it was a nasty one. Ask anybody in the energy business and energy-producing regions how fondly they remember those years.

The current shipment contraction is potentially far worse. We can’t blame it on a sudden event like OPEC opening the spigots, nor is it focused on a particular sector. The Cass data shows declines everywhere, in everything.

Do I blame this on Trump’s trade war? Partially, yes, but I think more is happening. Years of flat wages forced many households to take on more debt. This has a cumulative effect; you can handle the payments for a while, but eventually things happen. Rising interest rates didn’t help. (In casual conversation, a friend told me his American Airlines Citibank card is now charging him 22% even though his credit score is over 800.)

This would once have been a normal pattern, not good but also not alarming. The economy had cycles and we dealt with them. But the long duration and weak magnitude of this growth phase is making the inevitable downturn potentially “feel” worse to many. The pain adds up and eventually becomes a recession.

via ZeroHedge News https://ift.tt/2GqOKc0 Tyler Durden

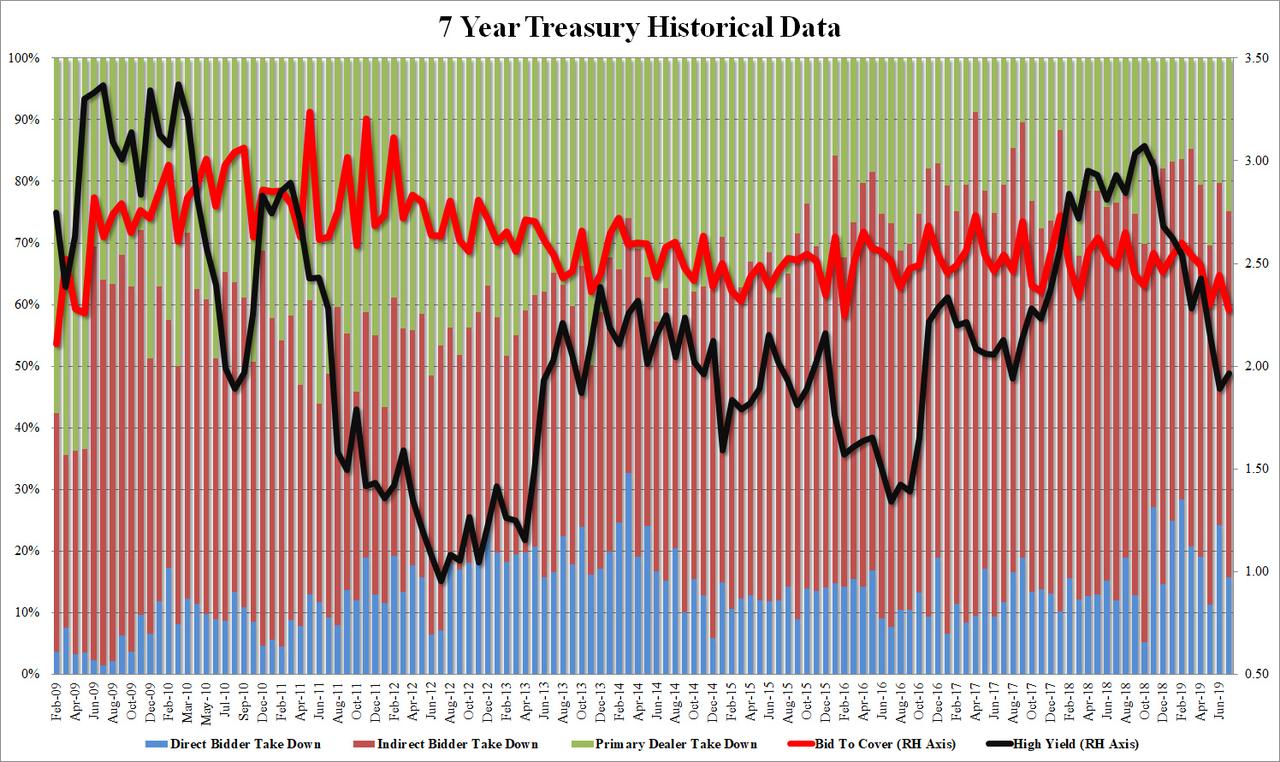

Starting with a medicore 2Y auction, progressing through one of the ugliest 5Y auctions in years, and concluding with today’s lackluster 7Y, this week’s treasury auctions – coming at a time when the Fed is about to push interest rates even lower – were unexpectedly weak.

Moments ago, the US Treasury sold $32 billion in 7Y paper at a yield of 1.967%, higher than last month’s 1.889% and a surprisingly big 1.4bps above the 1.953% when issued on a day when the rate market has generally whipsawed aggressively.

The bid to cover tumbled from 2.44 in June to just 2.274 today, which was not only below the 2.48 six auction average, but the lowest in two and a half years, since February 2016.

At least the internals were not terrible, with Indirects rebounding from last month’s 55.5% to 59.4%, just above the 58.7% recent average, however it was the Directs’ turn to slump, and with just $5.1BN of the bids tendered and accepted, the Direct takedown dropped to 15.8% from 24.23% last month, leaving 24.8% for dealers, slightly above the 19.9% recent average.

Overall, a poor, tailing auction concluding a week of dismal, disappointing Treasury sales, yet even despite the subpar demand, the Treasury still had little problem in finding buyers for another $110+ billion in US paper.

via ZeroHedge News https://ift.tt/2SF9eTu Tyler Durden

The Bushland Independent School District in Texas doesn’t have a substantial drug problem, but students as young as 12 will have to submit to drug testing if they wish to pursue their normal extracurricular activities.

Bushland students and parents have received a letter outlining the new program. Students participating in extracurricular activities or requesting a permit to park on campus will be tested at the beginning of the school year and could receive up to 10 random tests throughout the year. Under thenew rules, the teams and clubs that will now require testing include “football, volleyball, cross country, basketball, wrestling, golf, track, power-lifting, cheerleading, band, choir, theatre, UIL Academics, student council, lead council, FCCLA, robotics, VASE, speech and debate, FFA, chess, Ace Club, United Way Youth Council, gaming club, yearbook, Falcon Friends and 4H.”

If a student who consented to the first test then refuses to submit a saliva sample in a subsequent random test, the school will deem his or her test positive and will administer the associated consequences.

A positive test will be confirmed by a second test. Students will then have a two-day window to either challenge the results or provide a medical explanation. The district can request a student’s medical history from a doctor if it wishes to verify the explanation. If the positive result stands, students be suspended from activities, practices, competitions, parking, and social events held by the school. Students can appeal the decision, but the suspensions will stand during the appellate process.

“The number one reason why we’re implementing the policy is to help our students have a drug-free school,” Superintendent Chris Wigington tells Reason. “We also want to take away the peer pressure—we want to give them a reason to say ‘no,'” he adds, suggesting that students could use the drug policy as a way to tell peers that they’re uninterested in drugs and alcohol.

According to Wigington, the district isn’t facing a big drug problem. It implemented the new policy, he says, to be “proactive.”

On a national level, a 2018 report from the National Institute on Drug Abuse found drug use among teenagers at one of its lowest points in 20 years.

from Latest – Reason.com https://ift.tt/2JT5XwU

via IFTTT

When Michigan Rep. Justin Amash declared his independence from the Republican Party on July 4, he instantly became one of the most controversial politicians in America. Donald Trump immediately took to Twitter to denounce Amash as a “total loser” and “one of the dumbest & most disloyal” members of the GOP.

Whether or not you agree with the five-term congressman’s choice to leave the Republican Party, he’s anything but dumb and unprincipled. Amash has been the most consistently libertarian member of Congress since taking office in 2011, repeatedly voting to reduce the size and spending of the federal government, to stop mass surveillance of American citizens, and to end wars that he believes lack constitutional authorization.

Reason‘s Nick Gillespie sat down with Amash, the 39-year-old son of Middle Eastern immigrants, to talk about what it feels like to be independent, why he won’t be joining Alexandria Ocasio-Cortez’s social-justice “squad” anytime soon, whether he thinks Donald Trump is racist, if he’s going to run for president as a Libertarian, and why he believes we need to talk more about love in national politics.

Interview by Nick Gillespie. Edited by Ian Keyser. Intro by Paul Detrick. Cameras by Jim Epstein and Meredith Bragg.

Photo Credits: Photos of Rep. Justin Amash; Credit: Stefani Reynolds/CNP/Polaris/Newscom Photos of President Donald Trump; Credit: MICHAEL REYNOLDS/UPI/Newscom Photos of Rep. Alexandria Ocasio-Cortez; Credit: Tom Williams/CQ Roll Call/Newscom Photo of President Donald Trump; Credit: KEVIN DIETSCH/UPI/Newscom Photos of Rep. Justin Amash; Credit: Bill Clark/CQ Roll Call/Newscom Photo of Rep. Justin Amash; Credit: Tom Williams/CQ Roll Call/Newscom Photo of Rep. Justin Amash; Credit: Jim West/ZUMA Press/Newscom Photos of Rep. Justin Amash townhall; Credit: Jim West/ZUMA Press/Newscom Photo of Rep. Justin Amash; Credit: Jeff Malet/SIPA/Newscom Photo of U.S. Capitol; Credit: Frank Fell/robertharding/robertharding/Newscom Photo of Rep. Justin Amash; Credit: Tom Williams/CQ Roll Call/Newscom

from Latest – Reason.com https://ift.tt/2GvLV9B

via IFTTT

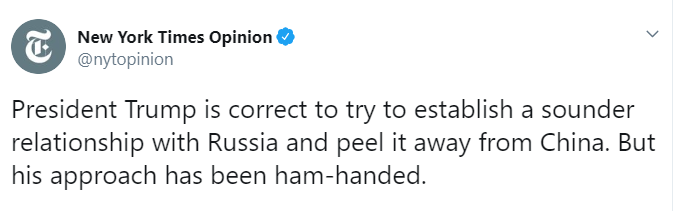

Meanwhile, in July 2019 no less than The New York Times editorial board laments that Trump-Kremlin relations are not close enough, as Trump’s “approach has been ham-handed” – the ‘paper of record’ now tells us.

Is this some kind of mea culpa? Not quite, perhaps more like being shamelessly self-unaware.

The above Times statement from this week is certainly real— absurd and astoundingly hypocritical as it all is (given the NY Times for years led the way with Russophobic and fear-mongering headlines, effectively undermining the ability of the US to establish a sounder relationship with Moscow, which it now calls for without an inkling of shame over its recent record) — but the below, unfortunately, is not…

via ZeroHedge News https://ift.tt/2OgWpA5 Tyler Durden

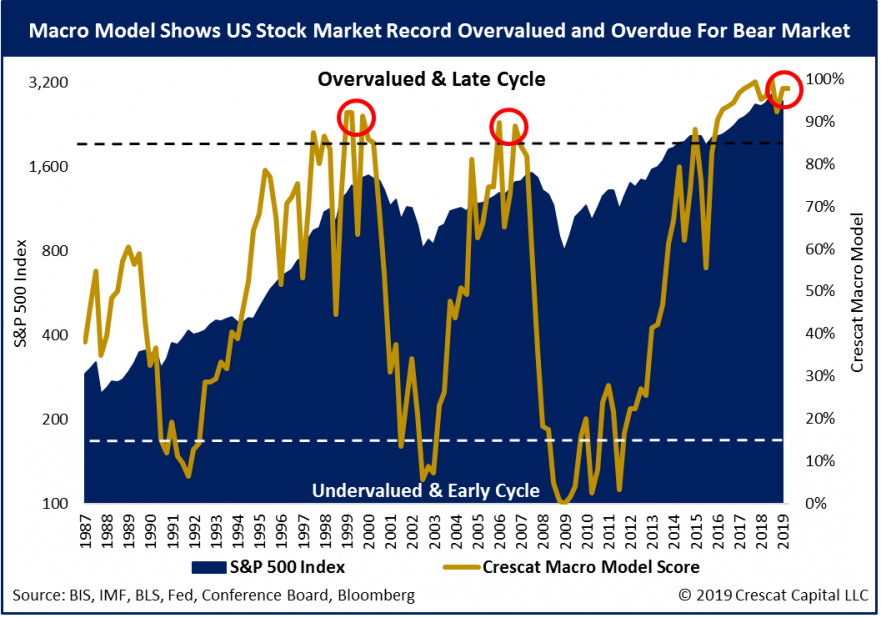

We believe there is an opportunity to capitalize on a material downturn in the business cycle based on the composite of timing and imbalance indicators in Crescat’s 16-factor macro model.

US Equity Markets

The downturn could be particularly brutal for US stocks because we are record late in a fading economic expansion and at historical high valuations relative to underlying fundamentals across a broad composite of eight measures that we follow at Crescat.

We hear two opposing valuation arguments from bulls today:

1. P/E ratios are reasonable; and

2. Valuations remain attractive relative to interest rates.

Let’s address them both.

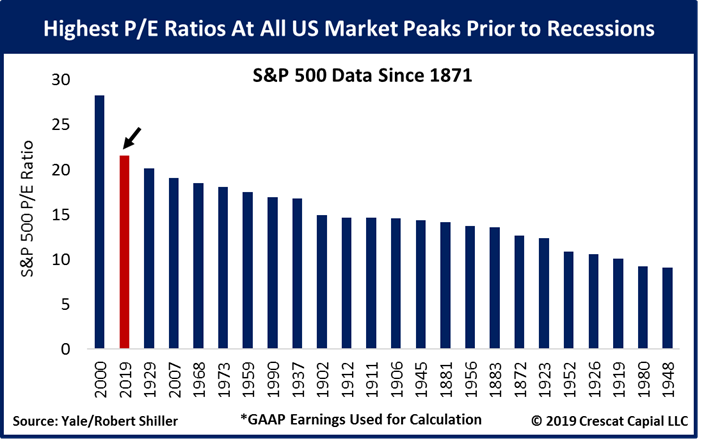

First off, P/Es often appear reasonable at business cycle peaks because that’s when earnings are their strongest. For instance, back in mid-1929, prior to the stock market crash and Great Depression, S&P 500 real earnings per share (on a GAAP standard) had been growing at a unsustainably high 20% year-over-year rate, almost as high as the fleeting 21% growth we just had in 2018. Similarly, profit margins are cyclical. They top out at the peak of an expansion, making P/Es appear artificially low. US corporate profit margins in 2018 were the highest they have been since 1929. P/Es are always a potential value trap at the peak of a cycle. But today, P/Es are not even that cheap. Going all the way back to 1871, today we would have potentially the second highest P/E ratio ever for the S&P 500 at a market top prior to a recession, worse than 1929 and the housing bubble.

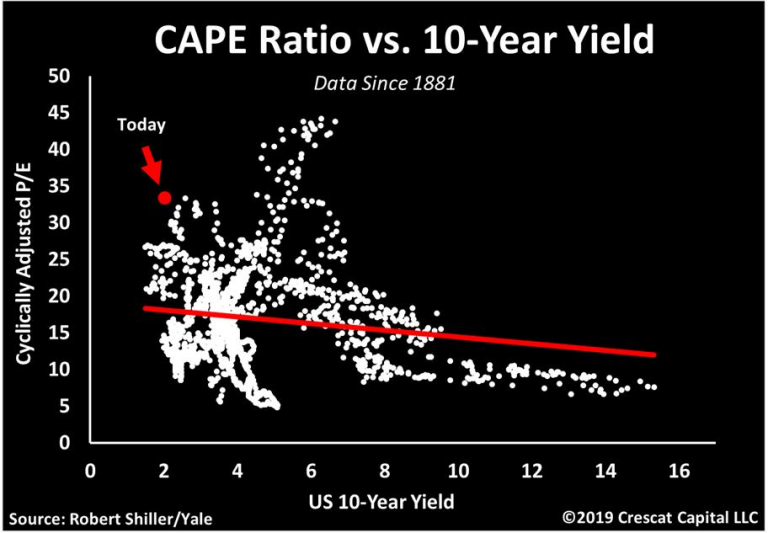

Tackling the second bull argument that low interest rates justify today’s high valuations, the flaw in this thinking is just as pronounced. The reality is that stocks have never been this expensive for how low the 10-year Treasury yield is today. It’s true that all else equal, low interest rates justify higher valuations. However, the lowest interest rates historically haven’t corresponded to the highest P/E markets because extremely depressed yields also signal fundamental problems in the economy. Ultra-low rate environments are often marked by highly leveraged economies where future growth is likely to be weak. Growth must also be discounted in the valuation formula.

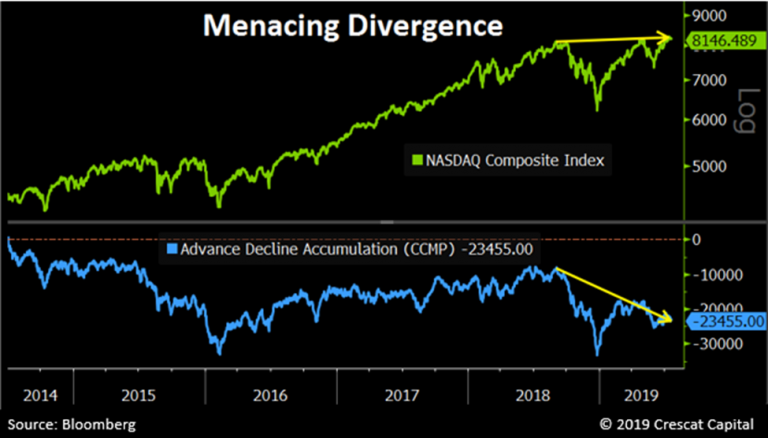

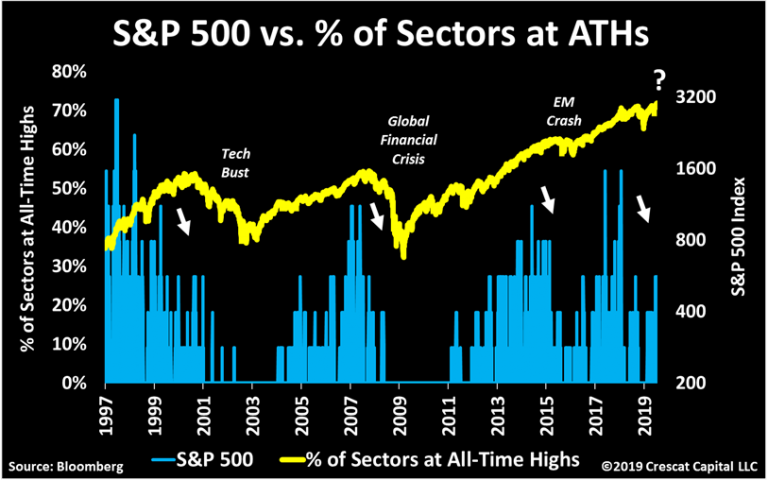

While many US equity indices have marginally broken out to new highs recently, they have done so in the face of weakening market internals. Equity indices are being propped up by a narrowing group of leaders. The deteriorating breadth is most evident in the NASDAQ Composite, home to today’s leading growth stocks. While the overall index has reached record levels, the number of declining stocks has significantly outpaced the number of advancing stocks since last September. The collapsing internals point to an exhausted bull market.

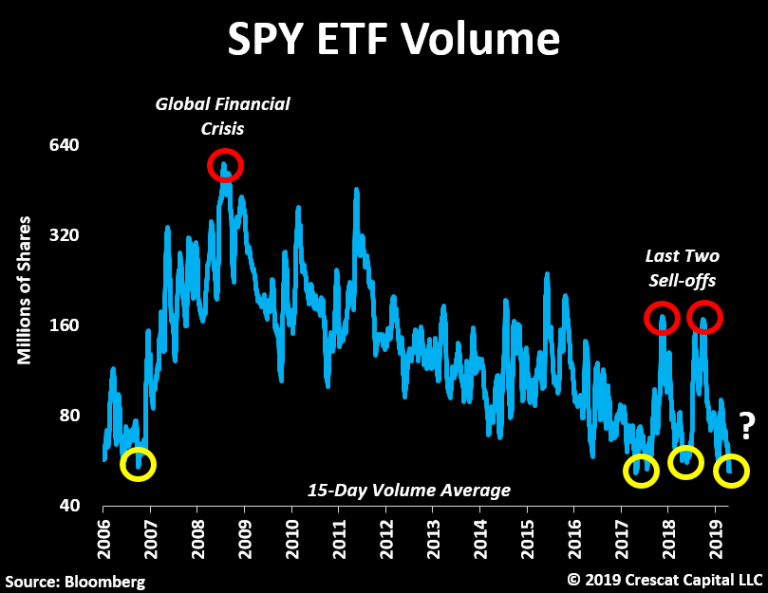

Stocks are also rising in defiance of extremely low volume. On July 16th, the SPDR S&P 500 ETF (SPY) had its lowest daily volume in almost 2 years. In a 15-daily average terms, volume is now as low as it was at the peak of the housing bubble and prior to the last two selloffs in 2018. Unusual calmness and breadth deterioration are not a good set up for record overvalued stocks.

The following chart is yet another illustration of how this recent rally in equities is running on empty, and again lacking substance. On July 15th, S&P 500 reached record levels, but only three sectors were at all-time highs. Market breadth today is faltering just as much as it did ahead of the last two recessions. In 2015, this was also the case, but back then only 20% of the yield curve was inverted. Now it’s close to 60%!

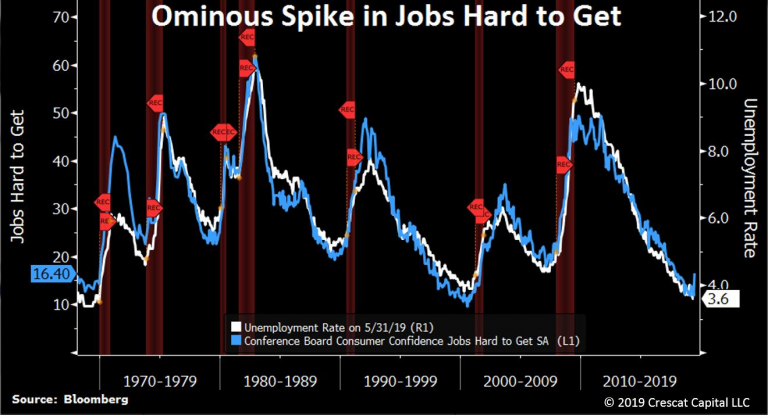

As we previously said, the unemployment rate has been one the most reliable contrarian indicators throughout history. It reaches a cyclical low prior to every recession since the 1970s. The year-over-year change, however, is what tends to confirm the turning points in the economy. Most of the times this rate shifted to positive, a market downturn followed. In this business cycle, the YoY change likely bottomed in late 2014 and it has now been flirting with the positive camp since then. However, other labor market indicators are already showing signs of weakening economic conditions. The Conference Board’s Jobs Hard to Get Index is one of them. It has recently spiked and is yet another classic late-cycle development in the economy.

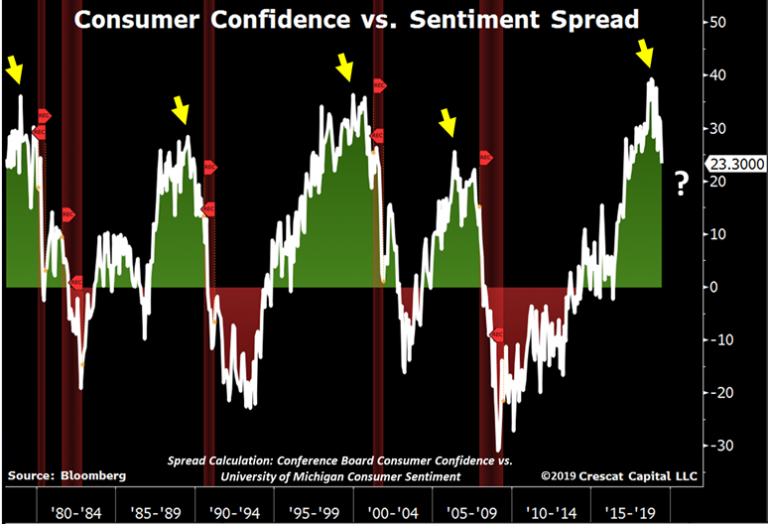

Consumer surveys are also critical to identify the stage of the economy we are in today. It’s another great contrarian indicator as strong consumer confidence has an uncanny relationship with market tops. We’ve noted this before, but since the 1960s, every time the Conference Board index surpassed the 135 level, it coincided with the peak of the economic cycle. The same source also reports two components of this survey that differentiate between consumer’s present situation and future expectations. As John Hussman originally pointed out, the spread between these two sub-indices tends to reach an extreme prior to a recession. That’s usually caused by consumers’ future expectations starting to fall first. The University of Michigan also publishes a survey on consumer sentiment. That compared with the Conference Board index forms another important indicator. All previous declines from cyclical highs in the spread between these two indices led to recessions. This time, the spread is plunging after reaching record levels.

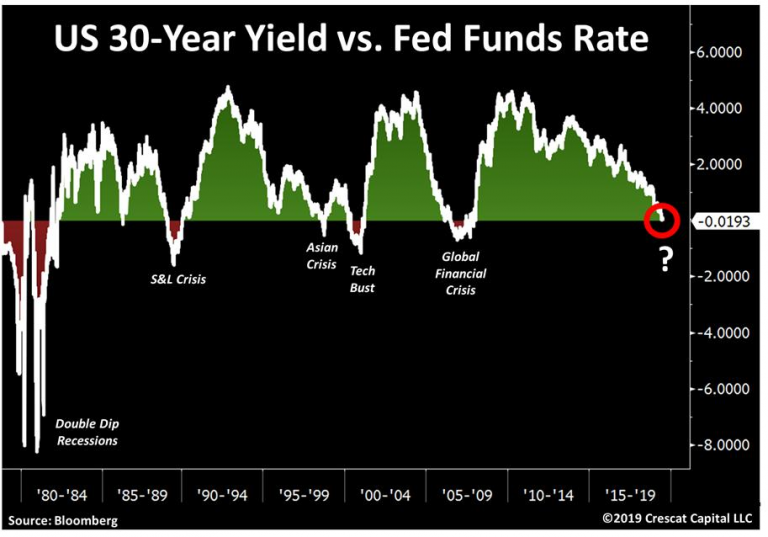

Crescat’s robust calculation of percentage of inversions in the US yield curve remains at recession-signaling levels. Over 55% of all 44 spreads are now inverted, being just as much as it was at the peak of the tech and housing bubbles. Nevertheless, another important development in credit markets occurred in the first week of July. As show below, the US 30-year yield dropped below the upper bound of the federal funds rate (FFR) for the first time since the global financial crisis. It’s one more bearish signal that adds to Crescat’s fire hose of cycle-ending macro data. The same warning occurred ahead of the GFC, tech bust, Asian crisis, S&L crisis, and 1980’s double dip recessions. The only false signal was in 1986, but one could argue that it did ultimately lead to the 1987 crash. Above all, as of July 2nd, we had the entire US Treasury curve below the Fed overnight rate. Perhaps the bond market is trying to tell us something.

Cracks in the market are spreading and it could be pointing to a market meltdown. Copper, for instance, is now diverging from the S&P 500 by over 35% since September of 2017. Last time this separation reached similar extremes was at the September 2018 market peak. Dr. Copper is reputed to have a Ph.D. in economics because of its ability to help predict turning points in the global economy. Because of copper’s widespread applications — from homes and factories to electronics and power generation and transmission — strengthening or weakening demand for the red metal can be a leading indicator for the economy at large. The decline of the industrial metal itself doesn’t necessarily tell us enough to call for a downturn in the economic cycle. However, its deterioration versus other risk assets in combination with a litany of macro indicators adds conviction to our overall bearish thesis.

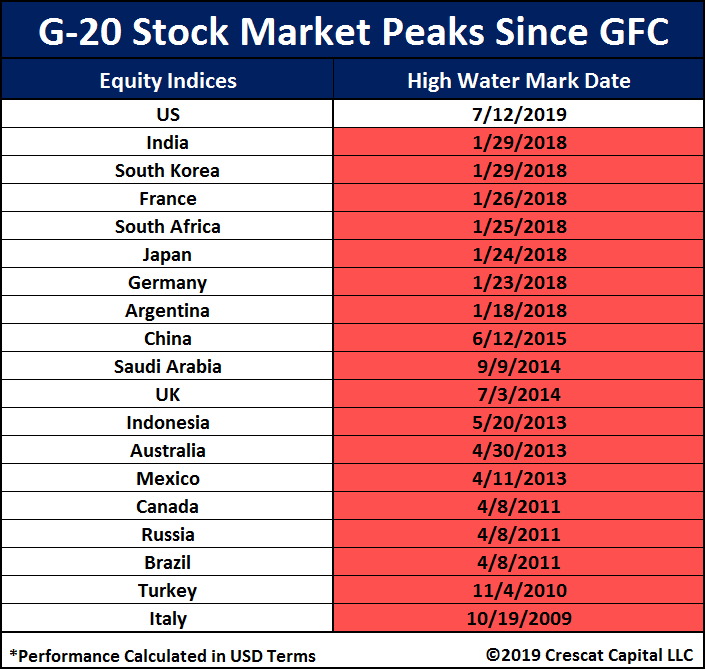

The US is the only equity market in the world to make new highs recently in US dollar terms. Every other G-20 index already peaked a long time ago, a troubling divergence. We believe the US stock market is likely to be the one to catch up to the downside.

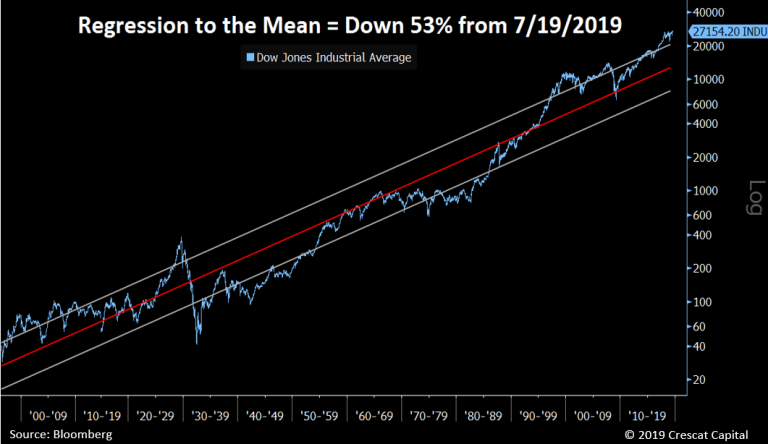

The US market is fundamentally and technically overvalued to an extreme. But, how much should we expect it to be down in a coming bear market? Just to get to mean historical valuations, it could be a 50% plunge. The problem is, a 50% decline would equate to the highest ever valuation at the depth of a bear market and recession in the US, so it could be a best-case scenario. That is how over-valued the US equity market is today! The downside in the market today is perhaps easiest to visualize in a logged version of the longest running US stock index, the Dow Jones Industrial Average.

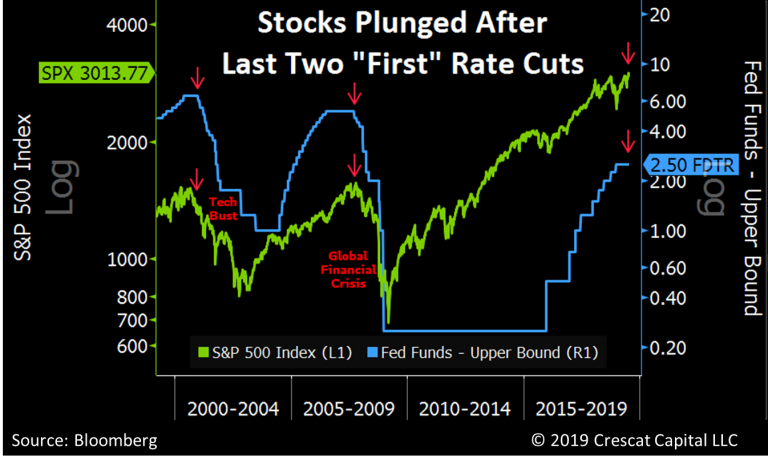

Conventional wisdom is that the first Fed rate cut is bullish, but this was not true with the last two business cycles as we clearly show in the chart below. It will likely not be true in this one either because we are record late into the expansion at historic high valuations. It’s true that all else equal, monetary easing is fundamentally bullish for stocks and the economy, while tightening is bearish. The problem is that central bank policy works with a lag. The delayed reaction to Fed interest rate policy is why our macro model uses the 24-month trailing rate-of-change in the federal funds rate as one of our factors to forecast the economy and the stock market.

The interest rate hikes and quantitative tightening of the last three years, are the substantial bearish macro drivers that have only now started to transmit into economic weakening in the US. Meanwhile, the Fed has also just acknowledged the deterioration in the overall global economy. We think the truth of the economic weakening matters more than the hope from imminent Fed easing. Only at the depths of the recession, when everyone else is panicking and dumping stocks that are already down substantially, should we get excited about Fed easing transmitting to a new bull market.

The Fed’s polices of near-zero interest rates and quantitative easing since the global financial crisis have created enormous asset bubbles in stocks and corporate credit. Investors’ speculative behavior is a natural reaction to cheap money and has played an integral role in inflating these bubbles. Just as asset prices rise in a positive feedback loop of easy credit, investor speculative behavior, consumer and business spending, so they decline in the opposite self-reinforcing fashion: credit defaults, credit tightness, investor risk aversion, and business and consumer retrenchment. Such is the natural ebb and flow of the business cycle.

The property market in the US is also richly valued, in our view, though home prices are not as frothy relative to income and household debt as they were in the housing bubble. The big housing bubbles in the world today by these measures are in China, Hong Kong, Canada, and Australia.

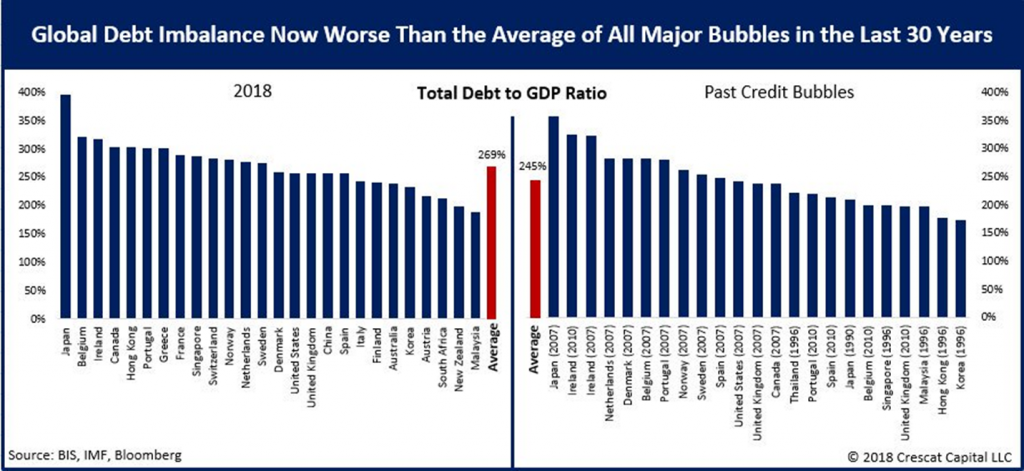

Because the US dollar is the largest fiat reserve currency, the Fed’s past accommodative policies has allowed other countries to pursue their own easy money schemes and accumulate record levels of debt. Across the globe, these levels are higher on average than they were prior to all major credit busts of the last 30 years.

China

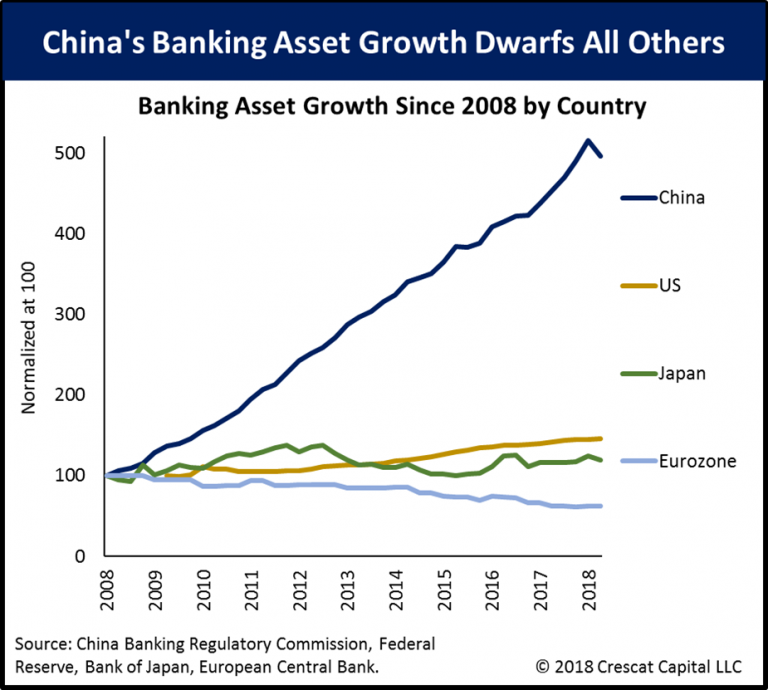

We have written extensively about China’s currency and credit bubble in past letters. China was responsible for over 60% of global GDP growth since the global financial crisis. The country’s massive investments in non-productive infrastructure assets was financed on credit and created high GDP growth but failed to add wealth or debt-servicing capacity. China has created an enormous currency and credit bubble in the process. The problem is that its central planners accomplished this incredible economic growth through an unsustainable growth in fractional reserve bank credit. Since 2008, China’s banking system assets have grown 400% to USD 40 trillion!

This insane level of expansion for a large economy was made possible because China’s communist leaders mandated high lending growth from its state-owned banks. At same time, they ignored the true write-down of non-performing loans.

As a result, we believe the value of China’s banking system today is grossly mismarked. The Chinese financial system in our view is a Ponzi scheme poised to unravel and is likely to be a major contributor to the coming global economic downturn. The Chinese citizens are the primary creditors who could be on the line, but the rest of the world that has invested in China will almost certainly suffer with them.

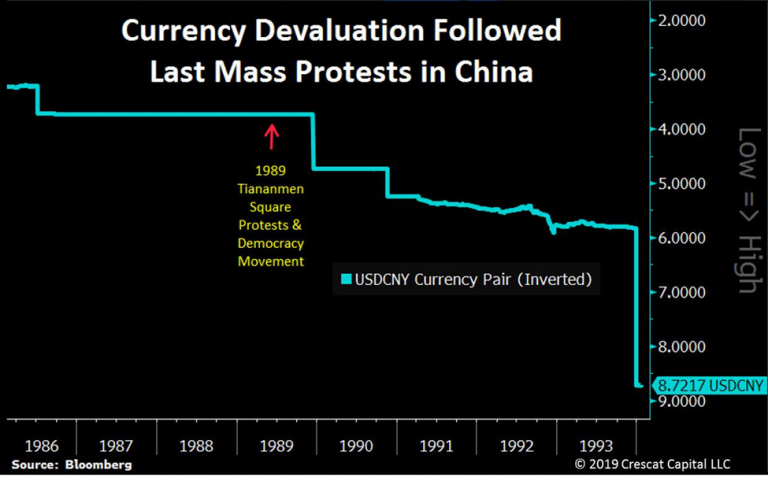

We believe the Chinese government will be forced to print money to recapitalize its banks and bail out its citizens to attempt to quell social unrest. The massive monetary dilution could lead to a currency crisis which is the lesson of almost every emerging market credit bubble in history from Latin America to Asia. Currency crisis is also the ultimate consequence of economic failure of centrally planned communism as we have learned from the Soviet Union to Venezuela.

Our outlook for both the Chinese yuan and Hong Kong dollar is extremely bearish and we are positioned accordingly in our global macro fund. The warning signs of the coming Chinese crisis are everywhere from the Trump administration’s year-long hardball on Chinese trade, to the recent Chinese government seizure of failed Baoshang Bank, to the current mass anti-Chinese Communist Party protests in Hong Kong.

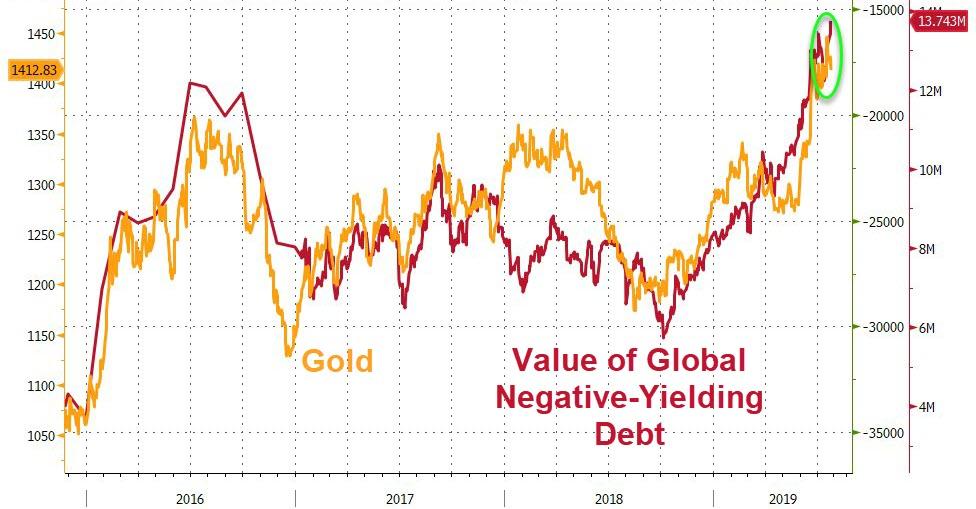

Precious Metals

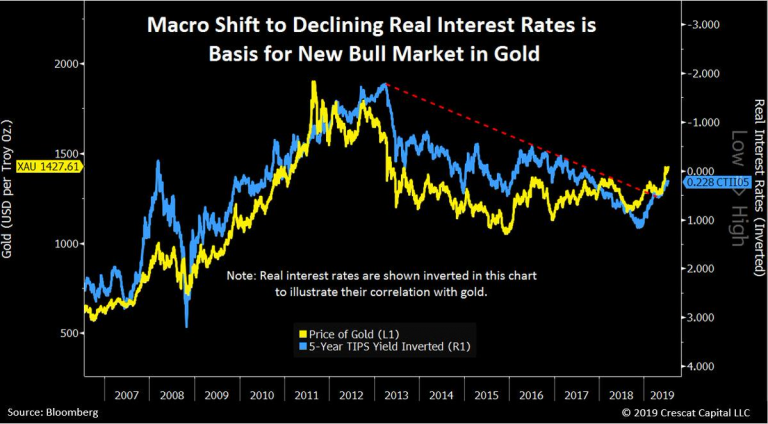

Precious metals are one of the few pockets of this market offering tremendous value to hedge against extreme monetary policies, bursting asset bubbles, and record global leverage. We see this opportunity playing out across gold, silver and related mining stocks. Gold is the ultimate form of money with a long history of storing value for investors and outperforming risk assets during market downturns. In our view, a new wave of global fiat currency debasement polices is now in its early stages. Gold should become a core asset for those who believe in this macro development, but it is still widely under-owned today.

With the Fed shifting back to easing mode as the global economy is faltering, new fuel has ignited a precious metals fire. It is still very early in the game in our analysis. Rate cuts point to a new trend of declining real yields to drive precious metals higher even before inflation returns. Below we show seven-year trends in real rates and gold that have just reversed.

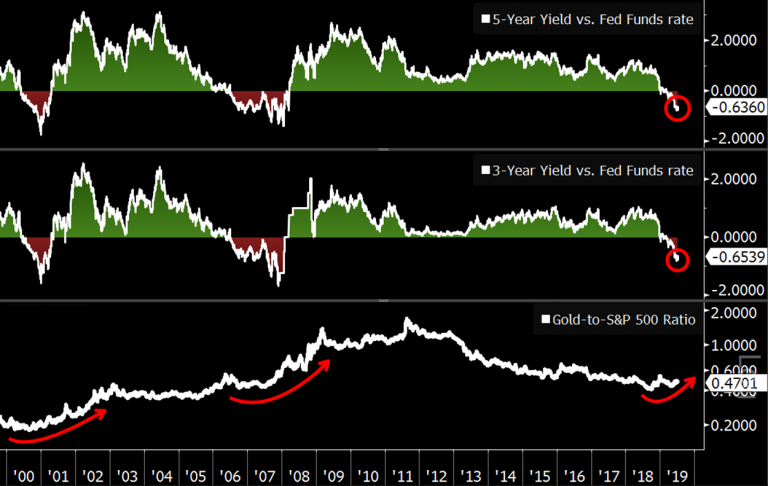

Credit markets tend to serve as a bellwether for stocks and the economy, and rising yield curve inversions happen to be great times to buy gold and sell stocks. For instance, 3 and 5-year yields have recently dipped below Fed funds rate for the first time since the global financial crisis and the tech bust. As history has shown, this is bullish for the gold-to-S&P 500 ratio.

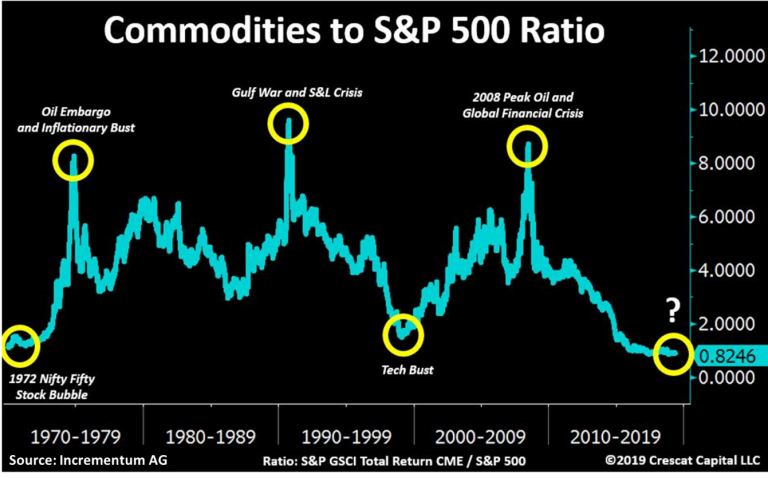

Another way to see how incredibly undervalued precious metals are relative to other risk assets is by looking at the relative performance. The commodities-to-S&P 500 ratio has just reached a fresh 50-year low. The last times we had such historic imbalances we were at the peak of the 2000 tech and the 1972 “Nifty Fifty” stock bubbles. If one uses a simpler version of this relationship, using the Dow Jones Industrial Average index, the ratio is well below the cyclical 1929 lows that lead to the Great Depression.

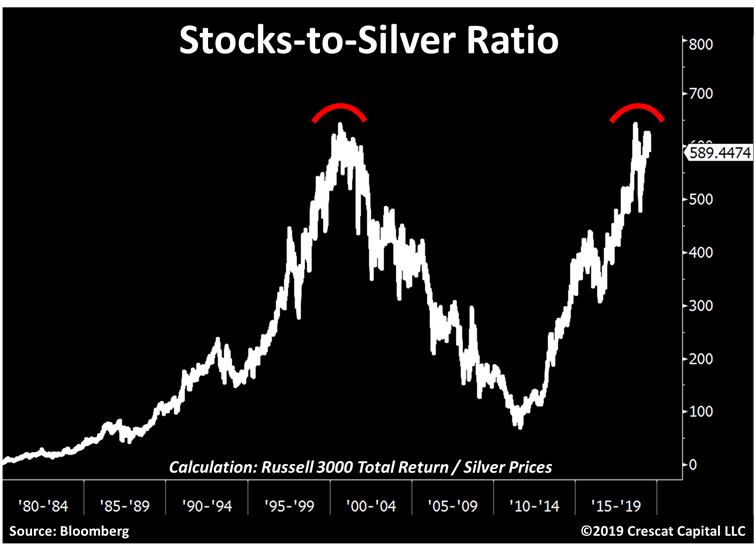

Silver, a more speculative version of gold, also looks historically cheap. One way to see this is by comparing it against the total return for broad US stocks. The Russell 3000-to-silver ratio is still near all-time highs. This puts into perspective the incredible opportunity likely ahead of us today and how truly early and undervalued it is. In technical terms, look at the double top formation after a retest of peak tech bubble levels.

We also feel very strongly that gold and silver mining stocks are undervalued as the current macro set up seems largely optimistic for precious metals. This entire industry has been through and eight-year bear market with some of these stocks down by over 80% since 2011.

via ZeroHedge News https://ift.tt/30UZRSo Tyler Durden

After spending nearly a month in a Swedish jail, where he was denied bail for being a “flight risk”, American grammy-nominated rapper A$AP Rocky has been officially charged by prosecutors with Assault Causing Actual Bodily Harm. If convicted, Rocky could be sentenced to up to 2 years in a Swedish prison.

The charges suggest that President Trump’s attempts to intervene in the case have been mostly ignored by the Swedes, who have insisted that their judicial system shouldn’t be tampered with. President Trump said on Twitter last Friday that he personally pledged to secure A$AP Rocky’s bail, and that he decided to personally reach out to the Prime Minister of Sweden on Rocky’s behalf after discussing the case with Kanye West.

However, prosecutors said Thursday that Rocky will be held in jail until his trial, a date for which has not yet been set. The trial will likely be held within the next two weeks, and could last for as long as three days. Two members of Rocky’s crew have also been charged with the same crime following a brawl outside a venue where Rocky was et to perform. They have also been held pending trial, TMZ reports.

Prosecutors reportedly told TMZ Thursday morning that they will not recommend the full 2-year sentence…but Rocky could still be hit with the maximum sentence if the sentencing judge decides it.

Videos that have circulated online show a man tailing Rocky and his crew despite being asked several times to leave them alone. In the beginning, A$AP can be heard telling his associates to calm down saying that nobody wants to go to jail. But the man – who was not charged – continued to instigate, and Rocky eventually lost his cool, and threw him to the ground in dramatic fashion.

Rocky’s antagonist was not charged with a crime by Swedish police.

Many of Rocky’s supporters in the US have accused the Swedish legal system of racism for prosecuting Rocky and his associates, but not the other man who was involved in the brawl. Rocky’s mother said in an interview with TMZ that she “don’t want to pull the race card…but that’s what it’s looking like.”

However, Sweden has refused to budge, and has insisted that Rocky will be prosecuted just like anybody else.

via ZeroHedge News https://ift.tt/2LHYB1y Tyler Durden

After receiving a speeding citation, defendant Dr. Nickesh Pravin Shah duped an employee into signing a letter falsely stating that defendant was responding to a medical emergency at the time of the traffic stop. Defendant’s attorney eventually entered the letter in evidence at his traffic trial.

After the traffic trial, defendant was charged with violating Penal Code sections 132 and 134 by preparing and offering the forged letter as false evidence. A jury found defendant guilty of both offenses, and the trial court suspended imposition of sentence and placed defendant on 36 months’] probation….

In early 2013, defendant accepted through a staffing agency a temporary position as a physician at a health clinic. The clinic was small, with just two physicians and a staff of approximately eight to nine people. The clinic hired defendant to care for the patients of one of the doctors who was on leave.

On the morning of April 3, 2013, at approximately 10:00 a.m., defendant was driving to work when a California Highway Patrol (CHP) officer stopped him for speeding. At the time of the stop, defendant was late for work, which was not unusual.

When informed of the reason for the stop, defendant told the officer that he was en route to a medical emergency and needed to be there within the next 10 minutes. The officer asked defendant the nature of the medical emergency, and defendant responded, “A gall bladder.” Defendant told the officer he would be performing surgery on the patient.

The officer asked defendant if there was someone who could confirm this information. Defendant gave the officer the name and telephone number of a supervisor at the clinic. Defendant said she would know if there was an emergency. The officer called the number and spoke to the supervisor. The supervisor denied there was an emergency and told the officer that defendant “was just late to see his regularly scheduled patients.” {This was not the first time that defendant falsely claimed he was responding to an emergency to avoid a speeding ticket. At trial, a San Francisco police officer testified that when he stopped defendant for speeding in 2010, defendant told the officer he was “on an emergency call” heading to the University of California, San Francisco, Medical Center. The officer asked for proof, but defendant was unable to substantiate the emergency.}

When the officer relayed this information, defendant responded that the supervisor must be working on the other side of the facility and unaware of the emergency. The officer, unpersuaded, cited defendant for speeding, but suggested that the district attorney might dismiss the citation if defendant could provide documentation showing that he was, in fact, responding to an emergency.

A couple of weeks later, defendant had his office manager sign a letter relating to the traffic stop. The letter stated: “This letter is to confirm that [defendant] was on his way to an emergency in order to attend to a patient at this facility on April 3rd, 2013[,] at 10:00 a.m. with severe abdominal pain and concern for a gall bladder infection.” The letter was dated April 16, 2013. Defendant, through his attorney, subsequently offered the letter in evidence at the trial on his speeding citation. The traffic court judge nevertheless found defendant guilty.

After the traffic trial, the prosecutor filed a felony complaint against defendant charging him with violations of Penal Code sections 132 and 134 for preparing and offering false and fraudulent evidence at the traffic trial…. The jury found defendant guilty of violating sections 132 and 134.

from Latest – Reason.com https://ift.tt/2OgQo6t

via IFTTT