What some auto manufacturers and industry experts were passing off as a slight hiccup for the auto industry is rapidly turning into a full-scale recession if not all out depression, one complete with a litany of layoffs in the global auto industry as sales in major countries like the United States and China have been steadily deteriorating for the last 18 months.

We’ve already seen massive planned layoffs from US auto makers like Ford, and now Nissan is the latest to join the mass layoffs bandwagon, with Kyodo reporting that Nissan will cut over 10,000 jobs globally, or over 7% of its entire global workforce.

This is likely in response to the deteriorating automotive market in China: recall in early July we repored that Nissan’s sales in China from January to June totaled 718,268 units, a 0.3% y/y decline.

In May, we reported that countries like China, the United Kingdom, Germany, Canada and the United States had all seen at least 38,000 job cuts over the last six months in the automotive sector. Daimler CEO Dieter Zetsche said in May that “sweeping cost reductions” are ahead to prepare for what he is calling “unprecedented” industry disruption

And now cue Nissan.

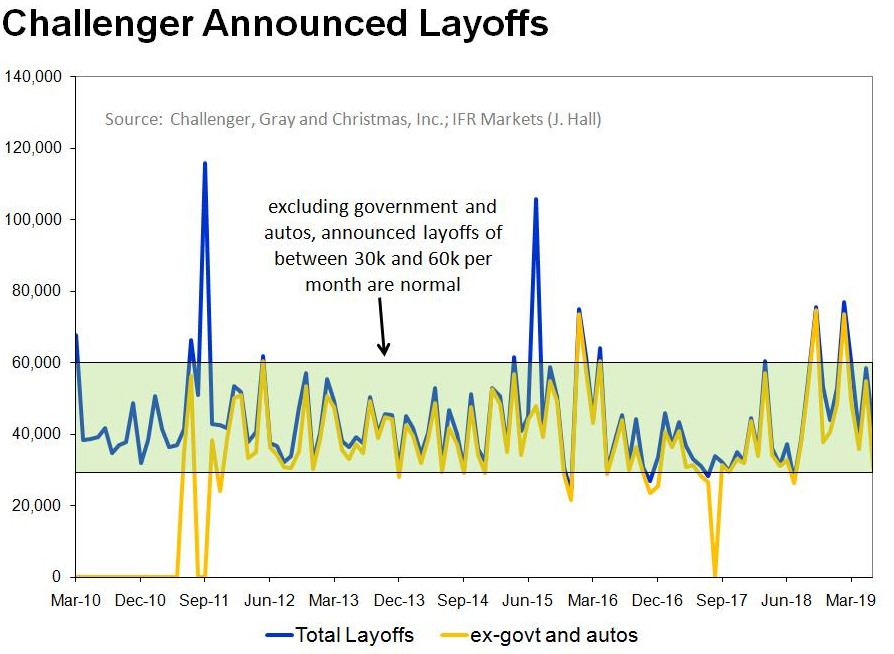

A few weeks ago we algo reported that over 25% of all June job cuts came from the automotive sector, according to Managing Economist for Refinitiv Jeoff Hall. Hall commented on Twitter that the industry’s 10,904 redundancies were the most in seven months and the second most in seven years. Hall also noted that excluding autos, there were only 31,073 job cuts in June, the fewest in 11 months, in low-normal range.

We reported about Ford’s plans to cut another 7000 jobs, representing 10% of its workforce worldwide, about a month ago. And the recession, which was likely due to happen regardless of market conditions, comes at the worst possible time. It could be exacerbated by the ongoing trade war, which foreign carmakers have warned could put 700,000 American jobs at risk.

This chart shows the job reductions in the six months prior to June 1.

Furthermore, at the beginning of June we noted that Bank of America had said that “the auto cycle had peaked”.

While Bank of America attributed much of the downturn in the manufacturing sector to the ongoing trade war, it singled out the automotive industry as a specific area for concern. Calling the problem a “classic story of demand/supply mismatch”, the bank pointed out that producers continue to ramp up output at a time when demand has softened.

via ZeroHedge News https://ift.tt/2Y0jyuQ Tyler Durden

As the FBI investigated whether Donald Trump was working with Russia, top bureau attorney Andrew Weissmann secretly approached a Ukrainian Oligarch’s US attorneys seeking dirt on President Trump, according to The Hill‘s John Solomon.

In exchange, the FBI was willing to drop an ongoing case against the Ukrainian – Dmitry Firtash, who was hit with 2014 corruption charges in Chicago alleging that he engaged in corruption and bribery in India linked to a US aerospace deal.

According to a defense memo recounting Weissmann’s contacts, the prosecutor claimed the Mueller team could “resolve the Firtash case” in Chicago and neither the DOJ nor the Chicago U.S. Attorney’s Office “could interfere with or prevent a solution,” including withdrawing all charges. “The complete dropping of the proceedings … was doubtless on the table,” according to the defense memo. –The Hill

Dmitry Firtash at the supreme court in Vienna on June 25

It was a desperate move for the FBI – which was grappling with a lack of evidence against Trump as the Steele dossier was turning out to be an embarrassing dud (“There’s no big there there,” lead FBI agent Pete Strzok texted a few days before Weissmann’s overture, writes Solomon).

At the same time, the DOJ’s evidence against Firtash in the 2014 case was also falling apart.

Two central witnesses were in the process of recanting testimony, and a document the FBI portrayed as bribery evidence inside Firtash’s company was exposed as a hypothetical slide from an American consultant’s PowerPoint presentation, according to court records I reviewed. –The Hill

In short, the DOJ had two high profile cases which were unraveling as Weissmann reached out.

Two weeks before the offer was made, Robert Mueller was appointed special counsel – tasked with continuing and expanding upon the FBI’s substantial investigative efforts (including espionage) against Donald Trump and anyone in his orbit.

Firtash’s legal team thought Weissman was probably overstepping his authority, as the special counsel’s office was still subject to DOJ oversight. They were also taken aback after Weissmann went to extraordinary lengths to enlist the Ukrainian by sharing prosecutorial theories the FBI was forming about Trump and his team.

Prosecutors in plea deals typically ask a defendant for a written proffer of what they can provide in testimony and identify the general topics that might interest them. But Weissmann appeared to go much further in a July 7, 2017, meeting with Firtash’s American lawyers and FBI agents, sharing certain private theories of the nascent special counsel’s investigation into Trump, his former campaign chairman Paul Manafort and Russia, according to defense memos.

For example, Firtash’s legal team wrote that Weissmann told them he believed a company called Bayrock, tied to former FBI informant Felix Sater, had “made substantial investments with Donald Trump’s companies” and that prosecutors were looking for dirt on Trump son-in-law Jared Kushner.

Weissmann told the Firtash team “he believes that Manafort and his people substantially coordinated their activities with Russians in order to win their work in Ukraine,” according to the defense memos. And the Mueller deputy said he “believed” a Ukrainian group tied to Manafort “was merely a front for illegal criminal activities in Ukraine,” and suggested a “Russian secret service authority” may have been involved in influencing the 2016 U.S. election, the defense memos show. –The Hill

Despite being ‘holed up’ in Austria for five years while fighting extradition charges to the US, Firtash turned down Weissmann’s plea overtures. His lawyers told John Solomon that he rejected the deal because he didn’t have credible information or evidence against Trump, Manafort, or anyone else Weissmann laid out in his theories.

In sealed Austrian court filings earlier this month, Firtash’s attorneys compared the DOJ’s 13-year investigation to medieval inquisitions, citing Weissman’s approach as politically motivated – and noting the “possible cessation of separate criminal proceedings against the applicant if he were prepared to exchange sufficiently incriminating statements for wide-ranging comprehensively political subject areas which included the U.S. President himself as well as the Russian President Vladimir Putin.”

Hilariously, the DOJ won a ruling in Austria to secure Firtash’s extradition to Chicago – Austrian officials reversed course after his legal team filed new evidence that included the Weissmann overture, according to the report.

That new court filing asserts that two key witnesses, cited by the DOJ in its extradition request as affirming the bribery allegations against Firtash, since have recanted, claiming the FBI grossly misquoted them and pressured them to sign their statements. One witness claims his 2012 statement to the FBI was “prewritten by the U.S. authorities” and contains “relevant inaccuracies in substance,” including that he never used the terms “bribery or bribe payments” as DOJ claimed, according to the Austrian court filing.

That witness also claimed he only signed the 2012 statement because the FBI “exercised undue pressure on him,” including threats to seize his passport and keep him from returning home to India, the memo alleges. That witness recanted his statements the same summer as Weissmann’s overture to Firtash’s team.

Firtash’s lawyers also offered the Austrian court evidence of alleged prosecutorial wrongdoing. –The Hill

Embarrassingly for the DOJ, a key document they submitted to Austria in support of Firtash’s extradition allegedly from his corporate files and purportedly showing evidence that he sanctioned a bribery scheme in India was actually a slide from a powerpoint presentation created by the McKinsey consulting firm as part of a hypothetical presentation on ethics for the Boeing Corp.

Firtash’s U.S. legal team told me it alerted Weissmann to DOJ’s false portrayal of the McKinsey document in 2017, but he downplayed the concerns and refused to alert the Austrian court. The document was never withdrawn as evidence, even after the New York Times published a story last December questioning its validity. –The Hill

“Submitting a false and misleading document to a foreign sovereign and its courts for an extradition decision is not only unethical but also flouts the comity of trust necessary for that process where judicial systems rely only on documents to make that decision,” Firtash’s US legal team told Solomon. “DOJ’s refusal to rescind the document after being specifically told it is false and misleading is an egregious violation of U.S. and international law.“

via ZeroHedge News https://ift.tt/2Yq9lHy Tyler Durden

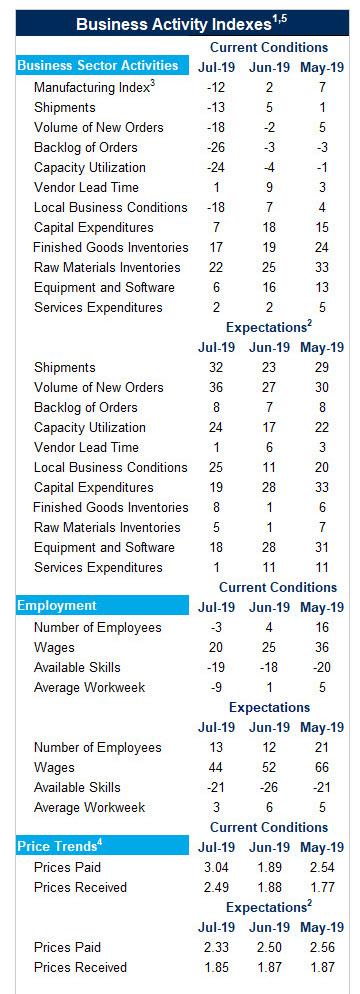

After a handful of mixed regional Fed survey, moments ago the Richmond Fed printed for the month of June, and if it serves as a tiebreaker, then the US economy is deep in a recession.

Expected to rebound modestly from already a near-contractionary print of 3 to 5 following the recent euphoric Philly Fed print, the mid-Atlantic index instead suffered its biggest drop in two years, dropping by 14 points to a whopping -12, the lowest print since January 2013…

… as all three components — shipments, new orders, and employment — registered declines.

The biggest reason behind the unexpected plunge – the orderbook has suddenly disintegrated as order backlogs fell to −26, the lowest reading since April 2009.

It gets worse: firms reported worsening local business conditions, as this index dropped from 7 to −18, its largest one-month drop on record. Of course, there was optimism, and respondents remained somewhat optimistic that conditions would improve in the coming months.

The weakness was broad based as Survey results further indicated that employment and the average workweek declined in July. However, wage growth continued among survey respondents. Firms continued to struggle to find workers with the necessary skills and expect that struggle to continue in the next six months.

The full table of components is below:

and visually:

The growth rates of both prices paid and prices received rose in July, as growth of prices paid outpaced that of prices received. Survey participants, on average, expected growth of both prices paid and prices received to slow in the near future.

The biggest paradox, however, is that just last week the Beige Book for the Richmond Area reported the following:

Since our previous Beige Book report, the Fifth District economy grew at a modest rate. Manufacturers saw a slight increase in shipments and new orders, but continued to face challenges from the current trade environment. Import volumes remained strong and, at one port, the composition of imports is shifting from China to other Asian countries.

Meanwhile, the actual Richmond Fed survey shows collapsing orders, shipments and employment.

It’s almost as if the US is now desperate to overtake China in the completely made up economic bullshit department, simply to justify whatever policy measure the Fed is undertaking next.

via ZeroHedge News https://ift.tt/2Z5QtKZ Tyler Durden

After May’s surprise rebound, existing home sales were expected to slow in June and dropped more than expected (falling 1.7% MoM against expectations of a modest 0.4%) to 5.27mm SAAR.

“Sales refuse to break out higher,” Lawrence Yun, NAR’s chief economist, said at a briefing in Washington.

“It doesn’t make economic sense” with job creation, rising wages and the stock market reaching records.

This is the 16th month of annual declines in existing home sales…

Home purchases declined in the South, the biggest region, to the slowest rate since January. Sales fell to a three-month low in the West. They increased in the Midwest and Northeast.

While rates have tumbled – helping affordability – the median home price rose 4.3% from last year to $285,700, erasing that affordability edge.

via ZeroHedge News https://ift.tt/2Z6gk5z Tyler Durden

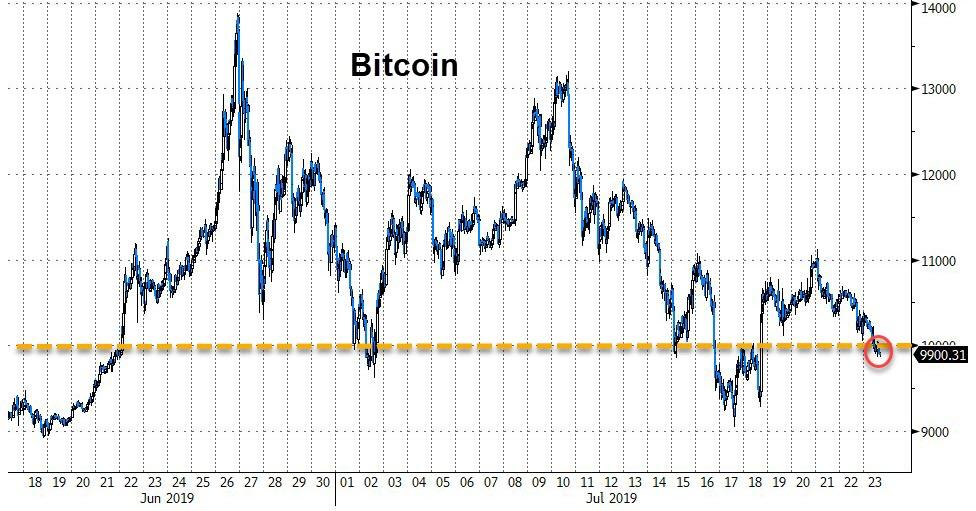

However, demand remains high elsewhere in the world, as CoinTelegraph’s William Suberg details, Venezuelans traded more bolivars for Bitcoin than ever before last week, but the statistics say more about fiat than cryptocurrency.

Data from Coin Dance, which tracks trading activity on P2PexchangesLocalbitcoins, Paxful and Bisq, confirmed the seven days to July 20 were Venezuela’s biggest on record.

During that period, users on LocalBitcoins alone generated volumes of over 57 billion bolivars, beating the previous all-time high of 49 billion, which appeared in the previous week.

Weekly LocalBitcoins Volume (Venezuelan Bolivar) Courtesy of Coin.dance

As Cointelegraph reported, Venezuela’s currency continues to suffer from runaway inflation, which estimates claim has reached 10,000,000%, leading citizens to resort to alternative means of storing value.

Yet as the bolivar count on Localbitcoins keeps growing, in Bitcoin terms, the number is falling. The 57 billion figure for last week equated to just 574 BTC — considerably less than in some previous weeks earlier this year.

Underscoring the weakening bolivar, Venezuela’s cryptocurrency trading is not supported by the government, which also imposed embargoes on foreign currency.

Earlier this year, the Lightning Torch transaction relay raised 0.4 BTC ($4,000) in funds among Bitcoin users for Venezuelans unable to escape the country.

via ZeroHedge News https://ift.tt/2Ob6lLf Tyler Durden

The next in a long line of moments of truth for the ECB will soon be upon us. And in typical fashion the market is gearing up to have a last-minute debate about whether they will stick to consensus expectations or surprise with a move this month rather than teeing one up for September. Traders love to drive themselves crazy. To make matters more fun, there isn’t even agreement on what sooner rather than later, bigger rather than less, will mean for the currency. Such is the extent of dollar bearishness.

Getting in under the wire, lest anyone be under the misapprehension that rate cutting is anything but a global phenomenon, are dovish comments by officials at several other central banks. They aren’t scheduled to imminently do anything, but seemingly want to make sure everyone knows they are on the case. This non-currency war gets more interesting by the week.

RBA’s Christopher Kent could have been speaking for a lot of his global peers when he said, that, in response to their recent rate cuts, the exchange-rate transmission mechanism has been working as one would expect. Adding, with what seems like great candor, without the rate cuts “the Aussie dollar might have been higher.” And I’m sure EUR/JPY being within shouting distance of the post-flash crash year-to-date lows wasn’t lost on BOJ’s Haruhiko Kuroda. The RBNZ just admitted to taking a new look at potential unconventional monetary policy should it be needed. So much for any breakout for the kiwi above $0.6815. Not to be outdone, Bank of Korea Governor Lee Ju-yeolassured parliament that he’s also ready to act if needed.

It has been quite a day on the monetary-policy front. No wonder so many of the world’s equity indexes are having a happy day.

It’s a testimony to just how ubiquitous are the promises and hints at further liquidity infusions, that PBOC Governor Yi Gang sounded positively hawkish when he said earlier Tuesday that China’s interest rates are at an appropriate level. More importantly, given all the allusions to “global headwinds”, he said the bank will set interest rate policy “based on its own situation.” Cue the next round of trade talks.

But the most important remarks came from the Bank of England’s Michael Saunders. He said, in a Bloomberg interview, that Brexit “vulnerabilities“ could prevent any rate hike even if their forecasts imply a need to do so. Talk about known unknowns.

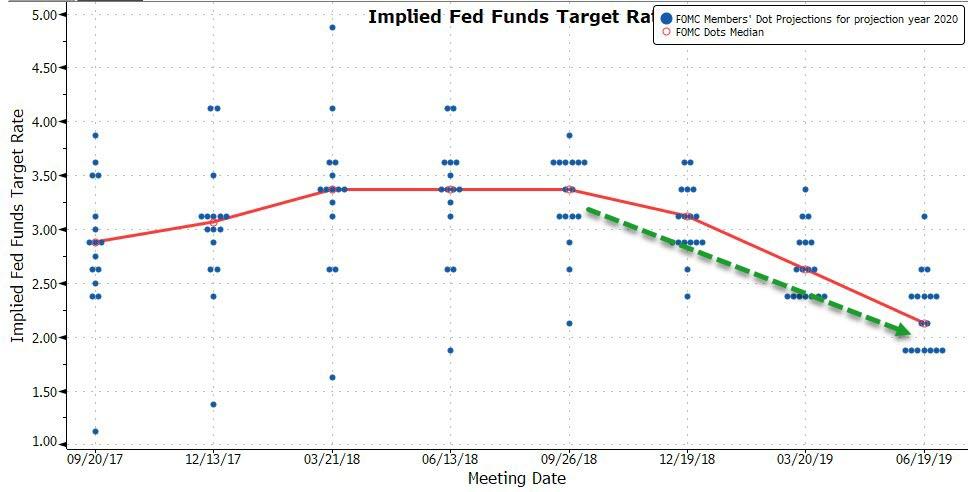

Once again, a central bank is inching closer to market pricing rather than the other way around. When I read this, I couldn’t help but think back to a comment made in 2012 by then Dallas Fed President Richard Fisher. In what at the time seemed like sacrilege, he said:

“I would caution, again, that at best, the economic forecasts and interest-rate projections of the FOMC are ultimately pure guesses.”

Boy was he right.

Yet it is a truth the market still struggles with as they continue to parse with great intensity the latest staff projections, dots and comments. Traders knew, or should have, what to do when forward guidance was having its hay day. When trying to discern policy-maker reaction functions, they hung on every word uttered in speeches. Comforted in the knowledge that everyone agreed that no surprises was the order of the day. During the period when data-dependence was purported to be the key, investors were told which numbers mattered most and went from there. We may now be entering a period of educated guessing.

NY Fed President John Williams’ comments got the lion share of last week’s attention. But it was actually Governor Richard Clarida’s comments that will have lasting import. He made it quite clear that the Committee is willing to make rate decisions based on forecasts. Gone are the “whites of their eyes” notion. And it’s going to make it harder to handicap what they are likely to do. You have to be impressed with their self-confidence.

The dollar, unsurprisingly, is having a good day. But both the Dollar and Bloomberg Dollar Indexes have risen right into resistance. Now it gets really interesting. Trading wise and, perhaps, politically.

via ZeroHedge News https://ift.tt/2OfdNVX Tyler Durden

The conservative, controversial, and buffoonish Boris Johnson has just been elected prime minister of the U.K. A triumphant Johnson promised supporters he would “deliver Brexit, unite the country and defeat Jeremy Corbyn” (leader of the U.K.’s center-left Labor Party).

Like President Donald Trump, Johnson “gained his country’s top political office by deploying celebrity, clowning, provocation and a loose relationship with the truth,” says the Associated Press.

Johnson’s ascension from mayor of London to highest non-monarch position in the country comes not after winning a nationwide general election—the next of which isn’t scheduled until May 2022—but courtesy of Conservatives votes only.

The party was asked to pick between Johnson and rival Jeremy Hunt to replace the current Tory prime minister, Theresa May. After what many considered a mismanagement of Brexit, May announced her resignation in May and will step down on Wednesday.

“We are going to get Brexit done on 31 October and take advantage of all the opportunities it will bring with a new spirit of can do,” said Johnson in a victory speech.

Johnson got 92,153 votes, according to the BBC, while Hunt received 46,656. “Almost 160,000 Conservative members were eligible to vote and turnout was 87.4” percent, the BBC reports.

Whether one finds Johnson’s election thrilling or horrifying, it’s something “that 12 months ago even his most die hard fans would have found hard to believe,” writes the BBC’s Laura Kuenssberg. Johnson “is a politician who is hard to ignore,” with “a personality, and perhaps an ego, of a scale that few of his colleagues can match. This is a man who even as a child wanted to be ‘world king’.”

Now that Boris Johnson is likely to be Britain’s next prime minister I don’t have to be as embarrassed this summer when I’m in London as I was last summer. Now they have their own Trump!

Like Trump, Johnson—a one-time novelist and an editor of The Spectator magazine—has a history of writing and comments that are…not woke, to put it mildly. In 2008, he famously referred to black people as “pickaninnies,” later saying he didn’t realize the term was offensive. In a 2002 op-ed, he said any problem in Africa “is not that we were once in charge, but that we are not in charge any more…the best fate for Africa would be if the old colonial powers, or their citizens, scrambled once again in her direction; on the understanding that this time they will not be asked to feel guilty.”

FREE MINDS

Hot wife billboards banned. In keeping with this Roundup’s U.K. theme, here’s an amusing and disturbing look at how U.K. regulations against sexist advertising are playing out. An air-conditioner repair company ran an add that said “Your wife is hot! Better get the air conditioning fixed.” This “was ruled inappropriate and banned from a city’s buses,” notes the BBC:

It was meant to appear on seven buses in Nottingham but Adverta, which places adverts on buses and trams in the city, blocked it and said it could cause offence.

Lee Davies, who designed the ad, said it was “a little bit of harmless fun”.

Prof Carrie Paechter, director of the Nottingham Centre for Children, Young People and Families, said the advert was “like something out of the 1950s” and called for it to be removed. “If I had young children, I wouldn’t want them passing that on the way to school, because of the messages it gives them about society,” she said.

FREE MARKETS

PayPal dumps child protection group. Federal pressure on payment processors to refuse service to sex workers—even legal ones—is often framed as a measure to stop human trafficking and child sexual exploitation. (Don’t ask how, it just is, OK?) Now even groups that work with sexually exploited minors may be getting caught up in the dragnet.

EMERGENCY: @PayPal has permanently disabled our account saying "we're unable to continue offering our services to you at this time due to the nature of your business and the risk it poses to PayPal."

The conservative, controversial, and buffoonish Boris Johnson has just been elected prime minister of the U.K. A triumphant Johnson promised supporters he would “deliver Brexit, unite the country and defeat Jeremy Corbyn” (leader of the U.K.’s center-left Labor Party).

Like President Donald Trump, Johnson “gained his country’s top political office by deploying celebrity, clowning, provocation and a loose relationship with the truth,” says the Associated Press.

Johnson’s ascension from mayor of London to highest non-monarch position in the country comes not after winning a nationwide general election—the next of which isn’t scheduled until May 2022—but courtesy of Conservatives votes only.

The party was asked to pick between Johnson and rival Jeremy Hunt to replace the current Tory prime minister, Theresa May. After what many considered a mismanagement of Brexit, May announced her resignation in May and will step down on Wednesday.

“We are going to get Brexit done on 31 October and take advantage of all the opportunities it will bring with a new spirit of can do,” said Johnson in a victory speech.

Johnson got 92,153 votes, according to the BBC, while Hunt received 46,656. “Almost 160,000 Conservative members were eligible to vote and turnout was 87.4” percent, the BBC reports.

Whether one finds Johnson’s election thrilling or horrifying, it’s something “that 12 months ago even his most die hard fans would have found hard to believe,” writes the BBC’s Laura Kuenssberg. Johnson “is a politician who is hard to ignore,” with “a personality, and perhaps an ego, of a scale that few of his colleagues can match. This is a man who even as a child wanted to be ‘world king’.”

Now that Boris Johnson is likely to be Britain’s next prime minister I don’t have to be as embarrassed this summer when I’m in London as I was last summer. Now they have their own Trump!

Like Trump, Johnson—a one-time novelist and an editor of The Spectator magazine—has a history of writing and comments that are…not woke, to put it mildly. In 2008, he famously referred to black people as “pickaninnies,” later saying he didn’t realize the term was offensive. In a 2002 op-ed, he said any problem in Africa “is not that we were once in charge, but that we are not in charge any more…the best fate for Africa would be if the old colonial powers, or their citizens, scrambled once again in her direction; on the understanding that this time they will not be asked to feel guilty.”

FREE MINDS

Hot wife billboards banned. In keeping with this Roundup’s U.K. theme, here’s an amusing and disturbing look at how U.K. regulations against sexist advertising are playing out. An air-conditioner repair company ran an add that said “Your wife is hot! Better get the air conditioning fixed.” This “was ruled inappropriate and banned from a city’s buses,” notes the BBC:

It was meant to appear on seven buses in Nottingham but Adverta, which places adverts on buses and trams in the city, blocked it and said it could cause offence.

Lee Davies, who designed the ad, said it was “a little bit of harmless fun”.

Prof Carrie Paechter, director of the Nottingham Centre for Children, Young People and Families, said the advert was “like something out of the 1950s” and called for it to be removed. “If I had young children, I wouldn’t want them passing that on the way to school, because of the messages it gives them about society,” she said.

FREE MARKETS

PayPal dumps child protection group. Federal pressure on payment processors to refuse service to sex workers—even legal ones—is often framed as a measure to stop human trafficking and child sexual exploitation. (Don’t ask how, it just is, OK?) Now even groups that work with sexually exploited minors may be getting caught up in the dragnet.

EMERGENCY: @PayPal has permanently disabled our account saying "we're unable to continue offering our services to you at this time due to the nature of your business and the risk it poses to PayPal."

The world’s largest central banks are preparing for a policy u-turn, some have questioned whether ‘more of the same’ from the ECB will be enough to revive the continent’s moribund economy. In fact, BlackRock CEO Larry Fink speculated that the ECB would need to start buying stocks for its stimulus to have any impact – though he acknowledged that there would be repercussions.

On Tuesday, just hours after his bank reported its best Q2 results in nine years, UBS Chief Sergio Ermotti sat down for an interview with Bloomberg and warned that the next round of monetary easing, which could begin with the ECB later this week, might risk bursting the tremendous asset bubble that has formed over the past decade of QE-driven policy.

“I’d be very, very careful about growing further the balance sheet of central banks,” Ermotti said. “We are at a risk of creating an asset bubble.”

If Europe wants to revive economic growth, it needs to focus on political and economic reforms, not rely on central bank money printing, which accomplishes little aside from inflating asset prices.

The ECB “can only help in a transition, it’s not a solution to the problem,” Ermotti said.

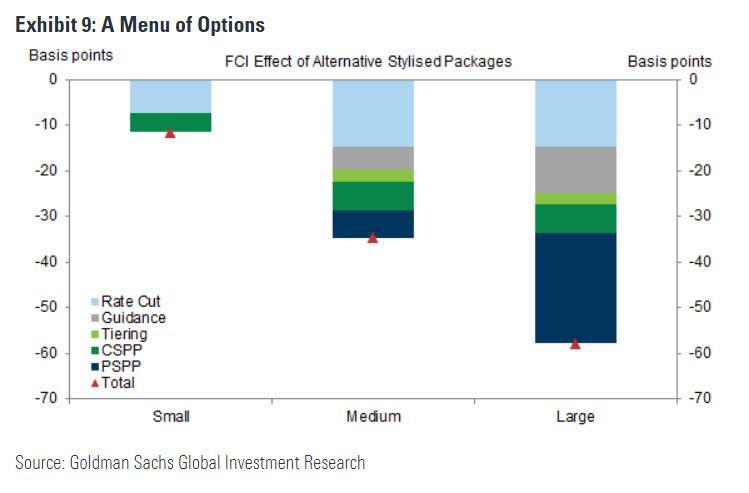

Unfortunately, at this point, the ECB is probably already set on its policy path. A team of analysts at Goldman Sachs laid out three “bundles” which Mario Draghi could unveil later this week as he sets the bank back on course for more stimulus before handing the reins to Christine Lagarde later this year. These “bundles” include small, medium and large bundles that reflect different levels of stimulus.

According to Bloomberg, money markets are pricing in a 40% chance of a 10-basis-point rate cut at Thursday’s meeting. They also expect the central bank to restart its asset-purchase program later this year. Net bond purchases by central banks will soon swing back above zero.

As anybody who has been paying close attention to US markets could tell you, the “about-face” by central banks, particularly expectations that the Fed will deliver a rate cut next week, has fueled a torrid rebound in stocks and bonds, creating a growing pile of debt with negative yields, and sending US benchmarks to new highs.

Though there has been a mild recovery in US economic data this month,in Europe, the rally seems to be based solely on expectations for more central bank stimulus, and nothing further.

“Asset prices went up but it’s not really correlated with investor sentiment,which is in my point of view, of course, a very dangerous development,” said Ermotti.

Still, many investors have remained on the sidelines this year, fearing the collapse of trade talks between Washington and Beijing, or some other risk event, could undermine markets. Ermotti said that client cash balances remain “very high,” which could also suggest that the melt up has more room to run, and that investors aren’t simply waiting to “sell the fact” when and if the ECB and the Fed cut interest rates.

“What they say is that they’re willing to step into the market if there’s a major correction,” Ermotti said.

Watch a clip from the interview below:

via ZeroHedge News https://ift.tt/32OVD0y Tyler Durden

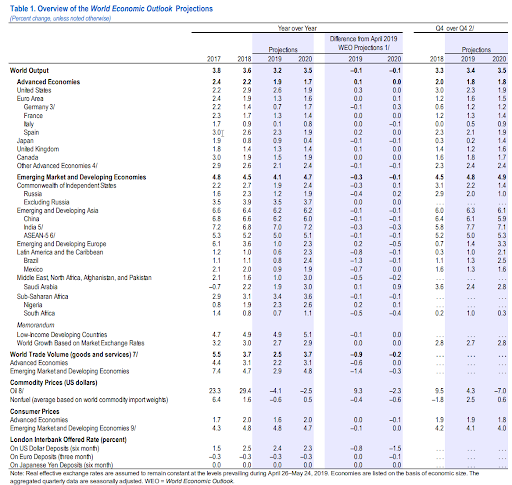

There’s good news, bad news, and goldillocks news from today’s IMF report.

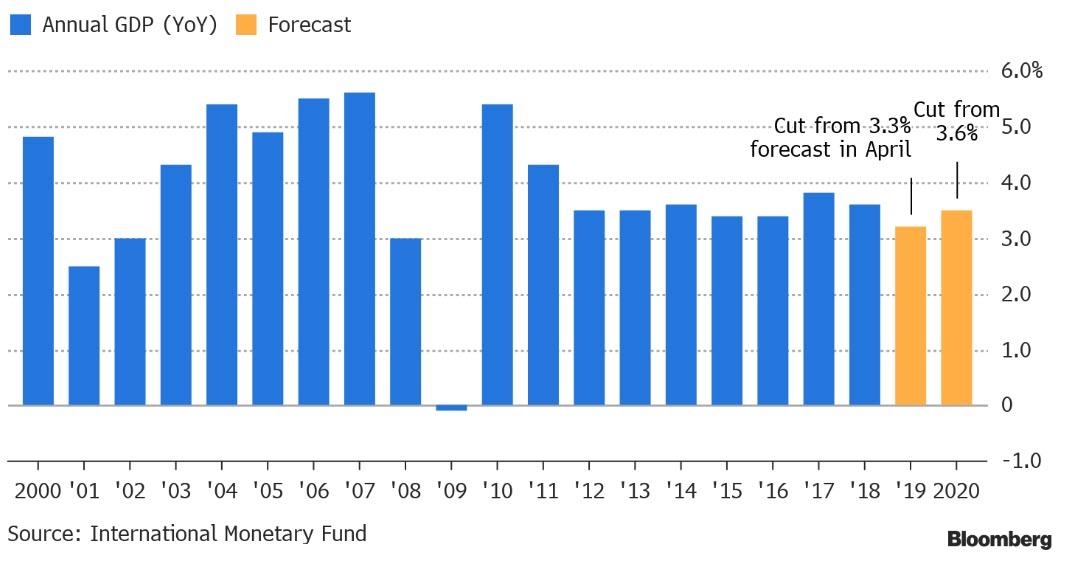

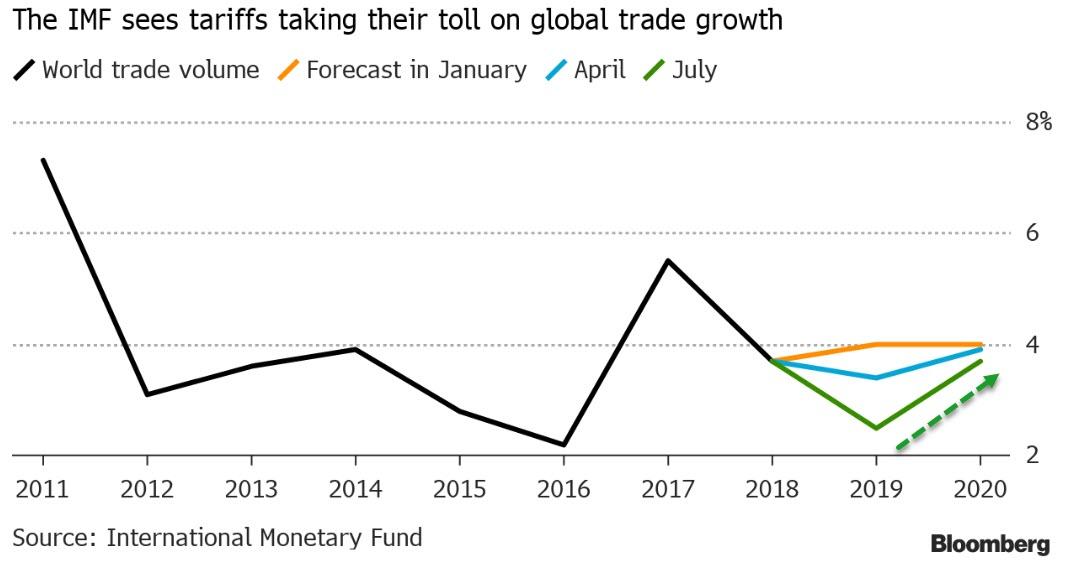

Bad News: For the fourth time in a row, The International Monetary Fund is downgrading its outlook for the world economy because of simmering international trade tensions.

The IMF expects the global economy to expand by a “sluggish” 3.2% in 2019, down from 3.6% in 2018 and from the 3.3% growth it forecast for this year back in April.

“The projected growth pickup in 2020 is precarious, presuming stabilization in currently stressed emerging market and developing economies and progress toward resolving trade policy differences,” the IMF said.

“The principal risk factor to the global economy is that adverse developments — including further U.S.-China tariffs, U.S. auto tariffs, or a no-deal Brexit — sap confidence, weaken investment, dislocate global supply chains, and severely slow global growth below the baseline,” the IMF said.

It forecasts 6.2% growth for the Chinese economy, slowest since 1990 when China faced sanctions following the brutal crackdown on pro-democracy demonstrations in Beijing’s Tiananmen Square.

Good News: The IMF boosts its forecast for the U.S. economy this year, citing expectations that the Federal Reserve will cut interest rates.

The fund now expects the U.S. economy to grow 2.6% in 2019, down from 2.9% last year but up from the 2.3% it forecast in April.

Goldilocks News: While the IMF saw global trade slowing this year more significantly as a result of the trade tensions, it predicted a bounce back to 3.7% growth in volumes in 2020, the same pace as 2018.

“It’s absolutely urgent to end these trade wars as soon as possible, to not escalate, and also to roll back the tariffs in place,” Chief Economist Gita Gopinath said in an interview with Bloomberg’s Tom Keene ahead of Tuesday’s report.

“That will have a big boost to business sentiment that will raise investment and be good for the global economy.”

Watch the press conference here:

via ZeroHedge News https://ift.tt/30Syybs credittrader

{kind=link}