Quick: Do you think you can prove to the satisfaction of an immigration officer that you have the right to be in the United States right now? Can you prove that you’ve been living in the United States for at least two years? If not, you risk getting deported under a new policy being pushed by President Donald Trump’s administration.

Today, the Department of Homeland Security (DHS), under Acting Secretary Kevin McAleenan, released a notice announcing plans to dramatically expand the “expedited removal” process.

This process generally bypasses judicial review hearings, meaning those subjected to it don’t get the typical due process mechanisms of those facing deportation (which can normally take months or years). Expedited removals already exist, but with restrictions: The process can be applied only to those who arrived to the United States by sea and have been in the country for less than two years; or to those who crossed the United States border by land, and are still within 100 miles of the U.S. border, and were in the United States for less than 14 days before encountering immigration officers.

The new policy would erase many of the geographic limitations. McAleenan says the DHS is “exercising its statutory authority” under a 1996 law to cover immigrants anywhere within the United States who have been here less than two years, regardless of how they arrived. So that 100-mile limit would go away under this new system. Any immigrant found anywhere in the United States would risk expedited removal if they “have not affirmatively shown, to the satisfaction of an immigration officer, that they have been physically present in the United States continuously for the two-year period immediately preceding the date of the determination of inadmissibility.”

The burden then is put on the immigrants to prove they’re here legally—or, if they can’t do that, that they’ve been here for more than two years. Otherwise they risk rapid deportation with little to no recourse.

Part of the justification for expanding the policy, the order explains, is the massive logjam in immigration enforcement procedures, which has caused a growing humanitarian crisis at several detention facilities near the border. McAleenan explains that the new policy would “help to alleviate some of the burden and capacity issues currently faced by DHS and [the Department of Justice] by allowing DHS to remove certain aliens encountered in the interior more quickly, as opposed to placing those aliens in more time-consuming removal proceedings.” They calculate that more than a third of the aliens they have detained from the interior of the United States (deeper than that 100-mile limit) would potentially qualify for expedited removal if immigration had been following these guidelines.

Regardless of how one feels about immigration levels and border enforcement, any fan of human liberty should be concerned when an arm of the executive branch proposes expanding the scope of how much it can enforce regulations without judicial review. It’s bad enough to deny aliens here due process. (Yes, the rights guaranteed by the Constitution are generally supposed to apply to noncitizens.) But what’s worse is what we already know from how DHS treats American citizens and legal immigrants within that 100-mile zone—with intrusive, unwarranted searches. This authority will most certainly be abused.

Just last week U.S. Customs officials detained three children, who are U.S. citizens, at O’Hare International Airport in Chicago, in the hopes of luring out their parents, who they believe are illegal immigrants. Expanding the power to remove people quickly is almost sure to hit people that it shouldn’t, and to be used to threaten immigrants and minorities even when they’re here legally.

The American Civil Liberties Union is already announcing plans to sue:

???? We are suing to quickly stop Trump's efforts to massively expand the expedited removal of immigrants.

Immigrants that have lived here for years will have less due process rights than people get in traffic court.

House Intelligence Committee Chairman Adam Schiff (D-CA) has pivoted from ‘deepfake doom‘ influencing the 2020 election, to downplaying an upcoming watchdog report by the DOJ’s Inspector General due sometime in September.

Speaking at the Aspen Security Conference (where he had a pow-wow with Fusion GPS founder Glenn Simpson last July), Schiff claims that DOJ Inspector General Michael Horowitz was co-opted into a scheme to protect President Trump by instigating a “fast track” report last year at Trump’s behest, according to the Washington Examiner‘s Daniel Chaitin.

Schiff claimed the president wanted McCabe, who briefly took over as acting FBI director after Trump fired James Comey in May 2017, investigated and his pension taken away and suggested someone such as former Attorney General Rod Rosenstein obliged the president by making a referral.

“The inspector general found that McCabe was untruthful. He may very well have been untruthful,” the California Democrat said, but noted that is not where main his concern lies.

…

The initiation of the inspector general’s inquiry in McCabe happened, Schiff said, “because the president wanted it politically.” He added, “Once you go down that road, it leads to disaster.” –Washington Examiner

“I have no reason to question the inspector general’s conclusion, but that investigation was put on a fast track. It was separated from a broader inspector general investigation, which is still ongoing,” said Schiff. “Why was that done? It was done so he could be fired to not get a pension. It was done to please the president when the initiation investigation is tainted.So are the results of that investigation.”

McCabe was fired on March 16, 2018 – less than two days before his planned retirement. Had he not been fired, he would have collected his full pension on his 50th birthday.

Of course, a GoFundMe campaign set up in the wake of McCabe’s firing raised $538,000 for his ‘legal-defense fund,’ so we imagine he’ll be OK unless the DOJ decides to pursue charges against the former Deputy Director.

In April 2018, it was revealed that the Justice Department inspector general referred its findings to the U.S. attorney’s office in Washington for possible criminal charges, and his lawyer confirmed as recently as February that McCabe was still under investigation.

McCabe, whom Trump has accused of planning to carry out an “illegal and treasonous” plan to oust him as president, has argued that his firing was an attempt to discredit the FBI and special counsel Robert Mueller’s investigation into Russian interference in the 2016 election. –Washington Examiner

It’s far from over…

While the Mueller investigation is over, Horowitz’s investigation into potential FISA abuse is significant – and Attorney General William Barr is now ‘weapons free’ to work with Horowitz to ‘investigate the investigators.’ According to the Examiner, “The inspector general can recommend prosecutions, and U.S. Attorney John Durham, whom Barr tasked to lead the review, has the ability to convene a grand jury and subpoena people outside of the government. Beyond that, Senate Judiciary Committee Chairman Lindsey Graham, a close Trump ally, has promised a “deep dive” into the origins of the Trump-Russia investigation after Horowitz completes his work.”

Two questions remain; will Schiff continue to push the taint angle, and will AG Barr and Horowitz’s efforts lead to any notable prosecutions before the 2020 election? Or ever?

via ZeroHedge News https://ift.tt/2JVhbQr Tyler Durden

If the head of a department can’t stay awake during meetings, is there any good reason to keep his department around? That’s the question we should be asking in the wake of Politico‘s exposé of a deeply dysfunctional U.S. Department of Commerce.

The problems reportedly start at the top, with Commerce Secretary Wilbur Ross. “He’s sort of seen as kind of irrelevant,” one unnamed advisor told Politico. “The morale is very low there because there’s not a lot of confidence in the secretary.” According to the source, routine meetings with senior staff have largely ceased because of Ross’s tendency to fall asleep during them.

This same lack of stamina, Politico says, is why Ross has been reticent to testify before Congress, preferring to send his staff instead. This has reportedly angered lawmakers, who have interpreted it as disrespectful.

A Commerce Department spokesperson pushed back against much of Politico‘s reporting, claiming that Ross is a “tireless” cabinet secretary. But even if this organ of the government is run with military-like efficiency, there’s still a good case for getting rid of it altogether.

Similar to the Department of Homeland Security (DHS), the Commerce Department is a hodgepodge of agencies, some important, others less so. A few are actively harmful.

Much of the department’s activities involve funneling federal subsidies to private business projects. Its Economic Development Agency (EDA) has given out grants from the wasteful ($35 million for a money-losing convention center in Cedar Rapids, Iowa) to the absurd ($1.7 million for a venue in New York that plans to host performances of dead comedians via holograms).

“In the four decades since its creation, EDA has funded professional football practice facilities, model pyramids, wine tasting rooms, and other clearly wasteful projects,” reads a 2012 report from the pro-market Competitive Enterprise Institute. The report also criticizes the EDA for measuring projects’ success by the number of jobs created (as opposed to value created) or by the amount of public investment a project attracts (which has seen the EDA give out awards to local governments for raising taxes).

The Commerce Department also enforces protectionist trade policies through its International Trade Administration (ITA). Domestic industries can petition the ITA to investigate whether foreign companies are engaged in “dumping” (selling at below-market prices) in the U.S. market or are receiving export subsidies from their home governments.

Should both the ITA and the U.S. Trade Commission—an independent body outside of the Commerce Department—find evidence of these unfair trade practices, the Commerce Department can order anti-dumping and countervailing duties to be placed on foreign imports.

The ITA has long been criticized for being biased in favor of U.S. industries, using opaque math to justify duties on foreign competitors. The agency has been on the front lines of the recent trade war with China, finding that everything from Chinese steel to Chinese quartz allegedly warrants anti-dumping duties. And that’s just from July.

Not everything the Commerce Department does in tied to crony capitalism. It also administers the Census and is in charge of the National Oceanic and Atmospheric Administration. But as with the Department of Homeland Security, we’d be better off if the Commerce Department were disbanded and its most objectionable agencies abolished. The more useful branches can be spun off as independent agencies or folded into other, less dysfunctional departments.

from Latest – Reason.com https://ift.tt/2OcUEUB

via IFTTT

Previously US allies had rebuffed and resisted White house calls for an anti-Iran naval forces, fearing it would worsen already soaring tensions, but it appears last Friday’s dramatic Iranian military seizure of two British tankers (with one, the UK-flagged Stena Impero still in Iran’s custody) has changed Europe’s tune.

Addressing Britain’s Parliament in London on Monday, UK Foreign Secretary Jeremy Hunt announced a “European-led maritime protection mission to support safe passage of crew and cargo” in the Persian Gulf. The goal, he described, would be to provide safe passage for international vessels in the vital oil transit waterway, protecting them from Iranian “state piracy”.

Image via UK Defence Journal

“Let us be clear, under international law Iran had no right to obstruct the ship’s passage, let alone board her,” Hunt told the House of Commons. “It was therefore an act of state piracy.”

“We will seek to put together a European-led maritime protection mission to support safe passage of crew and cargo in this vital region,” he said. However, he still sought to distance the new initiative from the US military build-up in the gulf.

“We have had constructive discussion with a number of countries in the last 48 hours and we will discuss later this week the best way to complement this with recent U.S. proposals in this area,” Hunt said.

The foreign secretary said the planned European mission was not part of the U.S. policy of exerting “maximum pressure” on Iran.

It was not clear which countries will join the protection force Hunt is discussing, or how quickly it can be put in place. — Associated Press

His announcement came the same day Iran paraded the Stena Impero’s international crew in front of cameras.

The majority of the crew was previously reported as having Indian nationality, and the government of India has over the weekend sought to negotiate their release with Tehran.

Immediately following last Friday’s escalation, which involved IRGC operatives fast-roping down to the Stena Impero’s deck, Hunt promised “robust” action and threatened “serious consequences” against Tehran. Iran, for its part, says it’s rightly responding to the UK’s early July seizure of the Grace 1, which been transporting 2 million barrels of Iranian oil to Syria.

An unnamed Western diplomat told Reuters last week, “The Americans want to create an ‘alliance of the willing’ who confront future attacks,” but at the time asserted, “Nobody wants to be on that confrontational course and part of a U.S. push against Iran.”

But it appears the UK’s hand has been forced, now establishing just such a force in the gulf. The Royal Navy currently has a couple of warships escorting tankers out of the region, with further new unconfirmed reports that it’s deployed a nuclear-powered attack submarine to the region to bolster its force.

via ZeroHedge News https://ift.tt/2M0kqIW Tyler Durden

If the head of a department can’t stay awake during meetings, is there any good reason to keep his department around? That’s the question we should be asking in the wake of Politico‘s exposé of a deeply dysfunctional U.S. Department of Commerce.

The problems reportedly start at the top, with Commerce Secretary Wilbur Ross. “He’s sort of seen as kind of irrelevant,” one unnamed advisor told Politico. “The morale is very low there because there’s not a lot of confidence in the secretary.” According to the source, routine meetings with senior staff have largely ceased because of Ross’s tendency to fall asleep during them.

This same lack of stamina, Politico says, is why Ross has been reticent to testify before Congress, preferring to send his staff instead. This has reportedly angered lawmakers, who have interpreted it as disrespectful.

A Commerce Department spokesperson pushed back against much of Politico‘s reporting, claiming that Ross is a “tireless” cabinet secretary. But even if this organ of the government is run with military-like efficiency, there’s still a good case for getting rid of it altogether.

Similar to the Department of Homeland Security (DHS), the Commerce Department is a hodgepodge of agencies, some important, others less so. A few are actively harmful.

Much of the department’s activities involve funneling federal subsidies to private business projects. Its Economic Development Agency (EDA) has given out grants from the wasteful ($35 million for a money-losing convention center in Cedar Rapids, Iowa) to the absurd ($1.7 million for a venue in New York that plans to host performances of dead comedians via holograms).

“In the four decades since its creation, EDA has funded professional football practice facilities, model pyramids, wine tasting rooms, and other clearly wasteful projects,” reads a 2012 report from the pro-market Competitive Enterprise Institute. The report also criticizes the EDA for measuring projects’ success by the number of jobs created (as opposed to value created) or by the amount of public investment a project attracts (which has seen the EDA give out awards to local governments for raising taxes).

The Commerce Department also enforces protectionist trade policies through its International Trade Administration (ITA). Domestic industries can petition the ITA to investigate whether foreign companies are engaged in “dumping” (selling at below-market prices) in the U.S. market or are receiving export subsidies from their home governments.

Should both the ITA and the U.S. Trade Commission—an independent body outside of the Commerce Department—find evidence of these unfair trade practices, the Commerce Department can order anti-dumping and countervailing duties to be placed on foreign imports.

The ITA has long been criticized for being biased in favor of U.S. industries, using opaque math to justify duties on foreign competitors. The agency has been on the front lines of the recent trade war with China, finding that everything from Chinese steel to Chinese quartz allegedly warrants anti-dumping duties. And that’s just from July.

Not everything the Commerce Department does in tied to crony capitalism. It also administers the Census and is in charge of the National Oceanic and Atmospheric Administration. But as with the Department of Homeland Security, we’d be better off if the Commerce Department were disbanded and its most objectionable agencies abolished. The more useful branches can be spun off as independent agencies or folded into other, less dysfunctional departments.

from Latest – Reason.com https://ift.tt/2OcUEUB

via IFTTT

With financial stress setting in for U.S. shale companies, some are trying to drill their way out of the problem, while others are hoping to boost profitability by cutting costs and implementing spending restraint. Both approaches are riddled with risk.

“Turbulence and desperation are roiling the struggling fracking industry,” Kathy Hipple and Tom Sanzillo wrote in a note for the Institute for Energy Economics and Financial Analysis (IEEFA).

They point to the example of EQT, the largest natural gas producer in the United States. A corporate struggle over control of the company reached a conclusion recently, with the Toby and Derek Rice seizing power. The Rice brothers sold their company, Rice Energy, to EQT in 2017. But they launched a bid to take over EQT last year, arguing that the company’s leadership had failed investors. The Rice brothers convinced shareholders that they could steer the company in a better direction promising $500 million in free cash flow within two years.

Their bet hinged on more aggressive drilling while simultaneously reducing costs. Their strategy also depends on “new, unproven, expensive technology, electric frack fleets,” IEEFA argued. “This seems like more of the same – big risky capital expenditures.”

EQT’s former CEO Steve Schlotterbeck recently made headlines when he called fracking an “unmitigated disaster” because it helped crash prices and produce mountains of red ink.

“In fact, I’m not aware of another case of a disruptive technological change that has done so much harm to the industry that created the change,” Schlotterbeck said at an industry conference in June.

IEEFA draws a contrast between Schlotterbeck and the Rice brothers. While the latter wants advocates a strategy of stepping up drilling in an effort to grow their way out of the problem, the former argues that this approach has been tried over and over with poor results. Instead, Schlotterbeck said that drillers need to cut spending and production, which could revive natural gas prices.

But while the philosophies differ – relentless growth versus restraint – IEEFA argues that “neither of these strategies seem viable.” On the one hand, natural gas prices are expected to stay below $3 per MMBtu, a price that is unlikely to lead to profits, IEEFA says. That is especially true if shale companies aggressively spend and produce more gas.

However, a strategy of restraint may not work either.

“[E]ven if natural gas producers coordinate their activities and reduce supply—a highly unlikely prospect—Schlotterbeck’s expectation that natural gas prices would inevitably rise is questionable,” IEEFA analysts wrote.

There are few reasons why natural gas prices might not rebound. For instance, any increase in natural gas prices will only induce more renewable energy. Costs for solar, wind and even energy storage has plunged. For years, natural gas was the cheapest option, but that is no longer the case. Renewable energy increasingly beats out gas on price, which means that natural gas prices will run into resistance when they start to rise as demand would inevitably slow.

A second reason why prices might not rise is because public policy is beginning to really work against the gas industry. IEEFA pointed to the recent decision in New York to block the construction of Williams Co.’s pipeline that would have connected Appalachian gas to New York City. In fact, New York seems to be heading in a different direction, recently passing one of the most ambitious and comprehensive pieces of climate and energy bills in the nation. Or, look to Berkeley, California, which just became the first city in the country to ban the installation of natural gas lines in new homes. As public policy increasingly targets the demand side of the equation, natural gas prices face downward pressure.

Another complication for natural gas producers is that the petrochemical industry, which is attracting tens billions of dollars in investment due to the belief that natural gas will remain cheap in perpetuity. Gas producers, who want higher prices, are in conflict with petrochemical manufacturers, who need cheap feedstocks.

“Companies like Shell, which is considering a $6 billion petrochemical investment, must choose: absorb a higher price cost structure for natural gas liquids (NGLs) needed to produce its product, while facing stiff global competition in the petrochemical business. Or, intensify capital commitments and take over the fracking business, hoping to find synergies through integration,” IEEFA noted.

“Both of these scenarios change the risk profile Shell has described to justify its aggressive expansion plans in the Ohio Valley.”

The upshot is that while companies like EQT undertake a major shift in strategy, the road ahead remains rocky either way. “More bankruptcies are all but certain as oil and gas borrowers must repay or refinance several hundred billion dollars of debt over the next six months,” IEEFA concluded.

via ZeroHedge News https://ift.tt/2y420Pg Tyler Durden

Apparently things at the Commerce Department are a disaster. To add insult to injury, 81-year-old commerce secretary Wilbur Ross doesn’t seem to be able to stay awake during meetings, according to The Daily Beast and Politico.

A new report says that Ross is rarely seen at the department and isn’t respected. A source said:

“He’s sort of seen as kind of irrelevant. The morale is very low there because there’s not a lot of confidence in the secretary… He’s not respected in the building.”

Ross also doesn’t hold meetings on a routine basis due to his “lack of stamina”. Another source said:

“Because he tends to fall asleep in meetings, they try not to put him in a position where that could happen, so they’re very careful and conscious about how they schedule certain meetings… There’s a small window where he’s able to focus and pay attention and not fall asleep.”

Ross’s staff refutes that notion, claiming that he frequently has “long” afternoon meetings. Commerce Press Secretary Kevin Manning said:

“Secretary Ross is a tireless worker who is the sole decision-maker at the department. He routinely works 12-hour days and travels often, with visits to seven countries and eight states in the last three months to advance the president’s agenda.”

Meanwhile, the Commerce Department has reached its “apex of dysfunction” and officials are trying to avoid having Ross testify at a congressional oversight hearing ever again.

“There’s a great deal of effort to shield him from testifying ever again,” said one source.

They continued:

“There was a great deal of concern to not have him testify expressed from the White House. Don’t do this, people. Don’t do this, he’s probably not the right guy to go there.’”

Theo LeCompte, a former top Commerce official said: “With our ongoing trade wars and the census looming, Commerce needs functional leadership in order to be effective, and right now they just don’t have it.”

via ZeroHedge News https://ift.tt/2YixRuo Tyler Durden

Authored by Steve Englander, Head, Global G10 FX Research and North America Macro Strategy at Standard Chartered Bank

The US government may find FX intervention irresistible; we are less enthusiastic. If US policy makers judge that foreign counterparts are artificially weakening their currencies, they might feel justified in doing the equal and opposite. And, there may be some substance to the Treasury’s complaints about currency manipulation. For example, we suspect that most private-sector analysts would see a weaker EUR as the major, and perhaps only, stimulus from further European Central Bank (ECB) easing. Still, implementing effective intervention is harder and more expensive than it looks, and would probably deliver less than expected even if successful.

Our expectations if the US were to intervene:

The US would be on its own – other countries would not join

The first intervention, even if small, would shock and weaken the USD by 2% or more

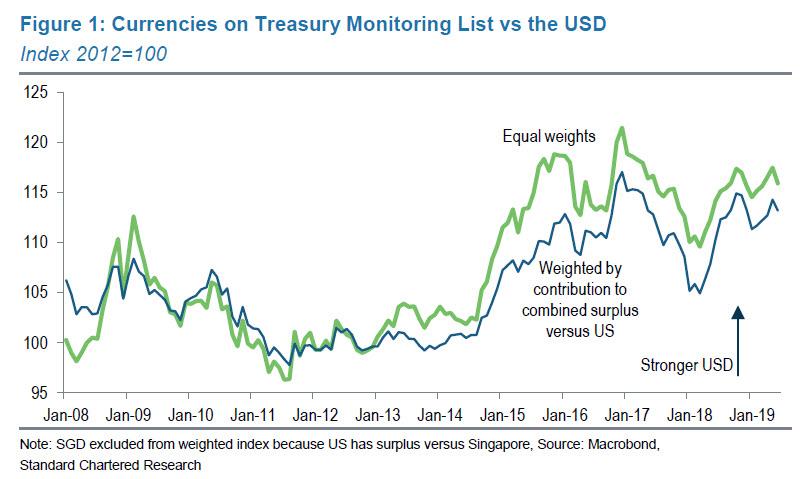

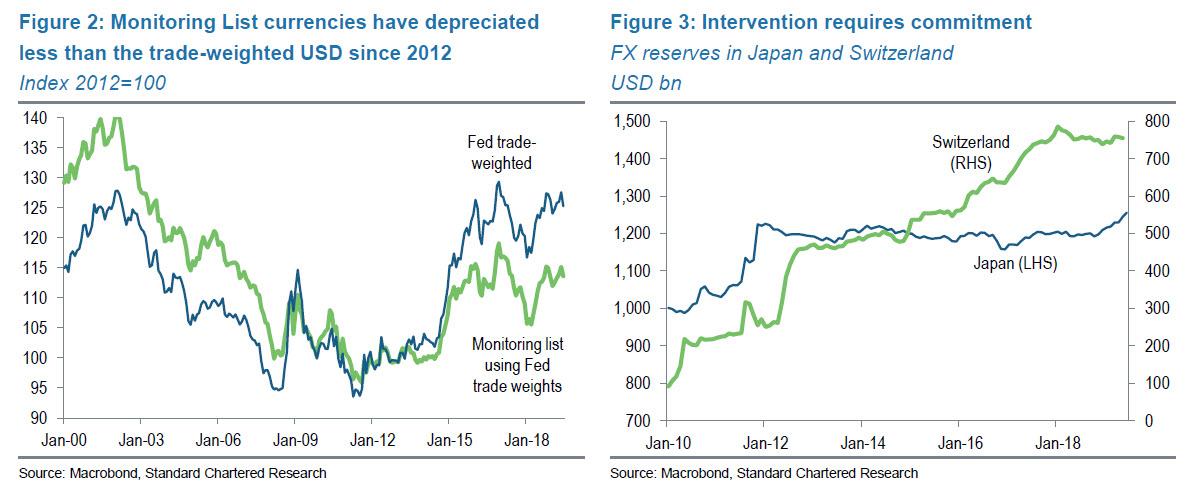

Of the seven currencies on the Treasury’s Monitoring List – the CNY, EUR, JPY, KRW, MYR, VND and SGD – intervention would be most likely in the EUR and JPY, the most liquid and freely traded; as a group, these currencies have depreciated about 15% since 2012 (Figure 1), but less than the currencies not on the Monitoring List (Figure 2)

Impact of small, sterilised intervention would diminish rapidly

A sustained FX effect would require a commitment of USD 200-400bn

Other central banks would push back, increasing the needed intervention size and diminishing the exchange rate effects

The administration’s harsh criticism of policies in these countries would make it hard to justify amassing a large portfolio of their currencies

Intervention is rare but doable

ESF has enough to start

The US has foreign exchange reserves of about USD 127bn, and the Exchange Stabilization Fund (ESF) has about USD 95bn. The intervention mechanism is creaky, as there has been no large-scale intervention in decades. There were small interventions selling JPY on behalf of the Bank of Japan (BoJ) in the early part of this decade and buying EUR in the early 2000s. The ESF would probably need to be augmented to avoid the perception that there is a limit to intervention; otherwise intervention could lose credibility quickly. As Fed officials have frequently acknowledged, the Treasury directs policy on exchange rates.

The debate in the policy and academic literature continues as to whether sterilised intervention – the US sells USD in the FX market but withdraws reserves domestically – is effective. There is a consensus that unsterilised intervention is more powerful than sterilised intervention because unsterilised intervention increases the supply of the currency being sold, whereas sterilised intervention does not alter the overall supply. Some argue, however, that the signalling effect of sterilised intervention gives such intervention some potency. If the Fed is as dovish as Chair Powell has conveyed, there is a case for unsterilised intervention. This would increase the impact of intervention by increasing the global supply of USD versus non-USD assets. The Treasury may prefer unsterilised intervention, but the norm has been for the Fed to sterilise interventions.

How much would it take?

The first time the US intervened – whether unsterilised or sterilised, the USD would probably move a long way, as occurred when the first verbal interventions by the Trump administration occurred. If subsequent interventions were small and isolated, they would likely become increasingly ineffective.

We do not know how big the cumulative interventions would have to be in order to be effective. Gross daily FX transactions were about USD 5tn in 2016, according to the Bank for International Settlements (BIS), and the USD was a leg on USD 4.4tn of these transactions. Such statistics are misleading, however, as most trading is not directional. Net demand for USD on a directional basis is relatively small on a daily basis. The US current account (C/A) deficit is about USD 520bn annually, so as a rough benchmark, there must be just over USD 2bn of USD net buying every business day to keep it steady.

It makes more sense to ask how much the USD would move if foreigners were willing to finance, for example, only 80% of the C/A deficit at current interest and exchange rates. We suspect the USD would weaken significantly if this were the case, but this would mean a USD 100bn shift in the net annual demand for US assets. Note that this is much closer conceptually to unsterilised than sterilised intervention, and such a shift in portfolio allocation among investors would probably reflect deeper concerns about relative asset-market performance than exchange rate valuation. Most likely, it would take a much higher level of sterilised intervention to have a major impact, and even an unsterilised move may not have the same effect as a private-sector capital allocation decision.

At the time of the 1985 Plaza Accord, the US C/A deficit was about USD 140bn and the USD was very vulnerable to intervention. Germany and Japan joined the US in intervention, investors were likely much longer USD after its extended sharp rise, and the USD was more overvalued than it is now. Estimates of total intervention then were about USD 10bn.

At present, the US C/A deficit is about USD 520bn annually, any US intervention is likely to be unilateral (if not opposed by other central banks), the overall FX market is at least 15 times larger, and USD positioning is not as overwhelming relative to the size of the market. These factors might increase the size of the intervention required.

If a commitment to extended intervention were made, we see a minimum of USD 100bn being required, and likely more than USD 200-400bn. Swiss reserves went up c.USD 400bn from the beginning of the euro-area debt crisis in 2010 to the collapse of the 1.20 peg in early 2015. Japanese reserves increased by USD 200bn from early 2010 to end-2011. These are rough ranges, but we do not think a few billion here and there will be enough to affect the USD substantially.

We draw a sharp distinction between short- and long-term intervention strategies. If the US Treasury called dealers to check prices, we would expect the USD to plummet… the first time. Selling a few billion USD for foreign currency would likely move the USD c.2% or more when it first occurred. If this were all that happened, the USD would likely bounce back.

If it looks as if the Treasury were trying to intervene on the cheap, selling a few billion USD here and there when investors leaned the wrong way, the likely market strategy would be to step aside during the immediate period of Treasury intervention and buy the USD back when the Treasury intervention stopped. Several interventions in Japan over 2010-11 exhibited this dynamic (Figure 4).

The day after

We come back to what we think is a poorly understood constraint on US intervention policy. The countries on the US Monitoring List for currency manipulation – China, Japan, Korea, Germany, Italy, Ireland, Singapore, Malaysia and Vietnam – have almost all been harshly criticised by the US for their economic, social and foreign policies. Allocating USD 200-400bn across these countries’ currencies would be no easy task.

The easiest currency in which to intervene would be the EUR, but the Trump administration has been lambasting euro-area economic and political policies non-stop. It would be a strange turnaround for an administration that has been so negative on Europe and its future to acquire a large exposure to the EUR. China and a few others have significant capital controls, so it is unclear how the Treasury would buy their currencies. It is also unclear how the US administration would feel about such exposure to China. Setting aside issues of practicality, intervention would mean being stuck with these currencies. Diversifying out of unwanted reserve currencies has been much harder than anticipated (see Reserve managers sell USD, private sector buys).

Most broadly, selling a strong currency to buy other countries’ weak currencies can push against private-sector capital flows. This administration would find it difficult to explain why acquiring a large portfolio of currencies belonging to political opponents is a good idea.

Small-scale maybe, large-scale tough

Given these considerations, we expect any Treasury intervention to be small but noisy. It would probably mostly in the EUR and JPY, counting on the other currencies to appreciate as part of a broader USD move.

We are not sure intervention will occur, and even less sure it would be a good idea. However, another round of USD strength – especially if driven by policy moves abroad that look as if they are driven primarily by currency considerations – could tip the scales. We doubt that large interventions leading to a big scaling-up of the reserve portfolio would occur.

Social Security Trust Fund in part a sovereign wealth fund?

The Social Security Trust Fund (SSTF) of around USD 3tn is wholly invested in US Treasuries. Portfolio theory suggests that the beneficiaries of Social Security are paying a very high premium for the security of US Treasuries, which in theory cannot default. Few private-sector portfolios hold only Treasuries; a well-designed portfolio would include both domestic and foreign non-Treasury assets.

Our modest proposal is that a portion of these assets could be explicitly managed as a retirement portfolio, similar to the Canada Pension Plan, the Petroleum Fund in Norway and other public retirement plans. These funds could be invested in foreign assets, and this capital outflow would tend to have a USD-softening effect. It would be difficult to argue that such a fund was a currency manipulation scheme, even if it had currency impact. It would have credibility in that its foreign assets would make sense on a risk-return basis, rather than consisting of a set of currencies bought in order to ‘punish’ trading partners. This credibility might mean that it would be more effective in driving down the USD than scattershot intervention.

via ZeroHedge News https://ift.tt/2y3jfAo Tyler Durden

With the Trump-Russia collusion narrative in smoulders, BuzzFeed – which notably published the fabricated ‘Steele’ dossier – has put forth a new bogeyman to explain a 2020 Trump victory (since of course the only way Trump could have beaten an establishment darling is with help).

Enter Ukraine

With the election of Ukraine’s new President, Volodymyr Zelensky, times have apparently changed. Long gone are the days of just 20 short months ago in which a Ukrainian court ruled that government officials meddled for Hillary in 2016 by releasing details of Trump campaign manager Paul Manafort’s ‘Black Book’ to Clinton campaign staffer Alexandra Chalupa.

Forget that Ukraine’s previous administration fired its top investigator who was leading a wide-ranging corruption probe into a Ukrainian energy firm whose board Hunter Biden sat on, Burisma Holdings (after Joe Biden threatened to withhold $1 billion in loan guarantees from the ‘scandal free’ Obama administration).

Nevermind that Russian President Vladimir Putin claimed in a recent interview with Oliver Stone that “it is perfectly obvious that Ukrainian oligarchs gave money to Trump’s opponents.” Perhaps Burisma’s owners are included in that list.

Now, the tables have apparently turned, according to BuzzFeed, which reports that two unofficial envoys reporting directly to Rudy Giuliani “have waged a remarkable back-channel campaign to discredit the president’s rivals and undermine the special counsel’s inquiry into Russian meddling in US elections.”

In a whirlwind of private meetings, Lev Parnas and Igor Fruman— who pumped hundreds of thousands of dollars into Republican campaigns and dined with the president — gathered repeatedly with top officials in Ukraine and set up meetings for Trump’s attorney Rudy Giuliani as they turned up information that could be weaponized in the 2020 presidential race.

The two men urged prosecutors to investigate allegations against Democratic frontrunner Joe Biden. And they pushed for a probe into accusations that Ukrainian officials plotted to rig the 2016 election in Hillary Clinton’s favor by leaking evidence against Paul Manafort, Trump’s campaign chair, in what became a cornerstone of the special counsel’s inquiry. –BuzzFeed

Parnas and Fruman “who both have troubled financial histories,” donated hundreds of thousands of dollars into top Republican committees, along with dozens of candidates’ campaigns, according to the report. While doing this, they promoted a new Ukrainian natural gas company using a photo of Parnas posing with President Trump and top House legislators.

Meanwhile, “Prosecutors in Kiev announced in March they would investigate the officials accused of trying to steer the election in Clinton’s favor — a month after meeting with Parnas, Fruman, and Giuliani…”

Parnas said he expected the information that he and Fruman advanced to become an important focus of Barr’s inquiry, and to dominate the debate in the run-up to the 2020 election. “It’s all going to come out,” he said. “Something terrible happened and we’re finally going to get to the bottom of it.”

In an exclusive interview with BuzzFeed News at the Trump International Hotel, the 47-year-old former stockbroker insisted he and Fruman were not paid for acting as intermediaries between the Ukrainian officials and Giuliani. “All we were doing was passing along information,” he said. “Information was coming to us — either I bury it or I pass it on. I felt it was my duty to pass it on.” –BuzzFeed

According to Parnas, the back channel to the Trump administration was initiated by Ukrainian officials who didn’t know how else to make the right connections. “They knew I was friends with the mayor,” he said, referring to Giuliani. “That was what kick-started the campaign to dig up information on Democrats in Kiev — an effort that “is not going away,” Parnas added. “We’re American citizens, we love our country, we love our president.””

Trump and Giuliani under fire

“Trump has either authorized Giuliani to engage in private diplomacy and deal-making or, even worse, remains silent while Giuliani and his dodgy band of soldiers of fortune engage in activities that severely undermine US credibility and are contrary to fundamental US interests,” said former federal prosecutor Kenneth McCallion, who once represented Ukraine’s former prime minister Yulia Tymoshenko, adding that Parnas and Fruman were “playing with fire” by not registering as foreign agents or being vetted by the US State Department.

Click here for the rest of BuzzFeed‘s in-depth investigation, pieced together after examining “scores of court filings and confidential financial records and interviewed dozens of people — including Parnas.”

It’s one of those “On a balmy evening in May, Lev Parnas and Igor Fruman hunkered down over a table on the terrace of the gleaming Hilton hotel tower in Kiev, a hookah pipe burning between them” type reports, so ‘hunker down’ and prepare for a long read.

via ZeroHedge News https://ift.tt/2JVDoxx Tyler Durden

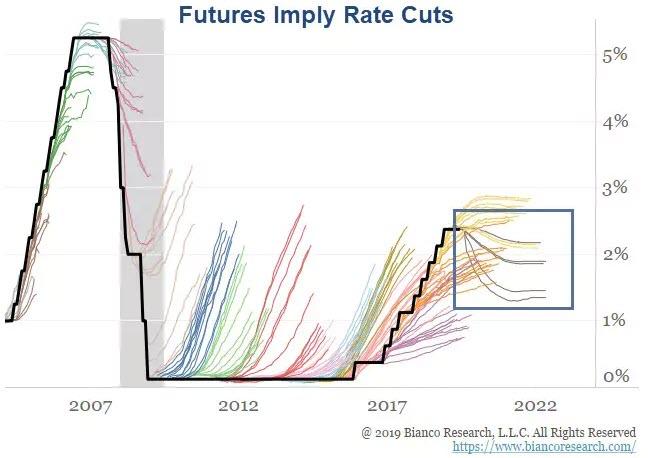

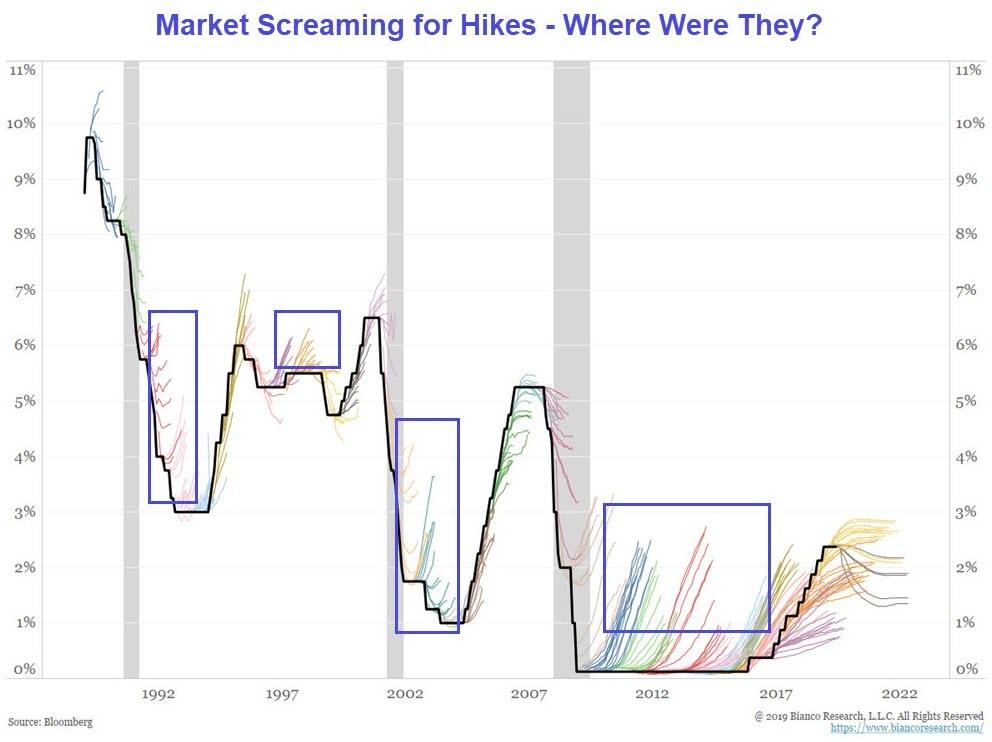

“Anything less would fail to fix the imbalances in the global bond market, continuing to weigh on economic sentiment,” says Bianco.

“By lowering its target for the federal funds rate by just a quarter point, the Fed risks no less than a recession. The Fed has a history of moving too slow to respond to evidence of weaker growth, and a bold move now would help ensure the economy achieves the rare soft landing.”

If the reason the Fed is cutting is the market is demanding it, what is the risk to cutting 50 now? Inflation? Mkt bubble? I think neither.

Chart courtesy of Bianco. The title and blue boxes are my anecdotes.

Bianco notes “In the 1990s the fed funds contracts only went out 6 months. That is why the lines are short. In the 2000s they went out a year, lines are a little longer. Around 2007 they started going out three years, the longest lines.”

Each calendar years is a different color.

So the yellow to the upper right is 2018 (each month end … so Jan 31, Feb 28 and so on, the forward curve projected up to 2021. Black, in a downtrend, is 2009)

The market was screaming for hikes for five years.

The Fed did not deliver.

Too Low, Too Long

That the Fed did not deliver hikes as expected is part of its asymmetric policy of keeping interest rates too low, too long,

Bubbles Blown

Without a doubt the Fed blew more bubbles, and likely the biggest in history.

The market responded with a prolonged yield-curve inversion.

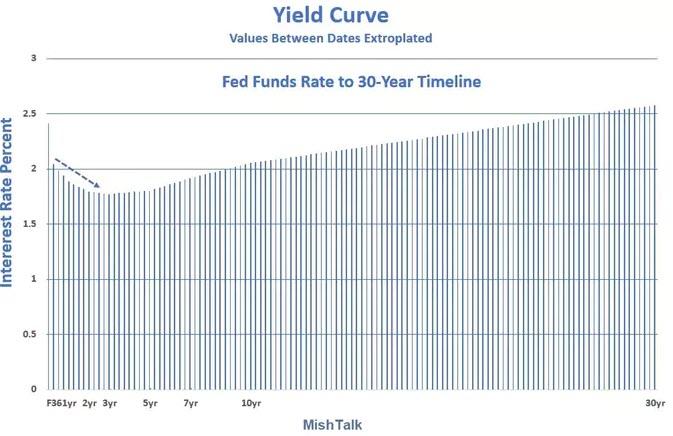

Yield Curve

Spread

The effective Fed Fund Rate is currently 2.41%.

The yield on the three-year Treasury Note is 1.80%.

The spread is -0.61 percentage points

Behind the Curve

Bianco is correct. The Fed is behind the curve.

And by his logic it’s not clear that 50 basis points is enough of a cut.

But to what avail?

So What? Bubbles Already Blown

Let’s return to Bianco’s opening gambit: “Anything less would fail to fix the imbalances in the global bond market, continuing to weigh on economic sentiment.“

The Fed, with its asymmetric too-low too-long policy blew bubbles that are impossible to fix.

Too Late for Insurance

Rate cuts now as economic insurance is like trying to buy insurance on your car after you wrecked it.

The bubbles have been blown.

Even if the Fed can correct current “imbalances” it cannot “unblow” bubbles anymore than it can unblow a horn.

Deflationary Bust Baked in the Cake

In the Fed’s foolish attempt to stave off consumer price deflation, the Fed sowed the seeds of a very destructive set of asset bubbles in junk bonds, housing, and the stock market.

The widely discussed “everything bubble” is, in reality, a corporate junk bond bubble on steroids sponsored by the Fed.

{kind=link}