By Peter Chatwell, head of rates at Mizuho

The phrase “mid-cycle adjustment” sent shudders through risk markets yesterday, during Powell’s press conference. Mid cycle! When corporate debt to GDP is at extremes, earnings growth slowing, and the US manufacturing sector close to contraction, this really does not look mid-cycle to us.

By delivering a 25bp insurance cut, the Fed actually tightened financial conditions for Main Street US, making subsequent easing more likely. The march higher of the USD is the main problem the Fed has to deal with. This has pushed our estimate of the neutral nominal Fed Funds rate much lower this year to under 1.4% and, with yesterday’s move, it could well fall further.

The Fed had many opportunities to reduce market expectations for an easing cycle, but did not take them. In so doing they have repeated the December 2018 hike error, wasting ammunition, and long term US rates will rightly continue to fall from here. For the first time under Trump’s leadership, we see value in long end Treasuries here, as a Fed policy-error trade (for example as a 2s30s flattener).

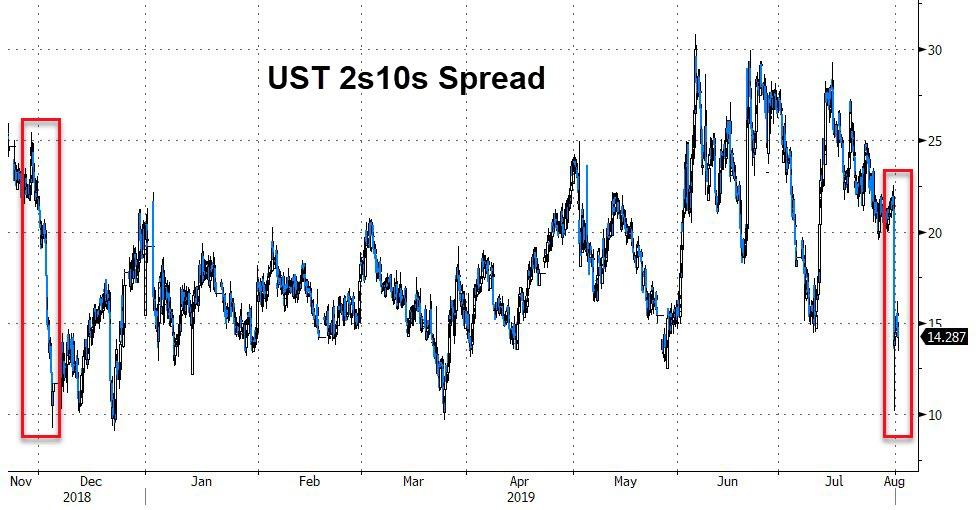

2s10s seems likely to invert in the near term, as the market digests the implications of a Fed which cut rates while simultaneously tightening financial conditions. Such a poor delivery of a cut puts the Fed closer to the zero lower bound, and therefore a liquidity trap. Inflation expectations should continue to fall in the US, and we would expect US corporate spreads and equities to see more selling flows.

Our conclusion is that the market will be proven correct- to prolong the cycle as the Fed is seeking, the Fed will need to ease further, by around 75bp from here just to reach neutral. Until then, expect long end Treasuries to be well bid, particularly as long-end carry just became a bit more favorable.

via ZeroHedge News https://ift.tt/2KeKEF0 Tyler Durden