Trump Praises ECB For “Depreciating The Euro”, Slams The Fed For Doing Nothing

When discussing the barrage of easing unleashed by the ECB moments ago, we said that as “we prepare for the ECB press conference in 30 minutes, that will be nothing compared to the angry twitter tirade we expect by president Trump who will demand that Powell immediately match everything that Powell has done.“

And sure enough, just about half an hour after the ECB announcement, Trump praised the European Central Bank, for “acting quickly, Cuts Rates 10 Basis Points. They are trying, and succeeding, in depreciating the Euro against the VERY strong Dollar, hurting U.S. exports….” And, as expected, the president lashed out at the Fed again, saying that “the Fed sits, and sits, and sits. They get paid to borrow money, while we are paying interest!”

European Central Bank, acting quickly, Cuts Rates 10 Basis Points. They are trying, and succeeding, in depreciating the Euro against the VERY strong Dollar, hurting U.S. exports…. And the Fed sits, and sits, and sits. They get paid to borrow money, while we are paying interest!

Of course, for a real-estate developer, negative rates is a beautiful prospect, and all Trump has to do to get negative rates in the US is to match the European recession in the US next. At that point the Fed should cut rates to zero, or negative, while sending the S&P to nosebleed levels, even as the US economy collapses.

No One Comes Back From This Uninjured. In one word, the devaluation is set to ESCALATE.

In fact, I term it Competitive Devaluation. There are several countries that will be the pioneers of it, but it will eventually reach the United States of America. In Europe and in Japan, we are closer to seeing it happening; in the next 2-5 years, you’ll hear about governments’ first official plans to do this.

They will NOT alert the media to notify the public to own gold and silver. They haven’t thus far (and they won’t going forward, either), and meanwhile, they’ve been accumulating them at the fastest pace in more than half a century.

The central banks want to buy gold, uninterrupted. Since they do not buy silver, the mania that will ensue in that niche market will be huge.

Not just gold and silver stand to gain from devaluation; companies that are able to increase prices and not lose consumers will be great winners as well. These are the world-dominators with pricing power, and I will profile my top-5 holdings for the Endgame Decade (2020-2029) in a Special Report due to be published by September 30th.

Real estate prices in metropolitan areas will also continue to rise; these are hard assets that are difficult to increase in supply, but my analysis is that of the three – world-class companies, precious metals, and real estate, silver will be the BEST PERFORMER.

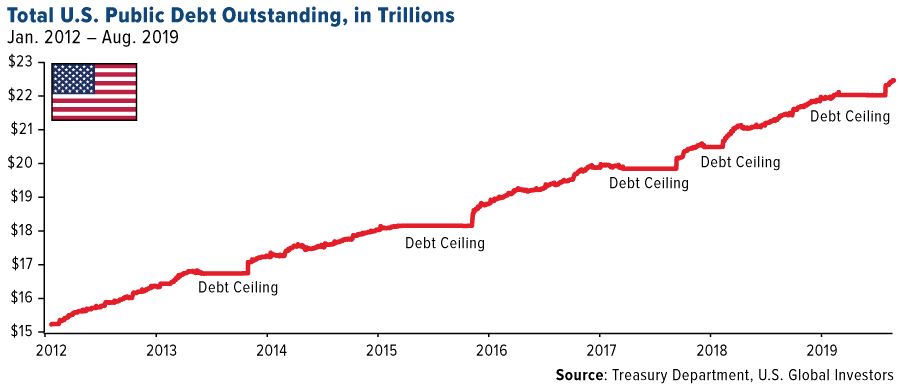

Courtesy: U.S. Global Investors

Central banks are not able to inflate the real debt levels away. The most extreme case of this is Japan, whose central bank has done ALMOST everything under the sun to relieve the country of its deflationary spiral and has failed miserably.

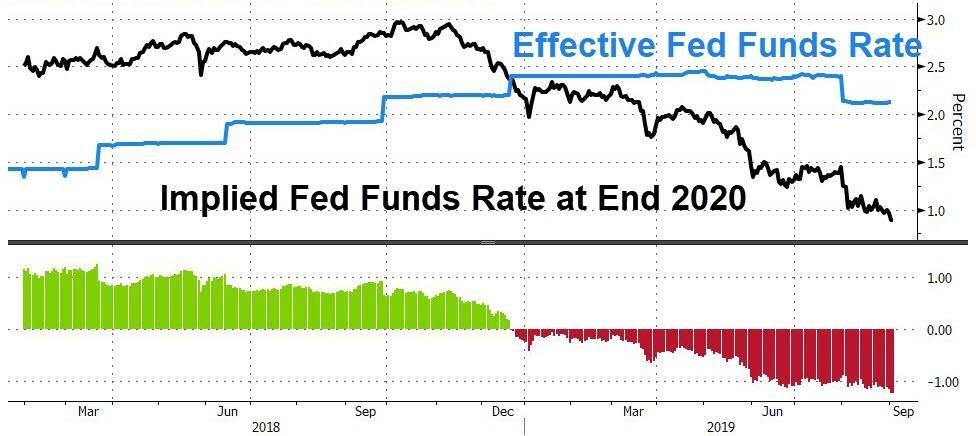

We are a few years from that because many countries have still not reached the negative-yield world. Trump’s entire argument is that the FED doesn’t need to have ammunition come next recession, because interest rates are never going higher again, so just slam the bid, shove the thing to ZERO, or lower and help monetize bonds.

That’s Trump’s attitude, and as bizarre as it sounds, it is becoming our way of life. Under this fiat monetary system, we are never going back to normalized rates; the path is Competitive Devaluation.

Debts will be written off, savings will become extinct and it’s all because our political systems, demographics projection, and growth curves do not align at all.

In the short-term, September will be a month of relief. The Treasury will be funded, the debt ceiling will be raised and dollar liquidity will be increased by the FED; they will lower rates with 100% uncertainty. Any other announcement and the markets will dive by 15%-20%, like in December.

Courtesy: Zerohedge.com

Of course, people living on a fixed income, who represent most of the individuals in the world (employees with salaries), will be HURT THE MOST.

Inflation has the same effect on society as poisoning the water supply: it contaminates and destroys one of the elementary requisites for an orderly society – a stable medium of exchange.

Worse, it diminishes trust in authorities.

Worst of all, it makes everyone a bit more extreme in their views and raises their primal instincts for survival; it reveals the violent side of the personality.

This past week, my wife, daughter and I have been enjoying the beauty and the architectural splendor of the Liguria Sea, the area known as the Italian Riviera, with the Cinque Terre UNESCO World Heritage Park and the magnificent Portofino peninsula.

When looking at all the tourists who flock these shores in August and early September, it is sometimes unimaginable to envision times in which people will be concerned about their basic needs, when mega-yachts dock on the picturesque marinas, but I can cite a list of more than 20 countries that saw this crisis in the 20th and 21st centuries hit them, seemingly out of the blue.

Just 11 years ago, the U.S. papered-over a major banking disaster. Argentina went from being one of the top-10 economic engines in the world to a criminal enterprise with corruption everywhere. Empires fall, due to mismanagement. Countries collapse, due to wrong policies. It’s the way of the world.

No one will like the endgame or leave it unscathed, but some will be in a better position to capitalize on the boom that follows. Priority No.1 is to meaningfully elevate the active income you derive from your career, by becoming a more valuable person. Priority No.2 is to invest the savings wisely.

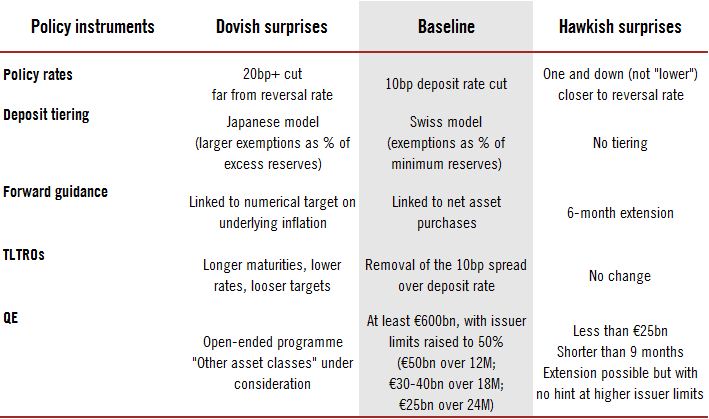

With the market worried that Mario Draghi could surprise hawkishly in his parting announcement…

… that is how the market initially interpreted today’s ECB press release, which cut already negative deposit rates for the first time since 2016 to stimulate the sagging European economy, but by a smaller than expected 10bps to -0.50% while restarting QE but by “only” €20 billion, less than the €30 billion baseline.

However, there was more than enough offsetting dovish bells and whistles, because while the restarted QE (or the Asset Purchase Program) was smaller than expected, it will be open-ended, and the ECB will run it “for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.”

Additionally, the ECB dropped calendar-based forward guidance and replaced it with inflation-linked guidance, noting that key ECB interest rates will “remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon.” Furthermore, the ECB eased TLTRO terms, with banks whose eligible net lending exceeds a benchmark, the rate applied in TLTRO III operations will be lower, and can be as low as the average interest rate on the deposit facility prevailing over the life of the operation; additionally, the maturity of the operations will be extended from two to three years.

Finally, as many expected, the ECB will introduce a two-tier system for reserve remuneration in which part of banks’ holdings of excess liquidity will be exempt from the negative deposit facility rate, in an attempt to mitigate the adverse impact to banks.

In short: a somewhat hawkish read on the rate cut and QE amount, but dovish on every other aspect, from the changed forward-guidance, to the open-ended QE, to the easing in TLTRO terms and to the introduction of a two-tier deposit system.

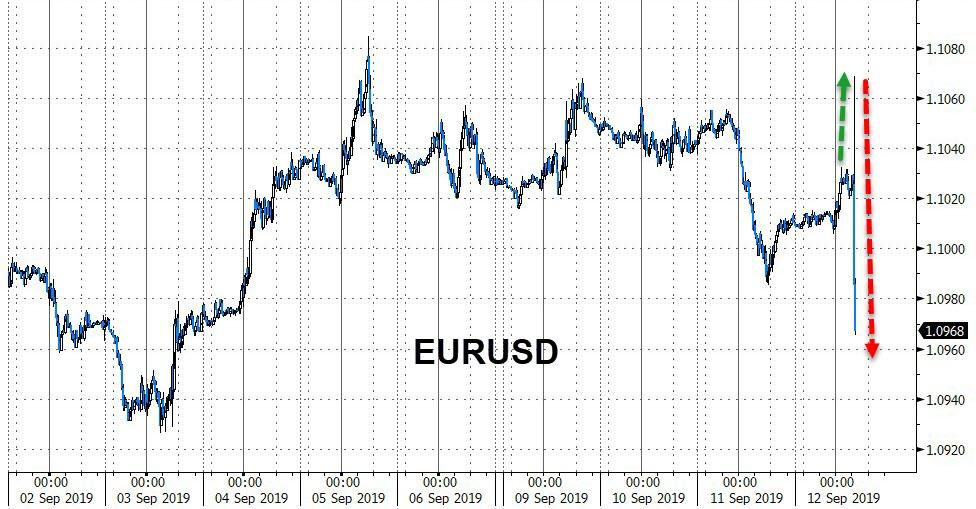

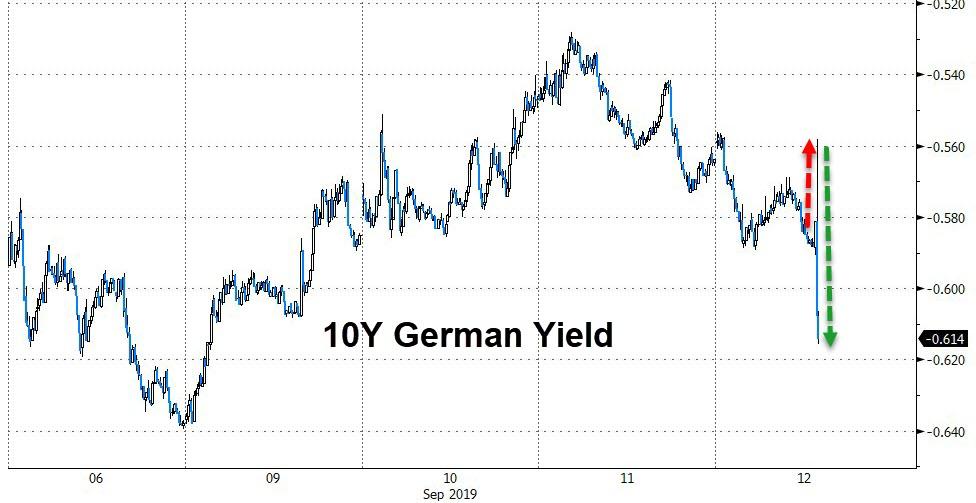

This was reflected in markets, with the EURUSD first spiking the tumbling …

… and the German bund following suit as the market realized the ECB was far more dovish than the kneejerk reaction suggested:

… with Italian yields tumbling to a record low of 0.783.

The full ECB press release is below:

At today’s meeting the Governing Council of the ECB took the following monetary policy decisions:

(1) The interest rate on the deposit facility will be decreased by 10 basis points to -0.50%. The interest rate on the main refinancing operations and the rate on the marginal lending facility will remain unchanged at their current levels of 0.00% and 0.25% respectively. The Governing Council now expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

(2) Net purchases will be restarted under the Governing Council’s asset purchase programme (APP) at a monthly pace of €20 billion as from 1 November. The Governing Council expects them to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.

(3) Reinvestments of the principal payments from maturing securities purchased under the APP will continue, in full, for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

(4) The modalities of the new series of quarterly targeted longer-term refinancing operations (TLTRO III) will be changed to preserve favourable bank lending conditions, ensure the smooth transmission of monetary policy and further support the accommodative stance of monetary policy. The interest rate in each operation will now be set at the level of the average rate applied in the Eurosystem’s main refinancing operations over the life of the respective TLTRO. For banks whose eligible net lending exceeds a benchmark, the rate applied in TLTRO III operations will be lower, and can be as low as the average interest rate on the deposit facility prevailing over the life of the operation. The maturity of the operations will be extended from two to three years.

(5) In order to support the bank-based transmission of monetary policy, a two-tier system for reserve remuneration will be introduced, in which part of banks’ holdings of excess liquidity will be exempt from the negative deposit facility rate.

And now we prepare for the ECB press conference in 30 minutes.

One benefit of teaching in a political science department with colleagues who also teach law-related subjects is that I have the freedom to create some unusual course offerings. In the spring, I taught a class on “Constitutional Difficulties in the Age of Trump.” Given student demand, I’m now teaching it again this fall (presumably for the last time).

There are downsides to teaching about Trump. He could blow up my syllabus with a tweetstorm that seems impossible to ignore. The class moves quickly through a lot of disparate material, leaving little time for a deep exploration of any particular area of constitutional law. There are topics of passing interest, that will hopefully be once again relegated to the realm of experts in a few years, if not a few months. There is, of course, the risk that students will be so absorbed in the emotional political and policy disputes surrounding the Trump presidency that they will not be able to think critically about the difficult constitutional issues that also surround this presidency.

Fortunately, students seem able to rise to the challenge. Over the course of the semester, they read both critics and supporters of the administration. They are required to write papers that defend positions that are both consonant with the administration’s objectives and that run counter to them. They learn that constitutional issues are generally more complicated than Twitter or cable news would have you believe, and they learn that it is possible to distinguish one’s views about a particular constitutional rule from one’s views about how a particular politician exercises discretion under that rule.

For undergraduates at least, there is something to be said for simply trying to make them more informed and critically engaged citizens. They are eager to better understand these disputes, and fortunately there are resources to help them achieve that. There is a cornucopia of high-quality, accessible, short commentary on current constitutional controversies from sites ranging from the Volokh Conspiracy to Lawfare to Just Security to Take Care. The class leans heavily on the hundreds of freely available excerpts of primary documents in American constitutionalism, from Supreme Court opinions to Office of Legal Counsel opinions to congressional hearings to state and lower court opinions, that my co-authors and I have generated as a companion to our casebook. Those materials can be found here. It is also a reminder that the “constitutional canon” regarding separation of powers issues includes a lot more than Supreme Court cases.

The Trump presidency might create the need to talk about such unusual constitutional issues as the 25th Amendment, self-pardons, and the First Amendment implications of blocking people on Twitter, but it is also an opportunity to draw students into a more serious engagement with Article II and the separation of powers. Given our polarized politics, divided electorate, and the eagerness of Democratic presidential candidates to issue their own creative executive orders, the basic constitutional challenges of presidential power don’t seem likely to be going away anytime soon.

This semester’s syllabus (with hyperlinks to most of the readings) can be found here.

from Latest – Reason.com https://ift.tt/31hcDeB

via IFTTT

One benefit of teaching in a political science department with colleagues who also teach law-related subjects is that I have the freedom to create some unusual course offerings. In the spring, I taught a class on “Constitutional Difficulties in the Age of Trump.” Given student demand, I’m now teaching it again this fall (presumably for the last time).

There are downsides to teaching about Trump. He could blow up my syllabus with a tweetstorm that seems impossible to ignore. The class moves quickly through a lot of disparate material, leaving little time for a deep exploration of any particular area of constitutional law. There are topics of passing interest, that will hopefully be once again relegated to the realm of experts in a few years, if not a few months. There is, of course, the risk that students will be so absorbed in the emotional political and policy disputes surrounding the Trump presidency that they will not be able to think critically about the difficult constitutional issues that also surround this presidency.

Fortunately, students seem able to rise to the challenge. Over the course of the semester, they read both critics and supporters of the administration. They are required to write papers that defend positions that are both consonant with the administration’s objectives and that run counter to them. They learn that constitutional issues are generally more complicated than Twitter or cable news would have you believe, and they learn that it is possible to distinguish one’s views about a particular constitutional rule from one’s views about how a particular politician exercises discretion under that rule.

For undergraduates at least, there is something to be said for simply trying to make them more informed and critically engaged citizens. They are eager to better understand these disputes, and fortunately there are resources to help them achieve that. There is a cornucopia of high-quality, accessible, short commentary on current constitutional controversies from sites ranging from the Volokh Conspiracy to Lawfare to Just Security to Take Care. The class leans heavily on the hundreds of freely available excerpts of primary documents in American constitutionalism, from Supreme Court opinions to Office of Legal Counsel opinions to congressional hearings to state and lower court opinions, that my co-authors and I have generated as a companion to our casebook. Those materials can be found here. It is also a reminder that the “constitutional canon” regarding separation of powers issues includes a lot more than Supreme Court cases.

The Trump presidency might create the need to talk about such unusual constitutional issues as the 25th Amendment, self-pardons, and the First Amendment implications of blocking people on Twitter, but it is also an opportunity to draw students into a more serious engagement with Article II and the separation of powers. Given our polarized politics, divided electorate, and the eagerness of Democratic presidential candidates to issue their own creative executive orders, the basic constitutional challenges of presidential power don’t seem likely to be going away anytime soon.

This semester’s syllabus (with hyperlinks to most of the readings) can be found here.

from Latest – Reason.com https://ift.tt/31hcDeB

via IFTTT

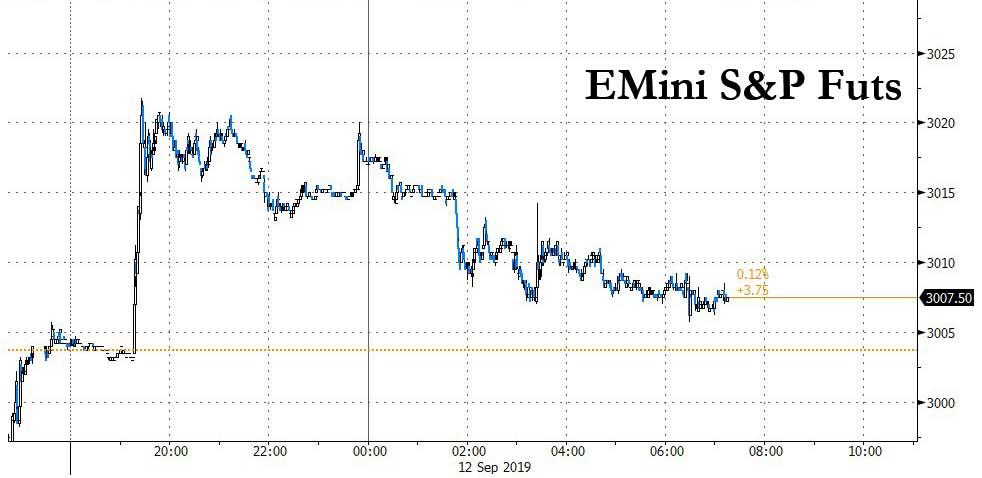

Rally Fizzles As Futures Fade Trade War De-Escalation, All Eyes On The ECB

World stocks and US equity futures climbed to their highest in six weeks on Thursday, even if much of the gains fizzled in the overnight session, while the ECB was set to offer new stimulus measures and the United States and China made mutual concessions in their trade dispute.

Late on Wednesday, President Trump announced on twitter he would delay an increase in tariffs on Chinese goods by two weeks, after China exempted some U.S. drugs and other goods from tariffs, as a sign of “goodwill” toward China. The two moves buoyed stock markets from Asia to Europe and put pressure on safe assets like the Japanese yen.

In response to the Trump tweet, Global Times editor in chief Hu Xijin said that China “Welcome this decision. It should be seen as a goodwill gesture the US side made for creating good vibes for the trade talks scheduled in early October. Yesterday China announced to remove 16 categories of US products from tariff list. Hope reciprocity of goodwill can continue.”

Welcome this decision. It should be seen as a goodwill gesture the US side made for creating good vibes for the trade talks scheduled in early October. Yesterday China announced to remove 16 categories of US products from tariff list. Hope reciprocity of goodwill can continue. https://t.co/OWjGIQ4TPl

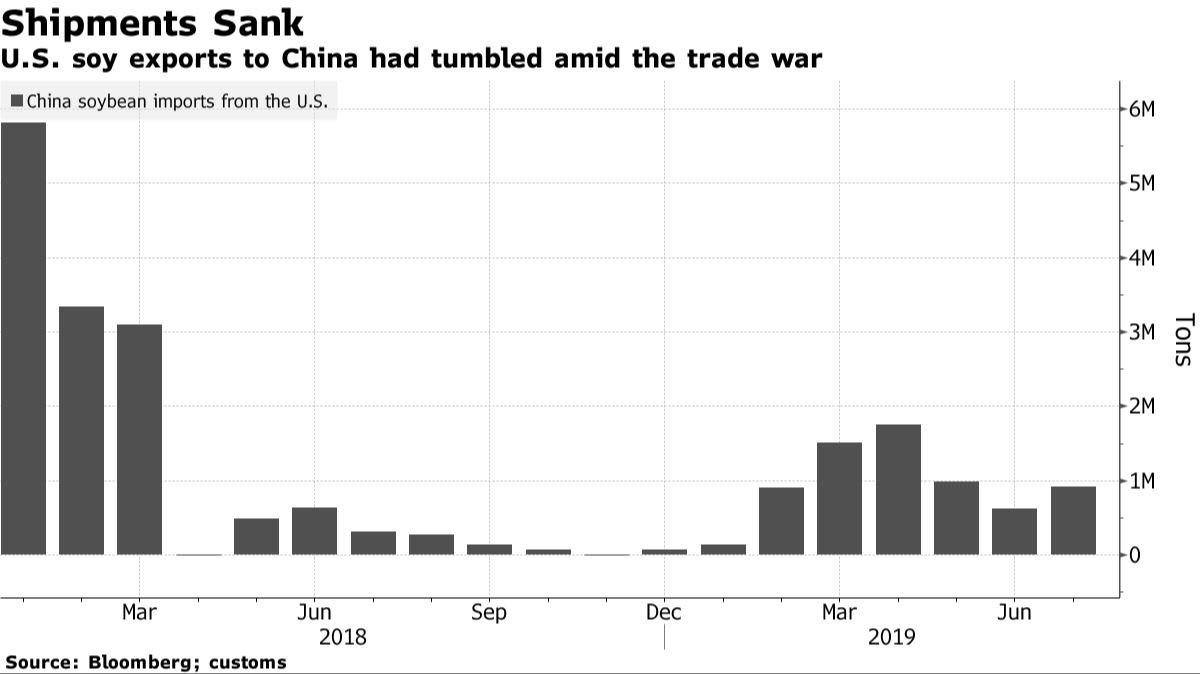

Meanwhile, China is considering whether to permit renewed imports of American farm goods including soybeans and pork, according to people familiar with the situation.

Still, some analysts said investors were getting too eager for good news on the U.S.-China trade war, and warned that the prospects of a quick resolution were still remote, they warned: “I don’t think we’re heading for a deal soon,” said Neil Wilson, chief market analyst at Markets.com. “The market is just buying on any kind of positive news – it seems hungry for anything. It’s setting itself up for a bit of disappointment.”

That may explain why after surging to just shy of all time high after the Trump tweet, futures have since faded much of the move.

The MSCI world equity index rose 0.1% to its highest since Aug. 1. It was on course for its seventh straight day of gains, its best winning streak in since early June.

Europe’s Euro STOXX 600 climbed to its highest in nearly seven weeks, but like US futures gave up most gains. Paris and London markets also relinquished early gains, though Frankfurt held onto a 0.2% advance. Wall Street futures gauges were up 0.1%.

Earlier in the session, Asian stocks rose for a second day, led by material producers and technology firms as trade tensions eased. Most markets in the region were up, with China leading gains. The Topix climbed 0.7% to a four-month high, as Daikin Industries and Daiichi Sankyo offered strong support. Japanese earnings revisions will likely bottom out next month, Citi equity strategist Tomochika Kitaoka wrote in a Sept. 12 note. The Shanghai Composite Index advanced 0.8%, with Kweichow Moutai and Ping An Insurance Group among major boosts. India’s Sensex fluctuated, as a rally in ICICI Bank countered declines in Reliance Industries and Tata Consultancy Services

With trade war apparently moving in the right direction, markets now focused on the ECB’s move, due at 745 ET, which also carries a risk of overly optimistic market expectations as major central banks worldwide have been loosening monetary policy, as inflation expectations are sliding and the powerhouse German economy is at risk of recession. Consequently, ECB President Mario Draghi has all but promised more support. But, as we discussed last night, the central bank’s exact moves are far from certain, and any decision that underwhelms markets could push up borrowing costs.

Among the likely measures are a cut in the ECB’s record-low minus 0.4% deposit rate, a multi-tier deposit rate, and new guidance on rates that would tie any move to certain inflation conditions. A new round of bond buying, the bank’s most potent weapon, is also an option – but policymakers from Germany to France are sceptical about that move.

“We could see some disappointment here. The challenge is more about forward guidance and reassurance for the future,” said Christophe Barraud, chief economist at Market Securities in Paris. “It would be surprising if the ECB launches a big stimulus right now ahead of uncertainties such as hard Brexit and the trade war.”

“Whether the ECB cuts rates by 10 or 20 bps is neither here or there. The big question is whether they restart QE, and if they don’t, we will see a further sell-off in bonds, especially longer-dated ones.” said Chris Scicluna, head of economic research at Daiwa Capital Markets.

In rates, Euro zone government bonds were steady in early trade, after rising from record lows reached a week ago on doubts that the ECB would resume asset purchases.

The optimism over trade and the looming ECB decision were felt in currency markets, too: the euro initially fell to a one-week low of $1.0983 overnight on expectations of ECB easing before steadying in morning trade, although it since spiked amid a wave of short covering. The euro has shed 3.5% since June. With risk-hungry investors emboldened, the Chinese yuan gained 0.4% against the dollar, touching a three-week high of 7.0855.

BMO’s FX strategist Stephen Gallo said he was surprised by the rebound, particularly in the yuan pushing beyond 7.10 to the dollar. “The bigger picture is one of a very tense geopolitical environment that is unlikely to be rectified quickly,” he said. The Japanese yen, a safe haven for nervous investors, fell to a six-week low against the dollar, and was last down 0.1% at 107.88.

In commodities, Brent crude futures fell as a meeting of the OPEC+ alliance yielded no discussion about increasing supply cuts. They focused instead on bringing Nigerian and Iraqi output down to their agreed quotas. Brent crude futures fell 69 cents, or 1.1%, to $60.12 a barrel, heading for a third session of losses.

Market Snapshot

S&P 500 futures up 0.2% to 3,008.25

STOXX Europe 600 up 0.02% to 389.78

MXAP up 0.5% to 159.07

MXAPJ up 0.5% to 513.33

Nikkei up 0.8% to 21,759.61

Topix up 0.7% to 1,595.10

Hang Seng Index down 0.3% to 27,087.63

Shanghai Composite up 0.8% to 3,031.24

Sensex down 0.1% to 37,233.50

Australia S&P/ASX 200 up 0.3% to 6,654.87

Kospi up 0.8% to 2,049.20

German 10Y yield fell 1.5 bps to -0.579%

Euro up 0.2% to $1.1028

Italian 10Y yield fell 5.0 bps to 0.629%

Spanish 10Y yield fell 3.2 bps to 0.223%

Brent futures down 0.6% to $60.46/bbl

Gold spot up 0.4% to $1,503.72

U.S. Dollar Index down 0.1% to 98.51

Top Overnight News from Bloomberg

Mario Draghi is embroiled in one of the most contentious policy meetings of his European Central Bank presidency as he prepares to ramp up monetary stimulus again despite skepticism from the euro area’s biggest economies

The U.S. and China are taking small steps to ease trade tensions, as negotiators prepare for the resumption of face-to-face talks in coming weeks. On Wednesday, Trump said he was postponing the imposition of 5% extra tariffs on Chinese goods by two weeks; China is considering whether to permit renewed imports of American farm goods including soybeans and pork

The full scale of the damage a no-deal Brexit could cause to the U.K. was revealed when Boris Johnson’s government published its worst-case scenario in a document it tried to keep secret. The five-page summary of no-deal planning, code-named Yellowhammer, was released late Wednesday

The Hong Kong Exchanges & Clearing Ltd. plan to take over London Stock Exchange Group Plc is running into multiple obstacles less than 24 hours after the surprise bid was launched, with the U.K. bourse leaning toward rejecting the offer in its current form, according to people familiar

As OPEC and its allies meet, the IEA said it faces a significant challenge in managing the market into 2020. Demand for the group’s crude in the first half of 2020 will be 1.4 million barrels a day below its August output as production surges from their competitors, including the U.S.

Asian equity markets were mostly higher as the region sustained the momentum from Wall St where US-China trade concessions fuelled the S&P 500 past the 3000 milestone and the DJIA back above 27k after China announced a tariff exemption list on imports from US, while US President Trump reciprocated by delaying the next round of tariffs on China to October 15th from October 1st. ASX 200 (+0.2%) and Nikkei 225 (+0.8%) were higher with support seen across the trade sensitive sectors in Australia although energy suffered amid recent losses in oil, while the Japanese benchmark was underpinned by a weaker currency and following better than expected Machine Orders data. Conversely, Hang Seng (-0.2%) and Shanghai Comp. (+0.8%) were mixed despite the encouraging trade developments as some suggested China’s olive branch could be to ease pressure from its weakening economy. The US delay of the tariff increase to 30% from 25% on USD 250bln of Chinese goods was also said to have left some dissatisfied in which Global Times noted comments that the postponement does not mean a big improvement as talks remain tough, while it was also suggested that the delay is far from enough and some called for a removal of the extra tariffs. Furthermore, the downside in Hong Kong was led by the blue-chip energy names and a slump in HKEX after its recent GBP 32bln proposal for LSE which could ultimately be rejected amid doubts regarding political risk and the deal structure. Finally, 10yr JGBs initially declined amid the improvement in trade relations and after similar pressure in USTs as yields rebounded, but later rebounded as support near 154.50 held and amid the BoJ presence for JPY 680bln of JGBs in the belly to super-long end.

Top Asian News

Turkey Can Go Big on Rate Cut Without Erdogan’s Iconoclast Nudge

Yahoo Japan to Pay $3.7 Billion to Take Over Maezawa’s Zozo

Iron Ore Glory Days Seen Numbered as China Demand Rolls Over

A mixed session for European equities thus far [Eurostoxx 50 +0.2%] after the trade-fuelled gains seen at the open somewhat dissipated ahead of the much-anticipated ECB meeting and US CPI data amid the risk that the Central Bank may disappoint. Sectors are mixed with energy the laggard amid price action in the complex. Turning to individual stocks, AB InBev (+3.8%) shares were bolstered to the top of the Stoxx 600 amid renewed efforts to explore an IPO of its Budweiser Brewing unit on the Hong Kong Stock Exchange. Meanwhile, sources stated that LSE (Unch) is poised to reject the GBP 32bln merger offer from the Hong Kong Exchange due to concerns over political risks and deal structure. On the flip side, Whitbread (-2.7%), Lloyds (-2.0) and Accor (-3.3%) are all lower on the back of broker moves. In terms of commentary from banks, BAML sees 5% upside in European stocks over the coming 6-months due to positive EZ PMI momentum. The bank targets Stoxx 600 at 395 points for year end (~389 at time of writing).

Top European News

France’s Bouygues Sells 13% Stake in Alstom for $1.2 Billion

TeamViewer IPO Gives Germany Its First Tech Champion in Decades

U.K. Earnings Would Still Rise in a No-Deal Brexit, Citi Says

Trainline Surges After U.K. Ticket Sales Prompt Guidance Rise

In FX, the EUR has reclaimed 1.1000+ status vs the Greenback and survived another test of technical support ahead of 0.8900 against the Pound having crossed the 100 DMA, but the Euro’s fate will ultimately depend to a large extent on how much policy easing the ECB delivers later, or what President Draghi says to address any disappointment/overexuberance in the post-meeting news conference and Q&A. Indeed, given the wide spread of options signalled by the Bank in July and clearly divergent leanings from the GC since, expectations are far more polarised than usual – see our full preview on the Research Suite. In the run up to 12.45BST and 13.30BST, a spread of hefty option expiries should keep Eur/Usd occupied and contained, with 1.1 bn at 1.0970-80, 1.5 bn at 1.1000 and 1.8 bn between 1.1040-55 vs the 1.1006-32 range so far.

NZD/AUD/CHF – The Antipodean Dollars are just outperforming the Franc at the head of the G10 ranks, as US-China trade relations continue to thaw via President Trump responding to Beijing’s goodwill gesture by delaying planned tariff hikes on Chinese goods for 14 days from October 1 to 15. However, the recently lagging Kiwi has benefited most this time, with Nzd/Usd regaining a firmer foothold above 0.6400, while the Aussie continues to face heavy resistance and cross-winds ahead of 0.6900 and over 1.0700 in Aud/Nzd. Meanwhile, Usd/Chf has retreated towards 0.9900 again, shrugging off softer Swiss producer/import prices, but aided by a broad Buck fade (DXY slipping back to pivot 98.500 compared to a 98.746 peak yesterday) and the aforementioned still defensive Eur (cross meandering from 1.0945 to 1.0915).

CAD/JPY/GBP – All on a softer footing, as the Loonie hands back more gains having failed to sustain its rally beyond 1.3150 and a further downturn in crude prices also weighs on sentiment ahead of US CPI, initial claims and more Canadian housing data. Usd/Cad has subsequently extended to almost 1.3200, in line with Usd/Jpy rising through 108.00 before waning around the 100 DMA (108.15), but holding above decent expiry interest at 107.50-60 (1.6 bn). Elsewhere, Sterling has faded some distance from recent peaks and short of 1.2350 amidst less than positive reports from the EU on the subject of a Brexit breakthrough, as the UK has still not provided a real alternative to the Irish border backstop. Cable is currently just above the 55 DMA (1.2311) circa 1.2325.

EM – Broad gains across the region in part due to the constructive US-China trade developments and the Dollar’s loss of momentum noted above, but with the Yuan also heeding another steady PBoC reference rate overnight, while the Lira has regained some composure into the CBRT after markedly underperforming of late amidst aggressive easing forecasts – again a more detailed primer is available via the Ransquawk website.

In commodities, WTI and Brent futures have been dipping in recent trade after a sideways overnight session, with the JMMC meeting in Abu Dhabi underway. Commentary from oil ministers has largely surrounded the need to bring compliance to 100% for all members. Sources also noted that the oil producers are holding discussions over whether to enhance compliance with oil cuts, which could result in an effective output reduction of around 400k bpd; although, this may be less than participants envisaged. Furthermore, the new-appointed Saudi Energy Minister stated that the Kingdom will continue to over-comply, whilst noting that Saudi October production will be 9.89mln BPD, up from the August level of 9.63mln BPD, which could have added pressure in the oil complex. WTI and Brent futures currently reside below 55.50/bbl and 60.50/bbl ahead of the ECB Monetary Policy decision. Elsewhere, gold prices have reclaimed the 1500/oz to the upside amid a weaker USD and nervousness that the ECB could disappoint. It’s also worth keeping in mind that President Trump delaying the China tariffs does not ultimately change the landscape in regard to sticking points, with China noting that talks remain tough and there will be no compromises on IP if it stalls China’s growth. Copper, on the other hand, has extended gains above the 2.60/lb level ahead of its 100 DMA at 2.66/lb amid continued hope that Chinese stimulus will buoy the demand side of the equation.

US Event Calendar

8:30am: US CPI MoM, est. 0.1%, prior 0.3%; CPI YoY, est. 1.8%, prior 1.8%

8:30am: US CPI Ex Food and Energy YoY, est. 2.3%, prior 2.2%; CPI Core Index SA, est. 264.1, prior 263.6

8:30am: Real Avg Hourly Earning YoY, prior 1.3%

8:30am: Initial Jobless Claims, est. 215,000, prior 217,000; Continuing Claims, est. 1.68m, prior 1.66m

9:45am: Bloomberg Consumer Comfort, prior 63.4

2pm: Monthly Budget Statement, est. $197.5b deficit, prior $119.7b deficit

DB’s Jim Reid concludes the overnight wrap

At the end of August, I pretty much finished this year’s annual Long Term Asset Return Study and am just administering the final touches to it ahead of a launch in the next 10 days. To celebrate the maiden voyage, I will be presenting the findings of the report at DB’s London HQ on Wednesday, September 25th at 8.30am (teas and coffees) for a 9am presentation. The report is entitled “The History and Future of Debt” and I specifically look at the record high levels of global debt and assess the likely future path using historical experience of how the level of indebtedness has ebbed and flowed through time. To register for the event please click here .

It won’t be a surprise to anyone that QE features heavily in the report both in historical terms and my belief that QE will eventually turn into helicopter money in the years ahead and that central bank holdings of government bonds will only grow and grow. With the crucial ECB meeting today, the main talking point in the near term is whether additional QE – that looked so nailed on a month ago – actually gets downplayed in the overall easing package or even postponed.

Before we preview the ECB in full, it’s worth highlighting the following overnight tweet from Mr Trump that shows some small signs of progress in the trade war. He tweeted that “at the request of the Vice Premier of China, Liu He, and due to the fact that the People’s Republic of China will be celebrating their 70th Anniversary….on October 1st, we have agreed, as a gesture of goodwill, to move the increased Tariffs on 250 Billion Dollars worth of goods (25% to 30%), from October 1st to October 15th”. Hu Xijin, of the Communist Party-controlled Global Times newspaper tweeted that he saw Mr. Trump’s decision as creating “good vibes” for the early-October talks. In addition, Bloomberg is reporting this morning that the Chinese government is considering whether to permit renewed imports of US farm goods including soybeans and pork, in a show of reciprocation of goodwill ahead of the upcoming face-to-face trade talks. In terms of markets reaction, the onshore Chinese yuan is up +0.41% this morning to 7.0872 alongside most Asian FX.

Equity markets are also heading higher on the news with the Nikkei (+0.89%), Shanghai Comp (+0.20%) and CSI 300 (+0.40%) all up. The Hang Seng is down -0.12%, weighed down by a slide in the city’s exchange thanks to the surprise $36.6bn takeover bid yesterday from Hong Kong Exchanges & Clearing Ltd for the London Stock Exchange Group Plc, a bold move that would upend the UK bourse’s combination with Refinitiv. South Korean markets are closed for a holiday. Elsewhere, futures on the S&P 500 are up +0.49% while yields have moved up by c. 2bps across the US treasury curve. As for overnight data releases, Japan’s August PPI came in one-tenth lower than consensus at -0.3% mom and July core machine orders stood at +0.3% yoy (vs. -3.7% yoy expected).

Back to the ECB preview now and the package today will likely include the first cut in the deposit rate since 2016 at what will be President Draghi’s penultimate meeting in charge. At time of writing, the market is split between seeing a 62.9% likelihood of a 10bp move lower, and a smaller 37.1% likelihood of a larger, 20bp cut. In their preview last Friday (link here ), our European economists wrote that they expect the ECB to announce a broad policy easing package, but they think the likelihood of QE being a part of that package have declined, as a result of opposition to new QE from some Governing Council members, along with the risk that further QE which flattens the yield curve would be counterproductive for banks. Their view is that there’ll be a 10bp deposit facility rate cut, upgraded forward guidance, and tiering, which would be more positive for banks.

In terms of the specifics, they expect the 10bp deposit rate cut will be followed by another 10bps in December, after Draghi has left office, and think the “or lower” easing bias will be maintained. On tiering, they think that the ECB will keep the mechanism simple, although this may come at the expense of a dynamic solution (one that adjusts continuously to the volume of excess liquidity). And on forward guidance, they think that the more likely option will be using guidance to strengthen the symmetry of the inflation target. The highest level of uncertainty relates to QE. After Draghi’s dovish Sintra speech, QE became part of baseline expectations. However, our economists are concerned about the inconsistency between QE – big QE at least – and tiering if the latter signals an emergent sensitivity to banking, especially given the fact that some ECB officials have spoken out against new QE over the last few weeks. Even the hawks haven’t really pushed back against rate cut expectations. Our economists adjusted their view on QE last week to anticipate a moderately more pro-banking outcome. That is, a steeper curve which results from no QE or QE targeted at the short end or QE targeted at private assets only. Less QE rather than more, which might be the compromise between hawks and doves, fits with the argument.

So this could be the meeting where the ECB implicitly acknowledges that the reversal rate across the whole curve is near to being breeched or has already been. It’s not a coincident that the Euro Bank Stoxx index hit 7 year lows on August 15th, the first day 10yr Bunds ever closed below -0.7%. In fact, over the last 30 years of data (7,715 days) the banks index has only closed lower than the August 15th level on 8 days, 4 during the 2012 Euro sovereign crisis and 4 in 1987. Not even the GFC/Lehman default period saw lower closes. The +12.99% rally since the recent trough has coincided with the yield sell-off, which has been largely associated with lower expectations for QE. Given how important the banking sector is to the European economy are we at a stage where no public-sector QE would actually be more positive for European growth and markets than some? An open question to you all.

Looking at markets now, it was another eventful day in fixed income yesterday with 10yr Treasuries swinging between gains and losses before ultimately selling off for the sixth consecutive session, up +1.0bps. The picture in Europe was more mixed, as 10yr bund yields ended -1.7bps, having been +1.9bps at their intraday high, while BTPs also fell -5.1bps and gilts closed flat. 30yr bund yields ended the session -2.0bps to almost close in negative territory once again, while in credit, US HY spreads rose +1.3bps to end their run of five successive moves tighter, and Euro HY also moved +1.1bps as they widened for a fourth consecutive session. IG supply still runs at high levels, which is causing some indigestion there.

It was a more consistent story in equity markets where advances were seen across the board. The S&P 500 (+0.71%), Nasdaq (+1.06%) and the Dow Jones (+0.85%) all closed higher with Apple leading the way (+3.18%) after the release of its new iPhone 11. Investor sentiment was boosted by the news we highlighted from the Asia session yesterday that China would be exempting a new list of products from import tariffs for 12 months from September 17. It comes ahead of a planned meeting next month where Chinese Vice Premier Liu He will be travelling to Washington. Trade-related stocks performed strongly, with the Philadelphia semi-conduct index up +1.46%. Yesterday’s strong credit data from China helped sentiment as well, as new yuan loans and aggregate financing both rose more than expected. In Europe, the STOXX 600 rose +0.85% to reach its highest level in 6 weeks, although the STOXX Banks index (discussed at length above) snapped a run of 5 consecutive gains to be down -0.21%.

Elsewhere oil fell further yesterday, with WTI -2.44%, after news reports that President Trump had looked at easing Iranian sanctions in order to agree a meeting with Iranian President Rouhani. Former National Security Advisor Bolton had taken a hawkish stance on Iran, and his resignation had already sent oil prices lower as markets reacted to the increased chances of diplomacy with Iran. Less risk of supply disruptions translates to a lower risk premium for the commodity. However, WTI prices are back up +0.90% this morning on the news of delay in tariff implementation mentioned above.

Earlier, President Trump had also tweeted about the Fed again, saying they “should get our interest rates down to ZERO, or less, and we should then start to refinance our debt.”

There was an interesting development yesterday in the Brexit saga, as the Court of Session in Scotland ruled yesterday that the prorogation of Parliament was ‘unlawful’, in another in a series of defeats for Prime Minister Johnson. All eyes will now be on the UK Supreme Court, which is set to hear the case on Tuesday. Meanwhile, a spokesman for the Conservatives ruled out a pact with the Brexit Party in an upcoming general election, which could have potentially monopolised the pro-Brexit vote under a single banner. Sterling fell -0.17%, coming a touch off its six-week high against the dollar.

It was a quite day for data with August US PPI the highlight. It rose to 1.8% (vs. 1.7% expected), while the PPI ex-food and energy rose to 2.3% (vs. 2.2% expected). Roll on CPI today.

Looking to the day ahead, the ECB decision and Draghi’s press conference is the main highlight, while the CBT are also meeting. Our CEEMEA team are expecting a 275bps rate cut, in line with expectations, which follows the 425bps cut at the July meeting, but they see the balance of risks tilting towards a larger-than-expected cut (potentially up to 400bps). They also updated their view on TRY, shifting to a more negative view (link here ) . In terms of data releases, we have Euro Area industrial production data for July, the final August CPI readings for France and Germany and Q2 unemployment from Italy. Meanwhile from the US, we’ve got August’s CPI readings and weekly initial jobless claims. Lastly on the political scene, we have another Democratic primary debate tonight, with the top 10 candidates vying for the nomination all on the same stage for the first time.

The Supreme Court has had a number of major statutory interpretation cases in recent years. These include Yates (is a fish a “tangible object”?) and Bond (was a contaminated doorknob a use of “chemical weapons”?). This term, the big statutory interpretation case is Bostock, consolidated with Zarda. (The filings are collected at the SCOTUSBlog case page.)

I have just posted a new draft paper that discusses Yates, Bond, Zarda and other cases. It is called The Mischief Rule, and (in my view) it poses challenging questions for statutory interpretation, especially about the role of context in understanding the text. Here is the abstract:

The mischief rule tells an interpreter to read a statute in light of the “mischief” or “evil”—the problem that led to the statute. The mischief rule has been associated with Blackstone’s appeal to a statute’s “reason and spirit” and with Hart-and-Sacks-style purposivism; it was rejected by Justice Scalia. But the rule is widely misunderstood, both by those inclined to love it and those inclined to hate it. This Article reconsiders the mischief rule. It shows that the rule has two enduringly useful functions: guiding an interpreter to a “stopping point” for statutory language that can be given a broader or narrower scope, and helping the interpreter prevent “clever evasions” of the statute. The mischief rule raises fundamental questions about the relationship of text and context, about the construction of ambiguity, and about legal interpretation when we are no longer in “the age of statutes.” In many of our present interpretive conflicts, the mischief rule offers useful guidance, for textualists and purposivists alike.

from Latest – Reason.com https://ift.tt/2UPs62Y

via IFTTT

The Supreme Court has had a number of major statutory interpretation cases in recent years. These include Yates (is a fish a “tangible object”?) and Bond (was a contaminated doorknob a use of “chemical weapons”?). This term, the big statutory interpretation case is Bostock, consolidated with Zarda. (The filings are collected at the SCOTUSBlog case page.)

I have just posted a new draft paper that discusses Yates, Bond, Zarda and other cases. It is called The Mischief Rule, and (in my view) it poses challenging questions for statutory interpretation, especially about the role of context in understanding the text. Here is the abstract:

The mischief rule tells an interpreter to read a statute in light of the “mischief” or “evil”—the problem that led to the statute. The mischief rule has been associated with Blackstone’s appeal to a statute’s “reason and spirit” and with Hart-and-Sacks-style purposivism; it was rejected by Justice Scalia. But the rule is widely misunderstood, both by those inclined to love it and those inclined to hate it. This Article reconsiders the mischief rule. It shows that the rule has two enduringly useful functions: guiding an interpreter to a “stopping point” for statutory language that can be given a broader or narrower scope, and helping the interpreter prevent “clever evasions” of the statute. The mischief rule raises fundamental questions about the relationship of text and context, about the construction of ambiguity, and about legal interpretation when we are no longer in “the age of statutes.” In many of our present interpretive conflicts, the mischief rule offers useful guidance, for textualists and purposivists alike.

from Latest – Reason.com https://ift.tt/2UPs62Y

via IFTTT

Turkish Lira Surges After Central Bank Cuts Rates More Than Expected

While the Turkish lira’s status as the world’s favorite carry currency is disappearing with every central bank rate cut, today’s news that the CBRT cut rates by a more than expected 325bps from 19.75% to 16.5% (consensus expected a 17.25%), although less than the whispered 500bps (following Erdogan’s warning that a major rate cut was coming), and down from a recent high of 24%…

… was enough to send the USDTRY tumbling – at least in initial kneejerk reaction – from 5.75 to 5.6830, after the central bank forecast inflation dropping beneath its July forecasts therefore expecting it to get back to target quicker than previously and signalling a normalizing economy following last years lira crisis.

While the rate cut was greater than expected, with Turkey’s inflation now surprisingly running far slower than most had expected in recent months, at just 15%, the real rate is still a solid 1.5%, even if it moves Turkey toward the end of the pack of major EMs in terms of real rates. Of course, how much the inflationary print is accurate, and whether any of the underlying economic assumptions reflect reality in Turkey rather than just what Erdogan wants – and just like Trump, Erdogan wants much lower rates reality be damned – is a different matter entirely.

The CBRT also saw inflation beneath July forecasts and said that keeping the disinflation process on track with the target path requires the continuation of a cautious monetary policy stance.

The central bank also said that the extent of monetary tightness will be dependent on underlying inflation – which just like in the US it is no longer seeing – and noted that the improvement in inflation expectations and mild domestic conditions support disinflation in core indicators.

“In addition to the stable course of the Turkish lira, improvement in inflation expectations and mild domestic demand conditions supported the disinflation in core indicators. In August, consumer inflation displayed a significant fall with the contribution of core goods, energy and food groups. Domestic demand conditions and the level of monetary tightness continue to support disinflation. Underlying trend indicators, supply side factors, and import prices lead to an improvement in the inflation outlook. In light of these developments, recent forecast revisions suggest that inflation is likely to materialize slightly below the projections of the July Inflation Report by the end of the year. Accordingly, considering all the factors affecting inflation outlook, the Committee decided to reduce the policy rate by 325 basis points. At this point, the current monetary policy stance, to a large part, is considered to be consistent with the projected disinflation path.”

In kneejerk response, the Turkish Lira, now yielding over 3% less against its FX pair surged, although these initial reactions tends to be unwound once the investing public, or in this case Mrs Watanabe, reads between the CBRT’s lines.

Beijing Considers Re-Authorizing Imports Of US Agricultural Products In Latest ‘Goodwill’ Gesture

Last night, we reported that President Trump had decided to delay a 5% increase in tariffs on Chinese goods by two weeks, supposedly out of respect for Beijing and its celebration of 70 years of Communist Party rule on Oct. 1. Trump’s decision came less than a day after China waived 25% tariffs on 16 types of US goods to try and “sweeten” the deal ahead of trade talks next month.

Now, in the latest tit-for-tat deescalation of trade tensions, Bloomberg reports that Beijing is considering whether to permit imports of American agricultural products including soybeans and pork, a move that would further alleviate trade tensions while bolstering support for Trump in the midwestern farm states that comprise a sizable chunk of his base. Foodstuffs and farm products were notably not included in the 16 goods exempted from tariffs earlier this week. According to the Ministry of Commerce, Chinese companies have started asking about prices for US soybeans and pork, a sign that they could restart imports in the near future.

Reopening the door to US soybean imports would come at a critical time for Beijing, which this week announced that it would start allowing imports of soy meal from Argentina to offset the drop in US raw soybeans. China halted imports of US farm products in August as trade talks broke down and President Trump ordered more tariffs on Chinese goods.

As fallout from the trade war hits the US and Chinese economies, pressure for a deal is rising.

Chinese officials welcomed Trump’s decision to postpone US tariffs, Ministry of Commerce spokesman Gao Feng said at a press briefing on Thursday. Gao noted that mid-level teams of trade negotiators will soon meet to prepare for higher level talks.

China has been struggling with a weak yuan, factory-price deflation and falling exports. Meanwhile, in the US, factory activity unexpectedly contracted in August for the first time in three years, highlighting the impact of slowing global growth and the trade war.

“Trump’s goodwill gesture suggests that the trade war is starting to bite and the US may be more eager to close a deal,” said Chua Hak Bin, an economist at Maybank Kim Eng Research Pte. in Singapore. “The clock is ticking and Trump’s approval ratings are sliding, with manufacturing now in recession.”

Still, despite the latest round of goodwill gestures, the two sides remain far apart on fundamental issues: Beijing insists that the US must drop all trade war tariffs as part of any deal, while Washington is demanding concessions on IP and state subsidies that Beijing has so far refused.

WSJ reported Thursday morning that Beijing is hoping to narrow the scope of negotiations with the US to only focus on trade matters, and put thorny national security issues on a separate track. Senior Chinese officials hope this approach will offer a path out of the current impasse, before a team of mid-level Chinese officials heads to Washington next week to prepare for the next round of high-level talks.

Will these ‘goodwill’ gestures lead to a breakthrough toward a deal? Or will they prove to be the latest in a series of false starts as the trade war nears the 18th month mark?