The New York Times chose to honor the 18th anniversary of the September 11 atrocity by blaming “airplanes” for carrying out the attack.

Yes, really.

“18 years have passed since airplanes took aim and brought down the World Trade Center,” the Times tweeted from its official account.

The tweet prompted an immediate backlash, with respondents furious the Times appeared to be absolving the terrorists of blame and pinning the responsibility on inanimate objects instead.

The newspaper later deleted the tweet and half way apologized, tweeting, “We’ve deleted an earlier tweet to this story and have edited for clarity. The story has also been updated.”

We’ve deleted an earlier tweet to this story and have edited for clarity. The story has also been updated.

The Times found itself in hot water only a few days ago for praising Mao Zedong, the Communist dictator who starved 45 million of his own people to death, as a “great revolutionary leader.”

They later had to delete and clarify that tweet. This one, appearing as it does on the anniversary of 9/11, is if anything worse.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Here is what I posted on the Volokh Conspiracy on the 10th Anniversary of 9/11:

On this tenth anniversary of 9/11, I am in New York, staying at a hotel in Time Square. On the train to the City, dogs swept the train in Philly, and another K-9 team boarded in Newark to ride to Penn Station. Penn Station has a detachment of national guard with automatic weapons. Security here in Time Square is intense. All cars approaching the square are given a police look over at check points. Trucks are given especially close attention. My guess is that, if there were any bad guys heading towards these targets, they turned tail. They are fearless only when attacking unarmed and defenseless people. But the police and military who are guarding us here tonight, for which I am grateful, cannot be everywhere at all times.

With this in mind, I thought it would be appropriate to mark this day with one of my earliest op-eds on National Review Online — before I joined the Conspiracy — that I published on 9/18/2001:

Saved by the Militia: Arming an Army Against Terrorism.

By Randy E. Barnett

September 18, 2001 11:30 a.m.

A well-regulated militia being essential to the security of a free state. . . .” The next time someone tells you that the militia referred to in the Second Amendment has been “superceded” by the National Guard, ask them who it was that prevented United Airlines Flight 93 from reaching its target. The National Guard? The regular Army? The D.C. Police Department? None of these had a presence on Flight 93 because, in a free society, professional law-enforcement and military personnel cannot be everywhere. Terrorists and criminals are well aware of this — indeed, they count on it. Who is everywhere? The people the Founders referred to as the “general militia.” Cell-phone calls from the plane have now revealed that it was members of the general militia, not organized law enforcement, who successfully prevented Flight 93 from reaching its intended target at the cost of their own lives.

The characterization of these heroes as members of the militia is not just the opinion of one law professor. It is clearly stated in Federal statutes. Perhaps you will not believe me unless I quote Section 311 of US Code Title 10, entitled, “Militia: composition and classes” in its entirety (with emphases added):

“(a) The militia of the United States consists of all able-bodied males at least 17 years of age and, except as provided in section 313 of title 32, under 45 years of age who are, or who have made a declaration of intention to become, citizens of the United States and of female citizens of the United States who are members of the National Guard.

(b) The classes of the militia are —

(1) the organized militia, which consists of the National Guard and the Naval Militia; and

(2) the unorganized militia, which consists of the members of the militia who are not members of the National Guard or the Naval Militia.”

This is not to score political points at a moment of great tragedy, though had the murderers on these four airplanes been armed with guns rather than knives, reminders of this fact would never end. Rather, that it was militia members who saved whatever was the terrorists’ target — whether the White House or the Capitol — at the cost of their lives points in the direction of practical steps — in some cases the only practical steps — to reduce the damage cause by any future attacks.

An excellent beginning was provided by Dave Kopel and David Petteys in their NRO column “Making the Air Safe for Terror.” Whether or not their specific recommendations are correct, they are too important to be ignored and they are not the only persons to reach similar conclusions about the need for effective self-defense. Refusing to discuss what measures really worked, what really failed, and what is likely to really work in future attacks — on airplanes and in other public spaces — for reasons of political correctness would be unconscionable. And we need to place this discussion in its larger constitutional context.

Asking all of us if we packed our own bags did not stop this attack. X-rays of all carry-on baggage did not stop this attack (though it may well have confined the attackers to using knives). And preventing us from using e-tickets or checking our bags at the street (for how long?) would neither have stopped this nor any future attack. All these new “security” proposals will merely inconvenience millions of citizens driving them away from air travel and seriously harming our economy and our freedom. As others have noted, it would be a victory for these murderers rather than an effective way to stop them in the future. A way around them will always be open to determined mass murderers. More importantly, none bear any relation to the attack that actually occurred on September 11th.

Ask yourself every time you hear a proposal for increased “security”: Would have in any way have averted the disaster that actually happened? Will it avert a future suicide attack on the public by other new and different means? Any realistic response to what happened and is likely to happen in the future must acknowledge that, when the next moment of truth arrives in whatever form, calling 911 will not work. Training our youth to be helpless in the face of an attack, avoiding violence at all costs will not work. There will always be foreign and domestic wolves to prey on the sheep we raise. And the next attack is unlikely to take the same form as the ones we just experienced. We must adopt measures that promise some relief in circumstances we cannot now imagine.

Here is the cold hard fact of the matter that will be evaded and denied but which must never be forgotten in these discussions: Often — whether on an airplane, subway, cruise ship, or in a high school — only self defense by the “unorganized militia” will be available when domestic or foreign terrorists chose their next moment of murder. And here is the public-policy implication of this fact: It would be better if the militia were more prepared to act when it is needed.

If the general militia is now “unorganized” and neutered — if it is not well-regulated — whose fault is it? Article I of the Constitution gives Congress full power “to provide for organizing, arming, and disciplining the Militia.” The Second Amendment was included in the Bill of Rights in large part because many feared that Congress would neglect the militia (as it has) and, because Congress could not be forced by any constitutional provision to preserve the militia, the only practical means of ensuring its continued existed was to protect the right of individual militia members to keep and bear their own private arms. Nevertheless, it remains the responsibility of Congress to see to it that the general militia is “well-regulated.”

A well-regulated militia does not require a draft or any compulsory training. Nor, as Alexander Hamilton recognized, need training be universal. “To attempt such a thing which would abridge the mass of labor and industry to so considerable extent, would be unwise,” he wrote in Federalist 29, “and the experiment, if made, could not succeed, because it would not long be endured.” But Congress has the constitutional power to create training programs in effective self-defense including training in small arms — marksmanship, tactics, and gun safety — for any American citizen who volunteers. Any guess how many millions would take weapons training at government expense or even for a modest fee if generally offered?

Rather than provide for training and encouraging persons to be able to defend themselves — and to exercise their training responsibly — powerful lobbying groups have and will continue to advocate passivity and disarmament. The vociferous anti-self-defense, anti-gun crusaders of the past decades will not give up now. Instead they will shift our focus to restrictions on American liberties that will be ineffective against future attacks. Friday on Fox, Democratic Minority Leader Dick Gephart was asked whether additional means we have previously eschewed should be employed to capture and combat foreign terrorists. His reply was appalling. Now was the time, he replied, to consider adopting a national identity card and that we would have to consider how much information such “smart” cards would contain.

Rather than make war on the American people and their liberties, however, Congress should be looking for ways to empower them to protect themselves when warranted. The Founders knew — and put in the form of a written guarantee — the proposition that the individual right to keep and bear arms was the principal means of preserving a militia that was “essential,” in a free state, to provide personal and collective self-defense against criminals of all stripes, both domestic and foreign.

A renewed commitment to a well-regulated militia would not be a panacea for crime and terrorism, but neither will any other course of action now being recommended or adopted. We have long been told that, in a modern world, the militia is obsolete. Put aside the fact that the importance of the militia to a “the security of a free state” is hardwired into the text of the Constitution. The events of this week have shown that the militia is far from obsolete in a world where war is waged by cells as well as states. It is long past time we heeded the words of the Founders and end the systematic effort to disarm Americans. Now is also the time to consider what it would take in practical terms to well-regulate the now-unorganized militia, so no criminal will feel completely secure when confronting one or more of its members.

from Latest – Reason.com https://ift.tt/2Acnk6k

via IFTTT

WeWork’s Flamboyant CEO Sees Net Worth Crash From $14 Billion To $3 Billiion Amid IPO Debacle

The ‘We’ Company founder Adam Neumann has had a terrible run this month, and while it’s hard to feel bad for a billionaire, Neumann has seen his net worth plunge to just a fraction of what it was just one week ago.

On Wednesday, the value of WeWork plunged to a new low of $15 billion, less than one-third of the $47 billion the startup was valued at during its most recent private funding round. Meanwhile, Neumann has watched the value of his 22% stake in the company he founded plunge from $14 billion to just $3 billion. That’snot high enough to earn a place in Bloomberg’s ranking of the world’s 500 richest people.

The prospects for WeWork’s IPO started sinking with a flurry of reports that started with WSJ reporting late last week that the company was considering taking the company public at a valuation of between $20 billion and $30 billion.

Its valuation has only continued to sink.

“Regulatory filings show that early investor Fidelity Investments cut its valuation on We Co. to $18.3 billion in March, well before Wall Street began to scale back its own expectations for an IPO. The predicted valuation is now as low as $15 billion, according to people with knowledge of the matter.”

According to Bloomberg the company’s valuation has shrunk as investors have gotten cold feet about a planned WeWork IPO. Some of the factors that have spooked investors include: its unusual corporate structure and other governance issues, as well as concerns that the company might never become profitable.

Moreover, investors are skeptical about Neumann’s leadership, and are concerned that he has been using WeWork as a personal piggy bank. The founder and CEO was recently forced to reimburse his company for a $5.9 million fee that the company paid to him for rights to its name.

Neumann moved to New York after spending five years in the Israeli Navy. In 2002, he enrolled in Baruch College, where he studied marketing and entrepreneurship. After a couple of failed product launches, including a women’s shoe line and baby pants with built in knee pads, he dropped out of school to pursue his entrepreneurial ambitions full time.

WeWork was founded by Neumann and Miguel McKelvey a decade ago, after the two got the idea for the company after sharing an office space in Brooklyn. Both founders shared a background of living and working in communal spaces; Neumann spent part of his childhood on a Kibbutz, while McKelvey grew up on a commune in Oregon.

Since its founding, WeWork has raised more than $12 billion and opened locations in more than 100 cities. During a 2017 interview with Israeli newspaper Haaretz, Neumann said that he viewed WeWork as a ‘kind of capitalist kibbutz’.

The latest news about Neumann’s fortune prompted a flurry of twitter wits to weigh in, perhaps to inspire investors like Soft Bank, which have lost billions of dollars thanks to their WeWork stake.

In “Epic” Industry Shift, Passive Funds Are Now Bigger Than Active

Several weeks ago, Bank of America predicted that if one extrapolates the existing trends in growing passive funds and shrinking active funds, the D-day when robots and ETFs overtake humans in asset allocation will take place some time in 2022.

In retrospect, Bank of America was wrong, because as Bloomberg just reported, this much anticipated “epic industry shift” in the $8 trillion stock-fund industry has just taken place, with the balance of power officially shifting away from humans.

Citing preliminary estimates released from Morningstar, Bloomberg reports that assets in “passive” mutual funds and exchange-traded funds tracking U.S. equity indexes surpassed those run by “active” stock-pickers for the first time last month.

Following the August flurry of fund outflows from active and inflows into passive funds, assets in equity index-tracking U.S. funds rose to $4.271 trillion, for the first time ever surpassing the $4.246 trillion run by stock-pickers. Specifically, investors added $88.9 billion to passive U.S. stock funds while pulling $124.1 billion from active managers this year through August, the Chicago-based firm estimated.

The inflection point, decades in the making, underscores changes upending a business built on the idea of pros getting paid to outsmart the masses.

And now that D-day for investors has come, the scramble by passive funds to attract even more investors (the only way this business makes sense at far lower margins is with volume and market share) will mean even lower asset management prices, and an even faster rotation out of active, as the market rapidly approaches the singularity that Michael Burry is now obsessed by: a world in which the passive investing bubble finally bursts, but not before markets become woefully inefficient and disconnected from fundamentals – as a reminder, index buying does not discriminate on a fundamental basis and does not reflect all new information available about the company, but merely rewards asset simply due to their presence in one index or another. Thus, in a feedback loop, the more popular and powerful passive investing becomes, the less relevant it will makes active investing, which will lead to even greater outflows from active and into passive.

The culprit behind all of this? Why the Fed of course, which over the past decade has become an activist central bank which has made any material market corrections impossible, thereby robbing – literally – active investors of their bread and butter: reward for getting the downside right, in addition to getting the upside.

There is some hope for humans yet: in international stock funds, active funds still surpass passive, but the gap is narrowing.

Actually, scratch that – none other than America’s most important banker, Jamie Dimon, speaking at an industry conference yesterday, made it clear what the future is for financial professionals: “The battle is more in the tech world at this point than in having brilliant traders.”

Here is what I posted on the Volokh Conspiracy on the 10th Anniversary of 9/11:

On this tenth anniversary of 9/11, I am in New York, staying at a hotel in Time Square. On the train to the City, dogs swept the train in Philly, and another K-9 team boarded in Newark to ride to Penn Station. Penn Station has a detachment of national guard with automatic weapons. Security here in Time Square is intense. All cars approaching the square are given a police look over at check points. Trucks are given especially close attention. My guess is that, if there were any bad guys heading towards these targets, they turned tail. They are fearless only when attacking unarmed and defenseless people. But the police and military who are guarding us here tonight, for which I am grateful, cannot be everywhere at all times.

With this in mind, I thought it would be appropriate to mark this day with one of my earliest op-eds on National Review Online — before I joined the Conspiracy — that I published on 9/18/2001:

Saved by the Militia: Arming an Army Against Terrorism.

By Randy E. Barnett

September 18, 2001 11:30 a.m.

A well-regulated militia being essential to the security of a free state. . . .” The next time someone tells you that the militia referred to in the Second Amendment has been “superceded” by the National Guard, ask them who it was that prevented United Airlines Flight 93 from reaching its target. The National Guard? The regular Army? The D.C. Police Department? None of these had a presence on Flight 93 because, in a free society, professional law-enforcement and military personnel cannot be everywhere. Terrorists and criminals are well aware of this — indeed, they count on it. Who is everywhere? The people the Founders referred to as the “general militia.” Cell-phone calls from the plane have now revealed that it was members of the general militia, not organized law enforcement, who successfully prevented Flight 93 from reaching its intended target at the cost of their own lives.

The characterization of these heroes as members of the militia is not just the opinion of one law professor. It is clearly stated in Federal statutes. Perhaps you will not believe me unless I quote Section 311 of US Code Title 10, entitled, “Militia: composition and classes” in its entirety (with emphases added):

“(a) The militia of the United States consists of all able-bodied males at least 17 years of age and, except as provided in section 313 of title 32, under 45 years of age who are, or who have made a declaration of intention to become, citizens of the United States and of female citizens of the United States who are members of the National Guard.

(b) The classes of the militia are —

(1) the organized militia, which consists of the National Guard and the Naval Militia; and

(2) the unorganized militia, which consists of the members of the militia who are not members of the National Guard or the Naval Militia.”

This is not to score political points at a moment of great tragedy, though had the murderers on these four airplanes been armed with guns rather than knives, reminders of this fact would never end. Rather, that it was militia members who saved whatever was the terrorists’ target — whether the White House or the Capitol — at the cost of their lives points in the direction of practical steps — in some cases the only practical steps — to reduce the damage cause by any future attacks.

An excellent beginning was provided by Dave Kopel and David Petteys in their NRO column “Making the Air Safe for Terror.” Whether or not their specific recommendations are correct, they are too important to be ignored and they are not the only persons to reach similar conclusions about the need for effective self-defense. Refusing to discuss what measures really worked, what really failed, and what is likely to really work in future attacks — on airplanes and in other public spaces — for reasons of political correctness would be unconscionable. And we need to place this discussion in its larger constitutional context.

Asking all of us if we packed our own bags did not stop this attack. X-rays of all carry-on baggage did not stop this attack (though it may well have confined the attackers to using knives). And preventing us from using e-tickets or checking our bags at the street (for how long?) would neither have stopped this nor any future attack. All these new “security” proposals will merely inconvenience millions of citizens driving them away from air travel and seriously harming our economy and our freedom. As others have noted, it would be a victory for these murderers rather than an effective way to stop them in the future. A way around them will always be open to determined mass murderers. More importantly, none bear any relation to the attack that actually occurred on September 11th.

Ask yourself every time you hear a proposal for increased “security”: Would have in any way have averted the disaster that actually happened? Will it avert a future suicide attack on the public by other new and different means? Any realistic response to what happened and is likely to happen in the future must acknowledge that, when the next moment of truth arrives in whatever form, calling 911 will not work. Training our youth to be helpless in the face of an attack, avoiding violence at all costs will not work. There will always be foreign and domestic wolves to prey on the sheep we raise. And the next attack is unlikely to take the same form as the ones we just experienced. We must adopt measures that promise some relief in circumstances we cannot now imagine.

Here is the cold hard fact of the matter that will be evaded and denied but which must never be forgotten in these discussions: Often — whether on an airplane, subway, cruise ship, or in a high school — only self defense by the “unorganized militia” will be available when domestic or foreign terrorists chose their next moment of murder. And here is the public-policy implication of this fact: It would be better if the militia were more prepared to act when it is needed.

If the general militia is now “unorganized” and neutered — if it is not well-regulated — whose fault is it? Article I of the Constitution gives Congress full power “to provide for organizing, arming, and disciplining the Militia.” The Second Amendment was included in the Bill of Rights in large part because many feared that Congress would neglect the militia (as it has) and, because Congress could not be forced by any constitutional provision to preserve the militia, the only practical means of ensuring its continued existed was to protect the right of individual militia members to keep and bear their own private arms. Nevertheless, it remains the responsibility of Congress to see to it that the general militia is “well-regulated.”

A well-regulated militia does not require a draft or any compulsory training. Nor, as Alexander Hamilton recognized, need training be universal. “To attempt such a thing which would abridge the mass of labor and industry to so considerable extent, would be unwise,” he wrote in Federalist 29, “and the experiment, if made, could not succeed, because it would not long be endured.” But Congress has the constitutional power to create training programs in effective self-defense including training in small arms — marksmanship, tactics, and gun safety — for any American citizen who volunteers. Any guess how many millions would take weapons training at government expense or even for a modest fee if generally offered?

Rather than provide for training and encouraging persons to be able to defend themselves — and to exercise their training responsibly — powerful lobbying groups have and will continue to advocate passivity and disarmament. The vociferous anti-self-defense, anti-gun crusaders of the past decades will not give up now. Instead they will shift our focus to restrictions on American liberties that will be ineffective against future attacks. Friday on Fox, Democratic Minority Leader Dick Gephart was asked whether additional means we have previously eschewed should be employed to capture and combat foreign terrorists. His reply was appalling. Now was the time, he replied, to consider adopting a national identity card and that we would have to consider how much information such “smart” cards would contain.

Rather than make war on the American people and their liberties, however, Congress should be looking for ways to empower them to protect themselves when warranted. The Founders knew — and put in the form of a written guarantee — the proposition that the individual right to keep and bear arms was the principal means of preserving a militia that was “essential,” in a free state, to provide personal and collective self-defense against criminals of all stripes, both domestic and foreign.

A renewed commitment to a well-regulated militia would not be a panacea for crime and terrorism, but neither will any other course of action now being recommended or adopted. We have long been told that, in a modern world, the militia is obsolete. Put aside the fact that the importance of the militia to a “the security of a free state” is hardwired into the text of the Constitution. The events of this week have shown that the militia is far from obsolete in a world where war is waged by cells as well as states. It is long past time we heeded the words of the Founders and end the systematic effort to disarm Americans. Now is also the time to consider what it would take in practical terms to well-regulate the now-unorganized militia, so no criminal will feel completely secure when confronting one or more of its members.

from Latest – Reason.com https://ift.tt/2Acnk6k

via IFTTT

Supreme Court Overrules California Judge; Grants Asylum Restrictions At Southern Border

The Supreme Court handed the Trump administration a big win Wednesday afternoon, after two injunctions against asylum restrictions were struck down. The ruling means that US Customs and Border Protection can immediately begin denying migrants asylum at the southern border if they haven’t first applied for safe haven in a “third country” while the greater legal battle over the issue plays out in the lower courts.

Dissenting from Wednesday’s decision were Justices Ruth Bader Ginsburg and Sonia Sotomayor.

#BREAKING: #SCOTUS grants stay of both July 24 and September 9 injunctions against Trump administration rule barring asylum from those who didn’t first apply in a “third country”; allows controversial policy to go into effect on a nationwide basis pending the government’s appeal. pic.twitter.com/Jpni90wsXG

San Francisco Federal Judge Jon Tigar issued a preliminary injunction in July blocking the policy after a coalition of migrant and civil rights groups represented by the American Civil Liberties Union challenged the rules in court, while the 9th US Circuit Court of Appeals narrowed Tigar’s injunction – relegating it to within the 9th Circuit’s jurisdiction. According to the Daily Wire‘s Kevin Daley, “That meant that the third-country transit bar could be applied to migrants intercepted in New Mexico or Texas, but not Arizona and California,” adding that “the 9th Circuit also said Tigar could reimpose a nationwide injunction if he made additional factual findings supporting such a move. Tigar did so and restored a nationwide injunction against the contested rule Monday.”

The ACLU styled Trump’s rules an “asylum ban” before the Supreme Court. The organization claims it violates two federal laws: the Immigration and Nationality Act (INA) and the Administrative Procedure Act (APA).

The INA establishes a general rule that all-comers may apply for asylum, the ACLU argued. Though there are narrow circumstances in which asylum can be denied based on the availability of a third-party alternative, the ACLU believes those conditions are not met here. The plaintiffs also say the new rules should have been subject to a public notice and comment period. –Daily Wire

Approximately 350,000 asylum-seekers have been arrested year-to-date, hailing primarily from El Salvador, Guatemala and Honduras.

The case is No. 19A230 Barr v. East Bay Sanctuary Covenant.

Last Minute Hurdle Emerges In The ECB’s Attempt To “Shock And Awe” Markets

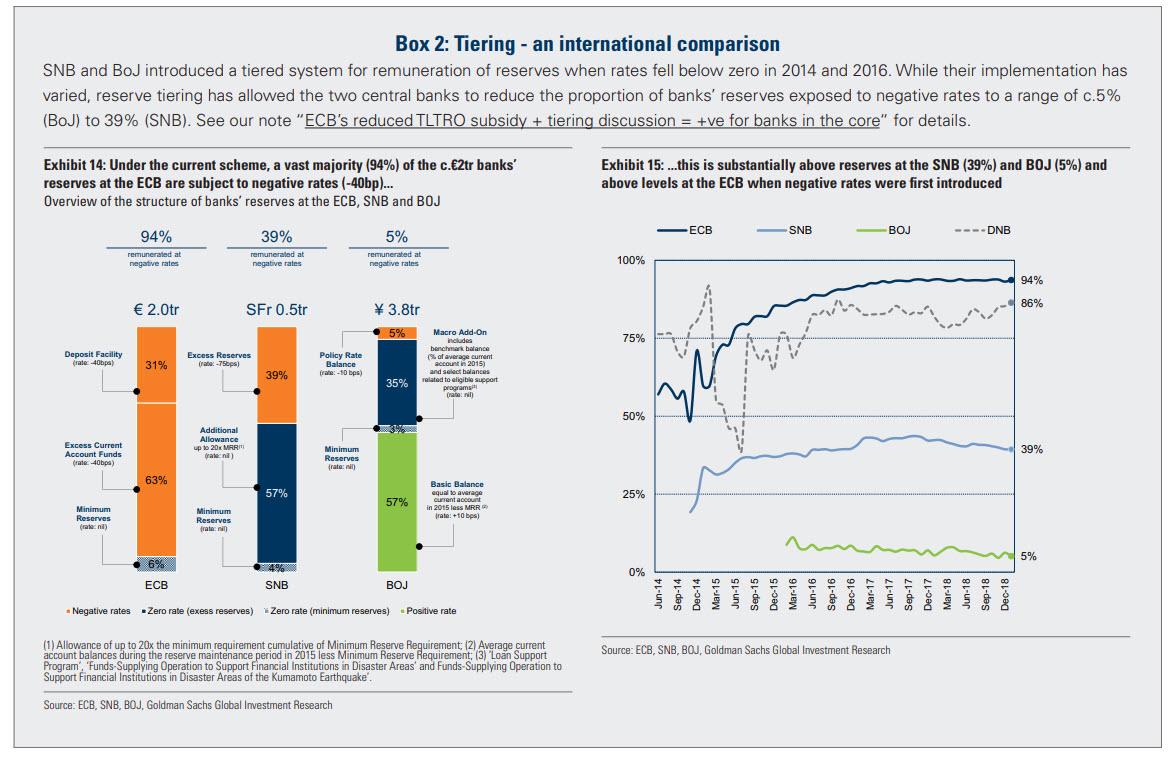

With just hours left until Mario Draghi has to “shock” markets with a bang in the ECB’s triumphant return to monetary easing, unleashing even lower rates and a new round of QE, which however as Goldman warned this morning has to be coupled with rate-tiering or else risks destabilizng Europe’s already frail banking system, the outgoing central banker may instead settle for a whimper.

Can’t wait for his retirement to begin and dump 5 years of failed monetary policy in the lap of Christine Lagarde.

As Mario Draghi approaches his Oct. 31 retirement, and prepares to welcome his replacement Christine Lagarde, who leaves the IMF’s reputation in tatters and scrambling to salvage a record loan to Argentina, the central banker has signaled plans for a massive burst of monetary stimulus to prop up a eurozone economy that is teetering on the verge of a recession with Germany’s economy already said to be contracting for two consecutive quarters.

As such most investor expect a roughly 50% chance of a 20bps rate cut to Europe’s already negative -0.40% deposit rate…

… coupled with a restart in roughly €30BN in corporate and sovereign bond purchases. This is, believe it or not, merely the “medium” package that the ECB will unveil according to banks, such as Goldman:

Yet for once, voices of reasons have emerged: why, if the ECB’s magic cocktail of negative rates and asset purchases, has achieved nothing for the past 5 years, will something be different this time? These same voices have also realized that by punting to the central banks for years, Europe has become crippled when it comes to providing the kind of fiscal stimulus boost that Europe truly needs.

What’s worse, these critical voices are multiplying, including a growing number from the ECB’s own 25-member rate-setting committee.

As the WSJ notes, on one hand, Draghi’s critics say the eurozone economy isn’t weak enough to warrant aggressive new measures just a year after the ECB began phasing out its €2.6-trillion bond-buying program. Borrowing costs for households, businesses and governments are so low, they argue, that easier money will have little effect. The bank’s key interest rate is already minus 0.4%.

Then there are those warning that the measures Draghi has extensively flagged – his “whatever it takes” swan song so to speak – which include further rate cuts and a new bond-buying program, risk leaving the bank with virtually no ammunition if the economy sinks further, while also exacerbating the risk of asset bubbles and damage to the region’s banks. Several eurozone governments moved in recent months to rein in excess lending, including France.

Even French members of the ECB committee are saying “Non!”. As Bill Blain noted earlier, we’ve got senior economists like Jurgen Stark, former ECB Chief Economist saying “with a second asset-purchase programme the ECB will continue to disturb markets and prices do not reflect the risks anymore…. All this is not thought through, just to be activist and show we are not at the end of our toolbox.” What is poor Draghi to do when even his former chief economist is warning that the ECB is pushing on a string and blowing an even bigger asset bubble?

“The ECB’s monetary policy is doing its duty, but it can’t do everything, and it certainly can’t perform miracles,” Bank of France Gov. François Villeroy de Galhau said in a recent interview with Swiss media.

On the other hand, there are those who say that even if Draghi does pull out a bazooka, it will one make a bad situation worse unless Draghi also launches rate tiering with Goldman warning overnight that “it’s critical that tiering accompanies further rate cuts if a large profit hit for the sector is to be avoided. A -20bp cut could lower €-banks EPS by ~6%. A tiering with efficiency on par with SNB scheme could offset ~30% of the hit.“

As we reported previously, in Goldman’s view, tiering is a critical part of any incremental easing package, as without it, “an extremely challenging operating environment becomes worse, and may push an increased number of banks towards breakeven, or even loss-making territory.”

* * *

All of those objections, the WSJ writes, “raise the prospect of a rare defeat at Thursday’s ECB meeting for Mr. Draghi, whose bold new policies held together the fractious currency union during the sovereign-debt crisis.”

One option for Draghi is to do the right thing, do nothing tomorrow, and leave the decision to restart bond buying to Christine Lagarde, who is set to take over the ECB presidency on Nov. 1. Why? Because Lagarde, who was most recently seen leaving Argentina in flames – in some cases literally – after the IMF’s disastrous intervention in the Latin American country, said last week that she would reassess the costs and benefits of the ECB’s controversial policy tools.

Of course, Draghi still has defenders – those who have been elevated from market idiots to sheer investing geniuses by central banks who have made any market correction impossible – who say that it is easier to combat a downturn before it has taken root than to reverse it afterward, pointing for example, to new factory orders in Germany which have plunged to recession levels in while Italy’s economy has flatlined.

This has led to such brilliant non-sequiturs as the following from Olli Rehn, head of Finland’s central bank and a member of the ECB’s rate-setting committee: “If you don’t do anything then you don’t have any side effects, but you don’t have any impact on the economy, either.” Which is a circular way of saying that if you don’t blow up the economy, you… don’t blow up the economy. One of the ECB’s biggest legacy doves, he called on the ECB to launch a broad package of stimulus measures, including substantial new bond purchases. He is also one of the first the pitchfork brigade will be going after when it all comes tumbling down.

All this uncertainty – for a central bank which for years was led by the mantra to telegraph confidence uber alles, no matter how clueless it was – over ECB policy underscores the political and economic challenges facing central bankers in responding to the global slowdown that has followed the China-U.S. trade war.

The biggest problem for the Eurozone is that for the past five years, any time stimulus was needed, the local politicians would come crawling to the ECB’s lobby in Frankfurt demanding just one more hit, as cutting rates was far more easier politically than pushing through unpopular fiscal stimulus. It’s also why eurozone governments, led by notoriously stingy Germany, were unwilling or unable to loosen purse strings to stave off a slowdown.

As such, in a delightful example of reflexivity, the recovery that Draghi’s policies helped engineer is now at risk of collapsing as the consequences of Draghi’s actions finally catch up with the ECB, while Europe’s economy growing at an annualized pace of just 0.8% in the second quarter and its manufacturing sector in recession.

The very dangerous bottom line, as Blain summarized this morning, is that institutions and markets are starting to lose faith in central bankers:

“I find myself surprisingly skeptical, probably for the first time” Stefan Gerlach, a former deputy governor of Ireland’s central bank, said in an interview. “Draghi does not seem to hesitate to bind the hands of his successor. I’m not sure the economy needs it. I’m not sure it achieves much. Some of the arguments the hawks are making sound sensible.”

it gets worse: even establishment types admit the ECB is at the end of the road.

“We are at the end of the efficiency of monetary policy,” France’s finance minister, Bruno Le Maire, said in an interview. “The risks that we are now facing are not related to financial stability [but] how to fuel growth. The response is not only in the hands of the ECB.”

And so, with political pressure rising on central bankers around the world, Draghi may want to leave Ms. Lagarde with room to maneuver according to the WSJ.

“The next ECB president will really need to come up with a game plan to deal with the next downturn,” said Elga Bartsch, head of macro research at BlackRock. “Just turning around and saying, ‘Sorry, we are out of policy options,’ is not going to serve the independence of central banks well.”

Knowing Draghi, however, the last thing he will do is go out with a whimper, so expect a bang for the simple reason that central bankers are now trapped, as Bill Blain explained this morning:

What really, really worries me this morning is the very real possibility markets are losing their faith in Central banks.

What if Central Banks were to ‘fess-up and admit ZIRP and QE has been utter bunkum, hasn’t worked and we need to do something else? What if such an outbreak of honesty triggers a Taper Tantrum of monstrous proportions? It would kill the bond market – just a time when investors are still putting in money to bonds out of stocks in search of yield and because they believe most corporates will weather the looming global recession!

Such a confidence collapse might be about to happen.

The last 10-years of distorted markets and addiction to Central Banks has been the consequence of unwise monetary experimentation,(aided and abetted by some extraordinarily stupid political decisions, like austerity, stupid regulation and bureaucratic behaviour – read my book: The Fifth Horseman for the whole picture).

Collectively, they’ve got the financial markets into their current mess. Bond yields are a massive bubble. Stocks are overvalued. We’re due a reset. Personally, I want to put more money into alternatives – real assets decorrelated from the distortions in financial assets. As a private PA investor, I’m struggling to find such funds to invest in! (IDEAS PLEASE?)

My current worry is Central Bankers are increasingly trapped. If they don’t keep interest rates artificially low rates, then both the bond and stocks bubbles will burst. Even if they sustain the illusion, but keep on cutting, its effectiveness is weakening. The bubbles may burst anyway. It will result in that most of amusing of financial moment… discovering who has been swimming without any swimwear.

Stocks should be in trouble because the global economy is going to slow. Bonds should be in trouble because low rates are not justified by inflation expectations (which are rising) or by deflationary threats – which are real, but not powerful enough to justify NIRP in a real world. Something has to give.

There are two forces at play.

The first is political: In the US, the president is trying to boost his re-election chances by screaming it’s the fault of the Central Bank for not juicing the economy more by slashing rates. In more sensible places, politicians are realising monetary policies don’t drive growth, so they want to juice economies with Fiscal policy – borrow more money to spend into growth.

The second force is overcoming the orthodoxy – which holds fiscal policy is dangerous because it hikes debt to levels where investors lose confidence in the economy. It’s a fair point that’s been proven many times.

All of which makes me look at the recent headlines in Europe; the number of ECB members openly disagreeing with Draghi’s calls to further ease, or German politicians arguing against a fiscal boost for the ailing German economy. These sound very negative and orthodox. But are we looking at a under the radar Central Banking coup in Europe?

According to a number of well briefed papers and articles, the ECB may not give us the easing and bond buying bonanza the markets have been promised. Even French members of the ECB committee are saying “Non!”. We’ve got senior economists like Jurgen Stark, former ECB Chief Economguesser saying “With a second asset-purchase programme the ECB will continue to disturb markets and prices do not reflect the risks anymore.” Or how about Olli Rehn’s recent gem: “if you don’t do anything, then you don’t have any side effects, but you don’t have any impact on the economy either!” Or the French Finance Minister, Bruno Le Maire: “We are at the end of the efficiency of monetary policy. The risks we are now facing are not related to financial stability, but how to fuel growth. The response is not only in hands of the ECB.”

Is it deliberate? If the ECB can’t keep buying.. then maybe its time for Plan B? These comments above all play into the hands of new ECB head, Christine Legarde, whose job will be to politically herd the felines of the ECB and European governments into a Fiscal Union to boost German and European fiscal spending.

Tomorrow’s ECB meeting is going to be critical. Don’t miss it.

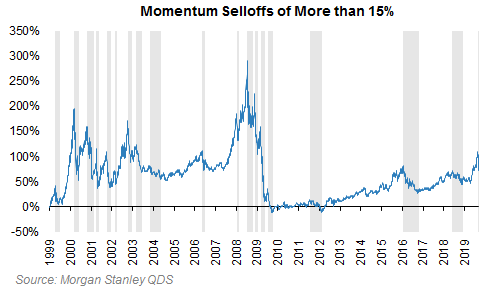

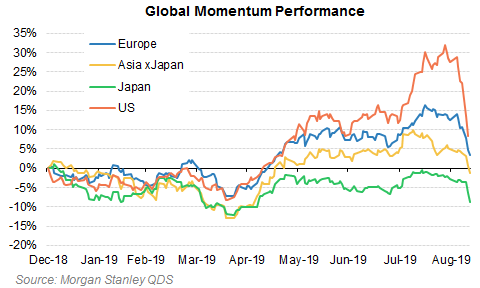

“This Move Is Incredibly Painful”: What’s Next For The Historic Quant Carnage?

As noted overnight, when it comes to the ongoing “quant carnage” which has manifested itself in a historic rotation out of the momentum factor and into value/low vol stocks, JPMorgan’s head quant Marko Kolanovic predicted that “the value rotation can continue and the broad market could move higher going into October negotiations, and if real progress is made, continue into a more sustained rally.”

So, setting the stage for another quant clash today is Morgan Stanley’s own, and highly respected, Quantitative and Derivative Strategies team, which disagrees with Kolanovic’s forecast for a lengthy factor mean-reversion, instead arguing that the bulk of the momentum selloff (and value short squeeze) is almost, or 75% over, even as QDS thinks that there will likely be additional (but slower) unwinds over the next few weeks.

Pointing out what most traders already know, MS notes that “this move is incredibly painful” because both the longs and the shorts are moving counter to positioning, as the long leg of Momentum (reflective of consensus longs – Tech, Defensives) is selling off and the long leg (reflective of consensus shorts – Cyclicals, Value) is rallying. As already discussed overnight, this is an incredibly rare occurrence: over the last week, the long leg selloff has been a 1 standard deviation event, while the short leg has rallied 4 standard deviations. According to Morgan Stanley, “there have only been 7 other weeks since 1999 where both the long and the short leg converged by more than 1 standard deviations each.”

Which leads us to the next obvious question: echoing what Marko Kolanovic said was the number one question from clients in light of such a historic move, namely “when will this end” in the aftermath of another nearly exactly flat day for the S&P 500, and another bloodbath for momentum, Morgan Stanley’s QDS head Chris Metli writes that history suggests the momentum selloff is 75% done, with some residual, if shallower, unwinds over the next few weeks. Specifically, the four factors governing the unwind according to the MS strategist remain: i) volatility (VaRs), ii) P/L, iii) the calendar, and iv) fundamentals.

Higher portfolio volatility (VaR) means less ability to take risk, and all else equal this should mean lower leverage and a continued de-grossing. Whether a quant fund explicitly managing to volatility or a discretionary manager watching VaR risk limits, all investors are sensitive to higher volatility in their portfolio (and yes, portfolio volatilities are higher despite VIX not moving here).

Most investors are still comfortably up on the year, which should slow a de-grossing. But given the size of this P/L shock and a rising focus on year-end, investor sentiment is poor and ability to buy dips is deteriorating.

In Morgan Stanley’s client conversations over the last two days, most investors are looking at this largely as a positioning-driven move, and not seeking to structurally change their portfolios. “This means that without a fundamental catalyst, this unwind is likely on the order of weeks instead of a multi-month regime shift”, according to Metli.

That said, portfolios are fragile – should there be a fundamental shock, this could continue to be very ugly and last much longer.

As a result, Morgan Stanley believes traders should be sensitive to other potential accelerants of an unwind:

The unwind could put more pressure on quant P/Ls, lessening their ability to provide liquidity and market making services to the larger market. The underperformance of sector-neutral momentum versus momentum that has sector tilts (sector-neutral more quant vs sector-tilt more discretionary) is worrisome here, according to MS.

CTAs and Risk Parity funds that are long bonds could need to sell if bond yields continue to rise, pushing bond yields higher still which could exacerbate the short squeezes in Value and the laggard leg of Momentum.

Derisking leading to more aggressive selling of longs, which can put pressure on broader markets and impact a broader set of investors (i.e. a replay of 4Q18).

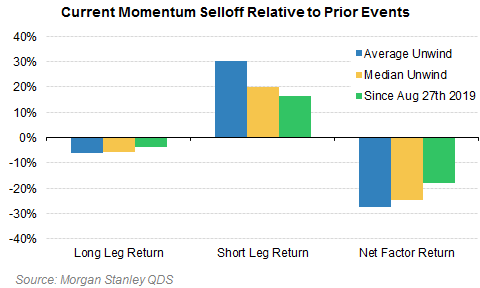

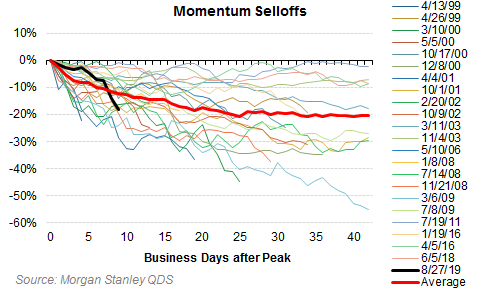

With that in mind, here is how the unwind looks so far compared to prior moves:

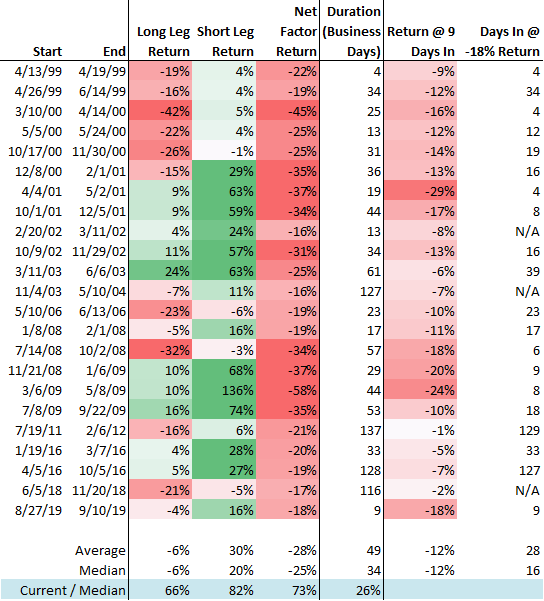

The median momentum move from peak to trough typically lasts 34 trading days and sees a -25% return (of which -20% comes from a rally in the short leg). This selloff has lasted only 26% of the typical duration of a selloff, but has already moved 75% of the way to the median in terms of price.

The above periods are selected by taking selloffs of 15% or more, separated if there was a 10-15% rally in between. But some of these declines can cluster, and cumulative momentum declines can get much worse with historical max drawdowns from peak of -30% or more.

This selloff has been very violent – tracking worse than average and worse than all but 3 prior declines at 9 trading days off the peak.

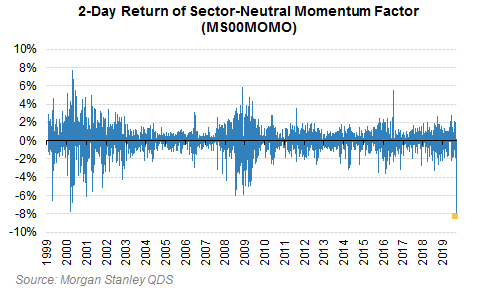

The two day move in sector-neutral momentum (MS00MOMO) is now the worst on Morgan Stanley’s records (back to 1999).

Other measures of momentum (non-sector neutral, MSZZMOMO or the Dow Jones index) aren’t quite as bad but still rank in the worst handful of observations on record.

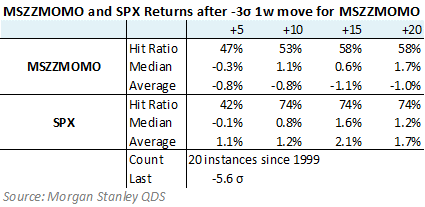

What typically happens to Momentum following a selloff of similar sharpness? It depends on how you look at it. When MSZZMOMO has sold off more than 5% in any given week the factor typically continued to sell off over the following few weeks.

But normalized for the vol environment, following 3-standard deviation Momentum selloffs subsequent returns were positive more often than not (although with a big left tail from a few very negative observations).

Notably SPX returns were typically positive after large Momentum declines, either way you measure it.

Yet while JPMorgan and Morgan Stanley disagree on the duration of the current move, they both agree on one key feature of the recent violent whiplash: namely, that this move is incredibly painful because both the longs and the shorts are moving counter to positioning – the long leg of Momentum (reflective of consensus longs – Tech, Defensives) is selling off and the long leg (reflective of consensus shorts – Cyclicals, Value) is rallying. In fact, according to Morgan Stanley, over the last week the long leg selloff has been a 1 standard deviation event, and the short leg has rallied 4 standard deviations. And the punchline: “there have only been 7 other weeks since 1999 where both the long and the short leg converged by more than 1 standard deviations each.”

Yet the disagreement between the two quants prompts reasserts itself as Metli issues a warning to Kolanovic, who sees a continuation of the current move as a bullish outcome, one which will ultimately lift most of the neglected risk assets: to the Morgan Stanley strategist, that could not be further from the truth, because “what started with simple short covering has spread into long selling, and the momentum unwind is now global. This means it is impacting a broader array of investors and could drive spillover into overall market if it persists.”

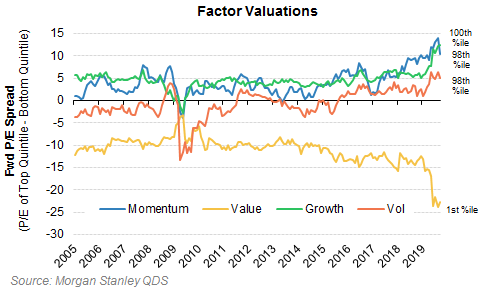

In parting, Morgan Stanley notes that while the price action has been violent, and the likelihood of a protracted move is small, the bank’s quants warn that only a small part of the excesses it flagged as risks in “What if Everyone is Wrong?” have been worked off. As such, factor valuations still remain painfully stretched…

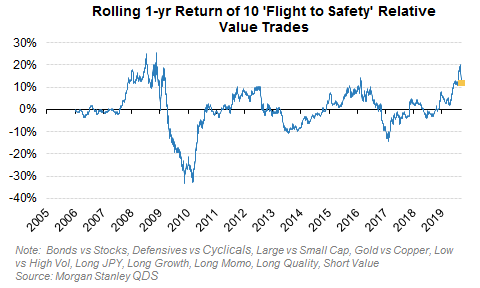

… and the flight to safety trade has hardly been fully unwound.

At the end of the day, it all goes back to central banks, and how much longer they will be able to delay the moment of historic mean reversion, i.e. to before the moment where central banks became equity market activists, and which – if Albert Edwards is right – will send the S&P back to the “generational low” of 666, if not lower.

Should Americans be prohibited by law from belonging to pro-gun rights organizations like the NRA?

“Among all likely voters, 23% favor declaring the NRA a terrorist organization in their home community, while 18% think it should be against the law to belong to pro-gun rights groups like the NRA.” On the other hand, 50% of voters have “a favorable impression of the NRA; 44% do not,” virtually the same numbers as in March 2018.

from Latest – Reason.com https://ift.tt/31aDokN

via IFTTT

Ilya Shapiro and I filed an amicus brief on behalf of the Cato Institute and Professor Jeremy Rabkin in DHS v. Regents of the University of California. We filed the brief “in support of DACA as a matter of policy but [the government] as a matter of law.” The caption caused quite a kerfuffle on social media. You should not judge a brief by its cover, we explained in a new SCOTUSBlog symposium essay:

Most Supreme Court amicus briefs are predictable. Groups that favor outcome A argue that the law supports outcome A. Groups that favor outcome B argue that the law supports outcome B. Occasionally, groups file cross-ideological briefs in which people of opposite political stripes unite to support a specific cause. But even these briefs fall into the same pattern: Regardless of ostensible ideological labels, all the groups on the brief support the policy outcome that the brief’s legal theory advances. . . .

We affirmatively support as a matter of policy normalizing the immigration status of individuals who were brought to this country as children and have no criminal records. (See Cato’s immigration work if you have any doubts.) Moreover, as a matter of first principle, people shouldn’t need government permission to work. But the president cannot unilaterally make such a fundamental change to our immigration policy — not even when Congress refuses to act.

Inside the brief, we advance an argument that was not presented, directly at least, by the government’s briefing in this case.

The attorney general reasonably determined that DACA is inconsistent with the president’s duty of faithful execution. Admittedly, the attorney general’s letter justifying the rescission is not a model of clarity. But it need not be. This executive-branch communication provides, at a minimum, a reasonable constitutional objection to justify DACA rescission. Specifically, it invokes the “major questions” doctrine – outlined by Justice Neil Gorsuch in dissent in Gundy v. United States – which is used “in service of the constitutional rule” that Congress cannot delegate legislative power to the executive branch.

Much to our pleasant surprise, after we filed the brief, President Trump addressed our position in his own inimitable way:

….President Obama never had the legal right to sign DACA, and he indicated so at the time of signing. But In any event, how can he have the right to sign and I don’t have the right to “unsigned.” Totally illegal document which would actually give the President new powers.

To be sure, the tweet has factual mistakes. For example, President Obama didn’t sign the “totally illegal document.” The Secretary of Homeland Security implemented DACA. But for once, the President’s social media account actual bolsters his case in court. He wrote that DACA “would actually give the President new powers.” In other words, DACA relied on a reading of the INA that would delegate legislative powers to the executive that he lacks. Stripped of all legal formalities, the presidential tweet concisely explains why DACA was inconsistent with the president’s duty of faithful execution. And it comes right from the commander in chief.

Candidly, this tweet is far more descriptive than the attorney general’s letter, which dances around the issue of what DACA’ “constitutional defects” are. In our brief, we offer a suggestion to the Court:

Here, the executive branch is on the same page: the previous administration’s reading of federal law that supports DACA would render parts of the INA unconstitutional. For that reason, the attorney general recommended, and the secretary decided, to rescind DACA. The Court should hesitate before reaching an alternate holding, in which the attorney general and the secretary of homeland security, as well as the solicitor general, were simply mistaken about the executive’s faithful execution. The better understanding is that the reference to DACA’s “constitutional defects” was framed in terms of the major questions and non-delegation doctrines, as Justice Gorsuch recognized in Gundy. But if there is any doubt about this important question, the government should be asked to represent its position about DACA’s “constitutional defects.”

With, or without the tweet, the record amply provides enough ground to justify the rescission of DACA.

from Latest – Reason.com https://ift.tt/309Ec8f

via IFTTT

{kind=link}