Saxo Bank: Sanguine Approach To Virus Impact Is Misplaced

Submitted by Eleanor Creagh of Saxo Bank

Summary: Despite the buy the dip mentality that returned to markets last week, Fridays risk off price action seems a more accurate reflection of the current state of affairs. Dip buyers likely jumped the gun last week as the reported coronavirus death toll surpassed the SARS total over the weekend and contagion fears mount following a series of outbreaks in Europe linked to a large business conference in Singapore and additional new cases confirmed on the Princess Dream cruise ship docked off the coast of Japan. We expect price action to remain volatile and continue to be highly susceptible to virus related headlines, jumping from one to the next.

* * *

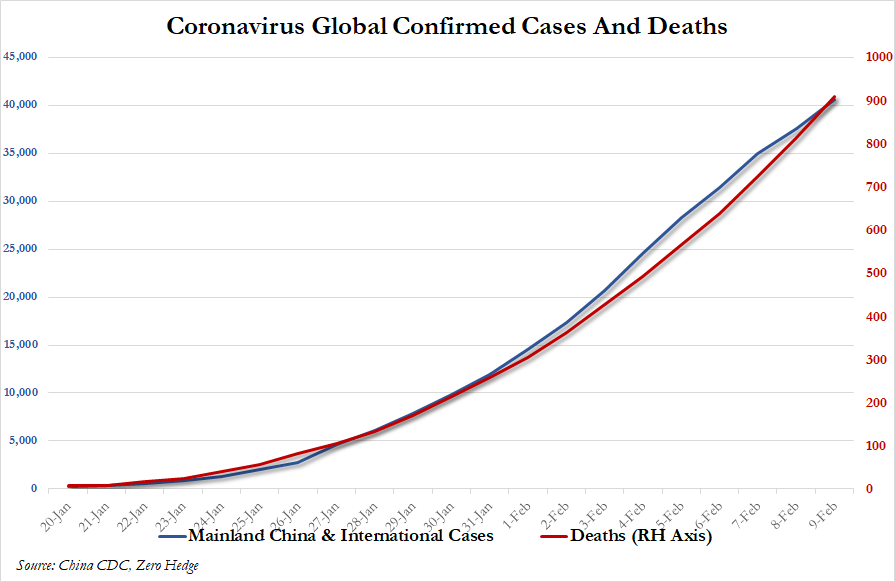

Over the weekend, new cases dropped in China, both in Hubei and outside Hubei. In the meantime, the global death toll increased to 910. Markets remain nervous as confirmed coronavirus infections outside of China mount and we think that risk-off price action will resurface. Downside risks are underpriced, most obviously so in Asia. Assessing the impact of the virus outbreak on global growth is no easy task, and as the human impact increases, so does the response and the economic impact. Singapore has now raised its alert level to Orange, the second highest level (same as the SARS outbreak). Companies continue to warn about the impact of ongoing disruption that will impact both sales and supply chains as factories, offices and shops remain closed and air travel is suspended, hitting both demand and supply.

This impact via the supply chain shock is likely to get worse before it gets better and that risk is not priced into equity markets. As the economic disruption prevails, the potential downwards revisions to growth and economic activity have the capacity to outweigh tentative green shoots, particularly across Asia and the Eurozone (via trade linkages with China). The German auto industry is heavily exposed to China and reports have surfaced that the factory shutdowns are making it hard to source key parts, notwithstanding the hit to sales. China accounts for about 40% of VW’s global passenger vehicle sales, and about 30% at Daimler and BMW. Wuhan and the rest of Hubei province, which has been on extended lockdown, account for 9% of total Chinese auto production, according to S&P Global Ratings. General Motors, Nissan, Renault, Honda and Peugeot owner PSA Group all have large factories in Wuhan. However, the reach extends far beyond the auto sector, from clothing and consumer goods to chemicals and tech, at some level inputs from China are crucial to most to major manufacturing supply chains around the world.

Globalisation has profoundly entwined supply chains, therefore shutdowns and production delays have the capacity to cause unexpected bottlenecks across many production lines even if the virus spread peaks soon. Most consumer electronics are made in China or at least have some component that is made in China, most notably iPhones, consumer gadgets, crystal displays, gaming consoles and LCD screens used in TVs, phones and cars. This leads us to believe that the current risk reward set up for equities generally is unfavourable and we favor defensive positioning and haven plays (gold, US rates).

The week ahead will be crucial for gauging how long it will be before production returns to full capacity, the longer term ramifications of the virus outbreak and the hit to supply chains. Critical markers will be how much of the lockdown across China’s industrial centres can be wound back and how quickly. And whether the contagion risks outside of China continue to escalate or whether the virus will be contained soon.

At this stage the hit to the US economy should be minimal, but China has been hit hard. Although in China the increases in the number of new “reported” cases is slowing, the impact on the economy will continue to grow as the knock on effects from extended shutdowns multiply. The direct effects on foregone sales and supply chains will hit many companies bottom lines, notwithstanding the secondary effects yet to trickle down via lower commodity prices and the like. 3 provinces and 60 cities, almost 400 million people, are now facing some level of lockdown as Beijing tries to contain the coronavirus outbreak. True GDP in Q1 is likely to be close to 0 and potentially negative depending on how protracted the shutdowns become, with risks to forecasts tilted to the downside as the virus still continues to spread along with knock on effects. This shock hits the Chinese economy at a particularly vulnerable period, when longer term structural pressures continue to weigh and activity levels were already precarious as the tariffs and hangover from the deleveraging drive have taken their toll on economic activity. Growth, already under pressure, now has to contend with an unprecedented impact which outweighs that of the 2003 SARS outbreak. China’s policy responses have been stepped up over the past week with liquidity injections helping to allay some investors’ fears and lend support to equity markets. However, these increased policy response signal the authorities anxiety levels are rising, despite the state media awash with proclamations to the contrary.

It is not just the hit to growth that comes at a bad time for China. The ongoing trade war between the US and China already had companies pulling production out of China, diversifying their supply chains and shifting to other countries in the Asian region. The present disruptions add to that conversation and the decision to reduce production dependence concentrated in one specific country and diversify supply chains outside of China.

Amidst these lingering concerns, the US remains well bid. With this USD strength comes an additional hit to growth as the strong USD tightens financial conditions globally, particularly in offshore funding markets. The strong dollar hinders reflationary pulses and curtails green shoots therefore cementing the path for weaker economic growth, adding to the haven bid for long term bond yields.

As ever, this laundry list of concerns is countered by the ongoing return of central bank largesse. Monetary policy, as always, remains a powerful determinant of asset prices, continued central bank liquidity injections lends underlying support to equity markets. With liquidity being pumped and low yields forcing risk seeking behaviour, dip buyers are there on the sidelines ready to step in as valuations correct. Also, as investors re-calibrate long term interest rate expectations at current levels, large amounts of capital is enticed up the risk spectrum into equity markets. Monetary policymakers have already exhibited their willingness to intervene with added stimulus measures in an attempt to extend the cycle, so, for as long as investors feel like central banks have their back and policy rates remain low the longer term tailwinds for equities remain. Though as outlined above, we caution that the current risk reward set up for equities generally is unfavourable and see the potential for risk-off dynamics to resurface.

Tyler Durden

Mon, 02/10/2020 – 09:25

via ZeroHedge News https://ift.tt/2tKn6DH Tyler Durden