“Going Nuclear”? Nomura Explains What More Central Banks Can Do

Via Nomura’s Global Markets Research Team,

There’s more road left for central banks, but there’s no denying it will be bumpy…

For most of the past decade following the global financial (and European sovereign debt) crisis, developed market central banks had been optimistic that economic conditions would, by this stage, have permitted them to move their policy levers closer to “normal”. Their monetary toolkits – having been reset – could then effectively deal with the next recession. Yet the next global crisis, in the form of COVID-19, has already arrived, and the deep contraction in output, incomes and spending it brings with it is are now at hand.

Not only have central banks not had opportunity to sufficiently rebuild their monetary armouries over recent years, but the speed with which policy easing has been required – and delivered – over a period of just two weeks means that in many cases, central banks look to be a spent force. After all, once interest rates have been cut to what is widely believed to be the effective lower bound (or close), provided huge amounts of liquidity to the market, loosened bank capital requirements and promised to pump many percentage points of GDP in the form of quantitative easing into the system, what’s left to do?

We do not deny that central banks have given almost all they have got. But there are still options left open.

Some, such as the ECB, could go further by cutting interest rates deeper into negative territory – after all, President Lagarde does not think rates have yet reached their effective lower bound (ELB). While lower rates could be useful (there is evidence to suggest that lending rates to the real economy are continuing to track official rates down, even from their current exceptionally low level), the impact of another, e.g., 20bp rate cut would very likely be minimal. Others, (e.g.,the Federal Reserve, Bank of Japan, Bank of England and Reserve Bank of Australia) have already arrived at their (self-imposed) ELBs.

Then there are asset purchases. The Fed is now conducting unlimited purchases, the Bank of England is buying around 9% of GDP in primarily Gilts and the ECB’s offering is of similar scale. Stepping up purchases even further is possible – after all, it’s not as if there will be any shortage of government bonds to buy once the fiscal cost of the virus and its impact on economies is tallied (though the ECB in particular may need to relax its self-imposed issue/issuer limits). Directing purchases to where they are most needed could be a next step – whether that be more corporate bonds in the UK (the Fed is supporting credit flows with their emergency powers but they do not currently have the authority to but corporate bonds), or going down the route of Japan and buying equity ETFs (which the BOJ has announced will be stepped up since the virus).

Yield curve control is a popular topic of discussion, as central banks learn from Japan’s experience. The Reserve Bank of Australia is now experimenting with YCC, announcing its decision last week to target the 3Y sovereign bond. And our US economics team thinks the Fed will end up effectively implementing a form of YCC to the extent that over the medium term they will use purchases of Treasurys to ensure that long-term rates do not needlessly constrain the recovery. While there may be moral hazard concerns about implementing YCC by the ECB, it would help the bond markets of those countries where yield spreads to Germany risk blowing out (e.g., Italy). Deploying the firepower of the ESM could also be a good method of containing spreads in Europe.

‘Big bazooka’ has been a term used to describe some central bank actions over the past 2 weeks. But an even bigger bazooka (helicopter money) is a last resort few central bankers seems willing to countenance currently (see here). Money transfers from central banks are a form of fiscal policy. US fiscal authorities announced plans to provide means tested rebates directly to qualifying individuals, so it’s not obvious that central banks need to provide that sort of support to the economy. It might happen (some countries may be more willing to go down this route than others), but space remains to expand conventional unconventional monetary policy (i.e., QE). Still, if the current crisis threatens to go “nuclear” (widespread bank failures etc.) all options must be on the table.

Federal Reserve

What the Fed has done

Over the past ten days the Fed has put in place essentially all of their available options to support the economy. They have:

-

Lowered short-term interest rates to their effective lower bound (ELB), and they have said that they intend to keep rates at those levels “until we’re confident that the economy has weathered recent events and is on track to achieve our maximum employment and price stability goals” (see Fed Cuts Rates to the ELB and Scales Up Asset Purchases, 16 March 2020).

-

They are providing liquidity to the financial system through expanded repo operations and have encouraged greater use of the discount window

-

Initiated open-ended purchases of Treasurys and agency MBS

-

Established a full range of liquidity and credit programs under Section 13(3) of the Federal Reserve Act. This includes:

-

Commercial Paper Funding Facility

-

Money Market Mutual Fund Liquidity Facility (MMLF)

-

Primary Dealer Credit Facility (PDCF)

-

Primary Market Corporate Credit Facility (PMCCF)

-

Secondary Market Corporate Credit Facility (SMCCF)

-

Term Asset-Backed Securities Loan Facility (TALF)

-

The Fed has also said that it intends to establish a “Main Street Business Lending Program to support lending to eligible small-and-medium sized businesses, complementing efforts by the SBA.”

-

-

Expanded central bank liquidity swap lines

During the GFC the Fed explored all options for using its existing authority to support the economy and the financial system. They did everything that they thought would help. Now, in response to the economic consequences of COVID-19 outbreak, the Fed has used all of the tools that they used during and after the GFC except the ones that were specifically designed to support financial institutions.

Going forward

We expect the Fed to use all the authority they have to support the economy.

Short-term interest rates

We expect the Fed to keep short-term rate at current levels – a target range for the funds rate of 0-0.25% – until a robust recovery is well establish and the economy is on track to get back to full employment with inflation at the Fed’s symmetric 2% target. We do not expect them to raise their targets for short rates before the end of 2021. Also, if the significant economic contraction lowers long-term inflation expectations, short-term rates could stay at low levels for longer. Even if inflation expectations remain anchored, transitory but substantial price shocks could keep rates from rising in anticipation of the introduction of a new inflation policy framework such as average inflation targeting.

Purchases of Treasurys and agency MBS

The immediate focus of the Fed’s asset purchases is market functioning. We expect the Fed to maintain the current high pace of asset purchases until markets normalize. That will likely take some weeks. Over the medium term we expect the Fed to use their purchases of Treasurys to ensure that long-term rates do not needlessly constrain the recovery. In effect the Fed may implement a form of yield curve control (YCC) as the economy transitions from extreme contraction to recovery with very high fiscal deficits. Given that the Fed is likely to keep rates low until the recovery is well under way, YCC is also likely to be tied to forward guidance for rates or conditioned on economic conditions.

It seems unlikely the Fed will be expanding their holding of agency MBS for an extended period of time. But we think the Fed will be slow to let the size of their holdings fall.

Separately, given signs of stress in the municipal securities market, the Fed is likely to expand the scope of their asset purchase programs, which currently include only Treasurys and MBS, by including short-dated municipal securities relatively soon. A couple of their lending facilities have already accepted municipal securities as eligible collateral, which lowers the hurdle for the Fed to start purchasing those assets.

Liquidity and credit programs

The Fed has established a broad range programs to support market liquidity and credit under Section 13(3) of the Federal Reserve Act. Under that authority the Fed can lend broadly as long as the the lending is “secured to the satisfaction” of the Fed. This is generally understood to mean that the Fed takes only diminimus credit risk. In that context the potential scale of these programs depends on the credit support provided by the Treasury. We think the big fiscal stimulus bill currently going through Congress will provide about $400bn in additional support for Fed 13(3) programs. That should allow these programs to provide considerable support across a range of financial markets.

Potential changes to the Fed’s authority

At this point we do not believe Congress is actively considering changing the Fed’s authority, although there have been some proposals in the Senate to allow the Fed to purchase longer-dated municipal securities. That said, given the severity of the economic contraction facing the US economy it is certainly possible that such changes may be considered in the future. Under Section 14 of the Federal Reserve Act, the Fed can currently only buy Treasurys, MBS, short dated municipal securities and sovereigns. In a recent speech President Rosengren raised the possibility that the Fed could be given the authority to purchase a broader range of assets including corporate bonds and potentially equities. In a recent op-ed, former Fed Chairs Bernanke and Yellen also suggested that Congress should consider giving the Fed the authority to buy corporate bonds. At this point we do not expect this to happen. But it is a possibility, particularly if COVID-19 proves to be an even bigger threat to the economy. It is also worth noting that in worst-case scenarios we expect long-term interest rates to be very low, i.e., positive, but close to zero. In that case there really is not anything else monetary policy can do to support fiscal policy.

The Bank of Japan: Toolkit almost empty, more dependence on fiscal becoming likely inevitable

Well before the spread of novel coronavirus, the Bank of Japan had already used up the full range of its unconventional toolkit. What the BOJ did in light of COVID-19 were halfhearted small tweaks in some of its unconventional tools. Despite the precautionary stance the BOJ takes against over-dependence on fiscal policy, it is likely inevitable for Japan’s policy mix to incline more towards the fiscal side.

Full range of unconventional tools almost used up

Well before the spread of novel coronavirus, the Bank of Japan had already used up the full range of its unconventional toolkit. QQE (Quantitative and qualitative Easing) deployed an asset purchase program ranging from government debt to risk assets like equity (ETF) and real estate (J-REIT) with a sizable target amount (at first JPY50trn, p.a, then JPY80trn. for JGBs, for example). In January 2016, the BOJ began its negative interest rate policy in addition to QQE. This full range of unconventional tools have eventually been synthesized into YCC (yield curve control) with two “pins” – on short and long (10-year maturity) term rates in an attempt to control the shape of the yield curve. Since July 2018 when the BOJ made its 10-year yield range and the amount of ETF purchases more flexible, the Bank has been inclined more towards communication methods to enhance the looseness of policy. This, in our opinion, has been the implicit signal that the Bank is running out of additional tools.

The reaction to COVID-19 shock

Then came the COVID-19 shock. In its emergency policy meeting on 16 March, the BOJ decided to facilitate corporate finance by increasing commercial paper and corporate bond purchase amounts by JPY2tn, p.a. and to increase ETF and J-REIT purchases to the upper bound – they are now twice as large as their respective targets (JPY6tn and JPY90bn). Those measures, however, are temporary, which illustrates the limits of the BOJ’s policy toolkit as well as hesitation of the Bank to take further risk on its own balance sheet. In particular, the BOJ looks to be bracing for increasing unrealised losses in ETF holdings, with 19,500 on the Nikkei average widely believed to be the breakeven level.

The accounting rule of the BOJ requires additional provision for the unrealised losses in ETFs that will decrease the Bank’s profit and the amount of funds transferable to the state.

Among the current unconventional tools of the BOJ, we do not totally rule out the possibility of a further deep dive into negative policy rates. However, as the BOJ concedes, this could cause a deterioration in the financial conditions of financial institutions, and we think would only be prescribed in the case of sharp JPY appreciation.

More dependence on fiscal policy inevitable

We judge that the BOJ’s reluctance to raise ETF/J-REIT purchase targets highlights the Bank’s precaution against financial dependence on the government. Despite this precaution, however, it seems likely inevitable for Japan’s policy mix to incline more towards the fiscal side. The government so far has decided upon only a small amount (JPY53bn +JPY431bn) of additional fiscal support targeted mostly towards COVID-19 medical spending. It may not be long before the government needs to take much bolder measures. Prime Minister Shinzo Abe announced he will decide a comprehensive stimulus package as early as at the beginning of April.

European central bank

In its ongoing (but presumably delayed) strategic review one area the ECB was intent on exploring was the monetary toolkit open to the central bank at times when more conventional levers have been fully deployed. The virus has meant that the ECB has been compelled to consider its options rather more hastily than it was expecting. As such, over the space of just two weeks, the ECB has:

i) provided more liquidity by introducing additional long-term repo operations;

ii) made its TLTRO-III operations more generous by lowering interest rates on the facility further;

iii) loosened its collateral policy and

iv) added an extra €870bn of asset purchases (worth 7.3% of GDP), including purchases of nonfinancial commercial paper. So what more could the ECB actually do?

Conventional

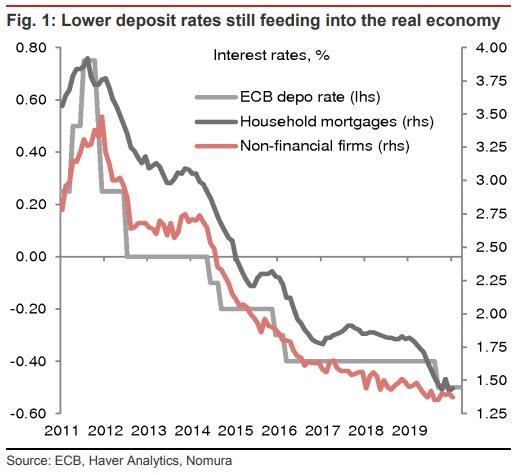

The ECB disappointed the market at its scheduled meeting in March in a number of ways, one of which was to not lower any further its deposit rate – which currently stands at – 0.50%. While much has been said about the ineffectiveness of lowering rates further from current levels, we continue to expect the ECB to cut rates by 20bp to -0.70% at its scheduled April meeting. There are a few justifications for this, in our opinion. First, ECB President Lagarde believes rates are not yet at their reversal level (the point at which lower rates reduce the incentive for banks to lend) nor their effective lower bound. By saying this it could mean that at least some on the Governing Council are willing to lower rates again. Even German Executive Board member Schnabel has suggested that rates have not reached reversal levels yet. Second, as the figure below shows, lowering the deposit rate may be expected to continue to have benefits in terms of lower interest rates experienced by the real economy.

Should the ECB lower its depo rate, then we would expect a simultaneous adjustment to the central bank’s tiering programme, which was introduced last September to support banks during a potentially extended period of negative rates. For example, the ECB could increase the minimum reserve multiplier from its current 6x to 10x should the Bank wish the programme to be as effective as that of the Swiss National Bank.

Unconventional

The ECB could also increase the size of its asset purchase programme. After all, in the statement accompanying its decision to add a further €750bn of purchases to the mix last week the ECB said that “The Governing Council is fully prepared to increase the size of its asset purchase programmes and adjust their composition, by as much as necessary and for as long as needed”.

However, the combined total of purchases that the ECB has already announced – €20bn per month being conducted pre-virus, plus €120bn announced at its scheduled March meeting and the €750bn of additional purchases in the Pandemic Emergency Purchase Programme (PEPP) – amount to some 8.8% of nominal euro area GDP. We think the next step from the ECB in relation to asset purchases will be to lift the issue and issuer limits, something that the ECB has already hinted at: “To the extent that some selfimposed limits might hamper action that the ECB is required to take in order to fulfil its mandate, the Governing Council will consider revising them to the extent necessary”. While it seems very unlikely that the ECB would consider getting rid of the capital key, it is clear the central bank can be flexible in its interpretation to allow more near-term buying of those markets that are particularly stressed while at the same time remaining true to the capital key over the long-term with respect to stocks of purchases.

Yield curve control is very likely being discussed as part of the ECB’s potential toolkit, since it could prove particularly beneficial for peripheral spreads. As discussed above, the current asset purchase programme and the new PEPP are being conducted by the ECB with maximum flexibility, meaning that the central bank can deviate from steady-state cross-country allocation of purchases to address the consequences of “flights to safety” (i.e., widening peripheral spreads). By imposing a cap on yields in Europe YCC could reduce spreads of peripheral countries vs core, though that may end up requiring more purchases of bonds of peripheral countries relative to the core – which would effectively be a stealthy abandonment of the capital key, something which would hardly sit well with some of the more hawkish members of the Governing Council.

Finally on the possibility of FX intervention – the ECB has intervened in the foreign exchange market in the past but typically in concert with other countries (e.g., 2000 and 2011). We are not convinced of the need for the ECB to step into the FX markets in either direction. The euro is already modestly (but not drastically) below its 20-year average, and were it stronger it would lower inflation expectations and potentially make financial conditions worse. If there was ever a time that countries should not play the zero sum game of competitive devaluations then it is now, with the entire world being affected by the virus.

Deeply unconventional

Helicopter money is one of the less likely options for the ECB. Banque de France Governor Villeroy in comments to Les Echos last week stated that “For Europe, there is no question of a helicopter money programme. The measures we have already taken or that we could take are more effective to get through the crisis”. It is worth noting that helicopter money (the printing of money by the ECB to be distributed to euro area governments to fund their fiscal programmes either without the associated purchase of an asset or with a promise that ECB would not accept payment on redemption of the asset) would not necessarily directly contravene the Treaty on the Functioning of the European Union (TFEU) Article 123 which prohibits monetary financing:

- Overdraft facilities or any other type of credit facility with the European Central Bank or with the central banks of the Member States (hereinafter referred to as “national central banks”) in favour of Union institutions, bodies, offices or agencies, central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of Member States shall be prohibited, as shall the purchase directly from them by the European Central Bank or national central banks of debt instruments

This Article governs ECB lending to European governments rather than outright unfunded cash injections. However, helicopter money would clearly fall foul of the spirit if not the letter of the law, and would have few friends among core European countries. Despite our view that helicopter money in the euro area is not just deeply unconventional but also highly unlikely, it is worth noting that Ms Lagarde’s predecessor, Mario Draghi, in September last year lent some support to at least considering the possibility. In response to a question from European lawmakers he said that such ideas (MMT) “have not been discussed by the Governing Council. We should look at them, but they have not been tested”.

ESM, OMT and “coronabonds”

There has been much debate about using the European Stability Mechanism (ESM) to provide support to European economies during the virus. The ESM was formed in the thick of the sovereign debt crisis in late 2012 to provide emergency funding for countries finding market access difficult. It has paid-in capital of €80bn from member states allowing it to borrow on the financial markets at competitive rates and on-lend to those countries in need. It’s lending capacity is €500bn, but with €90bn of loans outstanding (to Greece) its current fire power is €410bn (3.4% of euro area GDP).

Aside from being able to bail out countries with serious economic and funding problems, such as Greece during the sovereign debt crisis, the ESM is able to provide countries with sound economic conditions “precautionary financial assistance”. That is offered via either a Precautionary Conditioned Credit Line (PCCL), which requires a country to be compliant with the Stability and Growth Pact (SGP), or an Enhanced Conditions Credit Line (ECCL) with more onerous conditionality for countries which fail to meet those criteria.

One idea under consideration is the possibility of granting credit lines to multiple member states in order to avoid the stigma of any one country requesting such support. The advantage this would have is that those countries would then be automatically eligible for the ECB’s (thus far unused) Outright Monetary Transactions (OMT) scheme which allows the central bank to purchase unlimited (albeit subject to issue and issuer limits) quantities of a country’s sovereign bonds on the secondary market. Preliminary discussions among the eurogroup have centred around using the ECCL facility to lend up to 2% of an applicant country’s GDP.

This has the support of some on the ECB’s Governing Council, such as Banque de France Governor Villeroy who recently said that “I support from now the idea of exceptional European coronavirus loans, granted by the European Stability Mechanism”.

Another option is one suggested by Bank of Portugal Governor Calos Costa – that of common issuance (possibly by the ESM) in the form of “Corona bonds”, “with the proceeds being channeled to all Member States in need” in order to avert a second sovereign debt crisis. While this would have the added advantage of supplying the market with a safe European asset, there would be questions about how the funds would be allocated (perhaps depending on which countries were suffering the worst health emergencies because of the virus?) and there would clearly be significant push-back against any common bond (whatever its purpose) by countries such as Germany, the Netherlands and Austria. Even with Germany now facing a sharp rise in its own deficit after having announced a 4.5% of GDP fiscal package over the past week, and the virus raising serious existential questions about the euro area, it seems unlikely that hostility to debt mutualisation among the more hawkish countries will be any less than in the past.

Bank of England

The Bank of England is in much the same boat as many other central banks, having almost maxed out its conventional policy easing during the global financial crisis and with economic growth, the output gap and inflation having since failed to recover sufficiently for policy settings to be lifted much off their bottom rung. As a result, the starting point for monetary policy does not leave much room for conventional easing, but unlike the ECB the limits to bond purchases (e.g purchasing no more than 70% of the free float of a bond) are unlikely to be a constraint. There is, therefore, plenty of loosening that the Bank can implement even if it is questionable how impactful it will be at current levels of long-term interest rates.

Conventional

Between end-2007 and March 2009 the Bank lowered interest rates from 5.75% to just 0.50%, a level beyond which it was unwilling to cut at the time on account of it being the MPC’s then effective lower bound (ELB). The Bank’s motivation for this being the lower bound related to its concern about impaired transmission, with bank profitability being potentially squeezed and lending capacity thereby reduced. The Bank reduced further its view on how far it could cut to 0.25% from August 2016, and to 0.10% this month, explaining the reduction in the ELB by improved bank capitalisation and the introduction of a term funding scheme (most recently with incentives to lend to SMEs).

BoE policymakers have discussed the possibility of negative interest rates but have generally ruled the idea out. Current Governor Andrew Bailey’s predecessor Mark Carney said last year that “we don’t see it [negative rates] as an option” while external MPC member Jan Vlieghe in 2016 – despite saying the idea was theoretically possible – noted that it could “undermine the whole bank funding model”. A number of other central banks already have negative interest rates (ECB, BOJ, Riksbank, Danmarks Nationalbank, SNB) – while we would not entirely rule such a policy it seems highly unlikely that the Bank would entertain it before moving to more unconventional means. Guidance on rates – that they will remain at current levels for an extended period of time – may not be overly helpful in situations like the current one where such a statement does not really seem to be in doubt.

The Bank could try to make its current low interest rate policy more effective by improving further the terms of the new term funding scheme (TFSME) and thereby encouraging banks to take up more cash from the BoE at rates close to or at Bank Rate. The scheme will offer, over the coming 12 months, four-year funding of at least 10% of participants’ stock of real economy lending at interest rates at, or very close to, Bank Rate. Additional funding will be available for banks that increase lending, especially to small and mediumsized enterprises (SMEs). However, the Bank has already once improved the terms of this scheme and it is of course demand- rather than supply-led.

Unconventional

The most obvious form of unconventional monetary easing is of course large scale asset purchases, more of which the Bank has announced at its emergency meeting last week. The £200bn of largely Gilts but also high-quality corporate bonds that the Bank intends to buy is worth around 9% of GDP, more than the ECB’s new purchases worth 7.3% of GDP. The Bank could of course direct more of its purchases towards corporate bonds, or indeed other private assets such as asset backed securities and commercial paper, though the Bank and Treasury are already purchasing the latter in their recently announced Covid Corporate Financing Facility. This could help contain credit spreads during a period of acute stress for many firms. However, with fewer corporate bonds available to buy it is important that the Bank focuses on Gilts in order to deliver its large programme quickly enough to make a near-term difference. Another option could be to purchase equity exchange traded funds (ETFs) though this would require a fresh mandate from the Treasury given the increased taxpayer risk associated with such purchases.

Until recently the Fed had announced it would purchase $700bn of assets, made up of Treasurys and mortgage-backed securities. However, it has since gone further and announced instead that these purchases would now be open ended and that they would purchase some $625bn during the first week of operation alone. Open-ended purchases could be an option for the Bank, signalling that the Bank intends to both conduct more loosening and over a longer period of time.

Note that while central bank action has brought down yields, which had spiked as investors had begun to liquidate their positions in favour of cash (and as concerns mounted about sovereign debt sustainability, in some countries more than others), with long-term interest rates in the UK generally exceptionally low we think a more important channel through which QE will operate is that of portfolio rebalancing – in other words, by removing a large stock of gilts from the market this forces investors into other assets further down the risk curve.

One of the potentially more “standard” unconventional policies the Bank could consider is yield curve control (YCC). This has of course been the policy of the BOJ snce 2016 and has recently also been announced by the RBA. While QE focuses on purchasing a certain stock of assets at whatever price the market is willing to accept, YCC instead effectively offers to buy whatever volume of assets the market is willing to offer at a given price or yield. With the BoE already having committed to purchase a substantial amount of Gilts in the coming months at a significant pace, the need for YCC right now seems unlikely. However, should yields spike in government bond markets then YCC could yet be an option – though with UK yields often moving in lock-step with Treasuries and Bunds some sort of globally coordinated YCC policy could prove more effective.

Deeply unconventional

In an interview with Sky last week marking his first week in post, BoE Governor Andrew Bailey was quoted as saying “the Bank of England’s not done” and that “nothing is off the table”. The following day the Bank did of course announce an interest rate cut and asset purchases. But what could the Bank do if it deems that more is required – is a foray into the unknown, the ‘deeply unconventional’, possible?

It is important to be clear about what we are talking about here – namely, helicopter money, or Modern Monetary Theory (MMT). The idea is that a sovereign should never need to default on its domestic-currency debt because a government can always ask its central bank to print its way out. Effectively, what the Bank of England would be doing is printing money to hand over to the government in order to pay its bills. It is equivalent to the Bank printing money to buy government debt but at the same time committing to effectively ‘burning’ its claim on the government.

In our view this is unlikely.

First, there is plenty more space for the Bank to engage in ‘regular’ asset purchases (QE).

Second, and more important, MMT has the potential to lead to market panic (even more than we have now) by raising risk premia on government debt, causing potentially sharp falls in the currency which could contribute to what would be legitimate investor concerns about future inflation.

Tyler Durden

Thu, 03/26/2020 – 14:55

via ZeroHedge News https://ift.tt/2xn6ovD Tyler Durden