Alleged ‘Crisis Profiteer’ Arrested For Coughing On FBI Agents And Claiming He Had Tested Positive For COVID-19

We’re not the first to remark that the novel coronavirus outbreak has exposed the worst of humanity, from spring-breaker ‘covidiots’ to unscrupulous ‘entrepreneurs’ who hit every Costco and Wal-Mart in a 60 mile radius to stock up on cleaning supplies and medical supplies.

They then turned around and sold those same products on Amazon and eBay at ridiculous mark-ups. Some might call it ‘entrepreneurship’, others would call it ‘crisis profiteering’. Despite governors and AGs taking steps to prioritize prosecution of these ‘coronantrepreneurs’ – after all, many big box stores across the northeast and other parts of the country are still out of toilet paper – they persist, and sometimes, many try to act like what they’re doing isn’t a crime.

A south Brooklyn man was arrest last week for allegedly “coughing” on FBI agents who tried to arrest him after investigating him for selling medical supplies including N95 masks at illegal markups. The arrest was one of the first cases of profiteering in the New York area, though other incidences of “coughing” have occurred. One “knucklehead” is even facing terror charges.

The suspect, Baruch Feldheim, 43, was charged with assaulting federal officers and lying to them about his accumulation and sale of medical supplies, the U.S. Attorney’s office in New Jersey said in a statement released Monday, Bloomberg reports.

Ultimately, Feldheim wasn’t charged with profiteering, only with the charges stemming from assaulting the agents. The agents had been staking out Feldheim’s residence in Brooklyn, watching people leave with what appeared to be medical supplies. Prosecutors said that Feldheim sold supplies at markups as high as 700% to doctors and nurses.

Agents confronted Feldheim outside his home on Sunday (March 29). The FBI agents approached Feldheim outside his house, identified themselves and asked him to stay at a safe distance. In response, the agents said Feldheim “coughed in their direction without covering his mouth” and shouted that he had been diagnosed with COVID-19.

Hospitals in New York, New Jersey and elsewhere are running so short on masks and other vital medical gear that doctors and nurses are being forced to reuse disposable masks for days at a time. One doctor in New Jersey contacted Feldheim on March 18 through a WhatsApp chat group called “Virus2020!” and arranged to buy about 1,000 N95 masks and other goods for $12,000.

A report released today by the Office of the Inspector General for the Department of Justice (OIG) warns that the problems found with the FBI’s secret warrants to wiretap former Donald Trump aide Carter Page were not an anomaly. The agency regularly makes mistakes on its applications to the Foreign Intelligence Surveillance Amendment (FISA) Court when it asks for permission to secretly snoop on Americans.

Back in December, the OIG released a blockbuster report showing that FBI agents made a number of significant omissions and errors in their four warrant applications to snoop on Page in the hopes of determining if he was being unduly influenced by Russian officials during Trump’s 2016 presidential campaign.

Inspector General Michael Horowitz was so bothered by the problems with the Page warrants that he declared that the OIG would perform a deeper audit to see if FBI officials were following proper procedures with their other secret FISA warrants.

The results of that deeper audit were published today and they don’t look good for the FBI. The OIG report shows that the agency regularly neglects proper procedures when seeking FISA warrants.

The failing point appears to be adherence to the Woods procedures, a collection of policies implemented in 2001 to make sure that every fact and detail in a warrant application to the FISA court has been carefully vetted for accuracy and to document that process. The FBI failed to properly follow those procedures with Page. Based on this new report, it looks like this failing is a common problem.

How common? The OIG reviewed 29 FISA warrant applications. In 25 of them the OIG identified errors or “inadequately supported facts.” In the other four, the OIG couldn’t find the associated Woods files—records that document that the FBI agents did due diligence to verify factual accuracy—at all. In three of those cases, the OIG is not certain whether any Woods files even exist. So there’s essentially a problem with every warrant application the OIG looked at for this audit.

The report notes that the OIG is not evaluating whether these errors or omissions were material mistakes that would or should have impacted whether the original warrants should have been granted. But that’s not the point, and that’s why this audit is so important. Because the FISA warrant process is so deliberately secretive, its oversight is limited to the FISA court, which depends on the FBI to be honest about the procedures it is supposed to follow. The FBI has a lengthy internal process to double-check warrant applications. This report notes that the internal processes have found close to 400 errors in 39 FISA warrant applications across the last five years. Inspector General Horowitz writes:

We do not have confidence that the FBI has executed its Woods Procedures in compliance with FBI policy, or that the process is working as it was intended to help achieve the “scrupulously accurate” standard for FISA applications.

Horowitz recommends that the FBI put into place a system of examining past Woods procedures compliance problems to train FBI employees to do a better job. And he recommends that the FBI perform a “physical inventory” to make sure that there’s a Woods file for every warrant application submitted to the FISA court.

After the Page warrant audit was released, FBI Director Christopher Wray released a 40-point plan to correct procedures within the department. In the FBI’s official response to today’s OIG report, FBI Associate Deputy Director Paul Abbate contends that the changes that Wray is already introducing, such as more checklists and training, will help fix these problems moving forward.

It’s deeply disturbing that the OIG found problems with every single FISA warrant application it looked at. FISA warrants exist for the purpose of catching spies and terrorists, which is why so much secrecy is permitted. But mistakes and omissions in this secretive process have huge civil liberties implications for any citizen caught in the government crosshairs. Normally, citizens can turn to the courts for relief when warrants are misapplied. But that’s not the case with FISA warrants.

Historically, major crises have led to expansions of federal government power. As Robert Higgs documents in his classic book Crisis and Leviathan, this tends to happen even if the crisis was partly caused by misguided federal policies, and even if the federal response to the crisis has serious flaws of its own. So far, however, the coronavirus crisis seems like it might be an exception. There is some value to the decentralized nature of the response to the crisis, but also some risks. And it is far from clear that the crisis won’t ultimately result in a major expansion of federal power.

As Walter Olson documents in a Wall Street Journal op ed, so far it is state governments that have taken the lead in combating the virus. The “shut down” and “stay at home” orders that have affected millions of Americans are almost entirely issued by state and local authorities. These have also—so far—taken the lead in trying to boost the capacity of the health care system to handle the surge in coronavirus cases.

The federal government’s coronavirus “social distancing” guidelines, by contrast, are largely advisory. With the important exception of draconian new restrictions on international travel and migration, the lion’s share of coronavirus-related regulations affecting ordinary citizens are the work of state and local authorities. Donald Trump may have high TV ratings, but the actions of governors like Gavin Newsom (California), Andrew Cuomo (New York), and Mike DeWine (Ohio) are having a much bigger on-the-ground impact.

There is some value to this relatively decentralized approach to combating the virus. The US is a large and diverse nation, and it is unlikely that a single “one-size-fits-all” set of social distancing rules can work equally well everywhere. In addition, state-by-state experimentation with different approaches can increase our still dangerously limited knowledge of which policies are the most effective.

Moreover, if one policymaker screws up, his or her errors are less likely to have a catastrophic effect on the whole nation. Here, there is a tension in the views of those who both advocate a much more centralized policy but also (correctly in my view) believe that Donald Trump is often malicious or incompetent. The worse he is, the less we should want to see even more power concentrated in his hands.

As Olson points out, giving the states the lead role on public health issues is not a new idea, but one embedded in the original meaning of the Constitution. The Founding generation regarded most public health issues as primarily a state responsibility beyond the scope of the federal government’s enumerated powers. In his landmark 1824 opinion in Gibbons v. Ogden, Supreme Court Chief Justice John Marshall—who generally advocated a broad conception of federal power by the standards of the time—listed “Inspection laws, quarantine laws, [and] health laws of every description” as part of “that immense mass of legislation which embraces everything within the territory of a State not surrendered to the General Government.”

There is, in fact, a long history of state and local governments taking the lead in battling the spread of contagious disease. During the 1918-19 flu pandemic, state and local restrictions were the primary means of inhibiting the spread of the virus, while the federal government did very little.

While there is much to be said for state-led efforts, they also have at least two serious limitations in the current crisis. First, the coronavirus is—apparently—highly contagious and can spread quickly from one area to another. This means that a state or locality with overly lax policies can potentially “infect” its neighbors.

I lack the epidemiological expertise to assess the extent of this risk; it may vary from place to place. It is also possible that it can be mitigated by coordination between neighboring jurisdictions. Still, the possibility of “externality” effects—in which one state’s policies harm its neighbors—is a standard critique of decentralization. And the spread of a deadly disease is a particularly severe example of this problem, one that may be more difficult to address than many other types of externalities.

Second, one of the major checks on bad state and local policies is the ability of people to “vote with their feet” against them by moving elsewhere. Foot voting enables some people to escape harmful or oppressive government policies, and also gives jurisdictions incentives to avoid them in the first place, for fear of losing key parts of their tax base. In most situations, foot voting is one of the biggest advantages of political decentralization.

But its effectiveness is greatly reduced in our current situation situation. Though some states have enacted quarantine requirements on people entering from epidemic hot sports, interstate migration has not—so far—actually been banned. But even aside from legal restrictions, interstate movement in the midst of a pandemic will be extremely difficult, at best. Where it remains feasible, it could potentially risk spreading the disease further—at least until we have enough testing capacity to effectively screen would-be movers (and others).

Hopefully, foot voting will become safer more feasible again, as testing improves, and parts of the economy begin to recover. At the moment, however, it is nowhere near as effective as it would need to be to provide a meaningful constraint on ill-advised state and local policies. That includes both policies that are overly lax—and thereby allow the virus to spread—and those that are overly restrictive, and thereby cause more harm to liberty, the economy, and social welfare than can be justified by their health benefits.

Externalities and other similar problems might yet lead to a greater centralization of power during the crisis. Centralization could occur even in some areas where it isn’t really needed, because public opinion might prefer a seemingly strong federal hand on the tiller in the midst of a crisis. Political ignorance is widespread, and many voters may be unwilling or unable to objectively evaluate the effectiveness of either federal or state policies. For many, the default response to a terribly dangerous situation might be to clamor for large-scale intervention of the largest and most powerful government available.

It is also worth remembering that the massive $2 trillion “stimulus” bill passed by Congress has already caused a huge increase in federal spending, and made many more people, industries, and subnational governments more dependent on federal largesse. Much of what is in the bill may be a justified emergency measure. But that spigot—like other expansions of government power in the midst of crisis—may not be easy to cut off even after the emergency ends.

In sum, the coronavirus crisis has so far featured states taking the lead in crafting the US response. This federalist approach has some real value. But it has downsides, as well. It is too early to tell how severe those flaws are. Despite the current starring role of state governments, it is also too early to rule out the possibility that the coronavirus crisis will ultimately result in a major expansion of federal government power.

from Latest – Reason.com https://ift.tt/3ayr8zh

via IFTTT

Speaking to CNN’s Jake Tapper, National Institute of Allergy and Infectious Diseases Director Dr. Anthony Fauci suggested that between 100,000 and 200,000 deaths could occur. Fauci quickly added that he didn’t want to be held to that figure given model imperfections and constantly shifting pandemic trends. Earlier this week, President Donald Trump proffered that keeping the COVID-19 pandemic death rate to between 100,000 and 200,000 would mean that “we altogether have done a very good job.”

The White House coronavirus task force is reportedly taking into account the disease and deaths projections made by the University of Washington’s Institute for Health Metrics and Evaluation (IHME) model. If current social distancing and stay-at-home requirements are sustained through May, the model estimates that about 84,000 Americans will die of COVID-19 by the beginning of August. The model also forecasts that COVID-19 will peak on April 15 at around 2,214 daily deaths and that June 28 is likely to be the first day where COVID-19 deaths fall below 100 per day.

Interestingly, the number of U.S. COVID-19 deaths projected by the IHME model is similar to those that occurred during the 1957-58 pandemic flu. Researchers estimate that the global case-fatality rate—the percentage of infected patients who died of the disease—was about 0.67 percent for that flu pandemic. That is substantially higher than the typical seasonal flu rate of around 0.1 percent. For the United States, researchers estimate that about 25 percent of Americans were infected by that strain of influenza, killing about 116,000 of them. That would yield a case-fatality rate of 0.27 percent, about three times worse than the seasonal flu average. (A rough calculation assuming a 25 percent infection rate and the same case-fatality rate would project about 223,000 deaths from the current COVID-19 epidemic.)

One of the crucial differences between the 1957-58 flu and the current novel coronavirus epidemic is that no social distancing was implemented as public health policy back in the 1950s. In fact, a special late August 1957 meeting of the Association of State and Territorial Health Officers in Washington, D.C., concluded that, “there is no practical advantage in the closing of schools or the curtailment of public gatherings as it relates to the spread of this disease.”

A 2009 article in the journal Biosecurity and Bioterrorism noted that “no efforts were made to quarantine individuals or groups [in 1957-58], and a deliberate decision was made not to cancel or postpone large meetings such as conferences, church gatherings, or athletic events for the purpose of reducing transmission. No attempt was made to limit travel or to otherwise screen travelers.” Schools opened as usual and the disease swept across the entire country.

The Biosecurity and Bioterrorism authors concluded that the 1957 outbreak did not appear to have a significant impact on the U.S. economy. They cited a 2006 Congressional Budget Office calculation suggesting that another flu pandemic the size of the one in 1957-58 might reduce real GDP for the year by 1 percent but would likely not result in a recession. In cold-blooded terms, boosting the number of deaths by 100,000 above the annual toll of 1.7 million in 1957 had no deep and lasting effects on the U.S. economy.

As my Reason colleague Jacob Sullum asks, “Is preventing COVID-19 deaths worth a severe recession?” Sullum cogently argues that the answer depends on the lethality of the disease. Unfortunately, the public, politicians, and public health officials won’t have a clear answer to that vital question until population screening using serological antibody tests for COVID-19 infections is done.

My Reason colleague Brian Doherty cites a brand new study that suggests that early adoption of stringent public health measures, e.g., closing down schools, theaters, churches, and so forth, in response to the 1918 Spanish flu epidemic actually experienced a more robust economic bounce back than cities that reacted more slowly.

In the meantime, assuming that the epidemiological models are even approximately right, the chief reason why the number of COVID-19 deaths in the U.S. may be held down to 1957 pandemic flu levels is because modern public health officials have recommended social distancing measures instead of just letting the current epidemic run its course.

from Latest – Reason.com https://ift.tt/33YBS7D

via IFTTT

“Government help to business is just as disastrous as government persecution… The only way a government can be of service to national prosperity is by keeping its hands off.”

Congress has just approved an economically bloated $2.2 trillion spending relief bill, an amount more substantial than the GDP of all but a handful of countries. It is only the third massive relief bill, and we’ve been told several trillion dollars more would have to get spent. Then there are the trillions of dollars more of Federal Reserve Board liquidity injections.

We are starting to talk about real money here.

The politicians believe that sending $1,200 checks to people will “stimulate” the economy.

Among the many mistaken provisions of this new law is a welfare benefit to workers that pays them more money if they quit and become unemployed than if they stay on the job.

Here we go again.

A decade ago, during the height of the folly of the bank bailouts and trillions of dollars of spending for “shovel-ready projects” (that didn’t create jobs but plunged our nation into greater indebtedness), I noted in a Wall Street Journal article that with each successive bailout and multibillion-dollar economic stimulus scheme from Washington, the politicians were reenacting the very acts of economic stupidity that Ayn Rand parodied in her 1,000-page-plus 1957 novel “Atlas Shrugged.” In many surveys, “Atlas” rates as the second most influential book of all time behind the Bible.

For those of you who have not read it (first, shame on you!), the moral of the story is that politicians invariably respond to crises—that, in most cases, they created—by spewing out new, mindless government programs, laws and regulations.

These, in turn, generate more havoc and poverty, which inspires the politicians to spawn even more programs. At which point, the downward spiral repeats itself until there is a thorough societal collapse.

Isn’t this precisely what is happening now?

In the book, the well-meaning politicians pass bills such as the “Anti-Greed Act” to prevent companies and wealthy people from making too much money. Another of my favorites was the “Equalization of Opportunity Act,” which required successful people who invented things and started new businesses to share their wealth.

Now, in real life, Sens. Elizabeth Warren and Bernie Sanders propose legislation like this all the time.

They rant daily against “greedy” millionaires and billionaires (though Sanders dropped “millionaires” the moment he became one) and wonder whether the wealth producers of our economy deserve to exist at all.

And these two were competitive in the Democratic presidential nomination.

We are living through the Ayn Rand dystopia right now. We have given police-state powers to the government to shut down “nonessential businesses” and tell people whether they can play golf or go for a hike. Some of these measures may make sense based on public health, but at what point are we degrading the rights of individuals to choose risks for themselves?

At one point in “Atlas Shrugged,” the incompetent rent-seeking politicians finally have to admit that they have brought the economy to its knees with all the do-goodism.

Out of desperation, they ask the heroic business owners in society what they must do.

“First, abolish the income tax,” they are told.

Sound like a wild-eyed idea today? Guess what?

For the $2 trillion-plus that Congress has just spent to protect the economy, we could have completely eliminated the personal income tax on every worker and business this year.

Isn’t it abundantly evident which would have been the smarter choice to revitalize our economy?

I can just hear Warren shriek: “This would benefit ‘the rich!’“ But, of course, the people who are suffering most from the lockdown on the economy and other power grabs by the government today are the lowest-income workers.

In “Atlas Shrugged,” everyone gets poor, and if we stay on our current turn toward statism and don’t stand up for our rights, we will be poorer and a lot less free.

* * *

Stephen Moore is an economics journalist, author, and columnist. The latest of many books he co-authored is “Trumponomics: Inside the America First Plan to Revive Our Economy.” Currently, Moore is also the chief economist for the Institute for Economic Freedom and Opportunity.

Under Armor To Produce 100,000 COVID-19 Masks Per Week

America’s economy has transformed into a wartime economy. Companies are quickly changing over production lines to produce medical equipment that will aid first responders and health care systems with tools to win the fight against COVID-19.

Ford, GM, and Tesla have already pledged to make ventilators, mobilizing thousands of employees and erecting factories that could start producing these life-saving machines in the near term.

Under Armour is another company that is transforming some of its production lines to manufacture face masks, shields, and specialized fanny packs to support health care workers in the Baltimore–Washington Metropolitan Area, reported Maryland Daily Record.

Under Armour employee designing COVID-19 mask

The Baltimore-based sports apparel brand has held discussions with Johns Hopkins, MedStar Health, LifeBridge Health, and other regional care organizations about distributing face masks and other medical equipment to health care workers.

Under Armour expects to produce 100,000 masks per week.

“When the call came in from our local medical providers for more masks, gowns and supply kits, we just went straight to work,” Randy Harward, senior vice president of Advanced Material and Manufacturing Innovation at Under Armour, said in a statement.

“More than 50 Under Armour teammates from materials scientists to footwear and apparel designers from laboratories in Baltimore and Portland quickly came together in search of solutions,” Harward said.

We noted that shortages of protective gear at major hospital systems are so bad at the moment, that doctors and nurses have gone to local news oulets and social media to voice their concerns about a failing system. This has led to the firing of some health care workers, as their employers do not want the public to know about the horrid conditions.

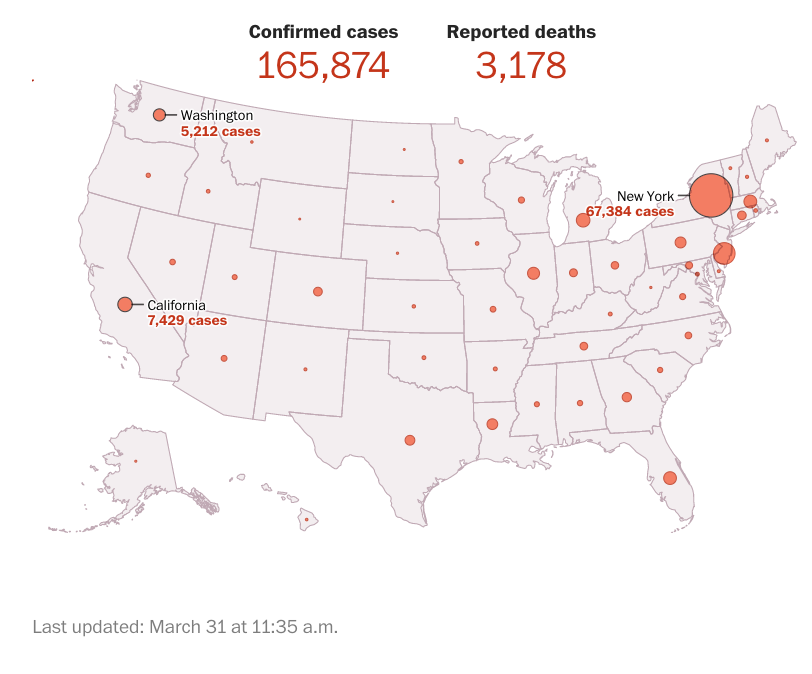

In Maryland, more than 1,660 people have tested positive for the virus, with 18 recorded deaths. Across the country, there are 165,874 confirmed cases and 3,178 deaths. The virus could peak next month, but it is anyone’s guess when the curve flattens. Even then, there’s a risk that the virus will return in several waves.

Under Armour isn’t the only company making masks and protective gear, CNBC’s Carl Quintanilla has the full list:

Now in the mask/gown business:

* UnderArmour

* Brooks Brothers

* GM

* Fanatics

* MyPillow

* Gap

* Neiman Marcus

* Nordstrom

* Eddie Bauer

* Ralph Lauren

* Canada Goose

* L.L. Bean https://t.co/vFbcNbDGj1

Speaking to CNN’s Jake Tapper, National Institute of Allergy and Infectious Diseases Director Dr. Anthony Fauci suggested that between 100,000 and 200,000 deaths could occur. Fauci quickly added that he didn’t want to be held to that figure given model imperfections and constantly shifting pandemic trends. Earlier this week, President Donald Trump proffered that keeping the COVID-19 pandemic death rate to between 100,000 and 200,000 would mean that “we altogether have done a very good job.”

The White House coronavirus task force is reportedly taking into account the disease and deaths projections made by the University of Washington’s Institute for Health Metrics and Evaluation (IHME) model. If current social distancing and stay-at-home requirements are sustained through May, the model estimates that about 84,000 Americans will die of COVID-19 by the beginning of August. The model also forecasts that COVID-19 will peak on April 15 at around 2,214 daily deaths and that June 28 is likely to be the first day where COVID-19 deaths fall below 100 per day.

Interestingly, the number of U.S. COVID-19 deaths projected by the IHME model is similar to those that occurred during the 1957-58 pandemic flu. Researchers estimate that the global case-fatality rate—the percentage of infected patients who died of the disease—was about 0.67 percent for that flu pandemic. That is substantially higher than the typical seasonal flu rate of around 0.1 percent. For the United States, researchers estimate that about 25 percent of Americans were infected by that strain of influenza, killing about 116,000 of them. That would yield a case-fatality rate of 0.27 percent, about three times worse than the seasonal flu average. (A rough calculation assuming a 25 percent infection rate and the same case-fatality rate would project about 223,000 deaths from the current COVID-19 epidemic.)

One of the crucial differences between the 1957-58 flu and the current novel coronavirus epidemic is that no social distancing was implemented as public health policy back in the 1950s. In fact, a special late August 1957 meeting of the Association of State and Territorial Health Officers in Washington, D.C., concluded that, “there is no practical advantage in the closing of schools or the curtailment of public gatherings as it relates to the spread of this disease.”

A 2009 article in the journal Biosecurity and Bioterrorism noted that “no efforts were made to quarantine individuals or groups [in 1957-58], and a deliberate decision was made not to cancel or postpone large meetings such as conferences, church gatherings, or athletic events for the purpose of reducing transmission. No attempt was made to limit travel or to otherwise screen travelers.” Schools opened as usual and the disease swept across the entire country.

The Biosecurity and Bioterrorism authors concluded that the 1957 outbreak did not appear to have a significant impact on the U.S. economy. They cited a 2006 Congressional Budget Office calculation suggesting that another flu pandemic the size of the one in 1957-58 might reduce real GDP for the year by 1 percent but would likely not result in a recession. In cold-blooded terms, boosting the number of deaths by 100,000 above the annual toll of 1.7 million in 1957 had no deep and lasting effects on the U.S. economy.

As my Reason colleague Jacob Sullum asks, “Is preventing COVID-19 deaths worth a severe recession?” Sullum cogently argues that the answer depends on the lethality of the disease. Unfortunately, the public, politicians, and public health officials won’t have a clear answer to that vital question until population screening using serological antibody tests for COVID-19 infections is done.

My Reason colleague Brian Doherty cites a brand new study that suggests that early adoption of stringent public health measures, e.g., closing down schools, theaters, churches, and so forth, in response to the 1918 Spanish flu epidemic actually experienced a more robust economic bounce back than cities that reacted more slowly.

In the meantime, assuming that the epidemiological models are even approximately right, the chief reason why the number of COVID-19 deaths in the U.S. may be held down to 1957 pandemic flu levels is because modern public health officials have recommended social distancing measures instead of just letting the current epidemic run its course.

from Latest – Reason.com https://ift.tt/33YBS7D

via IFTTT

Last year, the World Health Organization (WHO) officially classified video game addiction as a mental disorder. The classification is for people who demonstrate impaired ability to control their game playing and an “increasing priority given to gaming to the extent that gaming takes precedence over other life interests and daily activities,” despite “the occurrence of negative consequences.”

But now, with much of the global economy shuttered due to a pandemic, and health experts issuing increasingly strenuous recommendations for people to avoid leaving the house whenever possible, the WHO is encouraging people to stay home—and play video games.

The WHO is supporting a game industry initiative dubbed #PlayApartTogether, which is designed both to encourage people to play video games and to educate them about social distancing practices designed to slow the spread of the novel coronavirus. The initiative, according to USA Today, is backed by a roll call of major industry players, including Activision Blizzard, Riot Games, Unity Technologies, Amazon, Twitch, and YouTube Gaming.

There’s nothing inherently contradictory about the WHO’s messaging, but it does serve as a reminder that gaming has social and health benefits. Although video games have become far more popular in recent years, they are still sometimes subject to a cultural stigma, a perception that they are time-wasters at best, socially corrosive at worst. That stigma has been around for as long as I can remember, from the early 1990s congressional hearings on violence in games like Mortal Kombat to the continuing efforts by politicians and pundits to tie acts of real-world violence to playing video games—despite the persistent lack of evidence.

On the contrary, there is some evidence that video games can have health benefits, particularly when it comes to managing chronic pain. Multiple studies over the years have found that video games can help reduce physical pain and mental distress, control anxiety, and assist with trauma recovery. The reason why is simple: Games keep you engaged and focused on virtual tasks—and in the process, they distract you from what hurts, or from what nags at your mind. Today, with millions of Americans newly out of work, and many more stuck in an indefinite state of quasi-lockdown, it’s unfortunately probable that there are a lot of anxious, distressed people out there. Video games won’t solve their underlying problems. But they can distract them from those problems for a little while.

As I have written previously, many of today’s games also serve another purpose as well, one that’s increasingly valuable at a time when we’ve all been unexpectedly forced to become shut-ins: They connect you with other people. Multiplayer online games are joint activities for competitive and cooperative play, and some seem to act as much like social networks as anything else.

As for me, I’ve spent several recent evenings playing Doom Eternal, a high-energy, tactically complex, grindhouse throwback to the pulpy shooters of the 1990s. (If nothing else, its existence today, more than 25 years after Congress first took an interest in game violence, nearly all of which have seen declines in youth violence, suggests how misplaced the worries of the political class were.) And I’ve continued to plug away at Borderlands 3, which is currently serving up a smorgasbord of typically rare legendary weapons. Someday soon, I’ll probably play Control. At least once a day, I’ve thought it’s a real shame that Cyberpunk 2077, which is exactly the sort of gigantic, immersive game seemingly built for a nation of unexpected shut-ins, was pushed back from its original April release date.

What I’ve gained from these games hasn’t changed, but now, perhaps, it’s more valuable than ever: a break from the world, and a break from myself. Gamers have always understood the value of a little social distance.

from Latest – Reason.com https://ift.tt/2Uvwzt6

via IFTTT

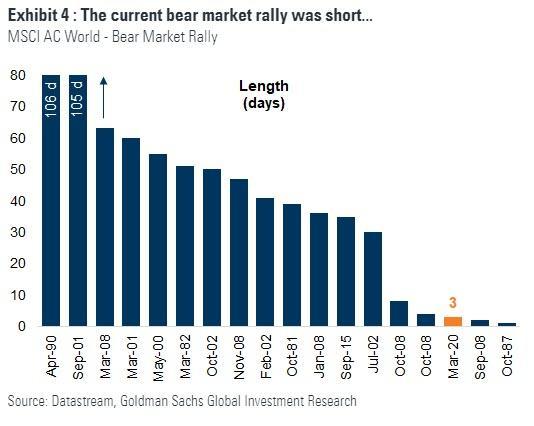

“We Are Buyers Of Dips”: Wall Street’s Biggest Bear Turns Bullish

For much of 2019, Morgan Stanley’s chief equity strategist Micheal Wilson issued a weekly sermon of fire and brimstone in his Monday Morning market takes, which contrasted with the euphoric pronouncements by his peers at other banks – most notably Goldman, which in December hilarious declared that the US economy is “structurally less recession-prone today”, which probably explains why three months later the same bank cut its Q2 GDP estimate to -34%…

… earning him the moniker of Wall Street’s biggest bear (a few permabearish exceptions such as Albert Edwards were excluded from the tally), not to mention quite a few angry clients. Then, in November, just as the melt up phase of the post “Not QE” market was kicking in sending stocks to all time highs every single day, Wilson got the proverbial tap on the shoulder, and threw in the towel raising his S&P “bull case” price target to 3,250, however not without a slew of warnings that the most likely outcome was another retest in stocks lower.

In retrospect, Wilson should have held fast to his bearish conviction as the unprecedented March market crisis confirmed he was spot on (even if for different reasons).

And yet, demonstrating just how fickle Wall Street fates can be, just as Goldman turned beyond bearish, warning today that the recent rally was just a bear market bounce…

… Wall Street’s “biggest bear”, Michael Wilson turned bullish, paraphrasing Michael Hartnett who famously says that “markets stop to panic when officials start to panic”, and in his latest strategy note writes that “crises lead to bailouts and this time it’s extreme given health angle. As a result, the inevitable credit crunch could be truncated this time, leaving us buyers of dips.”

Explaining the reasoning behind his reversal, Wilson first lays out how we got here, noting that “in the past month, we’ve experienced a full bear market (-20%) and full bull market (+20%)” extreme volatility which follows a period of extreme calm during which we observed some of the lowest volatility readings in history.

Then in an appeal to the Austrians inside all of us (by which we mean Zero Hedge readers), Wilson points out that as noted by Hyman Minsky, the onset of a market collapse can be brought on by the reckless speculative activity that defines an unsustainable bullish period – i.e. the Minsky moment.

Sound familiar? If one accepts that 4Q19 was a speculative frenzy driven by liquidity rather than fundamentals, such a conclusion is compelling.

This, incidentally, is Wilson’s – rather subdued – victory lap; it would have been far less subdued had Wilson not turned semi bullish in November, but since it may have been his job or his conviction, we’ll let it slide. That said, Wilson’s argument is spot on, and has to do with the fact that while Covid was the spark for the crisis, the gasoline that was poured on the crash was the unprecedented build up of the trillions in debt over the past decade, that lifted asset prices to their February all time highs…. and the resulting violent unwind. To wit:

Excess leverage explains the ferocity of the decline in risk assets and the economy. While the focus right now is on COVID-19 as the cause of the bear market, the conditions have to be in place for a market and economic crash like we have just experienced.

To Wilson, it is important to acknowledge how and why we got here “as it may help us understand and predict what happens from here” especially since “the necessary conditions for a Minsky-type moment referred to above require leverage in the system.”

So before moving on, Wilson explains that in his view there are two primary areas of excess leverage in this particular episode that have been building for the past decade – corporate credit and the shadow banks.

First on corporate credit.

We have never seen corporate leverage as high as it is now. Much of this credit was added because credit markets have rarely been so inviting to issuers. This is the direct result of the financial repression era orchestrated by central banks during and after the Great Recession. In short, the abnormally low cost of borrowing has encouraged companies to lever up and use this financial leverage to drive better earnings growth in what has been a sluggish economic recovery. Companies are capitalist entities and so they are simply acting in their fiduciary duty to shareholders when they behave in such a manner. Much of this financial arbitrage has been executed via share buybacks, which is now being criticized by members of Congress as they pass the largest fiscal stimulus in history. It’s important to note that low growth is very different from negative growth. Now that we have entered a recession, the corporate bond market knows the risk of default is much greater – hence the dramatic moves we have seen in credit spreads in the past month. As an aside, the correction in stocks really took a turn for the worse when tensions between Russia and OPEC caused a collapse in oil prices. This is what triggered the stress in corporate credit markets, in our view, which contributed significantly to the crash in stocks and the economy. Many acknowledge that credit markets are more important to the functioning of the economy than equity. As bad as the moves were in stocks this month, they were much worse in credit than they were in equities on a risk-adjusted basis.

Second is the shadow banks which are unregulated financial market participants.

Without singling out one particular group, these entities also ballooned in size and scope after the financial crisis. Some of this is due to the easy monetary conditions and low borrowing costs provided by central banks while it’s also due to the fact that the traditional banking system is more tightly regulated, which has allowed many of these entities to get bigger in direct lending type activities. Because the shadow banks are unregulated, they may have become too big, which is why they are now having an outsized impact on financial markets as they lever, like last year,and then de-lever like last month.

Of course, it is hardly news to anyone (at least on this site), that the same factor that crushed the system last time around, is also the same one that led to the current crisis – namely debt. The coronavirus was just the selling catalyst; and once the liquidation feedback loops kicked in and the debt had to be unwound, we got the quad-witching disaster of March 20 when the S&P was trading at levels below Trump’s inauguration. In any case, we compliment Wilson for daring to something which is increasingly frowned upon in the country of “free speech” – and twitter – tell the truth, especially when it is inconvenient. With that in mind, the good news, according to Morgan Stanley, is that the regulated banking system is stronger than normal for this part of the cycle – when we are entering a recession – which means credit should still remain available. The Fed has a viable system to get the capital they are providing to the places that need it most as the economy contracts and cash flows dry up. From that perspective, “this is very different than 2008-09 and one reason we believe the Fed’s extraordinarily aggressive actions to date, which include intervening in the corporate credit markets directly, will ultimately shorten the duration of this recession even if they can’t stop the severity of the slowdown in the very near term.”

And here is another instance of Wilson admirably telling the truth about what the Fed is doing:

They are, in effect, bailing out the bad actors in the corporate credit market, which should truncate the pain for both investors and issuers, and – eventually – the economy.

One final truth:

The fact that a health crisis is now the villain of this recession arguably makes this correction less painful than it would have been otherwise for credit markets, and the shadow banks.

After all one can’t really depose or sue a virus. In fact, one can almost claim that the coronavirus outbreak was perhaps the most “convenient” thing that could have happened to the US financial and debt bubble: by forcing a global economic reset, it gave a carte blanche to triple down on the same debt that crashed the system twice already… and will crash it again.

But not for some time… which is why in its response to the question that is number one among its clients (incidentally the same question posed by Goldman clients), namely “will US equity markets make fresh lows in this bear market”, Wilson answer that his short answer is no “for the major averages and most stocks.” The longer answer is based on several key factors Wilson thinks are unique to this correction:

1. Recent lows were made during what can only be described as a forced liquidation bylevered players – aka shadow banks… Both systematic strategies and active managers are now basically “sold out” and have very low risk/leverage at this point. In other words, it’s hard to imagine the kind of liquidation that we just witnessed in March could happen again from these much lower levels of leverage.

2. This past week, credit markets stabilized thanks to unprecedented support from the Federal Reserve and other central banks. After the past 10 years, we have no doubt in their resolve to stabilize both the funding and credit markets. Most investors we speak with agree and are actively looking to put capital into IG, Mortgages, Agency, Securitized paper and anything else the Fed has said they will be buying directly. Even high yield has responded positively, which the Fed is not buying. Perhaps the most positive market signal last week was the fact that high yield remained in positive territory on Friday even after equity markets sold off sharply into the close. The weaker US dollar is also a good sign that policy (both monetaryand fiscal) is now viewed as getting ahead of the curve.

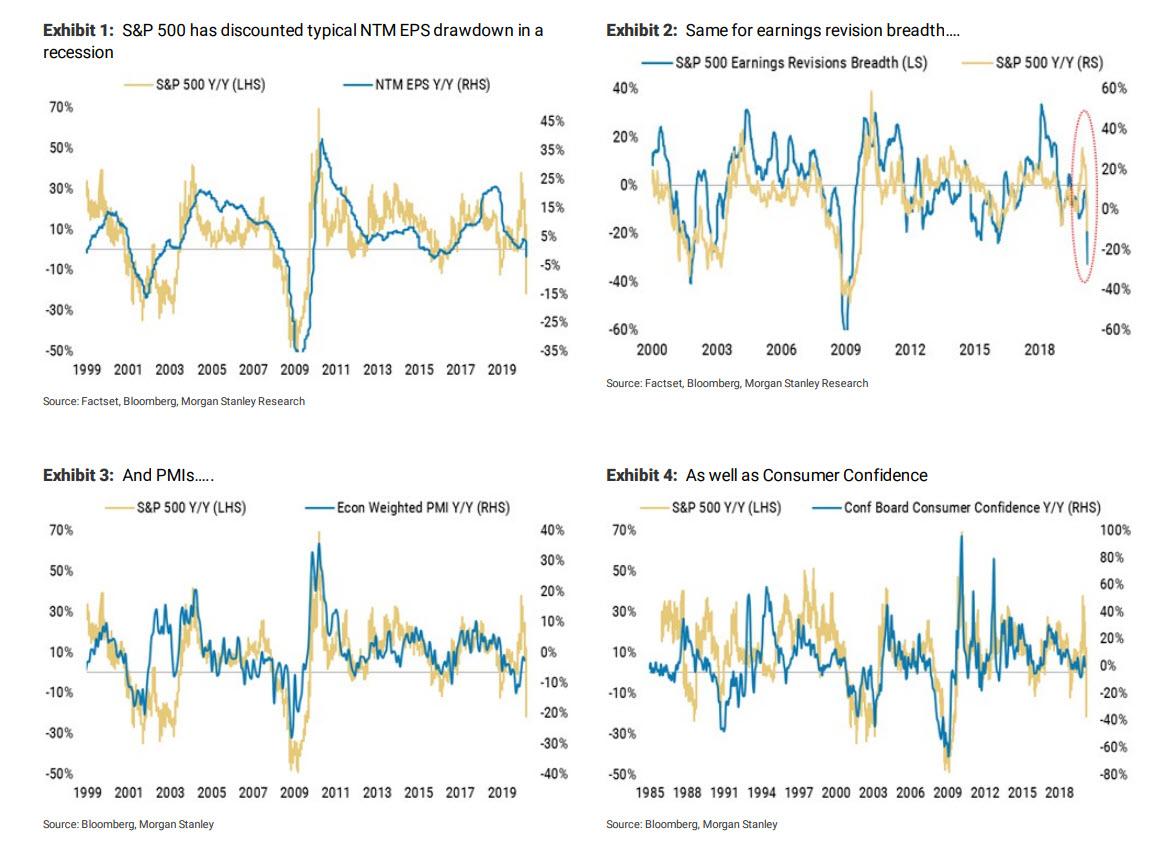

3. Economic and earnings data will be grim over the next month, but equity markets may have already discounted these revisions based on valuation and some simple relationships we track. First, the equity risk premium for the S&P 500 got as high as 700bps last Monday; it’s the second-highest level we have on record (2011 was higher post the downgrade of Treasuries to AA). If we look at this from a sector and stock standpoint, we are at all-time highs. We think this suggests the index can hold the old lows even if some of the most favored sectors and stocks do not. As for some simple relationships, we compare the y/y change in the S&P to the y/y change in earnings growth and revisions breadth, PMIs,and consumer confidence. Based on the 20% y/y decline in the S&P 500, a very rare event usually associated with recessions, we think the market has discounted the recessionary economic and earnings data we expect to see next month (Exhibits 1-4). Having said that, it has not discounted a full-blown financial crisis like we experienced in 2008-09.

4. Finally, from our hundreds of conversations with clients the past few weeks, there is a strong consensus for lower lows on a retest over the next month or two. While that doesn’t mean the consensus can’t be right, we would remind readers that we never got a retest of the December 2018 lows which happened under a similar type forced liquidation. Time-tested technical tools like retests with a positive divergence may not work as well in a world dominated by oversized shadow banks which have become the marginal buyer/seller that really sets the price in the short term

Wilson’s bullish conclusion is also the reason why the most bearish strategist on Wall Street just may be the most bullish one:

… rarely do markets become so dislocated as they have in the past month, but such are the conditions from which great investment opportunities are born. We have been less bullish than most over the past several years under the view we were headed toward the end of the cycle. While we never know what will tip us into a recession, the conditions for one have to be in place and the excesses in the credit world were exhibit A in that regard. Now that we are here, we would like to remind readers that bear markets end with recessions, they don’t begin with them.

And, ironically, this means that MS is now flipped with Goldman, which has turned bearish and is loathe to recommend buying here, anticipating another leg lower after the bear market rally ends, while Wilson and Morgan Stanley are now the most bullish bank (with the possible exception of JPMorgan):

Given that most stocks have been in a bear market for two years or longer, we recommend investors start buying stocks now because we cannot be sure if the next pull back will lead to lowers lows or not given we already experienced forced liquidation. Bottom line, we believe 2400-2600 on the S&P 500 will prove to be very good entry points for those with a time horizon of 6-12 months.

We’ll be sure to check back in 6-12 months. And speaking of “checking back”, last July another Wall Street bull, JPM’s Marko Kolanovic thought he spotted a similar bullish trade in the collapse of value stocks which he thought were a “once in a decade” buying opportunity while low vol/growth stocks were to be shorted. ALmost a year later, we can safely say that anyone who put on this “once in a decade” trade, which has seen the total obliteration of value stocks, has now been fired. We can only hope that Wilson doesn’t follow Kolanovic’s fate.

Dramatic Drone Footage Reveals Ghost Town As Hoboken Residents Shelter

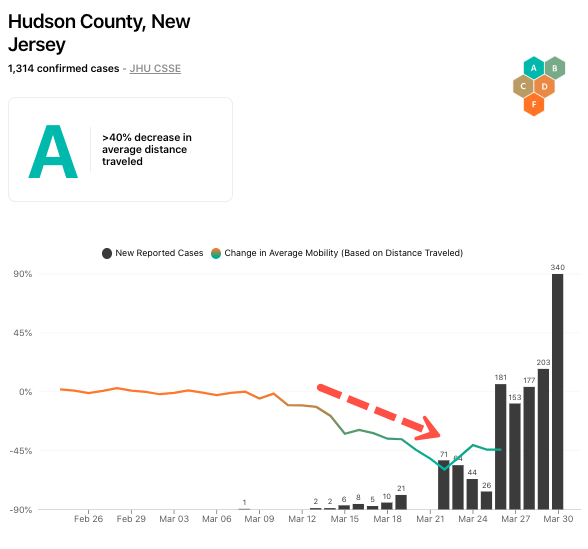

If Hoboken residents shelter-in-place, adhering to strict social distancing rules enforced by New Jersey, then the COVID-19 outbreak might peak around July 31, reported Patch Hoboken, citing a new analysis.

Columbia University researchers said the best-case scenario is that shuttering of non-essential businesses, closing of education systems, and banning mass gatherings, could support containment efforts. Still, current restrictions would need to be extended through the summer.

New Jersey issued the stay-at-home statewide public health order on March 21. Gov. Phil Murphy said, “Our social distancing directives are not polite suggestions.”

“They are there for a reason: to flatten the curve, to cut off the surge” of cases that lead to hospitalization and stress on the state’s health care system,” Murphy continued.

To get a better sense if people in Hudson County, New Jersey, or more specifically, Hoboken, are following social distancing rules, we turn to a new app called “Social Distancing Scoreboard,” which tracks the GPS location of smartphones in a geographical area, to monitor if people are following the public health order. The app gave Hudson County/ Hoboken an “A” for its residents following the new health measures.

With that being said, YouTube account Mingomatic provides new aerial coverage of Hoboken that shows how the area has transformed into a ghost town during the pandemic.

Several days ago, Mingomatic posted a video of Newark Avenue in Jersey City that showed the area was empty.

Life has come to a standstill for millions of people in New Jersey and New York amid a worsening virus crisis.

{kind=link}