Gundlach Says “Classic Bear Market Rally” Reminds Him Of 1999 Tyler Durden

Sat, 07/25/2020 – 16:20

Jeffrey Gundlach, the billionaire chief investment officer of DoubleLine Capital, was quoted by Reuters on Friday as saying the stock market’s parabolic move in the last couple of months reminds him of the days right before the Dot Com bust.

Gundlach, who oversees a $138 billion fund that is primarily invested in fixed income assets, was troubled by the rapid surge in government debt that has propped up the ailing economy.

He said the dollar would be pressured to the downside as deficits rise. Dollar weakness could boost equities in the short term, he said, adding that “ultimately it weakens as the debt situation is really remarkably bad for a developed country.”

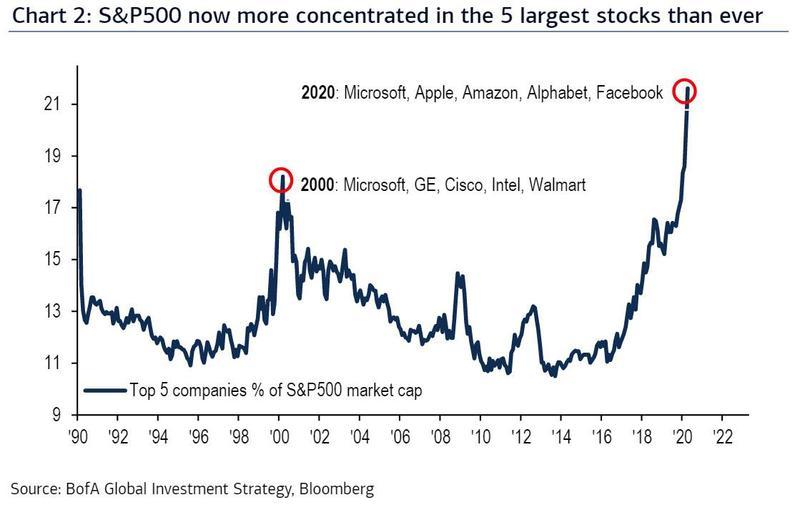

Gundlach voiced concerns about the V-shaped recovery in the S&P500 from its March lows, along with how much of the gains are concentrated in a handful of technology stocks.

He said the concentration in equity market leadership is mainly in FANG stocks (that is Amazon, Apple, Microsoft, and Google) and retail investors panic buying stocks “is classic bear market rally activity,” and a reminder of what he believes could be similar to the days right before the Dot Com implosion.

Gundlach warned today’s situation is “way worse because we don’t have the ability to cut interest rates” and have “used all the tools that are typically reserved for fighting economic problems.”

Gundlach said there could be more opportunities in overseas markets. His latest warning is similar to the DoubleLine Total Return Bond Fund webcast on July 9, where he said stocks are likely to fall from its “lofty” perch.

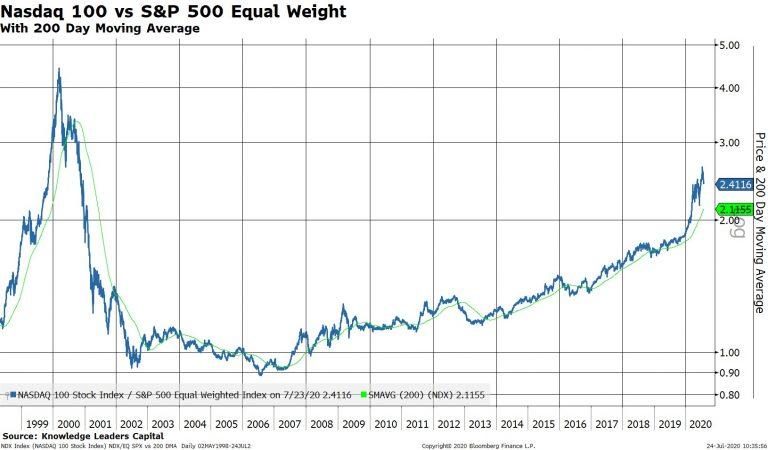

For more color on why Gundlach is convinced today’s move in stocks is a “bear market rally,” the first chart below is the ratio of tech-heavy Nasdaq 100 over S&P500, hitting levels not seen since the Dot Com peak as investors panic buy FANG stocks.

In early July, the ratio breached the Dot Com peak, implying high-flying tech stocks were more overvalued today than right before the bust in late 1999/2000. Shown below, the ratio has since faded below the 2000 peak, due mainly to valuation concerns.

Nasdaq 100 remains disconnected from reality as treasury yields slide due to stalling recovery.

Gold soars to decade high. Gundlach mentioned in his July webcast that he was still bullish on precious metals.

Gold rises as negative-yielding debt market value increases.

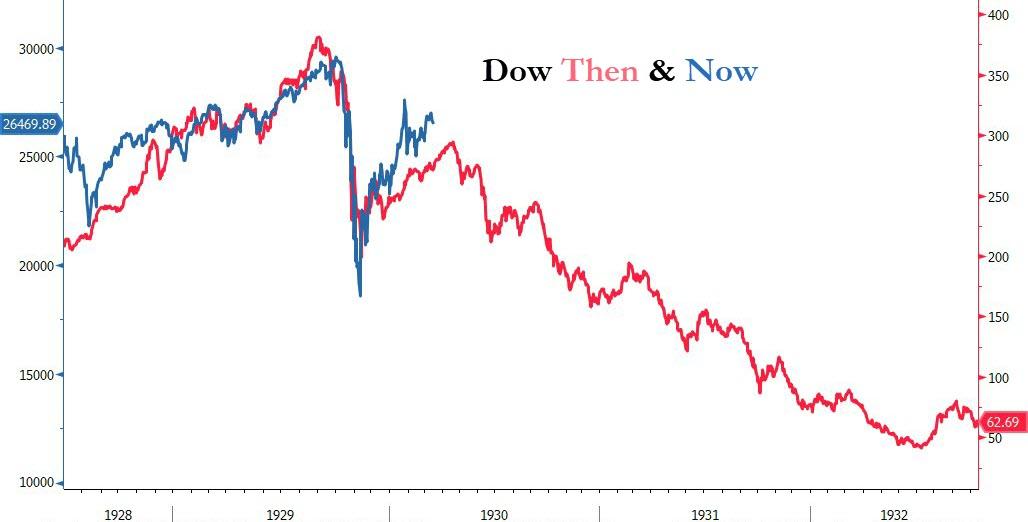

While Gundlach fears 1999, many are more concerned the current bear-market bounce is more akin to the 1930s collapse. Either way, this is far from over…

Gary Shilling believes a 1930s-style decline in the stock market is just ahead…

via ZeroHedge News https://ift.tt/3g1Dbb8 Tyler Durden

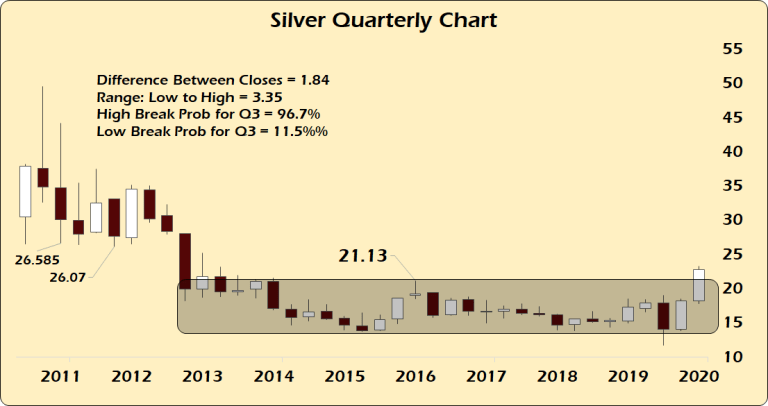

Gold and silver had bang up weeks. Gold closed yesterday afternoon on a cash basis above $1900, at $1901.95 just $18 shy of the all-time high set in September 2011 at $1920.

Silver, which has famously lagged behind gold for two years now, finally broke through the post-Brexit vote high of $21.13 (again cash basis) on Monday and never looked back, exploding above $23 to close this week at $22.77 an ounce.

The weekly prints weren’t even completed yet when I start seeing the calls in my inbox saying they are incredibly overbought. It’s an easy position to take into a breakout because of indicators like 200 day moving averages and Bollinger bands, because these this indicators are all about mean reversion strategies.

And, yes, markets always revert to the mean. But they also stay irrational far longer than you can stay solvent. This is especially true when central banks around the world pump trillions into the markets to keep them from collapsing.

Markets don’t trade on fundamentals or statistical regressions of the past.

Markets are forward-looking.

They trade on momentum and sentiment.

Instead of piling on some, frankly, superficial technical analysis about how silver is now X% above its 200dma and that means it’s overbought, the question one should be asking is, “What in the holy hell is going on here?”

I think there are a number of factors at play that have all lined up to answer that question.

The first is the most important, which I’ll focus on.

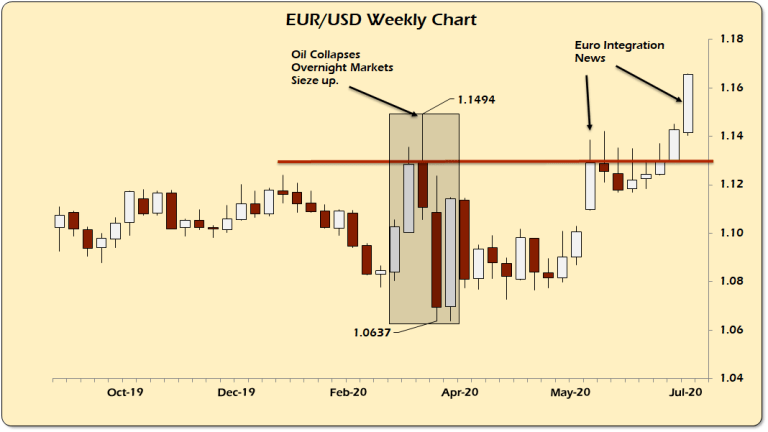

This week’s proximate cause was the breakdown of the U.S. dollar index (USDX) because of the shift in the political and fiscal structure of the European Union.

The USDX had been plumbing recent lows as the markets bought into a reflation trade surrounding the end of the COVID-19 lockdown around the world.

Gradually, all that money that was stuffed into the hands of the banks, the hedge funds and Blackrock as the U.S. treasury’s agent bid asset prices higher, honestly, across the board, with the exception of oil.

U.S. bond yields are at historic lows, stocks historic highs, gold now within $20 of its all-time high. But, what drove the USDX to new lows?

Why was the U.S. dollar the only thing seemingly on sale?

The sharp rise in the euro thanks to a successful European budget and COVID-19 crisis summit, the outcome of which, by the way, was never in doubt.

Because currency traders are now betting the farm — or at least signaling that they want to — that the European Union will now become a proper political and fiscal entity since the European Commission now has both taxing and spending authority directly.

This has been the thing the markets have been punishing the euro for for years. And now the process has begun.

The euro blew through the March high when capital flew out of U.S. assets for a short time to quell European bank solvency fears and then promptly rushed right back out the minute the worst of the crisis ended.

You look at this weekly chart of the euro and tell me markets give a rat’s ass about 200 day moving averages in a crisis (shaded area of extreme volatility)?

It’s clear from the chart that the March low in the euro was significant and a new weekly closing high is far more important than how far away it is from its historical average.

I was unconvinced in this rally in the euro until last week when the euro close strong for the first time above $1.13 (orange line, see chart). It had failed to convince traders going into a weekend they wanted to be long the euro, regardless of where it stood versus the long term.

Why this is important for gold is that gold has been trapped between two opposing forces for nearly a year now.

On the one hand is the safe haven trade that’s been in place since last year’s seizure of the repo markets in September — moving in concert with a strong dollar.

On the other is the reflation trade, relying on the kindness of central banks creating liquidity and positive market sentiment. This would cause the dollar to drop alongside gold as traders ran with the ‘happy days are here again’ trade.

All along gold was slowly grinding higher regardless of the dollar, and that told us there was a sentiment change underway. But, day-to-day, week-to-week, gold was trapped between these two trades, broadly.

But the spasm in March changed that dynamic as the dollar markets seized up and the world went into ‘sell everything not dollars’ mode. Gold always gets hit on those days and, in general, that’s where the most violent downdrafts in gold occur.

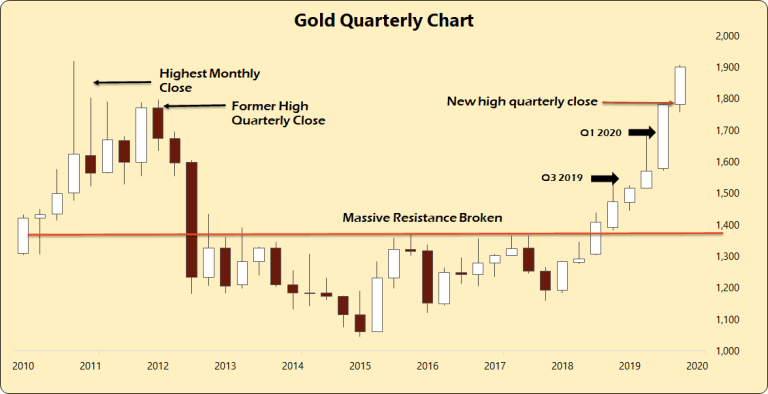

But, as I said, overall gold has been grinding higher as bulls kept supporting the price on pullbacks at higher levels. Because once gold broke above the post-Brexit high of $1375 last summer, it was now officially, technically in a bull market, having broken out of a six-year consolidation pattern on the quarterly chart.

Closing prices matter. And June’s strong close in gold told everyone that something had fundamentally changed. Look at the Q1 bar. Note how it closed above the Q3 2019 bar despite the markets locking up in early March.

That’s a very powerful signal. And it more than set the stage for the run we’ve seen for the past four months. With the huge move in Q2 gold should have sold off into the close on profit taking and book squaring.

It didn’t. In fact the shorts got killed and still are.

And that signals that the dynamic between the USDX and gold has been broken, at least for the time being. Gold is now trading independently of all other currencies, including the dollar.

Moving averages cannot capture pent up market energy like simply reading the candlesticks can. There is more predictive power in understanding the relationship of one bar to another and relating those change through time.

All of the things I just discussed in terms of gold’s quarterly performance were setup in the weekly and monthly charts at key moments in time. This is why I do twice weekly video Market Reports for my Patrons who benefit from seeing these strategic markets evolve on a regular basis.

Time and price are far more important than statistics. All statistics can do is give you pot odds of a move higher or lower. And right now, for the month of July, is gold overbought?

Yes.

So the odds for the rest of July state gold will see it’s all-time high at $1920 and run back into its burrow for a few weeks. It’s been a good run, but that high from September 2011 is historic and it should be respected by both bulls and bears.

But that’s the easy call. What’s far more important now is how gold closes this month. Because that sets up the probability of what it should do in August.

Because if gold were to close July where it closed this week, $1901.15, versus a high of $1906.68 and a low of $1757.71 then there is a 90% chance of gold breaking July’s high and just a 1.2% chance of gold breaking the July low.

And given that in any single month gold, on average, moves $80 and the difference between closing prices is $63, there is a excellent chance that breaking the July high in August will also create a new all-time high.

Those are the odds. There’s no arguing with the numbers. Being long gold here, despite the apparent frothiness is the right play. Until I see a weekly close that alters that picture, throwing some form of reversal signal which violates a previous low, gold is a buy right now.

Of course, at this level I’m looking for that signal to show up this week, the last week of July, to push the price back and alter the odds for August. It’s been the history of both gold and silver to get crushed into the monthly and quarterly closes to keep its momentum muted.

Silver’s position is even more interesting because silver is now two years behind gold in terms of the big picture (quarterly chart breakout) and hasn’t even had a chance to run before people are calling for it to collapse.

This week was the one where silver finally bested the post-Brexit high of $21.25 an ounce. It was set up by to huge weekly closes which pushed through near-term resistance above $18.00. Last week’s close at $19.32 was met with massive follow-through buying which pushed the price through what should have been stronger resistance above $20 which literally didn’t matter.

Look at the shaded area on the chart. That is a seven-year consolidation below $21 per ounce. A July close above that level sets up a move to the $26 area, the area that was support after the 2011 peak (see chart).

And you can see that silver is way beyond its normal trading behavior but coming off the strong June close there were 9.5:1 odds that silver would break the Q2 high in Q3 and use that as energy to challenge first the Q1 high and then the 2016 high. That it did all of these things in three weeks should tell you just how strong bullish sentiment is and how pent up the demand for silver was.

And because silver lagged gold all year, gold could easily flame out alongside stocks well before silver does. In fact, that’s my medium-term call.

Because silver isn’t as much a monetary metal nor is it a safe-haven asset like gold. So it could be telling us something is changing in the strategic metals complex which should scare all the ‘v-shaped’ recovery punters on CNBC.

* * *

Join my Patreon if you want help tying the headlines to the markets while give you clear analysis without the jargon. Install the Brave Browser if you want to slow down Google and Facebook tracking you everywhere you go.

via ZeroHedge News https://ift.tt/2OS52i2 Tyler Durden

Last week, ten Democratic Senators sent letters to Judge Lagoa and Luck of the Eleventh Circuit. The Senators asked the Judges to “explain” their involvement in the Florida felon disenfranchisement cases. (I wrote about the recusal issue here). Explain, or else what? In my post, I wrote that Congress’s only remedy against federal judges is impeachment. But on further thought, members of Congress could choose a far less intrusive remedy: a subpoena to testify. For example, could the House or Senate Judiciary Committee issue a subpoena to Judges Lagoa and Luck to testify why they decided not to recuse in this case.

Two years ago, I considered a related question during the Kavanaugh hearing. At the time, Rep. Jerrold Nadler, chair of the House Judiciary Committee, threatened to investigate Brett Kavanaugh if he was confirmed to the Court. He said, “We would have to investigate any credible allegations certainly of perjury and other things that haven’t properly been looked into before.” Presumably, such an investigation could have included a subpoena to Kavanaugh to testify before Congress. (I tend to start thinking and writing about events long before they happen; that is why I am always so quick to offer commentary when the event actually happens).

At the time, I asked Josh Chafetz, an expert on all things Congress, whether there was any precedent for Congress issuing a subpoena to a Supreme Court Justice. He identified one such instance. Here is an excerpt from pp. 196-197 of Congress’s Constitution.

In 1953, the House Un-American Activities Committee subpoenaed Justice Tom Clark to testify about decisions he had made as attorney general. The committee simultaneously subpoenaed former president Truman, which was immediately and widely recognized as a political blunder. Both Truman and Clark refused to testify (on similar grounds of executive and judicial independence from Congress), although Clark announced that he would answer written questions; in the resulting political firestorm, the committee declined to put questions to him or to proceed against either him or Truman.

This subpoena did not concern actions Clark took while on the bench. It instead focused on actions he took as Attorney General. Here, the subpoena was issued, but not enforced. In this clash between the legislative branch and the judicial branch, the judiciary prevailed.

But what would have happened if HUAC asked a federal court to enforce the subpoena? Would it be enforceable? Chafetz wrote that such a subpoena could be enforced:

Is there any reason to think that it would be categorically inappropriate today to bring judges before congressional committees? As this book has emphasized from the outset, judges are political actors, although they of course inhabit political roles different from, say, those of executive-branch officials. These different roles may make it politically dicey for a house of Congress to subpoena them—but this is not categorically different from any other subpoena.

Chafetz makes a textual point. The Speech or Debate Clause provides express protection for members of Congress from being questioned. But there are no express protections for federal judges, or the President:

Judges have no explicit protection from being questioned in Congress—in contrast to members of Congress, who are, as we shall see in the next chapter, privileged against being questioned “in any other Place” for their official activity—so it is only by inducing an overriding, free-standing constitutional principle of judicial independence that one could argue that they are categorically immune from congressional subpoena. But why should we make such an inductive step for judges, especially given the other, explicit independence-protecting measures?

Chafetz wrote this book several years before Trump v. Mazars. I think the Chief Justices’s opinion casts some doubt on the validity of congressional subpoenas for federal judges, but this issue is not clear cut.

First, Mazars put a lot of weight on the fact that the Court had never addressed “a congressional subpoena for the President’s information.” In contrast, the courts had considered the validity of subpoenas issued to the President in federal criminal proceedings (Burr and Nixon) and in a civil suit (Jones). Chief Justice Roberts found this novelty cut against the House’s subpoena. The Court found, “congressional subpoenas directed at the President differ markedly from congressional subpoenas we have previously reviewed.” Moreover, there has been a tradition of Congress and the Executive Branch voluntarily working out compromises over document requests.

There is no practice of Congress voluntarily requesting information from federal judges about internal judicial duties. I put aside the judiciary’s annual reports about mundane budgetary matters, which is subject to Congress’s oversight authority. During those hearings, the Justices routinely refuse to answer any substantive legal questions. As they should. And there is no practice of such subpoenas being issued to force a judge to testify about her official duties. The novelty of a congressional subpoena against a federal judge would cut against its validity.

Second, Roberts considered the separation of powers analysis: one branch was seeking information from another branch.

Here the President’s information is sought not by prosecutors or private parties in connection with a particular judicial proceeding, but by committees ofCongress that have set forth broad legislative objectives. Congress and the President—the two political branches established by the Constitution—have an ongoing relationship that the Framers intended to feature both rivalry and reciprocity. See The Federalist No. 51, p. 349 (J. Cooke ed.1961) (J. Madison); Youngstown Sheet & Tube Co. v. Sawyer, 343 U. S. 579, 635 (1952) (Jackson, J., concurring).That distinctive aspect necessarily informs our analysis of the question before us.

The Court added that “congressional subpoenas for the President’s information unavoidably pit the political branches against one another.”

I think the same sort of “rivalry and reciprocity” exists between Congress and the federal courts. Federal judges are different from the President. But the unique nature of judicial independence suggests there are similar separation-of-powers concerns at play. Perhaps that reason explains why the notion of congressional standing has been deemed so controversial. In such cases, Congress asks the court to adjudicate disputes with the executive branch. And the courts usually refuse to get involved.

Third, Mazars declined to adopt the Nixon “demonstrated, specific need” standard for the President’s tax returns. The President’s financial records are not like the privileged tapes at issue in the Watergate case. The Court stated, “We decline to transplant that protection root and branch to cases involving nonprivileged, private information, which by definition does not implicate sensitive Executive Branch deliberations.”

It is generally understood that judicial deliberations are confidential. I don’t think the phrase “privilege” is the correct descriptor, but the nature of internal proceedings come close to “privileged.” Judges, and their staff, generally pledge to keep matters internal. When internal judicial deliberations leak, it is often scandalous–especially at the Supreme Court. I think internal judicial deliberations are closer to privileged, executive-branch documents, then they would be to the President’s financial records. Therefore, a subpoena to a federal judge for internal discussions would have to meet some heightened standard–perhaps Nixon‘s “demonstrated, specific need” standard

Fourth, Mazars recognized that Congress has a power to request documents and testimony “in order to legislate.” Subpoenas must serve a “valid legislative purpose.” The Court added that Congress has an “important interests in conducting inquiries to obtain the information it needs to legislate effectively.” What does it mean to “legislative effectively” with respect to federal courts?

I think the category of laws Congress could enact with respect to the courts is far narrower than the category of laws Congress can enact with respect to the executive branch. Congress can enact general ethics legislation. Congress can establish new federal courts and judicial positions. (I’ll table for now whether Congress can eliminate federal courts and judicial positions). Congress can create new grounds for federal jurisdiction. (I’ll table for now the validity of jurisdiction stripping). In certain cases, Congress can establish specific rules of decision. For example, AEDPA only permits certain habeas relief if a lower-court decision violates “clearly established Federal law, as determined by the Supreme Court of the United States.” I think these sorts of legislation are all permissible.

But what about a subpoena to an individual federal judge to explain her decision in a specific case? Would this subpoena be appropriate to pursue any of these legislative ends? Or would such a request pursue a different, impermissible purpose? Specifically, would the subpoena in fact serve as a means to intimidate life-tenured federal judges? Chief Justice Roberts alluded to such impermissible purposes in Mazars. He wrote, “burdens imposed by a congressional subpoena should be carefully scrutinized, for they stem from a rival political branch that has an ongoing relationship with the President and incentives to use subpoenas for institutional advantage.” Congress should not be able to maintain an “institutional advantage” over the independent judiciary through the use of pretextual subpoenas.

Fifth, Congress retains the power to impeach federal judges. And as part of the impeachment process, I think the House would have a far greater interest to subpoena a judge. Consider an example where the House suspects a federal judge took a bribe in exchange for a favorable ruling. The House could request financial documents from the judge, as well as internal documents about that ruling. As a practical matter, the Department of Justice would likely investigate, and prosecute such corruption. But the House retains its own authority to request the documents, even in the absence of a federal prosecution.

What if the House chooses to impeach a judge because the House does not like a particular decision he rendered? (Think of the impeachment of Justice Samuel Chase.) Could the House subpoena the judge’s private records of the case? Maybe request draft opinions? Would these requests be valid? A more difficult question.

In any event, these sorts of requests would be pursuing a specific purpose: impeachment. I do not think an interest in crafting general ethics legislation would support a subpoena for internal judicial deliberations.

Sixth, in some cases, it may not be necessary for Congress to subpoena a judge. For example, if a judge issues a published opinion explaining why she chose not to recuse, then that information should address the House’s concern. Mazars recognized that “Congress may not rely on the President’s information if other sources could reasonably provide Congress the information it needs in light of its particular legislative objective.” I think a published opinion could provide the requested information by other means. Congress may disagree with the reasoning in the opinion, or find it unpersuasive. But the opinion can speak for itself, without the need for compelled testimony.

***

I have serious doubts about whether Congress has the power to subpoena a judge to testify about internal judicial matters. I think Congress could justify that subpoena as part of an impeachment inquiry. But a general need for information to craft legislation would not be suitable.

One final issue. I do not think lower, federal court judges would stand in a different position than Supreme Court Justices. True enough, the Constitution recognized the establishment of the Supreme Court. But the Constitution did not establish the members of the Court; those positions were created by statute. If Congress can issue a subpoena to a lower-court judge, I think a subpoena could also be issued to a member of the Supreme Court. What about the Chief Justice, you may ask? Stay tuned for my new paper with Seth Barrett Tillman.

from Latest – Reason.com https://ift.tt/3jDJTX1

via IFTTT

Last week, ten Democratic Senators sent letters to Judge Lagoa and Luck of the Eleventh Circuit. The Senators asked the Judges to “explain” their involvement in the Florida felon disenfranchisement cases. (I wrote about the recusal issue here). Explain, or else what? In my post, I wrote that Congress’s only remedy against federal judges is impeachment. But on further thought, members of Congress could choose a far less intrusive remedy: a subpoena to testify. For example, could the House or Senate Judiciary Committee issue a subpoena to Judges Lagoa and Luck to testify why they decided not to recuse in this case.

Two years ago, I considered a related question during the Kavanaugh hearing. At the time, Rep. Jerrold Nadler, chair of the House Judiciary Committee, threatened to investigate Brett Kavanaugh if he was confirmed to the Court. He said, “We would have to investigate any credible allegations certainly of perjury and other things that haven’t properly been looked into before.” Presumably, such an investigation could have included a subpoena to Kavanaugh to testify before Congress. (I tend to start thinking and writing about events long before they happen; that is why I am always so quick to offer commentary when the event actually happens).

At the time, I asked Josh Chafetz, an expert on all things Congress, whether there was any precedent for Congress issuing a subpoena to a Supreme Court Justice. He identified one such instance. Here is an excerpt from pp. 196-197 of Congress’s Constitution.

In 1953, the House Un-American Activities Committee subpoenaed Justice Tom Clark to testify about decisions he had made as attorney general. The committee simultaneously subpoenaed former president Truman, which was immediately and widely recognized as a political blunder. Both Truman and Clark refused to testify (on similar grounds of executive and judicial independence from Congress), although Clark announced that he would answer written questions; in the resulting political firestorm, the committee declined to put questions to him or to proceed against either him or Truman.

This subpoena did not concern actions Clark took while on the bench. It instead focused on actions he took as Attorney General. Here, the subpoena was issued, but not enforced. In this clash between the legislative branch and the judicial branch, the judiciary prevailed.

But what would have happened if HUAC asked a federal court to enforce the subpoena? Would it be enforceable? Chafetz wrote that such a subpoena could be enforced:

Is there any reason to think that it would be categorically inappropriate today to bring judges before congressional committees? As this book has emphasized from the outset, judges are political actors, although they of course inhabit political roles different from, say, those of executive-branch officials. These different roles may make it politically dicey for a house of Congress to subpoena them—but this is not categorically different from any other subpoena.

Chafetz makes a textual point. The Speech or Debate Clause provides express protection for members of Congress from being questioned. But there are no express protections for federal judges, or the President:

Judges have no explicit protection from being questioned in Congress—in contrast to members of Congress, who are, as we shall see in the next chapter, privileged against being questioned “in any other Place” for their official activity—so it is only by inducing an overriding, free-standing constitutional principle of judicial independence that one could argue that they are categorically immune from congressional subpoena. But why should we make such an inductive step for judges, especially given the other, explicit independence-protecting measures?

Chafetz wrote this book several years before Trump v. Mazars. I think the Chief Justices’s opinion casts some doubt on the validity of congressional subpoenas for federal judges, but this issue is not clear cut.

First, Mazars put a lot of weight on the fact that the Court had never addressed “a congressional subpoena for the President’s information.” In contrast, the courts had considered the validity of subpoenas issued to the President in federal criminal proceedings (Burr and Nixon) and in a civil suit (Jones). Chief Justice Roberts found this novelty cut against the House’s subpoena. The Court found, “congressional subpoenas directed at the President differ markedly from congressional subpoenas we have previously reviewed.” Moreover, there has been a tradition of Congress and the Executive Branch voluntarily working out compromises over document requests.

There is no practice of Congress voluntarily requesting information from federal judges about internal judicial duties. I put aside the judiciary’s annual reports about mundane budgetary matters, which is subject to Congress’s oversight authority. During those hearings, the Justices routinely refuse to answer any substantive legal questions. As they should. And there is no practice of such subpoenas being issued to force a judge to testify about her official duties. The novelty of a congressional subpoena against a federal judge would cut against its validity.

Second, Roberts considered the separation of powers analysis: one branch was seeking information from another branch.

Here the President’s information is sought not by prosecutors or private parties in connection with a particular judicial proceeding, but by committees ofCongress that have set forth broad legislative objectives. Congress and the President—the two political branches established by the Constitution—have an ongoing relationship that the Framers intended to feature both rivalry and reciprocity. See The Federalist No. 51, p. 349 (J. Cooke ed.1961) (J. Madison); Youngstown Sheet & Tube Co. v. Sawyer, 343 U. S. 579, 635 (1952) (Jackson, J., concurring).That distinctive aspect necessarily informs our analysis of the question before us.

The Court added that “congressional subpoenas for the President’s information unavoidably pit the political branches against one another.”

I think the same sort of “rivalry and reciprocity” exists between Congress and the federal courts. Federal judges are different from the President. But the unique nature of judicial independence suggests there are similar separation-of-powers concerns at play. Perhaps that reason explains why the notion of congressional standing has been deemed so controversial. In such cases, Congress asks the court to adjudicate disputes with the executive branch. And the courts usually refuse to get involved.

Third, Mazars declined to adopt the Nixon “demonstrated, specific need” standard for the President’s tax returns. The President’s financial records are not like the privileged tapes at issue in the Watergate case. The Court stated, “We decline to transplant that protection root and branch to cases involving nonprivileged, private information, which by definition does not implicate sensitive Executive Branch deliberations.”

It is generally understood that judicial deliberations are confidential. I don’t think the phrase “privilege” is the correct descriptor, but the nature of internal proceedings come close to “privileged.” Judges, and their staff, generally pledge to keep matters internal. When internal judicial deliberations leak, it is often scandalous–especially at the Supreme Court. I think internal judicial deliberations are closer to privileged, executive-branch documents, then they would be to the President’s financial records. Therefore, a subpoena to a federal judge for internal discussions would have to meet some heightened standard–perhaps Nixon‘s “demonstrated, specific need” standard

Fourth, Mazars recognized that Congress has a power to request documents and testimony “in order to legislate.” Subpoenas must serve a “valid legislative purpose.” The Court added that Congress has an “important interests in conducting inquiries to obtain the information it needs to legislate effectively.” What does it mean to “legislative effectively” with respect to federal courts?

I think the category of laws Congress could enact with respect to the courts is far narrower than the category of laws Congress can enact with respect to the executive branch. Congress can enact general ethics legislation. Congress can establish new federal courts and judicial positions. (I’ll table for now whether Congress can eliminate federal courts and judicial positions). Congress can create new grounds for federal jurisdiction. (I’ll table for now the validity of jurisdiction stripping). In certain cases, Congress can establish specific rules of decision. For example, AEDPA only permits certain habeas relief if a lower-court decision violates “clearly established Federal law, as determined by the Supreme Court of the United States.” I think these sorts of legislation are all permissible.

But what about a subpoena to an individual federal judge to explain her decision in a specific case? Would this subpoena be appropriate to pursue any of these legislative ends? Or would such a request pursue a different, impermissible purpose? Specifically, would the subpoena in fact serve as a means to intimidate life-tenured federal judges? Chief Justice Roberts alluded to such impermissible purposes in Mazars. He wrote, “burdens imposed by a congressional subpoena should be carefully scrutinized, for they stem from a rival political branch that has an ongoing relationship with the President and incentives to use subpoenas for institutional advantage.” Congress should not be able to maintain an “institutional advantage” over the independent judiciary through the use of pretextual subpoenas.

Fifth, Congress retains the power to impeach federal judges. And as part of the impeachment process, I think the House would have a far greater interest to subpoena a judge. Consider an example where the House suspects a federal judge took a bribe in exchange for a favorable ruling. The House could request financial documents from the judge, as well as internal documents about that ruling. As a practical matter, the Department of Justice would likely investigate, and prosecute such corruption. But the House retains its own authority to request the documents, even in the absence of a federal prosecution.

What if the House chooses to impeach a judge because the House does not like a particular decision he rendered? (Think of the impeachment of Justice Samuel Chase.) Could the House subpoena the judge’s private records of the case? Maybe request draft opinions? Would these requests be valid? A more difficult question.

In any event, these sorts of requests would be pursuing a specific purpose: impeachment. I do not think an interest in crafting general ethics legislation would support a subpoena for internal judicial deliberations.

Sixth, in some cases, it may not be necessary for Congress to subpoena a judge. For example, if a judge issues a published opinion explaining why she chose not to recuse, then that information should address the House’s concern. Mazars recognized that “Congress may not rely on the President’s information if other sources could reasonably provide Congress the information it needs in light of its particular legislative objective.” I think a published opinion could provide the requested information by other means. Congress may disagree with the reasoning in the opinion, or find it unpersuasive. But the opinion can speak for itself, without the need for compelled testimony.

***

I have serious doubts about whether Congress has the power to subpoena a judge to testify about internal judicial matters. I think Congress could justify that subpoena as part of an impeachment inquiry. But a general need for information to craft legislation would not be suitable.

One final issue. I do not think lower, federal court judges would stand in a different position than Supreme Court Justices. True enough, the Constitution recognized the establishment of the Supreme Court. But the Constitution did not establish the members of the Court; those positions were created by statute. If Congress can issue a subpoena to a lower-court judge, I think a subpoena could also be issued to a member of the Supreme Court. What about the Chief Justice, you may ask? Stay tuned for my new paper with Seth Barrett Tillman.

from Latest – Reason.com https://ift.tt/3jDJTX1

via IFTTT

Obama’s Top Economist Warns Of Catastrophic Risk To Economy If Stimulus Lapses Tyler Durden

Sat, 07/25/2020 – 15:20

Ex US Treasury Secretary and Obama’s National Economic Council director Larry Summers says he’s never seen a more uncertain recovery – particularly if Congress doesn’t act “strongly and quickly” to keep stimulus flowing during the pandemic.

Amazingly, this puts Summers on the same side of the fence as GOP lawmakers, who are currently pushing to extend enhanced unemployment benefits which lapsed on Friday – albeit to a lesser extent than the $600 per week granted under the CARES Act.

Summers also doesn’t envision the country emerging quickly from the current predicament, and has stressed that it’s not just about how big the next stimulus is – but how long the emergency measures last, according to Bloomberg.

“I personally doubt what I think is the market’s view, which is that we’re going to have most people vaccinated and life returning to normal, sometime by spring of next year,” Summers told “Bloomberg Wall Street Week” in an interview.

A growing body of evidence indicates America’s rebound is stalling, days before hundreds of billions of dollars’ worth of federal aid is set to expire. It could be weeks before the next round of stimulus is completed given wrangling between the White House and Congress; talks are expected to continue this weekend.

Millions of Americans have been kept afloat financially by supplemental unemployment checks that cut off this month, barring Congressional action. –Bloomberg

“Everybody makes a mistake — they focus on the size of the package, and they don’t focus on the duration of the package, so they don’t focus on the rate of flow of stimulus,” said Summers, adding “We need to maintain a very substantial fiscal impulse in the economy for quite some number of months.”

Summers also suggested that it would be far easier to ensure that health-care workers have masks than vaccinating the whole population – when (and if) a COVID-19 vaccine is developed.

Bloomberg also notes that Summers’ comments echo thoes of former NY Fed President William Dudley, who on Thursday said that the US economy would be weaker if they don’t and now to continue expiring unemployment insurance assistance.

“We’re basically right at the edge of a huge fiscal cliff with the expiration of the $600 a week unemployment compensation benefits,” Dudley told Bloomberg Television.

Perhaps Elon has a better solution?

As a reminder, I’m in *favor* of universal basic income

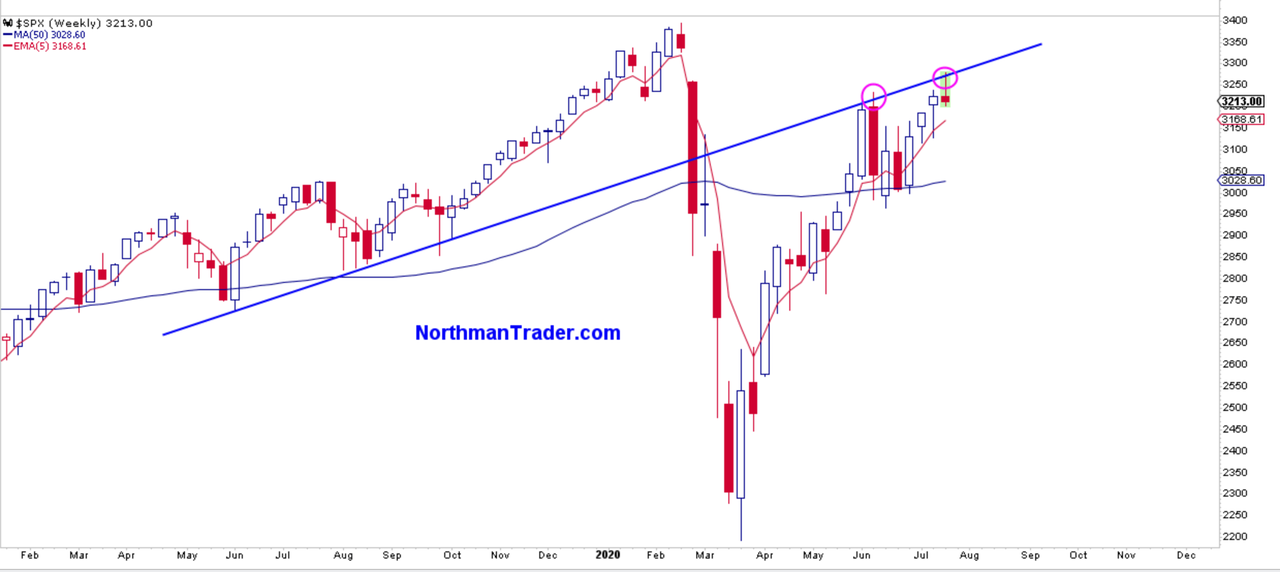

Last week we discussed the importance of the $NDX chart and after another rally to the previous highs $NDX reversed hard for a potential double top and broke its trend off of the March 23 lows. A technical move with potential significant implications upcoming earnings reports from $AAPL and $AMZN offering further rally potential notwithstanding.

But several observations are notable:

A week that was dominated by positive headlines at the beginning of the week, namely an EU stimulus package and a barrage of hopeful Covid vaccine headlines the initiative positive price action induced by these headlines ended up being sold leaving later buyers potential trapped:

Increasingly reality is challenging the narratives of hope, optimism and even momentum. Jobless claims keep coming in higher than expected, permanent layoffs are mounting as are permanent business closures. “The unemployment situation is really, really bad” as the prospect of persistent higher unemployment puts a dampener on the V shaped recovery narrative.

This as virus deaths in the US have been rising by over a thousand a day again for several days in a row and PPP benefits are about expire putting a heavy focus on whatever stimulus package Congress can agree to in the next week or two. Time is running out,, the clock is ticking and the US election is coming ever closer.

And there are threats mounting against big cap tech as the monopoly power of some of these companies is coming under ever closer regulatory scrutiny. Case in point was a WSJ article highlighting how Amazon met with startups under the guise of investing in these companies only to copy their ideas and then launch competing products.

Hence it is notable that the $SPX’s foray into new highs above the June highs was not only reversed but again stopped precisely at the very same trend line that was resistance in June:

This as earnings reports of big tech heavy weights such as $MSFT and $TSLA failed to inspire new buying but rather saw selling which spilled into the entire tech sector culminating in its breaking the up trend off of the March lows:

A rally driven by optimism, hope and liquidity suddenly finds itself reversing even with more hope, optimism and liquidity right at the point of another foray toward record valuations inside a recession:

Yesterday markets closed at 155.3% market cap vs GDP with negative earnings growth no less

The largest financial bubble ever. pic.twitter.com/6ETTPMzVAk

For a more in depth discussion of the issues please join us in this week’s edition of Straight Talk including what to watch for going forward:

* * *

Note: I’ll also be posting a separate Market Video focusing on the latest technical implications this weekend (For those not already signed up for these videos please see link to sign up).

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/3hAsnRv Tyler Durden

Watch: China Answers Houston Closure With Raid On US Consulate In Chengdu Tyler Durden

Sat, 07/25/2020 – 14:20

China has slammed what it says is a violation of international law after on Friday a group of US federal agents were seen forcing open doors at the Chinese consulate in Houston using power tools and crowbars on Friday as consular staff inside prepared to leave after its ordered closure.

The Trump administration had given China until 4pm Friday to vacate the Houston consulate. Mike Pompeo had charged that the consulate was “a hub of spying and intellectual property theft”.

China has shuttered the US consulate in Chengdu in response on Saturday:

Security was tight outside the U.S. consulate in the Chinese city of Chengdu as staff prepared to leave, while U.S. officials took over the closed Chinese consulate in Houston https://t.co/cnrA8r3FQJpic.twitter.com/3T5QyAELBB

US federal agents and local law enforcement entered the Chinese consulate compound in Houston earlier Friday in a series of black SUVs, trucks, two white vans and a locksmith’s van as a crowd of observers and news cameras observed from the edge of the diplomatic compound.

Initial access was reportedly gained when US officials forced open the back door of the facility using power tools.

BREAKING: US Dept. of State officials smash doors at Chinese Consulate in Houston, enter building pic.twitter.com/5LT6TiMLgt

— Breaking News Global (@BreakingNAlerts) July 24, 2020

Meanwhile, the promised “response” from Beijing has come as on Saturday the US consulate in Chengdu, capital of southwestern China’s Sichuan province, was ordered close by Chinese authorities in a tit-for-tat reaction.

Dozens of Chinese agents and police surrounded the American compound on Saturday as moving vans pulled up to its doors.

In Chengdu, a U.S. consulate emblem inside the compound was taken down and staff could be seen moving about. Three removal vans later entered the compound.

Police gathered outside and closed off the street to traffic in the southwestern Chinese city.

…A steady stream of people walked along the street opposite the entrance throughout the day, many stopping to take photos or videos before police moved them on.

Plain clothes officers detained a man who tried to hold up a sign. It was not clear what the sign said.

Neither side has yet to give official comment on the US consulate closure in Chengdu, but we wonder which path things will take at this point now that the score is somewhat “even” on the mutual diplomatic compound closures: either more will follow or there could be talks and tensions could momentarily cool.

Massive Chinese security presence outside of the US consular building in Chengdu on Saturday, via Reuters.

But at the rate things are going, and perhaps given the White House needs a “distraction” away from the ongoing coronavirus crisis ahead of the November election, it’s likely US-China downward spiraling reactionary actions will continue.

via ZeroHedge News https://ift.tt/3f03kpp Tyler Durden

When the Marxist mob used George Floyd’s death as an excuse to ramp up its ongoing war on policing, A&E instantly caved. That proved to be a costly decision. News broke Friday that the cable network has lost almost 50% of its viewers.

When it was founded back in 1984, the Arts & Entertainment Network was going to be a highbrow cable show, focusing on fine arts, documentaries, and dramas, many imported from Britain. A generation of women remembers being introduced to Colin Firth as Mr. Darcy in A&E’s Pride and Prejudice. This high brow fare, though, wasn’t bringing in revenue. By 2002, the station had shifted to reality series for younger viewers.

In 2016, A&E created Live PD. The show follows police departments across America and audiences loved it. According to Wikipedia,

In 2018, a survey by Inscape found Live PD to be the most-watched program among non-live (DVR and VOD) and over-the-top viewers in 2018. The series was credited with having reversed a decline in viewership experienced by A&E since the end of Duck Dynasty; Live PD was among the most-watched programs on cable television. [Footnotes and hyperlinks omitted.]

Live PD was a valuable franchise, one that gave Americans a chance to see police doing their day-to-day work. Viewers got a chance to learn that policing is not a cross between Beverly Hills Cop, the Simpson’s Chauncey Wiggums, and Hill Street Blues.

In May 2020, A&E ordered 160 new episodes of this cash cow. However, on June 6, A&E put the series on hold because of the anti-police riots. On June 9, the show’s host, Dan Abrams, was still tweeting out, “To all of you asking whether #LivePD coming back. . .The answer is yes. All of us associated with the show are as committed to it as ever.”

It took only one day for the show’s producers, working with co-owners, Disney Media Networks and Hearst Communications, to make a liar out of Abrams (and, incidentally, in a time of virus shutdowns and economic loss, to wipe out the jobs of all the people who worked on the show).

This is a critical time in our nation’s history and we have made the decision to cease production on Live PD. Going forward, we will determine if there is a clear pathway to tell the stories of both the community and the police officers whose role it is to serve them. And with that, we will be meeting with community and civil rights leaders as well as police departments.

It later turned out that those working closely with the show didn’t want to cancel it. However, cancel culture ruled the day. The Paramount Network had already canceled its long-running Cops show, which had an audience only a quarter the size of Live PD’s. A&E executives decided that, rather than standing on principle, it too had to bow down to the mob. Even worse for A&E, it also canceled all of Live PD’s successful spinoffs.

As more people and companies are learning, when you bow to the mob, you pay the price. In this case, it turned out that the Marxist mob wasn’t part of the A&E audience. As for the people who actually watched the show, when A&E canceled Live PD and its spinoff progeny, they had no reason to turn to that station. Their decision to abandon A&E cut A&E’s viewership in half:

Ratings for A&E Network have plummeted since it canceled the hit police reality show “Live PD” on June 10, a sign of how much the network relies on law-enforcement programming.

Average prime-time viewership for A&E between June 11 and July 19 was 498,000 people, down 49% from the same period last year, according to data from Nielsen. In the key demographics of adults 18-49 and 25-54, the declines are 55% and 53%, respectively.

The hemorrhage wasn’t limited to the cop shows that people like to watch:

A&E’s ratings declines go beyond prime time. Total daily average viewership in the weeks since the show was pulled is down 36% from a year earlier, to 319,000 people. In the 18-49 and 25-54 age groups, the declines are even larger: 42% and 46%, respectively.

When the audience vanishes, so does the money. A&E just kissed goodbye to around $292.6 million in advertising revenue, which is what the show brought in 2019. A&E was on track to an even better year in 2020. In the first quarter of 2020, it had earned $95.8 million in advertising money just for Live PD and its spinoffs.

Ever since the uber-leftists started pushing their agenda, corporations that caved have lost money. Like lemmings, though, in a frantic charge to insolvency other corporations have leaped off the same cliff despite the warning signs at the cliff’s edge saying, “Get woke, go broke.” One of these days, shareholders are going to start suing companies for these decisions.

via ZeroHedge News https://ift.tt/2OU7xAa Tyler Durden

The Recovery Has Reversed: What Goldman’s Real-Time Indicators Reveal About The State Of The US Economy Tyler Durden

Sat, 07/25/2020 – 13:20

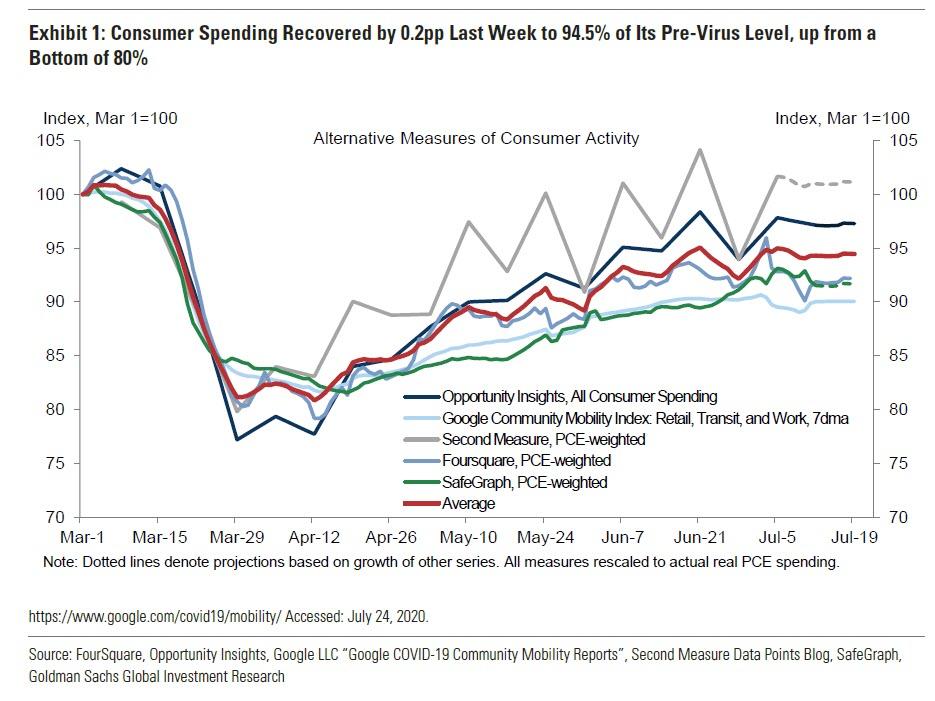

In its latest weekly activity update, Goldman – which on Friday saw tentative signs on hope in the spread of the covid pandemic finding “downward pressure on case growth” – looked at real-time economy indicator focusing on consumer and export activity, the labor market and inflation, and found that while the overall state of the economy is far stronger than where it was in March, the upward momentum has reversed and worse, signs of permanent scarring are beginning to emerge.

Here are the details:

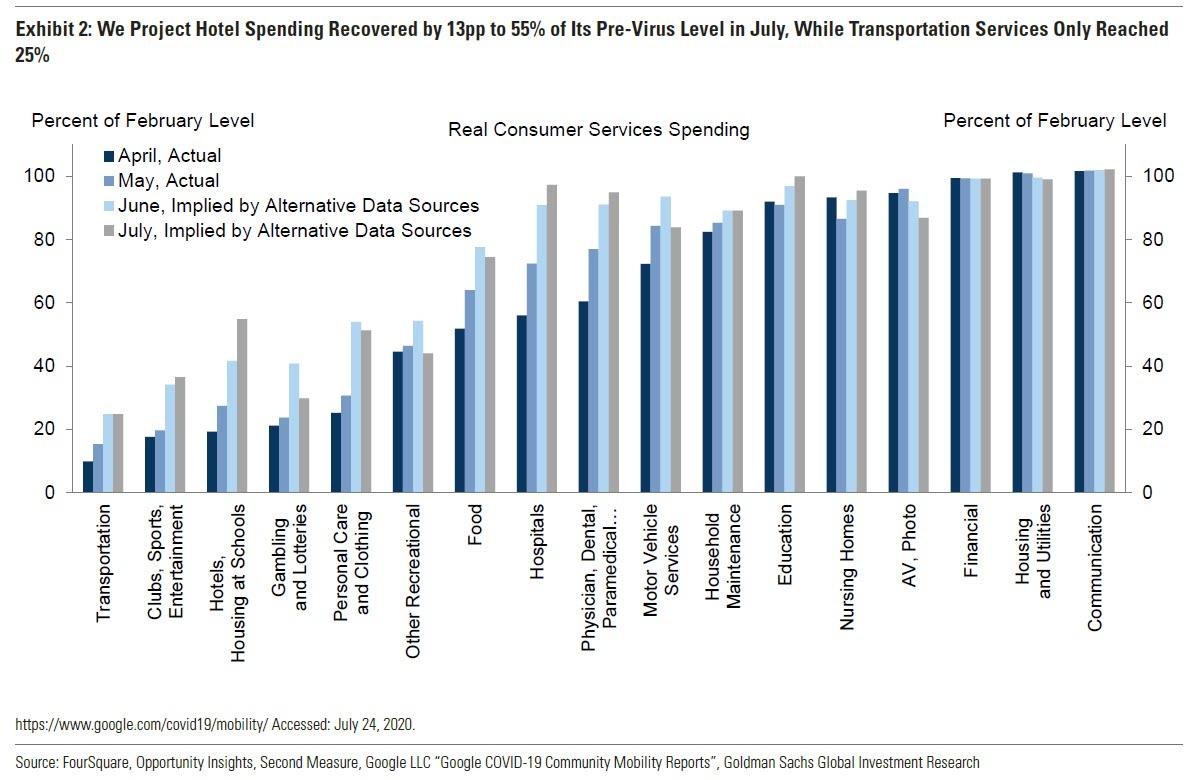

Consumer activity: Consumer spending measures rose by 0.2pp to 94.5% of the pre-virus level over the last week, up from an April bottom of 80%.

Of the highly-impacted consumer services industries, the hotel industry recovered the most in July, with foot traffic increasing by 13pp to 55% of the pre-virus level…

… while the transportation industry remains the most depressed, now only back to 25% of the pre-virus level.

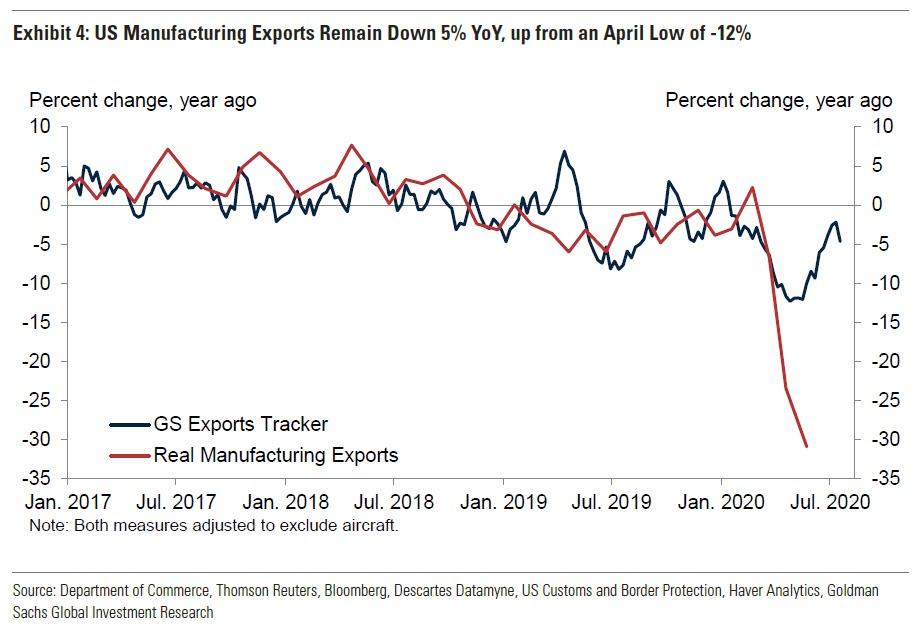

Export activity: Goldman’s export tracker indicates that manufacturing exports (ex-aircraft) partially rebounded over the early summer after declining sharply in the spring. Hinting at a possible reversal in activity, over the last four weeks, the tracker declined 5% year-over-year to 90% of the pre-virus level.

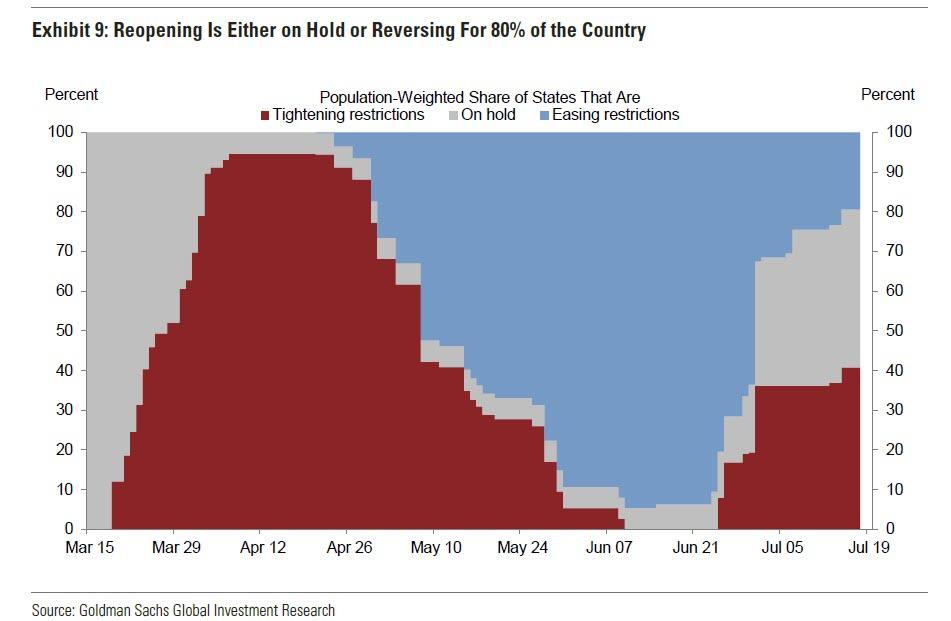

Labor market: High frequency data suggest that the labor market recovery is stalling due to the worsening virus situation. Workplace activity measures have declined in the states hit hardest with virus spread and moved sideways in others since late June.

Goldman’s trackers suggest that current household employment is roughly unchanged from the June survey, and that as of July 7 the unemployment rate had risen back up to 10.8% after falling to 10.5% in late June (vs. 11.1% in the June survey).

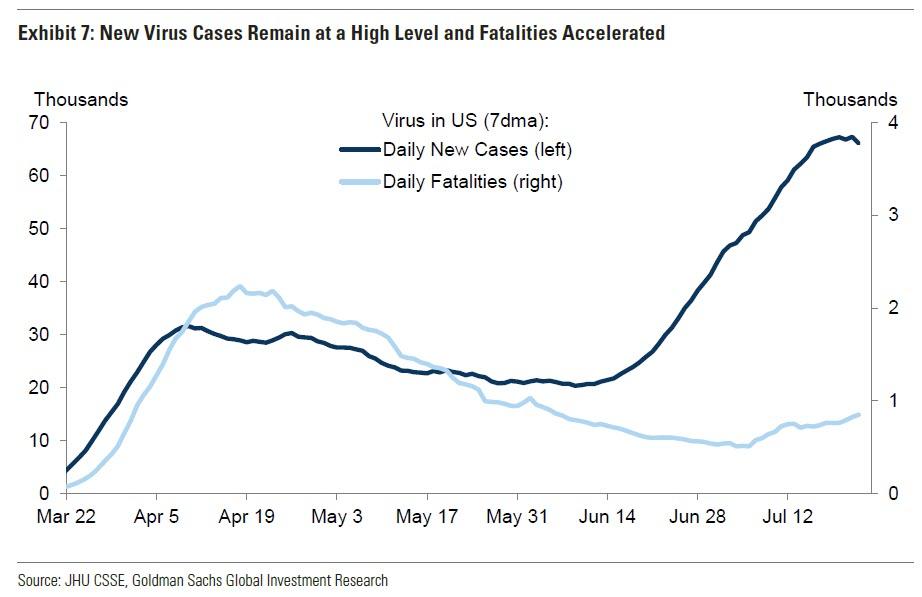

Virus spread: As we noted on Friday, when Goldman published a report discussing that the number of new covid cases is starting to flatten, the average number of the four gating criteria the federal government recommends for proceeding with reopening that states are meeting has risen over the past few days….

… as prevalence of COVID-like illness symptoms has declined in several states, potentially suggesting downward pressure on case growth.

But with the level of new cases already very high in several states and on average nationally, state government officials may remain reluctant to push forward with reopening. Please see our State-Level Coronavirus Tracker for greater detail.

Scarring effects: Signs of long-term damage to the economy are mixed. As of June, 83% of job losses since February are deemed temporary, though only 33% of new layoffs in California in July were temporary.

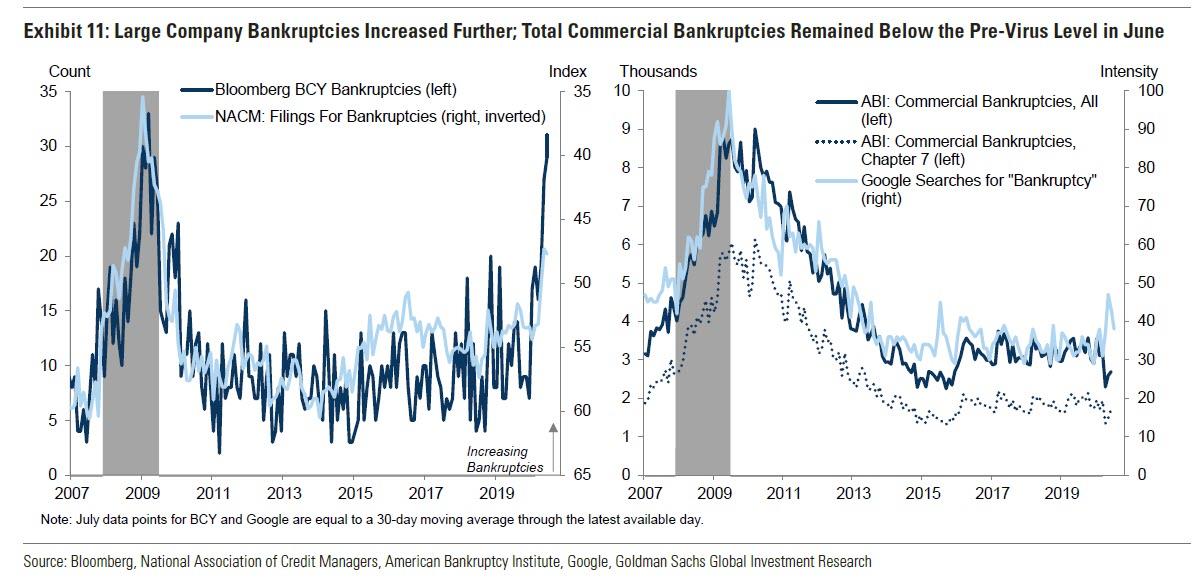

Large-company bankruptcies remain elevated so far in July.

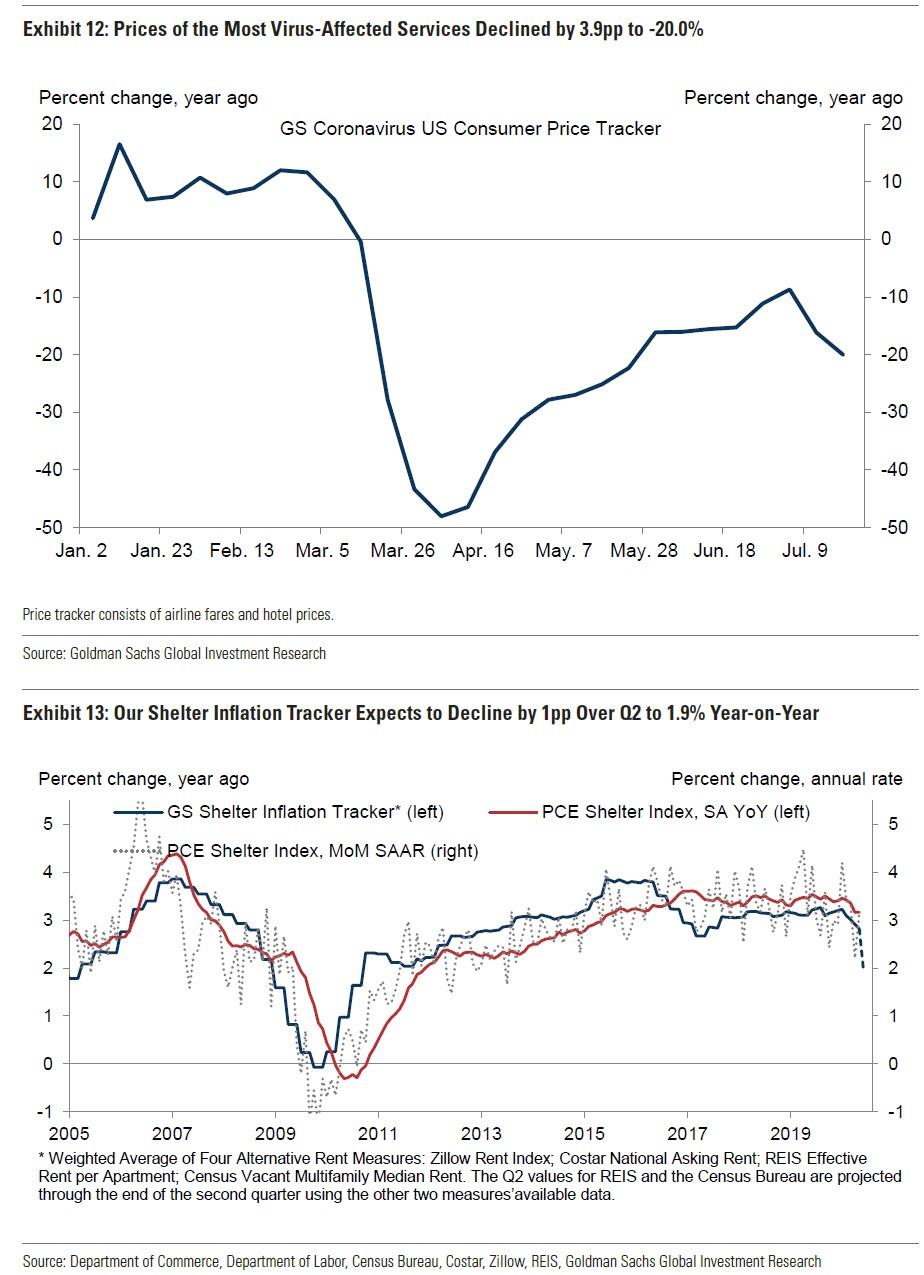

Inflation: Prices of virus-affected services such as hotels and airfares retrenched over the last two weeks and are now down 20% from pre-virus levels but remain well above the bottom of -48% from the beginning of April.

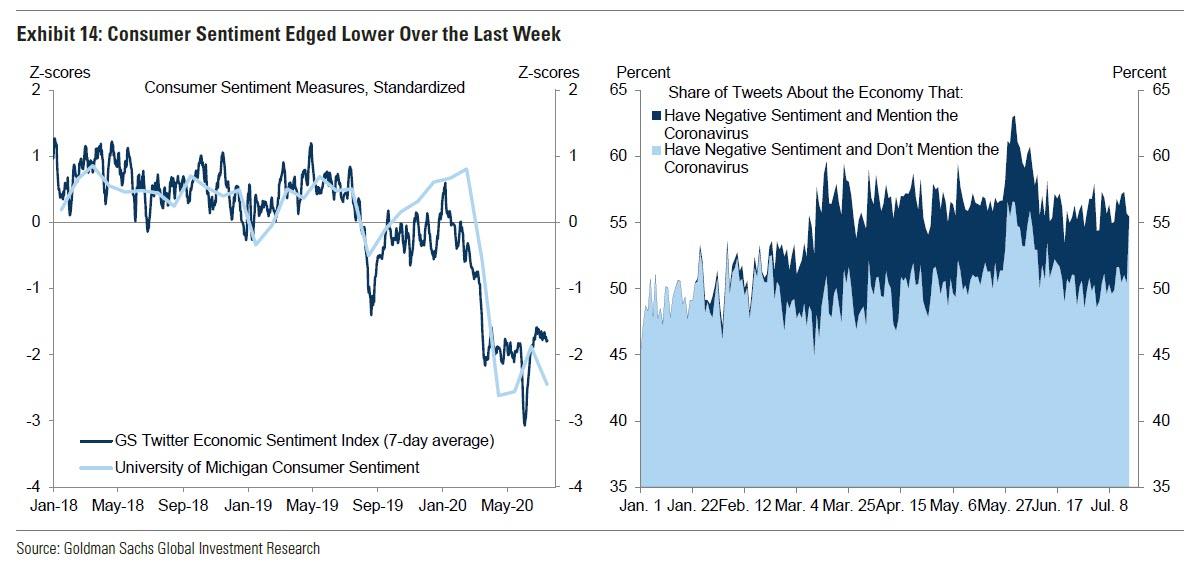

Finally, and perhaps most importantly, perhaps confirming the recent negative reversal in upward trends, consumer sentiment edged lower over the last week, with negative sentiment tweets stubbornly high.

via ZeroHedge News https://ift.tt/2WWADn5 Tyler Durden

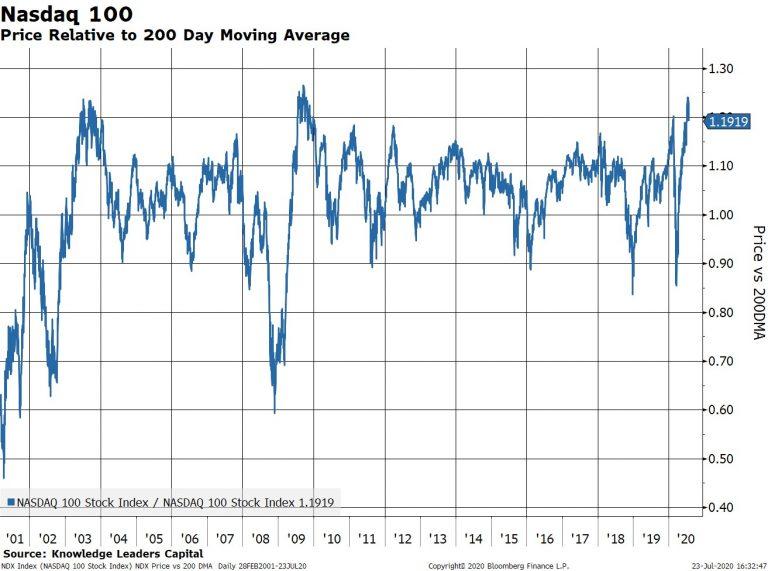

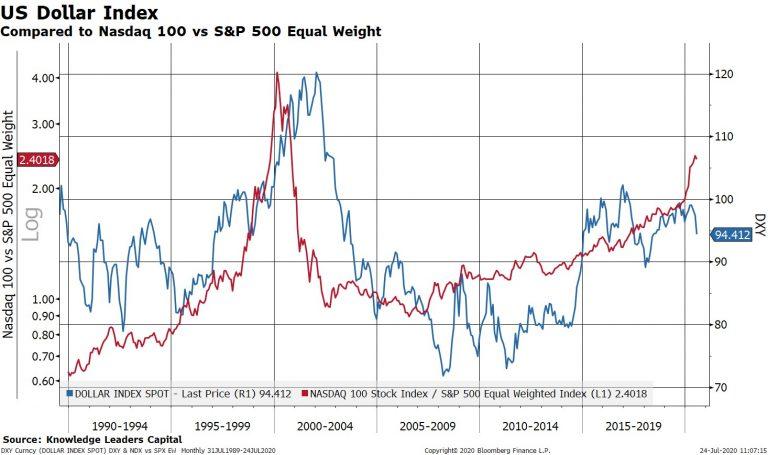

Here we are in the dog days of summer, and the hot weather is not the only thing making us a little queasy. The darling stock market group since 2011, the Nasdaq 100 stock index, has soared a cool 20% this year and well into all-time high territory. Indeed, the height is making us queasy from vertigo.

It wouldn’t be such a big deal if it weren’t for the nearly 30% outperformance of the Nasdaq 100 compared to the average US large cap stock so far this year. That’s right, while precious few (mostly) tech-related stocks are up about 20%, the equal weighted S&P 500 is down 8%.

Outperformance of tech vs the broad market is nothing new. It’s been happening since 2002. What is out of the ordinary currently is the magnitude of recent outperformance that pushed the relative ratio between the Nasdaq 100 and the equal weight S&P 500 to fully 27% above it’s 200-day moving average. This is…troubling…since the last time it happened was back in 1999.

But it doesn’t end there. The Nasdaq 100 is even extended relative to its own trend. Currently, the index 20% above its own 200-day moving average. This is a scenario that has happened only twice in the last 20 years: once in 2009 and once in 2003. Granted, both of those were notable periods in that the economy was emerging from recessions, just like today. But, in both cases the Nasdaq 100 ended up dropping back below that 200-day average over the months that followed. In other words, it would fit nicely with history for the Nasdaq 100 to take a breather here, and possibly give back some of those tremendous year-to-date gains.

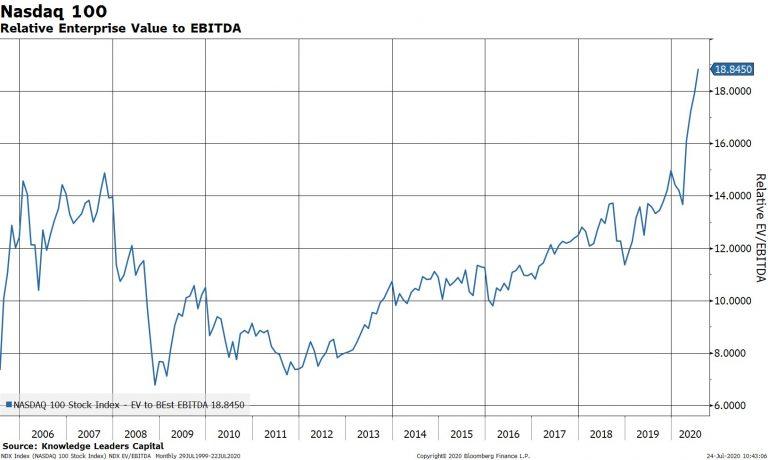

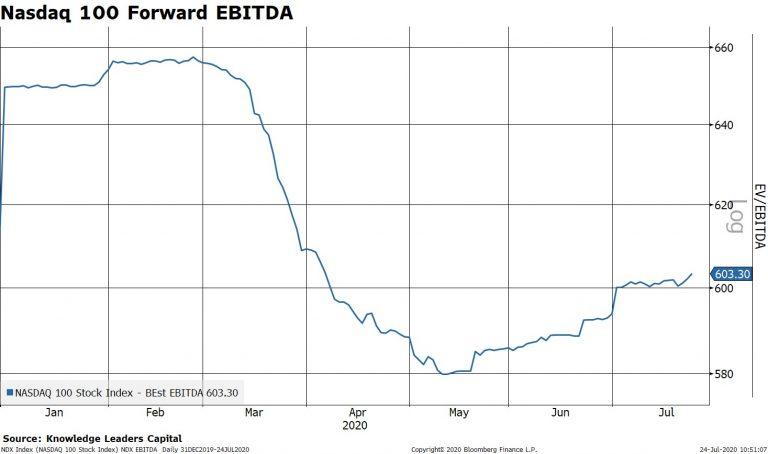

Another thing we find troubling is that much of the recent move in these high-flyers is due to multiple expansion rather than earnings or cash flow growth. That is, investors have been paying up for the potential of future growth as opposed to what cash flows are anticipated to be over the next 12 months.

We can see this clearly in the next chart showing enterprise value to EBITDA for the Nasdaq 100. It has expanded by 25% this year. That’s right, EV to EBITDA has expanded by 25% while these stocks are “only” up 20%. This implies that forward EBITDA expectations have actually contracted by 5%, which they have.

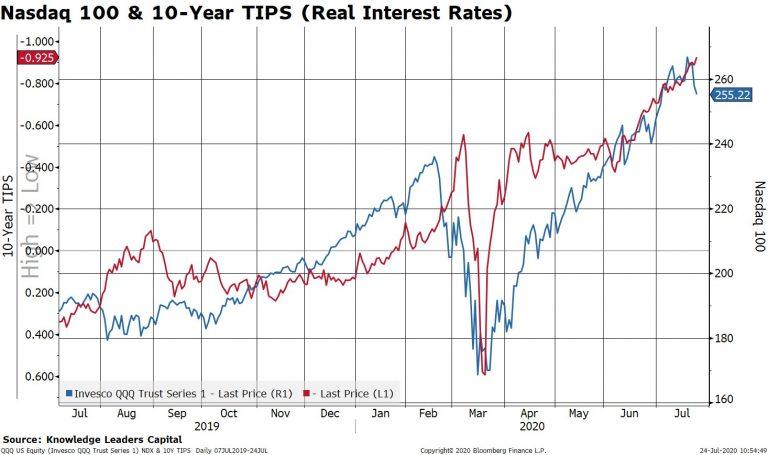

So, this obviously begs the question as to why would someone place a higher multiple on an earnings stream which is seemingly declining, highly uncertain, and likely much more volatile than in the pre-COVID world? Look no further than negative real interest rates. When real rates are negative and falling, there is zero opportunity cost to speculating on the growthiest area of the market, even if that growth is only realized in out years.

There is one thing though that could throw a wrench into this relationship, and that is the US dollar. If a new downtrend emerges – which in all fairness has not yet happened, but the probabilities seem to be rising – it would be anathema for the relative performance of the Nasdaq 100 vs the average stock.

The mechanism at work in this falling US dollar scenario is rising inflation expectations, in part due to imported inflation. As you can see below, as inflation expectations fall (blue line rising), the Nasdaq 100 outperforms (red line rising). This opposite is also true. The reason is that in a disinflation, tech is pretty much the only area that experiences a rising top line because it’s the growthiest sector in the economy. When even moderate inflation emerges, other companies are more easily able to grow top line sales. It’s the convergence of the relative sales growth that helps the average stock outperform tech in a moderate inflation scenario.

So, we find ourselves at an interesting juncture here. The tech theme is overbought and extended and the entire outperformance has been predicated on rising multiples. This raises the likelihood of a moderate setback in this area in the months ahead. Fair enough. What would be more concerning, and not just cause some queasiness but actual nausea, would be if the US dollar truly and fully establishes a downtrend.

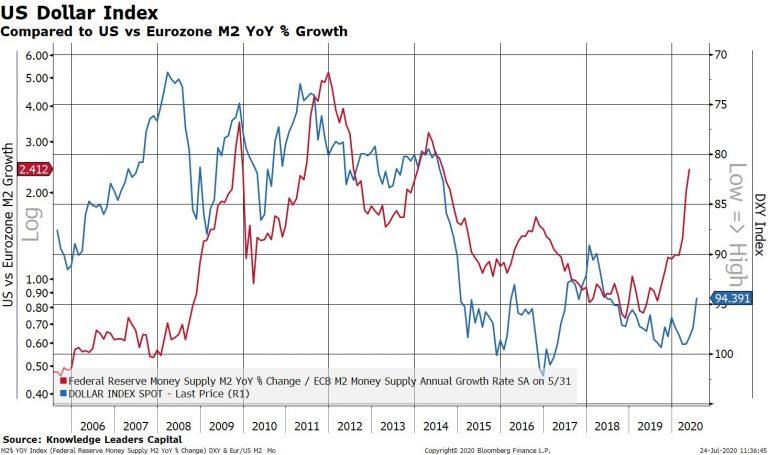

A continued relative expansion in the US dollar money supply vs the Eurozone money supply would certainly help get that US dollar downtrend established and help cause some moderate inflation at the same time.

As Father Friedman is famous for saying, “inflation is always and everywhere a monetary phenomenon”. That thesis will be tested in the coming quarters and years.

via ZeroHedge News https://ift.tt/2OWsASM Tyler Durden

{kind=link}