Republican Rancher Killed By COVID-19 Wins Seat In North Dakota Legislature Tyler Durden

Wed, 11/04/2020 – 08:00

In a race that – one could argue – has come to symbolize the American electorate’s feelings toward COVID-19 and the virus’s impact on their votes, a “Trump Republican” running for a seat in North Dakota’s state legislature has handily defeated his Democratic opponent – despite having succumbed to COVID-19 weeks ago.

David Andahl

The candidate, David Andahl, a Bismack rancher who died on Oct. 5 after winning a tough primary against an incumbent committee chairman, won the seat after winning the endorsement of Sen. Kevin Cramer, a fellow Republican who said “we need more Trump Republicans in the State Legislature,” according to Politico.

North Dakota has seen a surge in new cases over the last month, though its mortality rate has only just begun to creep higher. Andahl won a seat in ND’s eighth district, along with another Republican, who won the district’s other seat.

The rancher was hospitalized for four days in October before ultimately succumbing to the virus.

“He had a lot of feelings for his county and his country and wanting to make things better, and his heart was in farming. He wanted things better for farmers and the coal industry,” Andahl’s mother.

“So many things he was very passionate about, and was hoping that he could get into the Legislature and be of some help. He was looking forward to it. He was looking forward to being part of that.”

ND State Attorney General Wayne Stenehjem has determined that Andahl’s votes should be counted and that, should he win, his seat must be held vacant. The vacancy could then be filled either by a legislative member’s party or by voters in a special election.

via ZeroHedge News https://ift.tt/3er09Z6 Tyler Durden

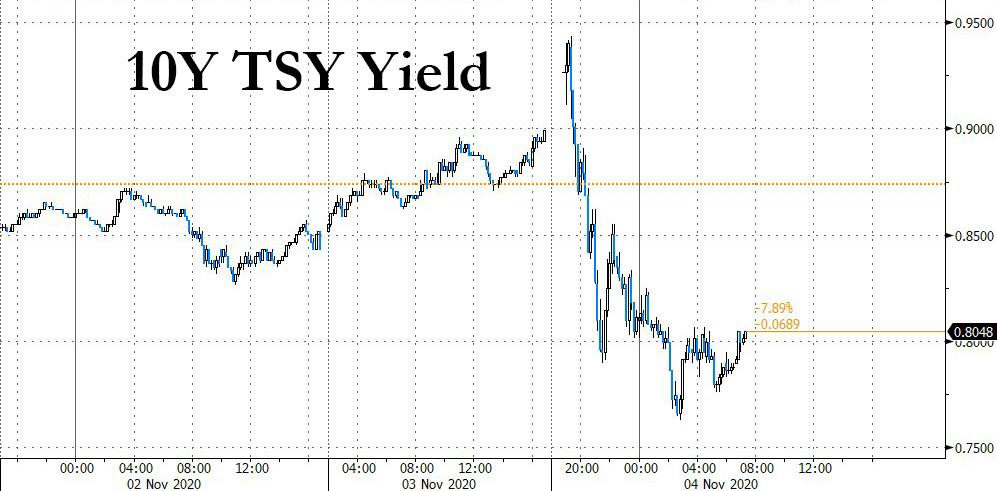

US equity futures fluctuated wildly as investors scrambled to price in shifting odds for Donald Trump’s re-election and control of the Senate after the president declared victory in an early morning announcement, warning he would call on the Supreme Court to stop counting ballots in states where he led, setting up a potentially protracted vote count and the implications for economic stimulus. Emini contracts on the benchmark equity gauge swung from a gain of 2.1% to a loss of 1.3%, and were trading up around +1% as of 7am, and just around 3,400.

While uncertainty over the outcome of the presidential race remains, there was virtually no doubt about the shape of the Senate where Republicans appear set to retain their majority, crushing hopes for a Blue Wave and a massive reflation trade as it will now be harder for lawmakers to approve a big new stimulus deal, which has boosted both Nasdaq futures, which was up 2.5% last…

… and 10Y Treasurys where yields tumbled from 0.94% to 0.80%,the biggest drop since June as the risk of an inflationary spike from a Blue Wave faded away.

In a night filled with Drama which saw the president win both Florida and Ohio, but lose Arizona with races in Wisconsin, Michigan, North Carolina, Georgia and Pennsylvania still to be determined, Trump said it was “a fraud on the American public” to continue counting ballots and he would ask the Supreme Court to intervene, even as he claimed to have won a second term.

After leading in Wisconsin for much of the night, Trump’s lead fizzled and with 95% of the vote reporting, Biden now has a 21,000 vote lead, while Biden is up just 8,000 in Nevada with 67% of the vote.

As a result of the reversal in momentum Biden’s betting odds at Betfair shot up as high as 69%, or roughly where they were trading when election results first started rolling in about 13 hours ago. In the interim, they tumbled below 20% at one point.

And so, after an initial burst of optimism that the election would be resolved quickly and Trump may emerge a shock winner for the second time in a row defying all the polls, with millions of votes in battleground states still being counted, and close contests in five key states, the presidential outcome may not be decided for days, or longer. It’s clear that the election is turning out to be messier and more drawn-out than Wall Street had hoped, especially now that Trump appears set to challenge the result in the Supreme Court.

“The uncertainties associated with a disputed election were what investors feared the most,” Nathan Sheets, chief economist at PGIM Fixed Income, wrote in a note to clients. “Blue-Wave scenarios are now off the table and the probability of gridlock has risen.”

In any case, the key takeaway so far is that Trump has performed better than polls guided, while Biden has not made as much progress in key areas as was expected.

In non-election news, Uber and Lyft stocks were trading higher after California voters sided with the ride-sharing companies in a question over their business model of employing drivers as independent contractors. Shares in both companies rose more than 14% in pre-market trading. On the other side of the world, problems for Jack Ma’s Ant Group are mounting after yesterday’s shock halt to its planned IPO, after China’s Banking and Insurance Regulatory Commission said it plans to discourage lenders from using Ant’s platforms, potentially cutting one of the company’s biggest sources of revenue.

There was some good news on the virus front, with signs the outbreak in Europe was easing, with the German infection reproduction rate falling below 1, even as widespread restrictions remain in place across the continent. Another piece of good news for parents is that there remains little evidence that children attending schools does anything to raise their risk of contracting the virus.

Meanwhile, in rates, treasury futures remain near high end of a wide daily range, which unfolded in high-volume trade as U.S. election results showed a tighter race than polls predicted. The curve bull-flattened as traders unwound bets on a Blue Wave that fueled bear-steepening in recent days. Yields were richer by 1bp to 12bp across the curve with 2s10s flatter by ~9bp, 5s30s by ~7bp; 10-year ~0.80 % vs session low 0.763%; its 18bp range is biggest daily swing since March. Treasuries outperformed bunds by 9bp, gilts by 6.5bp; since London open UST futures volume is almost three times the 20-day average. The next move in yields may hinge on Treasury Department’s quarterly debt-sales announcement at 8:30am ET.

Elsewhere, the dollar erased earlier gains against many of its major peers, while gold slipped. In Asia, Alibaba Group Holding Ltd. tumbled 7.5% in Hong Kong after China halted the initial public offering of Ant Group Co., in which Alibaba owns about a one-third stake.

Looking at today’s calendar, we get the ADP employment change data at 8:15 a.m, the September U.S. trade balance is at 8:30 a.m. October services and composite PMIs are at 9:45 a.m. with ISM non-manufacturing at 10:00 a.m. Oil traders will keep an eye on inventory data at 10:30 a.m. The U.S. officially withdraws from the Paris climate agreement today. Expedia Group Inc., Qualcomm Inc., and Fitbit Inc. are among the long list of companies reporting today.

Market Snapshot

S&P 500 futures up 1.1% to 3,398.50

STOXX Europe 600 up 0.8% to 358.74

MXAP up 0.3% to 175.40

MXAPJ down 0.01% to 580.99

Nikkei up 1.7% to 23,695.23

Topix up 1.2% to 1,627.25

Hang Seng Index down 0.2% to 24,886.14

Shanghai Composite up 0.2% to 3,277.44

Sensex up 1% to 40,645.99

Australia S&P/ASX 200 down 0.07% to 6,062.13

Kospi up 0.6% to 2,357.32

Brent futures up 2% to $40.50/bbl

Gold spot down 0.9% to $1,891.66

U.S. Dollar Index up 0.4% to 93.92

German 10Y yield fell 3.0 bps to -0.65%

Euro down 0.4% to $1.1666

Italian 10Y yield fell 1.4 bps to 0.622%

Spanish 10Y yield fell 2.7 bps to 0.083%

Top Overnight News

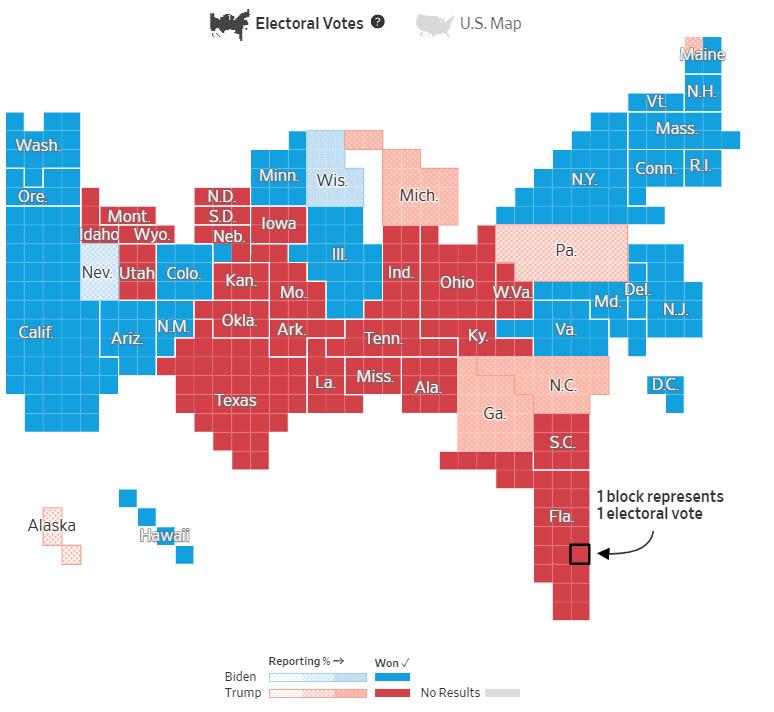

The U.S. election was roiled by President Donald Trump’s false claim of victory over Democratic nominee Joe Biden even with millions of ballots still to be counted in battleground states, and escalated by his threat to ask the Supreme Court to intervene. As of Wednesday morning, Biden had 238 electoral votes while Trump had 213, leaving both shy of the 270 needed to secure immediate victories.

The presidential battlefield is narrowing to a smaller number of states, with both President Donald Trump and Democrat Joe Biden still having paths to victory. Biden now has 238 electoral votes to Trump’s 213

Democratic chances of taking control of the Senate were greatly diminished after several vulnerable Republican incumbents including Joni Ernst in Iowa and Steve Daines in Montana fended off well-financed Democratic challengers in Tuesday’s election

Extreme election night volatility persisted in U.S. equity futures, with S&P 500 contracts swinging from steep losses to gains and back to losses, as investors worked to price in shifting odds for Donald Trump’s re-election and Senate races, a potentially protracted vote count and the implications for economic stimulus

A monthly survey showed demand at euro-area businesses fell for the first time in four months in October, led by a slump in services. That sector is being particularly affected by the new curbs, which are focused on restaurants and hospitality

U.K. Prime Minister Boris Johnson is set to push fresh coronavirus lockdown rules through the U.K. Parliament on Wednesday, facing down rebels in his own Conservative Party who reject the erosion of civil liberties they entail

The U.K.’s dominant services sector expanded at the slowest pace since June last month, a sign that the economy was weak even before new coronavirus curbs were introduced; IHS Markit’s Purchasing Managers Index for the industry stood at 51.4 in October, down sharply from 56.1 the previous month

Italy is poised to ban people from leaving or entering cities and towns in high-risk areas, likely including the financial capital Milan, as part of the government’s latest attempt to check the rapid spread of the coronavirus

A quick look at global markets courtesy of NewsSquawk

Asian equity markets and US equity futures were indecisive as participants digested the early results from the US election which have so far proved to be a tighter than expected race with betting markets even pricing in a greater possibility of US President Trump winning the election with markets even reflecting as high as a 65% chance President Trump winning the election. The results so far have suggested that President Trump has outperformed the polls, although results from some of the key battleground states are still to be announced. ASX 200 (-0.1%) was dragged lower by weakness in the commodity-related stocks and with the largest weighted financials sector pressured as banks adjusted to the lower rate environment, while Nikkei 225 (+2.0%) outperformed as it caught up to the prior day’s global rally on return from the holiday closure and with the USD/JPY-risk dynamic in play. Hang Seng (-0.2%) and Shanghai Comp. (-0.1%) were negative as President Trump remained in contention for a second term and with weakness in Alibaba and HKEX shares after the suspension of the Ant Group mega-IPO which had been set to debut tomorrow, but with downside capped in the broader market after Chinese Caixin Services and Composite PMIs conformed to the recent slew of strong China activity data. Finally, 10yr JGBs are higher amid the overnight indecision and following improved demand at the 10yr JGB auction, while prices also benefitted amid a surge in T-notes which were underpinned amid a closely contested auction with the results likely to be prolonged.

Top Asian News

China’s Fosun Kicks Off Biggest Pharma IPO in India

European cash equities trade mixed (Euro Stoxx 50 -0.3%), after opening with firm losses across the board in light of US President Trump prematurely declaring victory in the US election, whilst calling for voting to cease and stating that he plans to go the US Supreme Court. This sparked risk aversion across market as participants were seeking certainty from the election, something that did not come to fruition as the race remains tight with key battleground states to officially release results later this week, whilst the Senate race remains neck and neck. However, since then, the release of further projections in some states pointing to Biden has narrowed betting market odds, with implied probabilities suggesting a near-50% split for either candidate on Betfair. In terms of US equity futures performance, e-mini NQ outperforms (+2.2%) with some suggesting a reversal of the recent growth/momentum vs. value/cyclical trades that were placed on the back of a prospective “Blue Wave” which appears to now be off the cards, ES (+0.4%) and YM (-0.1%) lag in comparison with noteworthy underperformance in the e-mini Russell 2000 (-1.6%) as it bears the brunt of the unwind in positioning ahead of the election.

Top European News

Italy Readies National Curfew, Movement Bans for Risk Areas

CK Hutchison in Advanced Talks to Sell Tower Unit to Cellnex

U.K. Lockdown Set to Pass Parliament Despite Tory Revolt

Vestas Shares Slump as Trump Risk Spooks Green Investors

In FX, it remains to be seen whether Trump can pull off another victory against the odds, but for now the fact that he is still in with a chance of securing a 2nd term as US President is enough to keep the race alive and prevent challenger Biden from crossing the line. The final outcome may not be known today and markets are in the process of rewriting the playbook that was scripted on the premise that the latter would win via a landslide and perhaps resulting in a clean Blue Sweep. Moreover, the ongoing uncertainty has prompted a change in broad risk sentiment from outright bullish to cautious as is often the case when a major event hangs in the balance. Hence, the DXY has rebounded sharply from lows going into the election and as early vote counts came in, with the index now hovering near the top of a wide 93.070-94.308 range vs Tuesday’s 93.284-94.057 extremes ahead of a busy agenda on paper, including ADP as a proxy for NFP, but with the firm focus on whether Trump stays in the White House or Biden becomes the new resident.

AUD/NZD – In-fitting with the aforementioned too close to call battle for the Oval Office, it’s neck-and-neck down under for the dubious accolade of worst performing major between the Aussie and Kiwi. Indeed, while Aud/Nzd meanders within a 1.0707-1.0650 band, Aud/Usd has recoiled from 0.7200+ to sub-0.7100 and as low as 0.7050 at one stage, while Nzd/Usd is back below 0.6650 compared to peaks not far from 0.6750 in wake of NZ labour data revealing a steeper decline in jobs growth and spike in unemployment, albeit close to consensus.

CAD – The Loonie has also unwound gains vs its US counterpart after a wild overnight session and awaiting Canadian trade for some independent direction or at least temporary distraction from the 2020 US Election, with Usd/Cad around the middle of a 1.3300-1.3095 range.

GBP/CHF/EUR/JPY – Sterling seems to have survived another test of 1.2900 support against the Greenback, but is capped ahead of 1.3000 and well off dizzying 1.3100+ heights for Cable on the US Presidential limbo that poses additional hurdles for a UK trade deal and perhaps prospects of reaching a Brexit agreement with the EU that is already proving extremely elusive. Meanwhile, the Franc is back below 0.9100, Euro under 1.1700 and Yen beneath 104.50, but with decent option expiry interest at the 105.00 strike (1.4 bn) providing some support before any retest of circa 105.35 lows.

SCANDI/EM – The Nok is suffering from more pronounced fallout from the volatile, fluid and fragile market tone as it retreats through 11.0000 vs the Eur again, while the Cnh and Cny are both weaker on the basis that strained relations between Beijing and Washington are highly unlikely to improve if Trump triumphs. Elsewhere, the Rub looks somewhat betwixt and between against the backdrop of Brent recapturing the Usd 40/brl handle, but no conclusion in the US Presidential race.

In commodities, WTI and Brent front month futures have regained composure after experiencing downside on President Trump’s victory announcement alongside his intention to head to the US Supreme court. Price action overnight and in early EU hours have largely (and unsurprisingly) been dictated by the US election and accompanying risk sentiment, with WTI Dec back above USD 38.50/bbl (vs. low 37.26/bbl) whilst Brent Jan reclaims ground above USD 40.50/bbl. In terms of fundamentals, sources yesterday suggested that OPEC and Russia are mulling deeper output cuts early next year in a bid to strengthen the oil market, although no final decision has been made ahead of the JMMC (17th Nov) and the decision making OPEC/OPEC+ meetings on Nov 30th and Dec 1st. Elsewhere, spot gold and silver prices continue ebbing lower on account of the firmer Buck, with the yellow metal back below USD 1900/oz (vs. high 1916/oz) and spot silver sub-24/oz (vs. high 24.50/oz). The firmer Dollar has also weighed on the base metal complex with LME copper and lead on the backfoot.

US Event Calendar

7am: MBA Mortgage Applications, prior 1.7%

8:15am: ADP Employment Change, est. 650,000, prior 749,000

8:30am: Trade Balance, est. $63.9b deficit, prior $67.1b deficit

9:45am: Markit US Services PMI, est. 56, prior 56; Markit US Composite PMI, prior 55.5

10am: ISM Services Index, est. 57.5, prior 57.8

DB’s Jim Reid concludes the overnight wrap

If you’ve come here looking for certainty this morning then maybe turn away and look at the sports pages for last night’s results. Whatever happens now there are two conclusions so far from last night’s election. 1) this is one of the worst opinion polling performances in history, 2) this won’t have a firm conclusion for somewhere between several hours (probably days) to several weeks with the risk of court cases high.

If you’re looking for a sweeping balance of probability it is that Biden is slight favourite for the Presidency but the GOP slight favourite for the Senate. However expect such a scenario to take a while to be confirmed and be contested if correct.

In terms of the highlights so far, President Trump has now as good as won Florida and by a bigger margin than in 2016. The early signs it was going that way was the first indication early on in the night that it wasn’t going to be the smooth “Blue Wave” priced by the pollsters and the markets yesterday. Biden still has multiple pathways to the Presidency if he wins Arizona and a combination of Midwestern states, with Georgia still in play, but it would likely be close and likely contested. The Senate looks equally tight with Republicans ahead at the moment.

As we go to print Biden has just made a confident statement and suggested that every vote must be counted. At the same time Trump tweeted “We are up BIG, but they are trying to STEAL the Election. We will never let them do it. Votes cannot be cast after the Poles (sic) are closed”. This doesn’t suggest either side are close to conceding and fascinatingly Twitter has removed the above Trump tweet from its platform.

The biggest unknowns are the key Midwestern states (Michigan, Wisconsin and Pennsylvania) where the early/mail-in votes are expected to continue being counted in the coming days. North Carolina will still be counting ballots postmarked Nov 3 as long as they are received by Nov. 12th , the same with Pennsylvania but they will stop counting on Friday. Ohio is Nov 2 and the 13th on this measure while Iowa will count ballots until the 9th. So these close races could drag on for a few days.

The Senate composition is also yet to be determined, with Democrats needing to pick up 3 seats if Biden were to win, or 4 seats if Trump were to win, to control the senate after having lost a seat earlier in the night in Alabama. They were able to get one seat in Colorado, but are trailing in North Carolina, Maine and Iowa. They still have a chance in Montana, but the state is likely to be carried at the presidential level by Trump. There are also a pair of Senate elections in Georgia, with one already heading to a runoff in January. Vote counting from that state is delayed until likely later today and the missing votes are mainly from the large Democratic areas including Atlanta. On balance, the chances of Democrats taking the Senate have fallen in the early returns of the election and is likely to remain with Republicans but there is still a chance for it to flip. News outlets continue to expect Democrats to retain control of the House of Representatives.

For some template for what to expect going forward with all this uncertainty, our colleague Alan Ruskin looked at the market reaction to the disputed 2000 election (see here), and predictably US equities, bond yields and the USD lost significant ground during this period. Also see my colleague Henry’s look back at contested elections through US history here .

So far markets have been remarkably calm and are surprisingly not really pricing much risk, or concerns around a long contested battle ahead. Fiscal stimulus looks a longer way off at the moment than it did last night. Nevertheless, overnight markets had a positive US tone shortly after Trump pulled ahead in the Southeast, with S&P 500 futures jumping over +2%, while NASDAQ-100 futures were halted after jumping +3.5% at one point, gaining nearly +4.5% in after-market trading. This move has come off slightly and S&P futures are currently around half a percent higher with NASDAQ-100 futures settling at +2.38%. The Dollar had risen +0.80%, before now sitting at +0.34%. US Treasuries are -8.8bps lower, as the divided government and/or Trump Presidency is likely not to be as bearish for rates as the predicted “Blue Wave”.

In Asia the Nikkei (+1.72%) is leading the gains as it reopened post a holiday while the Hang Seng (+0.31%), Shanghai Comp (+0.18%) and Kospi (+0.59%) are also up. In terms of Asian EM FX, the Korean won (-0.22%), Indian rupee (-0.31%) and Chinese yuan (-0.38%) are some of the biggest underperformers.

This morning we also saw China’s October services PMI data come in at 56.8 (vs. 55.0 expected) bringing the composite reading to 55.7 (vs. 54.8 last month). In other news, the Times newspaper has reported overnight that David Frost and EU’s Barnier are expected to advise that a Brexit trade deal is possible. The report also added that they are expected to recommend a new round of talks beginning in London from this coming weekend.

Though it might seem like ancient history now, risk assets surged yesterday before the polls closed in the US, with the S&P 500 climbing a further +1.78% as investors moved to position themselves ahead of the results. Once again it was a broad-based rally, with every sector and over 90% of the companies in the index moving higher, and banks stocks led the charge on both sides of the Atlantic. Other US indices performed strongly as well, with the NASDAQ (+1.85%) and the Dow Jones (+2.06%) both advancing, while the VIX index of volatility fell -1.58pts on hopes that investors wouldn’t have to wait too long to find out the election outcome. And over in Europe it was a similar story, with the STOXX 600 (+2.34%), the DAX (+2.55%) and the CAC 40 (+2.44%) gaining significant ground, as the STOXX Banks climbed +4.24% to bring its gains over the last 3 sessions to +10.26%.

Safe havens struggled amidst this strength for risk assets, and the US dollar index was down -0.61% yesterday in its worst day since July while yields on 10yr US Treasuries were up +5.5bps to 0.900%, their highest level since early June. There was also a notable steepening of the Treasury yield curve, with the 2s10s curve steepening a further +4.1bps to its steepest level since February 2018. Meanwhile in Europe, there was a widening of spreads between core and periphery, with yields on 10yr bunds (+2.0bps) and gilts (+5.3bps) both rising, as those Italian BTPs (-1.4bps) and Spanish debt (-1.2bps) fell back.

Given the election results, the coronavirus was somewhat lower down the agenda yesterday, though cases continued to rise in Europe in particular, with Italy reporting another 28,244 cases and its highest number of deaths (353) since early May. Even Sweden, which has been associated with a more relaxed attitude in terms of restrictions, announced that there’d now be an 8-person limit on groups at restaurants. Dutch Prime Minister Rutte has extended the country’s partial lockdown until mid-December with some new restrictions as well. The Italian government is also reportedly drawing up plans for new restrictions, with restricted movement from and to high risk areas.

Finally, there wasn’t a great deal of data yesterday, though US factory orders for September increased by +1.1% month-on-month (vs. +1.0% expected).

To the day ahead now, and the main data highlight will be the October services and composite PMIs from around the world. Otherwise, there’s also the US trade balance for September and the ADP’s employment report for that month. Meanwhile ECB speakers include Panetta, Schnabel and Hernandez de Cos.

via ZeroHedge News https://ift.tt/3mPfjue Tyler Durden

Footage out of China shows people in Wuhan dancing in close proximity in a nightclub without a face mask in sight even as other European countries enter into a debilitating second lockdown.

The clip, published by France 24, highlights revelers who are not wearing masks or engaging in any kind of ‘social distancing’ dancing the night away.

“Europe is locked up China parties,” commented the user who posted the video.

This is not the first time that Chinese people congregating in large numbers with no regard for ‘social distancing’ has been highlighted and celebrated.

Back in August, video footage emerged out of Wuhan, the epicenter of the coronavirus outbreak, showing thousands of people packed together enjoying a pool party disco.

The Chinese Communist Party heralded the video as proof that the country had achieved a “strategic victory” in its fight against the coronavirus.

While China’s economy has rapidly recovered to pre-COVID levels, several European countries, including France, Germany and the UK, have just announced second lockdowns that could last for months.

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/32sVwt1 Tyler Durden

Physicians in Ontario report seeing an increasing number of people with advanced cancer. They say it is a result of the government shutting down “non-urgent” health procedures, including routine cancer screenings and cancer surgeries, for three months earlier this year to reduce the spread of coronavirus. Surgeons have since begun working through the backlog of cases, but the number of cancer surgeries performed between mid March and late October of this year is 19 percent below the same period last year. In all, the number of adult surgeries was down by 51 percent in that period compared to 2019.

from Latest – Reason.com https://ift.tt/3mRrMNU

via IFTTT

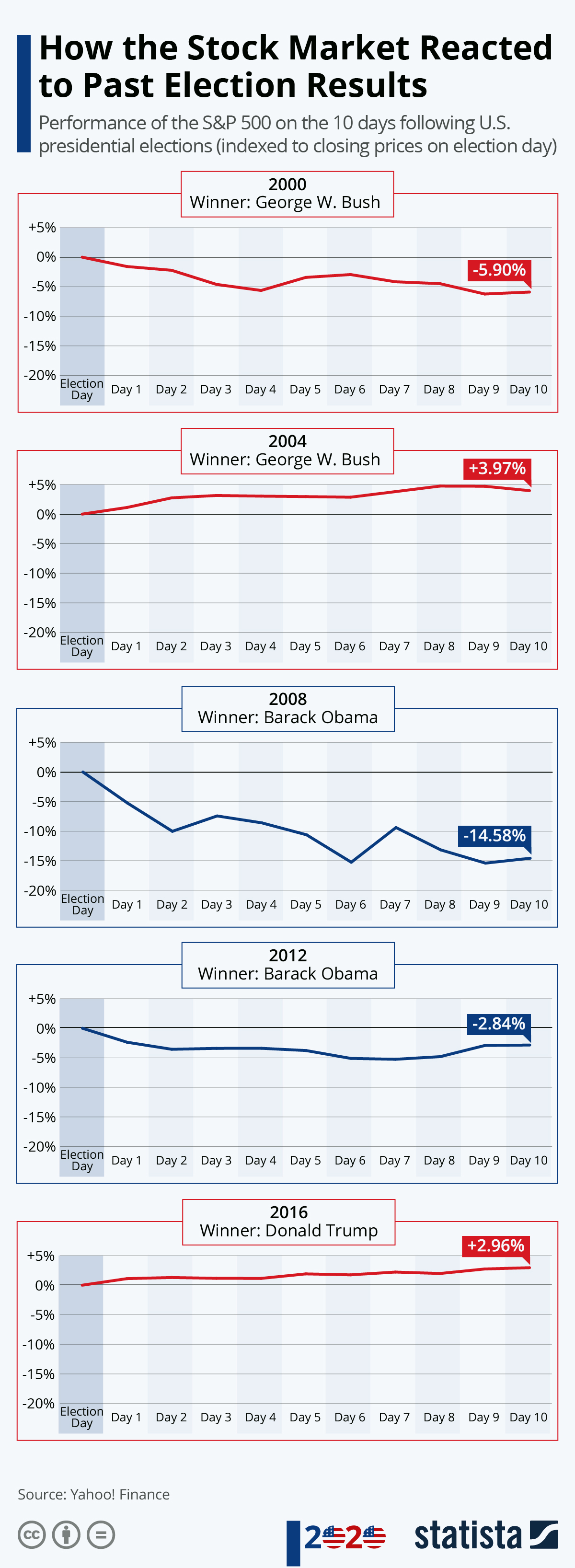

How The Stock Market Reacted To Past Election Results Tyler Durden

Wed, 11/04/2020 – 04:15

As the count continues and a contested US election becomes more and more likely, investors are faced with a high degree of uncertainty. Will markets react positively if Trump is reelected (deregulation, tax cuts, stimulus); or will a Biden win move the needle in the right direction, in the hope that he brings stability to the White House (and the promise of outsized stimulus trumping any fears of higher taxes)?

The election outcome will define the next four years and it’ll be interesting to observe the market’s initial reaction to the result. As the following chart shows, the past five presidential elections didn’t evoke extreme market reactions, with Barack Obama’s first triumph in 2008 a notable exception.

Back then, the S&P 500 dropped 10 percent the first two days after the election, although it needs to be noted that said election took place in the middle of the financial crisis, which left markets particularly volatile.

Trump’s victory four years ago did prompt an extreme market reaction overnight(1000 point crash in Dow futures followed by an even bigger rebound before the market opened the next day), given the surprising nature of his win over Hillary Clinton.

But after that initial insanity, the S&P 500 drifted just 1.1 percent on post-election day and continued its general upward trend the days that followed.

via ZeroHedge News https://ift.tt/34XFaKx Tyler Durden

Physicians in Ontario report seeing an increasing number of people with advanced cancer. They say it is a result of the government shutting down “non-urgent” health procedures, including routine cancer screenings and cancer surgeries, for three months earlier this year to reduce the spread of coronavirus. Surgeons have since begun working through the backlog of cases, but the number of cancer surgeries performed between mid March and late October of this year is 19 percent below the same period last year. In all, the number of adult surgeries was down by 51 percent in that period compared to 2019.

from Latest – Reason.com https://ift.tt/3mRrMNU

via IFTTT

Tightened restrictions, mandatory limits on public life, curfews, orders to stay-at-home, travel bans with invasive hoops, and all the other anti-corona policies that ostensibly aren’t lookdowns: they look like lockdowns, they quack like lockdowns, but in these euphemism-prone times we call them by any other names than lockdowns.

Maddeningly, the goalpost keeps shifting, updating life and language faster and better than George Orwell himself could have done.

First, we had to take precautions to flatten the curve. Hospitals and fears, remember? Then we had to stop traveling, or visit the mall ‒ because who needs that, anyway?

Then we had to wear cloth over our faces and stay away from each other. For the elderly’s sake, naturally.

Then we had to give up public life for everyone’s sake.

The next step, bravely taken by authoritarian politicians and epidemiologists across the Western world, is to intentionally overdo the restrictions ‒ “for now” ‒ so that we have any hope of getting freedoms back for the holidays.

No matter how hard these enlightened autocrats have squeezed, this badly-behaved virus refuses to listen. How odd, they must think; we passed a law, made an announcement ‒ why isn’t it working?

Back to your rooms, the Austrians said. After an explosive number of positive tests in the last week, enough with the provisional liberties and niceties, you’re grounded for the rest of November. Gatherings and cultural events are closed; Christmas markets are out. The Icelanders, already in the spring proclaimed corona free and all summer celebrated in puff pieces by Elizabeth Kolbert in The New Yorker and Adam Roy Gordon in the Atlantic, still dreamily speak of celebrating Christmas.

When the latest rounds of tighter and tighter restrictions came into effect this week, the government talking heads, and the prime minister in particular, told their subjects to give up on Halloween and the next few weeks. Let’s sacrifice these few weeks, they said, so that we can loosen restrictions for Christmas. Fat chance.

The Brits and the French have been even more adamant on setting timelines, or “circuit-breakers,” on their invasive policies. We strip you of liberties, dignities, and the things in which most people find joy ‒ but for a good cause, and just for a little while, okay?

The naivety here was always impressive. Fool me once, shame on you; fool me twice, shame on me. Most people could have plausibly believed what their politicians told them about timelines in the spring; this was a new situation, we didn’t know what the novel threat was, and old handbooks could be thrown out before anyone had time to object. The withdrawn freedoms would be rolled back in time, but as political economist Robert Higgs taught us long ago, never quite fully.

A little over half a year later, we’re going through the same ordeal again. With much better knowledge about the (overblown) risks, with much better tools in preventing spread and safeguarding the elderly. Still, it doesn’t seem to matter. The political overlords, not exactly known for their excellence in interpreting statistics, look at their exponential graphs ‒ and do the exact same thing they did in the spring.

It’s almost as if the virus doesn’t care about your crackdowns, your faster and harder tightening of the societal and commercial noose. If you squeeze people just a little bit more, maybe ‒ just maybe ‒ the virus will listen…? French ministers, like American policy-makers in the spring, started mandating what kinds of products may be on the supermarket shelves: soap is acceptable; makeup isn’t. The Germans, widely celebrated for their track-and-trace program and generous financial schemes, opted for a “mild” lockdown ‒ “just” for four weeks.Perhaps, suggested Holman Jenkins in the Wall Street Journal recently, “the bigger numbers might suggest we are grappling with a natural phenomenon over which we exercise little control.”

Take the bamboozled and highly infected discussion over mask-wearing. They’re effective, they’re not effective; they’re effective if you use them right; and even if they’re not, every little bit counts. In its beautiful infographic the New York Times describes how they work: “A good mask will have a large surface area, a tight fit around the edges, and a shape that leaves space around your nostrils and mouth.”

Even if accurate, we don’t need to go much further than our closest supermarket to notice that that’s not the kind of masks worn by most people. Most people wear loosely fitted, thin pieces of cloth that probably capture some particles ‒ what do I know? ‒ but is unlikely to approach the efficacy that its proponents describe. We reuse them without washing them ‒ can anyone really be bothered? ‒ we don’t put them on properly, they leak left-right-and-center.

The fallback line? Well, not individually but they’re part of a bigger package. The New York Times quotes Linsey Marr at Virginia Tech saying that “something is better than nothing.”

Perhaps every little helps in a what-otherwise-would-have-been sense, but that’s not how most decision-makers justify the above withdrawal of our liberties. Rather, they say that the infection rates are “too high,” the curve too steep, the hospital capacity for treatment too close for comfort. Presuming their honesty ‒ the faking of which I don’t put past them ‒ there’s scant evidence that aggregate mask use correlates in any way with infection rates.

Sweden, where virtually nobody outside hospital settings uses masks, has had lower 7-days rolling deaths per capita than the U.S. for four months straight; lower than the mask-wielding and lockdown-prone U.K. for almost two months. Even the much-praised German experience now has more people dying from (and with) Covid-19 than Sweden does. Infection rates and spread too: the trends since the height of summer or beginning of fall look the same, regardless if you’re a massively mask-wielding country or not.

Yes, it is possible that without widespread mask use among Americans and Brits, infection rates would have even higher and death rates too. I keep wondering, what would the numbers have to look like for you to even consider that what we’re doing isn’t working? That perhaps locking down societies, practically, doesn’t do much to combat the disease, but quite a lot to ruin people’s lives and livelihoods?

We can choose cherry-picked countries for our various cases all we like: the “success stories” of Vietnam, New Zealand, or Australia haven’t done things much differently than Denmark, Austria, France, U.K. or the U.S.: squeeze your populace, and say the magic incantations. Perhaps the virus deity will grant your wishes.

I’m reminded of two-decades old words by Jason Diakité (stage name ‘Timbuktu’), one of my favorite musicians and one of the most successful hip-hoppers in Sweden. In the early 2000s, he released a pretty obscure song called Ett Brev (“A Letter”) structured like a letter to the then-prime minister of Sweden. A political rapper ‒ naturally hard left like all good artists ‒ Diakité was objecting to the many frightening trends he saw in Europe: dismantled social safety nets, overburdened health care services, opposition and hatred towards immigrants. He explicitly included a list of countries where Nazis were allegedly “gaining the upper hand” in typical Antifa-like hyperbole: France, Italy, “BeNeLux,” and Sweden’s immediate neighbor Denmark. The list of places going radically south, as he saw it, was long.

In all of these places, “Forces for good have presumably surrendered.” Little did Diakité know that almost two decades after he penned those provocative lines, his words would ring true across most of the Western world.

The authoritarian threat of 2020 is very different, and instead of neo-Nazi movements of the early 2000s the culprits are established, well-meaning politicians and technocrats. Much like then, Sweden is depicted as a beacon of light, standing against a world gone mad, the last outpost of sanity and the values underpinning Western Liberal Democracy.

Most everywhere else, different rules apply: no matter the facts, we must squeeze harder. The badly-behaved virus must stop progressing, must cease and desist. Anything else, apparently, “just doesn’t seem worth it.”

via ZeroHedge News https://ift.tt/3epaGUB Tyler Durden

Radio Host Crushes Leading UK Epidemiologist’s Credibility Over (Unknown) Cost Of 2nd Lockdown Tyler Durden

Wed, 11/04/2020 – 02:45

In the most thorough demolition of an ‘expert’ epidemiologist who unabashedly advised the UK government of the desperate need for a second lockdown to “suppress” the virus, Independent SAGE member Professor Gabriel Scally was completely unable to respond when LBC’s Maajid Nawaz cornered him on how severely a lockdown would cost the nation.

As LBC’s Seán Hickey reports, Maajid asked whether the member of the Independent SAGE considers “the potential cost and deaths from having a lockdown and weigh them up.”

Professor Scally insisted that “you can’t have a response to this virus that doesn’t take into account the economic factors, social factors and the psychological factors” and his department would definitely take these factors into consideration.

He reiterated the over-used mantra that the bottom line is that “we have to stop the virus – we have to stop it spreading,” and a second national lockdown is the best way to do so.

However, when pushed on the cost, Scally told Maajid he hasn’t seen it, to which Maajid asked the epidemiologist after explaining that the sum is £2.4billion a day whether such funds could be spent elsewhere.

“I would imagine as a public health expert you would have some idea,” Maajid noted.

And that’s when Scally lost all ‘science’ credibility and barked back at Maajid:

“Oh, don’t be silly, you are really now being stupid…”

Which Maajid did not take kindly to the President of Epidemiology & Public Health at the Royal Society of Medicine’s response.

“Is the scientific evidence for why we need to go into lockdown being compared with the scientific evidence for what happens if we don’t and then the death that can come from lockdown versus the death that can come from not locking down compared and the costs compared so we can have a holistic approach to it. Have you done that work?”

“I would have done that work if I was a member of cabinet,” Professor Scally said, when Maajid Nawaz turned the screw.

Watch the full cringeworthy interview here:

And if that wasn’t enough to worry you, here is the same professor slamming The Great Barrington Declaration…

After that, is there any doubt about the politicization of these lockdowns? And why sheepishly following career ‘experts’ in bureaucracy – medical or otherwise – without a healthy dose of skepticism is surrendering entirely to The Great Reset.

Quite frankly, when you see an embarrassment like this, one has to wonder why the mainstream media is not asking similar questions?

via ZeroHedge News https://ift.tt/3oOGwPs Tyler Durden