We have discussed how the markets drifted from one stimulus headline to the next for the past several weeks. Stimulus. No Stimulus. As noted, the daily swings made it a challenging environment to navigate.

This past Thursday, in our daily “3-Minutes” video, we discussed the recent break of support, our indicators, and why there was no “safe place” to hide. The sell-off aligns with seasonal weakness but also the realization that “no stimulus” is coming.

As noted in the video, all of our “sell signals” have been intact for the last few weeks suggesting more downside risk near term. Those signals have now reversed to the point where we are likely to see a decent reflex rally starting as early as Monday. As noted in the year-to-date performance chart below, the market is 2-standard deviations below its 50-dma and is close to the September low support. Performance is positive year-to-date at 1.21%, which still argues for a re-election of the incumbent President.

Sold Out

Given the amount of selling over the last few weeks, it is not surprising to see most of our short-term technical indicators back at lows. Again, as noted above, such suggests that a reflexive rally is possible in the next few days.

Such a rally will provide an opportunity to rebalance portfolio risks accordingly. As we will discuss momentarily, the markets will begin to process the election’s impact on various sectors and the market itself.

However, the economy’s disconnect remains longer-term, which can not last as earnings come from economic activity. While the very short-term trading environment is conducive for a rally, the longer-term “investing” environment is still problematic with weakening relative strength, participation, and fundamental issues.

Depending on your investment time horizon, it is crucial to weigh both charts analysis concerning your current allocation, duration, and ability to withstand volatility.

Last week, I sat down with Richard Rosso, CFP, and Danny Ratliff, CFP, to discuss both candidates’ policies. The video below covers the impact of rising debts and deficits, long-term economic growth, and how markets have historically responded to an election.

Currently, the markets continue to trade in line with election year statistics. While the markets have certainly been under pressure over the last few weeks, the decline has remained orderly for the most part. As noted previously:

“Will policies matter? The short answer is, “Yes.” However, not in the short-term. Presidential platforms are primarily ‘advertising’ to get your vote. As such, a politician will promise many things that, in hindsight, rarely get accomplished.

Therefore, while there currently much debate about whose policies will be better for the stock market, historically and statistically speaking, it doesn’t matter much. A look back at all election years since 1960 shows an average increase in the market of nearly 8.4% annually (excluding the 2008 ‘financial crisis and current 2020 performance.” – Selloff Overdone

Please understand me. There is indeed downside risk to the market currently with plenty of catalysts at hand. However, given the markets have worked off a large amount of the previous overbought condition, it reduced the “risk” of a substantial market decline.

We will discuss how we are managing the market currently in a moment. But first, I wanted to touch on the GDP report.

A Word About That Boomer GDP Report

On Thursday, the Bureau Of Economic Analysis delivered “great” news. In the third quarter of 2020, the U.S. economy grew an astounding 33%. Here is a snip from CNBC:

“Coming off the worst quarter in history, the U.S. economy grew at its fastest pace ever in the third quarter as a nation battered by an unprecedented pandemic started to put itself back together.” – CNBC

Here is the problem.

You sit down at a poker table in Las Vegas with $100. On the first hand, you lose 31.4%—that hurt. However, on the other hand, you go “all-in” and win 33.1%.

So, you are now ahead, right?

Not so fast. Here is the math.

$100 X -31.4% = $68.6

$68.6 X 33.1% = $91.31

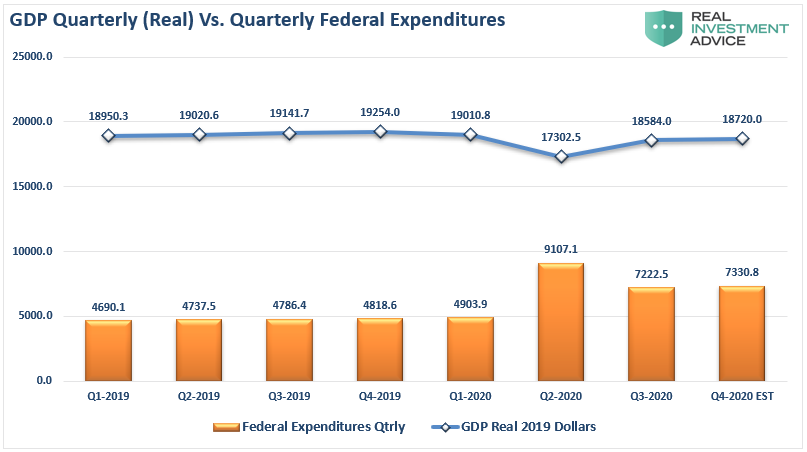

When it comes to the economy, the math is the same. As shown below, despite a “boomer” GDP report in Q3, the economy remains in one of the deepest recessions on record other than2008.

The bad news is that without further fiscal stimulus, economic growth will contract in Q4. Economic growth will contract if federal expenditures fall back to previous levels of roughly $4 Trillion per quarter. In Q4, expenditures will need a run rate of over $7 Trillion to grow the economy at 2%.

The Fed will have a lot of “monetizing” to do.

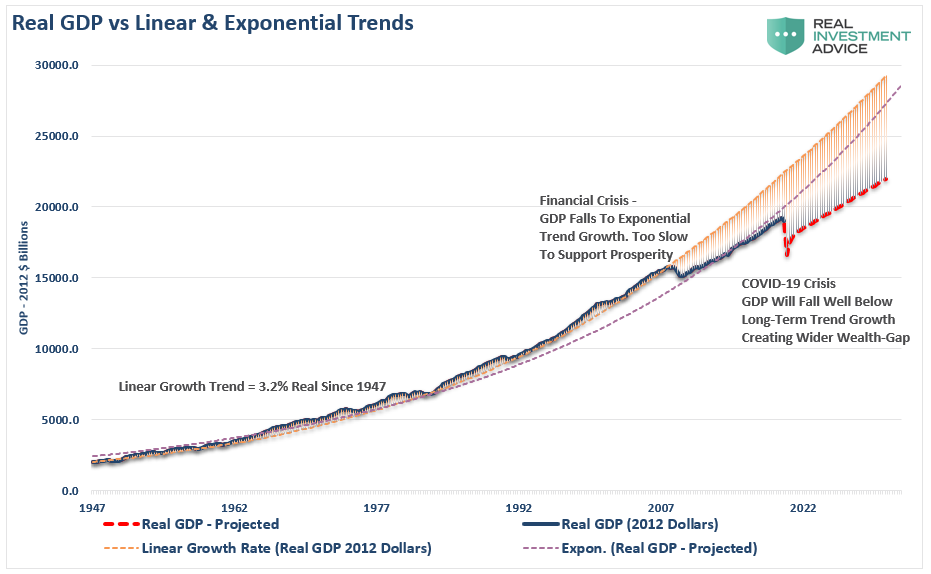

Growth Won’t Return To Pre-Pandemic Trends

Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.

The “COVID-19” crisis led to a debt surge to new highs. Such will result in a retardation of economic growth to 1.5% or less. As discussed recently,while the stock market may rise due to massive Fed liquidity, only the 10% of the population owning 88% of the market will benefit. In the future, the economic bifurcation will deepen to the point where 5% of the population owns virtually all of it.

However, this isn’t just my opinion. As noted by Zerohedge, a permanent loss in output in the U.S. is likely. BofA laid out the pre-covid trend growth and compared it to base case recovery.

Given the permanent loss in output and rising unproductive debt levels, the recovery will be slower and more protracted than those hoping for a “V-shaped” recovery. The “Nike Swoosh,” while more realistic, might be overly optimistic as well.

However, this is the most crucial point from BofA:

The U.S. economy will never return to either its long-term linear or exponential growth trends.

Such has important considerations for long-term investors when it comes to revenue, earnings, and market valuations.

But that is a topic for next time.

For now, let’s get through the election.

Don’t Be That Guy

Our friend Victor Adair shared some of his valuable trading wisdom with our RIAPRO Subscribers (30-day Free Trial) this week, which dovetails with our views.

“The most important thing I do with my trading is to constantly try to identify and monitor the risks I’m taking. Importantly, have strategies in place to control those risks. I think that contributes more to my trading success than picking what to buy or sell. Such is particularly the case given most traders lose money on more than half of the trades they make.

I use stops and keep the time horizon of my trading in sync with the time horizon of my analysis. I watch out for concentration (very important in this current “all one market” environment.) Importantly, I keep my size modest and I make sure no one trade is important. It’s just another trade.

But probably the most dangerous, elusive yet pervasive risk I have to deal with is my innate desire to assign some “reasonable cause” to price action. Such as, “Gold went up today because traders fear that the Fed will tolerate higher inflation.”

I say that’s dangerous because it’s SO easy to be “right” (make money on a trade) for the wrong reason. Once a trader assumes he knows what’s driving prices he’s going to be more aggressive. If he really was right for the wrong reason then he’s going to “dig in his heels” when the market goes against him. That is how you wind up losing WAY too much money.

I don’t want to be that guy.”

via ZeroHedge News https://ift.tt/2TFLUGi Tyler Durden

White House Slams Dr. Fauci As Outbreak Slows; Australia Sees First COVID-Free Day In 5 Months: Live Updates Tyler Durden

Sun, 11/01/2020 – 11:10

Summary:

US new cases retreat after back-to-back records

White House slams Dr. Fauci after latest interview

Australia sees first COVID-free day in 5 months

Netherlands extends run of declines

French government has plan for store owners

Germany won’t close borders

Iran imposes 5-day ban on non-essential travel

* * *

Yesterday, British PM Boris Johnson declared a new one-month “lockdown light” would begin starting late next week in a swift follow-up to a media trial balloon floated earlier in the day.

On Sunday, the focus shifted back to the US, which saw a sudden drop in new cases during the Halloween holiday. Only 81,227 new cases (according to Johns Hopkins count from its COVID dashboard) were added to the countrywide total on Saturday, after 2 straight days of national records.

As of Sunday morning, the US had 9,127,708 new cases, and 230,566 deaths, after crossing the 230k mark on Saturday.

As administration officials fanned out to various TV studios for the last round of Sunday Show interviews before the election, the White House released a statement Sunday morning slamming Dr. Anthony Fauci, after Dr. Fauci sat for a lengthy interview with the Washington Post that was published last night.

America’s top infectious-disease official has seemingly seized every opportunity to raise questions and criticisms of the Trump Administration’s coronavirus response in interviews with the press and town halls with other ‘experts’.

During the interview, Dr. Fauci warned that the US is “in for a whole lot of hurt” from COVID-19 over the fall and winter.

“We’re in for a whole lot of hurt. It’s not a good situation,” Anthony S. Fauci, the country’s leading infectious-disease expert, said in a wide-ranging interview late Friday. “All the stars are aligned in the wrong place as you go into the fall and winter season, with people congregating at home indoors. You could not possibly be positioned more poorly.”

Once again, Dr. Fauci predicted that the US could see cases surge to more than 100k new cases a week, and that deaths might finally climb, unless the US makes “abrupt changes” to its response. A couple days ago, Dr. Fauci finally openly endorsed a nationwide mask mandate, despite myriad evidence that masks don’t markedly low transmission.

Dr. Fauci also said he has “real problems” with Dr. Scott Atlas, a new advisor to President Trump who has in many ways supplanted Dr. Fauci as the president’s go-to advisor.

White House spokesman Judd Deere said in a statement that Dr. Fauci’s comments were “unacceptable”.

“It’s unacceptable and breaking with all norms for Dr. Fauci, a senior member of the President’s Coronavirus Taskforce and someone who has praised President Trump’s actions throughout this pandemic, to choose three days before an election to play politics,” White House spokesman Judd Deere said in a statement.

Deere added that Fauci was “choosing to criticize the president in the media and make his political leanings known by praising the president’s opponent — exactly what the American people have come to expect from The Swamp.” Dr. Fauci has praised Joe Biden’s campaign for allowing its candidate to sit in the basement, while claiming President Trump is tackling the outbreak from a different perspective, one focused on “the economy”.

Additionally, “Dr. Fauci may have just admitted that he is afraid the cure will be worse than the disease and that unlike the president he has no confidence in the American people to make the best choice for themselves armed with CDC best practices,” Deere said.

The CDC on Saturday reported 9,024,298 new cases, an increase of 99,750 from its previous count, and said that the number of deaths had risen by 1,009 to 229,109.

For the first time in 5 months, Australia reported zero new cases nationwide, the result of some of the most restrictive coronavirus-suppression efforts imposed anywhere outside mainland China.

The state of Victoria, the country’s biggest coronavirus hot spot which accounts for more than 90% of Australia’s 907 coronavirus-related deaths, saw zero new daily infections and no deaths for the second straight day.

Interestingly, Queensland voters on Saturday handed a victory to the incumbent Labor Party for a third term, a vote that signaled support for keeping the state’s internal borders closed, a measure which has put local authorities at odds with the federal government. Last week, the state of Victoria ended most of its 111-day-plus lockdown, one of the world’s longest and most restrictive (despite Australia’s relatively low infection numbers). Though the measures inspired protests, polls suggest that the public backs them by a slight majority. Victoria’s Chief Health Officer Brett Sutton said on Sunday that the state may see more movement restrictions eased in the coming days, though he offered few specifics.

“What allowances come…will absolutely be informed by what this week looks like,” Sutton said at a televised press conference. “To see 50,000 cases a day in France, to see Belgium sending patients outside the country because they’re so overwhelmed – that’s what we might have faced if we hadn’t been able to get on top of it.”

With a population of more than 20 million, Australia has seen fewer than 30k cases reported since the start of the pandemic. On Friday, federal officials warned citizens not to travel to the US, or most of Europe, due to heightened infection risks.

Here’s some more COVID-19 news from Sunday morning and overnight:

The Netherlands reported 8,740 new cases in the 24 hours to Sunday morning, extending a recent run of daily declines, the ANP news agency reported, citing data from the National Institute for Public Health and the Environment. That’s down from 9,819 cases reported on Saturday (Source: Bloomberg).

Iran will introduce a five-day ban on non-essential travel to and from 25 major cities, including the capital Tehran, from midday on Monday, the state-run Islamic Republic News Agency reported. The new restriction comes after the country recorded its highest daily death toll yet from Covid-19 (Source: Bloomberg)..

The French government plans to address the concerns of store owners affected by the country’s partial lockdown by imposing limits on supermarkets’ sale of non-essential items and the number of shoppers allowed at any one time, Finance Minister Bruno Le Maire said in a BFM TV interview. Le Maire said that if the outbreak slows, the government will try to find a way to allow stores to open in the coming weeks, possibly by using an appointment system for shoppers. He said online retailers such as Amazon.com Inc. shouldn’t be “the clear winner of this crisis to the detriment of local shops or even supermarkets.” The finance minister, who contracted coronavirus last month, said he had been “scared” for his own health.“I felt things could change dramatically for the worse,” he said. “I wouldn’t wish that on anyone — and I’m 51 and I’m in good health” (Source: Bloomberg)..

German Foreign Minister Heiko Maas said the country won’t close its borders even if the coronavirus numbers get worse, according to the Berlin-based newspaper Tagesspiegel. Infections rose by 11,614 in the 24 hours through Sunday morning, down from Thursday’s record of 23,553, according to data from Johns Hopkins University. The country is set to enter a partial one-month lockdown on Monday as Chancellor Angela Merkel tries to bring the outbreak under control (Source: Bloomberg).

via ZeroHedge News https://ift.tt/3jNx8rB Tyler Durden

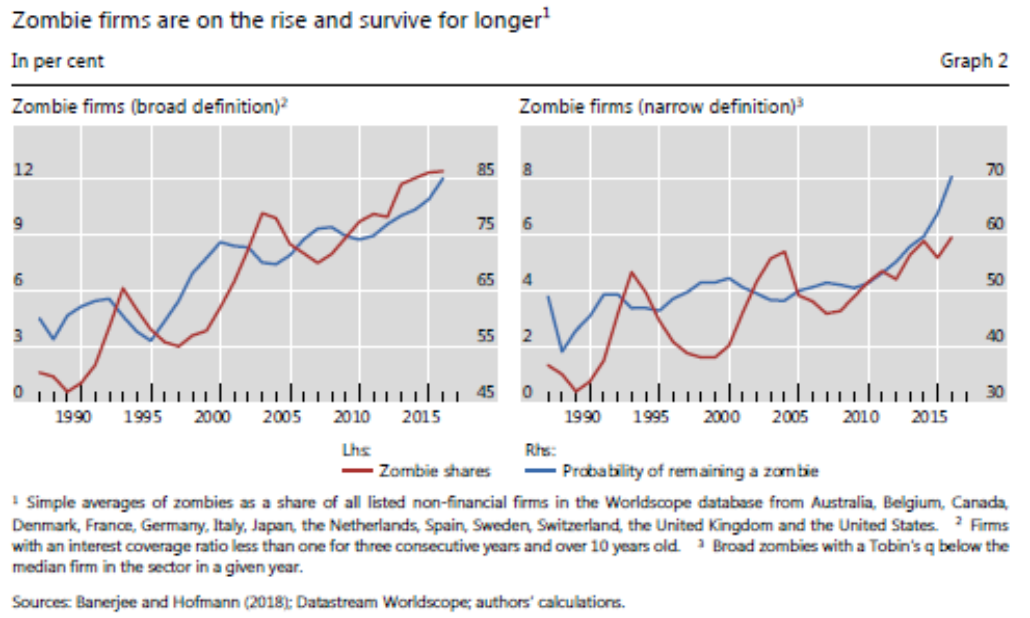

Governments the world over have been lamenting the lack of productivity growth for the last 15 years. In Australia this has been somewhat masked by our enormous population growth, which means that our GDP growth numbers look good on a headline basis but anaemic on a per capita basis. One standout explanation for at least part of this is the increasing proportion of companies in developed nations that meet the criteria of being zombie companies. Due to their over-indebtedness and lack of profitability, these companies tend to make investment decisions based on short term outcomes. Longer term investment in research, equipment and employees is cut back. Two recent articles on this topic caught my attention and together they show that the number of zombie companies is growing, and current policy settings point to this trend worsening in the years ahead.

An outstanding recent paper from Ryan Banerjee and Boris Hofmann at the BIS dug into two basic questions on zombie companies; are their numbers growing and why? Their study used data from listed companies in the US, Europe, Japan and Australia and two definitions for what constitutes a zombie business. Their broad measure is based on market value relative to asset value and their narrow measure (a more common method) captures firms over 10 years old that do not generate sufficient profits to cover their interest obligations for three consecutive years. The graphs below show that either way, there are more zombie businesses and they remain as zombies for longer. This is bad news for economic growth. Zombie firms should be either recapitalised, taken over by a stronger company or bankrupted; so that their assets can be used more efficiently.

The conclusion of the report highlights the obvious trade off central banks have been making for the last twenty years.

Lower (interest) rates boost aggregate demand and raise employment and investment in the short run. But the higher prevalence of zombies they leave behind misallocates resources and weigh on productivity growth.

The second article was from Robin Wigglesworth at the Financial Times. He argued that countries should consider removing the tax deductibility of interest payments for companies. Whilst this would reduce the efficiency of capital structures for companies it would encourage lower debts levels and thus improve resilience.

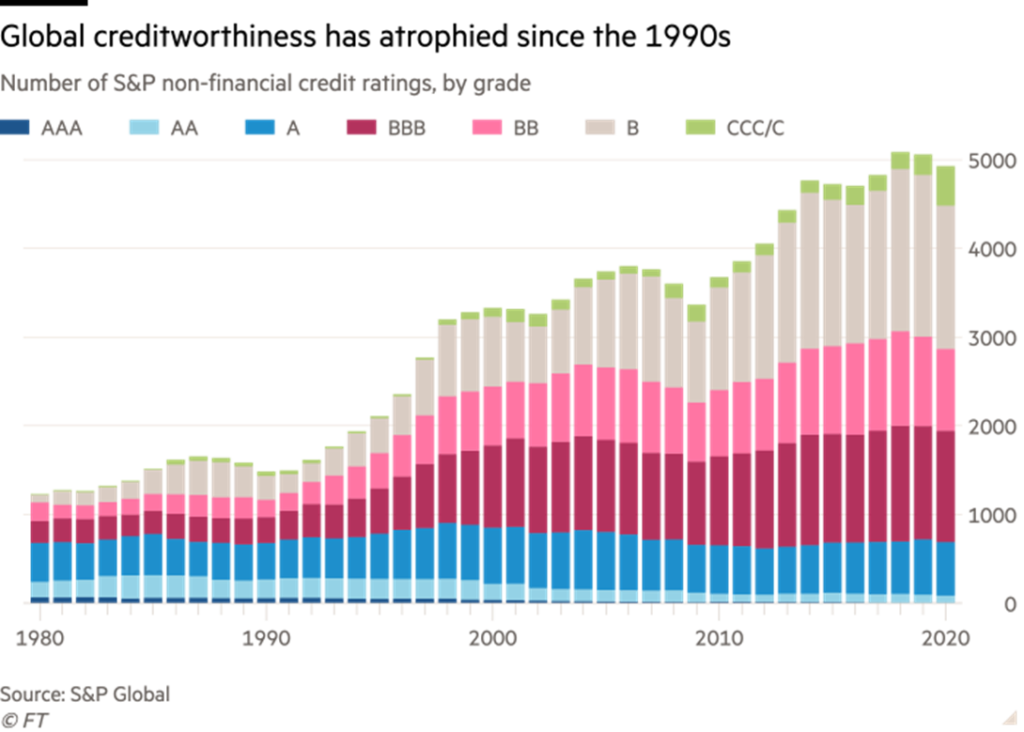

Robin included the graph below in the article, which shows three major trends over the last 25 years. First, companies that choose to have an investment grade credit profile have predominantly migrated to a BBB credit rating. Second, companies that choose to have a sub-investment grade credit profile have predominantly migrated to a B credit rating. Third, most rated companies are now choosing to have a sub-investment grade profile whereas 25 years ago most chose an investment grade profile. This all makes sense when the declining cost of debt is considered.

I agree with Robyn’s sentiments but disagree with his solution. Companies have become somewhat more ruthless in optimizing their capital structures in recent decades. However, the key driver of this is that central banks have chosen to reduce overnight rates thus lowering the long term cost of debt. With the addition of quantitative easing, investment grade rated corporates are typically borrowing at rates less than 2%. In Europe, 29% of corporate bonds were trading at negative interest rates at the end of September. Removing the tax deductibility will make no difference for investment grade borrowers when their cost of debt is minuscule relative to their cost of equity.

For sub-investment grade borrowers their cost of equity can exceed 15% when their owners are private equity, venture capital or founder/family offices. The average yield on American B rated high yield bonds is just 5.52%, so again debt looks cheap compared to equity. Removing tax deductibility will have some impact but getting overnight rates back to normal levels of 4-5% is needed to cure the disease rather than merely address the symptoms.

Given central banks have no intention of normalizing interest rates and unwinding quantitative easing any time soon, low interest rates will continue to allow for zombie companies to multiply. Economic growth will remain subdued, unemployment will be higher, and the cost of goods and services will be higher as productivity growth is suppressed. What has Japan has experienced for the last 30 years and Europe for the last decade is now our future.

Welcome to the zombie global economy.

via ZeroHedge News https://ift.tt/3mFspKu Tyler Durden

Pittsburgh Post-Gazette Endorses President Trump, Marking First GOP Endorsement In Almost 50 Years Tyler Durden

Sun, 11/01/2020 – 10:20

The Pittsburgh Post-Gazette – a well known paper in a key battleground state – came out on Sunday morning and announced their endorsement of President Donald Trump. It’s the first Republican the paper has endorsed for President since 1972 – nearly fifty years ago.

In an editorial called “The Man And The Record“, The Pittsburgh Post-Gazette makes the case for shaking off arguments about Trump’s personality and putting a focus on his record.

The editorial starts by asking what is important when choosing a president. “Isn’t the real question whether he has been taking the country, and the economy of this region, in the right direction these last four years? Can we separate the man from the record?”

The paper also started by acknowledging many of the personality flaws that are often brought up when discussing President Trump: “We share the embarrassment of millions of Americans who are disturbed by the president’s unpresidential manners and character — his rudeness and put-downs and bragging and bending of the truth.”

But then, it does something that many on the left are unable to do: it looks at, and judges Trump, based on his record.

Trump rally near Pittsburgh, PA on October 31, 2020.

“Let’s look at the Trump record,” the piece says. “Under Donald Trump the economy, pre-COVID, boomed, like no time since the 1950s. Look at your 401(k) over the past three years. Unemployment for Black Americans is lower than it has ever been, under any president of either party. Under Mr. Trump, our trade relationships have vastly improved and our trade deals have been rewritten. Thanks to him, middle America is on the map again and the Appalachian and hourly worker has some hope.”

It continues: “Has Mr. Trump done enough for these struggling fellow citizens? No. But he recognized them. Maybe he was not articulate, but he recognized their pain.”

The piece notes that Trump has put America first, the way he said he would:

No one ever asked the American people, or the people in ‘flyover,’ country, if they wanted to send their jobs abroad — until Mr. Trump. He has moved the debate, in both parties, from free trade, totally unfettered, to managed, or fair, trade. He has put America first, just as he said he would.

And it praises him for appointing Amy Coney Barrett: “He also kept his promise to appoint originalists to the Supreme Court of the United States. His third appointment, Amy Coney Barrett, is the best of all — a jurist whose mind and character and scholarship ARE first class. We hope she stands against both judicial and executive excess.”

And you can’t talk about Western PA without talking about the energy industry: “Finally, let’s talk about one of the most important concerns in this region — energy. Under Mr. Trump the United States achieved energy independence for the first time in the lifetimes of most of us. Where would Western Pennsylvania be without the Shell Petrochemical Complex?”

Finally the Post-Gazette rails Joe Biden as “too old for the job, and fragile” and says Kamala Harris “gives no evidence” of being ready to takeover for Biden:

Mr. Biden is too old for the job, and fragile. There is a very real chance he will not make it through the term. Mr. Trump is also too old but seemingly robust. But in Mike Pence, Mr. Trump has a vice president ready to take over, if need be. He is a safe pair of hands. Sen. Kamala Harris gives no evidence of being ready to be president.

“Donald Trump is not Churchill, to be sure, but he gets things done,” the paper concludes. You can read the full endorsement here:

This newspaper has not supported a Republican for president since 1972. But we believe President Trump, for all his faults, is the better choice this year.

Sword-Wielding Attacker Kills 2, Injures 5 In Quebec City Tyler Durden

Sun, 11/01/2020 – 09:57

Two people were stabbed to death and five more wounded in a horrific attack in Quebec City, Canada, on Saturday night, by a man dressed in medieval garments wielding a sword, according to RT News.

The incident occurred around midnight on Halloween, in the neighborhood of Old Quebec.

Quebec City Mass Stabbing:

– 2 dead, 5 injured, after stabbing attack in Quebec City, Canada

– The suspect, who is now in custody, was dressed in medieval clothes

– Stabbings occurred near the National Assembly

Quebec City Police advised all residents in the area to remain indoors, effectively canceling trick or treat festivities as a massive search for the killer, dressed in medieval garments, was underway for about an hour.

Around 0100 ET Sunday, police made an announcement that an arrest was made:

Hours later, around 0420 ET, police tweeted, the situation was “under control,” and the suspect did not indicate that he “acted for motivations other than personal.”

CBC News quoted police spokesperson Etienne Doyon who said the five injured victims were taken to local hospitals for medical treatment. He wouldn’t comment on whether the attacks were random or perhaps motivated.

A Twitter user allegedly captured the suspect on video.

Reuters noted at 0935 ET, Quebec City Police published a statement indicating the suspect is not affiliated with any terror organization.

Nevertheless, the incident took place after a month of religiously motivated stabbings has left France in shock. French officials have warned their country is under “attack” by “Islamist and terrorist madness.”

via ZeroHedge News https://ift.tt/2TGRWGy Tyler Durden

In 2020 alone, the Wall Street owned and controlled Fed poured over $9 trillion dollars into the hands of unnamed trading houses that’s been used for rampant speculation.

Nothing went to Main Street where it’s badly needed during a time of unprecedented economic collapse.

The Fed long ago abandoned its mandate to stabilize the economy, smooth out the business cycle, maintain healthy sustainable growth, create price stability, control inflation, and work for the betterment of everyone.

In his book titled “Tragedy and Hope,” historian Carroll Quigley said the following:

“(T)he powers of financial capitalism had (a) far-reaching aim, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole.”

“This system was to be controlled in a feudalist fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent private meetings and conferences.”

Led by major Wall Street banks, they’ve moved closer to absolute global control of money, credit and debt to dominate economies, politics, commerce, and imperial adventurism.

Former Bank of England director Josiah Stamp minced no words, saying:

“Banking was conceived in iniquity and was born in sin.”

“The bankers own the earth.”

“Take it away from them, but leave them the power to create money, and with the flick of the pen they will create enough deposits to buy it back again.”

“However, take it away from them, and all the great fortunes like mine will disappear and they ought to disappear, for this would be a happier and better world to live in.”

“But, if you wish to remain the slaves of bankers and pay the cost of your own slavery, let them continue to create money.”

The expression about money being the root of all evil leaves what’s most important unexplained.

Money power in private hands — the power to create and control it — exceeds all others.

Notably in the hands of major Wall Street banks, they control its value, supply, and availability.

Easy money, market manipulation, deregulation, reckless speculation, counterproductive fixes, unsustainable debt, and evil intent pushed things toward economic collapse.

In league with Washington, profits are privatized, losses socialized. Main Street is sacrificed for Wall Street.

The Fed bears full responsibility for the mother of all market bubbles.

What can’t go on forever won’t. Bubbles always burst. It’s just a matter of when.

As the saying goes, the bigger they are, the harder they fall.

The big bang when this one goes will resonate worldwide.

Famed investor Jeremy Grantham is noted for his scholarly, sober market assessments.

He correctly predicted the end to Japan’s land and market bubble, the dot.com craze, overvalued US housing, and financial excess that produced the 2008-09 US market crash.

Based on exhaustive research, he explained that bubbles always pop.

“(W)e live in a mean-reverting world in investing,” he long ago said.

All bubbles revert to their median valuation — “no exceptions ever.”

Interviewed days earlier, he said the colossal US equity market bubble will burst in weeks or months.

Timing is imprecise, not the eventual outcome.

Today’s US market bubble “is unlike any other,” he explained.

“It is a rally without precedent – the fastest in this time ever and the only one in the history books that takes place against a background of undeniable economic problems.”

To gauge when when peak valuation may have occurred, look for signs of “crazy” behavior, he said.

“That was not lacking in the rally off the COVID low.”

“That was a late-stage rally with a rapid surge in prices.”

“Another sign of craziness is the flood of interest in special-purpose acquisition companies (SPACs).”

He called them “give me your money and trust me that I will do something useful with it” situations.

“That is a real testimonial to the speculative nature of the market.”

“The stories are everywhere and are what you need for a bubble to break.”

Today, “(y)ou cannot be as certain as in prior bubbles” because of unique characteristics of what’s going on.

But if confidence breaks with stocks way overvalued, “you are looking at substantial declines.”

The music will stop like always before. It’s coming sooner or later for certain.

via ZeroHedge News https://ift.tt/35UC49m Tyler Durden

Global Wine Production Slumps For Second Year As Industry Crushed By Virus Tyler Durden

Sun, 11/01/2020 – 08:45

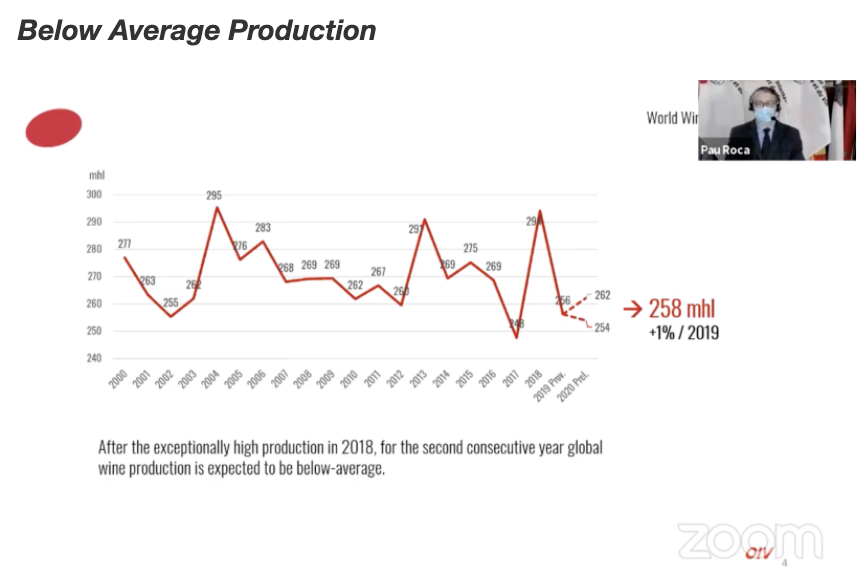

The International Organization of Vine and Wine (OIV) released its global wine production report, warning that after the high production year of 2018, for the second consecutive year, wine production volume will be below average, due to low volumes from South America and European output caps following the virus-induced downturn that crippled sales.

In a zoom call, OIV Director General Paul Roca said the virus-induced global downturn has resulted in declining wine prices, output slumps, and dented demand.

Roca said the pandemic worsened geopolitical tensions, and in some regions, led to tariffs, and a decline in international trade. He said lockdowns and other social distancing measures limited the flow of goods through cities and towns, along with hindering flows on an international basis, adding that the disruption led to disorder in distribution channels, limited production at wine-making facilities, and also resulted in inventory builds.

“The situation differs from country to country depending on the length of lockdown measures, the consumption habits of the population and the elasticity of the substitution between wine and other beverages, and also the relevance of the regular channel or the development level of the eCommerce channel,” he said.

OIV estimates the 2020 global wine output will be around 253.9 million and 262.2 million hectolitres, with a mid‑range estimate at 258 million hectolitres. As OIV points out in the slide below:

“After the exceptionally high production in 2018, for the second consecutive year global wine production is expected to be below-average.”

In terms of supply, Roca said the current situation is not entirely “bad news” given the abundance of worldwide inventory:

“This is not necessarily bad news for the sector given the current context, where wine stocks are still relatively high, and geopolitical tensions, climate change and COVID-19 pandemic are generating a high degree of volatility and uncertainty in the global wine markets,” he said.

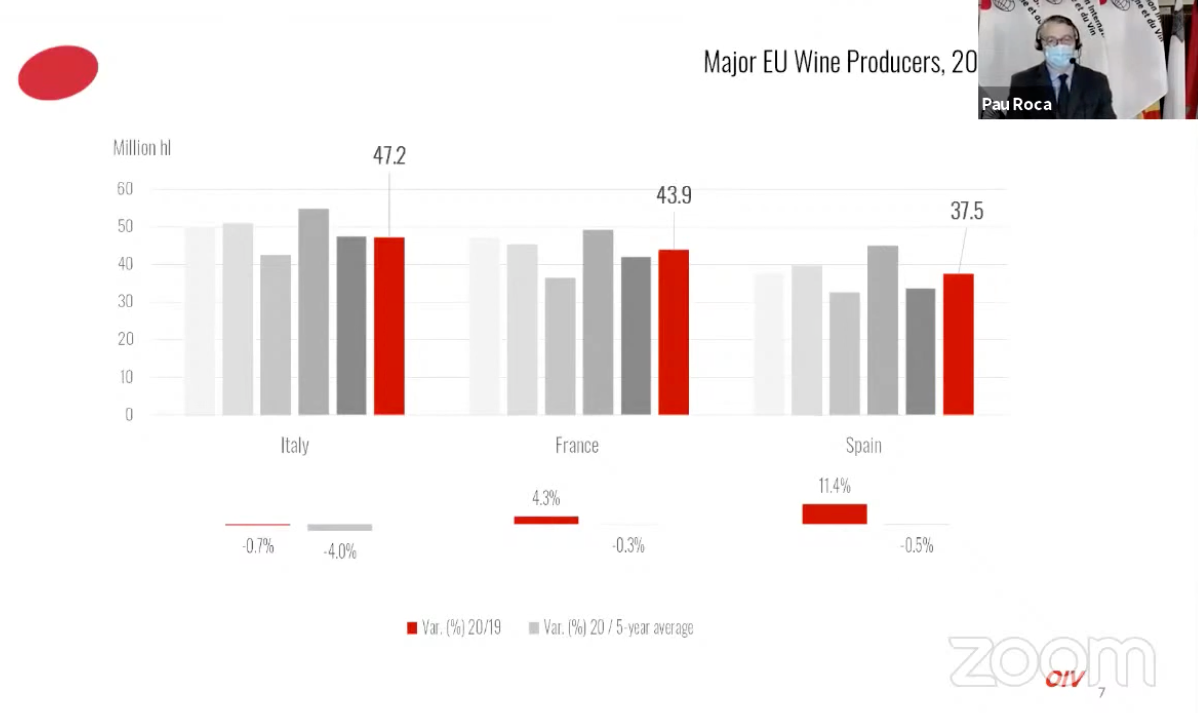

OIV said Europe had desirable growing conditions but output remained lower than average as producers and governments limited production during the virus pandemic. France collected 20% fewer grapes this year because of the collapse in sales. Expectations for the world’s three largest wine producers – Italy, France, and Spain – will have output around 159 million hectolitres, up 5% over 2019 levels but still below average.

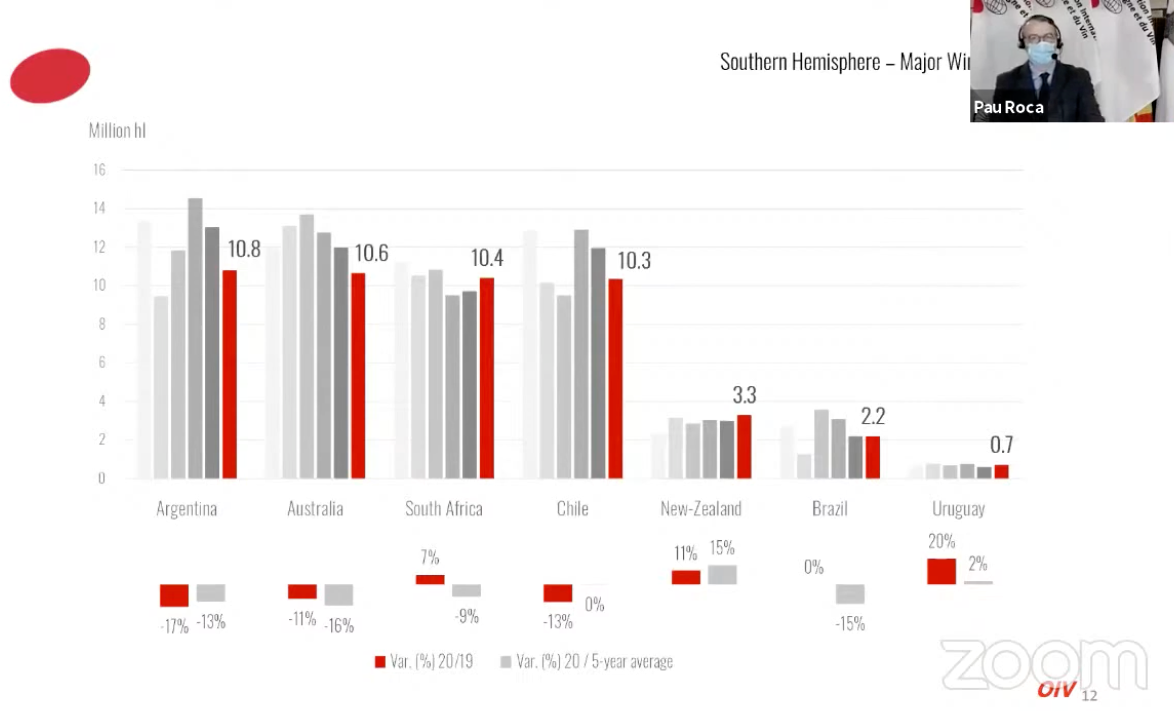

As for wine country in the Southern hemisphere, output totals could decline by as much as 8% from 2019 to 49 million hectolitres. The largest declines were seen in Argentina (-17% YoY), Chile (-13%) and Australia (-11%).

In the US, output estimates for the 2020 year are around 24.7 million hectolitres, up 1% YoY, but OIV notes the forecast could be heavily revised because of the wildfires in Napa Valley, California.

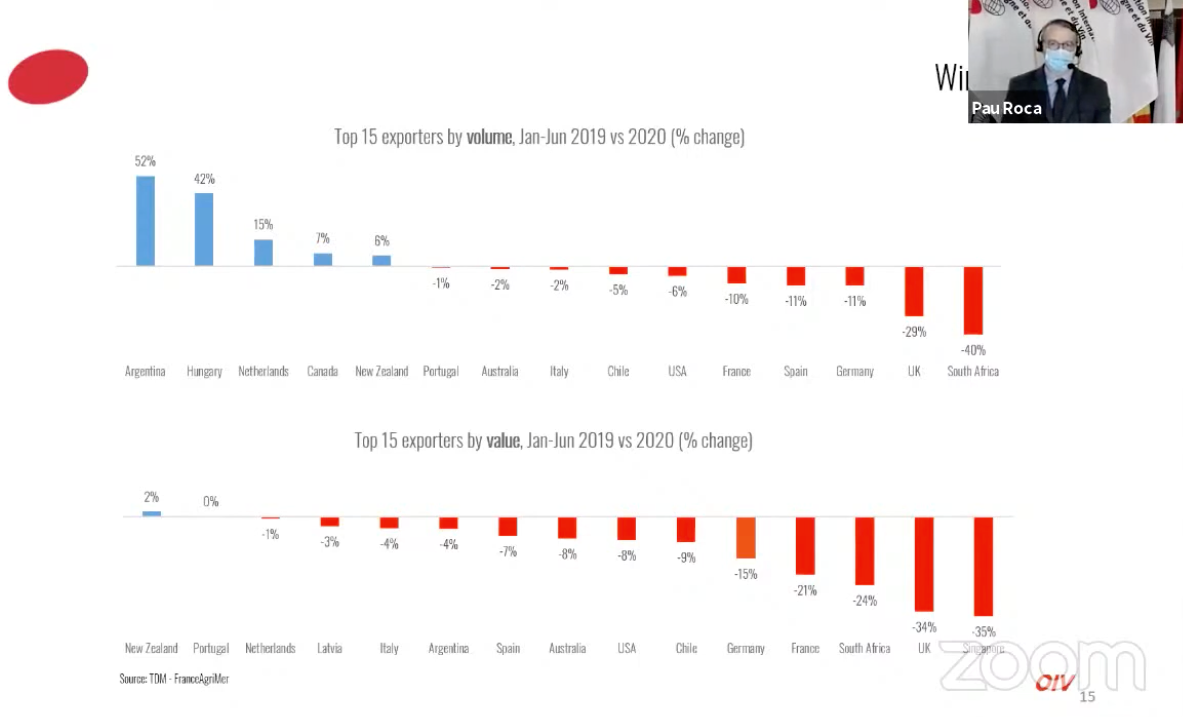

Top 15 Exports By Volume And Value

Here’s the full OIV press conference

To sum up, the global wine industry was already under pressure before 2020, the virus pandemic just made everything worse.

via ZeroHedge News https://ift.tt/3edI2WD Tyler Durden

Trump Versus Biden And The Transatlantic Trade Relationship Tyler Durden

Sun, 11/01/2020 – 08:10

Authored by Maartje Wijffelaars and Philip Marey of Rabobank

Summary:

A Biden victory could pave the way for a more constructive international collaboration on a broad range of topics between the US and Europe and the reversal of steel and aluminum tariffs hikes; it may also put the car tariff threat to bed.

That said, the EU’s push for regulation of big tech, a digital services tax, and a carbon border adjustment mechanism, as well as relatively low defense spending and its protective agriculture policy would likely remain areas of transatlantic tension.

Finally, we expect the EU to be willing to cooperate more with the US on how to deal with China, albeit in a less aggressive way than the US. This means that a Trump victory would put more pressure on the EU stance regarding China than a Biden win.

With the US presidential elections coming up, this raises the question of whether the result actually matters for the EU. After all, it is no secret that the transatlantic relationship has worsened over the past few years. Should we expect the relationship to be healed if Biden wins the presidency?

We argue below that the outlook for transatlantic cooperation on a broad range of topics would indeed improve under a Biden presidency, that steel and aluminum tariffs might be reversed and that the threat of new tariff hikes would lessen. That said, some areas of transatlantic tension would likely remain and an overarching trade deal – including zero tariffs and barriers on non-car related industrial goods and lower barriers to services trade, as agreed by Juncker and Trump back in 2018 – seems as unlikely under Biden as under Trump.

With Trump in the White House, we think the US would continue to act unilaterally on many fronts and use the threat of raising (car) tariffs in order to force the EU to comply with multiple US requests. As such, it is likely that tariffs on a (very) small portion of EU-US trade would probably increase, although a hike on car tariffs and a full-fledged transatlantic trade war would still remain a downward risk rather than a given. Should that risk materialize, though, it would have large negative economic consequences.

Below we take a closer look at how the Transatlantic relationship has evolved in recent years and which factors may change under a different US presidency and which factors are expected to be insensitive to the election outcome.

Transatlantic relationship turned sour

Unilateralism trumping multilateralism

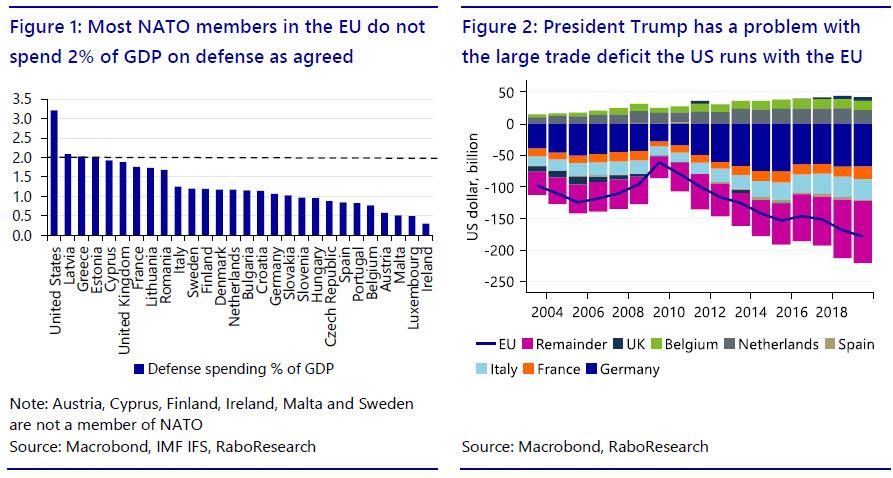

The Trump administration, compared to its predecessors, has chosen for a more unilateral foreign policy approach and has struck an assertive rather than cooperative tone towards the EU. Over the past few years the US has withdrawn from the Paris climate agreement; blocked the appointment of judges for the WTO’s appellate body, effectively paralyzing the international trade body; put in motion its withdrawal from the WHO, to be effective from 6 July 2021. It has also stalled OECD talks on a global tax reform for large multinational companies, including big tech; and has stoked fears the US may reduce support to NATO, over frustration that many non-US members do not pay their fair share, i.e. 2% of GDP.

Steel and aluminum tariffs and car tariff threats

International trade has played a key role in the more assertive tone by the US. By using the threat of import tariff hikes the US has been pushing the EU to increase its defense spending (Figure 1), more actively fight China’s unfair trade practices, ban Huawei from the EU’s 5G network, open up its agriculture market and lower tariffs on US cars (Figure 2).

In response, the EU has tried to accommodate US demands on certain points. For example, several member states have ramped up defense spending and have banned Huawei, whilst the EU has lowered barriers on imports of US beef and lobster. However, the broader picture is that the EU has mainly tried to talk its way out of higher tariffs on its goods, while threatening to retaliate US tariff hikes it deems unjust. So far, the US has indeed hiked steel and aluminum tariffs in 2018, which the EU retaliated, while EU cars have so far been able to dodge that bullet. However, not all ‘tensions’ can be directly related to the more assertive stance by the Trump presidency. One of them is the ongoing dispute between the two biggest aircraft manufacturers in the world.

The Airbus – Boeing dispute

Last year, the US raised tariffs on Airbus jets and on a basket of other EU goods such as wines and cheeses, in total targeting USD 7.5 billion EU products (1.5% of US imports from the EU27+UK). These tariff hikes are the result of a 16-year old dispute between the EU and the US over state subsidies to Airbus and Boeing, respectively. The EU’s trade commissioner Dombrovskis hopes that the US will drop these tariffs, now that the WTO (in October 2020) has authorized the EU to impose tariffs on USD 4 billion of US products to retaliate subsidies to Boeing (1.2% of EU27+UK imports from the US). Yet if the US will not drop those, the EU stands ready to increase tariffs on Boeings and other sensitive US goods, probably over the course of November. Hence, the quality of the relationship between the US and Europe could still play a role in the outcome of this particular dispute.

The EU taking on big tech and climate change

Finally, on tariffs and threats, the Trump administration has indicated that it is not amused by the EU’s plans for a carbon border adjustment tax, tougher regulation on (big) tech and a tax on digital services. The US argue it discriminates against US firms and has warned the EU that it would retaliate any protectionist move in this regard, i.e. any move disproportionally harming US firms. In fact, in response to the unilateral implementation of a digital services tax in France last year, the US published a list of French products it would target with 25% higher import tariffs should France go ahead with its plans to collect the tax. The US has warned others with similar plans, such as Italy and Spain, to be mindful. The EU has responded by threatening to retaliate. So far, France has delayed the collection of the tax and the US has refrained from activating the tariffs, at least until 6 January 2021.

The risk of additional US import tariffs in this respect remains alive, especially since OECD talks to reform the global tax regime seem to be heading nowhere and most EU countries are determined to make tech giants pay taxes where they are earned. The EU is due to present a revised plan for the digital services tax early next year and implement it by January 2023 at the latest. With the agreement on the new EUR750bn crisis recovery fund, the drive to come up with ‘own sources’ of funding has increased. According to the latest known proposal, the EU expects to collect about EUR 1.3 billion annually with the tax, to be used to pay interest and/or redemptions related to the Recovery Fund.

In short, the Transatlantic relationship has been under strain during the last four years under a Trump presidency, whilst the EU is also increasingly working on its own agenda. The US presidential election result could either intensify/accelerate the recent trend or attenuate it, although we believe a full reversal is unlikely, as we explain below.

Biden versus Trump

Backpedaling from unilateralism back to multilateralism?

We expect a renewed Trump administration would continue its America First strategy as described in the previous section, while a Biden win would pave the way for more constructive international collaboration on several topics. For example, a Biden administration would be expected to engage with the EU to, among other things, reform the WTO, by following up this year’s joint statement by the US, the EU and Japan on industrial subsidies and forced technology transfers. In the meantime, it would likely lift the US’ current blockage of judges for the appellate body, supporting the revival of the WTO’s appeal court. Note, though, that while this would soften tensions between the EU and the US, WTO reform will still be very difficult. China would need to approve as well, while formulating a framework on how to adequately detect unfair state aid is far from straight forward. Hence, apart from striving for WTO reform, a Biden administration would likely also look for other ways to team up with the EU to fight China’s unfair trade and investment practices. Given that Biden – like Trump – would adopt a harsh stance against China.

Other areas for improved cooperation would be the fight against climate change – with Biden expected to reaffirm US commitment to the Paris climate agreement – and possibly OECD negotiations on global tax reform. That said, it would remain very difficult for the EU, eager to tax big tech income generated at its soil, and the US, desperate to protect their big tech companies, to find common ground. As long as negotiations are ongoing the EU could chose not to implement a digital services tax on its own, but if negotiations prove to be heading nowhere, the EU may still move ahead unilaterally. Indeed, if no consensus can be found at the EU-27 level, several member states may start collecting the tax on their own.

Finally, Biden is expected to reinvigorate US commitment to NATO, while continuing Trump’s push for higher defense spending in the EU. The latter is a challenging aim, because this belongs to the prerogative of the member states. Furthermore, the COVID-19 crisis has already emptied governments’ pockets and history makes Germany wary of investing extensively in its armed forces. Consequently, we believe, this issue will remain a source of transatlantic tensions.

Tariffs, threats and a new transatlantic trade deal

Turning to trade, the risk of new tariff hikes would likely decline under a Biden administration. A reversal of Trump’s steel and aluminum tariffs and, as a consequence, EU retaliatory tariffs seems likely. They currently affect about 1.5% of EU goods exports to the US and 1% of goods travelling from the US to the EU (Figures 3). Furthermore, the threat of car tariffs could be expected to fall by the wayside.

That said, not much progress on an overarching liberalizing trade deal, lowering tariffs on a broad range of (industrial) goods, should be expected. The US currently insists that barriers to agriculture trade will be subject to trade talks as well, yet the EU’s hands are tied (see below). Disagreement seems virtually impossible to overcome. Moreover, plans for an EU digital services tax and a carbon border adjustment mechanism may not go down well with a Biden administration either. Nor would a Biden victory lead to an easy fix for the 16-year old Airbus – Boeing dispute we would argue.

The key difference with a Trump administration, we feel, is that a Biden administration would be more willing to talk with the EU to come up with a negotiated solution on these topics, thus reducing the risk of future tit-for-tat tariff hikes.

If Trump wins he is unlikely to change course. In that case we should expect additional US tariff hikes as the EU, or at least many of its member states, would move forward with a digital services tax. The EU would retaliate. The Airbus-Boeing dispute would arguably also be more difficult to resolve leading to EU tariff hikes related to the Boeing ruling and possibly higher US tariff hikes related to the Airbus ruling. The higher tariffs could have a substantial impact on individual producers, but the total direct macro-economic impact would likely be close to zero. Meanwhile, the threat of car tariff hikes- to push the EU to adhere to different US demands – would remain very much alive, stoking uncertainty. Still, implementation of such car tariffs and a full escalation of the transatlantic trade dispute would continue to be a risk rather than our base case. Should it materialize, the impact would be substantial, though. Especially for economies with large car exports to the US and large car industries, such as Germany, Hungary and Italy. A year ago, we calculated that car production in these countries could shrink by as much as 5%, if the US would hike import tariffs on European cars to 25% (Figure 4).

The EU and its agriculture policy

Common Agricultural Policy has been one of the pillars of the EU. Several Member States have a strong agricultural lobby to protect their domestic farmers and substantially lowering existing import barriers will likely prove to be a bridge too far. At the same time, ideological differences when it comes to genetically modified organisms – generally being approved faster in the US than the EU – will be difficult to overcome. Changes in GMO approval regulations have been made in the past, but they usually are very time consuming and often opposed by both politicians and non-profit groups. So in short, in our view the EU is not likely to make big concessions in this area. This means that a Trump victory would put more pressure on the EU than a Biden win. Trump is likely to take a more aggressive approach on agriculture. Keep in mind that rural areas tend to vote Republican. In a future publication we will dive deeper in the agriculture dossier, also addressing the possible impact of escalation or de-escalation for different F&A subsectors.

The EU and China

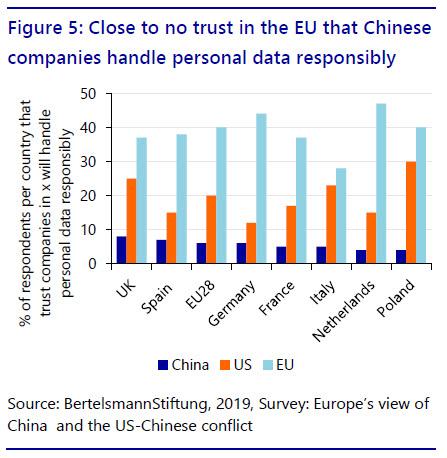

Over the past years, the EU has stepped up its effort to tackle unfair trade practices and investments by China, as well as potential security risks related to takeovers and investments by Chinese companies. This has happened alongside increasing negative views on China among EU citizens according to PEW research. According to a poll by the BertelsmannStiftung in 2019 EU citizens also have close to no trust in Chinese companies handling personal data responsibly (Figure 5). The COVID-19 crisis also seems to have done China no good in the opinion of EU citizens. This suggests that in many large countries there is broad support for a tough(er) approach vis-a-vis China and Chinese companies. At the same time, though, some Eastern European member states, such as the likes of Hungary (which are lacking in the abovementioned surveys), could be expected to hold on to a different view given their governments’ friendliness towards China.

With regard to international trade, the European Commission has far-reaching powers, but approving foreign investments in for example 5G networks ultimately falls within the remit of member states themselves. All the European Commission can do (and has done in this respect) is to create awareness and shape guidelines with screening tools for FDI investment and hostile takeovers in strategic sectors and to prevent unfair competition in bids which are due to state aid. Unlike the US, the EU has stopped short of hiking tariffs to force China to open up its markets and alter its policy of state subsidies and forced technology transfers. Instead it is trying to move the country via dialogue on further cooperation and urging for WTO reform. Going forward, while toughening up, the EU is likely to continue to follow the path of dialogue and unlikely to neglect the importance of its economic ties with China.

Meanwhile, growing awareness in member states on (security) risks related to especially investment in the 5G networks has led to the exclusion of Huawei in some countries, and heavy debates and altered legislation, lowering Huawei’s chances, in others. From France to Poland and Sweden to Italy. Even Germany, a country with large trade ties with China, is considering legislation effectively preventing Huawei from taking part in its next generation 5G network. Yet an EU-wide outright ban on the Chinese IT company as the Trump presidency has been calling for, appears unlikely. So it remains to be seen whether the EU is being viewed as doing enough in these respects. Moreover, especially Eastern member states, have in fact intensified cooperation with China over the years, by signing up to the one-belt-one-road initiative. Recently Hungary, for example, even welcomed the plan for a R&D center of Huawei in its capital. So while many member states seem to be following more or less the same route, especially when concerning data security risks, some are deliberately following a different path.

All in all, going forward we expect the EU to be willing to cooperate more with the US on how to deal with China, but in a less aggressive way than the US. This means that a second Trump term would put more pressure on the EU stance regarding China than a Biden administration. President Trump is taking a more confrontational approach regarding China than we expect from a President Biden. What’s more, the multilateral approach that Biden has in mind will also lead to smaller repercussions for the EU if it does not fall in line with the US than Trump’s bilateral approach. At the same time, developments in the past years suggest that while the EU is not blind for US threats and pressure, a Biden administration could be more successful in getting the EU on board with its China policy because it would treat the EU as an equal partner, while the Trump administration does not, tarnishing the EU in its honor and forcing it to increasingly work on its own agenda.

In short

We expect a Biden victory to pave the way for more constructive international collaboration on a broad range of topics and the reversal of steel and aluminum tariffs hikes. It may also put the car tariff threat to bed. That said, the EU’s push for regulation on big tech, a digital services tax, and a carbon border adjustment mechanism, as well as relatively low defense spending and its protective agriculture policy would likely remain an area of mutual tension.

A rise in tit-for-tat tariffs on a small group of products would be more likely with Trump in the White House and, we expect Trump to keep the threat of car tariff hikes alive, stoking uncertainty. But the latter’s implementation and a full escalation of the transatlantic trade dispute would continue to be a risk rather than our base case.

Progress on an overarching trade deal, substantially lowering the barriers to trade, seems limited under either president. All in all, while the atmosphere and risks would greatly differ, the direct positive macro-economic impact of an improved transatlantic (trade) relationship under Biden and the negative impact of a strained relationship under Trump seems limited. Clearly, uncertainty and the downward economic risk related to a Trump presidency would be much larger.

via ZeroHedge News https://ift.tt/381Enu0 Tyler Durden

‘Le Grand Escape’ From Paris: Footage Shows Record-Breaking Traffic Gridlock Hours Before Lockdown Tyler Durden

Sun, 11/01/2020 – 07:35

Viral footage out of France shows what reports described as hundreds of miles of traffic jams in an around the French capital at the close of this week just as a Macron-mandated second national lockdown went into effect Friday.

The new lockdown measure took effect Friday at midnight with a 9pm curfew, which requires all residents to stay at home other than for essential work or medical reasons. It appears that hours before the lockdown went active, Parisians rushed to get out of the city, as one viral video showed. The stay-at-home orders have been issued to be in effect for one month – at least until December 1.

Incredible traffic jam in Paris as people try to leave the city before 9 pm curfew and before confinement begins at midnight. Traffic is barely moving in every direction as far as the eye can see. Lots of honking and frustrated drivers. pic.twitter.com/6Zn2HCxuPl

As of midnight Parisian time, people were ordered to stay at home except for essential work or medical reasons, resulting in many relocating to more rural areas to wait out the month-long lockdown, the BBC reported.

Video posted to Twitter showed never-ending streams of crawling headlights on every road in every direction. There also were reports of restaurants jammed with diners enjoying a last meal out for the time being.

It was also likely exacerbated by many people simultaneously attempting to return to their residences given this week is a school holiday that ends with Catholic All Saints Day on Sunday.

Trains heading out of Paris at Gare de Lyon, via Rex Features/The Independent

Restaurants, bars, and night venues were also reported packed and overflowing as many Parisians tried to slip in their last night out for a month.

Macron in making the initial announcement Wednesday said France must “brutally apply the brakes” to avoid being “submerged by the acceleration of the epidemic”. France is currently the fifth most infected country at over 1.3 million COVID-19 cases to date.

#Coronavirus: Paris has seen hundreds of miles of traffic jams as people tried to leave the city ahead of France’s new national lockdown https://t.co/wdZ7dH2Nee

The Danish newspaper that provoked violent worldwide protests after publishing cartoons of the Prophet Mohammad in 2005 has refused to do so again, with its editor-in-chief commenting, “Violence works.”

The decision follows the beheading of school teacher Samuel Paty in Paris for showing similar cartoons to pupils in his class and another attack yesterday in Nice during which three people were killed near a church, including a woman who was decapitated.

The culprit in Paris was a Chechen refugee who French authorities had given residency papers to back in March, while the jihadist in Nice was a boat migrant who arrived in Italy from Tunisia last month.

Now Jacob Nybroe, editor-in-chief of Jyllands-Posten, says his newspaper will not accept ads being run by Danish political party the New Right, which includes cartoons of Mohammad, due to the risk of a violent backlash.

The cartoons are being run in collaboration with Charlie Hebdo to “show support for the victims of Islamic violence,” but Nybroe says his newspaper can play no part in it.

“Security for us is unfortunately not a theoretical, moral, or political consideration,” Nybroe said.

“I wish it was different, that we could express ourselves freely, as we do in all other matters. But violence works,” he added.

“Only in one circumstance do we show caution – that is, in fact, a censorship inflicted on us by threats: we do not show drawings of the Prophet Muhammad,” Nybroe explained.

After Jyllands-Posten published 12 cartoons to spark a debate about criticism of Islam, the move prompted global violent riots as well as numerous threats against newspaper staff.

The backlash was described by former Danish Prime Minister Anders Fogh Rasmussen as “Denmark’s worst international crisis since World War II.”

Three other Danish newspapers said they would review the cartoons before deciding whether to publish them.

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/3oPpwsC Tyler Durden

{kind=link}

{kind=link}