I’ve just finished up a rough draft of my The Right to Defy Criminal Demands article, and I thought I’d serialize it here, minus most of the footnotes (which you can see in the full PDF). I’d love to hear people’s reactions and recommendations, since there’s still plenty of time to edit it. You can also see all the posts here.

[* * *]

Criminals create risks for society—risks for their intended targets, and risks for bystanders. By defying criminals’ demands, the criminals’ victims may anger the criminals, and the criminals may respond by retaliating in ways that harm third parties.

Yet the law ought not in effect help criminals implement their demands by imposing liability on the defiant victims. People must have the freedom to refuse to obey such demands, even when the refusal creates some extra risk.

Free citizens have a legal obligation to obey the law. But they shouldn’t have a legal obligation to obey criminals. Kipling was dealing with limits on kings when he wrote of

Ancient Right unnoticed as the breath we draw—

Leave to live by no man’s leave, underneath the Law.

Yet the same is equally true of living by no criminal’s leave. Giving criminals’ demands legal effect undermines their victims’ dignity, precisely because it subjects people not only to the democratically endorsed coercion of the Law but to the arbitrary tyranny of the criminal. And it undermines the Law’s rightful claim to be the one authority that may use the threat of violence to set the rules of behavior.

Market bottom? Is it in? That was the main question I got last week, and I even discussed it with Charles Payne of Fox Business. It’s the one answer everybody is searching for. Is it time to “load up the truck” for the next leg of the bull market or go to cash?

It certainly is a problem now, given that January had a rough start for the S&P 500. But, of course, such brings up the age-old Wall Street axiom “so goes January, so goes the year.”

Chart courtesy of Zerohedge (ahead of last two day rally)

As of this past Friday, the damage is quite apparent. As noted by Zerohedge:

“Nasdaq is down 5 straight weeks (16% from its highs) – the longest losing streak since 2012 – while Small Caps are down 22% from their highs (in a bear market)“

After a year, investors believed they “could do no wrong,” now it seems as if “nothing is going right.”

When the “bull is running,” we believe we are smarter and better than we are. As a result, we take on substantially more risk than we realize as we continue to chase market returns and allow “greed” to displace our rational logic. Like gambling, success breeds overconfidence as the rising tide disguises our investment mistakes.

Unfortunately, during the subsequent completion of the full-market cycle, our errors return to haunt us. Always too painfully and tragically as the loss of capital exceeds our capability to “hold on for the long-term.”

Such is where many investors find themselves today, hoping for a return of the bull market to bail them out of bad investment strategies.

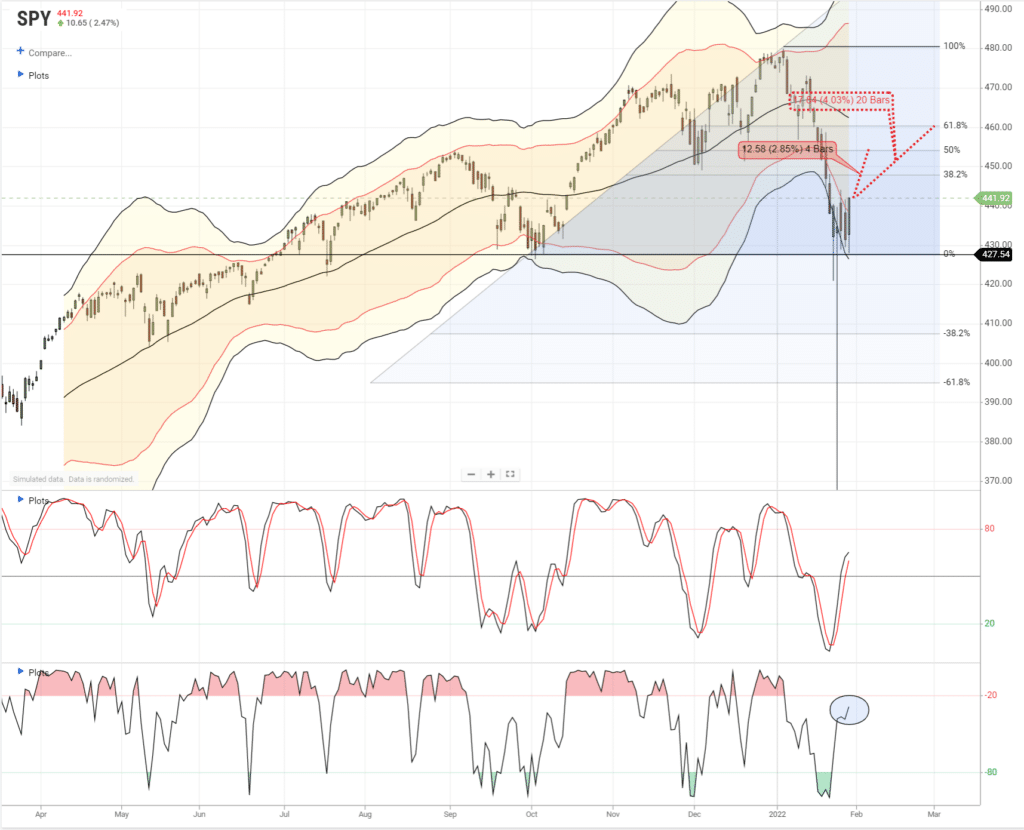

So, is a bottom in? First, let’s look at the technical backdrop.

The markets do look to be stabilizing, as shown below, and are holding the October lows. That 100% Fibonacci retracement, and multiple rally attempts, triggered a short-term buy signal. All of this is short-term bullish.

Furthermore, our Simplevisor Money Flow analysis is also at extreme oversold levels. Such usually provides a sustainable rally, particularly when the indicator is at extreme lows and triggering a “buy” signal as it is currently.

However, while the technicals suggest a short-term bottom is getting established, we are concerned that may limit any bounce to a 50% to 61.8% Fibonacci retracement of the recent decline. From Friday’s close, such would entail a further rally of roughly 3-4% before the market runs into the broken 50-day moving average.

At that juncture, most of the oversold indicators will be back to overbought, and we could potentially see a reversal to retest the recent lows. There are a couple of reasons we suspect such will be the case:

There are a lot of “trapped longs” that will look to “sell” into the rally.

A reversal of the previous tailwinds from earnings and economic growth,to tighter monetary policy, liquidity and inflation.

As JP Morgan noted this past week:

‘Given the lack of strong capitulation, it is not yet clear whether this rebound should be any more than short-term and tactical in nature. In addition, how discretionary investors perform if there is a bounce could be critical. Given many captured a large amount of the decline, if they don’t capture most of the rebound, it could continue to create risks.” – via Zerohedge

As is always the case, nothing is a guarantee. But there is a crucial risk developing.

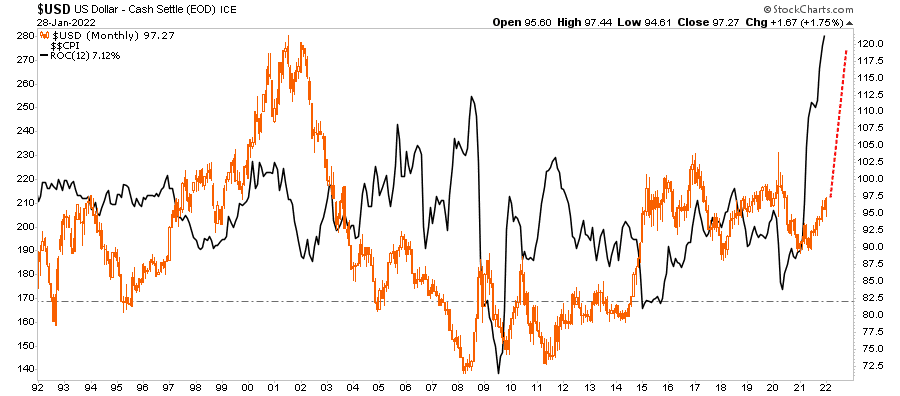

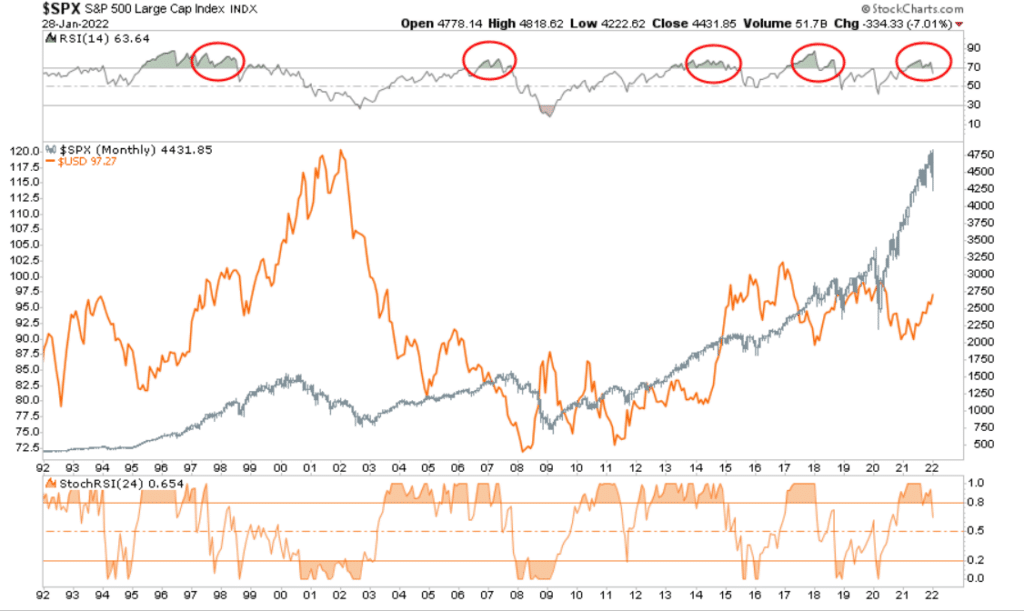

The Dollar Is Key

With inflation surging short-term due to the impact of massive floods of liquidity against a supply-constrained economy, such suggests that the U.S. dollar is just beginning to play catchup. Furthermore, with tensions rising between Russia and Ukraine, it will not be surprising to see global fund flows into U.S. Treasuries, which will push the dollar higher as a “safety trade” for global reserves.

Historically, a surging U.S. dollar undermines both the stock and commodity markets (per our discussion yesterday), as a strong dollar negatively impacts exports which comprise about 40% of corporate revenues.

With the markets extremely overbought, as shown below, such suggests that we could well be in the midst of a more significant correctional process. If such is the case, then we could be seeing a shift in market dynamics from “buying dips” to “selling rallies.”

As we have noted previously, there are more than just a few headwinds facing us in 2022.

The Fed is reversing liquidity and tightening monetary policy.

Fiscal policy supports no longer exist.

Current inflation is impacting consumption

Economic growth is slowing dramatically (Atlanta Fed GDP Now at 0.1% for Q1)

Earnings growth will slow.

Profit margins remain under pressure from higher input costs and wages.

Valuations remain elevated

These challenges could lead to a more challenging investment dynamic this year.

But the Fed is likely the catalyst to the next correction.

The Fed Is Walking Into A Trap

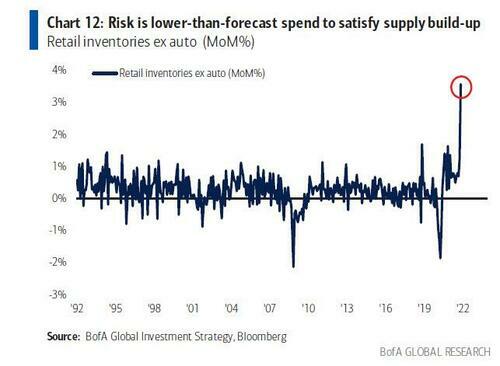

There are more than a few reasons why we believe that “disinflation” is a more significant threat in 2022 than inflation. With inventories surging and liquidity reversing, prices will fall as a supply glut occurs. As BofA noted recently:

“Inflation is annualizing 9%, and real earnings are falling to a recessionary 2.4%. Stimulus payments to US households are evaporating from $2.8tn in 21 to $660bn, and there is no buffer from excess savings with the rate at 6.9%, which is lower than 7.7% in 2019). There is a huge inventory build in retail products (ex-auto), while the upcoming weak US consumption most likely catalyst for consensus cuts in GDP/EPS.”

In a simple word, this is very “deflationary.”

However, the Fed intends to hike rates to combat an inflationary surge that has most likely peaked. If such is the case, the Fed is walking into the same trap as before. Notably, the Fed probably won’t be able to hike more than 1% before creating the next crisis.

For all of these reasons, we agree that a short-term bottom may be in as it is “hard to kill a bull market.”

However, investors should use rallies to rebalance risk and take on a more cautionary posture as we head into 2022.

Will there be a time to “start loading up the truck” again? Yes.

“But after a lot more pain, the time to buy will come, and that’s usually marked by the transition from panicking stock markets to panicking Fed officials.” – BofA

I’ve just finished up a rough draft of my The Right to Defy Criminal Demands article, and I thought I’d serialize it here, minus most of the footnotes (which you can see in the full PDF). I’d love to hear people’s reactions and recommendations, since there’s still plenty of time to edit it. You can also see all the posts here.

[* * *]

Criminals create risks for society—risks for their intended targets, and risks for bystanders. By defying criminals’ demands, the criminals’ victims may anger the criminals, and the criminals may respond by retaliating in ways that harm third parties.

Yet the law ought not in effect help criminals implement their demands by imposing liability on the defiant victims. People must have the freedom to refuse to obey such demands, even when the refusal creates some extra risk.

Free citizens have a legal obligation to obey the law. But they shouldn’t have a legal obligation to obey criminals. Kipling was dealing with limits on kings when he wrote of

Ancient Right unnoticed as the breath we draw—

Leave to live by no man’s leave, underneath the Law.

Yet the same is equally true of living by no criminal’s leave. Giving criminals’ demands legal effect undermines their victims’ dignity, precisely because it subjects people not only to the democratically endorsed coercion of the Law but to the arbitrary tyranny of the criminal. And it undermines the Law’s rightful claim to be the one authority that may use the threat of violence to set the rules of behavior.

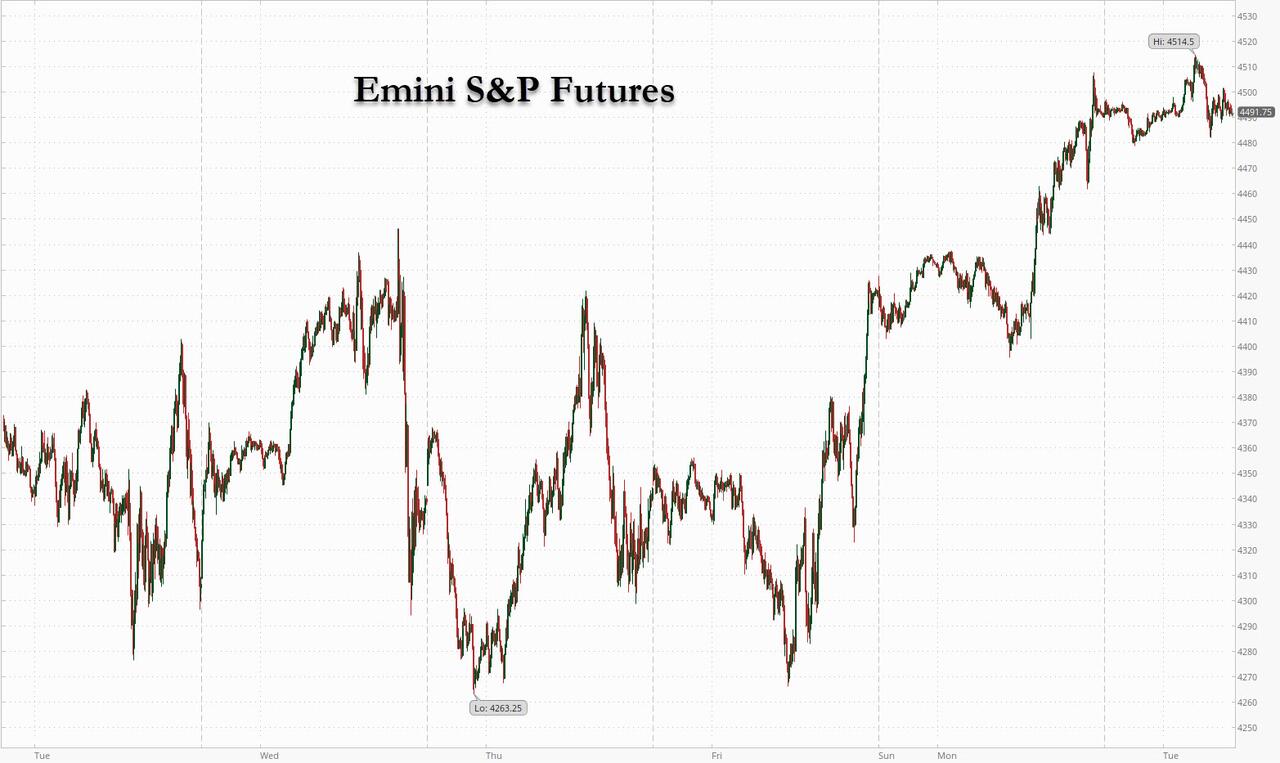

Futures Reverse Gains As Nail-biting Volatility Enters February

World stocks began the new month on firmer ground, after a volatile January, as reassuring comments from Federal Reserve officials helped to calm rate-hike jitters even though US futures failed to extend recent gains. After closing out January with a furious two-day, dip-buying meltup thanks to a flood of inbound month-end rebalancing, US index futures briefly traded through Monday’s highs, backed by decent rally in European equities where financials outperformed, boosted by solid UBS earnings, before dipping lower as the volatility seen in past days lingered. At 7:00am ET, emini S&P futures traded 0.23%, or 10.5 points lower, Nasdaq futures were also red, some 31 points or 0.15% lower, and Dow futures dropped 0.2% as investors weighed cautious rate-hike commentary from Fed officials and awaited earnings from firms including Alphabet and General Motors. Treasuries climbed and the dollar weakened. Oil fell, but held close to seven-year highs.

Videogame makers were in focus after Sony said it will buy Bungie, the developer behind the popular Destiny and Halo game franchises, for $3.6 billion. In another busy day ahead for earnings, AMD rose in premarket trading amid expectations its results Tuesday will show market-share gains. Other notable premarket movers:

UPS (UPS US) rose 7.3% premarket as the postal firm benefited from higher prices and rising holiday deliveries to post profit that beat analyst estimates.

Spire (SPIR US) shares gain as much as 27% in premarket trading after the satellite-imaging and data company released preliminary 4Q numbers ahead of analysts’ targets and guided toward higher 2022 revenue.

Harley-Davidson (HOG US) shares have valuation support at current levels, while the market appears to be pricing in an overly negative outlook, Morgan Stanley writes, upgrading stock to equal-weight. Shares up 0.8% premarket.

Knightscope (KSCP US) declines 14% in premarket trading, set to come down from a high reached on Monday as retail investors piled into the security-camera and robotics company, tripping two trading halts along the way.

Earnings season has provided a healthy breadth of beats so far: of the 182 companies in the S&P 500 that have reported earnings so far this season, more than 82% have beaten or met,

“Investors continue to buy the dips almost everywhere this week, with market sentiment boosted by a strong earning season so far where most companies have beaten expectations,” says Pierre Veyret, technical analyst at ActivTrades. “Technically speaking, most indices have registered solid rebounds over major support zones and are now challenging key resistance levels.”

In a jawboning fest on monday, four Fed officials said they’ll back interest-rate increases at a pace that doesn’t disrupt the economy, calming markets unnerved by previous hawkish messages from the central bank. Investors are now debating whether the rally that pared the worst monthly rout in the S&P 500 since March 2020 will continue. They are also focusing on earnings releases to gauge the strength of the economic recovery.

“Good news is that some Fed officials are finally out trying to soothe investors’ nerves saying that they still want to avoid unnecessarily disrupting the U.S. economy,” Ipek Ozkardeskaya, a senior analyst at Swissquote, wrote in a note. “But what will really make the difference is the quantitative tightening and given the steep rise in Fed’s balance sheet since March 2020, even halting the growth would be an abrupt change.”

In Europe, the Stoxx Europe 600 Index rose 1%, led by financial services and basic-resource stocks. UBS shares surged 6% after the lender beat estimates. Telecoms were the only industry group in red. European tech stocks rallied again, with the Stoxx Tech Index rising as much as 2.1%, among the top-performing sectoral gauge in Europe. Sector added to 3.5% gain Monday, lifted higher by overnight rally in the U.S., with the Nasdaq 100 Index +3.4%. Semiconductor makers and pandemic winners lead gains, with BE Semi +4.5%, Deliveroo +3%, ASMI +2.8%, ASML +2.6% and Just Eat Takeaway.com +2.8%. Here are some of the biggest European movers today:

UBS shares gained as much as 7.5% in early European trading, the biggest intraday gain since April 2020, after the Swiss lender posted largely better-than-expected results and analysts cheered the new financial targets.

HeidelbergCement shares rise as much as 4.7% after the company reported preliminary 4Q revenue that Stifel analyst Tobias Woerner says was “reassuring.”

Faurecia shares rise as much as 4.4% as the shares resume trading after being suspended all of Monday ahead of the closing of the Hella acquisition. The deal is a key milestone that allows the French auto parts firm to start implementing synergies, says Citi analyst Gabriel Adler (buy).

Ubisoft shares rise as much as 3.7% in positive readacross after Sony said it will buy U.S. video game developer Bungie for $3.6b. The acquisition indicates the sector is consolidating, says Citi (buy).

Hexagon shares soar as much as 23%, the most since 2009, after it signs deal with a commercial truck maker to provide battery packs for electric heavy-duty vehicles.

Shares in U.K. clothing retailer Joules plunge as much as 34%, to the lowest since April 2020, after reporting that revenue and profit before tax for the 9 weeks to Jan. 30 fell short of the board’s expectations.

Saipem falls as much as 15%, extending Monday’s 30% plunge, as brokers including Mediobanca downgrade the oil drilling specialist after it warned on 2021 earnings and said it would hold discussions with creditors and shareholders for financing.

Earlier in the session, Asian stocks rose as the latest remarks from Federal Reserve officials helped ease fears of aggressive U.S. monetary tightening. The MSCI Asia Pacific Index added as much as 0.5%, with the information-technology and financial sectors providing the biggest boosts. Japan’s Keyence and Murata Manufacturing contributed most to the advance, with both releasing quarterly earnings results after market closed in Tokyo. Equity gauges in New Zealand and India led gains, with many markets in the rest of Asia shut for holidays. China, Hong Kong, South Korea, Singapore and Taiwan were among bourses closed for the Lunar New Year break. “Now that markets are finding calm, buying is kicking into individual stocks of companies that have reported solid earnings or are expected to,” said Shogo Maekawa, a strategist at JP Morgan Asset Management in Tokyo. Asian shares may extend gains if U.S. data this week on employment and ISM manufacturing don’t rattle the market, Maekawa added. Fed officials said they want to avoid unnecessarily disrupting the economy as they prepare to start raising rates, mitigating market concern over a 50 basis-point move in March. “You always want to go gradually,” Kansas City Fed President Esther George told the Economic Club of Indiana. Asia’s stock benchmark fell 4.4% in January, its biggest such drop since July, hit by concern that faster-than-expected U.S. rate hikes will cool the global economic recovery.

Japanese stocks pared large morning gains, with the Topix finishing little changed, as automakers slid. Chemical and machinery makers also dragged on the Topix, which wiped out a gain of as much as 1.3%. The Nikkei closed 0.3% higher, paring a 1.5% advance, with TDK and Shionogi the biggest boosts. Both gauges had risen about 3% over the previous two sessions. “There’s a lot of tussle between buyers and sellers due to month-end and month-start trading,” said Hiroshi Namioka, chief strategist at T&D Asset Management. “Shares of companies with robust earnings are being bought, but those without any specific leads to go on seem to be exposed to selling pressure.”

Indian stocks rose after the annual federal budget pledged to step up spending in a bid to support a business recovery in Asia’s third-largest economy. The S&P BSE Sensex climbed 1.5%, its biggest advance in a month, to 58,862.57 in Mumbai. The NSE Nifty 50 Index rose 1.4%. Fifteen of the 19 sector indexes compiled by BSE Ltd. rose, led by a gauge of metal stocks that jumped the most in six months. Finance Minister Nirmala Sitharaman’s strong push for infrastructure-led growth and investment centered around sectors like railways, roadways, logistics and energy will benefit most metal companies, according to Priyesh Ruparelia, a vice president at ICRA Ltd. A measure of capital goods companies also jumped the most in a year. The nation plans to boost capital spending by 35% to 7.5 trillion rupees ($100 billion) in the next financial year that starts in April in a bid to sustain a recovery in growth disrupted by the pandemic. “With growth-oriented focus intact in the budget, we expect economic and capital market buoyancy to remain,” said Vijay Chandok, managing director at ICICI Securities Ltd.

Waves of volatility have swept across markets after the Fed signaled swifter monetary-policy tightening to curb inflation than many had expected. Investors need to “get used to this up and down volatility” as there’ll likely be more of it, Nancy Davis, chief investment officer at Quadratic Capital Management, said on Bloomberg Television.

In rates, Treasuries bull flattened as spreads unwound a portion of Monday’s steepening move with yields richer by up to 3.5bp across long-end of the curve. US Treasury yields were richer by 2bp to 3.5bp across the curve with 2s10s, 5s30s spreads both flatter by almost 1bp each; 10-year yields around 1.75%, with bunds lagging by 1.5bp and gilts outperforming by 1bp in the sector. In European bonds, focus remains on the front-end of the curve as rate hike premium continues to build — German 2-year yields are cheaper by almost 4bp on the day, trading above the European Central Bank’s deposit rate for the first time since 2015. Gilts outperform in early London session. IG dollar issuance slate includes Kommuninvest $1b 2Y SOFR; two companies priced $1.8b Monday as sales activity continues to drop off in volatile backdrop.

In FX, Bloomberg Dollar Spot index falls 0.3%. NOK, CHF and SEK outperform in G-10, CAD and euro lag. The Bloomberg Dollar Spot Index slumped as the greenback weakened against all of its Group-of-10 peers. Gains were led by the Swiss franc, which advanced a second day as it rebounded after adverse month-end flows; Scandinavian currencies were also among the top gainers amid supportive risk sentiment. The euro headed for a third day of gains, boosted by an unwind of the latest rally for downside exposure through options; the common currency rose by as much as 0.3% to 1.1269, raising questions on whether its latest weakness was more down to month-end flows rather than hawkish Fed bets. French inflation rose 3.3% from a year earlier in January, a sharper gain than the 2.9% economists estimated following December’s 3.4% advance. The pound rallied against a broadly weaker dollar, with domestic focus remaining on the Bank of England’s meeting this week. Figures showed U.K. house prices registered their strongest start to the year since 2005, before mortgage data due later Tuesday. The Aussie reversed an earlier loss after the RBA said it’s ready to be patient on interest rates even as it ceased its bond-purchase program. Overnight- indexed swaps continued to price in four rate hikes by the central bank this year. The Kiwi also advanced, in part on purchases against Aussie post RBA. Japan’s bonds extended a decline to a fourth day amid growing speculation that the central bank will step in to slow a rise in yields. The yen gained for third day.

Crypto markets were varied in which Bitcoin traded sideways around 38.5k and Ethereum gained over 2%.

In commodities, crude futures fade a sharp drop. WTI finds support near $87 before recovering back on to a $88-handle. Brent trades flat near $89.20. Most base metals trade in the green; LME nickel rises 1.3%, outperforming peers, LME lead and tin lags. Spot gold rises roughly $10 to trade near $1,807/oz

U.S. economic data slate includes January Markit manufacturing PMI (9:45am), ISM manufacturing, December construction spending and JOLTS job openings (10am); while AMD, Alphabet, Electronic Arts, Exxon, General Motors, Gilead, PayPal, Stanley Black & Decker, Starbucks and UPS are among companies reporting results.

Market Snapshot

S&P 500 futures down 0.3% to 4,490.00

STOXX Europe 600 up 0.8% to 472.72

MXAP up 0.4% to 185.38

MXAPJ up 0.3% to 606.58

Nikkei up 0.3% to 27,078.48

Topix little changed at 1,896.06

Hang Seng Index up 1.1% to 23,802.26

Shanghai Composite down 1.0% to 3,361.44

Sensex up 1.3% to 58,793.71

Australia S&P/ASX 200 up 0.5% to 7,006.04

Kospi up 1.9% to 2,663.34

Brent Futures down 0.9% to $88.45/bbl

Gold spot up 0.5% to $1,805.93

U.S. Dollar Index down 0.16% to 96.38

German 10Y yield little changed at -0.01%

Euro up 0.2% to $1.1258

Brent Futures down 0.9% to $88.45/bbl

Top Overnight News from Bloomberg

Money markets are wagering on the BOE raising rates five times by 25 basis points and a move of that magnitude from the ECB by December. That spurred a renewed selloff in bonds across the continent on Monday, and challenges ECB policy makers including President Christine Lagarde who have pushed back against the idea of raising borrowing costs this year

Euro-area manufacturers are taking a more aggressive approach to price setting — another signal that inflation won’t slow quickly after stronger- than-expected readings from the region’s biggest economies. Output prices rose at the second-fastest rate on record in January, according to a survey of purchasing managers by IHS Markit released Tuesday. While there were some signs of supply- chain problems easing, robust demand allowed firms to pass on higher costs to customers

German joblessness fell at a much faster pace than anticipated in January as the economy comes to terms with coronavirus curbs to contain surging infections. Unemployment in Europe’s largest economy declined by 48,000, pushing the jobless rate down to 5.1%. Economists had forecast a drop of just 6,000

European natural gas prices plunged after Russian shipments via a key route crossing Ukraine rebounded. Futures slumped as much as 9.1% as deliveries into Slovakia through the Velke Kapusany interconnection point on the border with Ukraine returned to normal levels, according to data from grid operator Eustream

Russian President Vladimir Putin meets Tuesday with Hungarian leader Viktor Orban, his closest friend in the European Union, as Western countries continue their diplomatic press to deter Moscow from attacking Ukraine

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were positive but with upside limited amid mass holiday closures for the Lunar New Year. ASX 200 (+0.5%) rose above 7,000 with the index further underpinned as the RBA stuck to a dovish tone. Nikkei 225 (+0.3%) was kept afloat after lower unemployment although retraced gains as JPY strengthened. Nifty 50 (+1.4%) outperformed as focus in India centred on earnings and the budget announcement.

Top Asian News

Europe Is Losing Nuclear Power Just When It Really Needs Energy

Winners and Losers in India’s Budget Aiming to Bolster Growth

Widespread Bullying, Harassment Detailed in Rio Tinto Report

India Plans Record Borrowing to Fund Modi’s Growth Ambitions

European bourses are firmer taking impetus from the holiday-thinned APAC handover and Monday’s US close; albeit, benchmarks are off best levels, Euro Stoxx 50 +1.0%. Sectors are all in the green though Telecom lags while Basic Resources, Banks and Tech do well amid base metals, UBS (+7.0%) earnings and the NQ/NXPI read-across respectively. Stateside, US futures are relatively contained but have moved directionally with European peers, the NQ remains the current modest outperformer.

Top European News

U.K. Mortgage Approvals Rise to 71k in Dec. Vs. Est. 66k

Slovenia Mulls Law on Swiss-Franc Loans Slammed by Lenders, ECB

Europe Is Losing Nuclear Power Just When It Really Needs Energy

In FX, DXY sheds more Fed rate hike premium and month end rebalancing momentum. Franc rebounds firmly as yields recede and SNB President Jordan sets sights on keeping track of inflation. Sterling underpinned by risk appetite and firm UK macro releases. Kiwi turns table on Aussie after encouraging NZ trade data and RBA pledges patience on tightening after confirming removal of QE. Rouble on front foot ahead of call between Russia’s Foreign Minister Lavrov and US Secretary of State Blinken, but Lira lurching after Turkey’s manufacturing PMI slows to the brink of stagnation. BoJ is under less pressure to shift yield target than market thinks, sources cited by Reuters say. Sources say the central bank has many tools to combat rising yields; BoJ currently prefers market operations.

In commodities, WTI and Brent are pivoting the mid-point of ~USD 1.50/bbl ranges that have seen a test of yesterday’s trough for Brent at worst thus far. Total OPEC+ production was lower by 824k/BPD than the required production in December, via JTC cited by Energy Intel’s Bakr; overall compliance in December was 122%. Goldman Sachs, on OPEC+, sees growing potential for a faster ramp-up, given the pace of the recent rally and likely pressures from importing nations. Spot gold/silver are firmer picking up from the pressure seen in recent sessions. Though, gold remains near the USD 1800/oz mark and as such the 200-, 100- & 50-DMAs. The German government has insisted in talks with Western partners that any sanctions on Russia would allow a loophole for it to continue buying energy from Russia, according to WSJ sources.

US Event Calendar

9:45am: Jan. Markit US Manufacturing PMI, est. 55.0, prior 55.0

10am: Dec. JOLTs Job Openings, est. 10.3m, prior 10.6m

10am: Dec. Construction Spending MoM, est. 0.6%, prior 0.4%

10am: Jan. ISM Manufacturing, est. 57.5, prior 58.7, revised 58.8

10am: Jan. ISM Employment, est. 53.0, prior 54.2, revised 53.9

10am: Jan. ISM New Orders, est. 58.0, prior 60.4, revised 61.0

10am: Jan. ISM Prices Paid, est. 67.0, prior 68.2

DB’s Jim Reid concludes the overnight wrap

Since it’s the start of February today, we’ll shortly be publishing our monthly performance review looking at various financial assets for the month just gone. Undoubtedly the main theme in January was the continued hawkish pivot by a number of central banks in light of continued and persistent inflationary pressures, which led investors to price in a much more rapid hiking cycle over the months ahead. This was particularly the case from the Fed, where futures are now pricing in around two additional 25bp hikes in 2022 relative to the start of the month. That meant that multiple asset classes including equities, credit and sovereign bonds all lost ground, though oil was a notable exception amidst rising geopolitical tensions between Russia and the West over Ukraine. Full details in the report out shortly.

That theme of growing conviction in the likelihood of tighter monetary policy was evident in yesterday’s session too, where investors continued to dial up the probability of numerous rate hikes taking place this year. In fact, we crossed a number of fresh milestones yesterday, the biggest of which was that Fed funds futures priced in 5 full hikes this year for the first time at one point in trading, although by the close that had fallen back a tad to 4.94 hikes. Bear in mind it was only 2 weeks earlier that futures had moved to price in 4 hikes by the December meeting, but they now see 4 hikes being complete by the September meeting, so you can get a sense of how quickly things are shifting here.

Speaking of the Fed, we had our first rush of post-communications blackout speakers yesterday, hearing from regional Presidents Barkin, Bostic, Daly, and George. It was a pretty good sampling of the ideological hawk-dove spectrum on the Committee, and didn’t do much to dissuade the market from its recent shift towards pricing a tighter policy path.

Without much in the way of incremental information, Treasury yields were relatively calm, as the 2yr yield rose +1.6bps, while the 10yr yield very little changed, increasing +0.7bps to 1.78%. This led to a modest flattening of the 2s10s curve yet again, which closed beneath 60bps yesterday for the first time since October 2020. So still some way from inverting, but it was less than a year ago that the slope peaked at 158bps. Plus as we’ve been writing about recently, the 2s10s has historically flattened by an average of around 80bps in the first year during Fed hiking cycles since 1955. So it’ll be interesting to see how that plays out relative to the historic playbook assuming the hikes do start in March as anticipated.

Rising expectations about rate hikes led to a fresh selloff among sovereign bonds in Europe, where yields on 10yr bunds were up +5.5bps to close in positive territory for the first time since May 2019, at 0.01%. And there was a similar move higher elsewhere, with yields on 10yr OATs (+5.7bps) at their highest since April 2019, and those on 10yr gilts (+5.8bps) at their highest since February 2019. The major outperformer were BTPs, who saw a more subdued +1.2bps rise following the move to re-appoint Sergio Mattarella as President, a move which will allow the continuity of the Draghi government.

In Asia this morning, a number of markets are closed due to the Lunar New Year holidays, including in China and South Korea. However, the Nikkei (+0.26%) is trading higher, with tech stocks leading the way following their outperformance on Wall Street. Separately, Australia’s S&P/ASX 200 (+0.49%) is up after the Reserve Bank of Australia held its cash rate at +0.1% following a monthly policy meeting. In line with the move in a more hawkish direction that we’ve been seeing globally, the central bank announced it would terminate its bond purchase program on February 10 and indicated not to raise rates until inflation is within its target band. However, the decision was a dovish one in other respects, with the RBA remaining vague about the timing of liftoff, and saying in their statement that ending bond purchases “does not imply a near-term increase in interest rates”, and reiterating their message that they won’t raise rates “until actual inflation is sustainably within the 2 to 3 per cent target range.”

In terms of other economic news, the January manufacturing PMIs have begun to come out in Asia, with Japan’s (55.4) and Australia’s (55.1) readings both in expansionary territory. Otherwise, Japan’s labour market continued to show signs of progress in December, with the unemployment rate down to 2.7% (vs. 2.8% expected), while the jobs-to-applicant ratio improved to +1.16 in December from previous month’s +1.15. Looking forward, equity futures in the US are pointing to a weak start with those on the S&P 500 (-0.27%) moving lower.

Back to yesterday, and growing expectations of tighter monetary policy failed to stop further equity advances, with the S&P 500 advancing for consecutive days for just the second time this year, up +1.89%. Before you ask, there was a late afternoon rally in the New York session, but it was much smaller than in recent sessions, and the VIX fell -2.83ppts for the second straight session, down to 24.83. Nevertheless, that still leaves the index down -5.26% over January as a whole and marks its worst monthly performance since March 2020 at the height of the initial wave of the pandemic. Tech stocks were a particular outperformer yesterday, with the NASDAQ (+3.41%) recovering to avoid a -10% negative return for the month, having been on track for its worst monthly performance since 2008 before yesterday’s rally. Those gains were led by the megacap tech stocks, with the FANG+ index (+5.83%) seeing its best daily performance in over 10 months as all 10 companies in the index moved higher on the day. European indices put in a decent performance too, with the STOXX 600 up +0.72%.

In other news, the relentless march higher in oil prices continued, with Brent Crude (+1.31%) closing above $91/bbl for the first time since 2014, although this morning it’s since fallen back beneath $90/bbl again. As it happens, Brent ends the month as the top-performing asset in the main sample of our performance review, having achieved a gain of +17.33% since the start of the year. That comes ahead of the OPEC+ group’s meeting tomorrow in which they’ll make their latest output decision.

On the data side, the first look at Euro Area GDP in Q4 showed a +0.3% expansion (vs. +0.4% expected), though Italy’s Q4 growth came in slightly stronger than expected at +0.6% (vs. +0.5% expected). That’s a notable milestone for the Euro Area economy in that it’s the first quarter where GDP has exceeded its pre-Covid peak. Separately, the German inflation data for January showed the year-on-year number subsiding to +5.1% on the EU-harmonised measure, down from +5.7% the previous month and a second consecutive decline. However, that was still higher than the +4.3% reading expected, representing a big upward surprise, and our economists have lifted their 2022 headline CPI average inflation forecast to +4.2% in response (link here).

To the day ahead now, and data releases include the global manufacturing PMIs for January and the ISM manufacturing reading from the US. On top of that, there’s US construction spending for December and the JOLTS job openings for the same month. And over in Europe, there’s Germany’s retail sales for December and unemployment for January, France’s CPI for January, the Euro Area unemployment rate for December and UK mortgage approvals for December. Finally, today’s earnings releases include ExxonMobil, Paypal, UPS, Starbucks and General Motors.

AT&T Slides After Slashing Dividend, Unveiling Warner Media Spinoff

In a move that was widely anticipated by Wall Street, AT&T has just decided to cut its dividend to $1.1/share and spin off its Warner Media subsidiary, which will be merged with AT&T’s partner, Discovery.

Despite being widely expected – the company was trading at a ridiculously high dividend yield north of 8.2% – the decision sent AT&T shares sliding 2% in premarket.

Wall Street analysts generally see AT&T as a ‘buy’, although some have lowered their long-term price targets in recent weeks. AT&T reported earnings and sales that generally surpassed expectations for the quarter just last week.

CEO John Stankey said last week during the earnings call that he was unsure about whether to spin off Warner Media (which owns premium TV/streaming hitmaker HBO). But apparently, he has changed his mind as the blandishments of the 100% cash deal valued at $43 billion were simply too tempting to ignore – especially as the telco fights with Verizon for dominance in 5G, which is a capital intensive endeavor. The deal is the latest step by Stankey to unwind the expansionist legacy of his predecessor.

The firm’s decision to cut its dividend will also help it retain more of its money, which can be repurposed toward CapEx and growth.

Tesla Recalls Tens Of Thousands Of Vehicles On “Rolling Stop” Function, NHTSA Says

Following a massive recall in December, Tesla, Inc. recalls tens of thousands of more vehicles due to software issues that could put certain vehicles at risk of a fender bender.

According to the National Highway Traffic Safety Administration (NHTSA), Tesla recalls 2016-2022 Model S and Model X, 2017-2022 Model 3, and 2020-2022 Model Y because of the “rolling stop” feature in the Full Self-Driving (Beta) software may allow the car to automatically roll through an all-way stop intersection without coming to a stop.

NHTSA said this recall affected nearly 54,000 Tesla vehicles (various models listed above). The Austin, Texas-based company will perform an over-the-air software update to disable the “rolling stop” functionality.

Shares of Tesla fell around 1% premarket to $927. Last month, the stock plunged into a bear market, dropping as much as 34% but rallying on the last day of the month by a little more than 10%.

Tuesday’s recall follows December’s massive recall of 475,000 vehicles. The recall consisted of vehicles that could be prone to wiring harness damage and quality issues with the front truck (or, as some call it, a “frunk”).

Tesla has been plagued with countless quality control issues. Some owners have reported bumpers ripping off in adverse weather conditions, roofs flying off, and trim and paneling gaps, among many other defects.

… and it’s not just us reporting Tesla defects.

For example, Car and Driver lambasted Tesla over the summer. They said Tesla Model S, Model 3, and Model Y were “hampered by quality problems” and said, “the cruise control system on the Tesla Model Y abruptly stopped working with no warning.” Sharon Silke Carty, Car and Driver’s editor-in-chief, told CNN: “All of a sudden I was going 30 in the middle of the highway.”

CNet and Consumer Reports have also trashed the Model Y for quality issues.

In his bestselling new book, Woke Racism: How a New Religion Has Betrayed Black America (Portfolio), New York Times columnist and Columbia University linguist John McWhorter argues that the ideas of Robin DiAngelo, Ibram X. Kendi, and the Times‘ 1619 Project sharpen racial divides while drawing attention away from actual obstacles to improving quality of life for black Americans.

McWhorter first explored his idea of anti-racism as “Our Flawed New Religion” in a 2015 piece for The Daily Beast and continued the theme in a series of articles for Reason in 2020. “I think something is really distracting people in my world lately into supposing that they’re supposed to fall for a kind of purposeless extremism in order to be good people,” McWhorter says.

Contrary to critics’ vituperative claims, Woke Racism is in no way a right-wing book; McWhorter notes that he’s never voted Republican in his life. “I consider my company to be left-leaning people who read The New York Times and The Atlantic,” he says. “If it were 1960, everybody would think of me as a normal liberal. I would be this Adlai Stevenson–voting, pointy-headed liberal person.” Since the late ’60s, though, the idea has taken hold that “on race, radicalism is default.” Though this attitude has ebbed and flowed over time, McWhorter argues that today’s anti-racist crusaders evince a quasi-religious fanaticism that ends up hurting, not helping, the plights of black Americans.

In November, McWhorter spoke with Reason‘s Nick Gillespie about what white people get out of cooperating with this ideological agenda, what black people gain by “performing” victimhood, and what needs to change so that all Americans can get on with creating a more perfect union.

Reason: What’s the elevator pitch for Woke Racism: How a New Religion Has Betrayed Black America?

McWhorter: There is a group of people who are committed to what they call social justice, certain enough of their moral purity that they are willing to hurt other people if they don’t agree with their principles. Their notion is that they are saving people who are living under the power of white hegemony. Not only are these people mean and unpleasant to deal with, but in the name of social justice for black people, they often either don’t care about black people for real, or they’re hurting black people. I wrote Woke Racism not as some boring statement from the right wing about family values and people pulling themselves up by their bootstraps. This is a book saying there are black people who need help. The people who are calling themselves black people’s saviors don’t understand this. What they’re caught up in is more about virtue signaling to one another than helping people who actually need help.

We’re talking about woke activism—authors like Robin DiAngelo, Ibram Kendi, Ta-Nehisi Coates. Why is it important that you call it a religion?

I call it a religion partly because of formal similarities between it and especially devout Christianity, starting with white privilege as original sin. Not only are those parallels important, but I have a heuristic reason for it. Some people were expecting Woke Racism to be an examination of the nature of religion and wokeness and what the parallels are. Nobody would have read that book. They shouldn’t have; it’s not that important.

I consider it useful to think of this as a religion so that people can understand that we can’t have productive exchanges with the particular kind of person I’m writing about. Many people think, “Well, if we could only get them to understand that we need a plurality of ideas.” Or people ask me, “How can I get that kind of person to not call me a racist?” You can’t. That’s what they do.

You’re unlikely to try to convince somebody that Jesus does not love them; you’re unlikely to try to talk someone out of their religious faith. Framing it as a religion gets across that idea better than just calling it an ideology.

You critique terms such as systemic racism. Are we past the age of systemic racism?

Racism in the present tense is much harder to identify than racism in the past. I don’t like that term, not because of the systemic, but because of the racism. I think it’s a real stretch of our cognition to go from racism being an attitude to racism referring to inequities within a system that are racial. You end up talking about inequities that have a very different nature, and you refer to them all with the term racism, which implies that there’s this one particular issue. We can’t help thinking that it’s partly this emotion, this bias, when really the problems are often due to all sorts of things today, even if they were due to racism in the past. It’s a dangerously oversimplified way of looking at the complexities and the inequities in a society.

For example, redlining. Go back to a redlined neighborhood in 1950; most of the people in it were white. That’s something that we don’t talk about. Redlining was not as racially targeted as a lot of people seem to almost want it to have been. It was about class. Nevertheless, a vastly disproportionate number of black people were caught in these same neighborhoods, so black people suffered disproportionately from redlining. Is that the reason today that a certain wealth gap between white and black people exists? To some extent, yes. But if you actually look at the numbers, if you distinguish between medians and averages, if you distinguish between regions of the United States, if you distinguish between social class, the wealth gap is not what people say.

Certainly the fact that so few black people could build up equity back in the day, not that long ago, was a matter of racism. But today, to look at the wealth gap and say, “This is systemic racism”—no. That was way back in the past. Today, there’s inequity. What do you do about it? Do you give black people a certain amount of money? Do you give black people houses? How much of a house? How much money? It’s complicated. And that’s usually not really what people mean.

What are we talking about, that it is racism? That’s a very odd way of using tense. Racism did something that created a disparity today.

When you look at American culture in 1960 and 1970 on the issue of race, there was a massive transformation. Can you talk a little bit about that?

The two-parent family is still a norm [back in 1960], even with poor black people. Welfare is a mean-spirited little program where you’ve always got the social worker knocking on the door and you’re encouraged not to stay on it for very long. There’s a general idea that how Martin Luther King looked at things was the standard and reasonable way of thinking about race: “Let’s get rid of segregation, view people by the content of their character.”

You go to 1970 and there’s this whole new mood—the black power mood. The new idea is, “We can’t do our best because you won’t let us. And therefore you have to accept that we won’t do our best, and that sometimes we’ll do our worst.” Gradually the notion settles in that doing your worst or not doing your best is almost what black authenticity is, because you stand as a totemic demonstration of white racism. 1960s racism is about segregation. By 1970, it’s standard in certain circles that racism is still present and indestructable because it’s structural.

Because of the welfare revolution in 1966, it starts to become regular for people to just stay on welfare, with no one concerned about whether they get job training. The knocking on the door dwindles in the early ’70s, and it becomes this multigenerational program. It’s not anybody’s fault. Black America turned upside down between ’60 and ’70.

I think that civil rights up to about 1966 and [black activist] Stokely Carmichael and people yelling “black power” and not knowing what it meant—that’s where it went wrong. And we’re still stuck talking about these things the way those people did.

There’s fascinating changes in polling data about race and outcomes in American life. By the end of the Barack Obama years, there was much more racial animosity. According to Gallup and Pew, black people feel that racism has become a bigger issue in their lives, and a lot of white people agree. Do you give any credence to that narrative?

None whatsoever. Obama starts being president in 2009, and then comes the Tea Party, and everybody thinks that that’s mostly because of his race. But I always ask: If John Edwards, with his pretty boy white self but basically the same policies as Obama, had become president, would there have been no Tea Party? I don’t think it would have been any different. The Tea Party happened the way it did because in 2009 Twitter became default, as did Facebook. Those things completely changed the contours of our lives even more than cellphones did.

Then on the American race scene, two things happened: Trayvon Martin’s murder and Michael Brown’s murder. Those two things taught educated America and beyond that black people labor under the threat of being unjustifiably killed by stray or racist white cops.

The saddest thing in the world is that it’s become quite clear over the passage of time that the way both of those events were portrayed was complete myth. I was behind the people protesting both of those cases at the time. I now feel fooled, just like we all feel fooled by, bless his heart, Colin Powell. What happened to Trayvon Martin was not that he was killed unjustifiably by George Zimmerman. It was an unfortunate episode, but Trayvon Martin was also a very different person than we’re led to think. And then also with Mike Brown, it was a lie. For reasons we’ll never know, he kept on charging at that police officer. The idea that [the officer who killed Brown] just shot this guy dead with his hands up in the air—it’s false.

Barack Obama’s Justice Department, headed by Eric Holder, did an exhaustive investigation of the Michael Brown killing and came to the conclusion that you just articulated.

Yet the myth will never die.

The Brown incident did reveal a system of peonage that whole communities, particularly poor communities, often disproportionately black, were held under. You look at places like Ferguson, Missouri, where cops would give out huge numbers of tickets for speeding and other kinds of violations simply to gin up their own budgets.

Yeah, that was real. There are times when there’s a racial disparity where it really does need to have the whistle blown on it. Stop-and-frisk in New York City had gone way, way too far. I wrote about that often and made a lot of people mad. With Ferguson, you learned about how unjust policing in general and all the fines being levied were. But the thing is the level of fury, the level of property destruction, that happened in Ferguson was about Mike Brown. The level of destruction and fury was not about people getting a lot of tickets and spending a night in jail. There could have been a more constructive way of addressing those things.

If the only way that we can get at those real things is to tell a big lie, that’s really a sad way of looking at how sociopolitical change has to happen.

Is blackness as tight a category as it used to be? It was in the late ’90s that the U.S. census allowed a multiracial category for the first time without horrible motivations behind it.

There’s a certain kind of person who is hopelessly devoted to the idea that the essence of blackness is laboring under this oppression from whites. The reality is that those category memberships are going to have to fray. We come from a time when [mixed-race kids] had to accept as they got older that they were black in effect. And that made sense in 1975; there was less room to maneuver in the culture. That’s not true now.

Some people hearing me say that are thinking I mean that I don’t like blackness or that I’m ambivalent about it. But I just think that the category is beginning to not make sense. That includes my daughters. I don’t know if they, when they’re 40, are going to identify as black women, as opposed to just mutt women growing up in an upper-middle-class world, where everybody has a different flavor. What they’re basically becoming is modestly affluent American urban kids.

I worry these days that when people say blackness, what they mean is, roughly, not being buttoned up like Episcopalian whites. I worry that blackness is thought of as, roughly, jamming. I mean this as more than just dancing, but that there’s something that black people are in touch with in terms of rhythm. That blackness is not being too exact—we’re seeing that in so many educational materials. It runs throughout the culture that to be black is to not be precise, is to not be responsible for getting the exact answer. You have a rhythm; you jam. You don’t sit in one place; it’s about the beat. And I worry that [this sense of] blackness is primitive, you know?

The writer Christopher Lasch has a passage about how the term survivor slipped out of postwar narratives of people who survived death camps and gulags. By the end of the ’60s, Betty Friedan was talking about how being an affluent suburban housewife was a form of concentration camp; survivorship had gone from being specific to the Holocaust to more general. We’re in an age now where being a survivor—and making people around you aware of your trauma—seems to be how we talk about everything.

There were psychologists who started doing sessions between white people and black people, where white people’s responsibility was to sign on to the idea that they were creating what we’re now calling trauma among black people. And that lives on in [diversity, equity, and inclusion] initiatives. It starts out as a useful way to call attention to the fact that people are hurting. It’s an analogy. Somebody who’s been teased in school hasn’t suffered the way somebody did in the Holocaust, but you can say that both people are survivors. Once that settles in and people stop processing it as extreme, you do have this usage of the term—kind of like the way we use the term racism—that stops being terribly useful, and sometimes can be almost manipulative and destructive of a person.

In your book, you talk about ways to make things better for black Americans. You suggest three things: End the drug war, teach reading properly, and get past the idea that everyone should go to college.

If there’s no black market selling hard drugs on the street, you can’t drop out of school and do that. There’s no way to avoid getting some kind of legal work. And that’s not always going to be fun when you’re from an underserved community, because life is hard. If you’ve grown up somewhere where you aren’t taught well, and you aren’t taught how to do anything, you’ve got a problem. So not only do you end the drug war, because it destroys black communities by creating that black market temptation that sends people to prison and often to death, but then you also want to have something to catch those men. Those men should be caught in a system that cherishes and funds and values vocational education, with the idea being that he’ll learn how to fix air conditioners and heaters and make a thoroughly middle-class living for the rest of his life.

The idea that what that person needs to do after high school [is to] go spend four years “expanding their mind” in ways that frankly don’t much expand the mind—college is something that should be a choice for some people the way it was before 1945 and the G.I. Bill. I suspect what most people would rather do is go train for a career. If you want to go to college later in your life, that should be allowed, but it shouldn’t be considered the default rite of passage. I cringe whenever I hear anybody talking to an audience about poor people and saying that college needs to be made more available. No, vocational school needs to be more available!

Teach reading properly—how did you come up with that?

That sounds so wonky. It sounds like I must have some sort of particular commitment to pedagogy. It’s not that. Something that keeps kids, especially ones not from book-lined homes, from engaging with school is being taught reading wrong. It started with the whole controversy over whether Ebonics should be used in the schools in Oakland in 1997. If you were a part of that controversy, you learned about problems with reading that would lead anybody to think that the issue was black dialect. That wasn’t the problem.

You wrote a whole book showing that black dialect is a really effective form of communication.

I also wrote another book saying that black dialect is not the reason that poor black kids have trouble learning to read standard English. It’s that they weren’t being taught to read right at all. If you’ve got a good phonics program, you’ve got a kid who will not, at around 8 years old, turn away from school because they just find reading too difficult.

I’m not sure how many [readers of the book] have the experience of knowing somebody who’s about 25 years old, grew up the hard way. I’ve known black people like this; there are white people like it too—somebody where you’re at the restaurant and they’re moving their lips when they read the menu because, you know, menus are tough to read. Almost always, it’s somebody who went to a school where they basically just threw some kid books at them and had them take it in by osmosis. That’s not how you teach people how to read. It really worries me because, disproportionately, black kids suffer from that.

So I really do think: Have kids learn to read so they’re less likely to drop out of school. Then, when they leave school, no black market within the neighborhood. I completely understand why people would choose that, but that shouldn’t be available. What should be available is good, solid vocational training so that they can go out into the world and lead the kinds of productive lives that their grandfathers did. I’m modeling this on black communities in big cities in, say, 1949. That was no paradise by any means, but most black men worked legal jobs.

What are your rhetorical and discursive strategies for dealing with the “elect,” your term for social-justice activists?

There’s a certain kind of person who thinks that battling power differentials is supposed to be central to everything we do. The idea is that those power differentials exist, and until they don’t, everything else is fiddling while Rome burns. That kind of person, if you disagree with them, calls you a white supremacist.

There are two things that we have to do: One is we have to get used to being called that name and walking on, instead of thinking that [being] called a racist on social media stains us like Hester Prynne. And two, that kind of person needs to be told, “No.”

I think a lot of us, especially since June 2020 and [the killing of] George Floyd, have thought, when that person comes along talking about social justice and hegemony and intersectionality, and tells you that we’re going to change all of our procedures, and if you disagree, we’re going to call you names on social media or get you fired, that our job is to say yes.

The people calling for that need to be told no. They don’t need to be abused, but just: “No. We don’t agree with you that battling power differentials should be the center of our endeavor here. It will be one of about a dozen things that we do. It will not be the center. And if you don’t like it, you have to leave. And I don’t care what you call me.”

This interview has been condensed and edited for style and clarity. The full video version can be viewed here.

According to data compiled in a report by Stars & Stripes, US warships more than doubled their presence in the Black Sea in 2021 compared to the year before.

The report said US warships spent about 182 collective days in the Black Sea in 2021. Last year, Stars & Stripes reported that the US Navy spent 82 days in the Black Sea in 2020.

While the 2021 numbers were significantly higher than the previous year, they were still lower than 2014, when the US-backed coup in Kyiv led Russia to take Crimea. In 2014, US warships spent about 210 days in the Black Sea. But two years after the coup, the number was down to 58.

The recent increase of US and NATO activity in the Black Sea is viewed as a major provocation in Moscow and was part of the reason why Russia sent more forces to its bases in western Russia and on the Black Sea in Crimea, what the West portrays as a troop buildup along Ukraine’s border.

Still, defense pundits in think tanks tied to the US military establishment are arguing for a larger US naval presence in the Black Sea. Without it, they argue, “The result is an emboldened Russian President Vladimir Putin, who is orchestrating a stranglehold on Ukrainian ship traffic in the adjoining Sea of Azov and harassment of NATO ships in the Black Sea, said Foggo, now dean of the Arlington, Va.-based Center for Maritime Strategy.”

“He and other analysts say that regardless of the outcome of the current situation in Ukraine, the U.S. must take the lead in developing a NATO Black Sea strategy,” the report added.