Biden To Pitch Climate Agenda, Revival Of “Build Back Better” During First State Of The Union Address

Beginning at 2100ET on Tuesday, President Joe Biden will deliver his first State of the Union address (newly elected presidents don’t deliver a SOTU during the year in which they first take office). According to a summary of his planned remarks released by the White House Sunday night, it appears Biden appears to focus on domestic issues, while media reports have claimed that he will discuss the steps his administration has taken to sanction Russia.

On the domestic side, Biden’s main goal will be pitching a revival of his domestic agenda, which collapsed after Sen. Joe Manchin effectively killed Biden’s “Build Back Better” infrastructure plan in the Senate.

Some of the key issues raised in the outline include fighting inflation (or “reducing the cost of everyday expenses working families face”), the administration’s crackdown on corporate power and influence (or “promoting fair competition to lower prices, help small businesses thrive, and protect consumers”), helping revive America’s unions (“enacting the Protecting the Right to Organize Act”), raising the federal minimum wage to $15, and “a national comprehensive paid family and medical leave program”.

Citing sources from inside the White House, Bloomberg reported Monday that Biden plans to pitch his stalled climate legislation, framing it as “a way to battle inflation and save the average American family $500 per year”. Although convincing ordinary working Americans to care about climate change is certainly a tall order.

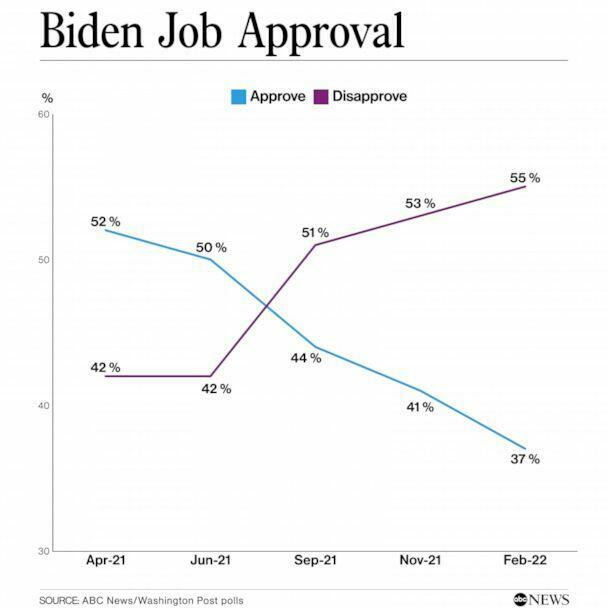

BBG also acknowledged that Biden is making his pitch at a time when his approval ratings have “dropped precipitously”. We noted the other day that, according to one popular poll (the ABC/Washington Post poll), Biden’s approval rating has fallen to a fresh all-time low of 37%.

On the climate change front, Biden’s claim that his green energy initiatives will save families money is based on calculations from “the Rhodium Group”. Biden also plans to discuss how $47 billion in climate change funding from last year’s infrastructure bill is being deployed.

The proposal comes after Biden’s sweeping Build Back Better economic package – which included tax credits for renewable power and clean energy manufacturing – stalled in Congress.

The administration’s estimate of savings is based on an analysis by the Rhodium Group last October that said clean energy tax credits, investments in efficiency and other changes necessary to pare U.S. greenhouse gas emissions will help consumers financially. According to Rhodium’s assessment, households would save roughly $500 a year in energy costs in 2030, under a mix of federal regulations, state actions and congressional legislation.

It represents a sop to climate activists, who have been pressuring the administration to frame the fight against climate change as something that could save American families money.

For years, environmental advocates have urged politicians to frame the fight against climate change as something that can yield big economic dividends. Biden will embrace that narrative in his speech, linking tax credits for renewable power and electric vehicles with household savings.

Circling back to Biden’s domestic agenda, it appears he plans to avoid using the word “inflation”, referring instead to “price increases” while he tries to revive support for his flagging domestic agenda.

On the Russia front, NPR reports that Biden plans to discuss the steps his administration has taken to threaten the financial stability of Russian President Vladimir Putin.

He’s also expected to talk about Judge Ketanji Brown Jackson, his pick to replace retiring Supreme Court Justice Stephen Breyer. Jackson is the first Black woman to be nominated to the country’s highest court.

Another aspect of his plan for fighting inflation is to make American industry “more competitive” in an effort to drive down prices (ironically, his agenda also includes plans to raise wages, which would likely have the opposite effect).

Here’s what the administration’s summary said about “promoting fair competition to lower prices”.

President Biden will explain that we can also lower costs by promoting fair competition in the U.S. economy. The Administration has taken decisive actions in the first year to stop the trend of corporate consolidation, increase competition, and deliver concrete benefits to America’s consumers, workers, farmers, and small businesses. He will also announce new actions the Biden-Harris Administration is taking this year to tackle some of the most pressing competition and consumer protection problems across our economy. Specifically, he will announce new steps to:

And in addition to paycheck fairness, Biden also plans to announce more assistance for low-income students trying to go to college.

Providing up to more than $2,000 in additional assistance to low-income students by increasing the Pell Grant award. President Biden will note that broad access to education beyond high school is increasingly important for economic growth and competitiveness in the 21st century, but also remind us that higher education has become unaffordable for too many families. Over 6 million students depend on Pell Grants to finance their education, yet the amount of money in these grants has not kept up with the rising cost of college and DREAMers still do not have access. During his State of the Union Address, President Biden will call on Congress to increase the maximum Pell Grant award by more than $2,000.

Finally, here’s what Deutsche Bank said about the State of the Union:

While not everything in the document will eventually become policy, it is a useful barometer of the administration’s current thinking. In short, Biden plans to champion the historically strong economic recovery while unveiling a plan to help slow inflation, which includes making American manufacturing jobs more productive and competitive, strengthening domestic supply chains, requesting legislation that reduces costs of health care, energy, and education, reducing the deficit, promoting competition, and eliminate barriers to jobs.

Biden is also reportedly expected to discuss his administration’s efforts to roll back COVID-inspired measures, like the CDC’s new masking guidance.

Republican Gov. Kim Reynolds of Iowa will deliver the GOP response to the SOTU, and Democratic Rep. Rashida Tlaib, a Michigan representative and member of the ultra-liberal “squad” will deliver a rebuttal from the progressive left, a new SOTU tradition of the Democratic party.

Meanwhile, here are what Biden voters thought were his greatest accomplishments over the last year…

Sell energy stocks? Such certainly seems counter-intuitive advice given high oil prices, geopolitical stress, and surging inflation. However, some issues suggest this could indeed be the time to “sell high.”

Before we go further, it is essential to state that I am not recommending selling energy stocks in total. As is always the case, portfolio management is about minimizing risk and preserving capital. Reducing energy exposure by selling portions of existing positions is more prudent.

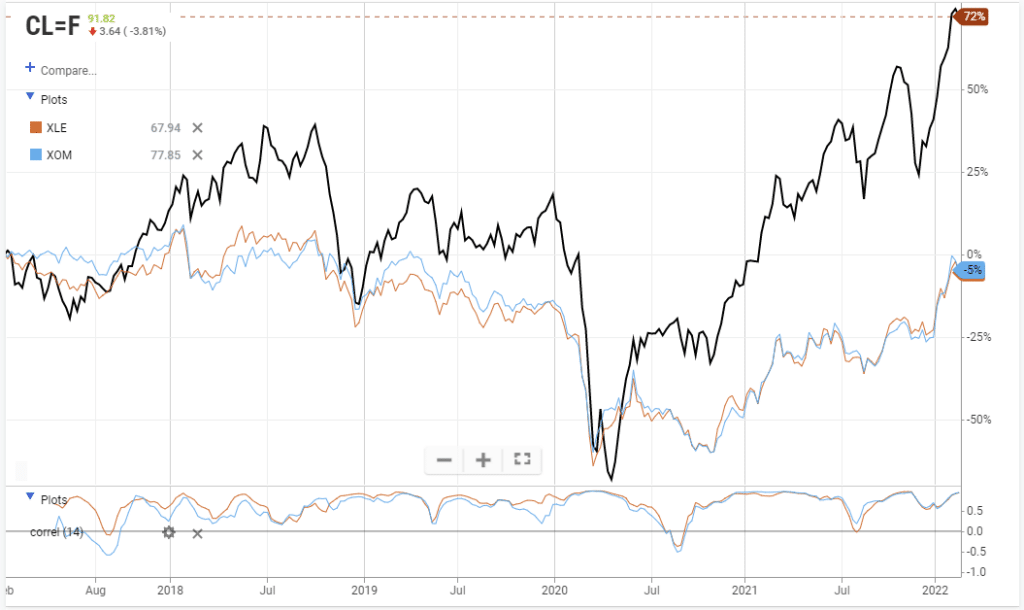

As shown, there is a high correlation between the price of oil, the energy sector as represented by SPDR Energy ETF (XLE,) and even oil stocks like Exxon Mobil (XOM.) Therefore, if oil prices decline, energy stocks will also. Profit-taking helps to preserve the accumulated gains.

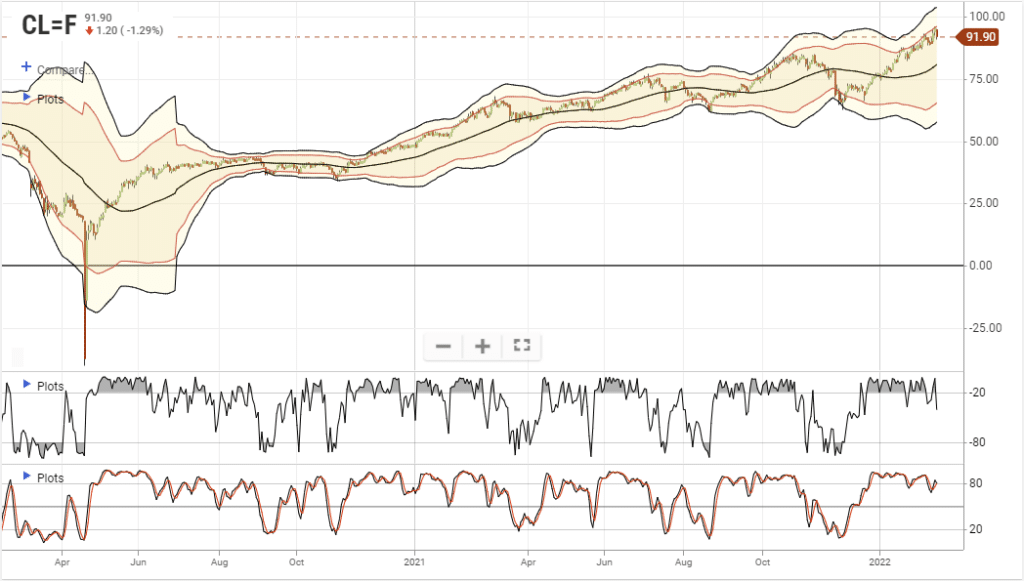

It is worth noting that while oil prices have surged sharply since 2020, oil stocks have not had the same recovery. Oil prices are pushing more extreme overbought conditions and are ripe for a correction back into the $70 range.

In an isolated environment, such a correction would provide an ideal opportunity to increase exposure to, rather than selling in its entirety, energy stocks.

We are concerned about other dynamics that could signal a more significant correction in the making.

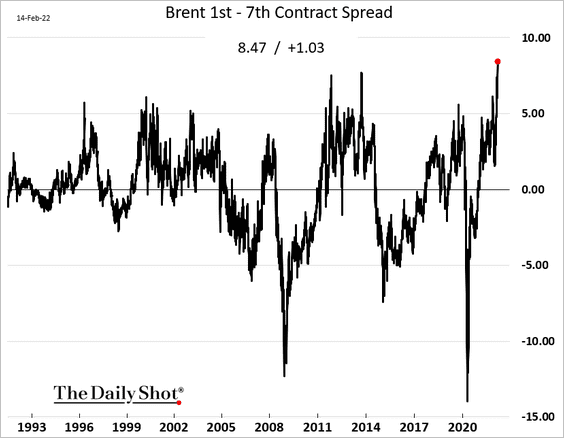

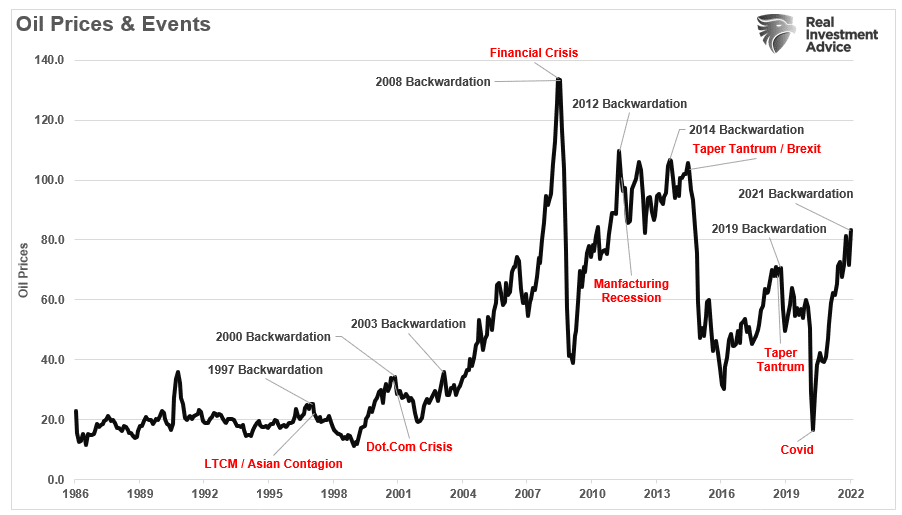

Backwardation

The first is “backwardation.”

Should a futures contract strike price be lower than today’s spot price, it means there is the expectation that the current price is too high and the expected spot price will eventually fall in the future. This situation is called backwardation.

For traders and investors, lower futures prices or backwardation is a signal that the current price is too high. As a result, they expect the spot price will eventually fall as the expiration dates of the futures contracts approaches.

Backwardation can occur as a result of a higher demand for an asset currently than the contracts maturing in the future through the futures market. The primary cause of backwardation in the commodities’ futures market is a shortage of the commodity in the spot market. Manipulation of supply is common in the crude oil market. For example, some countries attempt to keep oil prices at high levels to boost their revenues. Traders that find themselves on the losing end of this manipulation and can incur significant losses.– Investopedia

Currently, the backwardation in the Brent Crude market is at the highest level since 1992.

If we look at those peaks in backwardation, they align with previous peaks and more severe financial events.

Given the extreme level of backwardation currently, such suggests that considering a process to reduce oil-related risk (aka sell energy stocks) may be prudent.

However, it isn’t just backwardation we need to consider.

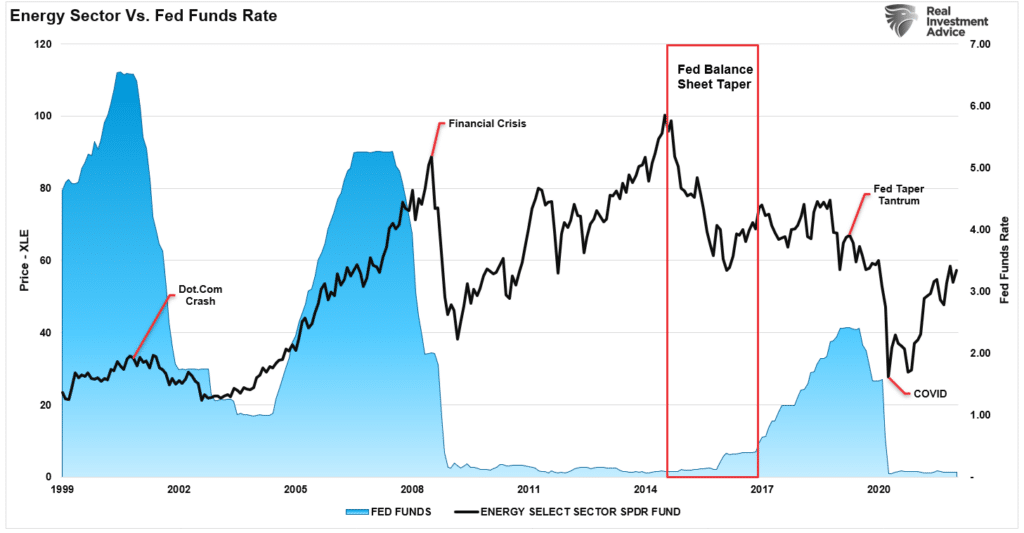

Fed Tightening

The surge in “artificial inflation” from the flood of liquidity against a supply shortage will eventually revert to a disinflationary trend. Debt and demographics will also continue to drive deflationary pressures leading to a reversal of the inflation trade.

However, for now, as the fear of inflation rose, investors piled into the commodity trade. While commodity prices rose due to the supply shortage, the reversal of that liquidity, and rebuilding of inventories, will ultimately undermine those assets. Such will coincide with a rather sharp decline in interest rates as deflation sets in.

Of course, slowing economic growth and deflationary pressures will contribute to the decline in oil prices. One of the things that could generate that environment, sooner than later, is the Federal Reserve tightening its monetary policy.

Historically, when the Fed has hiked rates or tapered its balance sheet, oil prices fall due to slower economic growth. Such should not be surprising since oil prices are a function of supply and demand.

While the recent rally in energy stocks has been quite strong, the Fed is about to aggressively tighten monetary policy with the sole goal of combating inflation. In other words, to bring down inflation, they will slow economic growth, which reduces demand for commodity-based products.

Unfortunately, I suspect it won’t be just oil prices and energy stocks that get brought down in the process.

High Prices

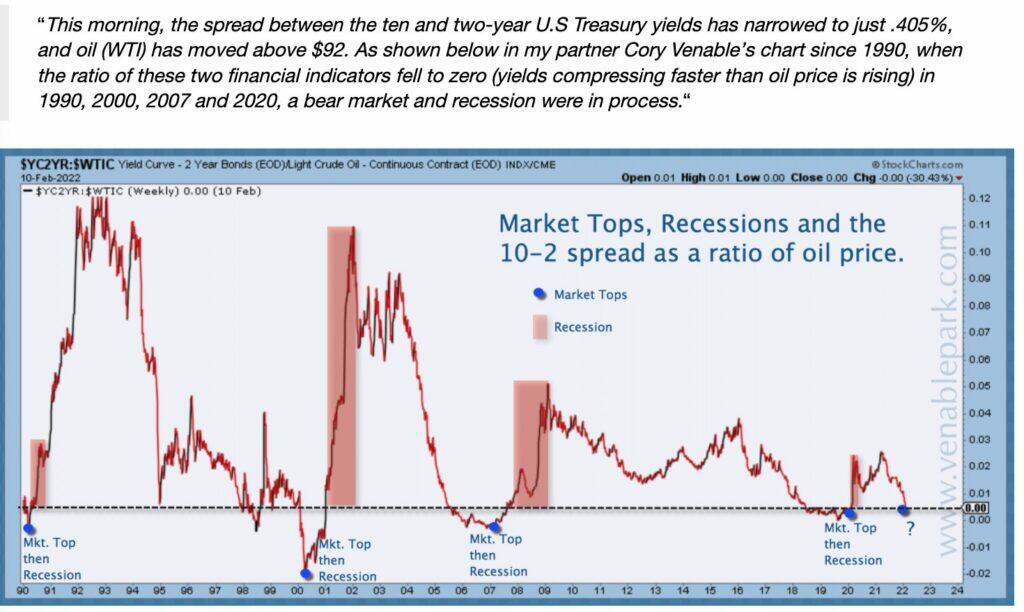

Lastly, the best cure for “high prices” in oil is “high prices.”

“The only way to balance this market over the medium term remains high oil prices to slow demand growth,” analysts at Energy Aspects via Bloomberg.

High oil prices do not exist in isolation. As oil prices, and other related commodities, increase in price, consumption will get negatively impacted. One of the indicators we continue to monitor is the yield curve. The chart below from Cory Venable shows the 10-2 yield spread as a ratio to oil prices.

The decline in the yield spread is enough to warrant caution about a rapidly slowing economy. However, combine already slowing economic growth with high oil prices and a Fed tightening monetary policy, and you have a perfect environment for a reduction of oil prices.

In other words, selling energy stocks to take profits may be a good idea.

Profit Taking Seems Prudent

When it comes to commodities and hard assets in general, they can be an exhilarating and profitable ride on the way up. However, as shown in the charts above, the trade ends badly.

Will this time be different? Such is unlikely to be the case for two reasons.

As shown by Goldman Sachs, inflation will reverse later this year.

Secondly, as the country moves toward a more socialistic profile, economic growth will remain constrained to 2% or less, with deflation remaining a consistent long-term threat. Dr. Lacy Hunt suggests the same.

Contrary to conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year-end and undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.

As he concludes:

The two main structural impediments to traditional U.S. and global economic growth are massive debt overhang and deteriorating demographics both having worsened as a consequence of 2020.

The last point is crucial. As the liquidity gets removed from the system, the debt overhang will slow consumption as incomes get diverted from productive activity to debt service. As such, the demand for commodities will weaken.

While the oil trade indeed “bloomed” with the rise of inflation and flood of liquidity in the economy, there is every indication we are very late into that trade.

For investors, selling energy stocks (taking profits) into current strength seems prudent.

A number of states have seen their pandemic-era eviction moratoriums morph from an emergency stopgap measure into institutionalized limits on evictions. Not Missouri.

The Show-Me State was one of just eight that did not adopt any eviction moratorium during COVID-19. Several state lawmakers are proposing to go further with a series of bills that would strip local governments and courts of their power to impose their own eviction bans.

“The bottom line is [eviction moratoriums] put landlords in an unfair situation. We talk a lot about government or bureaucratic agencies picking winners and losers. And I certainly felt like that that was done unlawfully,” said Rep. Chris Brown (R–Kansas City) according to the St. Louis Post-Dispatch, which first reported on the bills Friday.

The county circuit courts that cover Kansas City and St. Louis, Missouri’s two largest cities, both adopted their own local eviction moratoriums during the early months of the pandemic. Those were soon replaced by the federal eviction moratorium issued by the Centers for Disease Control and Prevention (CDC) in September 2020.

When the U.S. Supreme Court struck down the CDC eviction order in August, the St. Louis County Council responded by passing its own weekslong eviction moratorium. It re-upped this eviction ban for a few weeks in December in response to a rise in cases caused by the omicron variant.

Brown’s legislation, House Bill 1682, would specifically ban courts from suspending eviction proceedings of their own initiative without authorization from a state law. Another house bill sponsored by Rep. Jim Murphy (R–St. Louis County) would likewise forbid localities from banning evictions without the state Legislature’s approval.

These bills have received a negative reaction from some Democratic legislators and progressive activists.

In written testimony on Brown’s bill, Sarah Owsley, policy and advocacy director for Empower Missouri, credited eviction moratoriums with saving lives during the pandemic and preventing large numbers of out-of-work renters from losing their homes.

Like most pandemic mitigation measures, it’s not clear how effective eviction moratoriums were at preventing COVID-19 cases and deaths. Widely circulated studies showing a massive lifesaving effect of eviction bans have been roundly criticized as flawed and sloppy.

Oft-repeated predictions that the country would see an unprecedented “eviction tsunami” in the absence of moratoriums have also not played out. Evictions ticked upward after the CDC’s eviction order was struck down. But they remain below pre-pandemic averages almost everywhere in the U.S., including Missouri.

Even places that were desperately slow at distributing federally funded rental assistance did not experience an eviction spike.

Owsley argues in her written testimony that eviction moratoriums are rare policies that can be necessary for “weather and health emergencies.”

Prior to COVID-19, that is how eviction moratoriums operated. Their history during the pandemic suggests that eviction bans can also be incredibly sticky policies that, once imposed, are hard to back away from. The federal eviction moratorium was extended five times before it was finally struck down by the Supreme Court.

Missouri’s eviction legislation is part of a trend. As Reason‘s Eric Boehm has reported, lawmakers across the country are proposing and passing legislation that limits the emergency powers of governors and public health officials. Too often during the pandemic, these legislators argue, executives used those emergency powers to place extreme and persistent limits on business owners’ property rights.

That includes landlords, who were often forced by eviction moratoriums to provide effectively free housing to unscrupulous or even abusive tenants long after the immediate emergency of COVID-19 had faded.

By requiring the state Legislature to sign off on any moratorium, Missouri’s proposed ban on eviction bans will make that a little harder to get away with come the next emergency.

Ukraine Sells $277 Million In War Bonds, To Pay Interest For Other Creditors

Amid the fog of war, Ukraine raised 8.1 billion hryvnia ($277 million) in a sale of war bonds on Tuesday yielding 11%, in the country’s latest fundraising effort to tap into the global support for the country in its fight against Russia’s invasion.

The Ministry of Finance has placed military bonds worth UAH 8.1 billion.

As Bloomberg reports, the sale “encountered difficulties” that made it complicated for investors to buy, including a Ukraine finance ministry website which had cut off access from abroad to avoid cyber attacks. Furthermore, concerns over the settlement process for the bonds and the lack of information meant that some international bond funds remained on the sidelines.

On social media before Tuesday’s bond auction, users were asking the Twitter account of Ukraine’s finance ministry how to buy the bonds. Others pointed to alternative avenues for donations, such as the special central bank account.

Ahead of the emergency bond sale, Ukraine had been pursuing various crowdfunding initiatives, including collecting donations via bitcoin. Its central bank set up a special account last week where people around the world can donate, and the government shared details of crypto addresses to raise funds in Bitcoin and other digital tokens. By Tuesday morning, those accounts had received more than $17 million, according to blockchain analytics firm Elliptic. Including NGOs providing support to the military, total donations amount to $24.6 million, it said.

However, those hoping that the new funds will reach Ukraine’s suffering people, or even its military, will be disappointed: the only “winners” from today’s bond auction are other, existing creditors: shortly after the bond sale was completed, the country’s debt chief Yuriy Butsa told Bloomberg TV that Ukraine has paid about $300 million of bond interest to international investors due today, in effect recycling the entire new bond issue to avoid default. The bonds, which carry a 7.75% coupon, were issued in 2015 as part of Ukraine’s $15 billion debt restructuring, not to be confused with the debt restructuring that will have to follow in a few months when the country has no choice but to default on external creditors.

The account tracks the movements of some of Russia’s wealthiest businessmen, informing account followers of when and where their aircrafts take off and land along with a short summary of flight information, such as the location and duration of each trip.

The automated feed posted its first tweet on Sunday, the same day that the United States sanctioned two of Russia’s state-owned banks, the country’s sovereign debt, and elites with close ties to Putin.

Prior to the Biden administration’s sanctions, German Chancellor Olaf Sholz announced a freeze on the Nord Stream 2 pipeline, which would carry 55 billion cubic meters of natural gas from Russia to Germany each year.

Yet despite multiple sanctions from the West meant to financially cripple Russia’s elite, Sweeney’s account shows that many of them are still jet-setting across the globe in private planes.

So far, Sweeney’s account is tracking the Russian billionaire and businessman Roman Abramovich; a former scientist turned industrial magnate, Alexander Abramov; and the president of aluminum manufacturing giant Rusal, Oleg Deripaska.

The businessmen have traveled everywhere from Germany, the United Arab Emirates, Russia, and England in recent days, despite the UK’s Prime minister Boris Johnson announcing that the country has banned all Russian aircraft from entering UK airspace as part of its “largest-ever” package of sanctions against Russia in the wake of its invasion of Ukraine.

The ban pertains to aircraft on a scheduled service which is, “owned, chartered or operated by a person connected with Russia, or which is registered in Russia” according to Johnson’s announcement.

Yet data from Sweeney’s account shows that industrial magnate Alexander Abramov landed in London, England, on March. 1.

— Russian Oligarch Jets (@RUOligarchJets) March 1, 2022

In response to the UK’s ban on Russian planes entering the country, Russia’s civil aviation authority, Rosaviatsiya, has banned all flights by UK airlines to the country as well as transit flights.

Sweeney has also created a second account to monitor the private jets of president Putin himself but warned on Twitter that the account, called “Russian VIP & Putin Jets,” might not be as accurate because “there are a dozen VIP Russian planes and ADS-B coverage isn’t great in Russia.”

ADS-B stands for automatic dependent surveillance-broadcast and broadcasts information about an aircraft’s GPS location and altitude, among other things, enabling it to be tracked.

Sweeney made headlines last month when he created a Twitter account called “Elon Musk’s Jet” which tracked the businessman’s movements in his private plane through air traffic information gathered by bots.

However, the freshman at the University of Central Florida was promptly told to take down the account by Musk due to security risks.

While Musk initially agreed to Sweeney’s offer to remove the account if Musk paid him $50K, the Tesla chief later went back on the offer and allegedly blocked the teenager on social media.

Undeterred, Sweeney told The Epoch Times that he planned to launch a business called Ground Control to monitor the flight activity of private jets owned by other high-profile people, this time for a profit.

The Little Known Ukrainian Industry That Threatens To Make The Global Semi Shortage Far Worse

Right about the time the world was hoping to rise out of a semiconductor crisis, we’re learning that the conflict in Ukraine could plunge the world further back into a chip shortage.

Little known companies like Ukraine’s Cryoin play large roles in the global production of semiconductors, Wired noted this week. Cryoin, for example, makes the neon gas used to power lasers that make patterns on chips.

It supplies to the U.S., Europe, Japan, Korea, China, and Taiwan – and the ripple effects of disruption in its supply “can be felt around the world,” the report says.

Business development director Larissa Bondarenko told Wired that production came to a halt after Russia’s invasion last Thursday. “We decided that [our employees] should stay at home for the next couple of days until the situation is clearer, to make sure that everyone is safe,” she said.

She has said there’s no damage to the facility as of yet. “Cryoin has enough supplies to keep production going until the end of March,” the report says.

Bondarenko says the plant had planned to re-open but “missiles over Odesa”, where it is headquartered, meant that it was still too dangerous. She said she has been sleeping in her basement in her home, which is 30 minutes away. “Thank God we have one in our house,” she told Wired.

Lita Shon-Roy, president and CEO of TechCet noted that Ukraine’s neon industry was first set up to take advantages of gasses produced as a byproduct of Russian steel manufacturing.

“What happens in Russia is that those [steel] companies that have the facility to capture the gas will bottle it and sell it as crude. Then someone has to purify it and take out the other [gases] and that’s where Cryoin comes in,” she said.

“There were delays in shipments because of border crossing issues,” she said, talking about Russia’s annexation of Crimea in 2014.

She concluded: “The drive behind increased production is so strong that it is causing strain in the supply chain everywhere, even without a war. So there is no excess supply of this kind of gas that I know of, not in the Western world.”

Triggered by the Russian invasion of Ukraine, a range of sanctions against Russia by a range of countries have been rolled out. Many of these sanctions focus on the financial and economic realm.

Russian bank assets in UK to be frozen, totally shutting off its banking system from UK finance markets

ban on Russian state-owned and key strategic private companies from raising finance on the UK financial markets

punitive new restrictions on trade and export controls against Russia’s hi-tech and strategic industries

As regards financial institutions, the UK Foreign Office said that it will “freeze the assets of all Russian banks including a full asset freeze on VTB, Russia’s largest bank.”

Russian companies will be prevented from borrowing and raising finance on UK markets (i.e. banned from issuing transferable securities and money market instruments in the UK), while designated (sanctioned) banks will be prevented from accessing Sterling and clearing payments through the UK.

“target the core infrastructure of the Russian financial system – including all of Russia’s largest financial institutions and the ability of state-owned and private entities to raise capital – and further bars Russia from the global financial system. The actions also target nearly 80 percent of all banking assets in Russia.”

This includes sanctions targeting Russia’s two largest banks, Sberbank (which according to the US treasury is “the largest financial institution in Russia and is majority-owned by the Government of Russia”) and the aforementioned VTB Bank, the goal being to block Sberbank’s and VTB’s global foreign exchange transactions and prevent these banks using correspondent banks around the world.

The US Treasury sanctions also specifically target a range of additional Russian financial institutions, namely, Bank Otkritie (Russian state-owned), Novikom (Russian state-owned), and Sovcombank (privately owned), Alfa Bank (privately owned), and Credit Bank of Moscow (privately owned), and in addition prohibit a total of 13 Russian financial institutions from raising new debt or equity capital on US financial markets.

Furthermore, the US sanctions also target 11 Russian corporate entities which have been identified as being Russian Government owned. These entities including Sberbank (again), Gazprombank, Gazprom (natural gas producer), Gazprom Neft (oil producer and refiner), Transneft (Russia’s network of petroleum-related pipelines), Rostelecom (telecommunications), and Alrosa (diamond mining).

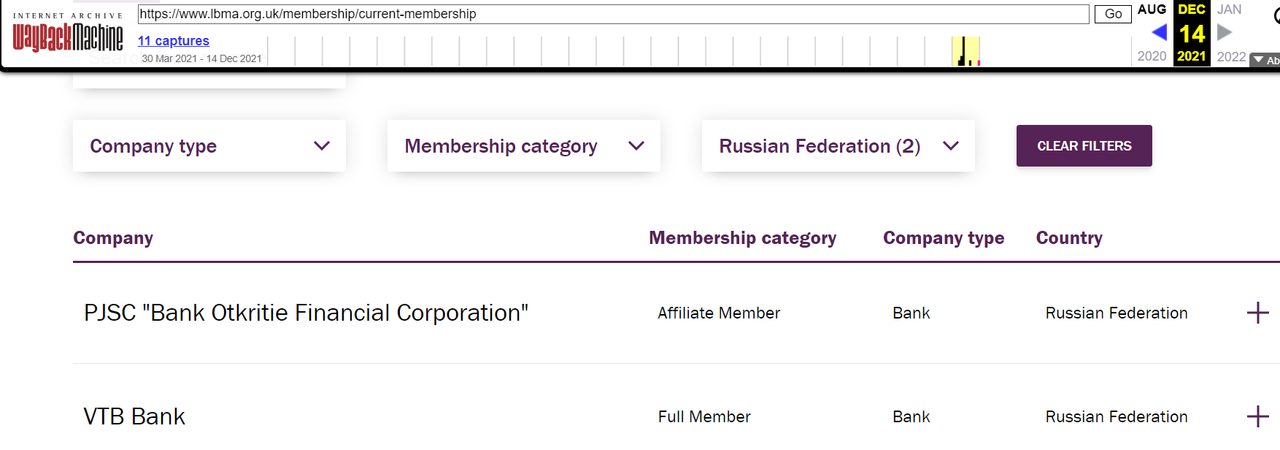

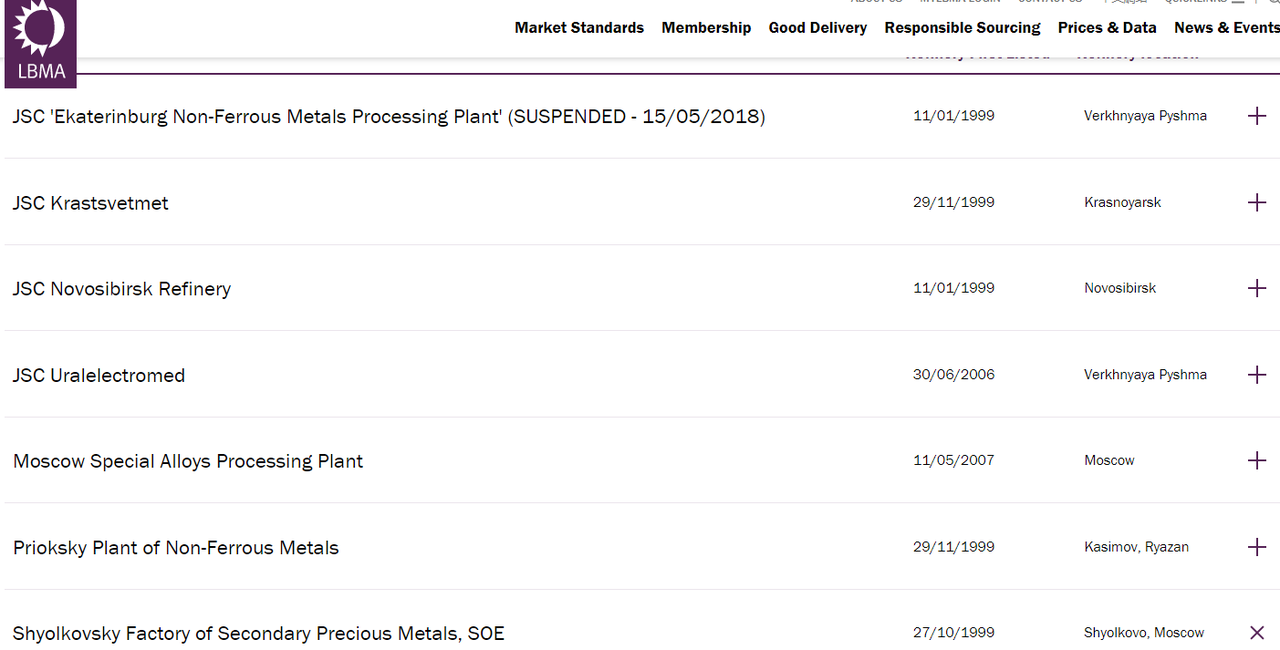

LBMA quietly drops Russia’s VTB Bank and Bank Otkrytie from its membership list, hoping no one will notice…. Previous list in screenshot. Current list here https://t.co/e4RA1VkZu4pic.twitter.com/HCVXvxBGXh

Across in Europe, the European Union (EU) has imposed its own set of sanctions against Russia, which in the economic / financial sector include assert freezes on Russian banks and blocking Russian access to capital markets and EU trading venues. This is a set of sanctions which in the words of the EU “will target 70% of the Russian banking market, and key state-owned companies, including in the field of defense”.

On Saturday 26 February, a coordinated group comprising the US, European Commission, France, Germany, Italy, Canada and UK announced that they will disconnect a certain number of Russian banks from the very important SWIFT international interbank payments system. Its not clear yet which banks this refers to.

“we commit to ensuring that selected Russian banks are removed from the SWIFT messaging system” so as to “ensure that these banks are disconnected from the international financial system and harm their ability to operate globally.”

As well as introducing SWIFT sanctions, this same group comprising the US, European Commission, France, Germany, Italy, Canada and UK have targeted Russia’s central bank, saying that they are committed to:

“imposing restrictive measures that will prevent the Russian Central Bank from deploying its international reservesin ways that undermine the impact of our sanctions.”

Final Boss – The Bank of Russia

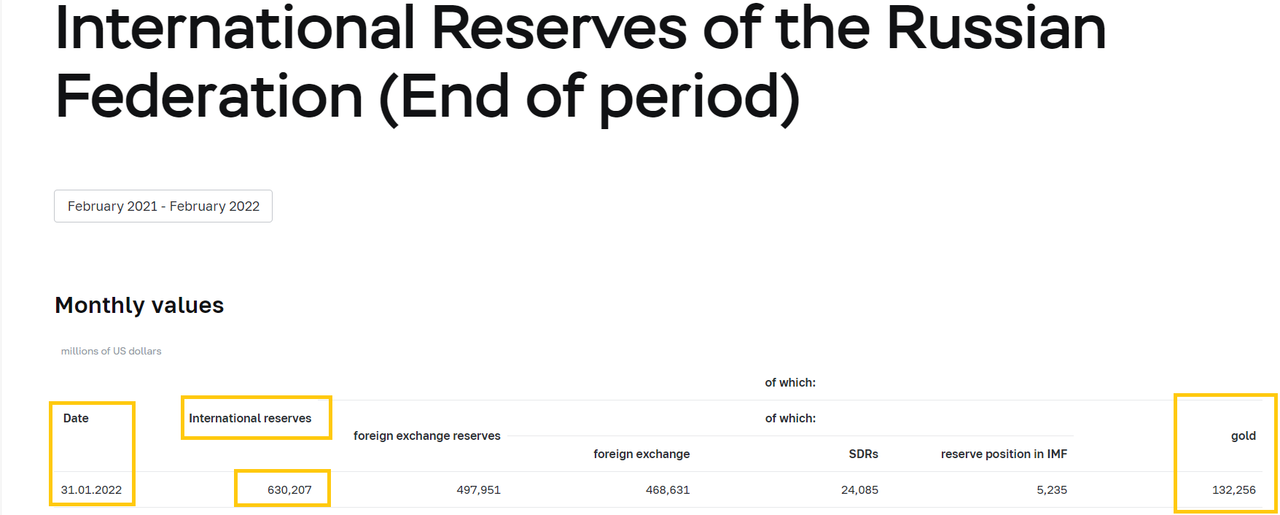

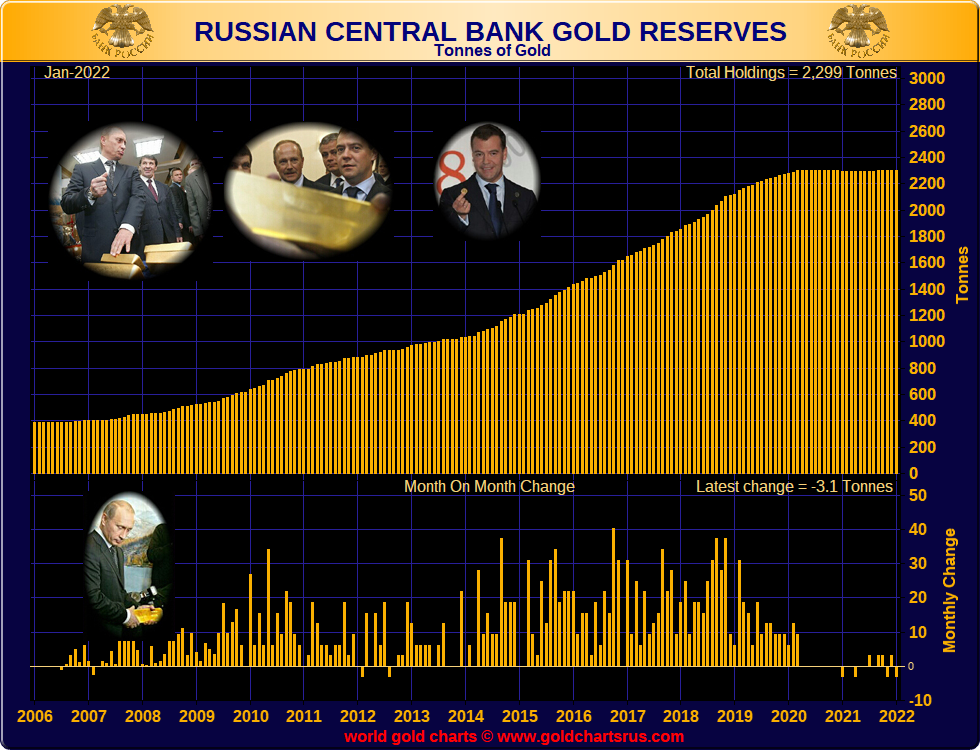

As of 31 January 2022, the Russian central bank held international reserves worth US 630.207 billion, of which US 497.951 billion was in foreign exchange reserves and US$ 132.256 billion was in gold. This equates to 79% in foreign exchange reserves and 21% in gold. See screenshot below.

The Bank of Russia’s foreign currencies comprise, in descending order of value, euros, US dollars, Chinese renminbi, pounds sterling and other currencies, so given the composition of these FX reserves, and given that it’s the US, UK and European Union who are doing the sanctioning, the Bank of Russia’s euros, US dollars and pounds which are held outside Russia on behalf of the Russian central bank are at imminent risk of being frozen.

Excluding the major Western currencies, this leaves the Russians with the Chinese renminbi as potentially accessible (assuming Chinese doesn’t bow to sanctions pressure). And it also leaves the Russian central bank with gold. A lot of gold.

Russia, via the Bank of Russia, holds 2299 tonnes of physical gold, and is now the fifth largest sovereign gold holder in the world, after steadily accumulating most of this gold since 2008. Notably, in late 2007, the Russian central bank still only held about 400 tonnes of gold, so Russia’s gold stockpile has increased by 600% since 2008. See chart below.

Two thirds of Russia’s gold reserves are held in vaults on Pravda Street in Moscow, with the other third held in vaults in St. Petersburg and Yekaterinburg. Russia’s entire gold accumulation strategy has been preparing for a scenario such as now, where gold will become crucial to the geo-political chess game amid heightened conflict risk and sanctions risk.

Right on cue, Russia just came out on 27 February and says it will resume gold buying:

“Russia’s central bank on Sunday [Feb 27] said it would resume buying gold on the domestic market from Feb 28, as it undertakes measures to try and ensure financial stability during Western sanctions against Moscow for its invasion of Ukraine.”

While today the UK Gov imposed a huge list of sanctions against Russian banks, companies & elites, the LBMA still has 6 Russian gold refineries on its LBMA Good Delivery List. This is odd given that in 2018, the LBMA suspended 1 Russian gold refinery due to ‘ownership issues’.

From an above reading of the various sanctions against Russia by Western powers, the one thing that stands out is that none of the sanctions so far have specifically mentioned gold nor access by Russia to the international gold.

Across the UK, US, and European sanctions, the common theme is freezing of bank assets, blocking the access of Russian banks and Russian companies to Western capital markets, sanctioning Russian government owned companies, banning various Russian banks from the SWIFT system, and attempting restrictive measures against the deployment of Russia’s international reserves.

While the “restrictive measures against the deployment of Russia’s international reserves” is interesting and could indirectly cover the ‘deployment’ of gold, given that all of Russia’s gold reserves held in Russian vaults, what exactly would ‘deploying’ mean when applied to the Russian gold?

LBMA quietly drops VTB and Otkrytie

It looks like we are about to find out. Because quietly and without acknowledgment, the Western bullion bank dominated London Bullion Market Association (LBMA), has gone and dropped Russian banks from its currently membership list. This refers specifically to Russian banks VTB Bank (which was a full member of the LBMA), and Bank Otkrytie (which was an affiliate of the LBMA).

Since, if you go to the LBMA current membership list, and look for these banks, they are no longer there. There are now zero LBMA members from the Russian Federation.

VTB Bank had joined the LBMA as a full member in March 2015. Bank Otkritie Financial Corporation (Bank FC Otkritie), which was formerly known as Nomos Bank, had joined the LBMA as an associate in November 2011. But just like that, VTB and Otkritie have now disappeared, without any Sanctions statements mentioning anything about the LBMA or indeed about any gold market. Maybe an enterprising Bloomberg or Reuters reporter who wants to pick up the story can ask the LBMA for an explanation.

The LBMA is Ignoring its own Sanctions Rules

But there is more, because also in the last few days, the LBMA has quietly added a short item to its news page titled “Sanctions: Timely Reminder” in which it states that:

“Under LBMA Good Delivery Rules, all GDL Refiners are required to comply with UN, EU, US, UK, or any other relevant, economic and/or trade sanction lists. Breach of any of the relevant Sanctions list would lead to removal from the GDL. Removal can involve a suspension or permanent de-listing.

If suspended, the Refiner will be transferred to the Former List, the Bars that it produced while on the List will still be considered Good Delivery. LBMA reserves the right to de-list Bars after an appropriate period in cases where production has ceased.

We will alert all relevant stakeholders of any changes to the Good Delivery List. For status updates, please visit the Current Good Delivery List.”

Before looking at this statement from the LBMA about Good Delivery refiners, note that while the LBMA went to the bother of adding a statement to its website under the title of “Sanctions”, it conveniently failed to mention that 2 of its members, VTB Bank and Bank Otkritie, have now been excluded as members of the LBMA. This is a typical LBMA distraction technique. Look over here at the Good Delivery List, but not over there at the Membership list.

Now back to the Good Delivery statement. As a reminder, the LBMA Good Delivery Lists refer to gold and silver list refineries whose gold and silver bars meet the required standard for acceptability in the London bullion market.

There are currently 6 Russian refiners listed on the LBMA current Good Delivery List for gold. These six refiners, using their short names, are Krastsvetmet, Novosibir, Uralelectromed, Moscow Special Alloys Plant, Prioksky and Shyolkosky.

There are currently 5 Russian refiners on the current LBMA Good Delivery List for silver, five of the same six as on the gold list, namely Ekaterinburg, Krastsvetmet, Novosibir, Uralelectromed, Prioksky and Shyolkosky.

In the latest version of the LBMA Good Delivery Rules, sanctions are addressed in Section 4, Compliance and Risk Management:

“4.4 Economic and Trade Sanctions

Bars must be capable of being delivered to, and held by, any person, including any person who falls within the definition of a US person identified in US sanctions, without violating any UN, EU, US, UK, or any other relevant, economic and/or trade sanction lists, or causing any person to violate any UN, EU, US, UK or any other relevant sanctions (collectively “Sanctions Rules”).

Refiners are to comply with all relevant economic/trade sanctions lists and are strongly advised to seek legal guidance where relevant.

Breach of any Sanctions Rules will lead to immediate removal from the List.”

Even a quick reading of these Good Delivery Rules suggests that all Russian refineries on the LBMA Good Delivery List are in breach of the LBMA’s own Good Delivery Rules. Why?

Because the Russian domestic gold market is an ecosystem in which the gold producers (miners) and gold refiners and the Russian commercial banks and the Russian central bank are all interconnected, and where commercial banks, such as Sberbank, VTB, Otkritie and Gazprombank sit in the middle, running the entire market. For details, see BullionStar’s Gold University article on the Russian Gold Market.

Russian banks such as Sberbank, VTB, Otkritie and Gazprombank buy the gold from the Russian gold mines, get the gold refined in the refineries such as Ekaterinburg, Krastsvetmet, Novosibir, Uralelectromed, Prioksky, and Moscow Special Alloys Plant, and then take delivery of the refined gold bars from the refineries and sell it on, including selling the refined gold bars to the Russian central bank.

All of these Russian banks are now on the sanctions lists. If Russian gold refineries do business with these Russian banks (which they have to do as the Russian banks are their clients), they will violate the UK – EU – US sanctions.

The Russian refineries, by also refining gold which then gets sold to the Russian central bank, will also then be facilitating the central bank in boosting and deploying its international reserve assets, which will too be in breach of the UK – EU – US sanctions. Then there is the issue of ownership of Russian gold refineries.

Russian State-Owned, LBMA Accredited

Back in May 2018, the LBMA ‘suspended’ one Russian refinery from its Good Delivery List. This refinery was Ekaterinburg, and according to Reuters, Ekaterinburg was suspended by the LBMA due to “ownership related issues”, essentially Ekaterinburg was controlled by Russian conglomerate Renova Group (headquartered in Moscow and with a subsidiary in Zurich) which was controlled by Russian oligarch Viktor Vekselberg.

The reason why this was a problem for the LBMA was that in April 2018, the US Treasury sanctioned Renova Group and Viktor Vekselberg, saying that:

“Renova Group is being designated for being owned or controlled by Viktor Vekselberg.

Viktor Vekselberg is being designated for operating in the energy sector of the Russian Federation economy. Vekselberg is the founder and Chairman of the Board of Directors of the Renova Group.”

In December 2019, the Renova Group sold 92% of Ekaterinburg, which is also known as EZOCM JSC, to a Russian company called Ural-Dragmet. Despite this sale, the LBMA still to this day has Ekaterinburg listed on the Good Delivery lists for gold and silver with the words ‘(SUSPENDED 15/05/2018)’.

But the important thing here is precedent. In 2018, the LBMA suspended Ekaterinburg due to its controlling entities Renova and Viktor Vekselberg being on a US Treasury sanctions list. So let’s look at the ownership of the other 6 Russian refiners on the LBMA Good Delivery Lists in terms of ownership.

The Gang of Six

LBMA refinery JSC Krastsvetmet is 100% Russian state-owned, as it is wholly owned by the Krasnoyarsk Region Administration of the Russian Federation. By the way, Krastsvetmet is Russia’s biggest gold refinery, and for example in 2018 Krastsvetmet refined 234 tonnes of gold (or 75%) out of a total of 314 tonnes of gold which was produced in Russia that year.

In fact, according to TASS News Agency in May 2019, the Governor of the Krasnoyarsk Region said that they were looking at the possibility of creating a holding company to unite these 3 LBMA refineries of Krastsvetmet, Moscow Plant of Alloys, and Prioksky Non-Ferrous Metals Plant, since they are all owned by the Russian Government.

Next up, LBMA refinery Novosibir (JSC Novosibirsk Refinery) was owned by the Russian Federation until 2017, when is was sold to a company called LLC Center of Property Management (or in Russian “ООО «Центр управления недвижимостью»”. Someone who speaks Russian may be able to trace back as to which property company made the purchase.

And lastly, there is LBMA refinery Shyolkovsky (full name Shyolkovsky Factory Of Secondary Precious Metals, and also known as Shchelkovo VDM). Its website is here.

In 2017, “a block of shares in JSC Shchelkovo Secondary Precious Metals Plant was sold at auction to JSC Novye Tekhnologii for 1 billion 515 million rubles. This was reported by the press service of the Auction House of the Russian Federation (RAD)”

The Shyolkovsky website says that:

“Since April 2017, the main partner of the Joint Stock Company ‘Shchelkovsky Plant of Secondary Precious Metals’ is the Joint Stock Company ‘Yuzhuralzoloto Group of Companies’”.

Yuzhuralzoloto (aka Uzhuralzoloto) was founded by Russian billionaire Konstantin Strukov, The Shyolkovsky website also says that “Our partners: jewelry factories, banks, defense, chemical and other industries.” And there is a large and prominent LBMA logo on the homepage of the Shchelkovsky website here.

LBMA, LPPM, Platinum and Palladium

Note too that the LBMA also administers the London Platinum and Palladium Market (LPPM), and there are two Russian refineries on both the current LPPM Good Delivery List for Platinum and the LPPM Good Delivery List for Palladium, namely “The Gulidov Krasnoyarsk Non-Ferrous Metals Plant” and the “Prioksky Plant of Non-Ferrous Metals” (a.k.a. Krastsvetmet and Prioksky).

You will note from the LBMA’s ‘Sanctions – Timely Reminder” statement, that it says:

“If suspended, the Refiner will be transferred to the Former List, the Bars that it produced while on the List will still be considered Good Delivery”.

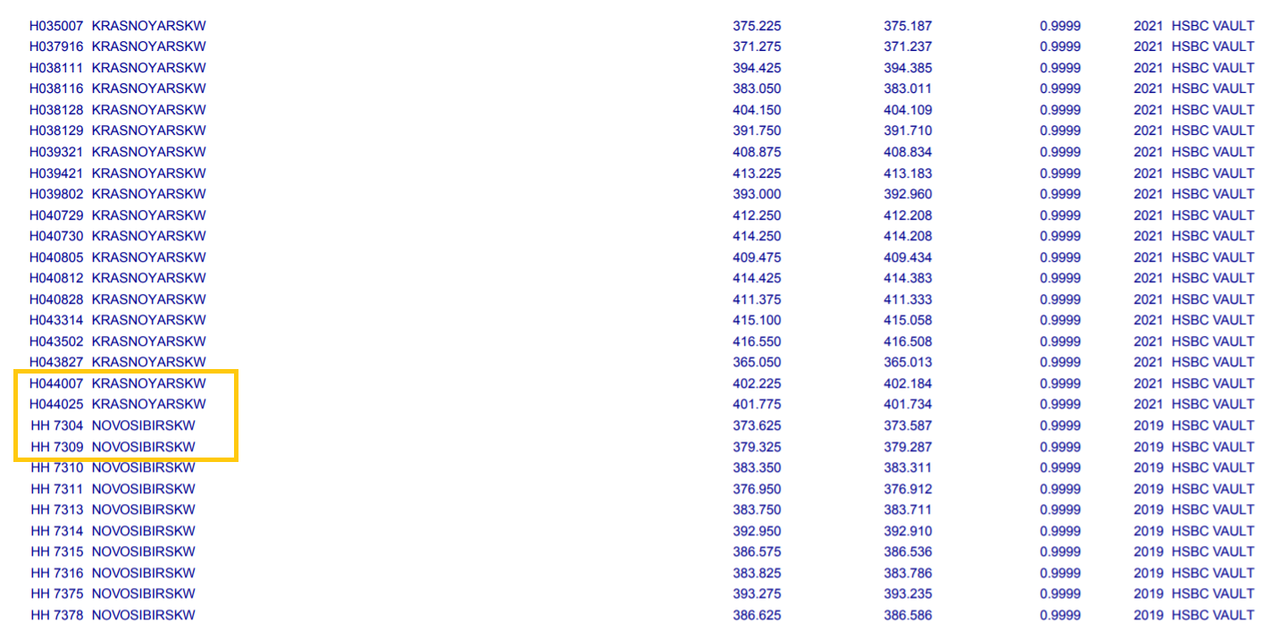

Why would the LBMA be so keen to point this out, and fixated that Russian bars, if transferred to Former Good Delivery would still be considered Good Delivery? Maybe it’s because there are nearly 1000 Russian 400 oz gold bars currently being held in the famous SPDR Gold Trust (GLD) in a vault in London (,either in the HSBC custodian vault or the Bank of England sub-custodian vault).

If you open the GLD bar list pdf and scroll to page1629, and then scroll down through to page 1646, see will see that the SPDR Gold Trust holds a huge number of gold bars from LBMA Russian refiners Novosibir, Prioksky, Krastsvetmet, Uralelectromed, I wonder how many GLD hedge fund and institutional investors know this? While gold bars from suspended Russian gold refineries may still be good delivery in the eyes of the LBMA, this is not the case in the eyes of traders.

Looking back to May 2018 at the time of Ekaterinburg’s suspension, Reuters said the following:

“Suspension from the list makes it harder for buyers and sellers to trade bars in the mainstream precious metals market, traders said.

‘”Our company would not touch any bars that are not LBMA-accredited,’ one trader at a major precious metals house said. ‘Most probably they are going to be in a secondary market.’

Conclusion

Events are running rapidly, and the coming week will be crucial to see how Russia and the Bank of Russia reacts to the SWIFT exclusions, and how the Bank of Russia will leverage its monetary gold reserves. Will Russia now accept gold for oil. What role will China play in all of this? Is the demise of the US dollar as world reserve currency at hand? Is the demise of the London fractional reserve paper trading gold system at hand?

In light of all of these new US – EU – UK sanctions against Russian banks, Russian state-owned and strategic private Russian companies, and Russian oligarchs, the LBMA bullion banks have a major headache on their hands in the coming week as regards the LBMA Russian refineries.

But don’t worry, because, according to Reuters in May 2018, LBMA CEO Ruth Crowell said that “due diligence in regard to the credibility of the lists is continuously reviewed on an ongoing basis”.

Why did the LBMA issue an empty statement on 24 February titled “Sanctions: Timely Reminder” which didn’t even mention the word Russia, didn’t mention that VTB and Otkritie are no longer LBMA members, and didn’t mention any of the 6 LBMA Russian Good Delivery refiners? Because I looked up all of that information about these Russian refineries in less than an hour and matched it against the US – UK – EU sanctions, and if I can do that, so too can the LBMA.

Or maybe its a case of “Gold, Too Important to Sanction”.

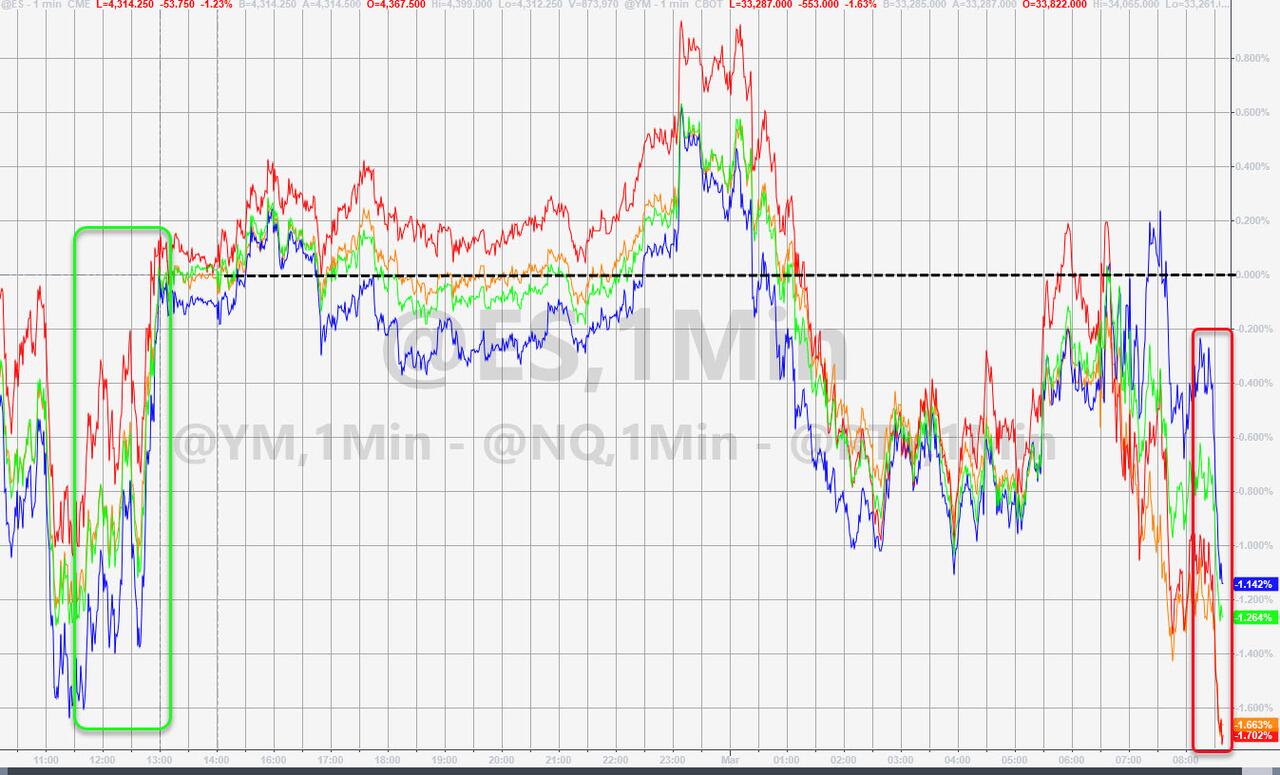

Stocks, Bond Yields Puke, Oil Explodes Higher After NATO ‘Emergency Meeting’ Headlines

Global stocks and bond yields were already getting hammered but reports that NATO foreign ministers will hold emergency meeting over Ukraine on Friday sparked another leg lower…

US Equities have erased yesterday’s late-day ramp-fest…

And Treasury yields are collapsing…

As are most of Europe’s sovereign yields.

And all of this as oil explodes higher, with WTI topping $105…

China “Extremely Concerned” About Rising Civilian Death Toll In Ukraine

On Tuesday China has again addressed the war in Ukraine, coming as Russia’s invasion has completed its first week. While prior official comments out of Beijing appeared to focus on condemning NATO expansionism while urging the West to take seriously Moscow’s ‘legitimate security concerns’ – this newest statement has sounded alarm over rising civilian casualties.

The foreign ministry statement said China “deplores” the outbreak of the conflict, saying it’s “extremely concerned” about civilians being harmed. The statement didn’t single out Russia, but still appears directed at Moscow given the words were conveyed in a phone call between Foreign Minister Wang Yi and his Ukrainian counterpart Dmytro Kuleba.

The statement said China respects the “sovereignty and territorial integrity of all countries” – but left it at a broad level without specifying further. “In view of the current crisis, China calls on Ukraine and Russia to find a solution to the issue through negotiations,” Wang Yi said, according to Bloomberg, and further underscored the need for “political settlement”.

Russian and Ukrainian media widely reported Tuesday that the next round of ceasefire talks are expected to take place Wednesday, along the Polish-Belarusian border. This as the civilian death toll in so far is being widely reported at over 400 killed.

“As the war continues to expand, the top priority is to ease the situation to prevent the conflict from escalating or even getting out of control, especially to prevent harm to civilians, and to ensure the safe and timely access of humanitarian aid,” Wang added. The Ukrainian top diplomat expressed hope for China’s mediation for a ceasefire.

In the phone call, the Ukrainian side urged China to press Putin to stop the war…

Meanwhile, China has an estimated6,000 citizens currently inside Ukraine, as its embassy there scrambles to initiate evacuation plans:

“There are missiles in the air, explosions and guns on the ground, and the two armies are fighting each other…How is it possible to ensure safety (to leave) in such circumstances?” Ambassador Fan Xianrong said in a video posted to the embassy’s social media account on Saturday, three days after the Embassy released plans for evacuate flights.

Beijing’s reaction to the Ukraine crisis has been under a microscope since the start of the Russian invasion, given the parallels of the situation with Taiwan. Beijing officials recently issued provocative comments saying Taiwan is “not Ukraine” – meaning China doesn’t at all see it as a sovereign entity to begin with.

For those of us who have covered the Hunter Biden scandal for years, one of the most prominent figures in his alleged influence peddling efforts is Devon Archer, his close friend and partner. Archer was sentenced yesterday by federal District Judge Ronnie Abrams to a year in jail. Archer is shown (far left) in this 2014 picture with Joe Biden and Hunter Biden.

Archer was convicted of defrauding the Wakpamni Lake Community Corporation of the Oglala Sioux Tribe in the handling of a $60 million bond offering. Hunter Biden was not implicated in those dealings.

Abrams was previously reversed after she set aside his 2018 jury conviction. In United States v. Archer, the Second Circuit found that Abrams abused her discretion in tossing out the verdict.

Abrams actually gave a lighter sentence than the 30 months requested by prosecutors, citing the pandemic conditions in prison as “extraordinarily difficult.” The lower sentence may have practically undermined any interest of federal prosecutors to reach a cooperation deal with Abrams in their ongoing investigation of Hunter Biden.

Archer was involved with Hunter as a board member on Burisma Holdings, an Ukraine-based energy company. He was also featured in the controversial picture with now President Joe Biden.

One of the most extraordinary exchanges found in Hunter’s text messages reportedly dealt with Archer complaining that he was arrested by Biden “appointees.” According to press accounts, Hunter Biden responded by assuring him that he was covered and “family”:

“Every great family is persecuted prosecuted in the US — you are part of a great family — not a side show not deserted by them even in your darkest moments. That’s the way Bidens are different and you are a Biden. It’s the price of power.”

That exchange is highly concerning since Hunter knew that he was a potential target of a criminal investigation. He was talking to a potential witness who could be used against him and his family in any investigation of their alleged influence peddling and foreign dealings.