9/2/1819: James Madison writes letter to Judge Spencer Roane criticizing McCulloch v. Maryland.

The post Today in Supreme Court History: September 2, 1819 appeared first on Reason.com.

from Latest https://ift.tt/1fzp5Us

via IFTTT

another site

9/2/1819: James Madison writes letter to Judge Spencer Roane criticizing McCulloch v. Maryland.

The post Today in Supreme Court History: September 2, 1819 appeared first on Reason.com.

from Latest https://ift.tt/1fzp5Us

via IFTTT

Why start your own business when you can tell other people how to run their operations without doing any of the work or assuming the risk yourself? That’s the apparent theory behind California’s A.B. 257, a bill just passed by legislators that would establish a council with the power to set wages and working conditions for fast food restaurants. It’s a measure likely to kill jobs, guaranteed to cause headaches for business owners, and that will probably prove a boon for the automation industry as well as for fans of failed experiments in 20th century authoritarian government.

“This bill would enact the Fast Food Accountability and Standards Recovery Act or FAST Recovery Act. The bill would establish, until January 1, 2029, the Fast Food Council (council) within the Department of Industrial Relations, to be composed of 10 members to be appointed by the Governor, the Speaker of the Assembly, and the Senate Rules Committee, and would prescribe its powers,” reads the text of A.B. 257, which passed both the Assembly and the Senate. “The purpose of the council would be to establish sector-wide minimum standards on wages, working hours, and other working conditions related to the health, safety, and welfare of, and supplying the necessary cost of proper living to, fast food restaurant workers, as well as effecting interagency coordination and prompt agency responses in this regard.”

The council would be made up of two state officials, four industry representatives, and four representatives of workers and unions. “The Governor shall appoint the representatives of the state agencies, fast food restaurant employees, fast food restaurant franchisees, and fast food restaurant franchisors. The Speaker of the Assembly and the Senate Rules Committee shall each appoint one representative of an advocate for fast food restaurant employees,” specifies the law.

Jurisdictions with populations greater than 200,000 could establish their own local councils to advise the state body regarding further regulations. Restaurant chains will be subject to the councils’ rules if they have 100 or more national outlets.

“In the wake of a pandemic that has been especially brutal to women of color and their families, our policy makers in Washington, D.C., have yet to make the investments we need to support caregivers and help families thrive—or to ensure that the economy is producing good, well-paying jobs in the face of rising inflation,” argued a coalition of progressive and labor groups in a letter dated August 10. “With A.B. 257, fast-food workers will win a seat at the table with decision makers and will gain the ability to shape industry-specific solutions to longstanding problems.”

If the idea of joint state-industry-labor councils dictating terms to nominally private enterprise sounds familiar, that’s because it’s been tried before. In 1934, The New York Times reported the creation in Italy of “22 councils of corporations to regulate all business” consisting of representatives of employers, employees, and government. The councils were responsible not just “for the administration of labour contracts but also for the promotion of the interests of its field in general,” as noted by the Encyclopedia Britannica. A.B. 257 doesn’t go quite that far, yet, but it certainly moves in that direction. To paraphrase Tom Wolfe, the dark night of fascism is always descending in Florida and yet lands only in California (though Florida has its own occasional bouts of authoritarianism).

The legislation not only resembles to a disturbing degree collectivist authoritarian experiments of the past, it also repeats their economic errors.

“A.B. 257 … would impose increased employee costs and onerous new workplace rules at a time when many are still struggling to get back on their feet after the devastating impacts of the government mandated COVID closures,” objects the California Restaurant Association, which represents the industry.

“The economic literature on minimum wage increases has become murkier in recent years, but the overwhelming majority of economists agree that large minimum wage increases in excess of productivity gains means that employers will operate at a loss as far as the effected workers go,” cautions the Cato Institute’s Michael D. Tanner. “It is unclear whether the Councils could prevent fast‐food franchises from laying off workers in the event of higher labor costs (already automated kiosks are replacing many fast food workers), but there is nothing they could do to prevent some franchises from closing down and leaving the state.”

As Tanner notes, raising the cost of labor makes it increasingly attractive for employers to replace human workers in existing restaurants and to plan future restaurants with a preference for automated systems over human employees.

“Increasing the minimum wage provides economic incentives for firms to adopt new technologies that replace workers,” Scott A. Wolla and F. Mindy Burton noted last year in an analysis for the Federal Reserve Bank of St. Louis. “That is, a higher minimum wage raises the cost of labor and increases the range of tasks that are susceptible to displacement by automation—especially the tasks of minimum wage jobs, which tend to be labor intensive and composed of low-skill tasks. For example, consider the self-checkout lanes at grocery stores and digital kiosks at a fast-rood restaurant …”

As that analysis suggests, the push in recent years for higher minimum wages has already spurred restaurant chains, including McDonald’s, to adopt self-service kiosks for ordering and robots for food preparation. The provisions of A.B. 257 can only make flesh-and-blood employees that much more expensive and uncompetitive.

Even government officials aren’t all enthused by the legislation’s vision of corporative decision-making for the fast-food industry. California’s own Department of Finance opposes the bill because of the high costs and regulatory fragmentation it poses. Gov. Gavin Newsom has yet to indicate whether he’ll sign the measure.

As it stands, California already offers a difficult environment for businesses to navigate, with a significant existing regulatory apparatus and a high minimum wage.

“States at the bottom of the list continued to suffer from reputations for high taxes, regulation and costs of living, with Washington at No. 46, followed by New Jersey, Illinois, New York and California,” Chief Executive magazine noted this year in its annual rankings of best and worst states for business.

If already substantial interventions in the market haven’t achieved the utopia that progressives desire, the fault may not lie with what’s left of economic freedom, but with the interventions themselves. Subjecting nominally private enterprise to the dictates of collectivist councils didn’t do any favors for 1930s Italy, and it’s not likely to have a better outcome in California of 2022.

The post California Bureaucrats Want to Take Over Your Local Fast Food Joint appeared first on Reason.com.

from Latest https://ift.tt/xptyUZM

via IFTTT

Even though Warren Jeffs resigned as president of the Fundamentalist Church of Jesus Christ of Latter Day Saints (FLDS), his followers continue to worship him as their prophet. Jeffs is currently serving a life sentence for sexually assaulting minors—at the time of his arrest in 2006, he had more than 70 wives and nearly a third of them were under the age of 17. A handful of Jeffs’ followers were also charged with sexual assault.

This religious community—the subject of Netflix’s latest true-crime docu-thriller, Keep Sweet: Pray and Obey—wasn’t finished with conflict after Jeffs and others were removed from the Yearning for Zion Ranch in Eldorado, Texas. Child Protective Services (CPS) returned to rip more than 450 children from their mothers on the compound. CPS claimed that because their religion represented a “pervasive belief system,” it was too dangerous to leave any children in the community. In horrifying raw footage from the raid, the children (including newborns) are seen crowding on buses and screaming for their parents. The Texas Supreme Court later found that the raid was not justified because CPS failed to prove the children were in immediate danger.

When faced with a choice between family and church, many FLDS members continue to choose the latter. This devotion has led to many broken families where the husband is exiled while his wife and children—who think obedience is their only choice—stay behind, or in the worst-case scenario, are reassigned to new husbands.

The post Review: After Cult Leader Was Convicted, His Compound Was Raided by Child Protective Services appeared first on Reason.com.

from Latest https://ift.tt/9I5qWCf

via IFTTT

If you want less expensive housing, you need more housing. And the way to get more housing is actually pretty simple: You have to let people build it.

But that seemingly simple solution has turned out to be incredibly difficult, mostly because of politics. More specifically, the problem is zoning.

Local zoning rules put limits on what can be built and where. Zoning rules restrict how high a building can be, or how many units can occupy a given parcel of land.

In some cases, they also require aesthetic features that can be cumbersome or expensive to build.

In other words, zoning makes housing more scarce—and more expensive.

In theory, President Joe Biden has staked out opposition to the worst of these building restrictions. While campaigning for president, he backed loosening zoning rules.

And the bipartisan infrastructure law Biden signed last year contained billions of dollars for transportation grants the administration indicated could go to localities that reformed strict zoning laws, as part of the administration’s Housing Supply Action Plan, which the White House has described as a plan to “ease the burden of housing costs.”

But that plan has produced disappointing results.

That’s the topic of this week’s episode of The Reason Rundown With Peter Suderman, featuring Reason Associate Editor Christian Britschgi.

Mentioned in this podcast:

“Joe Biden’s Use of Transportation Dollars To Incentivize Zoning Reform Is a Big Flop” by Christian Britschgi

“Environmental Lawsuits Tried To Block 50,000 Homes From Being Built in California in 1 Year” by Christian Britschgi

“Are San Francisco’s NIMBYs Finally Getting Their Comeuppance?” by Christian Britschgi

“Marc Andreessen’s High-Tech Fix for the Housing Crisis Lets Him Keep Being a NIMBY” by Christian Britschgi

Audio production and editing by Ian Keyser; produced by Hunt Beaty.

The post Christian Britschgi: Zoning Restrictions Worsen the Housing Crisis appeared first on Reason.com.

from Latest https://ift.tt/57leH2a

via IFTTT

Standing in what looked like some sort of medieval crypt, President Joe Biden last night gave a televised speech on the “battle for the soul of the nation.” On one level, it was quite ho-hum—so unrooted in anything of the moment, so lackluster in its delivery, so full of pablum and platitudes that it’s easy to wonder what the point of it all was.

But of course, on another level, the point was very clear. Biden’s soul of the nation speech was meant to rally people to vote for Democrats in the upcoming midterm elections, through a combination of pointing out the things Democrats have (allegedly) done right and, more emphatically, things former President Donald Trump and “MAGA Republicans” have done wrong.

In the speech, Biden repeatedly distinguished mainstream Republicans, who he implied believe in all the good American principles that Democrats do, from MAGA Republicans. MAGA Republicans are the kind of conservatives who “do not respect the Constitution,” “do not believe in the rule of law,” “do not recognize the will of the people,” and “represent an extremism that threatens the very foundations of our republic,” said Biden. They “refuse to accept the results of a free election,” “promote authoritarian leaders,” and “fan the flames of political violence.” They’re “determined to take this country backwards—backwards to an America where there is no right to choose, no right to privacy, no right to contraception, no right to marry who you love.”

Maybe the distinction was meant as cover against accusations that this was a totally partisan speech. Maybe it was an attempt to welcome “mainstream Republicans” or Republican-leaning independents over to Democrats’ side. But Biden’s premise here is tragically flawed, because “mainstream” Republicans today are MAGA Republicans. Maybe not quite the caricature of MAGA Republicans that Biden laid out. But Trump fans (with all that entails) are not some fringe. They’re at the center of today’s Republican Party and account for many of its candidates.

Biden is harking back to an era of “mainstream” Republicanism that no longer exists.

Holding up MAGA Republicans as particularly dangerous is also interesting given all the money Democrats have poured into MAGA Republican primary candidates. Their reasoning here is that it will be easier for Democrats to win in the general election against extremist, conspiracy-promoting GOP candidates than against nice, normie Republicans [OK?].

Even if these "MAGA Republicans" do not win in 2022 midterms, Democrats spending to boost the candidates' profiles gives them a bigger platform on the national stage — a platform that can be used to spread disproven theories about the 2020 election being stolen from Donald Trump. https://t.co/6RZexFnygK

— Anna Massoglia (@annalecta) September 2, 2022

Will it pay off as a political strategy? Maybe. But that doesn’t detract from the moral bankruptcy of it—and also undercuts Democratic claims that MAGA Republicans are existentially dangerous to democracy and civilized society. If that were true, wouldn’t it be more important to do anything possible to keep them out of office? If that were true, wouldn’t boosting them just to better Democrats’ midterm election odds be depraved?

There was perhaps a twinge of this convoluted strategy in Biden’s soul of the nation speech, which went quite heavy on condemning Trump and Trumpism. Baiting Republicans to vociferously defend Trump, or simply continuing to associate Republicanism and Trumpism in American minds, may benefit Democratic candidates in the midterms when it comes to independent/swing voters, who have been losing love for Trump in the wake of the January 6 hearings.

There’s a theory going around that Democrats want to keep focus on Trump—with the January 6 hearings, the Mar-a-Lago raid, etc.—so that he’ll decide to run again in 2024, because they believe he’ll be easier to beat than someone like Florida Gov. Ron DeSantis. To be clear, there’s no particular evidence for this (and in what world wouldn’t Democrats do January 6 hearings, etc., regardless?). But things like Biden’s speech last night make it seem not entirely implausible.

In any event, Biden’s soul of the nation speech last night was boring and entirely forgettable. But perhaps, in the post-Trump years, boring and totally forgettable isn’t something we should take for granted. Boring and forgettable is much better from a president than actively looney tunes and attempting to undermine democratic elections.

But there is a way in which Biden’s speech last night echoed Trump speeches: It was not simply a speech for all Americans. It was not designed simply to convey information, celebrate some national win, or reassure Americans in the wake of a disconcerting event. It seemed pretty clearly designed to rally people toward Democrats and against Republicans, just as many Trump speeches were designed to do the opposite. And no matter who’s doing it, it’s upsetting to see the presidential pulpit used in this way.

Backpage founders Michael Lacey and James Larkin before appeals court. It’s been nearly a year since a judge declared a mistrial in the case against Lacey, Larkin, and other former executives of the sex worker–friendly classified ad platform Backpage. U.S. District Judge Susan Brnovich declared the mistrial due to prosecutorial misconduct during the first week of the trial. Lacey and Larkin appealed to the U.S. Court of Appeals for the 9th Circuit, arguing that retrying them would be an unconstitutional exercise of double jeopardy. A three-judge panel of the court is scheduled to hear oral arguments in this appeal today, beginning at 12 p.m. Eastern Time.

Some in the European Union want to ban anyone born after 2010 from ever buying nicotine products.

A new petition argues for the EU to ban people born after 2010 from buying nicotine products. According to @LandlMichael from @vapers_alliance, age bans go against the Lisbon Treaty.

Listen here ???? pic.twitter.com/ZVQor8gnD9

— Consumer Choice Center (@ConsumerChoiceC) September 2, 2022

• “National test results released on Thursday showed in stark terms the pandemic’s devastating effects on American schoolchildren, with the performance of 9-year-olds in math and reading dropping to the levels from two decades ago,” reports The New York Times.

• Reason Editor in Chief Katherine Mangu-Ward on “the new abortion prohibition era.”

• Unnecessary restrictions on modular homes, co-housing, and short-term rental companies are exacerbating America’s housing crisis, writes Vanessa Brown Calder at the Cato Institute.

• In New York City, around 36 blocks surrounding Times Square will now be declared a gun-free zone. “What purpose is served by this?” asks Reason‘s Liz Wolfe.

• Republicans have lots of (rightful) criticism about current public health protocols. But do they actually have any plans to reform public health bureaucracies?

• An interesting Netflix documentary called Keep Sweet: Pray and Obey looks at the rise and fall of Fundamentalist Church of Jesus Christ of Latter Day Saints leader Warren Jeffs and “the unjustified taking of 450 children inside his religious community,” writes Natalie Dowzicky.

The post Biden's Presidential Address Was Actually a Campaign Speech appeared first on Reason.com.

from Latest https://ift.tt/qAogyDV

via IFTTT

From Fells v. SEIU, decided yesterday by the D.C. Court of Appeals in an opinion by Judge Joshua Deahl, joined by Judges Corinne Beckwith and John Fisher; not as colorful as the inimitable Memphis Pub. Co. v. Nichols (Tenn. 1978), but still an interesting modern example of the libel-by-implication doctrine:

Kendall Fells was a high-level employee within the Service Employees International Union (SEIU). After his seemingly forced resignation, SEIU issued a press statement tying his departure to an “ongoing investigation” that was triggered by another executive’s sexual misconduct, namely, sleeping with subordinates. In announcing Fells’ departure, the statement explained that Fells’ own “abusive behavior towards … predominantly female staff” was brought to light by that investigation. Fells sued SEIU for defamation and related claims. He contends that SEIU’s statement falsely implied that he was forced out due to sexual misconduct, when in fact, there is no dispute that Fells’ departure was not related to any sexual misconduct….

We conclude, contrary to the trial court’s view, that a reasonable jury could find SEIU’s statement falsely implied that Fells was ousted for sexual misconduct….

The core facts are not in dispute. Kendall Fells held various staff and leadership roles over the course of his thirteen-year career with SEIU. At the time of his resignation, Fells was interim President of the National Fast Food Workers’ Union, a labor organization within SEIU that grew out of the “Fight for $15” minimum wage movement that he championed. While Fells was in that role, SEIU’s President, Mary Kay Henry, began actively encouraging employees to report sexual harassment and abuse amid the #MeToo movement. As a result of several accusations involving inappropriate sexual relationships with subordinates, SEIU suspended its Executive Vice President, Scott Courtney, who resigned shortly thereafter. SEIU’s spokesperson told BuzzFeed News that Courtney engaged in “sexual misconduct and abusive behavior,” as revealed through a still-ongoing “internal investigation launched to look into … sexual misconduct and abusive behavior towards union staff.”

Ten days later, Fells resigned, seemingly under threat of termination. SEIU’s spokesperson issued a statement to multiple news outlets regarding Fells’ and another employee’s contemporaneous departure, indicating that those “personnel actions” were the result of its aforementioned “ongoing internal investigation” and pertained to “serious problems related to abusive behavior towards staff, predominantly female staff.” The statement in its entirety read as follows:

As a result of information that has come to light through our ongoing internal investigation, today SEIU took action on two senior staff. These personnel actions are the culmination of this stage of the investigation, which brought to light the serious problems related to abusive behavior towards staff, predominantly female staff. We know that progress does not stop with these personnel actions alone. [SEIU] President Henry has taken important steps toward ensuring that our workplace environment reflects our values, and that all staff is respected, their contributions are valued, and their voices are heard.

Several media outlets then published articles connecting Fells’ and Courtney’s resignations and, in at least one instance, expressly attributing Fells’ ouster to sexual misconduct allegations. In fact, as SEIU concedes, Fells’ departure was not related to any claims of sexual misconduct….

The court concluded that SEIU’s statement was “[1] in furtherance of the right of advocacy [2] on issues of public interest,” and thus presumptively covered by the District’s anti-SLAPP Act; and “[b]ecause SEIU made a prima facie showing in support of its special motion to dismiss under the Anti-SLAPP Act, the burden shifts to Fells to show that his defamation claim was ‘likely to succeed on the merits.'” But the court went on to say that “Fells demonstrated a likelihood of success on the merits so that his defamation claim may proceed,” which is to say that he “present[ed] an evidentiary basis that would permit a reasonable, properly instructed jury to find in the plaintiff’s favor”:

Fells has no viable claim for express defamation—SEIU’s statement did not expressly state he was terminated for sexual misconduct—leaving him to resort to a theory of implied defamation.

Defamation by implication concerns not what somebody literally stated, but what their statement implies…. [I]t is not enough that a statement can “be reasonably read to impart the false innuendo, but it must also affirmatively suggest that the author intends or endorses that inference.” Evidence that supports such a finding includes “suggestive juxtapositions, turns of phrase, or incendiary headlines.”

The SEIU statement at issue provided that Fells’ termination was “the culmination of this stage of the investigation, which brought to light the serious problems related to abusive behavior towards staff, predominantly female staff.” Recall that “the investigation” referenced was triggered by allegations that another recently ousted executive, Scott Courtney, was having inappropriate sexual relationships with subordinates. Fells argues that tethering his departure to the same internal investigation that led to Courtney’s ouster days earlier indicated that he, too, had engaged in sexual misconduct, at least absent any indication to the contrary…. “[A] defendant does not avoid liability [for implied defamation] by simply establishing the truth of the individual statement(s); rather, the defendant must also defend the juxtaposition of” its statements …. We agree that a jury could reach that conclusion.

SEIU counters that the internal investigation was not exclusively about sexual misconduct. It highlights that, upon Courtney’s resignation, SEIU’s spokesperson described the investigation as one “look[ing] into questions about [1] potential violations of our union’s anti-nepotism policy, [2] efforts to evade our Code of Ethics and [3] subsequent complaints related to sexual misconduct and abusive behavior towards union staff.” {SEIU seemingly refers to “nepotism” in a broad sense when discussing Courtney’s departure and the investigation surrounding it to include preferential treatment not just of family members, but of friends or sexual partners as well.} It is hard to see how that changes the calculus. Sexual misconduct, nepotism, and ethical breaches may all be of a piece, and in the context of the investigation prompting Courtney’s resignation, it appeared that they were. In light of that context, the most natural reading is that the investigation was into higher-ups giving preferential treatment to subordinates who acquiesced to their sexual advances—or disfavoring those who did not—checking each box of sexual misconduct, nepotism, and ethical breaches.

But even if that were not enough, there is a second problematic juxtaposition in SEIU’s statement suggesting that Fells engaged in sexual misconduct. It says that his ouster stemmed from “abusive behavior towards staff, predominantly female staff.” When coupled with the earlier reference to an investigation that resulted in another high-level executive’s departure for sexual misconduct—and especially in the midst of the roiling #MeToo movement—a reasonable jury could conclude that this statement indicated Fells’ misconduct was sexual in nature, and that SEIU intended to so imply. Indeed, a Breitbart article drew that exact inference, with a headline positing: Four SEIU Officials Out of a Job Because of Sexual Misconduct Charges.

The Supreme Court of Minnesota found a similar juxtaposition potentially defamatory in Phipps v. Clark Oil & Refining Corp. (Minn. 1987). In that case, a gas station attendant alleged that he was fired for refusing the request of a customer—who happened to be “handicapped”—to put leaded gasoline into a vehicle designed for unleaded gasoline. Gas station representatives then made factually accurate statements indicating that he had been fired “for failing to provide … service to a handicapped customer.” While technically true, the customer’s handicap had nothing to do with the employee’s refusal to assist them, and Phipps held that there was a triable question of fact as to whether the inclusion of the word “handicapped” gave rise to a false inference that the attendant refused to help the customer because of their handicap. Similarly here, it is not obvious why SEIU mentioned that the abuse was predominantly of women, and came to light as part of the investigation into Courtney’s sexual misconduct, if not to imply that Fells had engaged in conduct of the same nature. A jury could reasonably adopt Fells’ position that doing so amounted to defamation….

Congratulations to my friend Erik S. Jaffe (who is also a colleague of mine at Schaerr | Jaffe LLP, where I’m a part-part-part-time academic affiliate), who argued the case, on the victory. Note that I am writing this post solely in my academic capacity, and not out of any connection with Schaerr | Jaffe (the case came up in my daily Westlaw query for interesting new First Amendment cases).

The post New #TheyLied Libel-by-Implication Case, Related to Firing of Service Employees International Union appeared first on Reason.com.

from Latest https://ift.tt/if5o36k

via IFTTT

Nuclear Talks Unraveling As US Calls Iran Final Text Submission A Move “Backwards”

The White House has received Tehran’s awaited response to prior US stipulations regarding the final text of a restored JCPOA nuclear deal, and the initial reaction strongly suggests that negotiations are once again in peril even as the deal is at the ‘finish line’.

Politico bluntly observes of the latest, “The negative reaction from the Biden administration — as well as European sources — suggests that a revival of the 2015 nuclear agreement is not imminent as some supporters of the deal had hoped, despite roughly a year and a half of talks.”

A senior Biden administration official told the publication Thursday night, “We are studying Iran’s response, but the bottom line is that it is not at all encouraging,” and concluded further: “based on their answer, we appear to be moving backwards.”

The Europeans appear to be on the same page, with an EU diplomat who has seen Iran’s fresh response assessing that Iran’s answer was “negative and not reasonable”.

The details of what the Islamic Republic added to the text has yet to be revealed, but US officials only days ago suggested that the world was “closer” than ever to witnessing a restored deal.

Iranian President Ebrahim Raisi said earlier this week that without finding final settlement on the issue of the IAEA probe into traces of uranium found at undeclared nuclear sites, it remains that “talking about an agreement would be meaningless.” These words were also viewed as a negative sign that negotiators could be further from the finish line of a completed deal than previously thought.

Two additional factors loom large in the background which make a finalized deal increasingly unlikely: US domestic politics and a full court Israeli press to influence Biden officials. Concerning the former, Politico writes:

A deal to restore the 2015 agreement will likely face a review in Congress. But with midterm elections coming up in November, many Democrats in particular may want to avoid an Iran debate in the weeks immediately prior.

“With this opportunity squandered, it is now hard to imagine that a deal can happen before the midterms,” said Ali Vaez, a top analyst with the International Crisis Group.

Concerning America’s closest regional ally, starting next week Mossad chief David Barnea will be in Washington lobbying US intelligence counterparts and Biden administration officials to resist entering a “bad deal” – as Israeli leadership has long dubbed efforts in Vienna to restore the JCPOA.

Iran has called its own final text additions “constructive”…

Time will tell how “constructive” it is and whether it is truly “aimed at finalizing the negotiations.” This is #Iran‘s description of its own response. Khamenei made no mention of the JCPOA in his remarks this week on government priorities.https://t.co/MBqTFctM76

— Jason Brodsky (@JasonMBrodsky) September 1, 2022

The Times of Israel notes that “Barnea will be the third senior Israeli official to visit Washington in recent days to discuss the Iran deal, after Defense Minister Benny Gantz and national security adviser Eyal Hulata.”

Tyler Durden

Fri, 09/02/2022 – 08:25

via ZeroHedge News https://ift.tt/zSZeBm9 Tyler Durden

Power Company Seizes Control Of Thermostats In Colorado During Heatwave

Authored by Paul Joseph Watson via Summit News,

Around 22,000 households in Colorado lost the ability to control their thermostats after the power company seized control of them during a heatwave.

After temperatures soared past 90 degrees, residents were left confused when they tried to adjust their air conditioning and found locked controls displaying a message that said “energy emergency.”

Xcel confirmed to local news station Denver7 that “22,000 customers who had signed up for the Colorado AC Rewards program were locked out of their smart thermostats for hours on Tuesday.”

“I mean, it was 90 out, and it was right during the peak period,” Tony Talarico told the news station. “It was hot.”

Talarico said he is normally able to override the “energy emergency” message, but not on this occasion.

“So, our thermostat was locked in at 78 or 79,” he said.

When thousands of Xcel customers in Colorado tried adjusting their thermostats Tuesday, they learned they had no control over the temperatures in their own homes. via @jaclynreporting https://t.co/mgLEC6SEzR

— Denver7 News (@DenverChannel) September 1, 2022

Completely losing control over the temperature of your own home is presumably one of the many benefits of the green energy ‘Great Reset’ Americans will be forced to endure.

This story is yet another example of how smart meters will pave the way for energy rationing.

No doubt Americans who have them installed will increasingly find their thermostats remote controlled at the behest of energy companies whenever a dubious ‘crisis’ can be declared.

And if that sounds bad, just imagine what will happen if net zero green energy ‘climate lockdowns’ become normalized.

People in major European countries are already having their thermostats regulated in response to the energy crisis.

In Spain, at the height of summer, authorities have controversially banned air conditioning from dropping below 27°C (80.6°F) in all non-residential buildings, including shops, cinemas and cafes.

Onerous fines for those who flout the rules run all the way up to €600,000 euros for “serious violations.”

Similar rules have also been announced in Germany, Italy and France.

* * *

Brand new merch now available! Get it at https://www.pjwshop.com/

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Get early access, exclusive content and behinds the scenes stuff by following me on Locals.

Tyler Durden

Fri, 09/02/2022 – 08:05

via ZeroHedge News https://ift.tt/hWsQ10p Tyler Durden

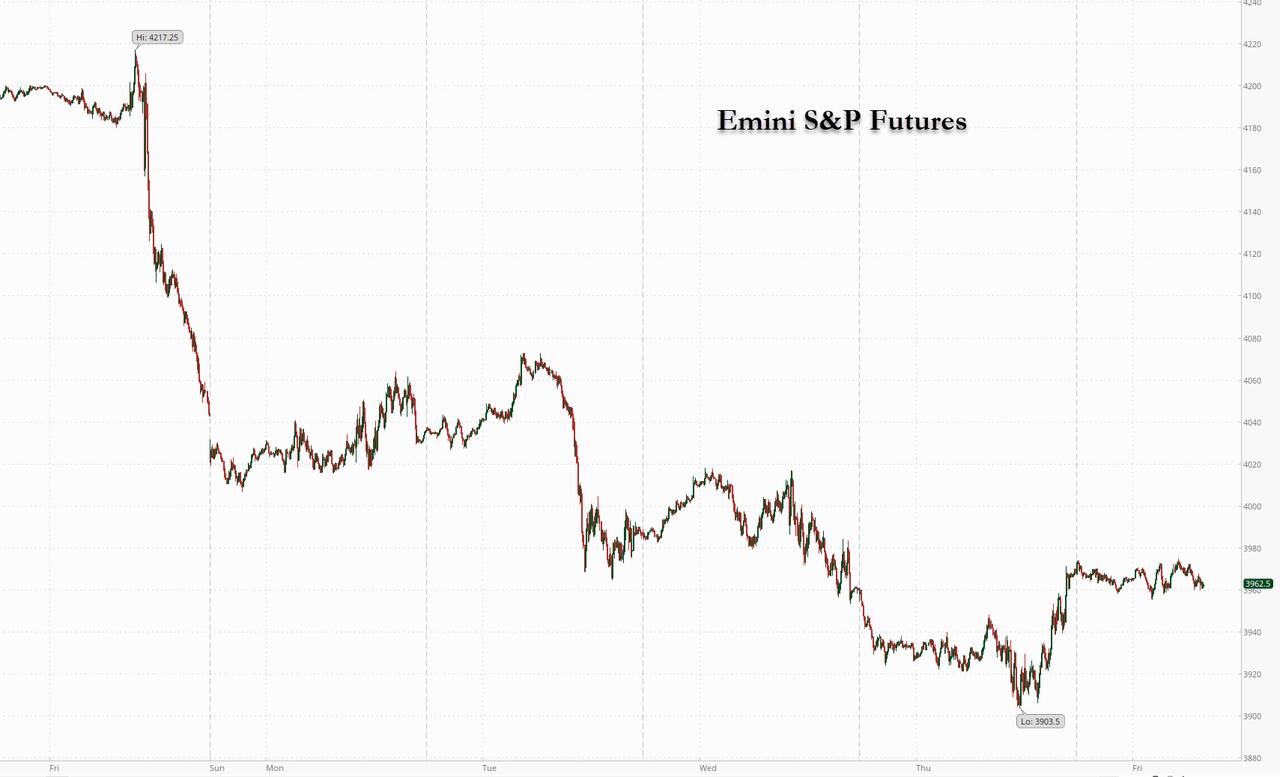

Futures Flat In Muted End To Turbulent Week With All Eyes On Payrolls

US futures dropped on Friday, ending a third straight week of declines, as investors eyed a key jobs report that will be pivotal for this month’s Fed rate hike decision. S&P futures fell 0.2% at 730 a.m. ET, with the underlying cash index down 2.2% this week. Nasdaq 100 futures fell 0.3%, with the tech-heavy index down 2.6% in the previous four days. The dollar index slipped from a record high and the euro strengthened. 10Y yield traded slightly lower, at 3.25%, following yesterday’s spike.

In pre-market trading, Lululemon jumped 10% after raising its full-year outlook. Meanwhile, Bed Bath & Beyond fell as much as 6%, putting the home-goods retailer on track for a weekly loss following its survival plan earlier in the week. Analysts raise PTs on the stock, though some flag higher inventory levels as a note of bearishness. Here are other notable movers:

The outlook for stocks has soured since mid-August after traders ramped up bets that the Fed will continue its aggressive monetary tightening, hurting the economy in the process. The S&P 500 has erased $2 trillion in market capitalization in the past five days, and has given up half of its gains made in the summer rally. Meanwhile, tech stocks have succumbed to rising rates, which are a headwind to the expensive growth sector.

“We don’t have a lot of reasons to be bullish in this type of environment for the next couple of weeks and months,” Meera Pandit, global market strategist at JPMorgan Asset Management, said on Bloomberg Television. “Yet when we think about the longer term perspective and the longer term investor, these are the types of level that can be fruitful in the long run.”

US stocks had outflows of $6.1 billion in the week to Aug. 31 – the biggest exodus in 10 weeks – according to a Bank of America’s Michael Hartnett, adding that investors expect “fast inflation shock, slow recession shock” as nominal growth continues to be boosted by surging consumer prices, fiscal stimulus, large household savings and the impact of the war in Ukraine.

Next up on investor minds is the August jobs report in under an hour, which is expected to show healthy payrolls growth following a stronger-than-expected US manufacturing report. This is how Goldman traders framed what to expect (full preview here): “we are still in a bad is good and vice versa set up for US stocks as Fed has made it clear that they want to see some froth exit the labor market in tandem with cooling inflation: i) Strong print here will clearly make 75bps much more likely on 9/21; ii) Inline print of 300k(ish) will keep pressure on this tape…anything close to last month’s shocking print of 528k would lead to real risk unwind into the wknd (I think at least a 200bp sell off). iii) Sweet spot for stocks tomorrow is a 0 – 100k headline reading…should get a 100+bp rally for S&P in this scenario after this recent drawdown. If we happen to get a negative number an even sharper rally”, and the pivot will be right back on the Q1 calendar.

“The risk of having another additional 75-basis-points hike is high and also to have a big rally on the real rates” depending on the outcome of the jobs report, said Claudia Panseri, a global equity strategist at UBS Global Wealth Management. “Volatility in the equity market will remain quite high until the picture on inflation becomes more clear than it is right now,” she told Bloomberg Television.

In Europe, the Euro 50 rose 0.9%, with Germany’s DAX outperforming peers, adding 1.5%, IBEX lags, rising 0.2%. Autos, financial services and energy are the strongest-performing sectors. Here are the biggest Europen movers:

Earlier in the session, Asian stocks fell, on course for their worst week in more than two months, as the dollar hit a new high amid worries about the Federal Reserve’s aggressive rate-hike path and as lockdowns continued in China. The MSCI Asia Pacific Index declined as much as 0.7%, set for a weekly loss of nearly 4%. TSMC and other tech stocks contributed the most to the benchmark’s drop as Treasury yields climbed, sending the Bloomberg Dollar Spot Index to a record high. Equity gauges in Hong Kong led declines in the region, dragged by the banking and tech sectors. Meanwhile, shares in Japan fell as the yen slipped to a 24-year-low against the dollar. Fresh lockdowns in China are also weighing on sentiment, putting the Asian stock benchmark on track for its third-straight weekly decline. The sell-off reflects broad concerns of an economic slowdown amid weaker manufacturing data in the region’s major tech exporters.

“Dollar momentum sees no sign of breaking,” Saxo Capital Markets strategists including Redmond Wong wrote in a note. “Fresh Covid lockdowns in China, in particular, the full lockdown of Chengdu and extended restriction in Shenzhen, have caused some demand concerns.” Investors will keep a keen eye on the US August jobs report due later Friday to gauge the Fed’s next move in its September meeting. While weak sentiment has kept Asian shares hovering near their two-year lows, hedge-fund giant Man Group said Asian stocks are set to outshine peers next year. The investment firm is betting on defensive stocks in India and Southeast Asia, Andrew Swan, Man GLG’s head of Asia ex-Japan equities, said in an interview

Japanese stocks fell as investors awaited key US employment figures and assessed the yen’s decline to a 24-year low against the dollar. The Topix Index dropped 0.3% to 1,930.17 as of the market close in Tokyo, while the Nikkei 225 was virtually unchanged at 27,650.84. Sony Group contributed the most to the Topix’s decline, decreasing 1.1%. Out of 2,169 stocks in the index, 738 rose and 1,307 fell, while 124 were unchanged. “The US jobs report won’t be very positive no matter what’s out,” said Tatsushi Maeno, a senior strategist at Okasan Asset Management. “If it’s strong, the FOMC will lean toward a 0.75% rate hike and on the other hand, if it’s weak, there could be talk of a recession.”

India’s benchmark equities index closed slightly higher, after swinging between gains and losses several times throughout the session, as investors tried to gauge the impact of the US Federal Reserve’s hawkish stance in a week marked by volatility. The S&P BSE Sensex rose 0.1% to 58,803.33 in Mumbai, but ended lower for a second consecutive week. The NSE Nifty 50 Index was little change on Friday. Housing Development Finance Corp and HDFC Bank provided the biggest support to the Sensex, which saw 19 of its 30 member stocks ending lower. Thirteen of the 19 sector indexes compiled by BSE Ltd. declined, led by a measure of oil and gas companies. “The effect of Jackson Hole is still revolving across financial markets, with a soaring dollar and falling equities as the main themes,” Prashanth Tapse, an analyst at Mehta Securities, wrote in a note.

In FX, the greenback fell against all of its Group-of-10 peers except the yen. The euro rose a fourth day in five against the greenback, to edge above parity. The pound languished near the lowest since March 2020 versus the dollar. Investors awaited the results of a vote to choose the country’s next prime minister on Monday, with expected winner Liz Truss aiming to cut taxes and increase borrowing. The Norwegian krone outperformed, and rebounded from a six-week low versus the greenback, amid a recovery in oil prices before an OPEC+ meeting on supply at which Saudi Arabia could push for output cuts. The yen weakened past 140 per dollar after a slight rally in Asian trading faded.

In rates, treasuries were little changed while European bonds slipped. The 10-year Treasury yield held steady near 3.26%; while gilts 10-year yield is up 2.6bps around 2.90% and bunds 10-year yield is up 2bps to 1.58%.

In commodities, WTI crude futures rebound 3% to around $89, within Thursday’s range; oil pared gains after news that the Group of Seven most industrialized countries is poised to agree to introduce a price cap for global purchases of Russian oil, while Russia looks set to resume gas supplies through its key pipeline. Gold rose $6 to around $1,704. Meanwhile, zinc headed for its biggest weekly loss in over a decade on concern Chinese demand will be hamstrung by new virus restrictions.

Bitcoin has reclaimed the USD 20k mark but the upward move is yet to gain any real traction amid the broader contained price action.

Looking to the day ahead now, the main highlight will be the US jobs report for August. Otherwise on the data side, there’s US factory orders for July and Euro Area PPI for July.

Market Snapshot

Top Overnight News from Bloomberg

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were indecisive with price action relatively rangebound after the mixed lead from the US and with the region lacking firm commitment as participants await the upcoming US NFP jobs data. ASX 200 was lacklustre as earnings releases quietened and with strength in financials offset by losses across the commodity-related sectors. Nikkei 225 traded subdued amid underperformance in large industrials although losses in the index were stemmed by retailers after several reported strong August sales. Hang Seng and Shanghai Comp were mixed as Hong Kong underperformed amid notable losses in developers and with the mainland choppy but ultimately kept afloat after the PBoC recently cut rates on its Standing Lending Facility by 10bps from August 15th and after several officials pledged measures.

Top Asian News

European bourses are firmer across the board as hawkish yield action in the EZ has eased from yesterday’s recent peaks, Euro Stoxx 50 +0.8%. Stateside, futures are contained and flat with all focus on the NFP report. Alphabet’s Google (GOOG) is planning to accept the use of third-party payment services on its smartphone app in national such as Japan and India but not the US, according to the Nikkei

Top European News

FX

Fixed Income

Commodities

US Event Calendar

DB’s Jim Reid concludes the overnight wrap

If I’m not here on Monday it’s not impossible that I’ve been eaten by a snake or a small crocodile, or poisoned by a tarantula. For our twins’ 5th birthday party this weekend we’ve hired a professional reptile handler to come round and show 30-40 overexcitable kids some interesting animals. If I’m not eaten or bitten I’m a bit worried he won’t do the full register on the way out and I’ll be left with a huge lizard hiding in my bed. All I can say is that for my 5th birthday party we just had pin the tail on the donkey and a few stale sandwiches. Life was so much simpler then.

Markets are pretty complicated at the moment with investors not being quite able to decide whether the newsflow was bad or good yesterday for risk assets. We went to both extremes with the US rallying back into positive territory by the close (S&P 500 +0.30% having been -1.23% just after Europe logged off). As the US starts it’s day a bit later we’ll have a fresh payroll print to throw into the mix which could be the swing factor between 50 and 75bps at the September Fed meeting.

Last month’s strong print ratcheted up expectations that the Fed could hike by 75bps for a third meeting in a row, and markets are still pricing that as the more likely outcome than 50bps, with futures now pricing in +67.7bps worth of hikes. In terms of what to expect today, our US economists are looking for +300k growth in nonfarm payrolls, which should be enough to keep the unemployment rate at its current 3.5%.

Ahead of that, the US labour market data we got yesterday was pretty good, continuing the run of decent releases over recent days. Initial jobless claims for the week through August 27 unexpectedly fell back to 232k (vs. 248k expected), and the previous week was also revised down by -6k. That’s the third week in a row that the jobless claims have fallen, marking a change from the mostly upward trend we’ve seen since late March. On top of that, the ISM manufacturing release also surpassed expectations, remaining at 52.8 (vs. 51.9 expected), with the employment component at a 5-month high of 54.2 (vs. 49.5 expected).

Treasuries lost significant ground on the day, even before the data, with the 2yr yield rising +1bps to hit another post-2007 high of 3.50%, whilst the 10yr yield rose +6bps to 3.25%. The moves were driven by higher real yields across the curve, with the 5yr real yield hitting a 3-year high of 0.849%. It was a similar story in Europe too, where yields on 10yr bunds (+2.2bps), OATs (+2.5bps) and BTPs (+3.3bps) rose. Those European moves came as investors grew increasingly confident that the ECB would hike by 75bps at some point this year, which was aided by the latest data that showed Euro Area unemployment fell to a new low of 6.6% in July. That’s the lowest level since the single currency’s formation, and means that the latest data is showing that the Euro Area simultaneously has the highest inflation and the lowest unemployment of its existence.

As discussed at the top, US equities turned round late in the session with the Nasdaq nearly making it back into the green (-0.26%) as well as the S&P after being -2.28% at 6pm London time. This was too late to save the European session as the STOXX 600 (-1.80%) took a significant hit. Sentiment was pretty downbeat from the outset after the lockdown of the Chinese city of Chengdu (population 21m) risked further disruption to supply chains and global economic demand. That said, the energy situation continued to develop in a positive direction, with German power prices for next year coming down by a further -9.11% to €523.40 per megawatt-hour. In fact they have halved since their intraday peak on Monday when they hit €1050, which just shows how amazingly volatile this market is right now. The EU is considering various interventions to deal with the current turmoil, including price caps and windfall taxes, and Commission President Von der Leyen is set to outline the measures in her State of the Union address on September 14.

Staying on commodities, the decline in oil prices continued yesterday thanks to fears of further Chinese lockdowns and hawkish central banks. Brent crude was down -4.28% to $92.36/bbl, which is a substantial decline since its closing level on Monday of $105.09/bbl. As we go to print, crude oil prices are showing some recovery with Brent futures +1.91% higher at $94.12/bbl. There was a similar negative pattern among industrial metals, with copper (-2.96%) down for a 5th day running on the back of those same fears about demand. Meanwhile in the precious metal space, gold (-0.79%) slipped below $1700/oz, while hitting its lowest since July intraday as markets priced higher interest rates, thus raising the opportunity cost of holding a non-interest-bearing asset.

Over in the FX space, a number of new milestones were reached yesterday, most notably a rise in the dollar index (+0.91%) to levels not seen since 2002. The greenback was supported yesterday by the strong data that added to expectations the Fed would keep hiking into next year, although the reverse picture was that the Euro fell back beneath parity against the dollar, and the Japanese yen fell to 140 per dollar for the first time since 1998. In Asia’ morning trade, the Japanese yen further weakened, touching 140.26 per US dollar. Here in the UK, sterling also fell just beneath the $1.15 mark in trading for the first time since March 2020.

In Asia this morning, the Nikkei (-0.21%), the Hang Seng (-0.58%), and the CSI (-0.20%) are trading lower with the Shanghai Composite (+0.28%) bucking the trend. Elsewhere, the Kospi (+0.04%) is struggling to gain traction after South Korea’s headline inflation slowed after six months of accelerating (more below).

Moving ahead, US stock futures are fairly flat with contracts on the S&P 500 (-0.08%) and NASDAQ 100 (-0.04%) treading water.

Early morning data showed that Korea’s inflation eased to +5.7% y/y in August (v/s +6.1% expected) from +6.3% in July as energy prices eased. MoM prices dropped -0.1% in August (v/s +0.3% expected) after rising +0.5% in the prior month thus providing some comfort to the Bank of Korea (BoK) in its yearlong tightening cycle.

Rounding off yesterday’s data, there was plenty to digest from the global manufacturing PMIs, although they mostly confirmed the picture from the flash readings we’d already got. In the Euro Area, the reading came in at 49.6 (vs. flash 49.7), and the US had a 51.5 reading (vs. flash 51.3). The UK had a stronger revision up to 47.3 (vs. flash 46), but it was still in contractionary territory and the lowest since May 2020. Elsewhere, German retail sales grew by +1.9% (vs. -0.1% expected).

To the day ahead now, and the main highlight will be the US jobs report for August. Otherwise on the data side, there’s US factory orders for July and Euro Area PPI for July.

Tyler Durden

Fri, 09/02/2022 – 07:52

via ZeroHedge News https://ift.tt/qPAuYvt Tyler Durden

“Good News Is Bad News” Dynamic Won’t Last Much Longer

By Simon White, Bloomberg Markets Live commentator and reporter

Recent better-than-expected US data has been bad for stocks and bonds as a less accommodative Fed leads to higher yields and lower stock prices. But that dynamic might soon reverse, as leading indicators point to a significant deterioration in growth through the rest of the year.

This week jobless claims, the headline ISM and the Conference Board’s consumer confidence have all exceeded expectations. Today we will also get the latest update for employment, with last month’s data delivering a big upside surprise.

The market is treating good news as bad news, as positive economic data is leading to higher shorter and longer-term yields, and thus causing stocks to drop.

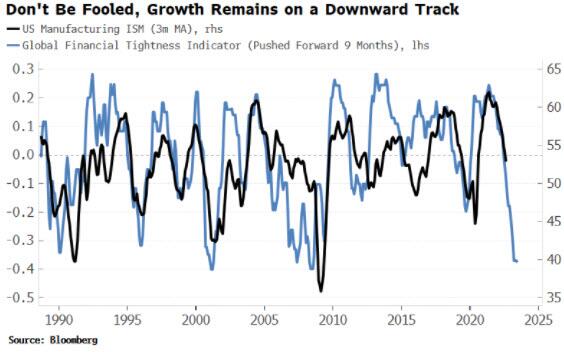

But don’t expect this to persist for much longer. Global financial conditions remain very restrictive. The Global Financial Tightness Indicator is very low, which anticipates the downward trend in the manufacturing ISM — a proxy for growth overall — will continue apace.

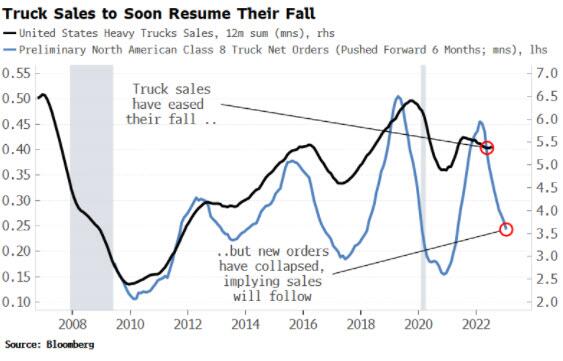

Truck sales are an excellent leading barometer of economic activity. Almost two-thirds of the dollar value of North American freight is moved by trucks. The fall in truck sales has been leveling off, but is likely to resume given the slump in truck new orders. This presages weaker economic activity ahead in the US.

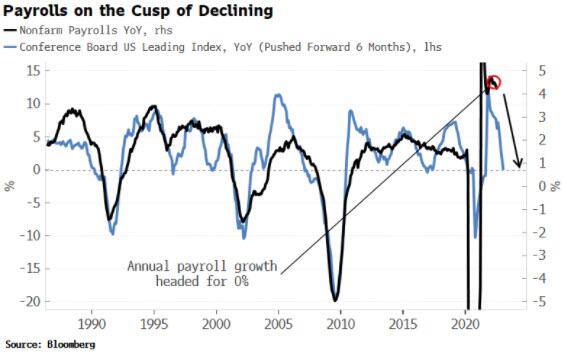

Payrolls is out later today, with last month’s data showing a huge upside surprise. But the same goes here: data should soon resume a downward track. The Conference Board’s Leading Index anticipates the y/y payroll growth will be flat by early next year, from over 4% currently.

Any recent let-up in economic data should be seen as a pause rather than a reprieve. The interim move lower in yields should soon re-assert itself, taking some pressure off equities.

However, the bigger picture is that bonds face more risk to the downside than the upside as it becomes apparent inflation is entrenched. Further, while liquidity remains poor and global financial conditions tight, stocks remain mired in a bear market, meaning a sustainable rally is off the cards, steep sell-offs are an ongoing risk, and the VIX should stay elevated.

Tyler Durden

Fri, 09/02/2022 – 07:40

via ZeroHedge News https://ift.tt/6YNIqFW Tyler Durden