Earlier today, USA Today published my new op ed on federalism and the coronavirus crisis. Here is an excerpt:

President Donald Trump provoked widespread criticism last week when he claimed he had “total” authority to reopen the economy, thereby overriding lockdown orders issued by numerous state governments. Democratic governors, such as Andrew Cuomo of New York, pushed back, arguing that such use of federal power would be “a total abrogation of the Constitution,” which leaves such decisions to the states.

More recently, the White House issued guidelines for reopening that are merely advisory. But Trump has not repudiated previous assertions of total authority and could potentially resort to them again if states do not act as he wishes.

At the same time, however, others on the left contend that the coronavirus crisis justifies weakening constitutional constraints on federal power, so as to ensure a cohesive national policy. For example, University of Illinois law school Dean Vikram Amar argues that constraints on federal power to regulate interstate commerce unjustifiably prevent the federal government from ordering a nationwide lockdown, and could also block it from requiring mandatory vaccination of all Americans when and if a vaccine becomes available. Others also argue against constitutional barriers to a comprehensive nationwide lockdown enforced by the federal government and a federal vaccination mandate.

If such arguments prevail, they will set a dangerous precedent. In a time of crisis, it is tempting to assume that we need to concentrate power as much as possible. But centralization can often make things worse rather than better. Moreover, consolidations of power that arise during crises often continue long afterwards.

I previously wrote about federalism and the coronavirus crisis here.

from Latest – Reason.com https://ift.tt/3amQMWL

via IFTTT

Earlier today, USA Today published my new op ed on federalism and the coronavirus crisis. Here is an excerpt:

President Donald Trump provoked widespread criticism last week when he claimed he had “total” authority to reopen the economy, thereby overriding lockdown orders issued by numerous state governments. Democratic governors, such as Andrew Cuomo of New York, pushed back, arguing that such use of federal power would be “a total abrogation of the Constitution,” which leaves such decisions to the states.

More recently, the White House issued guidelines for reopening that are merely advisory. But Trump has not repudiated previous assertions of total authority and could potentially resort to them again if states do not act as he wishes.

At the same time, however, others on the left contend that the coronavirus crisis justifies weakening constitutional constraints on federal power, so as to ensure a cohesive national policy. For example, University of Illinois law school Dean Vikram Amar argues that constraints on federal power to regulate interstate commerce unjustifiably prevent the federal government from ordering a nationwide lockdown, and could also block it from requiring mandatory vaccination of all Americans when and if a vaccine becomes available. Others also argue against constitutional barriers to a comprehensive nationwide lockdown enforced by the federal government and a federal vaccination mandate.

If such arguments prevail, they will set a dangerous precedent. In a time of crisis, it is tempting to assume that we need to concentrate power as much as possible. But centralization can often make things worse rather than better. Moreover, consolidations of power that arise during crises often continue long afterwards.

I previously wrote about federalism and the coronavirus crisis here.

from Latest – Reason.com https://ift.tt/3amQMWL

via IFTTT

Belgium’s number, which just passed 500 deaths per million, is the highest of any substantially sized country. (I set aside tiny San Marino, in which the rate is more than double that.) In the U.S., this would be equivalent of about 160,000 deaths, rather than the 40,000 we’ve suffered so far, though of course we should keep in mind the possibility that different countries’ numbers are hard to compare because of different reporting practices. And while it looks like the Belgian death rate is not increasing any more, and may even have begun to decline, there still seem to likely be many more deaths to come.

from Latest – Reason.com https://ift.tt/2VGt2HX

via IFTTT

Over the past few weeks, state governments across the Land of the Free have been feverishly proposing new legislation that will virtually guarantee the entire insurance industry is wiped out.

The root of the issue has to do with something called business interruption insurance.

Business interruption is a pretty common type of insurance that’s designed to protect business owners against a number of risks.

For example, let’s say you own a restaurant and you have a bad kitchen fire that forces you to shut down for a month.

You’d most like have a fire insurance policy to cover the direct damage of the fire. And a lot of companies would also have a business interruption policy to help them stay afloat during that one-month period while the business is closed for repairs.

But business interruption insurance has certain exclusions. It’s just like any other policy, and the insurers are very clear about what risks they do/do not cover.

A typical homeowner’s insurance policy, for example, covers your home against risks like theft, fire, and vandalism.

But most homeowner’s policies specifically exclude flooding. So any homeowner who wants to protect their homes from the risk flood damage can purchase a separate flood insurance policy.

Many insurance plans, including business interruption policies, also tend to exclude things like damage caused by war, government action, and “acts of God”.

But again, any business that wants to insure against those risks is free to seek additional coverage.

That’s the whole idea of insurance: customers are able to pick and choose which risks they want to insure against, and which risks they’re willing to take.

It’s fair to say that most business interruption policies don’t cover a worldwide pandemic that shuttered the entire global economy.

But there’s a growing trend now where state governments are proposing new legislation that would RETROACTIVELY force insurance companies to protect their policyholders against Covid.

This is totally nuts. The state governments are the ones that forced businesses to shut down.

Now they expect the insurance companies to pay for the consequences, even though the policies specifically state that they don’t cover this type of risk.

They might as well demand pay for every other uninsured hazard. Did your house flood and you didn’t have flood insurance? Well let’s retroactively force the insurance companies to pay for that too.

Pennsylvania, New York, Illinois, New Jersey, and several other states have proposed similar legislation, or threatened regulatory action.

(This trend is also picking up steam overseas; in the UK, for example, lawsuits are already pending against insurance companies for not paying out Covid-related claims.)

And given that just about EVERY business would qualify for this retroactive Covid coverage, there’s simply no way that the insurance industry would be able to afford such an indemnity.

Think about it– the federal government made $350 billion worth of loans available to small businesses earlier this month, and that money was 100% used up in about 2 weeks. And they just agreed on another $300 billion this morning.

So most insurance companies would be wiped out if this legislation passes… i.e. CUE THE GOVERNMENT BAILOUT of the insurance industry.

Just like airlines, hotels, hospitals, etc., the insurance company would be standing in line to suckle on that sweet taxpayer bailout teet, probably to the tune of another half-trillion dollars.

Of course, it goes without saying that the government doesn’t have the money for any this.

We’ve explored the government balance sheet many times in the past: Uncle Sam is already in the hole by MINUS $23 trillion according to the Treasury Department’s most recent financial statements.

And, over the last few years, even when the economy was incredibly strong, the federal government still managed to lose more than a trillion dollars a year.

Now that they have a real crisis to contend with, the deficit is going to swell to an unimaginable figure.

Frankly it doesn’t matter whether or not the insurance companies end up footing the bill.

If the insurance companies re forced to pay up, the government will likely bail them out. Otherwise the government will bail out businesses directly.

Either way, it’s pretty obvious the government is going to spend an unbelievable amount of money they don’t have… which means the central bank (Federal Reserve) will keep printing more money.

That’s how the system works: whenever the government wants to bail someone out, the Federal Reserve first conjures the bailout money out of thin air, and then ‘loans’ it to the Treasury Department.

Crazy, right?

The Federal Reserve has already printed trillions of dollars since this crisis started, and that may only be the warm-up round.

The longer this lasts, the more money they’re going to print… and the more they’ll end up debasing the currency.

We are obviously living in extraordinary times, and it’s perfectly reasonable to hope for the best.

But it would be irresponsible to willfully ignore what the government and central bank are doing here.

Conjuring infinite amounts of money out of thin air could have incredibly destructive consequences on the currency.

And that’s why, as I’ve written before, it’s definitely time to consider owning some real assets.

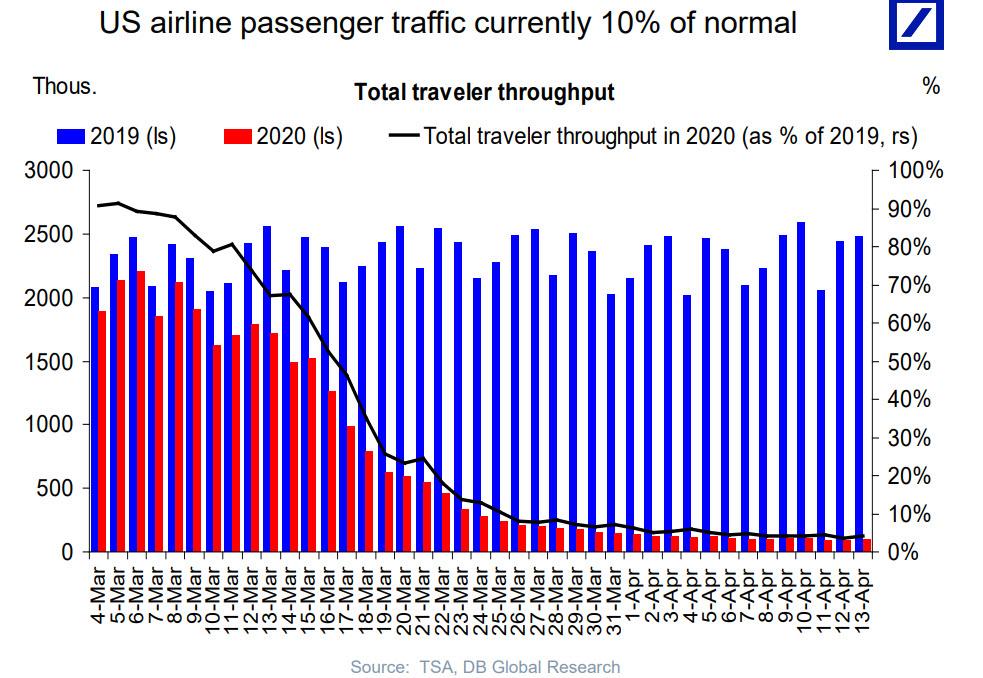

United Reports $2.1BN Loss As Airlines Brace To Fire 100,000 Once Bailout Loans Expire

United Airlines confirmed the carnage hitting US airlines today when it reported a $2.1 billion loss for first quarter as the coronavirus pandemic drove travel demand down to the lowest level in decades.

United said revenue plunged 17% in the first quarter from a year ago to $8 billion which as a reminder is largely due to the collapse in traffic in just the second half of March, so one can imagine what happens in all of Q2 should the situation fail to normalize.

With revenues unlikely to return any time soon even as losses mount, the Chicago-based airline said it applied for up to $4.5 billion in government loans on top of about $5 billion federal payroll grants and loans it also expects to receive to weather the crisis. As CNBC details, United was the first major U.S. airline to detail the results — while they are preliminary — of the virus on its results in the first three months of the year. The disease and harsh measures to stop it from spreading such as stay-at-home orders has ravaged air travel demand and and prompted carriers to slash most of their flights.

And as US airlines face a bleak future of depressed traffic and volatile revenue well into 2021, they are preparing to cut costs to the bone. As Bloomberg reports, the next big crunch date for airlines is this fall, when billions of dollars in government assistance will come to an end. As a result, key carriers including Delta and United have already begun openly contemplating how they will shrink operations, and one analyst expects that as many as 105,000 jobs could be lost industrywide.

“Without a quick improvement in demand, we could see the airlines look to shed 800 to 1,000 aircraft, which could result in a reduction of 95,000 to 105,000 airline jobs,” Cowen analyst Helane Becker wrote in an April 13 client note. “The rightsizing of the fleet and work force is an unfortunate truth.”

“The challenging economic outlook means we have some tough decisions ahead as we plan for our airline, and our overall workforce, to be smaller than it is today,” United’s chief executive and president, Oscar Munoz and Scott Kirby, wrote in an April 15 employee memo.

As a reminder, under the terms of the $50 billion government bailout, airlines are barred from slashing jobs through Sept. 30 but they’re already warning employees that cuts are almost inevitable. The planned contraction reflects a widespread belief that 2020 revenues could shrink to levels not seen in years. Recovery will probably be a long-term affair, said Cowen & Co., which predicted that ticket sales may not rebound to pre-pandemic levels until 2025.

A traveler checks in at an otherwise empty American Airlines counter inside San Francisco International Airport on April 2.

Unable to cut jobs or salaries while receiving grants to cover payroll, airlines will staff their typical summer peak largely as usual, even with millions of fewer travelers. But come fall, it will get ugly for employees unless the government bailout is rolled into 2021. “We’re going to be smaller coming out of this,” Delta CFO Paul Jacobson told employees last month. “Certainly quite a bit smaller than when we went into it.”

The upcoming mass layoffs will add to 87,000 employees – more than one quarter of the Big Three airlines’ workforce – who have taken voluntary leaves, early retirement or reduced work hours in the past two months.

Carriers face “the worst cash crisis in the history of flight,” with booked revenues down 103% year over year, according to industry lobby Airlines for America. Domestic flights are averaging just 10 passengers while international flights average 24, the group said.

Once laid off, those employees have years of unemployment to look forward to.

While airlines foresee an uptick in bargain-hunting leisure travelers this summer, rich travelers will take longer to win back. Corporations will be reluctant to assume the liability of putting employees back in the sky with Covid-19 still in wide circulation. Plus, many companies have learned to function via video conference—which is a lot cheaper than a business class seat.

According to Bloomberg, the airline industry generally has taken three to four years to fully recover from major disruptions, said Samuel Engel, head of the aviation group at consultant ICF. Economic downturns often accelerate trends that were already underway, like pulling down marginal routes and, more recently, the decline in demand for large aircraft, he said.

“The last couple of years, you have seen extensions of flights toward end of day and early morning, and growth of long, thin routes to secondary cities in Asia,” he said. “Those types of things get pulled back, and some don’t reappear until quite late in the economic cycle.”

“Gradual inflation has a numbing effect. It impoverishes the lower and middle class, but they don’t notice.”

– Andrew Bosomworth, PIMCO Germany, as quoted in Der Spiegel

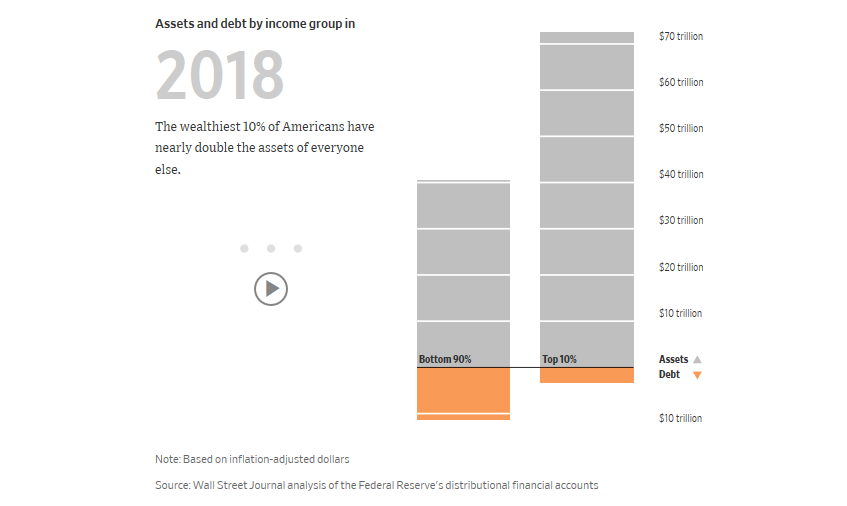

The rise of populism, evidenced by the success of Donald Trump, Bernie Sanders, and Alexandra Ocasio-Cortez, is rooted in the emergence of the greatest wealth and income inequality gap since the roaring ’20s.

According to the Economic Policy Institute, the top 1% take home 21% of all income in the United States, the largest share since 1928.

There are a variety of social, political, and economic factors driving this growing discrepancy, but one critical factor is ignored – The Federal Reserve.

The Fed has inserted itself into a key role in economic growth and, along with that, their contribution to the rising imbalances between economic classes.

The Wealth Gap Explodes

Over the last decade, as stock markets surged, household net worth reached historic levels. If one just looked at the data, it was clear the economy was booming.

However, for the vast majority of Americans, it really wasn’t. This was previously shown in data from the WSJ:

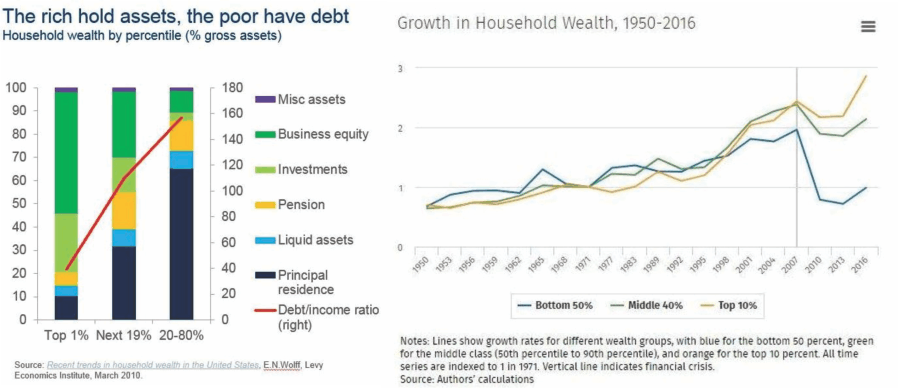

“The median net worth of households in the middle 20% of income rose 4% in inflation-adjusted terms to $81,900 between 1989 and 2016, the latest available data. For households in the top 20%, median net worth more than doubled to $811,860. And for the top 1%, the increase was 178% to $11,206,000.”

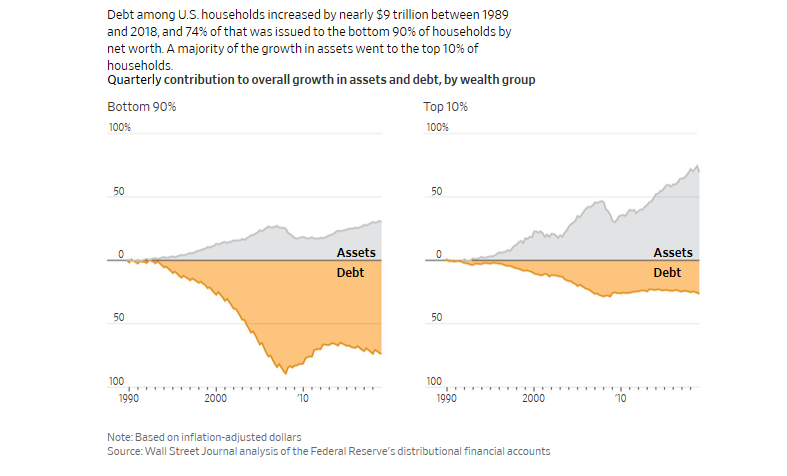

Put differently, the value of assets for all U.S. households increased from 1989 through 2016 by an inflation-adjusted $58 trillion. A full 33% of that gain—$19 trillion—went to the wealthiest 1%, according to a Journal analysis of Fed data.

What policy-makers, and the Federal Reserve missed, is the “stock market” is NOT the “economy.”

This “wealth gap,” can be directly traced back to a decade of monetary policy that almost solely benefited those who either had money to invest in the financial markets or were directly compensated through increases in corporate asset prices. However, those policies failed to produce substantial rates of either wage growth or full-time employment.

“But Lance, the media said that employment was at historic lows.”

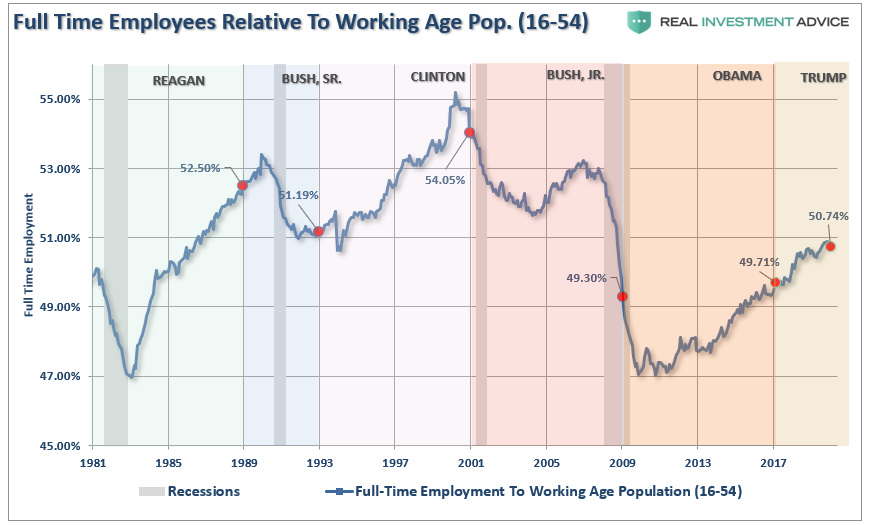

True, but this was because of a large number of individuals no longer counted as part of the labor force. If we take a look at “full-time employment,” which are the jobs supporting families, and strip out those over 54-years of age to remove the “but boomers are all retiring” nonsense, we see a very different picture of employment. The weak increase in full-time employment is a key factor behind why both economic and wage growth remained weak.

The New York Times recently went further into the numbers:

“America’s economy has almost doubled in size over the last four decades, but broad measures of the nation’s economic health conceal the unequal distribution of gains. A small portion of the population has pocketed most of the new wealth, and the coronavirus pandemic is laying bare the consequences of the unequal distribution of prosperity.”

Of course, a big contributor to the “wealth gap” was the rise in the stock market fostered by trillions of liquidity injected into the markets by Federal Reserve. As NYT noted:

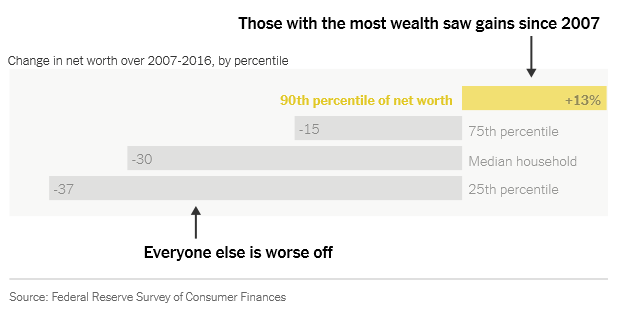

“The affluent, of course, do tend to own stock, and the median net worth of the richest 10 percent of households rose 13 percent from 2007 to 2016 (the last year for which the Fed has released data).

Another way to view this issue is by looking at household net worth growth between the top 10% and everyone else.

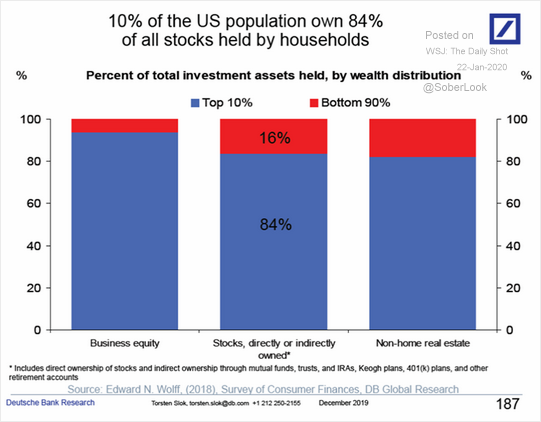

Since 2007, the ONLY group that has seen an increase in net worth is the top 10% of the population, which is also the group that owns 84% of the stock market.

This is not economic prosperity.

This is a distortion of economics.

The Fed Did It

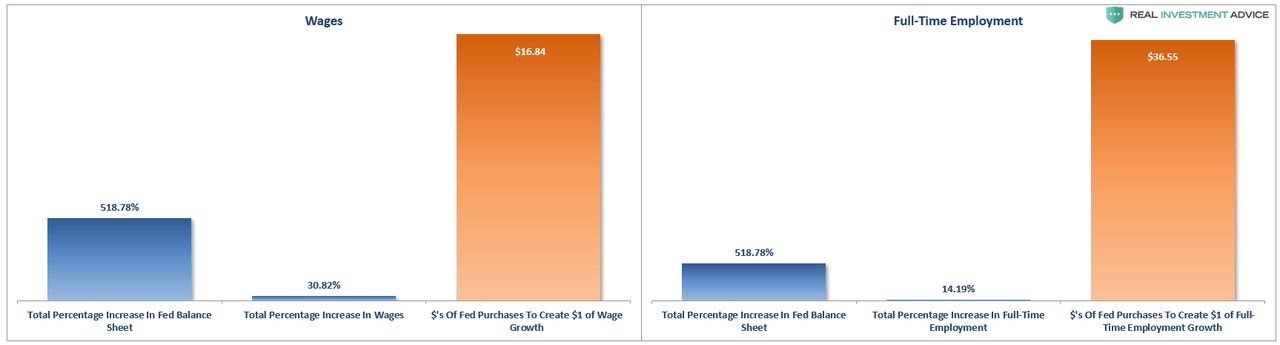

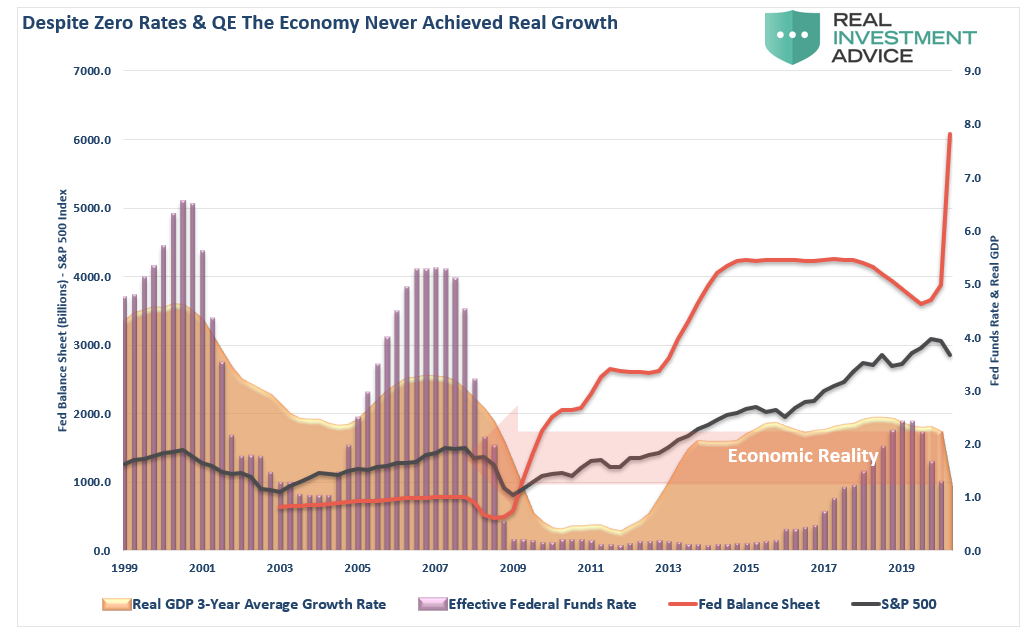

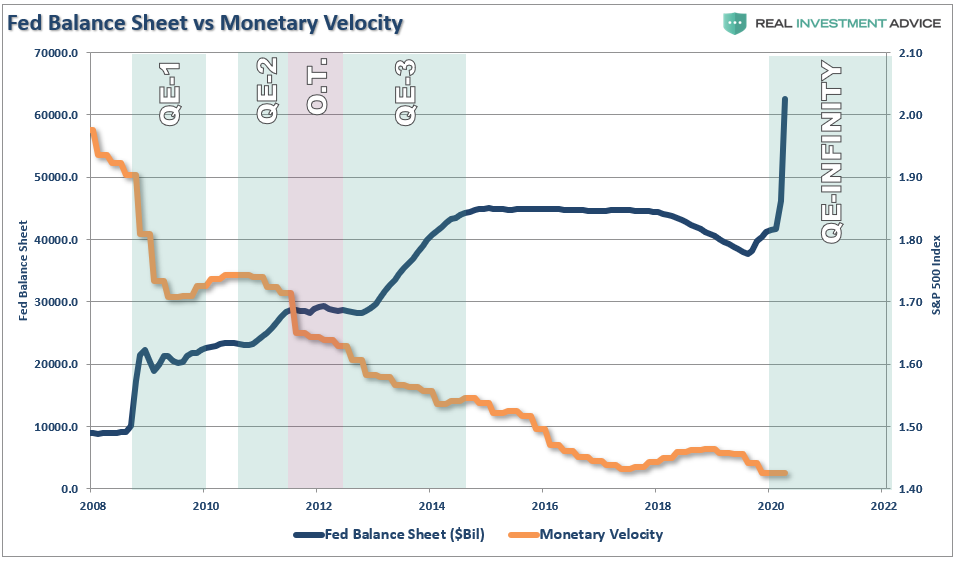

This can all be tied directly back to the Fed’s monetary interventions. From 2009-2016, the Federal Reserve held rates at 0%, and flooded the financial system with 3-consecutive rounds of “Quantitative Easing” or “Q.E,” and ensured that financial conditions remained extremely accommodative. In return, banks were supposed to use the low-rate environment to loan money to businesses, which would in turn expand capacity and hire workers, who would increase consumption boosting economic growth.

Unfortunately, it didn’t work out that way as monetary policy is a “disincentive” for banks to lend. Instead, liquidity was recycled into the stock market, through which they have a direct and vested interest. While stock prices rose, the bottom 90% of the economy struggled to make ends meet, which capped economic growth.

Of course, given the banks didn’t push the money into the economy, but bottled it up for their own financial interests, monetary velocity steadily declined.

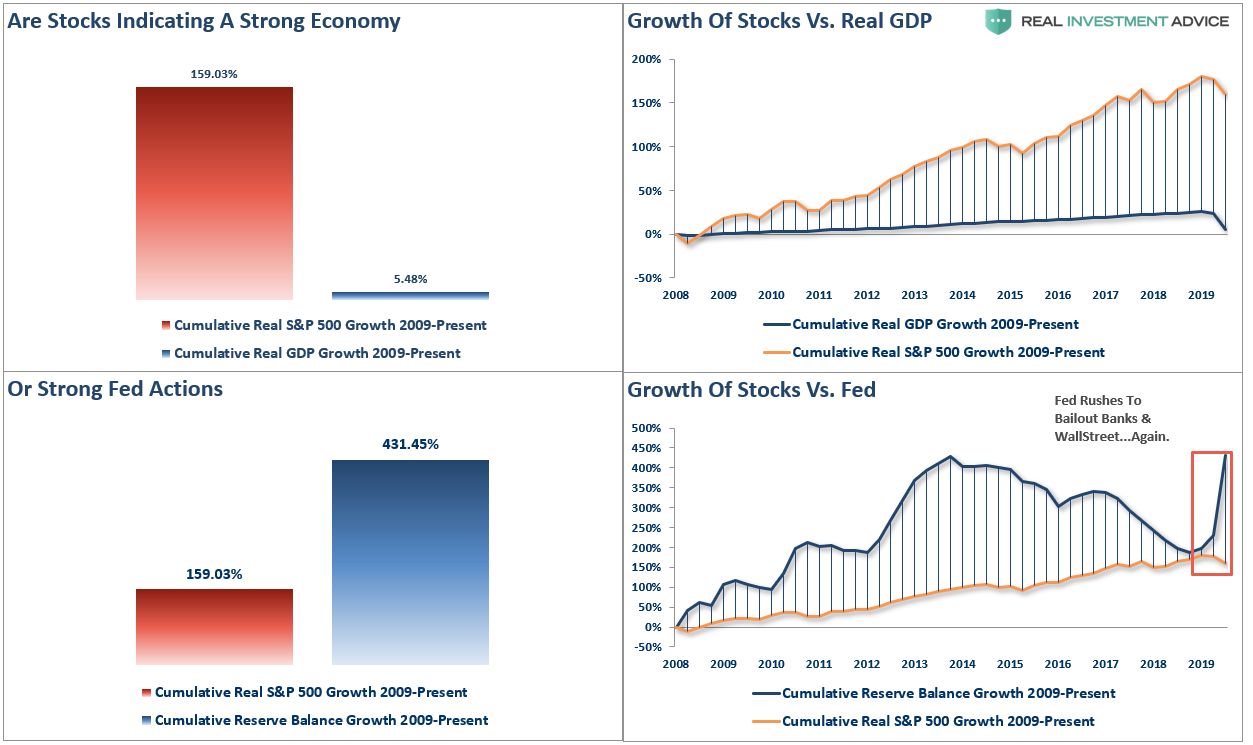

If we assume a 15% decline in GDP in the second quarter, the disparity between the Fed’s interventions, the stock market, and the real economy becomes abundantly clear. For 90% of Americans, there has not been, nor will there be, any economic recovery.

Not understood, especially by the Fed, is that the natural rate of economic growth is declining due to their very practices.

“Low, to zero, interest rates incentivize non-productive debt. The massive increases in debt, and particularly corporate leverage, actually harms future growth by diverting spending to debt service.”

The rise in corporate debt, which in the last decade was used primarily for non-productive purposes such as stock buybacks and issuing dividends, has contributed to the retardation of economic growth.

The Federal Reserve Act requires that monetary policy achieve maximum employment, stable prices, and moderate long-term interest rates. The problem is the Fed targeted a small, but consistent 2% rate of inflation. What they didn’t realize was those policies were creating a debt bubble which slowed economic growth and created deflationary pressures. The result was an increasing set of dynamics which harmed the poor and middle class while enriching the wealthy, and widened the inequality gap.

The Fed Has No Choice But To Make It Worse

With the economy now on the brink of an “economic depression,” and in the middle of an election year, the Federal Reserve had a choice to make.

Allow capitalism to take root by allowing corporations to fail, and restructure, after spending a decade leveraging themselves to hilt, buying back shares, and massively increasing the wealth of their executives while compressing the wages of workers. Or,

Bailout the “bad actors” once again to forestall the “clearing process” that would rebalance the economy, and allow for higher levels of future organic economic growth.

Obviously, as the Fed’s balance sheet heads toward $10 Trillion, the Fed opted to impede the “clearing process.”By not allowing for debt to fail, corporations to be restructured, and “socializing the losses,” they have removed the risk of speculative practices and have ensured a continuation of “bad behaviors.”

Unfortunately, given we now have a decade of experience of watching the “wealth gap” grow under the Federal Reserve’s policies, the next decade will only see the “gap” worsen.

While there are many hoping for a “V-shaped” recovery in the economy following the “restart” of the economy, the reality is that recovery may take much longer than expected.

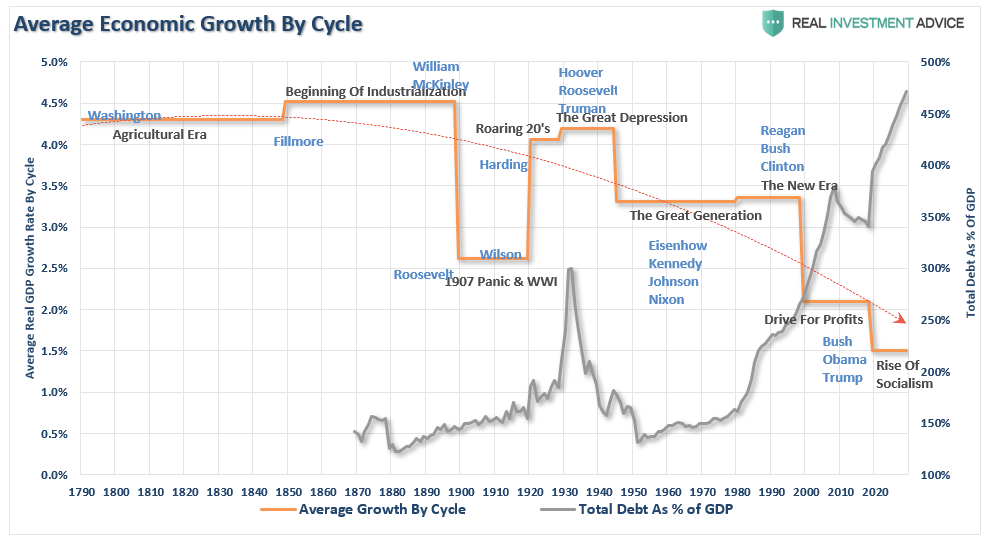

Furthermore, given that we now know that surging debt and deficits inhibit organic growth, the massive debt levels being added to the backs of taxpayers will only ensure lower long-term rates of economic growth. The chart below shows the 10-year annualized run rates of economic growth throughout history with projected debt and growth levels over the next decade.

History is pretty clear about future outcomes from the Fed’s current actions. More importantly, these actions are coming at a time where there were already tremendous headwinds plaguing future economic growth.

A decline in savings rates

An aging demographic

A heavily indebted economy

A decline in exports

Slowing domestic economic growth rates.

An underemployed younger demographic.

An inelastic supply-demand curve

Weak industrial production

Dependence on productivity increases

The lynchpin, like Japan, remains demographics and interest rates. As the aging population grows becoming a net drag on “savings,” the dependency on the “social welfare net” will continue to expand. The “pension problem” is also going to require further bailouts and more government debt.

Yes, another $4-6 Trillion in QE will likely be successful in inflating a third “bubble” to counteract the deflation of the last.

The problem is that after a decade of pulling forward future consumption to stimulate economic activity, a further expansion of the wealth gap, increased indebtedness, and low rates of economic growth, will weigh on future economic opportunity for the masses.

Supporting economic growth through increasing levels of debt only makes sense if “growth at all cost” uniformly benefits all citizens. Unfortunately, we are finding out there is a big difference between growth and prosperity.

An inflationary policy that minimizes concern for debt burdens, while accelerating the growth of those burdens, is taking a serious toll on economic and social stability.

The United States is not immune to social disruptions. The source of these problems is compounding due to the public’s failure to appreciate why it is happening. Until the Fed’s policies are publicly discussed and reconsidered, the policies will remain, and the problems will grow.

But for now, it seems the Fed simply has no other choice.

Belgium’s number, which just passed 500 deaths per million, is the highest of any substantially sized country. (I set aside tiny San Marino, in which the rate is more than double that.) In the U.S., this would be equivalent of about 160,000 deaths, rather than the 40,000 we’ve suffered so far, though of course we should keep in mind the possibility that different countries’ numbers are hard to compare because of different reporting practices. And while it looks like the Belgian death rate is not increasing any more, and may even have begun to decline, there still seem to likely be many more deaths to come.

from Latest – Reason.com https://ift.tt/2VGt2HX

via IFTTT

By a vote of 6-3, the U.S. Supreme Court held that the Constitution requires unanimous jury verdicts for convictions in criminal cases. Writing for the Court in Ramos v. Louisiana, Justice Neil Gorsuch explained that ” the Sixth Amendment right to a jury trial—as incorporated against the States by way of the Fourteenth Amendment—requires a

unanimous verdict to convict a defendant of a serious offense.” (Whether jury unanimity is required in cases involving “petty offenses” was not before the Court, as noted in a footnote to the opinion.) This decision overturned the conviction of Evangelisto Ramos, who was convicted by nonunanimous jury in Louisiana. Nonunanimous jury verdicts in criminal cases were also allowed in Oregon.

The division among the justices in Ramos is quite something:

GORSUCH, J., announced the judgment of the Court, and delivered the opinion of the Court with respect to Parts I, II–A, III, and IV–B–1, in which GINSBURG, BREYER, SOTOMAYOR, and KAVANAUGH, JJ., joined, an opinion with respect to Parts II–B, IV–B–2, and V, in which GINSBURG, BREYER, and SOTOMAYOR, JJ., joined, and an opinion with respect to Part IV–A, in which GINSBURG and BREYER, JJ., joined. SOTOMAYOR, J., filed an opinion concurring as to all but Part IV–A. KAVANAUGH, J., filed an opinion concurring in part. THOMAS, J., filed an opinion concurring in the judgment. ALITO, J., filed a dissenting opinion, in which ROBERTS, C. J., joined, and in which KAGAN, J., joined as to all but Part III–D.

Here’s how that breaks down: Six justices (Gorsuch, Thomas, Ginsburg, Breyer, Sotomayor, Kavanaugh, agreed with the Court’s bottom line conclusion, but Justice Gorsuch’s opinion is only joined in its entirety by three justices (Gorsuch, Ginsburg). Justice Alito’s dissent was joined by Chief Justice Roberts and Justice Kagan, in part.

Justice Thomas wrote separately because he wanted to “make clear that this right applies against the States through the Privileges or Immunities Clause of the Fourteenth Amendment, not the Due Process Clause.” Historically, the Court has incorporated rights against the states through the Due Process Clause. Many academics think this is an error, and Justice Thomas has long indicated he does as well.

One issue dividing justices in Ramos is the treatment of precedent, as the decision overturned Apodaca v. Oregon, a 1972 decision upholding the constitutionality of nonunanimous criminal convictions in state court. Both Justices Sotomayor and Kavanaugh wrote separately to discuss the reasons for overturning Apodaca. (Sotomayor also wanted to note the “racially biased origins” of laws allowing nonunanimous juries to convict people of criminal offenses.)

Justice Alito’s dissent stressed the importance of stare decisis. This issue also likely explains the Court’s lineup here, as Chief Justice Roberts and Justice Kagan are the Court’s most vocal defenders of upholding precedent (though not always in the same cases). Justice Kagan has become particularly vocal in her defense of stare decisis, so it’s also no surprise that she does not join the portion of Alito’s dissent that explains why, in his view, the argument for overturning Apodaca was not as strong as the argument to overturn precedents in other recent cases.

Today’s second opinion, Thryv v. Click-to-Call Technologies, concerning inter partes review of patent claims also had an interesting 7-2 lineup (if, perhaps, less interesting subject matter). Justice Ginsburg wrote for a seven justice majority. Justice Gorsuch, joined by Justice Sotomayor, dissented. Interestingly, Justices Thomas and Alito declined to join a small part of Ginsburg’s majority, and Sotomayor declined to join the last part of Gorsuch’s dissent.

Today’s third opinion (about which I hope to say more later), was Atlantic Richfield v. Christian, an interesting case involving the availability of state law remedies for hazardous waste site cleanups under the federal Superfund law. The Court was unanimous on some issues, but split 8-1 on one question, and 7-2 on another.

Chief Justice Roberts wrote the opinion for the Court in Atlantic Richfield. In the first part of his opinion, the Court unanimously concluded it had jurisdiction to hear the case. As noted above, the remainder of the opinion was either 8-1 or 7-2. Justice Alito dissented in part, on the basis that the Court was too permissive in allowing state court challenges to federally approved Superfund cleanups. Justice Gorsuch, joined by Justice Thomas, dissented from a different portion of the opinion which would preclude landowners from pursuing state common law remedies for hazardous waste site cleanups. In Justice Gorsuch’s view, the federal Superfund statute was intended to supplement traditional state law remedies, not supplant them. (Time permitting, I’ll write a separate post on this case after I’ve had the time to dig in.)

Two other tidbits: Justice Gorsuch was the one justice to write an opinion in all three cases decided today. Also, in today’s orders, the Supreme Court denied the Solicitor General’s request for oral argument time as an amicus for the first time in a decade.

from Latest – Reason.com https://ift.tt/2XS2ExA

via IFTTT

Harvard And Other ‘Well Endowed’ Colleges Face Backlash For Tapping Tens Of Millions In Stimulus Funds

Several US colleges with multi-billion dollar endowments have been tapping into the massive coronavirus stimulus passed by Congress and signed into law by President Trump in January.

As part of the $2 trillion Coronavirus Aid, Relief and Economic Security Act (CARES), $14 billion was set aside to support higher education institutions – ostensibly those without billions already in the bank.

Harvard, for example, which has a $40 billion endowment, will receive $8.7 million in federal aid. Harvard points out that at least half of which has been mandated for emergency financial aid grants to students, which we would note that they can cover themselves.

Hilariously, Harvard’s Crimson points to the risk that their endowment could shrink due to market volatility, and that the University’s financial situation is “grave.” On the other hand – buried halfway through the article, Rutgers Business School professor John Longo points out that “it is conceivable that Harvard’s market neutral and long/short hedge funds actually delivered positive returns,” adding “If this is the case, it would materially soften the blow from the sharp drop in equities from around the world.”

Let’s look at which other financially sound universities stuck their hands in the cookie jar, courtesy of Twitter user @Oilfield_Ranndo:

CARES Act funds to Univ of Pennsylvania:

$9,907,683

Univ of Pennsylvania President Amy Gutman’s salary:

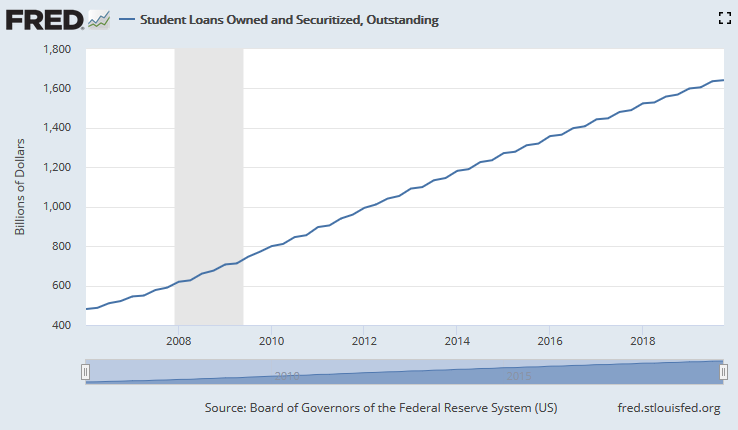

Nevermind the decade-plus these universities have been enjoying inflated tuition thanks to $1.6 trillion in student loans which may be about to default – which will undoubtedly stick taxpayers with an even larger bill.

Money manager and economist Michael Pento says the Federal Reserve has only massive money printing left to try to save the economy from the current and ongoing debt implosion. There is going to be lots of fresh cash needed.

Pento runs down a list of just few of the things the Fed will need to spend money on and says,

“We all should know more than 22 million people have lost their jobs in the last four weeks alone. That’s 22 million people, and the unemployment rate, according to me, is heading up to 15% to 17%. That, my friends, is a depression. We also have the Philly Fed (Manufacturing Index rating) come out with a -56.6. That’s a minus 56.6. That’s the worst ever. Empire State Manufacturing -78.2, which is the worst rating ever. Retail sales plunged in March 8.7%. That is also the worst reading ever. That’s the worst plunge ever, and that’s just March. In my opinion, it will be something worse in April because all of the month will be completely shut down. That’s 90% to 95% of the economy.”

Now you know why the Fed freaked out and started printing money at the highest pace ever. Pento predicts the Fed, who took $4.5 trillion onto its balance sheet as a result of the “Great Recession,” will explode “The Federal Reserve’s balance sheet to $10 trillion by end of the year.”

Pento says forget the so-called “V shaped recovery” because “you cannot simply turn back on the economy like a light switch. There’s no electricity.” On top of that, Pento points out that,

“Millions of people who have been thrown out of work have taken on even more debt . . . . So, the economy is not bouncing back.”

So, it is clear the Fed is going to print trillions of dollars in fresh cash to pay for bailouts, unemployment checks and debt payments to avoid massive defaults in the U.S. economy. Pento asks, “What kind of faith will people have in the purchasing power of their fiat currencies?”

“…If the Fed can print trillions of dollars with no consequences… why bother working? Everybody can just stay home and cash a check…This is a recipe for hyper-inflation. It’s been tried many, many times in history, and it has never worked…

The gap between the real economy, asset prices and debt and the underlying economy has never been greater…

You have a massive increase of insolvent debt…Then you are going to ad inflation to that mix? Think about the carnage that is to come. That is the real crash… We will partially recover from this virus. . . . We are now sending money, helicopter money, directly to consumers, and that will cause inflation.”

Pento predicts a “tsunami of inflation” is coming in the not-too-distant future. Pento says,

“People are losing faith in fiat currencies. The price of gold in other currencies is already at all-time record highs. Even in dollar terms it’s $1,700 per ounce and on its way to record highs. What is the government going to do when you have insolvency and inflationary implosion of the bond market? The real crash is coming…

A government cannot issue more debt to bail out an insolvent condition—fact.

A government cannot print more money to placate a market that is afraid of inflation—fact.

That’s what they are going to be faced with: Yields spiking because of inflation and insolvency concerns, and then there is nothing a government can do. It’s not going to be just the United States, it’s going to be the case globally… That’s when the money is no good, and the bonds are no good.”

Join Greg Hunter of USAWatchdog.com as he goes One-on-One with money manager and economist Michael Pento.

{kind=link}