On May 7, the Department filed a motion seeking leave from the district court to dismiss the charges against Michael Flynn. Despite Flynn’s repeated confessions and the district court’s prior rejection of arguments now made in support of Flynn, such as the argument that his lies were not “material” to ongoing investigations, Attorney General William Barr has decided to reverse course.

Rule 48(a) of the Federal Rules of Criminal Procedure provides that the federal government “may, with leave of court, dismiss an indictment, information, or complaint.” So what does it take for a court to grant the government “leave” to dismiss the indictment? A new (short) paper by Thomas Frampton provides some answers, some of which conflict quite a bit with the much political commentary about the case.

Here’s the abstract:

The conventional view of Rule 48(a) dismissals distinguishes between two types of motions to dismiss: (1) those where dismissal would benefit the defendant, and (2) those where dismissal might give the Government a tactical advantage against the defendant, perhaps because prosecutors seek to dismiss the case and then file new charges. In United States v. Flynn, the Department of Justice argues that Rule 48(a)’s “leave of court” requirement applies exclusively to the latter category of motions to dismiss; where the dismissal accrues to the benefit of the defendant, judicial meddling is unwarranted and improper. In support, the Government relies on forty-year-old dicta in the sole U.S. Supreme Court case interpreting Rule 48(a), Rinaldi v. United States. There, the Court stated that the “leave of court” language was added to Rule 48(a) “without explanation,” but “apparently” this verbiage had as its “principal object . . . to protect a defendant against prosecutorial harassment.”

But the Government’s position—and the U.S. Supreme Court language upon which it is based—is simply wrong. In fact, the “principal object” of Rule 48(a)’s “leave of court” requirement was not to protect the interests of individual defendants, but rather to guard against dubious dismissals of criminal cases that would benefit powerful and well-connected defendants. In other words, it was drafted and enacted precisely to deal with the situation that has arisen in United States v. Flynn: its purpose was to empower the Judiciary to limit dismissal in cases where the district court suspects that some impropriety prompted the Executive’s decision to abandon a case.

To be clear, there may be good reason for the district court to grant the Government’s motion to dismiss in United States v. Flynn. But the fiction that Rule 48(a) exists solely, or even chiefly, to protect defendants against prosecutorial mischief should be abandoned. This brief Essay recounts Rule 48’s forgotten history.

The crisis caused by the forced shutdown of the economy has given us some important lessons.

Number one, shutting down the economy entirely is a dangerous experiment with important long-term implications.

Number two, there is no such thing as “lives or the economy”.

Many countries have implemented support systems to address the pandemic while preserving the business and productive fabric. South Korea, with less than 300 dead in a 51 million population, published an unemployment rate of 3.8% and its economy, closer to China than many, is estimated to fall less than 1% in 2020. South Korea is also a country with lower government spending to GDP and lower healthcare spending per capita than the average of leading nations and the OECD. They are just better at managing.

A similar success in providing health support, managing the health crisis and keeping the business and economic fabric alive can be seen in Singapore, Taiwan, Austria, Switzerland, Denmark, Sweden, and other nations. It is not “lives or the economy”, it is “lives and the economy”. The voices that demand “Open America Now” are right, and the government is working to reopen the economy quickly, safely, and effectively.

The United States faces a deep contraction, massive job losses, and mounting debt. However, the nation can recover and prevent long-term depression. The V-shaped recovery may now be elusive, but the nation can recover at a reasonably fast pace and quicker than the eurozone or Japan if the government avoids copying those two examples. If the United States follows the path of massive intervention, huge government spending, and negative rates, American citizens may realize that copying Japan and the eurozone delivers Japan and eurozone-style stagnation.

A large stimulus bill has been passed, but this may prove ineffective if the shutdown remains.

The little demand that the stimulus plan may incentivize will go to sectors that already had overcapacity,while the bleeding in sectors that had no debt or access to subsidies remains.

In many cases, stimulus creates demand in the wrong areas, while the job losses and business closings rise exponentially in the sectors that are most impacted by the shutdown. The April jobs report signals a few risks to a rapid recovery. 80% of the jobs lost are classified as temporary. That is a good thing. However, a prolonged shutdown may move those unemployed figures to permanent. 7.7 million jobs were lost in Leisure and Hospitaliy, 5.5 of which came from bars and restaurants. Those jobs will not come back if the lockdown remains or if the return to activity includes severe restrictions. That is why it is so important to learn from the example of nations that have successfully managed to keep the economy open and provide equipment and protocols to guarantee the health of citizens.

No stimulus plan is going to bring back 7.7 million jobs lost in Leisure and Hospitality, 2.5 million lost in Education and Health Services and even less 4 million lost in Professional & Business Services and Retail Trade. What the April jobs report tells us is that no government plan is going to stop the bleeding of the Services sector.

That is why it is so dangerous to add another $3 trillion relief bill to an already large $2 trillion package. The first one was aimed at allowing businesses and citizens to endure the lockdown, the new “relief” plan passed by the House is very likely to add a lot more debt for no real result and create longer-lasting damages. It makes no sense to double the stimulus shortly after the first plan is announced when the results of the first package have not even been analyzed. Even more, adding trillions of spending to a forced shutdown is not going to improve the economy, only worsen the already challenging fiscal situation of the United States.

It would be ridiculous to pass a 29% of GDP total stimulus when the economy has not lost productive capacity, it is in a forced lockdown.

The interventionists try to tell us that there is a massive need for government spending to “rebuild the economy”. Yet the argument is simply farcical. The American productive capacity remains intact, its human and technological capital untouched and its competitive strengths unchallenged. More importantly, there is ample financial and investment capacity to recapitalize the economy if the shutdown is lifted.

The figures of deaths and infection risk prove the mistake of a generalized lockdown. Destroying the economy is a very bad experiment when the average mortality by age group shows a minimal impact on citizens of 70 years of age or less.

The United States government does not need to spend trillions, the Fed does not need to implement negative rates that have decimated the eurozone economy and sent it to stagnation. What the United States government needs to do is provide equipment and protocols for businesses to manage the pandemic, provide safety control measures to the high-risk age groups, and provide massive tests to guarantee the pandemic is under control. the government needs to open the economy now before a deep crisis becomes a deeper depression.

America does not need more trillion dollar bills. It needs less political interventionism.

via ZeroHedge News https://ift.tt/2TdWSmI Tyler Durden

This is a prime example of the lunacy future historians and generations are going to look back and see.

It wasn’t a spoof, but a real official press briefing held by New York’s Nassau County health officials just days ago. It was all about proper handling of balls to stay safe amid coronavirus.

Yes, we’renow to the point that bureaucrats have to treat us to infantile lectures on how to handle others’ balls. As if Tennis wasn’t already among the most ‘social distancing safe’ sports in the world, given the nature of how far apart players stand on the court — at least we think it was about tennis balls anyway, but aren’t quite sure.

“You can kick their balls, but you can’t touch them,” Nassau County Executive Laura Curran announced with a serious urgency.

Indeed, an apt description of the insane times in which we live, where government officials full of inflated self-importance have to break down how we handle each others’ balls.

“To avoid confusion between whose balls are whose you can use a marker like a sharpie to put an ‘X’… to put someone’s initials on them,” she added.

So to review: “if you’re playing tennis against someone who lives in the same house as you, treat their balls like your own… But if you’re playing against someone who lives elsewhere or you’re on a court next to other people not living with you, remember these tips”:

Kick their balls

To avoid confusion, mark your balls with an “X” or write your name on your balls.

IMPORTANTLY!: Don’t touch their balls with your hands.

Welcome to the year 2020 in America.

via ZeroHedge News https://ift.tt/2X7VmU2 Tyler Durden

Powell “60 Minutes” Preview: Full Recovery Could Take Until End Of 2021, Will Require A Coronavirus Vaccine Tyler Durden

Sun, 05/17/2020 – 17:14

Less than a week after Powell tried (and apparently failed) to convince the market negative rates aren’t coming to the US (right as the BOE’s Andy Haldane admits the UK is considering joining the rest of Europe into the monetary twilight zone of NIRP), and just days after the Fed’s semiannual Financial Stability report warned that “asset prices remain vulnerable to significant price declines should the pandemic take an unexpected course” traders will again be glued to their TVs at 7pm ET on Sunday evening when chair Powell sits down on CBS’s 60 Minutes – a little under 10 years after Ben Bernanke used the same venue to laughably declare that the Fed “could raise interest rates in 15 minutes if we have to,” adding “that time is not now” or apparently not ever – and will urge Americans to be patient as a full recovery may take until the end of 2021, and would require a coronavirus vaccine for people to “be fully confident” again.

Contrary to some satirical expectations…

FED’S POWELL SAYS A FED MANDATE TO BUY INDIVIDUAL STOCKS AND ETFs COULD BE A VACCINE ALTERNATIVE- 60 MINUTES INTERVIEW

… perhaps be expected in a centrally-planned world where the surreal, the absurd and financial reality are in a constant state of flux, Powell will do his best “optimistic Buffett” impression (now that Buffett is decidedly not optimistic, and is not only not ‘buying American’ but selling it, in both airlines and banks) and will say that “in the long run and even in the medium run, you wouldn’t want to bet against the American economy. The American economy will recover.”

The question is when, of course, and it is here that Powell’s message gets decided more downbeat: “Assuming there’s not a second wave of the coronavirus, I think you’ll see the economy recover steadily through the second half of the year,” the central bank chief said. Yet even if the recover does start as soon as Q2, “it may take a while. It may take a period of time. It could stretch through the end of next year [before things get back to normal]. We really don’t know.”

However, he added that “for the economy to fully recover people will have to be fully confident, and that may have to await the arrival of a vaccine.”

To be sure, Powell has achieved great success in restoring the stock market. Alas, as everyone knows by now, the market is not the economy, and more than 36 million Americans have lost their jobs since February as the economy shuttered to limit virus spread, even as the S&P500 is rapidly recovering virtually all of its losses. Meanwhile, countless companies, especially small businesses, are hurtling toward bankruptcy, while states and cities are confronting gaping budget shortfalls that could provoke a massive second wave of layoffs from the public sector.

“I would take a more optimistic cut at that, if I could,” Powell said, unable to take an optimistic cut. “And that is — this is a time of great suffering and difficulty. And it’s come on us so quickly and with such force, that you really can’t put into words the pain people are feeling and the uncertainty they’re realizing. And it’s going to take a while for us to get back.”

Powell’s cautious remarks follow his grave warning Wednesday that the economy faces lasting harm from the pandemic if the government doesn’t step up, which would require even more debt issuance by the US Treasury, and far even greater QE from Powell, something which Goldman warned could be a major problem for the Fed. The comments add support to calls for more congressional spending after the Democrat-controlled house voted through another $3 trillion in virus aid on top of a record $2.2 trillion package agreed in March (the Senate is expected to summarily vote down the latest massive stimulus).

After tonight’s interview, Powell has another virtual conference just 48 hours later, when he will be interrogated about the scale and timing of additional fiscal relief when he appears before the Senate Banking Committee on Tuesday. He’ll also be asked to tell Americans what to expect.

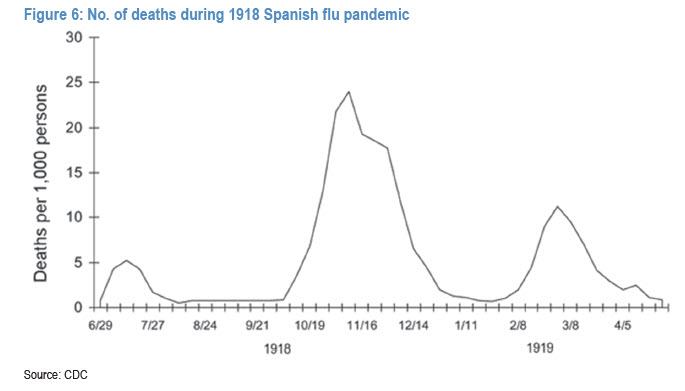

Finally, what if there is a second wave of the coronavirus, as there was during the Spanish Flu in 1917…

… and there is no recovery in late 2020 and 2021? Will Powell unleash negative rates and buy stocks to keep stocks from dropping in that case? For the answer watch tonight’s full interview as we assume CBS only leaked the boring parts.

via ZeroHedge News https://ift.tt/2zI8gAq Tyler Durden

“For Lease”: The Commercial Real Estate Apocalypse In Photos Tyler Durden

Sun, 05/17/2020 – 16:50

In early 2017, we first reported a bearish trade emerged which quickly gained popularity in the investment community, and was dubbed “The Next Big Short.” At the time, only a few bearish funds were positioned for a “retail apocalypse” that could spur a wave of defaults.

Fast forward to today, coronavirus outbreak, and the ensuing lockdown, has essentially frozen the commercial real estate market. Buildings that were once used for restaurants, offices, hotels, spas, and or anything else that is classified non-essential have seen soaring vacancies.

This is single handily sending the commercial property market into chaos. As vacancies soar, tremendous downward pressure is being put on almost every asset class tied to commercial real estate.

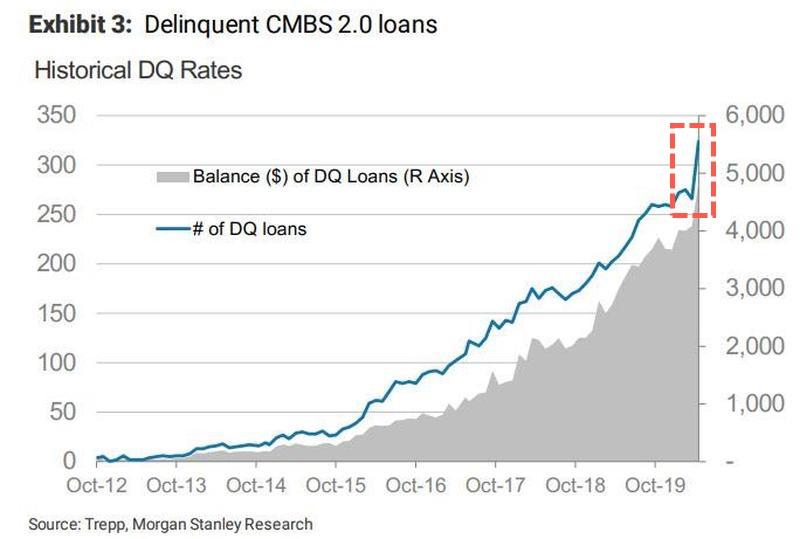

The latest TREPP remittance data compiled by Morgan Stanley showed a quarter of all commercial mortgage-backed securities (CMBS) could be on the verge of default. CMBS delinquencies surged to a new high in April as lockdowns continued:

With retail in disaster, a deluge of CMBS defaults is on the horizon. Shown below, the value of commercial mortgage-backed securities (CMBX Series 6 BBB- tranche) is collapsing…

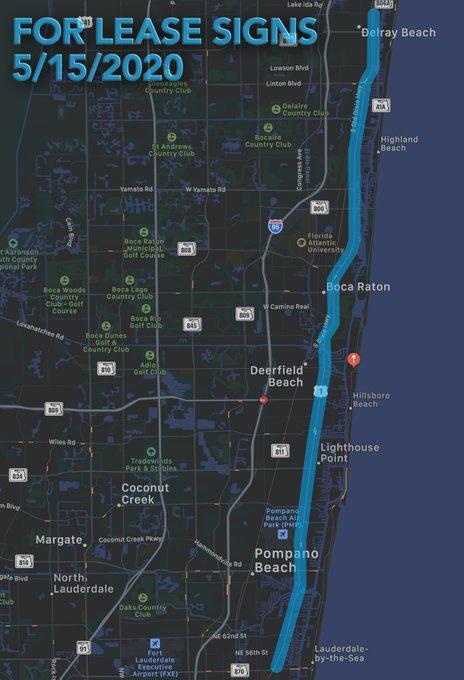

For more color on the collapse, mcm-ct.com created a “subthread showing the economic devastation down here in the Lighthouse Point to Delray Beach area on a main commerce/travel route…” It appears MCM recently drove up and down a stretch of highway in South Florida, an area of great wealth, and said, “three months ago one could count “For Lease” signs on this whole route on a few hands,” which now appears to have significantly multiplied during lockdowns.

Stretch of highway MCM traveled

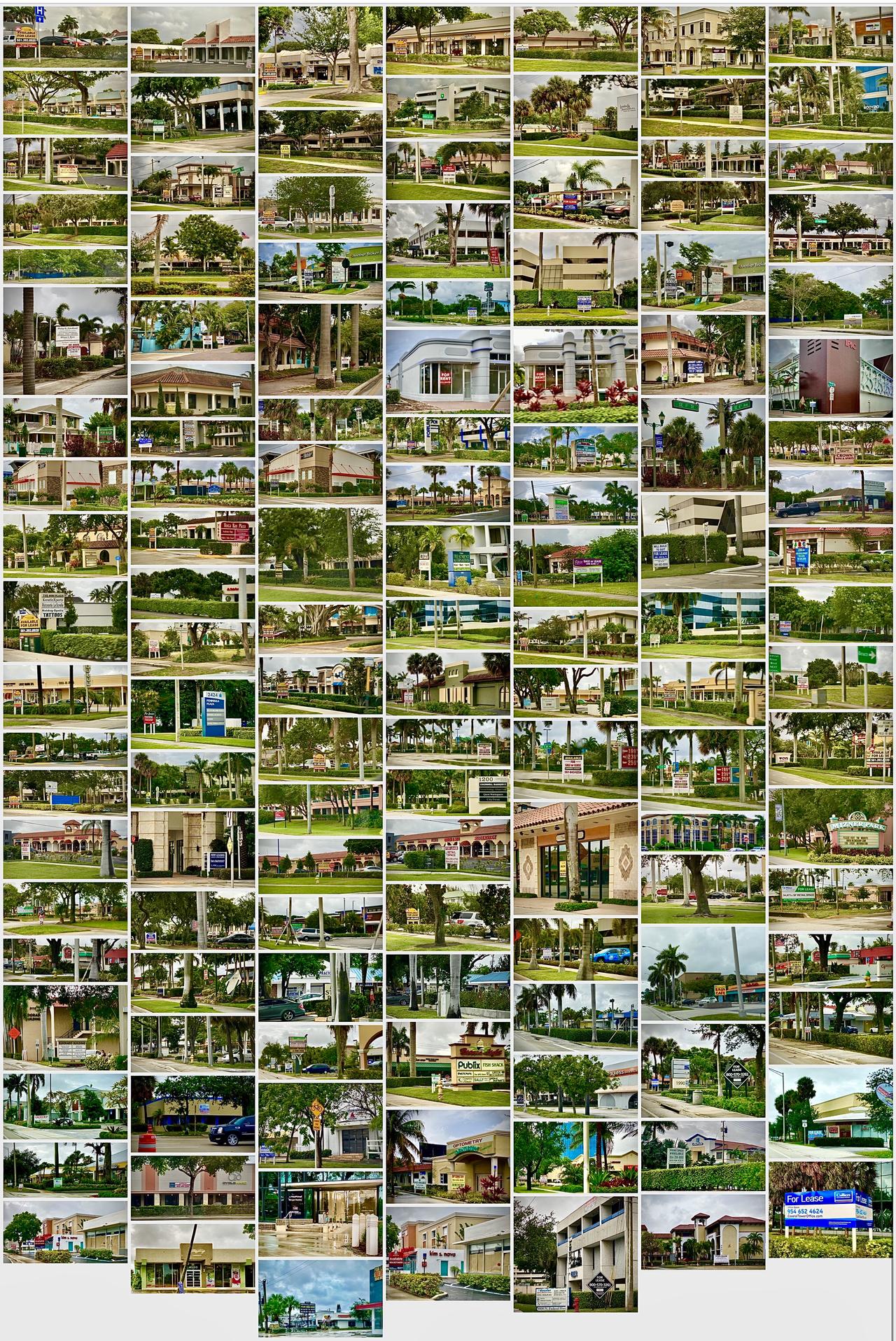

“Here are pictures of many (probably most of the “For Lease” signs as of yesterday…remember there used to be very few just months ago…each one of these comes with tragedy before it imo and needs a VERY CREDIT WORTHY NEW TENANT willing to make a big/long-term commitment,” mcm-ct.com tweeted.

“For Lease” signs along a stretch of South Florida highway

In a series of tweets, here is what MCM said about the current situation of the commercial real estate market in South Florida and the local economy:

Rebuilding credit worthiness from these aborted/terminated or insolvency related lease and business blow ups will take years. The only way this could have been prevented was if the government provided a national backstop directly BEFORE THESE SIGNS APPEARED

spoke to a lot of people recently – have yet to meet a person who got the full package of unemployment aid in FL

Many people have received the $1,200 federal government check but most have not gotten state unemployment. And many businesses are still waiting for business support

Many people do not know what to do or where to go or even how to get free food – yet these leases are suddenly going to be filled with credit worthy businesses willing to make 10 year risks based on a government that proved it will and can terminate their businesses at any time

I’m sorry, the one thing that people think when they start a business is THEY WILL DECIDE WHEN ITS OPEN barring Mother Nature or a War not self immolation and violation of constitutional rights by the US government

NOW WHEN YOU TAKE A LEASE OUT you need to factor business risk in but also add the risk of the government violating the constitution and your rights to the assessment as whether to put good money down to take on a business commitment & a lease

Regardless, the situation will take TWO YEARS BEFORE DAMAGED ENTREPRENEURS BEGIN TO BE ABLE TO REBUILD CREDIT SUFFICENT EVEN BE APPROVABLE TO TAKE A LEASE and that will be a minimum…and then there are the next waves of business that will decide to pack it in

The govt (esp marxists) screwed up a generation of business & its going to take 2 to 4 yrs to start to come back

they proved that SOCIALISM DOES NOT WORK because it does not & CAN NOT work EQUALLY for all because INTEGRITY/INDUSTRIOUSNESS/EFFORT IS NOT EFFECTIVE 4 GETTING ACCESS

And perhaps MCM is correct, as we’ve explained before, a recovery back to 2019 levels could take several years.

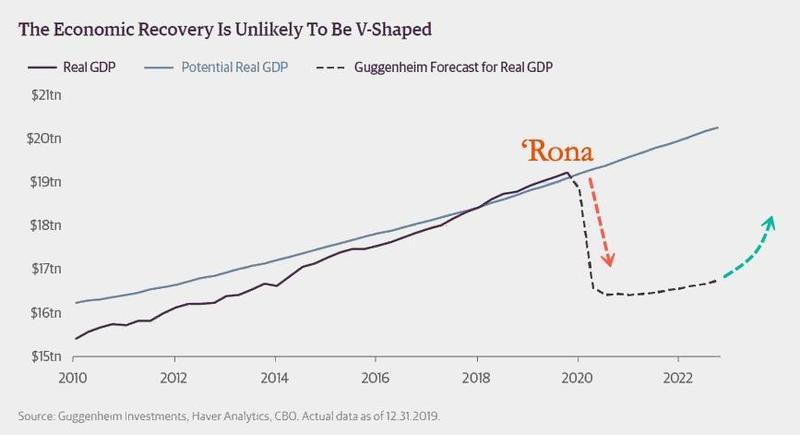

Not to mention, Scott Minerd, the chief investment officer of Guggenheim Investments, believes it could take upwards of “four years” for a recovery to take place adding that “to think that the economy is going to reaccelerate in the third quarter in a V-shaped recovery to the level where the gross domestic product (GDP) was prior to the pandemic is unrealistic.”

The disaster unfolding on main street America will be devastating.

via ZeroHedge News https://ift.tt/2LxSKto Tyler Durden

Although state lockdowns have served governors well as a heavy-handed show of force, the policies are a patent neglect of the many nuances inherent in human action.

They have led to a host of unintended consequences, including the emergence of a new health crisis – a dangerously sharp rise in mental illness. Though states are gradually wading out of lockdown, the damage has already been done and is here to stay.

Distress and Disorder

The science is clear that having meaningful human interactions is an inherent, biological need that all people share. But in the name of “public health,” people are prohibited from freely and peaceably congregating. There’s no church, no “nonessential” shopping, no going into work (for many), no girls’ nights out, no going to the gym, no visiting friends, no family get-togethers. Nothing. No sacrifice can be too great in the age of COVID per the “experts.” And that’s taken a harsh psychological toll on the nation.

Extensive study has, for years, correlated social isolation with poor mental health. The need for connection is as real now as it’s ever been. Since the US had already long suffered from a loneliness crisis, the stark and sudden crop up of stay-at-home orders made this immediately much worse. As Drs. Betty Pfefferbaum and Carol North found,

A recent review of psychological sequelae in samples of quarantined people and of health care providers…revealed numerous emotional outcomes, including stress, depression, irritability, insomnia, fear, confusion, anger, frustration, boredom, and stigma associated with quarantine, some of which persisted after the quarantine was lifted.

Being whisked from normal life into the repressive conditions of lockdowns is understandably damaging. The anguish people are feeling is at astronomical levels. Schoolchilden recently surveyed in Wuhan and Huangshi during stay-at-home orders reported symptoms of depression and anxiety at a rate far higher than normal.

The same seems to be holding true for the general US population. The Crisis Text Line—a free service providing crisis counseling over SMS—has reported a 40 percent increase in recent volume, averaging over 100,000 text conversations each month. In a Kaiser Family Foundation (KFF) poll from the end of March, 47 percent of respondents under stay-at-home orders reported that COVID-related stress had negatively impacted their mental health, compared to 37 percent of respondents not facing such orders. Twenty-one percent of stay-at-homers described that impact as “major,” compared to 13 percent those not locked down. Statistically speaking, that’s quite a significant gap, especially when scaled to a population of 330 million. Though there has been no reliable polling data since then, it’s easy to imagine how much worse the situation has become as the weeks have worn on.

Combine that with the financial aspect of the lockdowns, and there’s a recipe for absolute disaster. Under mandatory closure, an untold number of “nonessential” businesses—particularly small businesses—have gone insolvent or are on the brink thereof. That’s led to tens of millions of new jobless claims in just the past two months—amounting to the worst employment crisis in American history.

A vast literature connects economic downturns to a number of psychological issues, including anxiety, stress, and depression, which often spur on various high-risk behaviors. Although recessions are inherently stressful, mental health challenges usually emerge within the personal context of income and employment insecurity. With the economy in free fall, many millions of Americans have become worried about their ability to continue paying bills and putting food on the table going forward. The psychological impact that recessions have is capable of lasting for years, even after economic difficulties themselves have disappeared. With entire states having been locked down for weeks and months on end, public activity is only reemerging under the scourge of intense mental disturbance.

Self-Harm and Suicide

Although everyone is potentially at risk of developing symptoms of mental illness, those already struggling may be the most vulnerable. One user in a depression support group on Reddit recently posted, “I am going absolutely insane battling with my mind and being locked up in my house.” Another said, “Lockdown is making my depression the worst it’s ever been….I’d rather be dead than stuck in my house alone with my thoughts.” Rock-bottom feelings such as these are very often accompanied by a number of different maladaptive coping strategies, among them nonfatal self-harm.

For individuals already overloaded with anxiety and desperation, economic hardship is often the “final straw” leading to self-harm behaviors. An Irish study found the self-harm rate to have increased across the population following the Great Recession, with men between the ages of 25 and 44 impacted the most. Although this is far outside the usual age and sex demographic for self-harm, it may be explained by the heightened that stress working-aged men felt in their roles as primary breadwinners. A study in Britain after the crash also noted a spike in self-harm, associated particularly with areas seeing greater amounts of job loss. In an economy with people out of work more than ever before, that’s of considerable alarm.

Even without financial trouble, many may turn to hitting and cutting themselves just out of sheer loneliness. With face-to-face interaction hard to come by, there are few support systems for people to rely on. Despite serving a vital role in many capacities, Zoom calls clearly aren’t a cure for people’s woes, usually leaving users more exhausted than connected.

And although many health providers are providing patients with over-the-phone coverage, that sort of help may be much less effective for self-harmers. A 2013 Taiwanese study on the etiology of self-harm reasoned that “the structural conditions and quantity of support” may help alleviate the urge to self-harm more than “the quality of support received through specific networks.” Sheltered away from friends, many sufferers are left feeling that there is no escape, and telehealth services can do little to change that.

In all the lockdown mess, many have even reached the brink of suicide. The 2003 SARS outbreak led to an significant uptick in the suicide rate in Hong Kong—up to 18.6 suicides per 100,000 residents. The elderly population there was hit the worst, likely as a consequence of increased social isolation. Now, with community activities interrupted, many have become isolated from the gatherings that give their lives meaning—such as church, whose regular attendees face a suicide rate of one-fifth that of the rest of the population. “Living” means more than mere biological life—it involves a complex array of relationships, activities, and goals. But under lockdown, the world has been sapped of any semblance of true living.

Financial struggles are another common theme in suicide etiology. During the Great Recession, suicides spiked across the globe. Across just the US, the European Union, and Canada, research revealed more than ten thousand suicides connected to the downturn—again, particularly among men. Some fear that worse numbers could arise from the current economic crisis.

The Meadows Mental Health Policy Institute recently estimated that for every percentage point that the unemployment rate rises, the overall suicide rate rises 1.6 percent. Considering that last month the real unemployment rate rose to 22.8 percent (and possibly even higher), the US probably had nearly one thousand additional suicides in April stemming just from the economic shutdown. As job loss continues this month, more people are bound to take their lives—not to mention the untold effect that social isolation is having. Although national data isn’t yet available, many local suicide prevention centers have been reporting significant increases in hotline usage—around 20–30 percent on most days and as high as 100 percent on others.

Substance Abuse and Addiction

To manage lockdown stress, many have found themselves self-medicating and kicking back on old habits, which is exactly what prior research suggests. When the economy falls, the use of alcohol and other drugs tends to spike—especially among those who lose their jobs. Along with many financial stressors, spending more time at home intensifies the propensity for use, which stay-at-home orders and social distancing guidelines have only helped worsen.

People also seek out many addictive substances to find relief from social disconnection—which the brain can interpret as physical pain. That’s why it’s no surprise that the lockdowns have helped spell doom for those already suffering with addiction. Alone, it’s more difficult to resist relapse and misuse.

For the week ending April 25, year-over-year total off-trade alcohol sales were up 26.4 percent, down from a high of 55 percent in March when the lockdowns began. Online sales have exploded—recently growing in excess of 500 percent. But that’s not all because of people stocking up. The data has shown that more people have been buying more alcohol, of a higher proof and at a more frequent pace. That means that both consumption and sales have faced a significant uptick. Even as the rate of sales growth has slowly decreased in mid-April, year-over-year increases have remained quite high.

Alcoholics Anonymous and other nonemergency addiction resources have not been deemed “essential,” leaving those recovering to find help online or over the phone. Activity on internet support groups has shot through the roof, as have calls to addiction helplines. Many former addicts have fallen into relapse after years of sobriety, sending them back into the mire of struggles that they long thought they’d escaped.

Hard drug use is also on the rise—which is frightening, as the opioid crisis had already been wreaking havoc across the country. Call volume at the Substance Abuse and Mental Health Services Administration (SAMHSA) National Hotline was five times higher at the end of March than it had been at the beginning of the month, and harm reduction centers are operating at limited capacity. That’s left addicts with little recourse besides continued use.

Research indicates that even in periods of decreased income, drug use remains constant. Throughout the present crisis, addicts have remained addicts and still need their fix, despite recent disruptions in the meth and heroin supply chains. To avoid withdrawal symptoms, many switch to different substances, dealers, and means of ingestion—making use more imprecise and risky. There’s also the fear that addicts who have stockpiled substances are using them at a quicker pace. As with suicides, national data has yet to emerge, but some municipal and county offices have already reported a substantial jump in overdoses since the lockdown began. Although lockdowns are temporary, their effects can be irreversible.

Other addictive behaviors also seem to be on the rise. Tobacco sales, for one, have absolutely boomed. Industry giant Altria reported that in Q1 (quarter 1), shipments of its smokeable tobacco products rose 6.2 percent and oral tobacco shipments rose 2.8 percent. Although it’s unclear how much of that is due to people stocking up, both convenience stores and online sellers have recently noticed a significant uptick in demand as well. And an increase in use would follow the same pattern as what happened during the Great Recession.

Stressed and stuck at home, people have also ramped up their porn consumption. Since the lockdowns began, PornHub traffic has consistently been above average—with a high of 23.2 percent at the end of March, when the company offered all users free premium access. When used frequently, porn can rope users into a powerfully addictive cycle, engendering psychosexual difficulties such as low libido, sexual dissatisfaction, and erectile dysfunction—even in young men.

Online, many have also begun to try their luck at gambling. Global Poker—a popular online poker room—saw a 43 percent spike in use following lockdown orders, with a remarkable 255 percent increase in first-time players. Much of that may be new traffic from gamblers who had frequented brick-and-mortar casinos—a mere shifting of activity from one channel to another. But it comes at a cost: online gambling is associated with a number of increased risks for becoming addicted. The fallout from that could take decades to move past.

Conclusion

The politicians and medical experts basking in the COVID spotlight have traded the façade of an effective public health response for the hidden realities of mental illness. As talking heads repeatedly prattled the “flatten the curve” mantra, the curves for stress, suicide, and addiction all steepened. A study by the Well Being Trust concluded that “deaths of despair”—which include all suicide and substance-related fatalities resulting from fear, unemployment, and isolation—may total seventy-five thousand by the end of the COVID crisis. Their death knells rang out the moment governors committed their states to shutting down.

And among those who live, the residual psychological and behavioral effects will remain long after the lockdowns are over—possibly for the rest of their lives. Indeed, by overstepping individual judgment, the government imposed a one-size-fits-none solution so debilitating and unprecedented that the country will never truly recover. In the long run—aside from the blips and bumps of infection and disease—the state remains the true risk to the health of the nation.

via ZeroHedge News https://ift.tt/3dSuHS8 Tyler Durden

I had only dimly recalled the 2000 wreck of the Russian submarine Kursk, but I just came across a song about it that I very much liked, and that I wanted to share with our handful of Russophone readers. Here is something of the backstory, which one needs to know to understand the song (Chicago Tribune [Colin McMahon]):

Dmitry Kolesnikov’s body was the first to be positively identified from the wreck on the bottom of the Barents Sea … [among] the 118 crewmen who died after a pair of explosions devastated the submarine Aug. 12.

In a pocket of Kolesnikov’s uniform, divers also found a letter that the 27-year-old lieutenant captain wrote just before he died. For proud Russians, for Kolesnikov’s wife and family, the letter is a testament to loyalty and sense of duty.

Kolesnikov scribbled words of love to his bride of only four months. And in a more practiced, more disciplined hand, he recorded what he could of the events that led him and 22 other men to scramble to the Kursk’s last compartment and wait for a rescue that never came….

Kolesnikov’s documentation of survivors—according to his notes, the men lived for at least several hours—disproved the recent government versions that all 118 aboard died within minutes.

It also revived some of the anger against the government for its slow and confused response to the accident.

Here’s the song, from the Russian band DDT and its lead singer-songwriter, Yuri Shevchuk; you can read the Russian lyrics here, and an attempt at a somewhat rhyming and metered translation here. The song opens with the line,

Who about death will tell us a couple of honest words?

The music may at first seem like something of a mismatch with the theme , but I found that it worked for me.

from Latest – Reason.com https://ift.tt/3bJUZnX

via IFTTT

I had only dimly recalled the 2000 wreck of the Russian submarine Kursk, but I just came across a song about it that I very much liked, and that I wanted to share with our handful of Russophone readers. Here is something of the backstory, which one needs to know to understand the song (Chicago Tribune [Colin McMahon]):

Dmitry Kolesnikov’s body was the first to be positively identified from the wreck on the bottom of the Barents Sea … [among] the 118 crewmen who died after a pair of explosions devastated the submarine Aug. 12.

In a pocket of Kolesnikov’s uniform, divers also found a letter that the 27-year-old lieutenant captain wrote just before he died. For proud Russians, for Kolesnikov’s wife and family, the letter is a testament to loyalty and sense of duty.

Kolesnikov scribbled words of love to his bride of only four months. And in a more practiced, more disciplined hand, he recorded what he could of the events that led him and 22 other men to scramble to the Kursk’s last compartment and wait for a rescue that never came….

Kolesnikov’s documentation of survivors—according to his notes, the men lived for at least several hours—disproved the recent government versions that all 118 aboard died within minutes.

It also revived some of the anger against the government for its slow and confused response to the accident.

Here’s the song, from the Russian band DDT and its lead singer-songwriter, Yuri Shevchuk; you can read the Russian lyrics here, and an attempt at a somewhat rhyming and metered translation here. The song opens with the line,

Who about death will tell us a couple of honest words?

The music may at first seem like something of a mismatch with the theme , but I found that it worked for me.

from Latest – Reason.com https://ift.tt/3bJUZnX

via IFTTT

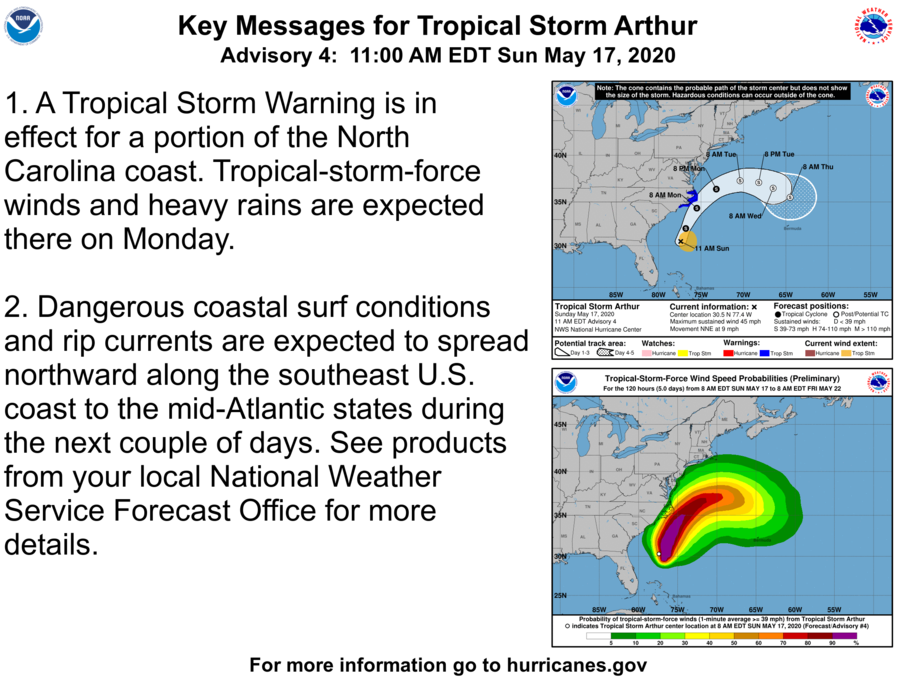

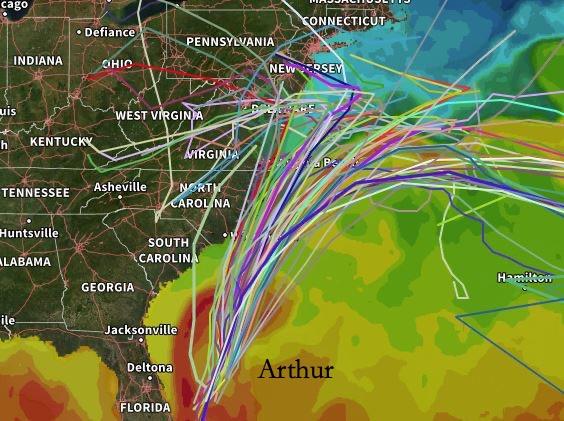

Tropical Storm Arthur, First Of Season, Sets Its Sight On Outer Banks Tyler Durden

Sun, 05/17/2020 – 16:00

About two weeks before the 2020 Atlantic hurricane season begins, a tropical storm developed on Saturday night off the coast of Florida. Forecasters are expecting the storm could strike eastern North Carolina on Monday.

AccuWeather Meteorologist Courtney Travis said while the official start of hurricane season is June 1, it is not uncommon in the last decade to see a preseason tropical system develop. The storm has been called Arthur and is the six consecutive year that a preseason tropical system has been observed.

As of Sunday morning, Arthur is sustaining winds of 40 mph and tracking off the Southeast coast and will pass North Carolina’s Outer Banks on Monday. Meteorologists say there is a low probability the storm makes landfall.

Tropical storm warnings and watches have been posted for coastal and some inland parts of North Carolina via the National Weather Service (NWS). This comes just days after the state reopened beaches due to virus-related lockdowns.

“Arthur is forecast to track to the north-northeast through Monday, a path which will take it very close to the Outer Banks of North Carolina,” AccuWeather Meteorologist Renee Duff said.

“There is a still the possibility that Arthur makes landfall where the barrier islands jut out near Cape Hatteras,” Duff said.

AccuWeather meteorologists say wind gusts could reach upwards of 60 mph across the Outer Banks into Monday as the storm passes through.

“Much of Arthur’s precipitation is out over the water, and will remain that way until the storm makes a closer approach to the East coast late Sunday night through Monday,” AccuWeather Meteorologist Brett Edwards said.

The million-dollar question is if the storm will hit the Outer Banks or just narrowly miss the coastal region and curl out to sea.

via ZeroHedge News https://ift.tt/2Zd4IAT Tyler Durden

“Good” Things That Are Bad, And “Bad” Things That Are Good Tyler Durden

Sun, 05/17/2020 – 15:35

Authored by Andrew Sheets, chief global strategist at Morgan Stanley

For all the sound and fury of the last month, global stock markets are roughly unchanged. Our overall strategic stance remains constructive, on the view that an improving trend in economic data will matter more than a poor level, risk premiums generally remain above average, policy support is aggressive and sentiment is reasonably cautious. We continue to think that the best way to express this positive view is buying corporate and securitized credit, selling equity and credit volatility and overwriting equity and credit indices.

Yet unchanged markets belie a host of uncertainties and the continuing stream of unprecedented developments. With much in flux, our focus today is on two “good” events that we think could actually be problematic, and two “bad” events that we’re more relaxed about.

Repeat something often enough and it will start to sound true. There’s an element of this in the idea that ‘lower interest rates are a positive for markets and the economy’, a notion that’s both a regular feature in financial commentary and hard-wired into many measures of financial conditions. Without belabouring the point, while lower rates are a good thing for demand and valuation all else equal, ‘all else equal’ is frequently not the case when yields are moving.

Which brings us to our first ‘good’ thing – negative interest rates: After April saw oil trade at a negative price, this week brought markets pricing negative short-term rates in the US and UK. A number of reasons could explain this, from record unemployment, to investor positioning, to comments by the US president. Yet while it’s tempting to see even lower rates as a potential positive, we would not.

Their track record, quite simply, is poor and provides plenty of circumstantial evidence that their damage to confidence and financial stability far outweighs the benefits. Since the eurozone and Japan implemented negative rates in June 2014 and January 2016, respectively, both regions have seen greater underperformance of their stock markets, economic growth, loan growth and bank valuations than the US (which kept rates positive). We think that the Fed’s long-standing reluctance to take rates negative is well founded, and our economists and interest rate strategists expect it to hold this line.

The second ‘good’ thing we’re worried about is a faster ‘reopening’ of the economy: Two weeks ago, market strength was attributed to the hope that many economies would see a faster easing of restrictions. But we think that this is backwards. Markets have historically been very forgiving of slow recoveries and extremely weak data, as long as they’re set to improve. But markets have low tolerance for losing that positive rate of change, which conjures up all sorts of terrible scenarios. We think that some of the weakness this week reflects increasing market concerns about that sort of relapse, especially in the US.

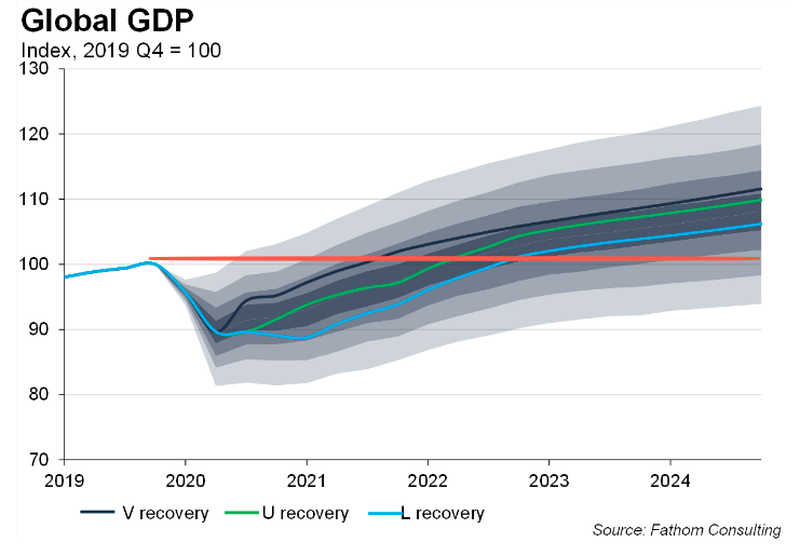

In turn, while we frequently hear that the market isn’t prepared for a slow, ‘U-shaped’ recovery, we would be more relaxed: After all, a ‘U’ implies that the worst is behind us, and the rate of change is positive. History suggests that markets routinely look ahead. And for all the talk that ‘the market is expecting a V-shaped recovery’, this is really not the impression we get from discussions with investors or from the leadership within the market. We think that actual economic expectations are pretty modest, as reflected in the low level of interest rates, the valuation discount of cyclicals and very high investor cash balances.

If a U-shaped recovery is one ‘bad’ development we’re actually more relaxed about, inflation is the second: For obvious reasons, there’s broad agreement among investors and economists that 2020 will see powerful deflationary forces unleashed by a collapse in demand. But opinions are divided about what comes after. My colleague Chetan Ahya and our global economics team believe that 2021-22 is more likely to see inflation than disinflation, as a gradual recovery in demand, aggressive policy action and continued de-globalisation all help to normalise price levels.

Is this a problem for markets? We don’t think so. The inflation we’re forecasting results directly from expectations of better economic growth in 2021 and 2022, and thus only occurs in a scenario where the underlying economy is in better shape.

We think that central banks will continue to err on the side of caution and provide significant accommodation into 2021, even if inflation starts to pick up. And our work suggests that the best forward returns for equities and credit occur when inflation is materially below trend (as it is today). Inflation overshoots do not bode well for forward returns, but such an outcome is still a long way off.

via ZeroHedge News https://ift.tt/3bCbi6x Tyler Durden