Detroit Police Issue 736 Citations, Shutdown Dozens Of Parties During Lockdown

Detroit Police have touted on social media that they issued hundreds of citations and broke up dozens of parties during the coronavirus lockdown, reported Detroit Free Press.

A new Facebook post via the Detroit Police Department details how thousands of folks across Wayne County, or mainly in the Detroit Urban Area, have neglected to follow Gov. Gretchen Whitmer’s stay-home order.

The post reads: “Thank you Detroit for being the eyes and the ears of our community. Since April 4, Detroit Police Officers have checked over 10,631 locations, given 1,614 warnings, issued 736 citations, shutdown over 24 parties and closed 27 businesses to ensure compliance with the Governor’s “Stay Home, Stay Safe” Executive Order…”

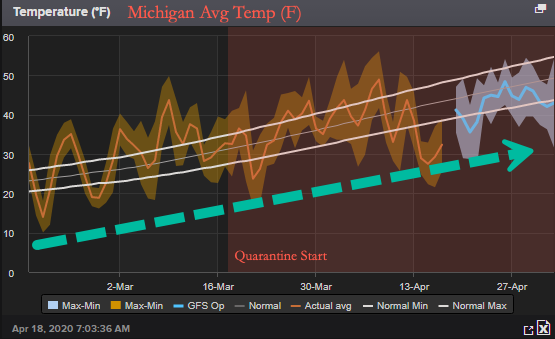

The incident report data was released on Friday and dated back to April 4. The problem developing, as shown in the chart below, is that warmer weather trends are ahead for Detroit, which means more and more people will be outside, and make it near impossible for police officers to enforce public health orders.

“Social Distancing Scoreboard,” an app that tracks the GPS location of smartphones and grades geographical regions, such as a town, county, and or even a state, on how well residents in those areas are abiding by the government-enforced social distancing rules, grades Wayne County, the area where Detroit resides, with a “C,” noting that residents are doing an okay job but not the best at following social distancing rules.

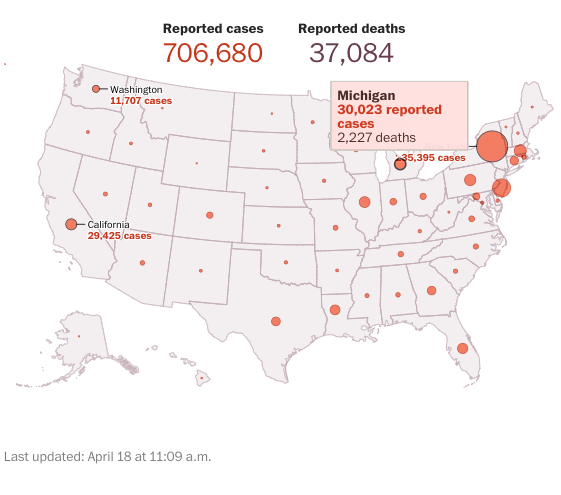

As of Saturday morning, 30,023 virus cases have been confirmed in Michigan, with at least 2,227 deaths.

Detroit police also said they shutdown 27 businesses that were illegally operating during the lockdown.

On Friday, Whitmer said the stay-at-home order would be relaxed on May 1. It came one day after conservative groups surrounded the state’s Capitol building and demanded a reopening of the crashed economy.

Warmer weather trends across the country are expected through April, making it near impossible for the government to enforce stay-at-home orders. This means probabilities will increase for a second coronavirus wave.

One year after a fire nearly destroyed the Notre Dame Cathedral in Paris, the cause of the blaze remains a mystery.

On April 15, 2019, the 850 year old gothic building was engulfed in flames, sending its iconic spire crumbling to the ground.

Despite police initially asserting that an electrical short circuit was the probable cause of the fire, Europe Echaffaudage said that the electricity supply to the two lifts on the site “was perfectly within specifications and well maintained.”

12 months on and there is no official conclusion as to how the fire started.

Le Journal des Arts reports that the coronavirus lockdown and the fact that the remains of the original scaffolding that the fire brought down is still on site has delayed the investigation.

“Experts still haven’t been able to gain access to the area where the blaze is believed to have begun, and that area will not be accessible until the scaffolding comes down,” reports ArtNet.

As we previously highlighted, following the blaze, the French government ordered state-employed architects not to give interviews to the media about the Notre Dame fire.

As the video below documents, in the days after the fire, BuzzFeed ran a fake news hoax denying that Muslims had celebrated the fire, despite evidence of this being manifestly provable.

I posted a video from Facebook showing users with Islamic names reacting to the burning cathedral with thumbs up and smiley face emoticons.

BuzzFeed then claimed in an article, “the video in question does not show what people on Facebook were reacting to.”

This was a complete lie. The video clearly shows the Notre Dame Cathedral burning in the background.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

It’s Not Just Toilet Paper, Seed Shortages Spread As Locked-Down Americans Turn To Growing Their Own Food

Americans are panic hoarding plant seeds as the coronavirus outbreak confines millions to their homes, crashes the economy, and disrupts food supply chains. This has resulted in people questioning their food security.

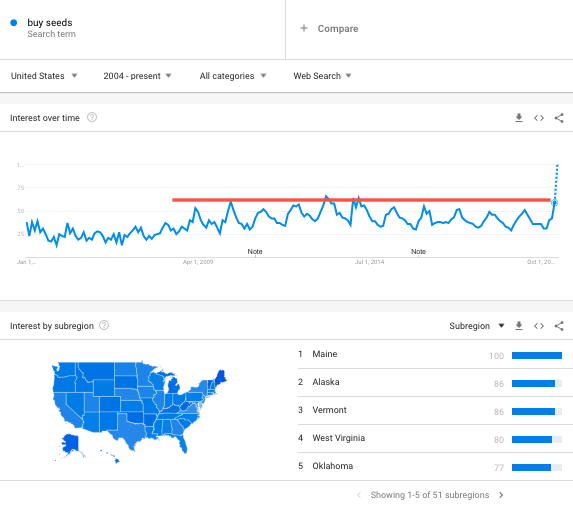

A Google search of “buy seeds” has rocketed to an all-time high across the US in March to early April, the same time as supermarket shelves went bare.

We’ve done a pretty good job of documenting the evolution of panic hoarding over the last several months. Americans started buying 3M N95 masks in mid-January, then non-perishables in February, followed by toilet paper, hand sanitizer, and guns.

Now apparently, plant seeds are the next big thing…

Seed companies who spoke with CBS News said they have stopped taking new orders after unprecedented demand. George Ball, chairman of Pennsylvania-based Burpee Seeds, said the recent increase in new orders is “just unbelievable.” The company will start accepting orders again on Wednesday after it stopped taking new ones for several days to catch up on the backlog.

Americans in quarantine are becoming increasingly concerned about their food security. What has shocked many is that food on supermarket shelves that existed one day, could be completely wiped out in minutes via panic hoarding. Some people are now trying to restore the comfort of food security by planting “Pandemic Gardens.”

“If I had to put my thumb on it, I would say people are worried about their food security right now,” said Emily Rose Haga, the executive director of the Seed Savers Exchange, an Iowa-based nonprofit devoted to heirloom seeds.

“A lot of folks even in our region are putting orders into their grocery stores and having to wait a week to get their groceries. Our society has never experienced a disruption like this in our lifetime.”

One of the most significant trends besides a crashed economy and high unemployment is that tens of thousands of Americans, mainly of the working poor, who just lost their jobs, are ending up at food banks. These facilities have reported surging demand, as a hunger crisis unfolds.

Today’s economic, health, and social crisis has made people realize that relying on supermarkets for food is not a safe bet. Some are now reverting to the land for survival.

Seed Savers Exchange noticed a surge in seed demand started in mid-March, the same time lockdowns across the country went into effect. The nonprofit has also halted new orders to catch up on the backlog.

“We received twice the amount of orders we normally receive,” the company said, adding it has had to hire more staff to deal with rising seed demand.

With America at war with coronavirus, the “Victory Gardens” our ancestors planted in WWI & II have now morphed into Pandemic Gardens. The surge in seed demand suggests a new trend of the 2020s is developing, one where reliance on corporations and government for survival are coming to an end for some people, as rural communities and living off the land is the safest bet in times of crisis.

And maybe now is the time to plant a Pandemic Garden considering Morgan Stanley is predicting a second coronavirus wave could arrive in the US later this year. In essence, that would mean more runs on supermarkets would be seen, jeopardizing food security for many.

Commentators routinely confuse the deflationary effects of a contraction of bank credit with the inflationary effects of central bank policies designed to offset it. Central banks always ensure their stimulus is greater, so inflation, not deflation, is always the outcome.

In order to understand bank credit, we must enter the mind of a banker and understand how it is created, why it is expanded and why expansion is always followed by a sharp contraction.

But we have now moved on from a simplistic credit cycle model, given the global economy was already facing a tendency for bank credit to contract before the coronavirus drove supply chains into the greatest global payment crisis in history. The problem is now so large that to maintain both economic stability and price levels for financial assets the central banks, led by the Fed, will have to issue so much base currency that fiat currencies will become almost worthless.

In these conditions the banks that survive the next several months will then begin to expand bank credit anew to buy up physical assets instead of their normal financial fare, sealing the fate of fiat currencies with a final expansion of bank credit as the banks themselves dump worthless currencies for real assets.

Introduction

Never has it been more important to understand the psychology and motivation behind changes in the level of bank credit at a time when governments and central banks are relying on commercial banks to transmit Keynesian stimuli to distressed borrowers. And never has it been more important for analysts to differentiate between deflationary forces that come entirely from the contraction of bank credit and inflationary forces that arise from central banks’ monetary policy.

Whether policies to rescue economies from the financial and economic effects of the coronavirus will actually get to the intended businesses depends largely on the transmission mechanisms for base money. While special powers for direct funding of large corporations may be implemented and the extension of public ownership to prevent bankruptcies of large players is very likely, commercial banks will be expected to play a central role in distributing monetary stimuli to businesses of all sizes. But since they regard small and medium size businesses as either too risky or not worth bothering with, it will be a struggle to get them to deliver the financial support intended.

In any advanced economy, a Pareto 80% of GDP is provided by small and medium-size enterprises. In a highly centralised banking system, for the banks that have access to the Fed through prime broker subsidiaries, SMEs are simply not worth bothering with. It leaves the majority of enterprises providing goods and services to the public out in the cold. Bankers looking through the dip will want to preserve more profitable relationships with large corporations and reduce their exposure to risky, expensive-to-administer smaller loans.

Despite the central banks’ generous intentions, the majority of businesses that rely on bank lending for working capital will therefore find finance frozen by bankers now driven by fear of risk instead of grasping lending opportunities underwritten by government support. Businesses with cash will learn that they are taxed by the debauchment of their money to subsidise failing competitors.

Investors who are used to getting positive returns solely on the back of expansionary monetary policies are now egging on the authorities to spend, spend and spend one more time. Penson funds and insurance companies in particular will now discover they are being lumbered with the cost of monetary expansion by an increasing depreciation of the currency, which escalates future liabilities. Ever since the investment industry pandered to the inflationary policies of central banks this outcome was inevitable, because both logic and sound economic theory tell us you cannot continually inflate your way out of trouble.

That end point is where we have now arrived. The state has come to rely completely on inflationary stimulation. The helicopters have warmed up and are ready to distribute monetary largess created by the magic of central banking, not just to individuals, but to their employers as well.

Mission impossible is to restore economic activity to where it was before the coronavirus shutdown. Politicians assume is can be achieved by deploying military precision. They have taken for themselves a mandate to sweep aside all bureaucracy and all objections to the role of the state. All it requires is for the banks as well as other critical actors to submit to their authority.

The credit cycle was turning down before the virus hit

It ignores the impact of the credit cycle, which was already turning down in the second half of last year. In response, the Fed first stalled its attempt to restore its balance sheet to normality and from September onwards was forced to publicly intervene to inject massive amounts of liquidity into the banking system through the repo market.

All was not well in wholesale dollar markets at least five months before the virus hit, so the problem is more complex than a simple return to normality when the virus passes. Furthermore, the authorities trying to keep the economy from imploding are out of their depth, so much so that individuals in the private sector are gradually realising it as well. Financial risk has escalated considerably, which has one effect: bankers will use every opportunity to reduce the size of their balance sheets. The authorities will struggle to get banks to hold fast, let alone distribute subsidies to producers and consumers alike.

Attempts at rescuing the global economy and supporting financial asset values upon which bank collateral is based will require massive inflation of base money, as outlined later in this article. But these attempts will have to fight bankers trying to control their lending risk in order to protect their shareholders’ capital from being wiped out. Their motivation to deflate bank credit will be greater than ever before.

An appreciation of the deflationary implications of the current phase of the credit cycle requires an understanding of how bank credit fluctuates and the predominantly psychological factors that drive it.

The origins of bank credit

The general public is not aware that there are two separate sources of money. The central banks are empowered to issue money, but commercial banks do so as well. One way they do this is by taking in deposits and then lending them to borrowers for an interest rate turn. When the borrower draws down the loan to make payments, more deposits are created as the payments are made.

A second course of money creation is simply by lending money into existence. In this case, the loan is created first, and as it is drawn down, deposits are created. This is regarded as the more usual practice, hence the description of the process being the expansion of bank credit. Any imbalances that arise between banks are resolved through the interbank market.

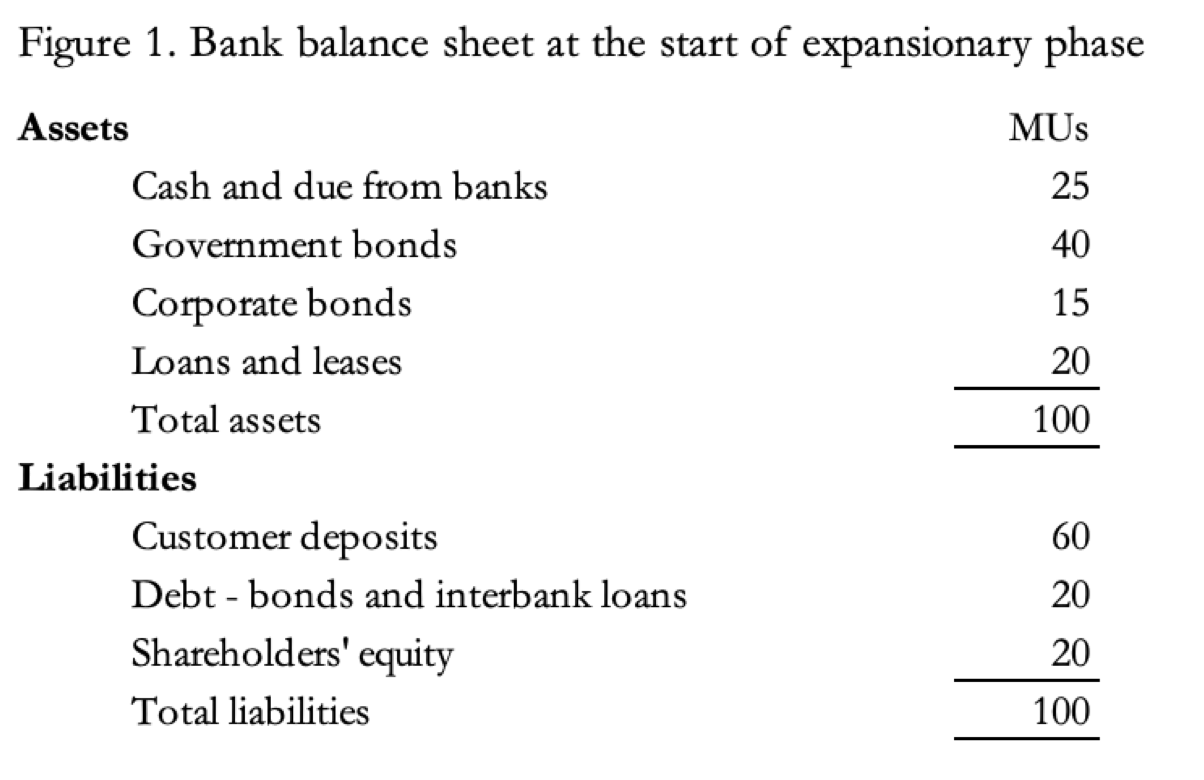

By these means a bank’s own capital becomes a fraction of the bank’s expanded liabilities, hence the term fractional reserve banking. Figure 1 shows the barebones of fractional reserve banking, with a bank’s balance sheet measured in monetary units (mu), early in a phase of credit expansion.

This balance sheet reflects a cautious approach to bank lending. Shareholders’ equity is valued at one third of customers’ deposits and is covered twice by government bonds, which will all be less than five years to maturity and is regarded in the banking system as the risk-free investment standard. At this stage of the credit cycle and with the banking community generally risk-averse, lending margins are profitable. The ratio of total assets to shareholders’ equity is five times. Put another way, profits and losses from changes in asset values are multiplied five times at the shareholder level.

Figure 2 shows the same bank’s balance sheet towards the end of the expansion phase of the credit cycle.

The economy has responded to both monetary stimulation from the government’s deficit spending and interest rate suppression by the central bank. The cohort of bankers has seen a lessening of lending risk and has responded by actively seeking lending opportunities among large corporations. Bankers are now lending increasingly to medium size corporations as well as investment grade rated borrowers where the margins are better. Falling unemployment and growing economic confidence decreases lending risk for credit card and other consumer debt, and the bank has extended additional credit for creditworthy customers. Liquidity from government bonds and bills has been drawn down in order to increase allocation to higher-yielding corporate debt. The balance sheet has expanded to give an overall gearing on shareholders’ equity of 12.5 to 1.

This means a two per cent margin averaged across total assets yields a 25% profit on share capital. But by the time this snapshot is taken, competition from other banks will have likely reduced lending margins generally, and the bank has responded by taking an even more aggressive lending stance, so lending margins overall are likely to be less generous than at the start of the credit cycle and loan quality will have deteriorated.

While shareholders are enjoying excellent returns, it has become a highly risky situation for the bank. The slightest pause in the economic outlook, whether it be from interest rates being raised by the central bank attempting to control the boom, or perhaps an exogenous factor, such as trade tariffs being raised between the bank’s jurisdiction and a major trading partner, will cause the directors of our bank to switch from greed to fear in a heartbeat. In our example, all it takes is losses of 12.5% of the bank’s assets to wipe out shareholders’ equity.

If one bank suspects there may be a deterioration in trade conditions, it is certain that others will as well, because they have similar business information. Due to the dangers of balance sheet gearing, bankers are exceedingly prone to groupthink.

When it happens, the switch from greed to fear travels like wildfire. But some banks are likely to be caught out, having been aggressive lenders trying to increase the size of their bank, often with a chief executive on an ego trip. Fred Goodwin at Royal Bank of Scotland was a recent example. Ignoring all signs of the ending of a cycle of credit expansion, Goodwin pushed through a consortium takeover of ABN-AMRO in October 2007, with RBS’s portion funded by debt. The bank’s balance sheet gearing became twenty-four to one.

With gearing of that sort very little needs to go wrong to wipe out shareholders equity, which is what happened. Failures of this type are an acute risk when the banking cohort has been lulled into a false sense of lending risk by a prolonged period of business stability combining with the siren’s beckoning of a financial bubble.

Reducing bank balance sheets without creating economic instability is virtually impossible. Driven by their groupthink, frightened bankers will seek to reverse credit expansion all at the same time. They sell corporate bonds in a market with no buyers. Spreads, the difference in yield between government bonds and riskier corporate debt, blow out, catastrophic for book values. Business and personal loan facilities are capped and withdrawn, driving many companies into the hands of insolvency practitioners. It can become a race between bankers to reduce the size of their balance sheets before their competitors, as the rapid withdrawal of bank credit triggers bankruptcies and unemployment. It has happened repeatedly for the last two hundred years.

The economic effect was summed up by economist Irving Fisher in the 1930s, who is forever associated with the theory of debt deflation. As the oxygen of credit is withdrawn, businesses get into trouble and banks begin to liquidate collateral. Liquidation of collateral drives their values even lower, exposing additional formally secured lending as no longer secured. Further collateral sales follow, driving collateral values down even further. And so on.

That was in the depression years, and Fisher’s point was to link the collapse of businesses, asset values and also the failure of banks themselves with the contraction of bank credit. Subsequently, central bank policy has focused on trying to anticipate and stop the deflation of bank credit in the first place, always ready to turn on the money spigot. The government then subsidises the economy by increasing its spending without raising taxes. By using the stimulus of unfunded government spending and central bank money creation, the government and its central bank are following the Keynesian economic playbook, which now sets the relationship between the state and private sectors.

Despite everything attempted by statist intervention, we still have periodic bouts of bank credit deflation. But matters have evolved from the simple model illustrated in Figures 1 and 2 above. Banking has become highly regulated, and banks now lend on a formulaic basis, set globally by the Basel Committee (we are on rules version 3) and by local regulators.

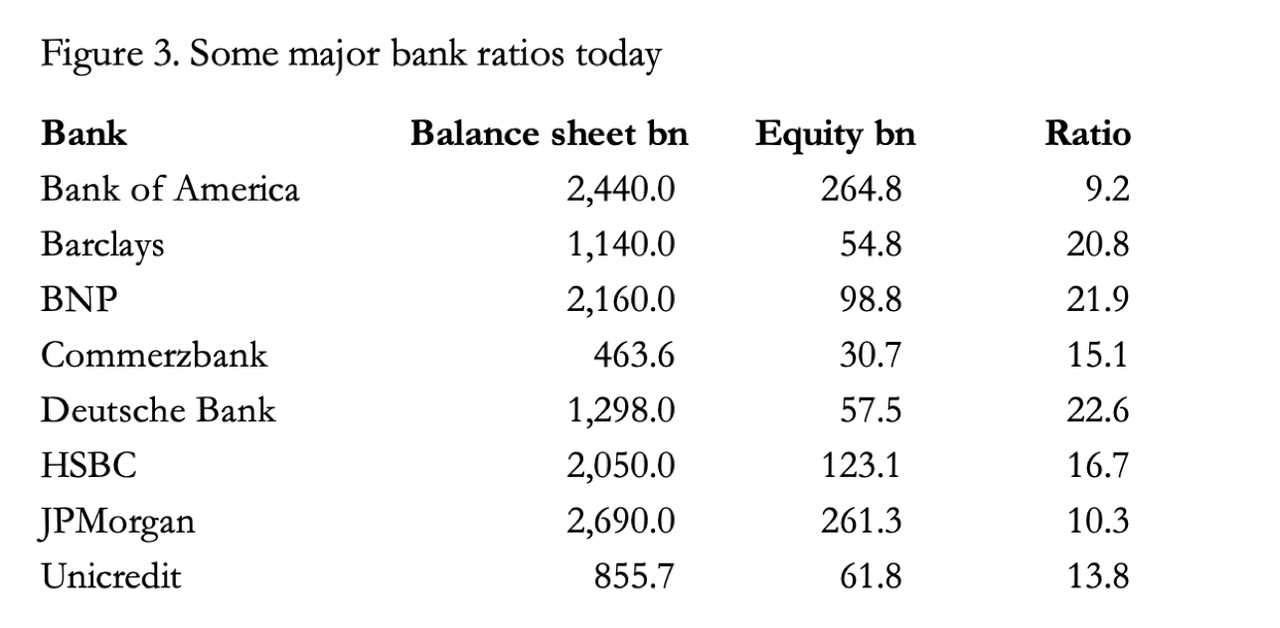

Earlier versions of these controls permitted Fred Goodwin to take the RBS balance sheet gearing to credit hyperspace. They say lessons were learned, but the only lessons learned by the regulators were new ways to keep their eyes shut and ears plugged. Stress testing of bank balance sheets assumes little more than a moderate recession and denies the likely consequences of anything worse. The economic crisis starts with a change in banking cohort groupthink, and not, as regulators with their useless stress tests assume, a decline in GDP, a rise in unemployment, a rise in price inflation, or Heaven forfend, an unexpected financial crisis. And if you think extreme bank leverage would have been controlled following the Fred Goodwin episode, think again. Figure 3 shows current balance sheet to equity ratios for a selection of major banks. Through the magic of modern accounting practice, they are almost certainly higher than reported.

From the few examples in Figure 3 we can anticipate bank failures to originate in Europe in the event of a general contraction of bank credit. Despite reducing its balance sheet significantly in recent years, Deutsche Bank is in Fred Goodwin territory, closely followed by BNP and Barclays. And the credit cycle has very obviously turned down again. The regulators persist in behaving like the three wise monkeys, wholly unaware there is a credit cycle and what these ratios indicate.

The large American banks are not so heavily geared, but that will not protect them from the global credit contraction that will now intensify.

Enter the coronavirus

We have made the important point that before the coronavirus lockdown, the credit cycle was already turning down. Liquidity strains had surfaced last September, with the Fed routinely supplying tens of billions of dollars of liquidity through the repo market.

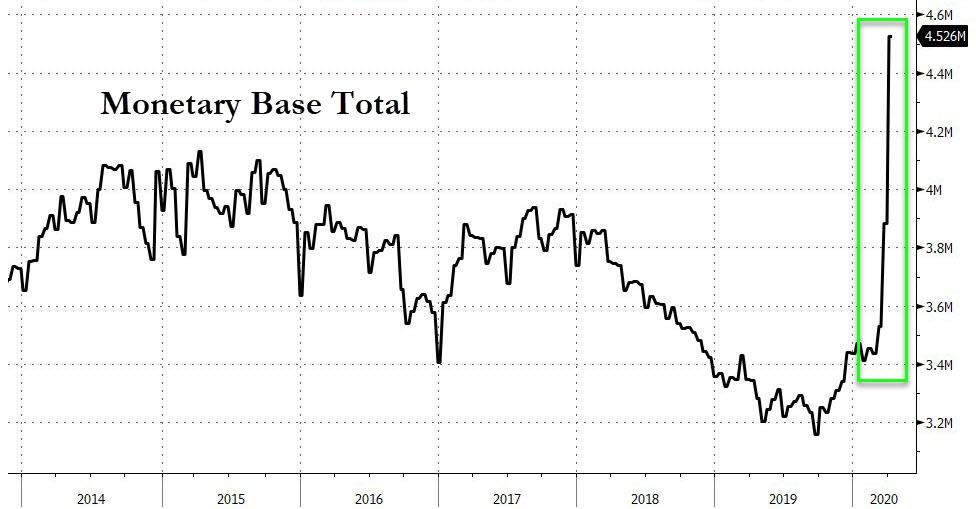

The monetary base, which represents the quantity of money in public circulation created by the Fed, is now growing at the fastest pace on record. But since January, a new problem arose: the disruption to production supply chains from the virtual shutdown of Chinese production due to the coronavirus.

The manufacture of anything requires multiple inputs, commonly referred to as supply chains. The concept of a supply chain suggests they are one dimensional: a series of production steps that go towards a single product. This is not the case. Supply chains are multidimensional and involve supplies from many sources in many jurisdictions at every production stage. The sequential shutdown of China, South Korea and much of South East Asia was followed by Europe, Britain and America. During these shutdowns almost all production and sales of non-food goods and non-essentials ceased.

While the assembly of a product progresses in one direction, payments flow backwards down the chain as each production step is delivered. The sum of the payments involved is far greater than the value of the final product. The global payment disruption is therefore significantly greater than the GDP number, which only consists of the sum total of final products bought by consumers. In the case of the US, an approximation of domestic payment disruption is contained in the gross output statistic, which is $38 trillion compared with a GDP of $21 trillion.

The US economy is significantly services-driven, with shorter supply chains on average than an equivalent manufacturing-based economy, such as China or Germany. If you add together supply chain payments abroad that feed into final goods sold in America, total payments for intermediate production stages in dollar-driven production probably add up to more than $50 trillion, the majority of which are now frozen.

To understand the impact of this new factor on bank credit, we must divide business customers into two classes; those with cash and those that depend on bank loans for working capital.

Both categories have establishment and other costs that continue despite the collapse in production. Those with cash liquidity draw it down to make payments, reducing bank deposits, which are recycled into other deposits which may or may not be with the same bank. When those deposits reduce existing overdrafts, bank credit contracts reflecting a loan repayment. When they amount to a simple transfer of deposit ownership, they do not.

The greater problem is with businesses that need loan cover for missed payments. There are so many of them with payment failures, bankers are being overwhelmed. Whether they realise it or not, they cannot afford to say no to demands for credit because Irving Fisher’s debt deflation problem is so urgent that to deny loan requests would likely end up wiping out the banks’ own shareholders’ capital and then some.

Supply chain payment failures are becoming a banking problem many times larger than the banking cohort shareholders’ capital. The ratio of US gross output to total equity capital for commercial banks in the US is nineteen times. In other words, unless the Fed can increase base money by at least that and somewhat more to compensate for a degree of bank credit contraction, the economy and the banking system will almost certainly crash.

In Germany, where the two major private banks shown in Figure 3 have balance sheet to equity ratios of 15.1 and 22.6, supply chain disruptions seem certain to lumber them with a fatal combination of dramatically widening commercial bond spreads and payment failures from the mittelstand.

Everywhere else, the problem is the same. The Fed has responded by reducing the cost of drawing down established central bank liquidity swaps lines, but they were only available to the ECB, the Bank of Japan, The Bank of England, Bank of Canada and the Swiss National Bank. Recognising the wider problem, on 19 March the Fed extended swap lines temporarily to the central banks of Korea, Australia, Brazil, Denmark, Mexico, New Zealand, Norway, Singapore and Sweden for six months. A notable absentee from the list is China, which one would have thought is the most important user of dollar liquidity based on trade. Politics trumps the delivery of monetary policy in defiance of the scale and urgency of the crisis.

The problems facing the whole banking system have never been greater. Individually, commercial banks are bound to take every opportunity to reduce their risk exposure before the market values of collateral, particularly equities, corporate debt and both residential and commercial property categories fall further in value. Banks will attempt to reduce their interbank exposure, particularly to European banks. Eurozone banks are likely to be the first to fail, needing state bail outs. Counterparty risk in over-the-counter derivatives becomes a major concern for all. And central banks are on a wing and a prayer if they think commercial banks will simply ensure liquidity gets to the right places in time to prevent a financial crisis.

The final crack-up boom

The Fed and other central banks can only blag solutions to a rapidly debasing currency, but the commitment to maintain financial asset values by printing money in the manner of John Law three hundred years ago will require such enormous amounts of base money as to bring forward the destruction of the fiat dollar and all the other fiat currencies. Banks will have fought for survival in this changed world, with many of them succumbing to public ownership.

In this rapidly deteriorating environment, it won’t be long before the smarter bankers realise that they can deploy the expansion of bank credit to acquire not financial assets, which will become worthless being priced in worthless currency, but real assets. The model adopted is likely to be that of Hugo Stinnes, who in 1920-Germany was known as the inflation king. Stinnes borrowed rapidly depreciating marks to buy up factories and property, amassing an empire of 4,500 companies and 3,000 manufacturing plants. Stinnes died in 1924, the year after the great inflation, and his empire subsequently collapsed.

Banks emulating Stinnes have an additional advantage. They can make acquisitions as principals by expanding bank credit again when they are confident that repayments when falling due will be worth significantly less. Bankers under the cover of nationalised banks might even direct the expansion of bank credit into newly created vehicles in which they have personal interests. This behaviour is atypical and might even have the support of a hapless state desperate for any form of financial stability.

This last act, the restoration of bank credit in its relationship with base money will add a rising multiple of the trillions of central bank base money scheduled to be issued in the coming months and will be a vital component of the crack-up boom with which all currency collapses end. The role of the banks as the medium with which the state seeks to tame free markets will ultimately hasten the end of the fiat currencies from which they have profited so much, and the end of central banking as well.

There’s no denying that a big chunk of the economy feels pretty screwed up right now for millions of working-class and middle-class Americans. There’s a widespread sense that obtaining housing, education, and health care was once fairly easy and cheap but has now become mind-bogglingly complex and expensive. Addressing anxiety around the increasing elusiveness of these building blocks of an archetypical American life is at the heart of virtually all rhetoric in the 2020 election cycle, with everyone from democratic socialist presidential hopeful Bernie Sanders to nationalist conservative Sen. Josh Hawley (R–Mo.) hastening to offer funeral orations for the American Dream—while also promising to resurrect it.

What follows is a forensic investigation into how the markets for health care, higher education, and residential housing got broken. The goal is not, in this issue, to offer a comprehensive set of solutions, though you’ll see hints about possible remedies throughout. Nor is it to challenge the premise that times are tough. There is much to celebrate in the modern American economy, but pointing out the ways in which things are pretty good overall doesn’t go far with people who feel like they are drowning.

Instead, we went looking for the moments at which these parts of our economy veered off track. When you reject the too-simple narrative about greedy corporations bleeding ordinary Americans dry, more complicated and (unfortunately) more intractable causes for the current crisis emerge. In each sector, well-intentioned efforts by the government to address real problems created the conditions for a vicious cycle of rent-seeking, cronyism, innovation suppression, crippled pricing mechanisms, spiraling spending, and growing debt. These are stories about how seemingly small policy changes can have big effects on incentives and choices down the line, for politicians and citizens alike.

If we’re going to restructure American politics around restoring some version of the American Dream—as both Republicans and Democrats seem keen to do—we should at least know what we’re facing and why. When you’re trying to fix something, it’s important to understand how it got broken in the first place.

For Reason‘s May 2020 issue deep-dive into how things got so bad, read:

There’s no denying that a big chunk of the economy feels pretty screwed up right now for millions of working-class and middle-class Americans. There’s a widespread sense that obtaining housing, education, and health care was once fairly easy and cheap but has now become mind-bogglingly complex and expensive. Addressing anxiety around the increasing elusiveness of these building blocks of an archetypical American life is at the heart of virtually all rhetoric in the 2020 election cycle, with everyone from democratic socialist presidential hopeful Bernie Sanders to nationalist conservative Sen. Josh Hawley (R–Mo.) hastening to offer funeral orations for the American Dream—while also promising to resurrect it.

What follows is a forensic investigation into how the markets for health care, higher education, and residential housing got broken. The goal is not, in this issue, to offer a comprehensive set of solutions, though you’ll see hints about possible remedies throughout. Nor is it to challenge the premise that times are tough. There is much to celebrate in the modern American economy, but pointing out the ways in which things are pretty good overall doesn’t go far with people who feel like they are drowning.

Instead, we went looking for the moments at which these parts of our economy veered off track. When you reject the too-simple narrative about greedy corporations bleeding ordinary Americans dry, more complicated and (unfortunately) more intractable causes for the current crisis emerge. In each sector, well-intentioned efforts by the government to address real problems created the conditions for a vicious cycle of rent-seeking, cronyism, innovation suppression, crippled pricing mechanisms, spiraling spending, and growing debt. These are stories about how seemingly small policy changes can have big effects on incentives and choices down the line, for politicians and citizens alike.

If we’re going to restructure American politics around restoring some version of the American Dream—as both Republicans and Democrats seem keen to do—we should at least know what we’re facing and why. When you’re trying to fix something, it’s important to understand how it got broken in the first place.

For Reason‘s May 2020 issue deep-dive into how things got so bad, read:

With countries around the world in quarantine or lockdown mode to deal with the Wuhan coronavirus or CCP virus pandemic, what can we expect in terms of economic fallout?

What will happen to the US, Chinese, and Hong Kong economies as the pandemic wanes?

And why is Hong Kong’s situation particularly perilous?

In this episode, we sit down with Kyle Bass, the founder and chief investment officer of Hayman Capital Management, a Dallas-based hedge fund. Bass is a founding member of the Committee on the Present Danger: China, and he is also Chairman of the Board of The Rule of Law Foundation.

This is American Thought Leaders 🇺🇸, and I’m Jan Jekielek.

This interview has been edited for clarity and brevity… emphasis ours.

Jan Jekielek: Kyle Bass, such a pleasure to have you back on American Thought Leaders.

Kyle Bass: Thank you. Great to be here, Jan.

Mr. Jekielek: Kyle, you’ve been this fierce speaker on the Chinese Communist Party’s culpability behind this virus. We’re going to talk about all sorts of economy-related stuff because this is your wheelhouse and everyone wants to hear.

Mr. Bass: I just think it’s important for the press to really think about, and for the world to think about what really happened in a timeline, and not some conspiracy theory because China won’t allow us in, and won’t allow our scientists to try to find patient zero and origin of the virus. And in fact, you’ve probably seen recent communiques between the Chinese Communist Party and their labs that their lab output has to be censored by the CCP, or that has anything to do with the Wuhan virus, [has to be approved] before it goes to the rest of the world. So, they are very sensitive on this topic—number one.

And number two, if you look back to the timeline, and you understand what happened, China has an enormous culpability. They actually have a legal liability, and one that’s a financial liability. I don’t know if you’ve seen various interviews in the last few days of U.S. legislators but there is a growing tide, of not only resentment, but a growing tide of people in the legislative branch of the U.S. and the UK governments, and now it’s bleeding into Australia and Canada, where they’re starting to say that we need to use the rule of law, the U.S. rule of law, the British Common Law, to start talking about reparations and getting the Chinese government to pay for their malign actions. And I think it’s important to note: on December 31, there were already 104 cases and 19 deaths in Wuhan. The Wuhan scientists, the heroes who first found this strange new pneumonia that was propagating itself so freely in Wuhan, not only were they arrested, and punished, and forced to retract statements that they had put on WeChat, but as you know, since then, one of the doctors who was 33 years old has died from the Wuhan virus.

Secondarily, that all happened in December. So by December 31, the government of Taiwan sent a white paper to the World Health Organization explaining that they had full evidence that there was human-to-human transmission, and that it was going to be a new global pandemic. And if you remember, on January 14, Tedros said to the world in a proclamation on a Tweet that this is not a global pandemic, and that he had just consulted with Xi Jinping and the Chinese, and that there is no evidence of human-to-human transmission—this is January 14. And then January 23, Xi Jinping closed down all air traffic from Wuhan to the rest of China. But he allowed Wuhan air traffic to travel to the rest of the world. Essentially, Xi Jinping knowingly infected the rest of the world. … “If he’s going to go down, the world is going to go down with him,” essentially what he was saying. That is not a responsible actor. That is not a government who’s ideologically aligned with the rest of the West. This is a government that basically covered up the truth. And we all know that they covered up the truth, but now, it’s actually after Neil Ferguson’s Boston Globe article, and now you see that the Chinese Foreign Ministry said on February 2 that it is xenophobic to close anyone’s borders to the Chinese, and that travel restriction shouldn’t be made. Xi Jinping himself shut down Wuhan, January 23; this is February 2, they’re telling the world this.

They are the most lying, coercive, manipulative government in the world, and you and I both know, they are committing the largest crimes against humanity prior to this outbreak of the sinister virus that God knows where it really came from—somewhere between the Wuhan wet market, the Chinese Center for Disease Control, which is right across the street, or maybe 20 miles north, at the Biosafety Level 4 lab in China. But the bottom line is, this disease has been unleashed on the rest of the world, and it was knowingly done so. And that’s why I’m so visibly upset about this.

And I think that you probably saw the Jackson Foundation in the UK, the Harvard professors in the U.S., are starting to set forth a legal framework for which international laws (that) China has broken, and the fact that there is a financial liability. As you remember, Chinese [SMEs] (small-medium enterprises) have businesses, and properties, and stock issued in all the various markets in the West. There is a way that we can go after them and grab their assets. And [Mitch McConnell] this morning in an interview on Maria Bartiromo’s show said that China also owns a trillion dollars of U.S. Treasury bills, and those are just book entry bills. We could actually grab and basically forgive that debt—basically cancel that debt. There are plenty of things the government can do here to make China pay for its actions. And the beauty of all that, Jan, is one thing we’ll never be able to do: the West will never stoop to China’s lows. We will never out-lie, we will never out-cheat, will never out-steal, the Chinese Communist Party—they’re the “best” in the world. But what we can do is we can use the foundational bedrock of our countries, the rule of law, and we can exercise and enforce our laws on them for their malfeasance. And that is the play, that is how we level the playing field, against such a tyrannical lying actor.

Mr. Jekielek: I was aware of all these facts, but the culpability is so obvious, right? It’s almost like it takes an extra level of crazy spin-doctoring to try to say, “No, China is the hero. The Chinese Communist Party took care of everything incredibly well, and now, world, you should probably thank us for that.”

Mr. Bass:I think Xi is overplaying his hand because seeing something like that and seeing something like what (Lijian) Zhao said that it was the U.S. military that brought it to Wuhan, their counterclaims are so outrageous that it makes them look stupid, and I think you have this scenario today where there are really four wars we could be fighting with China, and we’re fighting three of the four. There is the information/ narrative war that they’re active every single day fighting with us and the rest of the West. There is the cyber war, which they’ve been fighting for the last 20 years, and they fight it every single day—they’re on offense in the cyber war mostly. Then there’s the economic war. And then there’s the kinetic war. We’re fighting three or four wars with China as we speak, and one could say that the new battlefield, let’s say the battlefield of the 21st century, isn’t going to be with planes, and tanks, and boats. It’s going to be on the economic front, on the cyber front, on the narrative front.

There are 70-plus official Chinese blue-check accounts on Twitter, and they are either ambassadors or official ministry spokespeople for China. Twitter is banned in China; why do we let them on there? Why don’t we put a red propaganda diagonal sticker across every single thing they say? It is absolutely insane that we allow official Chinese accounts on Twitter without labeling them as propaganda, just like the Global Times, and Xinhua, and [inaudible], and all of these different Chinese propaganda outlets that disguise themselves as media. Again, there’s so many things that we need to do that are really easy to do.

Mr. Jekielek: If there is possibly a silver lining to this whole crazy situation, the suffering inflicted upon the world, … you and I both know this realization has been a long time coming. These aren’t new activities, as you’ve said.

Mr. Bass: Yes, the misery that China has brought to the rest of the world with this virus has really been shining a disinfecting light on global supply chains reliance. Think about this: we have Western democracies relying almost completely on a supply chain in a totalitarian, communistic nation. It’s actually insane when you lay it out like that, right? We could go back to our corporate boards and say, “Did you really do this? Because maybe you really weren’t thinking about the different potential avenues for supply chain connectivity.”

But to your point, there is a silver lining, because number one … you and I know Rosemary Gibson. Rosemary Gibson wrote the book in 2018 about the U.S. over reliance on China for prescription drugs and even OTC, over-the-counter drugs, where they manufacture 90% of the active pharmaceutical ingredients for all U.S. antibiotics. It’s actually crazy that we’ve let this happen. We’ve been with a really good [inaudible] from, let’s say, a microchip perspective, and from the perspective of strategic rivalry in very key technological areas, but we completely missed the drug—a national security problem. Well, the good news is, Jan, we’re not going to miss it anymore. We got this. We are going to legislate drug production here in the United States, so that no communistic sovereign actor can decide whether or not our military gets drugs to the hospital, or not—or population. Think about this: we get 100% of our blood pressure medicine from China. 100%. There are 700,000 people in the United States who take blood pressure medicine every single day. We have a 13-day supply. This is insane. This has to change. That’s the silver lining as these kinds of things will change.

Mr. Jekielek: Talk about leverage on the side of the Chinese Communist Party with just this one thing: the blood pressure medicine. It’s astounding. Tell me a little bit about what you’re seeing with respect to the economic situation globally. I’m looking at a headline right now in which the IMF says that the great lockdown is going to be worse than the global financial crisis.

Mr. Bass:I would name it the “sinister Wuhan virus lock-down”, right? The supernational institutions have all been infiltrated by the Chinese government, and so they call it “COVID-19”, you’re calling it the “coronavirus”—it’s the “Wuhan virus.” That is exactly where it came from. It’s how virus nomenclatures worked for hundreds of years; we should stay with that. And it’s not “racist” to call it something that it is. And so, I think from the perspective of the IMF and the economy, the U.S. alone has already lost 16 million jobs. … We think there’s been 4-5 million new (unemployment) filings last week. So we have 20 million jobs that have been lost today. That 16% unemployment in the US alone. And so, as you know, the better part of 3 billion people are under quarantine, homestays, today, and the global economy is off. And so, when you turn a $23 trillion economy like the U.S. off for between 60-90 days, you’re talking about a $6 trillion hole. We’re going to have to run a 15% or 16% fiscal deficit this year, at the very least. I actually think it will be bigger than that. Next year, it’s going to be north of 10%. During the global financial crisis, we never got wider than a 10% of the GDP fiscal deficit. So, the IMF is right in its numbers. The question is, can we bounce back quickly once we have a vaccine and treatment, and relax our social distancing? I think it’s going to be a little bit more difficult than markets imply at this moment in time.

Mr. Jekielek: I’m sure all your investors are running to asking questions about this: What is this going to look like? What does recovery look like? Is it V-shape? Is it U-shape? How fast are we going to actually be able to bounce back? Do you have any sense of this at this point?

Mr. Bass:It’s my view and our firm’s view that it’s going to be a W. It’s not going to be a U or V, or an L. I think that with people holed up in their apartments, their homes, and not able to work from their place of business, and the restaurants are closed, and the whole service economy’s off. When things start to become loosened, and people get out and start to get back to work, the animal spirits are going to be conjured in a positive way; not in the negative way that this began. But I think we’re going to see a lot of enthusiasm, a lot of optimism, because as Americans, we get out of bed every day and we’re very optimistic, and we have the best intellectual property in the world, the best educational institutions in the world. And so, I think we’re going to hit the ground running pretty hard.

I’m fearful—and I’m very dangerous because all I’ve read (are) a few white papers on the subject; I’m not a virologist by any stretch of the imagination—but it sure looks to me, we have 70 vaccines that are currently under research and review. And at some point in time, I believe that the world, given its intense focus on the subject, is going to develop a vaccine for this hideous Wuhan virus. But I think that’s probably going to take until the end of the year, Jan. So, I don’t know how international travel bounces back because I can tell you, I won’t get on an airplane until there’s no virus, right? I will never cross the pond again, until there’s a vaccine. And so, I don’t think you’re going to see the same level of business activity right away. And so, I say a W because I think we’re going to have an initial spurt, and then the question is when flu season comes back this fall, does it show itself again?

As we’ve seen in Singapore and Hong Kong, we’re having reinfection. And we’re actually having reinfections of those that are believed to have developed an antibody—[people] that have already recovered from the virus. And so, this is going to be a bit of a slog. And I think a W shape recovery is what we’re looking at. And I think, hopefully, Melinda Gates gave an interview a couple of days ago where she said, … “We think we’ll have a vaccine in the next 18 months.” If it’s 18 months from now, it’s a real problem, Jan. If we don’t get people back to work in the next 45-60 days, we’re going to have damage that’s irreparable, and we’re going to have a much longer lasting damage, and it will also damage the psyche of all the participants. If you remember, there was a profound change in the proclivities of those that suffered the Great Depression. … You probably heard from your father, and your father’s father, about an aversion to debt because it wiped people out back then. And not only did it affect that generation, the 1920s, 1930s, 1940s, but it also affected the baby boomers that were born to that generation, right? And so, there were two entire generations whose actions were influenced by one very specific, horrible financial event. And I believe this will be somewhat of a similar event from the perspective of how people operate their lives going forward. It will not go back to where it was.

Mr. Jekielek: Kyle, we just recently had a mental health expert, psychiatrist, pharmacologist, talk about the effect of this lockdown on suicide rates and a whole range of”side effects”. They’re not really “side” because they’re a direct result of what’s actually happening. I couldn’t help but remember this Tweet that you put out recently saying that perhaps there’s been a “delay in reporting” in the Chinese numbers. Well, it looks like there has been a “delay in reporting” the Tiananmen Square numbers, to that point. So, I’m guessing you don’t really believe the Chinese numbers. What are the implications of this?

Mr. Bass: I’d be willing to bet you, Jan, if you did a 100,000-person survey in the United States, every socio-economic group, and you ask them, “Do you believe the Chinese government numbers?” I would be willing to bet you today that would be an 85% super majority, “No.” … From the origin of the virus and 1.4 billion people, not one of them passed away from the virus when it’s on every continent, and we have millions of cases all over the world? And they say, “No official deaths today,” and I thought back, “Well, they haven’t ever officially reported any deaths from the Tiananmen Square incident, so maybe there’s just a ‘lag in reporting’.” It was a little tongue in cheek saying, “Why should we ever believe the Chinese government?” They just lied to the world in January, and they covered everything up, and now the world is where it is today, and somehow they want us to think that Huawei is the savior because Huawei is delivering masks to hospitals in New York City and Washington, DC. That’s it. Their soft diplomacy—”soft” because they’re delivering masks—it’s so clear what their motives are, and what they’re trying to do and take advantage of a situation that they created themselves. And it’s just ugly. And I think that even Joe Sixpack in the United States, even the guy that grabs a six pack of beer and goes to a NASCAR race, understands that the Chinese government is not trustworthy, they’re not our friends, and one could deem them to be our mortal enemy. And at some point in time, I think Wall Street’s view is going to have to change. And I think it’s happening now.

Mr. Jekielek: We were talking about the pharmaceutical industry sourcing just about everything from China. And I’m thinking about the Buy American executive order. It seems like a no brainer to repatriate critical medicine production. Why is this being stalled or slowed down?

Mr. Bass: I’m sure you’ve heard that the Chinese Communist Party decided that anyone that’s to move their supply chains out of China needs a permit to leave. I don’t know if you’ve heard that in the last couple of weeks. But for the last three years, really since the fourth quarter of 2016, when the Chinese completely closed off any kind of external foreign direct investment by rank and file Chinese and even the government—if you remember when they closed the door when they were having a serious currency devaluation problem—companies that do business in China, whether you’re Intel, or Sony, or BMW, or Chevron, those companies haven’t been able to get their dollars out of China, their dollar profits, since the fourth quarter of 2016. I know several of them have hired friends of mine that are former bureaucrats in U.S. administration who have relationships with Wang Qishan, with Xi, with his party, trying to get the money out. They haven’t been able to get the money out for four years, Jan, and now we’re being told that maybe you can’t get your supply chains out.

Shinzo Abe of Japan, as you probably saw, set forward a program of US$2.25 billion to pay the actual moving costs of the Japanese companies that want to move their supply chains back to Japan, from China. And you probably heard, even Larry Kudlow (Director of the United States National Economic Council) said, “We think that’s a great idea and we should do that.” I am all for setting aside and legislating a pool of capital to help our institutions leave China. And I think that’s, again, a moral imperative—I think we should be out of there. All of the cheap tennis shoes, and T-shirts, and trinkets we buy from China is nowhere near the amount of money that they steal from us every year in intellectual property. People say, “Well, if we just disengage with China, it’s going to cost us 2-2.5% of GDP. To that I say, “They steal 2% of GDP from us every year in intellectual property, and they earn a return on that. It’s actually a better deal for us to just stop. I know that sounds hyperbolic, but it’s just a fact.

Mr. Jekielek: You’ve been a big advocate of decoupling—bringing the economy out of China. Has anything changed with respect to that view, or the approach, since all this new information we have?

Mr. Bass: I think the silver lining of this horrible virus is that it’s going to accelerate this decoupling. We’re going to have forced decoupling from a national strategic perspective, let’s say, from our government, and I think there’ll be forced decoupling from many other Western governments. And then you’re also going to see corporate boards … forced to rethink their whole supply chain immediately. So, this is no longer, “Well, we’ll think about it next year, or maybe in our three- or five- year plan. We’ll think about how to maybe open our next factory in Vietnam, or Cambodia, or Mexico, or one of the other competitors to the Chinese factory floor.” Now, it’s forcing everyone to do it right away, and that’s a beautiful thing. So, all this has done is speed up something that had to have been done in the past, (but) people were just dragging their feet.

Mr. Jekielek: Can you foresee a situation where the Chinese Communist Party says, “Sorry, everything that’s in here, we’re keeping it”? They’ve already done that in a few instances—the nationalizing of certain factories and so forth.

Mr. Bass: Yes, I know of a company that I’ll leave unnamed, a very large public company, that has $10 billion in cash on its balance sheet as per its annual filing, and $1.5 billion of that money is in China. They haven’t been able to get it for four years, and I don’t know how they’re ever going to get it out, truthfully. And so, this is what I worry about: our pensions and all of the money that China has figured out how to coerce MSCI and the various index providers, the passive providers, to weigh China so heavily. In the MSCI Asia index, if you include U.S. listed ADRs, they’re now 48% of the index, right? They’re supposedly 15% of global GDP, but less than nine-tenths of 1% of global currency cross border transactions settle in Chinese currency. There is a Potemkin Village here. There is an economy that we give them the credit for because we dollarized it at the current dollar exchange rate… Think about this: They’re supposedly the second largest economy in the world, but they have a closed capital account. They’re not a real country. They are ideologically 100% different than the developed West, and economically, they couldn’t be more closed if you look at their capital account. They only have it open enough to buy the things that they need to buy, that they’re so desperate to buy. They have to buy food, they have to buy energy, they have to buy base materials, and they have to buy base metals. They have to buy those things from the rest of the world and they have to spend dollars. They need blood to fuel the CCP tumor, and that blood is dollars. And all they do, their entire MO with Belt and Road, and with cajoling the index players to figure out how to get U.S. dollars into China, because they need those dollars to buy things. No one will accept Chinese monopoly money because no one trusts the government. The beauty of this is once our government really understands this, we hold all the cards—the U.S. government holds all the cards.

Mr. Jekielek: I want to ask you about the realities of the Chinese economy and the Hong Kong economy. Before we go there, there’s been a number of very high-profile U.S.-listed Chinese companies that have basically lost most of their value because of fraud being discovered. What are the implications of that? Is this the beginnings of some kind of a trend?

Mr. Bass: I think it catches people by surprise. If we were to poll the population of the United States and say, “do you think Chinese companies that are listed on the US stock exchanges are subject to the same audits that US companies are?” They would probably say, “yes.” Well, that’s just not the case. They aren’t subject to the same Dodd Frank compliance features as US companies are. We gave China a pass, right? The whole Nixon-Kissinger view of China was to open up to this totalitarian, dictatorial regime, and let’s give them a taste of Western capitalism. Let’s bring wealth into their country in dollar terms, and what that should make them do, is open up and become more democratized, and also ideologically, maybe become more of a responsible “global actor.”

For anyone that’s questioned whether that’s worked out well or not, I think you see that they have gone the other way.

If you listen to Xi Jinping’s speech in the 19th Party Congress, his entire plan was to build a socialist system. They call it socialism with Chinese characteristics or Marxist, Leninist socialism. They want to build a socialist system to basically show the world that that system is better than Western capitalism. He said that in the 19th Party Congress. He is not trying to converge with the West, he’s trying to teach the West a lesson after their hundred years of being humiliated. Post Opium Wars and Hong Kong and Great Britain, one of those wars. I think it’s important to know that they don’t have any intention to westernize and converge. This is not a race for power. This is a simple ideological difference between two completely different cultures and governmental styles. I actually think it’s intractable. I think this relationship is impossible to solve.

So when we get into the financial aspects of this, this is where the Chinese propaganda machine has been so effective. A lot of people don’t know that every single joint venture with a US or European financial firm in China, the chief Asian economist of that JB has to be a member of the Chinese Communist Party. So when you think about the fact that Goldman Sachs Asia chief economist must be a member of the Chinese Communist Party, and Barclays Bank Asia, … or even the Chinese investment banks. Everything that gets written about the Chinese financial system is through the lenses of the perpetrator, right through the lenses of the propagandists that want to convey a message to the rest of the world. We all just …give them the benefit of the doubt. We say, ‘well yeah, they have a $13 trillion economy, and that is 15% of global GDP.” They are the second largest economy in the world, and if you purchasing power parity, many of the economists say, well, “China’s already wealthier the United States.” That is such complete crazy talk, but we just give them that benefit of the doubt of the US dollar exchange rate, which they manipulate on a nightly basis and a daily basis. They prop up their currency every single night in the foreign exchange markets, and their capital account is closed. Less than 1% of global transactions settle in their own currency. This is a house of cards.

If they were to open their capital account, how many wealthy Chinese people do you know, that can’t wait to buy more real estate in China and send their kids to school in China? They all want to send their kids to the west to learn from real schools, and they want to buy property that can’t be taken away from them because we have a rule of law. So their capital account would collapse them, if they opened it up. Their currency would drop 50%-60%. And then think about what their GDP would be. It wouldn’t be 13 trillion, it would be seven or six. Right? And so it’s important to know that again, we give them the benefit of the doubt of having this monstrous economy. It’s big, alright. And they’re influential to a certain extent, but it’s nowhere near as big as they say. Again, they must have dollars to make it work.

Mr. Jekielek: To your point with these Chinese Communist Party members being the top economists for the Asian operation of all these banks, I think this CCP virus disaster has shown how the political survival of the party is always above all other considerations, even human lives. Never mind talking about honest reporting of financial numbers.

Mr. Bass: That’s exactly right. When you look at a Marxist-Leninist socialist system, or socialism with Chinese characteristics, it’s always for the betterment of the party. They will trample human rights and basic rights of individuals in order to get to that goal and they make no mistake about that. And we know what they’re doing to the ethnic Uyghurs in northwest China and Xinjiang. We know what they did in Tibet, and we know what they’ve done to the Falun Gong and the Christians. They religiously persecute anyone that doesn’t hold President Xi, or Secretary Xi, above your God or whatever religion you want to practice. It’s actually crazy what they do. And again, we give them passes. Can you imagine if you explain to someone that you’re doing business with a regime that has more than a million prisoners of conscience locked up and is executing live organ harvesting on this population of political prisoners on a daily basis, and yet [companies] like Blackstone can’t wait to invest another dollar in China. People like Sheldon Adelson can’t wait to open another casino in Macau. You know why? Because they just let money blind them to the blatant human rights abuses of maybe one of the most tyrannical regimes that has ever lived. It’s crazy.

Mr. Jekielek: Kyle, I’m thinking of something that Alan Leung, one of the perennial pro-democracy people in Hong Kong, said. He said in Hong Kong they have a saying, “if we burn, you’ll burn with us”, i.e., if Hong Kong burns, China will burn as well. You recently showed me your Q1 report for Hong Kong, and honestly, my mouth was wide open. I was kind of feeling the fear. What is the reality around Hong Kong that you can talk about economically right now?

Mr. Bass:I think Hong Kong is the crucible. Hong Kong has always tried to exist as its own sovereign entity with its own rights under British common law. Back when Deng Xiaoping was negotiating the handover with Margaret Thatcher in the late 1970s, early 1980s, that discussion of the handover of Hong Kong, back to the Chinese, which was to happen in July of 1997 was being had in secret in the early 1980s. When it got around to Hong Kong and around Southeast Asia, who had been enjoying British common law, and essentially a vacation to British existence with a real respect for autonomy and human rights and everything that Hong Kong was so good at back then, when it got around that China was going to get its grimy mitts on Hong Kong, what happened? The currency actually collapsed. So between 1980-1983, the Hong Kong currency fell 50% value versus both the dollar and the pound. That’s what precipitated the Hong Kong monetary authority to peg the currency to the dollar because there were front page articles saying Hong Kong is a banana republic, and that it will be handed back to the Communist Party, and no one knows what they’re going to do with it.

So that was a crisis that precipitated the peg. 36 years later we are today. But think about this: July 1, 1997 was the handover of Hong Kong back to the Chinese. July 2 1997, the very next day is the day the Thai Baht broke its peg and collapsed 60% That is not coincidental. If you remember the Asian financial crisis happened during the handoff in 1997-98, you had an Asian crisis where all of a sudden they borrowed a lot of dollars, and their currencies collapsed versus the dollar and it blew apart many of those countries. This was the fear of the handoff of Hong Kong back to the Chinese actually happening.

So you had a crisis that precipitated it, which was a discussion of the handoff. The handoff itself caused another crisis. And here we are today where the Sino-British act of joint declaration of 1984 was signed, whereby China agreed to leave Hong Kong in situ, autonomous until at least 2047. That was the plan 1997 to 2047. They agreed to do it for 50 years. Now in 2047, it was just going to become another city in China. But was going to be a 50-year grace period. In 2019, the Chinese government decided that they wanted to put through a very slick extradition policy whereby any crime the Chinese government alleged anyone in Hong Kong committed they could simply grab them an extradite i.e. take all their personal freedoms away in an extrajudicial environment. That is what precipitated the protests, and that bill floated through the Hong Kong Legco (Legislative Council) in February of 2019, and the protests began in earnest June 1.

So you already have a significant uprising of the Hong Kongers. You saw a massive part of their population peacefully protest in the streets of Hong Kong this last summer, and what did you see happen? You saw their economy in the third and fourth quarter of last year drop north of a 10% real rate of GDP. It was clocking at the end of the fourth quarter down more than 15% of GDP. For those of you that aren’t economists, when you’re down 10% real GDP, that is not a recession, that is a depression. They are the most levered economy in the world. Their banks are 850% of their GDP and assets, and so when you think back to the European crisis, you had Iceland, Ireland and Cyprus. Remember how those dominoes fell? They fell in order of the size of the banking system. Those banking systems were enormous and they went unchecked. And so at the very first sign of loss, it detonated the entire sovereign.

What you have happening here, is you have the worst of all situations for Hong Kong. The Hong Kong leadership, Carrie Lam is a failed leader. She is polling at a 14% approval rating. I say this in my office and laugh. I say my door knob could poll at 14%. You could easily get 14% of 100% with anything. So that’s about as low as a political leader can get. She’s finished. She’ll be replaced one day very soon. The police of Hong Kong have lost the trust of the people. The people don’t trust the police. They don’t trust the leadership. The shelves are bare. They’re in a full quarantine, and it’s a failed state. Their GDP before the Wuhan virus was dropping at an annual rate of 15%. They have the most levered banking system in the world, and they’re entering a full depression.

So what you’re going to see is this concept is crucible of “one country two systems” being a complete failure because ideologically those two systems can’t exist together. These are mutually exclusive of one another. Either you have the heavy hand and rule by law, or you have a rule of law that is respected, everyone’s autonomy and personal freedoms are respected, and so are simple property ownerships and rights. That is all going to be taken away. I don’t know if you saw this, but there is this new person I showed you when you and I talked yesterday, who was just put into place. The butcher of Tibet, Luo Huining, is who the Chinese Communist Party decided should run the relationship between the CCP, China, and Hong Kong. Luo Huining doesn’t even speak Cantonese, and he’s in charge of Hong Kong. So what do you think’s going to happen next? So Hong Kong is this fascinating crucible of these two systems that can’t coexist, finally bashing heads together. This isn’t going to magically get better [where] trust is going to be resumed, and we … go back to the Hong Kong that we knew just about a year ago. Think about January of last year, everything was fine. And look at where we are today. By the way, we haven’t seen any of the numbers since the virus lockdown. So you can’t take an economy that’s 850% levered of GDP in the banks and turn it off, which is what’s happening.

Mr. Jekielek: Kyle, I’ve been speaking with a number of friends in Hong Kong about this. People are deeply worried, including US lawmakers. There has been an outpour of support from the west for Hong Kong. But how can Hong Kong even be helped in this situation? It is a big question mark in people’s minds. What can policymakers in the West do to help this? Or is there anything?

Mr. Bass:The die is cast. The pattern is set. They took on entirely too much leverage. Two of the largest banks in Hong Kong are two British banks with essentially no British depositors and their bankruptcy remote subsidiaries in Hong Kong. I think the die is cast. You can’t lever an economy that much. You can’t have real estate values at astronomical prices, and then all of a sudden turn the economy. You know what happens next, everyone knows what happens next. It doesn’t take a genius to know that they are going to have one of the ugliest banking crises that has ever happened to any country anywhere in the world. That is going to happen this year. Even if we come back from the Wuhan virus in the next few months, Hong Kong is already finished.

So if the good people of Hong Kong have fought the good fight, for those that can leave, I think they should leave. I think that you and I both know the Chinese surveillance state is going to be reviewing all the videos of the protests, and they’re just going to summarily incarcerate people and rip their liberties away from them. Hong Kong is just going to become another failed city within China. That is what’s going to happen. And it is going to happen 27 years too early. We know the people that are going to execute it. I know that is a grim view, but I can’t see another way out of this for Hong Kong. There are 85,000 US citizens and 200,000 British citizens that live in Hong Kong. You can bet this summer that they are all going to leave.

Mr. Jekielek: It is a very difficult situation, any which way you slice it. Hong Kong is basically also the conduit through which the foreign direct investment goes into China. So now let’s sort of open up the lens here. Let’s look at the Chinese economy, and what is happening with it. And how are the indexes responding to all this?

Mr. Bass:The index providers just claim that they practice free speech, very much like the ratings agencies did in the US going into the crisis. Post global financial crisis, the ratings agencies got regulated. These index providers in the US, such as the MSCI the FTSE, all these other ones in the West, are unregulated in the US, and they are actually regulated in Europe. Maybe the US should look to Europe for regulatory oversight, because they set the gold standard. They decide where hundreds of billions of dollars get invested, and they’re basically acting as fiduciaries, but they are not taking fiduciary liability. I think these index providers should be in real trouble going forward. I just believe this money will never come back. I believe that, to your point, much of it will get stuck in China and the relationship between the US and China is only going to worsen going forward.

Mr. Jekielek: What is the reality for the Chinese economy as we speak? They are saying it is business as usual, and everyone has gone back to work. Of course, we don’t trust the numbers. We know that, but there’s certainly been some recovery that has happened. Where do things stand?

Mr. Bass: China’s two largest trading partners by far, are the US and Europe. The US and Europe are off. We are closed. We’re at home. Our unemployment rates are skyrocketing in the mid-double digits. Our businesses are shut down. Who is China selling anything to right now is all I want to know. If their economy is fine, and only down a couple percentage points and “nothing to see here.” It is complete BS. Their banking system is 350% of their GDP. They are uber-levered. The leverage in their banks against real estate in tier one and tier two cities in China is enormous. They are going to have a crisis just like we are. The difference between crisis within China versus crisis out of China is that in China, they control everything. How many times have you heard? They are just China. They do what they want.

Internally, they print more RMB than any economy prints money anywhere in the world. They control the printing press, they control the police, they control the narrative, and they control the government. So internally, they can fix things by printing a lot of their money. Again, that makes their money worth a lot less when and if it ever converts to dollars, euros, yen or pounds. I think it’s important to know that they have an enormous amount of leverage. They have a huge fiscal deficit. Their fiscal deficit was almost 14% of GDP before the crisis. They were running a small current account deficit going into the crisis. Now the world is off. The IMF says global GDP is down 3.5% instead of plus 2-3%. That is a major shift in global GDP. If we get back to work, if we reopen our economy in the next 30-45 days, our GDP will end up dropping 10% or 11%. That’s what I think, and that’s what our numbers show us. If we don’t get back to work in the next 45-60 days, our GDP is going to drop a lot more and it’s going to be a real problem. So just imagine that our banks are one times levered to our economy. And off balance sheet if you include Fannie and Freddie, it’s about 1.3 times. China is 3.5 times levered, and Hong Kong is 8.5 times levered. Just think about the negative convexity of those two situations. They have got their hands full. They have 25 spinning plates, and when one plate drops, they’re all gonna drop.

Mr. Jekielek: Tell it to me like I’m five. Why does that create a more combustible situation?

Mr. Bass: You only need to look back at Iceland, Ireland, or Cyprus where let’s say you have had a GDP, for argument’s sake, of 100 billion dollars, and you had a trillion dollars worth of bank loans in your banks. Just imagine. Your GDP is 100 billion. Let’s say you have foreign exchange reserves of 10 billion dollars, and you have a trillion dollars worth of loans in your banks where 5% of the loans go bad or 10% of the loans go bad. God forbid, 10% of your loans go bad when you enter an economic depression. You are going to lose 100 billion dollars. Just think about that. That is your entire economic output. That is 10 times your reserves you’re gonna lose. So that’s why it’s such an enormous problem when you let your banking system grow unchecked, which is what Hong Kong has done.

Mr. Jekielek: Kyle, do you expect to see any change in the investment activity of some of these larger entities like CalPERS, that uses the indices to guide their investment?

Mr. Bass:You are opening an entire new can of worms here by bringing up CalPERS. I’m sure you know, their chief investment officer is actually a member of the Chinese Communist Party. He is the deputy director of China’s currency administrator. You don’t get a top five job in China unless you are part of the party elite. He managed the entire currency reserves for the Chinese Communist Party when he worked at SAFE, and now he somehow has weaseled his way in to be the CIO of the largest pension fund in the United States and he is shoveling dollars to China. That itself needs a full-scale investigation. He has already admitted to being part of the Thousand Talents Program, which I’m sure your viewers know what that is. There are about 70,000 members of the Chinese Communist Party that are instructed to infiltrate other economies and steal all intellectual property methods, business methods, and any kind of secrets and report back to the Communist Party. In fact, they have an award every year for the best theft and they give 750,000-1,000,000 dollars and you get a plaque. Ben Meng, the CIO of CalPERS, is a part of the Thousand Talents Program and a member of the Chinese Communist Party. That begs the question to me: who is your fiduciary responsibility to? In theory, if you are a Communist Party member, there is no one higher than Xi Jinping, even whatever God you want to worship. Yet, if you are the CIO of a massive pension fund, you must have a fiduciary responsibility to the teachers of California. I’m not sure where his loyalties lie. Actually, I’m pretty sure as to where they lie, and therefore that situation itself is crazy. How does that happen in our country? I’m not sure. And we need to change these things.

Mr. Jekielek: What about the different funds like the military thrift fund? These which, presumably, don’t have the same kinds of challenges that you are describing here, but have still made these decisions based on the indices. Have you heard anything about changes of approach?