After staying on the sidelines for the entire primary, President Barack Obama will officially endorse his former VP, longtime purported friend and now finally the presumptive Democratic nominee Joe Biden in the race for president.

NEW: Former President Barack Obama will endorse his former vice president Joe Biden in a video to be released this morning, according to a source close to the former president.

The endorsement is expected to come in the form of a video to be released via social media.

Late last week in a piece entitled “Barack Obama Wins The Democratic Primary”, Politico examined Obama’s reluctance to take the spotlight during the primary, and his weariness with the Democratic Party’s “bullshit”.

Though they tried to portray Obama as taking steps to bolster Biden behind the scenes, the details provided by the reporters don’t really support this. Instead, it looks like Obama sat out the whole primary, and didn’t even start talking about a Biden endorsement until after South Carolina, when Biden effectively clinched the nomination thanks to a strong debate performance, a solid win and the implosion of the Bloomberg campaign.

But some of his aides now concede that behind the scenes Obama played a role in nudging things in Biden’s direction at the crucial moment when the Biden team was organizing former candidates to coalesce around Biden.

“I know he did a few things,” said one longtime close adviser to Obama. “He was talking to Biden regularly in that period. I don’t know exactly what he said, but you can speculate! It’s noteworthy that he called Klobuchar and the others right when they got out.”

A person with knowledge of Obama’s conversation with Buttigieg after the former Indiana mayor exited the race explained it this way:

“Obama talked to Pete the night that Pete dropped out. When Pete told Obama that he was 99.9 percent of the way there in terms of endorsing Biden, I would say that Obama was encouraging. But I would also say that Obama was very careful not to be seen as putting a thumb on the scale. He and the people close to him are very careful about the optics – the 2016-style optics. Sanders and his supporters had reason to believe the party put the thumb on the scale for Hillary in 2016 and he wanted to avoid that. Obama wasn’t the driving force, but he was encouraging of people who had those instincts to rally around Biden. But he was very cautious and discreet in how he operated.”

A Democratic strategist added, “The truth is, he’d rather be on David Geffen’s yacht than dealing with internal Democratic party bullshit.”

And as the New York Times explained yesterday, while Biden appears to have a solid lead in ‘national’ polls, a close reading of polling data shows the race for the Electoral College is much closer than it seems, with the two candidates at a virtual draw, since the swing states that will decide the election have a disproportionate number of poorer whites with no college education who represent a huge chunk of the president’s base.

That’s because Biden’s bumbling primary campaign, where he frequently looked confused or even as if he were suffering from early-onset dementia, has not been forgotten, and the only reason that Biden even made it this far is because the public bought the DNC’s “most electable” narrative, hook, line and sinker.

It’s officially “anyone but Trump” 2020 as Bernie Sanders’ diehard fans weigh whether to just sit this one out.

The Cyberspace Solarium Commission’s report was released into the teeth of the COVID-19 crisis and hasn’t attracted the press it probably deserves. But the commissioners include four sitting Congressmen who plan to push for adoption of its recommendations. And the Commission is going to be producing more material – and probably more press attention – over coming weeks. In this episode, I interview Sen. Angus King, co-chair of the Commission, and Dr. Samantha Ravich, one of the commissioners.

We focus almost exclusively on what the Commission’s recommendations mean for the private sector. The Commission has proposed a remarkably broad range of cybersecurity measures for business. The Commission recommends a new products liability regime for assemblers of final goods (including software) who don’t promptly patch vulnerabilities. It proposes two new laws requiring notice not only of personal data breaches but also of other significant cyber incidents. It calls for a federal privacy and security law – without preemption. It updates Sarbanes-Oxley to include cybersecurity principles. And lest you think the Commission is in love with liability, it also proposed tort immunities for critical infrastructure owners operating under government supervision during a crisis. The interviews cover all these proposals, plus the Commission’s recommendation of a new role for the Intelligence Community in providing support to critical US companies.

In the news, Nick Weaver and I dig deep into the Google and Apple proposals for tracking COVID-19 infections. I’ve got a separate post in the works on the topic, but the short version is that I think Google and Apple have dramatically overvalued privacy interests and downgraded the job of actually tracking infections. Nick disagrees, believing that the privacy interests aren’t actually conflicting with the tracking goals, but we agree that the app should operate on an opt-out basis, not opt-in.

Maury explains the 5G-coronavirus conspiracy that has Brits burning cellular masts. And Nick explains how to make a “smart” lock spill its secrets, and how to fall foul of the FTC.

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

.

from Latest – Reason.com https://ift.tt/34C5yrB

via IFTTT

US State Department Cables Warned Of Potential ‘SARS-Like Pandemic’ After Visiting Wuhan Lab Experimenting With Bat Coronavirus

The US State Department received two cables from US Embassy officials in 2018 warning of inadequate safety at a Wuhan, China biolab conducting ‘risky studies’ on bat coronaviruses, according to the Washington Post, which notes that the cables have “fueled discussions inside the U.S. government about whether this or another Wuhan lab was the source of the virus.”

A US delegation led by Jamison Fouss, the consul general in Wuhan, and Rick Switzer, the embassy’s counselor of environment, science, technology and health took the unusual step of repeatedly visiting the Wuhan Institute of Virology (WIV) – which had become China’s first laboratory to achieve the highest level of international bioresearch safety (BSL-4) in 2015. The last of the visits, which occurred on March 27, 2018, was documented on WIV’s website and subsequently scrubbed (archive).

US officials were so concerned by what they saw that they warned of a potential pandemic stemming from the lab’s work on bat coronaviruses.

What the U.S. officials learned during their visits concerned them so much that they dispatched two diplomatic cables categorized as Sensitive But Unclassified back to Washington. The cables warned about safety and management weaknesses at the WIV lab and proposed more attention and help. The first cable, which I obtained, also warns that the lab’s work on bat coronaviruses and their potential human transmission represented a risk of a new SARS-like pandemic. –Washington Post

“During interactions with scientists at the WIV laboratory, they noted the new lab has a serious shortage of appropriately trained technicians and investigators needed to safely operate this high-containment laboratory,” reads a January, 2018 cable drafted by two officials from the embassy’s environment, science and health sections who met with scientists from the WIV.

Interestingly, the Chinese researchers were receiving assistance from the Galveston National Laboratory at the University of Texas Medical Branch and other U.S. organizations, however the Chinese had requested additional help. Consequently, the cables warned that the US should give the WIV additional support because of how dangerous the research on bat coronaviruses was.

As the cable noted, the U.S. visitors met with Shi Zhengli, the head of the research project, who had been publishing studies related to bat coronaviruses for many years. In November 2017, just before the U.S. officials’ visit, Shi’s team had published research showing that horseshoe bats they had collected from a cave in Yunnan province were very likely from the same bat population that spawned the SARS coronavirus in 2003.

“Most importantly,” the cable warns, “the researchers also showed that various SARS-like coronaviruses can interact with ACE2, the human receptor identified for SARS-coronavirus. This finding strongly suggests that SARS-like coronaviruses from bats can be transmitted to humans to cause SARS-like diseases. From a public health perspective, this makes the continued surveillance of SARS-like coronaviruses in bats and study of the animal-human interface critical to future emerging coronavirus outbreak prediction and prevention.”

According to the report, the bat coronavirus research was aimed at preventing the next SARS-like pandemic “by anticipating how it might emerge,” however according to the report “even in 2015, other scientists questioned whether Shi’s team was taking unnecessary risks.”

In October 2014, the U.S. government had imposed a moratorium on funding of any research that makes a virus more deadly or contagious, known as “gain-of-function” experiments.

WaPo is careful to note that ‘many‘ have said there’s no evidence that COVID-19 was engineered, and that concensus is that it came from animals, “that is not the same as saying it didn’t come from a lab, which spent years testing bat coronaviruses in animals,” according to Xiao Qiang, a research scientist at UC Berkeley.

“The cable tells us that there have long been concerns about the possibility of the threat to public health that came from this lab’s research, if it was not being adequately conducted and protected,” he said.

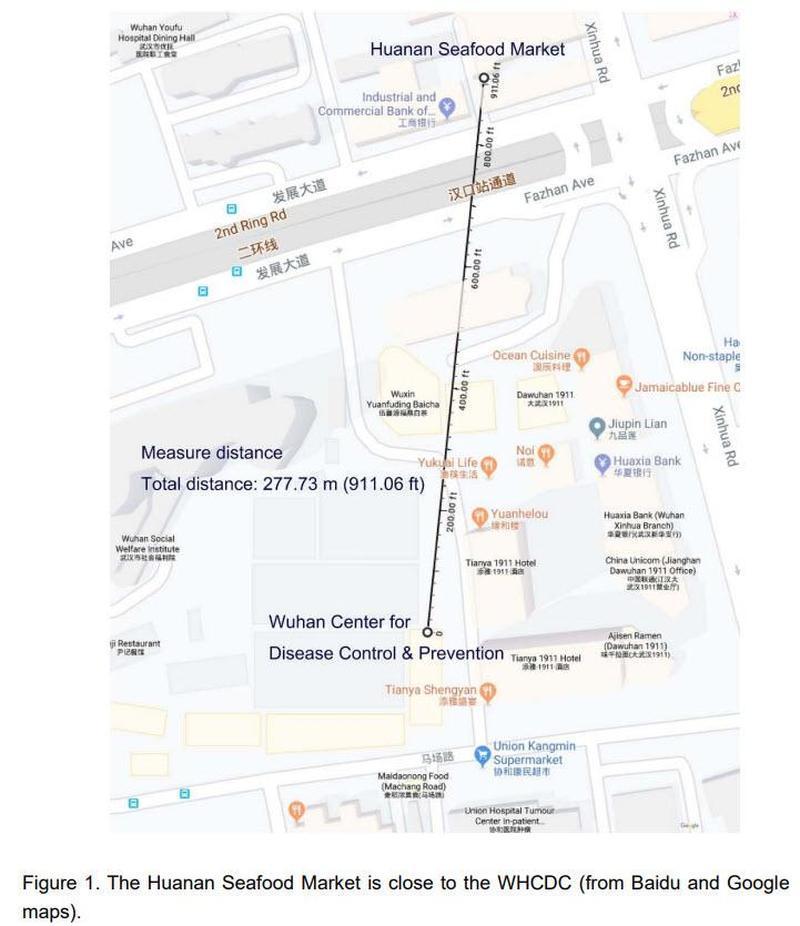

Meanwhile, similar concerns remain about the nearby Wuhan Center for Disease Control and Prevention Lab – a level 2 biosecurity facility, while the Chinese government refuses to say whether either lab was involved.

Notably, the Wuhan CDC is located roughly 900 feet from the wet market which accounted for roughly half of the new COVID-19 cases late last year.

That said, the report notes that the wet market didn’t sell bats – and the first known patient had no known connection to the market. That said, there’s nothing to say that an employee from the Chinese CDC didn’t accidentally infect themselves and go shopping for meat during the virus’s well known asymptomatic incubation period.

According to WaPo, citing sources familiar with the cables, the US embassy wanted to sound an alarm about the grave safety concerns at the WIV lab, “especially regarding its work with bat coronaviruses.”

“The cable was a warning shot,” said one US official. “They were begging people to pay attention to what was going on.”

Next, WaPo moves on to the ‘blame the Trump admin’ phase of the report, noting that “no extra assistance to the labs was provided by the US government in response to the cables” which “began to circulate again inside the administration over the past two months as officials debated whether the lab could be the origin of the pandemic and what the implications would be for the U.S. pandemic response and relations with China.”

Inside the Trump administration, many national security officials have long suspected either the WIV or the Wuhan Center for Disease Control and Prevention lab was the source of the novel coronavirus outbreak. According to the New York Times, the intelligence community has provided no evidence to confirm this. But one senior administration official told me that the cables provide one more piece of evidence to support the possibility that the pandemic is the result of a lab accident in Wuhan.

Of note, the Obama administration ‘paused’ funding to the WIV, which was lifted a year into Trump’s presidency according to the National Review.

“The idea that is was just a totally natural occurrence is circumstantial. The evidence it leaked from the lab is circumstantial. Right now, the ledger on the side of it leaking from the lab is packed with bullet points and there’s almost nothing on the other side,” said one WaPo source.

Meanwhile, the CCP has put a complete lockdown on information related to the origins of the virus – refusing to provide US experts with samples collected from the earliest cases, and quickly shutting down the Shanghai lab which published COVID-19’s genome on January 11th for “rectification.”

As WaPo notes, “Several of the doctors and journalists who reported on the spread early on have disappeared.”

On Feb. 14, Chinese President Xi Jinping called for a new biosecurity law to be accelerated. On Wednesday, CNN reported the Chinese government has placed severe restrictions requiring approval before any research institution publishes anything on the origin of the novel coronavirus.

And now – considering the source of the report, the bat’s out of the bag and the official narrative has been set – which we were called conspiracy theorists for positing three months ago.

One thing you hear a lot of is, “I’m no epidemiologist, but…”

The stock market will make new lows.

The bottom is in.

If we get a second round of infections, earnings will continue to be hurt and valuations are too high.

If we come up with a vaccine faster than we thought, the recovery could come sooner than we are expecting.

None of the above is all that convincing when making predictions about where equity prices are likely to go.

All we can go on is what we know now. Whether the policies put in place seem sensible and whether we can catch a break.

We know for a fact that global economic numbers will be horrid. We just don’t know for how long and to what lasting effect.

I’m not at all sure why there’s this fascination over arguing vehemently about the issue of this being a dead cat bounce or the resumption of the rally. The truth is, we haven’t seen this before. There have been some big, quick and tradeable moves. They counted if you caught them. And also if you didn’t. And now we move on.

Lots of markets are at interesting pivot levels. Which matter more in the moment than earning bragging rights over calling the next big one.

The S&P 500 at and around 2,800 matters. Euro Stoxx 50 anywhere between 2,900 and 3,000 is as well.

Get the little things right and the rest will be much more likely to work out as hoped.

Guessing where the next home run will come may be a coin flip at this point.

But we do know that the market has friends within the halls of the central banks. And they care about the level of asset prices. They’ve gone, or are going, pretty much all-in. Doing so doesn’t always work out and, absolutely, not necessarily in a straight line. But it’s worth factoring it into your calculus. We all know what the Fed has been up to. Thankfully, they did a masterful job keeping the financial plumbing functioning. In any case, they didn’t, and perhaps shouldn’t have, stopped there. But, I don’t for a second think they will be able and willing to “take it back” when the time is right as easily as they hope. We’ve seen this play before.

Bloomberg News ran a really eye-opening article this morning detailing the extent of the BOJ’s activities in supporting the economy. And markets. Apparently there is always room to do more. What’s a balance sheet for, if not to use it? The line, however, that stood out came in an attached table. In listing purchases of ETFs and J-REITS was the explanation, “No schedule is announced. They tend to be conducted when equities drop.”

As we wait to see how the various pivot levels play out, it’s worth paying attention to how Italian fixed income trades. BTPs sagged right from the get-go. They have tried to rally since. There was a lot of criticism in Italy over the weekend about the terms that Finance Minister Roberto Gualtieri agreed to last Thursday as part of the euro zone rescue package. And he received some harsh criticism by the populist parties. Whether this becomes a lasting political problem for the government remains to be seen. But it should be on the radar. The Europeans tend toward needing to take multiple bites at the apple. And, to be fair, their equities are up on the day.

Another thing to follow will be the dollar. Maybe it really is going down. It just is unlikely to do so as easily as many forecast. Rates are low. They are going to stay there. Who else can afford to be jacking up theirs?

Cruise Lines Say Bookings For 2021 Up 40% Despite Terrifying Series Of On-Board Outbreaks

Millions of Americans are terrified that the first pandemic in 100 years will mark a dramatic turning point in social interaction that might cause disruptive new changes in many aspects of society and the global economy. What they seem to be forgetting, in many cases, is that 50 million people died during the Spanish Flu outbreak of 1918 – marking a global disaster on a much grander scale even than COVID-19 – and, afterward, nothing really changed.

And according to thousands of armchair analysts tweeting out their views and dozens of more refined professionals sharing their outlook on CNBC, if there’s any industry that’s going to need a rethink, it’s going to be travel and leisure.

Experts have raised the possibility that nobody will go on cruises anymore, that the “one-meeting” business trip will become a thing of the past, and traveling abroad for brief vacations might also become far less common.

But as valid as they seem, there’s also reason to believe these concerns might be misplaced.

To wit: as BI notes, despite the staggering negligence of management and maddening 14-day quarantines endured by passengers – not to mention the dozens who have died and hundreds who have been sickened – reservations on American cruise lines have actually climbed for 2021.

Even with at least one major cruise line facing a criminal investigation, BI said that over the past 45 days, the cruise booking site CruiseCompete.com saw a 40% increase in its bookings for 2021 over its 2019 bookings.

For those wondering why Americans might want to go on a cruise after all of this, we have two ideas: 1) lower prices, 2) many Americans are idiots (as evidenced by the ‘Covidiots’.Those people have parents).

Shortly after the report was published, Morgan Stanley’s Mike Wilson appeared on CNBC to explain his bank’s revised outlook, and emphasized the varying “best, base, and worst”-cases. When he got to the “best” case, he noted that there’s still reason to believe that the ‘best case’ scenario might actually play out, and the massive fiscal stimulus coincides with a natural strong rebound to send the global economy into growth overdrive.

Here’s one more reason to support that thesis – and a 3,250 2020 price target.

“If you try to take a cat apart to see how it works, the first thing you will have is a non-working cat.”

On Thursday I posted a note on the Fed doing exactly what I predicted – a programme to buy high-yield junk. A sniffy Wall Street trader called me an imbecile – which is quite a big word for a Wall St trader. He told me the Fed is not buying junk bonds, just ETFs related to junk and levered finance. He yelled at me to get it right. Really..? Go figure. Same difference. Its detail. I confidently predict the Central Banks will be buying equity ETFs soon enough – which is buying equity. End of.

* * *

After a glorious 4 days Easter staycation over the best April weekend in history, do I feel refreshed enough to face another week in markets? As analysts simultaneously forecast global depression and record stock markets by year end, are we are into the realms of financial insanity? I have some seriously dark dystopian forebodings about where this could go…

Get over it… Smile.

But before we talk ourselves into giving up.. REMEMBER – things are never as bad as you fear they might be. (It doesn’t mean they are looking particularly good either.) If you are prepared for the worst, then you are less likely to be disappointed if it happens…

If you can’t make your mind up about markets, you are in good company. I have to admit I am beginning to wonder what some commentators are smoking – there is lot of hallucinogenic nonsense out there. But, the bottom line is the global economy is not dead. It is adapting. That means massive change. It means dropping current orthodoxy, and working out what is real today may well be dead and buried tomorrow, and front-running the completely new opportunities that are going to arise. It’s dangerous, but kind of exciting.

To face the future… get pragmatic.

First:

Work out why the market is fooling itself. Markets are scared of change, with a default position things will revert to “as-they-were.” This time they will not. There are a number of dangerous narratives playing out in markets at present – all of which expect things to revert to “same-as”.

1) C-19 is going to go away because of “curve flattening”, and we will have a vaccine in a few months time. No. We mighthave a vaccine in a year or so, and Might is not a winning market strategy. C-19 might not go away any time soon.

2) This is not a real war. No means of production like factories, ships, infrastructure have been destroyed. Everyone can start working again when the all clear sounds. No. As the old adage goes – 40% of American’s are one pay-check away from bankruptcy. A recent survey says nearly 40% have seen family members lose jobs, and 30% of Americans think their jobs are at risk.

3) Global trade will swiftly fill any supply gaps.No. Protectionism is going to play front and centre as countries seek to ensure they are not caught again.

The World had changed. Adapt to it.

Second:

Let’s remind ourselves of the disturbing reality.. A few examples to think about:

Stocks have just staged their best turnaround performance in over 80 years. The Global economy is heading for a 10-15% single quarter contraction.

Investment banks are calling the bottom on stock markets, to buy credit bonds, and predicting a V-Shaped recovery. Landlords, Lenders, Companies and Individuals are being sucked into a cascading landslide of defaults, missed payments, increasing debt, fear and panic.

Central banks are pumping cash into economies through QE infinity, governments are doing everything to get cash to companies to keep them going. Some support programmes are swift and are working. Others are delayed, with failed delivery exacerbating the sense of crisis. Markets are arbing the supports.

Asset managers say strict investment ESG guidelines have never been so critical. Moral Hazard has gone out the window when it comes to bailing out protectionism, payrolls and sectors.

The Financial sectors thinks it’s fantastic – witness the Goldman Sachs syndicate head bragging of his record first quarter new issue revenues in bonds, despite lockdown. People don’t have enough cash to put food on the table for their kids.

Investment banks are telling their staff to get back into their offices. C-19 is running rife around bankers who have gone back in.

Politics is creating new heroes. Everyone loves Boris. Trump gets testy when his C-19 record is questioned. Not a problem – the Democrats look determined to lose in November.

Third

My job is to try and make sense of it. Let’s lay all the pieces of the jigsaw on the table, and try to put them together.

Massive monetary stimulus through QE Infinity, and unlimited fiscal support via the promise of sector and company bailouts and nationalising payrolls, have fuelled the market’s expectations rally. NOT BECAUSE OF A STRONGER ECONOMIC OUTLOOK OR RISING COMPANY RESULTS. Distortion and disconnect is not sustainable long-term (although its pretty much fuelled markets since 2009).

The expectation is Central Banks can’t allow a market meltdown. Follow the Fed.. you won’t lose. Financial assets – bonds and stocks are rising. If you fear inflation, stocks and bonds are where to look for it.

There is no escape for Central Banks and Governments from the consequences of their actions – they can’t pull fiscal spending without crushing the economy, and they can’t pull back monetary market support for fear of crushing confidence. They have “crossed the diamond with the pearl” to create the ultimate market drug high, and markets can’t face cold-turkey. The merest hint of a taper tantrum today – and we’re talking massive market reset. Negative rates look inevitable.

A massive deflationary demand shock is under way as incomes crash, insecurity and uncertainty wipes out whole sectors, and governments predict massive GDP damage.

This week we will get a barrage of new doom-laden forecasts from the virtual Washington IMF/World Bank meetings. Plus, it’s the start of the US earnings season – so we get first look at Q1 business damage. They may shock markets, but we really need to know how companies plan to cope.

Investment firms are in serious trouble as dividends plummet. Asset managers need returns to pay investors. There are zero returns across financial assets. The only way to generate returns is to go yield hunting – meaning investors will take increased risk, piling into riskier assets like Emerging Markets. It’s another accident-waiting-to-happen the authorities can’t let happen. Expect further financial asset bailouts.

Where will all the cash go? Companies borrowing unlimited amounts of rescue money through governments are unlikely to rationalise making any serious investments into deflationary economies with 20% plus unemployment. Their response is more likely to be defensive, retrenchment via cost and job-cutting while determining what the future looks like. Depression will fuel depression.

Demand for get rich quick speculative fantastical stories – like Bitcoin, We Work and other implausibles – will push prices higher. Note how Tesla has bounced 40% plus off its recent lows despite the fact no one is buying cars. I’m pretty sure I’ll be writing about Softbank’s collapse in coming days/weeks/months.

Helicopter money support direct to consumers may alleviate immediate poverty by giving the masses a couple of day’s fish, but for those still with income and the knowledge to fish, it will magnify income inequality.

I’ve seen some investment banks predicting a 35% Q2 global GDP crash. Other analysts are looking at 2022 before we see global production recover. Sage old hedge fund managers are telling us it’s the “worst I’ve ever seen..”

What does the jigsaw show us? Ongoing uncertainty and insecurity, meaningless financial asset markets reflecting monetary and fiscal distortion rather than economic reality, low growth (if any), declining investment, soaring unemployment, rising social discontent.

Fourth:

What are the opportunities?

I suspect…. A massive refocus on what is real in the real economy. Make the assumption the global economy is going to recover and change to reflect the impact of C-19 Event. Working patterns will change. Microsoft is a good example – its cloud business is going through the roof. Office property? Not so hot. Global travel will return, but could take years. Go figure out what the future looks like. Fundamentals…

Who wants to own high risk financial assets in search of a few basis points in yield? Better returns will be made from owning real assets in the real economy. That is what Warren Buffet and others are waiting for – the opportunity to buy real companies and assets.. not overpriced stocks. Until the distortion of financial assets is undone – which looks pretty much impossible… I’d rather own real things…

Recovery is going to follow – Commodities could be a starting point. At the moment everyone is looking at depressed Oil prices, saying global demand has plummeted, despite China’s stronger than expected production numbers. At some point, sooner than expected, we will see commodity demand rise sharply.

I cycled round Southampton Docks on Saturday. There were five massive cruise liners laid up, empty. They cost about $750mm, and guzzle around $10mm a month to run in terms of debt service, crews, fuel, and the rest. How long can cruise companies haemorrhage money? Well… I read that cruise bookings for 2021 are actually up. Yep.. people still want to go to see the world from a luxury hotel room.

Or… we could figure out how to reset the global economy. More than a few folk are proposing a debt jubilee – but that would have enormous consequences.

Let’s finish on a fairy-tale…

The publican was worried – the bar was empty. No one was making any money and could afford to drink. Next day a German tourist walks into the bar. He says he needs a room for the night. The publican shows him both available rooms. The German says he will need to ask his wife. He gives the publican 100 Euros to hold the rooms. The publican immediately runs across to the grocers and pays off his 100 Euro tab. The grocer nips across to the butchers to pay the 100 Euros he owes for last week’s meat order. The butcher runs across to the undertaker to pay off the Euro 100 cost of his father’s recent funeral. The undertaker rushes off to the village Madam to pay for services rendered. She runs across to the pub, and pays the publican 100 Euros for the rooms she’d rented. The German returns with his wife, who doesn’t like either room, and the publican gives the German his 100 Euros back. The bar is full that evening…

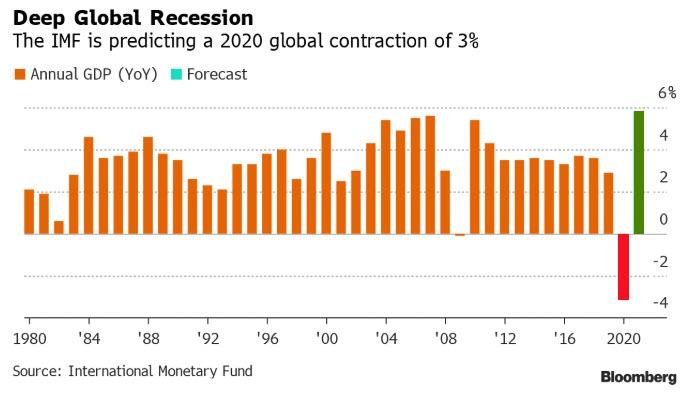

Oil Tumbles After IMF Slashes Global Growth Forecast

As if oil prices needed any more help on their downward spiral towards the teens, The IMF just slashed global growth to the worst since the ’30s.

“This crisis is like no other,” Gita Gopinath, the IMF’s chief economist, wrote in a foreword to its semi-annual report.

“Like in a war or a political crisis, there is continued severe uncertainty about the duration and intensity of the shock.”

As Bloomberg notes, The International Monetary Fund predicted the “Great Lockdown” recession would be the steepest in almost a century and warned the world economy’s contraction and recovery would be worse than anticipated if the coronavirus lingers or returns.

In its first World Economic Outlook report since the spread of the coronavirus and subsequent freezing of major economies, the IMF estimated on Tuesday that global gross domestic product will shrink 3% this year.

That compares to a January projection of 3.3% expansion and would likely mark the deepest dive since the Great Depression. It would also dwarf the 0.1% contraction of 2009 amid the financial crisis.

Of course, there is the hockey-stick recovery with IMF anticipating growth of 5.8% next year, which would be the strongest in records dating back to 1980, it cautioned risks lay to the downside.

The grim projections are a stark reversal from the IMF’s outlook less than two months ago (on Feb. 19, the fund told Group of 20 finance chiefs that “global growth appears to be bottoming out.”)… and now…

“Many countries face a multi-layered crisis comprising a health shock, domestic economic disruptions, plummeting external demand, capital-flow reversals and a collapse in commodity prices,” the IMF said.

“Risks of a worse outcome predominate.”

And the impact on the most economically-sensitive commodity is clear…

The IMF’s baseline scenario assumes that the pandemic fades in the second half of this year and that containment measures can be gradually wound down.

We suspect that is optimistic and that we’re gonna need more production cuts and more bailouts!

US Import, Export Prices Plummet In March As COVID Deflationary Drag Strikes

In what is perhaps not totally surprising, the deflationary winds of a global lockdown washed ashore in the US with a collapse in both US import and export prices (though both were modestly better than expected).

Import Prices fell 2.3% MoM (better than the -3.2% exp) and year-over-year plunged 4.1% (again better than 5.0% drop expected)

Export Prices fell 1.9% MoM (better than the -2.3% exp) and year-over-year tumbled 3.6%.

Source: Bloomberg

These are the biggest deflationary impulses since June 2016.

China’s deflationary export was not as significant as Canada and Asia Near-East…

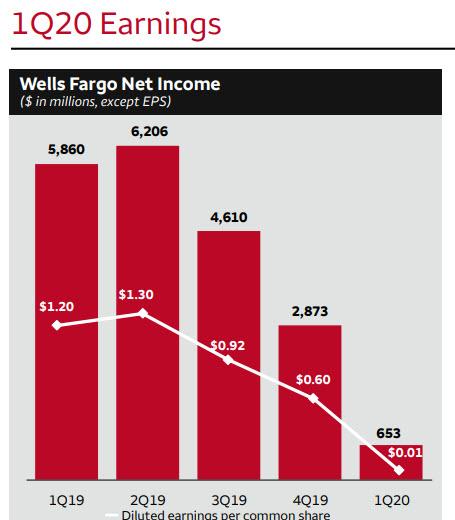

Wells Fargo Reports 1 Cent Profit After Loan Loss Provision Soars To $4 Billion

With JPM starting Q1 earnings season by taking a whopping $6.8 billion in covid-19 loan loss reserves in Q1, it appears that the bank is bracing for even more pain in Q2, even if the number was enough to allow JPM to report a profit in Q1 (albeit down some 69%, or the most since the financial crisis) instead of an outright loss. Moments after JPM, Wells Fargo followed suit, when it reported a surge in credit costs in the first quarter, setting aside $4 billion in loan-loss provisions in the first quarter, almost five times what it allocated a year ago and the most in a decade. Amusingly, despite this surge in provisions, Wells too reported an EPS profit, but the smallest possible of just 1 cent (!), down from $1.20 a year ago.

Net income dropped 89% to $653MM from $5.860BN a year ago, as a result of the following provisions:

$4.0 billion of provision expense for credit losses

$2.9 billion reserve build for loans

$909 million of net charge-offs for loans

$172 million of provision expense for debt securities, including $141 million reserve build (1) and $31 million in net charge-offs

$950 million of securities impairment

$621 million of net losses on equity securities from deferred compensation plan investment results, which were largely offset by a $598 million decline in employee benefits expense

$464 million of operating losses

$463 million gain on the sale of residential mortgage loans, reclassified to held for sale in 2019

$379 million of mortgage banking income vs. $783 million in 4Q19 on higher losses on loans held for sale, and higher

As Bloomberg points out, provisions for credit losses were $1.7 billion in community banking alone, which pretty much wiped out the division’s profit, down 95% from a year ago. Net interest income in the segment were little changed despite falling interest rates.

Net loan charge-offs were $909 million in the quarter, up about 18%. Reserve build was $3.1 billion, which was four times a year ago. CECL accounting is forcing banks to build up reserves faster on expectations of loans going bad. Thus even though charge-offs are slower to rise, reserves have to be built up front when the economy is doing bad.

“Wells Fargo plays an important role in the financial system and the economic strength of our country, and we take our responsibility seriously, particularly in these unprecedented times,” Scharf said in a statement Tuesday.

The San Francisco-based lender, and Warren Buffett’s favorite bank, has been constrained by a Federal Reserve order limiting bank assets to their end-of-2017 level following a series of scandals at the bank, though it was granted a temporary break last week to expand lending to small businesses. Total assets were just above that level at the end of the first quarter. Scharf said last week that Wells Fargo extended almost $70 billion in new and increased commitments and outstanding loans in March alone.

The bank was quick to assure the Fed that both its Tier 1 Ratio and its LCR Ratios were well above the regulatory minimum.

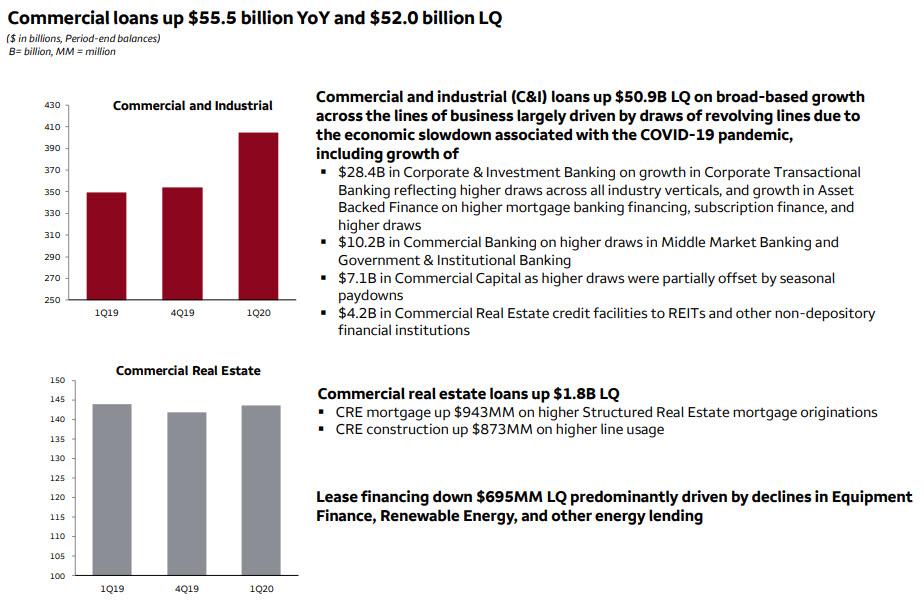

CFO John Shrewsberry outlined activities during the first quarter: “Commercial loans grew by $52 billion, deposits increased by $54 billion, we originated $48 billion of residential mortgage loans, and we raised $47 billion of debt capital for our clients.”

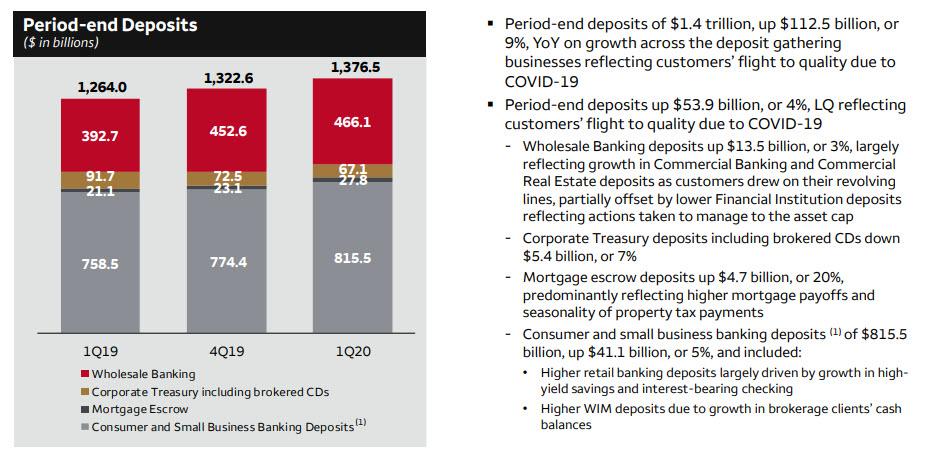

As expected, cash flooded the bank in this uncertain time, with period end deposits up $112.5BN to $1.4 trillion. Deposits have been flowing in to banks as lower interest rates and declining markets typically shift funds from money market funds and securities investments.

Commercial and industrial loans jumped $50.9 billion, largely as clients drew on their revolving credit lines because of the pandemic.

That said, consumer loans were down $4.4 billion from the previous quarter due to declines in credit card and mortgages.

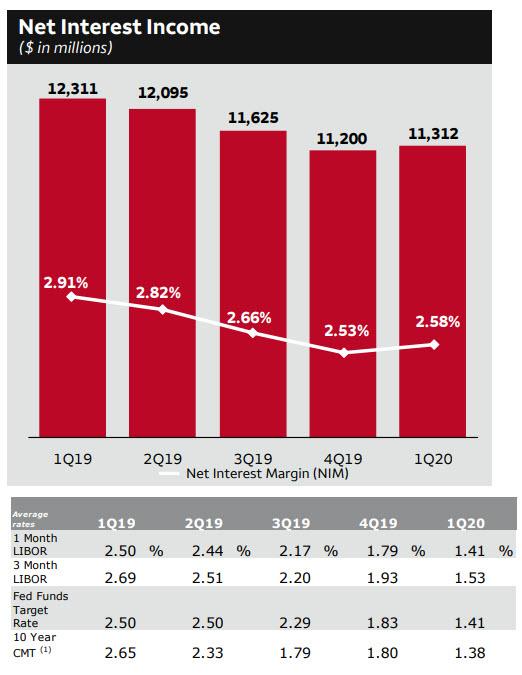

And something unexpected: despite the plunge in rates to all time lows, in Q1, Wells reported that its Net Interest Income actually rose to $11.3BN, from $11.2BN, a NIM of 2.58%, up from 2.53% in Q4, although there was less here than meets the eye, and the rebound was largely driven by subsequent adjustments, to wit:

$356 million higher hedge ineffectiveness accounting results reflecting large interest rate changes in the quarter

$84 million lower MBS premium amortization resulting from lower prepays

Partially offset by balance sheet repricing, including the impact of the lower interest rate environment, and one fewer day in the quarter.

Meanwhile, the NIM of 2.58% which was up 5 bps LQ and included:

~8 bps from hedge ineffectiveness accounting results

~2 bps from MBS premium amortization

~(5) bps from balance sheet mix and repricing

In other words, without the adjustments, NIM would have been flat Q/Q.

Curiously, interest Income rose even as average earning assets declined by $1.2 billion LQ:

Debt securities down $7.0 billion

Mortgage loans held for sale down $3.6 billion

Short-term investments / fed funds sold down $1.6 billion

Equity securities down $746 million

Loans up $8.5 billion

Noninterest income was uglier, dropping 31% Y/Y to $6.4BN from $9.3BN a year ago.

Finally, on staffing, Scharf says the company has enabled about 180,000 employees to work remotely, and with approximately 260,000 employees at year-end, which means about 69% if its staff are able to work remotely.