Democrats and Republicans weren’t the only voters to experience the pains and pleasures of Super Tuesday—third parties, which in 2016 had their best presidential showing in two decades, were also on the ballot in a handful of states.

Libertarian Party primaries and caucuses are nonbinding, which means that no delegates are awarded based on results. As ever, candidates for the nomination of the country’s third-largest party need to persuade a simple majority of the state L.P. delegates who attend the May 21-25 national convention in Austin, Texas. Still, the election results provide a snapshot of what party members are thinking less than three months out.

So far, the trend line is unmistakable—the Libertarian front-runner at this point is longtime libertarian-movement hand and Future of Freedom Foundation founder Jacob Hornberger. After previously winning the Iowa and Minnesota caucuses, and getting the second-most first-place votes in the New Hampshire primary as a write-in, Hornberger was the biggest human vote-getter in all three of the Super Tuesday primaries that have posted results so far.

In California, with 99.9 percent of precincts reporting, Hornberger led a field of 13 candidates with 17.5 percent of the vote. Tied for second with 11.6 percent were former military officer and Honolulu County Neighborhood Board member Ken Armstrong, and political satirist Vermin Supreme, the latter of whom previously won the New Hampshire primary. Lagging just behind at 11.4 percent was 1996 L.P. vice presidential nominee and academic Jo Jorgensen.

In Massachusetts, with 100 percent reporting (though the results are still unofficial), Hornberger was the leading vote-getting candidate with 12.6 percent, though he trailed that perennial L.P. favorite “None of the Above” (NOTA), which clocked in at 20 percent. Educator and controversialistArvin Vohra was next at 6.3 percent, followed by a 5.9 percent tie between Vermin Supreme and Dan “Taxation Is Theft” Behrman. Write-ins, which have not yet been broken down, amounted to a combined 26.3 percent.

And in North Carolina, as Elizabeth Nolan Brown reported this morning, Hornberger again paced the biped field with 8.7 percent, though NOTA stomped with 29.8 percent. (NOTA wasn’t on the ballot in California.) Just behind Hornberger with 8.2 percent was antivirus pioneer and international man of mysteryJohn McAfee, who promptly dropped out, threw his support behind Vermin Supreme, and announced his candidacy for vice president:

I regret That I am ending my campaign for President.

I am instead Attempting to run For the Vice Presidential slot.

Not on any of the three Super Tuesday Libertarian ballots were recent entrants Lincoln Chafee (the former U.S. senator and Rhode Island governor, who finished second in the Iowa L.P. caucus and tied for fourth in Minnesota); entrepreneur/ex-convict Mark Whitney (11th and fourth, respectively, in same), and former million-vote-getting Georgia gubernatorial candidate John Monds (15th and fourth).

Meanwhile, the leading fundraiser in the race, activist and veteran Adam Kokesh, finished sixth in California with 7.9 percent, tied for eighth in Massachusetts with 4.4 percent, and ninth in North Carolina with 3.5 percent.

With the Democratic nomination seesawing back into Joe Biden territory, dimming the prospects of a populist/nationalist vs. populist/socialist election, the allure for potential latecomers into the Libertarian race will surely lessen. This could well be the final field in the contest to be the third candidate on the ballot in all 50 states. Much can and will change between now and late May but, for the moment, Jacob Hornberger is your Libertarian front-runner.

from Latest – Reason.com https://ift.tt/2VJRBp2

via IFTTT

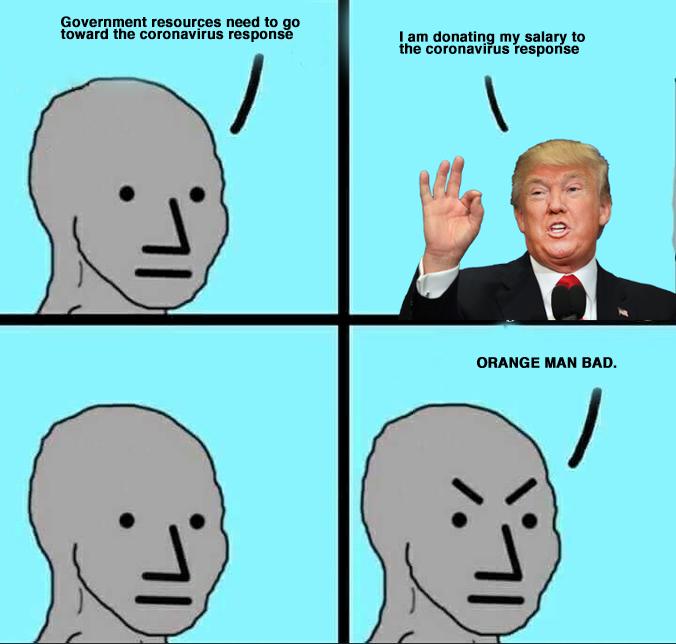

President Trump donated his fourth quarter salary to the Department of Health and Human Services this week in an effort to help fight the Coronavirus, but leftists are angry about it because… Orange man bad.

The donation of $100,000 is part of Trump’s promise to never take any salary while he is President. He has previously given away his salary to the Surgeon General’s office, border enforcement, and Veterans’ Affairs, to name but a few.

President @realDonaldTrump made a commitment to donate his salary while in office. Honoring that promise and to further protect the American people, he is donating his 2019 Q4 salary to @HHSGov to support the efforts being undertaken to confront, contain, and combat #Coronavirus. pic.twitter.com/R6KUQmBRl1

The move was nowhere near good enough for leftists though, who immediately compared the move to Hitler (an obvious starting point):

Hitler never took a salary. Now show his tax returns and document the millions he’s rinsed the tax payer for in terms of staying at his own properties, golf carts, and security for Eric.

This one called it a ‘drop in the bucket’ and got angry about Trump owning property:

REMINDER: Trump’s salary is a drop in the bucket compared to the money businesses, politicians, and foreign governments are funneling into properties he still owns and profits from while in office https://t.co/xhm32mkB6O

Who’d have thought Trump could do something before announcing it?

And this one repeated a fake narrative spread by Democrats that Trump defunded pandemic response:

This will really make up for the global pandemic Obama programs Trump dismantled, his defunding of pandemic response, bungled test kits, and golf outings that have cost more than 334 years of presidential salaries. https://t.co/Z3D1G3KY4A

In reality, Trump is pushing pharmaceutical companies to accelerate a vaccine for the coronavirus, and working closely with the CDC to contain the outbreak.

In addition, Trump presided over enhanced border controls and blocking flights from infected areas weeks ago, while Democrats did nothing:

So, the Coronavirus, which started in China and spread to various countries throughout the world, but very slowly in the U.S. because President Trump closed our border, and ended flights, VERY EARLY, is now being blamed, by the Do Nothing Democrats, to be the fault of “Trump”.

The Do Nothing Democrats were busy wasting time on the Immigration Hoax, & anything else they could do to make the Republican Party look bad, while I was busy calling early BORDER & FLIGHT closings, putting us way ahead in our battle with Coronavirus. Dems called it VERY wrong!

Travel Sector Collapses Into “Great Crisis” Amid Slump In Flight Bookings

Airlines have canceled more than 200,000 flights as Covid-19 nears pandemic status. Retail outlets at airports across the world have reported a significant drop in foot traffic, resulting in a collapse in sales at duty-free shops.

The Wall Street Journal notes a plunge in global travelers, particularly ones from China, has led to a steep decline of internationalist tourists at major airports. The result, so far, has been devastating, said the Moodie Davitt Report, a travel retail-intelligence service provider, who warned the airport retail industry at major Asian hubs had plunged 60-70% since the virus outbreak began.

“This is the greatest crisis the travel retail sector has faced, worse than [severe acute respiratory syndrome], the two Gulf wars or various financial crises,” the report said. “That’s largely driven by the fact that the Chinese traveler has become the epicenter of the sector over recent years and many retailers are worryingly reliant on them.”

Airports in Singapore and Thailand began to offer rent relief in February to retail outlets for the next 6-12 months. Officials at Hong Kong’s airport provided $205 million in assistance for industries directly or indirectly affected by declining air travel.

Geolocation data firm Advan Research said Los Angeles International Airport foot traffic declined 20% YoY in February, a similar decline of 15% YoY was seen in San Francisco’s airport over the same month.

New York’s John F. Kennedy International Airport’s Terminal 1 retail outlets have recorded a halving of sales in the last month, mostly because flights from the terminal are destined for Asia, and the US government has placed flight restrictions to China.

“Now we’re making $1,000 to $2,000 a day, compared to $4,000 on regular days and $8,000 on exceptionally good days,” said one airport retail operator at JFK.

Unibail-Rodamco-Westfield, a retail operator with stores at Los Angeles, Chicago, and New York airports, told The Journal that lower foot traffic has been visible since the virus outbreak.

“Unless the crisis persists beyond six months, I think many tenants will stay put and wait this out,” said Manny Steiner, founder of real-estate consulting firm Steiner Placemaking Advisory.

Twitter users are reporting airports across the world are “empty:”

Meeting family member at Beijing airport. Intl arrivals empty. Am told inspectors in hazmat suits taking passengers off the plane two at a time, they’ve been parked at the arrival gate for an hour now. They are serious about not letting virus take hold in Beijing. pic.twitter.com/jQaA8JCUfB

Yesterday, we flew out of one of the busiest airports in the world. Basically empty. Our flight was delayed two hours because they needed to disinfect it before we could board. In Seattle, we went through temp checks, paperwork for the CDC, questions, and given packets to read pic.twitter.com/O0ez8tQTwh

Democrats and Republicans weren’t the only voters to experience the pains and pleasures of Super Tuesday—third parties, which in 2016 had their best presidential showing in two decades, were also on the ballot in a handful of states.

Libertarian Party primaries and caucuses are nonbinding, which means that no delegates are awarded based on results. As ever, candidates for the nomination of the country’s third-largest party need to persuade a simple majority of the state L.P. delegates who attend the May 21-25 national convention in Austin, Texas. Still, the election results provide a snapshot of what party members are thinking less than three months out.

So far, the trend line is unmistakable—the Libertarian front-runner at this point is longtime libertarian-movement hand and Future of Freedom Foundation founder Jacob Hornberger. After previously winning the Iowa and Minnesota caucuses, and getting the second-most first-place votes in the New Hampshire primary as a write-in, Hornberger was the biggest human vote-getter in all three of the Super Tuesday primaries that have posted results so far.

In California, with 99.9 percent of precincts reporting, Hornberger led a field of 13 candidates with 17.5 percent of the vote. Tied for second with 11.6 percent were former military officer and Honolulu County Neighborhood Board member Ken Armstrong, and political satirist Vermin Supreme, the latter of whom previously won the New Hampshire primary. Lagging just behind at 11.4 percent was 1996 L.P. vice presidential nominee and academic Jo Jorgensen.

In Massachusetts, with 100 percent reporting (though the results are still unofficial), Hornberger was the leading vote-getting candidate with 12.6 percent, though he trailed that perennial L.P. favorite “None of the Above” (NOTA), which clocked in at 20 percent. Educator and controversialistArvin Vohra was next at 6.3 percent, followed by a 5.9 percent tie between Vermin Supreme and Dan “Taxation Is Theft” Behrman. Write-ins, which have not yet been broken down, amounted to a combined 26.3 percent.

And in North Carolina, as Elizabeth Nolan Brown reported this morning, Hornberger again paced the biped field with 8.7 percent, though NOTA stomped with 29.8 percent. (NOTA wasn’t on the ballot in California.) Just behind Hornberger with 8.2 percent was antivirus pioneer and international man of mysteryJohn McAfee, who promptly dropped out, threw his support behind Vermin Supreme, and announced his candidacy for vice president:

I regret That I am ending my campaign for President.

I am instead Attempting to run For the Vice Presidential slot.

Not on any of the three Super Tuesday Libertarian ballots were recent entrants Lincoln Chafee (the former U.S. senator and Rhode Island governor, who finished second in the Iowa L.P. caucus and tied for fourth in Minnesota); entrepreneur/ex-convict Mark Whitney (11th and fourth, respectively, in same), and former million-vote-getting Georgia gubernatorial candidate John Monds (15th and fourth).

Meanwhile, the leading fundraiser in the race, activist and veteran Adam Kokesh, finished sixth in California with 7.9 percent, tied for eighth in Massachusetts with 4.4 percent, and ninth in North Carolina with 3.5 percent.

With the Democratic nomination seesawing back into Joe Biden territory, dimming the prospects of a populist/nationalist vs. populist/socialist election, the allure for potential latecomers into the Libertarian race will surely lessen. This could well be the final field in the contest to be the third candidate on the ballot in all 50 states. Much can and will change between now and late May but, for the moment, Jacob Hornberger is your Libertarian front-runner.

from Latest – Reason.com https://ift.tt/2VJRBp2

via IFTTT

While recent generations have shown them reluctant to expand far beyond their borders, in the past few months Turkey has shown interest in overseas military engagements. Forces have been active in northern Syria with an eye toward regime change, and Turkey has also committed to military involvement in Libya.

That’s given Turkey two potential enemies to worry about, and given them each a potential new ally. The Syrian government and Libya’s self-proclaimed Libyan National Army (LNA) under Gen. Khalifa Haftar have agreed to cooperation, and signed a memorandum of understanding to confront Turkish aggression.

Gen. Khalifa Haftar, via Middle East Monitor.

The LNA’s adjoining government, the eastern-based Tobruk Parliament, has confirmed it will be opening an embassy in Damascus.

This will be the first Libyan embassy in Syria since the 2012 NATO-imposed regime change in Libya.

The Syrian regime of Bashar al-Assad reopened the Libyan Embassy in Damascus on Tuesday after an 8-year hiatus and handed it over to the “government” of east Libya-based renegade commander Khalifa Haftar.

The embassy was given to Haftar’s government after the two signed a memorandum of understanding to reopen embassies, the official SANA news agency reported.

The Syrian regime has become the first to recognize Haftar’s government, which does not have international recognition.

Since the LNA is heavily backed by much of the Arab world, their newfound alignment with Syria might open up the possibility of a Syrian rapprochement with those countries, most of whom had endorsed regime change in Syria as well.

Image via Commentary Magazine

With the Syrian “rebels” all but wiped out, they may find it’s easier to return to Damascus ties by way of common interests in Libya, and a common enemy in Turkey.

Thanks to a generous grant from the Stanton Foundation, and to the video production work of Meredith Bragg and Austin Bragg at Reason.tv, I’m putting together a series of 10 short, graphical YouTube videos explaining free speech law. Our videos so far have been

As usual for our episodes, the full script is also posted right below the video on YouTube.

We’d love it if you

Watched this.

Shared this widely.

Suggested people or organizations whom we might be willing to help spread it far and wide (obviously, the more detail on the potential contacts, the better).

Gave us feedback on the style of the presentation, since we’re always willing to change the style as we learn more.

Please post your suggestions in the comments, or e-mail me at volokh at law.ucla.edu.

from Latest – Reason.com https://ift.tt/2TnF4Gk

via IFTTT

Thanks to a generous grant from the Stanton Foundation, and to the video production work of Meredith Bragg and Austin Bragg at Reason.tv, I’m putting together a series of 10 short, graphical YouTube videos explaining free speech law. Our videos so far have been

As usual for our episodes, the full script is also posted right below the video on YouTube.

We’d love it if you

Watched this.

Shared this widely.

Suggested people or organizations whom we might be willing to help spread it far and wide (obviously, the more detail on the potential contacts, the better).

Gave us feedback on the style of the presentation, since we’re always willing to change the style as we learn more.

Please post your suggestions in the comments, or e-mail me at volokh at law.ucla.edu.

from Latest – Reason.com https://ift.tt/2TnF4Gk

via IFTTT

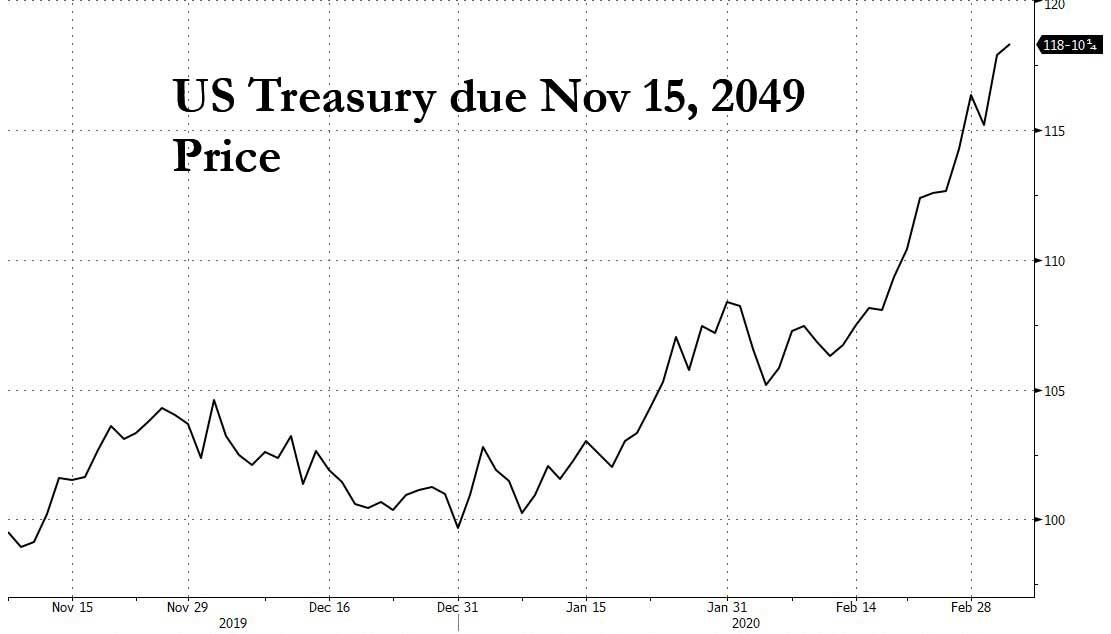

After Crushing Its Clients, JPMorgan Now Sees 50% Chance Of Zero Rates This Year

After telling its clients again, and again, and again to short US Treasurys, it’s time to call it: anyone who listened to JPMorgan has been quietly taken to one of the hundreds of portable crematoriums in Wuhan and even more quietly disposed of. Starting in January…

… continuing in early February…

… and again just last week…

… JPM went on a crusade against rates, and lost in epic fashion, with the 30Y going parabolic during JPM’s relentless shorting campaign and printing today at all time highs, which for anyone without an infinite balance sheet (such as, for example JPM thanks to its access to billions in repos after the repo market crisis JPM itself triggered) was a career-ending event.

So what does JPM do after the Fed admitted that any hopes for a mean-reversion are dead and buried, and rates are only going lower from this point on as the world sinks into the Japanification “NIRP trap”? Why it is kind enough to tell all those who listened to it and shorted bonds that its economics team now sees a 50% change that rates return to zero this year (with money markets now signaling ZIRP may be hit as soon as June).

Yet even in crushing defeat, JPM refuses to admit, well, defeat, and in a note published overnight by JPM’s economist and research teams and titled “Could US Treasury yields hit zero?“, and despite saying there is now a 90% chance of a recession, the bank – which until just a few weeks ago was praising the state of the US economy – is quick to point out that “this is not our base-case view, and our US rates team is forecasting 10-year US Treasury yields to reach 1.30% by mid-year 2020 and 1.60% by year-end.”

Oh ok. Unfortunately, with all of its rates clients now broke, it wasn’t exactly clear who, if anyone, will benefit from the bank’s “tremendous insight” and continued optimism about the future even as the entire world now sinks into an imminent virus-led recession.

The full note, for anyone who actually cares and wants to be put money that this time, finally, JPMorgan may be right, is below:

Could US Treasury yields hit zero?

A special message from Joyce Chang, Chair of Global Research As 10-year US Treasury yields reached an all-time record low of 1.09% on March 2nd, this report references J.P. Morgan’s latest global research on the risks and implications of returning to the zero lower bound. More of our research offerings can also be found on J.P. Morgan Markets.

In mid-January, we argued that low real interest rates are the preeminent macroeconomic challenge of our time as bond yields have been falling across the world for 40 years to historical lows, accelerating after the 2008 Global Financial Crisis. When we published our report posing the question, “What if US yields go to zero?”, the 10-year US Treasury yield stood at 1.80% (see J.P. Morgan Perspectives, What if US yields go to zero?, 16 January 2020). Weeks later, as fears of COVID-19 spreading to the rest of the world have intensified, 10-year US Treasury yields reached an all-time record low of 1.09% on March 2nd. Market pricing has shifted to reflect negative financial market feedback channels and sentiment effects, with many risk markets experiencing their worst drawdown in a decade over the past week. Last week, Fed Chair Jerome Powell implicitly acknowledged that current Fed policy may no longer be appropriate and a return to the zero lower bound must now be considered among the Fed’s appropriate policy responses to the outbreak. Our US economics team is forecasting that today’s emergency 50bp ease will be followed by another 25bp cut in April. We are also penciling in a 25bp rate cut from the Bank of England (BoE) at its March 26th meeting at the latest. Rates markets are pricing in an even greater “pandemic pivot” with the terminal Fed funds rate reaching ~50bp by mid-2021. Outside of the US, the market now prices two 25bp cuts from the BoE, while the Reserve Bank of Australia (RBA) has just eased by 25bp. EM central banks will remain accommodative, with at least 13 (out of 22) EM central banks easing this year. One of the recurring themes in optimal monetary policy near the zero lower bound is that when growth risks occur with policy rates within the neighborhood of zero, then the central bank should act early and aggressively. Our US economics research team sees a 50% chance that policy rates return to zero this year. To be clear, this is not our base-case view, and our US rates team is forecasting 10-year US Treasury yields to reach 1.30% by mid-year 2020 and 1.60% by year-end.

An update of our US recession probability framework based on market pricing as of today finds that rate markets are now implying that something that looks like an average US recession is at a very high 90% likelihood scenario even though we have not altered our full-year US growth forecast that dramatically. The US economy will avoid recession in 2020, but J.P. Morgan economics research now forecasts a 1Q20 stall in global GDP growth, representing the first time global growth has stalled outside of a recession. Our US economics team now expects growth of 0.5% in 1H20, followed by a rebound to 2.25% in 2H20 for a full-year forecast of 1.4% growth. However, given the rising risk of a return to the zero lower bound this year, we include a round-up of the reports published on this topic over the past few months as well as links to flagship publications, PowerPoint and video summaries.

Translation: we were catastrophically wrong about everything, so after you are done calculating your losses for listening to us and shorting the 30Y, here are all our reports on the topic which, you guessed it, were dead wrong too. You can use them for kindling in case you can’t afford to heat your house next winter.

“Imagine The Worst Case Scenario, Protect Yourself” – Ray Dalio Warns Virus Will “Annihilate” Some Markets

The coronavirus is a once-in-a-lifetime epidemic that will crush those who don’t defend for a worst-case scenario, Bridgewater co-founder Ray Dalio wrote in a Tuesday LinkedIn post.

I will repeat my overarching perspective, which is that I don’t like to take bets on things that I don’t feel I have a big edge on, I don’t like to make any one bet really big, and I’d rather seek how to neutralize myself against big unknowns than how to bet on them.

That applies to the coronavirus. Still, there’s no getting around having to figure out what this situation is likely to mean and how we should deal with it, so here are my thoughts for you to take or leave. In reading them please realize that I’m a “dumb shit” when it comes to viruses, though I do get to triangulate with some of the world’s best experts. So, for the little that they’re worth, here are my thoughts.

Three Perspectives

As I see it there are three different things going on that are related yet are very different and shouldn’t be confused:

1) the virus,

2) the economic impact of reactions to the virus, and

3) the market action.

They all will be affected by highly emotional reactions. Individually and together they lend themselves to a giant whipsaw with big mispricings, with the off chance that it will trigger the downturn that I have been worried would happen with both the big wealth/political gap and the end of the big debt cycle (when debts are high and central banks are impotent in trying to stimulate).

1) The Virus

The virus itself will almost certainly a) come and go and b) have a big emotional impact, which will most likely produce a big whipsaw.

It will most likely lead to an uncontained global health crisis that could have high human and economic costs, though how it is handled and what the consequences will be will vary a lot by location (which will also affect how their markets behave). Containing the virus (i.e., minimizing its spreading) will occur best where there are:

1) capable leaders who are able to make executive decisions well and quickly,

2) a population that follows orders,

3) a capable bureaucracy to enforce and administer the plans, and

4) a capable health system to identify and treat the virus well and quickly.

It will require the leaders to turn on “social distancing” quickly and effectively ahead of the virus accelerating and to withdraw it quickly as it declines. I believe that China will excel at this, major developed economies will be less good but OK, and those who are weaker than them in these respects will be dangerously worse.

For this reason, I am told that it’s likely that it will spread fast in these other countries and roughly in proportion to those four factors I just mentioned, and likely as a function of the weather (e.g., the hot weather in the Southern Hemisphere is thought to be an inhibitor). Because it is spreading fast to many countries and the reported cases and deaths are likely to increase rapidly, the news is likely to rapidly increase panicky reactions.

Also, in the US there will be much more testing happening over the next couple of weeks, which will dramatically increase the numbers of reported infected people, which will also probably lead to more severe reactions and greater social distancing controls. I am told that the stresses on hospitals could become very large, which will make handling the cases of all patients more difficult. In short, I am told that we should expect much more serious problems ahead.

2) The Economic Impact

Reactions to the virus (e.g., “social distancing”) will probably cause a big short-term economic decline followed by a rebound, which probably will not leave a big sustained economic impact. The fact of the matter is that history has shown that even big death tolls have been much bigger emotional affairs than sustained economic and market affairs. My look into the Spanish flu case, which I’m treating as our worst-case scenario, conveys this view; so do the other cases.

While I don’t think this will have a longer-term economic impact, I can’t say for sure that it won’t because, as you know, I believe that history has shown us that when

a) there is a large wealth/political gap and there is a battle against populists of the left and populists of the right and

b) there is an economic downturn, there are likely to be greater and more dysfunctional conflicts between the sides that undermine the effectiveness of decision making, and this is made worse when

c) there are large debts and ineffective monetary policies and

d) there are rising powers challenging the existing world powers.

The last time that happened was during the 1930s leading up to World War II, and the time before that was in the period leading up to World War I. Certainly, the wealth gap and political conflict leading to possible policy changes will be top of mind along with the coronavirus on this Super Tuesday.

3) The Market Impact

The world is now leveraged long with a lot of cash still on the sidelines—i.e., most investors are long equities and other risky assets and the amount of leveraging that has taken place to support these positions has been large because low interest rates relative to expected returns on equities and the need to leverage up low returns to make them larger have led to this. The actions taken to curtail business activities will certainly cut revenues until the virus and business activity reverse which will lead to a rebound in revenue. That should (but won’t certainly) lead to V- or U-shaped financials for most companies. However, during the drop, the market impact on leveraged companies in the most severely affected economies will probably be significant. We will show you what that looks like shortly. My guess is that the markets will probably not distinguish well between those which can and cannot withstand well the temporary shock and will focus more on their temporary hit to revenues than they should and underweight the credit impact—e.g., a company with plenty of cash and a big temporary economic hit will probably be exaggeratedly hit relative to one that is less economically hit but has a lot of short-term debt.

Additionally, it seems to me that this is one of those once in 100 years catastrophic events that annihilates those who provide insurance against it and those who don’t take insurance to protect themselves against it because they treat it as the exposed bet that they can take because it virtually never happens. These folks come in all sorts of forms, such as insurance companies who insured against the consequences that we are about to experience, those who sold deep-out-of-the-money options planning to earn the premiums and cover their exposures through dynamic hedging if and when the prices get near in the money, etc. The markets are being, and will continue to be, affected by these sorts of market players getting squeezed and forced to make market moves because of cash-flow issues rather than because of thoughtful fundamental analysis. We are seeing this in very unusual and fundamentally unwarranted market action. Also, what’s interesting is how attractive some companies with good cash yields have become, especially as many market players have been shaken out.

As far as central bank policies are concerned, interest-rate cuts and increased liquidity won’t lead to any material pickup in buying and activity from people who don’t want to go out and buy, though they can goose risky asset prices a bit at the cost of bringing rates closer to hitting ground zero. That’s true in the US. In Europe and Japan, monetary policy is virtually out of gas so it’s difficult to imagine how pure monetary policy will work. In Europe, it will be interesting to see if fiscal policy stimulations can pick up in this political environment. Also, in all countries, don’t expect much more stimulation coming from rate cuts because most of the rate cuts have already happened via the declines in bond and note yields which is what equities and most other assets are priced off of. So, it seems to me that containing the economic damage requires coordinated monetary and fiscal policy targeted more at specific cases of debt/liquidity-constrained entities rather than more blanket cuts in rates and broad increases in liquidity.

The most important assets that you need to take good care of are you and your family. As with investing, I hope that you will imagine the worst-case scenario and protect yourself against it.

“The Fed’s Shock and Awe emergency rate cut was awesome for all of 20 minutes..”

Yesterday’s 50 bp “emergency rate cut” capitulation by the Fed and the market’s subsequent down-spike tells us a lot about current sentiment. It’s not good. Following the lacklustre G7 call to discuss the crisis and more dither, the market basically concluded: “We don’t believe you can do “whatever it takes” to avoid recession and market crisis. Prove you can!”

The Feb has opened a whole can of worms, just as we face something unknown, unsettling, and completely outside the scope of markets – The Virus. For the Fed to make such a clear mis-step raises all kinds of concerns. The market is uncertain, swirling in doubt, and pondering the following questions:

Why has the Fed had caved into Trump’s demands for easing? The Fed’s credibility being questioned at such an early stage of a developing crisis won’t help.

Didn’t the Fed understand you can’t fight an exogenous supply side crisis with crude monetary easing?The sell-off demonstrated the market understands the limitations of monetary policy – pushing a heavy boulder up a hill with a wet length of wool hasn’t worked these past 12 years, why would It work now? The market will need further convincing the authorities can “do whatever it takes” – which means damaging long-term consequences and distortions to solve for short-term weakness.

Doesn’t the Fed read the headlines – and grasp the deluge of negative economic reality and remorselessly bad news requires full blooded fiscal and regulatory action?The authorities need to be acting to prevent a cascade of defaults caused by broken supply chains contaminating the whole financial system – potential causing a massive banking crisis. Rate cuts don’t do that. Fiscal measures to stall foreclosures, boost demand, and stimulate activity are required, perhaps with government stimulus through tax measures.

Why is the Fed using up its scarce policy ammunition at this point in a crisis that is still developing?With the 10 year T-bond at sub 1%, the Fed has limited scope for further cuts – what does it do next to try to placate markets? How dangerous is the policy outlook?

Does this mean the Fed Put is busted? Are we now likely to see even more manipulative measures – like a full-on QE asset purchase programme. Perhaps Trump will demand the Fed juices the equity markets? This is possible in the wake of a reinvigorated Democrat push.

And.. the killer conspiracy question:

What does the Fed know about Coronavirus that we don’t?

I suppose it didn’t help the WHO announced the mortality rate on the virus is more like 3.4% rather than the 1% typical for most categories of the flu soon after the Fed announcement. While China’s draconian containment policies seem to be working, based on slowing infection rates, most governments are planning for the worst case – Pandemic: transmission, infection and swamped hospitals.

Just read through the negative economic consequences being felt across the board. Smart money has completely written off the global cruise business. Airlines are reeling, laying off staff and cancelling flights. Chinese airlines are asking Airbus to delay deliveries. Weather satellites do suggest Chinese factories are re-opening – they can spot the NoX blooms from space! – but it will take time to ramp up supply chains, and they are vulnerable to a potential second wave of infection.

Where does the market go from here?

Some observers have pointed out the global stock markets are getting smaller as more companies go private and stock buybacks have reduced the number of shares in circulation. As 2/3 of S&P500 companies now pay dividends in excess of Treasury Yields, surely there is still upside for stocks, even if the global economy is headed for recession? The low level of bond yields apparently justifies higher P/E multiples.

Really? Surely lower yields mean a heightened risk environment, which means multiples should fall?

This is what drives yield tourism – artificially low yields forcing investors to take greater and greater risk in the search for returns. It has massive potential to end badly. Where will the pain strike?

Asset Managers were once 90% Gilt/Treasury holders have become risk takers and yield tourists. Today they are probably 30% junk and near junk bonds, 30% investment grade and 40% equity. The last 12 years has seen a massive and deliberate transfer of risk from systemically important banks, to a more diverse range of asset managers.

Banks understood risk. Their businesses were intelligence-led from their on-the-ground bankers and branches, feeding large backroom risk management teams with direct information to monitor every facet of the market. Risk now resides in fund managers, who have small Risk Management departments assessing what they read in the press. MiFid rules ensure they pay for puff put out by the investment bank research departments – many don’t bother. Asset manager risk departments may be good, but they lack the ancestral risk management DNA the banks once had.

The upside is the allocation of risk across the market has become massively more diverse. If one Asset Manager goes down because of risk management failure to exit in time, its far less damaging to the financial system in terms of contagion than a bank going down.

But what happens when the market basis suddenly shifts and the Asset Management universe suddenly tries to exit Corporate debt – doors locked, Junk bonds – doors locked, and equity markets crash. Who loses? Savers? And what happens then….

The next crisis is likely to be on the AM side – and that’s likely to create massive future liabilities for governments as pension saving disappear at a time when debt levels will be under pressure… Another sovereign debt crisis anyone? Just saying….

There is still lots of denial across the City about the Coronavirus panic.

A) If your question is: Why is the market panicking about a virus which seems marginally more dangerous than normal flu? …. you are asking the wrong question.

B) If your question is: Has the market over-estimated the economic consequences of the actions taken by the authorities to contain the virus? … you are on the right lines and looking for a buying opportunity.

C) If your question is: How much more damage can the global economy take before the G7 and central banks can’t help? … you are getting warm, and wondering about the implications if/when this turns into a major crisis…

Meanwhile – Back in the USA

Well done Mike Bloomberg – he’s won his own South Pacific stronghold in Samoa in last night’s SuperTuesday caucus! I wonder if the US dependency has got an extinct volcano he can model into a nice lair for the billionaire supervillain in waiting? 5 delegates cost Mike a lot.

The Democrat Party Core finally got its act together just in time to turn the nomination into a drag race between Joe Biden and Bernie Sanders. Biden won Texas, while Bernie stormed California. The endorsements should flow towards Biden. Will Bernie step aside and give him his support? Over the next few weeks there is a real prospect the Democrats will get their act together and make November 2020 a proper race. I expect the pressure will increasingly be on Trump. It all about the Economy Stupid!

{kind=link}

{kind=link}