Iran’s New Top Military Commander Vows To “Remove America From The Region” As Vengeance For Soleimani

Overnight we reported that the power vacuum at the top of Iran’s elite Quds Force, the military organization responsible for Tehran’s numerous proxies across the Mideast as well as Iran’s overall military strategy, was filled quickly in the aftermath of Qassem Soleimani’s killing, with the Jan 3 appointment of Esmail Ghaani, who none other than Ayatollah Ali Khamenei said was “one of the most prominent commanders” in service to Iran, and that the Quds force “will be unchanged from the time of his predecessor.”

Predictably, Ghaani wasted no time to make it clear that continuity would be preserved, saying that Tehran will avenge the assassination of Soleimani by driving the US out of the region, shortly after another Revolutionary Guard commander warned that dozens of American targets are “within our reach.”

“We promise to continue martyr Soleimani’s path with the same force… and the only compensation for us would be to remove America from the region,” Esmail Qaani said on Monday in an interview to local media ahead of the general’s funeral in Tehran.

Ghaani’s comments come just days after General Gholamali Abuhamzeh, who heads the IRGC in Iran’s southern Kerman province, said 35 US targets in the region as well as Tel Aviv were identified “long ago” and are “within our reach.”

Washington responded with a similarly-worded message, with Secretary of State Mike Pompeo threatening “lawful strikes” targeting “actual decision makers” if any American asset is in danger.

Echoing Ghaani’s warning, this morning Al Jazeera reported that an Iranian IRGC Air Force Commander said President Trump “must prepare coffins for his soldiers before” he makes threats to Iran, warning that the real revenge for Soleimani’s assassination is the removal of U.S. forces from the Middle East. It wasn’t clear just how Iran hopes to achieve that goal .

As the war of words has escalated, the Pentagon ordered 3,500 more troops from Fort Bragg’s 82nd Airborne Division to deploy to the Middle East. Meanwhile, as we reported overnight, Iraq’s parliament passed a resolution calling for the removal of foreign troops from the country.

When I moderated a debate on Espinoza v. Montana Dep’t of Revenue, I had a question for one of the Institute for Justice lawyers who represents Ms. Espinoza (and others, including Linda Greenhouse, had asked the same question as well). Here’s the issue:

A Montana school choice programs let parents use certain tax credits to pay for education at private schools, whether religious or secular.

The Montana Supreme Court held that this violates a Montana Constitution provision, which bars the government from making “any direct or indirect appropriation or payment from any public fund … for any sectarian purpose or to aid any church, school, academy, seminary, college, university, or other literary or scientific institution, controlled in whole or in part by any church, sect, or denomination.”

But rather than limiting the tax credit program to apply only to nonreligious private schools (which would have been much like what the Missouri government had done for the playground resurfacing grants in Trinity Lutheran Church v. Comer (2017)), the Montana court struck down the tax credit program altogether, as applied to secular schools as well as religious ones.

The plaintiffs argue that this decision violates the Free Exercise Clause because it is religiously discriminatory.

But, I asked, is it really religiously discriminatory, given that now all Montana private schools, religious and secular, are equally denied the tax credit?

The IJ people gave an answer there, and IJ’s David Hodges has kindly written it up for me to post:

In September, Linda Greenhouse of the New York Timesnoted something “odd” about Espinoza v. Montana Department of Revenue, a case that the Institute for Justice (IJ) will be arguing before the Supreme Court on January 22. Espinoza will determine whether the Montana Supreme Court was correct to shut down a school choice program that allowed parents to select religious schools as part of a generally available tax credit scholarship program. That court ruled that the program violated the state constitution’s prohibition on “indirect” funding of religious institutions.

What was odd to Greenhouse is IJ’s argument that a decision that prevented everyone—including the religious—from receiving a benefit could violate the religious neutrality principle of the First Amendment. After all, Greenhouse wrote, the Supreme Court in Palmer v. Thompson upheld a city’s decision to defy a swimming pool-integration order by closing the pool on the grounds that both the white and black residents of the town were equally deprived of a place to swim. The logic in Espinoza would seemingly follow: If a benefit is denied to everyone—black and white, religious and secular—then how can it discriminate against anyone? Put another way, so long as the effect is the same, how can the cause matter?

The answer lies in an Anatole France quote that the justices sometimes use to needle one another when they see a law as having an obvious pretext: “The law, in its majestic equality, forbids rich and poor alike to sleep under bridges, to beg in the streets, and to steal their bread.” For the Montana Supreme Court, the majestic equality of the law forbids both the religious and nonreligious to attend parochial school.

The underlying dynamic in Espinoza is not new to the Court. The desegregation era was replete with examples of cities justifying discrimination against African Americans by claiming the laws applied to everyone. For example, in Orleans Parish School Board v. Bush, the Court affirmed an injunction against Louisiana when it closed its public schools to avoid a desegregation mandate. In Griffin v. County School Board, the Court held that eliminating a public program to prevent the inclusion of a protected class is the same kind of unconstitutional discrimination as excluding that class in the first place. Finally, in Village of Arlington Heights v. Metro House Development Corporation, the Court explained that “[w]hen there is a proof that a discriminatory purpose has been a motivating factor in the decision…judicial deference is no longer justified.”

Given this context, Palmer is an outlier. In Palmer, the Court wrote that it was unclear whether the pool was closed for discriminatory reasons or benign ones like economic considerations. Absent more compelling evidence, the Court did not want to assume motive.

In Espinoza, by contrast, the Montana Supreme Court explicitly struck down the program because it included religious options. Simply put, if there were no religious options, the program would stand, but since there were religious options, the program had to go. Also unlike Palmer, there was no ambiguity in the record about whether the program was ended for discriminatory or budgetary reasons. (And this is without even addressing the sordid national and state history of anti-Catholic animus behind the Montana constitutional provision at issue known as the Blaine Amendment.) Finally, even if there were no “bad motives,” the text of the state constitutional provision itself clashed with the federal Constitution by disqualifying educational options because of religion—and nothing more.

In any event, both the perspective of time and subsequent caselaw have cast doubt on “neutral” laws and provisions that, as in Palmer, only seem to disadvantage one type of party. As the Court ruled in Trinity Lutheran Church of Columbia, Inc. v. Comer, a case that involved a state provision similar to that in Espinoza, excluding a party “from a public benefit for which it is otherwise qualified, solely because it is a church, is odious to our Constitution all the same, and cannot stand.”

In Espinoza, where the public benefit is for an individual, not a church, it would be an even greater constitutional injury to deny that benefit merely because it might be used at a religious school. As it was in matters of race, so too must it be in other consequential areas of constitutional law.

I’m on balance tentatively persuaded by this argument, but I’d be glad to also post a response, if someone is inclined to offer it.

from Latest – Reason.com https://ift.tt/2s2KmvY

via IFTTT

When I moderated a debate on Espinoza v. Montana Dep’t of Revenue, I had a question for one of the Institute for Justice lawyers who represents Ms. Espinoza (and others, including Linda Greenhouse, had asked the same question as well). Here’s the issue:

A Montana school choice programs let parents use certain tax credits to pay for education at private schools, whether religious or secular.

The Montana Supreme Court held that this violates a Montana Constitution provision, which bars the government from making “any direct or indirect appropriation or payment from any public fund … for any sectarian purpose or to aid any church, school, academy, seminary, college, university, or other literary or scientific institution, controlled in whole or in part by any church, sect, or denomination.”

But rather than limiting the tax credit program to apply only to nonreligious private schools (which would have been much like what the Missouri government had done for the playground resurfacing grants in Trinity Lutheran Church v. Comer (2017)), the Montana court struck down the tax credit program altogether, as applied to secular schools as well as religious ones.

The plaintiffs argue that this decision violates the Free Exercise Clause because it is religiously discriminatory.

But, I asked, is it really religiously discriminatory, given that now all Montana private schools, religious and secular, are equally denied the tax credit?

The IJ people gave an answer there, and IJ’s David Hodges has kindly written it up for me to post:

In September, Linda Greenhouse of the New York Timesnoted something “odd” about Espinoza v. Montana Department of Revenue, a case that the Institute for Justice (IJ) will be arguing before the Supreme Court on January 22. Espinoza will determine whether the Montana Supreme Court was correct to shut down a school choice program that allowed parents to select religious schools as part of a generally available tax credit scholarship program. That court ruled that the program violated the state constitution’s prohibition on “indirect” funding of religious institutions.

What was odd to Greenhouse is IJ’s argument that a decision that prevented everyone—including the religious—from receiving a benefit could violate the religious neutrality principle of the First Amendment. After all, Greenhouse wrote, the Supreme Court in Palmer v. Thompson upheld a city’s decision to defy a swimming pool-integration order by closing the pool on the grounds that both the white and black residents of the town were equally deprived of a place to swim. The logic in Espinoza would seemingly follow: If a benefit is denied to everyone—black and white, religious and secular—then how can it discriminate against anyone? Put another way, so long as the effect is the same, how can the cause matter?

The answer lies in an Anatole France quote that the justices sometimes use to needle one another when they see a law as having an obvious pretext: “The law, in its majestic equality, forbids rich and poor alike to sleep under bridges, to beg in the streets, and to steal their bread.” For the Montana Supreme Court, the majestic equality of the law forbids both the religious and nonreligious to attend parochial school.

The underlying dynamic in Espinoza is not new to the Court. The desegregation era was replete with examples of cities justifying discrimination against African Americans by claiming the laws applied to everyone. For example, in Orleans Parish School Board v. Bush, the Court affirmed an injunction against Louisiana when it closed its public schools to avoid a desegregation mandate. In Griffin v. County School Board, the Court held that eliminating a public program to prevent the inclusion of a protected class is the same kind of unconstitutional discrimination as excluding that class in the first place. Finally, in Village of Arlington Heights v. Metro House Development Corporation, the Court explained that “[w]hen there is a proof that a discriminatory purpose has been a motivating factor in the decision…judicial deference is no longer justified.”

Given this context, Palmer is an outlier. In Palmer, the Court wrote that it was unclear whether the pool was closed for discriminatory reasons or benign ones like economic considerations. Absent more compelling evidence, the Court did not want to assume motive.

In Espinoza, by contrast, the Montana Supreme Court explicitly struck down the program because it included religious options. Simply put, if there were no religious options, the program would stand, but since there were religious options, the program had to go. Also unlike Palmer, there was no ambiguity in the record about whether the program was ended for discriminatory or budgetary reasons. (And this is without even addressing the sordid national and state history of anti-Catholic animus behind the Montana constitutional provision at issue known as the Blaine Amendment.) Finally, even if there were no “bad motives,” the text of the state constitutional provision itself clashed with the federal Constitution by disqualifying educational options because of religion—and nothing more.

In any event, both the perspective of time and subsequent caselaw have cast doubt on “neutral” laws and provisions that, as in Palmer, only seem to disadvantage one type of party. As the Court ruled in Trinity Lutheran Church of Columbia, Inc. v. Comer, a case that involved a state provision similar to that in Espinoza, excluding a party “from a public benefit for which it is otherwise qualified, solely because it is a church, is odious to our Constitution all the same, and cannot stand.”

In Espinoza, where the public benefit is for an individual, not a church, it would be an even greater constitutional injury to deny that benefit merely because it might be used at a religious school. As it was in matters of race, so too must it be in other consequential areas of constitutional law.

I’m on balance tentatively persuaded by this argument, but I’d be glad to also post a response, if someone is inclined to offer it.

from Latest – Reason.com https://ift.tt/2s2KmvY

via IFTTT

David Douglas authored an essay in the ABA Journal, titled “The ethics argument for promoting equality in the profession.” He proposes a modification to ABA Model Rule 8.5.

The first portion of the rule would impose a duty on all attorneys to promote diversity and inclusion.

As a learned member of society with an ethical obligation to promote the ideal of equality for all members of society, every lawyer has a professional duty to undertake affirmative steps to remedy de facto and de jure discrimination, eliminate bias, and promote equality, diversity and inclusion in the legal profession.

The second portion of the rule is aspirational: lawyers should try to spend at least 20 hours a year to promote diversity and inclusion.

Every lawyer should aspire to devote at least 20 hours per year to efforts to eliminate bias and promote equality, diversity and inclusion in the legal profession. Examples of such efforts include but are not limited to: adopting measures to promote the identification, hiring and advancement of diverse lawyers and legal professionals; attending CLE and non-CLE programs concerning issues of discrimination, explicit and implicit bias, and diversity; and active participation in and financial support of organizations and associations dedicated to remedying bias and promoting equality, diversity and inclusion in the profession.

I have long criticized ABA Model Rule 8.4(g). It imposes an unconstitutional speech code for attorneys. In addition, Rule 8.4(g)’s comment creates a special carve-out for speech that promotes diversity and inclusion:

Lawyers may engage in conduct undertaken to promote diversity and inclusion without violating this rule by, for example, implementing initiatives aimed at recruiting, hiring, retaining and advancing diverse employees or sponsoring diverse law student organizations.

This comment creates an unconstitutional form of viewpoint discrimination. Eugene Volokh and I discussed this comment in a letter submitted to the Iowa Supreme Court:

Here, the critical language is “conduct undertaken to promote,” which in this context obviously includes speech promoting “diversity and inclusion.” Yet, this provision explicitly exempts one perspective on a set of divisive issues—affirmative action, alleged systemic prejudice, implicit bias, and the like—while continuing to potentially punish as “harassment” those who promote the opposite perspective. That disparate treatment constitutes unconstitutional viewpoint discrimination.

Consider a debate hosted by a bar association about affirmative action. One speaker promotes racial preferences as a means to advance diversity. His speech would be entirely protected under the proposed amendments. Another speaker critiques racial preferences in ways that some people view as racially “offensive.” His speech would not be protected under the proposed amendments.

The proposed ABA Model Rule 8.5 would suffer the same problem as the comment from 8.4(g). The Rule adopts a specific philosophical viewpoint–promoting diversity and inclusion–and makes it the orthodoxy for attorneys. Under this proposed rule, those who do not adopt that philosophy will be violating a “duty” and “ethical obligation.” Those who choose not to attend certain CLE classes would not be disregarding an aspirational goal.

Scott Greenfield pithily encapsulates the problem with this proposed rule:

You want to be a hero to the cause? Go for it. I’m just a lawyer trying to save lives one at a time.

Not every attorney agrees that “every lawyer has a professional duty to undertake affirmative steps to remedy de facto and de jure discrimination, eliminate bias, and promote equality, diversity and inclusion in the legal profession.” Far too many attorneys–especially academics–take this statement as an unassailable fact of life. It’s not.

Bar associations exist to promote and regulate the legal profession. They do not exist to promote specific ideologies. Indeed, they lack the power to promote ideologies. In my article, I discuss the limits on this authority:

As speech bears a weaker and weaker connection to the delivery of legal services, the bar’s justification in regulating it becomes less and less compelling. The bar lacks a sufficiently compelling interest to censor an attorney who makes a remark deemed “demeaning” at a CLE lecture, or makes a comment viewed as “derogatory” at the dinner table during a bar association gala. These are the sorts of problems that can be resolved by refusing to re-invite offending speakers—not by threatening to suspend or revoke a lawyer’s license. Here, the nexus between the bar’s mission to regulate the practice of law is far too attenuated to justify this incursion into constitutionally protected speech.

Bar associations should resist the urge to stray from their core functions. Not every lawyer wants to be a hero. Some simply want to be attorneys.

from Latest – Reason.com https://ift.tt/2s3Phgc

via IFTTT

David Douglas authored an essay in the ABA Journal, titled “The ethics argument for promoting equality in the profession.” He proposes a modification to ABA Model Rule 8.5.

The first portion of the rule would impose a duty on all attorneys to promote diversity and inclusion.

As a learned member of society with an ethical obligation to promote the ideal of equality for all members of society, every lawyer has a professional duty to undertake affirmative steps to remedy de facto and de jure discrimination, eliminate bias, and promote equality, diversity and inclusion in the legal profession.

The second portion of the rule is aspirational: lawyers should try to spend at least 20 hours a year to promote diversity and inclusion.

Every lawyer should aspire to devote at least 20 hours per year to efforts to eliminate bias and promote equality, diversity and inclusion in the legal profession. Examples of such efforts include but are not limited to: adopting measures to promote the identification, hiring and advancement of diverse lawyers and legal professionals; attending CLE and non-CLE programs concerning issues of discrimination, explicit and implicit bias, and diversity; and active participation in and financial support of organizations and associations dedicated to remedying bias and promoting equality, diversity and inclusion in the profession.

I have long criticized ABA Model Rule 8.4(g). It imposes an unconstitutional speech code for attorneys. In addition, Rule 8.4(g)’s comment creates a special carve-out for speech that promotes diversity and inclusion:

Lawyers may engage in conduct undertaken to promote diversity and inclusion without violating this rule by, for example, implementing initiatives aimed at recruiting, hiring, retaining and advancing diverse employees or sponsoring diverse law student organizations.

This comment creates an unconstitutional form of viewpoint discrimination. Eugene Volokh and I discussed this comment in a letter submitted to the Iowa Supreme Court:

Here, the critical language is “conduct undertaken to promote,” which in this context obviously includes speech promoting “diversity and inclusion.” Yet, this provision explicitly exempts one perspective on a set of divisive issues—affirmative action, alleged systemic prejudice, implicit bias, and the like—while continuing to potentially punish as “harassment” those who promote the opposite perspective. That disparate treatment constitutes unconstitutional viewpoint discrimination.

Consider a debate hosted by a bar association about affirmative action. One speaker promotes racial preferences as a means to advance diversity. His speech would be entirely protected under the proposed amendments. Another speaker critiques racial preferences in ways that some people view as racially “offensive.” His speech would not be protected under the proposed amendments.

The proposed ABA Model Rule 8.5 would suffer the same problem as the comment from 8.4(g). The Rule adopts a specific philosophical viewpoint–promoting diversity and inclusion–and makes it the orthodoxy for attorneys. Under this proposed rule, those who do not adopt that philosophy will be violating a “duty” and “ethical obligation.” Those who choose not to attend certain CLE classes would not be disregarding an aspirational goal.

Scott Greenfield pithily encapsulates the problem with this proposed rule:

You want to be a hero to the cause? Go for it. I’m just a lawyer trying to save lives one at a time.

Not every attorney agrees that “every lawyer has a professional duty to undertake affirmative steps to remedy de facto and de jure discrimination, eliminate bias, and promote equality, diversity and inclusion in the legal profession.” Far too many attorneys–especially academics–take this statement as an unassailable fact of life. It’s not.

Bar associations exist to promote and regulate the legal profession. They do not exist to promote specific ideologies. Indeed, they lack the power to promote ideologies. In my article, I discuss the limits on this authority:

As speech bears a weaker and weaker connection to the delivery of legal services, the bar’s justification in regulating it becomes less and less compelling. The bar lacks a sufficiently compelling interest to censor an attorney who makes a remark deemed “demeaning” at a CLE lecture, or makes a comment viewed as “derogatory” at the dinner table during a bar association gala. These are the sorts of problems that can be resolved by refusing to re-invite offending speakers—not by threatening to suspend or revoke a lawyer’s license. Here, the nexus between the bar’s mission to regulate the practice of law is far too attenuated to justify this incursion into constitutionally protected speech.

Bar associations should resist the urge to stray from their core functions. Not every lawyer wants to be a hero. Some simply want to be attorneys.

from Latest – Reason.com https://ift.tt/2s3Phgc

via IFTTT

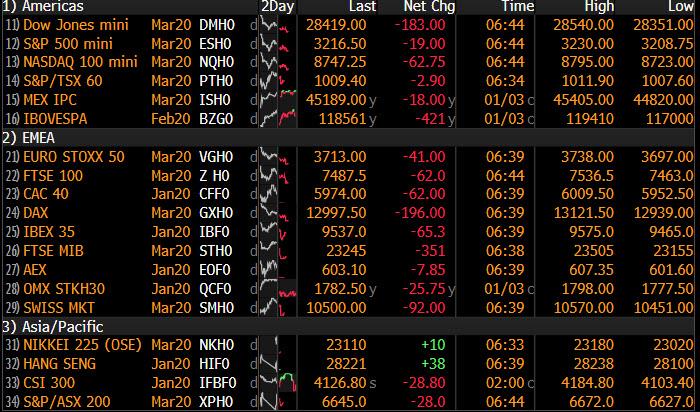

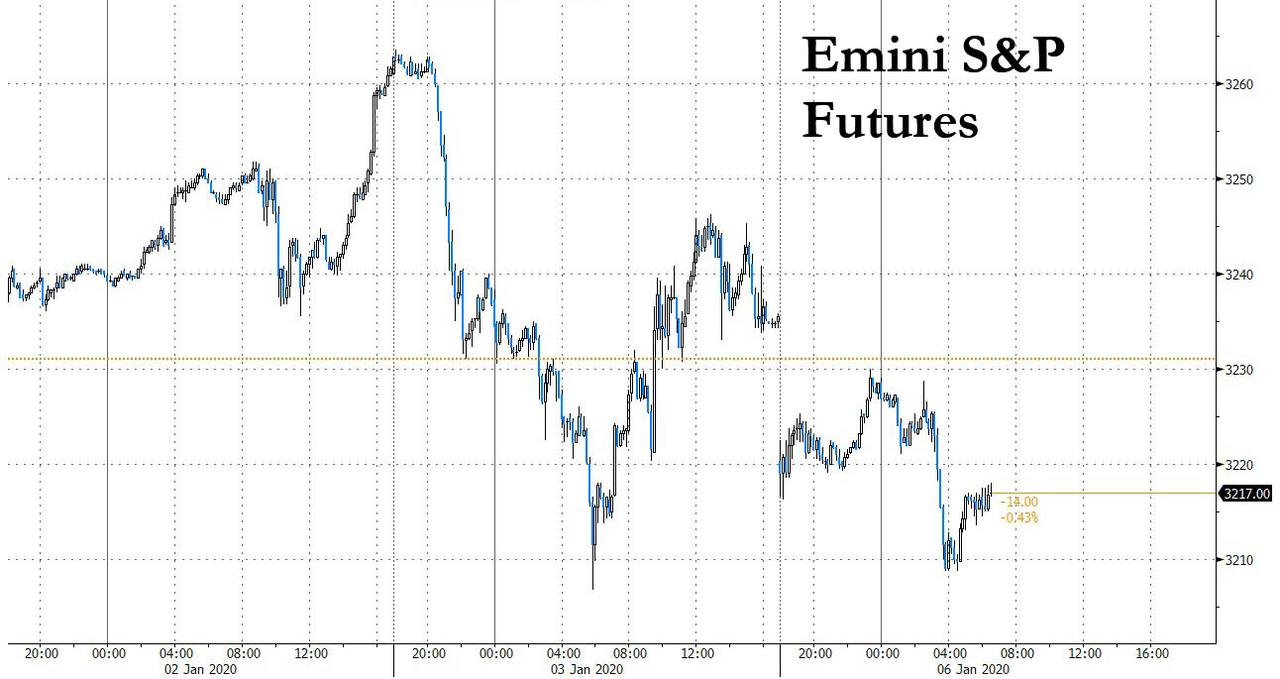

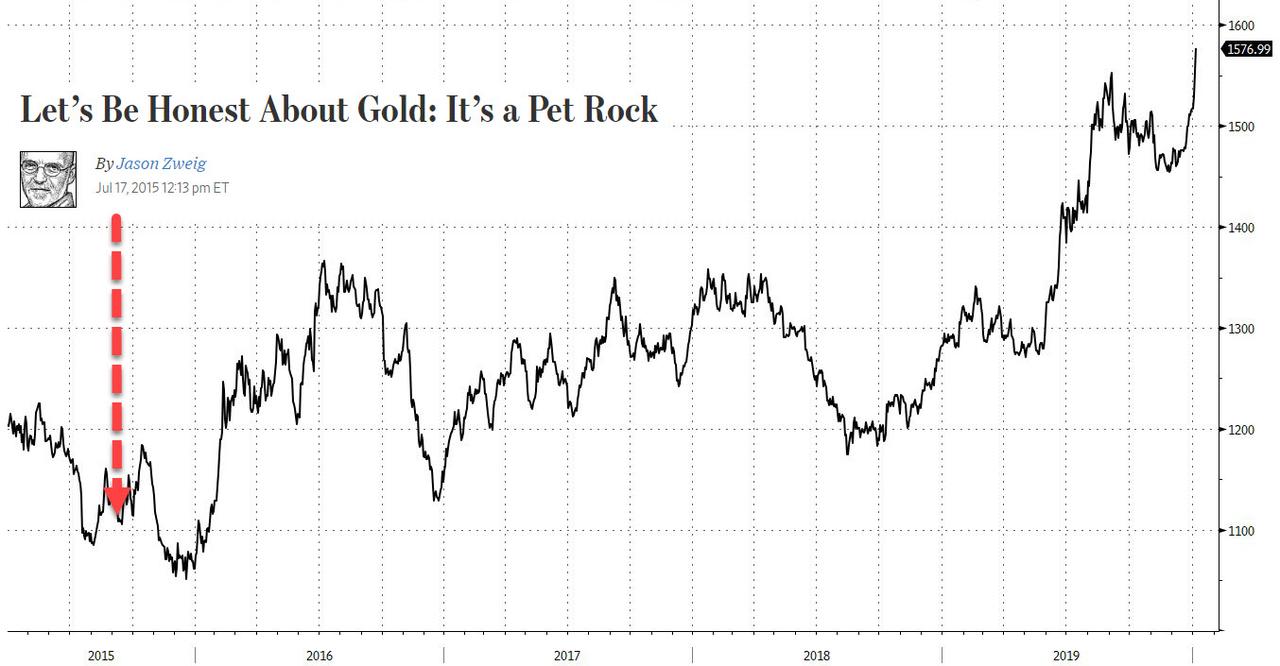

Futures Tumble, Gold Soars To 7 Year High As Iran Escalation Fears Spill Over

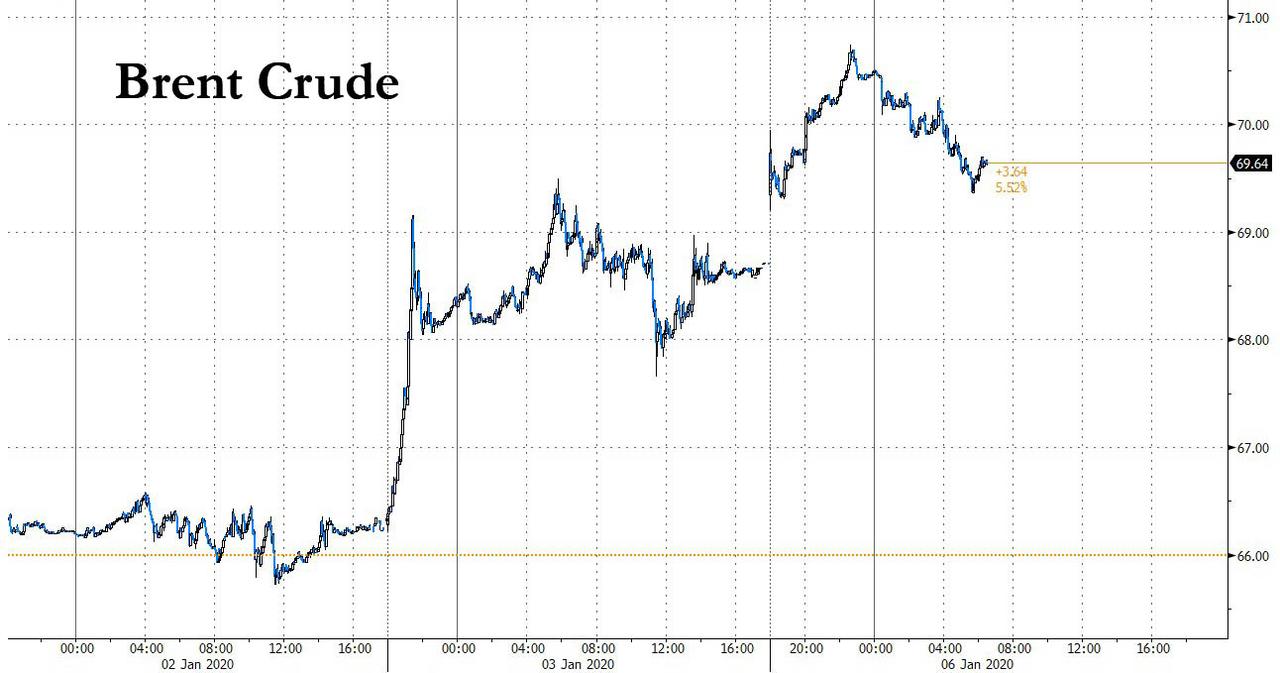

Global markets slumped, and US equity futures tumbled on Monday, wiping out gains for 2020 as tensions in the Middle East soared amid fears of escalation in the Middle East as investors pushed safe-haven gold to a seven-year high, and oil jumped to its highest since September.

The fallout from last week’s targeted US assassination of top Iranian General Qassem Soleimani escalated over the weekend, as the US said it detected a heightened state of alert by Iran’s missile forces (hardly a shock) as President Donald Trump warned the U.S. would strike back, “perhaps in a disproportionate manner”, if Iran attacked any American person or target. Also on Sunday, Iraq’s parliament on Sunday recommended US troops be ordered out of the country, while Trump threatened heavy sanctions on Iraq and said any US troop withdrawal would require Iraq to reimburse the US for billions spent on an air base.

And so, with algos once again looking at geopolitical risk as something more than merely a reason for the Fed to ease further, US equity futures slumped to red for 2020, with Boeing once again dragging down the Dow after a new, potentially “catastrophic” wiring issue was discovered on the 737 MAX…

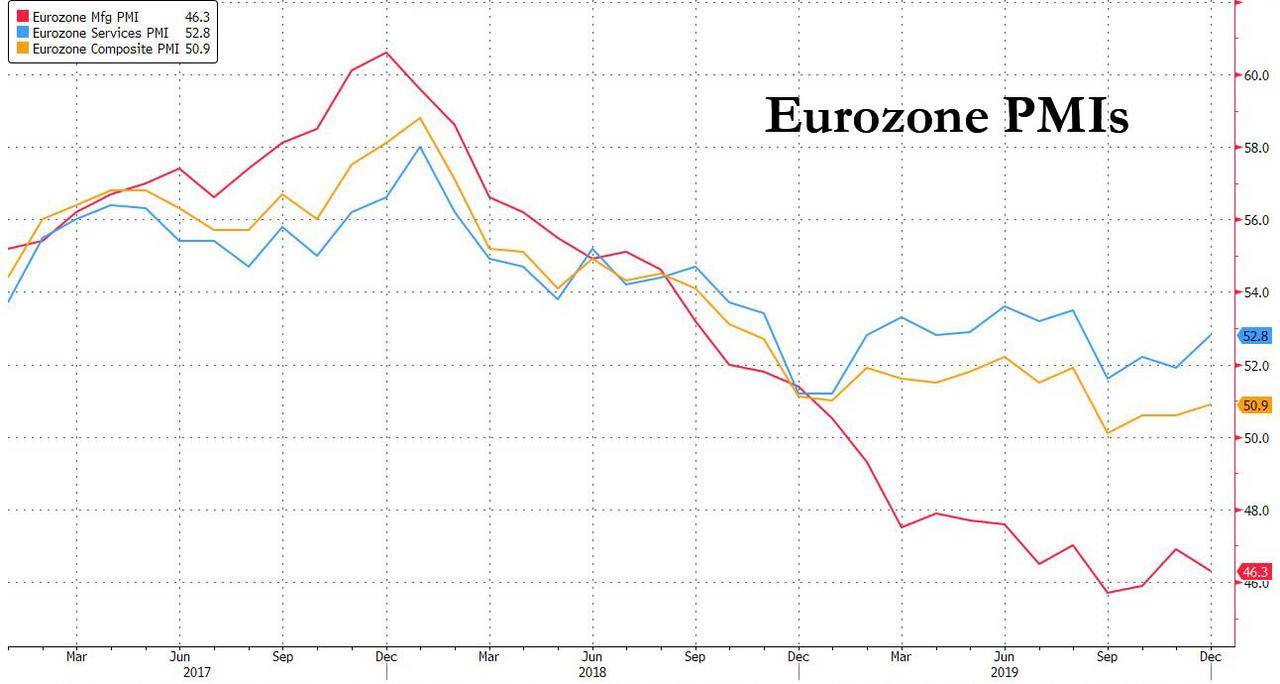

… as European shares extended losses and were set for their worst day in a week, with the European Stoxx 600 index down 1.12%. The European oil and gas stock index rose about 0.74% and was the sole gainer among its peers, hitting its highest since July as Brent briefly topped $70 overnight. Not even the strongest Eurozone Service PMI print since August, which at 52.8 came in well above the 52.4 expected, had any impact on the sudden dour mood.

Earlier in the session, Asian stocks fell, led by health care and consumer staples, as frictions between the U.S. and Middle Eastern countries ratcheted up. The MSCI Asia Pacific Index headed for its biggest drop since Aug. 26, on growing tensions following the killing of Soleimani. In Asia, Japan’s Nikkei slid almost 1.9% in a sour return from holiday, while stocks listed in Hong Kong and mainland China dropped in afternoon trade, with technology-related shares among the worst performers. Chinese shares, which had opened in the red, reversed their losses, as did Australian shares which ended the day flat. Hong Kong’s Hang Seng index lost 0.8%. Most other markets in the region were also down, with India’s S&P BSE Sensex Index and Japan’s Topix Index falling more than 1%.

MSCI’s All-Country World Index was down 0.43%, erasing all its new year gains in its biggest two-day fall since early December.

Naturally, the perpetually optimistic sellside hoped markets would quickly look beyond the recent geopolitical debacle: “Geopolitical events by their nature are unpredictable, but previous periods of increased tensions suggest that the impact on wider markets tends to be short-lived, with more lasting effects confined to local markets,” said Mark Haefele, chief investment officer at UBS Global Wealth Management, adding that “in general, this supports holding a diversified portfolio.”

Maybe Haefele will be right, but for now the market is not buying it, with spot gold surging another 1.6% to $1,579.72 per ounce, reaching its highest since April 2013, and making a delightful mockery of certain WSJ commodity “experts.”

At the same time, oil prices also extended gains on fears any Middle East conflict could disrupt global supplies; Brent futures rose as high as 2% to $70 a barrel, while U.S. crude climbed 1.7% to $64.12.

Commenting on the possible trajectory of oil, Bob McNally, president of Rapidan Energy Group said in a Bloomberg Television interview that potential retaliation for the U.S. killing of Qassem Soleimani could push Brent crude $3-$10 a barrel higher, “we think crude’s going up some more” because there will be further violence as Iran responds to the U.S. attack. “The odds of an overt U.S. military conflict with Iran went from about 5% to about 25%. We think crude has some more risk pricing to do.”

The rapid escalation of tensions in the Middle East continues to damp the enthusiasm that sent the S&P 500 Index to a record on its first trading day of the year. “Everyone got comfortable in that fact that the truce in the trade war had come through and the outlook for 2020 looked a little bit better and then we had another geopolitical reminder come through,” said Suncorp Group Financial Market Strategist Peter Dragicevich. “It’s going to be a big driver of markets in the short term.”

In rates, sovereign bonds benefited from the safe haven bid with yields on 10-year Treasuries down at 1.7725% having fallen 10 basis points on Friday.

In FX, the yen reached its strongest level in three months thanks to Japan’s massive holdings of foreign assets, as investors assume Japanese funds would repatriate their money during a true global crisis, pushing the yen higher. The Bloomberg Dollar index weakened, and the pound gained as the U.K.’s dominant services sector showed signs of strengthening at the end of 2019 following Boris Johnson’s decisive election victory. The euro eased to 120.61 yen having hit a three-week low. The risk sensitive currencies of Australia and New Zealand were on track for their fourth straight session of losses.

“Iran is almost certainly to respond in some scale, scope and magnitude,” said Lee Hardman, currency analyst at MUFG. Therefore “market participants are likely to remain nervous until there is more clarity over how geopolitical tensions between the U.S. and Iran will proceed”, Hardman said, noting that geopolitical tensions could hurt global economic growth, especially if the price of oil increases.

But while investors are having a hard time as they final have to learning to co-exist with an odd red color on their screens, nobody had a worse day overnight than the virtue signallers in Hollywood who were simply crucified by Ricky Gervais’ parting Golden Globes monologue.

On today’s economic calendar, we have the latest Markit services PMI report.

Market Snapshot

S&P 500 futures down 0.8% to 3,209.50

STOXX Europe 600 down 1.3% to 412.76

MXAP down 1% to 170.06

MXAPJ down 0.9% to 551.66

Nikkei down 1.9% to 23,204.86

Topix down 1.4% to 1,697.49

Hang Seng Index down 0.8% to 28,226.19

Shanghai Composite down 0.01% to 3,083.41

Sensex down 1.9% to 40,688.02

Australia S&P/ASX 200 up 0.03% to 6,735.71

Kospi down 1% to 2,155.07

German 10Y yield fell 2.1 bps to -0.299%

Euro up 0.2% to $1.1180

Brent Futures up 1.7% to $69.75/bbl

Italian 10Y yield fell 6.6 bps to 1.177%

Spanish 10Y yield fell 0.4 bps to 0.382%

Brent Futures up 1.7% to $69.75/bbl

Gold spot up 1.6% to $1,577.05

U.S. Dollar Index down 0.1% to 96.71

Top Overnight News from Bloomberg

Iran said on Sunday that it no longer considered itself bound by a 2015 nuclear agreement, while Iraq’s parliament voted to expel U.S. troops from the country

Yen bulls betting the currency will gain in times of stress face one formidable obstacle — Japanese demand for Treasuries. Japanese funds will pounce at every opportunity to buy the dollar cheaply and invest overseas given low domestic bond yields, said Satoshi Nagami, head of global strategies investment group at Sumitomo Mitsui DS Asset Management Co.

The yen’s correlation with the CBOE Volatility Index climbed to the highest in almost three years. Japan’s currency climbed to the strongest since October on Monday after the VIX index jumped last Friday. The correlation between the two has also been increasing as sentiment has swung more wildly in recent months due to global risk events such as the U.S.- China trade war, said Daisaku Ueno, chief currency strategist at Mitsubishi UFJ Morgan Stanley Securities Co. in Tokyo

Gold surged to the highest level in more than six years, with Goldman Sachs Group Inc. saying bullion offered a more effective hedge than oil to the crisis. Palladium extended gains to an all-time high

BNP Paribas SA is planning to join JPMorgan Chase & Co. and Citigroup Inc. by setting up an electronic currency trading and pricing platform in Singapore. The facility will support electronic trading of 50 currencies in spot, forward, swaps, non-deliverable forwards and options, according to a company statement

Asian equity markets kicked the week off mostly in the red following downside seen on Wall Street on Friday as US-Iran developments and dismal US ISM metrics weighed on sentiment. ASX 200 (Unch) was initially led lower by a bulk of its constituents in negative territory including its largest weighed financial sector, albeit losses were somewhat cushioned by gold miners and energy names as prices in the complexes rose amid the escalating geopolitical tensions, thus the index later pared losses. Meanwhile, Nikkei 225 (-1.9%) underperformed given the recent safe-haven demand in the JPY and as Japanese participants had the first chance to react to the Middle Eastern events after their extended New Year break. Elsewhere, Hang Seng (-0.8%) opened modestly in negative territory but extended losses as heavyweight financial names accelerated downside – with traders attributing the closures of local bank branches due to the protests, albeit the index later climbed off lows as energy names benefitted from the surge in crude prices with oil-giants CNOOC and PetroChina notching gains in excess of 3%. Finally, Shanghai Comp (U/C) oscillated between gains and losses as the overall risk aversion in the market was countered by the tentative dates touted for the US-China Phase One signing and with the PBoC’s RRR cut going into effect today, releasing over CNY 800bln of long-term funds.

Top Asian News

Hong Kong Parents Eye Singapore Schools as Wild Protests Endure

Schuldschein Sets Record For the Third Consecutive Year in 2019

India Stocks Extend Drop as Oil Jumps on U.S.-Iran Rhetoric

Philippines Prepares to Evacuate Citizens in Middle East

European bourses are subdued this morning (Stoxx 50 -1.3%), as geopolitical tensions in the Middle-East weighs on price actions at present. An update on the Iranian situation is available in the Commodity section below. Indices are all in negative territory at present in Europe, with US futures painting a similar picture as well; price action this morning has seen the Dax and Stoxx 50 futures test key levels to the downside, with the Dax having convincingly given up the 13000 mark and the Stoxx 50 testing the 3700 handle on multiple occasions. In terms of sectors, it’s a similar story to Friday, with all sectors in negative territory aside from Energy which continues to benefit from the inflated oil prices; which is, in turn, assisting oil names such as BP (+1.8%) and Shell (+1.2%), and is helping to stem some of the FTSE 100’s losses – although, the bourse is firmly in negative territory. Turning to other notable movers, at the other end of the spectrum from the outperforming oil names, flight names such as Ryanair (-4.4%) and Air France (-3.8%) are weighed on by the crude market. Elsewhere, Metro AG (-5.0%) are suffering after a downgraded at JP Morgan, while ASML (-3.5%) are afflicted on reports that US President Trump’s Administration implemented a campaign to prevent the sale of the Co’s technology to China; do note, this reportedly began in 2018 and as such the significance and current situation may well have changed given the US-China trade war.

Top European News

Euro Zone Edges Away From Stagnation as Services Improve

U.K. Services Get Boost From Election as New Orders Increase

Takeaway Nears Final Victory in $8 Billion Just Eat Battle

European Car Stocks Fall as U.S., U.K. Auto Markets Weaken

In FX, the Pound was already benefiting from broad Dollar weakness amidst escalating US-Iran tensions and in wake of last Friday’s dire manufacturing ISM, but Cable derived some independent impetus from the final UK services PMI that beat consensus in contrast to manufacturing and construction, albeit only reclaiming the 50 level on post-GE relief that did not factor in the preliminary survey. Cable is hovering just shy of 1.3175 compared to lows circa 1.3064, and Eur/Gbp threatening 0.8500 bids even though the single currency also gleaned encouragement from largely firmer than forecast or flash Eurozone services PMIs and a more upbeat than anticipated Sentix index. Indeed, Eur/Usd is inching towards 1.1200 vs sub-1.1160 and further from very early 2020 lows under 1.1125.

CHF/CAD/NZD/AUD/JPY – Also firmer against the Greenback, as the DXY slips towards 96.500, with the Franc crossing 0.9700, Loonie eying 1.2950, Kiwi hovering around 0.6675 and Aussie back above 0.6950. However, the Yen is still finding 108.00 too tough to breach as Japanese markets return from their long New Year holiday and contacts suspect a major player is propping the headline pair.

NOK/SEK – More divergence between the Scandi Crowns, as Eur/Nok repels risk-off rebounds ahead of 9.9000 with the aid of oil’s ongoing rally, but Eur/Sek struggles to cap advances beyond 10.5000 and Nok/Sek extends its advance towards 1.0700 after breaking strong chart resistance below 1.0500.

EM – Risk aversion has prevented many regional currencies from taking advantage of general Buck underperformance, but the Rouble is also getting a boost from Brent and Rand has managed to overcome more Eskom power issues to bounce back above 14.3000 on what appears to be mainly technical grounds.

In commodities, WTI and Brent prices remain elevated on Iranian-US tensions, with prices higher by just shy of a USD 1.0/bbl at present; as crude prices have drifted off of their overnight highs as sentiment continues to deteriorate but the ferocity of newsflow has reduced as mourning proceedings are underway in the Middle-East for Soleimani. Weekend reports highlight that Iran has finalised a retreat from the nuclear deal, and will not be complying with any of the restrictions set out within this; additionally, Iraqi parliament has voted to begin developing plans to end the presence of US troops in the country. For reference, an analysis piece which outlines the impact on oil prices from the ongoing situation is available on the Newsquawk headline feed. The key views are JP Morgan believing that the stress on oil supply will be bearable, looking ahead focus is on whether the situation will disrupt supplies with UBS noting, at a minimum, US assets in the area are at risk – as is the broad infrastructure for oil supply in the region. Separately, ING posit that any substantial increase in crude prices could see US President Trump authorise use of the SPR, which currently has around 635mln barrels of supply. For reference, in 2018 the US consumed on average 20.5mln BPD, given this consumption rate this implies self-sufficiency for the US of roughly one month; excluding additional US production which last week stood at 12.9mln barrels and would significantly extended such a period of self-sufficiency. In terms of metals, spot gold is well supported on the aforementioned tensions with the precious metal having printed a high just over USD 1587/oz overnight, which is a 6-year high for the safe haven. Price action picked up once the USD 1557/oz mark was surpassed, with contacts noting a number of stops were likely present around this figure. Additionally, the yellow metal will be gleaning support from a softer dollar this morning, with the DXY having printed multiple fresh session lows throughout the session.

US Event Calendar

9:45am: Markit US Services PMI, est. 52.2, prior 52.2

9:45am: Markit US Composite PMI, prior 52.2

DB’s Jim Reid has returned from vacation, and concludes the overnight wrap:

As I left for my hols before Xmas I received the seasonally uplifting message from our CEO wishing us all a happy holiday and imploring us to fully recharge our batteries ahead of starting back in January. Well on my first day back today my brain has just flashed up “5% battery – do you want to go into low power mode”. We had an awful 2-week holiday. My wife was in bed for 70% of it with severe flu and still was yesterday. I had a constant bad cough and the children took it in turns to be on industrial strength calpol. Bronte has applied for emancipation. I’ve been longing to return to work to recover and now my dreams have been fulfilled.

Already in the two business days this year markets have been up and down like me in the night on holiday administering medicine to the troops. In today’s EMR we’ll review some of the main action at the back end of last week and also include some bullets as to the major stories you may have missed over the Xmas/NY period if you’ve only just returned from holiday. A reminder that Henry put out the December, Q4, 2019 and full decade multi-asset returns last week (link here).

First lets have a quick look at what we can expect from this first full week of the new decade. Obviously it will be dictated by the seismic events surrounding Iran and the US (more later) but outside of this it’s not the busiest week for data but there are some key highlights still with today’s global services and composite PMIs, tomorrow’s US non-manufacturing ISM and Friday’s US payrolls (after last month’s surprise bumper print) being the main ones. On payrolls, the consensus is +167k, with the unemployment rate expected to remain at 3.5%, its joint lowest since 1969. This follows some fairly strong US employment data recently, with nonfarm payrolls growing by +266k in November, the most since January, while the 3-month moving average also rose above +200k for the first time since January. The full day by day week ahead is at the end.

Bringing you up to speed with markets over the holiday season and in 2020 to date now. Equities finished 2019 at record highs, with the S&P 500 up +28.88% over the year, its strongest annual performance since 2013, while in Europe the STOXX 600 was up +23.16%, its best year since 2009. Markets then had a bumper opening day of the decade on Thursday as Trump suggested he’d sign the phase one deal on January 15th and China announced an interest rate cut (see bullets below).

However, markets were soon knocked off their perch on Friday by the news that a US airstrike had killed the Iranian military commander Qassem Soleimani. In response, Iran’s Supreme leader Ayatollah Ali Khamienei said that “severe retaliation” awaited his murderers, raising fears over the potential for further escalation between the two sides. However, US President Trump said later on that “We took action last night to stop a war. We did not take action to start a war.” The remarks that the US wasn’t looking for conflict chimed with those by US Secretary of State Mike Pompeo, who tweeted on Friday that in a conversation with Russian foreign minister Sergei Lavrov, “I emphasized that de-escalation is the United States’ principal goal.” However the stakes were raised again on Saturday as Trump identified 52 Iranian sites the US would hit if Iran retaliates. Meanwhile on Sunday the Iraqi government voted to expel US troops from the country after a near 17 year period of presence there since the toppling of Saddam Hussein in 2003. In response, Trump said that US troops won’t leave without billions in payment for their base there – or if they do leave Trump would apply sanctions. Also the Iranian government said it no longer considers itself bound by the limits on the enrichment of uranium. Most importantly though we’re left waiting to see if we get an aggressive response from Iran with the whole Middle East likely feeling vulnerable. The US State department said on Sunday that there was ‘heightened risk’ of missile attacks near military bases and energy facilities in Saudi Arabia.

Meanwhile, Esmail Ghaani, the successor to Soleimani, said in an interview with Iranian state television aired today that “Certainly actions will be taken”. He also said that, “We promise to continue down martyr Soleimani’s path as firmly as before with help of God, and in return for his martyrdom we aim to get rid of America from the region.” So, a nervous time awaits markets. Elsewhere, NATO ambassadors are due to meet today in Brussels to discuss the situation in the Middle East.

Away from geo-politics, the SCMP reported over the weekend that the Chinese trade delegation tentatively plans to travel to the US on January 13 for the signing of the phase one deal.

This morning in Asia, crude oil continues to be a key mover with brent (+2.73%) and WTI (+2.38%) oil prices both up a further 2% after Friday’s c. 3% gain (see below). Meanwhile, most Asian markets are trading in the red with the Nikkei (-1.75%) leading the declines as it trades for the first time in 2020 after the holidays. The Hang Seng (-0.52%) and Kospi (-0.80%) including India’s Nifty (-1.10%) are also down while Chinese bourses (Shanghai Comp +0.63%) are up likely on the SCMP news mentioned above. In the Middle East, Saudi Arabia’s Tadawul index (-2.42%), Qatar’s Ex index (-2.14%), UAE’s DFM General (-3.06%), Kuwiat’s KWSE Premier Mkt (-4.07%) and Israel’s Tel Aviv 35 (-0.55%) were all down yesterday. As for Fx, most Asian currencies are trading weak this morning with the currencies of oil importing countries down. Elsewhere, futures on the S&P 500 are down -0.28% while 10yr treasury yields are down a further -1.6bps to 1.773% this morning. As for overnight data releases, Japan’s final December manufacturing PMI came in at 48.4 vs. 48.8 (flash) while China’s December Caixin services PMI came in at 52.5 (vs. 53.2 expected) and the composite PMI stood at 52.6 (vs. 53.2 in last month).

As the news of the US strike broke on Friday the biggest impact was seen in oil, with Brent crude up +3.55% on the day, bringing it to $68.60 per barrel, its highest closing level since just after the drone strike on Saudi oil facilities in September, while WTI also ended the session up +3.06%. Investors fled to safe havens elsewhere, with gold up +1.51% in its biggest daily rise since August, while the Japanese Yen was the strongest performing G10 currency on Friday, up +0.449% against the US Dollar. Equities sold off in response, with the S&P 500 (-0.71%), the NASDAQ (-0.79%) and the Dow Jones (-0.81%) all losing ground, while sovereign debt rallied, with 10yr Treasury yields down -8.9bps to 1.788% having touched 1.944% on Thursday. 10yr bunds closed the week at -0.284% having hit -0.16% (the highest since May) early on Thursday. MSCI’s emerging markets Europe, Middle East and Africa index declined by -0.78% on Friday.

Matters were not helped on Friday by the ISM manufacturing index from the US coming in at 47.2 in December (vs. 49.0 expected), which was the worst reading since June 2009 and below every estimate on Bloomberg. Looking at the index in more detail provided little encouragement, with the employment reading down to 45.1, the lowest since January 2016, new orders falling to 46.8, the lowest since April 2009, and production down to 43.2, also the lowest since April 2009. In terms of other data out Friday, the preliminary reading for German CPI rose to +1.5% (vs. +1.4% expected) in December, its highest level since June on the EU harmonised measure. However, unemployment rose by +8k in December (vs. +4k expected) but at still very low levels.

Finally from the Fed, we got the minutes on Friday from the FOMC’s December meeting, where rates were kept on hold following 3 consecutive 25bp cuts at the previous meetings. The overall takeaway, in line with the median dot showing policy remaining unchanged in 2020, is that “participants regarded the current stance of monetary policy as likely to remain appropriate for a time as long as incoming information about the economy remained broadly consistent with the economic outlook.” In a somewhat dovish note, the minutes said that “While many saw the risks as tilted somewhat to the downside, some risks were seen to have eased over recent months.” So it’s interesting that the risks are still seen as tilting to the downside. Other somewhat dovish points were that “Participants generally expressed concerns regarding inflation continuing to fall short of 2 percent”, and also that “various participants remarked that there were some indications that further strengthening in overall labor market conditions was possible without creating undesirable pressures on resources.” Thursday this week is a big day for Fed speak with Clarida, Williams, Evans and Bullard speaking.

Before the day-by-day week ahead, for those of you who are returning today and need a recap of other major events that have happened in the last two weeks since the EMR last appeared in your inboxes here’s the run-down of the main stories:

China: The People’s Bank of China lowered the required reserve ratio for banks by 50bps, helping to support domestic liquidity. Our China economics team released a note last week about the issue (link here), but they also write that the space for further cuts in the required reserve ratio “is becoming increasingly limited”, and their base case is that the PBoC won’t cut the RRR further in 2020.

US-China trade: President Trump announced that he would sign the Phase One US-China trade deal at the White House on January 15th. He also tweeted that “At a later date I will be going to Beijing where talks will begin on Phase Two!”

Brexit: UK MPs voted in favour of the Withdrawal Agreement Bill at second reading, which is the bill that ratifies the Brexit deal into UK law. MPs will be resuming debate tomorrow, though thanks to the Conservatives’ 80-seat majority following the election, the bill is expected to pass through the House of Commons easily. European Commission President Ursula von der Leyen will be meeting with Prime Minister Johnson on Wednesday.

North Korea: Kim Jong Un announced he would be introducing a “new strategic weapon”.

France: Strikes have continued over reforms to public sector pensions, with President Macron refusing to back down on the proposals. Bloomberg has now reported that unions are aiming for a fourth day of nationwide protests on January 9 and a fifth on January 11. The far-left CGT union is pushing to escalate the demonstrations, calling for a complete blockade of the country’s refineries from January 7 to 10. Elsewhere, a survey conducted Thursday and Friday by pollster Ifop and published on Sunday found that 44% support the strikers, down from 51% just before Christmas.

Spain: Following November’s inconclusive general election, Prime Minister Sanchez got the agreement he needed to form a new government after one of the Catalan separatist parties agreed that they would abstain in a confidence vote. Along with other abstentions, this means that Sanchez’s new coalition government between his Socialist Party and Podemos will be able to win a simple majority vote in parliament.

Data: Not much of significance to report over the last two weeks. The US data included the Conference Board’s consumer confidence reading coming in at 126.5 in December (vs. 128.5 expected). The preliminary durable goods orders reading for November was also worse than expected, down -2.0% (vs. +1.5% expected), as were new home sales in November at a seasonally-adjusted annual rate of +719k (vs. +732k expected). The final Euro Area manufacturing PMI for December was revised up to 46.3 (vs. flash 45.9), with the German reading revised up to 43.7 (vs. flash 43.4). However, the Italian reading fell to 46.2, its lowest level since April 2013. Meanwhile in the UK, the final reading of Q3 GDP was revised up to +0.4% qoq (vs. 0.3% in the prior estimate).

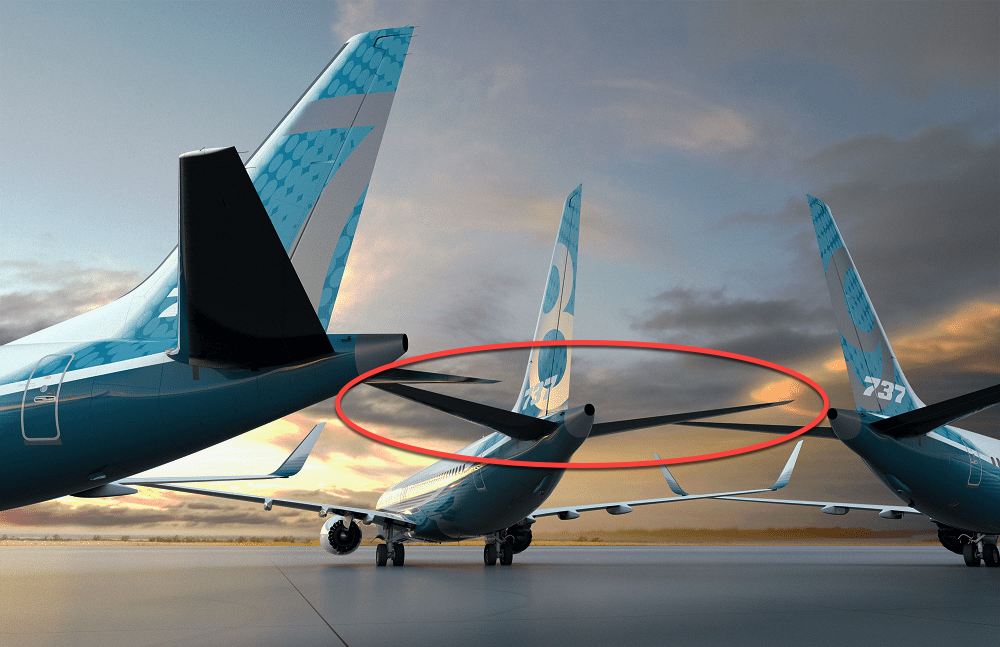

New, Potentially “Catastrophic” Wiring Issues Found In Boeing 737 Max

As if Boeing needed any more bad news.

The Federal Aviation Administration (FAA) conducted an internal audit in December of the Boeing 737 Max and found wiring issues could potentially cause a “catastrophic” short circuit at the rear of the plane and lead to a crash, a senior engineer at Boeing and three people familiar with the matter told The New York Times.

Boeing is examining if two wiring harnesses at the rear of the plane are too close together that would result in an electric short that would cause the plane’s tail to malfunction in flight, said one of the sources.

If Boeing decides to fix the wiring problem, it would mean that more than 800 Max jets would have to see wiring reconfiguration.

Of course, Boeing told The Times that the fix is relatively simple. Spokesman Gordon Johndroe said Sunday the “identified issue is part of a rigorous process, and we are working with the FAA to perform the appropriate analysis. It would be premature to speculate as to whether this analysis will lead to any design changes.”

It was unclear, however, if simple also means cheap, and some have speculated that a full-blown recall could cost tens ofd billions.

An FAA statement Sunday said investigators are “re-analyzing certain findings from a recent review of the proposed modifications to the Boeing 737 MAX.” The agency will “ensure that all safety-related issues identified during this process are addressed.”

The FAA said the wiring harnesses are too close together, located at the rear of the plane, would cause the motors that control the stabilizer, a horizontal fin on a plane’s tail, to malfunction (short circuit) and could lead to a potentially “catastrophic” crash.

Max engines have also become another focus for FAA investigators.

RE: Boeing 737 Max

Anyone who missed this post back in March should read throughly. The issue with the 737 Max is not a software issue, it’s a design issue. Boeing got desperate when Airbus released the NEO, so they too wanted a big engine. Merry Christmas $ba.d$bahttps://t.co/3I8z0p6ljn

All of these issues, of course, are separate from the MCAS software that was likely the cause of two separate Max crashes, killing 346 people. New Max issues could delay the ungrounding even further. There is no clear timeline of when the planes will return to the air.

Meanwhile, confirming that things are going from bad to worse, the WSJ reported that Boeing is mulling raising more debt to “improve finances”, read fund buybacks, as costs related to the grounding of its 737 MAX are raising. The paper reports that Boeing is also considering cutting CAPEX, freezing acquisitions and cutting on R&D to save cash. In total, analysts expect Boeing to raise as much as $5BN in additional debt to help cover expenditures that could rise to $15BN in 1H 2020. It was not clear if all of this new money, or just most of it, would to repurchasing BA shares.

In politics, this is a powerful wish and a commonly heard refrain. It’s the desire that propelled Donald Trump into the White House with a Make America Great Again cap perched atop his head. His campaign tapped into a longing for an imagined 20th century standard, when the United States was militarily, technologically, and commercially dominant abroad and relatively homogeneous at home.

Now Joe Biden is rallying voters against Trump using the same technique. Biden’s “no malarkey” campaign bus is powered by the fumes of goodwill he generated in his role as Barack Obama’s vice president. He is selling the pre-Trump normal, and plenty of Democratic primary voters seem to be buying.

One weird side effect of this strategy is that Biden is running a markedly conservative campaign in the literal sense of the word: He wants to go back, to conserve what we had under Obama. The contrast is stark with the socialists and progressives otherwise dominating the Democratic field. What if, the Biden campaign seductively asks, we could simply pretend the 45th presidency never happened?

The idea of a “return to normalcy” has worked before. Warren G. Harding ran for president under that banner exactly a century ago. He won despite being described by H.L. Mencken as a man “with the face of a moving-picture actor…and the intelligence of a respectable agricultural implement dealer” (and later, less generously, as “a downright moron”).

“America’s present need,” Harding declared, “is not heroics but healing; not nostrums but normalcy; not revolution but restoration; not agitation but adjustment; not surgery but serenity; not the dramatic but the dispassionate; not experiment but equipoise; not submergence in internationality but sustainment in triumphant nationality.”

Students of history will recall that his term ended not in equipoise but in a wave of scandal and an untimely death. I will leave you to draw your own conclusions about possible parallels for the centennial of those events.

Millennials and young Gen Xers actually use normal as a term of approbation. When I meet someone new, I’m offering a high compliment indeed if I say, “He seems really normal.” Perhaps as a result of my casual abuse of the word, even I—in a moment of frustration over the difficulty of staying on top of an erratic news cycle—have grumbled: “When will things be normal again?”

But I didn’t mean it. Because when it comes to politics, normal is terrible.

When things were normal—whether you benchmark to the Republican version or the Democratic version—politicians were still venal and governance shoddy. Americans were continually subjected to the depredations of the federal government in general and the president in particular. Normal was cronyist and authoritarian and profligate and petty. It was dominated by mushy compromise and zero-sum thinking. And the various tentacles of the state extended into every part of American life, from what we eat to what our kids learn in school to what we watch on TV.

Normal isn’t serenity and healing; it’s Teapot Dome. Going back to normal means going back to a time when many aspects of our political system were in dire need of reform.

When former Trump lawyer Michael Cohen testified before the House Oversight Committee, Rep. Elijah Cummings (D–Md.) said: “We have got to get back to normal.” But normal has always been scandalous and messy and dishonest. These hearings were just the latest in a long line of inquiries into politicians’ misbehavior.

Biden’s version of the lament is especially amnesiac, since it places the lost golden age a mere three years ago. If you are of voting age, you remember the Obama administration clearly. In these times of sustained high dudgeon, it can be easy to forget, but there was a lot of rather lofty dudgeon in those days too.

Donald Trump has shaken things up in Washington, just as he promised he would. But the result of that shakeup has not been, as many hoped, a demystification of the presidency, a draining of the swamp, or shift in public support away from centralization. It also has not been a return to American global hegemony, as others desired. Instead, there has been an increasing focus on the presidency, thanks in part to Trump’s personal insistence on live-tweeting his own administration.

His impeachment will, in the short run, make things more febrile in all the ways that people calling for normalcy lament. But as Gene Healy argues in this month’s cover story (page 18), we shouldn’t be too quick to dismiss impeachment and its ramifications as a tool for getting to a better status quo.

“If you elect me president, I promise you won’t have to think about me for 2 weeks at a time,” Democratic hopeful Michael Bennet tweeted in August. “I’ll do my job watching out for North Korea and ending this trade war. So you can go raise your kids and live your lives.”

Bennet was the 22nd entrant to the Democratic field and is an otherwise unremarkable moderate Colorado senator. (I had to double-check just now that he was, in fact, still in the race, so I guess he has kept his promise not to take up too much mental real estate.) Still, Bennet’s tweet offers an inkling of what our post-political future could look like—the thing people are actually longing for when they pine for “normal.”

Bennet told the L.A. Times editorial board that Biden’s project to Make America Normal Again was delusional. “The idea that the vice president says, ‘If we just get rid of Trump, then it will all go back to normal’ or the way it was, that doesn’t even reflect the history of the Obama administration. The last six years of that administration, we were paralyzed. We were immobilized.”

We don’t really want things to be normal. Normal wasn’t working. We want politics to function smoothly and without much attention. We want politicians to leave us alone.

As Bennet says, we should mostly be thinking about raising our kids and living our lives. When you’re not engaging with politics, and especially electoral politics, you are almost certainly spending your days making things better for other people in some tangible way. You’re making peanut butter sandwiches or buying groceries or sending an email someone was waiting for or showing up for your shift on time.

When politicians retire in shame or despair—a very normal phenomenon—they often say they are leaving politics to spend more time with their families.

At long last, a good idea.

from Latest – Reason.com https://ift.tt/2sQldF6

via IFTTT