What a week we just had in the precious metals market.

From a huge drop last Friday – which in the past would have presaged further declines the following week – to a significant rebound in the gold price, coupled this time with a major drop in the US dollar – which I will argue may be the signal for a switch to inflationary conditions.

First the chart

We see the nice deflationary trend of the past 18 months looks to have been decisively broken by last week’s action.

Although it will be a few weeks before we can be absolutely sure, last week suggests that we are about to embark on another bout of inflation, no doubt as carefully calibrated by the Masters of the Universe as they can fill a shot-glass of whiskey from a pool of liquidity the size of a football field. Either, like a small child pouring very carefully, they have poured only too much, or they have sloshed out enough whiskey to fill a large swimming pool, and we are about to see what happens when it all lands in a shot glass.

Now, why the need for some liquidity?

Another chart:

This graph plots the gold-copper ratio against its rate of change. I typically interpret this ratio as an indicator of the real world preference between bricks and mortar and financials. When the ratio is low, it’s a sign that people would rather make refrigerators than chase derivatives.

Rate of change is the vertical axis. Near the top of the chart means that the plot is shifting towards the right at high speed. Currently, the system is moving toward the right (ratio is increasing) at the fastest rate in the last couple of years.

To me, this means the real economy is degrading very quickly.

Thus the Fed may feel pressured to pump out some liquidity.

If we are moving into an inflationary cycle, then one consequence, according to this recent post, is a decrease in the gold-silver ratio. Given that moves tend to get larger as liquidity sloshes around the system, the gold-silver ratio could hit a significant low, implying a new all-time high for the silver price (in fiat terms).

Normally I would wait a few weeks to have greater certainty, but if there is a swimming pool full of whiskey heading for a shot glass I want to get as close to ground zero as possible with a bucket.

It’s almost never a good idea to use a public health crisis to score points against your political opponents—and if you’re going to do it, you really ought to try to describe the situation accurately.

Actually, that second part applies even when there’s no public health crisis.

It has, however, become fashionable for certain elements of the Very Online Left to use the ongoing coronavirus outbreak as evidence that libertarians either don’t actually exist or that we quickly abandon our principles in the face of a pandemic. This recent outbreak of libertarian bashing—which makes only slightly more sense than the claims made by some on the right that libertarians are secretly running everything in Washington, D.C. and plotting to get your kids addicted to porn—seems to have started with a pithy tweet from Atlantic writer Derek Thompson on March 3. But it’s become a ubiquitous online “take” since Sunday afternoon, when Bloomberg opinion writer Noah Smith logged on.

Libertarians: Government sucks, let's hollow out the civil service

*Pandemic comes, hollowed-out civil service is unable to respond effectively*

The take may have achieved its final form—at least let’s hope so—with The Atlantic‘s publication on Tuesday of an 800-word piece from staff writer Peter Nicholas carrying the headline (sigh) “There Are No Libertarians in a Pandemic.”

Nicholas tries to get away with this nonsense by setting up a false dichotomy. Trump is campaigning against socialism, you see, and libertarians also dislike socialism—so therefore the Trump administration must be libertarian. Right? Therefore, when Trump starts talking like a socialist himself—by promising coronavirus bailouts and the repurposing of disaster recovery funds to cover people who come down with COVID-19—it is proof positive that the libertarian world has abandoned its commitment to smaller government. Voila!

Perhaps TheAtlantic‘s editorial staff has self-quarantined from its duties—how else to explain how an otherwise thoughtful publication could allow a headline that confuses libertarianism with anything that the Trump administration is doing? For that matter, maybe Smith and Thompson believe that an army of strawmen are an effective defense against COVID-19. I hope it works out for them.

As a libertarian in a pandemic, let me first assure you that we do in fact still exist.

And, in fact, it is the free market—and, to a lesser extent, its defenders—who will help you survive the new coronavirus. All those groceries you’re stocking up on in advance of the expected collapse of civilization? They didn’t end up on grocery store shelves because government officials ordered it to happen or because someone was feeling particularly generous today. That gallon jug of hand sanitizer delivered to your front door less than 48 hours after you ordered it online? It didn’t show up because Trump tweeted it into existence or because the surgeon general is driving a delivery truck around the country.

Bottled water? Face masks? They’re available because someone is turning a profit by making and selling them. The first latex gloves were invented in the 1880s but the disposable variety that are so useful right now have “only been available since 1964, as innovated by the private company Ansell, founded by Eric Ansell in Melbourne, Australia. Thank you international trade,” notes Jeffrey Tucker, editorial director of the American Institute for Economic Research.

Sure, one consequence of the success of private enterprise in reshaping the world is an interconnected planet that allows for something like COVID-19 to spread more rapidly than would have been possible in the past. But modern technology has also allowed doctors, private enterprises, and (yes) governments to respond more quickly than ever before.

It also means that you’ll have access to nearly every piece of film, television, and music ever recorded by human beings if you have to self-quarantine for a week or two. It means that humans have the ability to live far healthier lives than they did in 1918, when a global flu pandemic killed 50 million people. The people who live through the current coronavirus outbreak because of stronger immune systems made possible by steady diets won’t show up on any list of statistics after the coronavirus has passed, but capitalism is at least partially to thank for their survival.

In short, if you had to pick any time in human history to live through a global pandemic, you’d be incredibly foolish not to pick the current time. And the reason you’d pick this moment in history probably has less to do with who is running the White House, the Centers for Disease Control and Prevention, or the World Health Organization, and more to do with the technological and medical advances made possible by free enterprise.

“What is the mighty contribution of government these days?” asks Tucker. “To order quarantines but not to tell you whether you can step outside, how you will get groceries, how long it will last, who you can invite in, and when it will all end. Don’t try to call the authorities. They have better and bigger things to worry about than your sorry plight that is causing you sleepless nights and endless worry. Thank goodness for digital technology that allows you to communicate with friends and family.”

Yeah, there are libertarians in a pandemic. We’re the ones willing to acknowledge how much more all of this would suck if the market didn’t exist.

from Latest – Reason.com https://ift.tt/2TEgzo5

via IFTTT

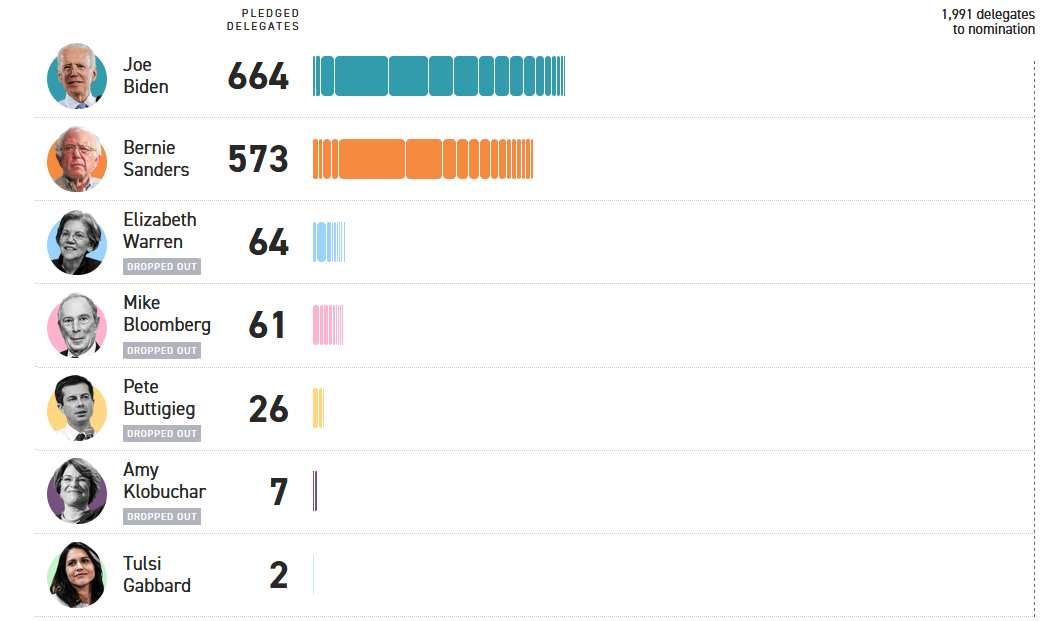

Tonight’s Primary: Sanders Needs Big Win In Michigan Tonight Or Biden Takes The Cake

Six states are holding primaries today – with Michigan awarding the most delegates, followed by Washington State, Missouri, Mississippi, Idaho and North Dakota. Results are expected to begin rolling in around 8 p.m. Eastern time.

Former VP Joe Biden has 664 delegates under his belt going into tonight’s voting, while Sen. Bernie Sanders (I-VT) trails with 573. After Sanders’ lost an early delegate lead on Super Tuesday, the Vermont democratic socialist needs a big win in Michigan to put him back in the game with its 125 delegates. If that doesn’t happen, it’s curtains for Bernie.

As the NY Post notes, Sanders won Michigan in 2016 in a stunning victory over Hillary Clinton by 18,000 votes. That said, “there are doubts Sanders can recreate that victory, with speculation rampant that Michigan this time could sound the death knell for his campaign.“

The reality of the situation is not lost on PredictIt betters, who have Biden sharply in the lead as the likely Democratic nominee.

WTI Maintains Gains Despite Much Bigger Than Expected Crude Build

Oil prices screamed higher (partly in response to investors’ rising skepticism about the escalating war of words between key oil exporters Saudi Arabia and Russia) bouncing after yesterday’s carnage. Today’s most notable headline was OXY cutting its dividend (by 86%), but that failed to worry bullish oil machines who bought with both hands and feet today.

Bloomberg’s Liam Denning noted:

Oxy’s decision to stretch itself to beat Chevron Corp. in a bid battle for Anadarko Petroleum Corp. left it vulnerable in an industry not exactly famed for its stability. This is just damage control on a grand scale.

API

Crude +6.407mm (+1.9mm exp)

Cushing +364k

Gasoline -3.091mm (-2.1mm exp)

Distillates -4.679mm (-1.8mm exp)

API was expected to report a continued trend from last week – more builds for crude and draws for products – but the data was more extreme with a much bigger than expected crude build and much bigger than expoected product draws…

Source: Bloomberg

WTI hovered around $34.60 ahead of the print and dipped very modestly

Oil prices are likely to come back under pressure unless Moscow and Riyadh agree to another round of production cuts, according to Harry Tchilinguirian, head of commodity strategy at BNP Paribas.

“If the oil market has to contend with both a positive supply shock and a negative demand shock, then prices are going to be extremely weak,” Mr. Tchilinguirian said.

Neither Riyadh nor Moscow stand to benefit from oil prices remaining at current levels or dropping lower, traders said, despite the production threats.

“All the Saudis are going to do is escalate to negotiate,” said Edward Marshall, commodities trader at Global Risk Management. “The Saudis have downplayed the necessity of a meeting, but I don’t think it’s in anyone’s interest to go lower, although it certainly can.”

But in order for prices to move even lower and stay there, “we need to see storage tanks being filled at a greater level than we originally thought following the coronavirus outbreak,” Mr. Marshall said.

The last week has seen The Dow make several 1000-point-plus swings which were more than a little startling for many investors, veering dangerously close to a precipice which has 1929 written all over it. Across the internet, panicky discussion has erupted over whether this foretells another 1987 collapse as Donald Trump warned, or something more akin to Black Tuesday of 1929. Others have pondered whether this is more similar to a 1923 Weimar hyperinflation where Germans became millionaires overnight (not much to celebrate when bread costs billions).

The fact of the oncoming collapse itself should not be a surprise- especially when one is reminded of the $1.5 quadrillion of derivatives which has taken over a world economy which generates a mere $80 trillion/year in measurable goods and trade. These nebulous bets on insurance on bets on collateralized debts known as derivatives didn’t even exist a few decades ago, and the fact is that no matter what the Federal Reserve and European Central Bank have attempted to do to stop a new rupture of this overextended casino bubble of an economy in recent months, nothing has worked. Zero to negative percent interest rates haven’t worked, opening overnight repo loans of $100 billion/night to failing banks hasn’t worked- nor has the return of quantitative easing which restarted on October 17 in earnest. No matter what these financial wizards try to do, things just keep getting worse.

Rather than acknowledge what is actually happening, scapegoats have been selected to shift the blame away from reality to the point that the current crisis is actually being blamed on the Coronavirus!

Deeper than Corona

Let me just state outright:

That while the coronavirus may in fact be the catalyzer for the oncoming financial blowout, it is the height of stupidity to believe that it is the cause, as the seeds of the crisis goes deeper and originated much earlier than most people are prepared to admit.

To start getting at a more truthful diagnostic, it is useful to think of an economy in real (vs purely financial) terms – That is: Simply think of the economy as total system in which the body of humanity (all cultures, nations and families of the world) exist.

This co-existence is predicated on certain necessary powers of production of food, clothing, capital goods (hard and soft infrastructure), transportation and energy production. After raw materials are transformed into finished goods, these physical goods and services move from points A to B and are consumed. This is very much akin to the metabolism that maintains a living body.

Now since populations tend to grow geometrically, while resources deplete arithmetically, constant demands on new creative discoveries and technological application are also needed to meet and improve upon the needs of a growing humanity. This last factor is actually the most important because it touches on the principled element that distinguishes humanity from all other forms of life in the ecosystem which Lincoln identified wonderfully in his 1859 Discoveries and Inventions Speech:

“All creation is a mine, and every man, a miner. The whole earth, and all within it, upon it, and round about it, including himself, in his physical, moral, and intellectual nature, and his susceptibilities, are the infinitely various “leads” from which, man, from the first, was to dig out his destiny… Man is not the only animal who labors; but he is the only one who improves his workmanship. This improvement, he effects by Discoveries, and Inventions.”

During a 1994 address to Russian scientists in Moscow, a modern adherent to Lincoln’s system (the late economist Lyndon LaRouche) addressed this concept from a modern perspective by asking:

“Mankind is different than any other animal; how do we prove this? And how does that bear on this question of technology? If the hominids-mankind-were higher apes or animals, we would have the population potential (approximately) of higher apes, baboons (which some people behave like), or chimpanzees. In that case, in the past 2 million years of the interglacial period, at no time would the human population of this planet have exceeded 10 million persons approximately… we have increased the world population to 5.3 billion people. Twenty or twenty-five years ago, we had the basis for, in a normal fashion, going to 25 billion people, without any great problem. In the past 30 years, we have destroyed so much of the planet’s productive technology and productive capacity, that we are in a disaster.”

What these men laid out in their own manner are not mere hypotheses, but elementary facts of life which even the most ardent money-worshipper cannot get around.

Of course money is a perfectly useful tool to facilitate trade and get around the awkward problem of lugging bartered goods around on your back all day, but it really is just that: a supporting element to a physical process of maintenance and improvement of trans-generational existence. When fools allow themselves to loose sight of that fact and elevate money to the status of a cause of all value (simply because everyone wants it), then we find ourselves far outside the sphere of reality and in the Alice in Wonderland world of Alan Greenspan’s fantasy world where up is down, good is evil, and humans are little more than vicious monkeys.

So with that in mind, let’s take this concept and look back upon today’s crisis.

Greenspan and the Controlled Disintegration of the Economy

When Alan Greenspan confronted the financial crisis of October 1987, markets had collapsed by 28.5% and the American economy was already suffering from a decay begun 16 years earlier when the dollar was removed from the fixed exchange rate and was “floated” into a world of speculation. This departure from the 1938-1971 Industrial growth model ushered in a new paradigm of “post-industrialism” (aka: nation stripping) under the new logic of “globalization”. This foolish decision was celebrated as the consumer-driven, “white collar society” which would no longer worry about “intangible things” like “the future”, infrastructure maintenance, or “growth”. Under this new paradigm, if something couldn’t generate a monetary profit within 3 years, it wasn’t worth doing.

Paul Volcker (Greenspan’s predecessor at the Federal Reserve) exemplified this detachment from reality when he called for the “controlled disintegration of society” in 1977, and acted accordingly by keeping interest rates above 20% for two years which destroyed small and medium agro industrial enterprises across America (and the world). Greenspan confronted the 1987 crisis with all the gusto of a black magician, and rather than re-connect the economy to physical reality and rebuild the decaying industrial base, he chose instead to normalize “creative financial instruments” in the form of derivatives, which quickly grew from several billion in 1988 to $2 trillion in 1992 to $70 trillion in 1999.

When Bill Clinton repealed Glass-Steagall bank separation of commercial and investment banks as his last act in office in 1999, speculators had un-bounded access to savings and pensions which they used with relish and went to town gambling with other people’s money. This new bubble continued for a few more years until the $700 trillion derivatives time bomb found a new trigger and the subprime mortgage market nearly burned the system down. Just like in 1987, and the collapse of the Y2K bubble in 2001, the Mammon worshipping wizards in the ECB and Fed solved this crisis by creating a new system of “bailout” which continued for another decade.

Today, western economies have been hollowed out of the very life blood that caused value by supporting human life in the first place.

The Ugly Truth of Today’s Crisis

New “sub-prime” bubbles have been created in the Corporate Debt sector which has risen to over $13.8 trillion (up 16% from the year earlier). A quarter of which is considered junk, and another half graded at BB by Moodies (a step above junk).

Household debt, student and auto debt has skyrocketed and since wages have not kept up with inflation causing even more unpayable debts have been incurred in desperation. Industrial jobs have collapsed consistently since 1971, and low paying service jobs have taken over like a plague.

The last report from the American Society of Civil Engineers concluded that America desperately needs to spend $4.5 trillion just to bring its decayed infrastructure up to safety levels. Roads, bridges, rail, dams, airports, schools all received near failing grades with the average age of Dams clocking in at 56 years, and many water pipes over 100 years old, and transmission/distribution lines are well over 60 years. The factories which once supplied those infrastructure needs are long outsourced, and much of the productive workforce that had that living knowledge to build a nation are retired or dead leaving a deadly generation knowledge gap in its place filled with millennials who never knew what a productive economy looked like (and aging baby boomers who have tried hard to forget what it was).

American farmers have probably been the most devastated in all this with dramatic population losses across the entire farm belt of America and the average age of farmers now 60 years. It was recently reported that 82% of U.S. Agricultural family income comes from off farms, as mega cartels have taken over all aspects of farming (from equipment/supplies, packaging and the even the actual farming in between).

Why was this permitted to happen? Well besides the obvious intention to induce “a controlled disintegration of the economy” as Volcker so coldly stated, the idea was always to create the conditions described by the late Maurice Strong (sociopath and Rothschild cut-out extraordinaire) in 1992 when he rhetorically asked:

“What if a small group of world leaders were to conclude that the principal risk to the Earth comes from the actions of the rich countries? And if the world is to survive, those rich countries would have to sign an agreement reducing their impact on the environment. Will they do it? The group’s conclusion is ‘no’. The rich countries won’t do it. They won’t change. So, in order to save the planet, the group decides: Isn’t the only hope for the planet that the industrialized civilizations collapse? Isn’t it our responsibility to bring that about?”

How do we get back to health?

Like any addict who wakes up one morning at rock bottom with the sudden terror that his death is nigh, the first step is admitting we have a problem.

This means simply: acknowledging the true nature of the current economic calamity instead of trying to blame “coronavirus” or China, or some other scapegoat.

The next step is begin to act on reality instead of continuing to take heroine (a fine metaphor for the addiction to derivatives speculation).

An obvious first step to this recovery involves restoring Glass-Steagall in order to 1) break up the Too Big to Fail banks and 2) impose a standard of judging “false” value from “legitimate” value which is currently absent from the modern psycho that lost all sense of needs vs wants. This would allow nations to re-create a purge of the unpayable fictitious debt and other claims from the system while preserving whatever is tied to the real economy (whatever is directly connected to life). This process is sort of akin to cutting a cancer.

At this point nation states will have re-asserted their true authority over the pirates of private finance controlling the Trans-Atlantic financial system like would-be gods of Olympus (unbounded perverted vices and all).

President Trump and other sane patriots from both parties of America would then have to figure out how to start the long but vital process of forcing credit to regenerate the destroyed productive base of America and Europe with a focus on advanced infrastructure, science and technological progress. This later investment into space science, atomic power, and transportation (high speed and magnetic levitation) would drive new breakthroughs necessary to overcome the current “limits to growth” that Green New Dealing oligarchs believe justify reducing the world population to less than two billion.

Where Franklin Roosevelt had to drive this process solo in the 1930s, today’s America luckily has a China-Russia alliance that have created a powerful “New Deal” of win-win cooperation in the form of the evolving Belt and Road Initiative with invitations for western nations to jump on board.

A bottle of your favorite Scotch whisky might cost a bit more this year, thanks to new tariffs imposed by the Trump administration that target European imports like alcohol, cheese, and wool.

President Trump ordered those tariffs last year as punishment for what the United States sees as unfair subsidies provided by the European Union to Airbus, a major airplane manufacturer based in France. In practice, the tariffs mean that American consumers of whisky and wine, among other things, will be paying higher import taxes in order to punish European producers—even though those industries are not at fault for the corporate welfare provided by their governments. The whole situation highlights the folly of using tariffs at all.

Written and narrated by Eric Boehm. Motion graphics by Lex Villena. You can read the full article that this video is based on here.

A bottle of your favorite Scotch whisky might cost a bit more this year, thanks to new tariffs imposed by the Trump administration that target European imports like alcohol, cheese, and wool.

President Trump ordered those tariffs last year as punishment for what the United States sees as unfair subsidies provided by the European Union to Airbus, a major airplane manufacturer based in France. In practice, the tariffs mean that American consumers of whisky and wine, among other things, will be paying higher import taxes in order to punish European producers—even though those industries are not at fault for the corporate welfare provided by their governments. The whole situation highlights the folly of using tariffs at all.

Written and narrated by Eric Boehm. Motion graphics by Lex Villena. You can read the full article that this video is based on here.

Stocks & Oil ‘Dead Bat Bounce’ On Fiscal Dreams, But Credit Crash Continues

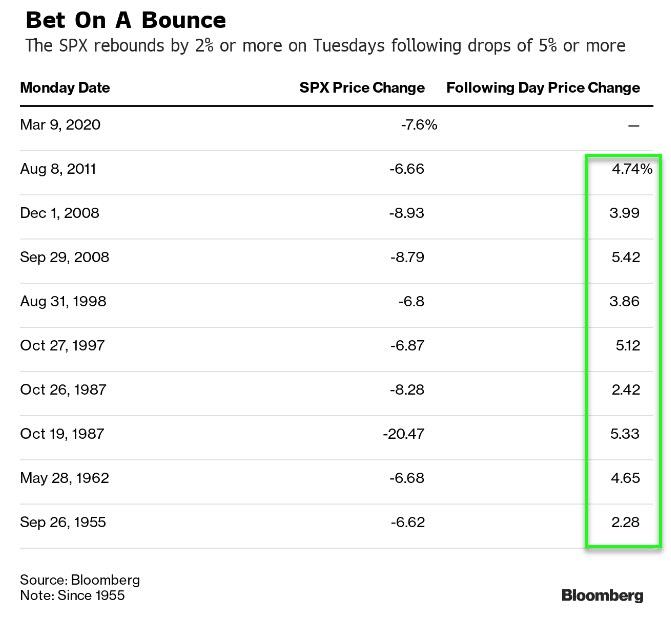

A Bounce today was expected… as Bloomberg details, prior to Monday’s steep decline, the S&P 500 had plunged by 5% or more to start the week on nine occasions since 1955.

On each of the following Tuesdays, the benchmark bounced back by 2% or more, data compiled by Bloomberg show.

Which means that a red close for stocks today would have been unprecedented in market history (and for a few brief minutes this morning, stocks went red). But as positive stimulus headlines struck, stocks accelerated higher… Dow ended over 1100 points higher and this was the S&P’s biggest day since Dec 2018.

Confirming that…”all is well”

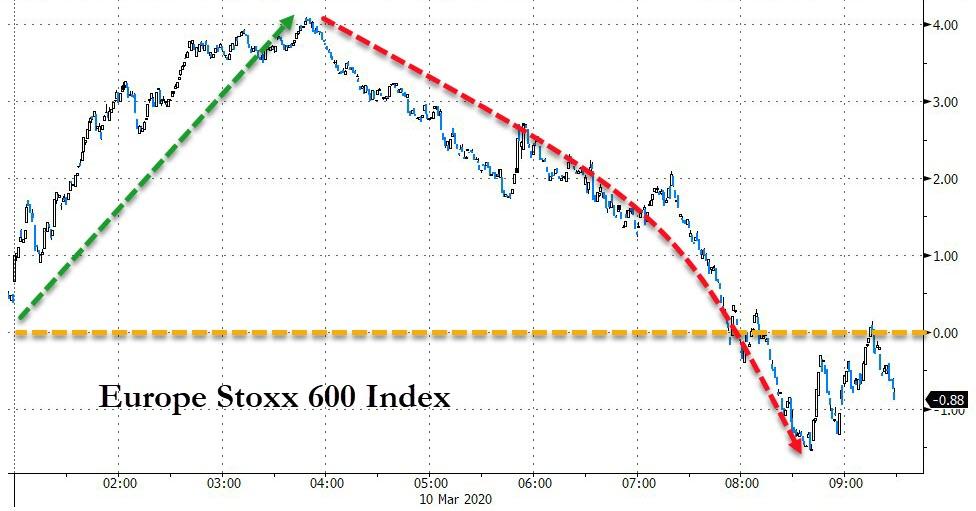

European stocks followed the US and bounced hard from yesterday’s losses, but by the close had erase all those gains as early optimism faded about measures to contain the coronavirus outbreak and provide economic stimulus to counter its impact.

Source: Bloomberg

The Stoxx Europe 600 Index fell 1.1% by the close to the lowest level since January 2019, wiping out gains of as much as 4.1%.

Source: Bloomberg

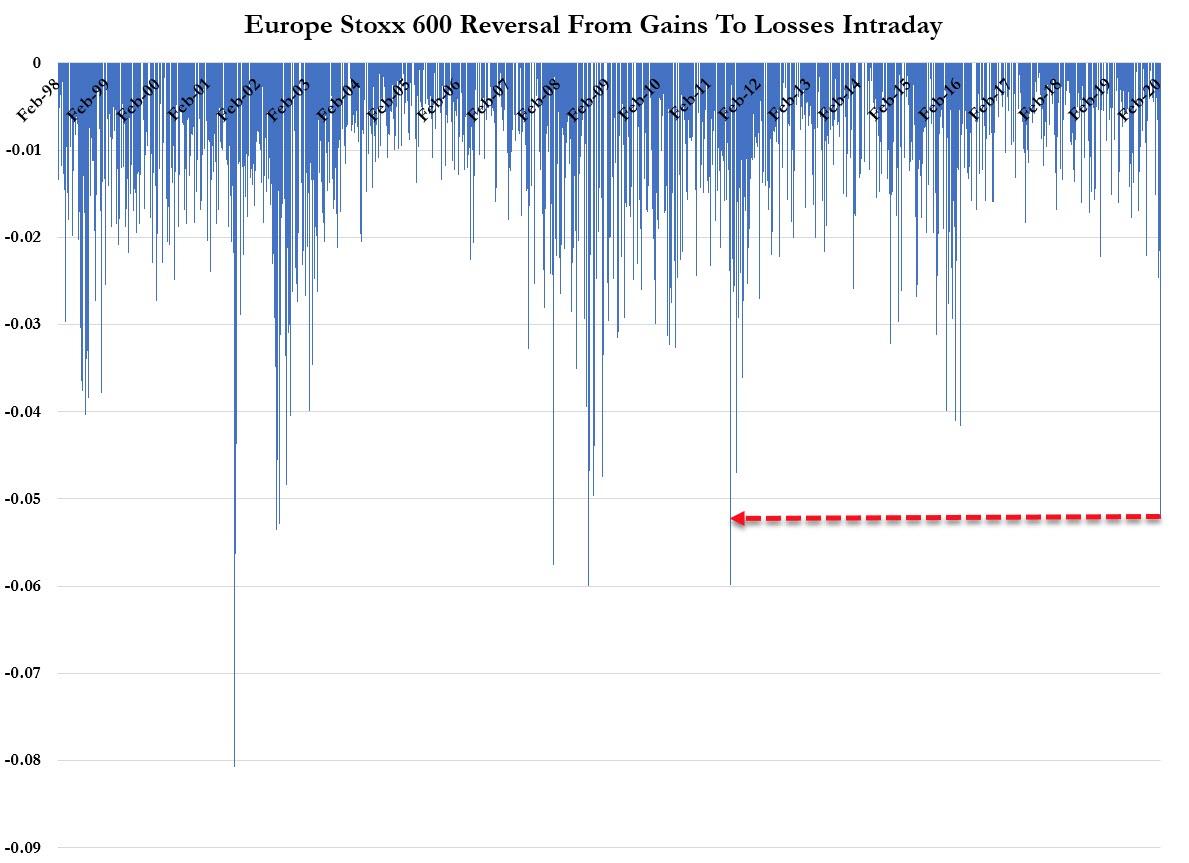

That turnaround was the biggest intraday reversal since August 2011.

While today’s bounce was very exciting, in context with yesterday’s drop, it;s not quite as impressive…

Be very careful trusting this as sustainable – one look at the level at which the machines ramped to suggests this move was extremely technical/algo-driven…

US markets all remain below their 200DMAs…

Bank stocks bounced along with everything else but remain well below Friday’s close…

Source: Bloomberg

Virus-related sectors rebounded hard today with Airlines erasing yesterday’s losses…

Source: Bloomberg

Factor-wise, markets were relatively untilted today – i.e. it was just systemic buying…

Source: Bloomberg

The energy sector ended green… but given oil’s rebound, the bounce was barely notable..

Source: Bloomberg

FANG Stocks rallied back but failed to clear yesterday’s losses…

Source: Bloomberg

Options markets ‘broke’ today, which briefly triggered a ramp in the underlying indices…

Source: Bloomberg

And before we all get too excited about today’s bounce, remember – fun-durr-mentals…

Source: Bloomberg

VIX pushed back below 50 today (after testing positive on the day briefly), but remains extremely elevated…

US credit markets were not playing along with stocks at all today… And despite VIX’s explosive move, credit protection costs have moved even more…

Source: Bloomberg

And just to ensure readers are not paying attention to malarkey like this overheard on CNBC: “IG bond yields have fallen which is the opposite of what happens in a crisis” – said in a way that was supposed to reassure you that everything is fine… except IG credit spreads are utterly exploding higher (even as yields slide due to the collapse in risk-free rates)…

Source: Bloomberg

Treasury yields exploded higher today, with dramatic steepening of the curve (30Y +29bps, 2Y +11bps)

Source: Bloomberg

10Y surged back to breakeven from Friday’s close…

Source: Bloomberg

The yield curve steepened dramatically – back to erase yesterday’s flattening…

Source: Bloomberg

The dollar soared higher today, erasing its losses since The Fed did an emergency 50bps rate-cut…

Source: Bloomberg

USDJPY also erased its drop from the weekend…

Source: Bloomberg

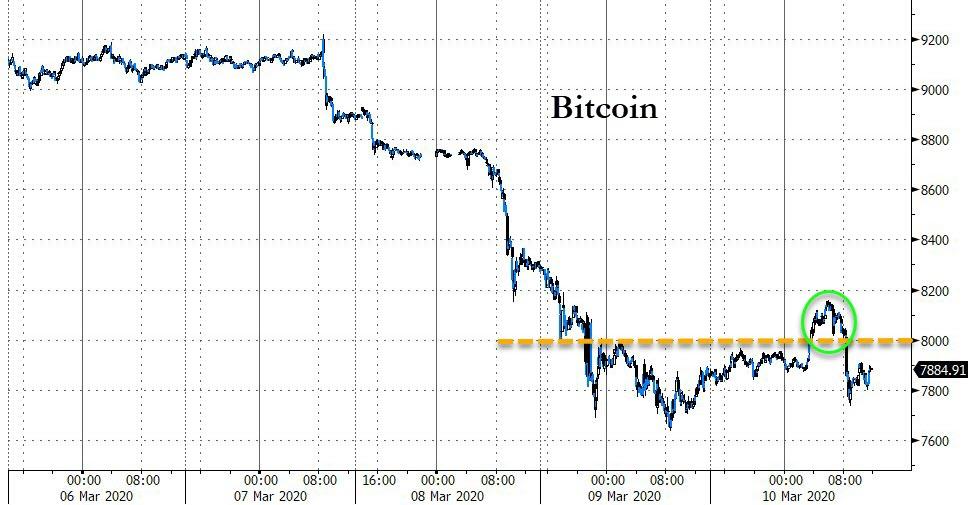

Cryptos were relatively flat on the day…

Source: Bloomberg

Bitcoin briefly pushed back above $8000, but quickly fell back…

Source: Bloomberg

Commodities were mixed today with PMs lower and crude and copper making gains…

Source: Bloomberg

Gold slipped lower today, with futures finding support at $1650…

And WTI soared 11% – though in context it’s got a long way to go…

Finally, US markets are now screaming for more than 3 rate-cuts by the time of the March meeting (in 10 days)…

Source: Bloomberg

And for a sense of the panic – the implied correlation of the S&P’s 500 components has soared to its highest since Nov 2011 – signaling ‘correlation-one’ regime is here, just as it was during the Lehman crisis and the European crisis.

A major airport in Atlanta has admitted that neither its own officials, nor the Department of Homeland Security are screening travellers arriving from Italy or South Korea, two countries where the coronavirus has hit the hardest outside of China.

Hartsfield-Jackson Atlanta International Airport in Atlanta, Georgia announced that while the CDC has demanded screening of passengers from China and Iran, no such screening is taking place for those coming in from Italy/South Korea, “because those countries are doing exit screenings.”

As per the CDC, In the US, airports are conducting entry screening for travelers from China and Iran.

People aren’t being screened when they arrive from Italy/South Korea, because those countries are doing exit screenings.

For more info, please visit: https://t.co/2dgrl0KFhr *NA

So, essentially, officials in the US are relying on the word of their foreign counterparts that sufficient screening is happening before people leave.

This jives with reports from those entering the US after returning from Italy, confirming that they were not stopped or screened.

Italy was yesterday placed on complete lockdown after deaths increased by nearly 60 percent overnight. From today, the movement of Italy’s population of 60 million has been severely limited by the government there, with travel only being permitted for “urgent, verifiable work situations and emergencies or health reasons”.

In South Korea there are almost 8000 cases of infections.

On Friday, President Trump told the media that “The tests are all perfect”:

“The [coronavirus] tests are all perfect. Like the letter was perfect. The transcription was perfect. This was not a perfect as that, but pretty good.” — is Trump referring to the transcript of his phone call with the Ukrainian president here? pic.twitter.com/FU5XxPTu7Z

Nearly $1 out of every $10 being spent to fund the global response to the new coronavirus outbreak is coming from private donors, according to a new tracking system put together by the Kaiser Family Foundation. That adds up to more than $725 million coming from non-profits, businesses, and foundations.

The Kaiser Family Foundation, a non-profit global health policy think tank and information center, put together this database and released it today to serve as a resource to show where money is coming from and going to in the global effort to fight the spread of the new coronavirus, called COVID-19.

The total that has been spent so far is $8.3 billion, which means the vast majority of spending has come from government sources. The top spender is the World Bank, which has outspent everybody else to the tune of $6 billion and has prioritized that spending in the poorest countries with the highest risk.

The U.S. government has given $1.285 billion to other countries. An important caveat: This database does not show a government’s domestic spending to contain and fight COVID-19 within its own borders. This is all about the international effort.

Unsurprisingly, the largest private donor is Tencent, the massive Chinese tech company that pretty much operates the country’s entire internet social structure and is worth more than $500 billion (in U.S. dollars). Tencent has donated $214 million towards containment efforts in China. Alibaba, the massive Chinese e-commerce company, has donated $144 million.

Here in the United States, the Bill and Melinda Gates Foundation is getting attention for its $100 million in total donations and its direct efforts to facilitate faster coronavirus testing and the development of potential treatments. It’s the largest U.S. private donor currently, but it’s not the only one. Google, Caterpillar, Mastercard, General Motors, and several corporations that run resorts and hotels (like MGM Resorts International) are contributing anywhere from hundreds of thousands to millions of dollars.

Most of the money right now is focused on assisting China, but it seems likely that as the coronavirus spreads we’ll see donations spread to other countries. The Kaiser Family Foundation also acknowledges that its figures are based on public reports of private donations. There may be other private donors that Kaiser has missed. The chart lists all of its sources.

Looking at the private donor list, it seems obvious why they’re donating to China. All of them have huge customer bases there, particularly the Las Vegas resort chains. They have a huge stake in making sure consumers of their goods and products don’t die off. That’s a great thing about capitalism—it creates incentives to assist in the fight against large scale crises.

Read the list here. It will be updated as the Kaiser Family Foundation hears of new donors, both government and private.

from Latest – Reason.com https://ift.tt/3cMxLzw

via IFTTT