President Trump’s former lawyer Michael Cohen has backtracked in a recent recorded phone call, claiming he’s not actually guilty for crimes he pleaded guilty to.

In a conversation with Trump-hating provocateur Tom Arnold, Cohen said that he hadn’t evaded taxes, and that a criminal charge linked to his home-equity line of credit was “a lie,” according to the Wall Street Journal.

Arnold recorded Cohen without his knowledge for approximately 36 minutes during a March 25 phone call, which Arnold provided to the Journal.

“There is no tax evasion,” said Cohen on the call. “And the Heloc? I have an 18% loan-to-value on my home. How could there be a Heloc issue? How? Right?…It’s a lie.”

Of note, Cohen is due to begin serving a three-year prison sentence on May 6 after testifying for more than 100 hours to federal and congressional investigators.

“You would think that you would have folks, you know, stepping up and saying, ‘You know what, this guy’s lost everything,’” Cohen told Arnold during the call. “My family’s happiness, and my law license,” he continued, “I lost my business…my insurance, my bank accounts, all for what? All for what? Because Trump, you know, had an affair with a porn star? That’s really what this is about.”

Cohen’s attorney, Lanny Davis, said: “Michael has taken responsibility for his crimes and will soon report to prison to serve his sentence. While he cannot change the past, he is making every effort to reclaim his life and do right by his family and country. He meant no offense by his statements.”

And while the White House and the Manhattan US attorney’s office declined to comment, Trump attorney Rudy Giuliani tweeted: “Poetic justice for a disbarred lawyer who surreptitiously recorded his client and numerous others including Chris Cuomo.”

Michael Cohen, in Recorded Phone Call, Walks Back Parts of Guilty Plea – The Wall Street Journal. Poetic justice for a disbarred lawyer who surreptitiously recorded his client and numerous others including Chris Cuomo. https://t.co/KTJ4DuTU8T

Since Cohen began composing for the Angry Democrats he has demonstrably lied under oath in his guilty plea and his testimony to Elijah “I’ll throw the book at you” Cummings. Report ignores all of this and provides no facts to evaluate Cohen’s credibility. One of many deceptions.

In August, Cohen pleaded guilty to a wide variety of mostly financial crimes, telling a judge at his December sentencing “I take full responsibility for each act that I pled guilty to.”

Mr. Cohen pleaded guilty to eight criminal charges brought by New York federal prosecutors, including campaign-finance violations in connection with hush-money payments to the two women, the former porn star Stormy Daniels and the former Playboy centerfold model Karen McDougal. Mr. Trump denies he had sex with either woman.

Mr. Cohen also admitted to five counts of evading personal income taxes and one count of understating his debt and expenses in an application for a $500,000 home-equity line of credit, or Heloc.

Mr. Cohen testified in February in the House of Representatives that Mr. Trump committed crimes, including directing the hush-money schemes during the 2016 presidential campaign involving the two women. “I never directed Michael Cohen to break the law,” Mr. Trump wrote on Twitter in December. –Wall Street Journal

Prosecutors in New York, meanwhile, said that Cohen has yet to acknowledge that he made false statements to banks, concluding “This signals that Cohen’s consciousness of wrongdoing is fleeting, that his remorse is minimal, and that his instinct to blame others is strong.”

via ZeroHedge News http://bit.ly/2DuZzbw Tyler Durden

Many financial assets, especially those that are the riskiest, are priced well above their respective fundamental values. A thank you primarily belongs to unprecedented monetary policy conducted on a domestic and global scale. The vast financial rewards and temporary economic stability attributed to central bank actions appear to be blinding many investors to the longer-term consequences of these actions and the implications for their investments in an era of monetary policy normalization.

Accordingly, we discuss the proverbial fly in the ointment, or what might prevent central bankers from being able to successfully “manage” markets with their extraordinary policies.

The Fed Put

Many investors assume that, if the equity markets decline in a meaningful way, the Federal Reserve (Fed) will once again spring into action to halt the decline. The so-called “Fed Put” is not new; in fact, it was originally coined the “Greenspan Put” due to the actions of Fed Chairman Alan Greenspan following the 1987 stock market crash. At that time, the Fed led by Greenspan added liquidity to the financial system to comfort investors and make them willing to buy financial assets. Ever since the Fed has been increasingly active vocally and via monetary policy in attempting to stem sharp market declines.

It is important to understand that the Fed does not stop stock market declines by purchasing stocks directly. They provide verbal influence and liquidity to banks which works its way through the financial plumbing to the markets. Therefore, and of huge importance, the effectiveness of Fed actions is highly dependent on the trust and willingness of investors. To retain this trust, the Fed must remain vigilant of market conditions.

The Fed’s attentiveness has been on full display since the Financial Crisis of 2008. On numerous occasions since the Crisis, relatively minor equity index declines elicited speeches by Fed members to subtly, and not so subtly, remind the market of their money printing capabilities. In fact, even when markets rested at all-time highs, they have been quick to remind the public of their abilities. The following two examples serve as evidence:

On the morning of October 15, 2014, with the S&P 500 down over 3% on the day and nearly 10% since mid-September, Federal Reserve Bank of St. Louis President and FOMC voting member James Bullard stated that QE might be extended. This was curious, to say the least, considering that in the weeks prior he mentioned that it was time to reduce QE. Bullard’s simple reminder of QE spurred the bulls to actions. From the moment he mentioned QE, the S&P 500 rallied over 2% and closed the day down less than 1%. In the two weeks following, it rose another 10% and closed the month at record highs. That action was later deemed the “Bullard Stick Save.”

We were recently reminded of this in the fourth quarter of 2018. By Christmas Eve stock markets were down nearly 20% over the preceding three months. Within a month, Jerome Powell and the Fed all but put an end to further rate hikes and halted quantitative tightening (QT). These actions were ultimately made official in the months following and all with negligible economic evidence to support such a sharp reversal in monetary policy.

Inflation and the U.S. Dollar

Over the last 30 years, the Fed’s primary weapon to support markets has been interest rate reductions using the Fed Funds target rate. Since 2008, money printing, technically known as quantitative easing (QE), was introduced as the zero bound on interest rates constrained the Fed from reducing the Fed Funds rate further. Lower interest rates and QE have proven to be an incredibly powerful driver of asset prices, but only as long as inflation is benign and the dollar is relatively stable.

Inflation: Before the low and stable inflation environment of the last 20 years, inflation was much more of a concern. From 1972 to 1980, inflation, as measured by annual changes in the consumer price index (CPI), increased from 3% to nearly 15%. Under Chairman Paul Volcker (1978-1987) and Arthur Burns (1970-1978), the Fed aggressively increased the Fed Funds rate to put a lid on inflation and reinforce confidence in the U.S. dollar. These leaders prescribed the necessary medicine with little regard for the stock market.

The graph below compares Fed Funds and CPI to the S&P 500 in the 1970s. Note that, in 1973 and 1974 under the chairmanship of Arthur Burns, the Fed aggressively removed liquidity from the financial system by raising the Fed Funds rate despite mounting losses in the S&P 500.

Data Courtesy: Bloomberg

Had the Fed sat on their hands out of concern for stock prices, it is quite likely inflation would have kept rising and the dollar may have been at risk of losing its status as the world’s reserve currency. That would have produced global turmoil along with massive repercussions for economic growth for years to come. The Fed prescribed medicine that would further aggravate current economic woes but with the promise of a healthier domestic and global economic environment in the future.

Currently, inflation hovers near the Fed’s target level and they characterize risks to growth as balanced. However, asset inflation resulting from the Fed’s easy money policies is soaring. Stock prices, as measured by prices and importantly valuations, and at or near record highs, largely due to excessive amounts of liquidity injected by global central banks to combat the financial crisis. Interest rates remain at historically low levels and credit spreads near some of the tightest levels of the last 50 years. Art, classic cars, high-end real-estate, and a host of other assets are engulfed in the same mania driving more traditional financial assets.

Recently we have seen some data from corporate earnings reports and corporate surveys that suggests inflation is starting to form. Although still weak, wages have also turned higher. Price pressures are still benign, but if inflation were to suddenly rise beyond the Fed’s 2% target, the Fed would become more vigilant.

While the Fed believes some inflation is a sign of a healthy economy, they do not want rampant inflation and the associated economic consternation resulting from significantly higher interest rates. Given the enormous debt burden of the U.S. government, corporations, and households, the impact of higher inflation and higher interest rates, is much greater now than at any time in history.

Despite their recent posture of patience and gradualism, if traditional measures of inflation were to move abruptly higher, the Fed will likely react with a more hawkish tone and likely raise Fed Funds rate and resume plans to reduce their balance sheet. While the intention would be to reverse inflationary pressures, the result may be to stoke them further. Monetary velocity will become an important data point to follow to gain insight on how Fed actions might affect prices.

Given the financial market’s dependence on an accommodative Fed and low interest rates, such actions would likely reverse the asset price inflation witnessed since 2009 when the Fed began conducting such extraordinary monetary policy.

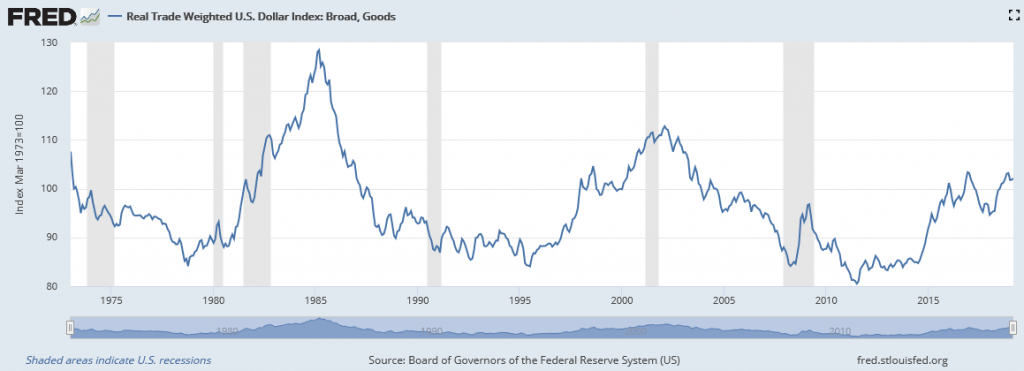

U.S. Dollar

The other factor allowing the Fed to maintain such extraordinary monetary policy is the relative stability of the U.S. Dollar. Following the double-digit inflation of the 1970s and the Fed’s drastic actions to bring it down, the dollar index rose dramatically as shown below. Upon peaking in 1985, the dollar eventually traded back to the low levels seen during the high inflation era of the late 1970s. Since that time, the dollar has been relatively stable.

As illustrated in the graph, one can spot weakness leading up to the 2008 crisis, but the dollar has since recovered. Somewhat counter-intuitively, the dollar has strengthened since 2011 despite the Fed printing money on an unprecedented scale. The reason lies in the way the value of the dollar is portrayed. The dollar index is essentially a weighted index based on cross-currency exchange rates between many of our largest trade partners. While the U.S. printed money, many other countries were following suit and the dollar was able to maintain its relative value.

Some of the recent strength in the dollar lies in the fact that QE has ended in the U.S. while it continues aggressively in many other developed nations. Furthermore, the Fed has been gradually raising interest rates and reducing the size of its balance sheet. These actions are currently on hold, but nonetheless, the Fed still has a more hawkish stance than most other developed nations.

A weak dollar has two major effects. U.S. exports increase as dollar-based goods are cheaper outside of the U.S., and goods imported into the U.S. from other countries become more expensive. As a net importing country, the net effect in the U.S. of the two factors above should be higher inflation. Additionally, a weak dollar bodes poorly for foreign investments in the U.S. Over 40% of publicly traded government bonds are held by foreigners, and a sizeable share of private lending/investment is done by foreign entities as well. When the dollar declines versus the domestic currency of the foreign entity, the value of these investments declines. This, in turn, makes further investment less likely and raises the possibility that current holdings might be liquidated.

For a country that is overly reliant on debt and needs to fund current consumption and the debts of years past, a weaker dollar is a big problem. Thus, it is likely the Fed would want to prop up the dollar in the event of significant weakness. In an inflationary environment, this would be accomplished through a higher Fed Funds rate, a reduced balance sheet and Fed rhetoric, all of which would likely be troubling for risk assets.

Summary

As we mentioned, the Fed Put is dependent upon an unspoken pact and high level of trust with investors. Investors will push markets higher and take on substantial risk in exchange for the implied protection of the Federal Reserve. Today, in the wake of the Fed’s most recent policy reversal based on weak stock prices, investor trust in the Fed is seemingly greater than ever. Although there has been a great deal of turnover among Fed members, there is currently little reason to suspect the Fed will change their methods or that investors will question the Fed’s intent.

In an economy transitioning from an ultra-easy policy stance to one less so, high inflation and/or pronounced dollar weakness can happen suddenly eliciting a more severe response from the Fed. If they are unable to effectively navigate the narrow path between accommodation and inflation vigilance, the trust in the Fed that is driving markets could disappear quickly.

With so many events converging to introduce new uncertainty into the economy, the stability of markets that investors have enjoyed and faith in the Fed seems very much in jeopardy.

via ZeroHedge News http://bit.ly/2IK7g23 Tyler Durden

I’m not used to seeing the government offer taxpayers a win/win.

But a little known provision snuck into Trump’s 2017 tax reform law is possibly the best tax-advantaged investment strategy offered in decades. And it will help some of the poorest areas of the US too.

It’s the brainchild of Sean Parker, the founder of Napster and the first major investor in Facebook.

Traveling in Tanzania, he realized none of the $2 billion worth of aid flowing into the country each year reached certain poor areas.

And he noticed something similar about the US, in the poor neighborhoods of San Francisco.

Here all his Silicon Valley buddies were sitting on record high gains in almost every asset class after a decade bull run. But they had no incentive to collect their gains, and invest them in the areas that needed it most.

The solution was Opportunity Zones.

It’s a win-win scenario. You get an amazing tax deal, while helping to solve the income disparity in the US.

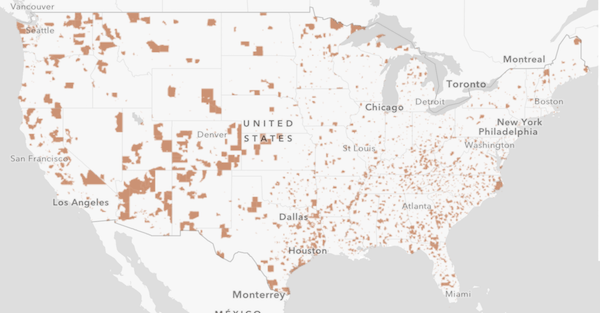

The legislation allowed states to designate “Opportunity Zones” in almost 9,000 distressed communities across the USA. These are areas with high poverty and unemployment.

Here’s how this opportunity works…

1. You sell your asset, and realize an initial capital gain (from stocks, bonds, crypto, real estate, gold, art or most anything else).

2. Within 180 days, you invest some or all of your gains into an Opportunity Zone Fund.

3. You defer paying tax on the initial capital gain until Dec 31, 2026. If you’ve held it for seven years, you get a 15% discount on that tax.

(Tax deferral allows you to delay paying taxes so your money can compound at a substantially higher rate.)

4. The Opportunity Zone Fund invests in an Opportunity Zone (it can buy an existing business, start a new business or even buy real estate).

5. If you hold that investment for 10 years, any capital gains you earn from the Opportunity Zone Fund are TAX FREE.

The rules are simple, and the funds are flexible.

But there will never be a better time than now to take advantage of Opportunity Zones.

The first reason is the simple math. You can only defer the capital gains tax until December 31, 2026.

That’s just seven years away, and you need to hold the Opportunity Zone investment for seven years to get the full 15% discount on your original capital gains tax. That means you need to realize and re-invest your gains by the end of 2019.

You’ll still get a 10% discount on your original capital gains tax if you hold the new investment for five years. So, in theory, you could take advantage of that up until the end of 2021…

But by then it might be too late…

That’s because the Bolsheviks are coming. And they hate this.

A few months ago, Amazon backed out of a plan to locate it’s second headquarters in New York City. The spot they picked to build HQ2, inject billions of dollars, and provide thousands of jobs, was inside an Opportunity Zone.

But all the benefits to NYC wasn’t enough for the Bolsheviks led by Alexandra Ocasio-Cortez. Amazon was still going to get some benefit from the deal.

It was a win-win, and the Bolsheviks are only interested in winning when the other guy loses. So they contented themselves with a lose-lose deal. And that’s what they have in store for all of America if they rise to power.

All the major 2020 Presidential candidates are clamoring to promise the highest taxes, the biggest wealth redistribution, the most assets confiscated.

But Bolsheviks threaten more than just Opportunity Zones.

People that chase away investments, demonize wealth, and raise taxes do not inspire confidence in the markets.

More likely they’ll crash the market, as everyone tries to sell before the tax rates are jacked up.

But even if the Bolsheviks don’t take power, market cycles only last for so long. Right now, we’re in an everything bubble, the longest bull market in history, with stock prices just about at all time highs.

No one has a crystal ball, but it can’t last forever.

Why not lock in these gains while asset prices are at all time highs?

It’s hard to imagine you’ll be worse off parking those gains in this extraordinary tax-advantaged vehicle. Gains that you can continue to invest tax-free.

But if you fast forward two years from now, you might be kicking yourself if the Bolsheviks come to power, collapse the market, and eliminate this tax opportunity.

There’s not really much downside here. It is definitely worth talking to your tax advisor or financial manager about.

We’ve already detailed Opportunity Zones for our premium Sovereign Man: Confidential members.

But because this is such an incredible opportunity, we’re releasing a redacted preview to all of our readers.

The Department of Justice has been dismissing child pornography cases in order to not reveal information about the software programs used as the basis for the charges.

An array of cases suggest serious problems with the tech tools used by federal authorities. But the private entities who developed these tools won’t submit them for independent inspection or hand over hardly any information about how they work, their error rates, or other critical information. As a result, potentially innocent people are being smeared as pedophiles and prosecuted as child porn collectors, while potentially guilty people are going free so these companies can protect “trade secrets.”

The situation suggests some of the many problems that can arise around public-private partnerships in catching criminals and the secretive digital surveillance software that it entails (software that’s being employed for far more than catching child predators).

With the child pornography cases, “the defendants are hardly the most sympathetic,” notes Tim Cushing at Techdirt. Yet that’s all the more reason why the government’s antics here are disturbing. Either the feds initially brought bad cases against people whom they just didn’t think would fight back, or they’re willing to let bad behavior go rather than face some public scrutiny.

An extensive investigation by ProPublica “found more than a dozen cases since 2011 that were dismissed either because of challenges to the software’s findings, or the refusal by the government or the maker to share the computer programs with defense attorneys, or both,” writes Jack Gillum. Many more cases raised issues with the software as a defense.

“Defense attorneys have long complained that the government’s secrecy claims may hamstring suspects seeking to prove that the software wrongly identified them,” notes Gillum. “But the growing success of their counterattack is also raising concerns that, by questioning the software used by investigators, some who trade in child pornography can avoid punishment.”

Courts have sought to overcome concerns that scrutiny would diminish the effectiveness of the software for law enforcement or infringe on intellectual property rights by ordering only secret and monitored third-party review processes. But federal prosecutors have rejected even these compromises, drawing worry that it’s not legitimate concerns driving their secrecy but a lack of confidence in the software’s efficacy or some other more nefarious reason.

Human Rights Watch (HRW) has raised questions about how much data (not just on defendants but on all Americans) these programs have been accessing and storing.

In February, HRW sent a letter to Justice Department officials expressing concerns about one such program, called the Child Protection System (CPS). TLO, the company behind the CPS system, has intervened in court cases to prevent disclosure of more information about the program or independent testing of it.

“Since the system is designed to flag people as suspected of having committed crimes, both its error rates and its potential to exceed constitutional bounds have implications for rights,” HRW states. Yet “it is unclear what information the Justice Department has about CPS’ potential for error (and on what basis).”

Prosecutors say they can’t share any details about it “because it is proprietary and not in the government’s possession,” notes HRW, which since 2016 has been researching cases involving the CPS system. “We fear that the government may be shielding its methods from scrutiny by relying on its arrangements with the non-profit,” states HRW. (Read more here.)

Another tool used in these cases, Torrential Downpour, was developed by the University of Massachusetts. The school has been fighting against the release of more information about Torrential Downpour, too. But defendants’ lawyers say it’s necessary after the program alerted authorities about alleged child porn on computers that couldn’t actually be found anywhere on the physical devices.

“An examination of the software being used to build cases should be allowed, but the entities behind the software won’t allow it and the government is cutting defendants loose rather than giving them a chance to properly defend themselves against these very serious charges,” writes Cushing. “I supposed it ultimately works out for defendants, but it only encourages the government to tip the scales in its favor again when the next prosecution rolls around with the hopes the next defender of the accused isn’t quite as zealous”

Plus, if these defendants really are innocent, than the government has publicly and falsely smeared them as sickos and then balked at allowing them a true opportunity to clear their names.

“These defendants are not very popular, but a dangerous precedent is a dangerous precedent that affects everyone,” HRW’s Sarah St.Vincent told ProPublica. “And if the government drops cases or some charges to avoid scrutiny of the software, that could prevent victims from getting justice consistently. The government is effectively asserting sweeping surveillance powers but is then hiding from the courts what the software did and how it worked.”

from Latest – Reason.com http://bit.ly/2W6SKEy

via IFTTT

The Department of Justice has been dismissing child pornography cases in order to not reveal information about the software programs used as the basis for the charges.

An array of cases suggest serious problems with the tech tools used by federal authorities. But the private entities who developed these tools won’t submit them for independent inspection or hand over hardly any information about how they work, their error rates, or other critical information. As a result, potentially innocent people are being smeared as pedophiles and prosecuted as child porn collectors, while potentially guilty people are going free so these companies can protect “trade secrets.”

The situation suggests some of the many problems that can arise around public-private partnerships in catching criminals and the secretive digital surveillance software that it entails (software that’s being employed for far more than catching child predators).

With the child pornography cases, “the defendants are hardly the most sympathetic,” notes Tim Cushing at Techdirt. Yet that’s all the more reason why the government’s antics here are disturbing. Either the feds initially brought bad cases against people whom they just didn’t think would fight back, or they’re willing to let bad behavior go rather than face some public scrutiny.

An extensive investigation by ProPublica “found more than a dozen cases since 2011 that were dismissed either because of challenges to the software’s findings, or the refusal by the government or the maker to share the computer programs with defense attorneys, or both,” writes Jack Gillum. Many more cases raised issues with the software as a defense.

“Defense attorneys have long complained that the government’s secrecy claims may hamstring suspects seeking to prove that the software wrongly identified them,” notes Gillum. “But the growing success of their counterattack is also raising concerns that, by questioning the software used by investigators, some who trade in child pornography can avoid punishment.”

Courts have sought to overcome concerns that scrutiny would diminish the effectiveness of the software for law enforcement or infringe on intellectual property rights by ordering only secret and monitored third-party review processes. But federal prosecutors have rejected even these compromises, drawing worry that it’s not legitimate concerns driving their secrecy but a lack of confidence in the software’s efficacy or some other more nefarious reason.

Human Rights Watch (HRW) has raised questions about how much data (not just on defendants but on all Americans) these programs have been accessing and storing.

In February, HRW sent a letter to Justice Department officials expressing concerns about one such program, called the Child Protection System (CPS). TLO, the company behind the CPS system, has intervened in court cases to prevent disclosure of more information about the program or independent testing of it.

“Since the system is designed to flag people as suspected of having committed crimes, both its error rates and its potential to exceed constitutional bounds have implications for rights,” HRW states. Yet “it is unclear what information the Justice Department has about CPS’ potential for error (and on what basis).”

Prosecutors say they can’t share any details about it “because it is proprietary and not in the government’s possession,” notes HRW, which since 2016 has been researching cases involving the CPS system. “We fear that the government may be shielding its methods from scrutiny by relying on its arrangements with the non-profit,” states HRW. (Read more here.)

Another tool used in these cases, Torrential Downpour, was developed by the University of Massachusetts. The school has been fighting against the release of more information about Torrential Downpour, too. But defendants’ lawyers say it’s necessary after the program alerted authorities about alleged child porn on computers that couldn’t actually be found anywhere on the physical devices.

“An examination of the software being used to build cases should be allowed, but the entities behind the software won’t allow it and the government is cutting defendants loose rather than giving them a chance to properly defend themselves against these very serious charges,” writes Cushing. “I supposed it ultimately works out for defendants, but it only encourages the government to tip the scales in its favor again when the next prosecution rolls around with the hopes the next defender of the accused isn’t quite as zealous”

Plus, if these defendants really are innocent, than the government has publicly and falsely smeared them as sickos and then balked at allowing them a true opportunity to clear their names.

“These defendants are not very popular, but a dangerous precedent is a dangerous precedent that affects everyone,” HRW’s Sarah St.Vincent told ProPublica. “And if the government drops cases or some charges to avoid scrutiny of the software, that could prevent victims from getting justice consistently. The government is effectively asserting sweeping surveillance powers but is then hiding from the courts what the software did and how it worked.”

from Latest – Reason.com http://bit.ly/2W6SKEy

via IFTTT

A University of Southern California assistant women’s soccer coach embroiled in the college admissions scandal will plead guilty and cooperate with prosecutors, according to the Wall Street Journal. Former coach Laura Janke will plead to one count of racketeering conspiracy by May 30 and, as a result, will forfeit $134,000 and likely receive the “low end” of potential jail time. She has also reportedly agreed to cooperate with prosecutors in the case, according to plea and cooperation agreements filed in court.

The maximum sentence she was facing was 20 years, but it is likely she will now get 27 to 33 months as a result of the plea. She’ll also be on supervised release for a term of 12 months. Janke must also pay any tax penalties related to payments she received. The length of her prison sentence is still going to be determined on how cooperative she is going to be as a witness, prosecutors said.

Janke

Another parent who worked with Janke also accepted a plea deal recently: Toby MacFarlane, a parent charged in the case, will plead guilty to one count of conspiracy to commit mail fraud and honest services mail fraud, according to the U.S. Attorney’s Office in Massachusetts. MacFarlane had already telegraphed his intent earlier this month to enter into plea discussions.

MacFarlane paid $450,000 to have his children admitted to USC as recruited athletes and, working with Janke, helped create fake profiles for the children. Janke then built profiles for both of MacFarlane’s kids: one for his daughter in 2013 claiming she was a soccer star and another in 2017 for his son, claiming he was a basketball player. Both children eventually wound up going to USC.

Janke was one of four USC officials charged in the case. Prosecutors say she created profiles for a number of William Rick Singer’s clients, stocking them with fake honors for their respective sports.

In another example, Janke helped fabricate a bogus athletic profile for the son of media executive Elisabeth Kimmel as an elite pole vaulter, despite him having no record of ever pole vaulting. Janke even used a photo of another individual pole vaulting as part of the submission, prosecutors say. Kimmel has plead not guilty to charges of mail fraud conspiracy and money laundering conspiracy.

Kimmel

Janke’s guilty plea stands in contrast with our latest update on the scandal, where we noted that some parents had decided to “punch back” and vigorously defend themselves in court.

“I expect a lot more guilty pleas,” Diane Ferrone, a criminal defense lawyer in New York who isn’t involved in the case, told Bloomberg about a week ago.

16 parents were recently indicted in the scandal about 2 weeks ago. Several weeks before that, we noted that parents charged in the scheme were seeking out “prison life consultants” to find out what life would be like in the big house.

We have been following the admissions scandal at length. As part of our coverage, we detailed how financial speaking gigs and elite high schools helped facilitate the scam for years. We’ve also covered the fallout from the scandal, like when UCLA’s Men’s Soccer Coach and former U.S. Men’s national team player Jorge Salcedo recently resigned from his position at the university as a result of taking bribes. We also wrote about how students were being encouraged to fake learning disabilities in order to cheat on college entrance exams.

We profiled Harvard test taking whiz Marc Riddell, who was a key piece of the scam, in March. Prior to that, we also reported on the tipster who gave the SEC the lead on the admissions scandal.

via ZeroHedge News http://bit.ly/2DwKq9U Tyler Durden

High school seniors in suburban Columbus, Ohio, get to take a class that could well be banned on many college campuses: a political science course where speakers from the most radical groups—from neo-Nazis to die-hard communists—are invited to present their views and answer questions.

Thomas Worthington High School has offered “U.S. Political Thought and Radicalism,” or “Poli-Rad,” since 1975. That’s the year teacher Tom Molnar, now retired, came up with the idea for the class, got it approved, and then realized there was no textbook on the topic. A student suggested he invite guest speakers from across the political spectrum, and that’s what Molnar did. (It’s notable that back then, the principal not only approved this idea, he called it “brilliant.”) Now the school’s newer sister school, Worthington Kilbourne High School, offers the class too.

Over the years, the speakers have included Bill Ayers of the Weather Underground (“Don’t be stupid like me when I was younger,” he told the class), white supremacist Richard Spencer, and Ramona Africa, sole survivor of the bomb police dropped on MOVE, the headquarters of the black (and animal) liberation organization to which she belonged.

Today about half of all seniors take the class, which involves reading up on the 20 or so speakers before they arrive, then listening and asking questions. WCMH-TV listed the questions the students are asked to focus on, which include: Why do people become part of these movements? Why do they choose the tactics they do? What are their goals?

Judi Galasso, who co-teaches the class today, told Julie Carr Smyth of the Associated Press that, “In 2019, no school board in America would approve a class like this, but in Worthington, there’s no way you could get rid of it.” The school’s principal, Pete Scully, told Smyth, “In 2019, our teachers generally are like, ‘You know what? Let’s redirect to a different topic, because that one sounds like it’s loaded with land mines. The idea of poli-rad is, you know what, let’s explore all those land mines and talk about them.”

Unlike some college professors, who find themselves unable to discuss a controversial topic without being accused of endorsing it, at Worthington there seems to be a solid understanding that there is a difference between studying radicalization and actually radicalizing students. In fact, the idea of “Let’s explore all those landmines” is probably the most radical idea to which the kids are being exposed.

The students—past and present—seem grateful for this, as well as for their school’s trust that they could handle it. As the AP reports:

Senior Tori Banks, 18, who took the course last semester, said it helped her expand her views and learn tolerance.

“If I weren’t in the class and I saw some of these speakers or people of certain stances walking around, I may feel uncomfortable,” she said. “But I think the way we do it in poli-rad is a very safe environment.”

Normally, calling a class a “safe environment” is a ridiculous overstatement. It implies that somehow other classes or venues are unsafe, simply because students will be hearing ideas that they disagree with or that make them uncomfortable.

But in Worthington’s case, the “safe” term is earned. The students aren’t hearing a white supremacist at a rally in Charlottesville, and they aren’t bunking with the MOVE folks in Philly.

What they are getting instead is the chance to hear from an array of speakers outside the mainstream, as well as the ever-more-rare chance to be treated as thoughtful humans who can grapple with ideas and people they disagree with, and not be harmed in the process.

As student Jonathan Conrad wrote in the school paper in 2016, the class “not only gives students an opportunity to hear major figures from all sides of the political spectrum, but it also gives students the opportunity to form their own beliefs away from parental influence.”

Let’s hope he gets some more of that at college.

from Latest – Reason.com http://bit.ly/2XGTVec

via IFTTT

Lately there’s been a ton of talk about Modern Monetary Theory. Most of it critical. MMT seems to evoke a visceral gagging reflex from most finance-types, kind of like that feeling when your inappropriate uncle makes a lewd joke about your aunt.

However, I have been fascinated by the subject. And no one is more surprised by that fact than me. Although I am an economics major, if you would have suggested spending hours listening to a neo-classical economics professor drone on about the virtues of some DSGE model, I would have told you I would rather lick subway handrails. Yet over the past month I have spent tens of hours listening to a variety of MMT professors’ lectures.

The reason? MMT explains many of the current conundrums vexing traditional economic theory.

Now, now – before you click delete on the rest of my post, hear me out.

After thinking about the problems that the majority seem to have accepting MMT, I have concluded it best to divide MMT up into two components. One is the descriptive theory on how things are. This part deals with debt flows, banking reserves, etc… It describes the way a modern economy works. The next part is the prescriptive part of MMT. After understanding how an economy operates, many MMT advocates have policy recommendations. The important thing to understand about these choices is that they are political decisions based on economic theory. One might disagree with these courses of action, but it doesn’t change the first part – the descriptive part of MMT.

I am dividing my article into two posts. Today’s installment will focus on how to use MMT in today’s world. It will examine if the descriptive part can help us with trades in the current environment. Tomorrow’s post will delve into the ramifications for the markets if the prescriptive portion of MMT is adopted.

So let’s get on with it!

Using MMT in today’s market environment

I am often told “gee it’s great that you (kinda) understand MMT, so if it ever gets implemented, you will be way ahead of the curve.” I think that’s selling MMT short.

There are plenty of practical applications for MMT in today’s market environment.

Ever wonder why the three rounds of quantitative easing by the Federal Reserve didn’t cause the CPI increases the hyper-inflationists warned about? Or why Europe’s continued extreme monetary policy has failed to lift their economy? Or my favourite – why Japan’s debt-to-GDP ratio of 250% hasn’t caused an incendiary inflationary currency collapse?

Although neo-classical economists have been at a loss to forecast these economic realities, these perplexing outcomes are easily explained using MMT.

But before we examine the trading applications of MMT, let’s back up and think about the theory.

My MMT break through moment

During one of my early MMT-lecture marathons, Professor Stephanie Kelton explained that the government spent first and borrowed second. This didn’t seem correct and I couldn’t square it in my mind. Surely the government can’t spend without first borrowing. How do they spend money they don’t have? I thought this might be the beginnings of MMT-induced hallucinations, but I decided to press on.

Then Stephanie made it even more complicated by asserting the government need not borrow at all – the concept that they needed to issue bonds was a purely self imposed restraint.

At this point my mind was spinning. I grabbed hold of the bed frame hoping to slow down this terrible ride. It was like learning that WWE wrestling wasn’t real. It completely blew my mind and made me question all my assumptions about how an economy works.

After some time trying to process this new reality, I eventually figured out that this spending would be inflationary.

But that’s the whole point!

MMT’ers believe there is no financial constraint but only a real resource limit (subject to certain restrictions – only for sovereign countries who issue their own debt and don’t have a pegged currency, yada yada yada). In essence, inflation is the real limiting factor.

At this point you are probably saying that sounds a little like a ponzi scheme. How can a government spend without there being repercussions?

Well, no MMT practitioner would ever claim there are no consequences to government spending, it’s just that this spending is not limited by the ability of the government to borrow.

Still don’t believe me? Let’s think about war. Why is there always money for war?

Do you think that after the Japanese bombed Pearl Harbor the United States government went to the bond market to borrow money to build back their navy? And do you think that if the bond market had not provided those funds the United States government would have said, “sorry – we really want to enter the war, but we will have to wait until market conditions allow us to finance our deficit spending.”

Of course you don’t. The government spent first and did not worry about borrowing.

But wait, the history buffs will say, “there were war bonds, so MacroTourist – you are wrong”.

Well, let’s think about this bond issuance within the confines of MMT theory. The government did not issue war bonds to finance the spending, but to alter the private sector’s behaviour. Recall, the only constraint is in real terms. The government did not want individuals competing by buying goods that were needed in the war. So the government issued War Bonds to change their spending not to finance the war.

The important thing to realize is that governments always spend first and that bond issuance is simply a way of controlling inflation and altering private sector behaviour.

Ok great, maybe you buy that argument, but it still doesn’t help in trading today’s market.

Yet it does. In fact, it changes everything.

First trade – Japan

Let’s take the poster-child for today’s growth-starved world – Japan. They were the first major economy to engage in quantitative easing and the amount of debt they have racked up is mind-blowing.

Over the years (actually it’s been more than a decade now) there’s been all sorts of doomsday predictions from high-profile hedge fund managers about how it will all come tumbling down in a terrible inflationary collapse. And yeah, there is no denying, I fell for this storyline harder than for Halle Berry in a Bond movie.

But over the past few years there’s been a little part of me that wonders why all these dire predictions have failed to materialize. The skeptics will say the debt burden will eventually catch up with Japan and that you can’t borrow your way to prosperity. Yeah, yeah. I get it. I know all the arguments because I once made them myself.

However, the first seeds of doubt about this theory were sown well before I had ever heard of MMT.

Back in 2017, there were two terrific interviews on Real Vision with Bill Fleckenstein and David Zervos. Fleck’s piece was titled, “Japanese Debt Wipeout can they get away with it?” (subscription required). It was transforming as it made me question everything I thought I understood about the Japanese endgame. And then David Zervos followed it up with “Deregulation & Debt Jubilees” (again subscription required).

Although there were subtle differences in their opinions, both Bill and David introduced the concept that maybe the Bank of Japan would simply tear up all the JGBs it owned and start over.

I can hear the groans again. You can’t just tear up debt. It doesn’t work that way!

Really?

The BoJ owns approximately 43% of the outstanding Japanese government debt.

That debt is sitting on their balance sheet and since interest rates are basically zero, it’s not doing much. The Japanese government issued that debt and then the Bank of Japan bought it back. It nets out to a zero between the two entities. We could have avoided the Japanese broker middlemen if the government had just spent the money and never bothered with the steps in between.

Wait, wait, wait…

Remember back to Stephanie’s comment that the government could spend money it doesn’t have and it didn’t even need to issue bonds? Well, in essence this is what the Japanese government is doing. Why bother issuing debt to only have the BoJ buy it back? Why not just spend the money and avoid the hocus-pocus in the middle?

Think back to the pushback you had about the government spending money directly. You probably thought it would cause hyper-inflation.

Yet where is the hyper-inflation in Japan?

Apart from a spike when the government raised the value-added tax rate, inflation has struggled in Japan. In fact, they have had more of a problem with deflation than inflation.

So even though the Japanese are running a deficit of between 3% and 4% of GDP with a debt-to-GDP of 250%, and then basically monetizing approximately half of that spending through quantitative easing, they still can’t hit their inflation target.

Which brings me to a comment made by Bill Mitchell – one of the core members in the group of founding MMT professors – and I am paraphrasing here, but he said something to the effect that there are different levels of deficits required for different economies. So whereas in Japan they might need a deficit of 10% of GDP to take up the resource slack, in another country, 1% surplus might be inflationary. It all depends on the external account and other macroeconomic factors.

But let’s go back to how this helps in our trading in today’s market. Bill Fleckenstein and David Zervos argued that a debt jubilee in Japan might not be as catastrophic as many predict. Their argument basically boils down to “the BoJ already owns the debt anyway, so it’s really just an accounting entry – from the BoJ to the Japanese government. Ripping up the bonds held on the BoJ balance sheet would have no real change to the economic situation. The currency would probably fall, but then foreigners might look at the circumstances and decide that with the Yen at 150 or 180 or 200, Japan is on sale. The real productive assets of Japan would have not changed, so they would buy Japan. Also, the new lower currency would be a boon for exports and the Japanese economy might take off.”

This was ground breaking to me. It showed originality in their thinking. And I suggest you watch both interviews in their entirety – I believe them to be that important.

However, after spending the last couple of months immersing myself in MMT theory, I have come to the conclusion that maybe even Bill and David are overestimating the effects of a Japanese debt jubilee. Let’s imagine for a second that the BoJ has already ripped up the JGBs it holds in secret behind closed doors. Would anything have changed in the real economy? I contend that no, nothing would have changed in the slightest. Therefore in my mind, whether they rip them up or not doesn’t matter.

The only real change would be that suddenly the Japanese government would have a lot more “perceived” room to spend. This ability to spend would be construed as inflationary by the market and therefore asset prices might change in anticipation of future policy changes.

I am not denying that markets would be confused by a Bank of Japan debt jubilee. Don’t forget all the hyperbolic warnings in the advent of the first US quantitative easing program, and then the continued end-of-the-world predictions in the second and third QE programs. The markets took quite a while to sort out the true ramifications of these policies. If Japan went down their debt jubilee road, there would be even more dire warnings emanating from the neo-classical and Austrian economic community.

But remember – the only thing that is actually inflationary is government policy changes going forward. Otherwise, the inflation has already been felt when the deficit was created.

Now what does this mean for trades today? Well, if you have been betting on Japan collapsing because of its high debt-to-GDP ratio, I humbly suggest you are looking at the wrong metric.

The only reason the current high debt-to-GDP ratio hampers the economy is because it influences government policy. If the Fleck/Zervos debt jubilee comes closer to reality, I would view any sell off in the Yen as a chance to buy Japan on sale.

But more importantly, maybe the high debt ratios are suppressing global equity managers allocation to Japan. Maybe they have been reluctant to invest in Japan in fear of a Japanese collapse. And yet, maybe it’s not coming and all their fear does is provide a great long term entry into Japanese equities by keeping them underpriced versus the rest of the world.

Next trade – Europe

Now that we understand the basics of MMT theory, let’s apply them to Europe. Remember that different economies require different levels of fiscal deficits. It’s not that MMT theory advocates that governments should always spend, but it does conclude it is foolish to administer increasing amounts of monetary stimulus in an attempt to kickstart an economy.

MMT’ers argue that the policy prescription of extremely accommodative monetary policy while insisting on fiscal austerity is a recipe for a moribund economy. Yet this is exactly what Europe is insisting to be the solution to their problem.

Before understanding the way a modern economy works, I was in the Bill Gross camp that the easy money in Europe would eventually cause the German bund to be the short of a lifetime. Now I have a little better idea about the timing of that trade.

I no longer believe there is any sense in being positioned for a secular short in bunds until we see Germany change their allowance for Europe to run government deficits. Italy is being chastised for trying to run a deficit of 2.5% of GDP, yet the United States is running more than 4%.

You might argue that Italy and the United States are completely different and that Germany is correct to insist on fiscal austerity throughout Europe. That’s a political decision with economic implications.

Regardless of whether I believe this policy prescription to be right or wrong, I am firmly convinced it will mean chronic poor economic performance in Europe. Therefore, avoid European equities and don’t short bunds until this changes.

Will there be tradeable rallies in European equities? For sure. But don’t get too bullish until European officials change their tune.

Final trade – United States

I wrote a piece titled “Trump: The first MMT President” where I outlined all the reasons the President’s policies were much more MMT-like than any on the right would care to admit.

I even saw a Vice-President Pence interview the other day where they asked him why the administration was pushing for lower rates if the economy was as strong as they bragged. His reply was quintessential MMT. Pence said, “because there is no inflation.”

As long as President Trump’s administration continues with their policies, then I suspect the United States economy will continue to outperform.

Now there are always many moving parts, but the United States’ economic policies are the best example of MMT at work. You might not like them. You might think tax cuts are not the best use of fiscal stimulus. Again, those are political considerations.

Knowing how modern economies work explains why America has outperformed Europe since the Great Financial Crisis, and although there are other secular influences also at work, don’t assume this trend will change until you see a shift in attitudes in either country regarding deficits and spending.

Summing it up

The majority of you will most likely still not be MMT converts. I get it. It’s difficult to accept the move from neo-classical or Austrian economics.

I would like to reaffirm one point. There are two parts to MMT; how the modern fiat-based economy works and then the policies that are advocated to maximize output under these conditions.

You might not like the political parts of MMT. I am not trying to convert anyone. Nothing is more annoying than when your best friend discovers some keto-diet and spends all day extolling its benefits.

But I will let you in on a little secret. When I wrote my original MMT piece – “Everything you wanted to know about MMT (but were afraid to ask)”, I was shocked by the individuals who reached out to me. Really impressive people who had spent time examining MMT and concluded that it was extremely useful in their analytical thinking. They sent me papers they had written, notes they had taken from their meetings with these MMT professors and analysis they had created in their attempt to better understand the modern economy and markets. The quality of these people and their thinking astounded me.

It’s easy to dismiss MMT as the ravings of the far-left, but if you do so, you are mixing economics with politics. MMT theory is extremely useful in understanding how the economy actually works. You might not like it. You might wish it were different. But I think the hallmark of a great trader/investor is to stay open-minded. In that vein, I think the MMT framework is a most useful tool for macro trading.

When Nixon went off the gold standard, economics changed. Yet all the textbooks are still based on this neo-classical economic thinking. Understanding that the old economic concepts no longer work and the current situation is much different, helps in accepting that MMT does a much better job at explaining today’s realities than any other framework.

So yeah, I guess I am proud to say that I think MMT is an extremely valuable tool. You might scoff at that idea. You might write me off as some wingnut. But just remember, I still like the Indy 500.

via ZeroHedge News http://bit.ly/2GzDfyp Tyler Durden

High school seniors in suburban Columbus, Ohio, get to take a class that could well be banned on many college campuses: a political science course where speakers from the most radical groups—from neo-Nazis to die-hard communists—are invited to present their views and answer questions.

Thomas Worthington High School has offered “U.S. Political Thought and Radicalism,” or “Poli-Rad,” since 1975. That’s the year teacher Tom Molnar, now retired, came up with the idea for the class, got it approved, and then realized there was no textbook on the topic. A student suggested he invite guest speakers from across the political spectrum, and that’s what Molnar did. (It’s notable that back then, the principal not only approved this idea, he called it “brilliant.”) Now the school’s newer sister school, Worthington Kilbourne High School, offers the class too.

Over the years, the speakers have included Bill Ayers of the Weather Underground (“Don’t be stupid like me when I was younger,” he told the class), white supremacist Richard Spencer, and Ramona Africa, sole survivor of the bomb police dropped on MOVE, the headquarters of the black (and animal) liberation organization to which she belonged.

Today about half of all seniors take the class, which involves reading up on the 20 or so speakers before they arrive, then listening and asking questions. WCMH-TV listed the questions the students are asked to focus on, which include: Why do people become part of these movements? Why do they choose the tactics they do? What are their goals?

Judi Galasso, who co-teaches the class today, told Julie Carr Smyth of the Associated Press that, “In 2019, no school board in America would approve a class like this, but in Worthington, there’s no way you could get rid of it.” The school’s principal, Pete Scully, told Smyth, “In 2019, our teachers generally are like, ‘You know what? Let’s redirect to a different topic, because that one sounds like it’s loaded with land mines. The idea of poli-rad is, you know what, let’s explore all those land mines and talk about them.”

Unlike some college professors, who find themselves unable to discuss a controversial topic without being accused of endorsing it, at Worthington there seems to be a solid understanding that there is a difference between studying radicalization and actually radicalizing students. In fact, the idea of “Let’s explore all those landmines” is probably the most radical idea to which the kids are being exposed.

The students—past and present—seem grateful for this, as well as for their school’s trust that they could handle it. As the AP reports:

Senior Tori Banks, 18, who took the course last semester, said it helped her expand her views and learn tolerance.

“If I weren’t in the class and I saw some of these speakers or people of certain stances walking around, I may feel uncomfortable,” she said. “But I think the way we do it in poli-rad is a very safe environment.”

Normally, calling a class a “safe environment” is a ridiculous overstatement. It implies that somehow other classes or venues are unsafe, simply because students will be hearing ideas that they disagree with or that make them uncomfortable.

But in Worthington’s case, the “safe” term is earned. The students aren’t hearing a white supremacist at a rally in Charlottesville, and they aren’t bunking with the MOVE folks in Philly.

What they are getting instead is the chance to hear from an array of speakers outside the mainstream, as well as the ever-more-rare chance to be treated as thoughtful humans who can grapple with ideas and people they disagree with, and not be harmed in the process.

As student Jonathan Conrad wrote in the school paper in 2016, the class “not only gives students an opportunity to hear major figures from all sides of the political spectrum, but it also gives students the opportunity to form their own beliefs away from parental influence.”

Let’s hope he gets some more of that at college.

from Latest – Reason.com http://bit.ly/2XGTVec

via IFTTT

{kind=link}

{kind=link}