On Friday, a unanimous panel of the U.S. Court of Appeals for the D.C. Circuit ordered Blumenthal v. Trumpdismissed for lack of Article III jurisdiction. In a brief, per curiam opinion, Judges Henderson, Tatel, and Griffith concluded that members of Congress lacked standing to sue President Trump over alleged violations of the Foreign Emoluments Clause. Individual members of Congress, they explained, lack standing to sue the President over alleged legal violations.

In Blumenthal, some 215 Members of Congress alleged that the President’s alleged violations of the Emoluments Clause deprived them of the opportunity to vote on whether the receipt of such emoluments was permissible, as anticipated by the text of the clause. The D.C. district court bought this argument and, more surprisingly, refused to allow an interlocutory appeal, prompting a rebuke from the D.C. Circuit.

In Friday’s decision, the D.C. Circuit panel explained that this suit was clearly barred by existing Supreme Court precedent, Raines v. Byrdin particular. In Raines, the Supreme Court concluded that individual members of Congress lacked standing to challenge the constitutionality of the Line-Item Veto Act. In Blumenthal, the D.C. Circuit recognized plaintiffs’ efforts to argue around Raines were completely unavailing, particularly in light of subsequent decisions.

The Supreme Court’s recent summary reading of Raines that “individual members” of the Congress “lack standing to assert the institutional interests of a legislature” in the same way “a single House of a bicameral legislature lacks capacity to assert interests belonging to the legislature as a whole,” Va. House of Delegates v. Bethune-Hill, 139 S. Ct. 1945, 1953–54 (2019), puts paid to any doubt regarding the Members’ lack of standing. Here, the (individual) Members concededly seek to do precisely what Bethune-Hill forbids. See Appellees’ Br. at 12 (asserting Members’ entitlement “to vote on whether to consent to an official’s acceptance of a foreign emolument before he accepts it . . . is not a private right enjoyed in [his] personal capacity, but rather a prerogative of his office.”).

The district court erred in holding that the Members suffered an injury based on “[t]he President . . . depriving [them] of the opportunity to give or withhold their consent [to foreign emoluments], thereby injuring them in their roles as members of Congress.” Id. at 62 (quotation marks omitted). After Raines and Bethune-Hill, only an institution can assert an institutional injury provided the injury is not “wholly abstract and widely dispersed.” Raines, 521 U.S. at 829. . . .

Our standing inquiry is “especially rigorous” in a case like this, where “reaching the merits of the dispute would force us to decide whether an action taken by one of the other two branches of the Federal Government was unconstitutional.” . . . Here, regardless of rigor, our conclusion is straightforward because the Members—29 Senators and 186 Members of the House of Representatives—do not constitute a majority of either body and are, therefore, powerless to approve or deny the President’s acceptance of foreign emoluments. . . . For standing, the Members’ inability to act determinatively is important, see Raines, 521 U.S. at 829, and, conversely, the size of their cohort is not—so long as it is too small to act. That is, we assess this complaint—filed by 215 Members—no differently from our assessment of a complaint filed by a single Member. . . .

The Members can, and likely will, continue to use their weighty voices to make their case to the American people, their colleagues in the Congress and the President himself, all of whom are free to engage that argument as they see fit. But we will not—indeed we cannot—participate in this debate. The Constitution permits the Judiciary to speak only in the context of an Article III case or controversy and this lawsuit presents neither.

Blumenthal was one of three Emoluments Clause cases filed against Trump. The other two, CREW v. Trump and D.C. v. Trump, are in the Second and Fourth Circuits, respectively. Standing has been an issue in all three cases (for some of the reasons I discussed in theseposts), and has divided the various appeals panels.

Bluementhal always presented the weakest case for Article III standing of the three, and so this case is likely at an end, while the others proceed. The Second Circuit accepted the argument that competitors have standing to challenge Emoluments Clause violations, while the Fourth Circuit did not. The Fourth reheard the case en banc in December, and a petition for en banc rehearing is pending in the Second.

While Article III courts may not be able to hear suits alleging Emoulments Clause violations (at least in the absence of a statute creating a cause of action and providing a more concrete basis for standing), that does not mean there are not serious substantive concerns. In all three cases, the courts have focused primarily on jurisdictional questions, not on the underlying merits, so none of these decisions should be taken as exonerations of the President’s conduct.

To this point, the Blumenthal opinion quotes from Justice Joseph Story’s Commentaries on the Constitution of the United States:

[a] patriot will not be likely to be seduced from his duties to his country by the acceptance of any title, or present, from a foreign power. An intriguing, or corrupt agent, will not be restrained from guilty machinations in the service of a foreign state by such constitutional restrictions.

from Latest – Reason.com https://ift.tt/2OEUJhH

via IFTTT

It’s Time To Ask Again What Really Happened To Ukraine’s Missing Gold

Now that the Trump impeachment farce is finally over, vindicating the president and in the process for the first time boosting the president’s approval rating higher than where Obama was at this time in his first term much to the embarrassment of Nancy Pelosi, whose impeachment gambit has backfired spectacularly (just as Nancy knew it would, and is why she delayed triggering it until a critical mass of ultra left-wing demands in Congress made it impossible for her to ignore any longer)…

… the Democrats’ great diversion from Trump’s core question – did the Bidens willfully engage in, and benefit from corruption in the Ukraine, corruption which may have been enabled and facilitated by billions in taxpayer funds originating from the Obama administration no less – is over.

However, while Trump has finally moved on beyond what in retrospect was a remarkable, if failed presidential coup attempt, orchestrated by the Ukraine lobby in the US, backed by the Atlantic Council and various other “deep-state” institutions and apparatchiks, and implemented by Congressional democrats who are now watching the chances of the Democratic party winning the 2020 presidential election melt before their eyes, some long overdue questions surrounding the Bidens’ involvement in Ukraine – one of the world’s most corrupt nations according to the World Economic Forum – especially around the time of the 2014 presidential coup and the months immediately following, are about to be asked, and haunt Joe Biden and his son like a very angry and vengeful ghost, only this time there will be no Trump impeachment to distract from revealing the shocking answers.

Needless to say, we are delighted by this outcome because as regular readers will recall, there are many unanswered questions that emerged back in 2014, some from following the money both in and out of Ukraine, and some from following the country’s gold, much of which was put on board a plane headed to the US in one cold, wintry night in March 2014, never to come back again.

But before we get there, first we need to a rather lengthy detour into the history of Ukraine corruption since the February 2014 Euromadian revolution, for the background on why Trump had to be stopped at all costs from asking either Ukraine, or anyone else, questions that may expose corruption involving Joe Biden in particular, and the Obama administration in general. To do that, we need to follow some $1.8 billion in US taxpayer funds that quietly went missing back in 2014, and most likely ended up in the offshore bank account of some Ukrainian oligarch; conveniently PJ Media’s senior editor Tyler O’Neill did just that almost two years ago, in March 2018. Here’s what he said back then, together with some additions from ZH:

In the last days of the Obama administration, then-Vice President Joe Biden took a “swan song” trip to Ukraine, a notoriously corrupt country where he had been the administration’s “point person.” On the eve of this trip, the country announced it would end a criminal investigation into an infamous company connected to the loss of $1.8 billion in aid funding — a company whose board of directors included Biden’s son Hunter.

The Biden family’s dealings with this Ukrainian company involved getting one of the country’s most notorious mob bankers, Ihor Kolomoiski, off the U.S. government visa ban list. Under Biden’s leadership, $3 billion in aid went to Ukraine, and his son’s company was implicated in the disappearance of $1.8 billion of that money. Peter Schweizer revealed the former vice president’s role in his new book “Secret Empires: How the American Political Class Hides Corruption and Enriches Family and Friends.”

Ihor Kolomoiski

Secretary of State John Kerry announced the U.S. support for Ukraine’s nationalist government in March 2014, a month after a mass uprising pushed pro-Russian President Viktor Yanukovych out of office and inspired a corresponding pro-Russian uprising in the east. It was also at this time that a leaked recording between US assistant secretary of state Victoria “Fuck the EU” Nuland and the US envoy to the Ukraine, Geoffrey Pyatt, emerged, a clip which as the FT said then “could also bolster [claims] that the protests that erupted against Ukraine’s President Viktor Yanukovich last November are being funded and orchestrated by the US.” In other words, the clip confirmed that the US was masterminding the entire “Euromaidan” process all along and deciding who should be in Ukraine’s next government. In short: what happened in Ukraine in February 2014 was another CIA-staged presidential coup. Finally, it was also the time that Biden became the Obama administration’s “point person” for the country.

On April 16, 2014, shortly after the February 2014 Ukrainian revolution which culminated with the overthrow of democratically-elected president Yanukovich, Biden met with Devon Archer, a former star fundraiser for John Kerry’s 2004 presidential run and business partner in Rosemont Capital with Biden’s son Hunter. (Federal agents would later arrest Archer in May 2016 for defrauding a Native American tribe.)

Less than a week later (April 22) came an announcement that Archer had joined the board of Burisma, a secretive Ukrainian natural gas company. On May 13, Hunter Biden would also join the company’s board.

On the day before Archer’s hiring, April 21, the vice president landed in Kiev for high-level meetings with Ukrainian officials. He spearheaded the effort to invest $1 billion from the U.S. and the International Monetary Fund (IMF) into Ukraine.

The vice president’s presence helps explain a conundrum. Burisma hired his son and Archer despite the fact that neither of them had any experience in the energy sector. Schweizer notes, “The choice of Hunter Biden to handle transparency and corporate governance of Burisma is curious, because Biden had little if any experience in Ukrainian law, or professional legal counsel, period.”

Furthermore, Hunter Biden “seemed undeterred by the fact that as he was joining the Burisma board the British government’s Serious Fraud Office (SFO) was seizing $23 million from [founder Mykola] Zlochevsky’s bank accounts.” Furthermore, a year after Biden joined the firm, “experienced industry observers warned investors that Burisma was still a company to be avoided.”

Mykola Zlochevsky

On the other hand, Ukraine is one of the most corrupt countries in the world. Out of 148 nations studied by the World Economic Forum, Ukraine ranks 143 for property rights, 130 for “irregular payments and bribes,” 133 for “favoritism in decisions of government officials,” and 146 for “protection of minority shareholders’ interests.”

Two major figures in this corruption feature prominently in Biden’s Ukraine investment.

Zlochevsky founded Burisma in Cyprus in 2006. He served as natural resources minister under Yanukovych, and gave himself the licenses to develop the country’s abundant gas fields. He also had a flare for lavishness, running a super-exclusive fashion boutique named after himself.

Burisma’s major subsidiaries ended up sharing the same business address as the natural gas firm controlled by Ukrainian oligarch Ihor Kolomoisky. He controlled the country’s largest financial institution, PrivatBank, through which the Ukrainian military and government workers got paid. He also owned media companies and airlines. In violation of Ukraine law, he maintained Ukrainian, Israeli, and Cypriot passports.

Kolomoisky gained a reputation for violence and brutality, along with lawlessness. Rival oligarchs have sued him for alleged involvement in “murders and beheadings” related to a business deal. He also allegedly used “hired rowdies armed with baseball bats, iron bars, gas and rubber bullet pistols and chainsaws” to take over a steel plant in 2006. He built his multibillion-dollar empire by “raiding” other companies, forcing them to merge with his own using brute force.

For these and other reasons, the U.S. government placed Kolomoisky on its visa ban list, prohibiting him from entering the country legally. In 2015, however, after Hunter Biden and Devon Archer had joined Burisma’s board, Kolomoisky was given admittance back into the U.S. According to a follow-up report in 2016, “today, the oligarch mainly resides in Switzerland. He spends much time in the United States and is getting less and less involved in the Ukrainian affairs.”

Archer and the younger Biden brought other benefits to Burisma, however. Archer represented the company at the Louisiana Gulf Coast Oil Exposition in 2015. Biden addressed the Energy Security for the Future conference in Monaco. The vice president’s son brought much-needed legitimacy to the shoddy gas company. Less than a month after Archer joined Burisma’s board, the company hired another Kerry lackey, David Leiter, as a lobbyist in Washington, D.C. He successfully lobbied for more aid to the country.

And Both Biden and Kerry championed $1.8 billion in taxpayer-backed loans given to Ukraine in September 2014 courtesy of the IMF. That money would go directly through Kolomoisky’s PrivatBank, and then it would disappear. According to the Ukrainian anti-corruption watchdog Nashi Groshi, “This transaction of $1.8 billion … with the help of fake contracts was simply an asset siphoning operation.”

What is even more fascinating, is that in the chaos following the February 2014 revolution, Ukraine appears to have embezzled money from none other than the IMF (whose biggest source of funds is the US). As German newspaper Deutsche Wirtshafts Nachrichten reported in August 2015, a huge chunk of the $17 billion in bailout money the IMF granted to Ukraine in April 2014 was discovered in a bank account in Cyprus controlled by, who else, Ukrainian oligarch Kolomoisky. As the German publication went on to add, in April 2014, $3.2 billion was immediately disbursed to Ukraine, and over the following five months, another $4.5 billion was disbursed to the Ukrainian Central Bank in order to stabilize the country’s financial system. “The money should have been used to stabilize the country’s ailing banks, but $1.8 billion disappeared down murky channels,” DWN wrote.

DWN also reported that according to the IMF, in January 2015 the equity ratio of Ukraine’s banking system had dropped to 13.8 percent, from 15.9 percent in late June 2014. By February 2015 even PrivatBank had to be saved from bankruptcy, and was given a 62 million Euro two-year loan from the Central Bank. “So where have the IMF’s billions gone?”

The racket executed by Kolomoiski’s PrivatBank was first uncovered by the Ukrainian anti-corruption initiative ‘Nashi Groshi,’ meaning ‘our money’ in Ukrainian.

According to Nashi Groshi’s investigations, PrivatBank has connections to 42 Ukrainian companies, which are owned by another 54 offshore companies based in the Caribbean, USA and Cyprus. These companies took out loans from PrivatBank totaling $1.8 billion.

These Ukrainian companies ordered investment products from six foreign suppliers based in the UK, the Virgin Islands and the Caribbean, and then transferred money to a branch of PrivatBank in Cyprus, ostensibly to pay for the products.The products were then used as collateral for the loans taken out from PrivatBank – however, the overseas suppliers never delivered the goods, and the 42 companies took legal action in court in Dnipropetrovsk, demanding reimbursement for payments made for the goods, and the termination of the loans from Privatbank. The court’s ruling was the same for all 42 companies; the foreign suppliers should return the money, but the credit agreement with Privatbank remains in place.

“Basically, this was a transaction of $1.8 billion abroad, with the help of fake contracts, the siphoning off of assets and violation of existing laws,” explained journalist Lesya Ivanovna of Nashi Groshi.

Then in March 2015, Kolomoiski, whom some have described as the Tony Soprano of Ukraine, and increasingly a pariah in the country that made him a billionaire was dismissed from his position as governor of Dnipropetrovsk after a power struggle with Ukrainian President Petro Poroshenko; the fraud was carried out while he was governor of the region in East-Central Ukraine.

“The whole story with the court case was only necessary to make it look like the bank itself was not involved in the fraud scheme. Officially it now looks like as if the bank has the products, but in reality they were never delivered,” said Ivanovna.

Such business practices, which earned Kolomoskyi a fortune estimated by Forbes in March 2012 to be $3 billion, were known to investigators beyond Ukraine’s borders; Kolomoiski was once banned from entering the US due to suspicions of connections with international organized crime but then Biden’s involvement quietly lifted the visa ban.

Despite these suspicions, Kolomoiski is unlikely to face justice, as he is currently living in exile in Switzerland , Israel and the US, after he fled Ukraine in early 2015. Not long after Kolomoiski fled Ukraine, in December 2016, Ukraine’s government nationalize his Privatbank in order to shore up Ukrainians’ savings. A Ukrainian lawmaker called it the “greatest robbery of Ukraine’s state budget of the millennium.” A few months earlier, in February 2016, the government seized Burisma founder Zlochevsky’s assets and placed him on Ukraine’s wanted list. The Ukrainian Prosecutor General’s Office seized Burisma’s gas wells.

Which brings us to January 2017, and when Joe Biden infamous arrived for his “swan song” visit and demanded, before the entire world, that the criminal investigation into Burisma was dropped.

Devon Archer left the scandal-plagued company at the end of 2016, although a clueless Hunter Biden remained on the board through October 2019 – well after his presence there sparked the biggest political scandal since the Bill Clinton impeachment – providing “legal assistance” in exchange for millions of dollars received from the gas giant. Archer and Biden have not been required to disclose their compensation from Burisma, but Bowling Green State University professorOliver Boyd-Barrett wrote, “Potentially, the Biden family could become billionaires.”

So did Joe Biden get Burisma off the hook for $1.8 billion in lost aid funding? Did he or his son get Kolomoisky off the visa ban list? To be sure, many questions still remain and were all conveniently swept under the rug over the “faux outrage” over the Trump impeachment farce. But now that the great impeachment diversion is over, these all too pressing questions can and finally should be asked.

Incidentally, anyone who is confused by the narrative above, and how $1.8 billion in taxpayer dollars “disappeared” in Ukraine starting in September 2014 when the money was deposited in PrivatBank, is encouraged to watch the following video by Glenn Beck who does a surprisingly good job at connecting the confusing dots behind what may be one of the greatest sovereign corruption and money heist stories in history.

The good news is that there are so many loose threads in this narrative, that any real probe will have little difficulty in getting to the bottom of where and how the $1.8 billion in US taxpayer funding to Ukraine “disappeared” and whether Biden, both father and son, are indeed involved.

And just to help them out, one place where any serious probe can start is with a story we wrote in March 2014, when citing a local media report, we shone light on a mysterious operation in which a substantial portion of Ukraine’s gold reserves were loaded onboard an unmarked plane, and flown to the US, just weeks after the February 2014 revolution.From the source, March 7, 2014:

Tonight, around at 2:00 am, an unregistered transport plane took off took off from Boryspil airport.

According to Boryspil staff, prior to the plane’s appearance, four trucks and two cargo minibuses arrived at the airport all with their license plates missing. Fifteen people in black uniforms, masks and body armor stepped out, some armed with machine guns. These people loaded the plane with more than forty heavy boxes.

After this, several mysterious men arrived and also entered the plane. The loading was carried out in a hurry. After unloading, the plateless cars immediately left the runway, and the plane took off on an emergency basis.

Airport officials who saw this mysterious “special operation” immediately notified the administration of the airport, which however strongly advised them “not to meddle in other people’s business.”

Later, the editors were called by one of the senior officials of the former Ministry of Income and Fees, who reported that, according to him, tonight on the orders of one of the “new leaders” of Ukraine, all the gold reserves of the Ukraine were taken to the United States.

Needless to say there was no official confirmation of any of this taking place, and in fact our report, in which we mused if the “price of Ukraine’s liberation” was the handover of Ukraine’s gold to the Fed at a time when Germany was actively seeking to repatriate its own physical gold located at the bedrock of the NY Fed, led to the usual mainstream media mockery.

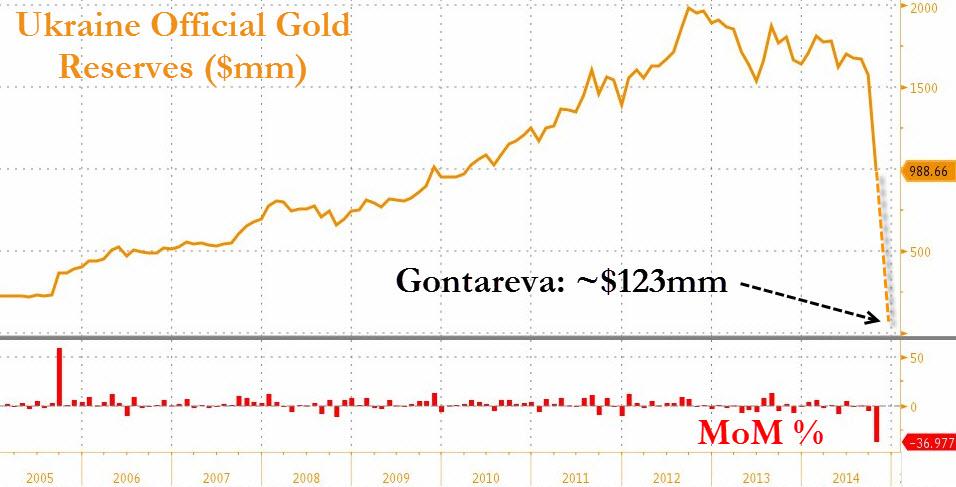

But then everything changed in November 2014, when in an interview on Ukraine TV, none other than the then-head of the Ukraine Central Bank, Valeriya Gontareva (who, became head of the Ukraine central bank in June 2014 when she replaced Stepan Kubiv and also presided over the nationalization of Kolomoiski’s PrivateBank in December 2016), made the stunning admission that “in the vaults of the central bank there is almost no gold left. There is a small amount of gold bullion left, but it’s just 1% of reserves.”

As Ukrainareported at the time, this stunning revelation means that not only has Ukraine been quietly depleting its gold throughout the year, but that the latest official number, according to which Ukraine gold was 8 times greater than the reported 1%, was fabricated, and that the real number is about 90% lower.

According to official statistics the NBU, the amount of gold in the vaults should be eight times more than is actually in stock. At the beginning of this month, the volume of gold was about $ 1 billion, or 8% of the total gold reserves. Now this is just one percent.

Assuming Gonaterva’s admission was true, it would imply that the official reserve data at the Central Bank was clearly fabricated, prompting questions about just how long ago the actual gold “displacement” took place. Could it have been during a cold night in March when “more than 40 heavy boxes” full of gold were loaded up on the plane and flown off to an unknown destination in the US?

To help out in this puzzle, we got some additional information from Rusila, which in Nov 2014 reported that “Ukraine’s gold reserves disappeared.”

According to recent data, the value of Ukraine gold should be $988.7 million. That is the value of gold proportion of gold in gold reserves is 8%. If you believe Gontareva, it turns out there is a mere $123.6 million in gold remaining. The figure is fantastic, considering that the amount of gold at the end of February (when the new authorities have already taken key positions) was $1.8 billion or 12% of the reserves.

In other words, since the beginning of the year gold reserves dropped almost 16 times. Gold stock in February were approximately 21 tons of gold, the presence of which was once proudly reported by Sergei Arbuzov, who led the NBU in 2010-2012. So what happened to 20.8 tons of gold?

Explaining the dramatic reduction in the context of the hryvnia devaluation through gold sales is impossible. After all, 92% of the reserves of the National Bank is in the form of a foreign currency that is much easier to use to maintain hryvnia levels and cover current liabilities. Besides since March the international price of gold has plummeted. Selling gold under such circumstances is a crime. In fact it would be more expedient to increase gold reserves through currency conversion in precious metals.

But apparently the result is not due to someone’s negligence or carelessness. The gold reserve has been actively carted out of the country, as a result of the very vague economic and political prospects of Ukraine. Something similar happened to the gold reserves of the USSR – when the Gorbachev elite realized that perestroika is leading the country to the abyss, gold simply disappeared in an unknown direction.

Oddly enough there was no official gold reduction just prior to the time when Victoria “Fuck the EU” Nuland was planning Yanukovich’s ouster, and as shown above, quite the contrary: Ukraine’s gold pile was increasing with every passing year… until it collapsed in early 2014. It is a little more odd that it was during the period when Ukraine was “supported” by its western allies that several billion dollars worth of physical gold – the people’s gold – just “vaporized.”

Which brings us to the $1.8 billion question: what happened to Ukraine’s gold, because if the now former central banker’s story is accurate, that’s roughly the amount of gold that quietly left the country just days after the US-backed presidential coup. And, it is also roughly how much taxpayer-funded Ukraine aid, procured by Joe Biden while his son was working at Burisma, is now missing.

At this point, there are certainly many pressing questions but one stands out: was the real “quid pro quo” not one of Trump holding up payments to Kiev in exchange for a probe of Biden – which after reading all of the above is more than warranted – but if the quo, namely US support for regime change in Ukraine and almost two billion in now missing taxpayer funds which ended up in an oligarch’s bank and mysteriously “vaporized” but not before said oligarch hired the son of the US vice president, wasn’t the quid to some 40 tons of Ukraine leaving forever to an unknown destination in the US.

We hope that Trump’s second term will provide ample time and opportunity to answer this critical question, and just to set off investigators on the right track, we believe that any investigation should begin with the former central bank head, Gontareva, who he also fled to London where she now lives in self-appointed exile and where she now “fears for her life” after one of her homes near Kiev was badly damaged in an arson attack, and was also injured in August when she was knocked down by a car in London. Failing that, one can always check the flight manifests and the cargo contents of all planes that left the Ukraine and arrived in the US on March 7, 2014 with a cargo consisting of billions of dollars in gold…

In a fiasco for the ages, the blue party faceplants in Iowa…

Monday, February 3rd, just before 9 p.m., the airport Holiday Inn, Des Moines. A crowd of supporters and volunteers for Senator Bernie Sanders is buzzing. After four years of being shat upon by party officials and media allies alike (CNN and MSNBC are seen in Sanders crowds as Goebbelsian arms of the Democratic National Committee), Vermont’s anti-corporate crusader has defied odds and soared in polls. All that remains is the Schadenfreude orgasm of a victory speech.

A young animal rights lawyer named Colin Grace is explaining how he got turned on to Bernie. “Honestly, it started by looking into some of the causes of 2008,” he laughs. “Well, then I found weed and became a libertarian.”

A nearby supporter with long hair under a standard issue Spin Doctors wool weed-smoking hat perks up.

“Dude, should we all smoke right now?” smiles at a fortysomething named David, patting his chest pockets.

“I’ve got the most enormous J.”

Everyone laughs. David and his wool-and-fleece costume looks nothing like the younger Grace in a blue blazer and collar — Grace was a caucus precinct captain tonight — but their stories sound the same. Two elements are near-constants in Sanders crowds: life experience with a broken system (Grace told a story of corporate-captured regulators killing an animal rights bill he worked on), and feelings of sympathy for a Senator also seen as getting the short stick from establishment cheats.

“I was third party in 2016. I supported Gary Johnson,” says Grace.

“But then, even from the sideline, I thought, ‘Man, the DNC is rigging this against Sanders.”

“They’re dirty, man,” David agrees.

“They don’t even try to hide it.”

Nods all around. The group breaks up to hunt for a TV. The results are about to come in. A young woman in a blue Bernie shirt mutters as she walks toward the conference room: “I can’t wait to see Wolf’s face.”

There was so much scummery to avenge: from Chris Matthews on MSNBC suggesting Sanders wouldn’t stop his car to help someone injured on the side of the road, to CNN running a late-breaking story that the DNC was employing “troll fighters” to combat a Russian “disinformation” campaign (presumably to help Sanders), to the DNC changing debate rules to allow billionaire ex-Republican Michael Bloomberg to buy his way in, to an $800,000 attack ad campaign from former Democratic strategist Mark Mellman, to reports that at least some DNC members were contemplating a return of superdelegates to stop Bernie.

It was all out war, between what one Andrew Yang supporter described as being between “the screwers and screwees.” It felt like the same kind of below-the-belt mudslinging progressives used to associate with Republican hitman Lee Atwater.

Sanders supporters felt sure they’d overcome. With a win, all that invective was just another indication of righteousness.

“It just tells me he pisses off the right people,” Grace quipped. Then he walked off to catch the victory speech, and all hell broke loose.

* * *

Yesterday’s really gone.

In 1993, liberal America sang along at the Bill Clinton inaugural ball with Lindsey Buckingham and Stevie Nicks (and Michael Jackson, whoops). “Don’t Stop” was “Ding, dong, the witch is dead!” for the smart set. The New Democrats ushered in a new reign for youth and modernity against Reagan-Bush reaction.

That’s done. After a vote in Iowa that reeked of third-world treachery — from monolithic TV propaganda against the challenger to rumors of foreign intrusion to, finally, a “botched” vote count that felt as legitimate as a Supreme Soviet election — the Democrats have become the reactionaries they once replaced.

Coinciding with the flatulent end of the party’s impeachment gambit, and the related news that Donald Trump is enjoying climbing approval ratings, the Blue Party was exposed as an incompetent lobby for doomed elites, dumb crooks with nothing left to offer but their exit.

Waukee, Iowa, Thursday, January 30th. Activist Tracye Redd, a Waterloo native who’d repped Black Lives Matter and Greenpeace in the past and was currently “bird-dogging” candidates for the Center for Biological Diversity, approached former Vice President Joe Biden after a speech. He asked if Biden would agree to work toward phasing out fossil fuels.

Before he knew it, Biden was sticking a finger in his chest and angrily reading off credentials. “Go back. 1986. I was the first one ever to introduce a climate change bill,” he snapped.

“I thought to myself, ‘Great, you did that in 1986, but if we’ve got a million species facing extinction, so it’s clearly still a problem,’” Redd remembers.

Biden pushed again. “Politifact said it’s a game changer,” Biden jabbed, adding: “I’ve been working my whole life.” He poked Redd in the sternum on fact, work, whole, and life, then walked away like he’d dropped a mic.

The scene was so bizarre that Redd says he could only respond by instinct, drawing on post-Trayvon Martin strategies for black men to keep safe in charged situations. “You know, ‘Yessir, no sir,’ don’t talk back, keep your hands visible…”

Biden in this race has, on multiple occasions, looked close to grabbing prospective voters by the ears and speed-eating their faces off to thwart questions. A few days before the exchange with Redd, he grabbed a former state representative named Ed Fallon by the jacket lapel and asked, “You believe Bernie can do something, and by 2030? Only relaxing when Rollins gasped he was for Tom Steyer. Often he looks around like he expects a thumbs-up for giving in to his rage-response.

In Cedar Rapids on February 1st, Jaimee Warbasse, a mother, hairstylist, and onetime caucaser for Hillary Clinton, was feeling anxious. Just days were left before the vote, and unusually, she was undecided. Her husband Matt called her with good news: Joe Biden was going to appear at the Roosevelt Middle School, just down the street.

“I was glad,” Warbasse recalls. “When he was Vice President, I thought he’d make a good president… I was hoping to meet him, so I could feel more comfortable voting for him.”

Iowans take presidential politics seriously. Perhaps only New Hampshire residents could comprehend. When deciding whom to stand for, Iowans expect to physically meet their candidate. This is seen as a two-way obligation: Voters should make an effort to meet the hopefuls, but candidates also have to make themselves available.

Warbasse was slightly put out that she had not met Biden. “There were more opportunities to see the other candidates,” she said. She went to his speech, then got in a greeting line, shouting, “Undecided voter over here, Joe!”

She invited him to make his case. “I haven’t seen much of you,” she said. Why should she vote for him?

Biden moved inches from her face, gripped her hand (throughout: “we’re talking minutes,” she said) and gave a political clip-art answer, about how he’s a guy who says what he means and means what he says, etc.

When Warbasse didn’t respond with enthusiasm, his mood turned. “If I haven’t swayed you today, then I can’t sway you,” he snapped.

Warbasse was shocked.

“It was like he was waiting for people to tell him what a wonderful person he was,” she says. “It was super bizarre.”

These scenes have been laughed off as irrelevant dementia, but Biden’s outbursts are in keeping with a long pattern of establishment Democrats being outraged at having to explain their shit records.

The Biden jab came from the same place as the counter-accusatory finger Bill Clinton thrust at Black Lives Matter protesters in Philadelphia in 2016, for questioning the Crime Bill and talking about “super predators” (“Maybe you thought they were good citizens. She didn’t!” Clinton shouted). It was the same impatience that got Nancy Pelosi huffing over progressives and “the Green Dream or whatever.”

Democratic campaign events have long been more pep rally than discussion, more about the terribleness of Republicans than substance. “They’re so used to events where everyone is rooting for them,” says Redd. “It’s like, ‘No, we’re actually here to challenge you on issues that matter.’”

Biden performed surprisingly well all year in polls, but he headed into Iowa like a passenger jet trying to land with one burning engine, hitting trees, cows, cars, sides of mountains, everything. The poking incidents were bad, but then one of his chief surrogates, John Kerry, was overheard by NBC talking about the possibility of jumping in to keep Bernie from “taking down” the party.

“Maybe I’m fucking deluding myself here,” Kerry reportedly said — mainstream Democrats may not have changed their policies or strategies much since Trump, but they sure are swearing more — then noted he would have to raise a “couple of million” from people like venture capitalist Doug Hickey.

Kerry later said he was enumerating the reasons he wouldn’t run, though those notably did not include humility about his own reputation as a comical national electoral failure, or because there’s already a candidate in the race (Biden) he’d been crisscrossing Iowa urging people to vote for, but instead because he’d have to step down from the board of Bank of America and give up paid speeches. French aristocrats who shouted “Vive le Roi!” on the way to the razor did a better job advertising themselves.

With days, hours left before the caucuses, there were signs everywhere that the party establishment was scrambling to find someone among the remaining cast members to stop what Kerry called the “reality of Bernie.”

But who? Yang said smart things about inequality, so he was out. Tulsi Gabbard was Russian Bernie spawn. Tom Steyer was Dennis Kucinich with money. Voters had already rejected potential Trump WWE opponents like the “progressive prosecutor” (Kamala Harris), the “pragmatic progressive” (John Delaney), “the next Bobby Kennedy” (Beto O’Rourke), “Courageous Empathy” (Cory Booker), Medicare for All can bite me (John Hickenlooper), and over a dozen others.

Former South Bend, Indiana Mayor Pete Buttigieg seemed perfect, a man who defended the principle of wine-based fundraisers with military effrontery. New York magazine made his case in a cover story the magazine’s Twitter account summarized as:

“Perhaps all the Democrats need to win the presidency is a Rust Belt millennial who’s gay and speaks Norwegian.”

(The “Here’s something random the Democrats need to beat Trump” story became an important literary genre in 2019-2020, the high point being Politico’s “Can the “F-bomb save Beto?”).

Buttigieg had momentum. The flameout of Biden was expected to help the ex-McKinsey consultant with “moderates.” Reporters dug Pete; he’s been willing to be photographed holding a beer and wearing a bomber jacket, and in Iowa demonstrated what pundits call a “killer instinct,” i.e. a willingness to do anything to win.

Days before the caucus, a Buttigieg supporter claimed Pete’s name had not been read out in a Des Moines Register poll, leading to the pulling of what NBC called the “gold standard” survey. The irony of such a relatively minor potential error holding up a headline would soon be laid bare.

However, Pete’s numbers with black voters (he polls at zero in many states) led to multiple news stories in the last weekend before the caucus about “concern” that Buttigieg would not be able to win.

Who, then? Elizabeth Warren was cratering in polls and seemed to be shifting strategy on a daily basis. In Iowa, she attacked “billionaires” in one stop, emphasized “unity” in the next, and stressed identity at other times (she came onstage variously that weekend to Dolly Parton’s “9 to 5” or to chants of “It’s time for a woman in the White House”). Was she an outsider or an insider? A screwer, or a screwee? Whose side was she on?

A late controversy involving a story that Sanders had told Warren a woman couldn’t win didn’t help. Jaimee Warbasse planned to caucus with Warren, but the Warren/Sanders “hot mic” story of the two candidates arguing after a January debate was a bridge too far. She spoke of being frustrated, along with friends, at the inability to find anyone she could to trust to take on Trump.

“It’s like we all have PTSD from 2016,” she said. “There has to be somebody.”

* * *

Just after sundown, February 2nd, Jethro’s BBQ n’ Pork Chop Grill, Johnston, Iowa. The Niners are up on the Chiefs 3-0 and this gymnasium-sized sports bar is packed. Most everyone in seats is a supporter of Minnesota Senator Amy Klobuchar.

Everyone else in the massive crowd seems to be a reporter or cameraperson. You can’t step two feet in the Des Moines area on caucus weekend without hitting press. It’s like an angry God shook a box of us through the clouds.

When the candidate herself shows up, media engulf her with a three-level swarm. Klobuchar ends up inside a row of cameras inside a row of hacks carrying notebooks, inside a row of taller hacks on tippy-toes.

“I’m asking you to run for me,” she cries, to the scattered real people somewhere beyond the press.

“Just like those guys are running on the field. I’m asking you to take this over the goalposts for me. I’m asking you to score a touchdown for — okay, enough!”

Guffaws! Reporters love “Amy,” who goes by one name behind press ropelines, like Shakira, or Sinbad. She’s their take on a star. “Amy” in the last week surged in polls, having overtaken Warren in some surveys, hitting as much as 10, 12, and 13 percent.

Klobuchar is a pure distillation of “electability,” i.e. a Washington reporter’s idea of what a Midwesterner finds charming. She isn’t funny, but her tireless marketing of her funniness matches the reportorial concept of what a “sense of humor” is in politics.

Her ability to speak at length without revealing deep ideological belief is also prized by our kind. This is what Washington for decades told people they wanted, instead of health care, peace, job security, etc.

Scott Thompson, the former mayor of a downstate Illinois town called Rushville, sees it differently. The congenial labor economist dressed in a big green “Amy” t-shirt has a long-standing ritual, asking every reporter who approaches him to sign a clipboard.

“Five today,” he says, chuckling. He holds it up: He’s running out of space.

Thompson’s experience in government disinclines him to politicians who offer facile solutions. He wrestles with the Bernie phenomenon, saying he understands it more now than he used to, as he sympathizes with those who are so mad, they’ve lost faith in the system.

“But at some point,” he says, “you have to stop being pissed off and start working.” He pauses. “If you want to fight just to fight, go into boxing, you know?”

That Sunday night, a 36-year-old Minnesotan named Chris Storey called a number he’d been given, for a woman who was chair of the Waukee 4 district. Thanks to a new rule allowing out-of-state volunteers to be precinct captains, he was set to represent the Sanders campaign there.

“We got along, it was great,” he recalls.

“She told me she was looking forward to seeing me the next day.”

The next day, caucus day, Storey showed up at Shuler Elementary School in Clive, Iowa. The same official he’d spoken with the night before met him at the door.

“It was like two different people,” he recalls.

“I was told there was a written directive from the county chair that nonresidents could not be precinct captains.”

Sanders had to get a last-minute replacement captain in Waukee 4, someone not formally aligned with the campaign. He fell short of viability there by five votes. County chair Bryce Smith, who made the decision, said he was responding to a late directive from the Iowa Democratic Party that said they would allow one nonresident captain per campaign, per precinct, but “the discretion of the chair is what goes,” i.e. this ultimately was a judgment call for county chairs. Smith said he didn’t like the change to the longstanding rule — “What’s stopping a campaign from hiring professional persuaders and high profile people?” he asked — and decided to bar nonresident captains. The IDP has not yet commented.

As a result, some would-be captains in Dallas County from multiple different campaigns were pulled off the job (Smith said he got “five, six, eight” calls to complain). Meanwhile, in other districts, nonresident captains were common.

Caucus participants later in the week would offer an eyebrow-raising number of other issues: bad head counts, misreported results, misreads of rules, wrong numbers, telecommunications errors, and other problems.

The basics of the caucus aren’t hard. You enter a building that is poorly ventilated, too small, and surrounded by mud puddles — usually a school gym. You join other people who plan on voting your way, gathering around the “precinct captain” for your candidate. If your pile of people comprises 15% of the room or more on the first count, your candidate is deemed “viable” and you must stay in that group. If your group doesn’t reach 15%, you must move to a new group or declare yourself undecided. There is a second count, and it should be done.

When historians pore over the Great Iowa Catastrophe of 2020, much of the blame will be focused on Acronym and Shadow, the two firms associated with the balky app that was supposed to count caucus results. For the conspiratorial-minded, the various political connections will be key: Acronym co-founder Tara McGowan is married to Buttigieg strategist Michael Halle, while former Obama campaign manager David Plouffe sits on Acronym’s board. Shadow had also been a client of both the Buttigieg and Biden campaigns in 2019.

But garden variety disorganization and stupidity were the major storylines underneath the terrible optics. From the first moment the caucus proceedings were delayed Monday night due to what the Iowa Democratic Party called “inconsistencies in the reporting,” Sanders supporters in particular felt in déjà vu territory. Orlando native Patty Duffy, an out-of-stater who captained for Sanders in the small town of Milo, had flashbacks to the run-up to the Hillary-Bernie convention.

“It was like we were back in 2016,” Duffy said. “Except this was worse.”

* * *

What happened over the five days after the caucus was a mind-boggling display of fecklessness and ineptitude. Delay after inexplicable delay halted the process, to the point where it began to feel like the caucus had not really taken place. Results were released in chunks, turning what should have been a single news story into many, often with Buttigieg “in the lead.”

The delays and errors cut in many directions, not just against Sanders. Buttigieg, objectively, performed above poll expectations, and might have gotten more momentum even with a close, clear loss, but because of the fiasco he ended up hashtagged as #MayorCheat and lumped in headlines tied to what the Daily Beast called a “Clusterfuck.”

Though Sanders won the popular vote by a fair margin, both in terms of initial preference (6,000 votes) and final preference (2,000), Mayor Pete’s lead for most of the week with “state delegate equivalents” — the number used to calculate how many national delegates are sent to the Democratic convention — made him the technical winner in the eyes of most. By the end of the week, however, Sanders had regained so much ground, to within 1.5 state delegate equivalents, that news organizations like the AP were despairing at calling a winner.

This wasn’t necessarily incorrect. The awarding of delegates in a state like Iowa is inherently somewhat random. If there’s a tie in votes in a district awarding five delegates, a preposterous system of coin flips is used to break the odd number. The geographical calculation for state delegate equivalents is also uneven, weighted toward the rural. A wide popular-vote winner can surely lose.

But the storylines of caucus week sure looked terrible for the people who ran the vote. The results released early favored Buttigieg, while Sanders-heavy districts came out later. There were massive, obvious errors. Over 2,000 votes that should have gone to Sanders and Warren went to Deval Patrick and Tom Steyer in one case the Iowa Democrats termed a “minor error.” In multiple other districts (Des Moines 14 for example), the “delegate equivalents” appeared to be calculated incorrectly, in ways that punished all the candidates, not just Sanders. By the end of the week, even the New York Times was saying the caucus was plagued with “inconsistencies and errors.”

Emily Connor, a Sanders precinct captain in Boone County, spent much of the week checking results, waiting for her Bernie-heavy district to be recorded. It took a while. By the end of the week, she was fatalistic.

“If you’re a millennial, you basically grew up in an era where popular votes are stolen,” she said.

“The system is riddled with loopholes.”

Others felt the party was in denial about how bad the caucus night looked.

“They’re kind of brainwashed,” said Joe Grabinski, who caucused in West Des Moines.

“They think they’re on the side of the right… they’ll do anything to save their careers.

An example of how screwed up the process was from the start involved a new twist on the process, the so-called “Presidential Preference Cards.”

In 2020, caucus-goers were handed index cards that seemed simple enough. On side one, marked with a big “1,” caucus-goers were asked to write in their initial preference. Side 2, with a “2,” was meant to be where you wrote in who you ended up supporting, if your first choice was not viable.

The “PPCs” were supposedly there to “ensure a recount is possible,” as the Polk County Democrats put it. But caucus-goers didn’t understand the cards.

Morgan Baethke, who volunteered at Indianola 4, watched as older caucus-goers struggled. Some began filling out both sides as soon as they were given them.

Therefore, Baethke says, if they do a recount, “the first preference should be accurate.” However, “the second preference will be impossible to recreate with any certainty.”

This is a problem, because by the end of the week, DNC chair Tom Perez — a triple-talking neurotic who is fast becoming the poster child for everything progressives hate about modern Dems — called for an “immediate recanvass.” He changed his mind after ten hours and said he only wanted “surgical” reanalysis of problematic districts.

No matter what result emerges, it’s likely many individual voters will not trust it. Between comical videos of apparently gamed coin-flips and the pooh-poohing reaction of party officials and pundits (a common theme was that “toxic conspiracy theories” about Iowa were the work of the Trumpian right and/or Russian bots), the overall impression was a clown show performance by a political establishment too bored to worry about the appearance of impartiality.

“Is it incompetence or corruption? That’s the big question,” asked Storey.

“I’m not sure it matters. It could be both.”

* * *

Iowa was the real “beginning of the end,” to a story that began in the Eighties.

Following the wipeout 49-state, 512 electoral vote loss of Walter Mondale in 1984, demoralized Democratic Party leaders felt marooned, between the awesome fundraising power of Ronald Reagan Republicans and the irritant liberalism of Jesse Jackson’s Rainbow Coalition.

To get out, they sold out. A vanguard of wonks like Al From and Senator Sam Nunn at the Democratic Leadership Council devised a marketing plan: two middle fingers, one in each direction.

They would steal financial support for Republicans by out-whoring them on economic policy. The left would be kneecapped via “triangulation,” i.e. the public reveling in the lack of choices for poor, minority, and liberal voters.

Young pols like Bill Clinton learned they could screw constituents and still collect from them. What would they do, vote Republican? Better, the parental scolding of disobedient minorities like Sister Souljah combined with the occasional act of mindless sadism (like the execution of mentally ill Ricky Ray Rector) impressed white “swing” voters, making “triangulation” a huge win-win — more traction in red states, less whining from lefty malcontents.

Democrats went on to systematically rat-fuck every group in their tent: labor, the poor, minorities, soldiers, criminal defendants, students, homeowners, media consumers, environmentalists, civil libertarians, pensioners – everyone but donors.

They didn’t just fail to defend groups, but built monuments to their betrayal. They broke labor’s back with NAFTA, embraced mass incarceration with the 1994 Crime Bill, and ushered in the Clear Channel era with the Telecommunications Act of 1996. Welfare Reform in 1996 was a sellout of the Great Society (but hey, at least Clinton kept the White House that year!). The repeal of the Glass-Steagall Act gave us Too Big to Fail. Shock Therapy was the Peace Corps in reverse. They sold out on Iraq, expanded Dick Cheney’s secret regime of surveillance and assassination, gave Wall Street a walk after 2008, then lost an unlosable election, which they blamed on a conspiracy of leftist intellectuals and Russians.

Still, if you were black, female, gay, an immigrant, a union member, college-educated, had been to Europe, owned a Paul Klee print or knew Miller’s Crossing was a good movie, you owed Democrats your vote. Why? Because they “got things done.”

Now they’re not getting much done, except a lost reputation. That feat at least, they earned.

To paraphrase the Joker:

What do you get when you cross a political party that’s sold out for decades, with an electorate that’s been abandoned and treated like trash?

“End That Son Of A Bitch”: Duterte Moves To Terminate Philippines’ Military Pact With US

President of the Philippines Rodrigo Duterte is moving to terminate the shaky US-allied country’s military pact with the United States after Washingtonrevoked former police chief and now Senator Ronald “Bato” Dela Rosa’s US visa last month. The close Duterte ally stands accused of widespread of widespread war crimes, including ordering extrajudicial killings of thousands during the Southeast Asian Pacific nation’s brutal ongoing ‘war on drugs’ — raging since 2016.

An enraged Duterte had threatened last month: “I’m warning you… if you won’t do the correction on this, I will terminate the… Visiting Forces Agreement,” and declared provocatively “I’ll end that son of a bitch”— in reference to the pact which provides legal immunity to US military drills.

Philippine President Rodrigo Duterte, via Getty/NYT

Filipino Foreign Affairs Secretary Teodoro Locsin testified before the country’s senate this past week that termination of the agreement will “negatively impact” defense and economic ties between Washington and Manila.

“The president said he is terminating the VFA,”Defense Secretary of the Philippines, Maj. Gen. Delfin Lorenzana told ABS-CBN News on Friday. “I asked for clarification and he said he is not changing his decision.”

President Duterte previously gave Washington a month to fix its “mistake” related to punitive action against Dela Rosa and said he wasn’t bluffing. The AP described the history of the key military pact as follows:

The security accord, which took effect in 1999, provides the legal cover for American troops to enter the Philippines for joint training with Filipino troops.

A separate defense pact subsequently signed by the treaty allies in 2014, the Enhanced Defense Cooperation Agreement, allowed the extended stay of U.S. forces and authorized them to build and maintain barracks and other facilities in designated Philippine military camps.

Perhaps more significantly Duterte went so far as to declare in late January that he will ban some US senators from visiting the Philippines unless Washington backs down. He’d also told members of his cabinet not to visit the US.

Former Philippines national police chief Roland Dela Rosa (now senator) in 2017, via the AFP.

Since Manila initiated its aggressive militarized crackdown on illegal drugs starting in 2016, thousands of civilian drug suspects have been left dead across the country, mostly in deeply impoverished areas, resulting in condemnations from the United Nations and human rights groups. Most of these killings also took place outside of any courtroom or judicial setting.

Dela Rosa was tasked as President Duterte’s top enforcer, gaining him popularity among right-wingers and the military in the country, but infamy among others.

The OPCW has released a briefing note summarising the recent “independent investigation” into their recent Titanic-sized leaks.(You can read the summary at the link above, or the full “independent” report here).

It’s a fairly narrow statement, focusing entirely on the two unnamed inspectors (Inspector A and Inspector B) who worked with the Working Group on Syria, Propaganda and Media to leak the censored reports. (There is not a word about the e-mails later released by WikiLeaks).

You won’t be surprised to know that the report finds the two leakers, Ian Henderson and “Alex”, were wrong to leak the confidential information.

In that sense, it’s entirely self-contradictory. Attempting to tell us the information is at once “sensitive”, and also incomplete, incorrect and easily refuted.

Of course, none of that refutation is present here, because that wasn’t the remit of this report. This is just an investigation into the “Possible Breaches of Confidentiality” and not the veracity of the leaks, or the pertinence of the information therein.

Sometimes an incredibly narrow purview is a sound defence against an undesirable reality.

There’s really no new information here, just six pages of waffle telling us very little we didn’t already know. It’s not a report that really means anything at all. It’s just something that the OPCW literally had to say. Institutions have immune responses, they simply must attack their critics. It’s automatic.

If a CIA whistleblower were to announce the sky was blue, the CIA would release a memo claiming to have no official records concerning the visual appearance of our atmosphere and detailing the leaker’s history of alcohol abuse.

Attacking whistleblowers is just a reflex of self-defence, the most base instinct of every lifeform.

In its content and tone, this report is a clear example of that behaviour. Far more a smear and hit piece than a refutation or investigation (at one point it even straight-up lies about Ian Henderson’s career at the OPCW).

Essentially, it’s just a series of attacks on the competence and motivations of the whistleblowers, even to the point of attempting to deny them that status:

Inspectors A and B are not whistle-blowers.”

The head of OPCW bafflingly declares, before going on to explain:

They are individuals who could not accept that their views were not backed by evidence. When their views could not gain traction, they took matters into their own hands and breached their obligations to the Organisation. Their behaviour is even more egregious as they had manifestly incomplete information about the Douma investigation.”

See – they’re not “whistleblowers”, they’re just individuals who believed that some documents being kept secret should be made public, and “took matters into their own hands”.

Apparently, that’s different from being a whistleblower. Somehow.

As with so much else in the current political sphere, it’s not so much an argument as an exercise in semantics.

Just as Julian Assange’s arrest became a debate over whether or not he was “really a journalist”, and “antisemitism” is redefined to increasingly ludicrous vagueness, here we are confronted by a memo essentially saying “ignore these leaks, these people are not real whistleblowers”.

It’s really not a report designed to make a case or prove a point. It won’t convert anybody or change a single mind. It’s just there to be at the other end of a link. To supply gate-keeping “journalists” with soundbites to bounce back and forth across twitter and blockquote in their articles.

A final redoubt to provide mainstream attack-dogs like Chris York or Scott Lucas some cover as they make a hasty retreat.

In that sense, it’s already doing its job:

NEW – @OPCW statement demolishes the #Douma CW conspiracy theory pushed, amongst others by @ClarkeMicah.

Damming putdown of the supposed OPCW whistleblowers championed by various British academics who claim Syria wasn’t behind Douma chemical attack. This comes from the OPCW itself: pic.twitter.com/EFsGrSzULz

Hawkish Senators Demand Twitter ‘Obey Sanctions’ By Banning Iran’s Leaders

At this rate all Iranian media sources and official accounts could soon be banned in the West, leaving journalists without a clue of what Tehran’s leaders actually think, and without official statements. The semi-official Fars news English website was knocked offline two weeks ago by US Treasury order (the international server host conformed, making Fars transfer its site hosting to within Iran), but the latest in a growing list of “purges” whether on YouTube or other platforms.

And now US senators are leading the charge to get Iran’s leaders banned from Twitter, as The Hill reports:

A group of Republican senators lead by Sen. Ted Cruz (Texas) sent a letter to Twitter on Thursday asking the platform to suspend the accounts of Iranian Supreme Leader Ayatollah Ali Khamenei and Foreign Minister Mohammad Javad Zarif to comply with U.S. sanction law.

The letter to CEO Jack Dorsey argues that an executive order from last summer imposing sanctions on Khamenei and those acting on his behalf prohibits Twitter from providing services to the two Iranian officials.

Sen. Marco Rubio, R-Fla. and Sen. Ted Cruz, R-Texas. Image source: AP.

Ironically, Twitter itself is blocked inside Iran on order of Tehran authorities, notwithstanding Iranian residents often easily getting around these restraints.

Foreign Minister Zarif is actually verified on Twitter despite being personally sanctioned by the US Treasury, and regularly uses it to issue statements to the world in reaction to White House policies or in response to President Trump’s words on Iran.

The hawkish group of Republican senators including Cruz, Tom Cotton (Ark.), Marsha Blackburn (Tenn.) and Marco Rubio (Fla.) wrote in the letter to Twitter: “While the First Amendment protects the free speech rights of Americans — and Twitter should not be censoring the political speech of Americans — the Ayatollah enjoys zero protection from the United States Bill of Rights.”

“And, as the leader of the world’s leading state sponsor of terrorism — directly responsible for the murder of hundreds of U.S. citizens — the Ayatollah and any American companies providing him assistance are entirely subject to U.S. sanctions laws,” they added.

Iran’s top diplomat often directly engages President Trump on Twitter:

.@realdonaldtrump is better advised to base his foreign policy comments & decisions on facts, rather than @FoxNews headlines or his Farsi translators

It was also sent to the White House, as well as Treasury Secretary Steven Mnuchin – who previously enforced bans on Iranian media entities – and top administration officials.

The letter was first reported Friday, and Twitter did not immediately issue a response. But the US company is not expected to take action, given it announced in 2018 it would not suspend accounts of world leaders, given it “would hide important information people should be able to see and debate,” according to a prior official company statement.

“It would also not silence that leader, but it would certainly hamper necessary discussion around their words and actions,” Twitter said at the time.

Pakistan’s parliament passed a resolution Friday that calls for the public hanging of convicted child killers and rapists.

AFPreports that the resolution, which is non-binding, comes after a number of high-profile child sex-abuse cases have scandalized the South Asian nation in recent years, leading to major outbreaks of unrest and riots.

Parliamentary affairs minister Ali Muhammad Khan, who presented the resolution in the lower house of the legislature, said that child killers and rapists “should not only be given the death penalty by hanging, but they should be hanged publicly.”

“The Quran commands us that a murderer should be hanged,” the minister added.

While the resolution was swiftly passed by a majority of lawmakers, human rights minister Shireen Mazari has emphatically stated that it does not enjoy the backing of the government.

“The resolution passed in [the National Assembly] today on public hangings was across party lines and not a govt-sponsored resolution but an individual act. Many of us oppose it – our [Ministry of Human Rights] strongly opposes this. Unfortunately I was in a mtg and wasn’t able to go to NA.”

Federal Minister for Science and Technology Fawad Chaudhry also condemned the passage of the resolution.

“Strongly condemn this resolution. This is just another grave act in line with brutal civilisation practices [sic]. Societies [should] act in a balanced way, [barbarity] is not an answer to crimes. This is another expression of extremism.”

However, Pakistan has struggled to come to grips with rampant crimes of child sexual abuse.

A child rapist was hanged in October 2018 after his crime in Kasur, near Lahore, sparked days of nationwide protests and unrest.

Six-year-old victim Zainab Fatima Ameen was attacked by a 24-year-old man who later confessed to raping and murdering the young girl.

In 2015, authorities busted a huge paedophilia ring in Kasur. In the massive scandal, it was found that at least 280 children were being sexually abused by a gang who blackmailed parents with threats to publicly release the videos.

In March 2016, Pakistan criminalized sexual assault against minors, child pornography and trafficking. Only acts of rape and sodomy had previously been punishable by law.

Human rights NGO Amnesty International also condemned the recent passage of the bill by the lower house of parliament, with AI Deputy South Asia Director Omar Waraich noting that “public hangings are acts of unconscionable cruelty” with no place in a society that respects people’s rights.

Continuing, the advocate said:

“Executions, whether public or private, do not deliver justice. They are acts of vengeance and there is no evidence that they serve as a uniquely effective deterrent.”

A number of human rights groups have demanded that the country reinstate a moratorium on the death penalty. Capital punishment was reintroduced following the 2015 Army Public School massacre that claimed the lives of 151 people.

Sarah Belal, the executive director of anti-death penalty group Justice Project Pakistan, told AFP:

“There is no empirical evidence to show that public hangings are a deterrent to crime or in protecting the psycho-social well-being of children.”

“Moments Of Triggering”: Rashida Tlaib Explains Why She And Ilhan Omar Held Hands During The State Of The Union

Tuesday night’s State of the Union was a triumphant moment for President Trump, a time where he celebrated his cresting popularity at the beginning of a critical election year. Despite seizing control of the House a little more than a year ago, the Dems appear despondent and scattered – an impression not helped by the embarrassment in Iowa (how can you convince the country you’re ready to rule when you can’t even rig a goddamn caucus without the whole world finding out?).

Yet, just as we suspected, some of the most memorable moments from Tuesday’s speech happened off the podium (and we’re not talking about Nancy Pelosi dramatically ripping up Trump’s speech because the president didn’t shake her hand).

One of those moments was just shared with the public by Rep. Rashida Tlaib, who said during a discussion on Friday that she and fellow Muslim Rep. Ilhan Omar huddled together in the audience during President Trump’s speech, as the president praised American strength, industry and ingenuity – qualities that the two radical Democratic lawmakers loath.

According to Tlaib, she and Omar sat together during the speech because they fully expected to be ‘triggered’ by Trump’s words. And just as they expected, there were “moments of triggering”.

“There were moments of triggering…I kept holding your hand…we intentionally sat next to each other to support each other.”

Here’s the clip:

Rep. Rashida Tlaib says that during the State of the Union, she had to hold hands with Ilhan Omar during “moments of triggering.” pic.twitter.com/jCgrYkRG32

We have a question for ‘the triggered’. What about people who are really in danger of being triggered? What about drug addicts whose lives could literally be placed in jeopardy if they’re triggered by something that makes them want to use? What do the intersectional feminists have to say about that?

Distortion: Investors Are Un-Cautiously Optimistic

Once again they took all the pain away.

As NorthmanTrader.com’s Sven Henrich notes, what looked like the beginning of a larger market correction, amid renewed reductions in global growth outlooks, was again aborted in its tracks by renewed panic interventions by central banks, namely the PBOC which injected vast amounts of liquidity, cut rates and banned short selling as the Fed continued on its track of massive repo liquidity injections and continued treasury bill buying and voila: New market highs.

The net effect was so violent that the previous week’s sell-off was forgotten by Monday morning, by Tuesday $NDX made new highs again, by Wednesday $SPX made a new all time close highs and by Thursday $DJIA, $SPX and $NDX all made new all time highs with most of the market gains for the week driven by magic overnight gap ups and marked by tight intra-day ranges. Nothing matters or so it seems.

The liquidity wave continues to dominate the market action, yet the warning signs keep mounting, the distortions keep expanding in a market that is dominated by a handful of stocks that control the index price action via historically unprecedented market cap expansion while the broader market shows marked weakness beneath.

Yields again croaked, not confirming any notion of reflation with the 10 year closing at 1.58%, banks didn’t make new highs, neither did small caps, or transports, the laggers keep lagging.

Are central banks and their interventions leading investors off a cliffI asked this week, as sentiment indicates desperation to buy every conceivable dip abandoning all sense of risk. Yet corporate insiders are selling strength and asset managers did not buy the rally to new highs, rather continued to reduce long exposure signaling that not all are in the ‘pile in at all cost’ camp.

Indeed Mohamed El-Erian, who previously urged investors to resist the temptation to buy this dip, put out another warning out on Friday:

In riding big liquidity-driven #markets, #investors should remember the surfer analogy:

The bigger the wave …

the greater the ride;

the more tempted you are to stay on;

the more uncertain the when and how it breaks; and

Only the best of surfers get off really smoothly.

Confidence is high, as it is in every market bubble, confidence that investors all can get off the train in time. So far this confidence continues to be validated as markets are continuing to avoid any damage that the fundamental global economy would indicate while valuations remain historically stretched and central bank liquidity injections continue to control the price action.

Yet did this vertical surge in equity prices last week put in conditions for a larger sell-off still to come? Indeed did the rejection of new highs amid building negative divergences signal something more sinister? Or will the distortions in markets run unabated forever ignoring all risks?

For the technical market review please see the market video below:

Please be sure to watch it in HD for clarity. To get notified of future videos feel free to subscribe to our YouTube Channel. For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

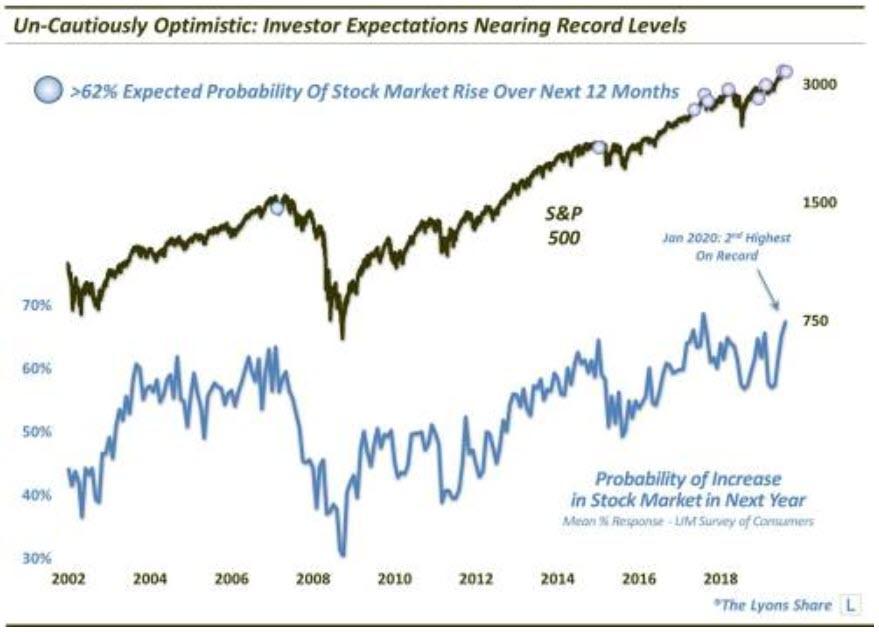

Markets, it is said, like to climb a “wall of worry”. Of course, the theory is that an abundance of worry on the part of market participants suggests that there is ample money “on the sidelines” available to enter the market and perpetuate a rally. Such a condition was arguably present this past fall as stocks were nearing the end of a months-long consolidation. The prolonged sideways market action seemed to inflict investors with a healthy dose of skepticism and caution towards the prospects for stock. That caution helped fuel the subsequent breakout and extended run to new highs that continues today. That caution, however, does not continue today.

In the monthly University of Michigan Survey of Consumers, one of the questions asked of respondents is their estimation of the “probability of an increase in the stock market in the next year”. In January, the mean response to the question reached 65.6%. That is the 2nd highest level on record since the inception of the survey question in 2002 (only the reading at the intermediate-term top in January 2018 was higher, at 66.7%).

Of course the concern is that once expectations get too high, it may be a sign that most of the potential investable dollars are already in the market. Therefore, there may be relatively little fuel remaining to boost stock prices.

Looking historically at the survey, we see that in addition to elevated reading in early 2018, high readings were also observed in July 2007, June 2015 and late 2018. Obviously, those immediately preceded either cyclical or major intermediate-term tops.

So is the market on the verge of a significant top? Only time will tell. Prior extreme bullish readings in the UM survey certainly have had a consistent record of preceding rough patches in the market. With that being said, sentiment can be an imprecise timing tool. There is no reason why stocks can’t continue to rally in the face of extreme optimism — temporarily. However, such a rally at this point would occur without the benefit of the proverbial wall of worry.

“Executions In Central Park”: MSNBC’s Matthews Warns Of Socialist Sanders ‘Dictatorship’ In Surreal Clip

MSNBC’s Chris Matthews shocked his fellow pundits Friday night following the New Hampshire primary debate by suggesting Democratic Socialist Bernie Sanders could erect a future dictatorship in which establishment political figures would be “executed”.

In a rant that has to be seen to be believed Matthews said of a potential Sanders presidency:

“You know, I have my own views of the word socialist and I’ll be glad to tell them, share them with you in private,” Matthews said. “They go back to the early 1950s. I have an attitude about them. I remember the Cold War. I have an attitude towards Castro, and I believe if Castro and the Reds had won the Cold War, there would have been executions in Central Park and I might’ve been one of the ones executed and certain other people would be there cheering. So, I have a problem with people who took the other side.”

Did Chris Matthews just imply Bernie Sanders is going to start assassinating people?? WTF?? pic.twitter.com/yuSIr9zLyp

Matthews then immediately pivots from the historical reference to “executions in Central Park” if “the Reds had one” back to Sanders.

“I don’t know who Bernie supports over these years. I don’t know what he means by socialism. One week it’s Den-mahk, we’re going to be like Den-mahk,” the MSNBC host said, mimicking Sanders’ Brooklyn accent. “Ok, that’s harmless. That’s basically a capitalist country with a lot of good social programs. Den-mahk is harmless.”

The self-styled moderate Democrat who in the past has admitted he’s “more conservative than people think I am” set off a firestorm of controversy among progressives who’ve pointed out both MSNBC and CNN’s consistently negative coverage, which in this instance devolved into suggesting that Sen. Sanders could start political executions and assassinations if he gets in power.

During the rant, Matthews leaves his fellow MSNBC panelists somewhat speechless and surprised at how far he took the Cold War analogy, though Chris Hayes meekly pushed back a bit:

“He’s clearly in the Denmark category,” Hayes gently pointed out.

“Is he?!” Matthews shot back.

“Yeah,” Hayes replied.

“How do you know? Did he tell you that?” Matthews pressed.

Matthews had clearly implied that Sanders himself “would be there cheering” on executions in Central Park if the Communists had won.

The live commentary Friday night immediately and predictably unleashed outrage among progressives and Bernie supporters online, confirming in their minds the mainstream’s conspiring to prevent a Bernie Sanders primary nomination for president.

However, it will be interesting to see the degree to which Trump himself taps into these same arguments against Sanders’ well-known socialist agenda should the Vermont senator actually become the Democratic Party nominee.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}