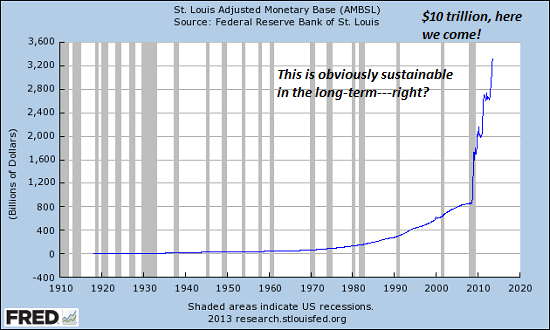

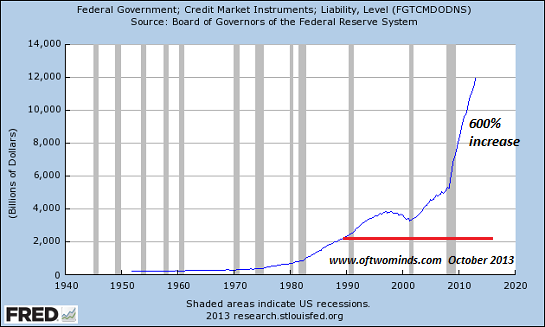

The US Federal Reserve Bank has been easing quantitatively (QE) for 4 years now, since 2009. Over this period, average daily trading volume in the US Treasury market has reduced from 500bln 10yr equivalents per day to 350bln 10yr equivalents. 350bln 10yr equivs may still seem like a big number…but this is a 30% decrease in trading volumes, and that is a reduction not only in volume, but liquidity. Some readers out there might think”so what?” or “whats the big deal if the US Treasury market is less liquid than it used to be?” The answer rests in the ultimate lenders of capital, and the structure of the Treasury market which is of great concern to participants of this market. Investors (yes, a rarely used word these days) prefer to invest in assets that are liquid, especially when that asset is designated as a “risk free” asset. Liquidity = ability to enter / exit at tight spreads without affecting the market price for the security. The US treasury market used to be the deepest most liquid bond market in the world. This characteristic of the UST market has significantly faded as QE has run its course, and the result is a reduction in actual “investors” of US government debt. This is partly why the US Fed is still doing QE. If the Fed doesn’t buy US govt bonds…who will? The value of the USD has been cheapened by QE, and that significantly increases the risk in holding UST debt. Think about that for a moment..the US Fed’s actions have increased the risk of holding UST paper. UST paper is supposed to be the “risk free” asset against which everything else is judged. If the “risk” of holding the “risk free asset” increases…how are investors to measure “risk.”

I will leave it to the reader to draw parallels to the situation as it is currently playing out in Japan.

The Fed engaged in QE for 4 specific goals.

1) Push investors out the credit curve (from UST –> corp bonds –> Stocks)

2) Reduce / keep down interest rates to fund US Govt spending

3) Increase inflation (for example, prop up the housing market)

4) Decrease unemployment

Of these 4 goals, #s 1-3 are credible. #4 is not so clear.

#5 is not a “goal” but an unintended side effect.

5) Reduced secondary market net supply while increasing supply of the currency = reduced trading volume = reduced liquidity

I suppose i could repeat the phrase, “when the only tool you have is a hammer…every problem looks like a nail”

Here is a direct example of #5

This week is the refunding for long term UST debt (10yr notes and 30yr bonds).

With the QE induced reduction in trading volume and liquidity, expect the remaining market trading participants to continue selling UST’s ahead of the auctions…to “make room” before bidding on bonds in the upcoming auctions (remember, primary dealers are required to bid for their pro-rata share of every auction…so about 5% each). As the US Fed continues to print USD to buy UST, the world incrementally loses trust in the value of the USD. Think of the tipping point (currently taking place in Japan as well).

Of course, there has been talk and speculation of the Fed reducing / ending their QE program. Unfortunately, there is no way for the US Fed to “exit” their QE program. The only exit option is to wait for the debt to mature and swap IOU’s with the US Treasury.

The market is a discounting function, in that it discounts future expected values in the current price of assets. This means that ultimately, when the market realizes that the Fed cannot exit its QE position (i’m amazed this hasn’t happened yet), the discounting function requires the price of UST debt to drop, yields to rise, and the currency to cheapen. And here is where the Fed holding a sizable portion of all outstanding UST debt becomes both a problem, solution, and problem again.

1) Problem: QE reduces value of the currency, and thus (reduces desire / increases risk) of holding long term US govt debt.

2) Solution: the central bank steps in and buys the long term debt, inflating financial assets

3) Financial asset inflation translates into consumer price inflation

4) Problem: –> see problem #1

5) The modern world hasn’t figured out #5 yet, however Japan is on the path to experience #5 before the US.

It is hard to imagine life in the US falling over due to financial failure, as happened in Greece and Cyprus. Of course in the US it would be slightly different, as the US can print money and inflate away certain problems. The scary part is when those who have been inflated out of being able to survive get hungry enough to riot…that is when chickens in the US will come home to roost. This is a slowly building phenomenon…it does not happen overnight. And every slowly building phenomenon has a “tipping point.”

Back to the markets….

As volume and liquidity decrease with the path of QE, we continue to get closer to the moment when the market actually discounts this reality. This is the only reason US bond yields are as low as they are (the same could be said for European Govt bonds). The market hasn’t fully discounted this “non-exit exit.” Similar statements could be said about the situation in Spain, France and Italy. Amazing our ability for cognitive dissonance, no?

While this all sounds oddly familiar to a ponzi scheme (the kind that goes along fine until one day it implodes)…the effect today is a reduction in both liquidity and trading volume which has created “volatility gaps” or “bifurcated volatility” This is simply recognizing the path that we are currently on. I don’t expect the govt (US, Europe, China or Japan) to reverse course…its just important to recognize where we are on the path.

Here is the real purpose of this article….how should i change my trading strategy to adapt to this new volatility regime?

Until recently, the average daily trading range for 10yr note futures (the most liquid UST security) was 20 ticks or about 8 bps (a tick here is 1/32nd of 1 USD of face). Of course when we say “average” that implies some daily vol ranges are bigger than 20 ticks…and some are smaller. Days with significant ECO data (NFP, FOMC, large duration auctions, Housing data, CPI, ect..) expect larger than average trading ranges and volatility. Days with less significant ECO data expect less volatility and smaller trading ranges. This basic concept still holds true today…but the gap in average volatility between a big vol day and a small day has increased (much like the gap between the rich and the poor). In today’s market, a large vol day might see a 12-16bp range…and a “normal” small vol day might see only 3-5bp trading range. 5 years ago, these vol range were more like 5-8bps and 10-18 bps. The result is that during the intermittent “slow periods” the market is extraordinarily slow..and during high vol events, the market reprices so fast that large entities do not have the ability to change their position before the market has significantly repriced. This is what we call a reduction in liquidity. As a small individual trader, you may think this does not have a significant impact on your day-to-day life. But as an investor in the institution (do you have a bank account? do you have a pension fund?…then you do have a stake here) this affects us all as the cost of hedging interest rate risk has significantly increased.

So, as a day trader, how do we respond to this change in the structure of market volatility? It means that the average mean reversion trades have much smaller ranges. If you “need” to make X dollars per day trading…and intraday vol is reduced, then you must therefore trade larger size, with more

leverage to make up for the reduction in average volatility. This poses a problem to our internal risk manager. Increased size / leverage on your account means tighter stops in terms of price ranges (for example, risking 5k to make 15k). With larger size you will lose 5k faster if the market moves against you. So, this increases the probability that you will get stopped out, and thus decreases the expected value of your mean reversion trading strategy. An option is to not increase your trading size / leverage. However, with the smaller vol ranges, this implies that you will not be able to hit your revenue targets, and this has caused banks and hedge funds to look elsewhere for their trading / liquidity providing business. This is why trading volatility has decreased…market participants have simply gone elsewhere…which reduces not only trading volume but liquidity.

These conditions are what drive traders (liquidity providers) out of an illiquid market, and into a different, more liquid market. Illiquid Markets tend to be “sticky” when trading volumes are small..and “gap” when trading volumes increase.

So, what is my advice? You could either take your stake, pull out and go find another more liquid venue to trade (FX perhaps?). Trust me….you would not be the first. For the remaining traders…there is still opportunity..but that opportunity comes with increased risk. This is the hallmark of an emerging market (yes, we are still talking about the US Treasury market). This all sounds reminiscent of stories about traders who blew up when volatility “gapped.” LTCM is the most famous, but there are numerous others.

To be clear, i’m not advocating traders leave the UST market..i’m simply pointing out that market structure has changed…and in order to survive, we as traders (intraday liquidity providers) must either change with it….or be pushed into insolvency.

So how do we change our trading strategy with this decreased average volatility? We need to be more aggressive. This applies both during the slow mean reversion trading days, as well as the trending trading days. Gone are the days where you can sell a good pop…or buy a good dip. Now, you need to figure out your intended direction, and initiate trade closer to the middle. This of course increases the risk that you will get stopped out if you are making such decisions on a random basis. You have to “know” what will happen next. Does this describe how you “feel” about the US Treasury market?

Yup…still talking about the US Treasury market here. Surprised??

-GovtTrader

http://govttrader.blogspot.com/

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/YT4iK2akOMY/story01.htm govttrader

Suicides are

Suicides are

As President Obama’s

As President Obama’s If it’s not clear

If it’s not clear

{kind=link}