Is someone a little bit nervous ahead of the year’s most anticipated IPO?

![]()

|

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/BG8svnQTopE/story01.htm Tyler Durden

another site

Is someone a little bit nervous ahead of the year’s most anticipated IPO?

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/BG8svnQTopE/story01.htm Tyler Durden

Overnight Media Digest

WSJ

* Democratic senators took their complaints about the troubled launch of the federal health law directly to the White House, as some in the party warned they would face voter backlash next year if the problems weren’t fixed.

* The White House heralded President Obama’s phone call with Iranian counterpart Hasan Rouhani earlier this fall as a foreign-policy milestone born of a rush of last-minute diplomacy. But top National Security Council officials began planting the seeds for the exchange months earlier in a series of secret meetings and telephone calls.

* Cash is returning to emerging markets, sparking stock rallies and a surge in fundraising. Calm in the United States, combined with low rates, has spurred global investors to try to juice returns before the end of the year.

* China has approved two domestic fund managers to offer products in the United States that for the first time would give investors there indirect access to shares traded in Shanghai and Shenzhen.

* Nestlé is slimming down. The Swiss food giant has struck a deal to sell its struggling Jenny Craig diet business unit to North Castle Partners, a U.S. buyout firm.

* Wall Street’s bonus season should be a good one for those who manage other people’s money. But for many bond traders and merger bankers, 2013 could be a year to forget.

* Senior U.S. regulators are reviewing the risks associated with the asset management industry, including a preliminary study of some of its top players, like Fidelity and BlackRock .

* Wal-Mart Stores Inc suffered from a website glitch Wednesday that set off a shopping frenzy as customers tried to snap up expensive items, such as computer monitors and televisions, for less than $10.

* A Manhattan federal judge on Wednesday approved one piece of the $1.8 billion settlement between the Justice Department and hedge-fund group SAC Capital Advisors LP, saying whether or not he thinks the penalty is appropriate is “irrelevant.”

* Bank of America Corp Chief Executive Brian Moynihan painted a picture of modest economic growth in the U.S., but said he expects the Federal Reserve to continue its pace of bond buying until stronger signs of expansion appear.

FT

Twitter’s priced its initial public offering above the expected range at $26 per share on Wednesday, pushing its valuation to $18 billion as it capitalised on strong investor demand.

Royal Dutch Shell is expected to soon file a formal exploration plan with the U.S. government for the Chukchi Sea off the northwest coast of Alaska.

British credit data provider Experian agreed to buy U.S. healthcare data firm Passport Health Communications for $850 million on Wednesday, sending its shares down more than 6 percent amid fears that it had overpaid.

U.S. alternative asset manager Carlyle Group LP reported an 11 percent drop in third-quarter profit on Wednesday, hurt by fewer portfolio company sales and listings.

British discount retailer Poundland kick-started plans for a London share sale on Wednesday with its private equity owner Warburg Pincus picking investment banks Credit Suisse Group AG and JPMorgan Chase & Co to advise it on the listing that could value the company at between 700 million pounds and 800 million pounds ($1.1 billion to $1.3 billion), according to people familiar with the situation.

Brazil’s Vale SA reported its first quarterly profit increase in more than two years on Wednesday, as China’s steelmakers replenish stocks and aggressive cost-cutting plan at the world’s second-largest miner starts to pay off.

NYT

* Twitter’s initial public offering, which values the company at roughly $18 billion, is a sign of its maturity, even as it combats slowing growth.

* Giant retailer Amazon announced a program to pay independent bookstores to sell its e-books and popular reading devices.

* Federal prosecutors and SAC Capital Advisors cleared a legal hurdle on Wednesday after Judge Richard Sullivan said he would sign off on the civil portion of the hedge fund’s insider trading guilty plea and roughly $1.2 billion penalty.

* Google said it would appeal a French court’s ruling that it strip from its search results nine images of the former European racing chief Max Mosley.

* Certain products on the Walmart website displayed wildly low prices Wednesday morning, such as a kayak for $11 or a treadmill for $33, according to news reports and Walmart. There was even a $579 projector available for $8.85.

* Time Warner reported mostly upbeat earnings on Wednesday, and television was the biggest reason. The company reported earnings of $1.18 billion for the third quarter of 2013, compared with $822 million for the same quarter a year ago, a 44 percent increase.

* Video-rental chain Blockbuster will c

lose the 300 stores that it still has in the next two months, said the company’s owner, Dish Network.

* Wall Street’s financial advisers, asset managers and underwriting investment bankers can expect their 2013 bonuses to rise as much as 15 percent, according to a closely watched compensation survey to be released on Thursday.

* The move by the activist hedge fund Clinton Group to try to oust senior executives at the Internet and shopping network ValueVision is poised to become a bitter battle.

Canada

THE GLOBE AND MAIL

* Canadian Senators Mike Duffy, Pamela Wallin and Patrick Brazeau have been suspended without pay from the Senate over their expense claims, but they may have other avenues to collect money from the taxpayers of Canada.

* Canada is a global steward of the seas with the longest coastline in the world stretched along three oceans, but that role is at risk, says a new report.

Reports in the business section:

* Canada’s crude oil discount is back with a vengeance, as pipeline congestion, recent refinery fires and ever-increasing supply from the oil sands hammer prices.

* Canada’s Chemtrade Logistics Inc is in advanced talks to buy General Chemical Corp, two people familiar with the matter said on Wednesday, in a deal that could value the specialty chemicals maker at around $1 billion.

NATIONAL POST

* The Parti Quebecois’ controversial charter of values is being rebranded, and its official new name is less than succinct. It will be tabled on Thursday as a bill in the legislature under the formal title: Charter Affirming the Values of Secularism and the Religious Neutrality of the State, as Well as the Equality of Men and Women, and the Framing of Accommodation Requests.

* Los Angeles may be home to three-hour traffic delays and Toronto may host perpetually backed-up downtown thoroughfares, but according to a new report by a Netherlands-based GPS manufacturer, traffic congestion in Metro Vancouver beats them all.

FINANCIAL POST

* British Columbia is touting an immense oil and gas resource identified by a new study of the province’s emerging shale prospects as a competitive advantage in the race to develop a liquefied natural gas industry.

* Qatar Holding LLC, a foreign arm of the Qatar Investment Authority, will buy about $200 million of an offering of convertible debentures announced by BlackBerry earlier this week, according to a report by the Sovereign Wealth Fund Institute.

China

SHANGHAI SECURITIES NEWS

– Two academic institutions on Wednesday started issuing China’s first ocean development index, the Xinhua Ocean Development Index, which rose 23.18 percent a year on average from 2006 to 2011, faster than an annual 10.52 percent growth in China’s gross domestic product (GDP) during the period.

– China’s big four state banks extended 182 billion yuan ($29.8 billion) in new local-currency loans in October, the lowest monthly lending in 2013, mainly due to seasonal factors which typically make banks’ deposits drop in October.

CHINA SECURITIES JOURNAL

– Some mainland Chinese banks, including Agricultural Bank of China, Bank of China and China Development Bank, may win approval to issue bonds in Taiwan before the end of this year — the first time for Chinese companies to float debt in Taiwan.

– China Life Anbao Fund Management Co, the first Chinese stock mutual fund owned by an insurer, China Life Insurance (Group) Co, was established on Wednesday.

CHINA BUSINESS NEWS

– The Hong Kong Stock Exchange plans to start evening trading in yuan futures early next year in the latest sign of the rising global status of the Chinese currency.

CHINA DAILY

– China plans to raise its whole-year target of installed solar capacity to 12 gigawatts in 2014, an increase of 20 percent from the original target, in an attempt to stimulate the sector.

PEOPLE’S DAILY

– A commentary by this mouthpiece of the Chinese Communist Party urges officials to stop pursuing achievements during their terms at the cost of environment so as to win promotions — a common practice in China at present.

Fly On The Wall 7:00 AM Market Snapshot

ANALYST RESEARCH

Upgrades

American Eagle (AEO) upgraded to Buy from Hold at Brean Capital

HomeAway (AWAY) upgraded to Strong Buy from Outperform at Raymond James

Parker-Hannifin (PH) upgraded to Buy from Hold at Jefferies

Rocket Fuel (FUEL) upgraded to Outperform from Perform at Oppenheimer

Synaptics (SYNA) upgraded to Overweight from Neutral at JPMorgan

Two Harbors (TWO) upgraded to Buy from Neutral at Sterne Agee

Williams-Sonoma (WSM) upgraded to Buy from Hold at BB&T

Downgrades

51job (JOBS) downgraded to Underweight from Equal Weight at Morgan Stanley

Abercrombie & Fitch (ANF) downgraded to Underperform from Buy at BofA/Merrill

Aimco (AIV) downgraded to Sector Perform from Outperform at RBC Capital

Devon Energy (DVN) downgraded to Neutral from Outperform at Credit Suisse

Garmin (GRMN) downgraded to Neutral from Buy at BofA/Merrill

Genesis Energy (GEL) downgraded to Market Perform from Outperform at Wells Fargo

IAMGOLD (IAG) downgraded to Underweight from Equal Weight at Barclays

InnerWorkings (INWK) downgraded to Market Perform from Outperform at William Blair

Meadowbrook Insurance (MIG) downgraded to Neutral from Buy at Compass Point

SkyWest (SKYW) downgraded to Market Perform from Outperform at Raymond James

Talisman Energy (TLM) downgraded to Sector Perform from Outperform at RBC Capital

Initiations

Manitowoc (MTW) initiated with an Outperform at Credit Suisse

TripAdvisor (TRIP) initiated with a Hold at Cantor

Twitter (TWTR) initiated with a Buy at Cantor

Twitter (TWTR) initiated with an Outperform at RBC Capital

HOT STOCKS

Toll Brothers (TOL) agreed to purchase Shapell Homes for about $1.6B in cash

RDA Microelectronics (RDA) received acquisition proposal of $18 per ADS from Unigroup

Nestle (NSRGY) solds Jenny Craig in North America and Oceania, terms not disclosed

AES Corp. (AES) to sell Cameroon businesses for $220M of net equity proceeds

Activision Blizzard (ATVI) sees ‘challenging’ Q4 due to increased competition

Siemens (SI) sees FY14 earnings growth at least 15%, plans EUR 4B share buyback over next 24 months

Qualcomm (QCOM) sees lower growth rate in 2014, sees completing $4B in stock repurchases in FY14

Whole Foods (WFM) raised dividend 20%, announced additional $500M share repurchase, sees 33-38 store openings in FY14, 35-40 in FY15

YRC Worldwide (YRCW) met with International Brotherhood of Teamsters, postponed Q3 earnings call

EARNINGS

Companies that beat consensus earnings expectations last night and today include:

Prestige Brands (PBH), Towers Watson (TW), Brookdale Senior Living (BKD), Prudential (PRU), Sanchez Energy (SN), EOG Resources (EOG), Transocean (RIG), Omega Protein (OME), Genco Shipping (GNK), Giant Interactive (GA), EnerSys (ENS), Activision Blizzard (ATVI), Primerica (PRI), ProAssurance (PRA), Walter Investment (WAC), Genpact (G), Whole Foods (WFM)

Companies that missed consensus earnings expectations include:

Fairway Group (FWM), Coty (COTY), Visteon (VC), Delek US (DK), Checkpoint Systems (CKP), Kronos Worldwide (KRO), Cal Dive (DVR), Willbros Group (WG), BioScrip (BIOS) Neenah Paper (NP), Luby’s (LUB), tw telecom (TWTC), Markel (MKL), Flotek (FTK), Rosetta Stone (RST), American Water (AWK), PHH Corp. (PHH), Qualcomm (QCOM)

Companies that matched consensus earnings expectations include:

Corrections Corp. (CXW), ACADIA (ACAD), CenturyLink (CTL), ARC Document Solutions (ARC), Noo

dles & Company (NDLS), Envestnet (ENV), CBS (CBS)

NEWSPAPERS/WEBSITES

SYNDICATE

Twitter (TWTR) 70M share IPO priced at $26.00

Armstrong World (AWI) files to sell 6M shares of common stock for holders

Carrizo Oil & Gas (CRZO) 4.5M share Secondary priced at $44.00

Diamondback Energy (FANG) 2M share Secondary priced at $53.46

Forum Energy (FET) files to sell 6M shares of common stock for holders

Glowpoint (GLOW) files to sell 6.43M shares of common stock for holders

Hospitality Properties (HPT) files to sell 8M shares of common stock

Ikanos(IKAN) 25M share Spot Secondary priced at $1.00

Integra LifeSciences (IART) 3.5M share Secondary priced at $40.00

Intuit (INTU) files to sell 116K shares of common stock for holders

KAR Auction (KAR) 23.9M share Spot Secondary priced at $27.60

LGI Homes (LGIH) 9M share IPO priced at $11.00

MRC Global (MRC) files to sell 17.49M shares of common stock for holders

Mavenir Systems (MVNR) 5.45M share IPO priced at $10.00

Midcoast Energy (MEP) 18.5M share IPO priced at $18.00

Millennial Media (MM) files to sell 24.75M shares of common stock for holders

Norcraft (NCFT) 6.4M share IPO priced at $16.00

Ramco-Gershenson (RPT) files to sell 4.5M shares of common stock

Tableau Software (DATA) 7.7M share Secondary priced at $65.00

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/3vfhNQP_dnk/story01.htm Tyler Durden

Moments ago the Czech Republic officially entered the global currency wars with the first currency intervention in 11 Years

This has led to the biggest Koruna drop in 4 years. Whoever was long the EURCZK, take the rest of the day off:

Some more from Bloomberg:

Full statement here:

CNB keeps interest rates unchanged, decides on interventions

The CNB Bank Board decided at its meeting today to keep interest rates unchanged. The two-week repo rate was maintained at 0.05%, the discount rate at 0.05% and the Lombard rate at 0.25%.

The Bank Board also decided to start using the exchange rate as an additional instrument for easing the monetary conditions. The CNB will intervene on the foreign exchange market to weaken the koruna so that the exchange rate of the koruna against the euro is close to CZK 27.

The history of the settings of the main instruments of monetary policy and the Bank Board minutes are available at

http://www.cnb.cz/en/monetary_policy/instruments/index.html#mpi

http://www.cnb.cz/en/monetary_policy/bank_board_minutes/index.html

Repo rate: The CNB’s key monetary policy rate, paid on commercial banks’ excess liquidity as withdrawn by the CNB in two-week repo tenders.

Discount rate: A monetary policy rate which as a rule represents the floor for short-term money market interest rates. The CNB applies it to the excess liquidity which banks deposit with the CNB overnight under the deposit facility.

Lombard rate: A monetary policy interest rate which provides a ceiling for short-term interest rates on the money market. The CNB applies it to the liquidity which it provides to banks overnight under the lending facility.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/W7oCLJ2eL-o/story01.htm Tyler Durden

When it comes to US equities today, the picture below summarizes it all…

… the only question is whether the NYSE breaks to celebrate the year’s overhyped social media IPO.

Aside from the non-event that is the going public of a company that will likely not generate profits for years, if ever, the overnight market has been quiet with all major stock indices in Asia trading modestly lower on the back of a modestly stronger dollar, although the main currency to watch will be the Euro (German Industrial production of -0.9% today was a miss of 0.0% expectations and down from 1.6% previously), when the ECB releases its monthly statement at 7:45 am Eastern when it is largely expected to do nothing but may hint at more easing in the future. On the US docket we have the weekly initial claims (expected at 335k) which now that they are again in a rising phase, have been the latest data item to be ignored in the Bizarro market, as well as the latest Q3 GDP estimate, pegged by consensus at 2.0%.

Key US Events

Market Recap from RanSquawk:

Stocks traded lower in Europe this morning, although financials outperformed and credit spreads tightened as market participants positioned for the upcoming ECB policy decision. Financials were supported by an encouraging set of earnings by Commerzbank, SocGen and Credit Agricole, with Commerzbank also seen among the best performing stocks in the German DAX index this morning up over 9%. Even though the benchmark borrowing rate is expected to be held unchanged by the ECB, the Euribor curve flattened, albeit marginally. At the same time, Bunds failed to benefit from the risk averse sentiment and traded near the unchanged mark as market participants not only awaited the outcome of policy meetings by the BoE and the ECB, but also digested supply from Spain and France. Going forward, apart from awaiting monetary policy decisions, attention will also be paid to the release of the latest weekly jobless data, as well as the 1st estimate of Q3 US GDP growth from the US.

Overnight bulletin summary from RanSquawk and Bloomberg

Asian Headlines

Moody’s senior VP Byrne said that Japan needs more tax revenue from companies and also needs more fiscal discipline.

EU & UK Headlines

German Industrial Production SA (Sep) M/M -0.9% vs. Exp. 0.0% (Prev. 1.4%, Rev. 1.6%)

German Industrial Production WDA (Sep) Y/Y 1.0% vs. Exp. 0.8% (Prev. 0.3%, Rev. 0.9%)

Eurogroup head Dijsselbloem said Greece is unlikely to see a debt writedown, with little support for such a writedown.

Spanish bond auction results, sells EUR 4.03bln vs. Exp. EUR 3-4bln.

– Sells EUR 2.38bln in 3.75% 2018, b/c 1.9 (Prev. 2.47) and avg. yield 2.871% (Prev. 3.059%)

– Sells EUR 1.15bln in 4.4% 2023, b/c 2.6 (Prev. 1.96) and avg. yield 4.164% (Prev. 4.269%)

– Sells EUR 0.507bln in 5.90% 2026, b/c 2.4 (Prev. 1.55) and avg. yield 4.469% (Prev. 4.540%)

French bond auction results, sells EUR 6.49bln vs. EUR 5.5-6.5bln.

– Sells EUR 4.283bln in 2.25% 2024 (new line), b/c 1.975 (Prev. 1.88) and avg. yield 2.41% (Prev. 2.37%)

– Sells EUR 2.21bln in 3.25% 2045, b/c 1.891 (Prev. 2.28) and avg. yield 3.41% (Prev. 3.60%)

US Headlines

More than a dozen anxious Senate Democrats facing re-election next year met with President Obama at the White House Wednesday to review the administration’s progress in fixing technical problems hobbling the rollout of the Affordable Care Act.

Equities

Stocks traded lower in Europe this morning, though the stock index in Germany outperformed following an encouraging set of earnings by Siemens, Commerzbank and Adidas. Consumer goods led the move higher, also largely driven by earnings with Continental and Adidas among the best performers there.

In terms of the European reporting season, analysts at Deutsche Bank note that sales beats are at historic lows of 36% (vs. long-term average of 59%), with EPS beats at 50% (vs. long-term average of 57%). The US remains stable with EPS beats at 75%, slightly ahead of the long-term average. Sales beats (54%) have improved marginally in the last week.

Finally, Twitter raised USD 1.82bln in its IPO after 70mln shares were

sold at USD 26 each. For more US equity related stories see Daily US Equity Opening News at 1400GMT/0800CST.

FX

EUR/USD and GBP/USD traded steady, as market participants refrained from making a directional commitment ahead of the key risk events.

EUR/GBP implied 1m vols fell below the 100DMA line this morning, though

the trend remains in a bullish price pattern. Looking elsewhere, AUD underperformed overnight following the release of weaker than expected jobs data out of Australia which showed Employment Change at 1.1K vs. Exp. 10.0K.

Commodities

China October 21-31 average daily steel output at 2.098mln tonnes which is down 0.4% from the previous 10 days, according to China Iron and Steel Association data.

China’s importers of refined copper have been asked by Codelco to cut term shipments in the H1 of 2014, according to sources.

Ahead of talks between the P5+1 and Iran due to begin today, a senior US administration official said the US wants first steps from

Iran to be the halting and rolling back of parts of its nuclear

programme. The official added that the US is willing to offer reversible sanction relief if Iran takes acceptable steps on its nuclear programme.

China’s CNOOC to raise natural gas supplies by 22% to 12.8bcm over winter demand period.

Libya’s state-oil NOC resumes loading at the 160,000 bpd capacity Mellitah port.

There is no obvious link between the EUR22bn order book for the Italian sovereign retail bond (named BTP Italia) and the warning by the head of Italy’s business association yesterday that the country is in a ‘worrying’ deflationary situation. But as Portugal 10y benchmark yields fell by another 22bp to below 6%, the subtle message is that investors are rushing to pick up yield in whatever credit they can as deflation worries intensify. Is the ECB equally as worried or does it believe that the drop in annual CPI to 0.7% in October is transitory?

Only 3 out of 70 strategists and economists expect the ECB to cut rates today, but this does not hide the fact that many expect the bank to prepare the ground for a rate cut in December, before possibly announcing another LTRO in the New Year. The logic is straightforward: with inflation moving further away (down) from the ECB’s unique policy target of below but close to 2%, it will take more time for inflation to return to 2% over the relevant policy horizon. Therefore, lower rates can be justified. The NZD, AUD and GBP are better currencies to express short EUR views than vs the USD, at least until we get US payrolls data out of the way tomorrow. With investors already braced for a dovish message, the skew is for a EUR squeeze higher on a more neutral statement from Draghi and outlook for inflation that will require no major adjustment. That was, after all, the message from the European Commission on Wednesday, even with a 2014 EUR/USD assumption of 1.36.

From the US today we have the advance estimate of Q3 GDP. Our forecast is for 2.3% annualised growth, ahead of the 2.0% consensus. A negative surprise should see a pull back in US 10y swap rates and a flatter curve, though momentum is unlikely to be strong given that payrolls are due tomorrow. We look for initial claims to have risen to 340K.

In the UK, the BoE is expected to leave Bank Rate and the Asset Purchase Target unchanged at 0.50% and £375bn respectively. The basis for the MPC meeting today is the Inflation Report next week and so any reaction in sterling and swaps is likely to be delayed until then. We reiterate our view for lower EUR/GBP and wider UK/EU swap spreads.

The Czech National Bank (CNB) and the Malaysian central bank are also due to make their benchmark rate decisions. The CNB has had a loose monetary policy stance for some time with its benchmark rate at 0.05% and is unlikely to change its stance. However, a tight vote is expected on FX intervention as was the case in September. The Malaysian central bank is also expected to keep its policy rate on hold at 3.00%, which could add support for further gains in USD/MYR.

We conclude with Jim Reid’s overnight recap by way of Deutsche Bank

Today is the the main European action of the week i.e. today’s ECB meeting. We also have the 1st estimate of Q3 US GDP growth today and payrolls tomorrow so its fair to say that the relatively quiet week so far will likely spring into life before the weekend. For today, DB’s European Economics team expect the ECB to reiterate its easing bias but not to announce any concrete decisions, with forward guidance being maintained. In the press conference they anticipate greater focus on low inflation which should enhance the ECB’s lower for longer forward guidance message. They don’t expect any action on the fast shrinking LTRO’s. The policy move they see as most likely in the near future is a rolling forward of the fixed price, full allotment regime for liquidity which is currently scheduled to end in mid-2014. With the results of the AQR/EBA not being released until late 2014, they expect the full allotment regime to be pushed to mid-2015. They also expect the press conference to touch on the EUR exchange rate. But here, our economists expect Draghi to deflect the exchange rate’s relevance via its impact on inflation forecasts – again part of the ECB strategy to use the fear of lower inflation to strengthen the credibility of forward guidance.

As for US GDP, regular readers will be aware by now that the EMR focuses heavily on the nominal GDP print as well as the real number due to the need to try to erode the huge debt facing the developed world as quickly as is possible. Current consensus expectations are for 2% real growth with the price index 1.4% higher thus implying annualised nominal GDP of 3.4%. The first two quarters of the year have hovered at around 3% on this measure taking us back down to levels last seen in the early stages of the recovery in 2010. So if today’s number is at consensus it’s another very low nominal US GDP reading relative to history, albeit one that Europe would currently be very happy with. However a continued low reading should keep the Fed aware of their duel mandate responsibilities and maybe the Fed and the market should factor in low inflation into the taper debate more than they currently do. There seems to be an automatic assumption that inflation will return to ‘normal’ next year. So definitely one to watch today. For the record DB US economist’s are forecasting 3% real growth today – well ahead of consensus.

Ahead of today’s risk events, markets have been trading with a cautious tone. All major stock indices in Asia are ticking lower this morning led by the Hang Seng (-0.8%) and the TOPIX (-0.5%). On the fixed income side, USTs are slightly firmer across the curve as are ACGBs and JGBs which follows a mixed day for fixed income yesterday as markets debated the potential for a lower-for-longer rate path from the Fed. Following a volatile week, most Asian currencies are firmer against the USD overnight with the exception of the AUD which is down half a cent versus the greenback following a tick up in the Australian unemployment rate to 5.7% in the month of October. After gaining 0.3% yesterday on market chatter that the ECB will hold fire on further rate cuts today, EURUSD is broadly unchanged heading into today’s governing council meeting.

With one-third of the European Q3 reporting season behind us, DB’s equity strategist Jan Rabe has provided an update on corporate earnings performance. The conclusion is that European expectation beats remain well below their long-term averages for both EPS and Sales, while Asian and US beats are broadly in line with past reporting seasons. With 214 of the Stoxx600 companies having reported as of today, the European reporting season looks more and more likely to remain a weak one: Sales beats are at historic lows of 36% (vs. long-term average of 59%), with EPS beats at 50% (vs. long-term average of 57%). The picture is more upbeat elsewhere, The US remains stable with EPS beats at 75%, slightly ahead of the long-term average. Sales beats (54%) have improved marginally in the last week. In Asia, EPS beats now standing at 49% and Sales beats (54%) are slightly ahead of long-term average (53%).

Earnings aren’t really the main story at the moment with liquidity still the dominant theme. Indeed as equity markets push up against record highs and global credit indices trade at or near multiyear tights, it’s fair to say that financial conditions have eased considerably over the past few months. Indeed, close to a record number of corporates have been taking advantage of strong funding conditions to tap credit markets and a number of corporate have been issuing debt to buy back more expensive legacy debt. Bloomberg points out that this year’s rate of global corporate credit issuance is not too far from 2012’s record levels. Issuance this year to date of $3.31 trillion compares with $3.44 trillion in the same period of 2012, when a record $4 trillion of the debt was eventually issued. Interestingly, despite the volatility in Q2 and Q3, emerging market companies have issued $235bn of corporate bonds this year, already surpassing last year’s record (Financial Times).

Turning to today’s docket, up first will be Spanish and German industrial output numbers. Attention will then turn to the

BoE policy announcement which will be followed shortly after by the ECB meeting. Draghi holds his press conference 45 minutes after that. Note that Draghi will also be speaking later in the day at a conference organised by Germany’s Die Zelt newspaper. Stateside, we get initial jobless claims, and consumer credit numbers today, in addition to advanced Q3 GDP print. The Fed’s Dudley and Stein will be speaking today.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/m9SCSJBkBrY/story01.htm Tyler Durden

![]() Two weeks ago we learned that

Two weeks ago we learned that

the National Security Agency (NSA) has been spying on the

chancellor of Germany and on the president of the United States.

Last week we learned that it has spied on the Pope and on the

conclave that elected him last March. This week we learned that it

also has spied on the secretary general of the United Nations and

has hacked into the computer servers at Google and Yahoo. Andrew

Napolitano says this isn’t the government to which we

consented.

from Hit & Run http://reason.com/blog/2013/11/07/andrew-napolitano-asks-how-can-the-nsa-s

via IFTTT

In California, Lincoln High

In California, Lincoln High

School cheerleaders had planned to hold a car

wash fundraiser until the San Jose Environmental Services

Department stepped in. City officials say all such car washes

violate water discharge laws, which bar anything other than

rainwater from flowing into storm drains.

from Hit & Run http://reason.com/blog/2013/11/07/brickbat-talking-about-the-car-wash

via IFTTT

Newsday’s Lane Filler and Ross Clark of The

Times and The Spectator are the co-winners of Reason

Foundation’s 2013 Bastiat Prize, which honors the writing that best

demonstrates the importance of individual liberty and free markets

with originality, wit, and eloquence.

“Lane Filler and Ross Clark, each in their own way, channel the

spirit of Bastiat to communicate the importance of freedom to the

pursuit of happiness,” said Julian Morris, vice president of Reason

Foundation and founder of the Bastiat Prize.

Filler and Clark split $15,000 in prize money and received

engraved crystal candlesticks at the Reason Media Awards tonight in

New York City.

Dhiraj Nayyar of India Today was awarded

third-place and $1,000. Honorable mentions went to The

Economist’s Tamzin Booth, Stephanie Slade of

U.S. News and World Report, and The Atlanta

Journal-Constitution’s Kyle Wingfield.

Previous Bastiat Prize winners include Virginia Postrel, Anne

Jolis, Tom Easton, Bret Stephens, John Hasnas, A. Barton Hinkle,

Amit Varma, Jamie Whyte, Tim Harford, Mary O’Grady, Robert Guest,

Brian Carney, Sauvik Chakraverti and Amity Shlaes.

In celebration of Reason magazine founder

Lanny Friedlander, who passed away in 2011, the first-ever Lanny

Friedlander Prize was awarded

to Wired co-founders Louis Rossetto and Jane

Metcalfe for their impact helping people understand the power of

free minds and free markets

through Wired’s analysis of technology,

business, and culture.

from Hit & Run http://reason.com/blog/2013/11/06/lane-filler-ross-clark-win-bastiat

via IFTTT

Newsday’s Lane Filler and Ross Clark of The

Times and The Spectator are the co-winners of Reason

Foundation’s 2013 Bastiat Prize, which honors the writing that best

demonstrates the importance of individual liberty and free markets

with originality, wit, and eloquence.

“Lane Filler and Ross Clark, each in their own way, channel the

spirit of Bastiat to communicate the importance of freedom to the

pursuit of happiness,” said Julian Morris, vice president of Reason

Foundation and founder of the Bastiat Prize.

Filler and Clark split $15,000 in prize money and received

engraved crystal candlesticks at the Reason Media Awards tonight in

New York City.

Dhiraj Nayyar of India Today was awarded

third-place and $1,000. Honorable mentions went to The

Economist’s Tamzin Booth, Stephanie Slade of

U.S. News and World Report, and The Atlanta

Journal-Constitution’s Kyle Wingfield.

Previous Bastiat Prize winners include Virginia Postrel, Anne

Jolis, Tom Easton, Bret Stephens, John Hasnas, A. Barton Hinkle,

Amit Varma, Jamie Whyte, Tim Harford, Mary O’Grady, Robert Guest,

Brian Carney, Sauvik Chakraverti and Amity Shlaes.

In celebration of Reason magazine founder

Lanny Friedlander, who passed away in 2011, the first-ever Lanny

Friedlander Prize was awarded

to Wired co-founders Louis Rossetto and Jane

Metcalfe for their impact helping people understand the power of

free minds and free markets

through Wired’s analysis of technology,

business, and culture.

from Hit & Run http://reason.com/blog/2013/11/06/lane-filler-ross-clark-win-bastiat

via IFTTT

Submitted by Michael Krieger of Liberty Blitzkrieg blog,

The “authorities” can shut down website after website, but the tide of new technology and the human spirit itself cannot and will not be overcome. This is the hard lesson that statists and collectivists will be learning the hard way in the years to come, as decentralization and freedom stage a gigantic, peaceful revolution. A revolution that is already in full swing and gaining tremendous momentum with each passing day.

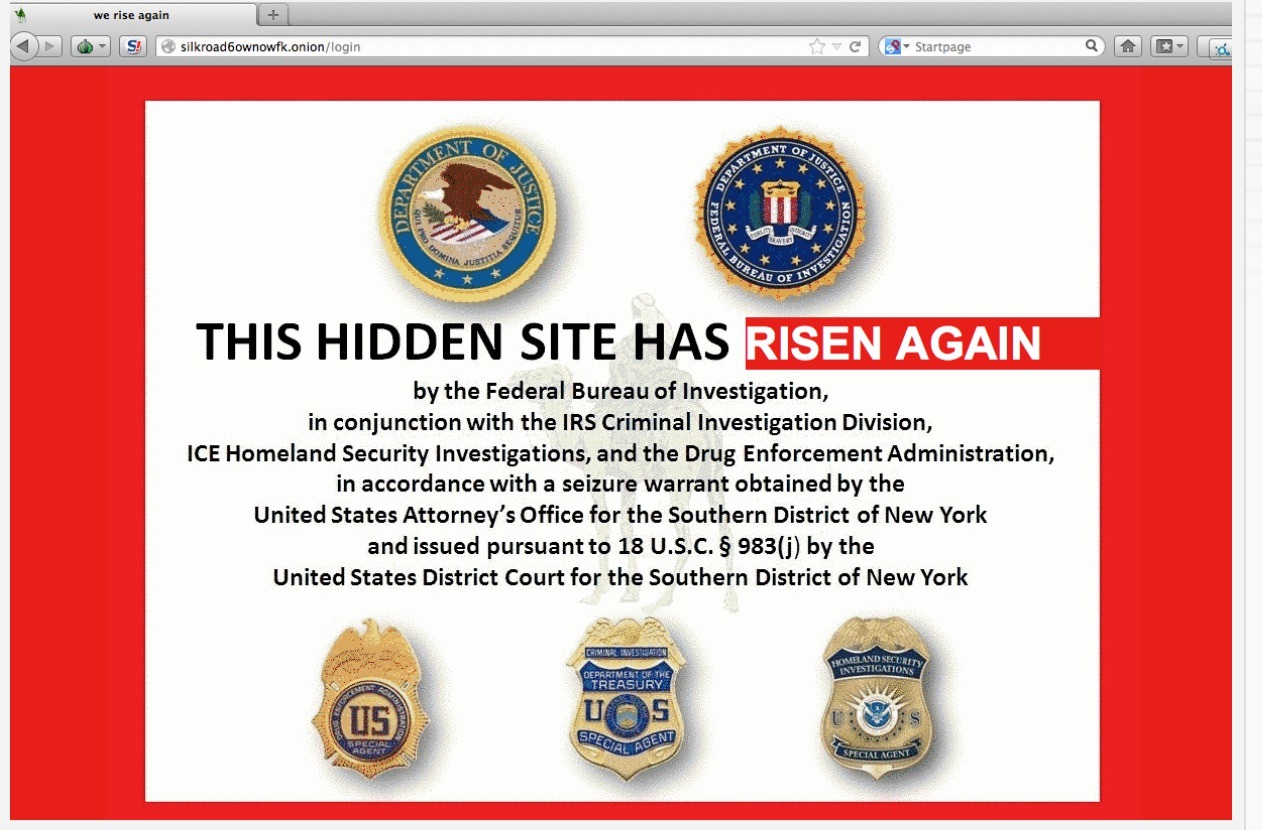

It took only a little over a month for Silk Road 2.0 to launch on the “dark web,” and there are already close to 500 illegal drug listings. As part of the new service there is even a new security feature that allows users to use their PGP encryption key as an extra authentication measure. The login page itself is even a parody of the Department of Justice’s seizure of the original site in early October. This is what you see when you visit:

More from Forbes:

On Wednesday morning, Silk Road 2.0 came online, promising a new and slightly improved version of the anonymous black market for drugs and other contraband that the Department of Justice shut down just over a month before. Like the old Silk Road, which until its closure served as the Web’s most popular bazaar for anonymous narcotics sales, the new site uses the anonymity tool Tor and the cryptocurrency Bitcoin to protect the identity of its users. As of Wednesday morning, it already sported close to 500 drug listings, ranging from marijuana to ecstasy to cocaine. It’s even being administered by a new manager using the handle the Dread Pirate Roberts, the same pseudonym adopted by the previous owner and manager of the Silk Road, allegedly the 29-year-old Ross Ulbricht arrested by the FBI in San Francisco on October 2nd.

The only significant visible change from the last Silk Road, spotted by the dark-web-focused site AllThingsVice that first published the site’s new url, is a new security feature that allows users to use their PGP encryption key as an extra authentication measure. It also has a new login page, parodying the seizure notice posted by the Department of Justice on the prior Silk Road’s homepage, with the notice “This Hidden Site Has Been Seized” replaced by the sentence “This Hidden Site Has Risen Again.”

“You can never kill the idea of Silk Road,” read the twitter feed of the new Dread Pirate Roberts twenty minutes before the site’s official launch.

Many more of Silk Road’s users seem reassured, however, by the fact that Silk Road 2.0 is being managed in part by known administrators from the original Silk Road, particularly a moderator known as Libertas who has served as one of the more vocal leaders of the Silk Road community since Ulbricht, the alleged Dread Pirate Roberts, was arrested.

Full article here.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/3o569LFwKZ0/story01.htm Tyler Durden

Chinese officials are worried. Not about inflation… not about growth… not even about pollution per se… but security. As the South China Morning Post reports, government officials are raising concerns about the function of its vast network of surveillance cameras because of the thick smog blocking visibility for some of them. In a truly central-planned world, there is nothing more dangerous that not being able to keep an eye on the population and officials fear that threat of terrorism could be heightened on smoggy days. Improving air quality in China has been often discussed but a new military team is looking for a solution (as security trumps health it would appear) – harsher punishments on polluters are needed to help improve air quality in China, a senior Chinese official said here on Tuesday.

So,

China Invasion 101 – Wait for a smoggy day…

To the central government, the smog that blankets the country is not just a health hazard, it’s a threat to national security.

Last month visibility in Harbin dropped to below three metres because of heavy smog. On days like these, no surveillance camera can see through the thick layers of particles, say scientists and engineers.

To the authorities, this is a serious national security concern.

…

Existing technology, such as infrared imaging, can help cameras see through fog or smoke at a certain level, but the smog on the mainland these days is a different story. The particles are so many and so solid, they block light almost as effectively as a brick wall.

“According to our experience, as the visibility drops below three metres, even the best camera cannot see beyond a dozen metres,”

…

The government has come to realise the seriousness of the issue and commissioned scientists to come up with a solution.

The National Natural Science Foundation of China funded two teams, one civilian and one military, to study the issue and has told the scientists involved to find solutions within four years.

…

“Most studies in other countries are to do with fog. In China, most people think that fog and smog can be dealt by the same method. Our preliminary research shows that the smog particles are quite different from the small water droplets of fog in terms of optical properties,” she said.

“We need to heavily revise, if not completely rewrite, algorithms in some mathematical models. We also need to do lots of computer simulation and extensive field tests.”

…

“On the smoggiest days, we may need to use radar to ensure security in some sensitive areas,” he said.

…

“It has to be a contingency device,” Zhang said.

And the harsher penalties are coming… (via English.cn)

Harsher punishments on polluters are needed to help improve air quality in China, a senior Chinese official said here on Tuesday.

Xie Zhenhua, deputy head of the National Development and Reform Commission, told a press conference less use of coal and emission reduction for automobiles were also crucial to tackle air pollution.

He said increased air pollutants caused by growing social consumption of fossil fuels were the main cause of the worsening smog, which has severely affected people’s health.

Those who take irresponsible decisions that lead to severe environmental consequences need to be punished according to the law, he said.

![]()

| |

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/0HeLVl221Iw/story01.htm Tyler Durden