Authored by Peter Schweizer via The Gatestone Institute,

-

For Ray Dalio, moral relativism is great for business.

-

Bridgewater’s business is investment funds. Having more of those in China means more money for Bridgewater. It is really that simple. But in China business deals are not done with fellow capitalists who are dedicated to economic liberty and the free flow of capital to its most rational uses.

-

Dalio is willfully ignorant defense of Chinese communism… it is the calculated hypocrisy of the rope-selling capitalist.

-

Major American businesses are more worried about the prospect for growing or even losing their Chinese business revenues than about standing up against tyranny abroad, the silencing of Americans at home, and the outspoken intention of the Chinese Communist Party to supplant the United States — and the freedom that comes with it — as the world’s preeminent nation.

-

Apple also bowed to the Chinese government’s demand to give it full access to the data of its customers in China, even banning apps that would allow ordinary Chinese citizens to bypass their government’s sophisticated surveillance.

-

This is in contrast to Apple’s refusal in 2016 of an FBI request to break into the encryption of its iPhone after a domestic terrorist mass shooting incident in San Bernardino, California. Tim Cook told Apple employees at the time that his refusal was based on civil liberties concerns, which apparently did not stop him from agreeing to the Chinese Communist Party’s demands.

-

“Of course, Apple and Nike publicly claim to decry slave labor. But to be clear, the behavior we are seeing from US corporations is not about a company surviving: It’s about discontent with just hundreds of millions of dollars, desiring instead billions of dollars.” — Jake Tapper, CNN, December 5, 2021.

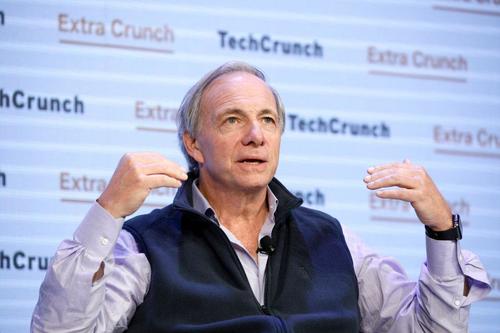

One of the sadder realities of modern business is seeing how China has managed to co-opt and make hostages of American capitalists dazzled by the riches of the Chinese market. Ray Dalio (pictured) of Bridgewater Associates is just the latest financial titan to play the “Who am I to judge how another country runs itself?” card. (Photo by Kimberly White/Getty Images for TechCrunch)

One of the sadder realities of modern business is seeing how China has managed to co-opt and make hostages of American capitalists dazzled by the riches of the Chinese market. Ray Dalio of Bridgewater Associates is just the latest financial titan to play the “Who am I to judge how another country runs itself?” card.

For Dalio, moral relativism is great for business.

Bridgewater’s business is investment funds. Having more of those in China means more money for Bridgewater. It is really that simple. In China, however, business deals are not done with fellow capitalists who are dedicated to economic liberty and the free flow of capital to its most rational uses. They are conducted with western-educated, government-tied, military-tied, intelligence-tied Chinese kingpins and princelings who understand their ultimate loyalty is to the Chinese Communist Party.

After the Wall Street Journal reported that Dalio had raised $1.25 billion to create Bridgewater’s third investment fund in China, Dalio was asked by a CNBC host the frequently asked questions about doing business in China, given its many human rights abuses. Dalio demurred, claiming “I can’t be an expert in these types of things.” When asked in the same interview about the Chinese regime “disappearing” tennis star Peng Shuai from the public view for a month, Dalio stuttered out the explanation that the Chinese regime is really “like a strict parent.” He even tossed in the moral relativist’s favorite argument:

“And then I look at the United States and I say, well, what’s going on in the United States and should I not invest in the United States because other things, err, human rights issues or other things?”

For a man once described by former FBI director James Comey as “one smart bastard,” Dalio’s willfully ignorant defense of Chinese communism looks pathetic. It is actually even worse than that — it is the calculated hypocrisy of the rope-selling capitalist.

Dalio is actually deeply knowledgeable about how things work in China. He has called Wang Qishan, the second most powerful man in the Chinese Communist Party, a “personal hero.” In his 2017 book, Principles, Dalio confessed, “Every time I speak with Wang, I feel like I get closer to cracking the unifying code that unlocks the laws of the universe.”

Jamie Dimon of JPMorgan might not have quite Dalio’s level of reverence for someone known throughout China as “Xi’s enforcer,” but Dimon came to understand the importance of the “Who am I to judge?” principle of business etiquette in China. While in Hong Kong recently, Dimon casually joked that “the Communist Party is celebrating its 100th year. So is JPMorgan [referring to the firm’s Chinese business]. And I’ll make a bet we last longer.”

That will not do. And sure enough, Dimon quickly walked back the comment. “I regret and should not have made that comment. I was trying to emphasize the strength and longevity of our company,” he said. A corporate spokesperson said the bank was committed to China and that Dimon had made clear during the discussion in Boston that “China and its people are very smart and very thoughtful… Dimon acknowledges that he should never speak lightly or disrespectfully about another country or its leadership,” the spokesperson added.

It is tempting to write off such obviously insincere apologies as simply a necessary part of business etiquette — the flattery necessary to make a buck in a hostile environment. That is what most Americans assume when they read stories about basketball star Lebron James upbraiding another NBA team’s general manager for supporting pro-democracy protesters in Hong Kong. James, who earns millions in licensing fees for jerseys and other items bearing his name and likeness in China, said that Houston Rockets’ GM Daryl Morey was “either misinformed or not really educated on the situation” regarding Chinese repression of dissent in the territory.

But this masks a darker implication: that major American businesses are more worried about the prospect for growing or even losing their Chinese business revenues than about standing up against tyranny abroad, the silencing of Americans at home, and the outspoken intention of the Chinese Communist Party to supplant the United States — and the freedom that comes with it — as the world’s preeminent nation. There is a dangerous parallel between the thought-policing that has been mainstreamed on American college campuses and the self-censorship of American business.

Apple’s Tim Cook pioneered the company’s entrance into China as Apple’s operations chief, which helped make Apple the most valuable company in the world. Apple now assembles nearly all of its products and earns a fifth of its revenue in the China region. Apple also bowed to the Chinese government’s demand to give it full access to the data of its customers in China, even banning apps that would allow ordinary Chinese citizens to bypass their government’s sophisticated surveillance. This is in contrast to Apple’s refusal in 2016 of an FBI request to break into the encryption of its iPhone after a domestic terrorist mass shooting incident in San Bernardino, California. Tim Cook told Apple employees at the time that his refusal was based on civil liberties concerns, which apparently did not stop him from agreeing to the Chinese Communist Party’s demands.

In 2015, President Xi stopped off in Silicon Valley before meeting with President Barack Obama, meeting the heads of Amazon, Airbnb, Facebook, and Microsoft. According to Matt Sheehan’s book, The Transpacific Experiment: How China and California Collaborate and Compete for Our Future, after Xi entered the gathering a thunderstruck Cook asked, “Did you feel the room shake?”

Viewed simply as the over-enthusiastic gushing of a businessman with dollar-signs for eyes, Cook’s swooning, Dimon’s kowtowing, or Dalio’s feigned ignorance of Chinese repression as “strict parenting” are cringeworthy enough. But with China flexing its muscles on the world stage more every day, one must wonder, is there any line they won’t cross?

It was all too much for Jake Tapper of CNN, who did not mince words in criticizing them all: “The millionaires and billionaires of Hollywood and the NBA and the IOC and Wall Street are all so eager for Chinese cash, they’re pretending none of this is happening,” he recently said.

“Of course, Apple and Nike publicly claim to decry slave labor. But to be clear, the behavior we are seeing from US corporations is not about a company surviving: It’s about discontent with just hundreds of millions of dollars, desiring instead billions of dollars.”

Tapper concluded, “There is no amount of money that can buy enough soap to wash that blood off their hands.”

* * *

Peter Schweizer, President of the Governmental Accountability Institute, is a Gatestone Institute Distinguished Senior Fellow and author of the best-selling books Profiles in Corruption, Secret Empires and Clinton Cash, among others.