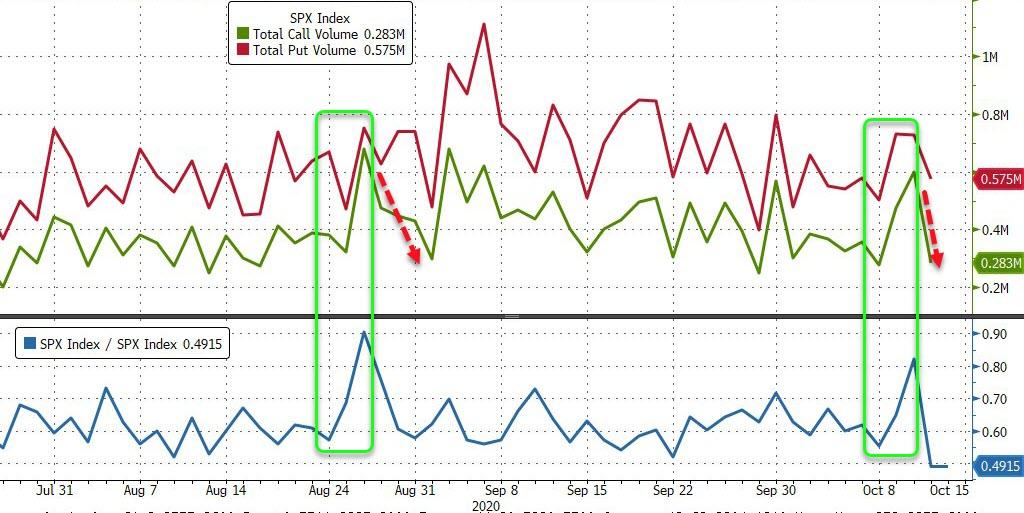

Mnuchin’s “difficult to get a deal done before the election” prompted weakness in stock markets but a glance at Nasdaq and it would seem that as op-ex looms on Friday, the ‘gamma-squeezers’ have backed off…

Source: Bloomberg

It’s a mad, mad world for sure…

While Trannies managed gains today, all the majors ended clustered together in the red, led by Nasdaq and Small Caps (ugly close)…

With The Dow and Small Caps back into the red for the week…

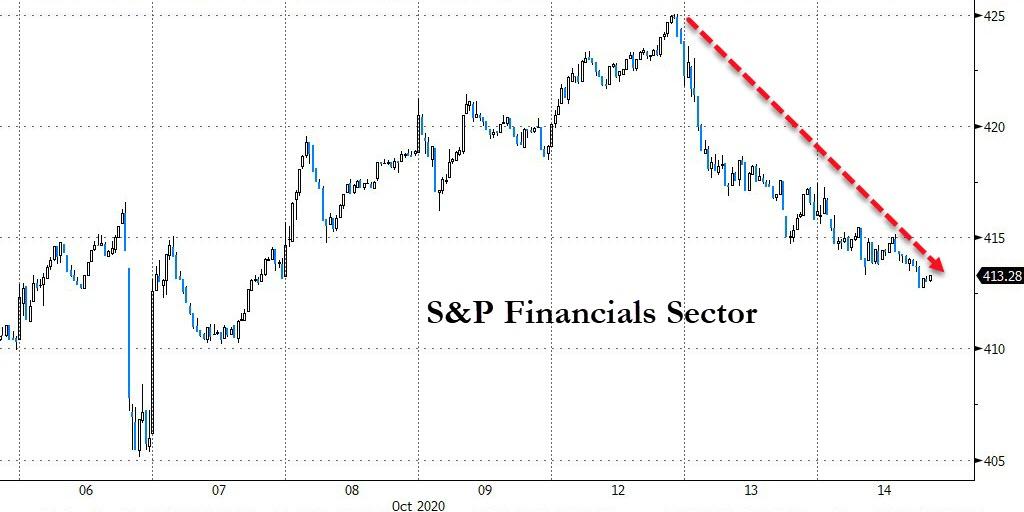

Banks were battered again…

Source: Bloomberg

Led by BofA and Wells Fargo…

Source: Bloomberg

Financials continue to track the Treasury curve…

Source: Bloomberg

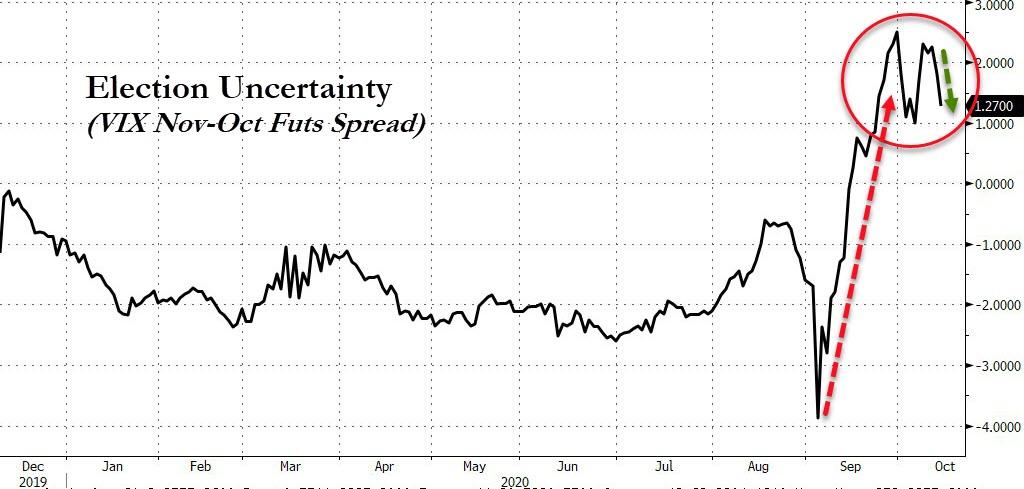

Election uncertainty improved modestly today but remains highly elevated…

Source: Bloomberg

HY bond spreads reached back to their tightest since COVID…

Source: Bloomberg

Treasury yields were modestly bid today, led the long-end…

Source: Bloomberg

With 30Y back at 1.50%…

Source: Bloomberg

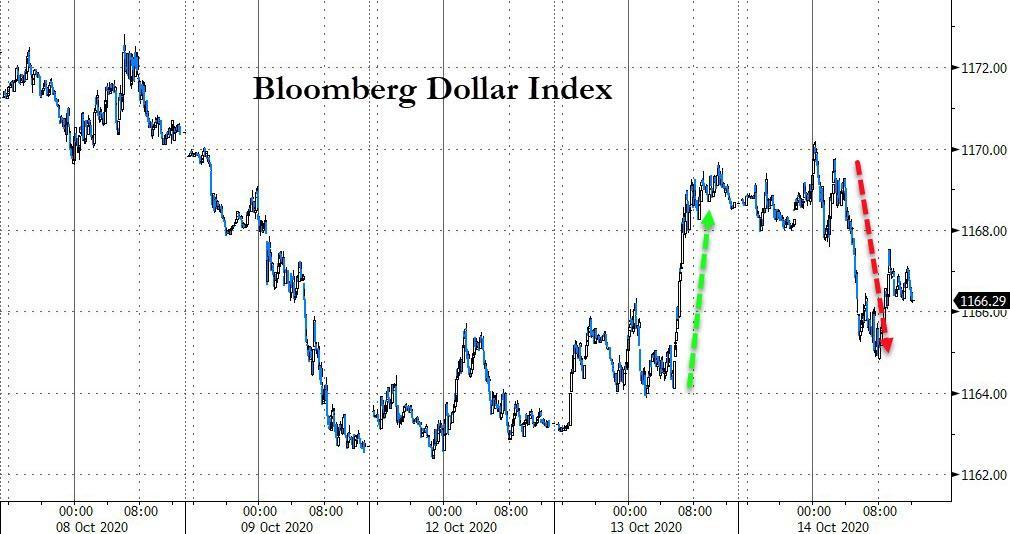

The dollar dumped today (as cable rallied), erasing yesterday’s gains…

Source: Bloomberg

Cryptos were broadly lower today…

Source: Bloomberg

Gold futures rallied back above $1900…

Silver futures bounced higher off $24…

And oil gained with WTI back above $41 ahead of tonight’s API inventory data…

Finally, “do you even lift?”

Source: Bloomberg

1000% since the March lows – ‘natural’ gains!

via ZeroHedge News https://ift.tt/317aKDk Tyler Durden

Traders Puzzled By “Mysterious Mega Flows” In Biggest Tech ETF Tyler Durden

Wed, 10/14/2020 – 15:40

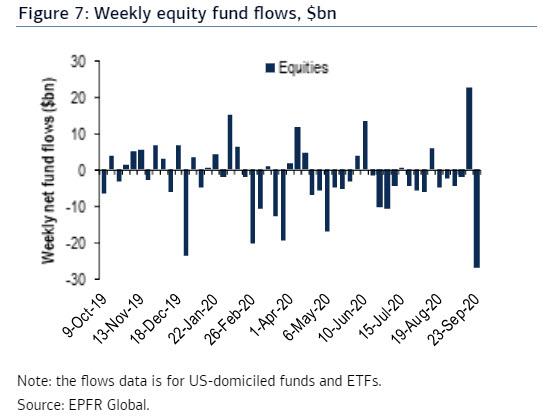

Three weeks ago, when looking at the latest EPFR fund flows we said that traders are getting whiplash after the “fastest ever fund flows swing from euphoria to despair” as US equity funds and ETFs reported $26.87 BN of outflows in the last week of September, the we observed the largest weekly outflow since December 2018 and the third largest outflow ever, more than reversing a $22.67bn inflow one week earlier; this was the third the biggest weekly swing in fund flows in history, and showed “how extreme market sentiment has become, and how it can seemingly swing overnight from euphoria to despair.”

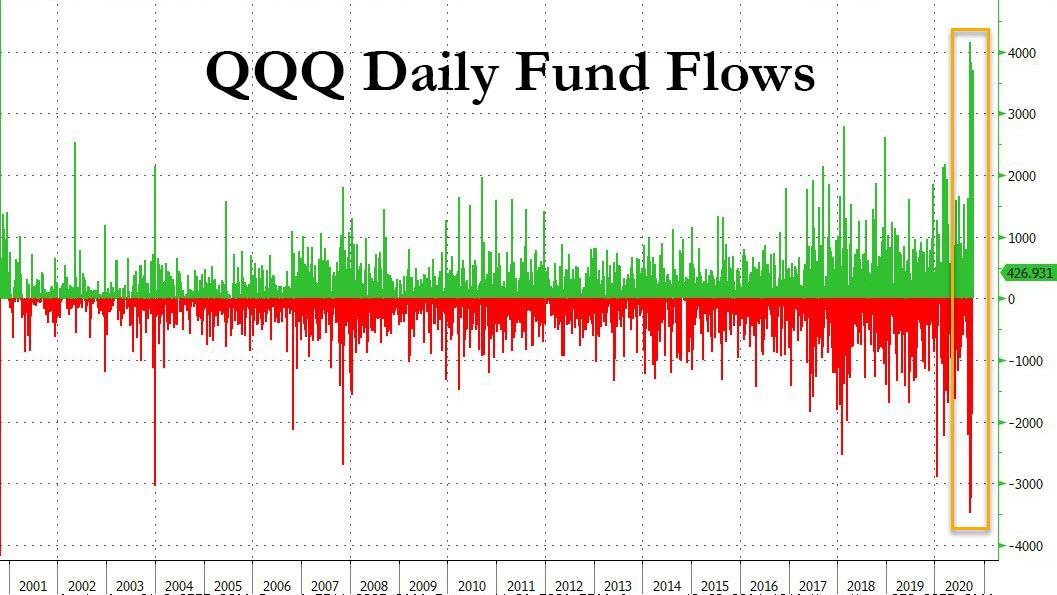

We also showed that similar, if even more acute swings, were observed in the QQQs the world’s largest tech ETF which tracks the Nasdaq, saying that “the QQQ fund posted record $3.5 billion outflows on Monday amid a Nasdaq slump, then got $4 billion the following day as sentiment recovered.”

In retrospect, this was not a bug but a feature, because today Bloomberg follows up on these wild swings, which have only gotten wilder since, and writes more than two weeks after our original observations that the “amount of cash cycling through one of the world’s largest exchange-traded funds is turning heads across Wall Street.”

According to Bloomberg’s calculations, the$146BN QQQ ETF, the largest tech ETF in the world, has seen a staggering $1.5 billion in daily flows (either in or out) over the past month, following the previously discussed largest withdrawal in two decades in late September, followed by its largest influx in the same time period one day later. The ETF saw $3 billion of inflows the following week, ahead of a $3 billion exit the next day. This week brought another $3.7 billion inflow in a single day.

The startling spike in the size of flows is clearly visible in the chart below, where the new “regime” is highlighted in yellow…

… with the consistency and sheer magnitude of the “mega flows” has analysts at odds over what’s driving them, Bloomberg’s Katherine Greifeld writes, “given that they don’t appear to line up with any rebalancing schedule or model portfolio shifts.

One possible explanation is that the recent surge in retail option trading has left the ETF as a hedging vehicle, while some say that renewed appetite among retail investors is fueling the flows. Others speculate that the cash churn amounts to a massive tug-of-war over the outlook for technology shares, which have staged a remarkable 73% rally since the March lows.

Another argument validating that this is largely a byproduct of retail traders is the just observed record inflows in the 3x inverse SQQQ Nasdaq ETF (see our post “Robinhooders Discover 3x Levered ETFs” from a month ago on how retail traders are flooding into 3x levered ETFs).

“That tells me there is a lot of day trading going on related to the Nasdaq 100,” said Tribeca Trade Group CEO Christian Fromhertz. “They’re super liquid and really move on Covid-related headlines.”

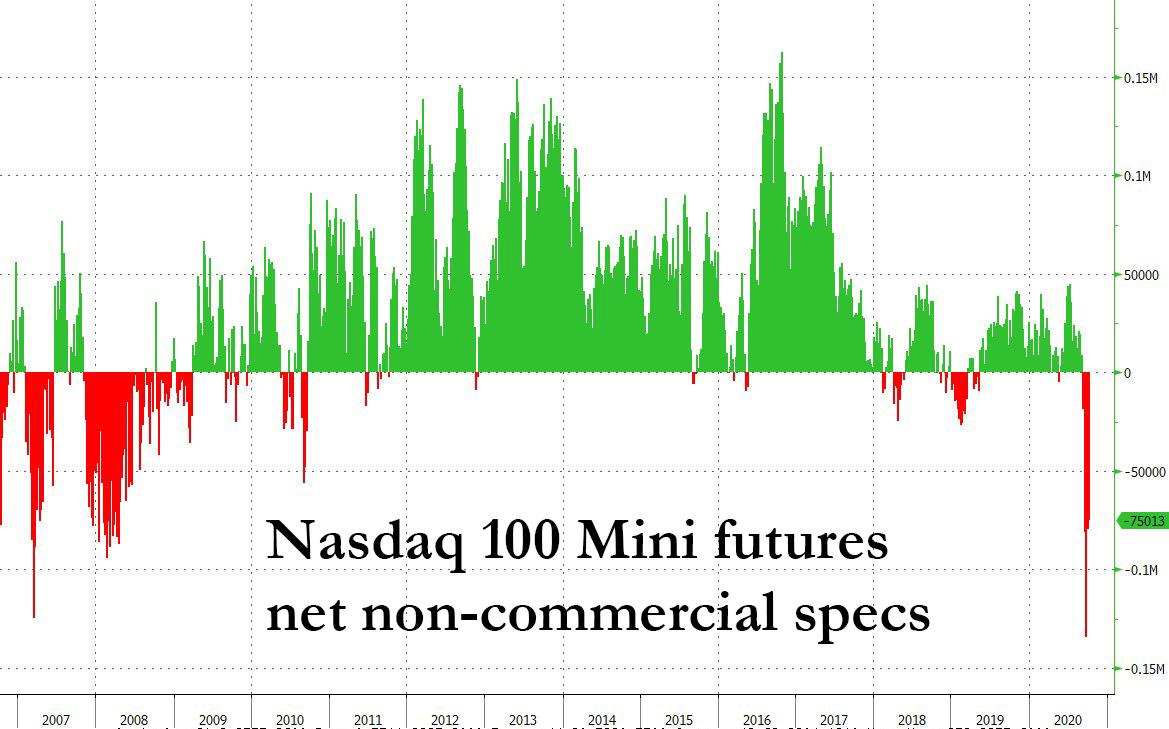

That said, options certainly play a role too. As Bloomberg explains, the “massive cash movements may be a byproduct of building options appetite” as roughly 3.7 million options contracts tied to Apple traded on Tuesday, well above the stock’s 20-day average of 1.95 million, in what many saw another attempt by SoftBank to forced a gamma short squeeze, which coupled with a near-record short position in Nasdaq futures unleased a massive 4% surge in the tech index.

Meanwhile, the latest sighting of “Nasdaq whale” SoftBank, meant that call open interest in Facebook, Amazon.com, Netflix, Alphabet, Apple and Microsoft averaged 12.9 million contracts over the 30 days through Friday, the highest since early 2019.

And here is another brief explanation of how dealer gamma works (for a much more comprehensive take, please read “All You Ever Wanted To Know About Gamma, Op-Ex, And Option-Driven Equity Flows.)” As Bloomberg notes, dealers selling calls will typically buy the underlying stock in order to delta hedge their position. However, with FAANGs comprising nearly half of QQQ, buying the ETF works as a “quick and dirty hedge,” according to Steve Sosnick.

“This is where the concentration comes into play,” said Sosnick, chief strategist at Interactive Brokers. “It would not be surprising that dealers would find themselves hedging the huge call activity with QQQ — especially when Facebook and Google followed along.”

Finally, it’s possible that this is nothing more than institutions using the QQQ to express a view on the future of the tech sector, and getting caught in the recent whiplash forcing them to be stepped out on both sides of the trade.

Whatever the reason, there is no sign of the outsized flows ending any time soon: “There’s a battle between top callers and those who believe tech has further to run,” said ETF Store president Nate Geraci. “The swings between massive inflows and outflows reflects that battle.”

via ZeroHedge News https://ift.tt/3nKoeOO Tyler Durden

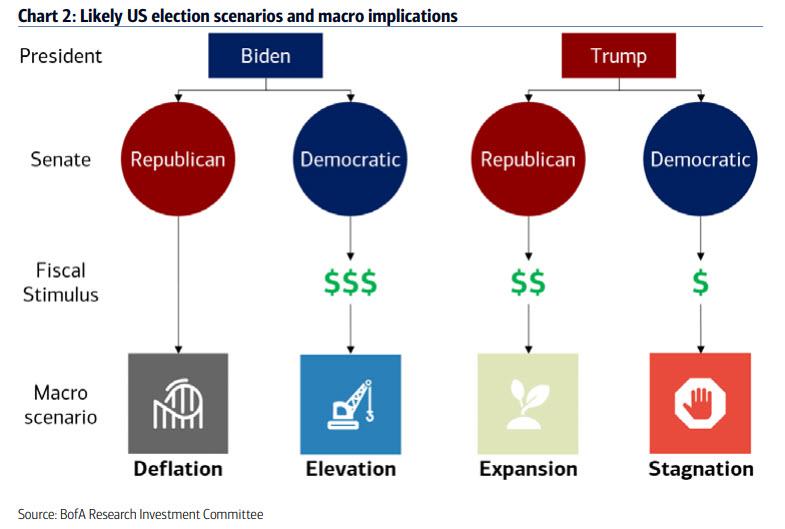

Here Are The 4 Election Scenarios For Markets, And How To Trade Them Tyler Durden

Wed, 10/14/2020 – 15:22

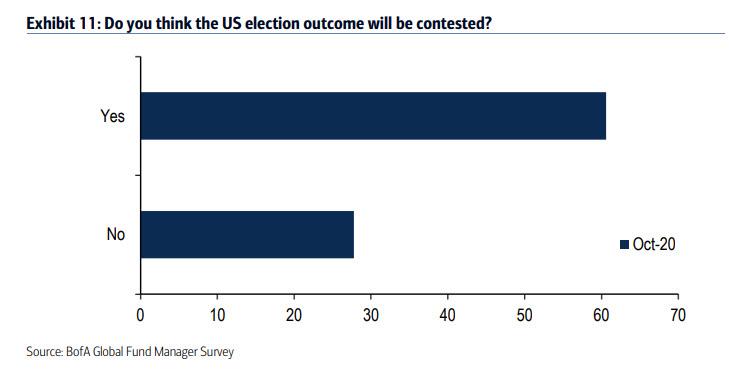

While the latest Fund Manager Survey from BofA revealed that a vast majority of investors are concerned about a contested election, and the resulting volatility this may entail especially if (when) the Supreme Court is called in to decide the next president…

… no matter the ultimate outcome, investors are curious how to trade – and hedge – the various possible outcomes, so much so that BofA’s Jared Woodard writes that the impact of various election scenarios is the “top question investors are posing.”

So, in the latest note from BofA’s Research Investment Committee, Woodard and team proceed to give an answer, highlighting that the most important consequence of the US election “will be the amount and composition of fiscal stimulus” and noting that since Congress controls the budget and the House majority is likely to stay Democratic, the Senate outcome is the most important one to watch. The 4 key scenarios are laid out in the chart below, whose investment implications BofA dissects next:

Before going into the details, Woodard gives some “general tips for investing around elections”:

For a trade, buy political dips;

For an investment, watch the first 200 days;

Don’t touch the core portfolio.

With that in mind let’s dig in starting with…

1. President Biden + Democratic Senate = Bullish Elevation

While many investors say they fear the impact of a “Democratic sweep” because of higher expected taxes and greater regulation, BofA counters that a unified government would be bullish:

The desire to maintain majorities through midterm elections in two years incentivizes a pro-growth, pro-employment agenda now (fiscal stimulus, industrial policy) & redistribution only later (if ever). This is particularly urgent for Democrats, who have struggled historically to motivate voters in midterms;

Even if progressives impose new taxes & regulations, the bank expects that the planned consumption and investment incentives would more than offset the drag.

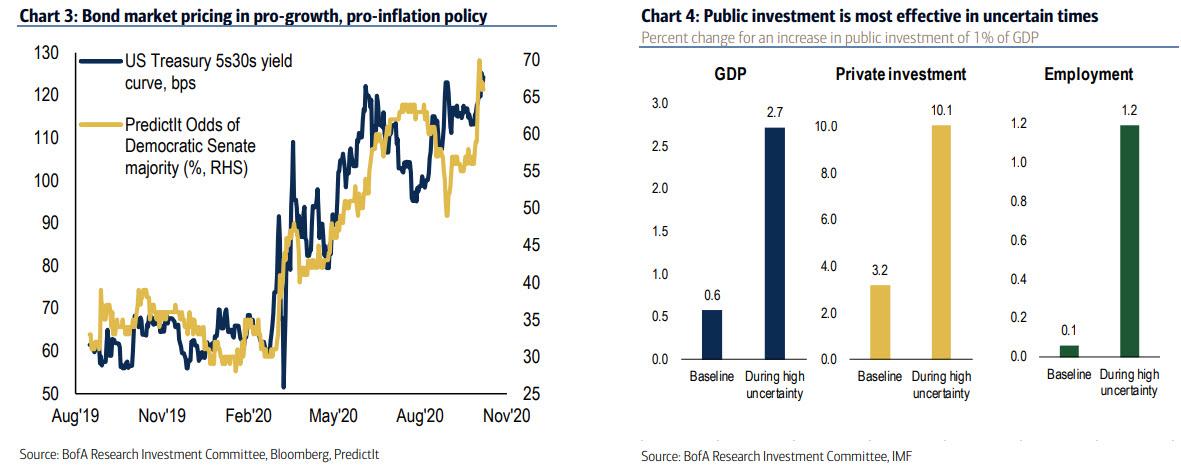

As an aside, Woodard notes that voters are tired of gridlock citing a recent Gallup Governance survey, where only 23% said they favor a Congress and Presidency controlled by different parties, the 2nd-lowest reading in history. Markets also seem prepared to accept a “blue wave”, with equities rising and the yield curve steepening in tandem with odds of a Democratic Senate majority (Chart 3).

Unified governance (by either party) is also the key condition for BofA’s bullish macro Elevation scenario, as continued CARES Act-style economic support can, at best, return the US economy to the levels achieved at the end of 2019. That was still lead to an environment of stagnant growth and scarce profits. As such, a step-change to 3%+ GDP & higher productivity requires major new investments in R&D, capex, and a broader base of household demand; such policy shifts “require bold leadership and a governing majority, not tepid incrementalism.”

Next, Woodard claims that the timing is certainly right, citing a new IMF study which found that public investment is most effective in periods of high uncertainty, like this one. Using data across 107 countries over the last 30 years, the study found that, on average, new public investment worth 1% of GDP raised economic growth over the subsequent two years by 2.7%, private sector investment by 10%, and employment by 1.2% (Chart 4).

Trades: as has already been widely priced in by the market, expect a continued 2016-style “rowdy rotation” away from crowded secular stagnation beneficiaries (large caps, defensives, tech, bonds) and toward inflation assets (small caps, cyclicals, financials, commodities).

Likely winners: renewable energy, advanced industrials, electric vehicles, telecommunications, banks and silver;

Likely losers: health insurers, mega-cap tech, for-profit education, and media (NY Times +326% since Trump win vs. +4% in the 4 years prior).

2. President Biden + Republican Senate = Bearish Gridlock

Hardly “rocket surgery”, if Republicans retains the Senate they are very likely to block further stimulus under a Democratic President, which BofA says would be bearish for economic growth, corporate profits and financial markets (but it would be bullish for more stimulus from the Fed). In any case, as BofA sarcastically puts it, “after $21tn of monetary & fiscal stimulus in 2020, $0 of follow-on support would be deflationary.”

Indeed, political parties historically have used obstructionist tactics when out of power to thwart key legislation, most often through the “rediscovery” of commitments to “fiscal discipline”. As an example, BofA cites the budget austerity during 2012-2015 as a major reason for the slow economic recovery.

Trades: “in this scenario investors should prepare for lower returns and higher volatility. Raise cash and buy Treasuries, munis, and high-quality corporate bonds.”

3. President Trump + Any Senate = Uncertain Stagnation

This is the “status quo” scenario: after the election, basic support packages may be easier to pass, but BofA doubts whether President Trump and a Democratic House would find enough common ground to pass transformative, pro-growth legislation. The case of infrastructure is instructive: both parties agree on the need for more resources for transportation, energy security, etc., but talks have always broken down over “red line” issues like immigration. That said, with a GOP Senate, investment may come more easily for R&D and industries relevant to national security.

However, the risk of volatile stagflation also rises with a divided government. Policies that have increasingly bipartisan appeal, such as regulating Silicon Valley or countering the threat from China, would require massive (and in this case, unlikely) domestic public investment to offset related frictions.

Trades: long stagnation winners e.g. tech, consumer discretionary, large caps, IG bonds…but with less leverage and lower market beta.

4. Contested election = Buying Opportunity

Contrary to various doomsday predictions for what happens on Nov 4, BofA’s Nitin Saksena points out that options markets imply a move of 3.6% in the S&P 500 the day after November 3rd, only modestly above the recent historical average of 2.9%. However, instead of focusing on the day after, markets are pricing in greater odds of a contested election than ever before, with more volatility possible through December (although forward vol has certainly declined substantially in recent weeks).

According to BofA, “there are several unusual but plausible scenarios and no real historical precedent.” The bank does note that in 2000 the Supreme Court decided the election, but it suggests returns from that period are hardly analogous “since the set of possible outcomes now is wider and more politically fraught.”

That said, according to Woodard, the most important thing to know is that “the same features of the US economy that made every investor in the world desperate to buy US assets in 2020 will still exist in 2021, no matter the election outcome: the deepest and most liquid financial markets, strong institutions, the rule of law, and the most productive, creative workforce”.

BofA’s recommended trades for a contested election: treat any market decline on a contested election as an opportunity to buy risky assets and sell volatility (and if the worst case scenario happens, investors can just hope that they get a bailout… just like America’s banks.)

via ZeroHedge News https://ift.tt/3nPefb2 Tyler Durden

On Wednesday, The New York Post published an attention-catching original report: “Smoking-gun email reveals how Hunter Biden introduced Ukrainian businessman to VP dad.” In the previously unreleased email, which was allegedly sent on April 17, 2015, an executive with Burisma, the Ukrainian natural gas company, thanks Hunter Biden for “giving an opportunity” to meet Joe Biden, according to The NY Post.

It’s a story that merits the attention of other journalists, political operatives, national security experts, and also the public at large—not least of all because there are serious questions about its accuracy, reliability, and sourcing. And yet many in the media are choosing not just to ignore the story, but to actively encourage others to suppress any discussion of it.

Indeed, two mainstream reporters who acknowledged (and criticized) the Post‘s scoop—The New York Times‘ Maggie Haberman and Politico’s Jake Sherman—faced thunderous denunciation on Twitter from Democratic partisans simply for discussing the story. Center for American Progress President Neera Tanden accused Haberman of promoting disinformation, and New York Times columnist Michelle Goldberg told Sherman that he was helping nefarious conservative activists “launder this bullshit into the news cycle.” Historian Kevin Kruse asked why they were “amplifying” the story.

Note that both Haberman and Sherman raised serious questions about the veracity of the story, questions that certainly deserve answers. According to The New York Post, the email was obtained from the hard drive of a computer that may or may not have belonged to Hunter Biden. Someone allegedly gave the laptop to a computer repair store owner in Delaware in 2019. The FBI took possession of the laptop in December 2019, according to The New York Post—but not before the store owner copied the hard drive and sent it to former New York Mayor Rudy Giuliani, an attorney for President Donald Trump and a central figure in the Trump-Ukraine-Biden kerfuffle. Former Trump advisor Steve Bannon then learned about the email and contacted The New York Post.

Giuliani and Bannon are political operatives with a long history of shady activity, so the fact that they were the intermediary sources for this story does raise red flags. But that doesn’t mean the story is untrue. For what it’s worth, The New York Post included photographs from the hard drive that allegedly confirms its authenticity. However, even if everything contained within the story turned out to be true, it still would not prove that the sought-after meeting with Joe Biden actually took place. A spokesperson for Biden said on Wednesday that according to Biden’s schedule, he never met with the Burisma official.

This is the work of journalism—to ask questions, to probe, to find and share the truth. Haberman and Sherman were right to let their audiences know that The New York Post story exists, and they were right to challenge it. Many others in the media apparently believe the public cannot be trusted with such a challenging article. They have not merely shamed people for sharing it online, but also want to make it difficult for people to read the report at all.

Facebook Communications Director Andy Stone, a former Democratic staffer, announced that the social media platform would limit the article’s distribution pending a fact-checker’s review. He directed users to Facebook policy, which states that “in many countries, including in the US, if we have signals that a piece of content is false, we temporarily reduce its distribution pending review by a third-party fact-checker.”

While Facebook is within its rights to take action against content it believes is factually misleading, this seems like a tough standard to enforce evenly. News articles in the mainstream press frequently contain information that is thinly or anonymously sourced, and sometimes proves to be inaccurate. It’s one thing for social media platforms to take swift action against viral content that is very obviously false or incendiary, like conspiracy theories about coronavirus miracle cures or voter fraud. It’s quite another for the platform to essentially make itself a gatekeeper of legitimate journalism, or a very selective media watchdog that appears to be more concerned about bad reporting when it comes from right-leaning outlets than left-leaning outlets, given the partisan leanings of social media company’s internal policy setters.

The obvious result will be a double standard, and an unsustainable one: The right will claim (correctly) that social media companies are biased against questionable conservative content, while the left will claim (also correctly) that plenty of misinformation eludes the moderators. Of course, the oft-proposed solution to the problems with platform content curation is to reform or repeal Section 230, which immunizes online platforms from some lawsuits. This idea is popular with everybody from Trump and Biden to Sen. Elizabeth Warren (D–Mass.) and Sen. Josh Hawley (R–Mo.), even though the obvious result of removing tech platform’s liability protection would be even moreaggressive moderation. New York Post op-ed editor Sohrab Ahmari tweeted that Facebook’s handling of the Hunter Biden scoop makes the case for modifying Section 230, but without Section 230, Facebook would—for legal reasons—be even more reticent about letting users share unverified claims.

Such an outcome would be bad for a free and open society, for the same reason that it is wrong for the mainstream media to attempt to keep the public wholly ignorant of stories they would rather not tell. The information will get out, and its better for journalists to contextualize—to add to our understanding—rather than pretend it doesn’t exist.

In defending his decision to publish the Steele dossier, which contained unverified, dubious, and speculative information, then-BuzzFeed News Editor in Chief Ben Smith (now a media critic for The New York Times) wrote the following: “You trust us to give you the full story; we trust you to reckon with a messy, sometimes uncertain reality.” That’s a lesson the entire media should take to heart, and apply evenly, no matter the inconvenience of the narrative.

from Latest – Reason.com https://ift.tt/34SFadq

via IFTTT

Judge Amy Coney Barrett testifies at her Senate confirmation hearing.

In a post published yesterday, I explained why Amy Coney Barrett is unlikely to vote to strike down the entire Affordable Care Act in Texas v. California, the case on that subject currently before the Supreme Court. In that post, I also described the background of the case and the issues at stake, in some detail.

Yesterday and today, Judge Barrett answered a number of questions about the ACA at her confirmation hearings. What she said doesn’t definitively tip her hand on how she might vote. But it does further reinforce my impression that she is unlikely to give the plaintiff Republican states and the Trump administration what they want. Most notably, she confirmed that she had voted to strike down the residual individual mandate but also sever it from the rest of the ACA in a recent moot court on the subject:

Supreme Court nominee Amy Coney Barrett said she did not strike down the Affordable Care Act (ACA) but did find its individual mandate unconstitutional in a recent moot court case, while stressing her actions in the moot court case did not actually reflect how she might rule on ObamaCare if confirmed to the high court….

“The vote was, in the panel, the majority said that the mandate was now a penalty and was unconstitutional but severable,” Coney testified in front of the Senate Judiciary Committee, referencing a moot court case she participated in at William & Mary Law School. “I voted to say that it was unconstitutional but severable.”

Barrett stressed that the moot court was just a hypothetical exercise and does not necessarily reflect her actual views of the case. But it is still at least somewhat indicative.

In addition, Barrett repeatedly stressed that the case currently before the Supreme Court comes down to severability, which is a different issue from the constitutionality of the individual health insurance mandate (a question on which she had been critical of Chief Justice Roberts’ 2012 ruling that the mandate should be upheld because it could be interpreted as a tax). This distinction is a crucial one, and Barrett’s emphasis on it further reinforces the view that she is unlikely to strike down the ACA as a whole.

I am far from the only commentator to reach this conclusion about Barrett’s position on the ACA case. Indeed, this seems to be an emerging consensus among experts. Yesterday, prominent liberal constitutional law scholar Eric Segall (who is no fan of Barrett’s) wrote that he “agree[s] with my libertarian friend on this” (the friend in question is me). That is at least somewhat notable, because he and I don’t agree on very many other constitutional law issues.

Earlier today, famed liberal Harvard Law School Professor Laurence Tribe tweeted that “[d]espite the great harm a Justice Coney Barrett will do, I predict she’ll join a 7-2 Supreme Court majority in holding the individual mandate severable from the rest of the ACA, including the protection of preexisting conditions. But she’ll join a 5-4 invalidation of the mandate.” I think the majority in favor of severability might well be even bigger than 7-2, and that the vote on invalidation of the mandate is likely to be 6-3 (with Roberts joining the other conservatives in holding that the residual mandate is now unconstitutional because it can no longer be considered a tax). But Tribe and I agree on the likely outcomes of the two parts of the case.

In my earlier post, I also explained why it’s highly unlikely that the plaintiffs will prevail on severability even if Barrett does vote in favor of their position. At least three of the other conservative justices signaled their hostility to that view in the recent robocall case, decided in June.

In my view a ruling striking down the residual individual mandate would be a significant decision enforcing constitutional limits on federal power. But it will have virtually no effect on the state of the ACA, given that the then-Republican controlled Congress rendered the mandate toothless in 2017. The fate of the ACA is what concerns the vast majority of other people interested in the case. ACA supporters should be happy to know that the law isn’t actually in real peril—at least not from this case.

Co-blogger Jonathan Adler points out that Barrett might potentially recuse herself from participating in the ACA case, because of her earlier involvement in the moot court on the subject. Unlike lower-court judges, Supreme Court justices have near-total discretion over recusal issues. I am skeptical that the moot court creates bias or conflict of interest sufficient to necessitate recusal. But I’m not an expert on recusal ethics, and therefore could be missing something here. If Barrett does recuse, she would, of course, have even less impact on the outcome of the case than I currently expect!

As I have emphasized previously, the history of ACA-related litigation is littered with failed expert predictions, including some of my own. In this instance, however, the evidence of the justices’ attitudes on severability is very strong, and the expert agreement on the subject cuts across ideological lines (which was not true in the debate over most previous ACA cases).

There are plenty of legitimate reasons to complain about the rushed nature of this confirmation process (I share some of those concerns myself), and also plenty of room for disagreement about Barrett’s jurisprudence (a topic I plan to write more about later this week). But she is unlikely to vote to strike down all of the ACA, and even more unlikely to have a decisive impact on the resolution of that issue.

from Latest – Reason.com https://ift.tt/34QPMt6

via IFTTT

In our latest episode I interview David Ignatius about the technology in his latest spy novel, The Paladin. Actually, while we do cover such tech issues as deepfakes, hacking back, Wikileaks, and internet journalism, the interview ranges more widely, from the steel industry of the 1970s, the roots of Donald Trump’s political worldview, and the surprisingly important role played in the Trump-Obama-Russia investigation by one of David Ignatius’s own opinion pieces.

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug! Our thanks to Ken Weissman of Weissman Sound Design for the new theme music.

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

from Latest – Reason.com https://ift.tt/34VH2lz

via IFTTT

Cryptocurrency exchange Coinbase holds approximately 994,904 Bitcoin in cold storage, according to ChainInfo, a Bitcoin analytics platform. By today’s prices, this amounts to over $11 billion.

The amount of Bitcoin held by Coinbase in cold storage has actually decreased since the end of last year. In December 2019, it was reported that Coinbase was holding 966,230 Bitcoin. Yet, Bitcoin’s price has grown significantly since then—up to its current value of $11,420. And as Bitcoin’s price continues to rise, Coinbase’s reserves grow more valuable by the day.

“It might be the world’s largest honeypot, a lot of people surely wish they had a quantum computer,” Elias Strehle, researcher at Blockchain Research Lab, told Decrypt.

A Bitcoin surrounded by several altcoins. Image: Shutterstock

Coinbase’s increased hold on Bitcoin could represent somewhat of a security risk for the crypto industry. Should Coinbase’s cold storage holdings ever be exploited, there would be a lot of Bitcoin at stake. However, the exchange does maintain strict security protocols and even tries to attack itself to check for any weaknesses.

Coinbase’s holdings have also potentially undermined the decentralization of the crypto industry.

However, distinctions between Coinbase and a traditional bank can still be made.

“One problem is that Coinbase would have a hard time redeeming those Bitcoin,” said Strehle, adding, “So they can’t secretly become a bank by using their Bitcoin under custody as working capital.”

Yet, Coinbase’s Bitcoin holdings are by far greater than any other crypto exchange. According to ChainInfo, crypto exchanges Huboi and Binance hold 323,655 ($3.7 billion) and 289,691 ($3.3 billion) Bitcoin respectively, with crypto exchange Kraken holding 126,509 ($1.4 billion) Bitcoin.

And if Bitcoin’s price continues to rise, these exchanges will be looking after even bigger treasure chests.

via ZeroHedge News https://ift.tt/2SU4Alh Tyler Durden

On Wednesday, The New York Post published an attention-catching original report: “Smoking-gun email reveals how Hunter Biden introduced Ukrainian businessman to VP dad.” In the previously unreleased email, which was allegedly sent on April 17, 2015, an executive with Burisma, the Ukrainian natural gas company, thanks Hunter Biden for “giving an opportunity” to meet Joe Biden, according to The NY Post.

It’s a story that merits the attention of other journalists, political operatives, national security experts, and also the public at large—not least of all because there are serious questions about its accuracy, reliability, and sourcing. And yet many in the media are choosing not just to ignore the story, but to actively encourage others to suppress any discussion of it.

Indeed, two mainstream reporters who acknowledged (and criticized) the Post‘s scoop—The New York Times‘ Maggie Haberman and Politico’s Jake Sherman—faced thunderous denunciation on Twitter from Democratic partisans simply for discussing the story. Center for American Progress President Neera Tanden accused Haberman of promoting disinformation, and New York Times columnist Michelle Goldberg told Sherman that he was helping nefarious conservative activists “launder this bullshit into the news cycle.” Historian Kevin Kruse asked why they were “amplifying” the story.

Note that both Haberman and Sherman raised serious questions about the veracity of the story, questions that certainly deserve answers. According to The New York Post, the email was obtained from the hard drive of a computer that may or may not have belonged to Hunter Biden. Someone allegedly gave the laptop to a computer repair store owner in Delaware in 2019. The FBI took possession of the laptop in December 2019, according to The New York Post—but not before the store owner copied the hard drive and sent it to former New York Mayor Rudy Giuliani, an attorney for President Donald Trump and a central figure in the Trump-Ukraine-Biden kerfuffle. Former Trump advisor Steve Bannon then learned about the email and contacted The New York Post.

Giuliani and Bannon are political operatives with a long history of shady activity, so the fact that they were the intermediary sources for this story does raise red flags. But that doesn’t mean the story is untrue. For what it’s worth, The New York Post included photographs from the hard drive that allegedly confirms its authenticity. However, even if everything contained within the story turned out to be true, it still would not prove that the sought-after meeting with Joe Biden actually took place. A spokesperson for Biden said on Wednesday that according to Biden’s schedule, he never met with the Burisma official.

This is the work of journalism—to ask questions, to probe, to find and share the truth. Haberman and Sherman were right to let their audiences know that The New York Post story exists, and they were right to challenge it. Many others in the media apparently believe the public cannot be trusted with such a challenging article. They have not merely shamed people for sharing it online, but also want to make it difficult for people to read the report at all.

Facebook Communications Director Andy Stone, a former Democratic staffer, announced that the social media platform would limit the article’s distribution pending a fact-checker’s review. He directed users to Facebook policy, which states that “in many countries, including in the US, if we have signals that a piece of content is false, we temporarily reduce its distribution pending review by a third-party fact-checker.”

While Facebook is within its rights to take action against content it believes is factually misleading, this seems like a tough standard to enforce evenly. News articles in the mainstream press frequently contain information that is thinly or anonymously sourced, and sometimes proves to be inaccurate. It’s one thing for social media platforms to take swift action against viral content that is very obviously false or incendiary, like conspiracy theories about coronavirus miracle cures or voter fraud. It’s quite another for the platform to essentially make itself a gatekeeper of legitimate journalism, or a very selective media watchdog that appears to be more concerned about bad reporting when it comes from right-leaning outlets than left-leaning outlets, given the partisan leanings of social media company’s internal policy setters.

The obvious result will be a double standard, and an unsustainable one: The right will claim (correctly) that social media companies are biased against questionable conservative content, while the left will claim (also correctly) that plenty of misinformation eludes the moderators. Of course, the oft-proposed solution to the problems with platform content curation is to reform or repeal Section 230, which immunizes online platforms from some lawsuits. This idea is popular with everybody from Trump and Biden to Sen. Elizabeth Warren (D–Mass.) and Sen. Josh Hawley (R–Mo.), even though the obvious result of removing tech platform’s liability protection would be even moreaggressive moderation. New York Post op-ed editor Sohrab Ahmari tweeted that Facebook’s handling of the Hunter Biden scoop makes the case for modifying Section 230, but without Section 230, Facebook would—for legal reasons—be even more reticent about letting users share unverified claims.

Such an outcome would be bad for a free and open society, for the same reason that it is wrong for the mainstream media to attempt to keep the public wholly ignorant of stories they would rather not tell. The information will get out, and its better for journalists to contextualize—to add to our understanding—rather than pretend it doesn’t exist.

In defending his decision to publish the Steele dossier, which contained unverified, dubious, and speculative information, then-BuzzFeed News Editor in Chief Ben Smith (now a media critic for The New York Times) wrote the following: “You trust us to give you the full story; we trust you to reckon with a messy, sometimes uncertain reality.” That’s a lesson the entire media should take to heart, and apply evenly, no matter the inconvenience of the narrative.

from Latest – Reason.com https://ift.tt/34SFadq

via IFTTT

Judge Amy Coney Barrett testifies at her Senate confirmation hearing.

In a post published yesterday, I explained why Amy Coney Barrett is unlikely to vote to strike down the entire Affordable Care Act in Texas v. California, the case on that subject currently before the Supreme Court. In that post, I also described the background of the case and the issues at stake, in some detail.

Yesterday and today, Judge Barrett answered a number of questions about the ACA at her confirmation hearings. What she said doesn’t definitively tip her hand on how she might vote. But it does further reinforce my impression that she is unlikely to give the plaintiff Republican states and the Trump administration what they want. Most notably, she confirmed that she had voted to strike down the residual individual mandate but also sever it from the rest of the ACA in a recent moot court on the subject:

Supreme Court nominee Amy Coney Barrett said she did not strike down the Affordable Care Act (ACA) but did find its individual mandate unconstitutional in a recent moot court case, while stressing her actions in the moot court case did not actually reflect how she might rule on ObamaCare if confirmed to the high court….

“The vote was, in the panel, the majority said that the mandate was now a penalty and was unconstitutional but severable,” Coney testified in front of the Senate Judiciary Committee, referencing a moot court case she participated in at William & Mary Law School. “I voted to say that it was unconstitutional but severable.”

Barrett stressed that the moot court was just a hypothetical exercise and does not necessarily reflect her actual views of the case. But it is still at least somewhat indicative.

In addition, Barrett repeatedly stressed that the case currently before the Supreme Court comes down to severability, which is a different issue from the constitutionality of the individual health insurance mandate (a question on which she had been critical of Chief Justice Roberts’ 2012 ruling that the mandate should be upheld because it could be interpreted as a tax). This distinction is a crucial one, and Barrett’s emphasis on it further reinforces the view that she is unlikely to strike down the ACA as a whole.

I am far from the only commentator to reach this conclusion about Barrett’s position on the ACA case. Indeed, this seems to be an emerging consensus among experts. Yesterday, prominent liberal constitutional law scholar Eric Segall (who is no fan of Barrett’s) wrote that he “agree[s] with my libertarian friend on this” (the friend in question is me). That is at least somewhat notable, because he and I don’t agree on very many other constitutional law issues.

Earlier today, famed liberal Harvard Law School Professor Laurence Tribe tweeted that “[d]espite the great harm a Justice Coney Barrett will do, I predict she’ll join a 7-2 Supreme Court majority in holding the individual mandate severable from the rest of the ACA, including the protection of preexisting conditions. But she’ll join a 5-4 invalidation of the mandate.” I think the majority in favor of severability might well be even bigger than 7-2, and that the vote on invalidation of the mandate is likely to be 6-3 (with Roberts joining the other conservatives in holding that the residual mandate is now unconstitutional because it can no longer be considered a tax). But Tribe and I agree on the likely outcomes of the two parts of the case.

In my earlier post, I also explained why it’s highly unlikely that the plaintiffs will prevail on severability even if Barrett does vote in favor of their position. At least three of the other conservative justices signaled their hostility to that view in the recent robocall case, decided in June.

In my view a ruling striking down the residual individual mandate would be a significant decision enforcing constitutional limits on federal power. But it will have virtually no effect on the state of the ACA, given that the then-Republican controlled Congress rendered the mandate toothless in 2017. The fate of the ACA is what concerns the vast majority of other people interested in the case. ACA supporters should be happy to know that the law isn’t actually in real peril—at least not from this case.

Co-blogger Jonathan Adler points out that Barrett might potentially recuse herself from participating in the ACA case, because of her earlier involvement in the moot court on the subject. Unlike lower-court judges, Supreme Court justices have near-total discretion over recusal issues. I am skeptical that the moot court creates bias or conflict of interest sufficient to necessitate recusal. But I’m not an expert on recusal ethics, and therefore could be missing something here. If Barrett does recuse, she would, of course, have even less impact on the outcome of the case than I currently expect!

As I have emphasized previously, the history of ACA-related litigation is littered with failed expert predictions, including some of my own. In this instance, however, the evidence of the justices’ attitudes on severability is very strong, and the expert agreement on the subject cuts across ideological lines (which was not true in the debate over most previous ACA cases).

There are plenty of legitimate reasons to complain about the rushed nature of this confirmation process (I share some of those concerns myself), and also plenty of room for disagreement about Barrett’s jurisprudence (a topic I plan to write more about later this week). But she is unlikely to vote to strike down all of the ACA, and even more unlikely to have a decisive impact on the resolution of that issue.

from Latest – Reason.com https://ift.tt/34QPMt6

via IFTTT

Elizabeth Warren Lashes Out At Disney For 28,000 Layoffs That Happened As A Result Of Gov’t-Mandated Shutdowns Tyler Durden

Wed, 10/14/2020 – 14:40

Senator Elizabeth Warren, once again displaying her exceptional business acumen, has lashed out at Disney for the company’s recent layoffs which, ironically, occurred to due government forcing its theme parks to close in jurisdictions like California. Disney’s theme parks employed more than 100,000 people prior to the crisis.

Warren criticized the layoffs not by looking at what the government did to catalyze them, but rather by examining Disney’s financial decisions in the years leading up to the pandemic, according to Reuters.

She wrote in a letter to Disney Executive Chairman Bob Iger and Chief Executive Officer Bob Chapek on Tuesday: “I would like to know whether Disney’s financial decisions have impacted the company’s decision to lay off workers. It appears that – prior to, and during the pandemic – Disney took good care of its top executives and shareholders – and now is hanging its front-line workers out to dry.”

Warren seems to be unaware that Disney “front line workers” may also be shareholders in the company. But hey, how dare a company do what is in the best interest of its shareholders? We wonder if Warren, who was revealed to own stock in companies like IBM back in 2019, would urge companies of stock she held to make decisions that were bad for shareholders.

Regardless, she called Disney’s decision to pay dividends and buyback stock before the pandemic as “short sighted”. Meanwhile, the shares in IBM Warren was said to have held survived over the last half decade mostly on buybacks, tax breaks and financial engineering.

Warren, apparently unaware what the point of laying people off to save money is, also asked about whether Disney would cover healthcare premiums for the laid off employees. Meanwhile, “Disney has continued to provide healthcare benefits to furloughed workers for the last six months,” according to Reuters.

She also noted that Disney spent $47.9 billion on share buybacks from 2009 to 2018 and that Disney spent $5.4 billion on dividends in 2018.

Warren has said she wants an answer to her letter by October 27. We’re sure Disney, who is under no obligation to answer letters from anybody, will enjoy outsourcing their response to whatever PR firm they are paying using the money they saved by laying off their workforce.

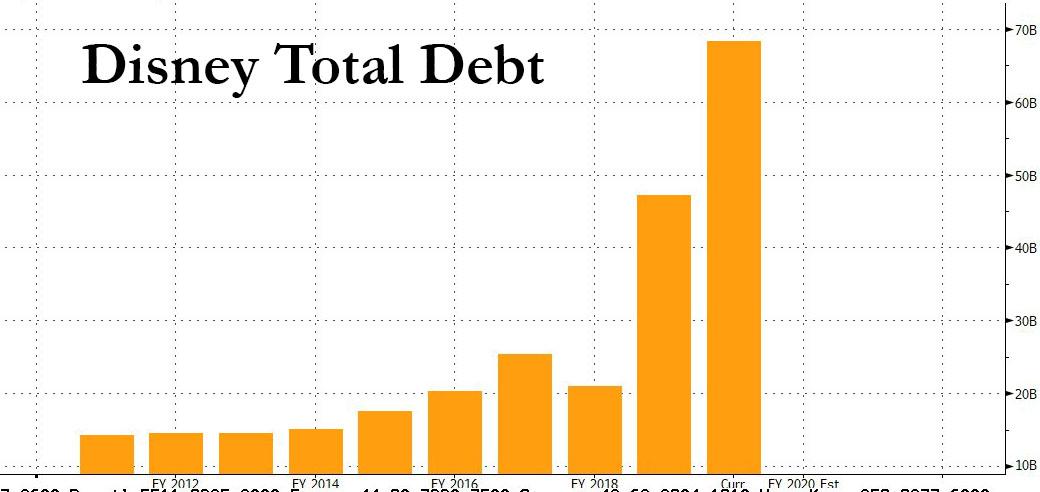

Recall, about two weeks ago we noted that Disney was laying off 28,000 workers in its U.S. resort business. We noted then that although one could “understand” the plight of management, which is scrambling to boost cash flow after it saddled the company with record debt in recent years…

…it probably would make all those soon-to-be-laid off workers feel a little bit better if most of that newly issued debt hadn’t gone to pay for stock buybacks the benefited upper management.

“As heartbreaking as it is to take this action, this is the only feasible option we have in light of the prolonged impact of Covid-19 on our business,” Josh D’Amaro, the chairman of the parks division, said in a memo to workers at the time.

The cuts were made across the company’s various businesses including theme parks, cruise ships and retail businesses. While the layoffs also include executives, they focused on part-time workers: 67% of those getting a pink slip were part-time workers.

As part of its farewell package, Disney said it would offer benefits to the workers being cut, including 90 days of severance.

via ZeroHedge News https://ift.tt/2FrR8BY Tyler Durden