Rabo: Brexit Was Always Inevitable If Politicians Understood UK Drinking Habits Tyler Durden

Wed, 09/23/2020 – 09:20

By Michael Every of Rabobank

Markets were briefly roiled yesterday by the Fed’s Evans being misquoted in suggesting that the Fed might do the complete opposite of what it has just pledged to stick with – not doing anything for years and years and years, almost regardless of what inflation (doesn’t) do for years and years and years.

Further roiling can be expected in the UK as the same government who weeks ago was telling people “Go back to the office or risk losing your job,” is now telling them they will be working from home for the next six months, and that restrictions could get tighter yet. For example, only being able to drink until 9pm not 10pm?

Apart from the obvious “whocouldadnooed?” incompetence, it is stunning that a British government misunderstands its own people so badly. The infamous UK ‘closing time’ was only introduced around a century ago in 1914‘s Defence of the Realm Act to try to ensure that WW1 munitions workers would not be so hung-over that they couldn’t work the next day. Back then, it was 10.30pm and “Last orders!” or “Time, ladies and gentlemen, please!” needed to win the war. Now it’s 10pm, apparently.

The key point (or pint) is that British culture just adapted to drinking the same quantity of alcohol as before, but in a shorter time: sobriety was notably not increased. Hangovers were not decreased. Quite the opposite in fact.

The fact pubs are closing an hour earlier for six months was literally all the UK news was talking about last night: Donald Trump and Xi Jinping’s clashing speeches at the UN hardly got a look in. One would think politicians, who are not afraid of the odd drink –they have a subsidised bar, after all– would know this.

(Adrian Edmondson): “One thousand, five hundred and seventy four gin and tonics, please, Monica.”

(Rik Mayall): “LARGE ones.” .

‘Mr. Jolly Lives Next Door’ (1988)

As a co-worker in New York put it yesterday, one would think perhaps the UK is one giant pub. Indeed, perhaps it always was. This certainly isn’t the first time UK politicians have put the ideal ahead of the real and the drinking culture at the heart of UK identity.

Tony Blair –who I suddenly picture with a Campari and soda or a Babycham, trying to fit in at a rough 1980’s northern Working Men’s Club where Bernard Manning is on the week after– massively liberalised the Licensing Laws in the 2000s. Suddenly, pubs could stay open until 1 or 2am or later. “Ah-ha!” cried the Blairites. “Brits will now sup their drinks slowly until the wee hours in outside pavement cafes while discussing arthouse cinema and Sartre, and we will have turned the UK into continental Europe.”

That was the plan.

What actually happened in many locations was a get-‘em-in-let’s-have-another-I-love-you-you-know-did-you-spill-my-pint-vomit-and-blood-and-tears-and-half-a-kebab-down-the-shirt-broken-beer-bottle-in-the-face-where’s-my-taxi-here-come-the-rozzas nightly apocalypse that started at 7pm and went on well until dawn. Good job there wasn’t a war on.

In other words, Brexit was perhaps always inevitable if politicians understood UK drinking habits – though to be fair the Scandinavians, who are capable of some pretty epic drinking of their own, somehow manage to do so without trying to fight everyone in the EU shirtless.

One will certainly need a stiff drink in the next few months, however, if the British government’s claim that 7,000 trucks a day could be stuck in lines at the port of Dover in a “reasonable worst case” if it exits the EU without better customs preparation, and that traders should prepare for January. (The people doing that prep are apparently the same ones doing the UK’s Covid testing and the track and trace system.) That would mean an 80% decline in normal goods flow, and so an 80% decline in imported goods on shelves.

You want a UK pub-style apocalypse all day long? Try all that drinking on an empty stomach – or less of the drinking too if it is imported booze you are after.

In short, both the EU and the UK are negotiating over Brexit trade terms, but the latter seems to, again, be shirtless and shouting “Come and have a go if you think you’re hard enough!” while swaying from side to side.

There are of course other global parallels with well-intended effects to try to corral liquidity: which brings us back to the Fed, the ECB, the BOJ, the BOE, the BOC, the RBA, the RBNZ (who just left rates on hold), the PBOC, etc., etc., and the mother of all hangovers that looms at some point.

(Policeman): “Are you drunk, sir?”

(Adrian Edmondson): “Of course I am, I’m out of my bloody mind. I’ve just spent three thousand quid in there.”

‘Mr Jolly Lives Next Door’ (1988)

What is the crumpled what-you-hope is money you want to be drunkenly fumbling for in your pocket when the bills for all of this come due?

via ZeroHedge News https://ift.tt/3kHmm7k Tyler Durden

Hunter Biden Raised ‘Counterintelligence And Extortion’ Concerns, May Have Participated In Sex Trafficking: Senate Report Tyler Durden

Wed, 09/23/2020 – 09:05

A long-awaited Senate report on Hunter Biden’s financial dealings with Ukrainian, Chinese and Russian businesses created potential “criminal financial, counterintelligence and extortion concerns,” and alarmed US officials who perceived an ethical conflict of interest and flagged potential crimes ranging from sex trafficking to bribery.

The findings are contained in a joint report by the GOP-led Senate Homeland and Government Affairs and Senate Finance Committees, released just six days before the first Presidential Debate between Joe Biden and President Trump.

OUT TODAY: Report with @chuckgrassley found millions of dollars in questionable financial transactions between Hunter Biden & his associates and foreign individuals, including the wife of the former mayor of Moscow. https://t.co/R1MxQ4xGKP

According to the Daily Caller’s Chuck Ross, suspicious financial transactions between Hunter Biden’s firms and foreign nationals from Russia and China – including a CCP-linked Chinese businessman, raised serious concerns. What’s more, Hunter’s seat on the board of Ukrainian energy giant Burisma while his father served as the Obama administration point-man for Ukraine, worried State Department officials in 2015 and 2016.

One official, Amos Hochstein, told the Senate Homeland Security and Senate Finance committees that he said to then-Vice President Joe Biden in October 2015 that Hunter Biden’s position on the board of Burisma “enabled Russian disinformation efforts and risked undermining U.S. policy in Ukraine.”

Hunter Biden, now 50, joined Burisma’s board of directors in April 2014, shortly after his father, Joe Biden, took over as the Obama administration’s chief liaison to Ukraine. –Daily Caller

As Ross notes, while the report does not produce direct evidence of wrongdoing by Hunter Biden, Republicans say the evidence paints a troubling picture of Biden receiving “millions of dollars from foreign sources as a result of business relationships that he built during the period when his father was vice president of the United States and after.”

Hunter Biden also received a $3.5 million wire transfer from Elena Baturina, the wife of the former mayor of Moscow, according to the report.

And as Just The News‘ John Solomon writes, “Perhaps the most explosive revelation was that the U.S. Treasury Department flagged payments collected overseas by Hunter Biden and business partner Devon Archer for possible illicit activities.“

The so-called Suspicious Activity Reports flagged millions of dollars in transactions from the Ukrainian gas company Burisma Holdings, a Russian oligarch named Yelena Baturina, and Chinese businessmen with ties to Beijing’s communist government, the report said. Senate investigators have yet to determine if the FBI or others investigated the concerns. –Just The News

“The Treasury records acquired by the Chairmen show potential criminal activity relating to transactions among and between Hunter Biden, his family, and his associates with Ukrainian, Russian, Kazakh and Chinese nationals,” reads the 87-page report. Other transactions involving Biden-controlled firms were flagged for “potential criminal financial activity,” including wire transfers to Hunter’s Uncle, James Biden.

The report focuses on millions of dollars in wire payments that Hunter Biden’s firms received from Ye Jianming, the founder of CEFC China Energy Co., and Gongwen Dong, a U.S.-based associate of Ye’s.

According to Republicans, Ye has “extensive” connections to the Chinese government.

The Senate report says that on Aug. 4, 2017, a subsidiary of Ye’s company called CEFC Infrastructure Investment (US) LLC, wired $100,000 to Owasco, the Biden law firm.

A month later, on Sept. 8, 2017, Hunter Biden and Gongwen Dong applied for a $100,000 line of credit under a shell company they formed called Hudson West III LLC, according to the Senate report.

Biden, his uncle James, and James’s wife, Sara Biden, accessed the account through credit cards, and spent $101,291 on what Republicans call “extravagant items,” including plane tickets, hotels, restaurants and items at Apple stores. –Daily Caller

Meanwhile, according to US government records cited in the report, concerns were raised over potential ties to sex and human trafficking rings.

“Hunter Biden paid nonresident women who were nationals of Russia or other Eastern European countries and who appear to be linked to an Eastern European prostitution or human trafficking ring,” the report reads.

Senate Homeland Security and Governmental Affairs Committee Chairman Ron Johnson told Just The News that the sheer volume of potentially illegal activity in Hunter Biden’s foreign dealings left Joe Biden vulnerable to illicit influence or extortion.

“The report raises serious questions that former Vice President Biden needs to answer. There are simply too many potential conflict of interest, counterintelligence and extortion threats to ignore,” he said.

The Biden campaign has called the Senate report an effort to “subsidize a foreign attack against the sovereignty of our elections with taxpayer dollars” and to push a “long-disproven, hardcore rightwing conspiracy theory.”

Biden campaign’s @AndrewBatesNC calls Sen. Ron Johnson’s report on Burisma/Hunter Biden an effort to “subsidize a foreign attack against the sovereignty of our elections with taxpayer dollars” and to push a “long-disproven, hardcore rightwing conspiracy theory” pic.twitter.com/LRDKEdu0fK

The findings, as compiled by the Daily Wire‘s Ryan Saavedra:

In early 2015 the former Acting Deputy Chief of Mission at the U.S. Embassy in Kyiv, Ukraine, George Kent, raised concerns to officials in Vice President Joe Biden’s office about the perception of a conflict of interest with respect to Hunter Biden’s role on Burisma’s board. Kent’s concerns went unaddressed, and in September 2016, he emphasized in an email to his colleagues, “Furthermore, the presence of Hunter Biden on the Burisma board was very awkward for all U.S. officials pushing an anticorruption agenda in Ukraine.”

In October 2015, senior State Department official Amos Hochstein raised concerns with Vice President Biden, as well as with Hunter Biden, that Hunter Biden’s position on Burisma’s board enabled Russian disinformation efforts and risked undermining U.S. policy in Ukraine.

Although Kent believed that Hunter Biden’s role on Burisma’s board was awkward for all U.S. officials pushing an anti-corruption agenda in Ukraine, the Committees are only aware of two individuals — Kent and former U.S. Special Envoy and Coordinator for International Energy Affairs Amos Hochstein — who raised concerns to Vice President Joe Biden (Hochstein) or his staff (Kent).

The awkwardness for Obama administration officials continued well past his presidency. Former Secretary of State John Kerry had knowledge of Hunter Biden’s role on Burisma’s board, but when asked about it at a town hall event in Nashua, N.H. on Dec. 8, 2019, Kerry falsely said, “I had no knowledge about any of that. None. No.” Evidence to the contrary is detailed in Section V.

Former Assistant Secretary of State for European and Eurasian Affairs Victoria Nuland testified that confronting oligarchs would send an anticorruption message in Ukraine. Kent told the Committees that Zlochevsky was an “odious oligarch.” However, in December 2015, instead of following U.S. objectives of confronting oligarchs, Vice President Biden’s staff advised him to avoid commenting on Zlochevsky and recommended he say, “I’m not going to get into naming names or accusing individuals.”

Hunter Biden was serving on Burisma’s board (supposedly consulting on corporate governance and transparency) when Zlochevsky allegedly paid a $7 million bribe to officials serving under Ukraine’s prosecutor general, Vitaly Yarema, to “shut the case against Zlochevsky.” Kent testified that this bribe occurred in December 2014 (seven months after Hunter joined Burisma’s board), and, after learning about it, he and the Resident Legal Advisor reported this allegation to the FBI.

Hunter Biden was a U.S. Secret Service protectee from Jan. 29, 2009 to July 8, 2014. A day before his last trip as a protectee, Time published an article describing Burisma’s ramped up lobbying efforts to U.S. officials and Hunter’s involvement in Burisma’s board. Before ending his protective detail, Hunter Biden received Secret Service protection on trips to multiple foreign locations, including Moscow, Beijing, Doha, Paris, Seoul, Manila, Tokyo, Mexico City, Milan, Florence, Shanghai, Geneva, London, Dublin, Munich, Berlin, Bogota, Abu Dhabi, Nairobi, Hong Kong, Taipei, Buenos Aires, Copenhagen, Johannesburg, Brussels, Madrid, Mumbai and Lake Como.

Andrii Telizhenko, the Democrats’ personification of Russian disinformation, met with Obama administration officials, including Elisabeth Zentos, a member of Obama’s National Security Council, at least 10 times. A Democrat lobbying firm, Blue Star Strategies, contracted with Telizhenko from 2016 to 2017 and continued to request his assistance as recent as the summer of 2019. A recent news article detailed other extensive contacts between Telizhenko and Obama administration officials.

In addition to the over $4 million paid by Burisma for Hunter Biden’s and Archer’s board memberships, Hunter Biden, his family, and Archer received millions of dollars from foreign nationals with questionable backgrounds.

Archer received $142,300 from Kenges Rakishev of Kazakhstan, purportedly for a car, the same day Vice President Joe Biden appeared with Ukrainian Prime Minister Arsemy Yasenyuk and addressed Ukrainian legislators in Kyiv regarding Russia’s actions in Crimea.

Hunter Biden received a $3.5 million wire transfer from Elena Baturina, the wife of the former mayor of Moscow.

Hunter Biden opened a bank account with Gongwen Dong to fund a $100,000 global spending spree with James Biden and Sara Biden.

Hunter Biden had business associations with Ye Jianming, Gongwen Dong, and other Chinese nationals linked to the Communist government and the People’s Liberation Army. Those associations resulted in millions of dollars in cash flow.

Hunter Biden paid nonresident women who were nationals of Russia or other Eastern European countries and who appear to be linked to an “Eastern European prostitution or human trafficking ring.”

Imagine if this was anyone with the last name Trump?

via ZeroHedge News https://ift.tt/2FWwudr Tyler Durden

Belarus’ Lukashenko Sworn-In At ‘Secret’ Ceremony To Avoid Protests Tyler Durden

Wed, 09/23/2020 – 08:55

After his Aug.9 controversial reelection to a sixth term, Belarusian President Alexander Lukashenko has been sworn in during an event international reports describe as a “secret ceremony” which was held with no prior announcement.

Belta state news agency was the first to report the swearing in on Wednesday, the first indication of which were eyewitness reports of widespread street closures in Minsk and even allegations of intentional internet outages as the presidential motorcade sped through the streets.

“Alexander Lukashenko has taken office as President of Belarus. The inauguration ceremony is taking place in these minutes in the Palace of Independence,” Belta reported.

Фотография с инаугурации Лукашенко, которая началась без анонса и телетрансляции.

In his few recent public appearances, Lukashenko has donned combat gear, including a bullet proof vest and black utility clothes, while carrying an automatic rifle.

Armored vehicles have also now for weeks protected the president’s residential complex in Minsk after almost every weekend demonstrations have swelled to an estimated 100,000 – including marches which seek to confront the strongman who has already been in office for 26 years.

The AP reports that “Lukashenko’s official website did not make any announcement and the ceremony was not shown live on state television, apparently to avoid protesters gathering.”

Most likely Lukashenko is going to have his inauguration today. Nothing has been announced but in central Minsk there’s no mobile internet, all the major roads are blocked, police is everywhere, buses bring people to Lukashenko’s palace. This is what 80% of support look like. pic.twitter.com/MT76JqhWUo

Lukashenko and his supporters have warned there’s a NATO-sponsored “color revolution” unfolding. Russian intelligence officials have alleged the same thing.

Last week for example, the director of Russia’s foreign intelligence service SVR, Sergey Naryshkin, charged thatthe United States is “stage managing” the unrest in Belarus, which has since the contested election sought to oust Lukashenko from office.

via ZeroHedge News https://ift.tt/2HmWWNL Tyler Durden

“I would worry less about the gods and more about the fury of a patient man.”

As the market sort of rallies on the back of Fed Head Jerome Powell suggesting the lack of US stimulus might be a problem, thereby anticipating a new stimulus will come – for that is the way markets think. Meanwhile, there are a number of themes discernible amongst the noise that is the Market this morning…

Follow the money: Ragnar acts….

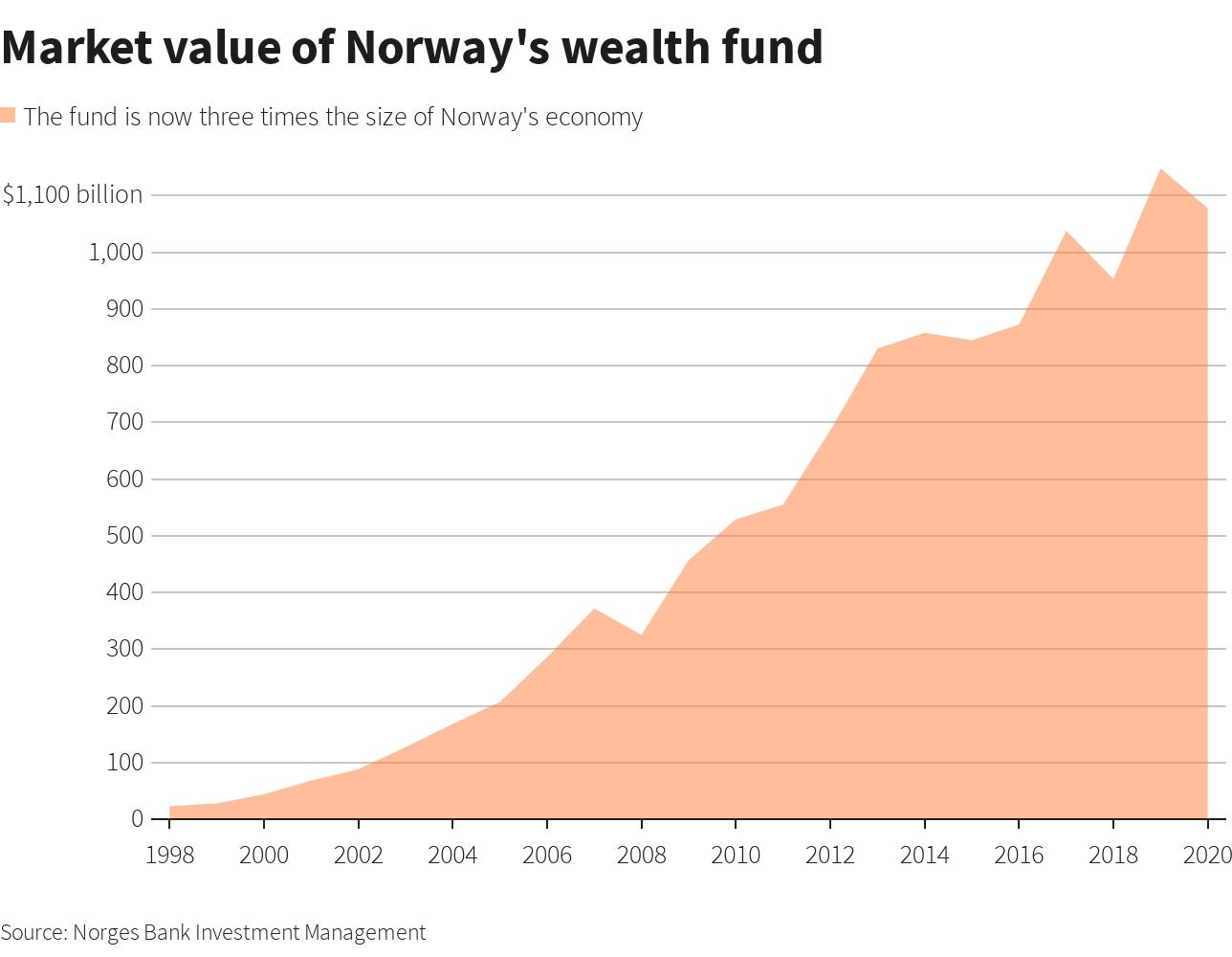

The Norwegians are pivoting their $1.15 trillion pension fund away from European stocks towards US equites. The FT says the Nogs are going to cut Europe from 33% to 26.5% while raising US allocations to 48%. “Better represents the distribution of value creation” said the Minister of Finance. It makes sense: US stocks represent some 65.5% of global market cap. Europe? Not so much. Yet Europe was 50% of Norway’s equity allocation as recently as 2012.

The timing is significant. There is much talk about how overvalued US stocks look and how Federal government stimulus, over-easy policy by the Fed, and Donald Trump’s constant talking-up of US Stocks and tax-handouts, have boosted US valuations and driven the continuation of a 11-year bull market. On the other hand, it’s been NIRP (Negative interest rates), QE Infinity and “do-what-ever-it-takes” that’s stopped European stocks and sovereign debt tumbling into the abyss these last few years.

The US has posted positive growth. Europe… less so.

Whatever, it’s an “Ouch” moment for Europe. The announcement was wrapped up in diplomatic flannel, but it’s clear the Nogs don’t have much faith in European recovery prospects, or believe Europe is relatively undervalued compared to the US – a common investment theme in European Investment Bank “research”in recent months…

Interesting fact – during the last unpleasantness with Germany, the Norwegian Government based itself in Edinburgh, at Riccarton which is now Heriot-Watt University’s campus. As a result my student days involved carousing with lots of wild Nog students – they are brilliantly bad and funny people. Celebrating their national day was something on an eco-hazard. I called one of my Norwegian chums to ask his view on the portfolio shift. (He’s a banker.. but definitely would have been a Viking in a former life.)

He told me the “team” (the fund and politicians) are concerned about the Norwegian economy being too closely aligned with the faceless bureaucracy of Brussels the reality of the Japanification of Europe and low growth prospects. They need growth to continue the shift of their economy towards a more global and sustainable perspective. Politically they remain neutral.

It’s fascinating to get an outsider’s view. There are three problems in Europe likely to lead to continued underperformance relative to the US and Asia:

i) The inability of EU member states to reconcile domestic policy agendas with real fiscal union hampers effective recovery at the regional level. There are serious issues in terms of delivering regional policy goals – including endemic corruption in parts of East and South Europe. These need strong domestic government, rather than centralised power projection from Brussels.

ii) The ECB’s ineffectual and unreliable tinkering with increasingly ineffective monetary stimulus is doing little to address long-term growth and employment outside Germany. Its simply sustaining what is broken, rather than replacing it. The current debate about ending QE Infinity early sums up the lack of direction and clear objectives within the ECB.

iii) While Europe is sinking, there are more attractive relative opportunities elsewhere. It makes sense to move.

There is a fourth issue, which is apparently causing concern at the political level. Some Norwegian politicians are increasingly “unhappy” at the way Norway is increasingly painted as some kind of vassal state by Brussels in terms of being “subject” to EU laws and paying for the privilege of access. They see the EU’s domestic leaders as distracted and focused internally on issues like the pandemic, immigration and employment, while the EU is effectively run by an unelected clique of officals in Brussels focused on the preservation of the union – which isn’t reflecting tensions building up between the states and the union. The way the relationship with Norway has been used to justify the EU’s position re Brexit negotiations has particularly jarred some politicians in Oslo.

While one Norwegian banker is not representative of the entire nation – he makes a lot of sense. It’s a single perspective, but the Norwegians have faith in the global economy, but not so much in Europe.

European Banks

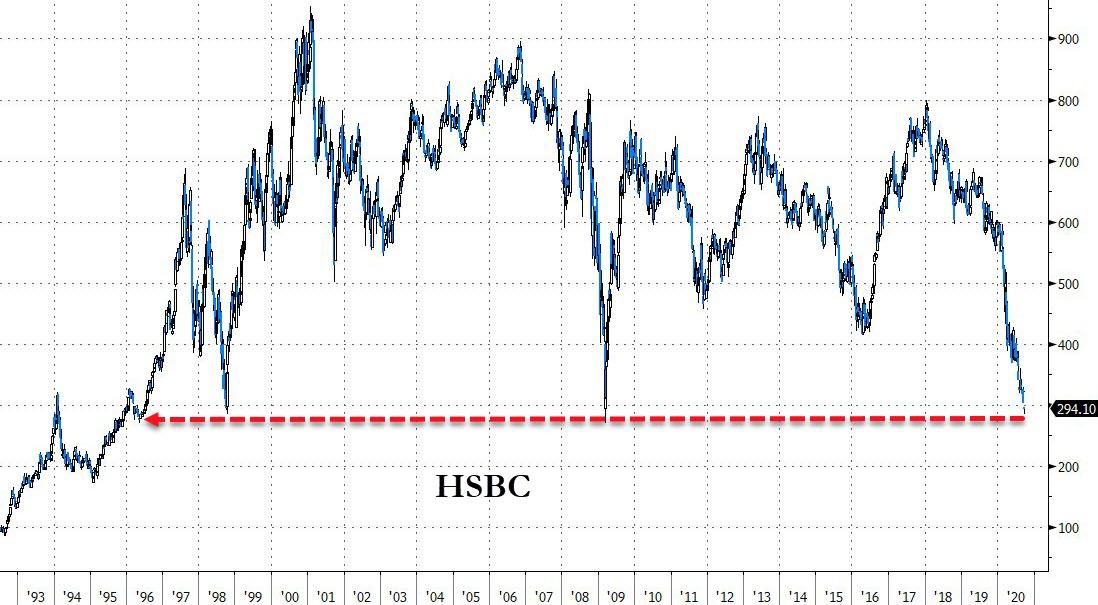

10 years ago I wrote that HSBC was my “banker stock”. It was then the European bank we’d always be able to rely on and the one European financial institution I was confident of getting my money back from. I invested heavily in deeply discounted HSBC pref notes at the depth of the 2008/09 banking crisis – confident they wouldn’t need a bail-out. It was a great trade.

Today, HSBC heads my list of stocks to avoid – utterly. It’s facing an irrecoverable multiple whammy of irreconcilable issues:

It’s going to take massive Pandemic bad-loan provisions – the $11 bln it was talking about earlier this year are going to look a massive underestimate.

It’s a tech dinosaur plagued by legacy systems that need replacement and reinvention and internal bureaucracy – while new nimble digitally based Fintechs are set to eat it’s lunch.

It’s got the looming political crisis in Hong Kong, the source of the bulk of its profits that have subsidised its lacklustre global efforts for years. It’s likely to suffer massive disruption if the HK$ currency peg breaks, trigger massive corporate defaults. Its corporate reputation is tarnished as a result of the China trap.

It’s top of the Chinese government sh*t list as the easy name to hit. It’s likely to be put on the new “unreliable entity list” for perceived collusion with the US over Huawei and as a bargaining chip.

What makes me smile is HSBC’s claim to be the best bank to advise clients on ESG (Environmental, Social and Governance issues.) That’s a bad joke. ESG is not just about the environment – it’s about how firms treat people, customers and staff. HSBC is the only major UK bank that is taking advantage of the UK pensions act 2011 to reduce contracted staff pensions via clawbacks. It’s shaping up to be an enormous “Social” ESG failure – a bank that apparently is willing to inflict harm and damage on its own staff at the end of their careers doesn’t care much for stakeholder society. And it’s a reason HSBC service is so appalling – staff morale has collapsed in the face of redundancies and the pensions issue. Clients looking for ESG advice should be looking at HSBC as a warning… not a teacher.

As for Governance, that’s another terrible black mark. For the last 12 years HSBC has been walking on regulatory tenterhooks – terrified if it made another mistake on money laundering then it would attract the full ire of the SEC and other regulators. In the noughties it made the mistake of assuming putting the Hexagon logo on some newly acquired Mexican banks somehow made them pristine. Nope. They simply legitimised drugs money. For the next decade their board was compromised by the fear of another mistake. It caused management paralysis from the top – culminating in a serious of mistakes like the appointment of the short-lived John Flint as CEO and the disastrous continuation of internal appointments to senior roles. The genetics of HSBC’s management remain about as diverse as a family of one-eyed hillbillies – but considerably less talented.

And now… it turns out HSBC “multi-year journey” to cleaning up its act re money laundering and other nefarious banking practices were equally dire. As the BBC highlighted on Panorama earlier this week – it deals with some shady characters.

HSBC remains a massive sell for the reasons listed above. It’s not a recovery stock. It’s not going to be a bargain – because every single one of these issues is going to get worse. Not better. It’s a massive short.

Tesla Battery Day

I don’t need to say much about Tesla’s much anticipated battery day. As we all know Elon Musk is a master of the “Overpromise and Underdeliver” school of stock-market hype. His preferred mode is to make the same promise again and again, state the downright obvious as if was some deep insight, and keep saying these things again and again in the hope investors don’t notice and think it done.

Yesterday’s battery day saw Tesla announce they will make batteries cheaper and better. They will launch a $25,000 affordable car! Fantastic. What stunning insights into Tesla’s path to riches.

Darn… I can’t just leave it like that. Tesla admitted it doesn’t actually have new battery designs or a new manufacturing process to make them. Musk said “We do not have an affordable car. That’s something we will have in the future. We’ve got to get the costs of batteries down.”

Tesla is a serial underdeliverer. Three years might be thirty in Musk-speak. The stock crashed 6% following battery day. Wake me up when it is down 80%. At that point I’m a buyer.

via ZeroHedge News https://ift.tt/303Z1EK Tyler Durden

Supreme Court justices often try to retire during the presidency of someone sympathetic to their jurisprudence. Of course, that doesn’t always work: Justice Scalia died after almost 30 years on the high court trying to wait out President Barack Obama, and Justice Ginsburg died after nearly 27 years trying to outlast President Trump.

Over all, though, strategic retirements give the justices too much power in picking their own successors, which can lead to a self-perpetuating oligarchy. The current system also creates the impression that the justices are more political actors than judges, which damages the rule of law. It may even change the way the justices view themselves.

The specific proposal is straightforward and in line with what others have proposed: Each justice serves for a single 18-year term. With the size of the Court fixed at nine justices, this would mean one new justice every two years. Terms are staggered so that nominations are made in the first and third year of each presidential term. This means a one-term President gets two nominations; a two-term President gets four nominations. (My co-blogger Orin Kerr outlined a similar proposal on Twitter the other day.)

Calabresi notes than an 18-year term would not pose a treat to judicial independence, but would eliminate the incentive to pick comparatively young nominees. It would also eliminate the problem of strategic retirements. For what it’s worth, an 18-year term is longer than terms for equivalent judicial offices in other constitutional democracies.

The details matter, as do transition rules.

In the case of early retirements or deaths, the president would nominate and the Senate would confirm a replacement to fill out the unexpired term with no possibility of reappointment.

Justice Ginsburg’s successor should serve an 18-year term. The eight current justices should draw lots as to who serves terms of two, four, six, eight, 10, 12, 14 or 16 years as the amendment goes into effect.

Failure to confirm a justice by July 1 of a president’s first or third year should lead to a salary and benefits freeze for the president and all 100 senators, and they should be confined together until a nominee has been approved. The vice president would act as president during this time and the Senate would be forbidden from taking action whatsoever on any of its calendars.

I will admit I am not entirely sure about this last bit – how and where would such confinement occur? how would it be enforced? – but the underlying principle seems right to me.

Limiting or cutting off the terms of existing justices would undoubtedly require a constitutional amendment. But a forward-looking proposal of the sort Calabresi outlines might be achievable by statute. The relevant constitutional language has always been understood to require life tenure, but there may be room to redefine the duties of the office. For instance, a statute could define the office of Supreme Court justice as 18 years serving as part of the Supreme Court, followed by continued judicial service riding circuit and filling in on the Supreme Court in cases of recusals or temporary vacancies. No justice would be removed from office or have their salary reduced, so this might do the trick. (Of course, whether the Supreme Court would uphold such a law in a legal challenge is another question entirely.)

There are other issues to consider were Supreme Court justices term-limited, such as whether there should be limits on types of future employment (to limit the incentive to rule in favor of potential future employers, a problem that sometimes arises on state courts), and whether a similar term limit should be imposed upon other judges. Nonetheless, the underlying idea of term-limiting justices to turn down the temperature on Supreme Court nominations is a good one.

from Latest – Reason.com https://ift.tt/32WIKDm

via IFTTT

Supreme Court justices often try to retire during the presidency of someone sympathetic to their jurisprudence. Of course, that doesn’t always work: Justice Scalia died after almost 30 years on the high court trying to wait out President Barack Obama, and Justice Ginsburg died after nearly 27 years trying to outlast President Trump.

Over all, though, strategic retirements give the justices too much power in picking their own successors, which can lead to a self-perpetuating oligarchy. The current system also creates the impression that the justices are more political actors than judges, which damages the rule of law. It may even change the way the justices view themselves.

The specific proposal is straightforward and in line with what others have proposed: Each justice serves for a single 18-year term. With the size of the Court fixed at nine justices, this would mean one new justice every two years. Terms are staggered so that nominations are made in the first and third year of each presidential term. This means a one-term President gets two nominations; a two-term President gets four nominations. (My co-blogger Orin Kerr outlined a similar proposal on Twitter the other day.)

Calabresi notes than an 18-year term would not pose a treat to judicial independence, but would eliminate the incentive to pick comparatively young nominees. It would also eliminate the problem of strategic retirements. For what it’s worth, an 18-year term is longer than terms for equivalent judicial offices in other constitutional democracies.

The details matter, as do transition rules.

In the case of early retirements or deaths, the president would nominate and the Senate would confirm a replacement to fill out the unexpired term with no possibility of reappointment.

Justice Ginsburg’s successor should serve an 18-year term. The eight current justices should draw lots as to who serves terms of two, four, six, eight, 10, 12, 14 or 16 years as the amendment goes into effect.

Failure to confirm a justice by July 1 of a president’s first or third year should lead to a salary and benefits freeze for the president and all 100 senators, and they should be confined together until a nominee has been approved. The vice president would act as president during this time and the Senate would be forbidden from taking action whatsoever on any of its calendars.

I will admit I am not entirely sure about this last bit – how and where would such confinement occur? how would it be enforced? – but the underlying principle seems right to me.

Limiting or cutting off the terms of existing justices would undoubtedly require a constitutional amendment. But a forward-looking proposal of the sort Calabresi outlines might be achievable by statute. The relevant constitutional language has always been understood to require life tenure, but there may be room to redefine the duties of the office. For instance, a statute could define the office of Supreme Court justice as 18 years serving as part of the Supreme Court, followed by continued judicial service riding circuit and filling in on the Supreme Court in cases of recusals or temporary vacancies. No justice would be removed from office or have their salary reduced, so this might do the trick. (Of course, whether the Supreme Court would uphold such a law in a legal challenge is another question entirely.)

There are other issues to consider were Supreme Court justices term-limited, such as whether there should be limits on types of future employment (to limit the incentive to rule in favor of potential future employers, a problem that sometimes arises on state courts), and whether a similar term limit should be imposed upon other judges. Nonetheless, the underlying idea of term-limiting justices to turn down the temperature on Supreme Court nominations is a good one.

from Latest – Reason.com https://ift.tt/32WIKDm

via IFTTT

Even though at the September FOMC meeting, the Fed indicated it plans to hold interest rates at zero at least through 2023 and it plans to continue quantitative easing at current levels, the markets said, “That’s not enough.”

The markets need more. This bubble is so much bigger than the one that we had back then (2008) that it requires far more air coming from the Fed to keep it from deflating. So, we need more. The Fed needs to talk about negative interest rates. The Fed needs to commit to bigger quantitative easing.”

Of course, in effect, the central bank is calling for more QE as Jerome Powell eggs on Congress to pass additional fiscal stimulus.

Any additional fiscal stimulus automatically requires more monetary stimulus, because where is the government going to get the money for the fiscal stimulus? It’s going to get it from the Fed. That’s what supposedly makes it a stimulus is that the government is going to run larger deficits. It’s going to spend money it doesn’t have.”

But there is concern that if Congress and the White House can’t get some type of fiscal stimulus package passed, the Fed won’t just provide more monetary stimulus on its own.

All that monetary stimulus is going to do, absent the fiscal stimulus, is pump up the asset markets – the stock market, the real estate market, or bond market. It’s not going to do anything for the real economy. I think the Fed believes that what will help the real economy is the fiscal stimulus. Now, the Fed is wrong. That’s not going to help the real economy either.”

With all of the political turmoil, ratcheted up by the death of Ruth Bader Ginsburg, the possibility of getting a fiscal stimulus deal done appears less likely.

Peter said he thinks the stock market will continue to be shaky and the sell-off could even gain momentum unless we get a concrete commitment to more monetary stimulus from the Fed, which may require something coming from Congress in terms of fiscal stimulus.

Which again, doesn’t stimulate the economy. But it will stimulate the markets. It will provide the addicts on Wall Street the drug they need in order to bid stock prices higher.”

But Peter said he thinks even if Congress can’t get a stimulus deal done, the Fed will ultimately act on its own.

Because the Fed will see the weakness in the market as a sign that the economy is going to weaken because it realizes that it is the wealth effect that is powering whatever recovery it thinks is in progress. And so if that is in jeopardy, I think the Fed will act unilaterally.”

No matter how you get it – more stimulus is bullish for gold and silver in the long-term. This recent dip could be a nice buying opportunity.

via ZeroHedge News https://ift.tt/3iVWEv7 Tyler Durden

Futures Extend Rebound As Nike Soars, Tesla Tumbles; Powell On Deck For 2nd Day Tyler Durden

Wed, 09/23/2020 – 08:09

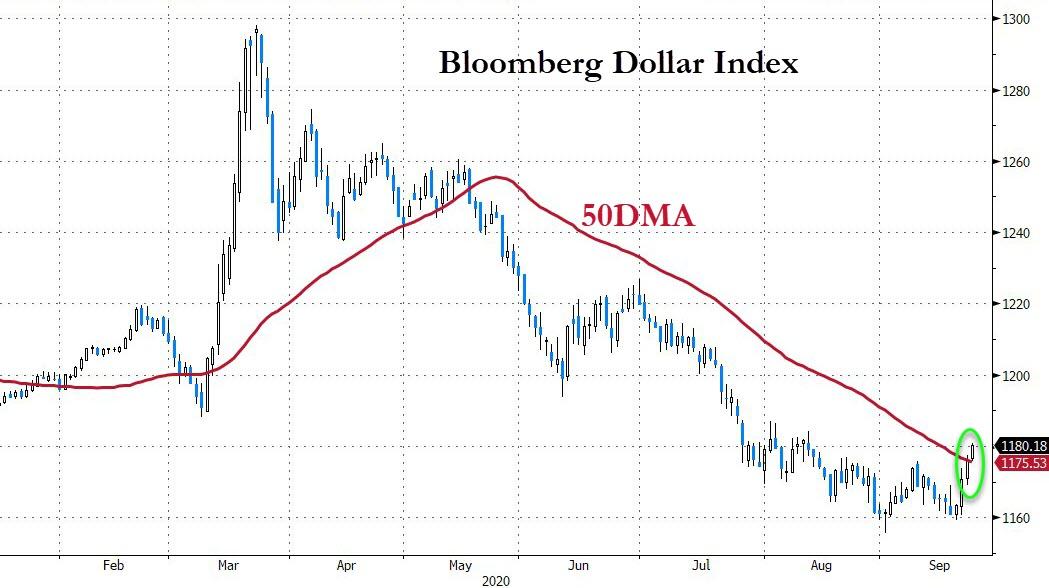

S&P futures and global stocks rose on Wednesday for the second day as Tuesday’s global rebound extended after the recent correction, ahead of data that would throw light on the pace of an economic recovery from a coronavirus-driven recession. Investors also waited for a second speech from Fed Chair Jerome Powell who will appear before the House Select Subcommittee on the coronavirus to discuss the central bank’s response. The dollar extended its impressive Tuesday gains while 10Y yields were fractionally higher.

Nike was set for a record open after a stunning quarterly earnings report. Shares of the world’s largest athletic shoe maker surged 13.2% in premarket trading as its digital sales, especially in North America, helped offset a fall in sales at traditional brick-and-mortar stores. The Dow constituent was set to drive the blue-chip index higher for a second straight day, clawing back more of the sharp declines from Monday that were driven by fears of another round of lockdowns to contain a global surge in COVID-19 cases.

On the other end, Tesla fell 4.8% in premarket trading as the goals announced at Tuesday’s “Battery Day” event was a dud and Musk failed to impress with his promise to cut electric vehicle costs. Oracle headed lower after a report by a state-backed Chinese newspaper said Beijing was unlikely to approve a proposed deal by the software maker and Walmart for ByteDance’s TikTok.

Meanwhile, Russia’s largest internet company Yandex surged 9.2% in premarket after it said it’s in talks to buy TCS Group Holding Plc for about $5.48 billion. Elsewhere, the FAANGs edged higher before the bell. The group has borne the brunt of the declines this month after fuelling a Wall Street rally since March.

Overall sentiment remains skittish as doubts about more U.S. fiscal stimulus and growing political uncertainty in the run-up to the Nov. 3 presidential elections have kept investors from making big stock market bets.

“We are seeing a solid bounce, but it’s in the context of a very sharp pullback on Monday, which was a reset,” said Neil Wilson, chief market analyst in London for Markets.com. “We had bulls just tipping their toes back in the water, and the higher closes — as small as they were — seems to have been enough to cue today’s gains.”

“If we get a second (COVID-19) wave, it could have a significant impact on the election itself and that’s why markets have been wobbly in the last few days,” said Andrea Cicione, head of strategy at TS Lombard in London.

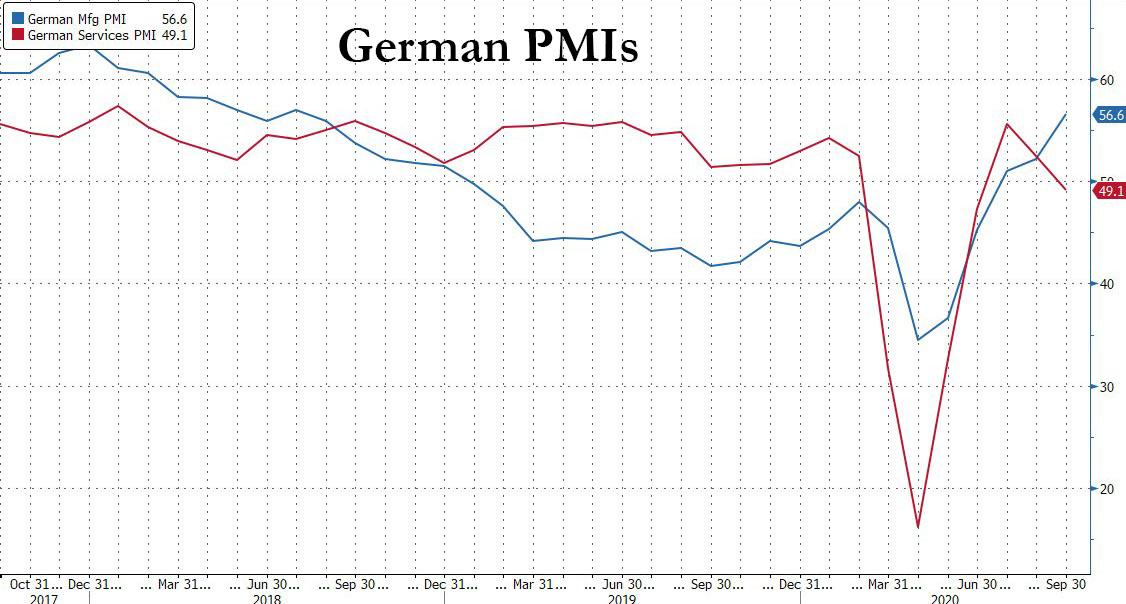

In Europe, the Stoxx 600 Index climbed 1.5%, the biggest gain in two weeks, helped by a jump German stocks after manufacturing data rose to a two-year high. Auto companies and travel stocks led the advance in Europe, with gains of 2.8% for both. Despite stronger German mfg PMI, the service sector stumbled and broader Eurozone data showed eurozone business growth ground to a halt this month with the post-Covid economic recovery stumbling this month, as the latest Euro area composite PMI declined by 1.8pt to 50.1 in September, notably below expectations. Across sectors, the overall decline was concentrated in the service sector, with the pace of recovery in manufacturing reaccelerating from August:

Euro Area Composite PMI: 50.1, consensus 51.9, last 51.9.

Euro Area Manufacturing PMI: 53.7, consensus 51.9, last 51.7.

Euro Area Services PMI: 47.6, consensus 50.6, last 50.5.

And the sharp divergence in Germany:

Germany Composite PMI: 53.7, consensus 54.0, last 54.4.

German Services PMI: 49.1, consensus 53.0, last 52.5

German Manufacturing PMI: 56.6, consensus 52.5

Earlier in the session, Asian stocks were fractionally higher, with health care rising and energy falling, after falling in the last. Markets in the region were mixed, with Australia’s S&P/ASX 200 and Singapore’s Straits Times Index rising, and India’s S&P BSE Sensex Index and Taiwan’s Taiex Index falling. The Topix declined 0.1%, with Daiichi Kigenso and Land Co falling the most. The Shanghai Composite Index rose 0.2%, with EGing Photovoltaic Technology and Jinko Power Technology posting the biggest advances

Chinese state-run media decounced the TikTok deal as “an American trap” and a “dirty and underhanded trick” as sentiment in Beijing swings against the proposal. TikTok owner ByteDance said it would remain in control of the new entity that would be created in the agreement, pushing back on President Donald Trump’s assertions that Oracle Corp. would be in control. The wider context of resistance from China is that the country’s leaders do not want to be seen to be pushed around by unilateral U.S. actions.

Looking at today’s main event in markets, Fed Chair Powell is in Congress again testifying to a House select subcommittee on the coronavirus response from 10:00 a.m. Yesterday he said the U.S. economy has a long way to go before it is fully recovered and that more support will be needed.

In other overnight news, while there is still very little progress on reaching a new stimulus deal, there was some relief late yesterday when an agreement to keep the government funded through Dec. 11 was reached, avoiding a shutdown just before the election. More importantly, Republican moves to get a confirmation hearing for Trump’s Supreme Court nominee in the coming weeks now seem unstoppable, after Democrats gained little support in the Senate for a delay.In FX, the dollar advanced a fourth day – its best run since June – after breaking above a key technical resistance level. The Bloomberg dollar index was up as much as 0.3% to highest since Aug. 12, but pared some advance as the euro erased losses. The euro erased losses, after falling to 1.1672 in early London trading, after mixed PMI data out of the region weighed initially yet as European equities extended gains, but then the common currency reversed course. The pound also steadied after dropping following comments by Foreign Secretary Dominic Raab on not being able to rule out a nationwide shutdown. The Australian dollar led declines after influential Westpac Banking Corp. economist Bill Evans predicted the central bank would cut interest rates at its Oct. 6 meeting; the New Zealand dollar also slipped, with the central bank maintaining the size of its quantitative easing program and keeping rates unchanged.

MSCI’s index of developing-nation stocks was little changed on Wednesday after falling more than 2% in the previous two days. The gauge for currencies dropped to its lowest level since Sept. 14, with the rand among the worst-hit as outflows from South Africa’s bond market surged. The average emerging-market sovereign-risk premium was unchanged, according to JPMorgan indexes. Central banks remain in focus, with policy makers in the Czech Republic forecast to follow their Thai counterparts and keep rates on hold. China’s yuan fixing was weaker than expected for a second day, reinforcing speculation that the central bank wants to slow the currency’s biggest quarterly rally since 2008.

In rates, treasury yields are slightly cheaper in early U.S. trading as Asia-session gains – led by steep gains for Aussie bonds – eroded ahead of 5-year note auction. Yields are cheaper by about 0.5bp from intermediates to long end with 10-year around 0.675%, trading broadly in line with bunds; gilts outperform slightly, about 0.5bp richer vs. Treasuries. Treasury auction cycle resumes with $53b 5-year note at 1pm ET, concludes with 7-year Thursday. Italian bonds rallied to send 30-year yields to an all-time low with investors continuing to snap up the securities on fading domestic political risk and support from European institutions. Elsewhere, Zambia became the first African country to ask bondholders for relief since the onset of the coronavirus.

In commodities oil was unchanged after fluctuating earlier, while gold continues to slide, dropping below $1,900 earlier and sliding below the 50DMA.

Looking at the day ahead, in addition to Powell speaking in the House, there is a slew of Fed speakers today, including Cleveland Fed President Loretta Mester, Chicago Fed President Charles Evans, Boston Fed President Eric Rosengren, Minneapolis Fed President Neel Kashkari, Atlanta Fed President Raphael Bostic, Fed Vice Chair for Supervision Randal Quarles and San Francisco Fed President Mary Daly. Latest U.S. government crude stockpile data is at 10:30 a.m. President Trump is due to speak to state attorneys general on social media abuses. The UN General Assembly continues.

Market Snapshot

S&P 500 futures up 0.5% to 3,314.00

STOXX Europe 600 up 1.3% to 362.11

MXAP up 0.09% to 171.12

MXAPJ up 0.2% to 557.55

Nikkei down 0.06% to 23,346.49

Topix down 0.1% to 1,644.25

Hang Seng Index up 0.1% to 23,742.51

Shanghai Composite up 0.2% to 3,279.71

Sensex down 1% to 37,353.04

Australia S&P/ASX 200 up 2.4% to 5,923.93

Kospi up 0.03% to 2,333.24

German 10Y yield fell 0.8 bps to -0.513%

Euro down 0.2% to $1.1689

Italian 10Y yield fell 5.2 bps to 0.661%

Spanish 10Y yield fell 1.8 bps to 0.217%

Brent futures up 0.4% to $41.87/bbl

Gold spot down 1.1% to $1,879.89

U.S. Dollar Index little changed at 93.94

Top Overnight News from Bloomberg

The European Central Bank risks legal trouble if it tries to extend the “emergency powers” of its pandemic bond-buying plan to its other asset-purchase program, according to Executive Board member Yves Mersch

SNB President Thomas Jordan has taken his foot off the pedal after the most aggressive currency intervention in five years early in the outbreak of the coronavirus pandemic

The euro area’s economic recovery stalled this month as consumers fretted about a resurgence of the coronavirus and governments reinstated restrictions to control the spread of the disease

Banks from Goldman Sachs Group Inc. to HSBC Holdings Plc have hit pause on plans to return workers in London after Prime Minister Boris Johnson appealed to Britons to work from home to help tame a resurgent coronavirus

JPMorgan Chase & Co. is moving about 200 billion euros ($230 billion) from the U.K. to Frankfurt as a result of Britain’s exit from the European Union

A quick look at global markets courtesy of NewsSquawk

Asian equity markets traded mixed and failed to take full impetus from the rebound across their global peers, with the region tentative amid ongoing US-China tensions and with Japan suffering post-holiday blues on return from the extended weekend. Nonetheless, ASX 200 (+2.4%) outperformed and is on track for its best day in seven weeks as tech names led the broad advances after they found inspiration from the resurgence of the sector stateside, with sentiment also buoyed by increasing calls for the RBA to cut rates at next month’s meeting after RBA Deputy Governor Debelle recently outlined policy options. Nikkei 225 (U/C) was subdued as it played catch up to the recent days’ weakness and with Panasonic shares pressured alongside fellow Tesla supplier LG Chem after the EV-maker’s Battery Day Event fell flat where Elon Musk announced plans for a reduction in costs and to manufacture its own batteries, while he also showcased the Model S Plaid which is to be available next year. Conversely, Fujifilm Holdings was at the other side of the spectrum after announcing its Avigan drug met the primary endpoint in Phase 3 COVID trials. Hang Seng (+0.1%) and Shanghai Comp. (+0.2%) were indecisive as the continued PBoC liquidity efforts were offset by ongoing US-China tensions after US President Trump put China on blast for the spread of the coronavirus at the virtual UN meeting, while Beijing later criticized President Trump of spreading “political virus”. In addition, the uncertainty regarding the TikTok deal persists and the US House also overwhelmingly passed the forced labour bill which would ban imports from China’s Xinjiang region that were produced using forced labour. Finally, 10yr JGBs were higher amid the risk averse tone in Japan and with the BoJ also in the market for nearly JPY 1.3tln of JGBs in up to 10yr maturities, while it also offered to purchase 3yr-5yr corporate bonds.

Top Asian News

Hong Kong’s BEA Is Said to Press Ahead With Life Insurance Sale

Richard Li’s FWD Said to Plan Up to $3 Billion Hong Kong IPO

Malaysia Leader Calls for Stability After Anwar Claims Majority

Hong Kong Traders Chased 1,600-1 Odds to Buy IPO That Flopped

European equities are back on the grind higher (Euro Stoxx 50 +1.7%) after experience a fleeting blip lower on the back of French Services PMI dipping back into contractionary territory on second wave woes. The region picked up the baton from a mixed APAC handover, with reports also noting that the ECB as called upon Brussels to make the EU Recovery Fund a permanent measure. Bourses in the EU are seeing broad-based gains, whilst UK’s FTSE (+2.2%) ploughs ahead initially with the aid of a softer Sterling. Meanwhile UBS Wealth Management sees UK domestic banks falling 15-20% and insurance stocks decline by 7-10% in a no-deal Brexit scenario, but expects double digit positive returns from UK equities over the next 9-12 months in the event of a deal. Sectors in Europe are higher across the board with a slight cyclical/value bias, although material names do not fare so well amid the USD-induced declines across the metals complex. Consumer Discretionary meanwhile tops the charts with the aid of Nike (+13% pre-mkt) post-earnings, who beat on both top and bottom lines whilst reporting digital sales +82% YY – thus bolstering the likes of Adidas (+5.7%), Puma (+4.6%) and JD Sports (+5.1%). In terms of the breakdown, Travel & Leisure leads the gains, closely followed by Autos and Banks. Turning to individual movers, Osram Licht (+14.6%) is the top Stoxx 600 gainer after ASM (+1.4%) has signed a denomination and profit and loss transfer agreement with Osram as part of the takeover process.

Top European News

Europe’s Economic Revival Put on Hold by Virus Resurgence

U.K. Recovery Slows as Households Start to Rein In Spending

Sunak Urged to Save U.K. Firms From ‘Ruin’ of Covid Curbs

Merkel Resists Full Ban on Huawei, Making Germany an Outlier

In FX, the Dollar has extended its impressive recovery rally, partly in relief that the House finally passed the stopgap spending bill to avert a Government shutdown, but mainly as the Greenback continues to regain its global safe-haven and reserve status amidst the ongoing resurgence in COVID-19 that is accelerating outside the US and notably across Europe again. As a result, the index breached 94.000 and topped out just above 94.250, with several Buck/major pairings looking very vulnerable near or through psychological/round number levels.

AUD/NZD – Dovish RBA calls via Westpac and NAB both looking for 15 bp cuts at the October meeting, plus a dovish RBNZ hold overnight, leaving the door wide open for more easing and in the offing or in the pipeline, an FLP by the end of 2020, according to the accompanying statement, have all added further pressure on the Aussie and Kiwi, with the former struggling to stay above 0.7100 and latter even less assured around 0.6600 ahead of NZ trade data.

CAD – Some solace for the Loonie from relative stability in oil prices, but not enough momentum to convincingly reclaim 1.3300+ status within a 1.3345-1.3294 range awaiting the reopening of Canadian Parliament by PM Trudeau.

CHF/EUR/GBP/JPY – All narrowly mixed vs the Dollar, but not before losing grip of 0.9200, 1.1700, 1.2700 and 105.00 handles respectively in advance of Thursday’s quarterly SNB policy review and following mixed Eurozone/UK prelim PMIs where services sector weakness outweighed manufacturing strength to keep the composite readings compressed. However, Sterling was undermined by domestic factors related to the coronavirus and warnings from Foreign Minister Raab about latest restrictions not going far enough to rule out the risk of reverting to full lockdown. Cable plumbed fresh lows around 1.2677 and Eur/Gbp retested recent peaks circa 0.9220 in response, but the Pound has subsequently received a reprieve from EU’s Barnier expressing determination to strike a Brexit trade deal. Elsewhere, pretty standard commentary from BoJ Governor Kuroda has marked the return of Japanese markets from their 4-day break, but not really the Yen between 104.91-105.19 parameters eyeing mega option expiries for tomorrow that span 105.00 in an even tighter band (104.90-105.10).

SCANDI/EM – The Norwegian Crown continues to slip closer towards the sentimental if not technically significant 11.0000 level vs the Euro regardless of crude finding a base as noted above, but the Swedish Krona is still benefiting from Riksbank rigidity on the repo staying at the zero lower bound until this time in 2023. On that note, the Turkish Lira will be looking for continuity and some much needed support from the CBRT on Thursday via a form of indirect tightening as it plumbs almost daily record lows, and more immediately the Czech Koruna has the CNB to provide direction, albeit with no change in rates expected.

In commodities, WTI and Brent front month futures have nursed the losses seen in APAC hours, as sentiment in Europe picks back up after the EZ Services PMI fell back contraction but manufacturing topped estimates across the board. The initial weakness in the crude markets stemmed from a surprise build in the Private Inventory data (+0.7mln vs. Exp. -2.3mln), whilst concern remains over the demand implications from the reimposition of lockdowns and quarantine travel rules, with the Gazprom CEO also noting that we are seeing global oil demand recovery slowing down due to pandemic, and expects global oil consumption to return to pre-crisis level in H2 2021. In terms of the reopening supply from Libya, reports yesterday noted that next week could see output of some 260k BPD (vs. 1mln BPD pre-blockade), although analysts at ING downplay the relevance, noting that “In the current environment, where there are clear concerns over demand, additional supply will do little to help rebalance the market.” Something else to be aware of: reports noted that Chinese refiners are requesting additional import quotas for the fourth quota, having had taken advantage of the lower oil prices earlier this year. Desks note that further quota allocation could support the physical market. Aside from that, news-flow has remained relatively light for the complex thus far, WTI Nov meanders around USD 39.85/bbl (vs. low USD 39.26/bbl), while its Brent counterpart resides around 41.85/bbl (vs. low 41.21/bbl), awaiting the weekly EIA inventory data – with headline crude stocks seen drawing 2.325mln barrels. Elsewhere, precious metals initially succumb to the firmer Dollar and broader gains in stocks. Spot gold moves further below the USD 1900/oz mark to find support at USD 1875/oz, and has picked up given the most recent slip in the USD, whilst spot silver found a current base around the USD 23/oz level. Base metals are also mostly lower – with LME copper weighed on by the firmer Buck and lackluster China performance, whilst Dalian iron ore futures fell for a third straight days as higher shipments from mainstream miners weighed on prices.

US Event Calendar

7am: MBA Mortgage Applications, prior -2.5%

9am: FHFA House Price Index MoM, est. 0.45%, prior 0.9%

9:45am: Markit US Manufacturing PMI, est. 53.5, prior 53.1; Services PMI, est. 54.5, prior 55; Composite PMI, prior 54.6

Fed Speakers:

9am: Fed’s Mester Discusses Payments and the Pandemic

10am: Powell Appears before House Panel on Covid-19

11am: Fed’s Evans Discusses the U.S. Economy and Monetary Policy

12pm: Fed’s Rosengren Discusses U.S. Economy

1pm: Fed’s Kashkari Discusses Public Health

1pm: Fed’s Bostic Speaks to Hale County Chamber of Commerce

2pm: Fed’s Quarles Gives Speech on the Economic Outlook

3pm: Fed’s Daly Discusses Labor Force Implications of Covid-19

DB’s Jim Reid concludes the overnight wrap

I suspect this won’t be the last Zoom call I do from home after the U.K. yesterday effectively encouraged those who can work from home to do so – and possibly for the next 6 months. Today also sees a big change in the weather here as the Indian Summer has come to an abrupt end. Winter is coming in more ways than one. On the virus we’ve revamped our daily cases and fatality tables that appear in the PDF (click view report above) and given they are sorted worst to best they show that the U.K. is certainly not at the top of the second wave, but restrictions are nonetheless being tightened as case numbers build (4,926 yesterday and the highest since early May). In addition to WFH guidance, all hospitality venues must now close at 10pm daily from Thursday. In a nationwide address Johnson stressed the desire to avoid a full lockdown scenarios saying, “we must do all we can to avoid going down that road again.” Though if the infections continue to rise the government naturally left the option on the table. Meanwhile in Scotland, First Minister Nicola Sturgeon went even further, with a ban on households visiting other households indoors.

In Europe, the summit of EU leaders planned for this Thursday and Friday has now been postponed to the following week, after the President of the European Council, Charles Michel, went into quarantine because a security officer had tested positive. We also heard from German Chancellery Minister Braun that it is not the country’s ‘first choice’ to close borders to neighboring countries with high level of infections, citing the economic challenges. So here again we see a level of moderation in policy enactment during the second wave. Can this continue as the virus spreads? Cases are also rising in the US again, with the daily rate of people testing positive for the first time jumping to 5.9% in Florida after being under 5% for the better part of the last 2 weeks. We also saw some vaccine related news yesterday with the Washington Post reporting that the US FDA is expected to spell out a tough, new standard for an emergency authorisation of a coronavirus vaccine as soon as this week that will make it exceedingly difficult for any vaccine to be cleared before Election Day.

The virus news flow has been a difficult backdrop for markets this week but US markets started to gather some momentum after Europe went home last night. There was a particular reversal in US technology stocks, which continued to outperform after the late-session rally on Monday. The S&P 500 broke a four-day slide and gained +1.05%, however cyclicals sectors like Banks (-1.89%), Autos (-1.13%) and Energy (-1.03%) continued to lag. Retail (+3.64%), Media (+2.24%) and Software (+1.94%) all the led the S&P higher as the tech gains saw the NASDAQ rally +1.71%. This could again signal that the stay-at-home trade is coming back into vogue with further restrictions being seen in Europe. Europe still saw a slight recovery from Monday’s worst day for three months as the STOXX 600 climbed +0.20% higher.

Asian markets are mixed this morning with the Nikkei (-0.36%) and Kospi (-0.25%) both down while the Hang Seng (-0.01%) and Shanghai Comp (+0.02%) are trading broadly flat and the Asx (+2.15%) is up partly helped by stronger preliminary PMIs (more below). Japanese markets have reopened post 2 days of holiday. In overnight news, Tesla’s “Battery Day” event came short of expectations for a blockbuster leap forward as the company laid out a roadmap to build a $25,000 car only by 2023 which disappointed some. The stock was down -7% in aftermarket trading. This is also weighing on Nasdaq futures (-0.38%) while those on the S&P 500 are trading broadly flat.In fx, the US dollar index is up a further +0.25% this morning after yesterday’s +0.47% advance.

In other news, the US House passed a stopgap funding bill to keep the government operating through Dec. 11 after both parties in Congress and officials at the White House struck a deal to provide aid to farmers and food assistance for low-income families. The temporary spending bill will now move to the Senate for a vote.

Today, investors will be watching out for the flash PMIs for September, which will give us an early indication of how the global economy has fared this month. Overnight we’ve already had readings from Japan and Australia, with Japan struggling to recover further as manufacturing PMI rose by just 0.1 pt to 47.3 while the services reading improved to 45.6 (vs. 45.0 last month). Australia’s readings were a bit more robust with manufacturing PMI climbing to 55.5 (vs. 53.6 last month) and the services reading printing at 50.0 (vs. 49.0 last month). Australia’s reading seem to be helped partly by the easing of lockdown in Victoria, the second largest state. With infections rising again in Europe, not least in the UK, France and Spain, the question is to what extent this will impact on economic activity there as well. DB’s Peter Sidorov put out a piece yesterday (link here) in which he writes that his analysis points to a slight upside risk to the Euro Area PMI because of mobility trends, which has been rising in September. We’ll get those releases this morning.

Back to yesterday, and Fed Chair Powell appeared before the House Financial Services panel, where he again stressed the need to keep the virus under control and for further policy actions from “all levels of government.” Secretary Mnuchin who testified alongside the Fed Chair said that he and the President he would continue to seek Congressional agreement on further fiscal stimulus. Though now Congress seems like it will be more focused on a supreme court confirmation than fiscal stimulus in the short term. The Fed Chair said the Fed has only purchased $1.5 billion in loans so far through its Main Street Lending Program. The program is a $600 billion facility backed by Treasury funds, which aims to provide credit to small-mid sized companies. Mnuchin did bring up the idea of reallocating some of the unused money in Fed facilities to other uses, though it would require congressional approval.

There were a few other central bank headlines. From the ECB, we had Fabio Panetta of the Executive Board saying that “the risks of a policy overreaction are much smaller than the risks of policy being too slow or too shy to react and the worst-case scenarios materialising.” And over in the UK, Bank of England Governor Bailey downplayed the prospect of an imminent move to negative rates after last week’s MPC minutes showed that they were exploring the operational considerations of such a move.

In fixed income, there was a sharp narrowing of sovereign bond spreads in Europe, particularly following the regional election results in Italy that were regarded as positive for the government’s stability. Yields on 10yr BTPs fell -5.2bps to their lowest levels in almost a year, moving below the levels they were at before the pandemic hit the country in late February. And with the selloff for bunds, that sent the BTP-bund spread down -7.7bps to 1.37%, its lowest level in 7 months. Elsewhere, US Treasury yields saw a slight +0.5bps move higher, as the dollar index climbed a further +0.35% to reach its highest level in nearly 2 months.

Staying on the US, and with less than 6 weeks now until the election, President Trump said that he’d announce his choice this Saturday at 5pm (Washington Time) on who would replace Justice Ruth Bader Ginsburg on the Supreme Court. In a positive development for Trump, Senator Mitt Romney said that he’s in favour of moving forward with a confirmation vote on Trump’s choice, which leaves just 2 Republican senators out of the 53-member caucus who have opposed going ahead with a vote. With Trump’s choice on Saturday and the first debate between himself and Biden this Tuesday, the coming week will be one of the most important yet ahead of election day on November 3rd.

Looking at yesterday’s data, existing home sales in the US rose to an annualised rate of 6.00m in August, in line with expectations, and the most since 2006. Meanwhile the Richmond Fed’s manufacturing survey rose to 21 (vs. 12 expected). Finally, the advance consumer confidence reading from the Euro Area in September rose to -13.9 (vs. -14.7 expected). This was its highest level since March, but still some way below the -6.6 reading back in February before the full impact of the pandemic became apparent.

To the day ahead now, and the aforementioned flash PMIs will be one of the key highlights. Otherwise, there are an array of Fed speakers, including Chair Powell before the House Select Subcommittee on the Coronavirus Crisis, as well as the Vice Chair Quarles, Mester, Evans, Rosengren, Kashkari, Bostic and Daly. The ECB’s Hernandez de Cos will also be speaking.

via ZeroHedge News https://ift.tt/304fPvr Tyler Durden

{kind=link}